Embed Size (px)

Citation preview

RRP $10

www.australianshareholders.com.au

06A three pronged investment strategy

172017 AGM wrap

11BlueScope Steel Limited (BSL)

Women and retirement savingsWhy do women have less than half

EQUITYSTANDING UP FOR

SHAREHOLDERS

FEBRUARY | MARCH 2018 VOL 32 #2

2 FEBRUARY | MARCH 2018 EQUITY

FEATURES THIS MONTH

04 Women and retirement savingsAustralian women on average have approximately half the level of men’s superannuation savings. This is the case both while women are at work and also once women have retired. Karen Volpato, Senior Policy Advisor at AIST, outlines some policies which could help address this discrepancy.

06 A three pronged investment strategyAs the local share market has clocked off on 2017 with double-digit percentage gains (all-in) for the second calendar year in a row, Rudi Filapek-Vandyck, Editor of FNArena, wonders whether it is time for investors to zoom in on what has been happening underneath the surface of this unexpectedly robust bull market?

11 BlueScope Steel Limited (BSL)BlueScope (BSL) has undergone an amazing transformation since the company demerged from BHP in 2002. Rod McKenzie, the Victorian Company Chairman, outlines the background and prospects for this company.

EQUITYSTANDING UP FOR

SHAREHOLDERS

FEBRUARY | MARCH 2018 Vol 32 #2

03From the CEO

16Brickbats and Bouquets

12AGM reports

20Conference activities

08Top 7 myths about ETFs busted

18Giving exposed

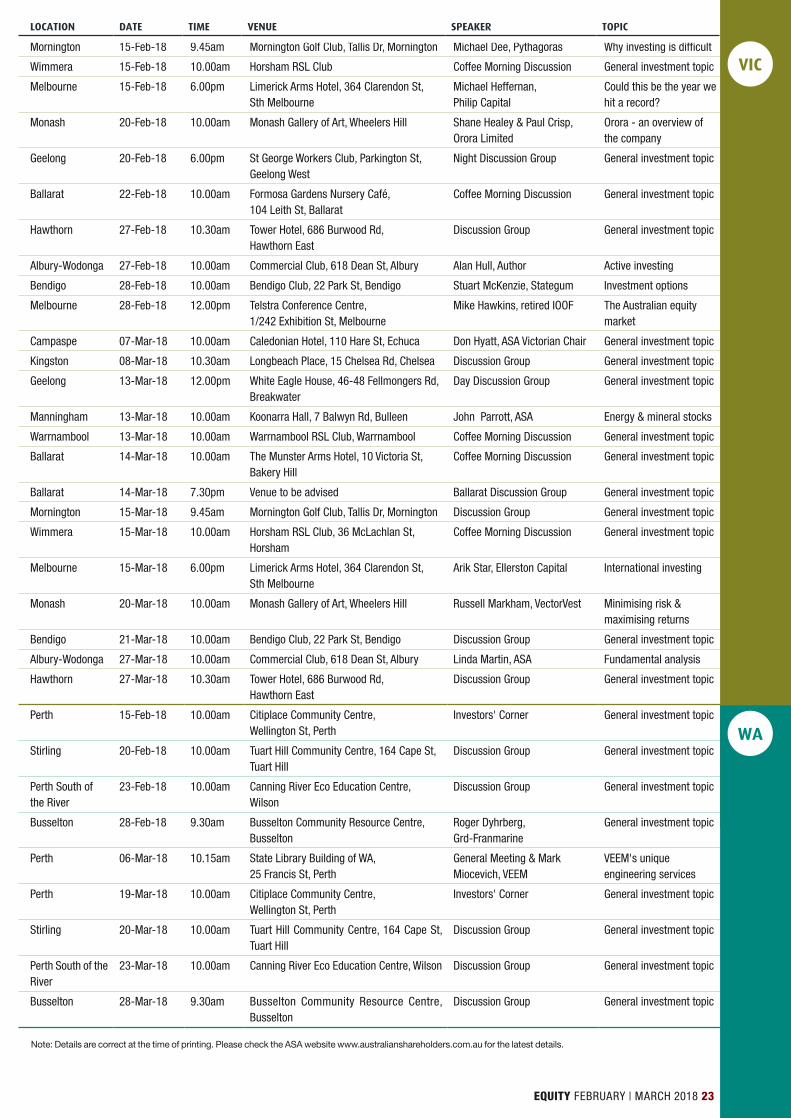

22Calendar of events

07Call for director nominations 2018

172017 AGM wrap

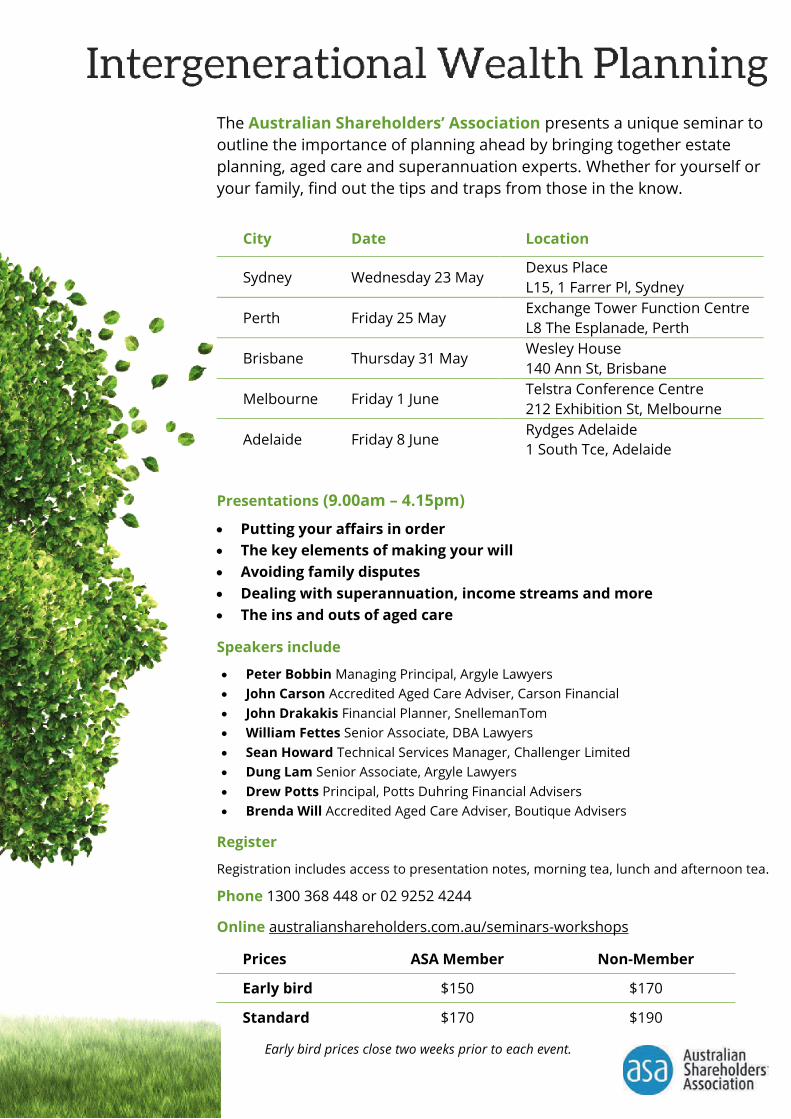

21Intergenerational wealth planning seminars

10Can socially responsible investing and good returns coexist? YES

19News desk

EQUITY FEBRUARY | MARCH 2018 3

As an ASA member, you get more from your retail investment journey than if you go it alone, whether you’re a retail shareholder, an SMSF trustee or an individual investor. With the ASA you can network and grow with a community of like-minded investors. Our ongoing learning and education allows investors to hone their financial knowledge and investment skills.

Helping educate investors to become more informed is one of ASA’s core missions. For that reason, we have always believed that we have a role to play in improving financial literacy in Australia. Last year we applied for a Financial Literacy Australia grant and, I am delighted to advise, our application was successful. We were advised in December 2017 that we would be awarded a grant of $110,186 to assist women 65+ to build confidence to participate in financial decision-making.

Research indicates that typically women over 65 are not actively engaged in the management of their investment portfolio and/or self-managed superannuation fund — often due to lack of confidence and low financial literacy levels. While this is not true of ASA female members, who are already showing agency in financial decision-making, it is recognised in the research literature as being true of a large percentage of women of this age.

As women tend to outlive men and inherit a financial plan, there is an imperative to improve older women’s financial investment knowledge and confidence. This is because for women without basic investment knowledge, consulting a financial adviser can be an overwhelming experience. Also, without agency over their financial futures, older women may also be vulnerable to family members taking over and those family members may be incompetent, or worse, predatory.

Our project addresses both the knowledge/information aspects and the emotional/relational aspects of gaining financial agency. One goal is to empower older women whose partners have always managed the finances with an understanding of basic investment and financial concepts knowledge. We aim to demystify these concepts and assist women to understand them. Another objective is to give older women the confidence to have conversations with their partners, children and financial advisers about how the investments and finances are structured. We want to help women explore the emotional triggers to which they may be vulnerable (such as guilt or shame) and assist them to be able to deal with offers of assistance from family and friends with regard to managing their financial affairs. Importantly, the aim is also to assist them to find the confidence both to judge if they want to accept such offers and hold a discussion with professional advisers about their financial future.

The pilot will be run in Victoria in 2018, with plans to run free workshops across the country in 2019 after completion of the pilot. Evaluation is a significant aspect of the project — the grant provides for us to work with experts in evaluation to assess if we achieved the desired outcomes. Importantly, given the emphasis on evaluation, results of the project will help inform ASA if the small behavioural workshop approach we are undertaking in this project could be applied to different demographic groups and form part of our ongoing education.

We hope that our members will assist us in spreading the word — many of you may know women who could benefit from this project. We are recording expressions of interest to participate now, with the proviso that the pilot workshops will only be run in Victoria. But any expressions of interest will be retained for when we roll out the main project across the country — we will maintain confidentiality in relation to them.

I look forward to reporting to you on the evaluation of the pilot project. E

FROM THE CEOBy Judith Fox

BOARD OF DIRECTORSDiana D’Ambra BCom MCom FCA MAICD, ChairmanGeoffrey Bowd BCom MComAlison Buxton BCom (Marketing) GAICDDavid Fletcher BAcc CA GAICDAllan Goldin BA BLawDon Hyatt BAppSc DipEd M Ed MACEStephen Mayne BCom GAICD

NATIONAL OFFICEJudith Fox BA(Comm) MCA FGIA MAICD CEO

Fiona Balzer BComm SFFin GAICD Policy & Advocacy Manager

Sarina Devi BBus(Acct) ADipBus Administration Officer

Silvana Eccles BA(Modern Languages) National Operations & Education Manager

Kris Nuñez AdvDipBus(Advert) Events & Marketing Officer

Kristy Wan BA(Comm) Content & Design Officer

STATE BRANCHESACT Edward Patching [email protected] Richard McDonald [email protected] Bryan Moore [email protected] Brad Martin [email protected] Don Hyatt [email protected] WA Barry Nunn [email protected]

EQUITY EDITORSilvana Eccles [email protected]

CONTACT DETAILSTELEPHONE 1300 368 448 02 9252 4244

FAX 02 9071 9877

ADDRESS Suite 11, Level 22 227 Elizabeth Street Sydney NSW 2000

PO Box A398 Sydney South NSW 1235

ABN 40 000 625 669

EMAIL [email protected]

WEBSITE www.asa.asn.auwww.australianshareholders.com.au

DISCLAIMERThis material in EQUITY is provided for information only. No responsibility or any form of contractual, tortious or other liability is accepted for decisions made on the basis of the information contained herein. Nothing in EQUITY is intended or should be interpreted as being investment advice. Investment advice can only be obtained from persons who are licensed in accordance with the Corporations Act. Views expressed in articles in EQUITY do not necessarily reflect ASA policy. The ASA does not endorse or favour any specific commercial product or company. The ASA is often able to negotiate discounts or benefits for ASA members however the inclusion of discounts or advertisements in EQUITY, on the ASA website or within other ASA communications does not constitute an endorsement for the products, services or companies mentioned.

COPYRIGHTAll material published in EQUITY is copyright. Reproduction in whole or in part is not permitted without written authority from the Editor.All graphs for the AGM and BIG Reports derive from Morningstar. Any correspondence regarding matters covered in this magazine should be addressed to the Editor.

4 FEBRUARY | MARCH 2018 EQUITY

Women and retirement savingsWhy do women have less than half?By Karen Volpato Senior Policy Advisor, Australian Institute of Superannuation Trustees (AIST) Money Management’s Woman of the Year Financial Services 2018

Australian women on average have approximately half the level of men’s superannuation savings. This is the case both while women are at work and also once women have retired. Women face a greater risk of poverty in old age when compared with men. Over 30 percent of older women are living in poverty. These problems are exacerbated by women having higher life expectancies than men.

The gender gap in superannuation savings results from the inequalities which women face over their lifetime. The gender superannuation savings gap (what a woman’s superannuation savings is compared with a man’s savings) is not only about superannuation.

The superannuation gender gap experienced in Australia occurs elsewhere. The European Union has said the “gender pension gap amounts to around 40 percent for the European Union as a whole. This gap reflects gender differences in employment — notably pay, working hours and career duration. … Reducing the gap will require a combination of determined equal opportunity policies across several fields before people reach pensionable age, but this will only have positive effects over the long term.”

1. Women’s superannuation savings gapIn addressing any issue, it’s first important to have orienting data. The following chart compares women’s and men’s superannuation savings in Australia.

Source: Workplace Gender Equality Agency’s submission to the Senate Economics Reference Committee – Economic Security for women in retirement 2015

2. What are the key causes of the gap?This is a quick snapshot of some of the key causes, which relate to employment issues, policy issues, and the nature of the superannuation system itself.

• Workforce inequalities (eg. participating in the workforce, pay, part time and casual work, and job segregation (work

roles women do compared with men, the level of support for child care costs).

• Life cycle constraints contributing to the superannuation gender gap (eg. child rearing, caring for aged parents, and unemployment).

• Superannuation system inequalities (eg. taxation, and a lack of superannuation paid on parental leave).

• Gender lens should be applied to policy development.

3. Workforce inequalitiesSuperannuation is a combination of how much people save, investment returns, what fees and costs deducted, and the impact of superannuation policy settings (eg. taxation, and interaction with the age pension).

To help understand why women’s superannuation savings are less than men’s, it is important to examine how women’s experiences at work are different (including comparisons with peer countries).

Women’s workforce participation ratesAustralia is closing the gap between women’s and men’s workforce participation rates. The gap has lessened from 17.8% in 2001-02 to 11.1% in 2016. While this is good news in terms of saving into superannuation, Australian women do more part time work than in other OECD countries. Gender equality in earnings will not happen unless there is more equal working time.

Women’s pay gapAustralia’s gender pay gap is currently 15.3%: this gap has wavered between 15% to 19% for over 20 years. Australia sits roughly in the middle of OECD countries in terms of the level of the gender pay gap.

Job segregation“Job segregation” means both what types of industries women work in compared with men as well as the level of the roles women work in within an industry.

A 2012 analysis of OECD data by K Rawstron found that in the mid-1980s, “Australia held the title for the most sex segregated labour force in the OECD area.” In 2015-16, the Workplace Gender Equality Agency found that six in 10 Australian employees work in an industry which is dominated by one gender. Job segregation impacts on levels of pay and therefore superannuation savings.

Level of support for child care costsWomen’s workforce participation rate is, in part, linked to the degree of financial support for child care. The International Monetary Fund has noted that if the price of child care is reduced by 50 percent, the labour supply of young mothers will rise in the order of 6.5-10 percent. The OECD has noted that Australia has a relatively low spend on early child hood education and childcare compared with other OECD countries.

EQUITY FEBRUARY | MARCH 2018 5

4. Lifecycle constraintsUnpaid time spent by women contributes to the superannuation gender gap. Australian women spend more time on unpaid work such as caring for household members or in doing housework than women in other OECD countries.

5. Superannuation system inequalities Women’s savings inequalities leading up to retirement are highlighted and indeed exacerbated by policy settings.

TaxationIn 2013, the International Monetary Fund found that women are more responsive to taxes than men. This could be applied to various areas which impact on the superannuation gender gap including applying lower tax rates for secondary earners (eg. Canada), tax incentives to return to work, as well as to the superannuation system itself.

Currently, the superannuation tax system disproportionately adversely affects women (as well as male part-time and low income earners). This is because of the three stages of taxing superannuation:

1. Concessional tax on money being paid into superannuation.

2. Concessional tax on money invested in superannuation.

3. Zero tax on money being withdrawn from superannuation if the person is aged 60 years or more. Previously, there was tax on retirement moneys if they were over a certain threshold.

Women who are generally paid less than men and accumulate less money in superannuation than men are ‘hit’ by stage 1 and 2 and usually do not accumulate sufficient money to have been affected by stage 3. The current taxation system favours those who earn more and accumulate superannuation savings over a long time. A re-distribution of tax concessions is needed.

Contributions while not workingIn order to recognise that women do take career breaks (and, indeed, to encourage women back to work), superannuation payments should also be made on paid parental leave.

Superannuation employer contributions on all wages paidCurrently, employers do not have to pay Superannuation Guarantee contributions on wages of below $450 per month. This primarily affects women and other part-time and low income wage earners.

A kick-startWomen in Super and AIST advocate that an additional annual $1,000 government contribution into super should be made for low income earners, to better support those with inadequate retirement savings.

AdequacyThe progressive increase to Superannuation Guarantee contributions from 9.5% to 12% of wages has been put on hold.

6. A gender lens should be applied to policy development

In order to reduce a problem such as women’s superannuation savings gap, it is important that:

1. The problem should be recognised.

This could be done by including in an objective for the superannuation system that the system is well adapted to meeting the needs of women and men.

2. The problem should be regularly measured.

This is occurring through the Workplace Gender Equality Agency.

3. Any proposed policy changes should be assessed to gauge whether the women’s superannuation savings gap would be reduced.

AIST has developed a method for addressing this — the AIST-Mercer Super Tracker. Policies can be put through the Tracker to see whether the 10 key performance indicators are improved or adversely affected by the proposed policy. One of the key performance indicators is the gender superannuation gap.

Concluding remarksThis article has reported some of the key inputs which generate a lower superannuation savings balance for women. Some solutions — such as the $1,000 kick start contribution — may be a faster item to implement. Many other solutions — such as reducing the gender pay gap — may have a longer term timeframe. All of these key issues need constant monitoring. In 2015, the Senate Economics References Committee for Economic Security for women in retirement provided an extremely useful plan for helping to close the superannuation gender gap. Most of the recommendations remain unimplemented at this stage E

6 FEBRUARY | MARCH 2018 EQUITY

As the local share market has clocked off on 2017 with double-digit percentage gains (all-in) for the second calendar year in a row, maybe it's time for investors to zoom in on what has been happening underneath the surface of this unexpectedly robust bull market?

No doubt, this year's shareholders in a2 Milk (A2M), Mineral Resources (MIN), WiseTech Global (WTC), et al cannot help but showcase a big smile connecting ear to ear, but most Australians also have a large exposure to banks, Telstra, Wesfarmers and other large cap companies and those have largely been laggards over the past five years.

Since mid-2012, most indices in Australia have generated circa 7% ex-dividends per annum. For the ASX20 that number drops to a mere 5% per annum.

On my assessment, what we are witnessing here is the gradual but undeniable impact from technological disruption, regulatory scrutiny and increased competition; factors that within the Australian context were always going to impact hardest on sectors that not so long ago were dominated by well-entrenched duopolies that are by now forced to defend their turf, and to rethink their strategy.

Witness recent restructuring announcements made by Telstra, QBE, National Australia Bank, Santos, Origin Energy and AMP.

But, of course, none of the problems these companies are facing today started earlier last year. In each case there is but a valid argument to be made the operational environment started to get tougher back in 2012. It takes a while before management teams acknowledge the new environment is here to stay.

Then they still have to formulate a response.

It would be premature to now take the view these companies will remain operating under a huge cloud permanently, but at the same time, keeping the fingers crossed that tomorrow everything shall be alright seems rather optimistic. Such challenges and processes take time and they seldom go hand in hand with excellent shareholder return in the meantime.

Which is why I am advocating investors adopt a risk-updated, three layered view of the local share market:

Group one: companies that are under threat and need to review their modus operandi and their strategy to stay relevant in the future;

Group two: companies that are not impacted by changing dynamics and might possibly even be beneficiaries;

Group three: upcoming companies that are inflicting the disruption to existing market positions and business models.

It goes without saying each of these three groups represents a different risk profile. In a generalised sense, companies in group one should de-rate until more clarity is forthcoming about how each company is dealing with the threats and challenges coming towards it. Companies in group two should trade at a premium. They represent the least risk from a sustainable operational point of view.

Is it coincidence then that quality healthcare stalwarts like CSL (CSL) and Cochlear (COH) are trading at a premium to the broader market, as well as to their own historical market premia?

Companies in group three offer lots of potential and excitement, but many are in early stage development still and thus highly vulnerable themselves to sudden changes, incumbent responses and unforeseen pitfalls. Note that in some cases young companies that IPO-ed at

the ASX only a few years ago have already been disrupted before they managed to fulfil the promises upon which they became a listed public entity. iSentia (ISD) comes to mind, as well as Freelancer (FLN).

Most importantly, just like the internet was real in the 1990s, very few of the original internet champions are still around twenty years later. Just because innovation and disruption are tangible and real today, this does not mean that all emerging innovators and disruptors will by default prove successful. Surely the dismal experience with OnePage serves as a stern warning about the risks involved in group three.

For companies in group one, it's probably best investors resist looking over their shoulder into the past when trying to assess what the future might bring. On my observation, the past five years have impacted through two very different scenarios for companies and/or sectors affected.

Under a best case scenario, share prices carve out an extended sideways channel of multi-year duration on price charts. Probably the best example of this is being provided by Wesfarmers whose share price has traded between mid-$30s and mid-$40s since late 2012. It doesn't take much imagination to see a similar trend on price charts for Australian banks, with the exception of Macquarie Group (MQG).

Things look a lot worse in case of scenario number two whereby share prices end up being encapsulated inside a long term down trend. Take a look at a multi-year price chart of Coca-Cola Amatil and you shall have no problem understanding what I am talking about. FlexiGroup is another example.

The experience from mining and energy stocks between 2012 and early 2016 shows buying cheap stocks doesn't work when there's a persistent down trend. At least companies such as BHP (BHP), Fortescue Metals (FMG) and Whitehaven Coal (WHC) have since been rescued by a significant recovery in commodity prices. But what about Myer? Fairfax Media?

Investors trying to scoop up cheap looking stocks better make sure they are not committing themselves to value traps dressed up like a long-term opportunity. Telstra (TLS) comes to mind too.

As far as group three is concerned, here there are always plenty of promising, exciting stories, but many prove ephemeral as business models are immature and unproven and the future remains as unpredictable as ever. Yet, the years past have also proven Australia remains an outstanding breeding ground for high quality, fast growing, sustainable new technology companies. Names like Wisetech Global (WTC), Altium (ALU) and Appen (APX) are increasingly attracting widespread praise and investor attention.

There is every reason to assume these companies will be around for a long while, and growing strongly for many more years. This is how micro cap stocks become small cap stocks, then mid-cap. This process is arguably well-advanced for the companies mentioned.

Admittedly, strongly rising share prices have excited ever more traders and investors and valuations seem a lot less attractive than they were only a short while ago, but an experienced investor knows the importance of patience and of being ready when opportunity knocks. I suggest keep a list, do your research, add regular updates and market observations.

But don't shy away as these companies represent Australia's, and the world's, future.

A three pronged investment strategyBy Rudi Filapek-Vandyck Editor, FNArena

Other names that come to mind at significantly lower valuations include Integrated Research (IRI), Nanosonics (NAN), Class (CL1) and, of course, one of my personal long-standing favourites, TechnologyOne (TNE).

There are not many companies on the ASX that can boast double-digit growth in earnings per share in each of the years that make up the past decade, with notable exception of the financial year just passed when growth didn't exceed 9%. That was a bad year in TechnologyOne parlance (!).

And boy did investors take notice. TechnologyOne shares have lagged the broader market in 2017. In my view, share price weakness post the stock going ex dividend in late November provides an excellent buying opportunity for investors looking for an attractive long term investment.

Analyst Gareth James at Morningstar is of a similar mindset. Morningstar has a stringent valuation based rating methodology and below $5.22 the shares are on the cusp of being upgraded to Accumulate from Hold, this despite the fact the PE multiple sits around 29.6x on FY18 estimates.

Apart from the company's 99% customer retention rate, and a conservative and lazy balance sheet (no debt), Morningstar suggests investors should zoom in on the projected 15% EPS CAGR for the

decade ahead. That's even better than the 11% average that has been achieved over the decade past.

I note that Bell Potter too has now added TechnologyOne to its list of top stock picks for 2018, alongside fellow tech stocks The Citadel Group (CGL) and Appen, as well as emerging disruptors such as AfterpayTouch (APT), OneVue Holdings (OVH), and others.

Watch list of ASX-listed stocks & disruptors for long term investors

Afterpay Touch APT Online lay-by (but it's about data really)

Appen APX Speech technology and search algorithms

Altium ALU Electronics design software for engineers

Class CL1 SMSF administration software

Corporate Travel CTD Travel management for the corporate market

Hansen Technologies HSN Customer care and billing software

Integrated Research IRI Diagnostics for business-critical computing

TechnologyOne TNE Enterprise software moving into the cloud

Wise Tech Global WTC Integrated supply chain logistics management

Xero XRO Cloud service for accountants

By Rudi Filapek-Vandyck, Editor FNArena. FNArena offers unique tools and analysis for self managing investors at www.fnarena.com. ASA members can request a one month free trial via [email protected]

In accordance with clause 43(c) of our constitution we are calling for nominations to our Board of Directors. Nominations can only be received at least eight weeks, but no more than twelve weeks, prior to the AGM to be held in Sydney on Tuesday 22 May 2018. Nomination forms are available: www.australianshareholders.com.au/asas-own- corporate-governance and is to be signed by two other members. Nomination period: Tuesday 27 February 2018 to COB Tuesday 28 March 2018

CALL FOR DIRECTOR NOMINATIONS 2018

All nominations must consist of the following: 1. A completed ASA director nomination form 2. Your curriculum vitae highlighting your skills, expertise, experience and a statement outlining how you can enhance the education offerings, advocacy and overall growth of ASA. All nominations must be received at the registered office of the ASA by no later than COB Tuesday 28 March 2018 or emailed to [email protected]. For further information please call 1300 368 448.

E

8 FEBRUARY | MARCH 2018 EQUITY

Exchange traded funds (ETFs) have grown to become an increasingly popular investment vehicle for Australian retail and institutional investors with around $35 billion invested in the sector. Despite their success, or likely because of it, there are a number of myths being spread about ETFs. This article provides the facts behind ETFs and busts some common myths.

Myth 1: ETFs are a fadETFs have, in fact, been on the scene for almost 30 years. The world’s first ETF was launched in Canada in 1990, and the first ETF listed in the US in 1993 and 2001 in Australia.

ETFs are passive funds that are traded on an exchange. They aim to track a benchmark index, in contrast to active funds, which seek to outperform a benchmark. The rise of passive investing since the GFC has coincided with a significant decline in active investing. It has been well documented that passive funds now far exceed flows to active funds. This trend is reflected in in Australia.

Myth 2: ETFs are riskier than managed fundsETFs are in fact managed funds, that is, investors’ money is pooled together and managed by a professional investment manager.

Standard or ‘physical ETFs’ buy the investments such as stocks or bonds that are in the underlying index. If you invest in an ETF, you will own units or shares in the ETF just like a managed fund and your main investment risk is the performance of the underlying assets, that is, the risk that asset prices will rise and fall in line with market movements.

The difference with managed funds is that ETFs are traded on the ASX, which provides greater liquidity. They are fully transparent so investors know in which assets they are invested. ETFs are generally lower cost than equivalent unlisted managed funds.

Myth 3: All ETPs are ETFsThere are many new types of exchange traded products (ETPs) that are not ETFs. Products labelled ‘exchange traded managed funds,’ ‘quoted managed funds,’ 'exchange traded commodities', 'exchange traded notes' or 'exchange traded securities' are not ETFs. A key feature of ETFs is the transparency of their portfolio holdings, which are reported daily.

Myth 4: ETFs are for short-term investorsA common myth is that ETFs are short term trading instruments only. But like any listed security, ETFs can be bought on an exchange and held for the long term. Investors buy ETFs to diversify and position their portfolios to achieve particular investment outcomes. A popular strategy is using ETFs as a core strategy and adding individual positions, or satellites, around that core.

Myth 5: ETFs create bubbles and inefficienciesA very common claim is that ETFs are responsible for market inefficiencies and create ‘bubbles’. This is a myth. In Australia, ETFs do not own enough of the stock market to move it in any meaningful way. The ASX’s total stock market value is $1.9 trillion, up from $1.5 trillion dollars in 2012. In that time ETFs grew from

$10 billion in 2012 to be around $35 billion, today of which only around 40% is invested in Australian equities.

So, ETFs represent just 1.7% of the stock market. Not nearly enough to move it let alone justify the claims they are creating the next bubble. In the US, the story is similar as the graph below illustrates.

Myth 6: ETFs create bubbles Even though ETFs are a small part of US equities, According to Bloomberg, they account for around 30% of the trading volume – double what it was 10 years ago.

Bloomberg claims “if more and more people stop trading stocks and bonds in favour of ETFs, it will drive up trading costs in the underlying securities while potentially making it more difficult to exit on big sell-off days.”

But currently in Australia ETFs represent just 2.5% of trading volume. This is nowhere near enough to distort share trading here.

Myth 7: ETFs inefficiently allocate resourcesAnother criticism of ETFs is that because of their large flows, ETFs have been distorting the market by buying stocks that active fund managers wouldn’t necessarily buy. The table below illustrates that active funds are buying the same stocks as the market capitalisation index in almost similar proportions.

Top 5 holdings of S&P/ASX 200 and select Active Managers

Source: Morningstar Direct, as at 30 September 2017. Stock highlighted orange appear in S&P/ASX 200 top 5.

The fact is, the ETF industry has recorded consistently high growth since its beginnings. As more ETF products are launched in Australia, investor choice is set to increase which is great for ASX investors. However, as ETFs grow, more will be written about them and its important investors educate themselves to understand the differences between myths and reality. E

Top 7 myths about ETFs bustedBy Arian Neiron Managing Director, VanEck Australia

This information is issued by VanEck Investments Limited ABN 22 146 596 116 AFSL 416755 (‘VanEck’). This is not a solicitation to buy or an offer to sell shares of any investment in any jurisdiction. It is general information only and not financial advice. It does not take into account any person’s individual objectives, financial situation or needs. Before making an investment decision in relation to any VanEck funds, you should read the relevant PDS and with the assistance of a financial adviser consider if it is appropriate for your circumstances. PDSs are available at www.vaneck.com.au or by calling 1300 68 38 37.

EQUITY FEBRUARY | MARCH 2018 9

Free 3 month subscription to the

Switzer ReportSwitzer is pleased to offer all ASA members a complimentary 3 month membership to the Switzer Report. The Switzer Report is a leading investment newsletter and website for self-directed investors.

When you subscribe, you’ll receive access to:

Our expert team of investment professionals

Our model income and growth stock portfolios

Weekly stock recommendations

Exclusive subscriber Q&A forum

The 2018 Investment Outlook

Monthly interactive webinars and more.

To receive your free subscription, visit

Switzer.com.au/ASA today!

Switzer ASA 3.indd 1 19/1/18 3:10 pm

10 FEBRUARY | MARCH 2018 EQUITY

Over the last few years, there has been a significant increase in the interest in environmental, social and governance (ESG) investing. According to a paper released recently, over $8trn of the $40trn of money managed in the USA is now under some form of Sustainable and Responsible Investing (SRI) or ESG, up 33% since 2014 and up fivefold from $1.4trn in 2012 for money run by fund managers.

In many respects Australian fund managers have been caught unready for this change. If we look at the Mercer survey data for January 2017, the Global Equities strategy section contains 127 global funds that are sold in Australia. Of this, only 5 are classed as SRI funds. It is somewhat better for Australian equities with 157 funds in the survey, of which 13 are SRI. If we were to use the ratio of assets in the USA, the number of SRI funds should be 27 and 34 respectively.

One reason could be that there is a view amongst many people (and particularly fund managers) that “you can’t have your cake and eat it too”: that SRI results in lower returns for investors and the investors have to pay a price to be responsible.

In some ways this misconception, of accepting lower returns for being ethical, goes against another tenant of conventional investing wisdom: buy good businesses. The grandfather of long term investing, Warren Buffett, discusses a lot in his letters to shareholders the importance of ethics and the quality of the character of the people running the businesses he owns.

Implicitly he is saying that businesses that have an ethos and focus on ‘doing the right thing’ by staff and customers, should generate higher returns. Now admittedly he is discussing the character of the people rather than the nature of the business, and some people would find owning Coca Cola unethical.

And it is this differentiation between good people and bad unethical businesses that opens an interesting next line of inquiry.

What do the statistics say?UBS recently published an excellent summary of recent academic literature1 looking at this question of whether SRI negatively affects investor returns. The conclusion was that it did not.

Verheyden, Eccles & Feiner (2016)2 wanted to look at whether a portfolio manager would be put at a disadvantage in terms of performance, risk and diversification if he/she were to start from a screen based on ESG criteria. The empirical evidence shows that all ESG-screened portfolios have performed very similarly to their respective underlying benchmarks, if not slightly outperforming

them. Put differently, the findings of the paper show that – at the very least – there is no performance penalty from screening out low ESG-scoring firms of each industry.

This is consistent with our own experience as portfolio managers at Hunter Hall, where we were able to outperform against an all-inclusive benchmark, despite having a restricted ownership list.

Taking another tack, Nagy, Kassam & Lee (2016)3 wanted to see if not only do highly rated ESG outperform, but do companies get rewarded for improving (going from OK to good)? The answer was yes and unequivocally yes. Both outperformed, but the improvers outperformed at double the rate.

But the most interesting article is one by Statman and Glushkov (2016)4. They created what they called “Top Minus Bottom” (TMB) where stocks were ranked on their ESG criteria and then modelled how being long the ‘better ranked’ versus the ‘worse ranked’ performed. This concept is similar to the studies above and could be called the “good screen”.

The innovation was to look at “Accepted Minus Shunned” (AMS) separately. Here the authors looked at the returns from stocks commonly accepted in SRI funds versus those that are typically avoided – shunned companies are those with operations in the tobacco, alcohol, gambling, military, firearms and nuclear industries. Call this the “negative screen”.

Like the earlier studies, it was found TMB outperformed the broader market but interestingly the AMS (the bad screen) stocks didn’t outperform, i.e. the excluded stocks did better than the broader market.

But here is the interesting thing: AMS under performed by less than the TMB screen outperformed, i.e. it was a net positive for investors. I think it is this AMS effect that fund managers have focused on in their view that SRI/ESG does not work.

What does this mean for fund managers?Investors globally are demanding more focus from their fund managers on ESG issues. The implications of these studies is that ESG does not detract from returns and investors are therefore not irrational to ask for more focus on ESG and SRI issues by their money managers.

But it also says running a positive screen in combination with running a negative screen is a better way to generate returns for investors whilst also satisfying investor’s ethical investment needs. E

Can socially responsible investing and good returns coexist? YESBy Chad Slater Joint CIO, Morphic Asset Management

Source http://www.ussif.org/files/Infographics/Overview%20Infographic.pdf

Chad Slater co-founded Morphic Asset Management in 2012. He was previously a Portfolio Manager and Head of Currency and Macroeconomics at Hunter Hall for five years. He has worked at BT Investment Management, Putnam and the Federal Treasury over his 15-year career.1 Academic Research Monitor: ESG Quant Investing. Dec 2016. Please email us if you’d like a copy of the paper. 2 ESG for All? The Impact of ESG Screening on Return, Risk, and Diversification. Verheyden, T., Eccles, R. G., & Feiner, A. Journal of Applied Corporate Finance, 28(2), 47-55, 20163 Nagy, Z., Kassam, A. & Lee, Linda-Eling. (2016) Can ESG Add Alpha? An Analysis of ESG Tilt and Momentum Strategies, Journal of Investing, Vol. 25, No. 2, pp.113-124.4 Statman, M., & Glushkov, D. (2016). Classifying and Measuring the Performance of Socially Responsible Mutual Funds. Journal of Portfolio Management, 42(2),140-151.

DO THE RIGHT THING. IT WILL GRATIFY SOME PEOPLE AND ASTONISH THE REST.Mark Twain

EQUITY FEBRUARY | MARCH 2018 11

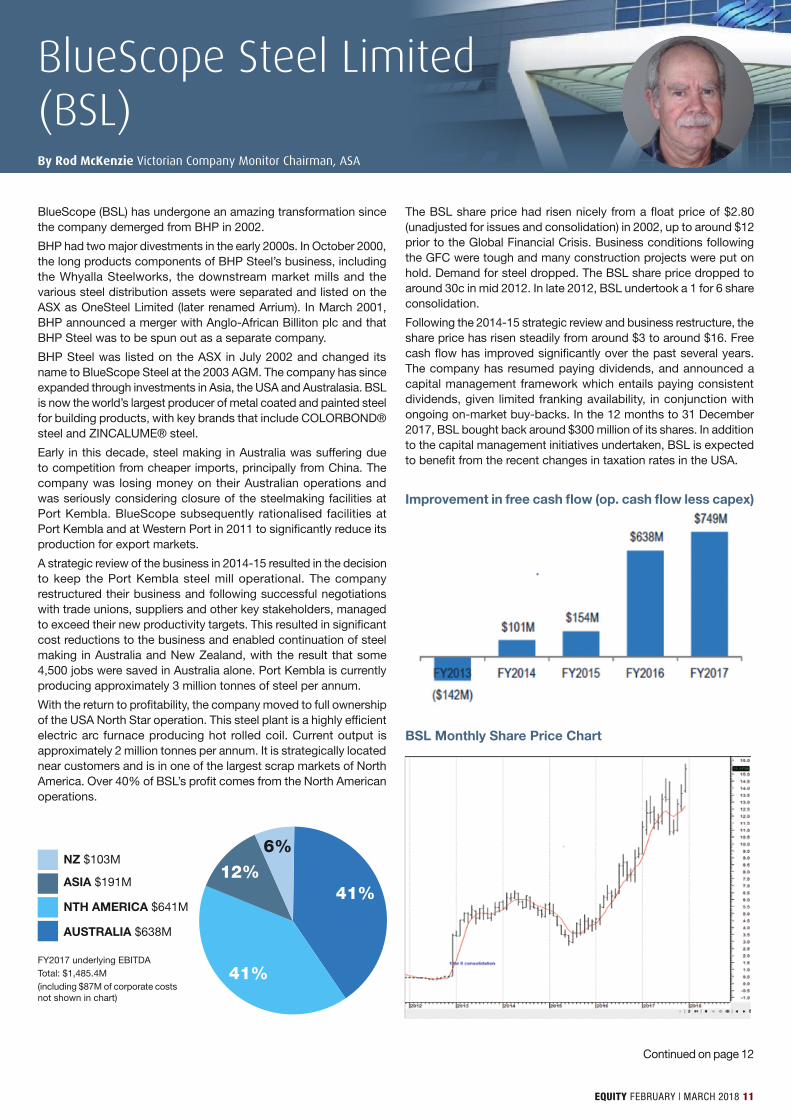

BlueScope (BSL) has undergone an amazing transformation since the company demerged from BHP in 2002.

BHP had two major divestments in the early 2000s. In October 2000, the long products components of BHP Steel’s business, including the Whyalla Steelworks, the downstream market mills and the various steel distribution assets were separated and listed on the ASX as OneSteel Limited (later renamed Arrium). In March 2001, BHP announced a merger with Anglo-African Billiton plc and that BHP Steel was to be spun out as a separate company.

BHP Steel was listed on the ASX in July 2002 and changed its name to BlueScope Steel at the 2003 AGM. The company has since expanded through investments in Asia, the USA and Australasia. BSL is now the world’s largest producer of metal coated and painted steel for building products, with key brands that include COLORBOND® steel and ZINCALUME® steel.

Early in this decade, steel making in Australia was suffering due to competition from cheaper imports, principally from China. The company was losing money on their Australian operations and was seriously considering closure of the steelmaking facilities at Port Kembla. BlueScope subsequently rationalised facilities at Port Kembla and at Western Port in 2011 to significantly reduce its production for export markets.

A strategic review of the business in 2014-15 resulted in the decision to keep the Port Kembla steel mill operational. The company restructured their business and following successful negotiations with trade unions, suppliers and other key stakeholders, managed to exceed their new productivity targets. This resulted in significant cost reductions to the business and enabled continuation of steel making in Australia and New Zealand, with the result that some 4,500 jobs were saved in Australia alone. Port Kembla is currently producing approximately 3 million tonnes of steel per annum.

With the return to profitability, the company moved to full ownership of the USA North Star operation. This steel plant is a highly efficient electric arc furnace producing hot rolled coil. Current output is approximately 2 million tonnes per annum. It is strategically located near customers and is in one of the largest scrap markets of North America. Over 40% of BSL’s profit comes from the North American operations.

The BSL share price had risen nicely from a float price of $2.80 (unadjusted for issues and consolidation) in 2002, up to around $12 prior to the Global Financial Crisis. Business conditions following the GFC were tough and many construction projects were put on hold. Demand for steel dropped. The BSL share price dropped to around 30c in mid 2012. In late 2012, BSL undertook a 1 for 6 share consolidation.

Following the 2014-15 strategic review and business restructure, the share price has risen steadily from around $3 to around $16. Free cash flow has improved significantly over the past several years. The company has resumed paying dividends, and announced a capital management framework which entails paying consistent dividends, given limited franking availability, in conjunction with ongoing on-market buy-backs. In the 12 months to 31 December 2017, BSL bought back around $300 million of its shares. In addition to the capital management initiatives undertaken, BSL is expected to benefit from the recent changes in taxation rates in the USA.

Improvement in free cash flow (op. cash flow less capex)

BSL Monthly Share Price Chart

BlueScope Steel Limited (BSL)By Rod McKenzie Victorian Company Monitor Chairman, ASA

Continued on page 12

FY2017 underlying EBITDATotal: $1,485.4M(including $87M of corporate costs not shown in chart)

NZ $103M

ASIA $191M

NTH AMERICA $641M

AUSTRALIA $638M

6%

12%41%

41%

Key risks to the business include the general economic climate, risks associated with dumping of cheaper overseas products, currency fluctuations and access to cheap, reliable energy for steel making operations. Some of these risks can be offset via currency hedging but supply of raw materials and supply of energy are critical to the ongoing economic operation of the business. BSL must maintain cost competiveness at Port Kembla to support a decision to reline the blast furnace in 10-15 years’ time. This major capital expenditure project will only be undertaken if the plant is profitable and the company can see a long-term future for steel making in Australia.

Steel is used in just about everything that is manufactured in the country. This includes steel structures, steel reinforcement in buildings, machinery construction and white goods. BSL – as a manufacturer of steel, is a major emitter of carbon dioxide. Conversion of raw materials to steel in a blast furnace involves a mix of iron ore, coal and coke and flux (limestone) supplied through the top of the furnace while a blast of hot air with oxygen enrichment is blown into the lower section. The end products are molten metal, slag and flue gases. These flue gases are a mix of

carbon dioxide, carbon monoxide, nitrous oxides and sulphurous oxides. Emissions are around 2.2 tonnes of CO2 equivalent per tonne of steel manufactured. The Port Kembla blast furnace is highly efficient and the company maintains close controls on energy efficiency and emissions. Whilst closure of the Port Kembla blast furnace would have the immediate effect of reducing BSL’s emissions, the equivalent steel production would have to be sourced from overseas operators with potentially higher overall emissions and the loss of almost 4,500 Australian jobs.

Strong management has been the key to BSL’s transformation. CEO & MD Paul O’Malley commenced in that role in 2007 and retired at the end of December 2017. Mr O’Malley was instrumental in restructuring the business and returning it to profitability. The company is in a much stronger financial position now than when he first took control. Incoming MD & CEO is Mark Vassella. The company is guided by a strong and experienced team of directors. The current chairman, John Bevan, took over from Graham Kraehe in 2015.

The ongoing focus on costs and the restructured business, should see BSL power on through the next decade. E

Surprise! A bank chair and CEO who stressed the importance of non-financialHappily very little time of the meeting was spent on past financial commentary. The chairman elaborated on the theme that to rebuild trust, business has to step outside traditional role as solely shareholder-focused organisations, and work in new ways that also put our customers and our communities at the centre of everything we do. The CEO carried this theme through with the statement our purpose is to shape a world where people and communities thrive. He then spent time outlining a number of initiatives the bank has undertaken with particular emphasis on utilising phones as mobile wallets and innovative products for small business.

After balance date the bank paid $50m and accepted liability for collusion on setting of the bank bill swap rate (BBSW). Staff have been fired, bonuses clawed back and new measures implemented to ensure does not happen again. No answer was provided to the ASA question as to the magnitude of the costs leading up to the decision to accept liability. Also after balance date the 20% holding in Shanghai Rural Commercial Bank was sold which will result in a $1.5 billion share buyback. Responding to ASA they will also consider some of the payments as special dividends. Although the sale won’t necessarily improve ROE, it should mean overall improvement on returns as executives can now focus on the parts of the business they are good at.

ASA believes that every shareholder should be given the opportunity to ask as many questions that they want, but 9 people asked basically the same two questions on climate change. Other questions dealt with tenure of auditors (30 years), last tender (never), the importance of treating staff better with change occurring (bigger retrenchment payments, more retraining).

More explanation was given as to why if ANZ did nothing dividends would drop by 300 basis points (amount and liquidity of capital that must be held plus bank tax). Target dividend rate was confirmed as 60-65% of profit.

Under the remuneration resolution discussion, ASA said that although the main relative total shareholders return hurdle for the long term incentive have not been met in 5 years, it was because the company had not performed as well as the comparative group which was not a reason to lower hurdles which CEO agreed with.

ASA voted for all the resolutions, with the final count of shares votes cast in favour in excess of 97%.

ANZ AGM

MONITORS: John Whittington, Allan Goldin attended AGM

Date 19th December 2017

Venue International Convention Centre Sydney

Attendees 301 shareholders plus 130 proxy holders and visitors

ASA proxies

8m shares (equivalent to 13th largest holder) from 1,956 proxies

Value of proxies

$236m

Proxies voted

Yes

Market cap $83 billion

Pre-AGM meeting

Yes with chairman David Gonski

1 year chart

BlueScope Steel Limited (BSL)Continued from page 11

EQUITY FEBRUARY | MARCH 2018 13

Effective business improvement and a new CEO in placeIt was the first meeting for new CEO Ms Jeanne Johns, a successful executive of major industrial and commodity-based businesses with experience in both the US and Asia, who commenced with the company in November 2017. Paul Brasher, the chairman, and CEO delivered presentations that did not add significantly to information provided in the annual report. While higher fertilizer volumes and improvement in the explosives market in the US have resulted in an increased profit and consequently some recovery in dividends and share price, both presentations reiterated the difficult conditions (price and cost pressures, exchange rates) under which the company operated, which confirms the importance of savings from Incitec’s business improvement programme ($176m in 2017). The recently announced loss of BHP explosive business was related to “increased capacity” in WA.

ASA asked questions about the timing of decisions and costs of the Gibson Island plant (more clarity in 3-6 months, costs will be balanced by the sale of land), impairment risk to Southern Cross (fully assessed) and the logic behind the share buy-back and its impact on LTI hurdles (best method of effective return of capital and impact not significant).

Other shareholders commented on the use of Western Sahara Phosphate rock (no purchases in 2017 and none so far this year) and the company’s increased output of greenhouse gases since 2011 (reflects the company’s growth, output per tonne of product has often decreased).

ASA also noted that directors had little “skin in the game”, asking whether the company had a policy (no was the answer). Only the chairman has a substantial holding (60,000), with other NED holding less than 20,000 shares as at 30 September 2017. On 24 November, after financial year end, we note Ms McGrath increased her shareholding to 25,008 shares.

On Ms McGrath’s re-election, ASA expressed concern about her workload. The chairman noted that Ms McGrath was very hard working and discussed with him any change in her other responsibilities such as her recent appointment as chair of Oz Minerals.

Ms McGrath was re-elected with 93.92% votes cast for the resolution. The other directors were elected and CEO performance rights passed with a vote over 99% and the remuneration report passed with a vote over 95%. All directors spoke briefly as to why shareholders should elect or re-elect them.

ASA spoke briefly with the chairman, CEO and non-executive director Kathryn Fagg after the meeting.

MONITORS: Ian Curry & Peter Aird

Date 21st December 2017

Venue Melbourne Exhibition Centre

Attendees 71 shareholders plus 54 visitors

ASA proxies

920,334 shares from 121 shareholders

Value of proxies

$3.5m

Proxies voted

Yes

Market cap $6.6 billion

Pre-AGM meeting

Yes with NED Kathryn Fagg

1 year chart

INCITEC PIVOT AGM

BANK OF QUEENSLAND AGM

Chairman Roger Davis delivers good results to happy shareholdersDirectors and executives socialised effortlessly with contented shareholders before the meeting over tea and snacks. We chatted with Belinda Jeffreys, Group Executive People and Communications, who told us the mood among staff was upbeat.

The meeting itself followed the usual formal protocol. Chairman Roger Davis spoke enthusiastically about BOQ’s excellent results this year and over the recent past. Shareholders were obviously happy which is not surprising given that BOQ enjoyed the highest total shareholder returns for 1, 3 and 5 years of any Australian listed bank. The 2017 year’s total return to shareholders was a robust 26.5%. Speaking to his re-election, Davis delivered a confident and factual but humble litany of the bank’s impressive accomplishments under his stewardship.

All items on the agenda passed with no significant protest votes on anything. The ASA was the only questioner on any agenda item.

ASA asked about directors’ skin in the game and received confirmation of the BOQ ‘understanding’ that directors should own one year’s worth of fees after three years on the board. Some directors were a bit short on ownership, and one claimed the problem lies in ‘blackout dates’, times in which directors have inside information that precludes them from acquiring more shares. We pointed out that certainly there must have been dates over the past six years (that particular director’s tenure) when she could have made a purchase. After the meeting, we were immediately approached by two directors with promises to ‘do better’ and acquire more shares. We had heard that story before and hope they would follow through on their promises during the 2018 year.

Matters post the 2017 AGM

One week following the AGM we received confirmation from BOQ’s Investor Relations representative that three directors had added to their holdings in BOQ. We are pleased and amazed that they were so quickly able to find a purchase date which didn’t conflict with their possession of inside information. Director Tredenick, who has been on the board for six years and who promised to ‘do better’ did not take the opportunity to increase her holdings this time.

MONITORS: Kelly Buchanan, Sally Mellick and Mike Stalley

Date 30th November 2017

Venue Hilton Hotel, Brisbane

Attendees 231

ASA proxies

1.45m shares (equivalent to 10th largest holder) from 317 proxies

Value of proxies

$19m

Proxies voted

Yes

Market cap $5.2 billion

Pre-AGM meeting

Yes with chairman Roger Davis

1 year chart

14 FEBRUARY | MARCH 2018 EQUITY

SEEK prepares for board renewalThe AGM started with the usual chairman’s address followed by CEO Andrew Bassat’s fast paced address which gave a broad overview of SEEK’s business performance and operations. During his address, Mr Chatfield announced that he would be stepping down as chairman of SEEK by around December 2018 and that a suitable replacement will be announced in due course. He also stated that long standing board member Colin Carter would also be stepping down in the early part of 2018. During his address, Mr Bassat spent a good portion of the AGM question time answering a variety of questions on performance as well as specifics of the business such as products and services. ASA had asked questions on international performance of the business and why it hadn’t seen improvements similar to those exhibited by the Australian arm, given both segments have been faced with depressed economic conditions. Andrew believes that the reinvestment is critical and that giving timelines and predicting outlooks is difficult.

We had asked about moving toward the inclusion of a remuneration table that includes an ‘actuals’ figure. ASA urged that a table is part of our efforts to educate our shareholders and to demonstrate that remuneration is a dynamic concept. Statutory reporting, while appears consistent does not explain the picture of the ups and downs of CEO pay. Chairman Neil Chatfield argued that all information that a shareholder needs to calculate actual figures can be ascertained in the annual report. Whilst this is true, a simple table will help eliminate the need to tease out figures from the annual report.

We also had a question from a shareholder with regard to the benefit of the Zhaopin privatisation and specifically how SEEK would make money from such a transaction. The chairman had explained that SEEK alongside private equity partners Hillhouse and FountainVest had bought back the public portion of shares outstanding. A question of defining new products and services was also asked to which Mr Bassat gave a detailed and elaborate response.

All items up for voting were approved. The remuneration report received 93% support and director election/re-election all receiving in excess of 97% votes in favour. Andrew Bassat’s equity rights and long term incentive resolutions did not fare as well, both receiving FOR votes of 89% and 72% respectively. ASA was later informed by SEEK company secretary that votes were negatively impacted by recommendations by proxy advisory Institutional Shareholder Services (ISS) and the Australian Council of Superannuation Investors (ACSI).

MONITOR: Claudio Esposito

Date 29th November 2017

Venue Sofitel on Collins, Melbourne

Attendees 30 shareholders plus 60 visitors

ASA proxies

305,320 shares from 98 shareholders

Value of proxies

$5.8m

Proxies voted

Yes

Market cap $6.4 billion

Pre-AGM meeting

Yes with chairman Neil Chatfield

1 year chart

SEEK AGM

Increasing profit, great future, low share priceThe CEO John Welborn gave an upbeat presentation outlining the great future prospects of their current African mines and future mines in Africa. With a long history on operating in the country, he stated that the company has a good understanding of the operating and social conditions that will lead to successful operations.

Gross profit increased to $177m from $155m, however NPAT decreased to $166m from $200m. While the dividend is only 2 cents per share, the company has a quirky arrangement with the Perth Mint to pay the dividend in gold bullion, or in cash, as selected by the shareholder. The Resolute share was $1.04 at the time of the meeting, compared with ten analysts’ forecasts ranging from $1.40 to $2.30 displayed by the CEO.

ASA questioned the board setup with director Peter Sullivan having five other directorships, and the CEO/Managing Director John Wellborn heavily involved in rugby in WA (Western Force). The chair replied that the board has successfully managed these outside interests and there is no deterioration in performance for the company.

ASA voted against the remuneration report due to the short-term incentive being entirely paid in cash and undisclosed internal targets. The FY17 result was 96% achieved, resulting in a short term incentive that looked like part of standard annual remuneration.

The long-term incentive uses a relative total shareholder target from a selected group of generally poor, low share price, performers, and pays 100% at the 75th percentile. For 100% award, they should beat all their peers. A second target, for reserve growth, pays 50% when growth is zero (production replaced with discoveries). This award should start at 0% for maintaining reserves as this is a day-to-day strategy to stay in business.

ASA voted in favour of the director elections. While Bill Price is no longer considered independent after 14 years on the board, three of the six person board are considered to be independent. ASA voted against the renewal of the performance rights plan, as this was just to preserve the 15% capital raising limit. To protect shareholders interests, vesting of performance rights should be included in the 15% capacity, and extra shares bought on market if required.

There were no other questioners on the resolutions.

All ten resolutions were passed with 99% support of shares voted, except for the re-election of director Henry Price where 89% of votes were cast in support.

MONITOR: Bob Kelliher

Date 28th November 2017

Venue Central Park Theatrette, 152-158 St Georges Tce Perth

Attendees 11 shareholders plus 46 visitors

ASA proxies

120,800 shares from 14 shareholders

Value of proxies

$125,600

Proxies voted

Yes

Market cap $748m

Pre-AGM meeting

Yes with chairman Martin Botha and director Yasmin Broughton

1 year chart

RESOLUTE MINING AGM

EQUITY FEBRUARY | MARCH 2018 15

First remuneration report strike for TPGExecutive chairman and CEO, David Teoh, opened the meeting, introduced key executives, and briefly reviewed the financial performance for the year and also confirmed margin headwinds that the group is facing as a result of the building of the NBN. This is considered by the board as the main reason for the fall in share price over the last year or so.

The CFO, Stephen Banfield, repeated the information in the annual report and explained the reconciliation from statutory net profit to underlying net profit. He also confirmed 2018 earnings before interest tax depreciation and amortisation (EBITDA) guidance of $800 to $815 million (compared to $891 million last). He also advised of TPG’s plans to build an internet system in Adelaide’s CBD that is 100 times faster than the NBN.

There were many questions from the floor mostly relating to operational matters, including one from ASA regarding cable versus wireless and the likelihood of cable becoming irrelevant in the future. ASA raised several issues regarding governance and remuneration disclosure. In particular, we suggested that there be more independent directors with an independent chairman. We also pointed out the company’s lack of disclosure regarding performance criteria used in the calculation of incentives, and stated that there should be some equity component in the award of short term incentives. The chairman, while polite, seemed to have little interest in any of these matters. He went on to advise that he had a very stable and not overpaid group of key personnel.

The matter of female board presence was also raised and the chairman stated that when they had the need for an additional board member or a replacement then this matter would be considered.

Mr Denis Ledbury spoke to his re-election as a non-executive director. ASA had several issues with his re-election, in particular, the claim as to his independence after 17 years on the board, the lack of an independent chairman and the fact that he has been chairman of the remuneration committee when the company has poor remuneration policy and governance.

ASA voted against the remuneration report and the re-election of Mr Ledbury. Proxy advisor, Ownership Matters, was reported in the media as being critical of remuneration policy disclosure. The voting outcome was the company receiving a first strike against the remuneration report with an against vote of 30% of shares voted (18% in 2016). The vote against Mr Ledbury was 16% votes cast. The board expressed disappointment with the remuneration report strike. It remains to be seen how they will respond in the 2018 report.

MONITORS: John Nesbitt, assisted by Mary Curran

Date 6th December 2017

Venue Barangaroo, Sydney

Attendees 55 shareholders plus 71 visitors

ASA proxies

1.1m shares from 176 shareholders

Value of proxies

$6.6m

Proxies voted

Yes

Market cap $5.6 billion

Pre-AGM meeting

Yes with NED Denis Ledbury

1 year chart

TPG TELECOM AGM

How much longer will Slater and Gordon remain a listed company?The attendance was barely half of that in 2016 possibly due to many shareholders having already divested. The anticipated fiery meeting did not eventuate.

Whereas at a normal AGM considerable time would be spent on the last year’s results the chairman just stated that details were already available in the annual report. No questions were asked as all present were aware that the primary purpose of this meeting was to decide on a major change in ownership and questions to the chairman and CEO regarding underperformance would be academic.

A major proxy advisor voted against the resolution for the remuneration resolution and there was a second strike (29% against). The ASA supported the resolution and said that although an against vote may seem punitive for poor company performance the implementation of remuneration policy in 2016-2017 had been firm and many issues were addressed following the 2016 strike.

A shareholder requested that each nominee director address the meeting. Merrick Howes stated that he would be representing only the interest of Anchorage. The ASA had intended to support the election of both Merrick Howes and Nils Stoesser but on hearing this abrogation of responsibility to represent all shareholders we voted against both of them. Both received 86% support. We supported James McKenzie who will be the next chairman. He spoke in recognition of proper governance responsibility and continued engagement with the ASA. He received 92% support.

A resolution to approve recapitalisation resulting in Anchorage Capital becoming a 95% shareholder was the major item of business. The ASA said that this outcome was a disaster for shareholders. Another said it was a catastrophe and the company should be put into administration so that shareholders could quickly claim tax losses. The chairman advised that shareholders could have divested and still could divest if they opted for tax losses. The ASA quoted from a press release we had issued in September i.e. “the deal with Anchorage Capital provides a recapitalisation platform which enables the opportunity for the security of the Australian business, its clients, employees and some hope for existing shareholders”. We said that this remains our position. The resolution was carried with 77% support and a subsequent resolution to apply a share consolidation on one for one hundred basis received 75% support. A major proxy advisor opposed both.

Following consolidation shares have been trading at with the code SGHDA at approximately $3.80. An offer to purchase a package of a value less than $500 is expected. The UK operation will not be a part of the ASX listed company. It remains to be seen how long Slater & Gordon will continue as a listed company.

MONITOR: Geoff Bowd

Date 6th December 2017

Venue Marriott Hotel Melbourne

Attendees 43 shareholders plus 26 visitors

ASA proxies

618,000 shares from 48 shareholders

Value of proxies

$25,000

Proxies voted

Yes

Market cap $15m

Pre-AGM meeting

Yes with chairman John Skippen

1 year chart

SLATER AND GORDON AGM

Historical landmark – a very different AGM from 200 years agoCelebrating a milestone a good quality book on WBC’s 200 years of operation was given out to those shareholders present and a well-presented book on ‘200 Women’ was available at reasonable cost.

Both chairman and CEO gave comprehensive overviews and these are available on WBC’s website. Copies of letter from pwc (WBC auditor) were available – this comprehensively answered a shareholder question about key internal processes adopted by pwc to ensure their (and members of WBC audit team) independence is not compromised.

The meeting was lengthy with domination mainly by one particularly unhappy shareholder, a distressed customer who has been in dispute with WBC for 6 years. A range of people raised issues around climate change generally and lending to companies such as Adani, Whitehaven Coal and Oil Search. Other questions/comments included CEO pay, political donations (no direct donations to political parties), length of product disclosure statements (looking at whether it is feasible to include a summary of main aspects), BT performance (some one-offs), partial sell down of BTIM, potential for buy backs and/or special dividends (nothing currently on the table), some compliments on their performance, extreme/offensive language of some Trading staff (as disclosed in current bank bill swap rate) case (chairman agreed it was not acceptable as well as regrettable that it was previously tolerated) and young people being a growing part of online business.

ASA complimented WBC on some of the positive aspects of WBC and its performance and acknowledged their 200 year achievement and the way they have leveraged that on various fronts. We asked for clarification on gender diversity figures for leaders and managers and WBC explained how they looked at their talent pipeline. We also queried current status of BBSW case with WBC indicating that it was close to finishing and then may be a while before judgement is handed down.

ASA notified their indication to vote against the remuneration report and the grant of equity to CEO, particularly as a fair value approach is taken on calculation methodology for allocation of performance rights. This is clearly outside ASA guidelines and out of line with other major banks as well as an increasing number of Top ASX 200 companies. ASA would also prefer a more rigorous vesting scale.

Votes cast were in favour of resolutions in a range of 93% for equity grant to CEO and up to 99.7% for re-election of Alison Deans.

MONITOR: Carol Limmer

Date 8th December 2017

Venue International Convention Centre Sydney

Attendees 515 shareholders plus 76 proxy holders and visitors

ASA proxies

11m shares from 2,164 shareholders

Value of proxies

$330m

Proxies voted

Yes

Market cap $107 billion

Pre-AGM meeting

Yes with chairman Lindsay Maxsted

1 year chart

WESTPAC AGM

BRICKBATS & BOUQUETS

BrickbatsTo NSX the operator of two stock exchanges (National Stock Exchange of Australia Limited and SIM Venture Securities Exchange Ltd), for not conducting a poll on the remuneration report. The AGM results from the November 2017 meeting recorded no remuneration strike on show of hands, but proxies were 80.9% against!

To Phileo Australia Limited who announced to the ASX a bonus of five million dollars to be paid to Mr Alfred Sung, Executive Director for long standing involvement with the company and in recognition of his excellent past performance in enhancing the growth and value of the company. The company has given minimal bonuses so remuneration reports have been approved in the past. Strange behaviour for a bonus to come out of the blue for a publicly listed company.

BouquetsTo Orocobre the mineral exploration company, for conducting its entitlement offer as a Pro-rata Accelerated Institutional with Tradeable Retail Entitlement Offer (PAITREO). Larger companies should take note, PAITREOs are retail shareholder friendly because they are fair.

Members are welcome to send in their suggestions to [email protected]. Comments included here do not necessarily reflect those of all members.

Date: Tuesday 27 March 2018 from 9.00am to 12.30pm, registration from 8.30am

Venue: Parramatta RSL, Cnr Macquarie & O’Connell Streets, Parramatta

Cost: $45 for ASA members and partners, $65 for non-members (members save $20)

To register: Call 1300 368 448 or go to australianshareholders.com.au/seminars-workshops

Arrium loss declarationKordaMentha has issued a loss declaration form for Arrium which allow members to realise their capital loss in 2017/18. You can download the loss declaration form from the creditor information section of KordaMentha website http://www.kordamentha.com/Creditors/Arrium-Group-of-Companies/Shareholders

Join us for seminar – 27 March

2017 AGM WRAP

Media coverage was solid, with more than one article published each day, for the quarter. The media pieces covered the ASA position in many of the monitored companies. By far the greatest coverage was devoted to Harvey Norman, where the chairman declines to speak directly with the ASA’s company monitor. Harvey Norman released the correspondence between the ASA and company to the ASX including the voting intentions, broadly distributing our concerns about the lack of board independence. ASA voted against all resolutions. A first strike on the remuneration report was narrowly avoided and there were significant against votes for director re-elections. Other meetings that were followed more intensely in the press were Commonwealth Bank, Ardent and Myer.

Both Ardent and Myer meetings had an element of struggle for control of each company. The financial results and share price performance for each company was disappointing and Ardent churned through three chairmen and three CEOS and two CFOs in one year. Major shareholders, Ariadne and Premier Investments, respectively, pitched for greater control of each company via the board rather than launching takeover offers.

For the entirety of 2017, overall ASA approval for remuneration reports increased to 67% for monitored companies (up from 62% last year). ASA voting was at odds with other shareholders in 17 of the 58 remuneration reports that received 98% support from votes cast, while supporting 24 out of the 43 receiving less than 90% support. For a number of companies, good price performance seemed to outweigh poor structure of rewards, while there were protest votes for poor performers despite significant changes to remuneration reports at other company meetings.

Focus issues garnered attention through the season. A number of companies have moved to use of face value (actual share price) rather than fair value for the allocation of equities (such as CSL, Qantas, Argo for 2018), while some included of a table of actual take home remuneration (e.g. CSL, Brambles). Board composition led to some against votes due to minority of independent directors and lack of diversity on a board. We saw a lift in director’s skin in the game at Incitec Pivot, Bank of Queensland (after the meeting). We took Beach Energy and WorleyParsons to task for a lack of fairness in capital raisings.

Our proxy position lifted by 1.7% on value for the 2017 when compared to 2016, while the number of proxies was down 5%. However last year 5% of the total 2016 proxies were represented by one meeting, the National Australia EGM to approve the CYBG demerger, where ASA received proxies from 1,532 holders with a share value of $190m. Each year a number of EGMs are held but they are not usually of this size. Nevertheless, we will be maintaining the focus on lifting the proxies awarded to the ASA during 2018.

Proxy positions were strong at the meetings where retail shareholders dominate the register. At the listed investment companies, Argo and AFIC, proxies awarded were equivalent to or greater than that of the largest shareholder. Proxies were equivalent to a top 10 shareholding for Commonwealth Bank, Bank of Queensland, Select Harvests, Woolworths, SCA Property Group and National Australia Bank, and equivalent to top 15 positions for Westpac, Platinum Asset Management, Retail Food Group, Telstra, BHP and ANZ Bank.

There were a number of first strikes for monitored companies with the following against votes: Karoon 56%, Myer 29%, Tatts 28% and TPG Telecommunications 30%. ASA voted in favour of the first three reports, and against TPG’s report. ASA voted in favour of the Karoon remuneration report, where no long-term incentive was paid due to a negative absolute TSR despite achieving a 60th percentile for its relative total shareholder return (TSR) hurdle. It seemed the major shareholders were dissatisfied with short-term incentive not being similarly cancelled.

In the case of TPG, little had changed from the prior year when an 18% against vote was recorded. While the quantum is not considered excessive and the long-term incentive plan duration had been extended from three to four years, there is no disclosure of performance criteria used for either the short- or long-term incentive plans.

Mineral Resources received a second strike with 41% vote against. In contrast, 99% of votes cast were against the spill motion. ASA voted in favour of the remuneration report after the company made changes to address two of our three concerns from 2016. Slater and Gordon also received a second strike – see the AGM report on page 15 of this issue.

As is usual for the ASA at this time of year, now we ready for the unfolding year’s challenges and opportunities. E

By Fiona Balzer Policy & Advocacy Manager, ASA

Year 2017

$ value of ASA proxies $3.9 bn

Proxies received 48,066

Companies monitored 174

Proxy collection companies 42

Company monitors 104

Average rem voting in favour

67%

Companies holding a poll 86%

EQUITY FEBRUARY | MARCH 2018 17

My first three months in the role of ASA Policy & Advocacy Manager was as expected, a whirlwind of voting intentions and AGMs. I have been amazed by the dedication of ASA company monitors and proxy collectors who attended 177 AGMs in the final quarter of the year. There were 126 pre-AGM meetings, and 141 Voting Intentions and AGM Reports were published. Logistics and the dedication of the ASA volunteers were crucial to the ASA attending 5 or more meetings on 11 separate days. The busiest day was 22 November, with 14 AGMs.

18 FEBRUARY | MARCH 2018 EQUITY

Whilst the festive season is now behind us, gift giving is not just limited to the goodies wrapped under the Christmas tree. This article considers the implications of gifting assets and making charitable donations and highlights certain factors that should be considered before making any gift.

Gift giving occurs for many reasons – supporting children, supporting charities, seeking tax deductions and estate planning – both whilst you are alive and after your death via your Will.

Gifting includes both giving away assets or money and also transferring assets for less than their market value. For example, if a parent transfers a property to their child for $200,000 but it's market value is $500,000, then this transaction includes a deemed gift of $300,000. Gifting is not, however, selling or reducing your assets to meet normal costs, for example giving away household items, or repaying a debt by transferring an asset in satisfaction thereof.

Social Security implicationsGifting assets will likely have implications for your entitlement to social security. For social security purposes, any 'gifts' made in the prior five years will be included in your asset and income tests and therefore may impact your eligibility for payments. Furthermore, gifting limits apply when you are receiving social security payments. These limits are $10,000 in one financial year and $30,000 in five financial years. Any gifts made which exceed these limits will be taken into account in your income and assets tests and may therefore negatively impact your entitlements.

It is important to note that social security not only considers gifts you may make but also a concept known as 'deprived income' – being income that you either refuse or give away and do not receive adequate compensation for. For example, Fred receives a superannuation pension of $6,000 per year and is offered an increase of $1,000 per annum. Fred refuses this increase as he doesn't want his Age Pension to be decreased. The $1,000 refused will be considered 'deprived income' and will be included in his income tests for the Age Pension regardless.