Embed Size (px)

Citation preview

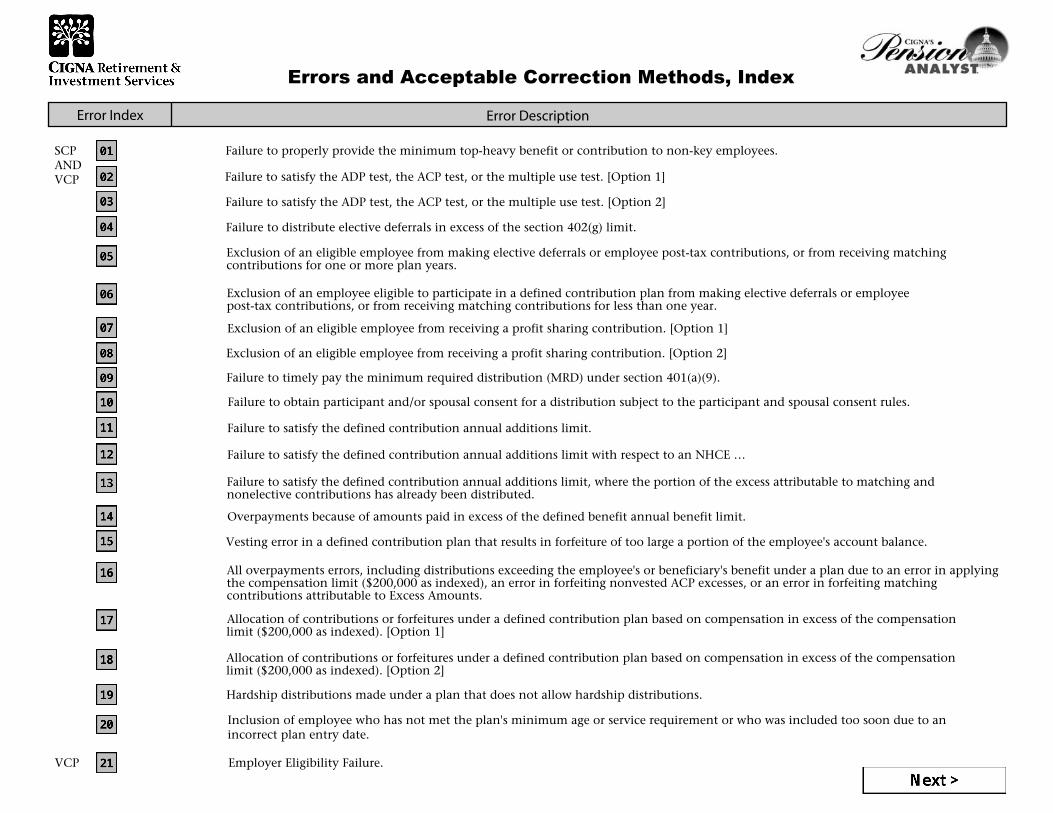

Errors and Acceptable Correction Methods, Index

SCP Failure to properly provide the minimum top-heavy benefit or contribution to non-key employees.ANDVCP Failure to satisfy the ADP test, the ACP test, or the multiple use test. [Option 1]

Failure to satisfy the ADP test, the ACP test, or the multiple use test. [Option 2]

Failure to distribute elective deferrals in excess of the section 402(g) limit.

Exclusion of an eligible employee from making elective deferrals or employee post-tax contributions, or from receiving matching � contributions for one or more plan years.

Exclusion of an employee eligible to participate in a defined contribution plan from making elective deferrals or employee �post-tax contributions, or from receiving matching contributions for less than one year.

Exclusion of an eligible employee from receiving a profit sharing contribution. [Option 1]

Exclusion of an eligible employee from receiving a profit sharing contribution. [Option 2]

Failure to timely pay the minimum required distribution (MRD) under section 401(a)(9).

Failure to obtain participant and/or spousal consent for a distribution subject to the participant and spousal consent rules.

Failure to satisfy the defined contribution annual additions limit.

Failure to satisfy the defined contribution annual additions limit with respect to an NHCE …

Failure to satisfy the defined contribution annual additions limit, where the portion of the excess attributable to matching and �nonelective contributions has already been distributed.

Overpayments because of amounts paid in excess of the defined benefit annual benefit limit.

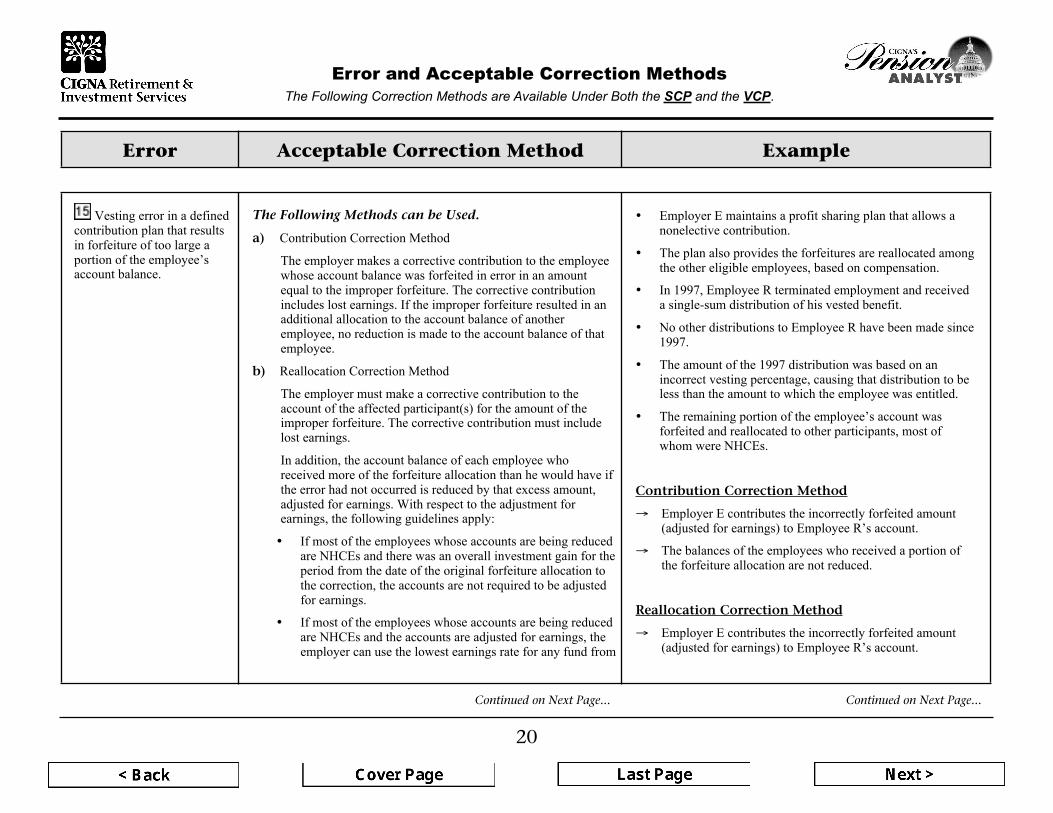

Vesting error in a defined contribution plan that results in forfeiture of too large a portion of the employee's account balance.

All overpayments errors, including distributions exceeding the employee's or beneficiary's benefit under a plan due to an error in applying�the compensation limit ($200,000 as indexed), an error in forfeiting nonvested ACP excesses, or an error in forfeiting matching�contributions attributable to Excess Amounts.

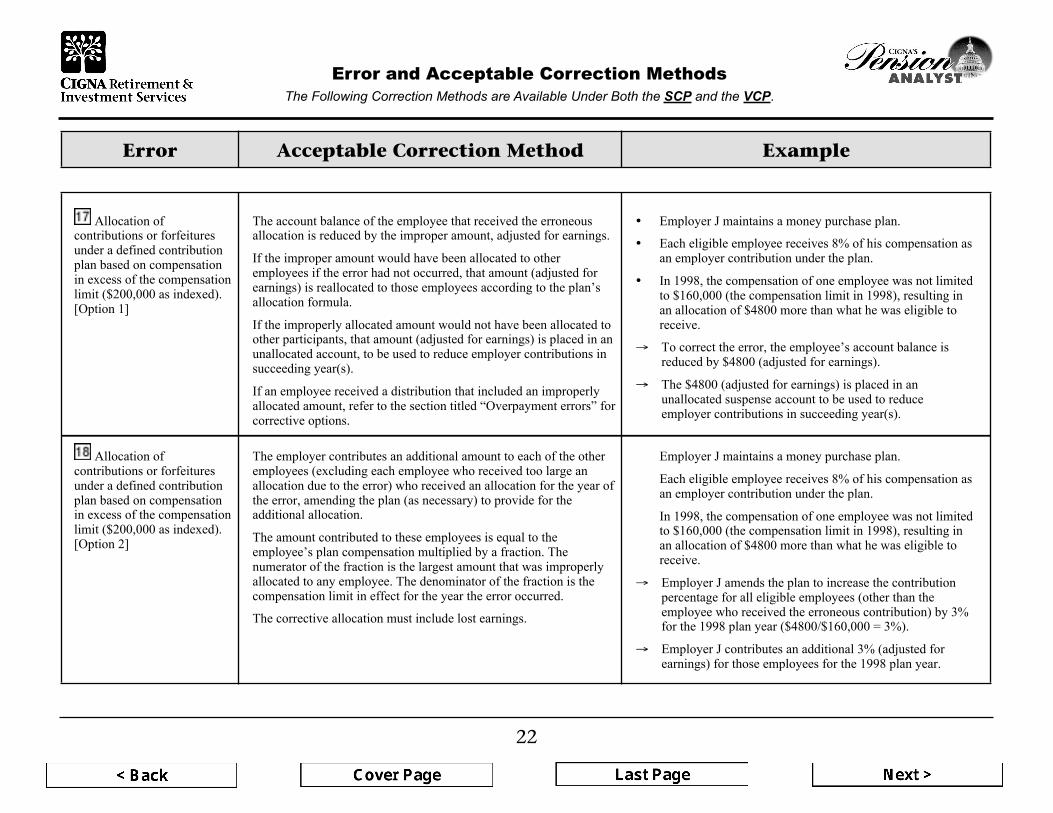

Allocation of contributions or forfeitures under a defined contribution plan based on compensation in excess of the compensation� limit ($200,000 as indexed). [Option 1]

Allocation of contributions or forfeitures under a defined contribution plan based on compensation in excess of the compensation�limit ($200,000 as indexed). [Option 2]

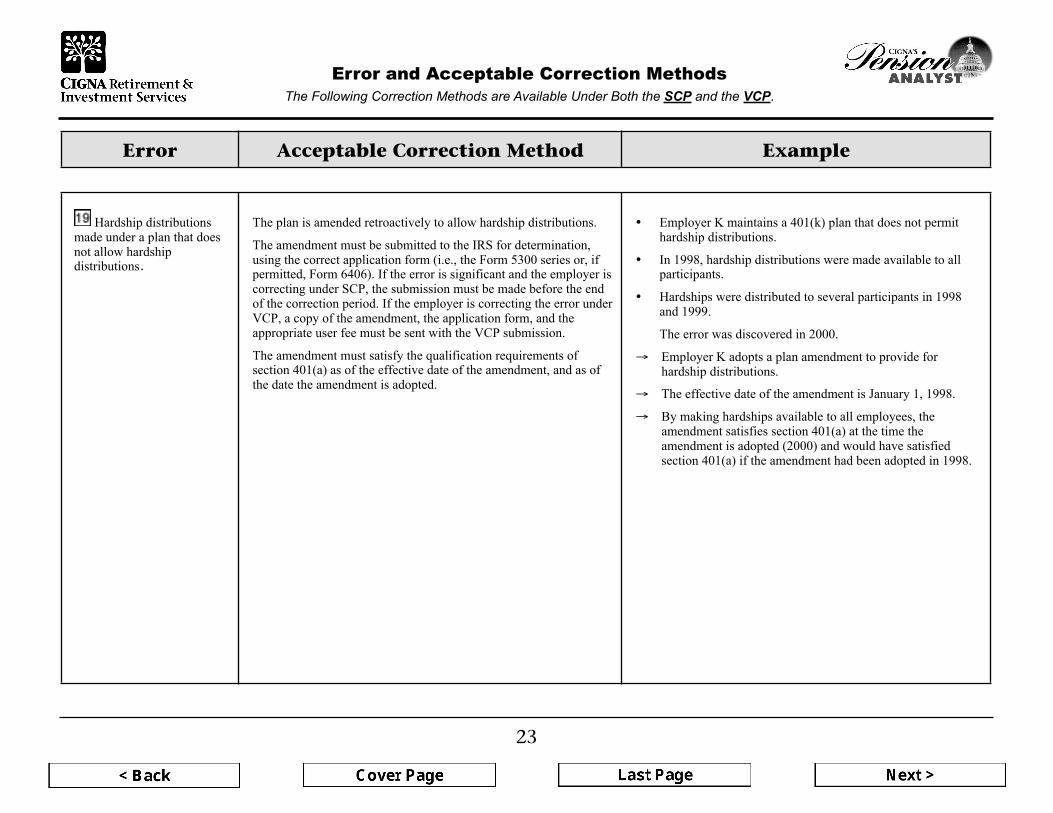

Hardship distributions made under a plan that does not allow hardship distributions.

Inclusion of employee who has not met the plan's minimum age or service requirement or who was included too soon due to anincorrect plan entry date.

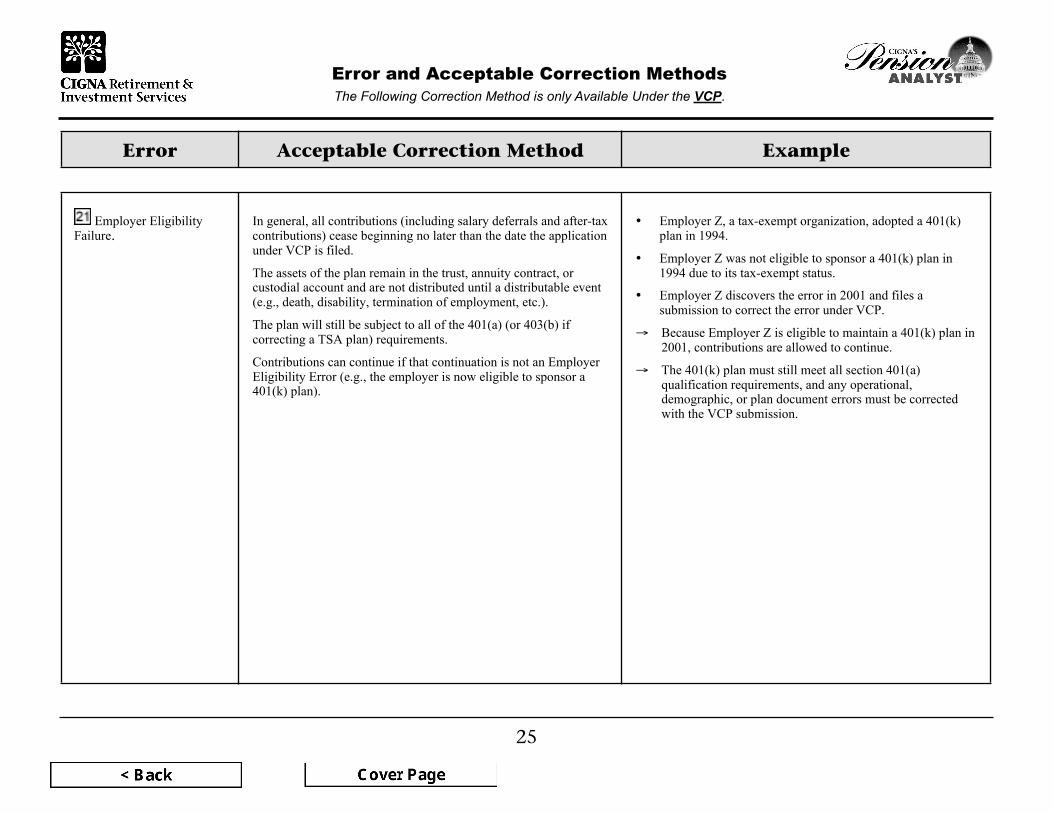

VCP Employer Eligibility Failure.

Error Index Error Description

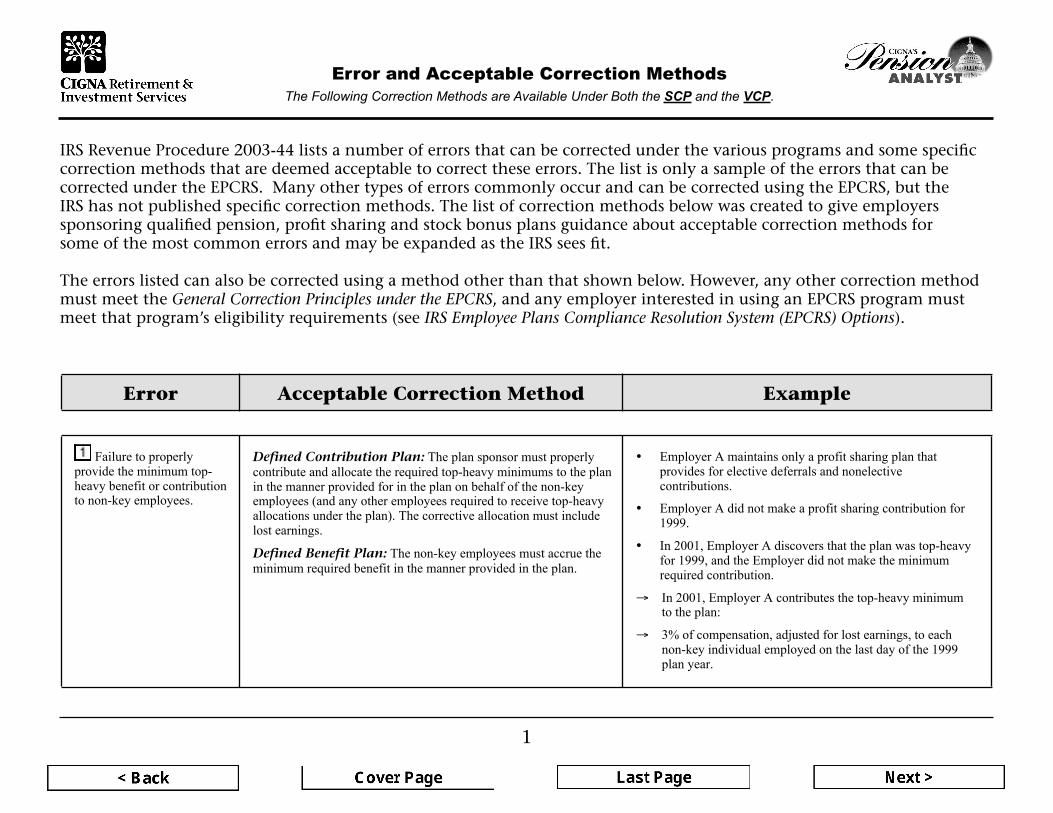

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

IRS Revenue Procedure 2003-44 lists a number of errors that can be corrected under the various programs and some specific correction methods that are deemed acceptable to correct these errors. The list is only a sample of the errors that can be corrected under the EPCRS. Many other types of errors commonly occur and can be corrected using the EPCRS, but the IRS has not published specific correction methods. The list of correction methods below was created to give employers sponsoring qualified pension, profit sharing and stock bonus plans guidance about acceptable correction methods for some of the most common errors and may be expanded as the IRS sees fit. The errors listed can also be corrected using a method other than that shown below. However, any other correction method must meet the General Correction Principles under the EPCRS, and any employer interested in using an EPCRS program must meet that program’s eligibility requirements (see IRS Employee Plans Compliance Resolution System (EPCRS) Options).

Errors and Acceptable Correction Methods

IRS Revenue Procedure 2003-44 lists a number of errors that can be corrected under the various programs and some specific correction methods that are deemed acceptable tocorrect these errors. The list is only a sample of the errors that can be corrected under the EPCRS. Many other types of errors commonly occur and can be corrected using theEPCRS, but the IRS has not published specific correction methods. The list of correction methods below was created to give employers sponsoring qualified pension, profitsharing and stock bonus plans guidance about acceptable correction methods for some of the most common errors and may be expanded as the IRS sees fit.

The errors listed can also be corrected using a method other than that shown below. However, any other correction method must meet the General Correction Principles underthe EPCRS, and any employer interested in using an EPCRS program must meet that program’s eligibility requirements (see IRS Employee Plans Compliance ResolutionSystem (EPCRS) Options).

1

Error Acceptable Correction Method Example

Failure to properlyprovide the minimum top-heavy benefit or contributionto non-key employees.

Defined Contribution Plan: The plan sponsor must properlycontribute and allocate the required top-heavy minimums to the planin the manner provided for in the plan on behalf of the non-keyemployees (and any other employees required to receive top-heavyallocations under the plan). The corrective allocation must includelost earnings.

Defined Benefit Plan: The non-key employees must accrue theminimum required benefit in the manner provided in the plan.

� Employer A maintains only a profit sharing plan thatprovides for elective deferrals and nonelectivecontributions.

� Employer A did not make a profit sharing contribution for1999.

� In 2001, Employer A discovers that the plan was top-heavyfor 1999, and the Employer did not make the minimumrequired contribution.

→ In 2001, Employer A contributes the top-heavy minimumto the plan:

→ 3% of compensation, adjusted for lost earnings, to eachnon-key individual employed on the last day of the 1999plan year.

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

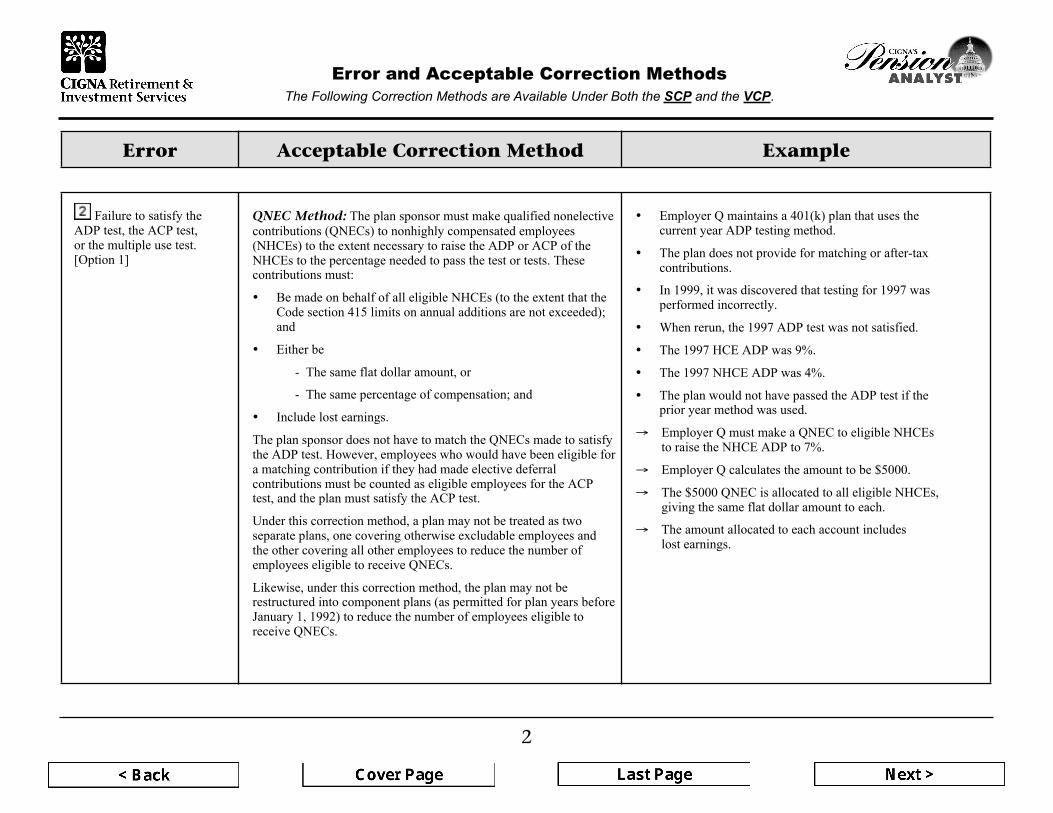

2

Error Acceptable Correction Method Example

Failure to satisfy theADP test, the ACP test,or the multiple use test.[Option 1]

QNEC Method: The plan sponsor must make qualified nonelectivecontributions (QNECs) to nonhighly compensated employees(NHCEs) to the extent necessary to raise the ADP or ACP of theNHCEs to the percentage needed to pass the test or tests. Thesecontributions must:

� Be made on behalf of all eligible NHCEs (to the extent that theCode section 415 limits on annual additions are not exceeded);and

� Either be

- The same flat dollar amount, or

- The same percentage of compensation; and

� Include lost earnings.

The plan sponsor does not have to match the QNECs made to satisfythe ADP test. However, employees who would have been eligible fora matching contribution if they had made elective deferralcontributions must be counted as eligible employees for the ACPtest, and the plan must satisfy the ACP test.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, under this correction method, the plan may not berestructured into component plans (as permitted for plan years beforeJanuary 1, 1992) to reduce the number of employees eligible toreceive QNECs.

� Employer Q maintains a 401(k) plan that uses thecurrent year ADP testing method.

� The plan does not provide for matching or after-taxcontributions.

� In 1999, it was discovered that testing for 1997 wasperformed incorrectly.

� When rerun, the 1997 ADP test was not satisfied.

� The 1997 HCE ADP was 9%.

� The 1997 NHCE ADP was 4%.

� The plan would not have passed the ADP test if theprior year method was used.

→ Employer Q must make a QNEC to eligible NHCEsto raise the NHCE ADP to 7%.

→ Employer Q calculates the amount to be $5000.

→ The $5000 QNEC is allocated to all eligible NHCEs,giving the same flat dollar amount to each.

→ The amount allocated to each account includeslost earnings.

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

3

Error Acceptable Correction Method Example

Failure to satisfy theADP test, the ACP test, or themultiple use test. [Option 2]

One-to-One Method: The plan sponsor

a) Distributes the excess amounts to the highly compensatedemployees (HCEs), and

b) Allocates an equal amount as a QNEC to the non-highlycompensated employees (NHCEs).

The excess amount to be returned to an HCE is the sum of anyexcesses determined from the ADP, ACP and multiple use tests,adjusted for earnings through the date of the correction.

Any amounts that were not vested as of the close of the plan year ofthe error are forfeited. Amounts forfeited are used according to theplan’s forfeiture provisions in place for the year of the error.

If an excess amount has already been distributed to an HCE, theemployer must notify the employee that the distribution was noteligible for favorable tax treatment, such as a tax-free rollover.

If an excess matching amount that should have been forfeited hasbeen paid to an HCE, this amount is an Overpayment that must becorrected (see Failure to satisfy the defined contribution annualadditions limit, where the portion of the excess attributable tomatching and nonelective contributions has already beendistributed).

The total QNEC amount to be allocated to NHCEs is the sum of allexcess contributions adjusted for earnings through the date of thecorrection, excluding forfeited related matching contributions.

The plan sponsor must pick the group of employees who will receivethe contribution from the following choices*:

� Individuals who were eligible to participate and were NHCEs inthe year of the error.

� Individuals who were eligible to participate and were NHCEsboth in the year of the error and the year of correction.

� Individuals who were eligible to participate and were NHCEs inthe year of the error, but who are still employees as of a date inthe year of correction that is no later than the date of correction.

� Individuals who were eligible to participate and were NHCEs

� Employer T maintains a 401(k) plan that uses the currentyear ADP testing method.

� The plan provides for matching and after-tax contributions.

� Matching contributions equal 50% of the sum of electivedeferrals and after-tax contributions that do not exceed 10%of the employee’s compensation.

� Matching contributions are subject to a 5-year gradedvesting schedule.

� Matching contributions are forfeited and used to reduceemployer contributions if associated elective deferrals orafter-tax contributions are distributed to correct an ADP,ACP or multiple use test failure.

� For 1997, only NHCEs made after-tax contributions.

� Two HCEs were eligible in 1997, Employee P andEmployee S.

� Employee P made elective deferrals of $8,000, which was10% of his compensation for 1997 ($80,000).

� Employee S made elective deferrals of $9,500, which was8% of his 1997 compensation ($118,750).

� Employee P received a matching contribution of $4,000(50% of $8,000).

� Employee S received a matching contribution of $4,750(50% of $9,500).

� Employees P and S were 100% vested in 1997.

� In 1999, it was discovered that testing for 1997 wasperformed incorrectly.

� When rerun, the 1997 ADP test was not satisfied.

� The 1997 HCE ADP was 9%.

� The 1997 NHCE ADP was 4%.

� The plan would not have passed the ADP test if the prioryear method was used.

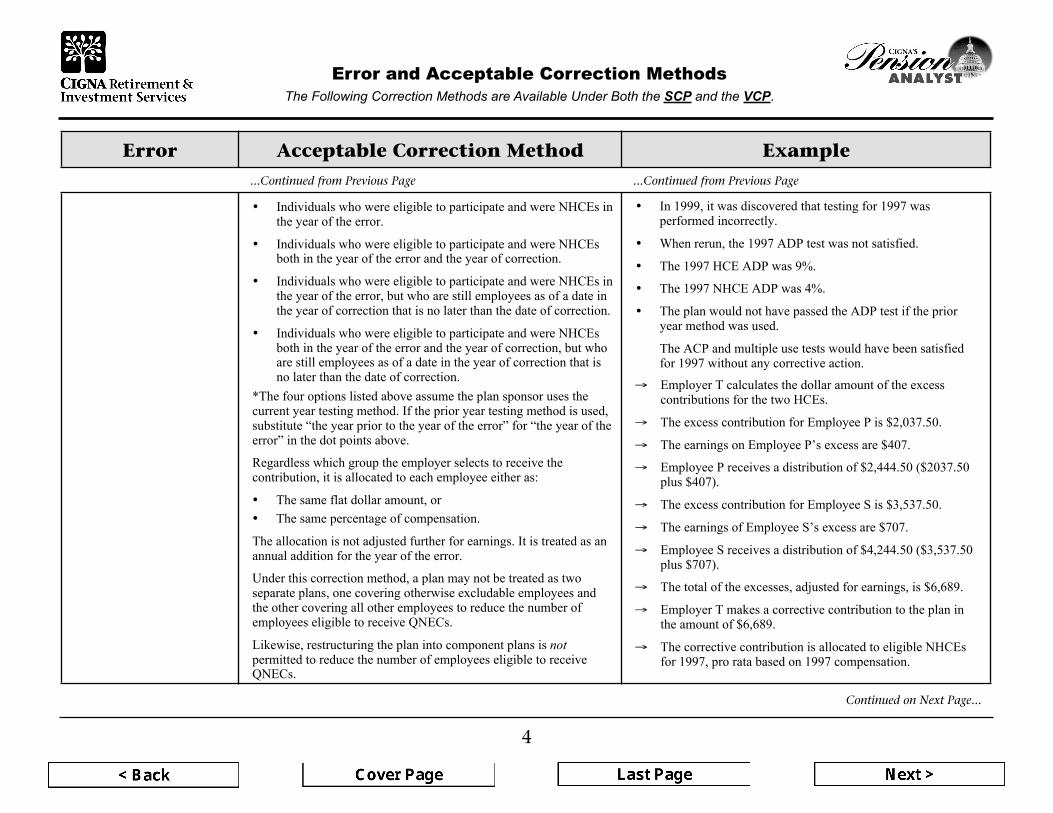

Continued on Next Page... Continued on Next Page...

both in the year of the error and the year of correction, but whoare still employees as of a date in the year of correction that isno later than the date of correction.

∞ The ACP and multiple use tests would have been satisfiedfor 1997 without any corrective action.

4

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

Error Acceptable Correction Method Example

Failure to satisfy theADP test, the ACP test, or themultiple use test. [Option 2]

One-to-One Method: The plan sponsor

a) Distributes the excess amounts to the highly compensatedemployees (HCEs), and

b) Allocates an equal amount as a QNEC to the non-highlycompensated employees (NHCEs).

The excess amount to be returned to an HCE is the sum of anyexcesses determined from the ADP, ACP and multiple use tests,adjusted for earnings through the date of the correction.

Any amounts that were not vested as of the close of the plan year ofthe error are forfeited. Amounts forfeited are used according to theplan’s forfeiture provisions in place for the year of the error.

If an excess amount has already been distributed to an HCE, theemployer must notify the employee that the distribution was noteligible for favorable tax treatment, such as a tax-free rollover.

If an excess matching amount that should have been forfeited hasbeen paid to an HCE, this amount is an Overpayment that must becorrected (see Failure to satisfy the defined contribution annualadditions limit, where the portion of the excess attributable tomatching and nonelective contributions has already beendistributed).

The total QNEC amount to be allocated to NHCEs is the sum of allexcess contributions adjusted for earnings through the date of thecorrection, excluding forfeited related matching contributions.

The plan sponsor must pick the group of employees who will receivethe contribution from the following choices*:

� Individuals who were eligible to participate and were NHCEs inthe year of the error.

� Individuals who were eligible to participate and were NHCEsboth in the year of the error and the year of correction.

� Individuals who were eligible to participate and were NHCEs inthe year of the error, but who are still employees as of a date inthe year of correction that is no later than the date of correction.

� Individuals who were eligible to participate and were NHCEsboth in the year of the error and the year of correction, but whoare still employees as of a date in the year of correction that isno later than the date of correction.

� Employer T maintains a 401(k) plan that uses the currentyear ADP testing method.

� The plan provides for matching and after-tax contributions.

� Matching contributions equal 50% of the sum of electivedeferrals and after-tax contributions that do not exceed 10%of the employee’s compensation.

� Matching contributions are subject to a 5-year gradedvesting schedule.

� Matching contributions are forfeited and used to reduceemployer contributions if associated elective deferrals orafter-tax contributions are distributed to correct an ADP,ACP or multiple use test failure.

� For 1997, only NHCEs made after-tax contributions.

� Two HCEs were eligible in 1997, Employee P andEmployee S.

� Employee P made elective deferrals of $8,000, which was10% of his compensation for 1997 ($80,000).

� Employee S made elective deferrals of $9,500, which was8% of his 1997 compensation ($118,750).

� Employee P received a matching contribution of $4,000(50% of $8,000).

� Employee S received a matching contribution of $4,750(50% of $9,500).

� Employees P and S were 100% vested in 1997.

� In 1999, it was discovered that testing for 1997 wasperformed incorrectly.

� When rerun, the 1997 ADP test was not satisfied.

� The 1997 HCE ADP was 9%.

� The 1997 NHCE ADP was 4%.

� The plan would not have passed the ADP test if the prioryear method was used.

∞ The ACP and multiple use tests would have been satisfiedfor 1997 without any corrective action.

*The four options listed above assume the plan sponsor uses thecurrent year testing method. If the prior year testing method is used,substitute “the year prior to the year of the error” for “the year of theerror” in the dot points above.

Regardless which group the employer selects to receive thecontribution, it is allocated to each employee either as:

� The same flat dollar amount, or

� The same percentage of compensation.

The allocation is not adjusted further for earnings. It is treated as anannual addition for the year of the error.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

→ Employer T calculates the dollar amount of the excesscontributions for the two HCEs.

→ The excess contribution for Employee P is $2,037.50.

→ The earnings on Employee P’s excess are $407.

→ Employee P receives a distribution of $2,444.50 ($2037.50plus $407).

→ The excess contribution for Employee S is $3,537.50.

→ The earnings of Employee S’s excess are $707.

→ Employee S receives a distribution of $4,244.50 ($3,537.50plus $707).

→ The total of the excesses, adjusted for earnings, is $6,689.

→ Employer T makes a corrective contribution to the plan inthe amount of $6,689.

→ The corrective contribution is allocated to eligible NHCEsfor 1997, pro rata based on 1997 compensation.

→ Employee P’s and Employee S’s matching contributionsrelated to the distributed excesses, adjusted for earnings,are forfeited.

→ The forfeited amounts are used to reduce contributions for1999 and subsequent years.

Continued on Next Page...

...Continued from Previous Page ...Continued from Previous Page

Failure to satisfy theADP test, the ACP test, or themultiple use test. [Option 2]

One-to-One Method: The plan sponsor

a) Distributes the excess amounts to the highly compensatedemployees (HCEs), and

b) Allocates an equal amount as a QNEC to the non-highlycompensated employees (NHCEs).

The excess amount to be returned to an HCE is the sum of anyexcesses determined from the ADP, ACP and multiple use tests,adjusted for earnings through the date of the correction.

Any amounts that were not vested as of the close of the plan year ofthe error are forfeited. Amounts forfeited are used according to theplan’s forfeiture provisions in place for the year of the error.

If an excess amount has already been distributed to an HCE, theemployer must notify the employee that the distribution was noteligible for favorable tax treatment, such as a tax-free rollover.

If an excess matching amount that should have been forfeited hasbeen paid to an HCE, this amount is an Overpayment that must becorrected (see Failure to satisfy the defined contribution annualadditions limit, where the portion of the excess attributable tomatching and nonelective contributions has already beendistributed).

The total QNEC amount to be allocated to NHCEs is the sum of allexcess contributions adjusted for earnings through the date of thecorrection, excluding forfeited related matching contributions.

The plan sponsor must pick the group of employees who will receivethe contribution from the following choices*:

� Individuals who were eligible to participate and were NHCEs inthe year of the error.

� Individuals who were eligible to participate and were NHCEsboth in the year of the error and the year of correction.

� Individuals who were eligible to participate and were NHCEs inthe year of the error, but who are still employees as of a date inthe year of correction that is no later than the date of correction.

� Individuals who were eligible to participate and were NHCEsboth in the year of the error and the year of correction, but whoare still employees as of a date in the year of correction that isno later than the date of correction.

� Employer T maintains a 401(k) plan that uses the currentyear ADP testing method.

� The plan provides for matching and after-tax contributions.

� Matching contributions equal 50% of the sum of electivedeferrals and after-tax contributions that do not exceed 10%of the employee’s compensation.

� Matching contributions are subject to a 5-year gradedvesting schedule.

� Matching contributions are forfeited and used to reduceemployer contributions if associated elective deferrals orafter-tax contributions are distributed to correct an ADP,ACP or multiple use test failure.

� For 1997, only NHCEs made after-tax contributions.

� Two HCEs were eligible in 1997, Employee P andEmployee S.

� Employee P made elective deferrals of $8,000, which was10% of his compensation for 1997 ($80,000).

� Employee S made elective deferrals of $9,500, which was8% of his 1997 compensation ($118,750).

� Employee P received a matching contribution of $4,000(50% of $8,000).

� Employee S received a matching contribution of $4,750(50% of $9,500).

� Employees P and S were 100% vested in 1997.

� In 1999, it was discovered that testing for 1997 wasperformed incorrectly.

� When rerun, the 1997 ADP test was not satisfied.

� The 1997 HCE ADP was 9%.

� The 1997 NHCE ADP was 4%.

� The plan would not have passed the ADP test if the prioryear method was used.

∞ The ACP and multiple use tests would have been satisfiedfor 1997 without any corrective action.

*The four options listed above assume the plan sponsor uses thecurrent year testing method. If the prior year testing method is used,substitute “the year prior to the year of the error” for “the year of theerror” in the dot points above.

Regardless which group the employer selects to receive thecontribution, it is allocated to each employee either as:

� The same flat dollar amount, or

� The same percentage of compensation.

The allocation is not adjusted further for earnings. It is treated as anannual addition for the year of the error.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

→ Employer T calculates the dollar amount of the excesscontributions for the two HCEs.

→ The excess contribution for Employee P is $2,037.50.

→ The earnings on Employee P’s excess are $407.

→ Employee P receives a distribution of $2,444.50 ($2037.50plus $407).

→ The excess contribution for Employee S is $3,537.50.

→ The earnings of Employee S’s excess are $707.

→ Employee S receives a distribution of $4,244.50 ($3,537.50plus $707).

→ The total of the excesses, adjusted for earnings, is $6,689.

→ Employer T makes a corrective contribution to the plan inthe amount of $6,689.

→ The corrective contribution is allocated to eligible NHCEsfor 1997, pro rata based on 1997 compensation.

→ Employee P’s and Employee S’s matching contributionsrelated to the distributed excesses, adjusted for earnings,are forfeited.

→ The forfeited amounts are used to reduce contributions for1999 and subsequent years.

*The four options listed above assume the plan sponsor uses thecurrent year testing method. If the prior year testing method is used,substitute “the year prior to the year of the error” for “the year of theerror” in the dot points above.

Regardless which group the employer selects to receive thecontribution, it is allocated to each employee either as:

� The same flat dollar amount, or

� The same percentage of compensation.

The allocation is not adjusted further for earnings. It is treated as anannual addition for the year of the error.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

→ Employer T calculates the dollar amount of the excesscontributions for the two HCEs.

→ The excess contribution for Employee P is $2,037.50.

→ The earnings on Employee P’s excess are $407.

→ Employee P receives a distribution of $2,444.50 ($2037.50plus $407).

→ The excess contribution for Employee S is $3,537.50.

→ The earnings of Employee S’s excess are $707.

→ Employee S receives a distribution of $4,244.50 ($3,537.50plus $707).

→ The total of the excesses, adjusted for earnings, is $6,689.

→ Employer T makes a corrective contribution to the plan inthe amount of $6,689.

→ The corrective contribution is allocated to eligible NHCEsfor 1997, pro rata based on 1997 compensation.

→ Employee P’s and Employee S’s matching contributionsrelated to the distributed excesses, adjusted for earnings,are forfeited.

→ The forfeited amounts are used to reduce contributions for1999 and subsequent years.

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

Error Acceptable Correction Method Example

*The four options listed above assume the plan sponsor uses thecurrent year testing method. If the prior year testing method is used,substitute “the year prior to the year of the error” for “the year of theerror” in the dot points above.

Regardless which group the employer selects to receive thecontribution, it is allocated to each employee either as:

� The same flat dollar amount, or

� The same percentage of compensation.

The allocation is not adjusted further for earnings. It is treated as anannual addition for the year of the error.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

→ Employer T calculates the dollar amount of the excesscontributions for the two HCEs.

→ The excess contribution for Employee P is $2,037.50.

→ The earnings on Employee P’s excess are $407.

→ Employee P receives a distribution of $2,444.50 ($2037.50plus $407).

→ The excess contribution for Employee S is $3,537.50.

→ The earnings of Employee S’s excess are $707.

→ Employee S receives a distribution of $4,244.50 ($3,537.50plus $707).

→ The total of the excesses, adjusted for earnings, is $6,689.

→ Employer T makes a corrective contribution to the plan inthe amount of $6,689.

→ The corrective contribution is allocated to eligible NHCEsfor 1997, pro rata based on 1997 compensation.

→ Employee P’s and Employee S’s matching contributionsrelated to the distributed excesses, adjusted for earnings,are forfeited.

→ The forfeited amounts are used to reduce contributions for1999 and subsequent years.

...Continued from Previous Page

5

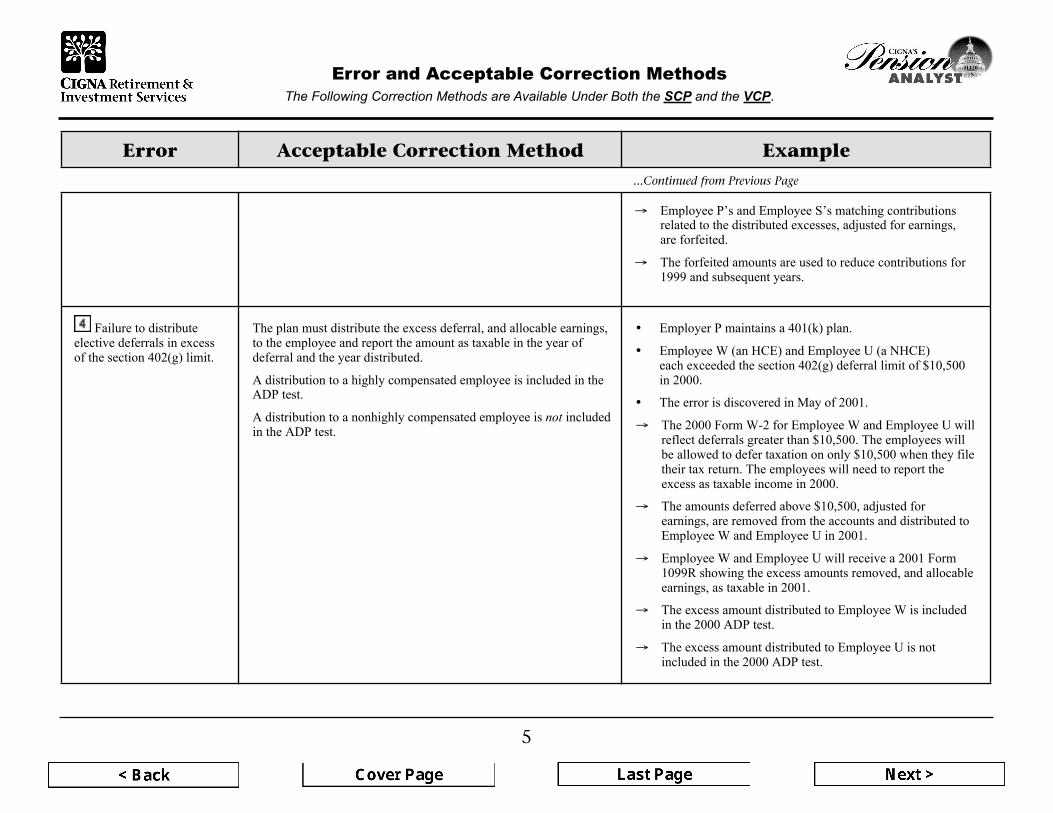

Failure to distributeelective deferrals in excessof the section 402(g) limit.

The plan must distribute the excess deferral, and allocable earnings,to the employee and report the amount as taxable in the year ofdeferral and the year distributed.

A distribution to a highly compensated employee is included in theADP test.

A distribution to a nonhighly compensated employee is not includedin the ADP test.

� Employer P maintains a 401(k) plan.

� Employee W (an HCE) and Employee U (a NHCE)each exceeded the section 402(g) deferral limit of $10,500in 2000.

� The error is discovered in May of 2001.

→ The 2000 Form W-2 for Employee W and Employee U willreflect deferrals greater than $10,500. The employees willbe allowed to defer taxation on only $10,500 when they filetheir tax return. The employees will need to report theexcess as taxable income in 2000.

→ The amounts deferred above $10,500, adjusted forearnings, are removed from the accounts and distributed toEmployee W and Employee U in 2001.

→ Employee W and Employee U will receive a 2001 Form1099R showing the excess amounts removed, and allocableearnings, as taxable in 2001.

→ The excess amount distributed to Employee W is includedin the 2000 ADP test.

→ The excess amount distributed to Employee U is notincluded in the 2000 ADP test.

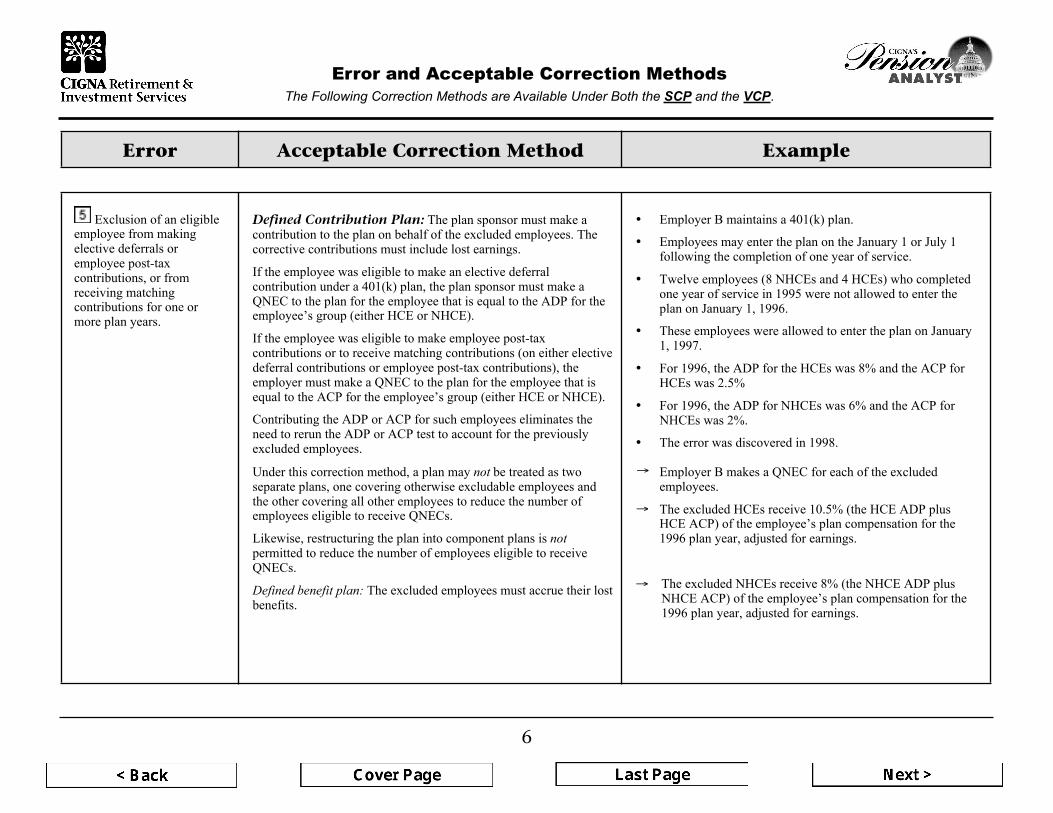

Exclusion of an eligibleemployee from makingelective deferrals oremployee post-taxcontributions, or fromreceiving matchingcontributions for one ormore plan years.

Defined Contribution Plan: The plan sponsor must make acontribution to the plan on behalf of the excluded employees. Thecorrective contributions must include lost earnings.

If the employee was eligible to make an elective deferralcontribution under a 401(k) plan, the plan sponsor must make aQNEC to the plan for the employee that is equal to the ADP for theemployee’s group (either HCE or NHCE).

� Employer B maintains a 401(k) plan.

� Employees may enter the plan on the January 1 or July 1following the completion of one year of service.

� Twelve employees (8 NHCEs and 4 HCEs) who completedone year of service in 1995 were not allowed to enter theplan on January 1, 1996.

If the employee was eligible to make employee post-taxcontributions or to receive matching contributions (on either electivedeferral contributions or employee post-tax contributions), theemployer must make a QNEC to the plan for the employee that isequal to the ACP for the employee’s group (either HCE or NHCE).

Contributing the ADP or ACP for such employees eliminates theneed to rerun the ADP or ACP test to account for the previouslyexcluded employees.

� These employees were allowed to enter the plan on January1, 1997.

� For 1996, the ADP for the HCEs was 8% and the ACP forHCEs was 2.5%

� For 1996, the ADP for NHCEs was 6% and the ACP forNHCEs was 2%.

� The error was discovered in 1998.

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

Failure to distributeelective deferrals in excessof the section 402(g) limit.

The plan must distribute the excess deferral, and allocable earnings,to the employee and report the amount as taxable in the year ofdeferral and the year distributed.

A distribution to a highly compensated employee is included in theADP test.

A distribution to a nonhighly compensated employee is not includedin the ADP test.

� Employer P maintains a 401(k) plan.

� Employee W (an HCE) and Employee U (a NHCE)each exceeded the section 402(g) deferral limit of $10,500in 2000.

� The error is discovered in May of 2001.

→ The 2000 Form W-2 for Employee W and Employee U willreflect deferrals greater than $10,500. The employees willbe allowed to defer taxation on only $10,500 when they filetheir tax return. The employees will need to report theexcess as taxable income in 2000.

→ The amounts deferred above $10,500, adjusted forearnings, are removed from the accounts and distributed toEmployee W and Employee U in 2001.

→ Employee W and Employee U will receive a 2001 Form1099R showing the excess amounts removed, and allocable

6

Error Acceptable Correction Method Example

earnings, as taxable in 2001.

→ The excess amount distributed to Employee W is includedin the 2000 ADP test.

→ The excess amount distributed to Employee U is notincluded in the 2000 ADP test.

Exclusion of an eligibleemployee from makingelective deferrals oremployee post-taxcontributions, or fromreceiving matchingcontributions for one ormore plan years.

Defined Contribution Plan: The plan sponsor must make acontribution to the plan on behalf of the excluded employees. Thecorrective contributions must include lost earnings.

If the employee was eligible to make an elective deferralcontribution under a 401(k) plan, the plan sponsor must make aQNEC to the plan for the employee that is equal to the ADP for theemployee’s group (either HCE or NHCE).

If the employee was eligible to make employee post-taxcontributions or to receive matching contributions (on either electivedeferral contributions or employee post-tax contributions), theemployer must make a QNEC to the plan for the employee that isequal to the ACP for the employee’s group (either HCE or NHCE).

Contributing the ADP or ACP for such employees eliminates theneed to rerun the ADP or ACP test to account for the previouslyexcluded employees.

� Employer B maintains a 401(k) plan.

� Employees may enter the plan on the January 1 or July 1following the completion of one year of service.

� Twelve employees (8 NHCEs and 4 HCEs) who completedone year of service in 1995 were not allowed to enter theplan on January 1, 1996.

� These employees were allowed to enter the plan on January1, 1997.

� For 1996, the ADP for the HCEs was 8% and the ACP forHCEs was 2.5%

� For 1996, the ADP for NHCEs was 6% and the ACP forNHCEs was 2%.

� The error was discovered in 1998.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

Defined benefit plan: The excluded employees must accrue their lostbenefits.

� Employer B makes a QNEC for each of the excludedemployees.

� The excluded HCEs receive 10.5% (the HCE ADP plusHCE ACP) of the employee’s plan compensation for the1996 plan year, adjusted for earnings.

→ The excluded NHCEs receive 8% (the NHCE ADP plusNHCE ACP) of the employee’s plan compensation for the1996 plan year, adjusted for earnings.

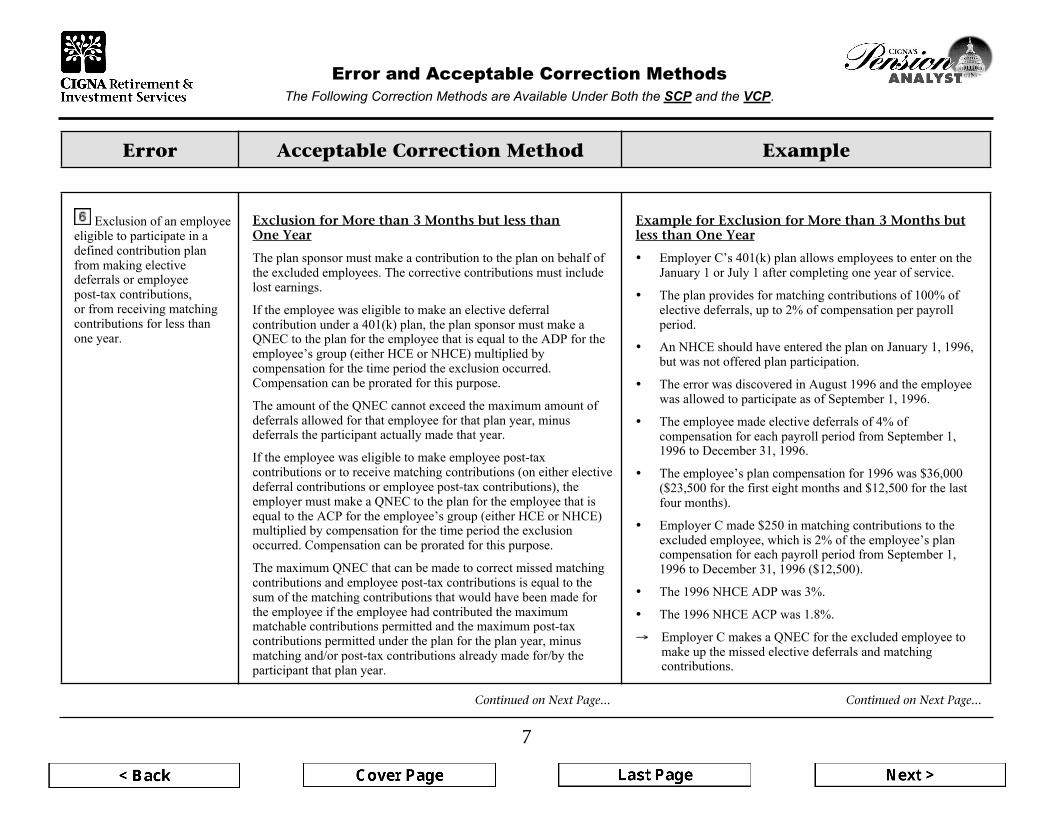

Exclusion of an employeeeligible to participate in adefined contribution planfrom making electivedeferrals or employeepost-tax contributions,or from receiving matchingcontributions for less thanone year.

Exclusion for More than 3 Months but less thanOne Year

The plan sponsor must make a contribution to the plan on behalf ofthe excluded employees. The corrective contributions must includelost earnings.

If the employee was eligible to make an elective deferralcontribution under a 401(k) plan, the plan sponsor must make aQNEC to the plan for the employee that is equal to the ADP for theemployee’s group (either HCE or NHCE) multiplied bycompensation for the time period the exclusion occurred.

Example for Exclusion for More than 3 Months butless than One Year

� Employer C’s 401(k) plan allows employees to enter on theJanuary 1 or July 1 after completing one year of service.

� The plan provides for matching contributions of 100% ofelective deferrals, up to 2% of compensation per payrollperiod.

� An NHCE should have entered the plan on January 1, 1996,but was not offered plan participation.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

Defined benefit plan: The excluded employees must accrue their lostbenefits.

� Employer B makes a QNEC for each of the excludedemployees.

� The excluded HCEs receive 10.5% (the HCE ADP plusHCE ACP) of the employee’s plan compensation for the1996 plan year, adjusted for earnings.

→ The excluded NHCEs receive 8% (the NHCE ADP plusNHCE ACP) of the employee’s plan compensation for the1996 plan year, adjusted for earnings.

Exclusion of an employeeeligible to participate in adefined contribution planfrom making electivedeferrals or employeepost-tax contributions,or from receiving matchingcontributions for less thanone year.

Exclusion for More than 3 Months but less thanOne Year

The plan sponsor must make a contribution to the plan on behalf ofthe excluded employees. The corrective contributions must includelost earnings.

If the employee was eligible to make an elective deferralcontribution under a 401(k) plan, the plan sponsor must make aQNEC to the plan for the employee that is equal to the ADP for theemployee’s group (either HCE or NHCE) multiplied bycompensation for the time period the exclusion occurred.Compensation can be prorated for this purpose.

The amount of the QNEC cannot exceed the maximum amount ofdeferrals allowed for that employee for that plan year, minusdeferrals the participant actually made that year.

Example for Exclusion for More than 3 Months butless than One Year

� Employer C’s 401(k) plan allows employees to enter on theJanuary 1 or July 1 after completing one year of service.

� The plan provides for matching contributions of 100% ofelective deferrals, up to 2% of compensation per payrollperiod.

� An NHCE should have entered the plan on January 1, 1996,but was not offered plan participation.

� The error was discovered in August 1996 and the employeewas allowed to participate as of September 1, 1996.

� The employee made elective deferrals of 4% ofcompensation for each payroll period from September 1,1996 to December 31, 1996.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

Defined benefit plan: The excluded employees must accrue their lostbenefits.

� Employer B makes a QNEC for each of the excludedemployees.

� The excluded HCEs receive 10.5% (the HCE ADP plusHCE ACP) of the employee’s plan compensation for the1996 plan year, adjusted for earnings.

→ The excluded NHCEs receive 8% (the NHCE ADP plusNHCE ACP) of the employee’s plan compensation for the1996 plan year, adjusted for earnings.

Exclusion of an employeeeligible to participate in adefined contribution planfrom making electivedeferrals or employeepost-tax contributions,or from receiving matchingcontributions for less thanone year.

Exclusion for More than 3 Months but less thanOne Year

The plan sponsor must make a contribution to the plan on behalf ofthe excluded employees. The corrective contributions must includelost earnings.

If the employee was eligible to make an elective deferralcontribution under a 401(k) plan, the plan sponsor must make aQNEC to the plan for the employee that is equal to the ADP for theemployee’s group (either HCE or NHCE) multiplied bycompensation for the time period the exclusion occurred.Compensation can be prorated for this purpose.

The amount of the QNEC cannot exceed the maximum amount ofdeferrals allowed for that employee for that plan year, minusdeferrals the participant actually made that year.

If the employee was eligible to make employee post-taxcontributions or to receive matching contributions (on either electivedeferral contributions or employee post-tax contributions), the

Example for Exclusion for More than 3 Months butless than One Year

� Employer C’s 401(k) plan allows employees to enter on theJanuary 1 or July 1 after completing one year of service.

� The plan provides for matching contributions of 100% ofelective deferrals, up to 2% of compensation per payrollperiod.

� An NHCE should have entered the plan on January 1, 1996,but was not offered plan participation.

� The error was discovered in August 1996 and the employeewas allowed to participate as of September 1, 1996.

� The employee made elective deferrals of 4% ofcompensation for each payroll period from September 1,1996 to December 31, 1996.

� The employee’s plan compensation for 1996 was $36,000($23,500 for the first eight months and $12,500 for the last

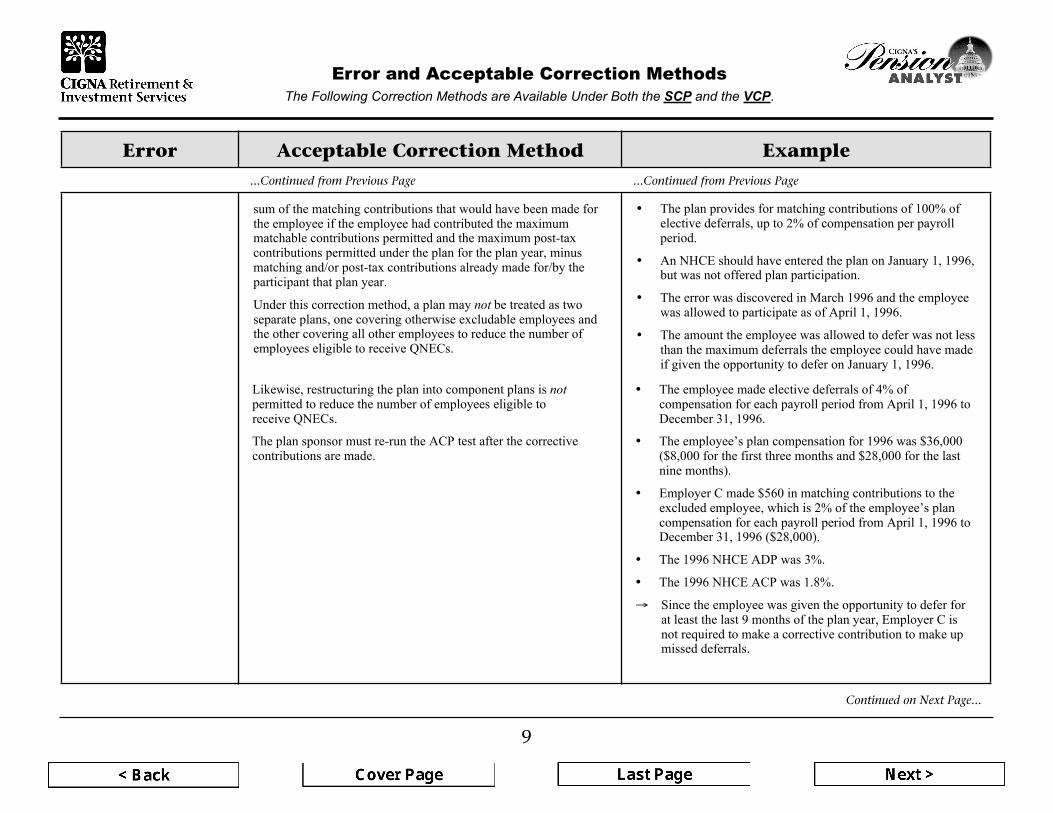

Compensation can be prorated for this purpose.

The amount of the QNEC cannot exceed the maximum amount ofdeferrals allowed for that employee for that plan year, minusdeferrals the participant actually made that year.

If the employee was eligible to make employee post-taxcontributions or to receive matching contributions (on either electivedeferral contributions or employee post-tax contributions), theemployer must make a QNEC to the plan for the employee that isequal to the ACP for the employee’s group (either HCE or NHCE)multiplied by compensation for the time period the exclusionoccurred. Compensation can be prorated for this purpose.

The maximum QNEC that can be made to correct missed matchingcontributions and employee post-tax contributions is equal to thesum of the matching contributions that would have been made forthe employee if the employee had contributed the maximummatchable contributions permitted and the maximum post-taxcontributions permitted under the plan for the plan year, minusmatching and/or post-tax contributions already made for/by theparticipant that plan year.

� The error was discovered in August 1996 and the employeewas allowed to participate as of September 1, 1996.

� The employee made elective deferrals of 4% ofcompensation for each payroll period from September 1,1996 to December 31, 1996.

� The employee’s plan compensation for 1996 was $36,000($23,500 for the first eight months and $12,500 for the lastfour months).

� Employer C made $250 in matching contributions to theexcluded employee, which is 2% of the employee’s plancompensation for each payroll period from September 1,1996 to December 31, 1996 ($12,500).

� The 1996 NHCE ADP was 3%.

� The 1996 NHCE ACP was 1.8%.

→ Employer C makes a QNEC for the excluded employee tomake up the missed elective deferrals and matchingcontributions.

If the employee was eligible to make employee post-taxcontributions or to receive matching contributions (on either electivedeferral contributions or employee post-tax contributions), theemployer must make a QNEC to the plan for the employee that isequal to the ACP for the employee’s group (either HCE or NHCE)multiplied by compensation for the time period the exclusionoccurred. Compensation can be prorated for this purpose.

The maximum QNEC that can be made to correct missed matchingcontributions and employee post-tax contributions is equal to thesum of the matching contributions that would have been made forthe employee if the employee had contributed the maximummatchable contributions permitted and the maximum post-taxcontributions permitted under the plan for the plan year, minusmatching and/or post-tax contributions already made for/by theparticipant that plan year.

� The employee’s plan compensation for 1996 was $36,000($23,500 for the first eight months and $12,500 for the lastfour months).

� Employer C made $250 in matching contributions to theexcluded employee, which is 2% of the employee’s plancompensation for each payroll period from September 1,1996 to December 31, 1996 ($12,500).

� The 1996 NHCE ADP was 3%.

� The 1996 NHCE ACP was 1.8%.

→ Employer C makes a QNEC for the excluded employee tomake up the missed elective deferrals and matchingcontributions.

employer must make a QNEC to the plan for the employee that isequal to the ACP for the employee’s group (either HCE or NHCE)multiplied by compensation for the time period the exclusionoccurred. Compensation can be prorated for this purpose.

The maximum QNEC that can be made to correct missed matchingcontributions and employee post-tax contributions is equal to thesum of the matching contributions that would have been made forthe employee if the employee had contributed the maximummatchable contributions permitted and the maximum post-taxcontributions permitted under the plan for the plan year, minusmatching and/or post-tax contributions already made for/by theparticipant that plan year.

four months).

� Employer C made $250 in matching contributions to theexcluded employee, which is 2% of the employee’s plancompensation for each payroll period from September 1,1996 to December 31, 1996 ($12,500).

� The 1996 NHCE ADP was 3%.

� The 1996 NHCE ACP was 1.8%.

→ Employer C makes a QNEC for the excluded employee tomake up the missed elective deferrals and matchingcontributions.

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

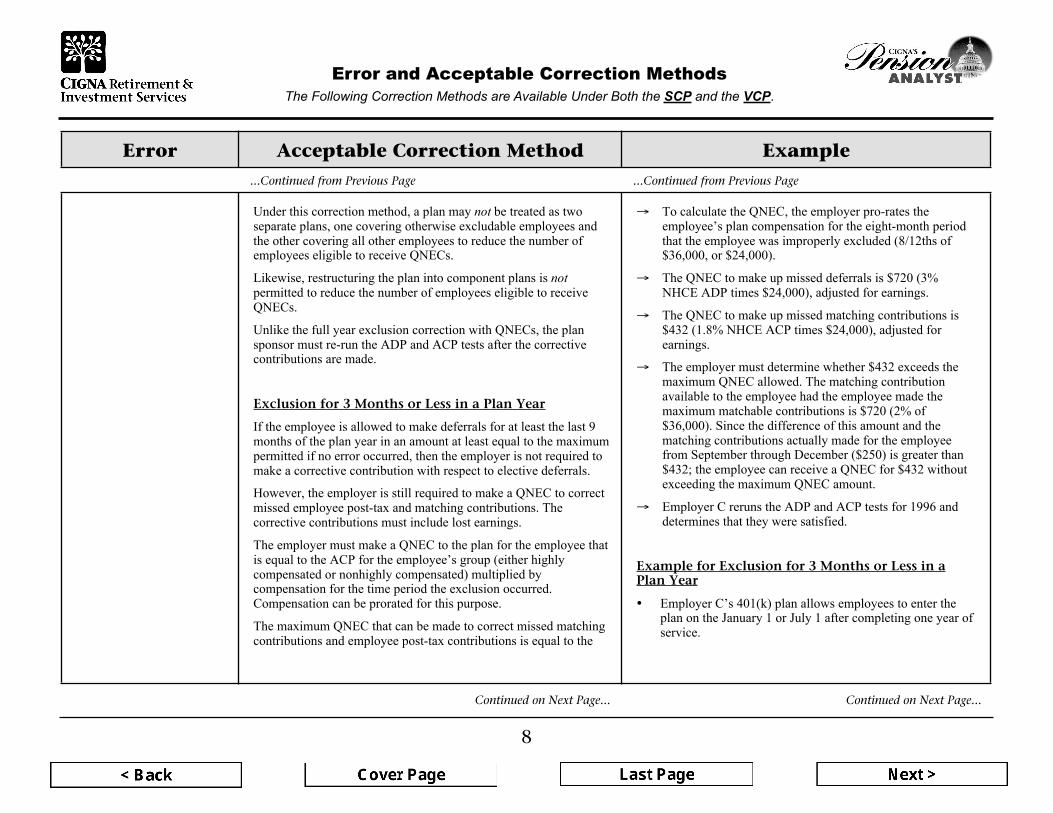

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

� Employer B makes a QNEC for each of the excludedemployees.

� The excluded HCEs receive 10.5% (the HCE ADP plusHCE ACP) of the employee’s plan compensation for the

7

Error Acceptable Correction Method Example

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

Defined benefit plan: The excluded employees must accrue their lostbenefits.

1996 plan year, adjusted for earnings.

→ The excluded NHCEs receive 8% (the NHCE ADP plusNHCE ACP) of the employee’s plan compensation for the1996 plan year, adjusted for earnings.

Exclusion of an employeeeligible to participate in adefined contribution planfrom making electivedeferrals or employeepost-tax contributions,or from receiving matchingcontributions for less thanone year.

Exclusion for More than 3 Months but less thanOne Year

The plan sponsor must make a contribution to the plan on behalf ofthe excluded employees. The corrective contributions must includelost earnings.

If the employee was eligible to make an elective deferralcontribution under a 401(k) plan, the plan sponsor must make aQNEC to the plan for the employee that is equal to the ADP for theemployee’s group (either HCE or NHCE) multiplied bycompensation for the time period the exclusion occurred.Compensation can be prorated for this purpose.

The amount of the QNEC cannot exceed the maximum amount ofdeferrals allowed for that employee for that plan year, minusdeferrals the participant actually made that year.

If the employee was eligible to make employee post-taxcontributions or to receive matching contributions (on either electivedeferral contributions or employee post-tax contributions), theemployer must make a QNEC to the plan for the employee that isequal to the ACP for the employee’s group (either HCE or NHCE)multiplied by compensation for the time period the exclusionoccurred. Compensation can be prorated for this purpose.

The maximum QNEC that can be made to correct missed matchingcontributions and employee post-tax contributions is equal to thesum of the matching contributions that would have been made forthe employee if the employee had contributed the maximummatchable contributions permitted and the maximum post-taxcontributions permitted under the plan for the plan year, minusmatching and/or post-tax contributions already made for/by theparticipant that plan year.

Example for Exclusion for More than 3 Months butless than One Year

� Employer C’s 401(k) plan allows employees to enter on theJanuary 1 or July 1 after completing one year of service.

� The plan provides for matching contributions of 100% ofelective deferrals, up to 2% of compensation per payrollperiod.

� An NHCE should have entered the plan on January 1, 1996,but was not offered plan participation.

� The error was discovered in August 1996 and the employeewas allowed to participate as of September 1, 1996.

� The employee made elective deferrals of 4% ofcompensation for each payroll period from September 1,1996 to December 31, 1996.

� The employee’s plan compensation for 1996 was $36,000($23,500 for the first eight months and $12,500 for the lastfour months).

� Employer C made $250 in matching contributions to theexcluded employee, which is 2% of the employee’s plancompensation for each payroll period from September 1,1996 to December 31, 1996 ($12,500).

� The 1996 NHCE ADP was 3%.

� The 1996 NHCE ACP was 1.8%.

→ Employer C makes a QNEC for the excluded employee tomake up the missed elective deferrals and matchingcontributions.

Continued on Next Page... Continued on Next Page...

8

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

Error Acceptable Correction Method Example

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

Unlike the full year exclusion correction with QNECs, the plansponsor must re-run the ADP and ACP tests after the correctivecontributions are made.

Exclusion for 3 Months or Less in a Plan Year

If the employee is allowed to make deferrals for at least the last 9months of the plan year in an amount at least equal to the maximumpermitted if no error occurred, then the employer is not required tomake a corrective contribution with respect to elective deferrals.

However, the employer is still required to make a QNEC to correctmissed employee post-tax and matching contributions. Thecorrective contributions must include lost earnings.

The employer must make a QNEC to the plan for the employee thatis equal to the ACP for the employee’s group (either highlycompensated or nonhighly compensated) multiplied bycompensation for the time period the exclusion occurred.Compensation can be prorated for this purpose.

The maximum QNEC that can be made to correct missed matchingcontributions and employee post-tax contributions is equal to thesum of the matching contributions that would have been made forthe employee if the employee had contributed the maximummatchable contributions permitted and the maximum post-taxcontributions permitted under the plan for the plan year, minusmatching and/or post-tax contributions already made for/by theparticipant that plan year.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

→ To calculate the QNEC, the employer pro-rates theemployee’s plan compensation for the eight-month periodthat the employee was improperly excluded (8/12ths of$36,000, or $24,000).

→ The QNEC to make up missed deferrals is $720 (3%NHCE ADP times $24,000), adjusted for earnings.

→ The QNEC to make up missed matching contributions is$432 (1.8% NHCE ACP times $24,000), adjusted forearnings.

→ The employer must determine whether $432 exceeds themaximum QNEC allowed. The matching contributionavailable to the employee had the employee made themaximum matchable contributions is $720 (2% of$36,000). Since the difference of this amount and thematching contributions actually made for the employeefrom September through December ($250) is greater than$432; the employee can receive a QNEC for $432 withoutexceeding the maximum QNEC amount.

→ Employer C reruns the ADP and ACP tests for 1996 anddetermines that they were satisfied.

Example for Exclusion for 3 Months or Less in aPlan Year

� Employer C’s 401(k) plan allows employees to enter theplan on the January 1 or July 1 after completing one year ofservice.

� The plan provides for matching contributions of 100% ofelective deferrals, up to 2% of compensation per payrollperiod.

� An NHCE should have entered the plan on January 1, 1996,but was not offered plan participation.

� The error was discovered in March 1996 and the employeewas allowed to participate as of April 1, 1996.

� The amount the employee was allowed to defer was not lessthan the maximum deferrals the employee could have madeif given the opportunity to defer on January 1, 1996.

Continued on Next Page... Continued on Next Page...

...Continued from Previous Page ...Continued from Previous Page

9

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

Error Acceptable Correction Method Example

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible to receiveQNECs.

Unlike the full year exclusion correction with QNECs, the plansponsor must re-run the ADP and ACP tests after the correctivecontributions are made.

Exclusion for 3 Months or Less in a Plan Year

If the employee is allowed to make deferrals for at least the last 9months of the plan year in an amount at least equal to the maximumpermitted if no error occurred, then the employer is not required tomake a corrective contribution with respect to elective deferrals.

However, the employer is still required to make a QNEC to correctmissed employee post-tax and matching contributions. Thecorrective contributions must include lost earnings.

The employer must make a QNEC to the plan for the employee thatis equal to the ACP for the employee’s group (either highlycompensated or nonhighly compensated) multiplied bycompensation for the time period the exclusion occurred.Compensation can be prorated for this purpose.

The maximum QNEC that can be made to correct missed matchingcontributions and employee post-tax contributions is equal to thesum of the matching contributions that would have been made forthe employee if the employee had contributed the maximummatchable contributions permitted and the maximum post-taxcontributions permitted under the plan for the plan year, minusmatching and/or post-tax contributions already made for/by theparticipant that plan year.

Under this correction method, a plan may not be treated as twoseparate plans, one covering otherwise excludable employees andthe other covering all other employees to reduce the number ofemployees eligible to receive QNECs.

→ To calculate the QNEC, the employer pro-rates theemployee’s plan compensation for the eight-month periodthat the employee was improperly excluded (8/12ths of$36,000, or $24,000).

→ The QNEC to make up missed deferrals is $720 (3%NHCE ADP times $24,000), adjusted for earnings.

→ The QNEC to make up missed matching contributions is$432 (1.8% NHCE ACP times $24,000), adjusted forearnings.

→ The employer must determine whether $432 exceeds themaximum QNEC allowed. The matching contributionavailable to the employee had the employee made themaximum matchable contributions is $720 (2% of$36,000). Since the difference of this amount and thematching contributions actually made for the employeefrom September through December ($250) is greater than$432; the employee can receive a QNEC for $432 withoutexceeding the maximum QNEC amount.

→ Employer C reruns the ADP and ACP tests for 1996 anddetermines that they were satisfied.

Example for Exclusion for 3 Months or Less in aPlan Year

� Employer C’s 401(k) plan allows employees to enter theplan on the January 1 or July 1 after completing one year ofservice.

� The plan provides for matching contributions of 100% ofelective deferrals, up to 2% of compensation per payrollperiod.

� An NHCE should have entered the plan on January 1, 1996,but was not offered plan participation.

� The error was discovered in March 1996 and the employeewas allowed to participate as of April 1, 1996.

� The amount the employee was allowed to defer was not lessthan the maximum deferrals the employee could have madeif given the opportunity to defer on January 1, 1996.

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible toreceive QNECs.

The plan sponsor must re-run the ACP test after the correctivecontributions are made.

� The employee made elective deferrals of 4% ofcompensation for each payroll period from April 1, 1996 toDecember 31, 1996.

� The employee’s plan compensation for 1996 was $36,000($8,000 for the first three months and $28,000 for the lastnine months).

� Employer C made $560 in matching contributions to theexcluded employee, which is 2% of the employee’s plancompensation for each payroll period from April 1, 1996 toDecember 31, 1996 ($28,000).

� The 1996 NHCE ADP was 3%.

� The 1996 NHCE ACP was 1.8%.

→ Since the employee was given the opportunity to defer forat least the last 9 months of the plan year, Employer C isnot required to make a corrective contribution to make upmissed deferrals.

→ Employer C does need to make a corrective contribution tomake up missed matching contributions.

→ The corrective contribution must include lost earnings.

→ To calculate the QNEC, the employer pro-rates theemployee’s plan compensation for the three-month periodthat the employee was improperly excluded (3/12ths of$36,000, or $9,000).

→ The amount of the QNEC calculated to make up missedmatching contributions is $162 (1.8% NHCE ACP times$9,000), adjusted for earnings.

→ The employer must determine whether $162 exceeds themaximum QNEC allowed. The matching contributionavailable to the employee had the employee made themaximum matchable contributions is $720 (2% of$36,000). The difference of this amount and the matchingcontributions actually made for the employee from Aprilthrough December ($560) is $160. Since the QNEC cannotexceed $160, Employer C makes a QNEC for $160 ratherthan $162.Employer C re-runs the ACP test for 1996 anddetermines that it was satisfied.

Continued on Next Page...

...Continued from Previous Page ...Continued from Previous Page

10

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

Error Acceptable Correction Method Example

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible toreceive QNECs.

The plan sponsor must re-run the ACP test after the correctivecontributions are made.

� The employee made elective deferrals of 4% ofcompensation for each payroll period from April 1, 1996 toDecember 31, 1996.

� The employee’s plan compensation for 1996 was $36,000($8,000 for the first three months and $28,000 for the lastnine months).

� Employer C made $560 in matching contributions to theexcluded employee, which is 2% of the employee’s plancompensation for each payroll period from April 1, 1996 toDecember 31, 1996 ($28,000).

� The 1996 NHCE ADP was 3%.

� The 1996 NHCE ACP was 1.8%.

→ Since the employee was given the opportunity to defer forat least the last 9 months of the plan year, Employer C isnot required to make a corrective contribution to make upmissed deferrals.

→ Employer C does need to make a corrective contribution tomake up missed matching contributions.

→ The corrective contribution must include lost earnings.

→ To calculate the QNEC, the employer pro-rates theemployee’s plan compensation for the three-month periodthat the employee was improperly excluded (3/12ths of$36,000, or $9,000).

→ The amount of the QNEC calculated to make up missedmatching contributions is $162 (1.8% NHCE ACP times$9,000), adjusted for earnings.

→ The employer must determine whether $162 exceeds themaximum QNEC allowed. The matching contributionavailable to the employee had the employee made themaximum matchable contributions is $720 (2% of$36,000). The difference of this amount and the matchingcontributions actually made for the employee from Aprilthrough December ($560) is $160. Since the QNEC cannotexceed $160, Employer C makes a QNEC for $160 ratherthan $162.Employer C re-runs the ACP test for 1996 anddetermines that it was satisfied.

...Continued from Previous Page

Likewise, restructuring the plan into component plans is notpermitted to reduce the number of employees eligible toreceive QNECs.

The plan sponsor must re-run the ACP test after the correctivecontributions are made.

� The employee made elective deferrals of 4% ofcompensation for each payroll period from April 1, 1996 toDecember 31, 1996.

� The employee’s plan compensation for 1996 was $36,000($8,000 for the first three months and $28,000 for the lastnine months).

� Employer C made $560 in matching contributions to theexcluded employee, which is 2% of the employee’s plancompensation for each payroll period from April 1, 1996 toDecember 31, 1996 ($28,000).

� The 1996 NHCE ADP was 3%.

� The 1996 NHCE ACP was 1.8%.

→ Since the employee was given the opportunity to defer forat least the last 9 months of the plan year, Employer C isnot required to make a corrective contribution to make upmissed deferrals.

→ Employer C does need to make a corrective contribution tomake up missed matching contributions.

→ The corrective contribution must include lost earnings.

→ To calculate the QNEC, the employer pro-rates theemployee’s plan compensation for the three-month periodthat the employee was improperly excluded (3/12ths of$36,000, or $9,000).

→ The amount of the QNEC calculated to make up missedmatching contributions is $162 (1.8% NHCE ACP times$9,000), adjusted for earnings.

→ The employer must determine whether $162 exceeds themaximum QNEC allowed. The matching contributionavailable to the employee had the employee made themaximum matchable contributions is $720 (2% of$36,000). The difference of this amount and the matchingcontributions actually made for the employee from Aprilthrough December ($560) is $160. Since the QNEC cannotexceed $160, Employer C makes a QNEC for $160 ratherthan $162.Employer C re-runs the ACP test for 1996 anddetermines that it was satisfied.

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

Error Acceptable Correction Method Example

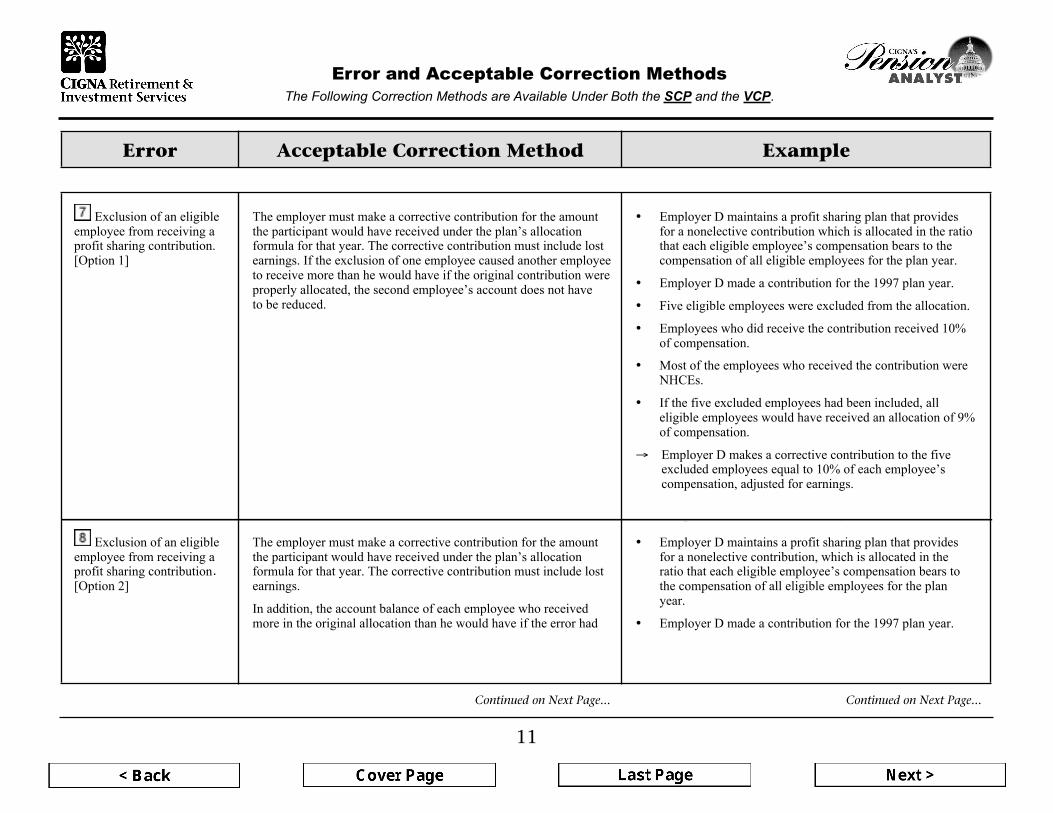

Exclusion of an eligibleemployee from receiving aprofit sharing contribution.[Option 1]

The employer must make a corrective contribution for the amountthe participant would have received under the plan’s allocationformula for that year. The corrective contribution must include lostearnings. If the exclusion of one employee caused another employeeto receive more than he would have if the original contribution wereproperly allocated, the second employee’s account does not haveto be reduced.

� Employer D maintains a profit sharing plan that providesfor a nonelective contribution which is allocated in the ratiothat each eligible employee’s compensation bears to thecompensation of all eligible employees for the plan year.

� Employer D made a contribution for the 1997 plan year.

� Five eligible employees were excluded from the allocation.

� Employees who did receive the contribution received 10%of compensation.

� Most of the employees who received the contribution wereNHCEs.

� If the five excluded employees had been included, alleligible employees would have received an allocation of 9%of compensation.

→ Employer D makes a corrective contribution to the fiveexcluded employees equal to 10% of each employee’scompensation, adjusted for earnings.

Exclusion of an eligibleemployee from receiving aprofit sharing contribution.[Option 1]

The employer must make a corrective contribution for the amountthe participant would have received under the plan’s allocationformula for that year. The corrective contribution must include lostearnings. If the exclusion of one employee caused another employeeto receive more than he would have if the original contribution wereproperly allocated, the second employee’s account does not haveto be reduced.

� Employer D maintains a profit sharing plan that providesfor a nonelective contribution which is allocated in the ratiothat each eligible employee’s compensation bears to thecompensation of all eligible employees for the plan year.

� Employer D made a contribution for the 1997 plan year.

� Five eligible employees were excluded from the allocation.

� Employees who did receive the contribution received 10%of compensation.

� Most of the employees who received the contribution wereNHCEs.

� If the five excluded employees had been included, alleligible employees would have received an allocation of 9%of compensation.

→ Employer D makes a corrective contribution to the fiveexcluded employees equal to 10% of each employee’s

Exclusion of an eligible The employer must make a corrective contribution for the amount � Employer D maintains a profit sharing plan that provides

11

employee from receiving aprofit sharing contribution[Option 2]

the participant would have received under the plan’s allocationformula for that year. The corrective contribution must include lostearnings.

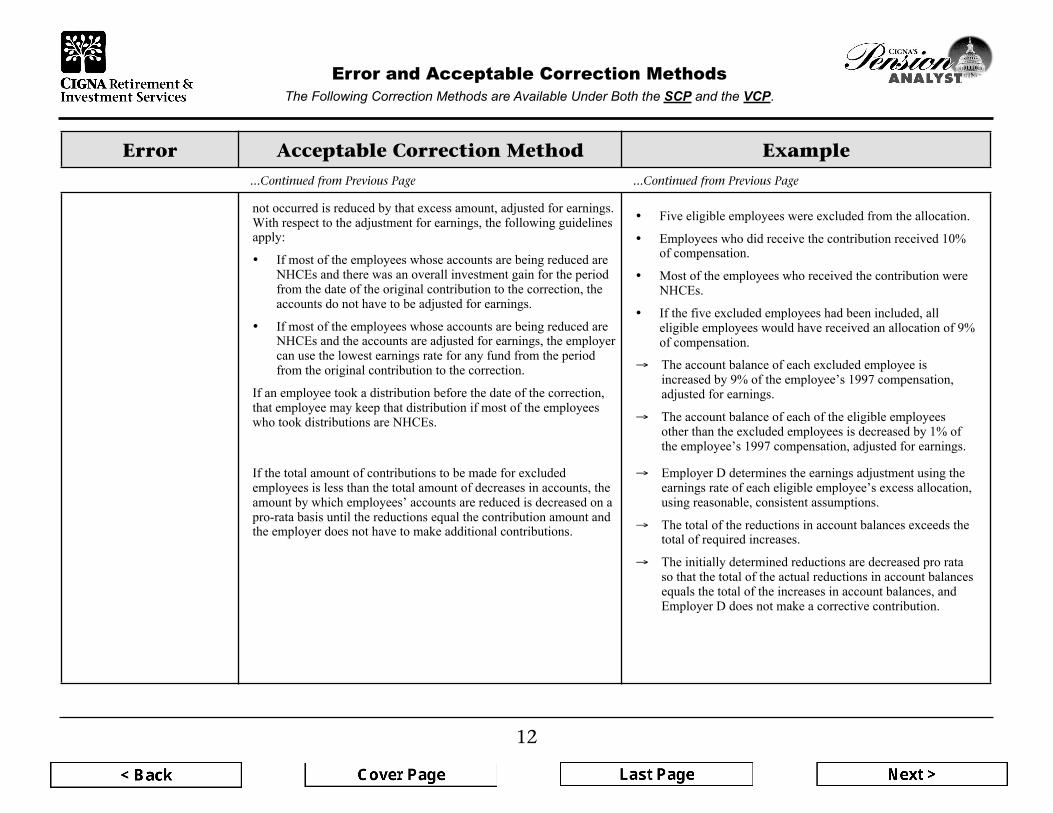

In addition, the account balance of each employee who receivedmore in the original allocation than he would have if the error hadnot occurred is reduced by that excess amount, adjusted for earnings.With respect to the adjustment for earnings, the following guidelinesapply:

� If most of the employees whose accounts are being reduced areNHCEs and there was an overall investment gain for the periodfrom the date of the original contribution to the correction, theaccounts do not have to be adjusted for earnings.

� If most of the employees whose accounts are being reduced areNHCEs and the accounts are adjusted for earnings, the employercan use the lowest earnings rate for any fund from the periodfrom the original contribution to the correction.

If an employee took a distribution before the date of the correction,

for a nonelective contribution, which is allocated in theratio that each eligible employee’s compensation bears tothe compensation of all eligible employees for the planyear.

� Employer D made a contribution for the 1997 plan year.

� Five eligible employees were excluded from the allocation.

� Employees who did receive the contribution received 10%of compensation.

� Most of the employees who received the contribution wereNHCEs.

� If the five excluded employees had been included, alleligible employees would have received an allocation of 9%of compensation.

→ The account balance of each excluded employee isincreased by 9% of the employee’s 1997 compensation,adjusted for earnings.

compensation, adjusted for earnings.

Exclusion of an eligibleemployee from receiving aprofit sharing contribution[Option 2]

The employer must make a corrective contribution for the amountthe participant would have received under the plan’s allocationformula for that year. The corrective contribution must include lostearnings.

In addition, the account balance of each employee who receivedmore in the original allocation than he would have if the error hadnot occurred is reduced by that excess amount, adjusted for earnings.With respect to the adjustment for earnings, the following guidelinesapply:

� If most of the employees whose accounts are being reduced areNHCEs and there was an overall investment gain for the periodfrom the date of the original contribution to the correction, theaccounts do not have to be adjusted for earnings.

� If most of the employees whose accounts are being reduced areNHCEs and the accounts are adjusted for earnings, the employercan use the lowest earnings rate for any fund from the period

� Employer D maintains a profit sharing plan that providesfor a nonelective contribution, which is allocated in theratio that each eligible employee’s compensation bears tothe compensation of all eligible employees for the planyear.

� Employer D made a contribution for the 1997 plan year.

� Five eligible employees were excluded from the allocation.

� Employees who did receive the contribution received 10%of compensation.

� Most of the employees who received the contribution wereNHCEs.

� If the five excluded employees had been included, alleligible employees would have received an allocation of 9%of compensation.

→ The account balance of each excluded employee is

Continued on Next Page... Continued on Next Page...

.

that employee may keep that distribution if most of the employeeswho took distributions are NHCEs. → The account balance of each of the eligible employees

other than the excluded employees is decreased by 1% ofthe employee’s 1997 compensation, adjusted for earnings.

from the original contribution to the correction.

If an employee took a distribution before the date of the correction,that employee may keep that distribution if most of the employeeswho took distributions are NHCEs.

increased by 9% of the employee’s 1997 compensation,adjusted for earnings.

→ The account balance of each of the eligible employeesother than the excluded employees is decreased by 1% ofthe employee’s 1997 compensation, adjusted for earnings.

12

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

Error Acceptable Correction Method Example

Exclusion of an eligibleemployee from receiving aprofit sharing contribution.[Option 1]

The employer must make a corrective contribution for the amountthe participant would have received under the plan’s allocationformula for that year. The corrective contribution must include lostearnings. If the exclusion of one employee caused another employeeto receive more than he would have if the original contribution wereproperly allocated, the second employee’s account does not haveto be reduced.

� Employer D maintains a profit sharing plan that providesfor a nonelective contribution which is allocated in the ratiothat each eligible employee’s compensation bears to thecompensation of all eligible employees for the plan year.

� Employer D made a contribution for the 1997 plan year.

� Five eligible employees were excluded from the allocation.

� Employees who did receive the contribution received 10%of compensation.

� Most of the employees who received the contribution wereNHCEs.

� If the five excluded employees had been included, alleligible employees would have received an allocation of 9%of compensation.

→ Employer D makes a corrective contribution to the fiveexcluded employees equal to 10% of each employee’scompensation, adjusted for earnings.

Exclusion of an eligibleemployee from receiving aprofit sharing contribution[Option 2]

The employer must make a corrective contribution for the amountthe participant would have received under the plan’s allocationformula for that year. The corrective contribution must include lostearnings.

In addition, the account balance of each employee who receivedmore in the original allocation than he would have if the error hadnot occurred is reduced by that excess amount, adjusted for earnings.With respect to the adjustment for earnings, the following guidelinesapply:

� If most of the employees whose accounts are being reduced areNHCEs and there was an overall investment gain for the periodfrom the date of the original contribution to the correction, theaccounts do not have to be adjusted for earnings.

� If most of the employees whose accounts are being reduced areNHCEs and the accounts are adjusted for earnings, the employercan use the lowest earnings rate for any fund from the periodfrom the original contribution to the correction.

If an employee took a distribution before the date of the correction,that employee may keep that distribution if most of the employeeswho took distributions are NHCEs.

� Employer D maintains a profit sharing plan that providesfor a nonelective contribution, which is allocated in theratio that each eligible employee’s compensation bears tothe compensation of all eligible employees for the planyear.

� Employer D made a contribution for the 1997 plan year.

� Five eligible employees were excluded from the allocation.

� Employees who did receive the contribution received 10%of compensation.

� Most of the employees who received the contribution wereNHCEs.

� If the five excluded employees had been included, alleligible employees would have received an allocation of 9%of compensation.

→ The account balance of each excluded employee isincreased by 9% of the employee’s 1997 compensation,adjusted for earnings.

→ The account balance of each of the eligible employeesother than the excluded employees is decreased by 1% ofthe employee’s 1997 compensation, adjusted for earnings.

If the total amount of contributions to be made for excludedemployees is less than the total amount of decreases in accounts, theamount by which employees’ accounts are reduced is decreased on apro-rata basis until the reductions equal the contribution amount andthe employer does not have to make additional contributions.

→ Employer D determines the earnings adjustment using theearnings rate of each eligible employee’s excess allocation,using reasonable, consistent assumptions.

→ The total of the reductions in account balances exceeds thetotal of required increases.

→ The initially determined reductions are decreased pro rataso that the total of the actual reductions in account balancesequals the total of the increases in account balances, andEmployer D does not make a corrective contribution.

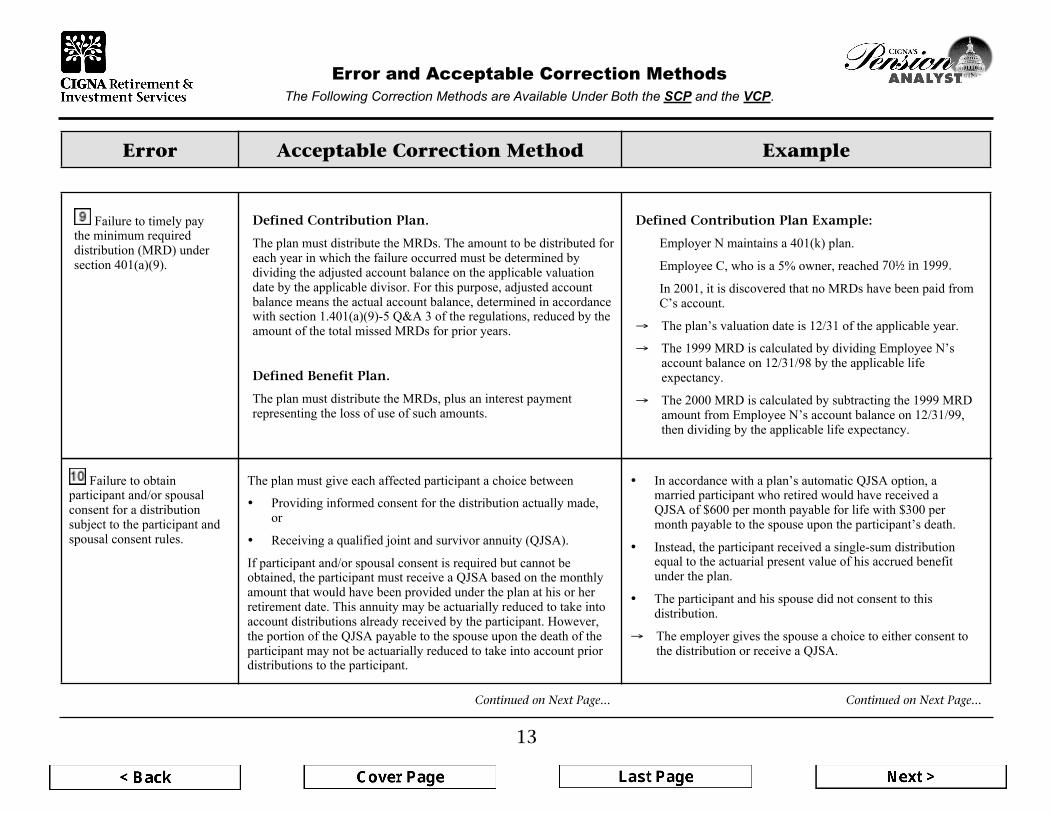

Failure to timely paythe minimum requireddistribution (MRD) undersection 401(a)(9).

Defined Contribution Plan.

The plan must distribute the MRDs. The amount to be distributed foreach year in which the failure occurred must be determined bydividing the adjusted account balance on the applicable valuationdate by the applicable divisor. For this purpose, adjusted accountbalance means the actual account balance, determined in accordancewith section 1.401(a)(9)-5 Q&A 3 of the regulations, reduced by theamount of the total missed MRDs for prior years.

Defined Benefit Plan.

The plan must distribute the MRDs, plus an interest paymentrepresenting the loss of use of such amounts.

Defined Contribution Plan Example:

∞ Employer N maintains a 401(k) plan.

∞ Employee C, who is a 5% owner, reached 70_ in 1999.

∞ In 2001, it is discovered that no MRDs have been paid fromC’s account.

→ The plan’s valuation date is 12/31 of the applicable year.

→ The 1999 MRD is calculated by dividing Employee N’saccount balance on 12/31/98 by the applicable lifeexpectancy.

→ The 2000 MRD is calculated by subtracting the 1999 MRDamount from Employee N’s account balance on 12/31/99,then dividing by the applicable life expectancy.

Failure to obtainparticipant and/or spousalconsent for a distributionsubject to the participant andspousal consent rules.

The plan must give each affected participant a choice between

� Providing informed consent for the distribution actually made,or

� Receiving a qualified joint and survivor annuity (QJSA).

If participant and/or spousal consent is required but cannot beobtained, the participant must receive a QJSA based on the monthlyamount that would have been provided under the plan at his or herretirement date. This annuity may be actuarially reduced to take intoaccount distributions already received by the participant. However,the portion of the QJSA payable to the spouse upon the death of theparticipant may not be actuarially reduced to take into account priordistributions to the participant.

� In accordance with a plan’s automatic QJSA option, amarried participant who retired would have received aQJSA of $600 per month payable for life with $300 permonth payable to the spouse upon the participant’s death.

� Instead, the participant received a single-sum distributionequal to the actuarial present value of his accrued benefitunder the plan.

� The participant and his spouse did not consent to thisdistribution.

→ The employer gives the spouse a choice to either consent tothe distribution or receive a QJSA.

...Continued from Previous Page ...Continued from Previous Page

Error and Acceptable Correction Methods

The Following Correction Methods are Available Under Both the SCP and the VCP.

If the total amount of contributions to be made for excludedemployees is less than the total amount of decreases in accounts, theamount by which employees’ accounts are reduced is decreased on apro-rata basis until the reductions equal the contribution amount and

→ Employer D determines the earnings adjustment using theearnings rate of each eligible employee’s excess allocation,using reasonable, consistent assumptions.

If the total amount of contributions to be made for excludedemployees is less than the total amount of decreases in accounts, theamount by which employees’ accounts are reduced is decreased on a

→ Employer D determines the earnings adjustment using theearnings rate of each eligible employee’s excess allocation,using reasonable, consistent assumptions.

Error Acceptable Correction Method Example

the employer does not have to make additional contributions. → The total of the reductions in account balances exceeds thetotal of required increases.