Embed Size (px)

Citation preview

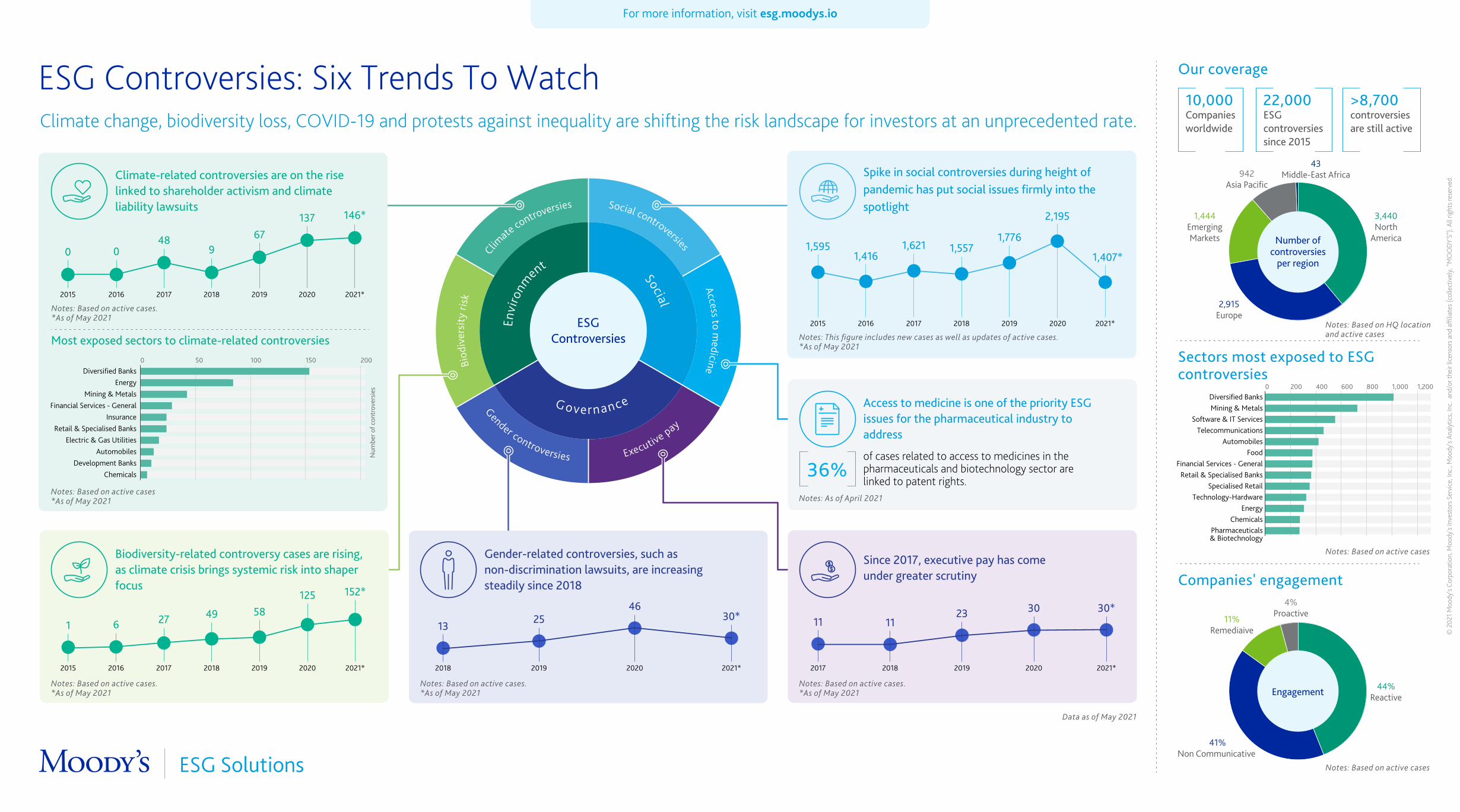

ESGControversies

Social

Envi

ronm

ent

G overnance

Climate controversies

Access to medicine

Gender controversies Executive pay

Social controversies

Biod

iver

sity

risk

Notes: Based on active cases.*As of May 2021

Notes: Based on active cases*As of May 2021

ESG Controversies: Six Trends To Watch

© 2

021

Moo

dy’s

Corp

orat

ion,

Moo

dy’s

Inve

stor

s Ser

vice

, Inc

., M

oody

’s An

alyt

ics,

Inc.

and

/or t

heir

licen

sors

and

affi

liate

s (co

llect

ivel

y, “

MO

OD

Y’S”

). Al

l rig

hts r

eser

ved.

For more information, visit esg.moodys.io

Number of controversies

per region

43Middle-East Africa

3,440North

America

2,915Europe

1,444EmergingMarkets

942Asia Pacific

Our coverage

10,000Companies worldwide

>8,700controversies are still active

22,000ESG controversies since 2015

Most exposed sectors to climate-related controversies

44%Reactive

41%Non Communicative

4%Proactive

11%Remediaive

Companies' engagement

Engagement

Sectors most exposed to ESGcontroversies

Gender-related controversies, such as non-discrimination lawsuits, are increasing steadily since 2018

Biodiversity-related controversy cases are rising, as climate crisis brings systemic risk into shaper focus

36%of cases related to access to medicines in the pharmaceuticals and biotechnology sector arelinked to patent rights.

Access to medicine is one of the priority ESG issues for the pharmaceutical industry to address

Climate change, biodiversity loss, COVID-19 and protests against inequality are shifting the risk landscape for investors at an unprecedented rate.

Notes: This figure includes new cases as well as updates of active cases.*As of May 2021

Spike in social controversies during height of pandemic has put social issues firmly into the spotlight

Climate-related controversies are on the rise linked to shareholder activism and climate liability lawsuits

Since 2017, executive pay has comeunder greater scrutiny

30*

2021*

30

2020

23

2019

11

2018

11

2017

146*13767

948

00

2015 2016 2017 2018 2019 2020 2021*

Notes: Based on active cases.*As of May 2021

Notes: As of April 2021

Data as of May 2021

1

2015

6

2016

27

2017

49

2018

58

2019

125

2020

152*

2021*

30*

2021*

46

2020

25

2019

13

2018

Notes: Based on active cases

Notes: Based on HQ locationand active cases

Notes: Based on active cases

Notes: Based on active cases.*As of May 2021

Notes: Based on active cases.*As of May 2021

1,5951,416

1,621 1,5571,776

2,195

202020192018201720162015

1,407*

2021*

0 50 100 150 200

ChemicalsDevelopment Banks

AutomobilesElectric & Gas Utilities

Retail & Specialised BanksInsurance

Financial Services - GeneralMining & Metals

EnergyDiversified Banks

Num

ber o

f con

trov

ersi

es

0 200 400 600 800 1,000 1,200

Pharmaceuticals& Biotechnology

ChemicalsEnergy

Technology-HardwareSpecialised Retail

Retail & Specialised BanksFinancial Services - General

FoodAutomobiles

TelecommunicationsSoftware & IT Services

Mining & MetalsDiversified Banks

Non-Financial Corporates: Rating Activity During COVID-19

Then & Now: the number of speculative grade corporate issuers pre-COVID-19 was significantly higher versus pre-2008 credit crisis

Recent downgrades represent a small percentage of the total non-financial corporates rated universe*

Majority of downgrades within speculative grade*

Late cycle reports highlighted corporate credit stress prior to COVID-19

Top 10 sectors most affected by COVID-19*

The spread of the coronavirus has placed significant stress on the global economy, but corporate downgrades reveal a thorough and measured approach to credit during turbulent times.

© 2

020

Moo

dy’s

Corp

orat

ion,

Moo

dy’s

Inve

stor

s Ser

vice

, Inc

., M

oody

’s An

alyt

ics,

Inc.

and

/or t

heir

licen

sors

and

affi

liate

s (co

llect

ivel

y, “

MO

OD

Y’S”

). Al

l rig

hts r

eser

ved.

For more information, visit moodys.com/coronavirus

Q4 2007

Investment GradeSpeculative Grade

54% 46% 37%

SECTOR % DOWNGRADED WITHIN SECTOR

54

32

35

44

56

34

40

35

65

Increase in B3s heightens market's vulnerability to a new default cycle

Current weak credit quality could fuel Caa issuers’ defaults in next downturn

As low-rated spec-grade universe expands, more rated companies will likely default or be downgraded in the next downturn

Global CLOs – in a severe downturn scenario, credit quality declines significantly, impairing junior tranches

Loan and bond convergence: investors pave way for lower recoveries in next downturn

The top 10 ways loan investors are forfeiting protections

25MAY2019

09SEP

2019

29OCT2019

05SEP

2019

09SEP

2019

13NOV2019

FALLEN ANGELS IN DETAIL “Fallen Angels” are entities that move frominvestment grade to speculative grade

66%increase in 2019 speculative grade rated issuer count vs. 2007

Company Limited

Systems Limited

942Speculative Grade

121Investment Grade

227

91

176

583

178

5Aa

A

Baa

Ba

B

Caa

Ca1Aaa

Total downgrades

1,063~30% of total

corporate rated universe

Q4 2019

Mar 1 – Nov 30, 2020

Mar 1 – Nov 30, 2020

Total # of downgrades per category, Mar 1 – Nov 30, 2020

Proportion of publicly rated issuers by category

Proportion of publicly rated issuers by category

88% increase in B-rated issuers vs. 2007

VIEW REPORT

VIEW REPORT

VIEW REPORT

VIEW REPORT

VIEW REPORTVIEW REPORT

63%

Hotel, Gaming & Leisure

Apache Corporation

Carnival Corporation

Automotive

Services: Consumer

Energy: Oil & Gas

Aerospace & Defense

Advertising, Printing & Publishing

Transportation: Consumer

Retail

Consumer goods: Durable

31

*Includes all publicly-rated nonfinancial corporate entities; excludes subsidiaries and project finance-related corporations

About 1% of companies across all rating categories were under review for downgrade at the end of November, about the same at 1% at the end of October and 8% at the end of April. An additional 30% had negative outlooks.

SpeculativeGrade:

942

InvestmentGrade:

86

FallenAngels:

35

11%of total IG

rated population

38%of total SG

rated population

Media: Diversified & Production

APAC EMEAAMER

Gap, Inc. (The)Macy's, Inc.Michael Kors (USA), Inc.

ZF Friedrichshafen AG

Assets Management Co., Ltd.

Calculation reflects percentage of corporate families with at least one downgrade since March 1. Some corporate families include multiple issuers and some issuers have received multiple downgrades. Percentages reflect current number of issuers in each sector; ratings withdrawn since 1 March 2020 are excluded.

Exhibit does not include DIC Corporation (APAC) or Wirecard (EMEA) because these ratings have been withdrawn.

Explore our infographics hubDiscover the latest insights at mdy.link/infographics

Auto sector performance will shape global growthdue to high interconnectedness

For more information, visit moodys.com

Automakers & Part Suppliers

$337 BN

Auto sales unlikely to reach pre-crisis level before mid-2020s

Workforce % Manufacturing % Exports %

Auto sector has significant impact on global economyGlobal exports totaled $1.3 billion

Base case 20202019 actual Base case 2021

3.8%US

6.1%EU

8.3%Japan

17.7%US

14%EU

21.6%Japan

9.4%US

12.6%EU

22%Japan

12,825 K14,900 K

US

17,100 K11,410 K13,406 K

W. Europe

16,309 K3,292 K3,951 K

E. Europe

4,115 K2,470 K2,964 K

India

3,528 K4,360 K4,665 K

Japan

5,129 K23,200 K23,780 K

25,769 K

China

Fundamental auto trends, including stricter emissions regulation, autonomous driving and connectivity, lead to increasing number of touchpoints with other industries.

-8.2%-10%2.5%-11.8%

-30%20%

-4.4%-35%15%

0.9%-30%17.5%

-2.7%-20%20%

-1.4%-15%7%

-1.2%-25%16.2%

Metals & Mining

$209 BNRated debt outstanding

Rising number of batteries in AFVs will

drive demand for cobalt, nickel and copper

Media & Telco

$1,300 BNRated debt outstanding

Connectivity will drive demand for bandwidth,

offsetting 5G investmentTechnology

$977 BNRated debt outstanding

Rising use of digital systems will spur demand

for chips and software

Oil & Gas

$1,434 BNRated debt outstanding

AFV growth will slow demand for diesel

and gasoline

Utility &Infrastructure

$1,587 BNRated debt outstanding

AFV growth will drive demand for power

and capex

Number and growth rates represent Moody’s forecast for Light Vehicle Registrations.

2,018 K2,321 K

Argentina/Brazil

3,105 K

© 2

020

Moo

dy’s

Corp

orat

ion,

Moo

dy’s

Inve

stor

s Ser

vice

, Inc

., M

oody

’s An

alyt

ics,

Inc.

and

/or t

heir

licen

sors

and

affi

liate

s (co

llect

ivel

y, “

MO

OD

Y’S”

). Al

l rig

hts r

eser

ved.

Younger riders return to cities for reduced rent, social / work opportunities

Ridership will grow in 2021...

...but large costs will contribute to slow return to financial stability

US mass transit: ridership faces a long, slow recoveryThe coronavirus pandemic will continue to hurt mass transit systems’ financial performance across the United States. Lockdowns, unemployment, remote working, office closures and slowdowns in the retail and leisure industries have led to large drops in ridership, which will not approach pre-pandemic levels for many years.

To learn more, read the report

Ridership rebounding slower than jobs; multiple factors impeding return to normal service

Key revenues

2019

2020*

2021*

2022*

2023*

Year-over-year % change

0%

4.7 billion

7.4 billion

6.0 billion

9.9 billion

8.9 billion

30%

18%

32%17%

24%

31%

7%

9%

15%

10%

34% 53%

30%

37%

30%

44%44%

60%

43%52%

Top ten issuers by ridership numbers

R

R

R

RR

RR

R

R

RJ

NY MTAChicago Transit AuthorityLos Angeles County MTAWMATAMBTASEPTASan Francisco MTABARTMARTADenver RTD

JJ

JJ

J

J

J

J

J

Aggregate US transit ridership

Salaries & benefits

Fixed costs (pensions, etc)

System operations

Facility maintenance

Capital projects

Impeding factors

Ridership % recovered

Jobs % recovered

R

J

Recovery is calculated as the number of jobs/riders added since the trough in April through September as a percentage of the number of jobs/riders lost from January to April.

* = Projected

Fares 30%

Taxes21%

Federal aid16%

Down 5.7% $25B one-time2020 stimulus Down 53%

in 2020

20%

23%

28%

-52%

Traffic congestion will push people back onto mass transit

Suburban riders moving further out and become 2x per

week rail riders

Subway riders moving to suburbs and

becoming rail riders

Increased car usage in certain cities

Transit riders being locked in due to low income and lack of alternate transport

CITY

COUNTRY

SUBURBS

Long-term migration and usage trends that could

reshape mass transit

Public health concerns

Slow job recovery in key sectors

Temporary and permanent remote work

Remote schools and universities

Access to alternate transportation

Potential transit capacity limits

Potential service cuts

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer / entity page on www.moodys.com for the most updated credit rating action information and rating history.

© 2021 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S CREDIT RATINGS AFFILIATES ARE THEIR CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S (COLLECTIVELY, “PUBLICATIONS”) MAY INCLUDE SUCH CURRENT OPINIONS. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEE APPLICABLE MOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’S CREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS, NON-CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS OR PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing its Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDIT RATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any credit rating, agreed to pay to Moody’s Investors Service, Inc. for credit ratings opinions and services rendered by it fees ranging from $1,000 to approximately $5,000,000. MCO and Moody’s Investors Service also maintain policies and procedures to address the independence of Moody’s Investors Service credit ratings and credit rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold credit ratings from Moody’s Investors Service and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any credit rating, agreed to pay to MJKK or MSFJ (as applicable) for credit ratings opinions and services rendered by it fees ranging from JPY125,000 to approximately JPY550,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.