Embed Size (px)

Citation preview

Essays on Antitrust Issues for Horizontal andVertical Mergers

Mariana Alves da Cunha

Tese de Doutoramento em Economia

Orientada por:

Professor Doutor Helder Vasconcelos

Professora Doutora Paula Sarmento

Porto, Dezembro 2014

For my grandfather (in memoriam).

Biographical Note

Mariana Alves da Cunha was born on October 18, 1987, in Porto, Portugal.

She concluded her undergraduate studies in Economics in 2008 and Master studies in

Economics in 2010, both from Faculdade de Economia e Gestao, Universidade Catolica -

Centro Regional do Porto. Her Master’s dissertation entitled “Eficiencia do Sector de Energia

Electrica na Uniao Europeia” has been supervised by Professor Carlos Santos.

During her Master studies, Mariana has taught at Universidade Catolica - Centro Regional

do Porto (2008-2010): Microeconomics, Econometrics and Mathematics.

In September of 2010, she started her PhD in Economics at Faculdade de Economia da

Universidade do Porto, under the supervision of Professors Helder Vasconcelos and Paula

Sarmento. Her most recent research on mergers has been presented in conferences, as the

4th and 5th edition UECE Lisbon Meetings: Game Theory and Applications (both in Lisbon,

Portugal) and the 8th Annual Meeting of the Portuguese Economic Journal (Braga, Portugal).

Her research has also resulted in two publications in the Journal of Industry Competition in

Trade.

i

Acknowledgements

During my PhD thesis, I received support from many people. I am gratefull to them all.

First of all, I would like to express my gratitude to my supervisors Helder Vasconcelos

and Paula Sarmento from whom I have learned a lot in many ways along this journey. This

work would not be possible without their continuous support, encouragement and guidance.

Their incentives certainly made me go further and I deeply thank them for the patient and for

being present whenever I needed help.

I am also grateful to all of those who have comment some of the essays in this thesis at

conferences and seminars. I would like to highlight the valuable suggestions and comments

of Professors Antonio Brandao, Helder Valente, Joana Pinho, Joao Correia da Silva, Ricardo

Ribeiro and Sofia Castro Gothen.

I gratefully acknowledge FCT (Fundacao para a Ciencia e Tecnologia) for financial sup-

port through a doctoral grant reference SFRH/BD/70000/2010.

I am indebted to a number of friends that have made my PhD a more pleasant experience:

Rita, Miriam, Vera, Diogo, Filipe and Tiago.

Finally, a word of gratitude goes to my boyfriend, Nuno, and to my parents and brother,

for all their unconditional support, love and (huge) patience, during all these years.

Mariana Cunha, Porto, 2014.

ii

Resumo

A presente tese inclui quatro ensaios sobre questoes de polıtica de concorrencia na analise de

fusoes horizontais e verticais. No primeiro ensaio estudamos fusoes horizontais quando as

empresas tem comportamentos estrategicos assimetricos. Alem disso, analisamos uma fusao

sequencial num cenario onde: (i) as empresas concorrem a Stackelberg; (ii) inicialmente

as empresas sao simetricas, mas as fusoes podem dar origem a ganhos de eficiencia e, por

consequencia, a assimetrias de custos entre as empresas; e (iii) todas as fusoes tem de ser

submetidas a aprovacao pela Autoridade da Concorrencia. Em particular, consideramos dois

tipos de Autoridades da Concorrencia: uma Autoridade da Concorrencia mıope, que avalia

a proposta de fusao sem antecipar que poderao existir outras fusoes subsequentes, e uma

Autoridade da Concorrencia com visao futura, que antecipa a estrutura final de mercado, no

caso da primeira fusao ser aprovada.

O segundo ensaio utiliza um modelo semelhante ao caracterizado no primeiro ensaio.

Neste ensaio estudamos a lucratividade das fusoes, o problema do free-riding e os efeitos in-

duzidos das fusoes no bem estar social e no bem estar dos consumidores, quando as empresas

concorrem a Stackelberg e as fusoes geram assimetrias de custos entre as empresas existentes

na industria. Em particular, mostramos que as conclusoes sobre a lucratividade das fusoes,

os efeitos no bem estar e a existencia do problema do free-ridding depende de forma crucial

dos ganhos de eficiencia gerados pelas fusoes.

No terceiro ensaio exploramos o papel da incerteza na decisao de fusao e no seu controlo

pelas autoridades de concorrencia. Num cenario de concorrencia a Cournot, consideramos

que as fusoes podem gerar ganhos de eficiencia incertos e que todas a fusoes tem de ser

iii

submetidas para aprovacao da Autoridade da Concorrencia. O objectivo deste ensaio e nao

so estudar o impacto da incerteza na probabilidade da fusao ser proposta pelas empresas

e aceite pela Autoridade da Concorrencia mas tambem analisar de que forma a incerteza

influencia os incentivos das empresas que ficam de fora da fusao a prosseguirem estrategias

de free-riding.

Por fim, no quarto ensaio analisamos de que forma a integracao vertical aumenta os in-

centivos ao conluio das empresas retalhistas. O principal contributo deste ensaio e realcar a

relacao entre dois tipos de estrategias das empresas: a integracao vertical e o conluio, num

cenario em que nem todas as empresas aceitam o acordo colusivo (conluio incompleto).

iv

Abstract

This thesis comprises four essays on antitrust issues for horizontal and vertical mergers. In

the first essay we study horizontal mergers when firms have asymmetric strategic roles. In this

essay we assume a sequential merger formation game in a setting where: (i) firms compete a

la Stackelberg; (ii) all firms are ex-ante symmetric, but as mergers may give rise to endoge-

nous efficiency gains, cost asymmetries between the remaining firms in the industry may be

created; and (iii) every merger has to be submitted for approval to the Antitrust Authority. In

particular, we consider two possible types of Antitrust Authorities: a myopic Antitrust Au-

thority, that evaluates a merger proposal without anticipating possible subsequent mergers,

and a forward looking Antitrust Authority, which is able to anticipate the ultimate market

structure if the merger is approved.

The second essay uses a framework similar to the previous one. In this essay we inves-

tigate mergers’ profitability, free-riding problem and induced effects on social and consumer

welfare when firms are in a Stackelberg market and mergers can create cost heterogeneity

between the remaining firms in the industry. In particular, we show that conclusions about

the merger profitability, the social welfare effects and the existence of a free-riding problem

crucially depend on whether the merger creates synergies.

In the third essay we explore the role of uncertainty in merger control and in merger de-

cisions. In a Cournot setting, we consider that mergers may give rise to uncertain efficiency

gains and that every merger has to be submitted for approval to the Antitrust Authority. We

assume that both the Antitrust Authority and the firms in the industry face the same uncer-

tainty about the future efficiency gains induced by the merger. The purpose of this essay is

v

not only to study the impact of the existence of uncertainty in the likelihood of the merger

being proposed by the firms and accepted by the Antitrust Authority but also to analyze how

the uncertainty affects outsider firms’ incentives to free-ride on it.

Finally, the fourth essay analyzes how vertical integration increases downstream firm’s

incentives to collude. The main contribution of this essay is to highlight the importance of

considering, simultaneously, two types of firms’ strategies: vertical integration and collusion,

in a context where some firms have no incentives to collude (incomplete collusion).

vi

Contents

1 Introduction 1

2 Efficiency gains of mergers in Stackelberg markets with an active Antitrust Au-

thority 5

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.2 Basic Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.3 Before the merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.4 Merger involving the two leader firms . . . . . . . . . . . . . . . . . . . . . 13

2.4.1 Merger of two leaders under a Myopic AA . . . . . . . . . . . . . . 14

2.4.2 Merger of two leader firms under a forward looking AA . . . . . . . 19

2.5 Extensions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

2.5.1 Social Welfare standard . . . . . . . . . . . . . . . . . . . . . . . . 24

2.5.2 Other merger possibilities . . . . . . . . . . . . . . . . . . . . . . . 26

2.6 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

3 Mergers in Stackelberg Markets with Efficiency Gains 37

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

3.2 Baseline Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

3.2.1 Pre-merger equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . 41

3.3 Merger Effects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

3.3.1 Insiders’ Profitability . . . . . . . . . . . . . . . . . . . . . . . . . . 44

vii

3.3.1.1 Numerical simulation results on merger profitability . . . . 49

3.3.2 Free-riding problem . . . . . . . . . . . . . . . . . . . . . . . . . . 51

3.3.3 Consumer Surplus and Social Welfare . . . . . . . . . . . . . . . . . 53

3.3.3.1 Consumer Surplus Standard . . . . . . . . . . . . . . . . . 54

3.3.3.2 Social Welfare Standard . . . . . . . . . . . . . . . . . . . 57

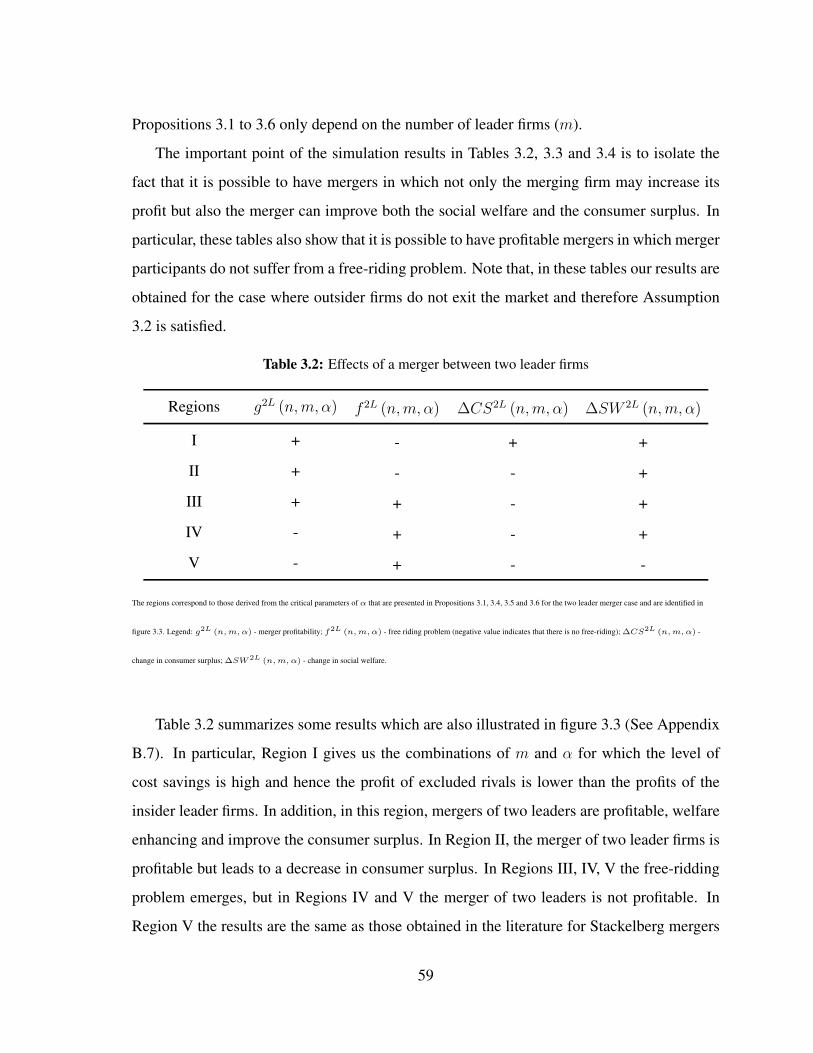

3.4 Simulation Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

3.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

4 Uncertain Efficiency Gains and Merger Policy 81

4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

4.2 Basic Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

4.3 Pre-Merger equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

4.4 Merger Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

4.4.1 Product Market Competition . . . . . . . . . . . . . . . . . . . . . . 89

4.4.2 Expected Profits and Consumer Surplus . . . . . . . . . . . . . . . . 90

4.4.3 Antitrust Authority’s Decision . . . . . . . . . . . . . . . . . . . . . 94

4.4.4 Merger Decision . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

4.4.5 Free-riding Problem . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.5 Numerical Application . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

4.6 Concluding Remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

5 Does Vertical Integration Promote Downstream Incomplete Collusion? An Eval-

uation of Static and Dynamic Stability 113

5.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

5.2 The Baseline Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118

5.2.1 The Model without Vertical Integration . . . . . . . . . . . . . . . . 122

5.2.1.1 Collusive Results . . . . . . . . . . . . . . . . . . . . . . 122

5.2.1.2 Cournot Equilibrium . . . . . . . . . . . . . . . . . . . . 124

viii

5.2.1.3 Deviation Results . . . . . . . . . . . . . . . . . . . . . . 125

5.2.2 The Model of Vertical Integration with a cartel member . . . . . . . . 127

5.2.2.1 Collusive Results . . . . . . . . . . . . . . . . . . . . . . 127

5.2.2.2 Cournot equilibrium . . . . . . . . . . . . . . . . . . . . . 130

5.2.2.3 Deviation Results . . . . . . . . . . . . . . . . . . . . . . 130

5.2.3 The Model of Vertical Integration with a fringe firm . . . . . . . . . 134

5.2.3.1 Collusive Results . . . . . . . . . . . . . . . . . . . . . . 134

5.2.3.2 Cournot equilibrium . . . . . . . . . . . . . . . . . . . . . 136

5.2.3.3 Deviation Results . . . . . . . . . . . . . . . . . . . . . . 136

5.3 Welfare analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

5.4 Discussion of Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

5.5 Concluding Remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144

Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

References 155

ix

List of Figures

2.1 Merger of two leaders: equilibrium outcomes with a myopic AA. . . . . . . . 18

2.2 Merger of two leaders: equilibrium outcomes with a forward looking AA. . . 23

2.3 Merger of two leaders: equilibrium results with a myopic SW-maximizer AA. 24

2.4 Merger of two leaders: equilibrium results with a forward-looking SW-maximizer

AA. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

2.5 Merger of two followers: equilibrium outcomes with a myopic AA. . . . . . 27

2.6 Merger of two followers: equilibrium outcomes with a forward looking AA. . 27

2.7 Merger of one leader and one follower: equilibrium results with a myopic AA. 28

2.8 Merger of one leader and one follower: equilibrium results with a forward

looking AA. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.1 Merger profitability for n = 6 and m = 3 . . . . . . . . . . . . . . . . . . . 47

3.2 ∆Consumer Surplus . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

3.3 Critical parameters of α for a merger between two leader firms . . . . . . . . 78

3.4 Critical parameters of α for a merger between two follower firms . . . . . . . 79

3.5 Critical parameters of α for a merger between a leader and a follower firms . 80

4.1 AA’s decision (m = 2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99

4.2 AA’s decision (m = 3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

4.3 AA’s decision (m = 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

4.4 AA’s decision (m = 2, 3, 4) . . . . . . . . . . . . . . . . . . . . . . . . . . 102

5.1 Model’s critical discount values for K=F+2 . . . . . . . . . . . . . . . . . . 141

x

5.2 Model’s critical discount values for K=F+3 . . . . . . . . . . . . . . . . . . 141

xi

List of Tables

2.1 Efficiency gains results, by region and by AA for each merger case . . . . . 30

3.1 Efficiency gains conditions for profitable mergers and no exit . . . . . . . . . 49

3.2 Effects of a merger between two leader firms . . . . . . . . . . . . . . . . . 59

3.3 Effects of a merger between two follower firms . . . . . . . . . . . . . . . . 60

3.4 Effects of a merger between a leader and a follower firms . . . . . . . . . . . 61

5.1 Static and Dynamic Stability Results - Model 1 . . . . . . . . . . . . . . . . 126

5.2 Static and Dynamic Stability Results - Model 2 . . . . . . . . . . . . . . . . 133

5.3 Static and Dynamic Stability Results - Model 3 . . . . . . . . . . . . . . . . 137

5.4 Welfare analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

xii

Chapter 1

Introduction

The present thesis is organized in five chapters. This first chapter gives an overview of the

thesis’s organization and familiarizes the reader with the main research topics. Each research

question is answered in its own chapter as an independent essay, consisting of introduction

that includes the literature review and some practical applications, methodology, discussion

of the results, conclusion and policy implications. Some of these individual essays are, how-

ever, related to each other and some overlap in content is inevitable, especially with regard to

the assumptions of the theoretical models.

Horizontal mergers in concentrated industries are an important issue for antitrust authori-

ties. Mergers can reduce industry competition and hence result in higher prices, which could

harm consumers. However, a merger can also be welfare-enhancing if it generates efficiency

gains, increases incentives for innovation or creates synergies and scale economies among

firms. Then, the efficiency gains might offset the increased market power and result in higher

social welfare. Therefore, the horizontal merger could actually lead to more efficient firms

and to lower prices, which benefits consumers. Usually, the welfare analysis of mergers

assumes that firms have incentives to merge because this could increase their profits by in-

creasing the prices or reducing the costs. Stigler (1950) argued that firms that do not merge

(outsiders) may also benefit more than the participants (insiders). With the merger, the new

firm will reduce its production and then the industry price will increase. However, the non-

1

participants firms will expand their output and therefore will have higher profits due to the

high industry price.

The first essay (Chapter 2) is concerned with horizontal mergers, in a setting where the

firms in the market have asymmetric strategic roles. In this essay we assume a sequential

merger formation game in a setting where: (i) firms compete a la Stackelberg; (ii) all firms are

ex-ante symmetric, but mergers may give rise to endogenous efficiency gains and, therefore,

cost asymmetries between the remaining firms in the industry; and (iii) every merger has to

be submitted for approval to the Antitrust Authority. In particular, we consider two possible

types of Antitrust Authority: a myopic Antitrust Authority, that evaluates a merger proposal

without anticipating that this merger might trigger other subsequent mergers, and a forward

looking Antitrust Authority, which is able to anticipate the ultimate market structure a merger

will lead to, if approved. We find that these two types of Antitrust Authority adopt similar

decisions whenever a merger would not trigger the exit of outsider firms. The Antitrust

Authorities’ decisions are, however, shown to be very different when evaluating exit-inducing

merger proposals.

The second essay (Chapter 3) is related to the previous one and is concerned with merg-

ers’ profitability, free-riding problem and induced effects on social and consumer welfare of

mergers, when firms are in a Stackelberg market and mergers can create cost heterogeneity

between the remaining firms in the industry. We find that under certain conditions regarding

the cost benefits resulting from mergers, the so called “free-riding” problem is eliminated and

mergers are not only profitable but also welfare enhancing, even with linear costs.

The assessment of the efficiency gains resulting from a merger usually raises an informa-

tion issue for antitrust authorities. Although some mergers can actually generate significant

efficiency gains, these are usually difficult to measure and verify. In practice, it is often the

case where both the firms and the antitrust authority cannot predict exactly the post-merger

efficiency gains, implying that they are not aware of all the conditions they are going to

face after the merger. Sometimes, only after the merger firms and antitrust authorities will

understand the true level of the merger’s induced efficiency gains. For instance, some phar-

2

maceutical firms may adopt merger decisions without knowing whether their R&D efforts

will be successful or not. Also, any type of firms’ investment could generate uncertainty

about future costs and, sometimes, a merger could actually occur before the uncertainty is

resolved.

In the third essay (Chapter 4), we explore the role of uncertainty in merger control and

in merger decisions. In a Cournot setting, we consider that mergers may give rise to uncer-

tain efficiency gains and that every merger has to be submitted for approval to the Antitrust

Authority. We assume that both the Antitrust Authority and the firms in the industry face the

same uncertainty about the future efficiency gains induced by the merger. The purpose of

this essay is to contribute to the literature that studies the efficiency gains’ role in merger de-

cisions, departing from a deterministic environment by considering a setting in which there

is (symmetric) uncertainty. The present essay then contributes to fill the gap in the extant

literature by assuming that, when firms propose the merger to the Antitrust Authority, all

the players (insider, outsiders and Antitrust Authority) are uncertain about the post-merger

efficiency gains and therefore they decide by considering the expectations on those gains.

Once the merger is consummated, both insider and outsider firms can observe the efficiency

gains and compete a la Cournot. This analysis is useful to the Antitrust Authority in order

to more properly evaluate merger proposals, when there is uncertainty about the cost savings

that mergers may induce. It is shown that an increase in the degree of uncertainty benefits

both insider and outsider firms but also the consumers. Further, when uncertainty is high,

there is a greater likelihood that firms propose a merger to the Antitrust Authority and the

Antitrust Authority accepts it. Interestingly, however, although uncertainty enhances merger

approval chances, it also decreases merger’s stability, by increasing outsiders’ incentives to

free-ride on it.

Theoretical literature on vertical integration has also gained a great contribution from re-

searchers on industrial economics for many years. The analysis of the anticompetitive effects

of vertical integration has been a debated topic of research in Industrial Organization. Vertical

integration can have negative impacts on welfare due to coordinated effects, that is, vertical

3

integration may improve the sustainability of collusion among competing firms. Antitrust

authorities have remained concerned that vertical integration might facilitate collusion at up-

stream and downstream levels. Vertical integration facilitates collusion if, after the merger,

upstream or downstream firms are able to coordinate in a more effectively way than if they

were operating separately.

The fourth essay (Chapter 5) is about how vertical integration increases firm’s incentives

to collude. The literature suggests that there is a relationship between vertical integration

and collusion. Particularly, vertical integration might ease the collusive agreements, by sup-

porting the punishment and monitoring mechanisms and by allowing the agreement between

firms. Moreover, the models presented in the literature study if vertical integration facilitates

upstream or downstream collusion and differ mainly on the assumptions chosen. It is possible

to verify that most of these studies concluded that vertical integration facilitates collusion in

downstream or upstream level. The main contribution of the fourth essay is to highlight the

importance of considering, simultaneously, two types of firms’ strategies: vertical integra-

tion and collusion, in a context where some firms have no incentives to collude (incomplete

collusion). Then, we try to answer the following question: does vertical integration promote

incomplete collusion? This research topic could be very important for antitrust authorities be-

cause they are concerned with the impacts of vertical integration on collusion and how these

two types of strategies might affect social welfare. We find that a vertical merger between

an upstream firm and a downstream cartel or fringe firm promotes downstream collusion, un-

der certain conditions on the market size. Moreover, a welfare analysis shows that consumer

surplus increases with the vertical merger since it partially eliminates the double marginaliza-

tion problem. The results obtained could modify the formulation of policies towards vertical

mergers.

All of these questions are interesting and also bring some important insights that could

be helpful for the antitrust authorities’ intervention. In this context, all these issues seem to

be important for antitrust authorities when deciding whether or not to accept a horizontal or

vertical merger.

4

Chapter 2

Efficiency gains of mergers in

Stackelberg markets with an active

Antitrust Authority

2.1 Introduction

The large body of previous literature on the effects of horizontal mergers has argued that

Antitrust Authorities should pay particular attention to the balance between anticompetitive

price (market power) effects and pro-competitive merger related efficiency improvements

(see e.g. Williamson (1968) and Farrell and Shapiro (1990)).1

The European Commission (EC), in practice, has so far never used efficiency gains ar-

guments to clear a merger. When the merging parties use the “efficiency defence argument”

reporting that the merger would generate cost reductions, this claim usually has been dis-

missed by the EC. The EC uses the efficiency offence argument arguing that although the

merger would benefit the consumers in the short-run, in the long-run rival firms have incen-

tives to exit the industry and then the merging firm would become a monopolist, thereby

1The analysis of merger-induced efficiencies was introduced into the US Merger in 1997 (Section 4) and

into the European Merger Guidelines in 2004 (European Commission Horizontal Merger Guidelines, 2004/03,

Article 7).

5

harming consumers’ welfare. This efficiency offence argument has received some atten-

tion by economists, providing an informal discussion of efficiency offence arguments in EC

practices, such as Padilla (2002). The efficiency offence argument has also been formally

analyzed on a static and a dynamic framework (Motta, 2004; Motta and Vasconcelos, 2005).

However, to the best of our knowledge, scarce attention has been devoted to the study of

efficiency defence arguments, in contexts where merging parties have asymmetric strategic

power.

In this paper, we contribute to close this gap in the literature by studying an endogenous

merger formation game wherein: (i) merging parties compete a la Stackelberg; (ii) all firms

are ex-ante symmetric, but mergers may give rise to endogenous efficiency gains and, there-

fore, cost asymmetries between the remaining firms in the industry; and (iii) every merger

must be submitted for approval to an Antitrust Authority (AA). In particular, we consider

two possible types of AA: a myopic AA, that evaluates a merger proposal without antici-

pating that the corresponding merger might trigger other subsequent mergers, and a forward

looking AA, which is able to anticipate the ultimate market structure a merger will lead to if

approved.

Although in reality there are merger waves (or sequential mergers), usually the AAs rarely

adopt forward-looking decisions when analyzing a merger case, since it is hard to predict the

future behavior of the firms. Also AAs might make mistakes in predicting that following a

merger, outsiders might leave. However, the economic literature (eg. Motta and Vasconcelos

(2005) and Nocke and Whinston (2010)) has emphasized the need for those AAs to predict

which is the ultimate market structure, after the first merger takes place. Recently, the Centre

on Regulation in Europe (CERRE) published a dossier to the European Commission (EC)

where it includes some recommendations on the future regulatory policy in network industries

(CERRE, 2014). This report highlights that the EC and national competition authorities

should pay particular attention to the dynamic issues when investigating mergers such as,

in electronic communications and media markets and concludes that the merger policy is

currently not very good at assessing the dynamic effects of mergers, given its static focus on

prices. In this sense our paper is a theoretical contribution that suggests that when predicting

6

the possible impact of the merger, possible reactions by the outsiders (defensive mergers)

should be properly taken into account. More particularly, before concluding that a merger

will create such a more efficient merged entity that rivals would not be able to compete with

it, AAs should consider whether in the industry at hand there exists room for further mergers

allowing outsiders to attain similar efficiency levels, and/or whether the outsiders might be

able to enhance efficiency through internal growth.

Within this theoretical structure, we find that, when evaluating a two-firm merger pro-

posal, both myopic and forward-looking AAs adopt similar decisions if the proposed merger

would not trigger the exit of outsider firms in case it was approved (and no further mergers

take place). Nevertheless, their decisions are shown to be in sharp contrast when evaluating

exit-inducing merger proposals, i.e, in the region where efficiency gains and the fixed costs

are sufficiently high such that the merger would trigger the exit of outsider firms. In particu-

lar, under some circumstances, while the myopic AA blocks the merger under an efficiency

offence argument, the forward looking AA approves the very same merger proposal, since

it correctly anticipates that this merger will be followed by a subsequent defensive merger

involving the outsider firms of the first merger. This will lead to a duopoly situation wherein

even though firms have asymmetric strategic power, they end up being equally sized and

equally efficient, to the benefit of consumers.

This paper is mainly related to three strands in the extant literature. Firstly, it is related

to the literature on endogenous horizontal mergers, since we explicitly model the merger

formation process. Important references in this literature are Kamien and Zang (1990),

Gowrisankaran (1999), Faulı-Oller (2000), Horn and Persson (2001a,b), Motta and Vasconce-

los (2005), Fumagalli and Vasconcelos (2008), Fumagalli and Nilssen (2008), Banal-Estanol

et al. (2008), Vasconcelos (2010) and Nocke and Whinston (2010), to name a few.2

Secondly, our paper is also related to the previous literature that incorporates an active AA

into the merger formation game. Few studies have introduced the AA as an active player, such

as, Motta and Vasconcelos (2005), Fumagalli and Nilssen (2008), Fumagalli and Vasconcelos

2Other papers also assumed sequential game but with exogenous mergers, such as Nilssen and Søgard

(1998) and Salvo (2006).

7

(2008), Vasconcelos (2010) and Nocke and Whinston (2010).

Thirdly, this paper is also related to the branch of the literature that deals with the eco-

nomic analysis of merger control by taking into account the efficiency defence argument.

The efficiency defence argument refers to the case where the AA approves the merger if the

efficiencies caused by the merger more than compensate for the induced increase of market

power. Some papers include the AA’s efficiency defence argument when evaluating a merger

and some also analyze the role of structural remedies introduced by the AA after the merger

takes place, such as, Roller et al. (2000), Motta and Vasconcelos (2005), Fumagalli and

Nilssen (2008), Fumagalli and Vasconcelos (2008), Banal-Estanol et al. (2008), Vasconcelos

(2010) and Nocke and Whinston (2010).3

Our paper is closely related to Motta and Vasconcelos (2005)’s paper, who also studied

endogenous mergers, where each merger has to be approved by the AA. Motta and Vascon-

celos (2005) show that if the AA does not anticipate subsequent merging, such a myopic

AA could actually make wrong decisions. However, if the AA correctly anticipates that

the merger is followed by other mergers, no efficiency offence argument is justified. Like

Motta and Vasconcelos (2005), we also consider that the AA maximizes consumer welfare

and, therefore, the AA approves both mergers if consumer surplus increases (i.e. if prices

decrease).4

There are two major differences between Motta and Vasconcelos (2005) framework and

the setting used in this paper. First, Motta and Vasconcelos (2005) assume that the mergers

3The inclusion of an efficiency defence argument could bring an asymmetric information problem with

respect to the merger’s efficiency gains between the AA and the merging firms. Some papers consider the issue

of asymmetric information about merger-specific efficiencies, such as, Gonzalez (2004), Medvedev (2004),

Lagerlof and Heidhues (2005), Cosnita and Tropeano (2009), however, this analysis is far beyond the scope of

this paper.4By assuming that the AA evaluates mergers according to a consumer surplus standard this does not mean

that this is always better than the total welfare standard. However, as Lyons (2002) argued, the consumer

surplus standard is applied in most antitrust jurisdictions. Other papers also study how the AA should apply the

consumer surplus standard when challenging a merger, such as Besanko and Spulber (1993), Neven and Roller

(2005), Vasconcelos (2010), Nocke and Whinston (2010), Jovanovic and Wey (2012), among others.

8

occur under symmetric Cournot competition. In contrast, in this paper is assumed that the

mergers occur when firms have asymmetric strategic power and, therefore, it is assumed that

different types of mergers may occur in an industry characterized by Stackelberg competi-

tion.5 This assumption implies that, in the setting proposed in the current paper, when the

efficiency gains are very small (or even when there are no efficiency gains) a merger between

two firms will always be proposed because it still is profitable, which is not the case under

Cournot. When there is no strategic power advantage for any firm we obtain the well known

Salant et al. (1983) merger’s paradox: a merger between two firms with the same strategic

power that creates a firm of the same type is always unprofitable for the merging firms, unless

more than 80% of the firms in the industry merge or there are sufficiently high fixed costs.

Also, we found that in an asymmetric strategic power industry, the AA will be more severe

when blocking the mergers since the interval of efficiency gains where mergers are usually

accepted is greater under Stackelberg than under Cournot. Second, Motta and Vasconcelos

(2005) consider, under the forward looking AA, that after the defensive merger occurs, the

firms of the first and the second merger are allowed to seek a merger to a monopoly. However,

in this paper, we rule out merger to monopoly since we want to analyze the competitive effects

of merger proposals in which both at the status quo industry structure and in the merger

induced industry structure firms do have asymmetric strategic power.

Although this paper encompasses a theoretical exercise, it is also motivated by the prof-

itability of real-world mergers involving firms with asymmetric strategic power. A case in

point is the DRAM (Dynamic Random Access Memory) industry, where the leading man-

ufacturers announce their production plans in advance and manufacturers, which enter the

market later, respond by adjusting their quantity of DRAM produced. In addition, in this

specific industry, the last decades have witnessed a wave of mergers.6 Another example is

Microsoft’s dominance in software markets. In this case, although Microsoft usually makes

5See Daughety (1990), Feltovich (2001), Huck et al. (2001), Escrihuela-Villar and Faulı-Oller (2007), Hey-

wood and McGinty (2007, 2008) and Brito and Catalao–Lopes (2011) on the profitability of mergers involving

Stackelberg firms operating in a context without merger induced synergies.6For details, see Escrihuela-Villar and Faulı-Oller (2007) and the references cited therein.

9

decisions first, other smaller companies typically react to Microsoft’s actions when making

their own decisions. Obviously, these subsequent followers’ actions, in turn, affect Microsoft

(see e.g. Graham (2013)). In both examples, it seems reasonable and plausible to analyze

both firms and AA decisions when firms have asymmetric strategic power.

The remainder of the paper is organized as follows. Section 2.2 introduces the baseline

assumptions of the model. Section 2.3 presents the results before the merger. Section 2.4

analyzes the post-merger industry structure under two different scenarios regarding the be-

haviour of the AA (myopic and forward looking), for the case in which the merger involves

two leaders. In Section 2.5, we discuss two extensions of the benchmark model. In particular,

we extend the analysis by assuming that now both AAs consider the effects of the two-leader

merger on social welfare, instead of considering only the effects on consumer surplus. Fur-

ther, we also present the results obtained for alternative types of mergers. Finally, Section

2.6 concludes the paper by discussing the results obtained. All proofs and details on the

calculations are relegated to the Appendix.

2.2 Basic Model

We consider a market with N = 4 firms. We assume a two stage-game. First, all leaders

simultaneously choose their output levels. Second, all followers simultaneously choose their

output levels, after observing the leaders’ choices. We assume that there are two leaders

and two followers that compete in quantities over a linear demand P = 1 − Q, where Q =

QL +QF .

What distinguishes firms is the amount of capital they own. Hence, the cost function of a

firm which owns ki units of the industry capital and produces qi units of output is given by:

C(qi, ki, α) = αKkiqi + kif

where α ≥ 0,N=4∑i=1

ki = K = 4 and f > 0.

The total supply of capital is assumed to be fixed to the industry (and equal to K =

4 units) and ki is firm i’s capital holdings. By assuming that the total quantity of capital

10

available in the industry is fixed, we are also assuming that entry is very difficult in this

industry. This cost structure was proposed by Motta and Vasconcelos (2005). Each firm

operates with a constant marginal cost of production, but the level of its marginal cost is a

decreasing function of its capital holdings, ki. In addition, it is assumed that there exists a

plant specific fixed cost f , which has to be paid for each unit of industry’s capital owned by

the firm. This fixed cost could be, for instance, a plant specific fixed fee associated with an

energy suppliance contract. Also, at the status quo industry structure, each firm is endowed

with a single unit of capital (ki = 1), implying that all firms are symmetric in terms of costs.

However, cost asymmetries may arise as a result of a merger (or a series of mergers), that

is, assuming that two firms merge, the merged firm has now two units of capital and the

non-merged firms still have one unit of capital each. With this type of cost structure, we

capture two distinct cost effects induced by a merger. First, a merger brings the capital of

merging parties into a single larger entity and, therefore, gives rise to endogenous efficiency

gains. The higher the value of α is, the stronger the efficiency gains induced by a merger

are. Second, by creating a larger firm, the merger has also the effect of increasing fixed costs

proportionally. This effect is captured by the parameter f in the cost function.

We assume that there is Stackelberg competition and that firms are allowed to merge

before competition in the product market. However, when firms merge, they will have to ask

the Antitrust Authority (AA) for authorisation. Following Motta and Vasconcelos (2005) we

also assume that there are two different scenarios. First, we assume that the AA is myopic

and, hence, when deciding to accept or not the merger it does not take into account that

the merger can be followed by other mergers (Section 2.4.1). Second, we assume that the

AA is forward looking and anticipates the ultimate market structure a merger will lead to

(Section 2.4.2). Further, in order to keep the analysis simple, we assume a consumer-surplus-

maximizer AA.

11

2.3 Before the merger

As mentioned, at the status quo industry structure, firms are symmetric and each firm has one

unit of the industry capital. In addition, since there is a sequential output choice: first we

have leader firms decision and then the followers decide, we solve the game following the

usual backward induction procedure. So, each follower firm chooses qFi that maximizes their

profit, taking the output of the leader as given. The profit function of follower firm 1 is given

by:

max πF1 =

(1− qF1 −

2∑j=1

qLj − qF2

)qF1 − 4αqF1 − f

where qF1 , qF2 and qLj , with j = 1, 2, represent, respectively, the outputs produced by

each follower and each leader firm. By symmetry, all follower firms choose the same output

and, therefore, the best reply function of each follower firm is given by qF =1−qL1 −qL2 −4α

3.

Acting as a Stackelberg leader against the follower firms, each leader firm is going to produce

qLj = 1−4α3. Hence, we find that, at the symmetric initial market structure (L,L,F,F), the

equilibrium quantities, profits, market price, Consumer Surplus (CS), Producer Surplus (PS)

and Social Welfare (SW) are given by:

qLj (L,L,F,F) =1− 4α

3,with j = 1, 2 (2.1)

qFi (L,L,F,F) =1− 4α

9,with i = 1, 2 (2.2)

πLj (L,L,F,F) =1

3

(1− 4α

3

)2

− f (2.3)

πFi (L,L,F,F) =

(1− 4α

9

)2

− f (2.4)

P (L,L,F,F) =1 + 32α

9(2.5)

CS (L,L,F,F) = 32

(1− 4α

9

)2

(2.6)

PS (L,L,F,F) = 8

(1− 4α

9

)2

− 4f (2.7)

12

SW (L,L,F,F) = 40

(1− 4α

9

)2

− 4f (2.8)

From the analysis of equations (2.1) and (2.2) it can be demonstrated that when α ≥ 14,

then both leader and follower firms would not produce, i.e. qLj = qFi ≤ 0. Also, for leader

and follower firms to produce, their fixed costs should not be very high otherwise their profits

would be zero, that is, πL > 0 ⇔ f < 13

(1−4α

3

)2 ≡ f1 and πF > 0 ⇔ f <(

1−4α9

)2 ≡ f2.

Since f1 > f2, we only assume that f < f = f2. If f > f , follower firms will not produce

and could exit the market.

Assumption 2.1: Let:7

α <1

4≡ α; f <

(1− 4α

9

)2

≡ f (2.9)

This assumption is imposed to exclude the case in which firms do not produce at the status

quo industry structure.

2.4 Merger involving the two leader firms

Suppose that there is a merger proposal between the two leader firms in the industry. If the

merger occurs, then a larger and more efficient firm is created, owning ki = 2 units of the

industry capital.8 In this section, we analyze the results obtained for the two leader merger

case under two different scenarios regarding the behaviour of the AA: a myopic AA and a

forward-looking AA.

7This is the same as in Motta and Vasconcelos (2005).8In Section 2.5, we discuss the results obtained for two other merger cases.

13

2.4.1 Merger of two leaders under a Myopic AA

For a myopic AA the game is the following:

• First Stage: the two leader firms decide whether to propose a merger (they will do so,

if the merger gives higher profits).

• Second Stage: the AA decides whether to authorise or not the merger of two leaders

and it will not take into account that other mergers might occur.

In the post-merger equilibrium, the merged leader firm and the outsider follower firms

will choose their levels of output that maximize their profits. Hence, the equilibrium levels

of output for the merged leader firm and for outsider follower firms are given by:

QL (2L,F,F) =1 + 2α

2(2.10)

qFi (2L,F,F) =1− 10α

6, with i = 1, 2 (2.11)

Remark 2.1: qFi = 0, if α ≥ 110

and/or f >(

1−10α6

)2 ≡ f2L.

From equations (2.10) and (2.11) we can observe that level of efficiency gains has a

positive effect on insider’s quantity and a negative effect on outsiders’ quantity. When the

merger generates high cost savings, the insider firm produces more and therefore, the outsider

follower firms react by producing less quantity. Further, if the merger gives rise to high

synergies, the two follower outsider firms are constrained to exit the market. Also, if f > f2L,

follower firms are not able to cover the fixed costs and make positive profits.

Suppose for the moment that α < 110. From the equilibrium outputs above, one can

obtain, by substitution, the equilibrium levels of profits for the merged leader firm and for

each outsider follower firms:

π2L (2L,F,F) =1

3

(1 + 2α

2

)2

− 2f (2.12)

πFi (2L,F,F) =

(1− 10α

6

)2

− f (2.13)

14

Additionally, the equilibrium price, the CS, the PS and the SW are given by:

P (2L,F,F) =1 + 14α

6(2.14)

CS (2L,F,F) =1

2

(5− 14α

6

)2

(2.15)

PS (2L,F,F) =212α2 − 28α + 5

36− 4f (2.16)

SW (2L,F,F) =620α2 − 196α + 35

72− 4f (2.17)

After the merger, the market structure is (2L,F,F) or simply (2L), the monopoly industry

structure where only the merged firm is active. The resultant post-merger market structure de-

pends on follower firms’ ability to make positive profits or not. These two different scenarios

are analyzed in the equilibrium analysis of stage 2 that we discuss in turn.

Analysis of Stage 2 At the second stage of the game, the AA has to decide whether or not

to allow the two-leader merger, if the merger has been submitted for approval. The behaviour

of the AA, that depends on the two possible scenarios presented above, is as follows:

• If α < 110

and f <(

1−10α6

)2 ≡ f2L, then outsider follower firms are able to make

positive profits after the merger has taken place. If this is the case, then the AA decides

to authorise the submitted merger only if the prices after the merger are lower or equal

than the prices before the merger, that is, if Consumer Surplus (CS) increases with the

merger:

P (2L, F, F ) = 1+14α6≤ P (L,L, F, F ) = 1+32α

9

which is equivalent to1

22≈ 0.04545 ≤ α <

1

10(2.18)

Hence, in order to authorise the merger, the AA will require that the efficiency gains

are sufficiently high.

15

• If, instead, (i) α ≥ 110

; or (ii) α < 110

and(

1−10α6

)2 ≡ f2L < f < f ≡(

1−4α9

)2

then, from Remark 2.1, one has that the merger induces the two outsider follower firms

to exit the market. Therefore, the industry is characterized by a single monopolist

endowed with two units of capital. The equilibrium profit, price, CS, PS and SW for

the monopolist firm are given by:

π (2L) =

(1− 2α

2

)2

− 2f (2.19)

P (2L) =1 + 2α

2(2.20)

CS(2L) =1

2

(1− 2α

2

)2

(2.21)

PS(2L) =

(1− 2α

2

)2

− 2f (2.22)

SW (2L) =3

2

(1− 2α

2

)2

− 2f (2.23)

• Now, the AA faced with such a merger proposal inducing the exit by outsiders, will

decide to reject it if the following inequality holds:

P (2L) = 1+2α2

> P (L,L, F, F ) = 1+32α9

α <7

46≈ 0.15217 (2.24)

This implies that a merger would not be authorised by the (myopic) AA if efficiency

gains induced by the merger are sufficiently low.

Let us now turn to the analysis of the firms’ decisions at the first stage of the game.

Analysis of Stage 1 Following Motta and Vasconcelos (2005), we also assume that firms

have no administrative costs when submitting the merger to the AA.9 Also, when firms antic-

ipate that the merger will be blocked, they are indifferent between asking or not the AA for9Although the assumption that firms have zero administrative costs from submitting a merger is not very

realistic, assuming that these costs are zero does not matter much, since the equilibrium outcome would not

change if we assumed positive filing costs.

16

authorisation. Firms are assumed to propose a merger to the AA even in the case of indiffer-

ence.

In Stage 1, firms decide whether or not to submit a merger. Again we have to distinguish

two scenarios, depending on whether the merger triggers exit by outsiders or not.

• If α < 110

and f <(

1−10α6

)2 ≡ f2L, then outsider follower firms are able to make

positive profits after the merger has taken place. Anticipating this, insider leader firms

will then merge if the merger is profitable, that is if:

πL(2L, F, F ) =1

3

(1 + 2α

2

)2

− 2f ≥ 2πL(L,L, F, F ) = 2

[1

3

(1− 4α

3

)2

− f

],

(2.25)

which in turn implies that the merger is submitted to the AA for all parameter values in

Assumption 2.1.

Note, however, that from eq. (2.18) we have that the AA will only approve the merger

if α ≥ 122

. This means that for low values of the efficiency parameter, i.e. for α < 122

, the

two-leader merger will always be submitted but blocked by the myopic AA.

• If, instead, (i) α ≥ 110

; or (ii) α < 110

and(

1−10α6

)2 ≡ f2L < f < f =(

1−4α9

)2,

then the two-leader merger would trigger exit by outsiders if approved. Therefore, the

post-merger industry structure is characterized by a single monopolist endowed with

half of the monopoly capital. Consequently, the two leader firms will decide to merge

if:

π(2L) =

(1− 2α

2

)2

− 2f > 2πL(L,L, F, F ) = 2

[1

3

(1− 4α

3

)2

− f

], (2.26)

which holds for all α ∈ [0, α]. Thus, the two leader firms will always decide to submit

the merger to the AA.

The behaviour of a myopic AA, when deciding whether or not to authorise a merger

which would trigger the exit by the outsiders, can then be summarised as follows:

17

- If α ≥ 746

, then the two-leader merger will always be authorised. Outsider follower

firms would be pushed out of the market after the merger has taken place but efficiency

gains are so high that consumers would gain.

- If, instead, α < 746

, then the two-leader merger would not be authorised. Outsiders are

not able to survive and consumers would be worse off.

Figure 2.1 illustrates, for each possible region of parameters, the equilibrium outcome

obtained when there is a merger between two leaders, and thereby summarizes the results

obtained when the AA is characterized by a myopic behaviour. Inside the {} we identify

the type of market structure for each region, for instance, {2L,F,F} means that the market is

composed by a merged firm (merger of two leaders) and two independent outsider follower

firms.

Figure 2.1: Merger of two leaders: equilibrium outcomes with a myopic AA.

18

2.4.2 Merger of two leader firms under a forward looking AA

For a forward looking AA the game is the following:

• First Stage: the two leader firms decide whether or not to propose a merger (they will

do so, if the merger increases profits). If they decide to merge, they will have to ask to

the AA for authorisation.

• Second Stage: the AA decides whether to authorise the merger or not. If AA does not

authorise it, the game ends and firms stay in Stackelberg competition.

• Third Stage: if the AA decides to authorise the merger of two leaders at stage 2, it is

the turn of the next two outsider follower firms to decide if they want to merge or not.

If they do not propose a (defensive) merger, then the merger game stops and market

realisation occurs. If they do want to merge, they have to ask the AA for authorisation.

• Fourth Stage: the AA decides whether it wants to authorise the defensive merger

between outsiders of the first merger. If the AA rejects the merger, the merger game

stops and the product market stage occurs. If the AA accepts the new merger then we

have only two firms in the market.

In the present scenario, when making a decision on whether to allow or not the merger,

the AA takes into account that the merger may be followed by other mergers. Hence, after

the merger between two leaders, the market structure could be (2L,F,F), (2L) or (2L,2F).

As in the previous section, we proceed by solving the game by backward induction, and

thus we start by analysing Stage 4.

Analysis of Stage 4 At the fourth stage, the AA decides whether it wants to authorise or

not the defensive merger between outsiders (followers) of the first merger. Here, we have to

distinguish two situations:

• If: (i) α ≥ 110

; or (ii) α < 110

and(

1−10α6

)2 ≡ f2L < f < f ≡(

1−4α9

)2, the follow-

ers would exit the market if the defensive merger was rejected. The resultant market

19

structure would then be {2L}. Hence, the defensive merger is always approved if

P (2L, 2F ) < P (2L), that is, if:

P (2L, 2F ) = 1+6α4≤ P (2L) = 1+2α

2,

which is always true in the region of parameter values defined by Assumption 2.1.

• If, instead, α < 110

and f <(

1−10α6

)2 ≡ f2L, the followers would not exit the market if

the defensive merger was rejected. So:

– If the AA blocks the defensive merger, the resultant market structure is {2L, F,

F}, where the equilibrium price and profits are given by:

P (2L, F, F ) = 1+14α6

πL(2L, F, F ) = 13

(1+2α

2

)2 − 2f

πFi (2L, F, F ) =(

1−10α6

)2 − f

– If, instead the AA decides to approve the defensive merger, then the resulting

structure will be {2L, 2F}, that is, a duopoly with one leader and one follower,

owning half of the industry available capital each. Thus, the equilibrium price,

profits, CS, PS and SW in this market structure are given by:

P (2L, 2F ) =1 + 6α

4(2.27)

πL(2L, 2F ) =1

2

(1− 2α

2

)2

− 2f (2.28)

πF (2L, 2F ) =

(1− 2α

4

)2

− 2f (2.29)

CS(2L, 2F ) =9

2

(1− 2α

4

)2

(2.30)

PS(2L.2F ) = 3

(1− 2α

4

)2

− 4f (2.31)

SW (2L, 2F ) =15

2

(1− 2α

4

)2

− 4f (2.32)

20

Therefore, the AA will decide to block the merger between two followers if:

P (2L, 2F ) = 1+6α4≥ P (2L, F, F ) = 1+14α

6,

or equivalent if:

α ≤ 1

10. (2.33)

Therefore, the defensive merger will always be blocked if α < 110

and f2L < f < f ,

which is the case in the region under analysis.

Analysis of Stage 3 In this stage, we have to check whether the outsider follower firms will

decide to propose the merger or not.

• If: (i) α ≥ 110

; or (ii) α < 110

and(

1−10α6

)2 ≡ f2L < f < f ≡(

1−4α9

)2, the followers

would leave the market if the defensive merger was rejected. The resultant market

structure is then {2L}. Hence, the defensive merger is always proposed if:

πF (2L, 2F ) ≥ 0⇔(

1− 2α

4

)2

− 2f ≥ 0. (2.34)

which is always true in the region of parameter values obtained in Assumption 2.1.

• If, instead, α < 110

and f <(

1−10α6

)2 ≡ f2L, the defensive merger is not going to be

proposed because outsider follower firms anticipate that the defensive merger will be

rejected by the AA in the following stage.

Analysis of Stage 2 In the second stage, the AA has to decide whether or not to allow the

merger between the two leaders, if the merger has been submitted for approval.

• If: (i) α ≥ 110

; or (ii) α < 110

and(

1−10α6

)2 ≡ f2L < f < f ≡(

1−4α9

)2, the AA

anticipates that the merger between two followers is approved. Hence, the AA will

authorise the merger between two leaders if

P (2L, 2F ) = 1+6α4≤ P (L,L, F, F ) = 1+32α

9

α ≥ 5

74≈ 0.06757 (2.35)

21

• If, instead, α < 110

and f <(

1−10α6

)2 ≡ f2L, the followers will not leave the market,

the AA anticipates that the merger between two followers is blocked. Thus, the AA

will authorise the merger between two leaders if:

P (2L, F, F ) = 1+14α6≤ P (L,L, F, F ) = 1+32α

9

α ≥ 1

22(2.36)

Therefore, the merger will be authorised if α ≥ 122

.

Analysis of Stage 1 In Stage 1, leader firms decide whether or not to submit a merger.

Again we have to distinguish two scenarios, depending on whether or not the merger triggers

outsiders to exit the market.

• If: (i) α ≥ 110

; or (ii) α < 110

and(

1−10α6

)2 ≡ f2L < f < f ≡(

1−4α9

)2, leader

firms anticipate that the follower firms will merge. Therefore, the leaders will propose

a merger if:

πL(2L, 2F ) =1

2

(1− 2α

2

)2

− 2f ≥ 2πL(L,L, F, F ) = 2

[1

3

(1− 4α

3

)2

− f

],

(2.37)

which is always true in the region where α < α (Assumption 2.1).

• If, instead, α < 110

, the leader firms anticipate that followers will not merge. Hence,

the merger of two leaders is always proposed and accepted by the AA in the following

stage if:

πL(2L, F, F ) =1

3

(1 + 2α

2

)2

− 2f ≥ 2πL(L,L, F, F ) = 2

[1

3

(1− 4α

3

)2

− f

],

(2.38)

which, again, always holds under Assumption 2.1.

Figure 2.2 illustrates these results by presenting the full equilibrium outcome of the pro-

posed merger game wherein that the AA not only is an active player, but it also anticipates

the final equilibrium outcome a merger will lead to if approved.

22

Figure 2.2: Merger of two leaders: equilibrium outcomes with a forward looking AA.

Comparing the results obtained in Figures 2.1 and 2.2, we conclude that the AA decision

regarding the merger between two leaders only differs in the region of the efficiency parame-

ter (α) values where, after the merger, the (follower) outsiders would be constrained to exit in

the absence of a subsequent merger. In particular, while the myopic AA would only approve

the merger between leaders for very high efficiency gains levels (expecting that the merged

entity would be the monopolist of the market), the forward looking AA correctly anticipates

that monopoly will not be the final induced market structure resulting from the merger, if it is

approved. The first merger involving the two leaders will instead be followed by a defensive

merger formed by the two outsider follower firms, and the resulting market structure will be

composed of two symmetric firms (endowed with two units of capital each) with asymmetric

strategic power (one leader and one follower). This being the case, the forward looking AA

will only reject the merger between the two leaders if the induced efficiency gains are low

(i.e. if α < 574≈ 0.06757). Hence, there exist circumstances wherein while the myopic AA

would want to block a merger between two leaders, under an efficiency offence argument,

the forward looking AA authorises the very same merger proposal, since it correctly antic-

ipates that this first merger is going to be followed by a defensive merger, to the benefit of

consumers.

23

2.5 Extensions

In this section we study two possible extensions of the benchmark model. First, we investigate

the impact on our main results if we consider a total-welfare-maximizer AA. Further, we also

extend the analysis to other merger cases: merger between two followers and merger between

a leader and a follower.

2.5.1 Social Welfare standard

By considering an extended version of our endogenous merger formation game where the AA

adopts a total welfare standard, we show, in Figure 2.3, the decisions adopted by a myopic

AA.

Figure 2.3: Merger of two leaders: equilibrium results with a myopic SW-maximizer AA.

By contrasting the results in Figures 2.1 and 2.3, one concludes that the merger decisions

obtained for the myopic AA under the SW standard are similar to those obtained under the

CS standard. In particular, in both the “exit” and the “no exit” regions, the myopic AA

blocks the merger between two leaders, for low levels of the efficiency gains. However, by

adopting the SW standard, the myopic AA allows the merger of two leaders for a larger range

24

of the efficiency parameter. In the region where outsider follower firms are not constrained

to exit the market, the AA only rejects the merger if α < 18115

√31 − 199

230≈ 0.00626, and

before it rejected it if α < 122≈ 0.04545. When outsider follower firms are constrained

to exit the market, the AA rejects the merger of two leaders to monopoly if f2L < f < f

and f < f . Under the CS standard, the AA rejects the merger in a larger region, that is,122≤ α < 7

46≈ 0.15217, due to the fact that this type of AA does not take into account that

the merger also increases firms’ profits, which contributes to increase the social welfare.

Further, under the SW approach, the decisions of a forward-looking AA are illustrated in

Figure 2.4.10

Figure 2.4: Merger of two leaders: equilibrium results with a forward-looking SW-maximizer

AA.

So, contrary to what happened in the benchmark model (see Figure 2.2), the forward

looking AA, adopting a SW standard, always approves both mergers in the region where

outsider follower firms are constrained to exit the market. Under a CS standard and in the

region of 122< α < 5

74and f2L < f < f , the AA blocked the merger between the two leaders

because it decreased the CS. However, in the same region and under the SW standard, the AA10For more details on the calculations see Appendix A.

25

allows the merger because the induced increase in producers’ surplus more than compensates

for the decrease of CS and, therefore, the net effect is an increase in the SW.

2.5.2 Other merger possibilities

In this section, we analyze a modified version of the proposed merger formation game,

wherein the merger proposal involves two followers, where the resultant firm behaves as

follower or one leader and one follower, where the new firm behaves as leader. When a

leader merges with a follower in a market where firms compete in quantities, it is reason-

able to expect that the merged entity will behave as a leader for two reasons: (1) the merged

firm can still use the old commitment technology of the former leader firm and (2) it can

be checked that the merged firm would always rather be a leader than a follower. However,

when two followers merge it is not so straightforward to explain why two followers should

gain this commitment power by merging. Daughety (1990) studies mergers between two fol-

lowers that give rise to a leader using linear costs, however the author does not address why

the merger changes the strategic power of the insider firm neither considers the possibility

that the merger could generate efficiency gains. With convex costs, this case is analyzed by

Brito and Catalao–Lopes (2011). Hence, in this paper we assume that when two follower

firms merge, the resultant firm behaves as follower. In this section we also want to investigate

if the decisions of the two types of AAs change, when evaluating different mergers cases.11

First, we analyze the results obtained for the merger involving two follower firms, where

the resulting firm behaves as follower. Assuming that α < 16, in order to avoid that the

outsider leader firms exit the market and that f2F ≡ 12

(1−2α

3

)2. The decisions of both types

of AAs are summarised in Figures 2.5 and 2.6, respectively.

11More details on the calculations can be provided upon request to the authors.

26

Figure 2.5: Merger of two followers: equilibrium outcomes with a myopic AA.

Figure 2.6: Merger of two followers: equilibrium outcomes with a forward looking AA.

By comparing Figures 2.5 and 2.6, we conclude that, in the region where outsider leader

firms are not constrained to exit the market, both AAs approve the two-follower merger when

the efficiency gains are high (i.e. α > 110

). It turns out, however, that decisions are very

different in the “exit” region. In this region, while the myopic AA would only approve the

27

merger for high efficiency gains (expecting that the resulting firm with half of the industry

capital would become a monopolist), the forward looking AA correctly anticipates that a

wave of two mergers will take place instead (leading to a market structure where a unique

leader and a unique follower exist with half of the industry capital each) and, as a result,

always approves the first merger between the two followers, even if the efficiency gains are

low.

Suppose now, that there is a merger between one leader and one follower, where the

new firm behaves as a leader after the merger takes place. In this case, we assume that α < 18,

in order for the two outsider firms not be constrained to exit the market and that fLF ≡(1−8α

6

)2. For this merger case, the decisions from the two types of AAs are summarised in

Figures 2.7 and 2.8, respectively.

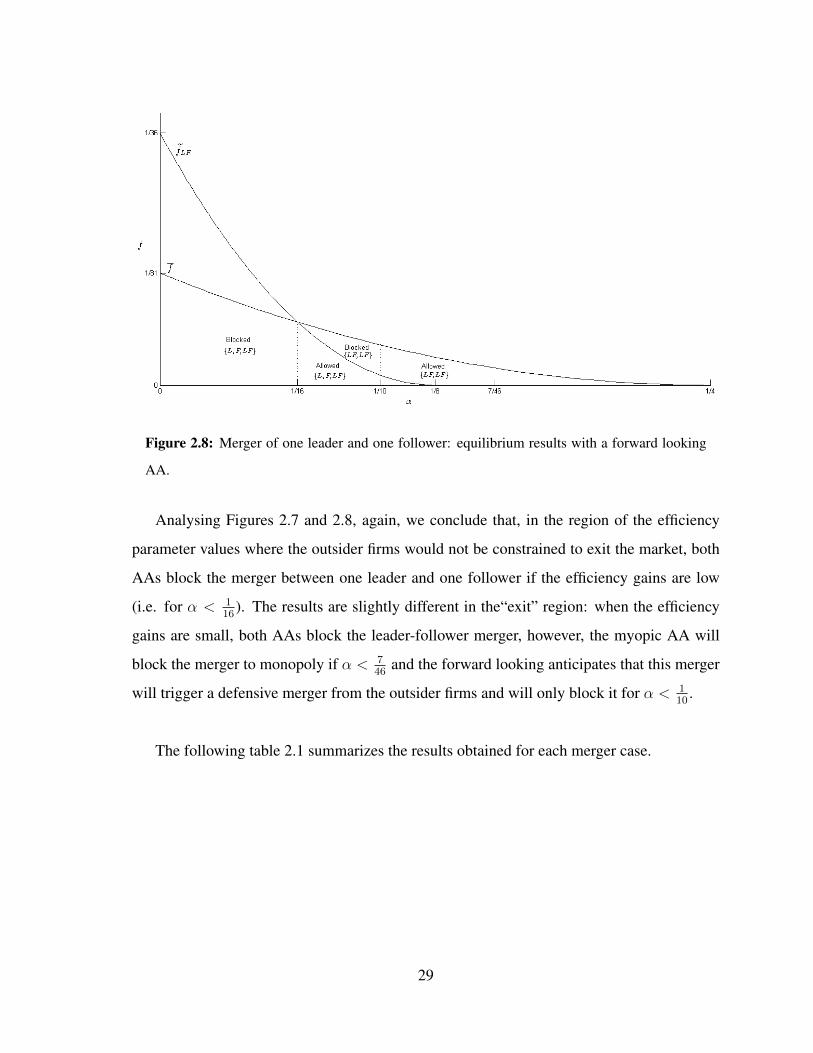

Figure 2.7: Merger of one leader and one follower: equilibrium results with a myopic AA.

28

Figure 2.8: Merger of one leader and one follower: equilibrium results with a forward looking

AA.

Analysing Figures 2.7 and 2.8, again, we conclude that, in the region of the efficiency

parameter values where the outsider firms would not be constrained to exit the market, both

AAs block the merger between one leader and one follower if the efficiency gains are low

(i.e. for α < 116

). The results are slightly different in the“exit” region: when the efficiency

gains are small, both AAs block the leader-follower merger, however, the myopic AA will

block the merger to monopoly if α < 746

and the forward looking anticipates that this merger

will trigger a defensive merger from the outsider firms and will only block it for α < 110

.

The following table 2.1 summarizes the results obtained for each merger case.

29

Table 2.1: Efficiency gains results, by region and by AA for each merger case

Myopic AA Forward Looking AA

No Exit Exit No Exit Exit

Cournot0 < α < 1

14: No Proposal 1

14< α < 3

22: Block {2} 0 < α < 1

14: {1,1,1,1} 1

14< α < 1

5: Allow {2,2}

114

< α < 16

: Allow {2,1,1} α > 322

: Allow {2} 114

< α < 16

: Allow {2,2} α > 15

: Allow {1}

2L (CS)0 < α < 1

22: Block {2L,F,F} 1

22< α < 7

46: Block {2L} 0 < α < 1

22: Block {2L,F,F} 1

22< α < 5

74: Block {2L,2F}

122

< α < 110

: Allow {2L,F,F} α > 746

: Allow {2L} 122

< α < 110

: Allow {2L, F,F} α > 574

: Allow {2L,2F}

2L (SW)

0 < α < 0.00626: Block {2L,F,F} α > 122∧ f > f : Block {2L} 0 < α < 0.00626: Block {2L,F,F}

α > 122

: Allow {2L,2F}0.02334 < α < 1

10: Allow {2L,F,F} f > f : Allow {2L} 0.00626 < α < 5

194: Allow {2L, F,F}

5194

< α < 110

: Allow {2L, 2F}

2F0 < α < 1

10: Block {L,L,2F} 0.12848 < α < 7

46: Block {2F} 0 < α < 5

74: Block {L,L,2F}

α > 0.12848: Allow {2L,2F}110

< α < 16

: Allow {L,L,2F} α > 746

: Allow {2F} 574

< α < 16

: Allow {L,L,2F}

LF0 < α < 1

16: Block {L,F,LF} 1

16< α < 7

46: Block {LF} 0 < α < 1

16: Block {L,F,LF} 1

16< α < 1

10: Block {LF,LF}

116

< α < 18

: Allow {L,F,LF} α > 746

: Allow {LF} 116

< α < 18

: Allow {L,F,LF} α > 110

: Allow {LF,LF}

2.6 Conclusion

In this paper we investigate the role of efficiency defence argument in a setting where mergers

involve firms with asymmetric strategic power and the merger formation game encompasses

the AA as an active player.

We study and compare the decisions of two different types of AA: first, we assume a

myopic AA, which accepts or rejects a given merger without considering that this merger

may be followed by other mergers; and, second, a forward looking AA, which anticipates the

final industry structure a merger will give rise to if approved. By so doing, we conclude that

the decisions of these two types of AAs turn out to be very different, for all studied two-firm

merger cases, when the proposed merger would induce outsiders to exit the market, in the ab-

sence of a subsequent merger. When this is the case, the myopic AA would not authorise any

merger proposal when the associated efficiency gains are sufficiently low, since it assumes

that the resulting merged entity would monopolize the industry. The forward-looking AA,

however, correctly anticipates that the first (proposed) merger will be followed by a merger

involving the outsider remaining firms and, therefore, makes a decision anticipating the fi-

nal industry structure the first merger will lead to if approved. By so doing, the forward

30

looking AA decides to approve a merger involving two leaders or a leader and a follower

if the induced efficiency gains are high enough, and decides to approve a merger between

two followers even if the resulting efficiency gains turn out to be low. Notice that when two

leader firms or one leader and one follower firm merge, the resulting merged entity will be a

leader in the post-merger industry structure, implying that it can explore more its enhanced

efficiency by making use of its first-mover advantage. Even if for the three merger cases

the final market structure is the same (2L, 2F) the decisions of a forward looking AA when

deciding whether or not to accept the merger of two leaders knowing that this is going to

be followed by a merger of two followers are different than when the first merger is of two

followers and followed by a defensive merger of two leaders. Interestingly, the two types of

AAs are shown to instead adopt similar behaviour when a merger is not supposed to trigger

exit by outsider firms if approved (and no further merger takes place). When this is the case,

and for all possible two-firm merger proposals, the AA will, regardless of its type, require

that induced efficiency gains are sufficiently high, so as to approve the proposed merger. Ob-

viously, the forward looking AA anticipates whether a subsequent merger will occur or not,

but the decisions of the two types of AAs regarding the first merger proposal end up being

qualitatively very similar.

Comparing these results with those obtained with symmetric strategic power (see Motta

and Vasconcelos (2005)), we conclude that, when firms compete a la Cournot, the two-firm

merger is not going to be proposed to the myopic AA, for low levels of the efficiency gains.

A different outcome is obtained when firms compete instead a la Stackelberg. In this case,

firms propose the merger for all levels of the efficiency gains. Further, differently from what

happens under Cournot competition, we find that, even without efficiency gains, a two-firm

merger is always profitable under Stackelberg. Additionally, the forward-looking AA has

similar behaviour under Cournot and in the two-follower Stackelberg merger case. However,

we note that in the two leaders or one leader and one follower merger cases the AA is more

severe and restrictive in a Stackelberg industry than in a Cournot industry due to the fact that,

in some specific circumstances, it does not allow the defensive merger or it blocks the merger

for a larger range of the efficiency parameter.

31

Further, we find that the myopic AA decisions, when evaluating a two-leader merger,

are very similar when it considers the SW or the CS standards. Regardless of the adopted

standard, the myopic AA always blocks the merger involving the two leaders for low levels

of the efficiency gains. Moreover, the decisions of the forward looking AAs are quite different

for each adopted standard, when outsider follower firms are confined to exit the market. In

this case, although the SW-maximizer AA always accepts the merger, the CS-maximizer AA

blocks it for low levels of the efficiency gains. Also, we conclude that the CS-maximizer AA

(myopic or forward-looking) is more restrictive when evaluating merger proposals than the

SW-maximizer AA.

Finally, not only the merger’s cost savings but also the fact that firms have different strate-

gic power may affect AA decision on merger cases. The framework and the assumptions we

have assumed are of a particular kind. Further research on the analysis of AA intervention

should consider what happens if there is an asymmetric information problem between the AA

and the merging firms concerning efficiencies due to mergers. Also, it would be interesting to

assume more than two leaders or two followers in the market. This would change the results

of merger profitability and the intervention of an AA that assesses mergers according to a

consumer surplus standard. We think that these are very interesting and useful subjects for

further research.

32

Appendix

A.1. Social Welfare Approach

A.1.1. Merger of two leaders under a Myopic AA

Analysis of Stage 2 First the AA has to decide whether or not to allow the merger, if the

merger has been submitted for approval.

• If α < 110

and f < f2L, then outsider follower firms are able to make positive profits

after the merger has taken place. If this is the case, then the AA decides to authorise

the submitted merger if the total social welfare increases:

SW (2L, F, F ) ≥ SW (L,L, F, F ),

which is equivalent to

α > 18115

√31− 199

230≈ 0.00626.

Since we are in region where α < 110

, hence the AA will require that the efficiency

gains are sufficiently high in order to authorise the merger between to leaders, that is18115

√31− 199

230≈ 0.00626 ≤ α < 1

10.

• If, instead, α ≥ 110

or α < 110

and f2L < f < f , hence the merger induces outsiders

to exit the industry and therefore the industry is characterized by a single monopo-

list. Now the AA will decide to reject the merger of two leaders if the social welfare

decreases, that is:

SW (2L) < SW (L,L, F, F )⇔ f < 4148α2−1588α+771296

≡ f .

Hence, the AA rejects the merger if f2L < f < f and f < f .

33

Analysis of Stage 1 The analysis of Stage 1 is the same as before.

• If α < 110

and f < f2L, then outsider follower firms are able to make positive profits

after the merger has taken place. Hence, insider leader firms will always submit the

merger however this will be blocked by the myopic AA for low levels of the efficiency

gains.

• If, instead, α ≥ 110

or α < 110

and f2L ≤ f < f, hence the merger gives rise to very

high synergies that leads to the two outsider leader firms to want to exit the market.

Also after the merger, the outsider fringe firms will have negative profits. Hence, the

merger induces outsiders to exit the industry and therefore the industry is characterized