Embed Size (px)

Citation preview

©2012 CliftonLarsonAllen LLP 1 1 1 1

©20

12 C

lifto

nLa

rso

nA

llen

LLP

Essential Financial Literacy Education: Resources to Keep Your Credit Union Compliant

Presented for the National Association of Federal Credit Unions

May 9th, 2012

©2012 CliftonLarsonAllen LLP 2

Speaker’s Biography – Greg Schwartz

• Greg Schwartz, CPA, CMA, is a principal in the Financial Institution Credit Union Group of CliftonLarsonAllen. Greg has been auditing credit unions for 25 years and his areas of expertise include audit and supervisory committee agreed-upon procedure engagements, GAAP and GAAS issues related to credit unions, supervisory committee issues, and review and evaluation of internal audit functions.

• Greg has worked with hundreds of credit unions all over the country and is considered an expert on credit union audit and accounting issues. He has made numerous presentations to credit union boards, supervisory committees and management on a variety of accounting and credit union issues.

• Greg graduated from Minnesota State University, Mankato, with a Bachelor of Science in Accounting and a minor in Computer Science. He is a CPA and a member of the American Institute of Certified Public Accountants (AICPA) and the AICPA credit union conference planning committee.

©2012 CliftonLarsonAllen LLP 3

Agenda

• Introductory Overview (10 minutes)

• Best Practice Ideas (70 minutes)

• Wrap-up and Questions (10 minutes)

©2012 CliftonLarsonAllen LLP 4

Introductory Overview

• NCUA Regulation 701.4, Issued February 2011

• Issued as a 5 page LCU

• Had 6 main parts

©2012 CliftonLarsonAllen LLP 5

Reg 701.4 – 6 Parts

• Part 1 – Delegating Responsibility

• Part 2 – Good Faith Effort

• Part 3 – Impartial

• Part 4 – Financial Literacy

• Part 5 – Rules and Sound Business Practices

• Part 6 – Information from employees

©2012 CliftonLarsonAllen LLP 6

Reg 701.4 – 6 Parts

• Part 1 – Delegating Responsibility

• Part 2 – Good Faith Effort

• Part 3 – Impartial

• Part 4 – Financial Literacy • Part 5 – Rules and Sound Business Practices

• Part 6 – Information from employees

©2012 CliftonLarsonAllen LLP 7

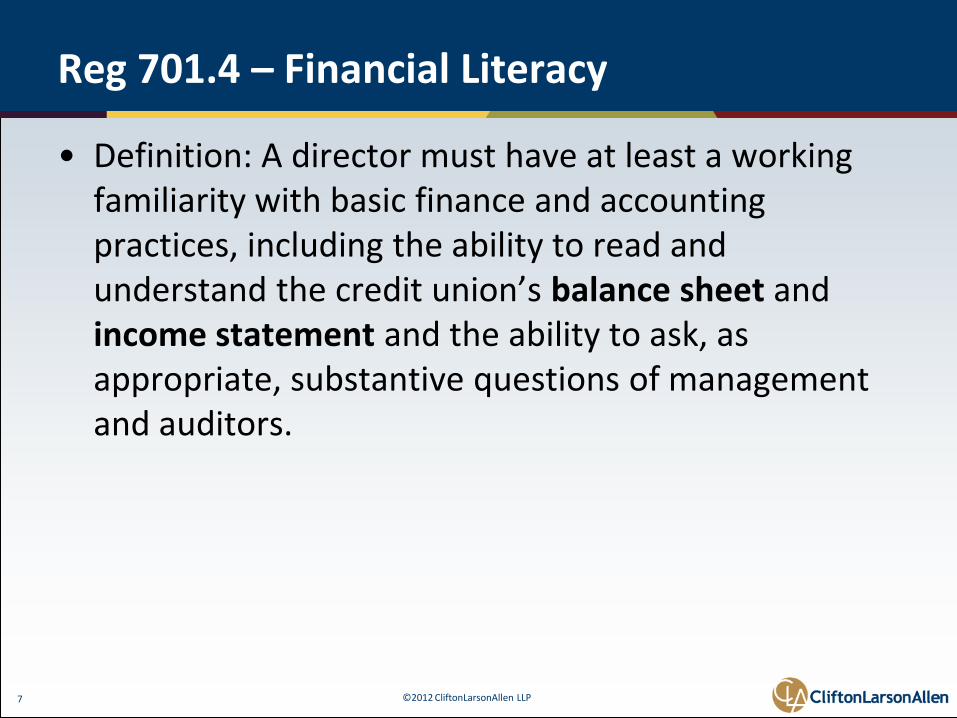

Reg 701.4 – Financial Literacy

• Definition: A director must have at least a working familiarity with basic finance and accounting practices, including the ability to read and understand the credit union’s balance sheet and income statement and the ability to ask, as appropriate, substantive questions of management and auditors.

©2012 CliftonLarsonAllen LLP 8

Reg 704.1 – Industry response

• Seminars

• Webinars

• Webcasts

• Workshops

• Boot Camps

• In-house training

• On-line training

©2012 CliftonLarsonAllen LLP 9

Reg 704.1 – Industry response

• Which was the Best?

©2012 CliftonLarsonAllen LLP 10

Reg 704.1 – Industry response

• They all were

“…it’s not so much where you are but what direction you are heading” …Oliver Wendell Homes

Significant focus on:

1. understand the credit union’s balance sheet and income statement and the ability

2. Understanding ratios

©2012 CliftonLarsonAllen LLP 11

What did we learn?

• This is a process not an event

• We can do the bare minimum or we can do it to extract the maximum value

• There are certain “Best Practice” concepts, as follows:

©2012 CliftonLarsonAllen LLP 12

“Best Practice” concept 1

• Understand Risk

We need financial literacy to manage risk

Or

Understanding risk improves financial literacy

©2012 CliftonLarsonAllen LLP 13

Risk Categories

• Risk is the potential that an event, expected or unanticipated, may have an adverse effect on the credit union's net worth and earnings. The categories of risk for credit union supervision purposes are:

◊ Credit

◊ Interest Rate

◊ Liquidity

◊ Transaction

◊ Compliance

◊ Strategic

◊ Reputation

• Any product or service may expose the credit union to multiple risks; these categories are not mutually exclusive.

©2012 CliftonLarsonAllen LLP 14

Credit Risk

• Credit risk is the current and prospective risk to earnings or capital arising from an obligor's failure to meet terms of any contract with the credit union or otherwise fail to perform as agreed.

• Credit risk exists in all activities where the credit union invests or loans funds with the expectation of repayment.

©2012 CliftonLarsonAllen LLP 15

Credit Risk Examples

• Private Label Securities

• 2nd Mortgages

• Corporate Credit Union Capital Accounts

• TDR’s

• All lending – the key is to manage it

©2012 CliftonLarsonAllen LLP 16

Interest Rate Risk

• Interest rate risk is the risk that changes in market rates will adversely affect a credit union's capital and earnings

©2012 CliftonLarsonAllen LLP 17

Interest Rate Risk - Example

• Current market rates – what happens when they go up?

©2012 CliftonLarsonAllen LLP 18

Liquidity Risk

• Liquidity risk is the current and prospective risk to earnings or capital arising from a credit union's inability to meet its obligations when they come due, without incurring material costs or unacceptable losses.

©2012 CliftonLarsonAllen LLP 19

Liquidity Risk - Examples

• Capital Corporate Credit Union

• NCUA Guarantee of Corporate Credit Union accounts

©2012 CliftonLarsonAllen LLP 20

Transaction Risk

• Transaction risk is the risk to earnings or capital arising from fraud or error that results in an inability to deliver products or services, maintain a competitive position, or manage information.

©2012 CliftonLarsonAllen LLP 21

Transaction Risk - Example

• Fraud

©2012 CliftonLarsonAllen LLP 22

Compliance Risk

• Compliance risk is the current and prospective risk to earnings or capital arising from violations of, or nonconformance with, laws, rules, regulations, prescribed practices, internal policies and procedures, or ethical standards.

©2012 CliftonLarsonAllen LLP 23

Compliance Risk - Examples

• Of the 7,600 credit unions, approximately 5,000 are operating under a DOR or LUA.

• Interest rate resets

• UBIT

©2012 CliftonLarsonAllen LLP 24

Strategic Risk

• Strategic risk is current and prospective risk to earnings or capital arising from adverse business decisions, improper implementation of decisions, or lack of responsiveness to industry changes.

©2012 CliftonLarsonAllen LLP 25

Strategic Risk – Examples

• ATM

• Overbuilt Brick and Mortar

• Internet

©2012 CliftonLarsonAllen LLP 26

Reputation Risk

• Reputation risk is current and prospective risk to earnings or capital arising from negative public opinion or perception.

©2012 CliftonLarsonAllen LLP 27

Reputation Risk - Examples

• Losing member data

• Bad press

©2012 CliftonLarsonAllen LLP 28

Risk Catagories

◊ Credit

◊ Interest Rate

◊ Liquidity

◊ Transaction

◊ Compliance

◊ Strategic

◊ Reputation

©2012 CliftonLarsonAllen LLP 29

What do we do with Risk

• Identify

• Measure

• Control

©2012 CliftonLarsonAllen LLP 30

Risk Identification

• Past due loans – an indication of loss (Credit)

• Member survey – an indication of service (Strategic)

• Teller cash counts – an indication of loss (Transaction)

©2012 CliftonLarsonAllen LLP 31

Risk Measurement

• Past due loans – start monitoring at 60 days (Credit)

• Member survey – investigate scores below 80 (Strategic)

• Teller cash counts – investigate over/short $5 (Transaction)

©2012 CliftonLarsonAllen LLP 32

Risk Control

• Past due loans – nonaccrual at days (Credit)

• Member survey – performance evaluation at 50 (Strategic)

• Teller cash counts – terminate if over $100 (Transaction)

©2012 CliftonLarsonAllen LLP 33

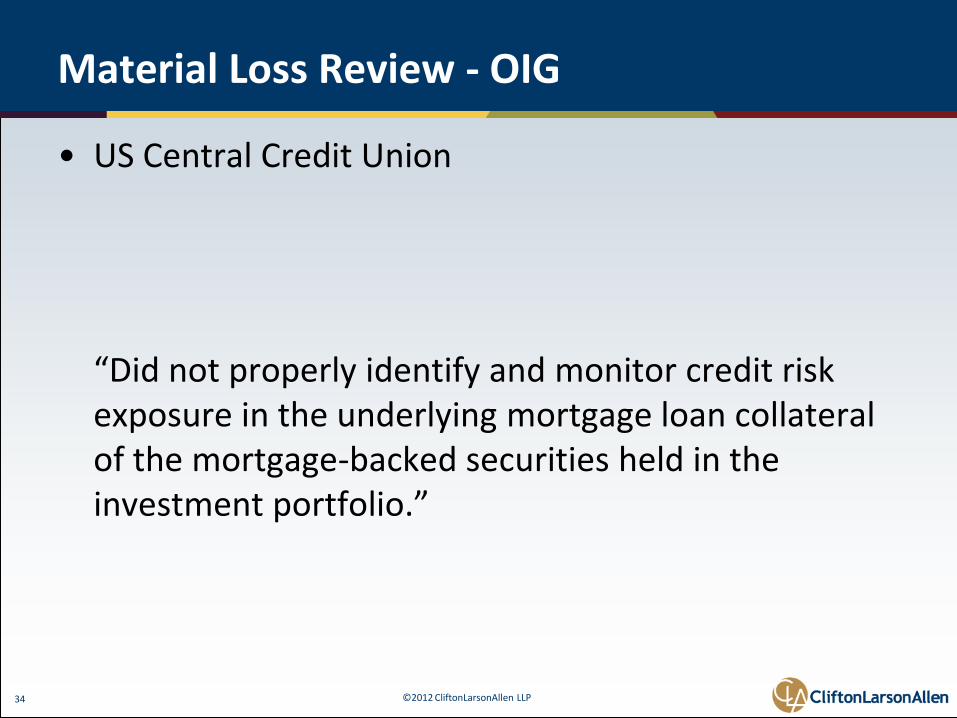

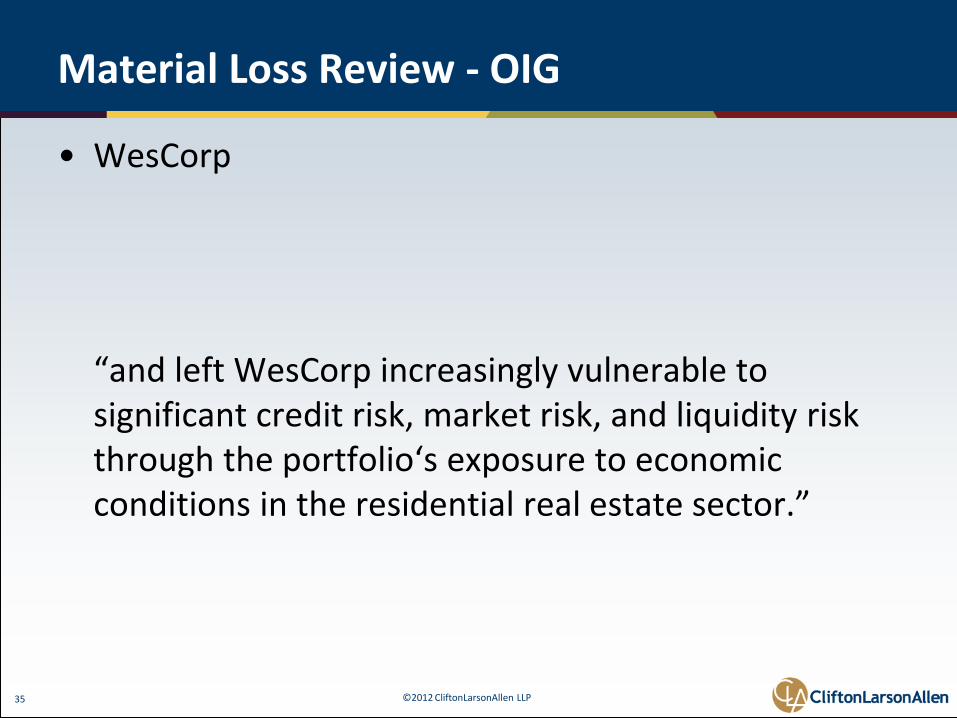

Material Loss Review - OIG

• Office of Inspector General does a Material Loss Review of significant losses to the insurance fund.

©2012 CliftonLarsonAllen LLP 34

Material Loss Review - OIG

• US Central Credit Union

“Did not properly identify and monitor credit risk exposure in the underlying mortgage loan collateral of the mortgage-backed securities held in the investment portfolio.”

©2012 CliftonLarsonAllen LLP 35

Material Loss Review - OIG

• WesCorp

“and left WesCorp increasingly vulnerable to significant credit risk, market risk, and liquidity risk through the portfolio‘s exposure to economic conditions in the residential real estate sector.”

©2012 CliftonLarsonAllen LLP 36

Material Loss Review - OIG

• Ensign Credit Union

“We determined Ensign failed because its Board of Directors and management did not implement appropriate risk management practices related to concentration and credit risks.”

©2012 CliftonLarsonAllen LLP 37

Material Loss Review - OIG

• Clearstar

“We concluded Clearstar failed because its Board and management did not implement proper risk management policies and procedures related to credit and concentration risk.”

©2012 CliftonLarsonAllen LLP 38

“Best Practice” concept 2

Clean-up the Financial Literacy “stuff”

• Board packets contain way too much detail information

• Many contain schedules or analysis that no one can remember where it came from

©2012 CliftonLarsonAllen LLP 39

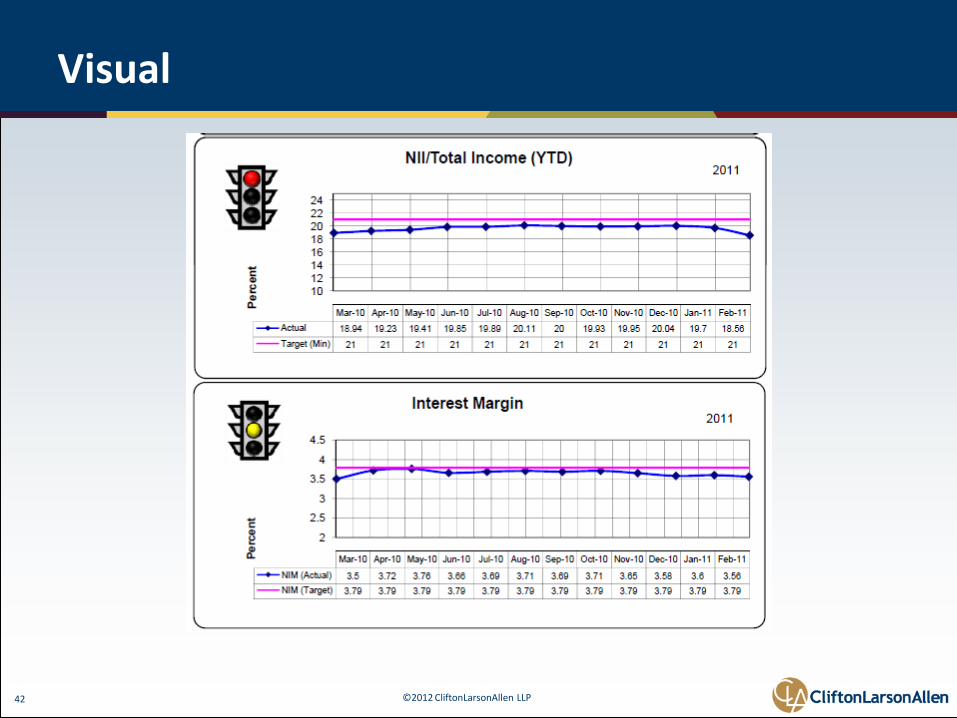

Board Packets

• Only relevant information

• Only summary information

• Make it visual

©2012 CliftonLarsonAllen LLP 40

Not Visual

• Jan 1.30 1.55

• Feb 1.38 1.30

• Mar 1.47 1.10

• Apr 1.56 1.20

• May 1.62 1.22

• June 1.71 1.28

• July 1.73 1.28

• Aug 1.70 1.37

• Sept 1.70 1.25

• Oct 1.69 1.19

• Nov 1.67 1.11

• Dec 1.58 1.04

©2012 CliftonLarsonAllen LLP 41

Visual

©2012 CliftonLarsonAllen LLP 42

Visual

©2012 CliftonLarsonAllen LLP 43

Non Visual

Listings Directory

• ALL | NYSE | NYSE ARCA | NYSE EURONEXT | NYSE ALTERNEXT Overview Name Region Industry To view an alphabetical list of listed companies, select a letter. A B C D E F G H I J K L M N O P Q R S T U V W X Y Z Other NYSE Technologies Global Market Data | as of 17:40 ET 01 May 2012 | Market data delayed

• Name Symbol Listing Last Trade Date/Time Volume Change % Change

• A. M. Castle & Co. CAS NYSE $ 12.80 01May12 16:02 ET 396,043 $ 0.59 4.40

• A. O. Smith Corporation AOS NYSE $ 47.65 01May12 17:23 ET 647,150 $ 0.05 0.10

• A.H. Belo Corporation AHC NYSE $ 4.27 01May12 16:36 ET 140,983 $ 0.14 3.17

• A.S.T. GROUPE ASP Euronext-PAR € 4.70 30Apr12 09:59 CET 1,107 € 0.00 0.00

• AAG Holding Company, Inc. GFW NYSE $ 25.46 01May12 15:56 ET 8,574 $ 0.01 0.03

• AAG Holding Company, Inc. GFZ NYSE $ 25.28 01May12 15:59 ET 10,019 $ 0.08 0.31

• AAR Corporation AIR NYSE $ 15.31 01May12 16:00 ET 458,017 $ 0.14 0.90

• Aaron's Inc. AAN NYSE $ 27.38 01May12 16:03 ET 476,922 $ 0.21 0.77

• ABB LTD. ABB NYSE $ 18.26 01May12 16:05 ET 3,004,206 $ 0.10 0.54

• Abbott Laboratories ABT NYSE $ 62.23 01May12 16:02 ET 6,149,396 $ 0.17 0.27

• ABC ARBITRAGE ABCA Euronext-PAR € 6.91 30Apr12 17:35 CET 26,196 € 0.01 0.14

• Abercrombie & Fitch ANF NYSE $ 53.02 01May12 16:00 ET 4,368,672 $ 2.85

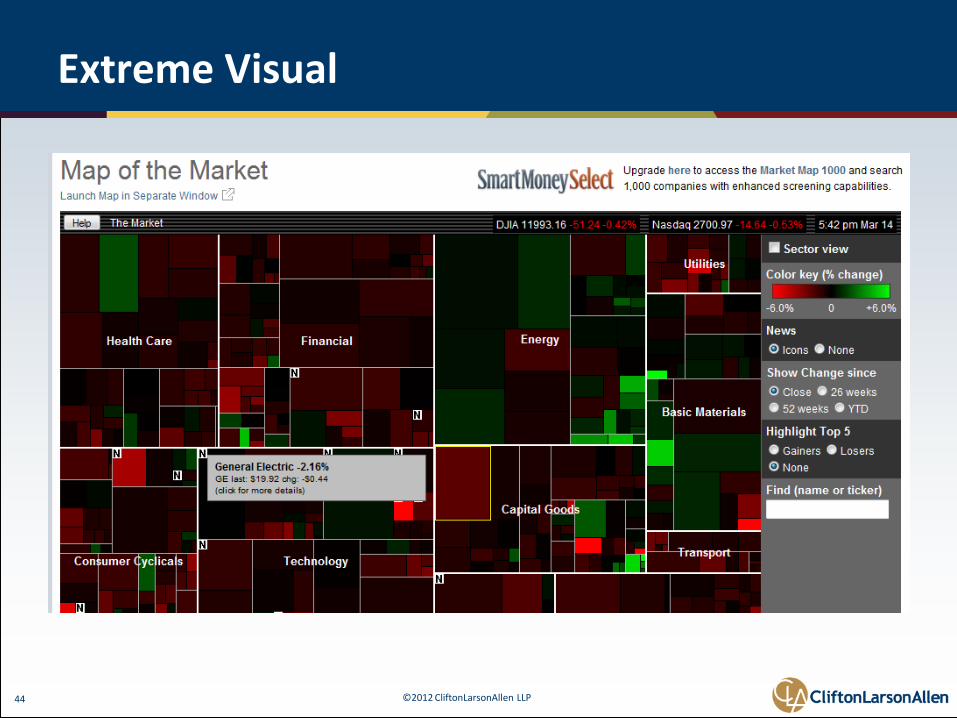

©2012 CliftonLarsonAllen LLP 44

Extreme Visual

©2012 CliftonLarsonAllen LLP 45

“Best Practice” concept 3

Significant focus on:

1. understand the credit union’s balance sheet and income statement and the ability

2. Understanding ratios

©2012 CliftonLarsonAllen LLP 46

“Best Practice” concept 3

• Train and practice key ratio literacy with your credit unions specific goals in mind:

©2012 CliftonLarsonAllen LLP 47

Capital Restoration

• Capital ratios

• Income ratios

• ALM tests

©2012 CliftonLarsonAllen LLP 48

Earnings Growth

• Spread analysis

• Operating expense ratios

©2012 CliftonLarsonAllen LLP 49

Growth

• Average balance growth

• New member growth

©2012 CliftonLarsonAllen LLP 50

“Best Practice” concept 4

• Understand the Control Structure

©2012 CliftonLarsonAllen LLP 51

Roles and Responsibilities: Management

• The Chief Executive Officer (top manager) of the organization has overall responsibility for designing and implementing effective internal control.

• More than any other individual, the chief executive sets the "tone at the top" that affects integrity and ethics and other factors of a positive control environment.

©2012 CliftonLarsonAllen LLP 52

Roles and Responsibilities: Board of Directors

• Management is accountable to the board of directors, which provide governance, guidance and oversight.

• Effective board members are objective, capable, and inquisitive.

• They have knowledge of the entity's activities and environment, and commit the time necessary to fulfill their board responsibilities.

©2012 CliftonLarsonAllen LLP 53

Internal Controls

• Preventative vs. Detective Controls

Approvals

Reconciliations

Passwords

Limits

Policy

©2012 CliftonLarsonAllen LLP 54

Internal Controls

• Segregation of Duties

No one individual handles a transaction from beginning to end

©2012 CliftonLarsonAllen LLP 55

“Best Practice” concept 5

• Extend the Financial Literacy movement to other reports

5300

Tax Returns (990 990T)

©2012 CliftonLarsonAllen LLP 56

NCUA Form 5300 and Tax returns

• Who at the credit union prepares?

• Who reviews ?

• Do we take any controversial positions?

©2012 CliftonLarsonAllen LLP 57

“Best Practice” concept 6

• Extend Financial Literacy to other financial processes

Budgeting

ALM

Complying with Credit Union Regulations

Complying with Consumer Regulations

©2012 CliftonLarsonAllen LLP 58

701.4 Part 5

• A director must direct the operations of the federal credit union in conformity with the Federal Credit Union Act, NCUA’s Rules and Regulations, other applicable laws, and sound business practices

©2012 CliftonLarsonAllen LLP 59

Budgeting – Old Goal

• 1% ROA

©2012 CliftonLarsonAllen LLP 60

Budgeting – Goals Today

• Much lower ROA – not necessarily our optimum goal

• Capital Restoration

• Smaller credit unions – growth to a critical mass

• Recover impaired assets

• Survival

Know the Goals

©2012 CliftonLarsonAllen LLP 61

Budgeting – Board Responsibility

• The primary responsibility of the board is to approve a budget that will achieve the organization’s goals while understanding the risks assumed in that budget

©2012 CliftonLarsonAllen LLP 62

Budgeting – Does the Budget…

• Plan increases in higher-risk loans?

• Plan increases in higher-risk investments?

• Plan expansion into new member groups?

• Plan expansion into new geographies?

• Plan streamlining the loan origination process?

©2012 CliftonLarsonAllen LLP 63

Budgeting – Does the Budget…

• Plan increases in higher risk loans?

• Plan increases in higher risk investments?

• Plan expansion into new member groups?

• Plan expansion into new geographies?

• Plan streamlining the loan origination process?

We are taking on additional Credit Risk

©2012 CliftonLarsonAllen LLP 64

Budgeting – Does the Budget…

• Anticipate an overly optimistic rate environment?

• Anticipate overly optimistic loan and deposit growth?

©2012 CliftonLarsonAllen LLP 65

Budgeting – Does the Budget…

• Anticipate an overly optimistic rate environment?

• Anticipate overly optimistic loan and deposit growth?

We are taking on additional Interest Rate Risk

©2012 CliftonLarsonAllen LLP 66

Budgeting – Does the Budget…

• Anticipate the ability to always obtain cheap borrowings?

• Anticipate the ability to always sell investments near par?

• Anticipate the ability to always originate high-rate loans?

©2012 CliftonLarsonAllen LLP 67

Budgeting – Does the Budget…

• Anticipate the ability to always obtain cheap borrowings?

• Anticipate the ability to always sell investments near par?

• Anticipate the ability to always originate high-rate loans?

We are taking on additional Liquidity Risk

©2012 CliftonLarsonAllen LLP 68

Budgeting – Does the Budget…

• Reduce internal audit resources?

• Reduce external audit resources?

• Reduce personnel resources to the point that control activities are reduced?

• Reduce insurance coverage?

• Not emphasize internal controls?

©2012 CliftonLarsonAllen LLP 69

Budgeting – Does the Budget…

• Reduce internal audit resources?

• Reduce external audit resources?

• Reduce personnel resources to the point that control activities are reduced?

• Reduce insurance coverage?

• Not emphasize internal controls?

We are taking on additional Transaction Risk

©2012 CliftonLarsonAllen LLP 70

Budgeting – Does the Budget…

• Not address the current business environment?

• Rely on old business models that do not work?

• Not consider new business models that may be the future?

• Not consider the infrastructure needed to achieve goals?

• Not consider the personnel resources needed to achieve goals?

©2012 CliftonLarsonAllen LLP 71

Budgeting – Does the Budget…

• Not address the current business environment?

• Rely on old business models that do not work?

• Not consider new business models that may be the future?

• Not consider the infrastructure needed to achieve goals?

• Not consider the personnel resources needed to achieve goals?

We are taking on additional Strategic Risk

©2012 CliftonLarsonAllen LLP 72

Budgeting – Does the Budget…

• Reduce controls over member data?

• Reduce resources devoted to safety and security?

• Reduce expenditures for new technology?

• Reduce expenditures over security training?

©2012 CliftonLarsonAllen LLP 73

Budgeting – Does the Budget…

• Reduce controls over member data?

• Reduce resources devoted to safety and security?

• Reduce expenditures for new technology?

• Reduce expenditures over security training?

We are taking on additional Reputation Risk

©2012 CliftonLarsonAllen LLP 74

ALM - Board Responsibilities

• Responsible for adopting a policy statement

• Responsible for establishing and approving policy limits

• Responsible for overseeing implementation of management responsibilities

• Responsible for periodic review of compliance with the credit union’s policy limits and management controls

©2012 CliftonLarsonAllen LLP 75

“Best Practice” concept 7

• Make Financial Literacy forward looking

IFRS

NCUA Rules and Regs

©2012 CliftonLarsonAllen LLP 76

“Best Practice” concept 8

• Extend Financial literacy training to all volunteers

©2012 CliftonLarsonAllen LLP 77

“Best Practice” concept 9

• Make Financial Literacy training a “process”