Embed Size (px)

Citation preview

7/25/2019 ET Article 1.Feb

http://slidepdf.com/reader/full/et-article-1feb 1/7

The Economic Times Wealth is available at an invitation price of `7/issue. To book your copy*, contact your newspaper vendor or call 011 - 39898090; Email: [email protected]; SMS ETWS to 58888

Learn and Keep PAGE 14

Family Finance PAGE 16

Q&A PAGE 18

PLUS

The week’s best stocks, mutua

loans and deposits.

ALSO INSIDE8FINANCIAL PLANNING

There is more to tax

planning than ELSSMost investors need to put

money into both ELSS and

provident fund for effective

tax planning.

26TECH

Apps that help you

make the switchMoving from Windows to

Mac or vice versa can be

tough. Cross platform apps

make the transition easier.

10STOCKS

Will aviation stocks

keep flying?Low fuel costs have

brought cheer to the air-

line sector, but investors

should be watchful.

NITIN SO

www.wealth.economictimes.com | Ahmedabad, Bengaluru, Chennai, Hyderabad, Kolkata, Mumbai, New Delhi, Pune | February 1-7, 2016 | 32 pages | `7

wealth

THE ECONOMICTIMES

THESE FINANCIAL STRATEGIES CAN HELP OPTIMISE

THE RETURNS FROM SAFE INVESTMENTS.

Prakriti Ojha from Mumbai

earns well, but prefers to invest in

low-risk bank deposits.

7/25/2019 ET Article 1.Feb

http://slidepdf.com/reader/full/et-article-1feb 2/7

NEHA PANDEY DEORAS

Many equity funds havechurned out compound-ed annual returns of over15% in the past 10 years.But Money Khanna ( see

picture) is more concerned about thenear-zero returns from the three large-cap funds she bought 18 months ago. “I

have not lost money but my investmenthas not moved much. A fixed deposit

would have at least earned some re-turns,” she says. The Mumbai-based ex-ecutive now invests mainly in the PPFand bank deposits.

There are many reasons why investorsprefer to be safe than sorry. Some ofthem just can’t stomach the volatilitythat comes with stock investments.

Khanna is one such investor. She itent with low returns from her invments as long as they are assureders may have had a bad experiencstocks, which is why they want to away. Take for instance HR profesPrakriti Ojha ( see picture). She is yearns reasonably well and doesn’ttoo many liabilities. But after she lmoney in a mis-sold Ulip, she has

These financial strategies can help optimise

the returns from safe investments.

MONEY TIPS FOR

LOW-RISKINVESTORS

Prakriti Ojha31 YEARS, MUMBAI

ANNUAL INCOME

`13 lakhINVESTS IN

PPF, life insurance

policies

REASON FOR RISK AVERSION

After losses from a mis-sold Ulip,

she has stayed away from

market-linked investments.

OUR RECOMMENDATION

Don’t shun equitiescompletely. Test yourrisk profile and start

putting small amountsin a balanced fund.

NITIN SO

02 CoverStoThe Economic Times Wealth, February 1-7, 2016

7/25/2019 ET Article 1.Feb

http://slidepdf.com/reader/full/et-article-1feb 3/7

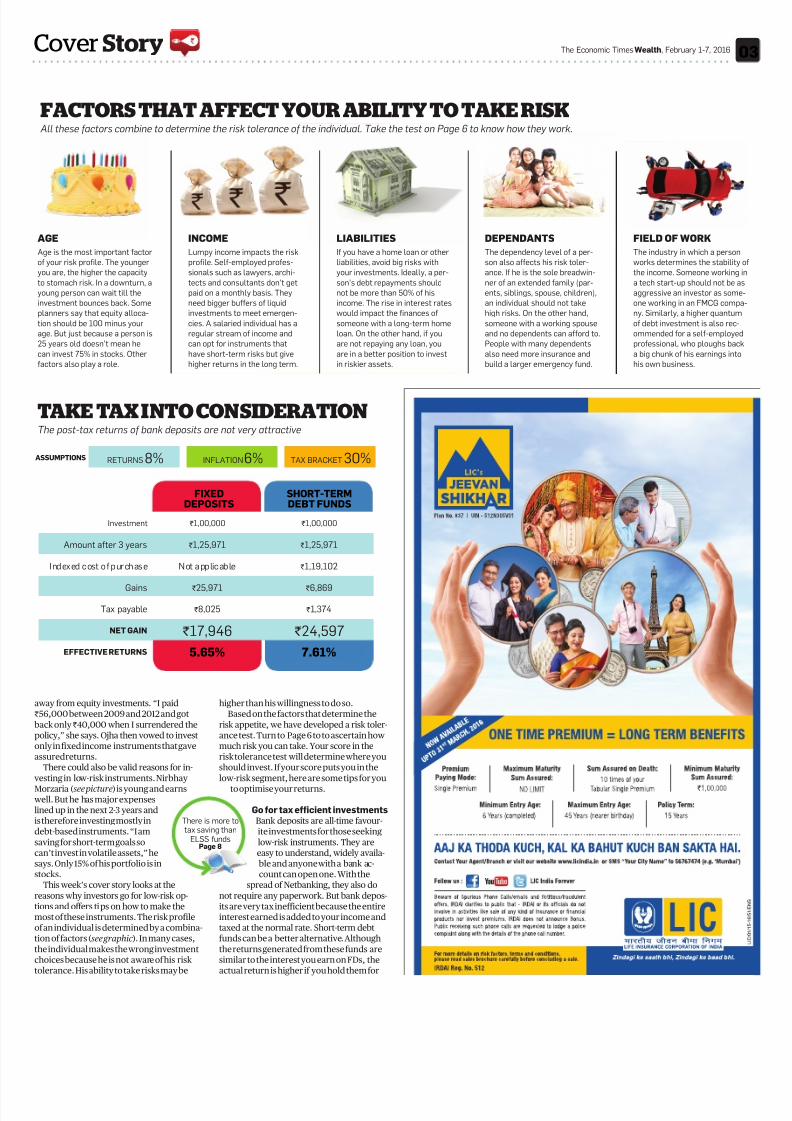

FACTORS THAT AFFECT YOUR ABILITY TO TAKE RISKAll these factors combine to determine the risk tolerance of the individual. Take the test on Page 6 to know how they work.

AGE

Age is the most important factor

of your risk profile. The younger

you are, the higher the capacity

to stomach risk. In a downturn, a

young person can wait till the

investment bounces back. Some

planners say that equity alloca-

tion should be 100 minus your

age. But just because a person is

25 years old doesn’t mean he

can invest 75% in stocks. Other

factors also play a role.

INCOME

Lumpy income impacts the risk

profile. Self-employed profes-

sionals such as lawyers, archi-

tects and consultants don’t get

paid on a monthly basis. They

need bigger buffers of liquid

investments to meet emergen-

cies. A salaried individual has a

regular stream of income and

can opt for instruments that

have short-term risks but give

higher returns in the long term.

LIABILITIES

If you have a home loan or other

liabilities, avoid big risks with

your investments. Ideally, a per-

son’s debt repayments should

not be more than 50% of his

income. The rise in interest rates

would impact the finances of

someone with a long-term home

loan. On the other hand, if you

are not repaying any loan, you

are in a better position to invest

in riskier assets.

DEPENDANTS

The dependency level of a per-

son also affects his risk toler-

ance. If he is the sole breadwin-

ner of an extended family (par-

ents, siblings, spouse, children),

an individual should not take

high risks. On the other hand,

someone with a working spouse

and no dependents can afford to.

People with many dependents

also need more insurance and

build a larger emergency fund.

FIELD OF WORK

The industry in which a perso

works determines the stabili

the income. Someone workin

a tech start-up should not be

aggressive an investor as som

one working in an FMCG com

ny. Similarly, a higher quantu

of debt investment is also re

ommended for a self-employ

professional, who ploughs ba

a big chunk of his earnings in

his own business.

TAKE TAX INTO CONSIDERATIONThe post-tax returns of bank deposits are not very attractive

ASSUMPTIONS RETURNS 8% INFLATION6% TAX BRACKET 30%

Investment `1,00,000 `1,00,000

Amount after 3 years `1,25,971 `1,25,971

Indexed cost of purchase Not applicable `1,19,102

Gains `25,971 `6,869

Tax payable `8,025 `1,374

NET GAIN `17,946 `24,597

EFFECTIVE RETURNS 5.65% 7.61%

FIXEDDEPOSITS

SHORT-TERMDEBT FUNDS

away from equity investments. “I paid`56,000 between 2009 and 2012 and gotback only`40,000 when I surrendered thepolicy,” she says. Ojha then vowed to investonly in fixed income instruments that gaveassured returns.

There could also be valid reasons for in-vesting in low-risk instruments. Nirbhay

Morzaria ( see picture) is young and earnswell. But he has major expenseslined up in the next 2-3 years andis therefore investing mostly indebt-based instruments. “I amsaving for short-term goals socan’t invest in volatile assets,” hesays. Only 15% of his portfolio is instocks.

This week’s cover story looks at thereasons why investors go for low-risk op-tions and offers tips on how to make themost of these instruments. The risk profileof an individual is determined by a combina-tion of factors ( see graphic ). In many cases,the individual makes the wrong investmentchoices because he is not aware of his risktolerance. His ability to take risks may be

higher than his willingness to do so.Based on the factors that determine the

risk appetite, we have developed a risk toler-ance test. Turn to Page 6 to to ascertain howmuch risk you can take. Your score in therisk tolerance test will determine where youshould invest. If your score puts you in thelow-risk segment, here are some tips for you

to optimise your returns.

Go for tax efficient investmentsBank deposits are all-time favour-ite investments for those seekinglow-risk instruments. They areeasy to understand, widely availa- ble and anyone with a bank ac-count can open one. With the

spread of Netbanking, they also donot require any paperwork. But bank depos-its are very tax inefficient because the entireinterest earned is added to your income andtaxed at the normal rate. Short-term debtfunds can be a better alternative. Althoughthe returns generated from these funds aresimilar to the interest you earn on FDs, theactual return is higher if you hold them for

There is more totax saving than

ELSS fundsPage 8

The Economic Times Wealth, February 1-7, 2016CoverStory

7/25/2019 ET Article 1.Feb

http://slidepdf.com/reader/full/et-article-1feb 4/7

ShraddhaDixit29 YEARS, THANE

ANNUAL INCOME

`5 lakhINVESTS IN

FDs, life insurance

policies and Ulips

REASON FOR RISK AVERSION

Barely 5-6% in equities. Prefers

FDs because she lacks knowledge

of stock markets and mutual funds.

OUR RECOMMENDATION

Use the existing Ulip toenhance exposure to

equities. Instead of tax-inefficient FDs, opt for

debt mutual funds.

Nirbhay Morzaria28 YEARS, MUMBAI

ANNUAL INCOME

`9 lakhINVESTS IN

PPF, bank FDs and

equity funds.

REASON FOR RISK AVERSION

Has big-ticket expenses coming up

in next 2-3 years. So, only 15% of

total portfolio allocated to equities.

OUR RECOMMENDATION

Avoid tax-inefficient FDs and put money in

debt funds if yourinvestment horizon is

more than 3 years.

HOW DEBT OPTIONS STACK UPThe VPF may be the best way to invest in debt in 2016. But the high rate

announced for 2015-16 may not sustain in the coming years.

10% SLAB 20% SLAB 30% SLAB

EPF and VPF 8.95 8.95 8.95 8.95

PPF 8.75 8.75 8.75 8.75

Tax-free bonds 7.50 7.50 7.50 7.50

Kisan Vikas Patra 8.70 7.80 6.91 6.01

NSCs 8.50 7.62 6.75 5.87

Bank deposits 8.00 7.18 6.35 5.53

INTEREST

RATE (%)

POST-TAX YIELD IN

DIFFERENT TAX SLABS (%)

*Ranked on basis of post-tax returns in 30% tax bracket

tion (EPFO) has recommended an interestrate of 8.95% for the current financial year,

which means it will earn equivalent to 12.95%from a bank deposit or bond for subscribersin the highest 30% tax bracket. But keep inmind that the higher rate is for the currentyear could change in the coming years. Tax-free bonds, on the other hand, offer assuredreturns for the entire term.

Avoid locking up for long-termDon’t put all your money into long-term op-tions. You never know when you may needit. Some banks levy a penalty on premature

withdrawals from a fixed deposit. It’s best to

split the investments and create a ladddeposits. If you have`4 lakh to invest, the amount in four deposits of `1 lakh for one, two, three and four years. Wh1-year deposit matures, reinvest the mproceeds in the 4-year FD. This will enquidity because you have one deposit ing every year. In case of regular investments, open multiple recurring deposthat even if you have to close one due treason, the others can continue.

Debt funds offer higher liquidity thaer long-term options such as PPF and VYou can withdraw from the debt fund oinvest on any day without any restricti

more than 3 years.There is a widely held misconception

that up to `10,000 earned from bank de-posits in a year is tax-free. This is not cor-rect. The exemption under Section80TTA is only for the interest earned onthe savings bank balance, not on fixed de-posits and recurring deposits. Also, eventhough five-year FDs are labelled tax-sav-

ing deposits, the interest they earn is fullytaxable.For investors in the 30% tax bracket

(taxable income of over `10 lakh a year),the returns from a 3-year FD can be as lowas 5.6%. On the other hand, the gains froma debt fund are taxed at 20% after adjust-ing for inflation. The net gain is close to200 basis points higher ( see table). “Plus,there are ways the capital gains can be setoff if you invest in a fund. No such optionsare available for interest income fromFDs,” says Bhuvana Shreeram, Head, Fi-nancial Freedom Golden Practices, aMumbai-based wealth management fund.

For salaried people, the VoluntaryProvident Fund may be a good option.The Employees Provident Fund Organisa-

NITIN SON

04 CoverStoThe Economic Times Wealth, February 1-7, 2016

7/25/2019 ET Article 1.Feb

http://slidepdf.com/reader/full/et-article-1feb 5/7

Money Khanna31 YEARS, MUMBAI

ANNUAL INCOME

`4 lakhINVESTS IN

PPF, FDs andmutual funds

REASON FOR RISK AVERSION

Equities account for only 7-8% of

her portfolio. She prefers options

that offer assured returns.

OUR RECOMMENDATION

Take risk tolerancetest. Start investing in

low-risk MIP fundsthat give better returns

than PPF and FDs.

Online access has made this even more con- venient.

Insurance plans force you to save

For some investors, the lack of flexibility can be a boon in disguise. Traditional life insur-ance plans give very low returns but they also

force investors to invest for the long-term. Thepremium notice that is sent to the policyholderevery year instils a discipline that mutualfunds can’t. “Mutual fund SIPs are usually for1-2 years. In some cases they may extend tothree years. A life insurance plan ensures thatthe policyholder keeps investing for 15-20years. He may get 100-150 basis point lower re-turn but at least he doesn’t stop investing,”

says R.M. Vishakha, Managing Director CEO of IndiaFirst Life Insurance Compa

The other good point is that the policycannot dip into the corpus before matur“We have seen clients start investing forchild’s education only to withdraw the m2-3 years later to go on a holiday. We reco

mend insurance plans for such investorcomplain that we are trying to sel l them pensive product but that is not the case.

just selling them discipline,” says SanjivManaging Director of Bajaj Capital.

Former havens no longer safe

There was a time when gold and real est were considered the safest investments

NITIN SONAWANE

The Economic Times Wealth, February 1-7, 2016CoverStory

7/25/2019 ET Article 1.Feb

http://slidepdf.com/reader/full/et-article-1feb 6/7

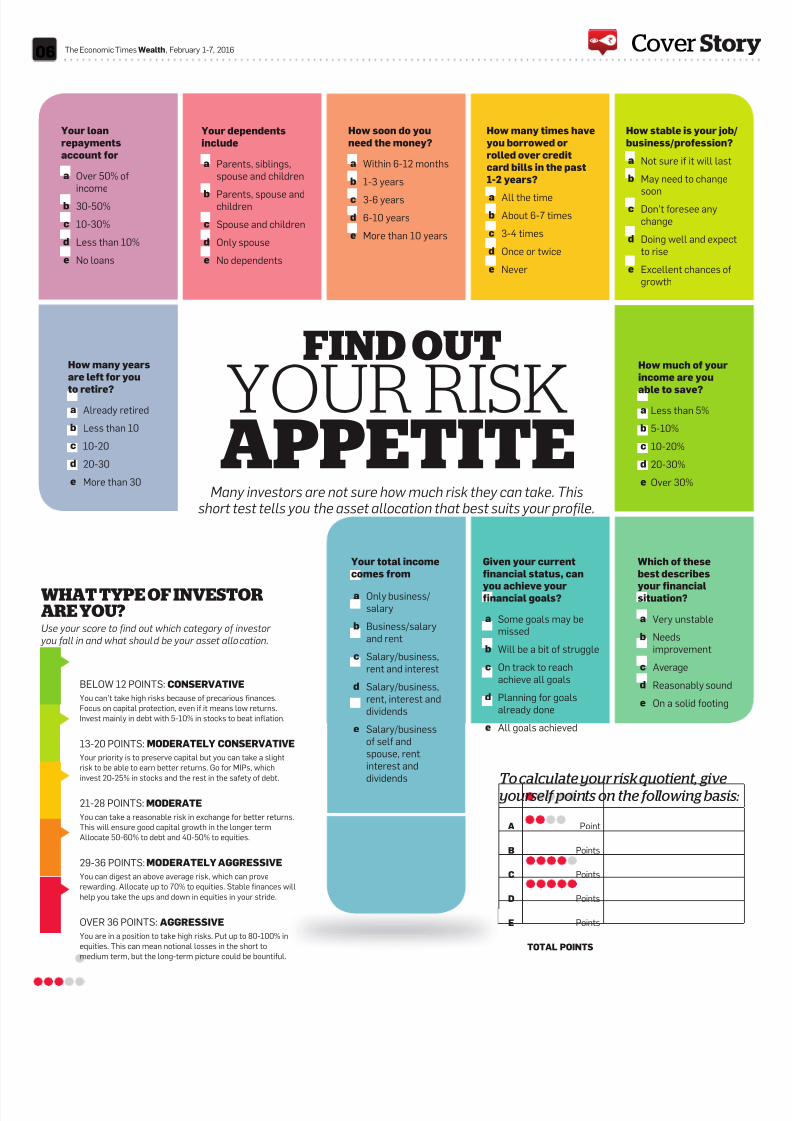

To calculate your risk quotient, give

yourself points on the following basis

WHAT TYPE OF INVESTORARE YOU?Use your score to find out which category of investor

you fall in and what should be your asset allocation.

A Point

B Points

C Points

D Points

E Points

TOTAL POINTS

FIND OUT

Many investors are not sure how much risk they can take. Thisshort test tells you the asset allocation that best suits your profile.

How many years

are left for you

to retire?

a Already retired

b Less than 10

c 10-20

d 20-30

e More than 30

Your loan

repayments

account for

a Over 50% of

income

b 30-50%

c 10-30%

d Less than 10%

e No loans

Your dependents

include

a Parents, siblings,

spouse and children

b Parents, spouse andchildren

c Spouse and children

d Only spouse

e No dependents

Your total income

comes from

a Only business/

salary

b Business/salary

and rent

c Salary/business,

rent and interest

d Salary/business,

rent, interest and

dividends

e Salary/business

of self and

spouse, rent,

interest and

dividends

How soon do you

need the money?

a Within 6-12 months

b 1-3 years

c 3-6 years

d 6-10 years

e More than 10 years

How many times have

you borrowed or

rolled over credit

card bills in the past

1-2 years?

a All the time

b About 6-7 times

c 3-4 times

d Once or twice

e Never

How stable is your job

business/profession?

a Not sure if it will last

b May need to change

soonc Don’t foresee any

change

d Doing well and expec

to rise

e Excellent chances of

growth

How much of your

income are you

able to save?

a Less than 5%

b 5-10%

c 10-20%

d 20-30%

e Over 30%

Which of these

best describes

your financialsituation?

a Very unstable

b Needs

improvement

c Average

d Reasonably sound

e On a solid footing

Given your current

financial status, can

you achieve yourfinancial goals?

a Some goals may be

missed

b Will be a bit of struggle

c On track to reach

achieve all goals

d Planning for goals

already done

e All goals achieved

BELOW 12 POINTS: CONSERVATIVE

You can’t take high risks because of precarious finances.

Focus on capital protection, even if it means low returns.

Invest mainly in debt with 5-10% in stocks to beat inflation.

13-20 POINTS: MODERATELY CONSERVATIVE

Your priority is to preserve capital but you can take a slight

risk to be able to earn better returns. Go for MIPs, which

invest 20-25% in stocks and the rest in the safety of debt.

21-28 POINTS: MODERATE

You can take a reasonable risk in exchange for better returns.

This will ensure good capital growth in the longer term.

Allocate 50-60% to debt and 40-50% to equities.

29-36 POINTS: MODERATELY AGGRESSIVE

You can digest an above average risk, which can prove

rewarding. Allocate up to 70% to equities. Stable finances will

help you take the ups and down in equities in your stride.

OVER 36 POINTS: AGGRESSIVE

You are in a position to take high risks. Put up to 80-100% in

equities. This can mean notional losses in the short to

medium term, but the long-term picture could be bountiful.

APPETITEYOUR RISK

06 CoverStoThe Economic Times Wealth, February 1-7, 2016

7/25/2019 ET Article 1.Feb

http://slidepdf.com/reader/full/et-article-1feb 7/7

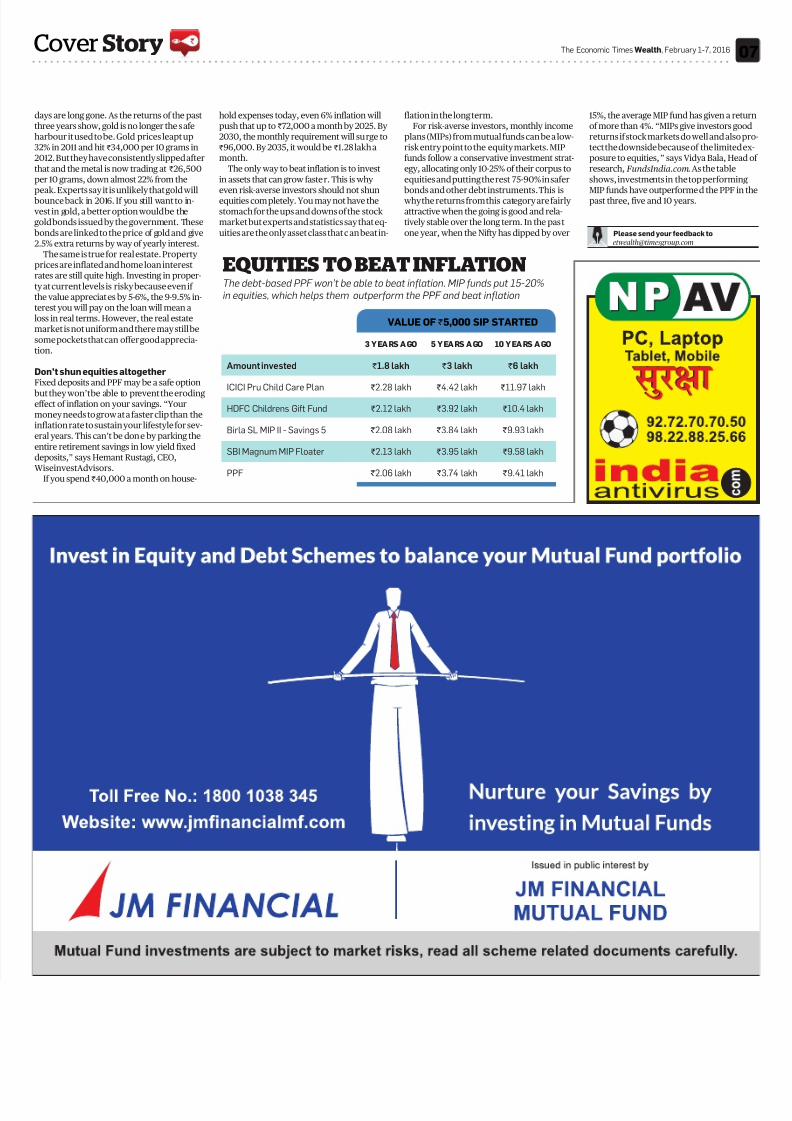

EQUITIES TO BEAT INFLATIONThe debt-based PPF won’t be able to beat inflation. MIP funds put 15-20%

in equities, which helps them outperform the PPF and beat inflation

3 YEARS AGO 5 YEARS AGO 10 YEARS AGO

Amount invested `1.8 lakh `3 lakh `6 lakh

ICICI Pru Child Care Plan `2.28 lakh `4.42 lakh `11.97 lakh

HDFC Childrens Gift Fund `2.12 lakh `3.92 lakh `10.4 lakh

Birla SL MIP II - Savings 5 `2.08 lakh `3.84 lakh `9.93 lakh

SBI Magnum MIP Floater `2.13 lakh `3.95 lakh `9.58 lakh

PPF `2.06 lakh `3.74 lakh `9.41 lakh

VALUE OF `5,000 SIP STARTED

hold expenses today, even 6% inflation willpush that up to `72,000 a month by 2025. By2030, the monthly requirement will surge to`96,000. By 2035, it would be `1.28 lakh amonth.

The only way to beat inflation is to investin assets that can grow faster. This is whyeven risk-averse investors should not shunequities completely. You may not have thestomach for the ups and downs of the stockmarket but experts and statistics say that eq-uities are the only asset class that can beat in-

flation in the long term.For risk-averse investors, monthly income

plans (MIPs) from mutual funds can be a low-risk entry point to the equity markets. MIPfunds follow a conservative investment strat-egy, allocating only 10-25% of their corpus toequities and putting the rest 75-90% in safer

bonds and other debt instruments. This is why the returns from this category are fairlyattractive when the going is good and rela-tively stable over the long term. In the pastone year, when the Nifty has dipped by over

days are long gone. As the returns of the pastthree years show, gold is no longer the safeharbour it used to be. Gold prices leapt up32% in 2011 and hit `34,000 per 10 grams in2012. But they have consistently slipped afterthat and the metal is now trading at `26,500per 10 grams, down almost 22% from thepeak. Experts say it is unlikely that gold willbounce back in 2016. If you still want to in-vest in gold, a better option would be thegold bonds issued by the government. Thesebonds are linked to the price of gold and give2.5% extra returns by way of yearly interest.

The same is true for real estate. Propertyprices are inflated and home loan interestrates are still quite high. Investing in proper-ty at current levels is risky because even ifthe value appreciates by 5-6%, the 9-9.5% in-terest you will pay on the loan will mean aloss in real terms. However, the real estatemarket is not uniform and there may still besome pockets that can offer good apprecia-tion.

Don’t shun equities altogetherFixed deposits and PPF may be a safe option

but they won’t be able to prevent the erodingeffect of inflation on your savings. “Yourmoney needs to grow at a faster clip than theinflation rate to sustain your lifestyle for sev-eral years. This can’t be done by parking theentire retirement savings in low yield fixeddeposits,” says Hemant Rustagi, CEO,Wiseinvest Advisors.

If you spend `40,000 a month on house-

15%, the average MIP fund has given a of more than 4%. “MIPs give investors returns if stock markets do well and altect the downside because of the limitposure to equities,” says Vidya Bala, Hresearch, FundsIndia.com. As the tableshows, investments in the top performMIP funds have outperformed the PPFpast three, five and 10 years.

Please send your feedback to

The Economic Times Wealth, February 1-7, 2016CoverStory