Embed Size (px)

Citation preview

Ethics and Professionalism“The Integrity of the Upright Shall Guide Them”

(Proverbs 11:3)

Learning Objectives

Reflect on the meaning and importance of ethics in personal and professional life

Define a profession; differentiate from trade Understand why professionals need ethics Understand basic ethical standards in the

Code of Professional Conduct for CPAs Learn and practice a process of ethical

decision making

Ethics: What is it?

“A discipline of good and evil and moral duty.” (Funk and Wagnalls)

Actions and how they affect people

Where did you get your ethics?

Parents Religion School Peers

Concepts at the heart of ethics

Fairness Trust Respect Compassion Cooperation“He hath showed thee, o man, what is good, and what doth the Lord

require of thee, than to do justly, and to love mercy, and to walk humbly with thy God.” (Micah 6:8)

The Sinking of the Titanic

What were the facts? Who were the stakeholders? What were the issues and values? What were the alternatives? What actions were taken? What were the consequences?

When God Comes to Work(managing religious diversity)

Facts? Stakeholders? Issues and values? Alternatives? Actions? Check?

The Heinz Dilemma Facts? Stakeholders? Issues and values? Alternatives? Actions? Check?

Ethical problem you faced today?

Facts? Stakeholders (persons involved)? Issues and values? Alternatives? Action? Did you check yourself?

What is a profession?

A group of people pursuing a learned art with a common calling

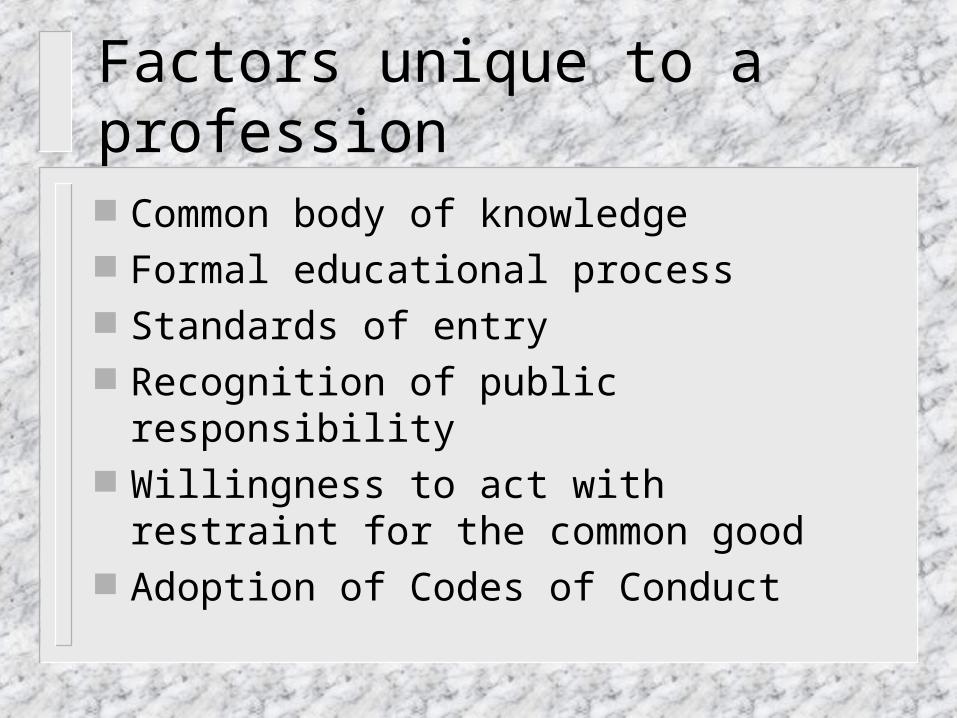

Factors unique to a profession

Common body of knowledge Formal educational process Standards of entry Recognition of public responsibility Willingness to act with restraint for the

common good Adoption of Codes of Conduct

Codes of Conduct for Accountants AICPA IMA IIA State Boards of Accountancy SEC

Code of Professional Conduct AICPA Professional Standards, Vol. 2 (ET) Composition

– Principles– Rules

Interpretations, Rulings

Applicability Compliance

Principles Preamble

– Requires all CPAs to assume the obligation of self-discipline above and beyond requirements of law.

– Calls for unswerving commitment to honorable behavior, regardless of personal advantage.

Article I -- Responsibilities Members should exercise sensitive

professional and moral judgments in all activities– Primary responsibility is to the “public”– Responsibility to cooperate with each other to

improve the art of accounting, maintain public confidence, and carry out self-governance.

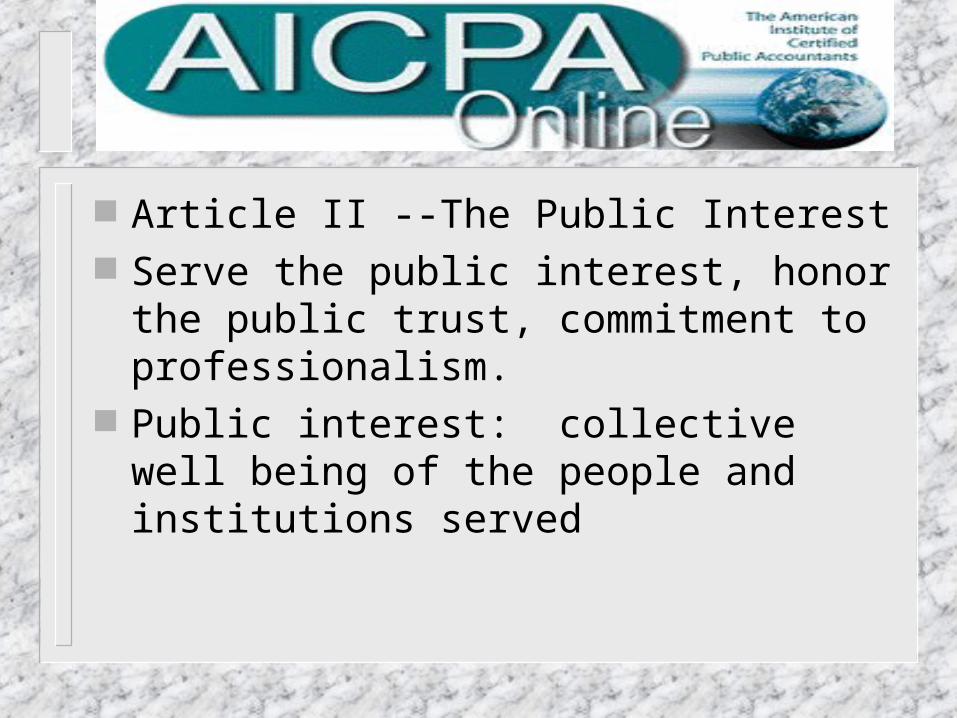

Article II --The Public Interest Serve the public interest, honor the public

trust, commitment to professionalism. Public interest: collective well being of the

people and institutions served

Article III --Members should perform with the highest sense of integrity

The test for all decisions: “What would a person of integrity do?”

Characteristics: – Honesty– Candor– Protective of confidentiality

Article IV -- A member should maintain objectivity and be free from conflicts of interest.

A state of mind: the distinguishing feature of our profession

Impartiality, intellectual honesty, freedom from conflicts of interest.

Requires independence in attest situations.

Article V -- Due Care. A member should observe the profession’s technical and ethical standards, strive continually to improve competence and quality of service, and be duly diligent in performing services.

Continual quest for excellence, commitment to life-long learning and improvement.

Requires assessment of competence, due diligence, planning and supervision..

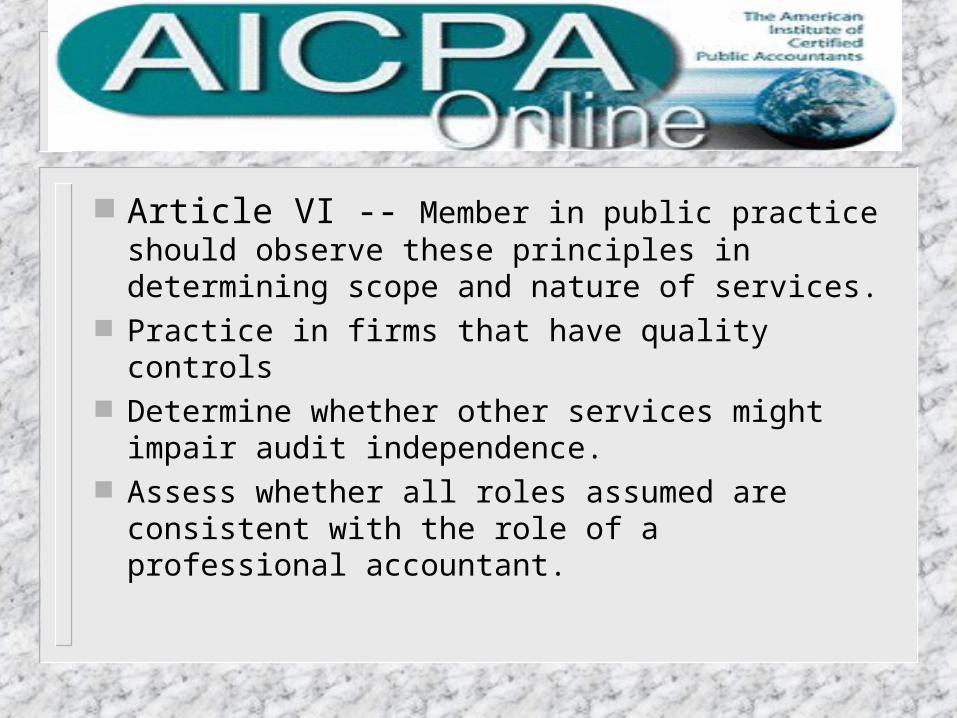

Article VI -- Member in public practice should observe these principles in determining scope and nature of services.

Practice in firms that have quality controls Determine whether other services might impair

audit independence. Assess whether all roles assumed are consistent

with the role of a professional accountant.