Embed Size (px)

Citation preview

ETHICS FOR TAX PRACTITIONERS

Published by Fast Forward Academy, LLChttps://fastforwardacademy.com(888) 798-PASS (7277)

© 2021 Fast Forward Academy, LLC

All rights reserved. No part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of the publisher.

2 Hour(s) - Ethics

IRS Provider #: UBWMFIRS Course #: UBWMF-E-00235-21-S

NASBA: 116347

CTEC Provider #: 6209CTEC Course #: 6209-CE-0074

The information provided in this publication is for educational purposes only, and does not necessarily reflect all laws, rules, or regulations for the tax year covered. This publication is designed to provide accurate and authoritative information concerning the subject matter covered, but it is sold with the understanding that the publisher is not engaged in rendering legal, accounting or other professional services. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.

To the extent any advice relating to a Federal tax issue is contained in this communication, it was not written or intended to be used, and cannot be used, for the purpose of (a) avoiding any tax related penalties that may be imposed on you or any other person under the Internal Revenue Code, or (b) promoting, marketing or recommending to another person any transaction or matter addressed in this communication.

COURSE OVERVIEW.............................................................................................................................................................. 9

Course Description ....................................................................................................................................................................... 9

Learning Objectives ...................................................................................................................................................................... 9

OVERVIEW OF ETHICAL PRACTICE...................................................................................................................................... 9

Introduction................................................................................................................................................................................... 9

IRS Supervision.............................................................................................................................................................................. 9

DEFINING TAX PREPARER ................................................................................................................................................... 9

Tax Return Preparer ..................................................................................................................................................................... 9

Safe Harbor Rules .......................................................................................................................................................................10

Practicing Before the IRS............................................................................................................................................................10

Tax Return Information..............................................................................................................................................................10

Disclosure & Consent .................................................................................................................................................................10

Defining Ethics.............................................................................................................................................................................11

The Benefits of Ethical Behavior ...............................................................................................................................................12

RESPONSIBILITY TO REMAIN CURRENT........................................................................................................................... 12

Continuing Education .................................................................................................................................................................12

REVIEW OF CIRCULAR 230................................................................................................................................................. 13

Stringent Standards....................................................................................................................................................................13

Duties ...........................................................................................................................................................................................13

Section 10.7 – Representing oneself ........................................................................................................................................14

Section 10.20 - Information to be furnished ...........................................................................................................................14

Section 10.23 - Prompt disposition of pending matters ........................................................................................................14

Section 10.24 - Assistance from disbarred or suspended persons ......................................................................................14

Section 10.25 - Practice by former government employees .................................................................................................14

Section 10.26 - Performance as a Notary ..............................................................................................................................14

Section 10.27 – Contingent Fees ...............................................................................................................................................15

Section 10.28 - Return of client’s records ................................................................................................................................15

Confidentiality Privilege ..........................................................................................................................................................15

Section 10.21 - Client Omissions - Duty to Advise ..................................................................................................................15

Advertising and Solicitation .......................................................................................................................................................16

Section 10.22 - Diligence as to Accuracy ..................................................................................................................................16

Section 10.29 - Conflict of Interest............................................................................................................................................17

Section 10.31 - Refund Check Negotiation ..............................................................................................................................17

Section 10.32 - Practice of law...................................................................................................................................................17

Section 10.33 - Best practices....................................................................................................................................................17

Section 10.34 - Standards with respect to tax returns and documents, affidavits and other papers..............................17

Section 10.37 - Requirements for Written Advice...................................................................................................................18

Section 10.50 - Sanctions ...........................................................................................................................................................18

Section 10.53 - Receipt of information concerning practitioner ...........................................................................................18

TAX PREPARER SANCTIONS AND PENALTIES.................................................................................................................. 18

Incompetence and Disreputable Conduct...............................................................................................................................18

Violations Subject to Sanction...................................................................................................................................................19

Penalties.......................................................................................................................................................................................19

Understatement of liability §6694 ............................................................................................................................................20

Aiding and Abetting ....................................................................................................................................................................20

Failures under §6695..................................................................................................................................................................21

Safeguarding Taxpayer Information.........................................................................................................................................22

Providing IRS with fraudulent information or documents ....................................................................................................22

Payment .......................................................................................................................................................................................22

EXAMPLES OF VIOLATIONS SUBJECT TO SANCTION ...................................................................................................... 23

Prompt Disposition.....................................................................................................................................................................23

Due Diligence ..............................................................................................................................................................................23

Due Diligence in Tax Return Preparation ................................................................................................................................23

Disreputable Conduct ................................................................................................................................................................23

RECENT EXAMPLES OF ABUSIVE RETURN PREPARER INVESTIGATIONS ....................................................................... 24

FS-2010-3, January 2010.............................................................................................................................................................24

Tax Fraud Conspiracy .................................................................................................................................................................24

$1 Million Tax Fraud ...................................................................................................................................................................25

Daughters of California .............................................................................................................................................................25

30 Months for Tax Fraud............................................................................................................................................................25

Filing False Returns.....................................................................................................................................................................25

BEST PRACTICES FOR TAX ADVISORS............................................................................................................................... 26

Best Practices ..............................................................................................................................................................................26

Recordkeeping ............................................................................................................................................................................26

CASE STUDIES..................................................................................................................................................................... 27

Case Study #1..............................................................................................................................................................................27

Case Study #2..............................................................................................................................................................................27

ADDENDUM A .................................................................................................................................................................... 27

Consent to Disclose Forms ........................................................................................................................................................27

Course Description 9

•

•

•

•

COURSE OVERVIEW

COURSE DESCRIPTIONEthics are the values that govern our decisions and actions. Some companies have clearly defined written codes of principles for determining the difference between good and bad behavior. Good ethics boils down to knowing the difference between right and wrong and choosing to do what is right. This course will explore the definition of ethics in the eyes of the Internal Revenue Service, as well as the important covenants contained in Treasury Circular 230, which governs practice before the IRS. Additionally, this course will discuss the various penalties and sanctions available for violation of the rules by individuals allowed to practice.

LEARNING OBJECTIVESAfter completing this chapter, you will be able to:

Explain the role of ethics in the tax preparation industry

Explain the IRS rules as outlined in Circular 230.

Identify common ethical violations and penalties.

Discuss procedures that promote compliance with ethical guidelines.

OVERVIEW OF ETHICAL PRACTICE

INTRODUCTIONTraditionally, the tax preparation industry has not had to endure the level of government regulation that some other industries have. With some notable exceptions, few states have mandated that preparers of income tax returns be licensed. As a tax system tends to function best when the public has confidence in the honesty and integrity of those providing advice and services, the need to promote, maintain—and on occasion—restore the public’s confidence in the profession of tax preparers is necessary. That is why some level of legal and ethical guidance is required.

IRS SUPERVISIONTax return preparers are subject to IRS scrutiny when it comes to how they conduct themselves with clients. The Internal Revenue Code (I.R.C.) provides specific penalties that may be assessed against tax return preparers who “cross the line” when it comes to representing a client’s interest. Tax return preparers are subject to not only specific statutory provisions, but also the regulatory provisions of Treasury Department Circular No. 230 – Tax Professionals, which provides for sanctions that are separate from, and in addition to, those defined in the I.R.C.

Tax practitioners and preparers are expected to comply with the statutory requirements set forth for return preparation standards, disclosure requirements, and conduct standards. Failure to do so could result in penalties, fines, and yes, even jail time. Therefore, the stakes regarding compliance are high. Even the most seasoned of tax return preparers can be blindsided by the various legal and ethical expectations and requirements set forth, if caught unaware.

DEFINING TAX PREPARER

TAX RETURN PREPARERA tax return preparer is defined by I.R.C. §7701(a)(36) and Treas. Reg. §301.7701-15. Section 7701(a)(36) defines a preparer as “any person who prepares for compensation, or who employs one or more persons to prepare for compensation, any return of tax imposed by subtitle A, or any claim for refund of tax imposed by subtitle A.” (Note that subtitle A references income taxes only).

10 Defining Tax Preparer

•

•

•

•

•

•

•

•

This section of the Code also discusses which individuals are not considered tax return preparers. Those are individuals who:

Furnish typing, reproducing, or other mechanical assistance.

Prepare a return or claim for their employer or for an officer or employee of the employer.

Prepare fiduciary returns or claims for refund for any person.

Prepare a claim for refund for a taxpayer in response to an audit notice of deficiency, if the audit determination affects the tax liability of the individual who prepares the claim for the other taxpayer.

Treasury Regulation section 301.7701-15(b) identifies an individual who prepares all or a substantial portion of a return or claim for refund as a tax preparer. However, what determines a “substantial portion” is often subjective. Some guidance is provided in the regulations that suggest “substantial” takes into consideration the length and complexity of the portion in question, the tax liability, or refund involved for that section, and the tax liability or refund for the return in its entirety.

SAFE HARBOR RULESRegulations do offer two safe harbor rules for determining what is considered non-substantial preparation. Nonsigning tax return preparers are not considered to have prepared a “substantial portion” of a return or claim for refund if the schedule, entry, or other portion of the return or claim for refund involves amounts of gross income, amounts of deductions, or amounts on the basis of which credits are determined that are:

Less than $10,000; or

Less than $400,000 and also less than 20 percent of the gross income as shown on the return or claim for refund (or, for an individual, the individual's adjusted gross income).

PRACTICING BEFORE THE IRSAccording to Circular 230, practicing before the IRS is broadly defined to include “all matters connected to a presentation to the IRS or any of its officers and employees relating to a taxpayer's rights, privileges, or liabilities under the federal tax laws.” Those individuals that prepare federal income tax returns, represent taxpayers before the IRS, or that render tax opinions are said to be “practicing” before the IRS.

TAX RETURN INFORMATIONInformation related to tax return preparation is defined as “any information, including, but not limited to, a taxpayer’s name, address, or identifying number, which is furnished in any form or manner for, or in connection with, the preparation of a tax return of the taxpayer.”

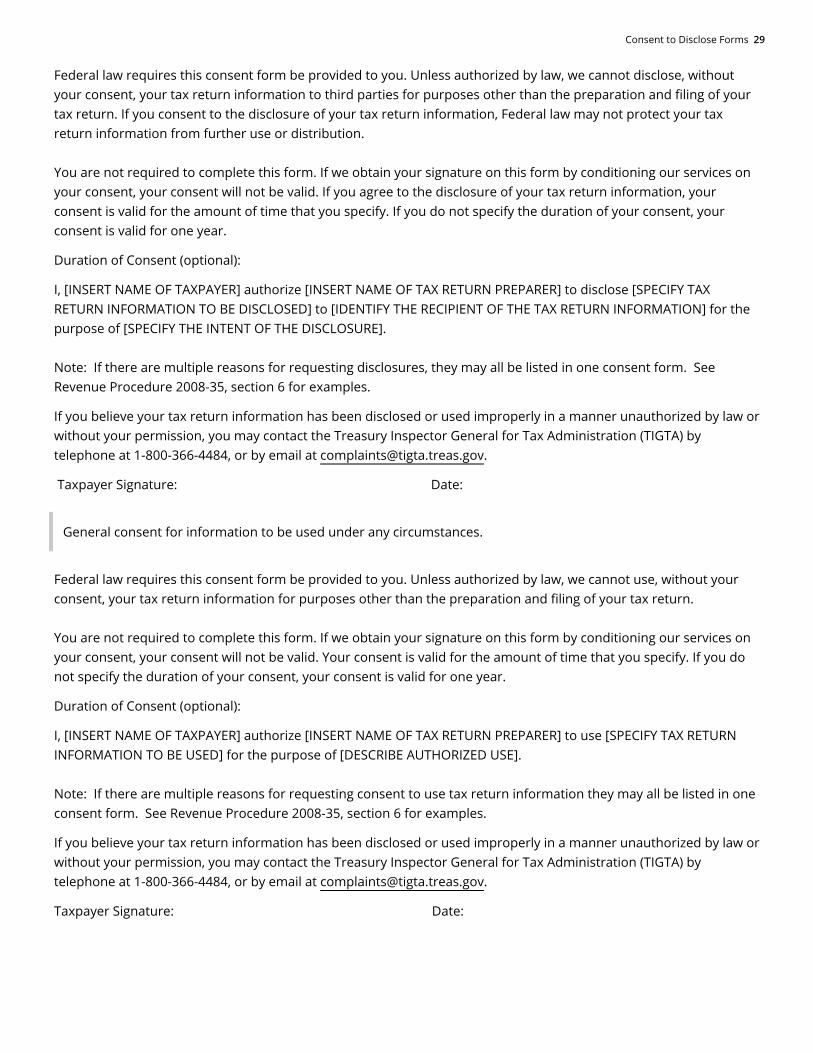

DISCLOSURE & CONSENTThere are certain situations in which a tax preparer may disclose information without a client’s consent. Treasury Regulation section 301.7216-2 provides 16 such examples. For instance, a preparer may disclose information, without the consent of a taxpayer, to another tax preparer for obtaining auxiliary services in connection with the preparation of a return. This is acceptable as long as the services provided are not substantive determinations or advice affecting the tax liability reported by the taxpayer.

In all other circumstances, tax preparers may disclose taxpayer return information, or use it for any purpose other than preparing and filing a return, only if the tax preparer has received the signed consent of the taxpayer beforehand. Generally, return information can be disclosed with the formal consent of the taxpayer when the preparer is:

Disclosing tax return information to a third party,

Using or disclosing information associated with another person’s return, or

Defining Ethics 11

•

•

•

•

•

•

•

•

•

•

Soliciting other business not related to tax matters.

Separate consents are required for each instance of disclosure and use. Consents must:

Include the name of the taxpayer and tax return preparer,

Contain the affirmative consent of the taxpayer (i.e., no opt-out clause allowed),

Be signed and dated by the taxpayer,

Identify intended purpose of disclosure/use,

Identify recipient of materials,

Describe the authorized information to be used/disclosed,

Include the applicable mandatory language provided in Section 4.04(a)-(c) of Revenue Procedure 2008-35. This language lets the taxpayer know they are not required to sign the consent, and if they do, can define a set time that consent remains in effect,

Include the mandatory language of Section 4.04(d) that refers the taxpayer to the Treasury Inspector General for Tax Administration, if they believe their tax information was disclosed or used improperly, and

If applicable, include the appropriate mandatory statement in Section 4.04(e) of Revenue Procedure 2008-35. This informs the taxpayer that their tax return information may be disclosed to a tax return preparer located outside the U.S.

Examples of a few situations in which consent is required, and the necessary language to include is demonstrated in Addendum A. Sanctions imposed for improperly disclosing return information are covered in the Penalties for Conduct section of this course.

DEFINING ETHICSTreasury Circular 230 lays the foundation for the ethical conduct of enrolled agents, CPAs, attorneys, and others practicing before the Internal Revenue Service. Contained within circular 230 are the standards of practice that all covered tax preparers must follow.

In addition to the rules provided in Circular 230, tax professionals also receive guidance from the professional organizations where they are members. For example, an enrolled agent who is a member of the National Association of Enrolled Agents agrees to uphold the NAEA Code of Ethics and Rules of Professional Conduct. A tax preparer who is also a CPA and a member of the American Institute of Certified Public Accountants (AICPA) has additional ethical tax practice standards for members of the AICPA. At the moment, only seven states have regulations governing the practice of tax return preparers—California, Connecticut, Illinois, Maryland, Nevada, New York, and Oregon. If you prepare returns for those states, you should review the guidelines established and rules of conduct. Attorneys and CPAs are also regulated by state licensing authorities.

12 Responsibility to Remain Current

•

•

•

•

THE BENEFITS OF ETHICAL BEHAVIOR

All paid tax return preparers are subject to civil penalties for actions ranging from knowingly preparing a return that understates the taxpayer’s liability to failing to sign or provide an identification number on a return they prepare. Tax return preparers who demonstrate a pattern of misconduct may be enjoined from preparing future returns. Additionally, the IRS may pursue and impose criminal penalties against a tax return preparer for the most severe misconduct.

Clearly, and for obvious reasons, avoiding penalties and staying out of the slammer provide motivation for a preparer to follow rules and maintain an ethical tax practice. While the consequences of being unethical are clearly defined for tax preparers, the benefits for practitioners who maintain high ethical standards are not. Let’s take a moment to consider some benefits of ethical behavior.

Clients are more likely to refer others to a tax preparer they believe will behave ethically.

People are more comfortable working with businesses that demonstrate ethical behavior. A taxpayer should prefer to work with a return preparer they feel is less likely to create a high risk for an audit by claiming unreasonable positions on their return.

A practice built on a solid foundation of adhering to tax regulations and ethical guidelines is less likely encounter regulatory scrutiny. This should make it easier for you to sleep at night.

In the event your practice is audited, your ability to demonstrate a culture of compliance with the regulations, including those surrounding ethical behavior will make your life easier.

RESPONSIBILITY TO REMAIN CURRENT

CONTINUING EDUCATIONOne of the most important duties of a tax return preparer is to stay up-to-date with the ever changing rules and regulations contained within the tax laws. The best way to accomplish this is to participate in regular continuing education courses. Continuing education is defined as being a type of learning activity geared towards professionals who are encouraged to maintain and expand a solid foundation of knowledge in their specific field of practice. Continuing education is usually a short unit of instruction attended in person, or via online, self-study format. Attendees earn credit hours for their attendance in continuing education courses and many professionals have a specific number of hours they are required to achieve to maintain professional designations.

In tax preparation, there are two levels of continuing education. The first level is a voluntary program aimed at preparers who have not achieved another form of credential or enrollment. The IRS, in 2014, launched a formal, voluntary program for unenrolled preparers called the Annual Filing Season Program (AFSP).

Stringent Standards 13

1.

2.

3.

4.

5.

The AFSP is an annual program of continuing education offered to tax preparers who wish to set themselves apart from other unenrolled preparers who choose not complete ongoing education in their industry.

The program allows these unenrolled preparers to obtain a specified number of hours (18 hours for unenrolled preparers and 15 hours for enrolled/credentialed preparers), at which point they will earn a Record of Completion and be listed in an IRS sponsored database which will be made available to the public.

With tax preparers, a significant change in their current ability to represent clients took effect in 2016. Previously, a tax preparer could represent a client whose return they prepared and signed if that client was subjected to an examination by the IRS. Prior to 2016, tax preparers had limited representation rights for these clients. As of 2016, only tax preparers who have earned the AFSP Record of Completion will maintain their limited representation rights. All other unenrolled preparers will lose this representation ability.

The second level of continuing education in tax preparation applies to Enrolled Agents. An enrolled agent is considered a tax expert. These individuals have successfully completed a 3 part exam covering individual tax, business tax and representation rules and procedures. Upon completion of these exams, an enrolled agent is required to obtain 72 hours of continuing education over a 3 year enrollment period, with a minimum of 16 hours completed each year. Failure to maintain the required continuing education credits will result in loss of enrolled agent status.

REVIEW OF CIRCULAR 230

STRINGENT STANDARDSAttorneys, certified public accountants, enrolled agents, and other individuals authorized to practice before the IRS who prepare returns are subject to additional Federal oversight. Collectively known as Practitioners, these individuals must adhere to the more stringent standards of practice promulgated in Part 10 of Title 31 of the Code of Federal Regulations and reprinted in Treasury Department Circular 230. Practitioners who violate these standards of practice or who are shown to be incompetent or disreputable may be censured, suspended or disbarred from practice. The IRS Office of Professional Responsibility is charged with investigating allegations of Practitioner misconduct and conducting disciplinary proceedings, where warranted.

Published by the Treasury Department, Circular 230 sets forth the regulations and best practices governing the practice of attorneys, CPAs, EAs, Enrolled Actuaries, appraisers, and any others coming before the IRS. Circular 230 regulations apply only to those who practice before the IRS and are not designed to alter or override other ethical standards to which practitioners may be accountable.

Circular 230 is divided into five subparts:

Subpart A - rules governing authority to practice

Subpart B - duties and restrictions relating to practice before the IRS

Subpart C - sanctions for violation of the regulations

Subpart D - rules applicable to disciplinary proceedings

Subpart E - general provisions

Under Circular 230, the Office of Professional Responsibility (OPR) is given the authority to suspend or disbar individuals from practicing before the IRS.

DUTIESPractitioners must promptly submit records or information requested by officers or employees of the IRS. When the Office of Professional Responsibility requests information concerning possible violations of the regulations by other parties, the practitioner must provide the information and be prepared to testify in disbarment or suspension proceedings. The IRS may exempt a practitioner from these rules if the information requested is privileged or the

14 Review of Circular 230

•

•

•

•

request is of doubtful legality. When making this determination the practitioner must be acting in good faith and on reasonable grounds.

SECTION 10.7 – REPRESENTING ONESELFSection 10.7 in Circular 230 also lays out exceptions and exclusions in regards to the types of people and situations that are NOT considered to be “practicing before the IRS” and are therefore exempt from Circular 230. The list is long but generally includes:

Individuals representing themselves.

Individuals who are not a practitioner may represent a taxpayer on a limited basis under some circumstances. For example, an individual may represent an immediate family member, a full-time employee may represent their employer, an officer, or full-time employee may assist a corporation, and a partner may assist a partnership. Additionally, an individual can represent an individual or entity before the IRS, if that party is located outside of the US.

Individuals participating in rule making.

Anyone can prepare a tax return, appear before the IRS as a witness for a taxpayer, or provide requested information to the IRS. Doing so, does not rise to the definition of “practicing before the IRS.”

Any tax practitioner who practices before the IRS and does not qualify for one of the exemptions outlined in subpart A, is subject to the Duties and Restrictions outlined in Subpart B. This section is truly the “meat and potatoes” governing tax practices.

SECTION 10.20 - INFORMATION TO BE FURNISHEDThis section requires a practitioner to submit promptly records or information upon a lawful request from the IRS. An exception is made if the practitioner believes in good faith and on reasonable grounds that the records or information is privileged. If the information requested is not in their possession or control, the practitioner must notify the IRS and supply any information as to the identity of who they believe has the requested records or information. They must also make a reasonable inquiry to their clients regarding who may have the information sought. Furthermore, a practitioner may not interfere with the lawful efforts of the IRS to obtain records or information unless they believe, in good faith and on reasonable grounds, that the record of information is privileged.

SECTION 10.23 - PROMPT DISPOSITION OF PENDING MATTERSShort answer is do not attempt to unreasonably delay the resolution of any matter before the IRS. Section 10.23 was written to ensure that no one party receives preferential treatment in matters before the IRS.

SECTION 10.24 - ASSISTANCE FROM DISBARRED OR SUSPENDED PERSONSTax practitioners may not knowingly accept (directly or indirectly) assistance from an individual who has been disbarred or suspended from practice before the IRS, if that assistance relates to a matter constituting practice before the IRS.

SECTION 10.25 - PRACTICE BY FORMER GOVERNMENT EMPLOYEESThis section outlines in detail the current federal statutes governing post-employment restrictions as they apply to former government employees.

SECTION 10.26 - PERFORMANCE AS A NOTARY A practitioner who is a notary public and has an interest in a matter before the IRS may not engage in any notary activities related to that matter. This section states the obvious. Notaries cannot be a party to any matter, benefit from any transaction, or have a conflict of interest with any matter administered by the IRS.

Section 10.27 – Contingent Fees 15

•

1.

2.

•

•

•

•

1.

2.

•

SECTION 10.27 – CONTINGENT FEESA practitioner is allowed to set their fees according to the complexity of the job; however, these fees cannot be unconscionable. A practitioner may not charge a contingent fee for services rendered in connection with any matter before the Internal Revenue Service. However, practitioners may charge a contingent fee in regards to services rendered by an IRS challenge to an original tax return or an amended return or claim for refund/credit that was filed within 120 days of the taxpayer receiving written notice from the IRS. They may also charge a contingent fee for services rendered in connection with any judiciary proceeding originating under the I.R.C.

A contingent fee is one that is based on whether or not a position taken on a return avoids challenge by the IRS. A practitioner may not charge a contingent fee for services in connection with any matter before the IRS, except:

Services related to an IRS examination or challenge of:

An original tax return, or

An amended tax return filed within 120 days of a taxpayer receiving a notice of examination.

For services rendered in connection with a claim for credit or refund filed solely in connection with the determination of statutory interest or penalties assessed by the IRS.

Services connected to a judicial proceeding.

SECTION 10.28 - RETURN OF CLIENT’S RECORDSIf a client requests, a practitioner is required to return promptly any and all records necessary for a client to comply with their federal tax obligations. Even if a client owes the practitioner money, they must comply with their responsibility under this section. A practitioner may however withhold a client’s current year completed tax return until payment is made.

The practitioner may retain copies of the records given to a client, and only records necessary for a client to comply with their federal tax obligation must be turned over. Other records the practitioner may have are exempt.

It is important to keep in mind that with reference to this section, state laws may differ. While this rule relates only to tax related records, most state accountancy laws require the immediate return of all client records.

CONFIDENTIALITY PRIVILEGE The confidentiality protection of certain communications between a taxpayer and an attorney (privileged communications) applies to similar communications between a taxpayer and any federally authorized tax practitioner.

One may not invoke this confidentiality privilege in any administrative proceeding with an agency other than the IRS.

The protection of this privilege applies only to tax advice given to the taxpayer by any individual who is a federally authorized tax practitioner. The confidentiality protection applies to communications that would be considered privileged if they were between the taxpayer and an attorney and that relate to:

Noncriminal tax matters before the IRS, or

Noncriminal tax proceedings brought in federal court by or against the United States.

This protection does not apply to any written communications between a federally authorized tax practitioner and certain representatives or employees of a corporation nor does it apply if the communication promotes a tax shelter to a corporation.

SECTION 10.21 - CLIENT OMISSIONS - DUTY TO ADVISEA practitioner generally may rely in good faith on information furnished by the client. The practitioner may not, however, ignore the implications of information furnished and must make reasonable inquiries if it appears to be incorrect or inconsistent. A practitioner who is aware the client has not complied with the rules and regulations of the IRS, or knows of any error or omission, must promptly advise the client concerning the existence of the error or

16 Review of Circular 230

omission and of the consequences of allowing them to remain uncorrected. If not corrected, the practitioner cannotsign the return. A practitioner may not advise a client to take a frivolous position on a return.

ADVERTISING AND SOLICITATIONTax practitioners can neither directly or indirectly solicit employment in matters related to the IRS, if such solicitation violates federal or state laws, or other applicable rulings. Any lawful solicitation must clearly identify it as such, and if applicable, identify the source of information used.

Fees are also covered in this section. A practitioner is permitted to publish a written schedule of fees such as fixed fees for routine services, hourly rates, fee ranges for particular services, and initial consultation fees. If a client is responsible for any costs incurred, a statement of fee information disclosing such costs must be provided. A practitioner may not charge more than their published rates for at least 30 calendar days after the last date on which the schedule of fees was published. Furthermore, practitioners are required to keep copies of all solicitation mailings for at least 36 months.

The practitioner may advertise using any method(s) he chooses. A practitioner may not make any advertising statement that is in any way false, fraudulent, coercive, misleading, or deceptive, or that violates any state federal or other applicable rule. A practitioner may not use the word “certified” or otherwise imply an employment relationship with the IRS. Phrases such as “enrolled (or admitted) to practice” or “enrolled to represent” before the IRS areallowable. If the practitioner publishes a schedule of fees, he must adhere to the schedule for at least 30 days from the last date of publication. Such a schedule must include fixed fees for specific routine services, hourly rates, range of fees for particular services and any fees charged for an initial consultation.

SECTION 10.22 - DILIGENCE AS TO ACCURACYThis section states that a practitioner must exercise due diligence in preparing or assisting in the preparation of all information related to IRS matters, as well as in determining the correctness of written representations made to the Department of Treasury and/or the IRS. Except as specified in Sections 10.34 and 10.37, a practitioner is presumed to have exercised due diligence, for purposes of this section, if the practitioner relies on the work product of another person, and for which reasonable care was taken in every respect.

A practitioner must exercise due diligence in preparing, approving, and filing tax returns and all other documents, as well as any oral statements relating to IRS or Treasury Department matters. The practitioner must use the same diligence in determining the correctness of oral or written statements made to clients with reference to any matter administered by the Internal Revenue Service. A practitioner will be presumed to have exercised due diligence if the practitioner relies on the work product of another person and the practitioner used reasonable care in engaging, supervising, training, and evaluating the person.

Section 10.29 - Conflict of Interest 17

•

•

•

•

•

•

•

SECTION 10.29 - CONFLICT OF INTERESTA conflict of interest exists if the representation of one client is directly adverse to another client or there is a significant risk that the representation of one or more clients will be materially limited by the practitioner’s responsibilities to another client, a former client or a third person, or by a personal interest of the practitioner. Practitioners may not represent a client if such representation causes or appears to cause a conflict of interest unless:

The practitioner reasonably believes that he will be able to provide competent and diligent representation to each affected client, and

The representation is not prohibited by law, and

Each affected client waives the conflict of interest in writing at the time the practitioner knows of the existence of the conflict of interest. The confirmation may be made within a reasonable period of time, but in no event later than 30 days after the practitioner becomes aware of the conflict.

SECTION 10.31 - REFUND CHECK NEGOTIATIONGenerally, a practitioner preparing tax returns cannot endorse or otherwise negotiate any check issued with respect to a client’s federal tax liability by the government. However, Form 2848 “Power of Attorney and Declaration of Representative” does allow a taxpayer to authorize the tax preparer to receive refund checks. Even with this exception, preparers are still forbidden from endorsing refund checks.

SECTION 10.32 - PRACTICE OF LAWThere is nothing in these regulations that should be taken as an authorization to practice law. The tax practitioner is not a lawyer, and does not play one on TV. Therefore, refrain from making any legal representations.

SECTION 10.33 - BEST PRACTICESTax preparers should give their clients the highest quality representation by adhering to the best practices outlined in this section and elsewhere. What constitutes best practices as defined by the IRS?

Communicating clearly with the client regarding the terms of the engagement.

Establishing the facts, determining which facts are relevant, evaluating the reasonableness of any assumptions or representations, relating the applicable law (including potentially applicable judicial doctrines) to the relevant facts, and arriving at a conclusion supported by the law and the facts.

Advising the client regarding the import of the conclusions reached, including, for example, whether a taxpayer may avoid accuracy-related penalties under the Internal Revenue Code if a taxpayer acts in reliance on the advice.

Acting fairly and with integrity in practice before the IRS.

SECTION 10.34 - STANDARDS WITH RESPECT TO TAX RETURNS AND DOCUMENTS, AFFIDAVITS AND OTHER PAPERSA practitioner must advise a client not to take a frivolous position on a document, affidavit, or other paper submitted to the IRS. They are required also to advise a client not to submit documents that may unnecessarily delay or impede the administration of the federal tax laws, or contain or omit information that demonstrates an intentional disregard for the rules and regulations of the Code, unless that document evidences a good faith challenge to the rules or regulations.

A practitioner may generally rely, in good faith, without verification upon information provided by the client when advising a client to take a specific position on a document submitted to the IRS. However, a practitioner is required to make reasonable inquiries about information furnished to them, if it appears to be incorrect, incomplete, or inconsistent with other factual assumptions.

18 Tax Preparer Sanctions and Penalties

•

•

•

•

•

•

•

•

•

•

•

•

•

•

SECTION 10.37 - REQUIREMENTS FOR WRITTEN ADVICEA practitioner may give written advice concerning Federal tax matters relating to a tax avoidance transaction or a tax shelter. Practitioners providing such written advice must comply with each of the following requirements:

Base the written advice on reasonable factual and legal assumptions (including assumptions as to future events);

Reasonably consider all relevant facts and circumstances that the practitioner knows or reasonably should know;

Use reasonable efforts to identify and ascertain the facts relevant to written advice on each Federal tax matter;

Not rely upon representations, statements, findings, or agreements (including projections, financial forecasts, or appraisals) of the taxpayer or any other person if reliance on them would be unreasonable;

Relate applicable law and authorities to facts; and

Not, in evaluating a Federal tax matter, take into account the possibility that a tax return will not be audited or that a matter will not be raised on audit.

SECTION 10.50 - SANCTIONSThis section states the Secretary of Treasury, after a determination, may publically censure, suspend, or disbar any practitioner from practice before the IRS, if they are shown to be incompetent or disreputable (see Section 10.51), fails to comply with any regulation in this part, intends to defraud, or willfully and knowingly misleads or threatens a client or perspective. It also gives the Secretary of Treasury the authority to impose a monetary penalty on any practitioner who engages in conduct subject to sanction.

SECTION 10.53 - RECEIPT OF INFORMATION CONCERNING PRACTITIONERIf an agent of the IRS has reason to believe that a practitioner has violated any of these provisions, they must make an immediate written report to the Director of the Office of Professional Responsibility regarding the suspected violation.

TAX PREPARER SANCTIONS AND PENALTIES

INCOMPETENCE AND DISREPUTABLE CONDUCTIncompetence and disreputable conduct for which the IRS may sanction a practitioner includes, but is not limited to, the following:

Conviction of any criminal offense under the Federal tax laws

Conviction of any criminal offense involving dishonesty or breach of trust

Conviction of any felony under Federal or State law for which the conduct involved renders the practitioner unfit to practice before the Internal Revenue Service

Giving false or misleading information, or participating in any way in the giving of false or misleading information to the Department of the Treasury or any officer or employee thereof, or to any tribunal authorized to pass upon Federal tax matters in connection with any matter pending or likely to be pending before them

Solicitation of employment as prohibited under §10.30, the use of false or misleading representations with intent to deceive a client or prospective client in order to procure employment, or intimating that the practitioner is able to improperly obtain special consideration or action from the IRS or any officer or employee thereof

Willfully failing to make a Federal tax return in violation of the Federal tax laws, or willfully evading, attempting to evade, or participating in any way in evading or attempting to evade any assessment or payment of any Federal tax

Willfully assisting, counseling, encouraging a client or prospective client in violating, or suggesting to a client or prospective client to violate, any Federal tax law, or knowingly counseling or suggesting to a client or prospective client an illegal plan to evade Federal taxes

Misappropriation of, or failure properly or promptly to remit funds received from a client for the purpose of payment of taxes or other obligations due the United States

Violations Subject to Sanction 19

•

•

•

•

•

•

•

Directly or indirectly attempting to influence, or offering or agreeing to attempt to influence, the official action of any officer or employee of the IRS by the use of threats, false accusations, duress or coercion, by the offer of any special inducement or promise of an advantage or by the bestowing of any gift, favor or thing of value

Disbarment or suspension from practice as an attorney, certified public accountant, public accountant, or actuary by any duly constituted authority of any State, territory, or possession of the United States, including a Commonwealth, or the District of Columbia, any Federal court of record or any Federal agency, body or board

Knowingly aiding and abetting another person to practice before the Internal Revenue Service during a period of suspension, disbarment, or ineligibility of such other person

Contemptuous conduct in connection with practice before the IRS, including the use of abusive language, making false accusations or statements, knowing them to be false, or circulating or publishing malicious or libelous matter

Giving a false opinion, knowingly, recklessly, or through gross incompetence, including an opinion that is intentionally or recklessly misleading, or engaging in a pattern of providing incompetent opinions on questions arising under the Federal tax laws.

Willfully failing to sign a tax return prepared by the practitioner when federal tax laws require the signature, unless the failure is due to reasonable cause and not due to willful neglect

Willfully disclosing or otherwise using a tax return or tax return information in a manner not authorized by the Internal Revenue Code, contrary to the order of a court of competent jurisdiction, or contrary to the order of an administrative law judge in a proceeding instituted under the Circular 230 instructions for sanction proceedings

VIOLATIONS SUBJECT TO SANCTIONThe IRS may sanction a practitioner if the practitioner willfully violates any of the regulations (not best practices), recklessly or through gross incompetence violates Circular 230 directives relating to: standards with respect to tax returns and documents, affidavits and other papers, requirements for covered opinions, procedures to ensure compliance, or requirements for other written advice.

PENALTIESReturn preparers are responsible for taking a reasonable position on a tax return. To be reasonable, there must be substantial authority for the position, or in the case of a disclosed position, a reasonable basis for the treatment of such item on the return.

The substantial authority standard is an objective standard involving an analysis of the law and application of the law to relevant facts. The substantial authority standard is less stringent than the more likely than not standard (the standard that is met when there is a greater than 50-percent likelihood of the position being upheld), but more stringent than the reasonable basis standard. There is substantial authority for the tax treatment of an item only if the weight of the authorities supporting the treatment is substantial in relation to the weight of authorities supporting contrary treatment. All authorities relevant to the tax treatment of an item, including the authorities contrary to the treatment, are taken into account in determining whether substantial authority exists. The weight of authorities is determined in light of the pertinent facts and circumstances.

Reasonable basis is a relatively high standard of tax reporting that is significantly higher than not frivolous or not patently improper. The reasonable basis standard is not satisfied by a return position that is merely arguable. If a return position is reasonably based on one or more of the authorities set forth in §1.6662–4(d)(3)(iii) (taking into account the relevance and persuasiveness of the authorities, and subsequent developments), the return position will generally satisfy the reasonable basis standard even though it may not satisfy the substantial authority standard.

Tax shelters have a higher standard and must have a confidence level of at least more likely than not (greater than 50 percent likelihood) that one or more significant Federal tax issue would be resolved in the taxpayer’s favor. A tax shelter, for purposes of the substantial understatement portion of the accuracy-related penalty, is a partnership or other entity, plan, or arrangement, with a significant purpose to avoid or evade federal income tax

20 Tax Preparer Sanctions and Penalties

•

•

•

•

•

•

•

1.

a.

b.

c.

2.

•

1.

2.

A tax return cannot contain frivolous positions, which have no basis for validity in existing law or which have been deemed frivolous by the United States Tax Court or other federal court. The IRS may assess penalties within 3 years after the taxpayer files the return. No proceeding in court without assessment for the collection of such tax shall begin after the expiration of such period. There is no statute of limitation for fraudulent returns.

Taxpayers and tax return preparers can use Form 8275, Form 8275-R, or Rev. Proc. 2008-14 to disclose items or positions, except those taken contrary to a regulation, that are not otherwise adequately disclosed on a tax return to avoid certain penalties.

The form is filed to avoid the portions of the accuracy-related penalty due to disregard of rules or to a substantial understatement of income tax for non-tax shelter items if the return position has a reasonable basis. It can also be used for disclosures relating to preparer penalties for understatements due to unreasonable positions or disregard of rules.

The portion of the accuracy-related penalty attributable to the following types of misconduct cannot be avoided by disclosure on Form 8275.

Negligence.

Disregard of regulations.

Any substantial understatement of income tax on a tax shelter item.

Any substantial valuation misstatement under chapter one of the Internal Revenue Code.

Any substantial overstatement of pension liabilities.

Any substantial estate or gift tax valuation understatements.

UNDERSTATEMENT OF LIABILITY §6694Penalties are applicable in the following circumstances where the understatement is:

Unreasonable positions – A penalty of $1,000 or 50% of preparer’s fee, whichever is greater.

A position lacking substantial authority is unreasonable if the preparer knew (or should have known) of the position, and

For undisclosed positions – The position does not have substantial authority.

For disclosed positions – The position does not have a reasonable basis.

For tax shelters – There was not a reasonable belief that the position would more likely than not be sustained on its merits.

If a return preparer understates tax liability on a return, the IRS will not impose a penalty if the preparer shows that there is reasonable cause and the tax return preparer acted in good faith.

Willful or reckless conduct – A penalty of $5,000 or 75% of preparer’s fee, whichever is greater.

Willful or reckless conduct is conduct by the tax return preparer that is a willful attempt in any manner to understate the liability for tax on the return or claim, or a reckless or intentional disregard of rules or regulations.

The amount of any penalty payable for willful misconduct is reduced by any penalty for an unreasonable position.

AIDING AND ABETTINGA civil fraud penalty is imposed under section 6701 for aiding and abetting understatements of the tax liability for another person or entity. This particular penalty applies to any individual – return preparer or not – that “aids, assists or advises in the preparation or presentation of a tax return, claim, or other document and that believe their assistance will be used in a material tax matter which will result in an understatement of the tax liability of another person.”

Failures under §6695 21

•

1.

2.

3.

4.

5.

•

In civil fraud matters, the IRS carries the burden of proof pursuant to I.R.C. section 6703. The penalty is usually $1,000. However, if the taxpayer is a corporation the penalty jumps to $10,000. The good news, if you can call it that, is that section 6694(a) and (b) penalties cannot be assessed in addition to the aiding and abetting penalty.

FAILURES UNDER §6695Any tax return preparer who fails to take certain actions may be assessed other penalties with respect to the preparation of tax returns for other persons. In the case of any failure relating to a return or claim for refund filed in 2022 (generally 2021 tax returns filed in 2022), the penalty amounts under §6695 are:

Penalty of $50 for each occurrence up to a maximum of $27,000 a year unless it is shown that such failure is due to reasonable cause and not due to willful neglect:

§6695(a) Failure to furnish copy of return to taxpayer – The tax preparer must furnish a completed copy of the return or claim for refund to the taxpayer no later than the time it is presented for the taxpayer’s signature.

§6695(b) Failure to sign return – The tax preparer must sign a tax return or claim for refund if the tax preparer has primary responsibility for the overall substantive accuracy of the preparation of the tax return or claim for refund.

§6695(c) Failure to furnish identifying number – A tax return preparer must obtain and exclusively use a PTIN, rather than a social security number (SSN), as the identifying number to be included with the tax return preparer’s signature on a tax return or claim for refund.

§6695(d) Failure to retain copy or list – A tax return preparer must keep a copy of the tax return, or retain, on a list, the name and taxpayer identification number of the taxpayer for whom the return was prepared. The records must be available for inspection for the 3-year period following the close of the return period during which the return or claim for refund was presented for signature to the taxpayer. A “return period” is the 12-month period beginning on July 1 of each year and ending on June 30.

§6695(e) Failure to file correct information returns – Each person who employs (or engages) one or more income tax return preparers to prepare any return of tax is responsible for retaining a record of the name, taxpayer identification number, and principal place of work during the return period of each income tax return preparer employed (or engaged) by the person at any time during that period. The record must be available for inspection upon request by the district director for the 3-year period following the close of the return period. (A penalty of $50 per return and $50 per item in return.)

§6695(f) Negotiation of check – Any tax return preparer who endorses or otherwise negotiates (directly or through an agent) a refund check (including an electronic version of a check) issued to the taxpayer (other than the preparer), shall pay a penalty of $545 with respect to each check. The penalty does not vary based on how much compensation the preparer receives from the taxpayer, the amount of the refund check, or the direct deposit. The penalty applies to a tax return preparer who directs the IRS to deposit a taxpayer's refund into a bank account in the preparer's name or into a bank account under the preparer's control. The preparer may not endorse or negotiate a check for a taxpayer even though the preparer was designated as the taxpayer's representative on a Form 2848, Power of Attorney. A tax return preparer may deposit a refund check into the taxpayer’s account. (A penalty of $545 per check, with no limit to a maximum penalty.)

A tax return preparer will not be considered to have endorsed or otherwise negotiated a check as a result of having affixed the taxpayer’s name to a refund check for the purpose of depositing the check into an account in the name of the taxpayer or in the joint names of the taxpayer and one or more other persons (excluding the tax return preparer). See Treas. Reg. 1.6695-1(f)(1).

TIP: Taxpayers sometimes request that their refunds be direct deposited into a bank account in the preparer’s name or into a bank account under the preparer’s control when taxpayers do not have their own bank account. Even if a

22 Tax Preparer Sanctions and Penalties

•

•

•

taxpayer has requested the direct deposit to be made in this manner, the preparer is still subject to the IRC 6695(f) penalty for complying with the request.

§6695(g) Failure to be diligent in determining eligibility for certain tax benefits – Any return preparer who fails to comply with due diligence requirements imposed to determine eligibility for, or the amount of, the credit allowable shall pay a penalty of $545 for each failure. Those who prepare returns that claim Earned Income Credit (EIC), American Opportunity Tax Credit (AOTC), Child Tax Credit (CTC) (including the Additional Child Tax Credit (ACTC) and the Credit for Other Dependents (ODC)), and Head of Household (HOH) filing status must not only ask all the questions required on Form 8867, Paid Preparer's Due Diligence Checklist, but must also ask additional questions when information seems incorrect, inconsistent or incomplete. In addition, the preparer must verify identity, prepare a computational checklist (Form 8867 or equivalent), and meet a recordkeeping requirement. (A penalty of $545 per failure, with no limit to a maximum penalty.)

A separate penalty applies with respect to each eligibility for, and amount of, credit claimed on a return or claim for refund for which the due diligence requirements are not satisfied. The $545 penalty applies to each failure.

SAFEGUARDING TAXPAYER INFORMATIONTax return preparers must obtain consent to use tax return information before tax return information is used and before returns are provided to the taxpayer for signature. Internal Revenue Code §7216 is a criminal provision enacted by the U.S. Congress in 1971 that prohibits preparers of tax returns from knowingly or recklessly disclosing or using tax return information. A convicted preparer may be fined not more than $1,000 or imprisoned not more than one year or both, for each violation.

In addition to criminal penalties, a civil penalty of $250 for each unauthorized disclosure or use of tax return information by a tax return preparer is imposed by § 6713. The total amount imposed on any person under § 6713 shall not exceed $10,000 in any calendar year.

Internal Revenue Code §6713 imposes a civil penalty of $250 on any person who is engaged in the business of preparing, or providing services in connection with the preparation of returns of tax, or any person who for compensation prepares a return for another person, and who:

Discloses any information furnished to him for, or in connection with, the preparation of any such return, or

Uses any such information for any purpose other than to prepare, or assist in preparing, any such return. Imposition of the penalty under Internal Revenue Code §6713 does not require that the disclosure be knowing or reckless as it does under Internal Revenue Code §7216.

Generally, unless otherwise specified, a written consent is effective for a period of one year from the date the taxpayer signs the consent. Disclosing tax return information to another tax preparer within the United States that is assisting in the preparation of the return generally does not require the consent of the taxpayer.

PROVIDING IRS WITH FRAUDULENT INFORMATION OR DOCUMENTSA criminal fine of $10,000 for individuals, and $50,000 for corporations, and up to one year in prison is applied under section 7207, which penalizes anyone who willfully delivers or discloses to the IRS any information knowing to be fraudulent or false as to any material matter.

PAYMENTThe tax preparer has 30 days to pay the penalty upon receipt of a demand for payment from the IRS. The preparer may elect to pay at least 15% of the amount of the penalty and file a claim for refund. If the claim for refund is denied

Prompt Disposition 23

(or 6 months have passed), the preparer has 30 more days to begin a proceeding in the appropriate U.S. district court for determination of liability.

EXAMPLES OF VIOLATIONS SUBJECT TO SANCTION

PROMPT DISPOSITIONTax practitioner Lawrence Slick has a client that is being audited by the IRS. Lawrence is representing his client in the matter and believes all the factual matters related to the audit can easily be resolved in 4 to 6 weeks. From a buddy that works at the IRS, Lawrence learns that the auditor assigned to his client’s case is set to retire in three months. Lawrence thinks that if he can drag his feet on the audit by raising a series of unreasonable objections until after the IRS agent retires, he might be able to get a new agent who would be more lenient. Unfortunately, for Lawrence, the only thing the delay will result in is a complaint filed by the Office of Professional Responsibility (OPR) against Lawrence for purposely delaying the conclusion of the audit, which is a violation of Section 10.23.

DUE DILIGENCEWillow Weed was a CPA who helped others file their federal tax returns every year. However, for whatever reason, Willow had failed to file her own tax returns for the past five years. As willfully failing to file your own return is a violation of the due diligence requirements, the OPR filed a complaint against Willow. She faces disciplinary action because of this “oversight.”

DUE DILIGENCE IN TAX RETURN PREPARATIONCharlie Gullible is a tax advisor who prepared individual and corporate tax returns. Betty and Barney Polson asked Charlie to prepare the tax return for their corporation, for which they were also shareholders. Charlie asked the Polsons questions about the company’s income and expenses, and although he believed some of the information provided didn’t seem factual, he prepared and submitted the returns to the IRS anyway. The IRS flagged the Polsons return and called them in for an audit. During the investigation, the Polsons admitted to “fudging” their income.

The OPR filed a complaint against Charlie alleging he failed to exercise due diligence under Section 10.22 when he did not determine the correctness of the representations he made to the IRS on the tax returns of the Polsons. Additionally, the OPR claimed Charlie failed to comply with the requirement to advise his clients of potential penalties and opportunities to avoid such penalties by disclosure, contained in Section 10.34(c). Charlie was found in violation and disciplined.

DISREPUTABLE CONDUCTGeorge Glutton was employed by ACME Accounting. While employed with ACME, George decided to make a little money on the side by preparing income tax returns for his friends and neighbors. These individuals were not clients of ACME, but that didn’t stop George from using the company’s tax preparation software and laptop computer to prepare the returns. Unfortunately, George forgot to remove ACME’s name from the paid preparer section of the tax return before he gave the copies to his friends. He then billed his friends using ACME invoices with his name only and kept the fees he received for these services. George thought this practice was fine and that his friends knew ACME was not responsible for the tax returns, even though the company’s name was displayed in the tax preparer section. He thought wrong.

24 Recent Examples of Abusive Return Preparer Investigations

RECENT EXAMPLES OF ABUSIVE RETURN PREPARER INVESTIGATIONS

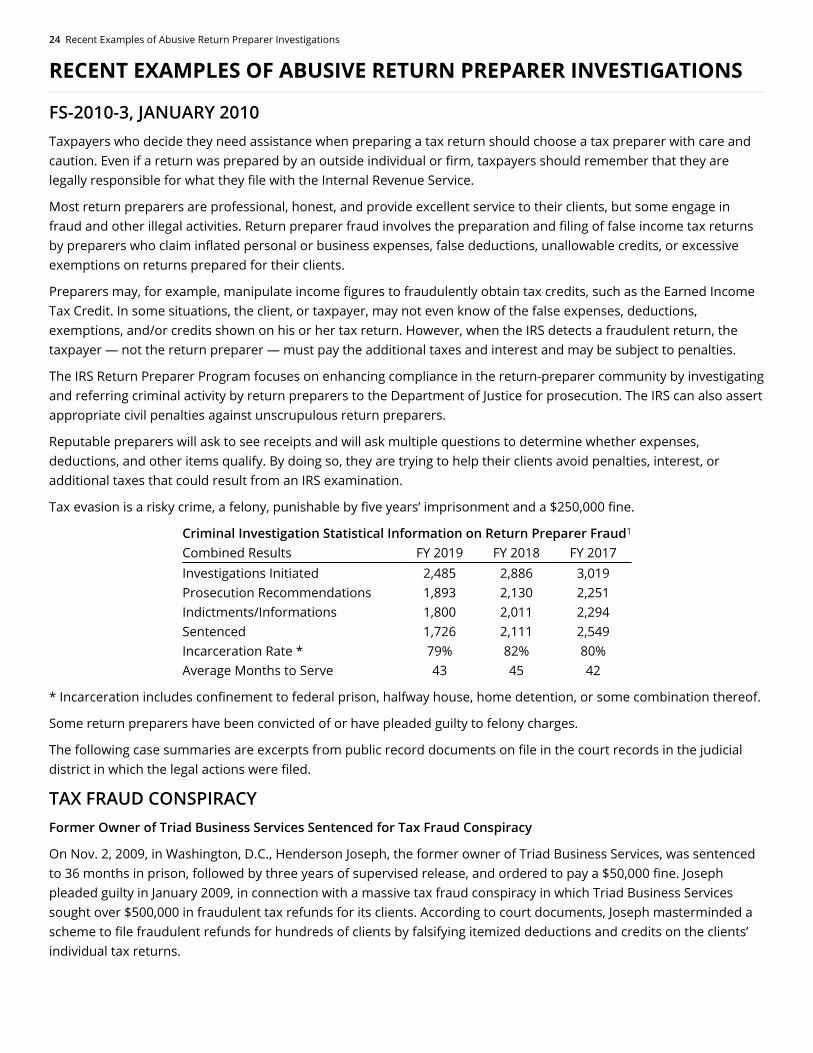

FS-2010-3, JANUARY 2010Taxpayers who decide they need assistance when preparing a tax return should choose a tax preparer with care and caution. Even if a return was prepared by an outside individual or firm, taxpayers should remember that they are legally responsible for what they file with the Internal Revenue Service.

Most return preparers are professional, honest, and provide excellent service to their clients, but some engage in fraud and other illegal activities. Return preparer fraud involves the preparation and filing of false income tax returns by preparers who claim inflated personal or business expenses, false deductions, unallowable credits, or excessive exemptions on returns prepared for their clients.

Preparers may, for example, manipulate income figures to fraudulently obtain tax credits, such as the Earned Income Tax Credit. In some situations, the client, or taxpayer, may not even know of the false expenses, deductions, exemptions, and/or credits shown on his or her tax return. However, when the IRS detects a fraudulent return, the taxpayer — not the return preparer — must pay the additional taxes and interest and may be subject to penalties.

The IRS Return Preparer Program focuses on enhancing compliance in the return-preparer community by investigating and referring criminal activity by return preparers to the Department of Justice for prosecution. The IRS can also assert appropriate civil penalties against unscrupulous return preparers.

Reputable preparers will ask to see receipts and will ask multiple questions to determine whether expenses, deductions, and other items qualify. By doing so, they are trying to help their clients avoid penalties, interest, or additional taxes that could result from an IRS examination.

Tax evasion is a risky crime, a felony, punishable by five years’ imprisonment and a $250,000 fine.

Criminal Investigation Statistical Information on Return Preparer FraudCombined Results FY 2019 FY 2018 FY 2017Investigations Initiated 2,485 2,886 3,019Prosecution Recommendations 1,893 2,130 2,251Indictments/Informations 1,800 2,011 2,294Sentenced 1,726 2,111 2,549Incarceration Rate * 79% 82% 80%Average Months to Serve 43 45 42

* Incarceration includes confinement to federal prison, halfway house, home detention, or some combination thereof.

Some return preparers have been convicted of or have pleaded guilty to felony charges.

The following case summaries are excerpts from public record documents on file in the court records in the judicial district in which the legal actions were filed.

TAX FRAUD CONSPIRACYFormer Owner of Triad Business Services Sentenced for Tax Fraud Conspiracy

On Nov. 2, 2009, in Washington, D.C., Henderson Joseph, the former owner of Triad Business Services, was sentenced to 36 months in prison, followed by three years of supervised release, and ordered to pay a $50,000 fine. Joseph pleaded guilty in January 2009, in connection with a massive tax fraud conspiracy in which Triad Business Services sought over $500,000 in fraudulent tax refunds for its clients. According to court documents, Joseph masterminded a scheme to file fraudulent refunds for hundreds of clients by falsifying itemized deductions and credits on the clients’ individual tax returns.

1

$1 Million Tax Fraud 25

$1 MILLION TAX FRAUDFormer Tax Preparer Sentenced for $1 Million Tax Fraud

On Oct. 16, 2009, in Kansas City, Donald Bushnell, a former tax preparer, was sentenced to 36 months in prison for fraudulently preparing nearly 300 tax returns that falsely claimed more than $1 million in business losses for his clients. Bushnell prepared 272 false and fraudulent federal tax returns from January 9, 2001, to June 6, 2005, for a total tax loss of approximately $1,088,720. Bushnell’s criminal conduct caused dozens of taxpayers to incur substantial costs, ranging between $200 and $400 per return, for interest and penalties.

DAUGHTERS OF CALIFORNIA Return Preparers Each Sentenced to 72 Months in Federal Prison

On Oct. 5, 2009, in Riverside, Calif, Karen Denise Berry of San Bernardino, Calif., and Carla Denine Berry of Rialto, Calif., the daughters of a patriarch of an income tax preparation business, were each sentenced to serve 72 months in federal prison and three years of supervised release. They were also ordered to pay $14 million in restitution to the IRS. Their father, Matthew Carl Berry, a Rialto tax return preparer, was previously sentenced to serve 108 months in federal prison, 36 months on supervised release, and ordered to pay over $15 million in restitution to the IRS, after having been previously convicted at trial on charges that he conspired with others to defraud the Internal Revenue Service and filed false personal income tax returns for the years 2001, 2002, and 2004. Karen Denise Berry and Carla Denine Berry, along with their father, Matthew Berry, were found guilty of conspiring with Ivan Taylor Johnson, of San Bernardino, Calif., and Valerie Madel Dixon, of Rialto to impede and obstruct the lawful functions of the Internal Revenue Service. Karen Berry and Carla Berry pleaded guilty before trial to various charges including conspiracy to defraud the IRS, aiding and assisting in the preparation of false tax returns, and subscribing to a false tax return. According to court papers, the false returns Berry prepared for clients, in conjunction with the returns prepared by Karen Berry, Carla Berry, Johnson and Dixon, caused losses of more than $45,000,000 in tax revenue to the IRS. Johnson and Dixon previously pleaded guilty to charges contained in the indictment. Johnson was sentenced to 35 months imprisonment followed by three years of supervised release and ordered to pay restitution to the IRS in the amount of $19,034,901. Dixon was sentenced to five years’ probation, including 10 months home detention, and ordered to pay restitution to the IRS of $19,034,901.

30 MONTHS FOR TAX FRAUDFlorida Tax Preparer Sentenced to 30 Months for Tax Fraud

On Aug. 6, 2009, in Orlando, Fla., Jean Marie Boursiquot was sentenced to 30 months in prison and ordered to pay $149,456 in restitution. Boursiquot pleaded guilty on May 21, 2009 to his role in a conspiracy to defraud the government. According to court documents, Boursiquot ran his own tax preparation company and prepared tax returns and amended tax returns for transient Haitian immigrants in Florida. Boursiquot had the IRS mail him the refund checks directly and deposited the checks into his business account. In 2002, Boursiquot received nearly $400,000 from the IRS and pocketed more than $250,000 of the money that was intended for his clients. In 2003, Boursiquot received more than $500,000 from the IRS and kept more than $400,000 of his clients’ money. Boursiquot did not file a tax return for the 2002 tax year and on his 2003 tax return he only claimed $41,341 in income.

FILING FALSE RETURNSTax Preparers Sentenced to Prison for Filing False Returns

On June 23, 2009, in Riverside, Calif., Matthew Carl Berry, of Rialto, Calif., was sentenced to nine years in prison after having been previously convicted on charges that he conspired with others to defraud the government and filed false personal income tax returns for the years 2001, 2002 and 2004. In addition to prison, Berry was ordered to pay $15,418,393 in restitution to the Internal Revenue Service and to spend three years on supervised release following his

26 Best Practices for Tax Advisors

•

•

•

•

•

•

•

release from prison. In addition to the conspiracy charges, the jury found Berry guilty of willfully filing false income tax returns with the IRS for the 2001, 2002 and 2004 tax years.

Louisiana Tax Preparer Sentenced for Preparing False Tax Returns

Dec. 11, 2008, in Shreveport, La., Clementine Rainey, a former tax preparer for Quick Tax in Shreveport, was sentenced to 21 months in prison and ordered to pay $111,000 in restitution for preparing false tax returns. Rainey pleaded guilty August 22, 2008, to one count of aiding the preparation of false returns. According to court documents, she admitted to preparing and filing false individual income tax returns for taxpayers for the years 2005 through 2007 by submitting fictitious W-2 employer and wage information.

Two Kenyan Women Sentenced for $15 Million Tax Fraud Conspiracy

On Nov. 13, 2008, in Kansas City, Loretta Wavinya and her sister, Lillian Nzongi, were sentenced to prison terms of 168 months and 70 months, respectively, for their roles in a multi-million dollar conspiracy to defraud the IRS. The Kenyan nationals lived in the Kansas City area and were involved in a wire fraud scheme that involved stealing the identities of hundreds of victims, primarily nursing home residents, which were used to seek more than $15 million in fraudulent federal tax refunds. Wavinya, a tax preparer and radiology technician who visited patients on-site at multiple nursing homes, pleaded guilty in June 2008 to using stolen identities to file more than 540 fraudulent federal tax returns using the names of more than 500 identity theft victims. The conspirators filed up to six state tax returns simultaneously with each federal return, causing a loss to at least 27 states.

BEST PRACTICES FOR TAX ADVISORS

BEST PRACTICESPractitioners should provide clients with the highest quality representation concerning federal tax issues by adhering to best practices in providing advice and in preparing or assisting in the preparation of a submission to the Internal Revenue Service. Best practices include the following:

Communicating clearly with the client regarding the terms of the engagement.

Establishing the facts, determining which facts are relevant, evaluating the reasonableness of any assumptions or representations, relating the applicable law to the relevant facts, and arriving at a conclusion supported by the law and the facts. The practitioner generally may rely in good faith without verification upon information furnished by the client. The practitioner may not, however, ignore the implications of information furnished to, or actually known by, the practitioner, and must make reasonable inquiries if the information as furnished appears to be incorrect, inconsistent with an important fact or another factual assumption, or incomplete.

Advising the client regarding the import of the conclusions reached, including, for example, whether a taxpayer may avoid accuracy-related penalties under the Internal Revenue Code if a taxpayer acts in reliance on the advice.

Acting fairly and with integrity in practice before the Internal Revenue Service.

RECORDKEEPINGIn general, practitioners must keep records for a period of three years. They must:

Keep records of completed CPE for four years following the date of renewal of enrollment