Embed Size (px)

Citation preview

EU audit legislationUnderstanding the legislation

and how it will affect you

October 2014

2 EU audit legislation | Understanding the legislation and how it will affect you

Key points• New European Union (EU) audit

legislation requires certain companies in the EU to rotate their statutory auditor and restricts the non-audit services they can obtain from their auditor. The legislation is wide-ranging and includes many other new requirements.

• Multinational companies headquartered outside the EU need to be aware of the requirements because they also apply to EU subsidiaries that meet the definition of an EU Public Interest Entity.

• The legislation includes a large number of options for EU Member States, which will lead to inconsistent application and a patchwork of different national requirements.

• Complying with the legislation will be challenging and will require advance planning. Companies should take steps now to understand if and how the legislation will affect them or their EU subsidiaries.

3

Who is this guide for?This guide is for all companies with operations in the EU, regardless of where in the world they are headquartered. It is designed to help companies understand the new EU audit legislation and how it may affect them.

What has changed?On 16 June 2014, new EU audit legislation entered into force. The legislation is wide-ranging and includes a mandatory audit firm rotation for EU Public Interest Entities (PIEs) and significant restrictions on non-audit services an EU PIE can obtain from its auditor.

EU Member States have until June 2016 to implement the legislation into their national laws, although the requirements for audit firm rotation are introduced over a longer period. The legislation includes a large number of Member State options, which will lead to inconsistent application and create a patchwork of different national requirements. We do not yet have a complete picture. Complying with the legislation will require advance planning, however, and companies should take steps now to understand if and how the legislation will affect them or their EU subsidiaries.

Will the legislation affect my company?The legislation is generally directed at audits of EU PIEs. The legislation also applies to EU PIE subsidiaries of companies headquartered outside the EU. Therefore, all companies with EU operations, wherever headquartered, will have to review their group structure to establish whether they are an EU PIE or have an EU PIE in their group. Many large multinational groups are likely to have more than one EU PIE.

The rest of this guide helps you determine if your company is an EU PIE or if you have an EU PIE in your group.

“All companies with EU operations, wherever headquartered, will have to establish whether they are an EU Public Interest Entity or have an EU Public Interest Entity in their group.”{ }

1 In the 2006 EU Statutory Audit Directive. Other, different PIE definitions exist around the world, notably that of the International Ethics Standards Board for Accountants (IESBA). For more information, go to the last page of this guide.

Understanding if your company is an EU PIE or if you have an EU PIE in your groupThe PIE concept is not new; an EU PIE definition was already included in the Statutory Audit Directive of 2006.1 The underlying EU PIE definition has not changed in the new legislation, although its scope has been expanded. As with the 2006 definition, the new legislation continues to allow the 28 EU Member States to supplement the PIE definition to include certain additional companies. Member States have until 16 June 2016 to bring their existing PIE definition into line with the new legislation, and we do not yet know how each Member State will do so. However, we do know how Member States have applied the existing 2006 definition, and this provides some guidance for the future.

Therefore, determining if you are an EU PIE is a two-step process:

1. Determine if you are covered by the baseline EU PIE definition (Part 1 of this guide)

2. Understand how the Member State in which you are incorporated has implemented the existing EU PIE definition (Part 2 of this guide)

Considerations for groups of companies The EU PIE definition applies to individual entities. There are no separate rules for groups of companies. Many large multinational groups are likely to have more than one PIE in the EU. In the case of a group of companies, the questions in part 1 should be answered from the perspective of each individual group company.

4 EU audit legislation | Understanding the legislation and how it will affect you

Where are you governed, and where are your securities issued and admitted?a. Are you governed by the law of an EU Member State?

• References to companies that are “governed by the law” of a Member State are understood to mean companies that are legally incorporated in that Member State.

• In some civil law regimes, domestic provisions mean that corporate law applies to companies that have their operational headquarters in that country, even though that company is incorporated elsewhere. Any company to which such a provision applied would also be regarded as governed by the laws of that Member State.

• Note that some uncertainty remains around the meaning of “governed by the law.” The interpretation above should be treated as draft and will be updated as more information becomes available.

b. Have you issued transferable securities?

• Transferable securities are classes of securities that are negotiable on the capital market, with the exception of instruments of payment.

• For a definition, see Appendix 1.

c. Are the transferable securities admitted to trading on a “regulated market” in an EU Member State?

• Regulated markets are defined in point 14 of Article 4(1) of Markets in Financial Instruments Directive (MiFID). Not all markets in the EU fall within this definition. For a definition and a list of Regulated Markets, see Appendix 2.

If the answer to (a), (b) and (c) is yes, you are an EU PIE. If the answer to any of (a), (b) or (c) is no, go to the next question.

Considerations for branches and funds • As explained above, credit institutions and insurance

undertakings in the EU are PIEs. Where an EU credit institution or an EU insurance undertaking has branches anywhere inside the EU, the European Commission has said that these will not qualify as EU PIEs. However, we recommend companies exercise caution and seek advice.

• In the Commission’s original proposals, AIFs and Undertakings for Collective Investments in Transferable Securities (UCITS) were included in the new PIE definition. However, as part of the EU legislative process, AIFs and UCITS were removed from the final PIE definition. However, where an AIF or UCITS is governed by the law of an EU Member State and has transferable securities admitted to trading on a regulated market in the EU, they will still be PIEs.

Part 1 Is my company covered by the baseline EU PIE definition?

Are you a “credit institution”?

• A credit institution is an undertaking, the business of which is to take deposits or other repayable funds from the public and to grant credits for its own account.

• Note that the EU audit legislation excludes from the EU PIE definition certain credit institutions. For a list and definition, see Appendix 3.

If yes, you are an EU PIE. If no, go to the next question.

1 2

Are you an “insurance undertaking”?

• An insurance undertaking includes:• Direct insurers• Life insurers • Undertakings carrying on reinsurance business

• Insurance broking is not within the definition, but a group “captive” insurer would be if it was established in the EU.

• For a definition, see Appendix 4.

If yes, you are an EU PIE. If no, go to Part 2.

Even if the answer to any of the questions in this section is no, you could still be a PIE depending on how the Member State in which you are located has implemented the EU PIE definition. Go to Part 2.

3

5

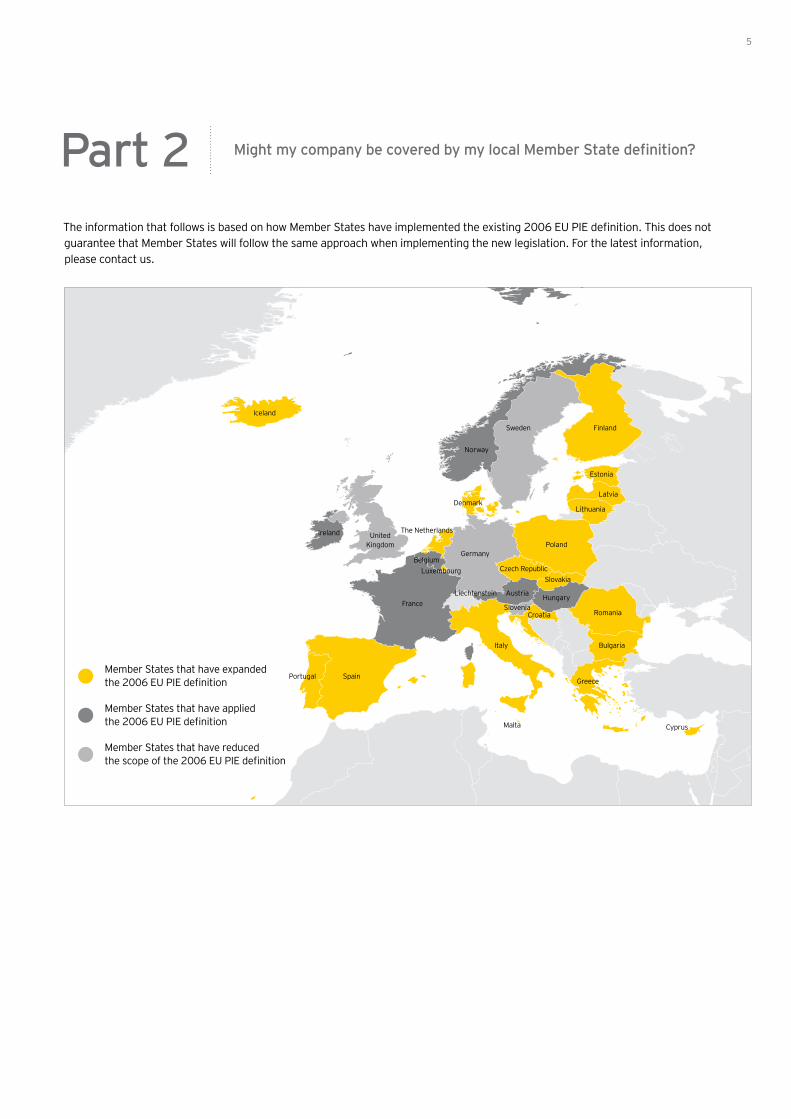

The information that follows is based on how Member States have implemented the existing 2006 EU PIE definition. This does not guarantee that Member States will follow the same approach when implementing the new legislation. For the latest information, please contact us.

Member States that have expanded the 2006 EU PIE definition

Member States that have appliedthe 2006 EU PIE definition

Member States that have reduced the scope of the 2006 EU PIE definition

Iceland

Denmark

The Netherlands

SpainPortugal

Italy

Romania

Bulgaria

Greece

CyprusMalta

Poland

Lithuania

Latvia

Estonia

FinlandSweden

Norway

Czech Republic

Austria

Slovakia

Hungary

CroatiaSloveniaFrance

Ireland

BelgiumGermany

Luxembourg

Liechtenstein

UnitedKingdom

Part 2 Might my company be covered by my local Member State definition?

6 EU audit legislation | Understanding the legislation and how it will affect you

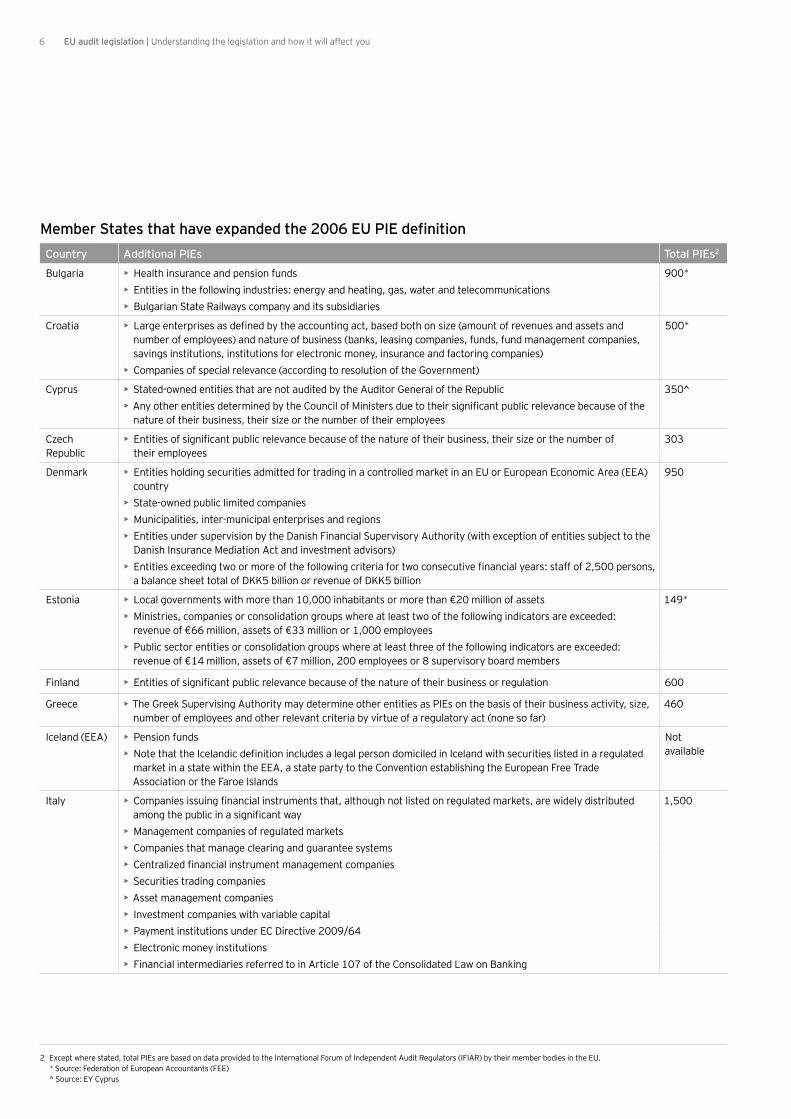

Member States that have expanded the 2006 EU PIE definitionCountry Additional PIEs Total PIEs2

Bulgaria • Health insurance and pension funds• Entities in the following industries: energy and heating, gas, water and telecommunications• Bulgarian State Railways company and its subsidiaries

900*

Croatia • Large enterprises as defined by the accounting act, based both on size (amount of revenues and assets and number of employees) and nature of business (banks, leasing companies, funds, fund management companies, savings institutions, institutions for electronic money, insurance and factoring companies)

• Companies of special relevance (according to resolution of the Government)

500*

Cyprus • Stated-owned entities that are not audited by the Auditor General of the Republic• Any other entities determined by the Council of Ministers due to their significant public relevance because of the

nature of their business, their size or the number of their employees

350^

Czech Republic

• Entities of significant public relevance because of the nature of their business, their size or the number of their employees

303

Denmark • Entities holding securities admitted for trading in a controlled market in an EU or European Economic Area (EEA) country

• State-owned public limited companies• Municipalities, inter-municipal enterprises and regions• Entities under supervision by the Danish Financial Supervisory Authority (with exception of entities subject to the

Danish Insurance Mediation Act and investment advisors)• Entities exceeding two or more of the following criteria for two consecutive financial years: staff of 2,500 persons,

a balance sheet total of DKK5 billion or revenue of DKK5 billion

950

Estonia • Local governments with more than 10,000 inhabitants or more than €20 million of assets• Ministries, companies or consolidation groups where at least two of the following indicators are exceeded:

revenue of €66 million, assets of €33 million or 1,000 employees• Public sector entities or consolidation groups where at least three of the following indicators are exceeded:

revenue of €14 million, assets of €7 million, 200 employees or 8 supervisory board members

149*

Finland • Entities of significant public relevance because of the nature of their business or regulation 600

Greece • The Greek Supervising Authority may determine other entities as PIEs on the basis of their business activity, size, number of employees and other relevant criteria by virtue of a regulatory act (none so far)

460

Iceland (EEA) • Pension funds• Note that the Icelandic definition includes a legal person domiciled in Iceland with securities listed in a regulated

market in a state within the EEA, a state party to the Convention establishing the European Free Trade Association or the Faroe Islands

Not available

Italy • Companies issuing financial instruments that, although not listed on regulated markets, are widely distributed among the public in a significant way

• Management companies of regulated markets• Companies that manage clearing and guarantee systems• Centralized financial instrument management companies• Securities trading companies• Asset management companies• Investment companies with variable capital• Payment institutions under EC Directive 2009/64• Electronic money institutions• Financial intermediaries referred to in Article 107 of the Consolidated Law on Banking

1,500

2 Except where stated, total PIEs are based on data provided to the International Forum of Independent Audit Regulators (IFIAR) by their member bodies in the EU. * Source: Federation of European Accountants (FEE) ^ Source: EY Cyprus

7

Country Additional PIEs Total PIEs2

Latvia • Listed entities • Credit institutions • Insurance and reinsurance undertakings • Asset management companies, AIF managers • Non-EU insurance company’s branches and non-EU reinsurer’s branches or private pension funds that provide

financial, insurance or reinsurance services

75*

Lithuania • Public companies whose securities are traded in the regulated market of the Republic of Lithuania and any other member state

• The bank and the Central Credit Union• Brokerage houses• Investment companies with variable capital and closed-end investment funds whose property management has

not been transferred to the management firm • Firms of management of undertakings of collective investment and pension fund(s)• Insurance undertakings and reinsurance undertakings• Central securities depository of Lithuania and Vilnius Securities Exchange

154*

Luxembourg • National regulation may also designate entities of significant public relevance because of the nature of their business, their size or the number of their employees (none so far)

450

Malta • Such other entities as may be prescribed by the Accountancy Board (none so far) 125

The Netherlands

• The Government may also designate other entities that are of significant public relevance because of the nature of their business or their size as PIEs

1,100

Poland • Issuers of securities allowed to trading in the regulated market of an EU Member State, excluding local self-government units, with their registered offices in the territory of the Republic of Poland

• National banks, branch offices of credit institutions and branch offices of foreign banks, as defined in the Banking Law

• Cooperative savings and loan associations, as defined in the act on cooperative savings and loan associations• Insurance companies and main branch offices of insurance companies as well as reinsurance companies, as

defined in the act on insurance activity• Electronic money institutions, as defined in the act on electronic payment instruments• Open-end pension funds and managing companies of pension funds, as defined in the act on the organization and

operation of pension funds• Open investment funds, specialized open investment funds and closed investment funds whose public investment

certificates have not been allowed to trading in the regulated market, as defined in the act on investment funds• Entities running brokerage business, excluding entities running the activities exclusively related to receiving and

transmitting orders of purchase or sale of financial instruments or in the scope of investment advisory services, as defined in the act on trading in financial instruments

500*

8 EU audit legislation | Understanding the legislation and how it will affect you

Country Additional PIEs Total PIEs2

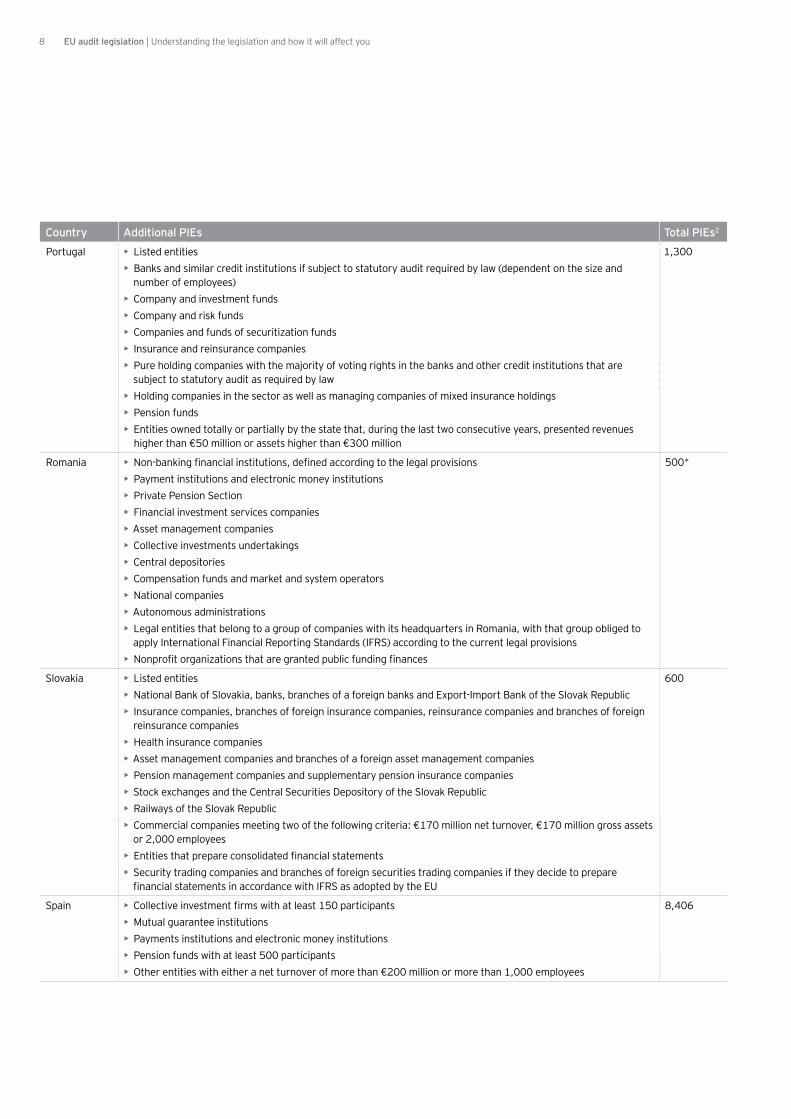

Portugal • Listed entities• Banks and similar credit institutions if subject to statutory audit required by law (dependent on the size and

number of employees)• Company and investment funds• Company and risk funds• Companies and funds of securitization funds• Insurance and reinsurance companies• Pure holding companies with the majority of voting rights in the banks and other credit institutions that are

subject to statutory audit as required by law • Holding companies in the sector as well as managing companies of mixed insurance holdings• Pension funds• Entities owned totally or partially by the state that, during the last two consecutive years, presented revenues

higher than €50 million or assets higher than €300 million

1,300

Romania • Non-banking financial institutions, defined according to the legal provisions• Payment institutions and electronic money institutions• Private Pension Section• Financial investment services companies• Asset management companies• Collective investments undertakings• Central depositories• Compensation funds and market and system operators• National companies• Autonomous administrations• Legal entities that belong to a group of companies with its headquarters in Romania, with that group obliged to

apply International Financial Reporting Standards (IFRS) according to the current legal provisions• Nonprofit organizations that are granted public funding finances

500*

Slovakia • Listed entities • National Bank of Slovakia, banks, branches of a foreign banks and Export-Import Bank of the Slovak Republic • Insurance companies, branches of foreign insurance companies, reinsurance companies and branches of foreign

reinsurance companies • Health insurance companies • Asset management companies and branches of a foreign asset management companies • Pension management companies and supplementary pension insurance companies • Stock exchanges and the Central Securities Depository of the Slovak Republic • Railways of the Slovak Republic• Commercial companies meeting two of the following criteria: €170 million net turnover, €170 million gross assets

or 2,000 employees • Entities that prepare consolidated financial statements • Security trading companies and branches of foreign securities trading companies if they decide to prepare

financial statements in accordance with IFRS as adopted by the EU

600

Spain • Collective investment firms with at least 150 participants• Mutual guarantee institutions• Payments institutions and electronic money institutions• Pension funds with at least 500 participants• Other entities with either a net turnover of more than €200 million or more than 1,000 employees

8,406

9

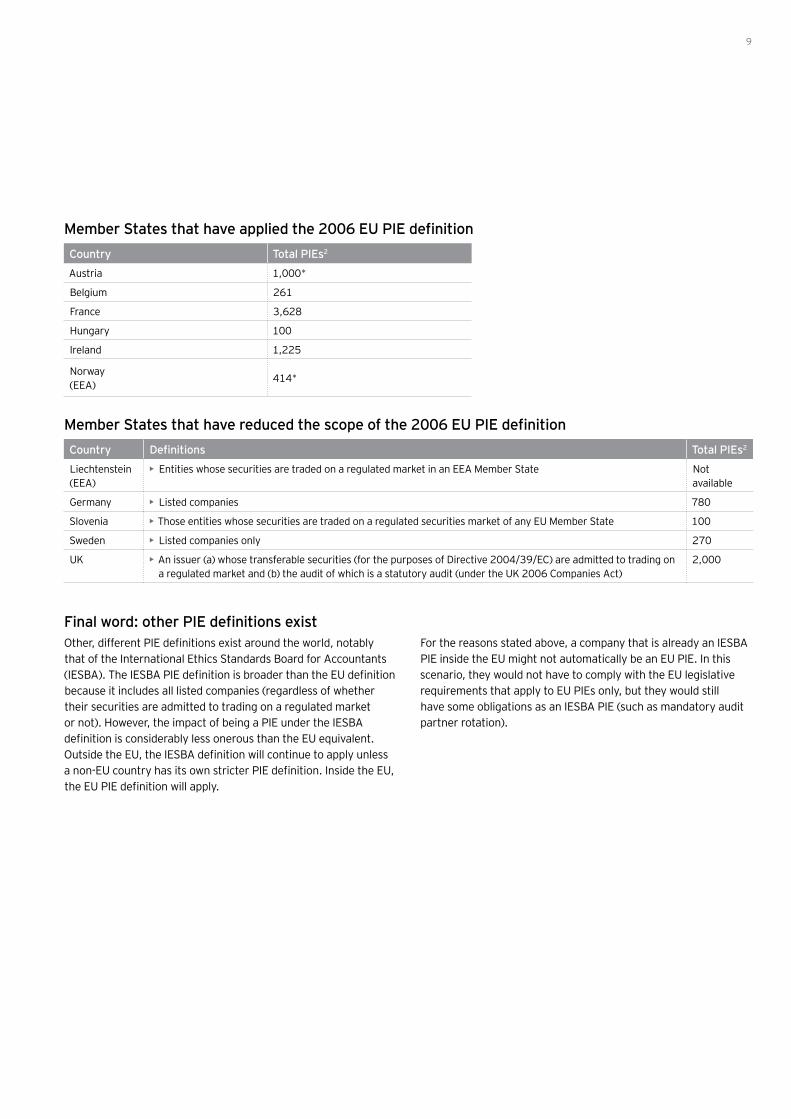

Member States that have applied the 2006 EU PIE definitionCountry Total PIEs2

Austria 1,000*

Belgium 261

France 3,628

Hungary 100

Ireland 1,225

Norway (EEA)

414*

Member States that have reduced the scope of the 2006 EU PIE definitionCountry Definitions Total PIEs2

Liechtenstein (EEA)

• Entities whose securities are traded on a regulated market in an EEA Member State Not available

Germany • Listed companies 780

Slovenia • Those entities whose securities are traded on a regulated securities market of any EU Member State 100

Sweden • Listed companies only 270

UK • An issuer (a) whose transferable securities (for the purposes of Directive 2004/39/EC) are admitted to trading on a regulated market and (b) the audit of which is a statutory audit (under the UK 2006 Companies Act)

2,000

Final word: other PIE definitions existOther, different PIE definitions exist around the world, notably that of the International Ethics Standards Board for Accountants (IESBA). The IESBA PIE definition is broader than the EU definition because it includes all listed companies (regardless of whether their securities are admitted to trading on a regulated market or not). However, the impact of being a PIE under the IESBA definition is considerably less onerous than the EU equivalent. Outside the EU, the IESBA definition will continue to apply unless a non-EU country has its own stricter PIE definition. Inside the EU, the EU PIE definition will apply.

For the reasons stated above, a company that is already an IESBA PIE inside the EU might not automatically be an EU PIE. In this scenario, they would not have to comply with the EU legislative requirements that apply to EU PIEs only, but they would still have some obligations as an IESBA PIE (such as mandatory audit partner rotation).

10 EU audit legislation | Understanding the legislation and how it will affect you

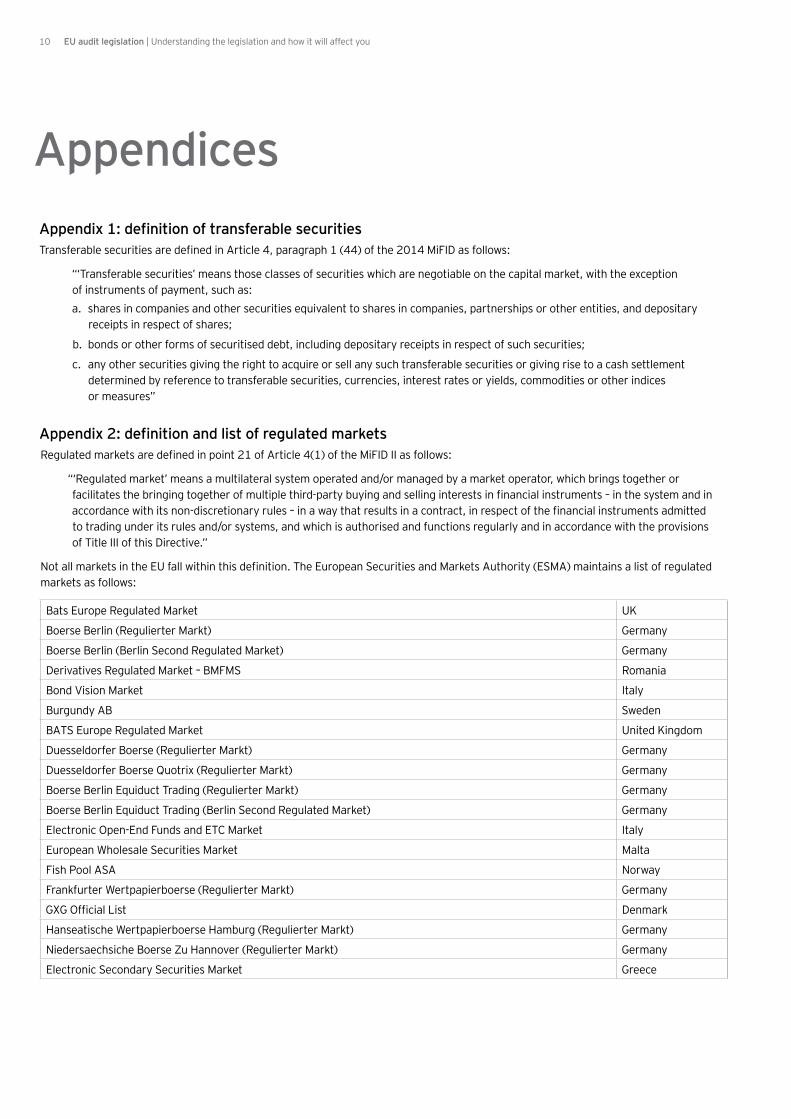

Appendix 1: definition of transferable securitiesTransferable securities are defined in Article 4, paragraph 1 (44) of the 2014 MiFID as follows:

“‘Transferable securities’ means those classes of securities which are negotiable on the capital market, with the exception of instruments of payment, such as:a. shares in companies and other securities equivalent to shares in companies, partnerships or other entities, and depositary

receipts in respect of shares;

b. bonds or other forms of securitised debt, including depositary receipts in respect of such securities;

c. any other securities giving the right to acquire or sell any such transferable securities or giving rise to a cash settlement determined by reference to transferable securities, currencies, interest rates or yields, commodities or other indices or measures”

Appendix 2: definition and list of regulated markets Regulated markets are defined in point 21 of Article 4(1) of the MiFID II as follows:

“‘Regulated market’ means a multilateral system operated and/or managed by a market operator, which brings together or facilitates the bringing together of multiple third-party buying and selling interests in financial instruments – in the system and in accordance with its non-discretionary rules – in a way that results in a contract, in respect of the financial instruments admitted to trading under its rules and/or systems, and which is authorised and functions regularly and in accordance with the provisions of Title III of this Directive.”

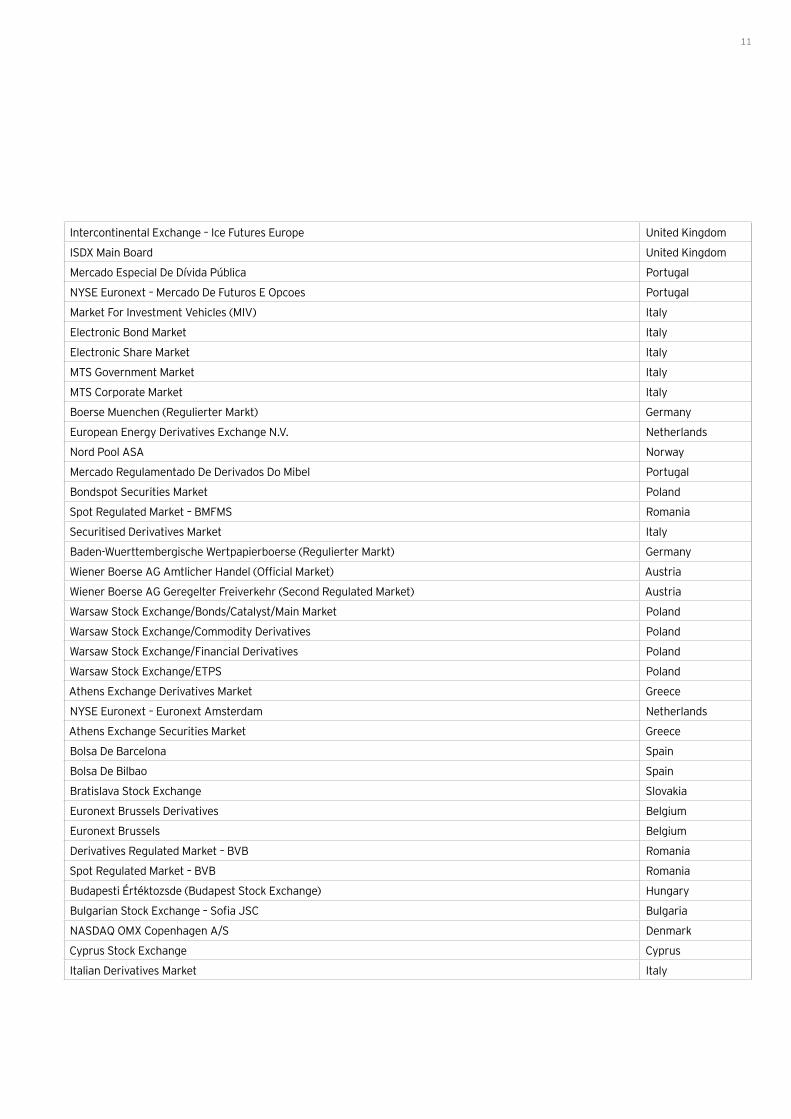

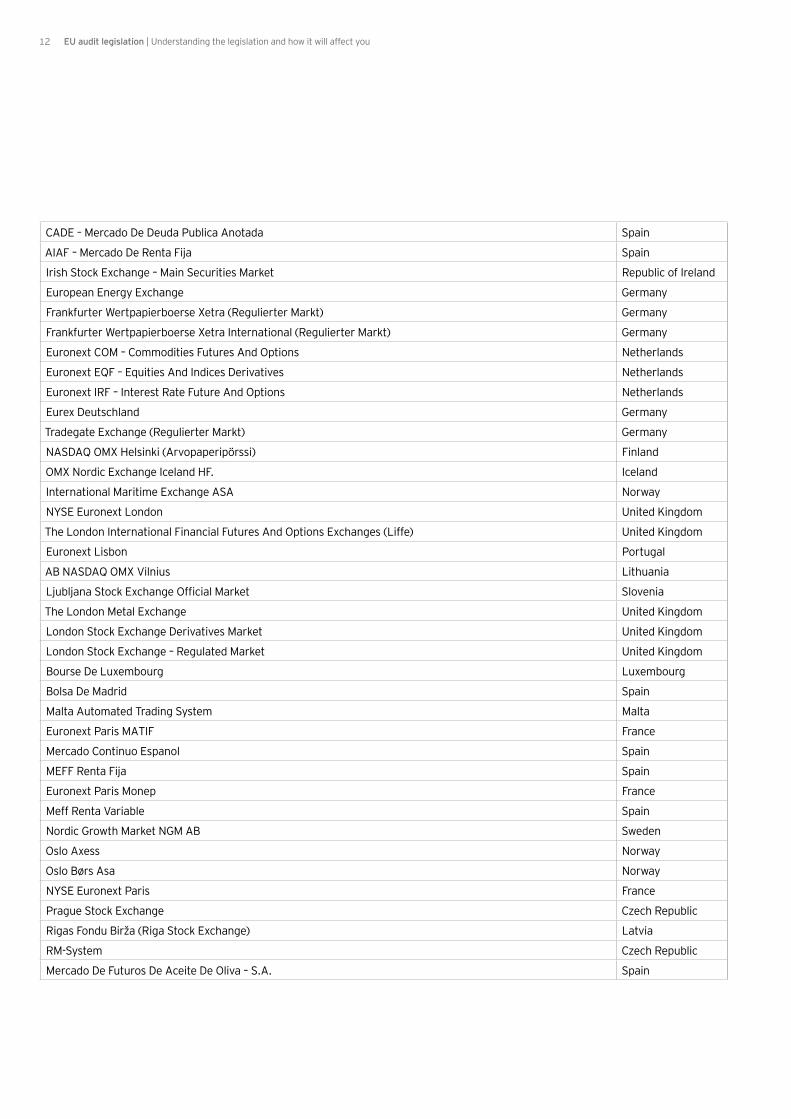

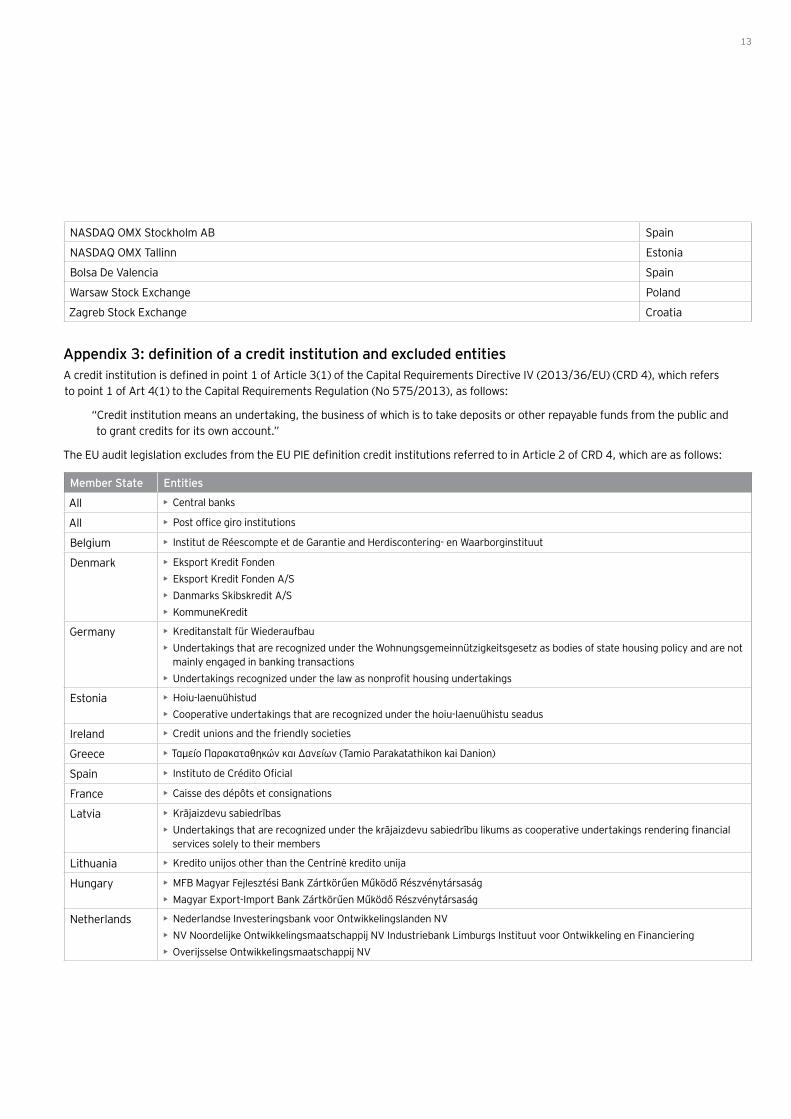

Not all markets in the EU fall within this definition. The European Securities and Markets Authority (ESMA) maintains a list of regulated markets as follows:

Bats Europe Regulated Market UK

Boerse Berlin (Regulierter Markt) Germany

Boerse Berlin (Berlin Second Regulated Market) Germany

Derivatives Regulated Market – BMFMS Romania

Bond Vision Market Italy

Burgundy AB Sweden

BATS Europe Regulated Market United Kingdom

Duesseldorfer Boerse (Regulierter Markt) Germany

Duesseldorfer Boerse Quotrix (Regulierter Markt) Germany

Boerse Berlin Equiduct Trading (Regulierter Markt) Germany

Boerse Berlin Equiduct Trading (Berlin Second Regulated Market) Germany

Electronic Open-End Funds and ETC Market Italy

European Wholesale Securities Market Malta

Fish Pool ASA Norway

Frankfurter Wertpapierboerse (Regulierter Markt) Germany

GXG Official List Denmark

Hanseatische Wertpapierboerse Hamburg (Regulierter Markt) Germany

Niedersaechsiche Boerse Zu Hannover (Regulierter Markt) Germany

Electronic Secondary Securities Market Greece

Appendices

11

Intercontinental Exchange – Ice Futures Europe United Kingdom

ISDX Main Board United Kingdom

Mercado Especial De Dívida Pública Portugal

NYSE Euronext – Mercado De Futuros E Opcoes Portugal

Market For Investment Vehicles (MIV) Italy

Electronic Bond Market Italy

Electronic Share Market Italy

MTS Government Market Italy

MTS Corporate Market Italy

Boerse Muenchen (Regulierter Markt) Germany

European Energy Derivatives Exchange N.V. Netherlands

Nord Pool ASA Norway

Mercado Regulamentado De Derivados Do Mibel Portugal

Bondspot Securities Market Poland

Spot Regulated Market – BMFMS Romania

Securitised Derivatives Market Italy

Baden-Wuerttembergische Wertpapierboerse (Regulierter Markt) Germany

Wiener Boerse AG Amtlicher Handel (Official Market) Austria

Wiener Boerse AG Geregelter Freiverkehr (Second Regulated Market) Austria

Warsaw Stock Exchange/Bonds/Catalyst/Main Market Poland

Warsaw Stock Exchange/Commodity Derivatives Poland

Warsaw Stock Exchange/Financial Derivatives Poland

Warsaw Stock Exchange/ETPS Poland

Athens Exchange Derivatives Market Greece

NYSE Euronext – Euronext Amsterdam Netherlands

Athens Exchange Securities Market Greece

Bolsa De Barcelona Spain

Bolsa De Bilbao Spain

Bratislava Stock Exchange Slovakia

Euronext Brussels Derivatives Belgium

Euronext Brussels Belgium

Derivatives Regulated Market – BVB Romania

Spot Regulated Market – BVB Romania

Budapesti Értéktozsde (Budapest Stock Exchange) Hungary

Bulgarian Stock Exchange – Sofia JSC Bulgaria

NASDAQ OMX Copenhagen A/S Denmark

Cyprus Stock Exchange Cyprus

Italian Derivatives Market Italy

12 EU audit legislation | Understanding the legislation and how it will affect you

CADE – Mercado De Deuda Publica Anotada Spain

AIAF – Mercado De Renta Fija Spain

Irish Stock Exchange – Main Securities Market Republic of Ireland

European Energy Exchange Germany

Frankfurter Wertpapierboerse Xetra (Regulierter Markt) Germany

Frankfurter Wertpapierboerse Xetra International (Regulierter Markt) Germany

Euronext COM – Commodities Futures And Options Netherlands

Euronext EQF – Equities And Indices Derivatives Netherlands

Euronext IRF – Interest Rate Future And Options Netherlands

Eurex Deutschland Germany

Tradegate Exchange (Regulierter Markt) Germany

NASDAQ OMX Helsinki (Arvopaperipörssi) Finland

OMX Nordic Exchange Iceland HF. Iceland

International Maritime Exchange ASA Norway

NYSE Euronext London United Kingdom

The London International Financial Futures And Options Exchanges (Liffe) United Kingdom

Euronext Lisbon Portugal

AB NASDAQ OMX Vilnius Lithuania

Ljubljana Stock Exchange Official Market Slovenia

The London Metal Exchange United Kingdom

London Stock Exchange Derivatives Market United Kingdom

London Stock Exchange – Regulated Market United Kingdom

Bourse De Luxembourg Luxembourg

Bolsa De Madrid Spain

Malta Automated Trading System Malta

Euronext Paris MATIF France

Mercado Continuo Espanol Spain

MEFF Renta Fija Spain

Euronext Paris Monep France

Meff Renta Variable Spain

Nordic Growth Market NGM AB Sweden

Oslo Axess Norway

Oslo Børs Asa Norway

NYSE Euronext Paris France

Prague Stock Exchange Czech Republic

Rigas Fondu Birža (Riga Stock Exchange) Latvia

RM-System Czech Republic

Mercado De Futuros De Aceite De Oliva – S.A. Spain

13

NASDAQ OMX Stockholm AB Spain

NASDAQ OMX Tallinn Estonia

Bolsa De Valencia Spain

Warsaw Stock Exchange Poland

Zagreb Stock Exchange Croatia

Appendix 3: definition of a credit institution and excluded entitiesA credit institution is defined in point 1 of Article 3(1) of the Capital Requirements Directive IV (2013/36/EU) (CRD 4), which refers to point 1 of Art 4(1) to the Capital Requirements Regulation (No 575/2013), as follows:

“Credit institution means an undertaking, the business of which is to take deposits or other repayable funds from the public and to grant credits for its own account.”

The EU audit legislation excludes from the EU PIE definition credit institutions referred to in Article 2 of CRD 4, which are as follows:

Member State Entities

All • Central banks

All • Post office giro institutions

Belgium • Institut de Réescompte et de Garantie and Herdiscontering- en Waarborginstituut

Denmark • Eksport Kredit Fonden• Eksport Kredit Fonden A/S• Danmarks Skibskredit A/S• KommuneKredit

Germany • Kreditanstalt für Wiederaufbau• Undertakings that are recognized under the Wohnungsgemeinnützigkeitsgesetz as bodies of state housing policy and are not

mainly engaged in banking transactions• Undertakings recognized under the law as nonprofit housing undertakings

Estonia • Hoiu-laenuühistud• Cooperative undertakings that are recognized under the hoiu-laenuühistu seadus

Ireland • Credit unions and the friendly societies

Greece • Ταμείο Παρακαταθηκών και Δανείων (Tamio Parakatathikon kai Danion)

Spain • Instituto de Crédito Oficial

France • Caisse des dépôts et consignations

Latvia • Krājaizdevu sabiedrības• Undertakings that are recognized under the krājaizdevu sabiedrību likums as cooperative undertakings rendering financial

services solely to their members

Lithuania • Kredito unijos other than the Centrinė kredito unija

Hungary • MFB Magyar Fejlesztési Bank Zártkörűen Működő Részvénytársaság• Magyar Export-Import Bank Zártkörűen Működő Részvénytársaság

Netherlands • Nederlandse Investeringsbank voor Ontwikkelingslanden NV• NV Noordelijke Ontwikkelingsmaatschappij NV Industriebank Limburgs Instituut voor Ontwikkeling en Financiering• Overijsselse Ontwikkelingsmaatschappij NV

14 EU audit legislation | Understanding the legislation and how it will affect you

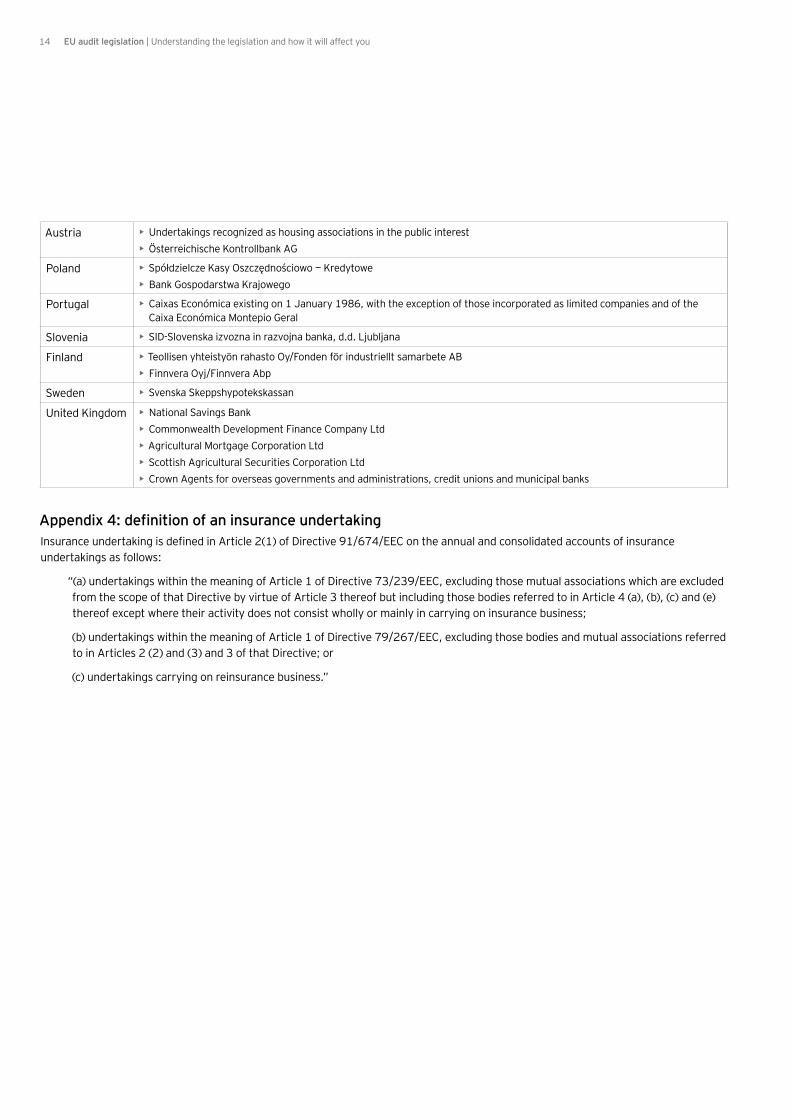

Austria • Undertakings recognized as housing associations in the public interest• Österreichische Kontrollbank AG

Poland • Spółdzielcze Kasy Oszczędnościowo — Kredytowe• Bank Gospodarstwa Krajowego

Portugal • Caixas Económica existing on 1 January 1986, with the exception of those incorporated as limited companies and of the Caixa Económica Montepio Geral

Slovenia • SID-Slovenska izvozna in razvojna banka, d.d. Ljubljana

Finland • Teollisen yhteistyön rahasto Oy/Fonden för industriellt samarbete AB• Finnvera Oyj/Finnvera Abp

Sweden • Svenska Skeppshypotekskassan

United Kingdom • National Savings Bank• Commonwealth Development Finance Company Ltd• Agricultural Mortgage Corporation Ltd• Scottish Agricultural Securities Corporation Ltd• Crown Agents for overseas governments and administrations, credit unions and municipal banks

Appendix 4: definition of an insurance undertakingInsurance undertaking is defined in Article 2(1) of Directive 91/674/EEC on the annual and consolidated accounts of insurance undertakings as follows:

“(a) undertakings within the meaning of Article 1 of Directive 73/239/EEC, excluding those mutual associations which are excluded from the scope of that Directive by virtue of Article 3 thereof but including those bodies referred to in Article 4 (a), (b), (c) and (e) thereof except where their activity does not consist wholly or mainly in carrying on insurance business;

(b) undertakings within the meaning of Article 1 of Directive 79/267/EEC, excluding those bodies and mutual associations referred to in Articles 2 (2) and (3) and 3 of that Directive; or

(c) undertakings carrying on reinsurance business.”

15

How we can helpFor a discussion about the new requirements of the legislation and how your company may be affected, please speak to your usual EY contact.

For more information, visit ey.com/publicpolicy.

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2014 EYGM Limited. All Rights Reserved.

EYG No. AU2696 1408-1300953 NY ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.