Embed Size (px)

Citation preview

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

12 February 2013

Europe

Equity Research

European Cable Sector Connections Series

The Cable Guys: Follow the leader

We launch coverage of the European cable sector, initiating with an Outperform rating on Prysmian (TP €19) and a Neutral rating on Nexans (TP €36). We analyse the key growth end markets, focusing on submarine cables and the SURF segment, and map out the global competitive landscape, taking a closer look at optical fibre & cables.

■ Attractive medium-term growth. We view submarine cables as an attractive market for both Prysmian and Nexans. On our analysis of recent contracts and industry relationships, we prefer Prysmian as a play on this theme as we believe it can take market share over the next five years. In the SURF segment we analyse the supply and demand of flexible pipes and show three capacity utilisation scenarios for Prysmian’s Flexible pipe plant.

■ Mapping the competitive landscape: Based on market size and

characteristics, we focus on optical fibre & cable and particularly the fast-growing Chinese market where we view the medium-term competitive threat as manageable. In Land High Voltage, we believe the competitive threat is well understood by the market but view the risk of pricing pressure as greater for Nexans due to its higher exposure to the Middle East.

■ Stock calls: We favour Prysmian for its 1) exposure to growth themes,

2) competitive positioning, 3) improving end market exposure and 4) self-help. We view risk/reward at Nexans as balanced, as its exposure to growth end markets is offset by 1) lack of valuation upside on reaching the low end of 2015 targets and 2) the relatively higher risk of near-term earnings volatility. Our €19 target price for Prysmian is derived using a 2013E sector multiple (ex lifts) vs the current discount of 10%. For Nexans our €36 target price is driven by a 8.1x 2014E EV/EBIT multiple (10% sector discount).

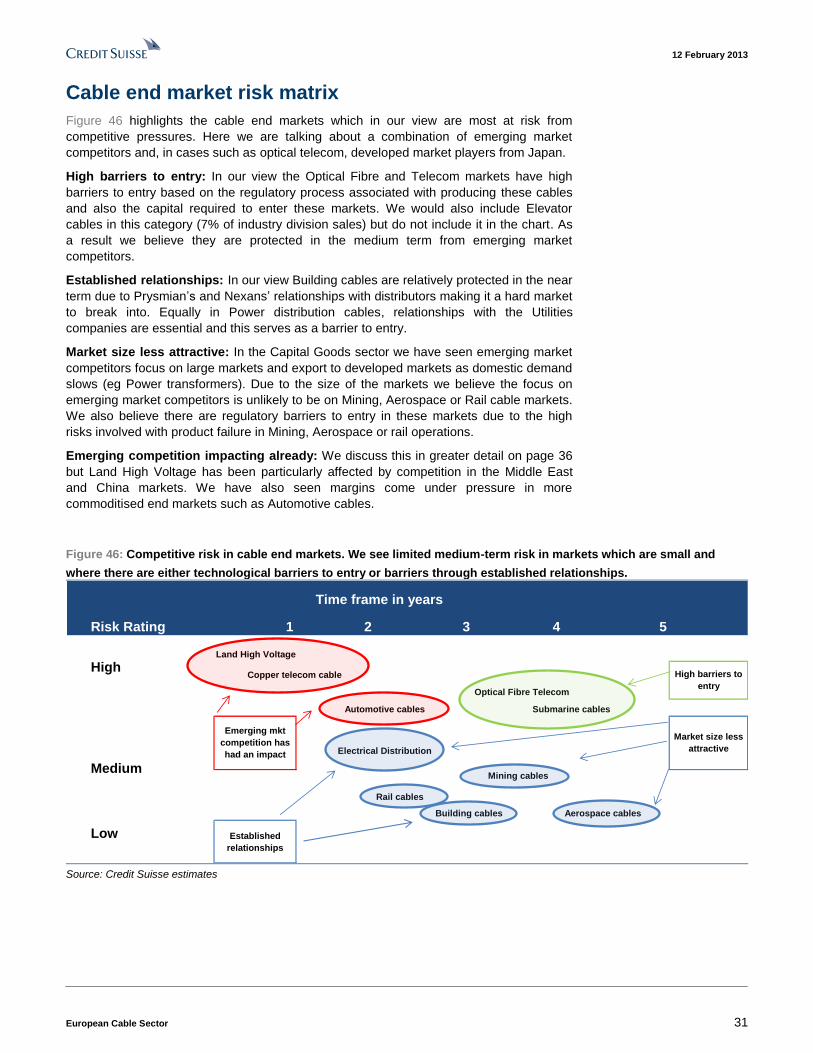

Figure 1: Competitive risk matrix in cable markets (more detail on page 31)

Risk Rating 1 2 3 4 5

Land High Voltage

Optical Fibre Telecom

Rail cables

Mining cables

Aerospace cables

Established

relationships

Low

Building cables

Market size less

attractive

High barriers to

entry

Electrical Distribution

Time frame in years

HighCopper telecom cable

Submarine cables

Medium

Automotive cables

Emerging mkt

competition has

had an impact

Source: Credit Suisse estimates

The Credit Suisse Connections Series

leverages our exceptional breadth of

macro and micro research to deliver

incisive cross-sector and cross-border

thematic insights for our clients.

Research Analysts

Max Yates

44 20 7883 8501

Andre Kukhnin CFA

44 20 7888 0350

Simon Toennessen

44 20 7883 6893

Jonathan Hurn, CFA

44 20 7883 4532

Julian Mitchell

212 325 6668

Specialist Sales: David Arnold

44 20 7883 3549

End-market primers series

This report contains a detailed primer on

the Global Cable end-market as well as in-

depth analysis of the key thematic

drivers. For other detailed global end-

market primers published by the team,

please click here:

Industrial Automation, Elevators, Global

Power Generation

12 February 2013

European Cable Sector 2

Table of contents Key charts 3

Executive summary 4

Prysmian Investment Case 7

Nexans Investment Case 8

Medium-term sector drivers 9

#1: Submarine cables 9

Submarine opportunity for Prysmian and Nexans 11

Prysmian’s market share may increase in the medium term 12

We also see greater project execution risk at Nexans 14

#2: SURF: Limited downside risk in the near term 19

Why is the market concerned about SURF products? 22

Scenario analysis for flexible pipe ramp-up 25

#3: Mapping the global cable competitive landscape 28

Global cable competitor growth and margin trends 30

Optical fibre cables: attractive in the medium term 32

Land HV: Expect more moderate pricing pressure 36

#4: Self-help is key to margin expansion 38

We expect €170m of Draka synergies by 2015E 39

Nexans: 2015 targets but limited near-term impact 44

Company section 47

Prysmian (PRY.MI) 48

Prysmian investment case 51

Nexans (NEXS.PA) 70

Nexans investment case 72

End market primer 91

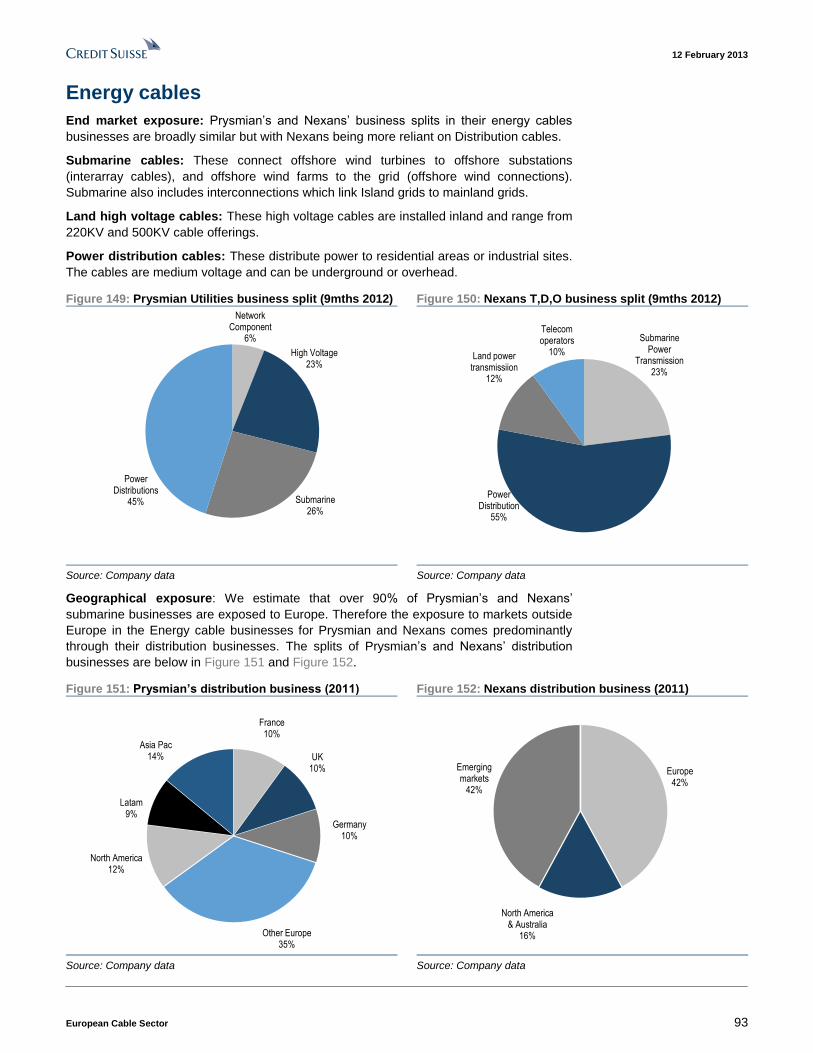

Energy cables 93

Building cables 97

Industrial cables 101

Telecom cables 105

Appendix: Further company details (Metal price impact,

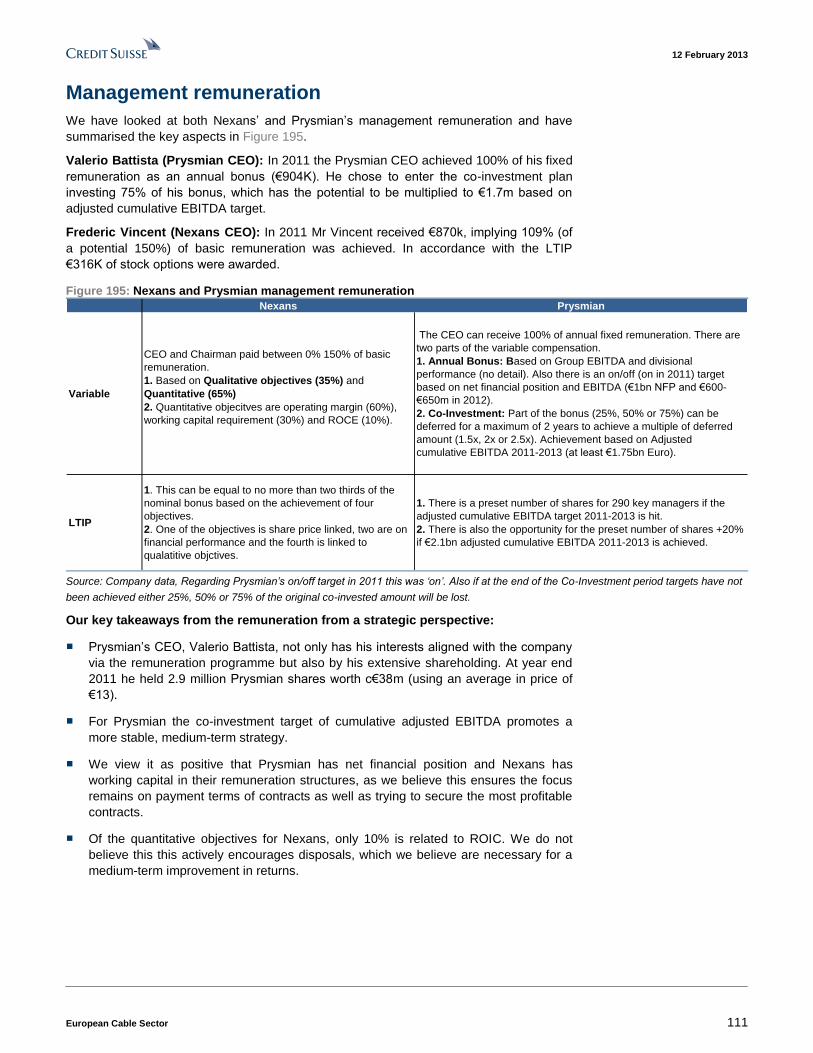

Management remuneration, Shareholder structure) 109

12 February 2013

European Cable Sector 3

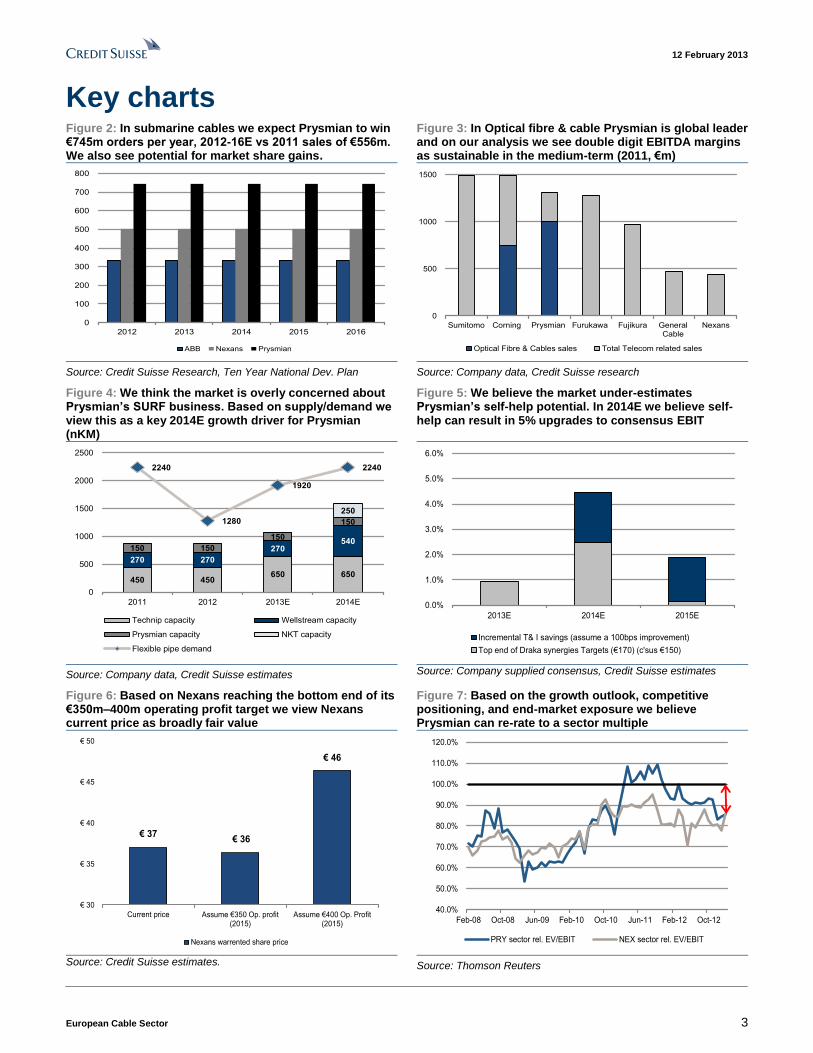

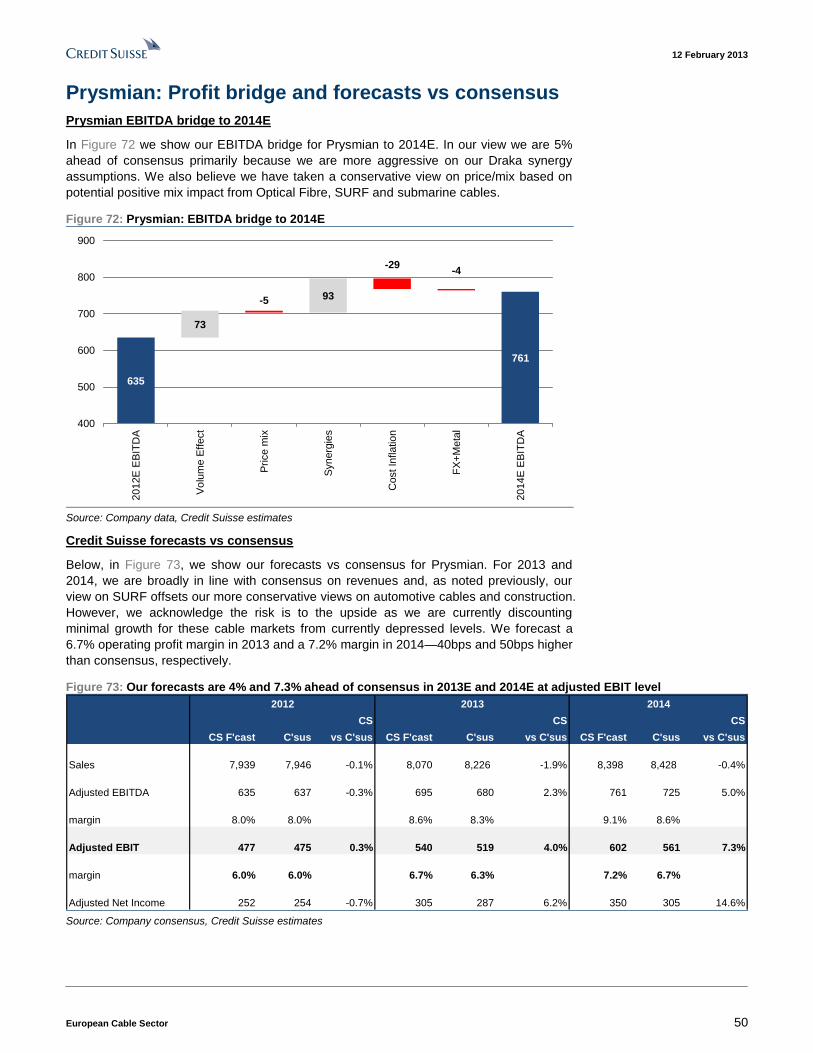

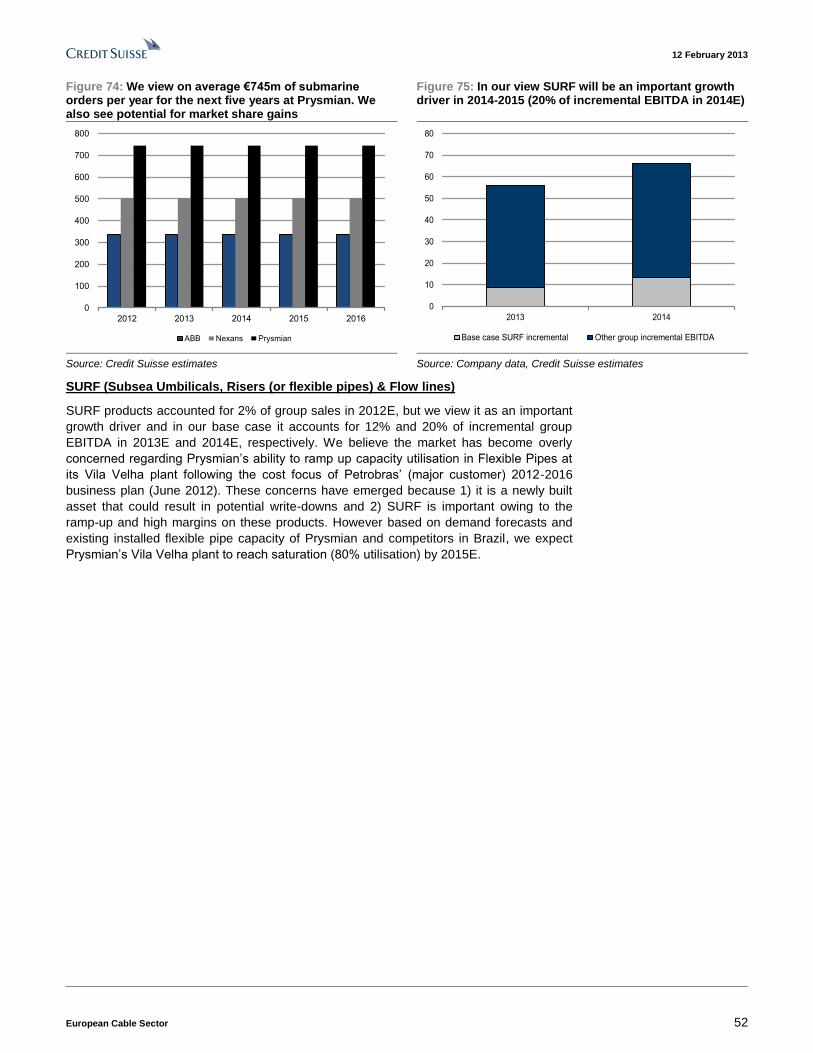

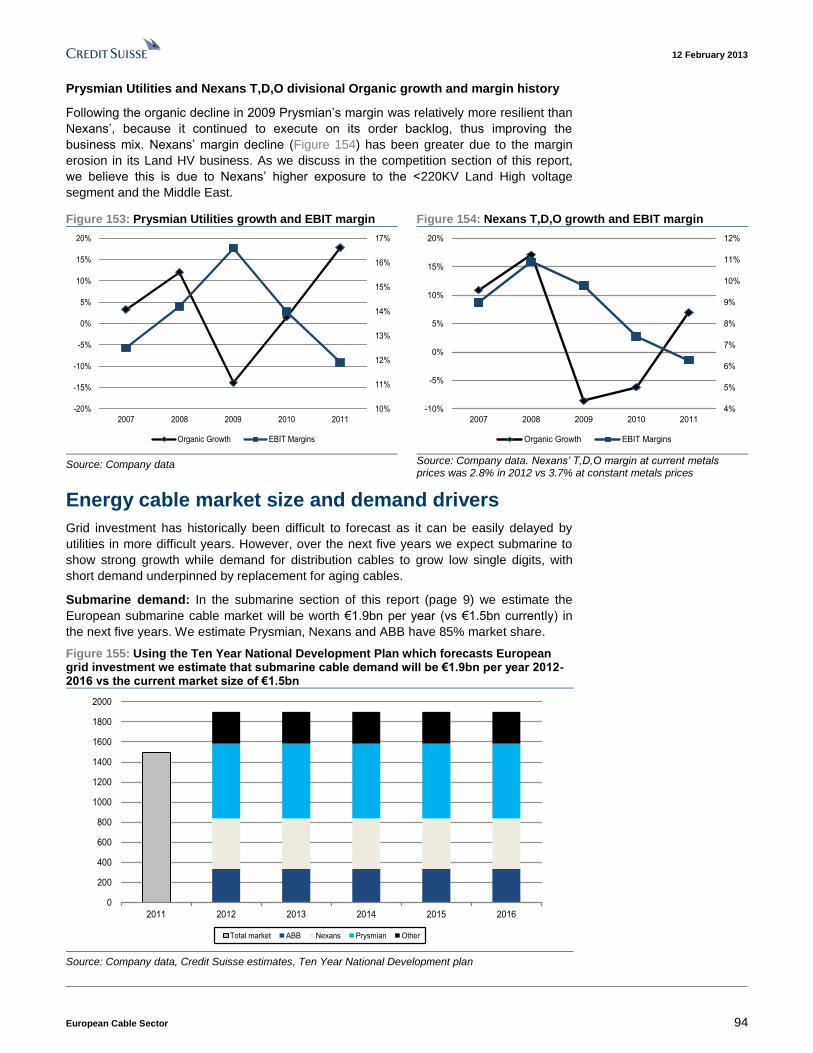

Key charts Figure 2: In submarine cables we expect Prysmian to win €745m orders per year, 2012-16E vs 2011 sales of €556m. We also see potential for market share gains.

Figure 3: In Optical fibre & cable Prysmian is global leader and on our analysis we see double digit EBITDA margins as sustainable in the medium-term (2011, €m)

0

100

200

300

400

500

600

700

800

2012 2013 2014 2015 2016

ABB Nexans Prysmian

0

500

1000

1500

Sumitomo Corning Prysmian Furukawa Fujikura GeneralCable

Nexans

Optical Fibre & Cables sales Total Telecom related sales

Source: Credit Suisse Research, Ten Year National Dev. Plan Source: Company data, Credit Suisse research

Figure 4: We think the market is overly concerned about Prysmian’s SURF business. Based on supply/demand we view this as a key 2014E growth driver for Prysmian (nKM)

Figure 5: We believe the market under-estimates Prysmian’s self-help potential. In 2014E we believe self-help can result in 5% upgrades to consensus EBIT

450 450650 650

270 270

270540

150 150

150

150

250

2240

1280

1920

2240

0

500

1000

1500

2000

2500

2011 2012 2013E 2014E

Technip capacity Wellstream capacity

Prysmian capacity NKT capacity

Flexible pipe demand

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2013E 2014E 2015E

Incremental T& I savings (assume a 100bps improvement)

Top end of Draka synergies Targets (€170) (c'sus €150)

Source: Company data, Credit Suisse estimates Source: Company supplied consensus, Credit Suisse estimates

Figure 6: Based on Nexans reaching the bottom end of its €350m–400m operating profit target we view Nexans current price as broadly fair value

Figure 7: Based on the growth outlook, competitive positioning, and end-market exposure we believe Prysmian can re-rate to a sector multiple

€ 37€ 36

€ 46

€ 30

€ 35

€ 40

€ 45

€ 50

Current price Assume €350 Op. profit (2015)

Assume €400 Op. Profit (2015)

Nexans warrented share price

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

110.0%

120.0%

Feb-08 Oct-08 Jun-09 Feb-10 Oct-10 Jun-11 Feb-12 Oct-12

PRY sector rel. EV/EBIT NEX sector rel. EV/EBIT

Source: Credit Suisse estimates. Source: Thomson Reuters

12 February 2013

European Cable Sector 4

Executive summary In this report:

■ Take an in-depth look at key growth markets in the sector focusing on Submarine

Cables (go to pages 9 to 18) and SURF products that are used in subsea oil

production (go to pages 19 to 27);

■ Map out the global cable competitive landscape in terms of growth rates and margins

among the large cable players (go to pages 29 to 31);

■ Take a deep-dive into the optical fibre & cable market, assessing the risk to Prysmian

both in the developed markets and the fast-growing Chinese market (pages 33 to 35);

■ Include a cable sector primer running through the key end markets for Prysmian and

Nexans (go to pages 91 to 108).

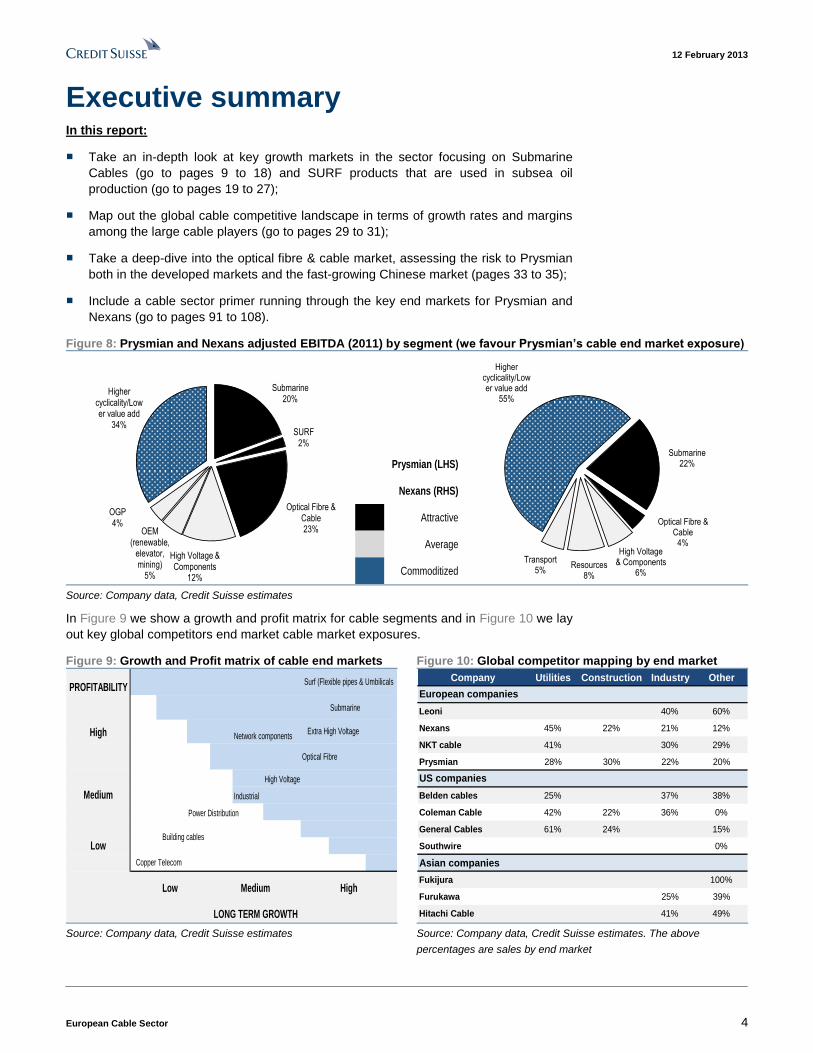

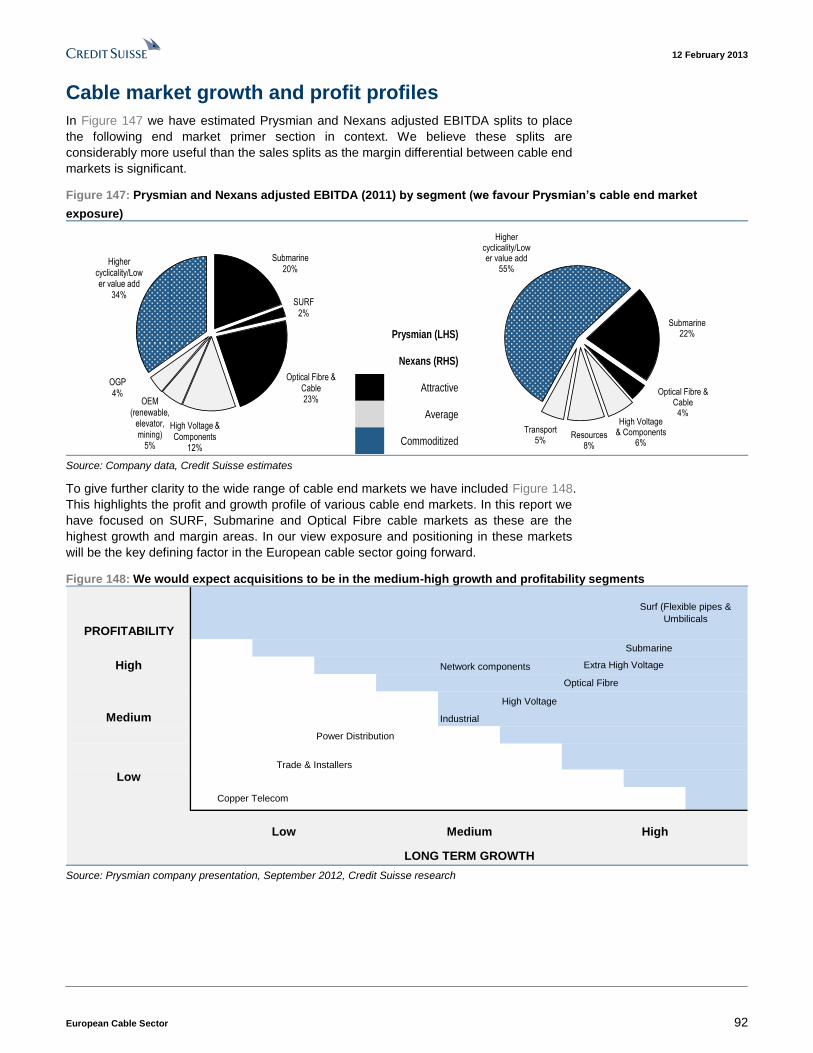

Figure 8: Prysmian and Nexans adjusted EBITDA (2011) by segment (we favour Prysmian’s cable end market exposure)

Submarine20%

SURF2%

Optical Fibre & Cable23%

High Voltage & Components

12%

OEM (renewable,

elevator, mining)

5%

OGP4%

Higher cyclicality/Lower value add

34%

Prysmian (LHS)

Nexans (RHS)

Attractive

Average

Commoditized

Submarine22%

Optical Fibre & Cable

4%High Voltage

& Components6%

Resources8%

Transport5%

Higher cyclicality/Lower value add

55%

Source: Company data, Credit Suisse estimates

In Figure 9 we show a growth and profit matrix for cable segments and in Figure 10 we lay

out key global competitors end market cable market exposures.

Figure 9: Growth and Profit matrix of cable end markets Figure 10: Global competitor mapping by end market

Submarine

Network components

Optical Fibre

High Voltage

Industrial

Power Distribution

High

LONG TERM GROWTH

Surf (Flexible pipes & Umbilicals

LowBuilding cables

Copper Telecom

Low Medium

PROFITABILITY

High Extra High Voltage

Medium

Company Utilities Construction Industry Other

Leoni 40% 60%

Nexans 45% 22% 21% 12%

NKT cable 41% 30% 29%

Prysmian 28% 30% 22% 20%

Belden cables 25% 37% 38%

Coleman Cable 42% 22% 36% 0%

General Cables 61% 24% 15%

Southwire 0%

Asian companies

Fukijura 100%

Furukawa 25% 39%

Hitachi Cable 41% 49%

US companies

European companies

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates. The above

percentages are sales by end market

12 February 2013

European Cable Sector 5

Medium-term sector drivers

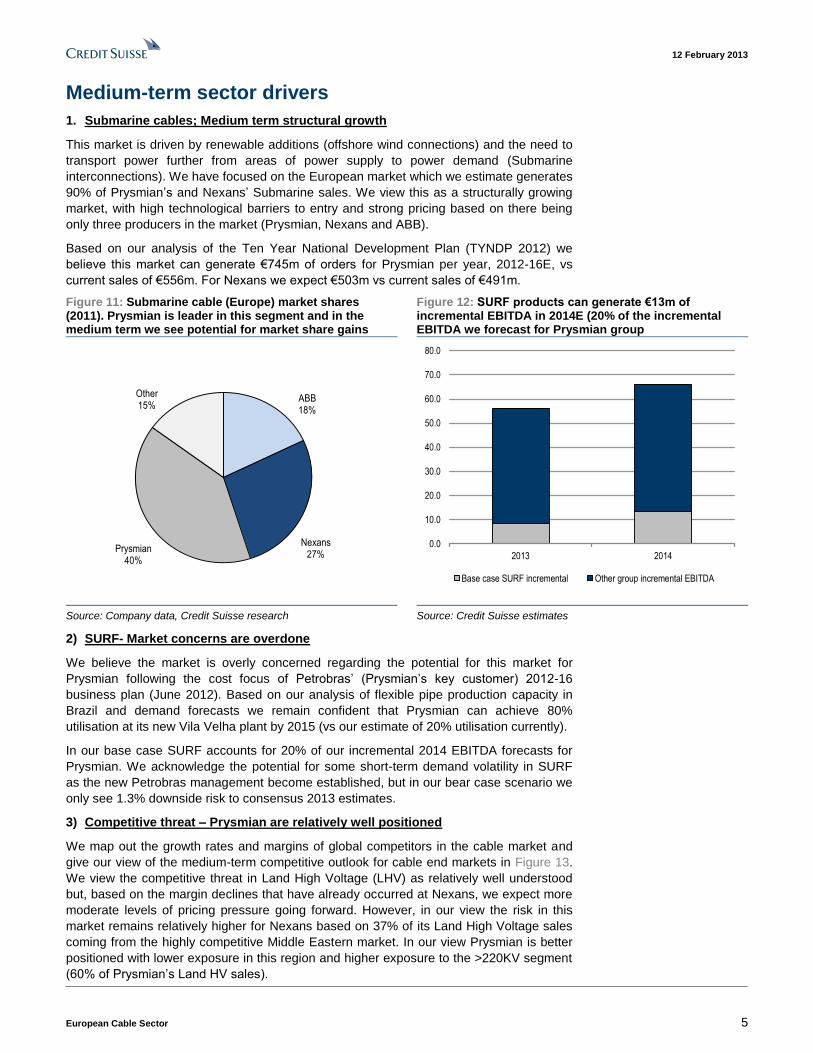

1. Submarine cables; Medium term structural growth

This market is driven by renewable additions (offshore wind connections) and the need to

transport power further from areas of power supply to power demand (Submarine

interconnections). We have focused on the European market which we estimate generates

90% of Prysmian’s and Nexans’ Submarine sales. We view this as a structurally growing

market, with high technological barriers to entry and strong pricing based on there being

only three producers in the market (Prysmian, Nexans and ABB).

Based on our analysis of the Ten Year National Development Plan (TYNDP 2012) we

believe this market can generate €745m of orders for Prysmian per year, 2012-16E, vs

current sales of €556m. For Nexans we expect €503m vs current sales of €491m.

Figure 11: Submarine cable (Europe) market shares (2011). Prysmian is leader in this segment and in the medium term we see potential for market share gains

Figure 12: SURF products can generate €13m of incremental EBITDA in 2014E (20% of the incremental EBITDA we forecast for Prysmian group

ABB18%

Nexans 27%

Prysmian40%

Other15%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2013 2014

Base case SURF incremental Other group incremental EBITDA

Source: Company data, Credit Suisse research Source: Credit Suisse estimates

2) SURF- Market concerns are overdone

We believe the market is overly concerned regarding the potential for this market for

Prysmian following the cost focus of Petrobras’ (Prysmian’s key customer) 2012-16

business plan (June 2012). Based on our analysis of flexible pipe production capacity in

Brazil and demand forecasts we remain confident that Prysmian can achieve 80%

utilisation at its new Vila Velha plant by 2015 (vs our estimate of 20% utilisation currently).

In our base case SURF accounts for 20% of our incremental 2014 EBITDA forecasts for

Prysmian. We acknowledge the potential for some short-term demand volatility in SURF

as the new Petrobras management become established, but in our bear case scenario we

only see 1.3% downside risk to consensus 2013 estimates.

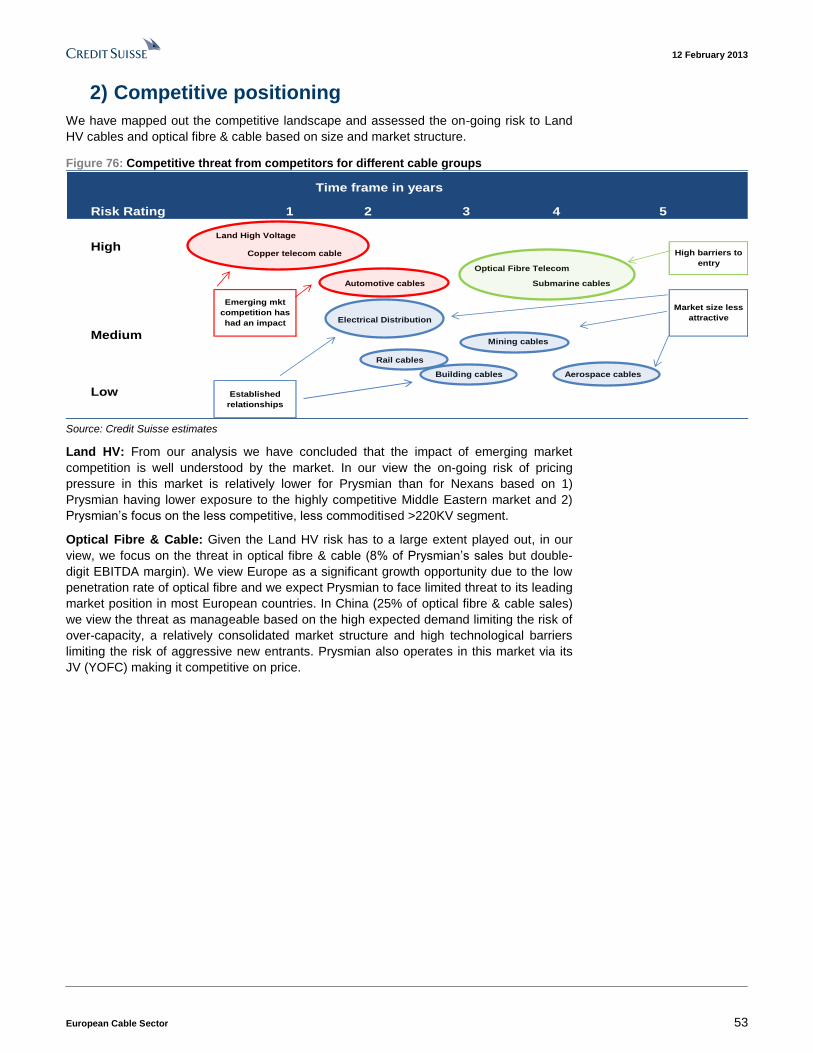

3) Competitive threat – Prysmian are relatively well positioned

We map out the growth rates and margins of global competitors in the cable market and

give our view of the medium-term competitive outlook for cable end markets in Figure 13.

We view the competitive threat in Land High Voltage (LHV) as relatively well understood

but, based on the margin declines that have already occurred at Nexans, we expect more

moderate levels of pricing pressure going forward. However, in our view the risk in this

market remains relatively higher for Nexans based on 37% of its Land High Voltage sales

coming from the highly competitive Middle Eastern market. In our view Prysmian is better

positioned with lower exposure in this region and higher exposure to the >220KV segment

(60% of Prysmian’s Land HV sales).

12 February 2013

European Cable Sector 6

Figure 13: Competitive risk matrix for key cable end markets (more detail on page 31)

Risk Rating 1 2 3 4 5

Land High Voltage

Optical Fibre Telecom

Rail cables

Mining cables

Aerospace cables

Established

relationships

Low

Building cables

Market size less

attractive

High barriers to

entry

Electrical Distribution

Time frame in years

HighCopper telecom cable

Submarine cables

Medium

Automotive cables

Emerging mkt

competition has

had an impact

Source: Credit Suisse estimates

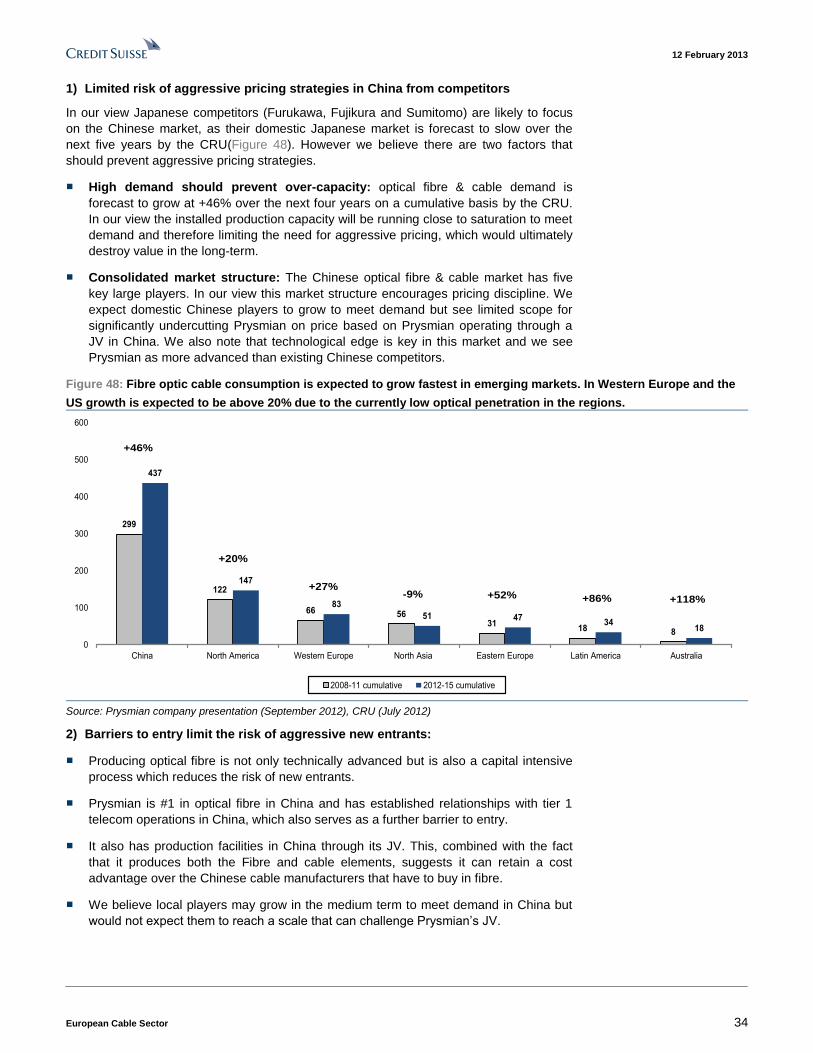

We have also focused on the threat in Optical Fibre and Cable where Prysmian is global leader and has 2011 sales of €1bn. In Europe (Prysmian’s core market) we see limited threat as we believe large Japanese competitors will likely focus on the faster-growing Chinese market in the medium term. Specifically in China we view the threat as manageable and see the market as attractive in the medium term based on 1) Prysmian’s #1 share in China through its JV with YOFC (Yangtze Optical Fibre & Cable), 2) greater pricing discipline due to the market structure (five key players), and 3) expected high demand limiting the risk of over-capacity and therefore the likelihood of pricing strategies. We expect local players to grow in size—however Prysmian operates primarily through its Chinese JV, making it competitive on price.

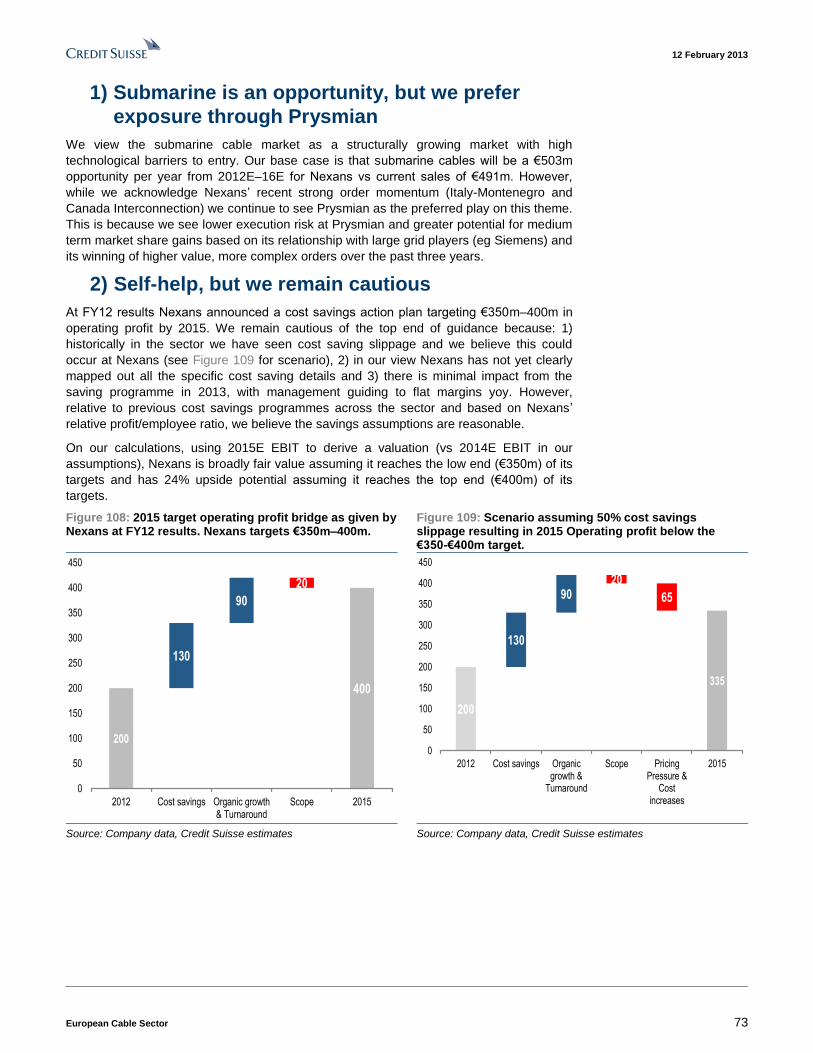

4) Self-help- Key driver of margin expansion in 2013/14

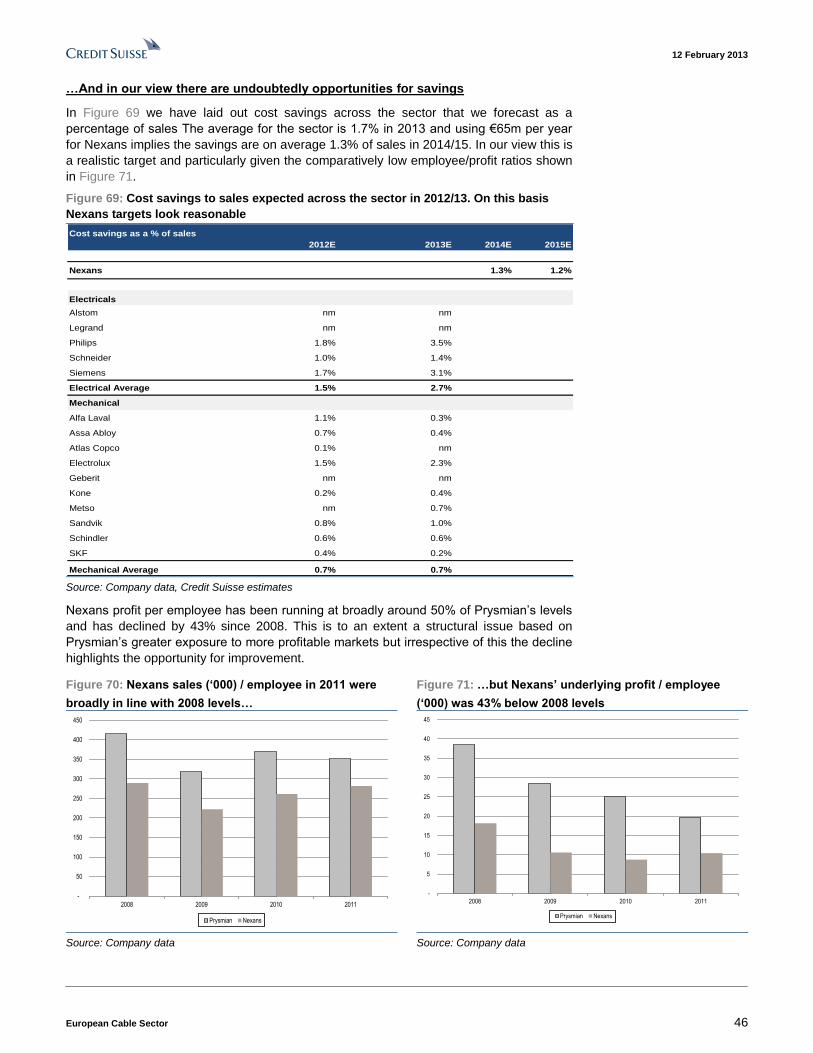

Prysmian: We believe Prysmian can achieve the top end (€170m) of synergies from its recent acquisition of Draka faster than consensus expects. We also see potential for further restructuring of its underperforming building cables business (Figure 14). Combined, we believe these factors could drive 5% upgrades to 2014 consensus EBIT.

Nexans: Nexans’ 2015 operating profit target is €350m–400m—our estimate is at the

lower end. We remain cautious because 1) we expect some slippage in targeted cost

savings, and 2) we believe details of the cost savings programme have not been finalised.

However, the level of saving as a percentage of sales is reasonable relative to the sector

(Figure 15) despite our caution on the eventual drop through to profits. If Nexans achieves

the low end of the targeted range we calculate the current price as broadly fair value.

Figure 14: In our Nexans Trade & Installers division restructuring scenario we estimate a 100bps improvement could generate €21m of savings

Figure 15: €65m of cost savings per year in 2014E–15E at Nexans looks credible relative to cost savings programmes across the sector as a % of sales

T&I restructuring scenario 100bps 200bps

2011 group employees 21,547 21,547

T&I (assume 30% of total) 6,464 6,464

Employee cost

Group Personnel Cost (€mn) 916 916

Implied annual employee salary (€,000) 42,512 42,512

Scenario cost savings

Targeted cost saving (€mn) 21 42

Implied redundancies (based on av salary) 494 988

as a % of T&I employees 7.6% 15.3%

as a % of group employees 2.3% 4.6%

Cost savings as a % of sales

2012E 2013E 2014E 2015E

Nexans 1.3% 1.2%

Electricals

Philips 1.8% 3.5%

Schneider 1.0% 1.4%

Siemens 1.7% 3.1%

Electrical Average 1.5% 2.7%

Mechanical

Alfa Laval 1.1% 0.3%

Assa Abloy 0.7% 0.4%

Electrolux 1.5% 2.3%

Metso nm 0.7%

Sandvik 0.8% 1.0%

SKF 0.4% 0.2%

Mechanical Average 0.7% 0.7% Source: Company data, Credit Suisse estimates Source: Credit Suisse estimates

12 February 2013

European Cable Sector 7

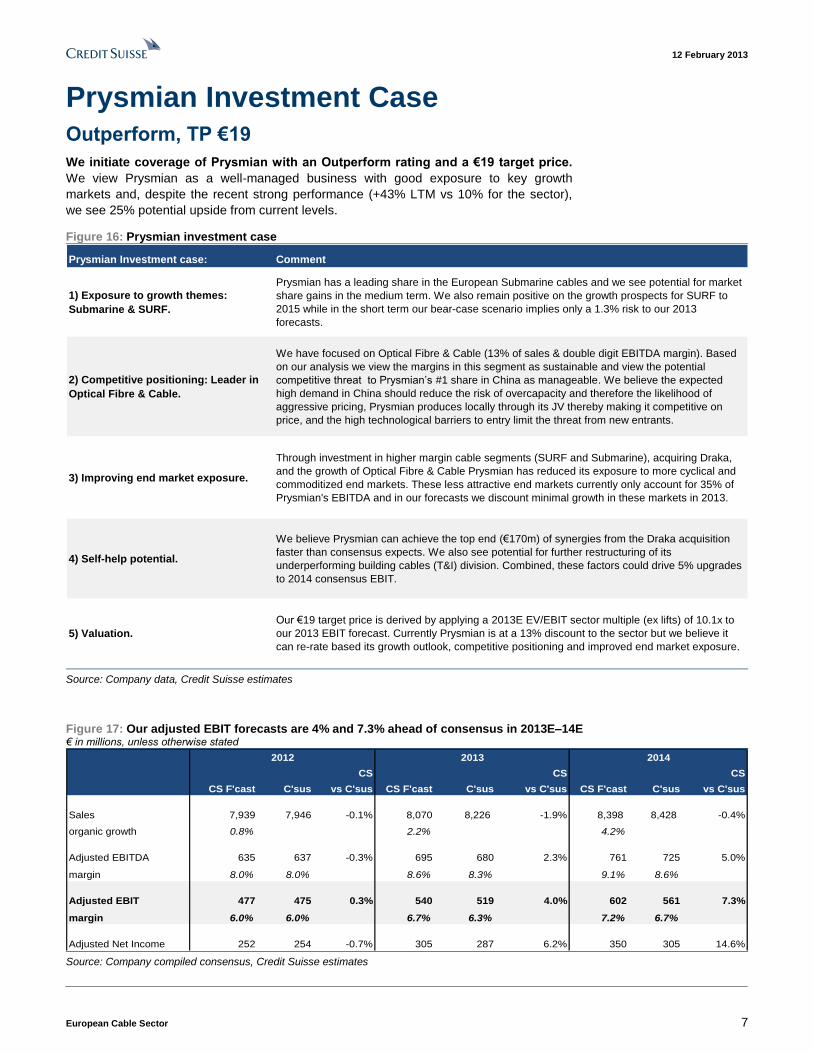

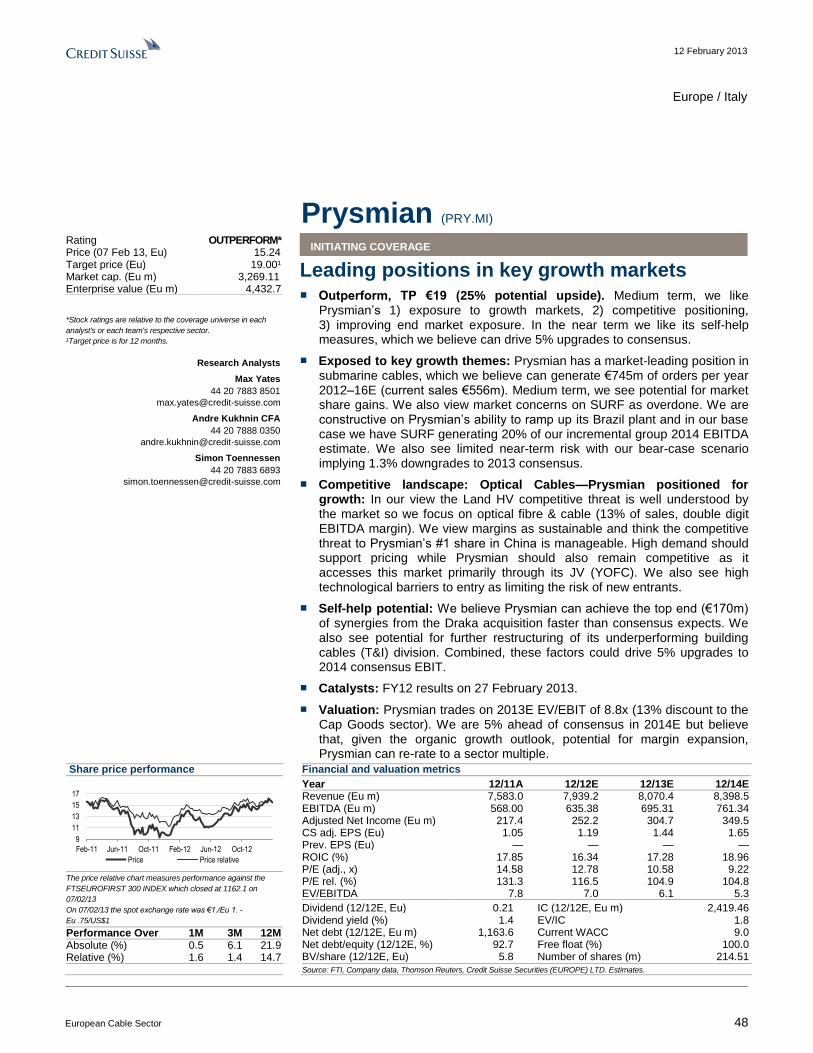

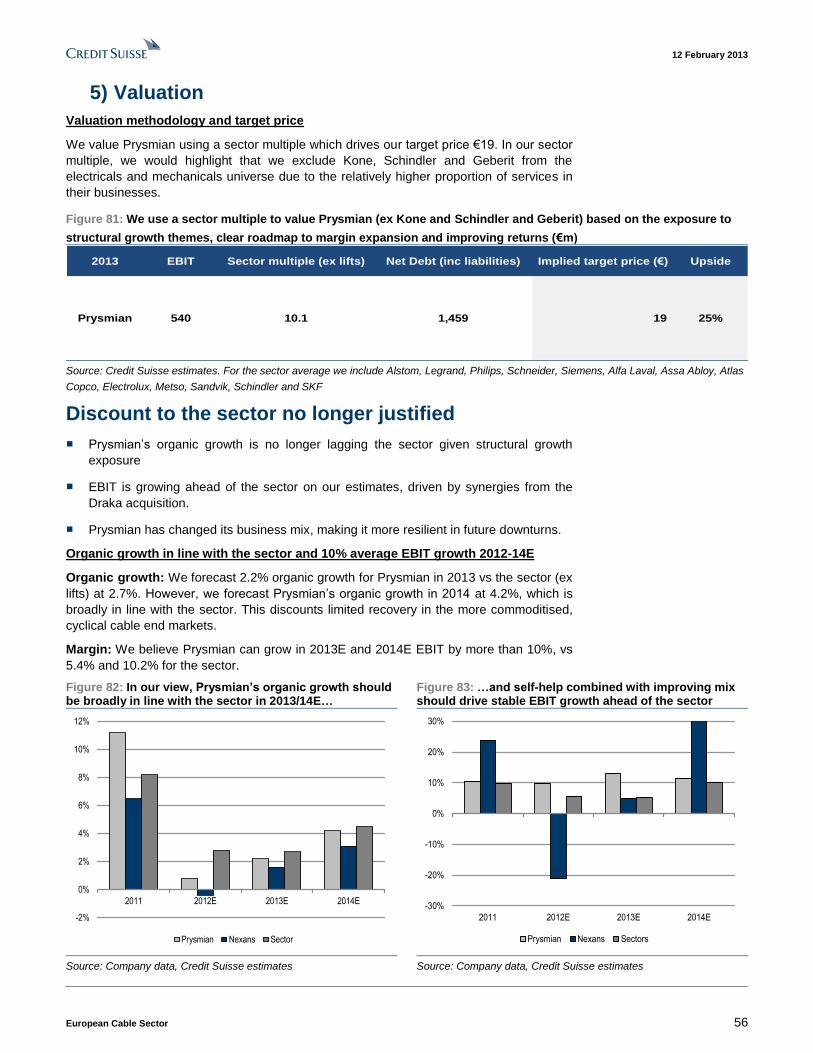

Prysmian Investment Case Outperform, TP €19

We initiate coverage of Prysmian with an Outperform rating and a €19 target price.

We view Prysmian as a well-managed business with good exposure to key growth

markets and, despite the recent strong performance (+43% LTM vs 10% for the sector),

we see 25% potential upside from current levels.

Figure 16: Prysmian investment case

Prysmian Investment case: Comment

1) Exposure to growth themes:

Submarine & SURF.

Prysmian has a leading share in the European Submarine cables and we see potential for market

share gains in the medium term. We also remain positive on the growth prospects for SURF to

2015 while in the short term our bear-case scenario implies only a 1.3% risk to our 2013

forecasts.

2) Competitive positioning: Leader in

Optical Fibre & Cable.

We have focused on Optical Fibre & Cable (13% of sales & double digit EBITDA margin). Based

on our analysis we view the margins in this segment as sustainable and view the potential

competitive threat to Prysmian’s #1 share in China as manageable. We believe the expected

high demand in China should reduce the risk of overcapacity and therefore the likelihood of

aggressive pricing, Prysmian produces locally through its JV thereby making it competitive on

price, and the high technological barriers to entry limit the threat from new entrants.

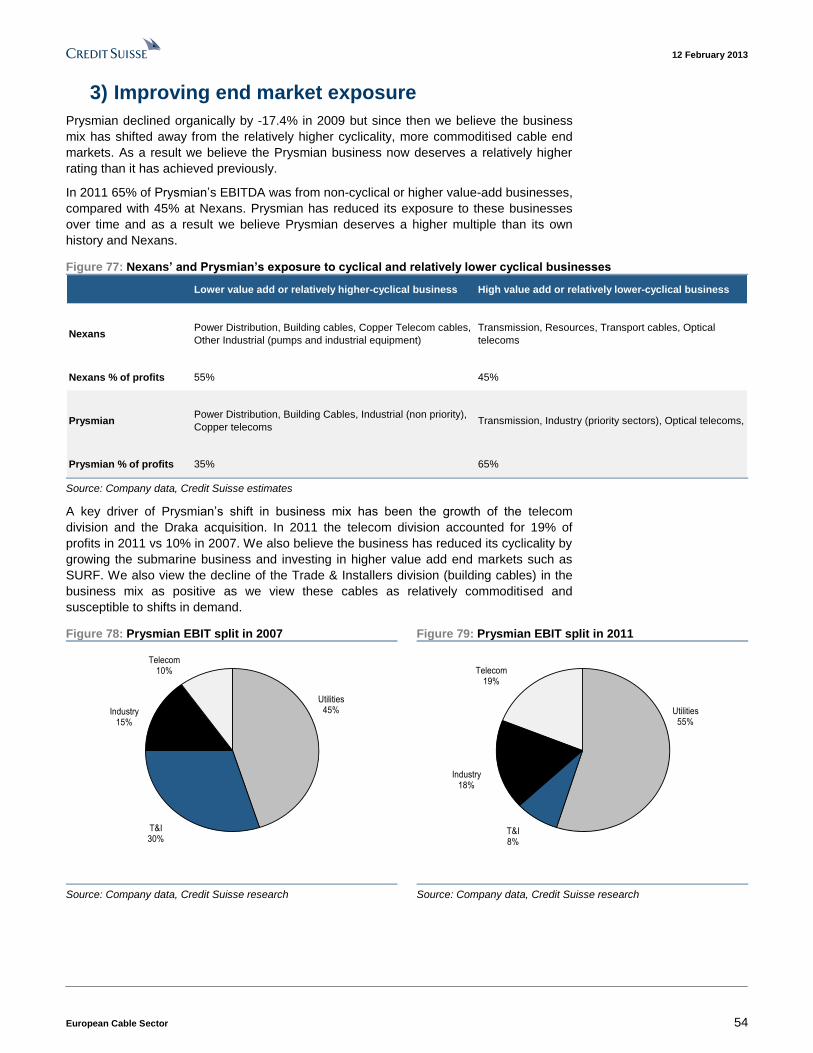

3) Improving end market exposure.

Through investment in higher margin cable segments (SURF and Submarine), acquiring Draka,

and the growth of Optical Fibre & Cable Prysmian has reduced its exposure to more cyclical and

commoditized end markets. These less attractive end markets currently only account for 35% of

Prysmian's EBITDA and in our forecasts we discount minimal growth in these markets in 2013.

4) Self-help potential.

We believe Prysmian can achieve the top end (€170m) of synergies from the Draka acquisition

faster than consensus expects. We also see potential for further restructuring of its

underperforming building cables (T&I) division. Combined, these factors could drive 5% upgrades

to 2014 consensus EBIT.

5) Valuation.

Our €19 target price is derived by applying a 2013E EV/EBIT sector multiple (ex lifts) of 10.1x to

our 2013 EBIT forecast. Currently Prysmian is at a 13% discount to the sector but we believe it

can re-rate based its growth outlook, competitive positioning and improved end market exposure.

Source: Company data, Credit Suisse estimates

Figure 17: Our adjusted EBIT forecasts are 4% and 7.3% ahead of consensus in 2013E–14E € in millions, unless otherwise stated

CS CS CS

CS F'cast C'sus vs C'sus CS F'cast C'sus vs C'sus CS F'cast C'sus vs C'sus

Sales 7,939 7,946 -0.1% 8,070 8,226 -1.9% 8,398 8,428 -0.4%

organic growth 0.8% 2.2% 4.2%

Adjusted EBITDA 635 637 -0.3% 695 680 2.3% 761 725 5.0%

margin 8.0% 8.0% 8.6% 8.3% 9.1% 8.6%

Adjusted EBIT 477 475 0.3% 540 519 4.0% 602 561 7.3%

margin 6.0% 6.0% 6.7% 6.3% 7.2% 6.7%

Adjusted Net Income 252 254 -0.7% 305 287 6.2% 350 305 14.6%

2012 2013 2014

Source: Company compiled consensus, Credit Suisse estimates

12 February 2013

European Cable Sector 8

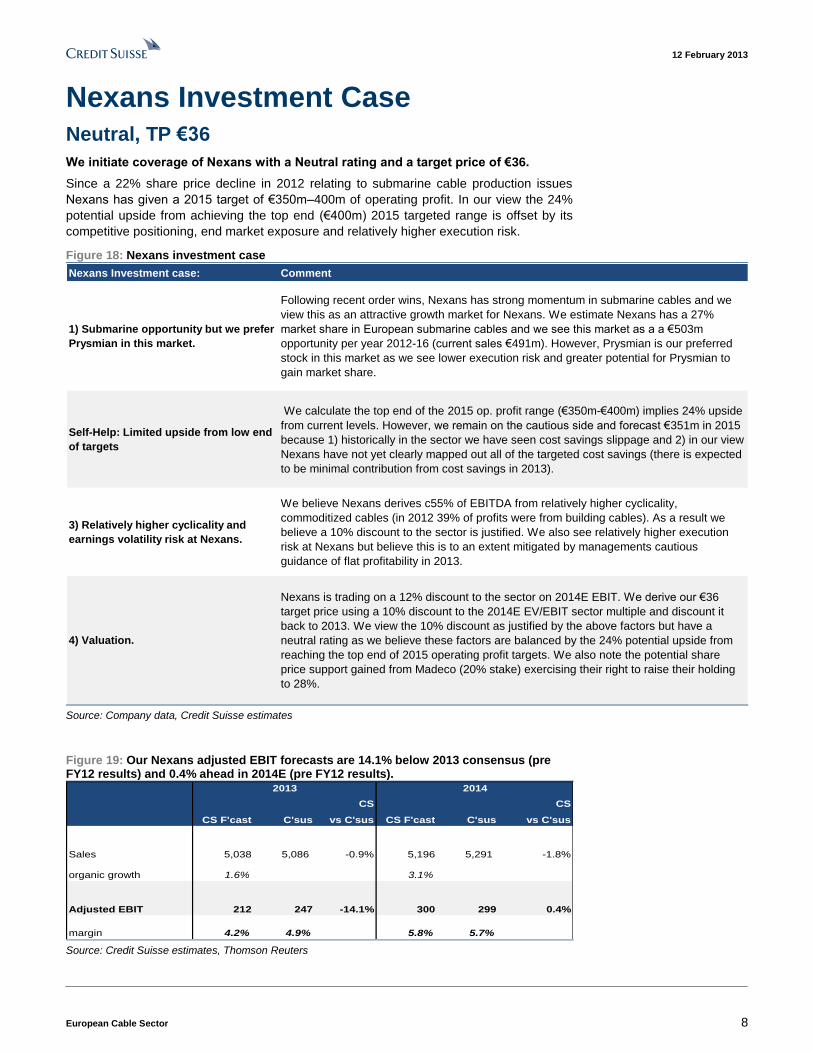

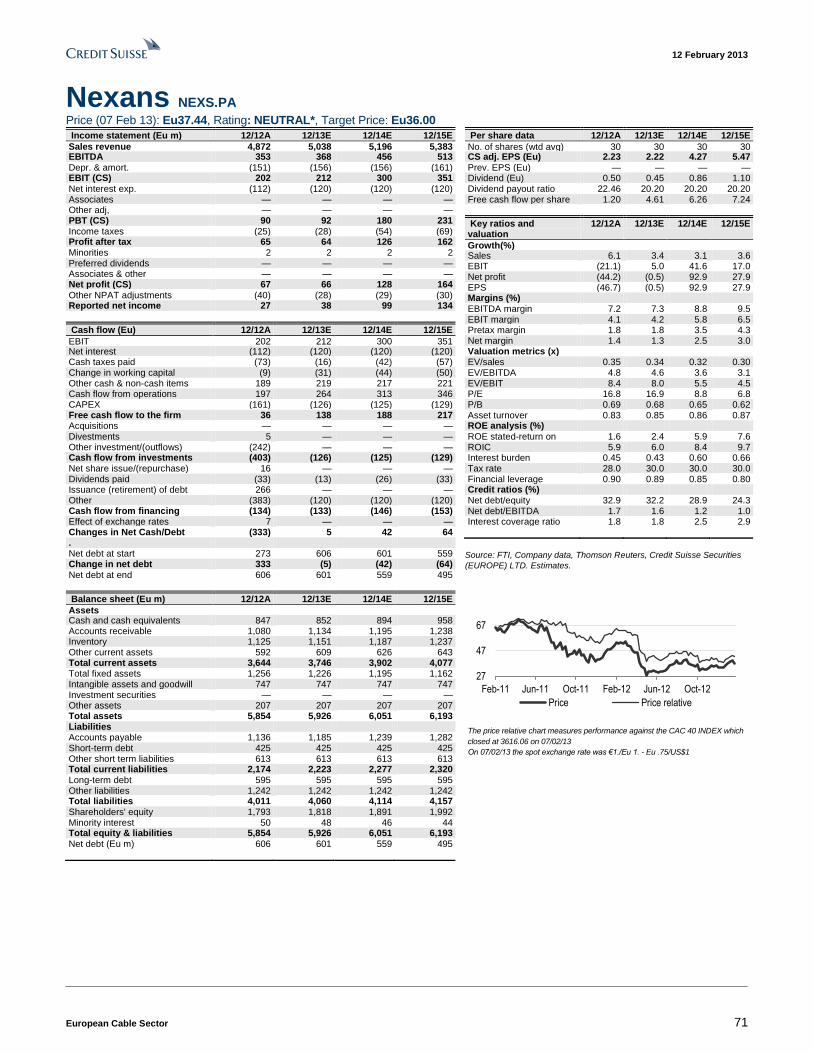

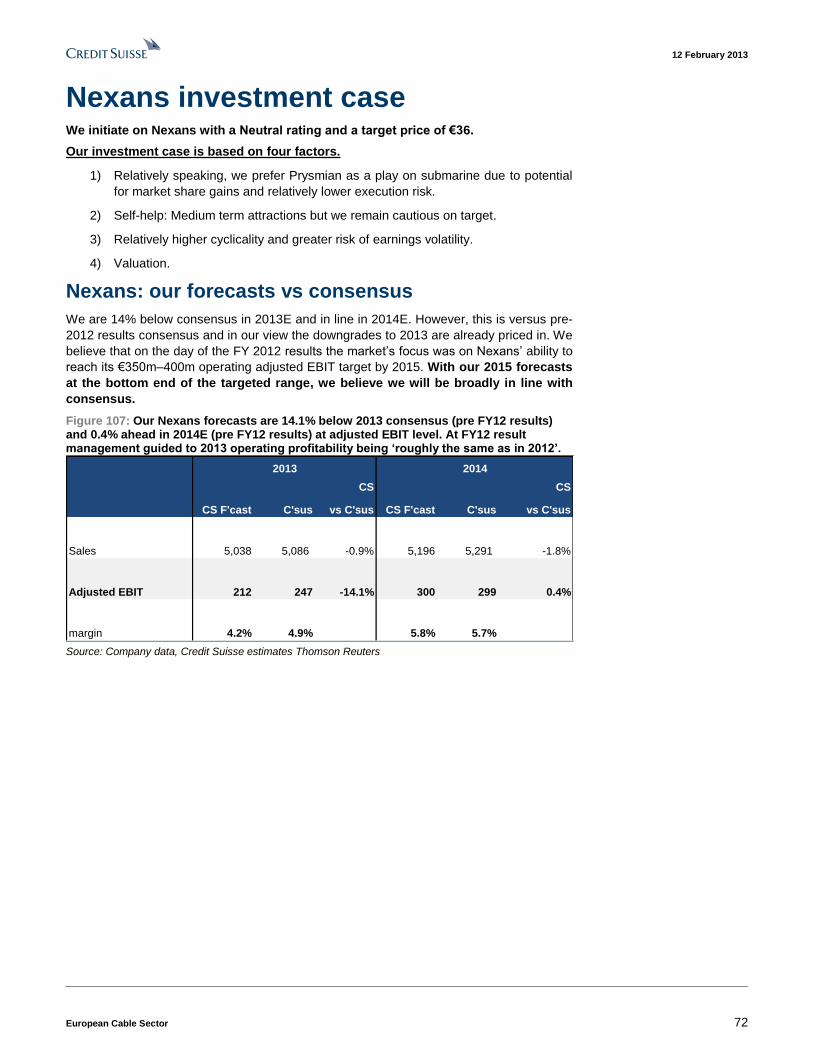

Nexans Investment Case Neutral, TP €36

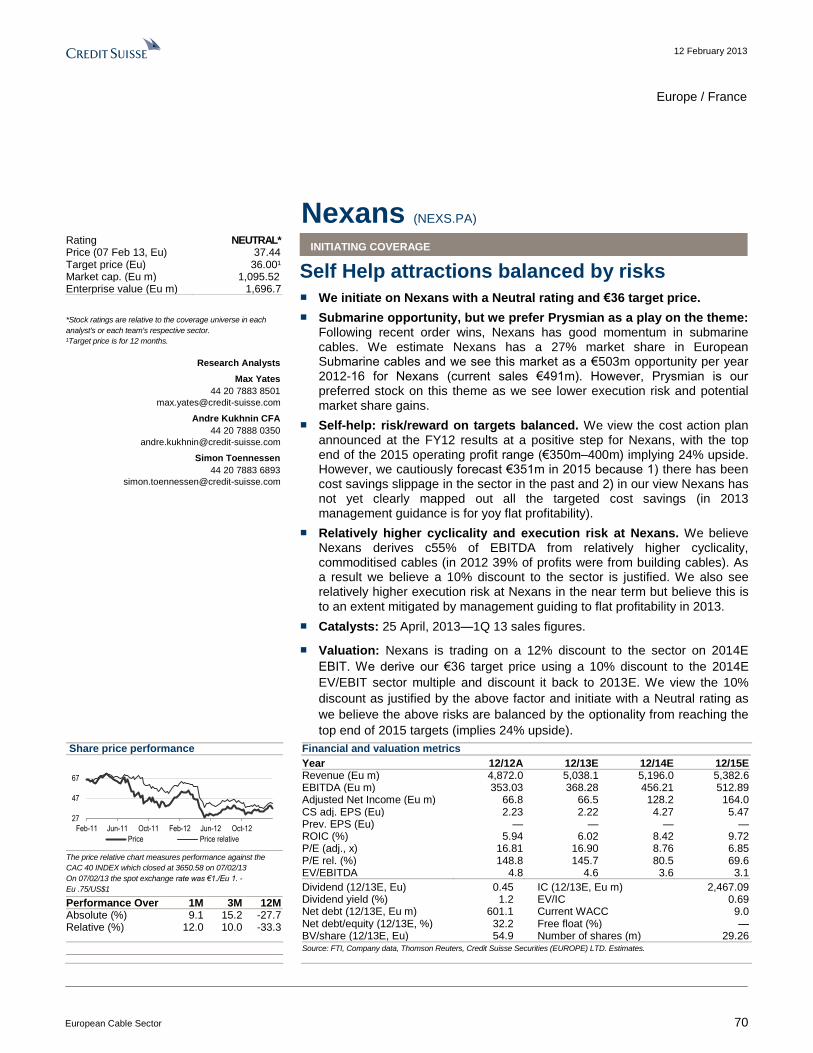

We initiate coverage of Nexans with a Neutral rating and a target price of €36.

Since a 22% share price decline in 2012 relating to submarine cable production issues

Nexans has given a 2015 target of €350m–400m of operating profit. In our view the 24%

potential upside from achieving the top end (€400m) 2015 targeted range is offset by its

competitive positioning, end market exposure and relatively higher execution risk.

Figure 18: Nexans investment case

Nexans Investment case: Comment

1) Submarine opportunity but we prefer

Prysmian in this market.

Following recent order wins, Nexans has strong momentum in submarine cables and we

view this as an attractive growth market for Nexans. We estimate Nexans has a 27%

market share in European submarine cables and we see this market as a a €503m

opportunity per year 2012-16 (current sales €491m). However, Prysmian is our preferred

stock in this market as we see lower execution risk and greater potential for Prysmian to

gain market share.

Self-Help: Limited upside from low end

of targets

We calculate the top end of the 2015 op. profit range (€350m-€400m) implies 24% upside

from current levels. However, we remain on the cautious side and forecast €351m in 2015

because 1) historically in the sector we have seen cost savings slippage and 2) in our view

Nexans have not yet clearly mapped out all of the targeted cost savings (there is expected

to be minimal contribution from cost savings in 2013).

3) Relatively higher cyclicality and

earnings volatility risk at Nexans.

We believe Nexans derives c55% of EBITDA from relatively higher cyclicality,

commoditized cables (in 2012 39% of profits were from building cables). As a result we

believe a 10% discount to the sector is justified. We also see relatively higher execution

risk at Nexans but believe this is to an extent mitigated by managements cautious

guidance of flat profitability in 2013.

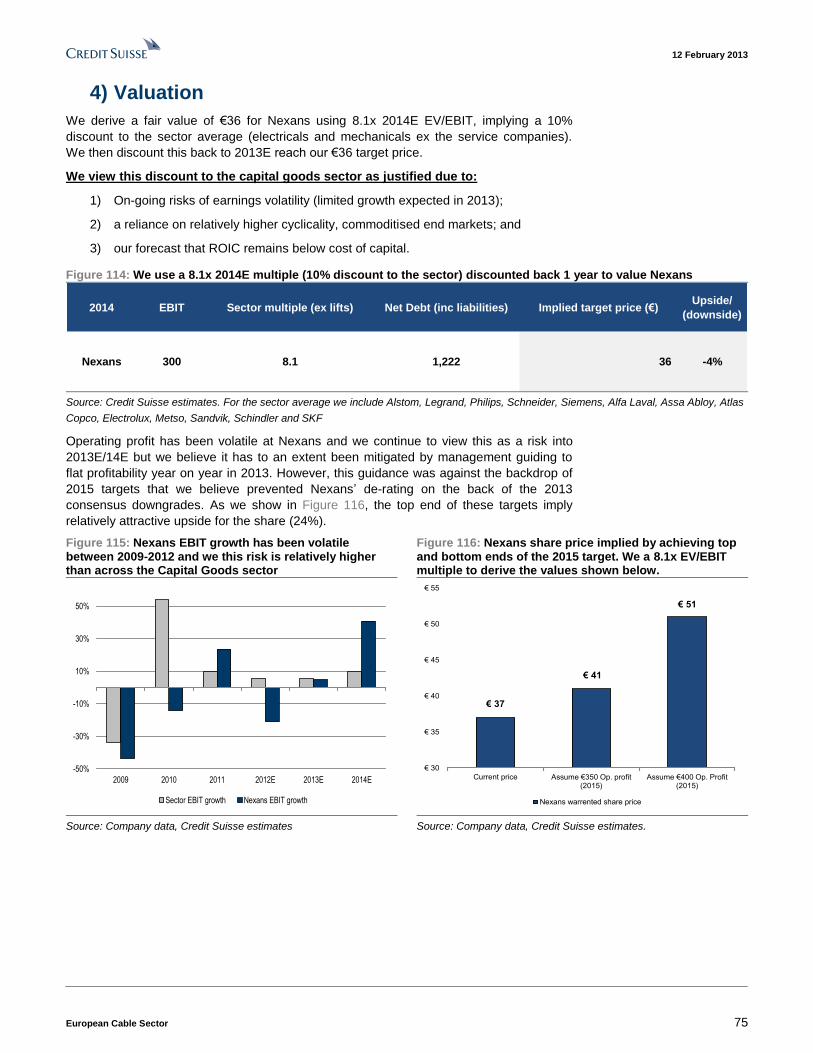

4) Valuation.

Nexans is trading on a 12% discount to the sector on 2014E EBIT. We derive our €36

target price using a 10% discount to the 2014E EV/EBIT sector multiple and discount it

back to 2013. We view the 10% discount as justified by the above factors but have a

neutral rating as we believe these factors are balanced by the 24% potential upside from

reaching the top end of 2015 operating profit targets. We also note the potential share

price support gained from Madeco (20% stake) exercising their right to raise their holding

to 28%.

Source: Company data, Credit Suisse estimates

Figure 19: Our Nexans adjusted EBIT forecasts are 14.1% below 2013 consensus (pre FY12 results) and 0.4% ahead in 2014E (pre FY12 results).

CS CS

CS F'cast C'sus vs C'sus CS F'cast C'sus vs C'sus

Sales 5,038 5,086 -0.9% 5,196 5,291 -1.8%

organic growth 1.6% 3.1%

Adjusted EBIT 212 247 -14.1% 300 299 0.4%

margin 4.2% 4.9% 5.8% 5.7%

2013 2014

Source: Credit Suisse estimates, Thomson Reuters

12 February 2013

European Cable Sector 9

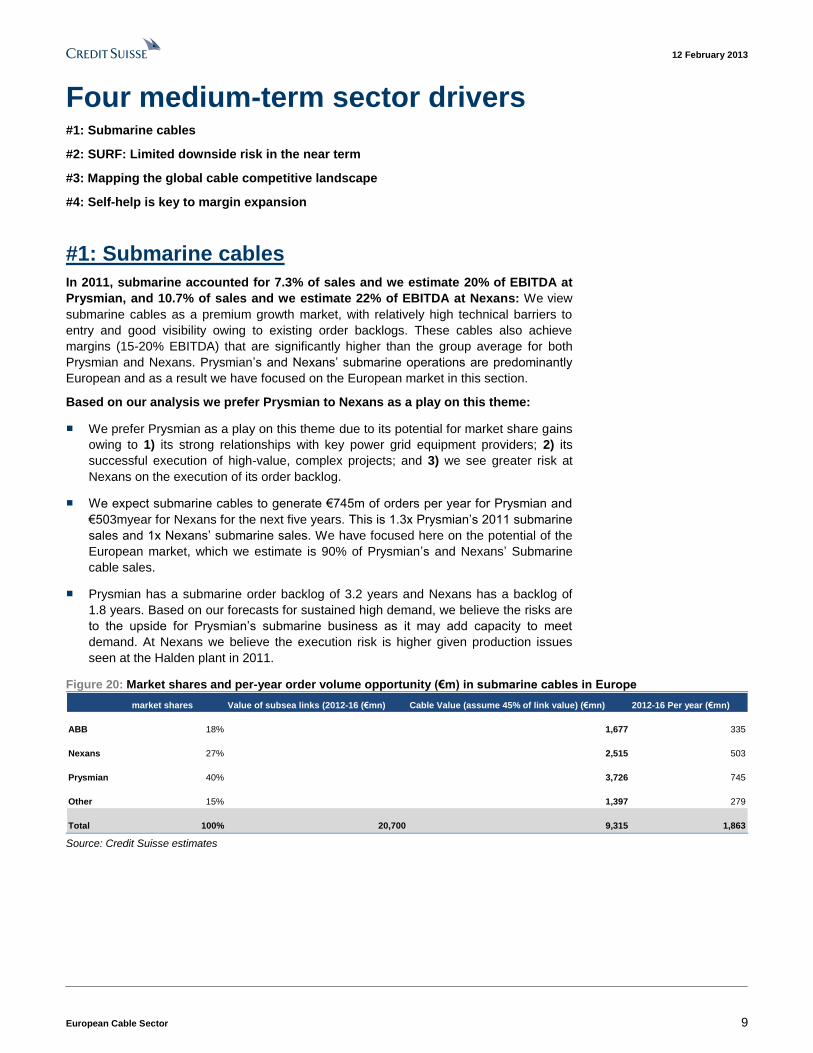

Four medium-term sector drivers #1: Submarine cables

#2: SURF: Limited downside risk in the near term

#3: Mapping the global cable competitive landscape

#4: Self-help is key to margin expansion

#1: Submarine cables

In 2011, submarine accounted for 7.3% of sales and we estimate 20% of EBITDA at

Prysmian, and 10.7% of sales and we estimate 22% of EBITDA at Nexans: We view

submarine cables as a premium growth market, with relatively high technical barriers to

entry and good visibility owing to existing order backlogs. These cables also achieve

margins (15-20% EBITDA) that are significantly higher than the group average for both

Prysmian and Nexans. Prysmian’s and Nexans’ submarine operations are predominantly

European and as a result we have focused on the European market in this section.

Based on our analysis we prefer Prysmian to Nexans as a play on this theme:

■ We prefer Prysmian as a play on this theme due to its potential for market share gains

owing to 1) its strong relationships with key power grid equipment providers; 2) its

successful execution of high-value, complex projects; and 3) we see greater risk at

Nexans on the execution of its order backlog.

■ We expect submarine cables to generate €745m of orders per year for Prysmian and

€503myear for Nexans for the next five years. This is 1.3x Prysmian’s 2011 submarine

sales and 1x Nexans’ submarine sales. We have focused here on the potential of the

European market, which we estimate is 90% of Prysmian’s and Nexans’ Submarine

cable sales.

■ Prysmian has a submarine order backlog of 3.2 years and Nexans has a backlog of

1.8 years. Based on our forecasts for sustained high demand, we believe the risks are

to the upside for Prysmian’s submarine business as it may add capacity to meet

demand. At Nexans we believe the execution risk is higher given production issues

seen at the Halden plant in 2011.

Figure 20: Market shares and per-year order volume opportunity (€m) in submarine cables in Europe

market shares Value of subsea links (2012-16 (€mn) Cable Value (assume 45% of link value) (€mn) 2012-16 Per year (€mn)

ABB 18% 1,677 335

Nexans 27% 2,515 503

Prysmian 40% 3,726 745

Other 15% 1,397 279

Total 100% 20,700 9,315 1,863 Source: Credit Suisse estimates

12 February 2013

European Cable Sector 10

Forecasting grid investment over the next 10 years

To forecast the submarine cable market we have used data from the Ten Year Network

Development Plan (TYNDP) 2012, which analyses required grid investment based on

research and feedback from stakeholders.

According to the TYNDP 2012 renewable capacity will increase by 250GW over the next

ten years. Renewable additions are most commonly away from the areas of high electricity

demand (eg off-shore wind) and as a result electricity will have to travel further through the

grid to meet demand. This is forecast to drive total investment in the grid of €104bn,

of which €23bn is for subsea cables.

In Figure 21 we show the TYNDP forecasts broken down by cable type for subsea cables

in the medium term (2012-2017) and the long term (2017-2022). We highlight that

submarine in this instance includes interconnections (to connect Islands or regions under

the sea) and off-shore wind connection cables (to connect off-shore wind farms to the

grid).

Figure 21: The TYNDP forecasts subsea cables in the medium term (2012-17) to account

for 46% of extra high voltage cables (KM)

0

10000

20000

30000

40000

Mid Term (2012-2017) Long Term (2017-2022)

Subsea Cables Overhead Lines Inland Cables Upgrades

Source: TYNDP 2012

From Figure 21 we would highlight:

■ Over the next ten years, €23bn is expected to be spent on subsea links and we

estimate 45% (€10.4bn) of this will be related specifically to cables and therefore

within Prysmian’s and Nexans’ addressable markets.

■ 90% (€20.7bn) of subsea links in the TYNDP are expected to be installed in the next

five years. This makes the total subsea link market (including substations, cables and

other equipment) valued at €4.1bn per year for the next five years.

■ Assuming 45% of the cost of subsea links is associated with the cables, we

estimate the total value of the cable market at €1.9bn per year.

12 February 2013

European Cable Sector 11

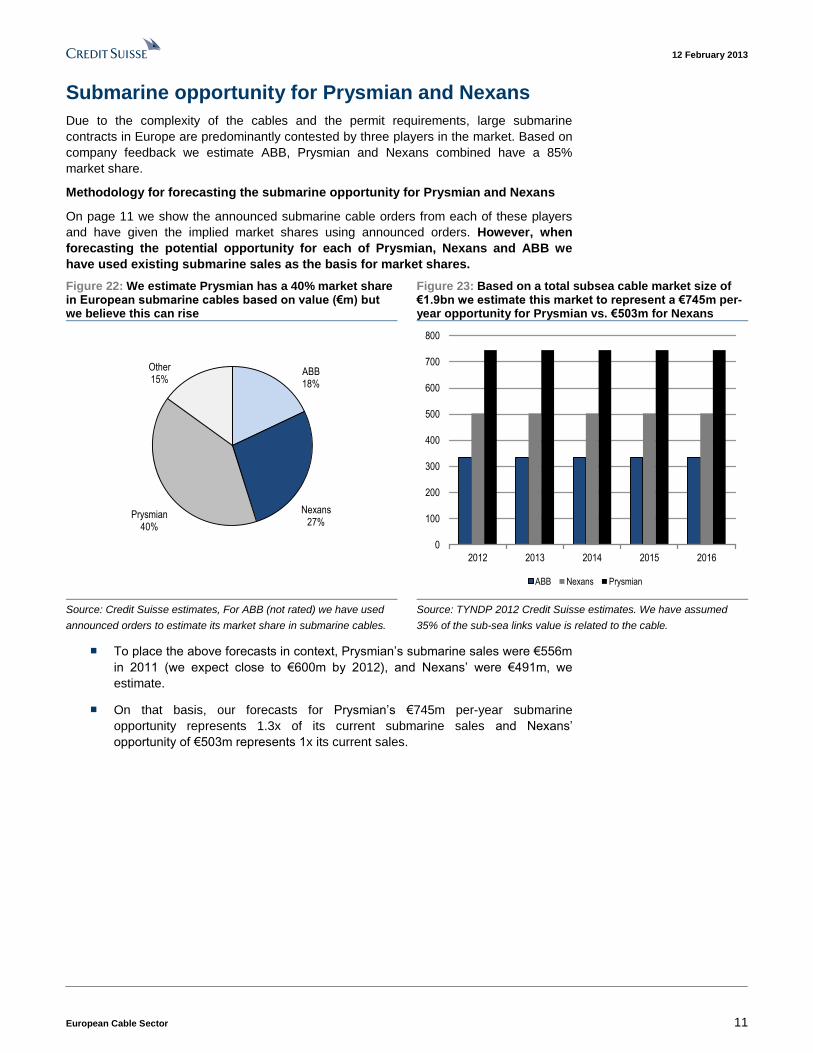

Submarine opportunity for Prysmian and Nexans

Due to the complexity of the cables and the permit requirements, large submarine

contracts in Europe are predominantly contested by three players in the market. Based on

company feedback we estimate ABB, Prysmian and Nexans combined have a 85%

market share.

Methodology for forecasting the submarine opportunity for Prysmian and Nexans

On page 11 we show the announced submarine cable orders from each of these players

and have given the implied market shares using announced orders. However, when

forecasting the potential opportunity for each of Prysmian, Nexans and ABB we

have used existing submarine sales as the basis for market shares.

Figure 22: We estimate Prysmian has a 40% market share in European submarine cables based on value (€m) but we believe this can rise

Figure 23: Based on a total subsea cable market size of €1.9bn we estimate this market to represent a €745m per-year opportunity for Prysmian vs. €503m for Nexans

ABB18%

Nexans 27%

Prysmian40%

Other15%

0

100

200

300

400

500

600

700

800

2012 2013 2014 2015 2016

ABB Nexans Prysmian

Source: Credit Suisse estimates, For ABB (not rated) we have used

announced orders to estimate its market share in submarine cables.

Source: TYNDP 2012 Credit Suisse estimates. We have assumed

35% of the sub-sea links value is related to the cable.

■ To place the above forecasts in context, Prysmian’s submarine sales were €556m

in 2011 (we expect close to €600m by 2012), and Nexans’ were €491m, we

estimate.

■ On that basis, our forecasts for Prysmian’s €745m per-year submarine

opportunity represents 1.3x of its current submarine sales and Nexans’

opportunity of €503m represents 1x its current sales.

12 February 2013

European Cable Sector 12

Prysmian’s market share may increase in the

medium term

We see Prysmian’s market share in the submarine market as well established and,

based on its ability to bring on new capacity, we see potential for this share to rise.

■ Prysmian has established relationships with key power grid equipment players, eg

Siemens. Siemens is not only prominent in installing offshore wind turbines in Europe

(74% share in 2012) but also in providing the substations to connect wind farms to the

grid (Figure 25).

■ Prysmian has the most experience in complex, high-value extra high voltage (EHV)

interconnections and in offshore wind connections, which are among the deepest and

furthest offshore connections that have been laid. The European Wind Energy

Association expects both the average water depth and distance to shore of projects to

increase over the coming years.

In our view, Prysmian is not only gaining ground in interconnections (traditionally Nexans’

core market) but also consolidating its position in offshore wind cables. In Figure 24 we

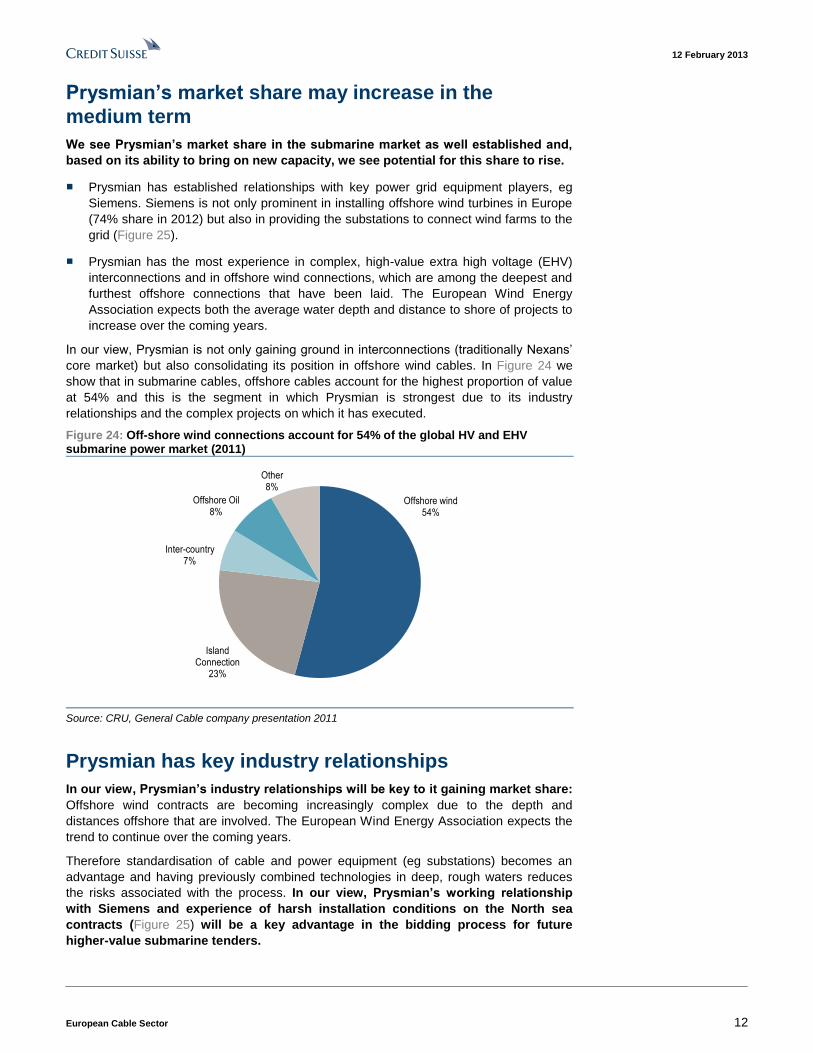

show that in submarine cables, offshore cables account for the highest proportion of value

at 54% and this is the segment in which Prysmian is strongest due to its industry

relationships and the complex projects on which it has executed.

Figure 24: Off-shore wind connections account for 54% of the global HV and EHV submarine power market (2011)

Offshore wind54%

Island Connection

23%

Inter-country7%

Offshore Oil8%

Other8%

Source: CRU, General Cable company presentation 2011

Prysmian has key industry relationships

In our view, Prysmian’s industry relationships will be key to it gaining market share:

Offshore wind contracts are becoming increasingly complex due to the depth and

distances offshore that are involved. The European Wind Energy Association expects the

trend to continue over the coming years.

Therefore standardisation of cable and power equipment (eg substations) becomes an

advantage and having previously combined technologies in deep, rough waters reduces

the risks associated with the process. In our view, Prysmian’s working relationship

with Siemens and experience of harsh installation conditions on the North sea

contracts (Figure 25) will be a key advantage in the bidding process for future

higher-value submarine tenders.

12 February 2013

European Cable Sector 13

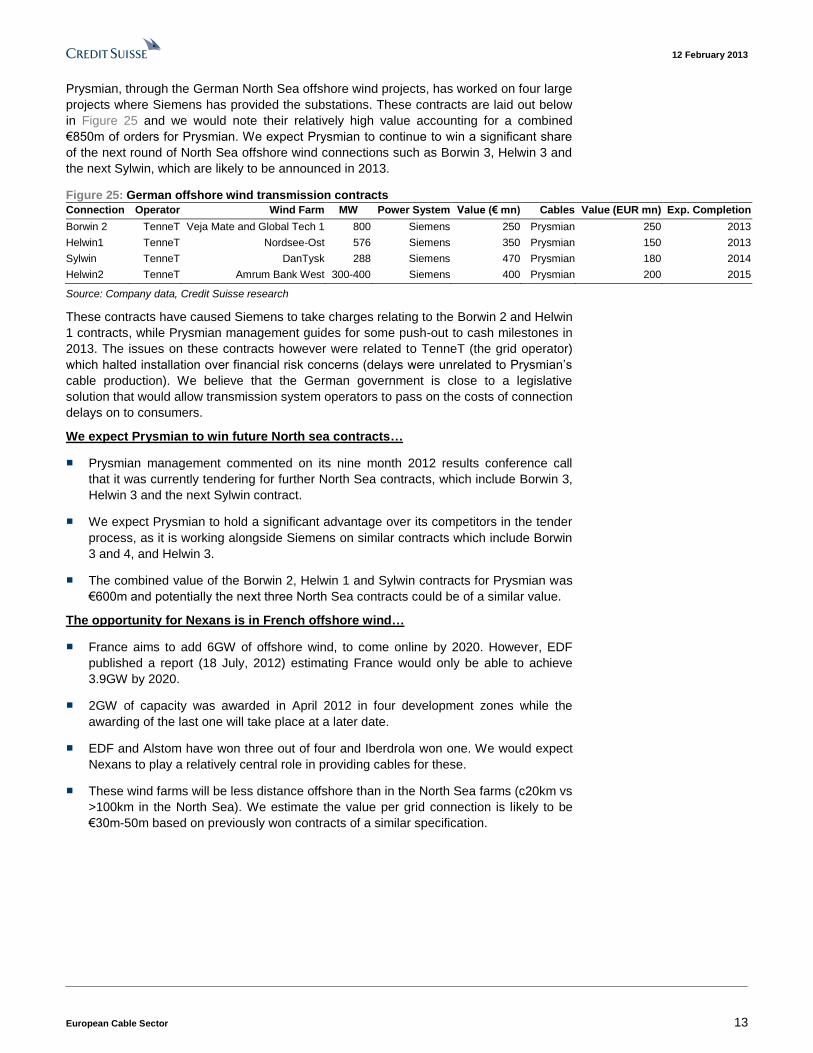

Prysmian, through the German North Sea offshore wind projects, has worked on four large

projects where Siemens has provided the substations. These contracts are laid out below

in Figure 25 and we would note their relatively high value accounting for a combined

€850m of orders for Prysmian. We expect Prysmian to continue to win a significant share

of the next round of North Sea offshore wind connections such as Borwin 3, Helwin 3 and

the next Sylwin, which are likely to be announced in 2013.

Figure 25: German offshore wind transmission contracts

Connection Operator Wind Farm MW Power System Value (€ mn) Cables Value (EUR mn) Exp. Completion

Borwin 2 TenneT Veja Mate and Global Tech 1 800 Siemens 250 Prysmian 250 2013

Helwin1 TenneT Nordsee-Ost 576 Siemens 350 Prysmian 150 2013

Sylwin TenneT DanTysk 288 Siemens 470 Prysmian 180 2014

Helwin2 TenneT Amrum Bank West 300-400 Siemens 400 Prysmian 200 2015

Source: Company data, Credit Suisse research

These contracts have caused Siemens to take charges relating to the Borwin 2 and Helwin

1 contracts, while Prysmian management guides for some push-out to cash milestones in

2013. The issues on these contracts however were related to TenneT (the grid operator)

which halted installation over financial risk concerns (delays were unrelated to Prysmian’s

cable production). We believe that the German government is close to a legislative

solution that would allow transmission system operators to pass on the costs of connection

delays on to consumers.

We expect Prysmian to win future North sea contracts…

■ Prysmian management commented on its nine month 2012 results conference call

that it was currently tendering for further North Sea contracts, which include Borwin 3,

Helwin 3 and the next Sylwin contract.

■ We expect Prysmian to hold a significant advantage over its competitors in the tender

process, as it is working alongside Siemens on similar contracts which include Borwin

3 and 4, and Helwin 3.

■ The combined value of the Borwin 2, Helwin 1 and Sylwin contracts for Prysmian was

€600m and potentially the next three North Sea contracts could be of a similar value.

The opportunity for Nexans is in French offshore wind…

■ France aims to add 6GW of offshore wind, to come online by 2020. However, EDF

published a report (18 July, 2012) estimating France would only be able to achieve

3.9GW by 2020.

■ 2GW of capacity was awarded in April 2012 in four development zones while the

awarding of the last one will take place at a later date.

■ EDF and Alstom have won three out of four and Iberdrola won one. We would expect

Nexans to play a relatively central role in providing cables for these.

■ These wind farms will be less distance offshore than in the North Sea farms (c20km vs

>100km in the North Sea). We estimate the value per grid connection is likely to be

€30m-50m based on previously won contracts of a similar specification.

12 February 2013

European Cable Sector 14

Prysmian has won higher value, higher specification

Submarine cable contracts

We also believe Prysmian may take share via winning the higher value, more

complex submarine contracts which we have seen since 2010.

In Figure 28 we have listed announced submarine contract wins in Europe—on average

Prysmian’s value per contract has been €266m vs. €105m per contract at Nexans.

The European Wind Energy Association expects the trend towards large projects to

continue over the coming years with both average water depth and distance to shore

expected to increase.

In the last two years, Prysmian has won large contracts including the €800m Westlink

interconnection and the German offshore wind contracts. Not only are these contracts of

significant value but the company is achieving record technical specifications on them.

■ For example, the €800m Westlink interconnection contract set a record in terms of

voltage for an insulated cable as it will achieve 600KV.

■ Similarly the German offshore wind connections in the North Sea have involved

Siemens’ Voltage Sourced Converters (VSC), which has allowed Prysmian to use

extruded HVDC cables for the connections. These were the first commercial 300KV

DC cables made using extruded technology, which has the advantage of being lighter

and less susceptible to faults than impregnated technology.

As a result of these advances, we expect Prysmian to remain the market leader with an

opportunity to extend its market share (in euro value terms) depending on its ability to

increase capacity. However, we expect Prysmian to remain at the forefront of cable

technology resulting in its winning the higher value submarine contracts.

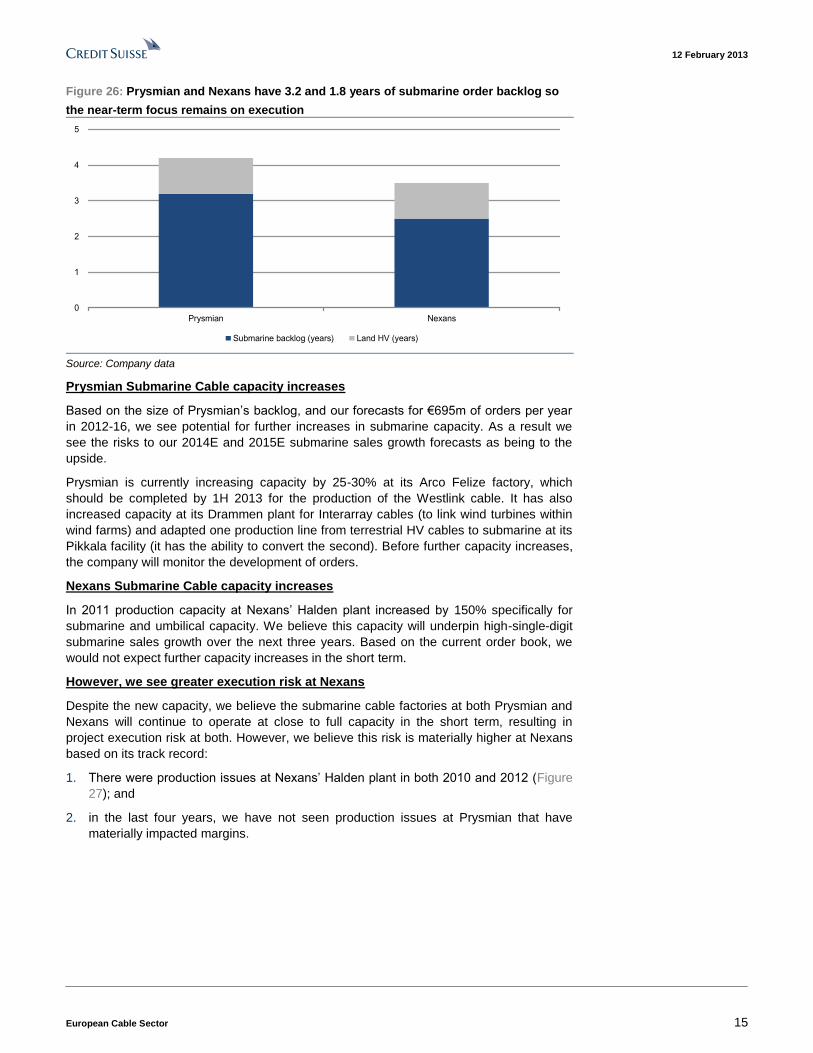

We also see greater project execution risk at Nexans

Submarine cable production processes are very complex. Due to undersupply in Europe,

Prysmian and Nexans’ submarine factories are running at full capacity. Figure 26 shows

Prysmian’s and Nexans’ order backlogs in submarine and high voltage cables, indicating

greater earnings visibility at Prysmian. We also believe there is greater execution risk at

Nexans based on a recent production issue at its Halden plant. Despite announced

plans to increase capacity at Prysmian, and past increases at Nexans, we expect

both to continue running their submarine plants at near-full capacity over the next

12 months.

12 February 2013

European Cable Sector 15

Figure 26: Prysmian and Nexans have 3.2 and 1.8 years of submarine order backlog so

the near-term focus remains on execution

0

1

2

3

4

5

Prysmian Nexans

Submarine backlog (years) Land HV (years)

Source: Company data

Prysmian Submarine Cable capacity increases

Based on the size of Prysmian’s backlog, and our forecasts for €695m of orders per year

in 2012-16, we see potential for further increases in submarine capacity. As a result we

see the risks to our 2014E and 2015E submarine sales growth forecasts as being to the

upside.

Prysmian is currently increasing capacity by 25-30% at its Arco Felize factory, which

should be completed by 1H 2013 for the production of the Westlink cable. It has also

increased capacity at its Drammen plant for Interarray cables (to link wind turbines within

wind farms) and adapted one production line from terrestrial HV cables to submarine at its

Pikkala facility (it has the ability to convert the second). Before further capacity increases,

the company will monitor the development of orders.

Nexans Submarine Cable capacity increases

In 2011 production capacity at Nexans’ Halden plant increased by 150% specifically for

submarine and umbilical capacity. We believe this capacity will underpin high-single-digit

submarine sales growth over the next three years. Based on the current order book, we

would not expect further capacity increases in the short term.

However, we see greater execution risk at Nexans

Despite the new capacity, we believe the submarine cable factories at both Prysmian and

Nexans will continue to operate at close to full capacity in the short term, resulting in

project execution risk at both. However, we believe this risk is materially higher at Nexans

based on its track record:

1. There were production issues at Nexans’ Halden plant in both 2010 and 2012 (Figure

27); and

2. in the last four years, we have not seen production issues at Prysmian that have

materially impacted margins.

12 February 2013

European Cable Sector 16

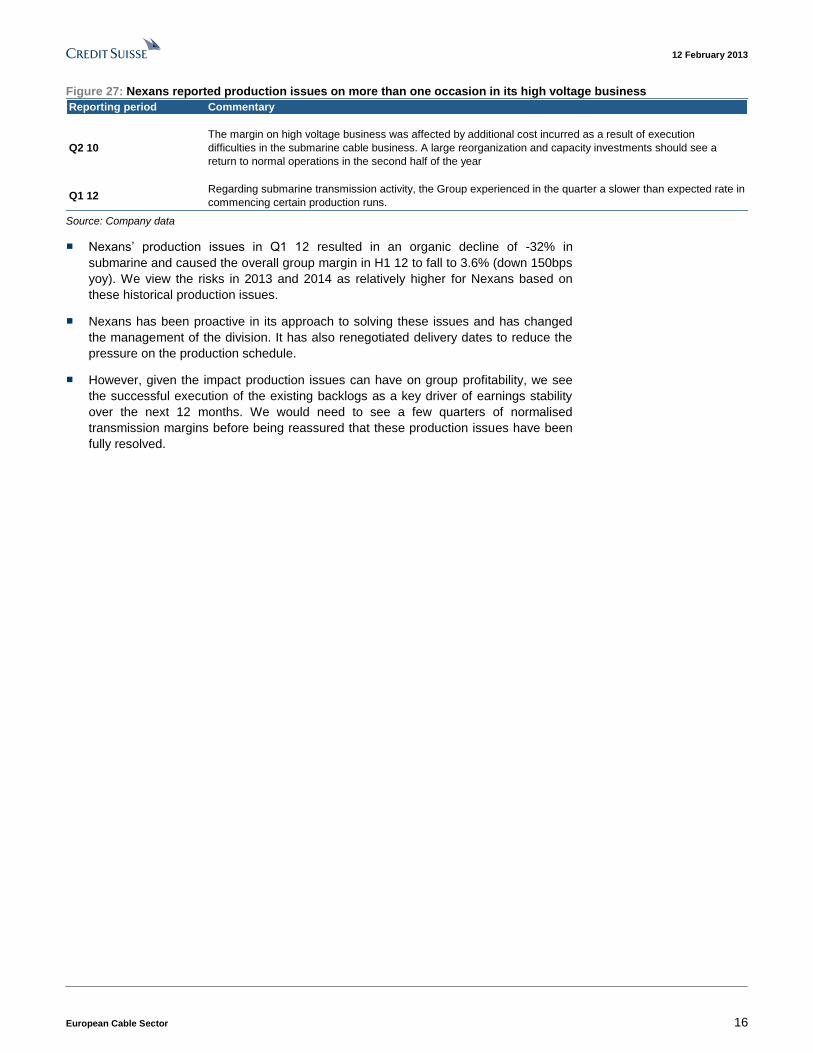

Figure 27: Nexans reported production issues on more than one occasion in its high voltage business

Reporting period Commentary

Q2 10

The margin on high voltage business was affected by additional cost incurred as a result of execution

difficulties in the submarine cable business. A large reorganization and capacity investments should see a

return to normal operations in the second half of the year

Q1 12Regarding submarine transmission activity, the Group experienced in the quarter a slower than expected rate in

commencing certain production runs. Source: Company data

■ Nexans’ production issues in Q1 12 resulted in an organic decline of -32% in

submarine and caused the overall group margin in H1 12 to fall to 3.6% (down 150bps

yoy). We view the risks in 2013 and 2014 as relatively higher for Nexans based on

these historical production issues.

■ Nexans has been proactive in its approach to solving these issues and has changed

the management of the division. It has also renegotiated delivery dates to reduce the

pressure on the production schedule.

■ However, given the impact production issues can have on group profitability, we see

the successful execution of the existing backlogs as a key driver of earnings stability

over the next 12 months. We would need to see a few quarters of normalised

transmission margins before being reassured that these production issues have been

fully resolved.

12 February 2013

European Cable Sector 17

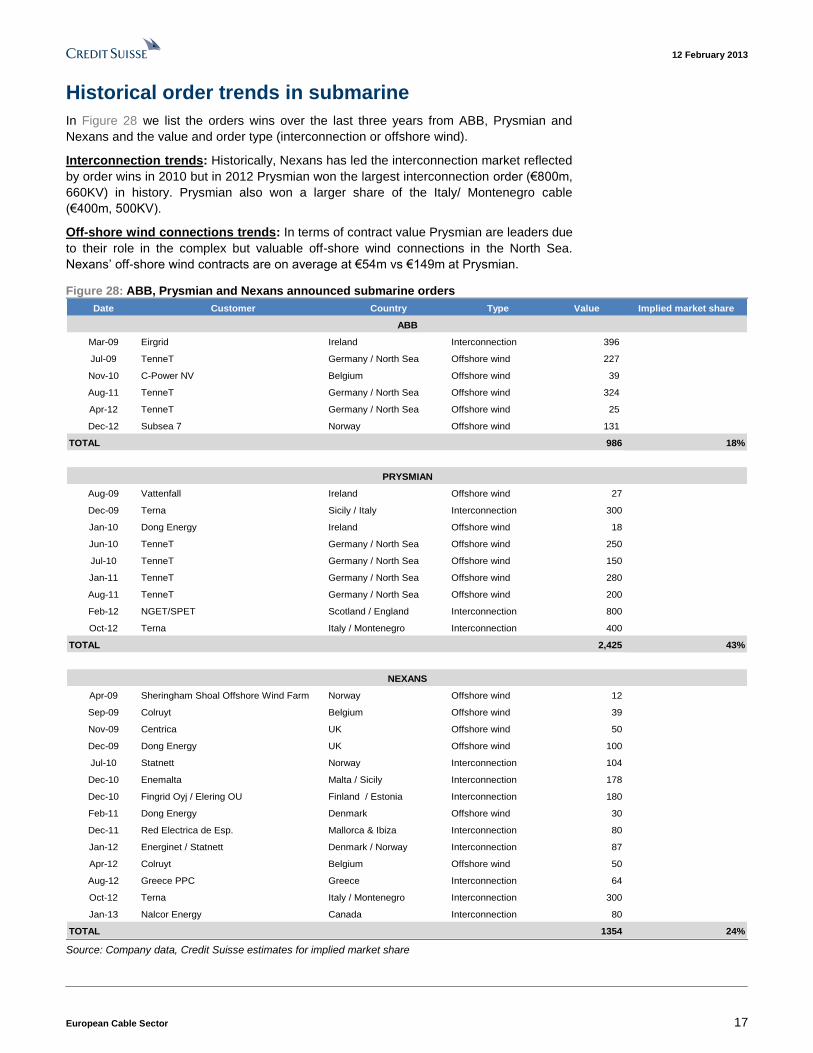

Historical order trends in submarine

In Figure 28 we list the orders wins over the last three years from ABB, Prysmian and

Nexans and the value and order type (interconnection or offshore wind).

Interconnection trends: Historically, Nexans has led the interconnection market reflected

by order wins in 2010 but in 2012 Prysmian won the largest interconnection order (€800m,

660KV) in history. Prysmian also won a larger share of the Italy/ Montenegro cable

(€400m, 500KV).

Off-shore wind connections trends: In terms of contract value Prysmian are leaders due

to their role in the complex but valuable off-shore wind connections in the North Sea.

Nexans’ off-shore wind contracts are on average at €54m vs €149m at Prysmian.

Figure 28: ABB, Prysmian and Nexans announced submarine orders

Date Customer Country Type Value Implied market share

Mar-09 Eirgrid Ireland Interconnection 396

Jul-09 TenneT Germany / North Sea Offshore wind 227

Nov-10 C-Power NV Belgium Offshore wind 39

Aug-11 TenneT Germany / North Sea Offshore wind 324

Apr-12 TenneT Germany / North Sea Offshore wind 25

Dec-12 Subsea 7 Norway Offshore wind 131

TOTAL 986 18%

Aug-09 Vattenfall Ireland Offshore wind 27

Dec-09 Terna Sicily / Italy Interconnection 300

Jan-10 Dong Energy Ireland Offshore wind 18

Jun-10 TenneT Germany / North Sea Offshore wind 250

Jul-10 TenneT Germany / North Sea Offshore wind 150

Jan-11 TenneT Germany / North Sea Offshore wind 280

Aug-11 TenneT Germany / North Sea Offshore wind 200

Feb-12 NGET/SPET Scotland / England Interconnection 800

Oct-12 Terna Italy / Montenegro Interconnection 400

TOTAL 2,425 43%

Apr-09 Sheringham Shoal Offshore Wind Farm Norway Offshore wind 12

Sep-09 Colruyt Belgium Offshore wind 39

Nov-09 Centrica UK Offshore wind 50

Dec-09 Dong Energy UK Offshore wind 100

Jul-10 Statnett Norway Interconnection 104

Dec-10 Enemalta Malta / Sicily Interconnection 178

Dec-10 Fingrid Oyj / Elering OU Finland / Estonia Interconnection 180

Feb-11 Dong Energy Denmark Offshore wind 30

Dec-11 Red Electrica de Esp. Mallorca & Ibiza Interconnection 80

Jan-12 Energinet / Statnett Denmark / Norway Interconnection 87

Apr-12 Colruyt Belgium Offshore wind 50

Aug-12 Greece PPC Greece Interconnection 64

Oct-12 Terna Italy / Montenegro Interconnection 300

Jan-13 Nalcor Energy Canada Interconnection 80

TOTAL 1354 24%

NEXANS

PRYSMIAN

ABB

Source: Company data, Credit Suisse estimates for implied market share

12 February 2013

European Cable Sector 18

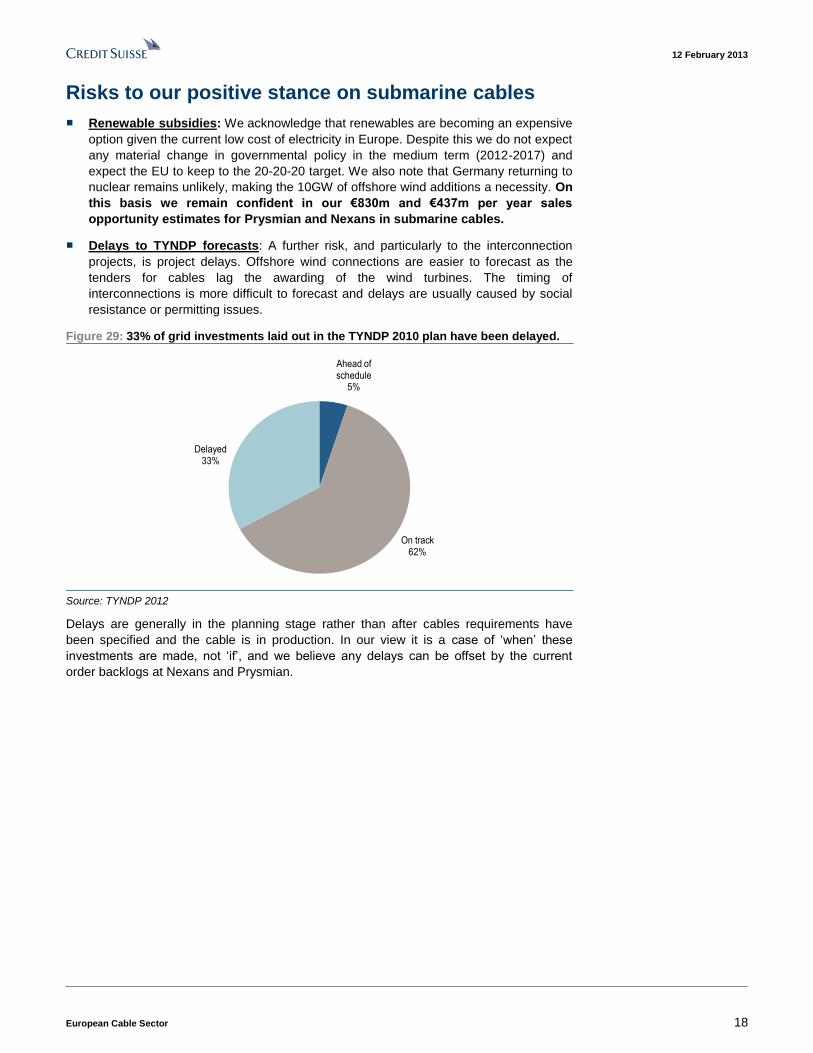

Risks to our positive stance on submarine cables

■ Renewable subsidies: We acknowledge that renewables are becoming an expensive

option given the current low cost of electricity in Europe. Despite this we do not expect

any material change in governmental policy in the medium term (2012-2017) and

expect the EU to keep to the 20-20-20 target. We also note that Germany returning to

nuclear remains unlikely, making the 10GW of offshore wind additions a necessity. On

this basis we remain confident in our €830m and €437m per year sales

opportunity estimates for Prysmian and Nexans in submarine cables.

■ Delays to TYNDP forecasts: A further risk, and particularly to the interconnection

projects, is project delays. Offshore wind connections are easier to forecast as the

tenders for cables lag the awarding of the wind turbines. The timing of

interconnections is more difficult to forecast and delays are usually caused by social

resistance or permitting issues.

Figure 29: 33% of grid investments laid out in the TYNDP 2010 plan have been delayed.

Ahead of schedule

5%

On track62%

Delayed33%

Source: TYNDP 2012

Delays are generally in the planning stage rather than after cables requirements have

been specified and the cable is in production. In our view it is a case of ‘when’ these

investments are made, not ‘if’, and we believe any delays can be offset by the current

order backlogs at Nexans and Prysmian.

12 February 2013

European Cable Sector 19

#2: SURF: Limited downside risk in the near term

SURF (Subsea Umbilicals, Risers (or flexible pipes) & Flow lines) accounts for 2% of

group sales but we view it as an important growth driver and in our base case it accounts

for 12% and 20% of incremental group EBITDA in 2013E and 2014E, respectively.

We believe the market has become overly concerned regarding Prysmian’s ability to ramp

up capacity utilisation (currently 20%) in flexible pipes at its Vila Velha plant following

Petrobras’ (largest customer) 2012-2016 business plan release (June 2012). This is

because 1) it is a newly built asset that could result in potential write-downs and 2) SURF

is an important growth driver for Prysmian owing to the flexible pipe capacity ramp-up and

high margins on these products. We have also looked at Saipem’s (Oil Field services)

profit warning on 30/01/13 and see limited threat to our thesis for the SURF business.

In our base case for SURF we assume it accounts for 12% of the incremental EBITDA we

forecast for the group in 2013 and 20% in 2014. Stress testing our assumptions using a

bear case only implies 1.3% downgrades to our group EBITDA forecast in 2013 and 2014.

We worked with our Petrobras analyst and looked at competitors (Technip), and

conclude that these concerns are overdone. We would highlight the following:

■ PROMINP forecasts demand for flexible pipes in 2014 at 2,240 nKM vs. installed

production capacity in Brazil of 1,590 nKM (nKM stands for normalised kilometres),

which we believe underpins our base case SURF assumptions.

■ In our base case we forecast a conservative rise to 35% flexible pipe capacity

utilisation in 2013 rising to 80% by 2015. In 2013 and 2014 respectively our SURF

forecasts account for 12% and 20% of incremental EBITDA for the group

■ In our bear case scenario we see potential for limited downgrades to consensus

(-1.3%). However we would also note that in our base case scenario we see

upside risk for the remaining 93% of sales in the industrial division as our

current forecasts imply limited growth in these areas.

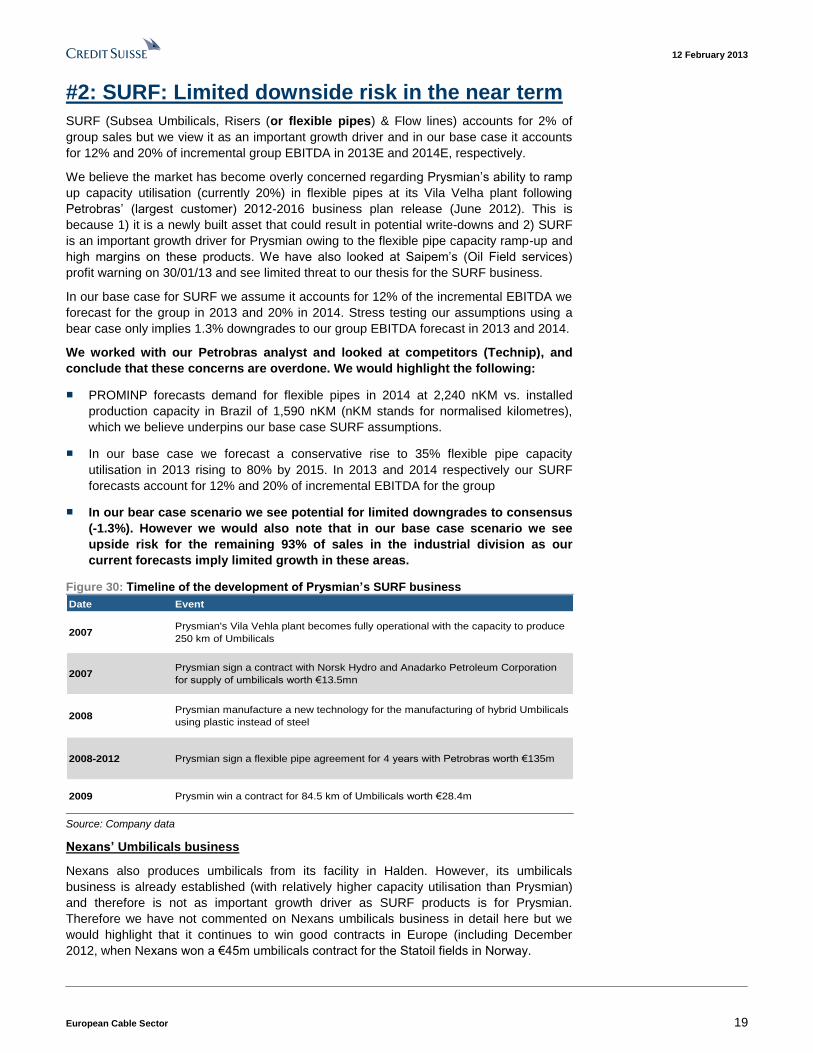

Figure 30: Timeline of the development of Prysmian’s SURF business

Date Event

2007Prysmian's Vila Vehla plant becomes fully operational with the capacity to produce

250 km of Umbilicals

2007Prysmian sign a contract with Norsk Hydro and Anadarko Petroleum Corporation

for supply of umbilicals worth €13.5mn

2008Prysmian manufacture a new technology for the manufacturing of hybrid Umbilicals

using plastic instead of steel

2008-2012 Prysmian sign a flexible pipe agreement for 4 years with Petrobras worth €135m

2009 Prysmin win a contract for 84.5 km of Umbilicals worth €28.4m

Source: Company data

Nexans’ Umbilicals business

Nexans also produces umbilicals from its facility in Halden. However, its umbilicals

business is already established (with relatively higher capacity utilisation than Prysmian)

and therefore is not as important growth driver as SURF products is for Prysmian.

Therefore we have not commented on Nexans umbilicals business in detail here but we

would highlight that it continues to win good contracts in Europe (including December

2012, when Nexans won a €45m umbilicals contract for the Statoil fields in Norway.

12 February 2013

European Cable Sector 20

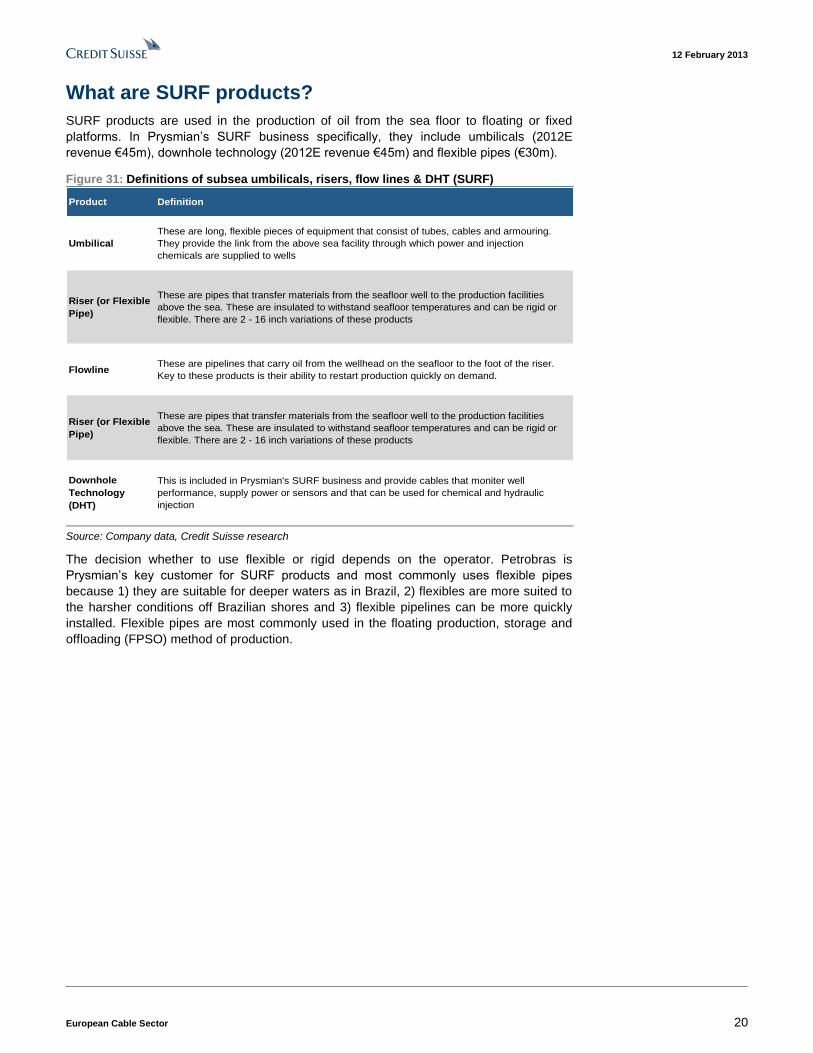

What are SURF products?

SURF products are used in the production of oil from the sea floor to floating or fixed

platforms. In Prysmian’s SURF business specifically, they include umbilicals (2012E

revenue €45m), downhole technology (2012E revenue €45m) and flexible pipes (€30m).

Figure 31: Definitions of subsea umbilicals, risers, flow lines & DHT (SURF)

Product Definition

Umbilical

These are long, flexible pieces of equipment that consist of tubes, cables and armouring.

They provide the link from the above sea facility through which power and injection

chemicals are supplied to wells

Riser (or Flexible

Pipe)

These are pipes that transfer materials from the seafloor well to the production facilities

above the sea. These are insulated to withstand seafloor temperatures and can be rigid or

flexible. There are 2 - 16 inch variations of these products

Flowline These are pipelines that carry oil from the wellhead on the seafloor to the foot of the riser.

Key to these products is their ability to restart production quickly on demand.

Riser (or Flexible

Pipe)

These are pipes that transfer materials from the seafloor well to the production facilities

above the sea. These are insulated to withstand seafloor temperatures and can be rigid or

flexible. There are 2 - 16 inch variations of these products

Downhole

Technology

(DHT)

This is included in Prysmian's SURF business and provide cables that moniter well

performance, supply power or sensors and that can be used for chemical and hydraulic

injection

Source: Company data, Credit Suisse research

The decision whether to use flexible or rigid depends on the operator. Petrobras is

Prysmian’s key customer for SURF products and most commonly uses flexible pipes

because 1) they are suitable for deeper waters as in Brazil, 2) flexibles are more suited to

the harsher conditions off Brazilian shores and 3) flexible pipelines can be more quickly

installed. Flexible pipes are most commonly used in the floating production, storage and

offloading (FPSO) method of production.

12 February 2013

European Cable Sector 21

Technical specifications of flexible pipes

■ Flexible pipes range from 2 inches to 16 inches in diameter.

■ The qualification process is complex, particularly for pre-salt conditions (water

depths of 2000KM+, high CO2 and H2S) which place extra pressure on the pipe.

■ Currently Technip and Wellstream are the largest producers of flexible pipes for

Petrobras and to an extent have a monopoly over the higher-end specification flexible

pipes.

■ Prysmian is qualified to produce 2- and 4-inch flexible pipes and is expected to gain

accreditation for 6-inch pipes from Petrobras in the near future. This broader offering

will allow Prysmian’s flexible pipes to be used in more locations in the Santos and

Campos basins.

The qualification process for flexible pipes is complex and makes flexible pipes relatively

R&D intensive. We believe there is a 4-5-year lead time for a new entrant to be able to

compete at the high end of the market, which is still dominated by Technip and

Wellstream.

On this basis Prysmian may be able to sell to the very high end (pre-salt) of the flexible

pipe market in 2014. However, qualification for high-end flexible pipes is not a formality

and NKT-flexibles have not managed to break the high-end duopoly of Technip and

Wellstream despite being in this market for a relatively long time.

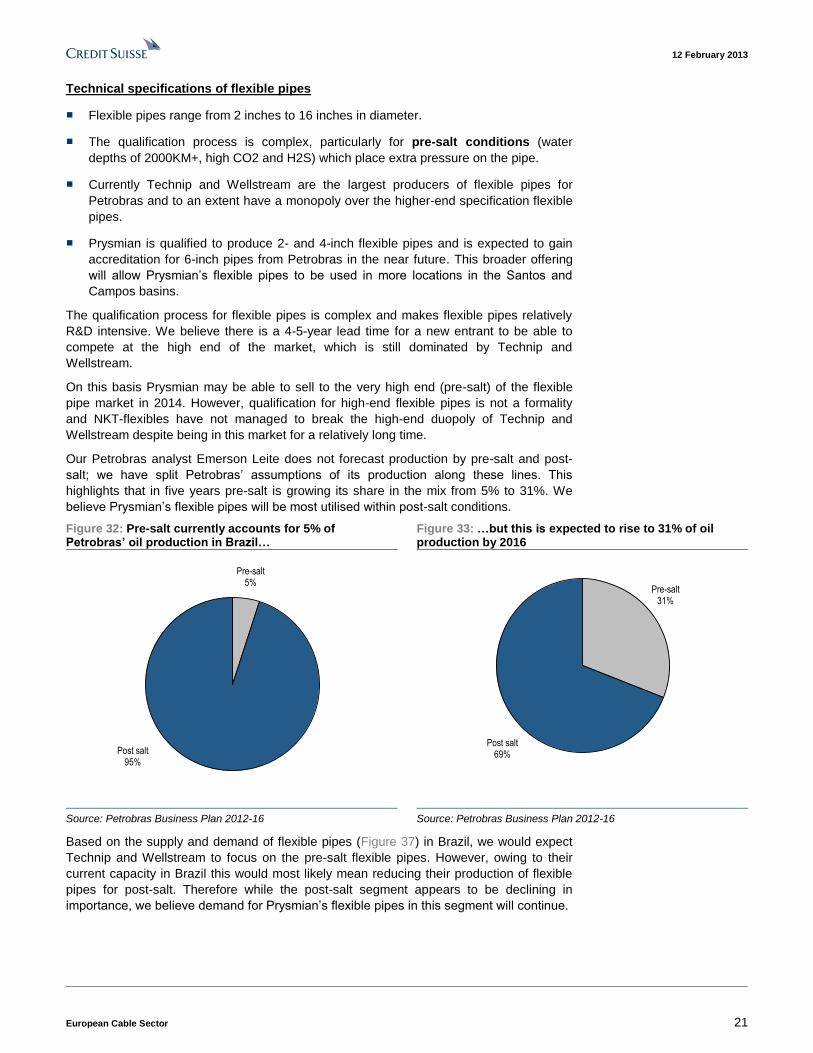

Our Petrobras analyst Emerson Leite does not forecast production by pre-salt and post-

salt; we have split Petrobras’ assumptions of its production along these lines. This

highlights that in five years pre-salt is growing its share in the mix from 5% to 31%. We

believe Prysmian’s flexible pipes will be most utilised within post-salt conditions.

Figure 32: Pre-salt currently accounts for 5% of Petrobras’ oil production in Brazil…

Figure 33: …but this is expected to rise to 31% of oil production by 2016

Pre-salt 5%

Post salt95%

Pre-salt 31%

Post salt69%

Source: Petrobras Business Plan 2012-16 Source: Petrobras Business Plan 2012-16

Based on the supply and demand of flexible pipes (Figure 37) in Brazil, we would expect

Technip and Wellstream to focus on the pre-salt flexible pipes. However, owing to their

current capacity in Brazil this would most likely mean reducing their production of flexible

pipes for post-salt. Therefore while the post-salt segment appears to be declining in

importance, we believe demand for Prysmian’s flexible pipes in this segment will continue.

12 February 2013

European Cable Sector 22

Why is the market concerned about SURF products?

Petrobras’ 2012-16 business plan and management change have had a negative

readacross to Prysmian based on the cost-saving focus that could affect the ramp-up of its

Vila Velha plant. While we do not believe it has materially affected consensus forecasts,

this was one of the bull cases for Prysmian in 1H12 and we believe recent news flow may

have weighed on the multiple. We assume only a moderate pick-up in capacity in

2013E, but based on the currently tight flexible pipe market in Brazil we expect

capacity saturation can be achieved by 2015.

Key points of the Petrobras 2012-2016 business plan

■ Exploration and production will account for 60% of Petrobras’ total investment

between 2012 and 2016 of US$236.5bn.

■ All projects under implementation or evaluation will be monitored and evaluated using

the physical and financial evolution of the project.

■ There are three structural programmes: 1) Campos basin operational efficiency

improvement programme, 2) operational cost optimisation programme and 3) local

content management programme.

We view these concerns as overdone

■ The cost of flexible pipe is low relative to the entire production process and therefore

we think it unlikely these will be a focus of Petrobras’ plan. Furthermore, as part of the

2012-16 plan Petrobras has committed to “maximizing the use of the Brazilian

equipment and services industry capacity…”. We believe this focus is positive for

Prysmian given it produces its flexible pipes locally at its Vila Velha plant in Brazil.

■ Petrobras continues to encourage large players (Wellstream and Technip) to add

Flexible pipe capacity in Brazil. Technip is installing a new plant and Wellstream is

planning plant expansions in 2013, reflecting the tight flexible pipe market in Brazil.

Demand for flexible pipes in Brazil is still forecast by PROMINP to be 40% higher

than installed flexible pipe capacity in 2014 (see Figure 37).

■ Prysmian has started to deliver flexible pipes produced at the Vila Velha plants outside

Brazil, which can help offset any short-term soft demand from Petrobras.

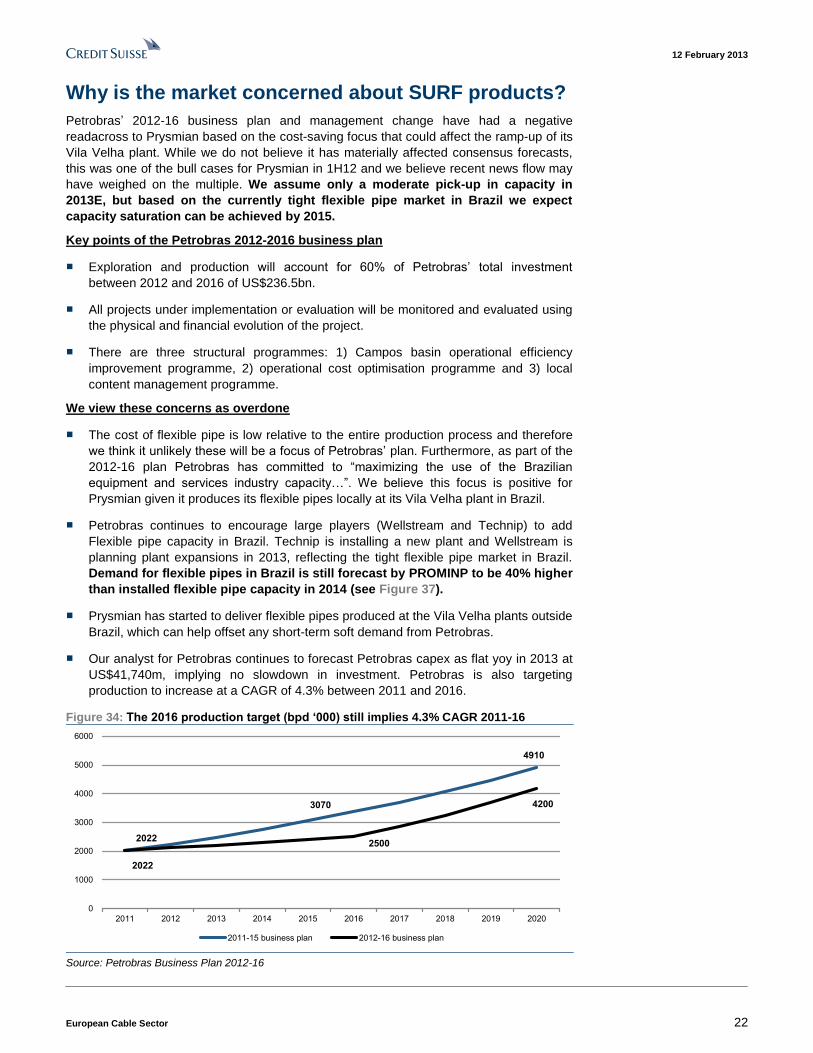

■ Our analyst for Petrobras continues to forecast Petrobras capex as flat yoy in 2013 at

US$41,740m, implying no slowdown in investment. Petrobras is also targeting

production to increase at a CAGR of 4.3% between 2011 and 2016.

Figure 34: The 2016 production target (bpd ‘000) still implies 4.3% CAGR 2011-16

2022

3070

4910

2022

2500

4200

0

1000

2000

3000

4000

5000

6000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

2011-15 business plan 2012-16 business plan

Source: Petrobras Business Plan 2012-16

12 February 2013

European Cable Sector 23

Further offshore O&G news flow: Read-across from Saipem profit warning

(30/01/13)

What happened? Following an internal review Saipem (offshore and on-shore E&C) pre-

announced 2012 profits 10% below consensus and guided for 2013 more than 50% below

consensus.

What’s changed: The review commented on lower activity in high-margin pre-09

contracts, competitive market conditions in 2009-11 in offshore and high levels of

investment in Brazil. New management has also taken a more conservative approach to

revenue recognition.

Read-across to Prysmian: Saipem is a small customer of Prysmian’s but this profit

warning does not change our view on the Prysmian flexible pipe ramp-up. This is because

the majority of the above issues are company specific and Brazil appears, given Saipem’s

higher investment, to have been one of areas of more resilient demand. As we have

mentioned Petrobras is Prysmian’s key customer and we therefore view flexible pipe

supply and demand in Brazil as a much clearer indicator of the potential for Prysmian’s

business.

Rising SURF EBITDA driven by flexible pipe ramp-up

We have focused on flexible pipes rather than on umbilicals and downhole

technology (DHT) because Prysmian has been producing umbilicals since 2007 and

expects to generate approximately €60m of revenue from umbilicals in 2012E. DHT is also

an established business acquired through Draka with products predominantly sold into the

US. We continue to expect both to grow at 5% over the next three years.

Therefore based on the ramp-up of flexible pipes, the incremental EBIT from SURF will be

driven by these products, rather than by umbilicals, where we estimate capacity utilisation

is currently c60% (vs c25% in flexible pipes). Our base case assumption is that flexible

pipe capacity is 80% utilised by 2015E.

Figure 35: Flexible pipes account for the lowest

proportion of SURF revenues but we believe they have

the greatest growth prospects over the next three years

(2012E)

Figure 36: Incremental SURF EBITDA will be driven by

flexible pipes as we estimate capacity is currently 20%

utilised compared with 60% for umbilicals

Umbilicals37%

Downhole Technology

38%

Flexible pipes25%

0%

10%

20%

30%

40%

50%

60%

70%

Umbilicals Flexible pipe

Capacity Utilization in 2012

Source: Company data, Credit Suisse estimates. * = Flexible pipes

are currently not higher margin but if both umbilicals and flexible pipes

were at saturated capacity flexible pipes would be

Source: Credit Suisse estimates

12 February 2013

European Cable Sector 24

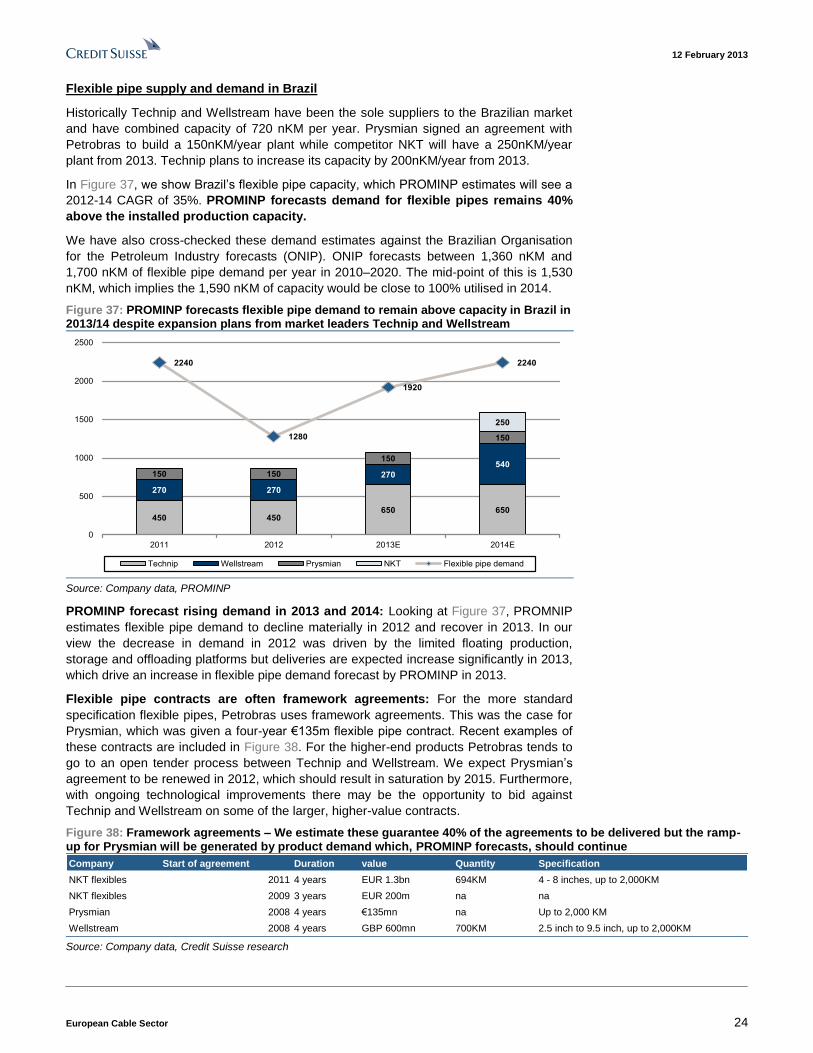

Flexible pipe supply and demand in Brazil

Historically Technip and Wellstream have been the sole suppliers to the Brazilian market

and have combined capacity of 720 nKM per year. Prysmian signed an agreement with

Petrobras to build a 150nKM/year plant while competitor NKT will have a 250nKM/year

plant from 2013. Technip plans to increase its capacity by 200nKM/year from 2013.

In Figure 37, we show Brazil’s flexible pipe capacity, which PROMINP estimates will see a

2012-14 CAGR of 35%. PROMINP forecasts demand for flexible pipes remains 40%

above the installed production capacity.

We have also cross-checked these demand estimates against the Brazilian Organisation

for the Petroleum Industry forecasts (ONIP). ONIP forecasts between 1,360 nKM and

1,700 nKM of flexible pipe demand per year in 2010–2020. The mid-point of this is 1,530

nKM, which implies the 1,590 nKM of capacity would be close to 100% utilised in 2014.

Figure 37: PROMINP forecasts flexible pipe demand to remain above capacity in Brazil in 2013/14 despite expansion plans from market leaders Technip and Wellstream

450 450650 650

270 270

270

540150 150

150

150

250

2240

1280

1920

2240

0

500

1000

1500

2000

2500

2011 2012 2013E 2014E

Technip Wellstream Prysmian NKT Flexible pipe demand

Source: Company data, PROMINP

PROMINP forecast rising demand in 2013 and 2014: Looking at Figure 37, PROMNIP

estimates flexible pipe demand to decline materially in 2012 and recover in 2013. In our

view the decrease in demand in 2012 was driven by the limited floating production,

storage and offloading platforms but deliveries are expected increase significantly in 2013,

which drive an increase in flexible pipe demand forecast by PROMINP in 2013.

Flexible pipe contracts are often framework agreements: For the more standard

specification flexible pipes, Petrobras uses framework agreements. This was the case for

Prysmian, which was given a four-year €135m flexible pipe contract. Recent examples of

these contracts are included in Figure 38. For the higher-end products Petrobras tends to

go to an open tender process between Technip and Wellstream. We expect Prysmian’s

agreement to be renewed in 2012, which should result in saturation by 2015. Furthermore,

with ongoing technological improvements there may be the opportunity to bid against

Technip and Wellstream on some of the larger, higher-value contracts.

Figure 38: Framework agreements – We estimate these guarantee 40% of the agreements to be delivered but the ramp-up for Prysmian will be generated by product demand which, PROMINP forecasts, should continue

Company Start of agreement Duration value Quantity Specification

NKT flexibles 2011 4 years EUR 1.3bn 694KM 4 - 8 inches, up to 2,000KM

NKT flexibles 2009 3 years EUR 200m na na

Prysmian 2008 4 years €135mn na Up to 2,000 KM

Wellstream 2008 4 years GBP 600mn 700KM 2.5 inch to 9.5 inch, up to 2,000KM Source: Company data, Credit Suisse research

12 February 2013

European Cable Sector 25

Scenario analysis for flexible pipe ramp-up

In Figure 39 we have included our base, bull and bear case assumptions for the ramp-up

of Prysmian’s flexible pipe capacity at its Vila Velha plant in Brazil. In each scenario, we

have assumed a price of $1,500 per metre of flexible pipe. Prysmian’s total capacity is

150KM per year but we assume saturation is 80% (or 120KM).

Base case: In our base case, we assume a small ramp-up to 35% utilisation in 2013,

which we believe fairly accounts for the impact of the new Petrobras business plan.

However, based on the production targets and forecast flexible pipe demand, we see a

material pick-up in utilisation in 2014E to 65% and capacity to be saturated by 2015E.

Bull case: Our bull case scenario implies a broadly stable ramp-up in capacity utilisation

to 85% in 2015E. Based on demand vs flexible pipe capacity in Brazil we see this scenario

as realistic but note that the current internal business plan at Petrobras may cause some

short-term demand volatility. This implies 1% upgrades to our 2014 EBITDA forecasts.

Bear case: Here we stress test our forecasts assuming no ramp-up in capacity in 2013

(which we view as highly unlikely) and then for 45% capacity to be achieved in 2015. We

also assume the umbilical and DHT businesses do not grow in 2013-15. However, we

reiterate our view that this is unlikely as the large flexible pipe players such as Technip

and Wellstream continue to add capacity in Brazil to meet increasing flexible pipe demand.

This implies 1.3% downgrades to our 2014 EBITDA forecasts.

12 February 2013

European Cable Sector 26

Scenario analysis for SURF contribution, 2012-2015

Figure 39: Scenario analysis for the ramp-up of flexible pipe capacity at Prysmian (€m)

Bull case Scenario 2012E 2013E 2014E 2015E

FLEXIBLE PIPES

KM of Flexible pipes 30 67 120 128

Implied utilization 20% 45% 80% 85%

Revenue 33.6 75.1 134.4 143.4

EBITDA 1.7 14.1 31.9 34.6

implied EBITDA margin 5.0% 18.8% 23.8% 24.1%

Umbilicals and DHT

Revenue 82.2 86.3 90.6 95.1

EBITDA margin 20% 20% 20% 20%

EBITDA 16.4 17.3 18.1 19.0

TOTAL SURF REVENUE 115.8 161.3 225.0 238.5

SURF EBITDA 18.1 31.4 50.0 53.6

INCREMENTAL EBITDA FROM SURF 13.3 18.7 3.6

Base Case Scenario 2012E 2013E 2014E 2015E

FLEXIBLE PIPES

KM of Flexible pipes 30 53 90 120

Implied utilization 20% 35% 60% 80%

Revenue 33.6 59.4 100.8 134.4

EBITDA 1.7 9.4 21.8 31.9

implied EBITDA margin 5.0% 15.8% 21.7% 23.8%

Umbilicals and DHT

Revenue 82.2 86.3 90.6 95.1

EBITDA margin 20% 20% 20% 20%

EBITDA 16.4 17.3 18.1 19.0

TOTAL SURF REVENUE 115.8 145.6 191.4 229.5

SURF EBITDA 18.1 26.7 40.0 50.9

INCREMENTAL EBITDA FROM SURF 8.6 13.3 11.0

Bear Case Scenario 2012E 2013E 2014E 2015E

FLEXIBLE PIPES

KM of Flexible pipes 30 30 45 68

Implied utilization 20% 20% 30% 45%

Revenue 33.6 33.6 50.4 76.2

EBITDA margin 5% 30% 30% 30%

EBITDA 1.7 1.7 5.9 12.3

implied EBITDA margin 5.0% 5.0% 11.7% 16.2%

Umbilicals and DHT

Revenue 82.7 82.7 82.7 82.7

EBITDA margin 20% 20% 20% 20%

EBITDA 16.5 16.5 16.5 16.5

TOTAL SURF REVENUE 116.3 116.3 133.1 158.9

SURF EBITDA 18.2 18.2 22.4 28.9

INCREMENTAL EBITDA FROM SURF 0.0 4.2 6.4 Source: Credit Suisse estimates

12 February 2013

European Cable Sector 27

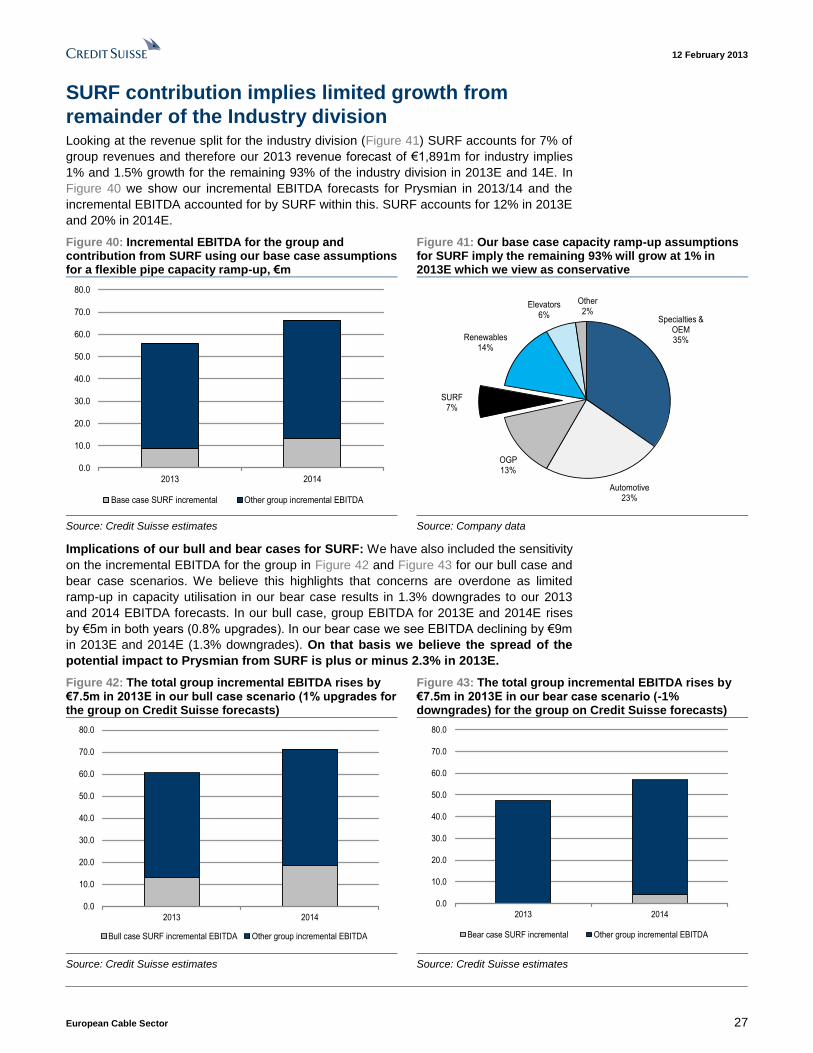

SURF contribution implies limited growth from

remainder of the Industry division Looking at the revenue split for the industry division (Figure 41) SURF accounts for 7% of

group revenues and therefore our 2013 revenue forecast of €1,891m for industry implies

1% and 1.5% growth for the remaining 93% of the industry division in 2013E and 14E. In

Figure 40 we show our incremental EBITDA forecasts for Prysmian in 2013/14 and the

incremental EBITDA accounted for by SURF within this. SURF accounts for 12% in 2013E

and 20% in 2014E.

Figure 40: Incremental EBITDA for the group and contribution from SURF using our base case assumptions for a flexible pipe capacity ramp-up, €m

Figure 41: Our base case capacity ramp-up assumptions for SURF imply the remaining 93% will grow at 1% in 2013E which we view as conservative

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2013 2014

Base case SURF incremental Other group incremental EBITDA

Specialties & OEM35%

Automotive23%

OGP13%

SURF7%

Renewables14%

Elevators6%

Other2%

Source: Credit Suisse estimates Source: Company data

Implications of our bull and bear cases for SURF: We have also included the sensitivity

on the incremental EBITDA for the group in Figure 42 and Figure 43 for our bull case and

bear case scenarios. We believe this highlights that concerns are overdone as limited

ramp-up in capacity utilisation in our bear case results in 1.3% downgrades to our 2013

and 2014 EBITDA forecasts. In our bull case, group EBITDA for 2013E and 2014E rises

by €5m in both years (0.8% upgrades). In our bear case we see EBITDA declining by €9m

in 2013E and 2014E (1.3% downgrades). On that basis we believe the spread of the

potential impact to Prysmian from SURF is plus or minus 2.3% in 2013E.

Figure 42: The total group incremental EBITDA rises by €7.5m in 2013E in our bull case scenario (1% upgrades for the group on Credit Suisse forecasts)

Figure 43: The total group incremental EBITDA rises by €7.5m in 2013E in our bear case scenario (-1% downgrades) for the group on Credit Suisse forecasts)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2013 2014

Bull case SURF incremental EBITDA Other group incremental EBITDA

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2013 2014

Bear case SURF incremental Other group incremental EBITDA

Source: Credit Suisse estimates Source: Credit Suisse estimates

12 February 2013

European Cable Sector 28

#3: Mapping the global cable competitive landscape

2011 operating profit margins at Prysmian and Nexans were 370bps and 330bps

respectively below peak, with increasing competition being one of the factors responsible

for the decline. In this section we have looked in detail at competitors’ growth rates and

margins, and Prysmian’s and Nexans’ recent commentaries to consider the broader

competitive landscape. Based on the threat in Land High Voltage being relatively well

understood we have focused on the threat in Optical fibre & cable.

Our conclusions from this analysis are:

■ Combined, Europe and the US account for 45% of Prysmian’s optical fibre & cable

sales and Prysmian has a leading market share in most European countries. In our

view the large Japanese competitors are unlikely to focus primarily on expansion in

this market and rather focus on China given the demand outlook.

■ In China (25% of Prysmian’s optical fibre & cable sales) we view the threat from

Japanese competitors to Prysmian’s leading market share as manageable. Given the

high expected demand (limiting the risk of over-capacity), and consolidated market

(five key players) we would not expect aggressive pricing strategies from competitors

that could ultimately destroy the longer-term value of this market.

■ Currently, domestic Chinese competitors do not represent a significant threat to

Prysmian in China, in our view. In the medium term we expect existing smaller players

to grow to meet demand but, based on the technology and high cost of developing

optical fibre, we see limited scope for new entrants. We also believe Prysmian can

continue to compete on price with existing domestic players as it produces locally

through its JV (YOFC).

■ In Land High Voltage (6% of Nexans’ sales and 7% of Prysmian’s sales) these

players, and particularly Nexans, have flagged emerging market competition in the

Middle Eastern and Chinese markets. We expect pricing pressure to moderate over

the next two years as prices have already fallen so significantly (Nexans now has a

low single digit EBITDA margin in Land HV compared with double digits previously).

However, we believe pricing pressure will continue to be of greater concern for

Nexans as 37% of its Land HV sales were in the Middle East in 2012 (vs 49% in

2010). We think Prysmian’s business has a greater focus on the higher voltage

segments, with only 40% of sales in the <220KV segment.

12 February 2013

European Cable Sector 29

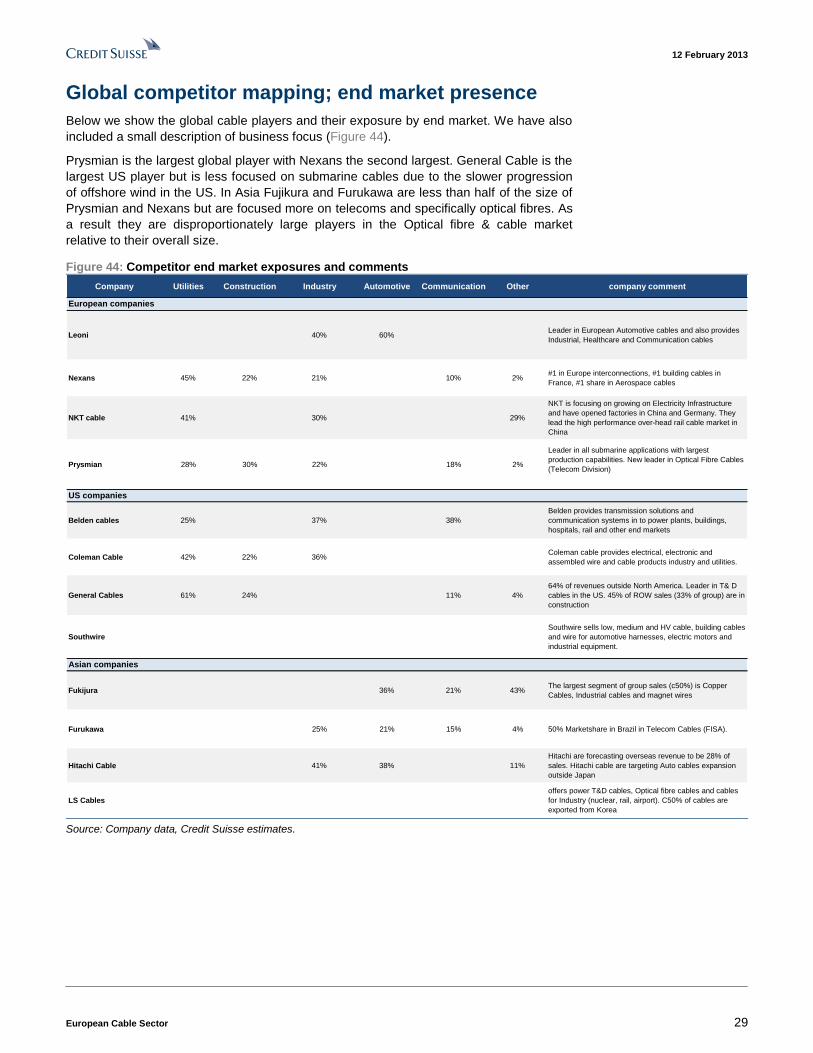

Global competitor mapping; end market presence

Below we show the global cable players and their exposure by end market. We have also

included a small description of business focus (Figure 44).

Prysmian is the largest global player with Nexans the second largest. General Cable is the

largest US player but is less focused on submarine cables due to the slower progression

of offshore wind in the US. In Asia Fujikura and Furukawa are less than half of the size of

Prysmian and Nexans but are focused more on telecoms and specifically optical fibres. As

a result they are disproportionately large players in the Optical fibre & cable market

relative to their overall size.

Figure 44: Competitor end market exposures and comments

Company Utilities Construction Industry Automotive Communication Other company comment

Leoni 40% 60%Leader in European Automotive cables and also provides

Industrial, Healthcare and Communication cables

Nexans 45% 22% 21% 10% 2%#1 in Europe interconnections, #1 building cables in

France, #1 share in Aerospace cables

NKT cable 41% 30% 29%

NKT is focusing on growing on Electricity Infrastructure

and have opened factories in China and Germany. They

lead the high performance over-head rail cable market in

China

Prysmian 28% 30% 22% 18% 2%

Leader in all submarine applications with largest

production capabilities. New leader in Optical Fibre Cables

(Telecom Division)

Belden cables 25% 37% 38%

Belden provides transmission solutions and

communication systems in to power plants, buildings,

hospitals, rail and other end markets

Coleman Cable 42% 22% 36%Coleman cable provides electrical, electronic and

assembled wire and cable products industry and utilities.

General Cables 61% 24% 11% 4%

64% of revenues outside North America. Leader in T& D

cables in the US. 45% of ROW sales (33% of group) are in

construction

Southwire

Southwire sells low, medium and HV cable, building cables

and wire for automotive harnesses, electric motors and

industrial equipment.

Fukijura 36% 21% 43%The largest segment of group sales (c50%) is Copper

Cables, Industrial cables and magnet wires

Furukawa 25% 21% 15% 4% 50% Marketshare in Brazil in Telecom Cables (FISA).

Hitachi Cable 41% 38% 11%

Hitachi are forecasting overseas revenue to be 28% of

sales. Hitachi cable are targeting Auto cables expansion

outside Japan

LS Cables

offers power T&D cables, Optical fibre cables and cables

for Industry (nuclear, rail, airport). C50% of cables are

exported from Korea

European companies

US companies

Asian companies

Source: Company data, Credit Suisse estimates.

12 February 2013

European Cable Sector 30

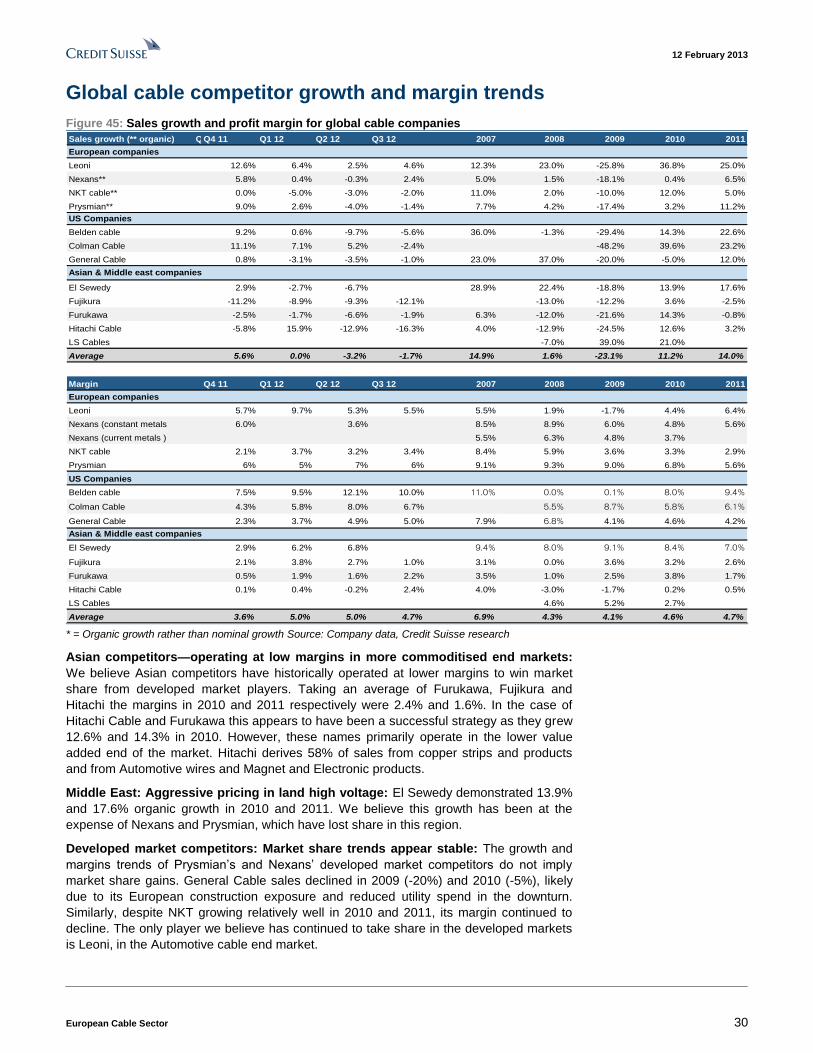

Global cable competitor growth and margin trends

Figure 45: Sales growth and profit margin for global cable companies

Sales growth (** organic) Q2 10Q4 11 Q1 12 Q2 12 Q3 12 2007 2008 2009 2010 2011

Leoni 12.6% 6.4% 2.5% 4.6% 12.3% 23.0% -25.8% 36.8% 25.0%

Nexans** 5.8% 0.4% -0.3% 2.4% 5.0% 1.5% -18.1% 0.4% 6.5%

NKT cable** 0.0% -5.0% -3.0% -2.0% 11.0% 2.0% -10.0% 12.0% 5.0%

Prysmian** 9.0% 2.6% -4.0% -1.4% 7.7% 4.2% -17.4% 3.2% 11.2%

Belden cable 9.2% 0.6% -9.7% -5.6% 36.0% -1.3% -29.4% 14.3% 22.6%

Colman Cable 11.1% 7.1% 5.2% -2.4% -48.2% 39.6% 23.2%

General Cable 0.8% -3.1% -3.5% -1.0% 23.0% 37.0% -20.0% -5.0% 12.0%

El Sewedy 2.9% -2.7% -6.7% 28.9% 22.4% -18.8% 13.9% 17.6%

Fujikura -11.2% -8.9% -9.3% -12.1% -13.0% -12.2% 3.6% -2.5%

Furukawa -2.5% -1.7% -6.6% -1.9% 6.3% -12.0% -21.6% 14.3% -0.8%

Hitachi Cable -5.8% 15.9% -12.9% -16.3% 4.0% -12.9% -24.5% 12.6% 3.2%

LS Cables -7.0% 39.0% 21.0%

Average 5.6% 0.0% -3.2% -1.7% 14.9% 1.6% -23.1% 11.2% 14.0%

Margin Q4 11 Q1 12 Q2 12 Q3 12 2007 2008 2009 2010 2011

Leoni 5.7% 9.7% 5.3% 5.5% 5.5% 1.9% -1.7% 4.4% 6.4%

Nexans (constant metals 6.0% 3.6% 8.5% 8.9% 6.0% 4.8% 5.6%

Nexans (current metals ) 5.5% 6.3% 4.8% 3.7%

NKT cable 2.1% 3.7% 3.2% 3.4% 8.4% 5.9% 3.6% 3.3% 2.9%

Prysmian 6% 5% 7% 6% 9.1% 9.3% 9.0% 6.8% 5.6%

Belden cable 7.5% 9.5% 12.1% 10.0% 11.0% 0.0% 0.1% 8.0% 9.4%

Colman Cable 4.3% 5.8% 8.0% 6.7% 5.5% 8.7% 5.8% 6.1%

General Cable 2.3% 3.7% 4.9% 5.0% 7.9% 6.8% 4.1% 4.6% 4.2%

El Sewedy 2.9% 6.2% 6.8% 9.4% 8.0% 9.1% 8.4% 7.0%

Fujikura 2.1% 3.8% 2.7% 1.0% 3.1% 0.0% 3.6% 3.2% 2.6%

Furukawa 0.5% 1.9% 1.6% 2.2% 3.5% 1.0% 2.5% 3.8% 1.7%

Hitachi Cable 0.1% 0.4% -0.2% 2.4% 4.0% -3.0% -1.7% 0.2% 0.5%

LS Cables 4.6% 5.2% 2.7%

Average 3.6% 5.0% 5.0% 4.7% 6.9% 4.3% 4.1% 4.6% 4.7%

European companies

US Companies

Asian & Middle east companies

European companies

Asian & Middle east companies

US Companies

* = Organic growth rather than nominal growth Source: Company data, Credit Suisse research

Asian competitors—operating at low margins in more commoditised end markets:

We believe Asian competitors have historically operated at lower margins to win market

share from developed market players. Taking an average of Furukawa, Fujikura and