Embed Size (px)

Citation preview

Corporate Presentation – October 2014

European DataWarehouse

Due Diligence using ED Cloud Pro – Webinar November 2016

Draft European Framework for Simple, Transparent and Standardised Securitisation (STS)

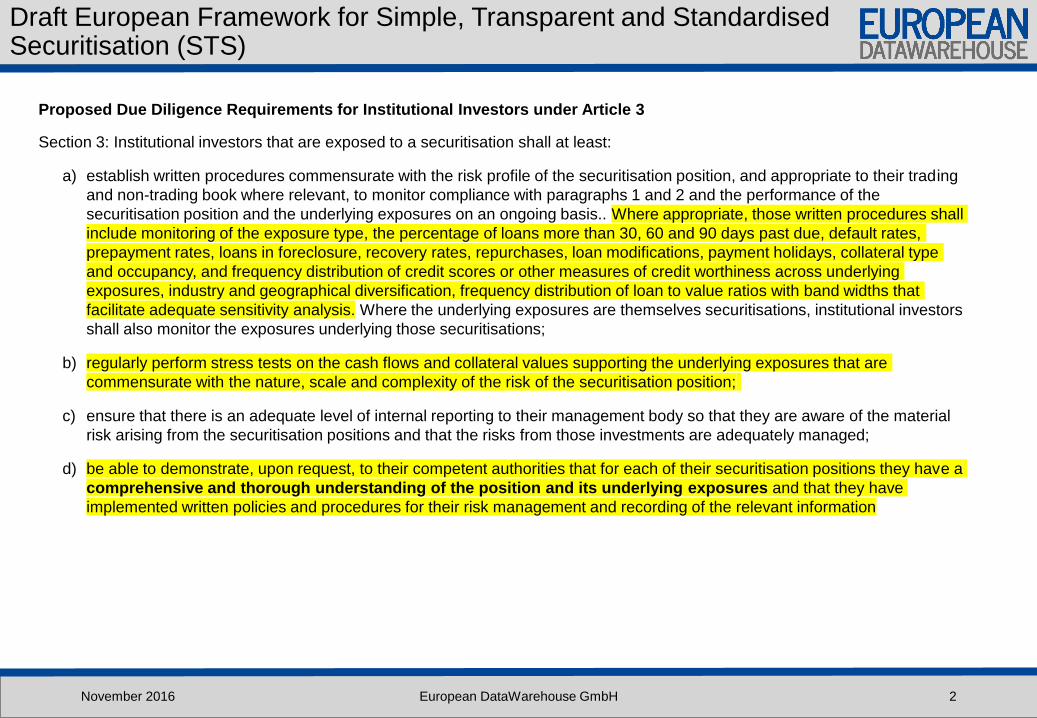

Proposed Due Diligence Requirements for Institutional Investors under Article 3

Section 3: Institutional investors that are exposed to a securitisation shall at least:

a) establish written procedures commensurate with the risk profile of the securitisation position, and appropriate to their trading

and non-trading book where relevant, to monitor compliance with paragraphs 1 and 2 and the performance of the

securitisation position and the underlying exposures on an ongoing basis.. Where appropriate, those written procedures shall

include monitoring of the exposure type, the percentage of loans more than 30, 60 and 90 days past due, default rates,

prepayment rates, loans in foreclosure, recovery rates, repurchases, loan modifications, payment holidays, collateral type

and occupancy, and frequency distribution of credit scores or other measures of credit worthiness across underlying

exposures, industry and geographical diversification, frequency distribution of loan to value ratios with band widths that

facilitate adequate sensitivity analysis. Where the underlying exposures are themselves securitisations, institutional investors

shall also monitor the exposures underlying those securitisations;

b) regularly perform stress tests on the cash flows and collateral values supporting the underlying exposures that are

commensurate with the nature, scale and complexity of the risk of the securitisation position;

c) ensure that there is an adequate level of internal reporting to their management body so that they are aware of the material

risk arising from the securitisation positions and that the risks from those investments are adequately managed;

d) be able to demonstrate, upon request, to their competent authorities that for each of their securitisation positions they have a

comprehensive and thorough understanding of the position and its underlying exposures and that they have

implemented written policies and procedures for their risk management and recording of the relevant information

November 2016 European DataWarehouse GmbH 2

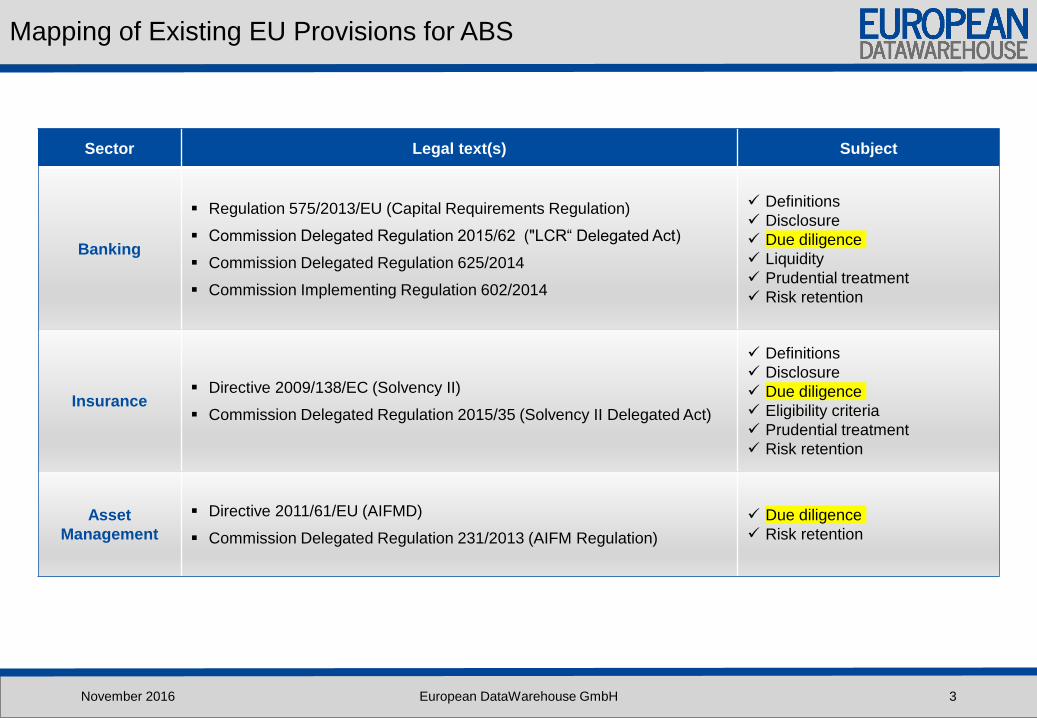

Mapping of Existing EU Provisions for ABS

Sector Legal text(s) Subject

Banking

Regulation 575/2013/EU (Capital Requirements Regulation)

Commission Delegated Regulation 2015/62 ("LCR“ Delegated Act)

Commission Delegated Regulation 625/2014

Commission Implementing Regulation 602/2014

Definitions

Disclosure

Due diligence

Liquidity

Prudential treatment

Risk retention

Insurance Directive 2009/138/EC (Solvency II)

Commission Delegated Regulation 2015/35 (Solvency II Delegated Act)

Definitions

Disclosure

Due diligence

Eligibility criteria

Prudential treatment

Risk retention

Asset

Management

Directive 2011/61/EU (AIFMD)

Commission Delegated Regulation 231/2013 (AIFM Regulation)

Due diligence

Risk retention

November 2016 European DataWarehouse GmbH 3

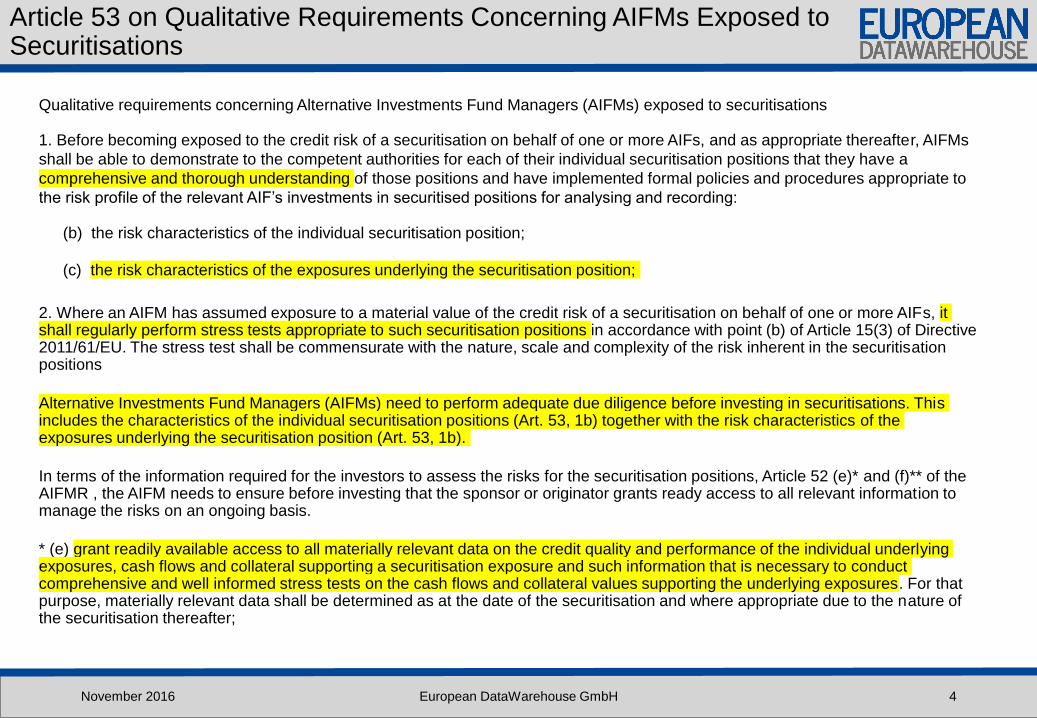

Article 53 on Qualitative Requirements Concerning AIFMs Exposed to Securitisations

Qualitative requirements concerning Alternative Investments Fund Managers (AIFMs) exposed to securitisations

1. Before becoming exposed to the credit risk of a securitisation on behalf of one or more AIFs, and as appropriate thereafter, AIFMs

shall be able to demonstrate to the competent authorities for each of their individual securitisation positions that they have a

comprehensive and thorough understanding of those positions and have implemented formal policies and procedures appropriate to

the risk profile of the relevant AIF’s investments in securitised positions for analysing and recording:

(b) the risk characteristics of the individual securitisation position;

(c) the risk characteristics of the exposures underlying the securitisation position;

2. Where an AIFM has assumed exposure to a material value of the credit risk of a securitisation on behalf of one or more AIFs, it shall regularly perform stress tests appropriate to such securitisation positions in accordance with point (b) of Article 15(3) of Directive 2011/61/EU. The stress test shall be commensurate with the nature, scale and complexity of the risk inherent in the securitisation positions

Alternative Investments Fund Managers (AIFMs) need to perform adequate due diligence before investing in securitisations. This includes the characteristics of the individual securitisation positions (Art. 53, 1b) together with the risk characteristics of the exposures underlying the securitisation position (Art. 53, 1b).

In terms of the information required for the investors to assess the risks for the securitisation positions, Article 52 (e)* and (f)** of the AIFMR , the AIFM needs to ensure before investing that the sponsor or originator grants ready access to all relevant information to manage the risks on an ongoing basis.

* (e) grant readily available access to all materially relevant data on the credit quality and performance of the individual underlying exposures, cash flows and collateral supporting a securitisation exposure and such information that is necessary to conduct comprehensive and well informed stress tests on the cash flows and collateral values supporting the underlying exposures. For that purpose, materially relevant data shall be determined as at the date of the securitisation and where appropriate due to the nature of the securitisation thereafter;

November 2016 European DataWarehouse GmbH 4

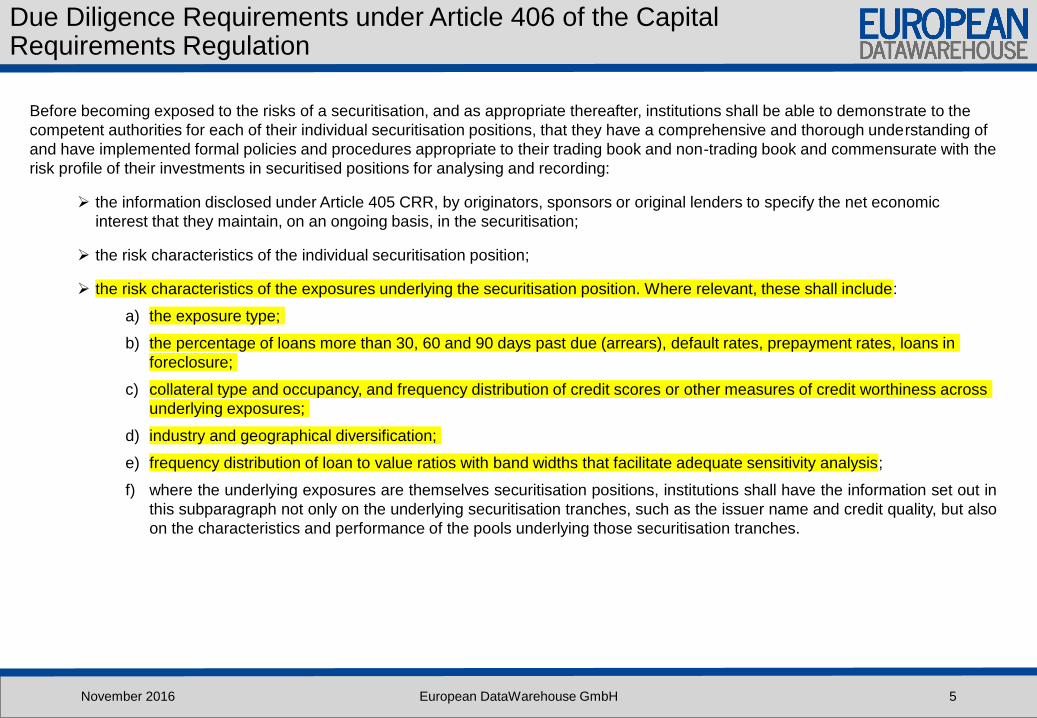

Before becoming exposed to the risks of a securitisation, and as appropriate thereafter, institutions shall be able to demonstrate to the

competent authorities for each of their individual securitisation positions, that they have a comprehensive and thorough understanding of

and have implemented formal policies and procedures appropriate to their trading book and non-trading book and commensurate with the

risk profile of their investments in securitised positions for analysing and recording:

the information disclosed under Article 405 CRR, by originators, sponsors or original lenders to specify the net economic

interest that they maintain, on an ongoing basis, in the securitisation;

the risk characteristics of the individual securitisation position;

the risk characteristics of the exposures underlying the securitisation position. Where relevant, these shall include:

a) the exposure type;

b) the percentage of loans more than 30, 60 and 90 days past due (arrears), default rates, prepayment rates, loans in

foreclosure;

c) collateral type and occupancy, and frequency distribution of credit scores or other measures of credit worthiness across

underlying exposures;

d) industry and geographical diversification;

e) frequency distribution of loan to value ratios with band widths that facilitate adequate sensitivity analysis;

f) where the underlying exposures are themselves securitisation positions, institutions shall have the information set out in

this subparagraph not only on the underlying securitisation tranches, such as the issuer name and credit quality, but also

on the characteristics and performance of the pools underlying those securitisation tranches.

Due Diligence Requirements under Article 406 of the Capital Requirements Regulation

November 2016 European DataWarehouse GmbH 5

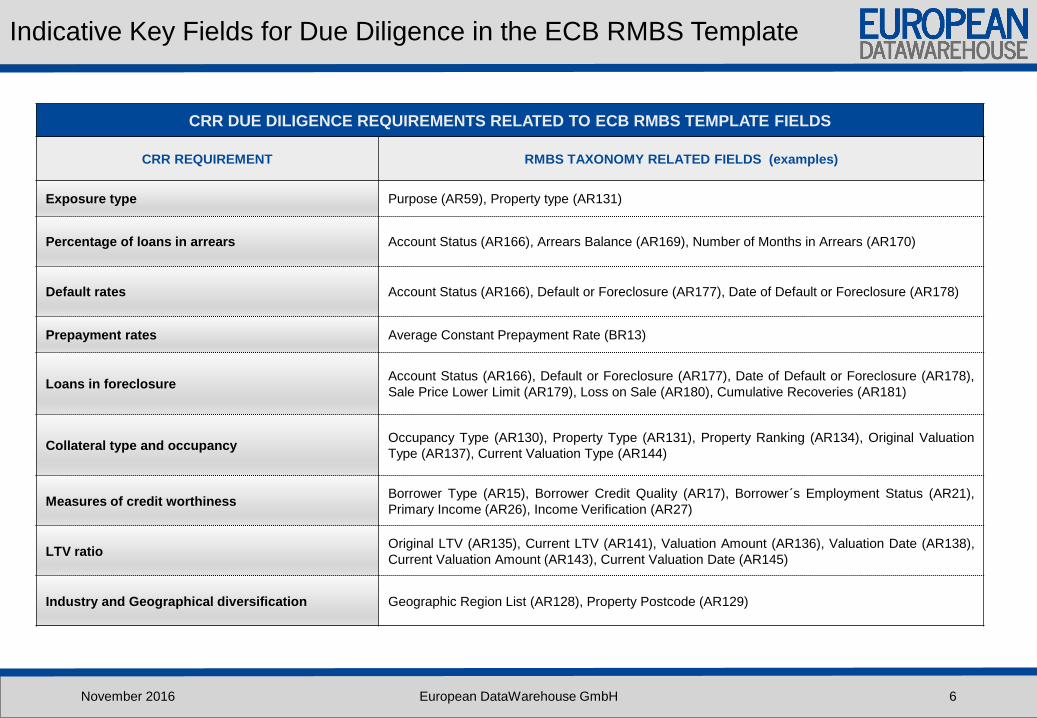

Indicative Key Fields for Due Diligence in the ECB RMBS Template

CRR DUE DILIGENCE REQUIREMENTS RELATED TO ECB RMBS TEMPLATE FIELDS

CRR REQUIREMENT RMBS TAXONOMY RELATED FIELDS (examples)

Exposure type Purpose (AR59), Property type (AR131)

Percentage of loans in arrears Account Status (AR166), Arrears Balance (AR169), Number of Months in Arrears (AR170)

Default rates Account Status (AR166), Default or Foreclosure (AR177), Date of Default or Foreclosure (AR178)

Prepayment rates Average Constant Prepayment Rate (BR13)

Loans in foreclosureAccount Status (AR166), Default or Foreclosure (AR177), Date of Default or Foreclosure (AR178),

Sale Price Lower Limit (AR179), Loss on Sale (AR180), Cumulative Recoveries (AR181)

Collateral type and occupancyOccupancy Type (AR130), Property Type (AR131), Property Ranking (AR134), Original Valuation

Type (AR137), Current Valuation Type (AR144)

Measures of credit worthinessBorrower Type (AR15), Borrower Credit Quality (AR17), Borrower´s Employment Status (AR21),

Primary Income (AR26), Income Verification (AR27)

LTV ratioOriginal LTV (AR135), Current LTV (AR141), Valuation Amount (AR136), Valuation Date (AR138),

Current Valuation Amount (AR143), Current Valuation Date (AR145)

Industry and Geographical diversification Geographic Region List (AR128), Property Postcode (AR129)

November 2016 European DataWarehouse GmbH 6

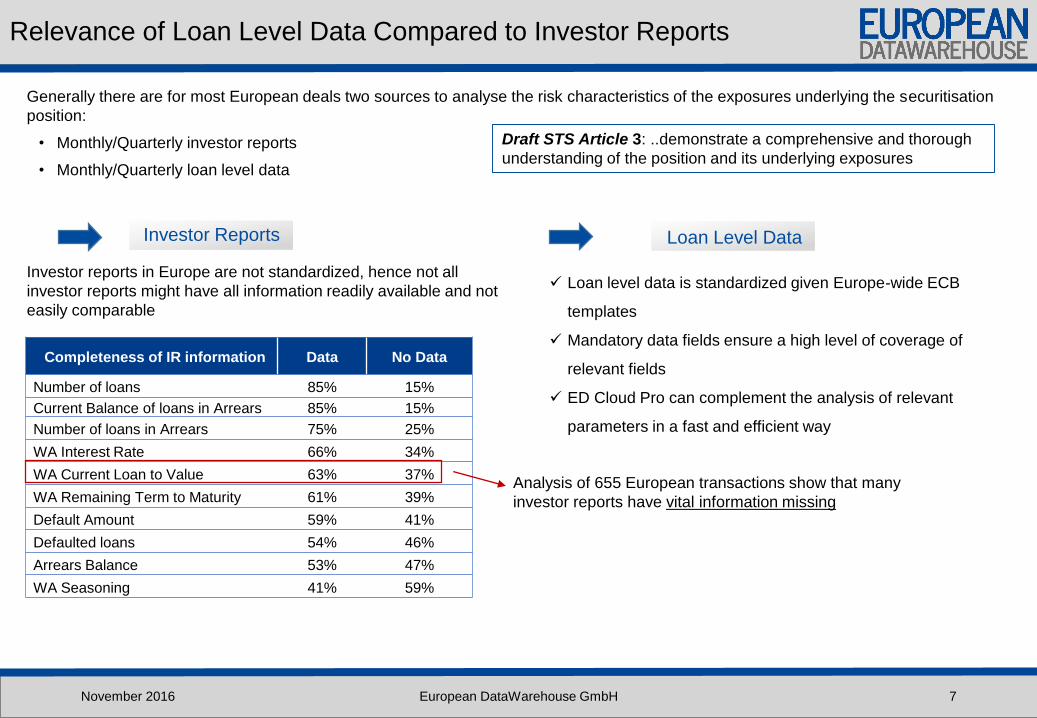

Relevance of Loan Level Data Compared to Investor Reports

November 2016 European DataWarehouse GmbH 7

Completeness of IR information Data No Data

Number of loans 85% 15%

Current Balance of loans in Arrears 85% 15%

Number of loans in Arrears 75% 25%

WA Interest Rate 66% 34%

WA Current Loan to Value 63% 37%

WA Remaining Term to Maturity 61% 39%

Default Amount 59% 41%

Defaulted loans 54% 46%

Arrears Balance 53% 47%

WA Seasoning 41% 59%

Generally there are for most European deals two sources to analyse the risk characteristics of the exposures underlying the securitisation

position:

• Monthly/Quarterly investor reports

• Monthly/Quarterly loan level data

Analysis of 655 European transactions show that many

investor reports have vital information missing

Investor reports in Europe are not standardized, hence not all

investor reports might have all information readily available and not

easily comparable

Loan level data is standardized given Europe-wide ECB

templates

Mandatory data fields ensure a high level of coverage of

relevant fields

ED Cloud Pro can complement the analysis of relevant

parameters in a fast and efficient way

Draft STS Article 3: ..demonstrate a comprehensive and thorough

understanding of the position and its underlying exposures

Investor Reports Loan Level Data

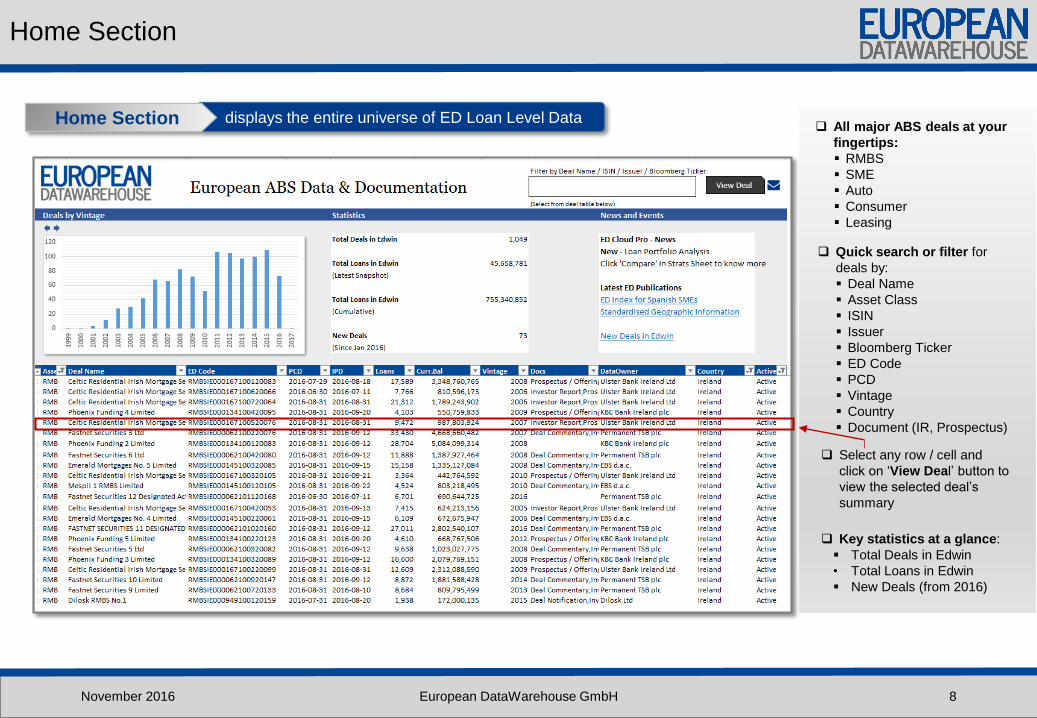

Home Section

November 2016 European DataWarehouse GmbH 8

Quick search or filter for

deals by:

Deal Name

Asset Class

ISIN

Issuer

Bloomberg Ticker

ED Code

PCD

Vintage

Country

Document (IR, Prospectus)

Key statistics at a glance:

Total Deals in Edwin

• Total Loans in Edwin

New Deals (from 2016)

Select any row / cell and

click on ‘View Deal’ button to

view the selected deal’s

summary

displays the entire universe of ED Loan Level DataHome Section All major ABS deals at your

fingertips:

RMBS

SME

Auto

Consumer

Leasing

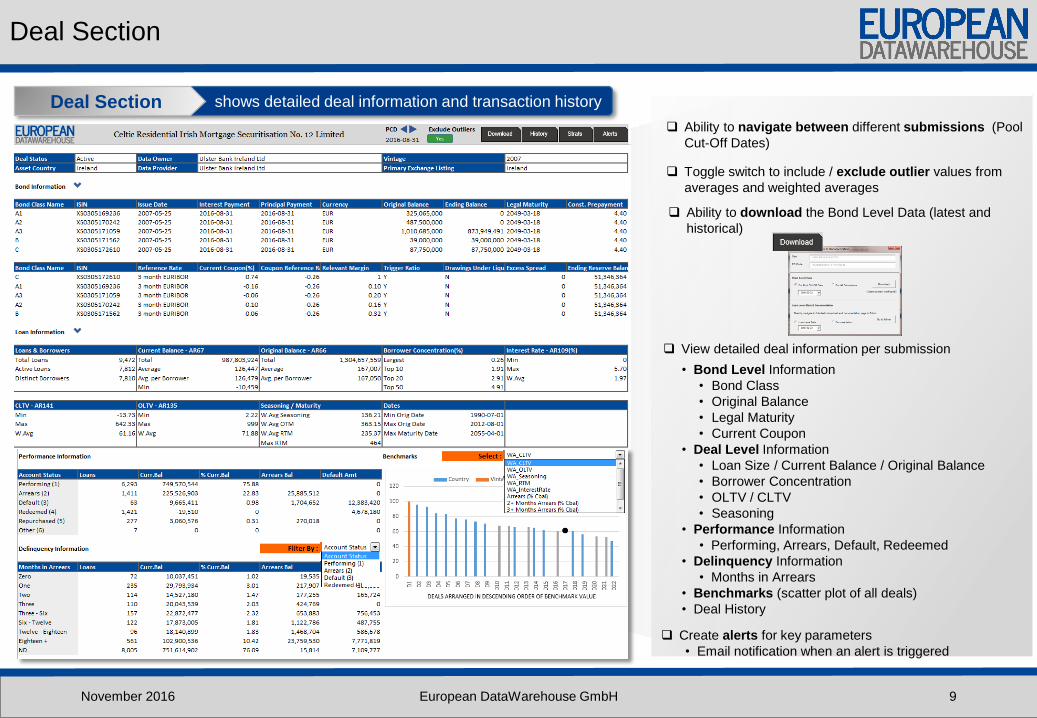

Deal Section

November 2016 European DataWarehouse GmbH 9

Ability to navigate between different submissions (Pool

Cut-Off Dates)

Toggle switch to include / exclude outlier values from

averages and weighted averages

View detailed deal information per submission

• Bond Level Information

• Bond Class

• Original Balance

• Legal Maturity

• Current Coupon

• Deal Level Information

• Loan Size / Current Balance / Original Balance

• Borrower Concentration

• OLTV / CLTV

• Seasoning

• Performance Information

• Performing, Arrears, Default, Redeemed

• Delinquency Information

• Months in Arrears

• Benchmarks (scatter plot of all deals)

• Deal History

shows detailed deal information and transaction historyDeal Section

Create alerts for key parameters

• Email notification when an alert is triggered

Ability to download the Bond Level Data (latest and

historical)

Data Owner

Data Provider

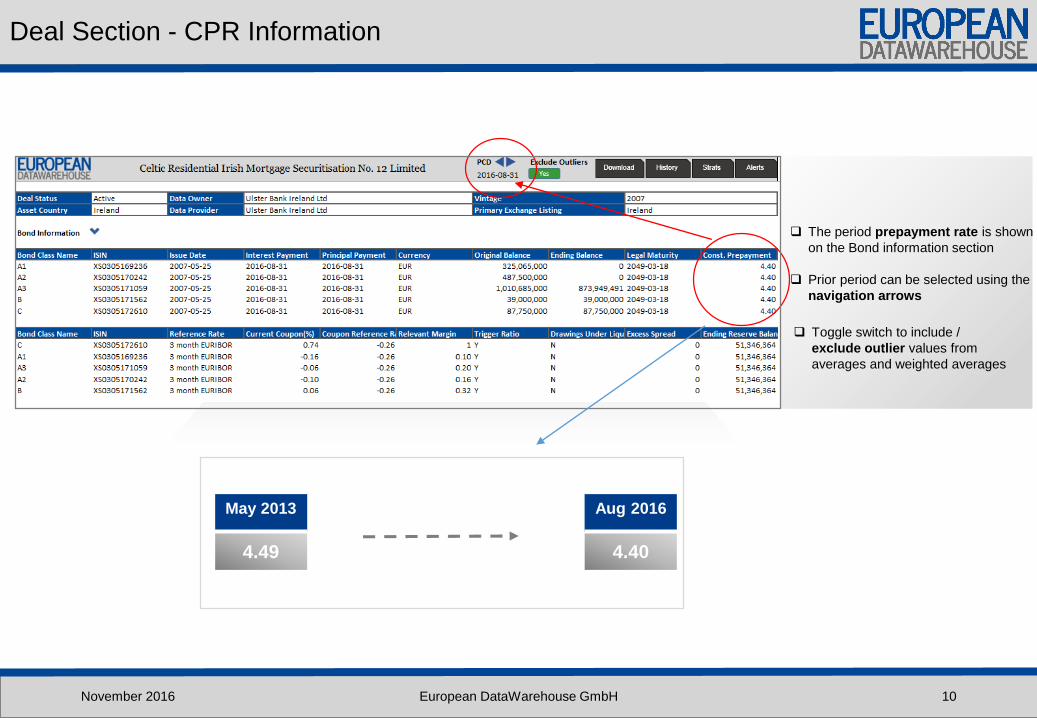

Deal Section - CPR Information

November 2016 European DataWarehouse GmbH 10

The period prepayment rate is shown

on the Bond information section

Prior period can be selected using the

navigation arrows

May 2013 Aug 2016

4.49 4.40

Toggle switch to include /

exclude outlier values from

averages and weighted averages

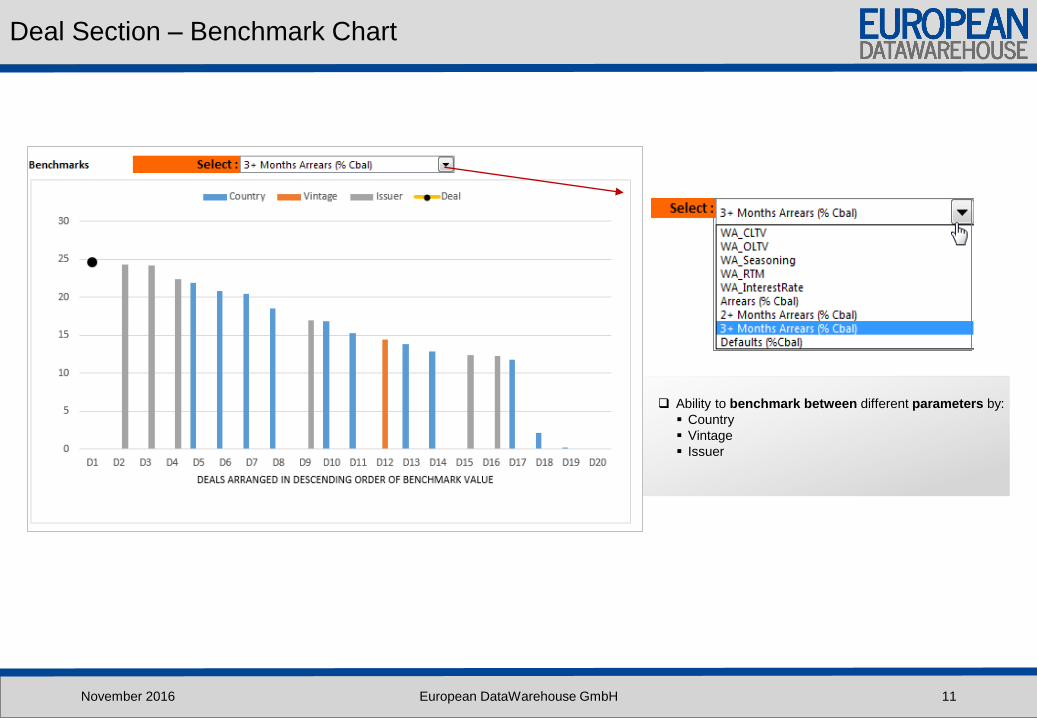

Deal Section – Benchmark Chart

November 2016 European DataWarehouse GmbH 11

Ability to benchmark between different parameters by:

Country

Vintage

Issuer

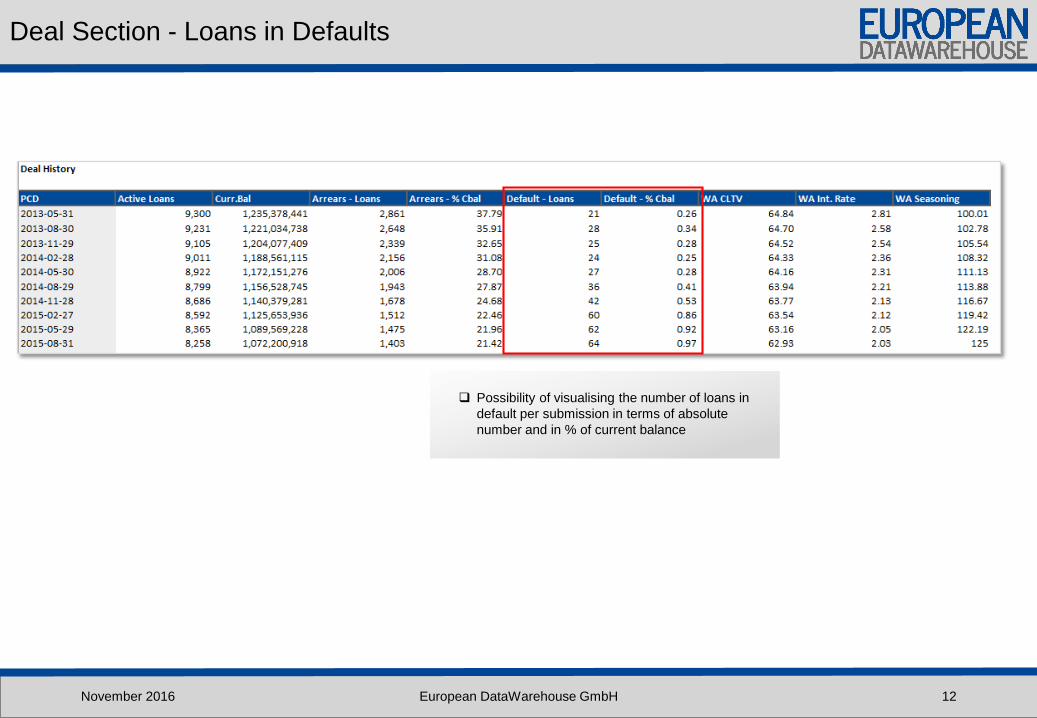

Deal Section - Loans in Defaults

November 2016 European DataWarehouse GmbH 12

Possibility of visualising the number of loans in

default per submission in terms of absolute

number and in % of current balance

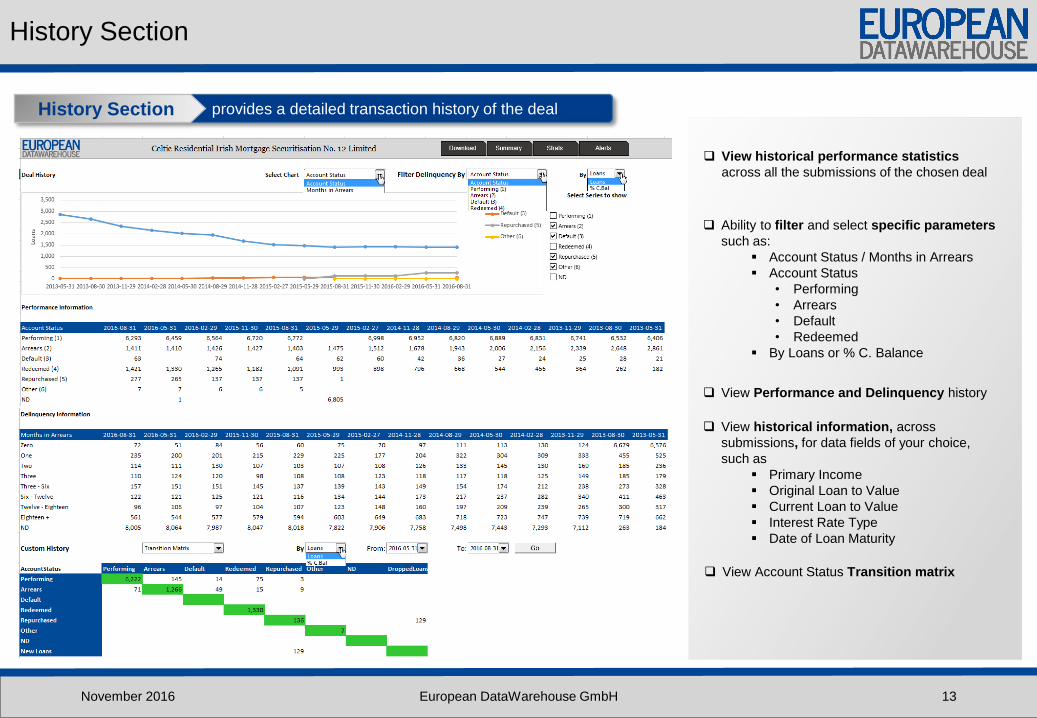

History Section

November 2016 European DataWarehouse GmbH 13

provides a detailed transaction history of the deal History Section

View historical performance statistics

across all the submissions of the chosen deal

Ability to filter and select specific parameters

such as:

Account Status / Months in Arrears

Account Status

• Performing

• Arrears

• Default

• Redeemed

By Loans or % C. Balance

View Performance and Delinquency history

View historical information, across

submissions, for data fields of your choice,

such as

Primary Income

Original Loan to Value

Current Loan to Value

Interest Rate Type

Date of Loan Maturity

View Account Status Transition matrix

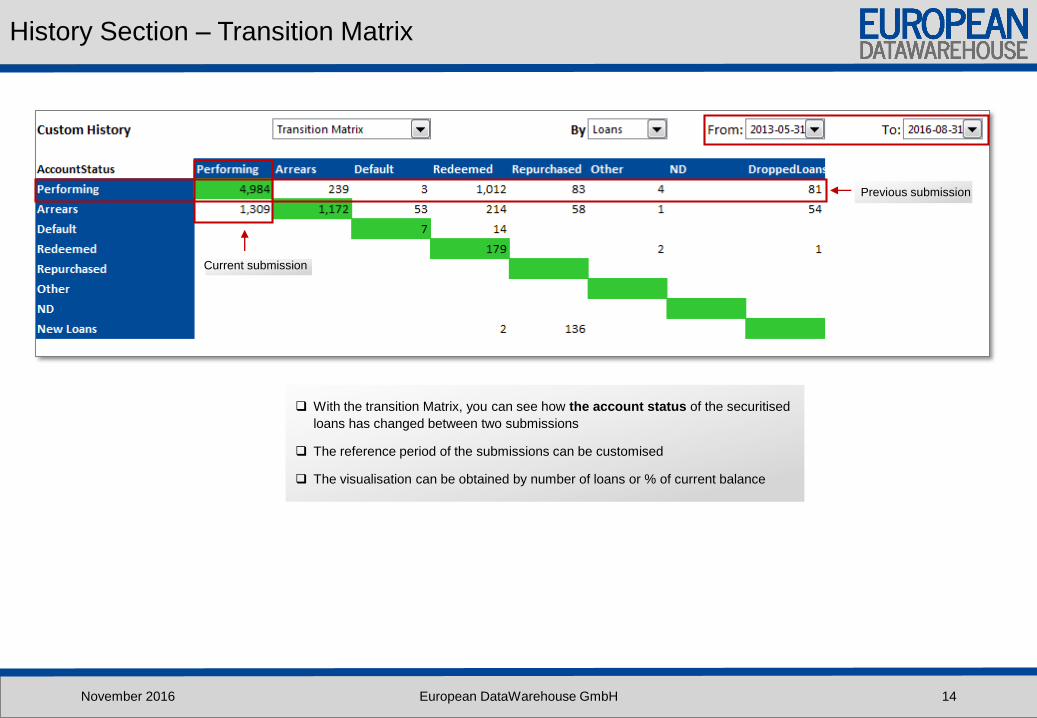

History Section – Transition Matrix

November 2016 European DataWarehouse GmbH 14

With the transition Matrix, you can see how the account status of the securitised

loans has changed between two submissions

The reference period of the submissions can be customised

The visualisation can be obtained by number of loans or % of current balance

Current submission

Previous submission

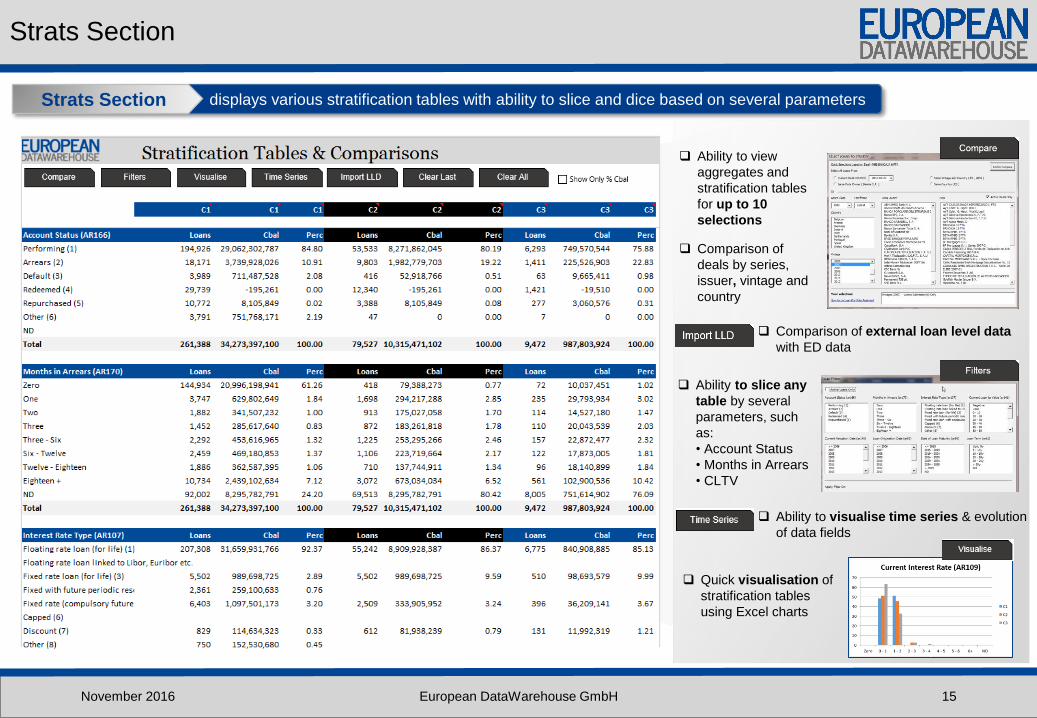

Strats Section

November 2016 European DataWarehouse GmbH 15

displays various stratification tables with ability to slice and dice based on several parametersStrats Section

Ability to view

aggregates and

stratification tables

for up to 10

selections

Comparison of

deals by series,

issuer, vintage and

country

Ability to slice any

table by several

parameters, such

as:

• Account Status

• Months in Arrears

• CLTV

Comparison of external loan level data

with ED data

Ability to visualise time series & evolution

of data fields

Quick visualisation of

stratification tables

using Excel charts

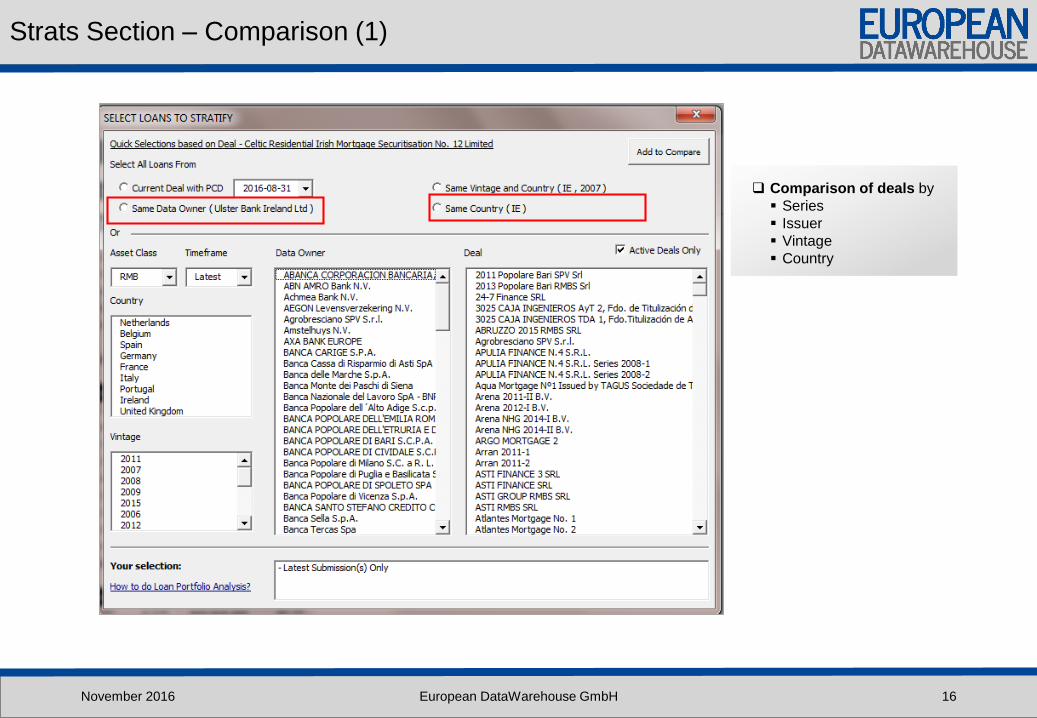

Strats Section – Comparison (1)

November 2016 European DataWarehouse GmbH 16

Comparison of deals by

Series

Issuer

Vintage

Country

Strats Section – Comparison (2)

November 2016 European DataWarehouse GmbH 17

Compare up to

10 selections

within the cloud

e.g

Country

Vintage

Issuer

Deal

Country Vintage Issuer Deal

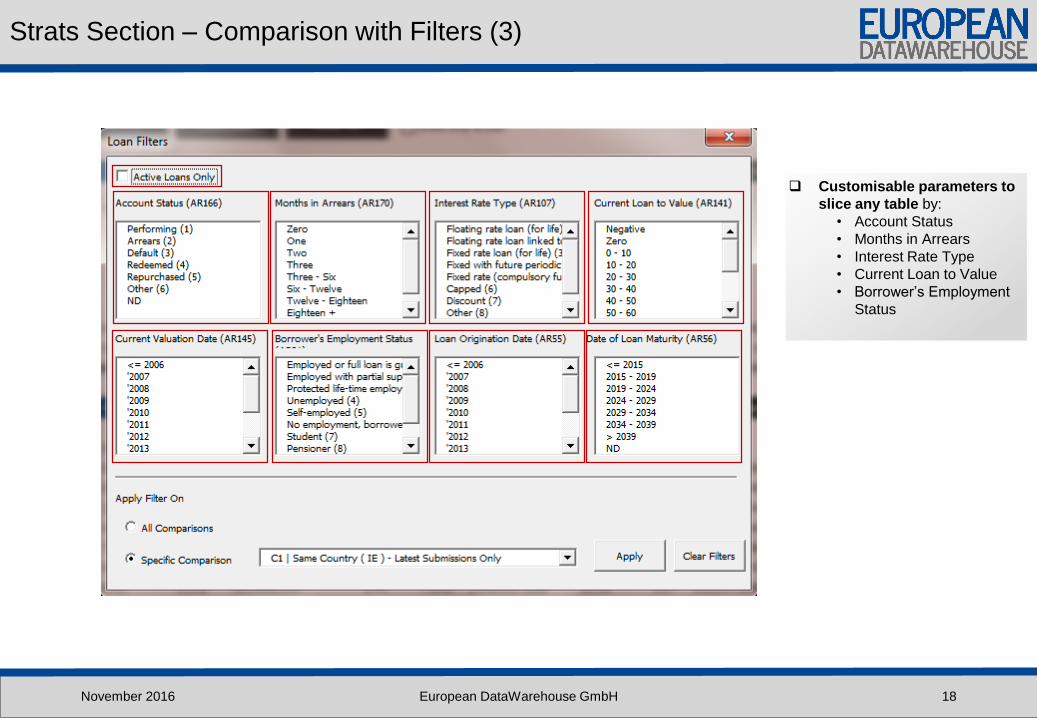

Strats Section – Comparison with Filters (3)

November 2016 European DataWarehouse GmbH 18

Customisable parameters to

slice any table by:

• Account Status

• Months in Arrears

• Interest Rate Type

• Current Loan to Value

• Borrower’s Employment

Status

November 2016 European DataWarehouse GmbH 19

APPENDIX

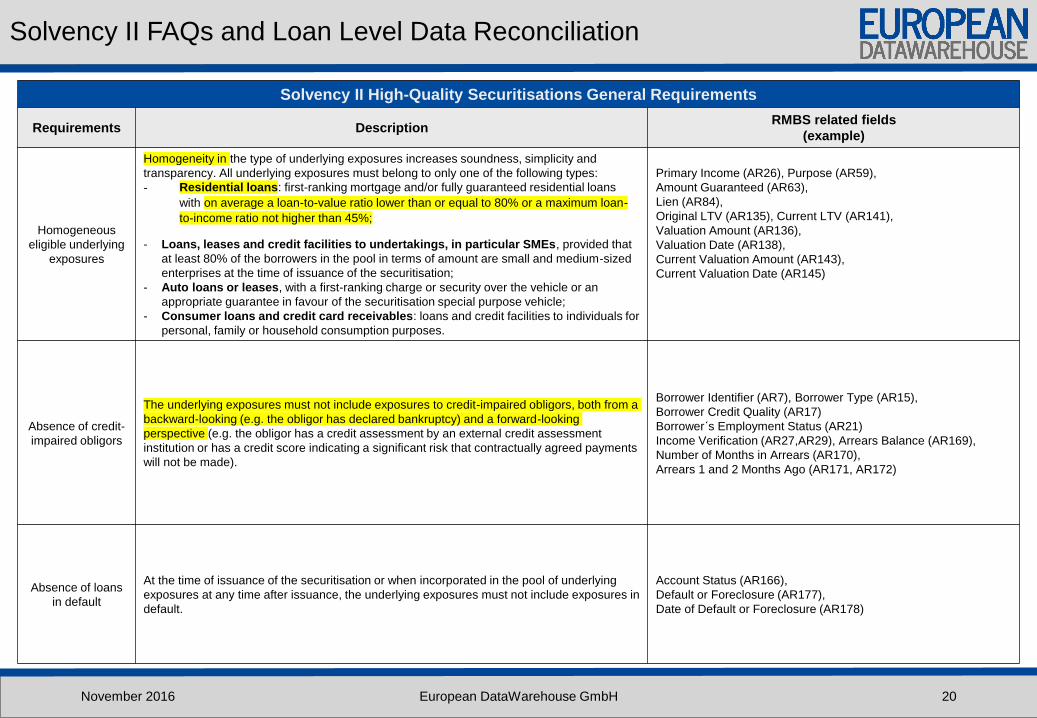

Solvency II High-Quality Securitisations General Requirements

Requirements DescriptionRMBS related fields

(example)

Homogeneous

eligible underlying

exposures

Homogeneity in the type of underlying exposures increases soundness, simplicity and

transparency. All underlying exposures must belong to only one of the following types:

- Residential loans: first-ranking mortgage and/or fully guaranteed residential loans

with on average a loan-to-value ratio lower than or equal to 80% or a maximum loan-

to-income ratio not higher than 45%;

- Loans, leases and credit facilities to undertakings, in particular SMEs, provided that

at least 80% of the borrowers in the pool in terms of amount are small and medium-sized

enterprises at the time of issuance of the securitisation;

- Auto loans or leases, with a first-ranking charge or security over the vehicle or an

appropriate guarantee in favour of the securitisation special purpose vehicle;

- Consumer loans and credit card receivables: loans and credit facilities to individuals for

personal, family or household consumption purposes.

Primary Income (AR26), Purpose (AR59),

Amount Guaranteed (AR63),

Lien (AR84),

Original LTV (AR135), Current LTV (AR141),

Valuation Amount (AR136),

Valuation Date (AR138),

Current Valuation Amount (AR143),

Current Valuation Date (AR145)

Absence of credit-

impaired obligors

The underlying exposures must not include exposures to credit-impaired obligors, both from a

backward-looking (e.g. the obligor has declared bankruptcy) and a forward-looking

perspective (e.g. the obligor has a credit assessment by an external credit assessment

institution or has a credit score indicating a significant risk that contractually agreed payments

will not be made).

Borrower Identifier (AR7), Borrower Type (AR15),

Borrower Credit Quality (AR17)

Borrower´s Employment Status (AR21)

Income Verification (AR27,AR29), Arrears Balance (AR169),

Number of Months in Arrears (AR170),

Arrears 1 and 2 Months Ago (AR171, AR172)

Absence of loans

in default

At the time of issuance of the securitisation or when incorporated in the pool of underlying

exposures at any time after issuance, the underlying exposures must not include exposures in

default.

Account Status (AR166),

Default or Foreclosure (AR177),

Date of Default or Foreclosure (AR178)

Solvency II FAQs and Loan Level Data Reconciliation

November 2016 European DataWarehouse GmbH 20

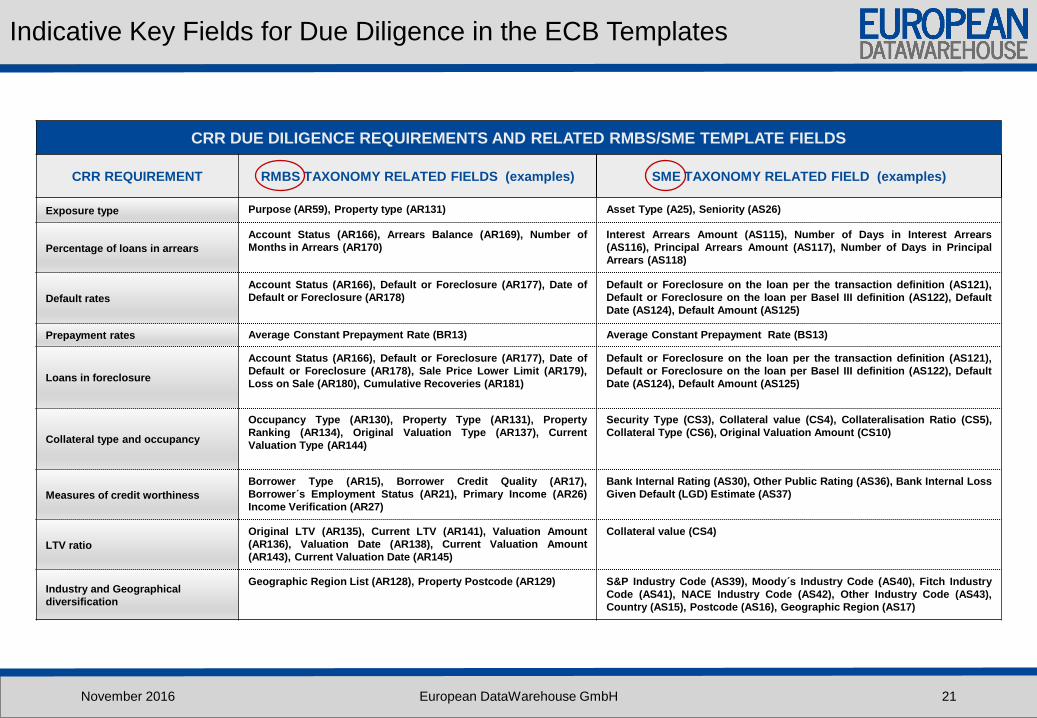

Indicative Key Fields for Due Diligence in the ECB Templates

CRR DUE DILIGENCE REQUIREMENTS AND RELATED RMBS/SME TEMPLATE FIELDS

CRR REQUIREMENT RMBS TAXONOMY RELATED FIELDS (examples) SME TAXONOMY RELATED FIELD (examples)

Exposure type Purpose (AR59), Property type (AR131) Asset Type (A25), Seniority (AS26)

Percentage of loans in arrears

Account Status (AR166), Arrears Balance (AR169), Number of

Months in Arrears (AR170)

Interest Arrears Amount (AS115), Number of Days in Interest Arrears

(AS116), Principal Arrears Amount (AS117), Number of Days in Principal

Arrears (AS118)

Default rates

Account Status (AR166), Default or Foreclosure (AR177), Date of

Default or Foreclosure (AR178)

Default or Foreclosure on the loan per the transaction definition (AS121),

Default or Foreclosure on the loan per Basel III definition (AS122), Default

Date (AS124), Default Amount (AS125)

Prepayment rates Average Constant Prepayment Rate (BR13) Average Constant Prepayment Rate (BS13)

Loans in foreclosure

Account Status (AR166), Default or Foreclosure (AR177), Date of

Default or Foreclosure (AR178), Sale Price Lower Limit (AR179),

Loss on Sale (AR180), Cumulative Recoveries (AR181)

Default or Foreclosure on the loan per the transaction definition (AS121),

Default or Foreclosure on the loan per Basel III definition (AS122), Default

Date (AS124), Default Amount (AS125)

Collateral type and occupancy

Occupancy Type (AR130), Property Type (AR131), Property

Ranking (AR134), Original Valuation Type (AR137), Current

Valuation Type (AR144)

Security Type (CS3), Collateral value (CS4), Collateralisation Ratio (CS5),

Collateral Type (CS6), Original Valuation Amount (CS10)

Measures of credit worthiness

Borrower Type (AR15), Borrower Credit Quality (AR17),

Borrower´s Employment Status (AR21), Primary Income (AR26)

Income Verification (AR27)

Bank Internal Rating (AS30), Other Public Rating (AS36), Bank Internal Loss

Given Default (LGD) Estimate (AS37)

LTV ratio

Original LTV (AR135), Current LTV (AR141), Valuation Amount

(AR136), Valuation Date (AR138), Current Valuation Amount

(AR143), Current Valuation Date (AR145)

Collateral value (CS4)

Industry and Geographical

diversification

Geographic Region List (AR128), Property Postcode (AR129) S&P Industry Code (AS39), Moody´s Industry Code (AS40), Fitch Industry

Code (AS41), NACE Industry Code (AS42), Other Industry Code (AS43),

Country (AS15), Postcode (AS16), Geographic Region (AS17)

November 2016 European DataWarehouse GmbH 21

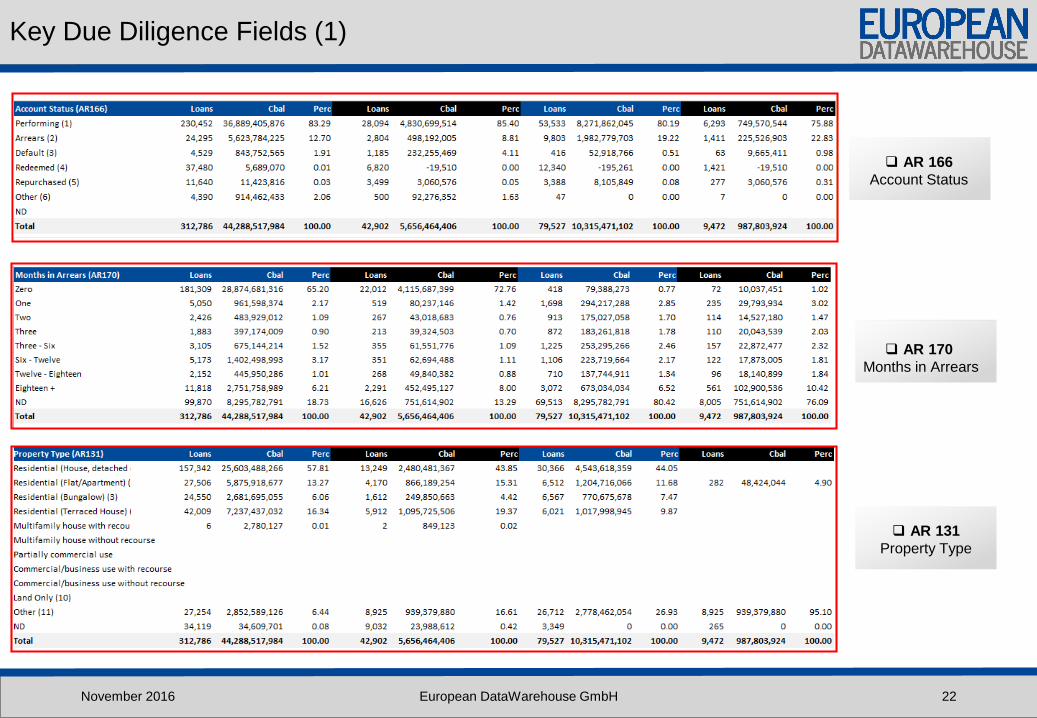

Key Due Diligence Fields (1)

November 2016 European DataWarehouse GmbH 22

AR 166

Account Status

AR 170

Months in Arrears

AR 131

Property Type

November 2016 European DataWarehouse GmbH 23

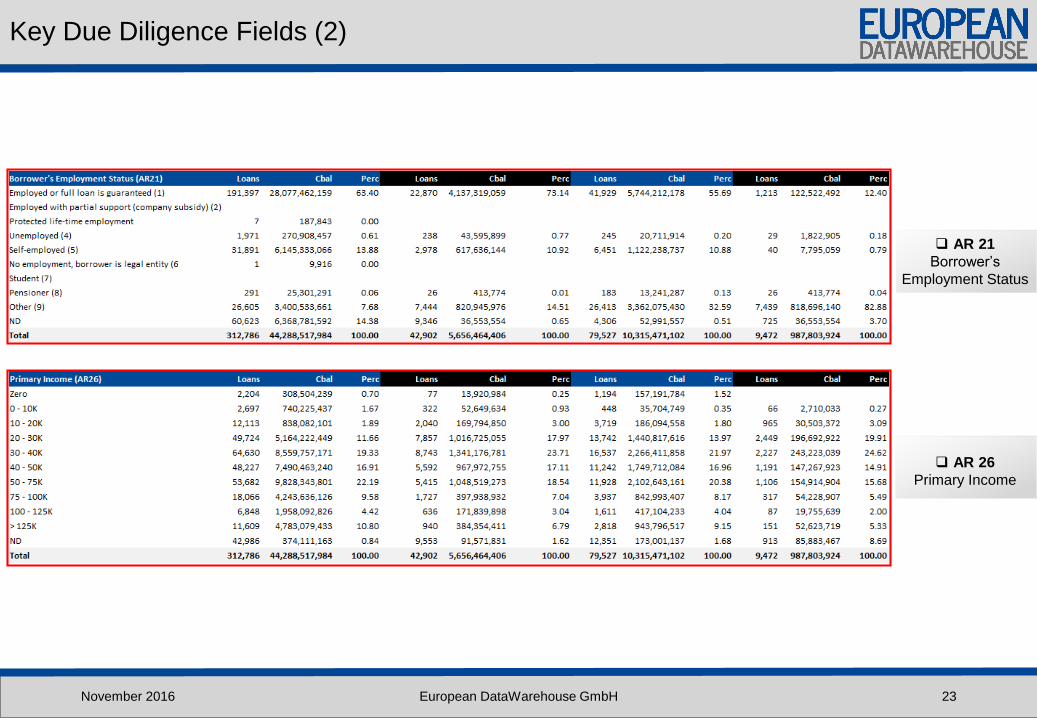

Key Due Diligence Fields (2)

AR 21

Borrower’s

Employment Status

AR 26

Primary Income

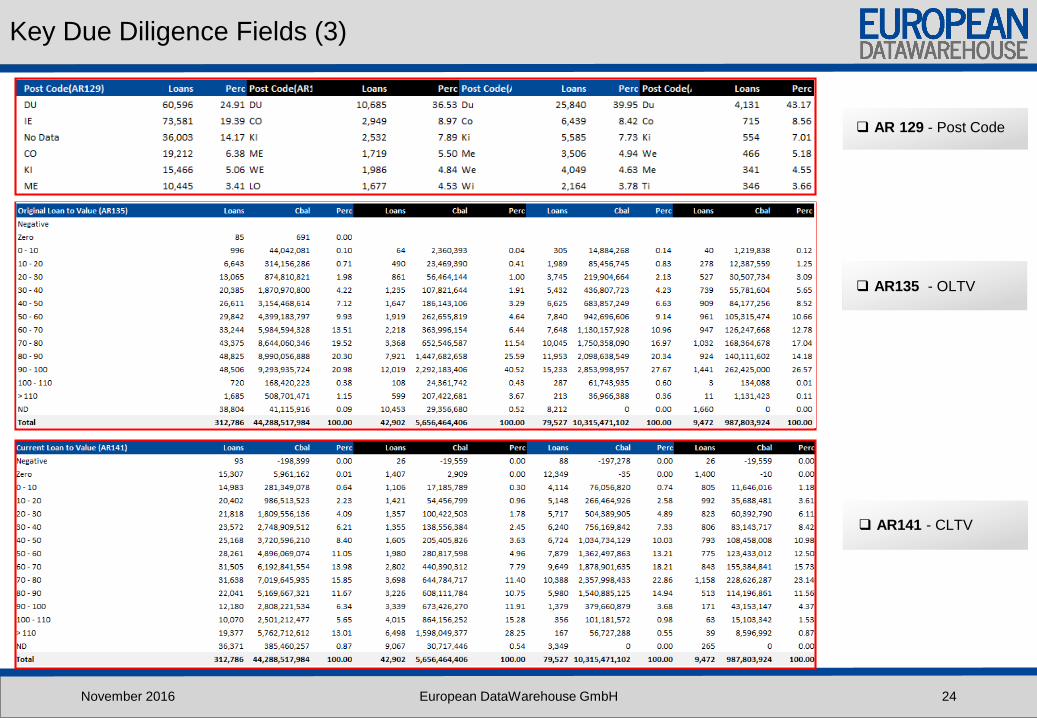

Key Due Diligence Fields (3)

November 2016 European DataWarehouse GmbH 24

AR 129 - Post Code

AR141 - CLTV

AR135 - OLTV

Contact Details

November 2016 European DataWarehouse GmbH 25

Corporate Address:

European DataWarehouse GmbH

Walther-von-Cronberg Platz 2

60594 Frankfurt am Main

GermanyEuropean Transparency Register ID Number: 781559916266-15

+49 (0) 69 8088 4300

www.eurodw.eu

This presentation (the “Presentation”) has been prepared by European DataWarehouse GmbH (the

“Company”) and is being made available for information purposes only.

The Presentation is strictly confidential and any disclosure, use, copying and circulation of this

Presentation is prohibited without the consent from the Company.

Information in this Presentation, including forecast financial information, should not be considered as

advice or a recommendation to investors or potential investors in relation to holding, purchasing or

selling securities or other financial products or instruments and does not take into account your

particular investment objectives, financial situation or needs. No representation, warranty or

undertaking, express or implied, is made as to the accuracy, completeness or appropriateness of the

information and opinions contained in this Presentation.

Under no circumstances shall the Company have any liability for any loss or damage that may arise

from the use of this Presentation or the information or opinions contained herein.

Certain of the information contained herein may include forward-looking statements relating to the

business, financial performance and results of the Company and/or the industry in which it operates.

Forward-looking statements concern future circumstances and results and other statements that are not

historical facts, sometimes identified by the words “believes”, expects”, “predicts”, “intends”, “projects”,

“plans”, “estimates”, “aims”, “foresees”, “anticipates”, “targets”, “may”, “will”, “should” and similar

expression.

The forward-looking looking statements, contained in this Presentation, including assumptions, opinions

and views of the Company or cited from third party sources are solely opinions and forecasts which are

uncertain and subject to risks.

Disclaimer