Embed Size (px)

Citation preview

European Gas Market:

Current State and

Perspectives

ENERGETIKA XXI

Saint-Petersburg State University of Economics

St. Petersburg, November 11, 2015

Sergei Komlev Head of Contract Structuring and Price Formation

Gazprom Export

© ZMB 2

Short-Term Trends on the European “Far Abroad” Gas Market

2

3Q 2014 3Q 2015 Changes, bcm Changes, %

Consumption 340.7 360.3 19.6 5.8%

Indigenous production* 191.1 193.6 2.5 1.3%

Net gas UGS

withdrawals/injections** -21.0 -6.2 14.8

Imports*** 170.6 172.6 2.2 1.3%

Sources: IEA, Eurostat, National Statistical Agencies, Estimates by Gazprom Export LLC as of October 2015

Consumption, Indigenous Production, Imports, and Gas Withdrawals

* Indigenous production includes Norway ** Plus means that withdrawals exceed injections and vice versa *** Consumption = Domestic Production + Gas withdrawals/injections balance of UGS + Import requirements.

Bcm

Gas consumption in Europe increased by 19.6 bcm or by 6% in 3Q of 2015 compared with Q3 of 2014. On the supply side indigenous production increased by 2.5 bcm or by 1.3%.

European companies injected only 6.2 bcm more gas than withdraw out of UGS in response to increase in demand. In Q3 2014 withdrawn volumes were 21 bcm. According to preliminary data, Far Abroad countries imports increased on par with the indigenous production.

28 93 162

176 0 0

223 223 223

37 121 213

151 192 237

241 185 89

Major Factors Affecting Gas Consumption in Europe*

2014 3Q 2015

1.Favorable weather conditions

(cold and long winter, hot summer)

2. Economic recovery

3. Use of gas in power generation

Total consumption 3Q 2015 to 3Q 2014 -10.1% +5.8%

3 * Factors for 3Q of 2015 and 2014 are specified in comparison with 5-year averages

© ZMB 4

Sources: PIRA, Gazprom Export LLC Estimates

1-3Q 2014 1-3Q 2015 ∆, bcm ∆, %

Total gas consumption 227.8 243.2 15.3 6.7%

Gas consumption in power

generation 45.6 52.4 6.8 15.0%

Share of power generation in gas

consumption 20.0% 21.5% 1.5 p.p.

Gas consumption in other sectors

182.3 190.8 8.5 4.7%

*EU Countries:

• Germany,

• Italy,

• United Kingdom,

• Netherlands,

• France,

• Spain

In the three quarters of 2015 demand for gas in power generation in six EU countries grew up by 15%, significantly above total

consumption growth.

The share of power generation sector also increased – up to 21.5% in the three quarters of 2015.

(bcm)

Demand for Gas in Power Generation

Demand for Gas in Power Generation for Six EU Countries*

*Set of Countries:

• Germany,

• Italy,

• United Kingdom,

• Netherlands,

• France,

• Spain

© ZMB 5

0

50

100

150

200

250

300

350

400

Switching price Actual NBP day-ahead

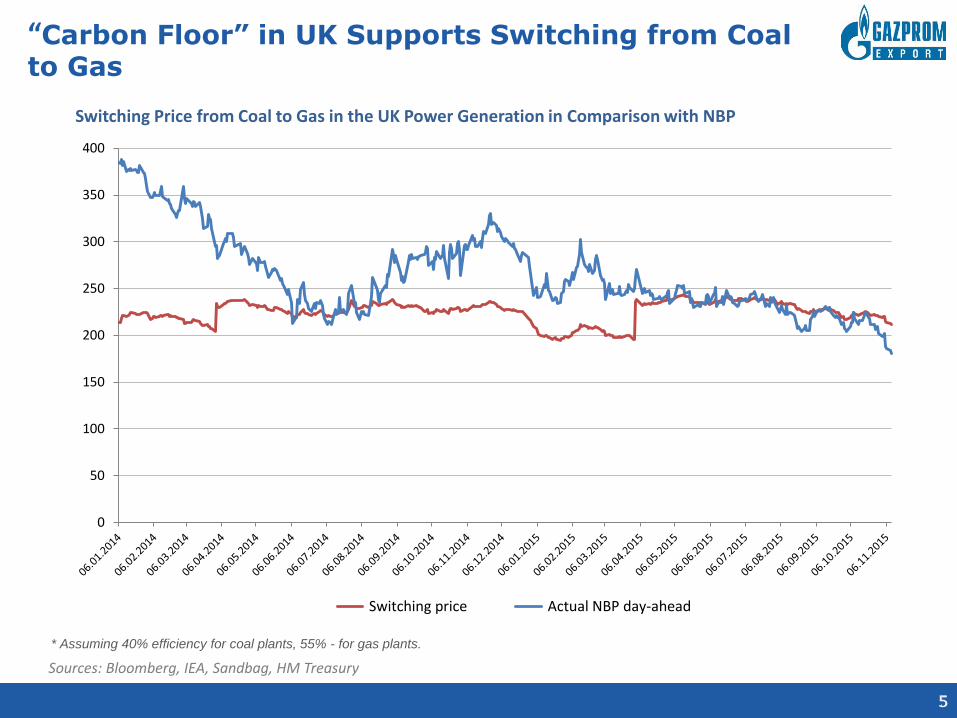

“Carbon Floor” in UK Supports Switching from Coal to Gas

Switching Price from Coal to Gas in the UK Power Generation in Comparison with NBP

5

Sources: Bloomberg, IEA, Sandbag, HM Treasury

* Assuming 40% efficiency for coal plants, 55% - for gas plants.

© ZMB 6

Deliveries by Major Countries 3Q of 2015

3Q 2014 3Q 2015 Changes, bcm Changes, %

Gazprom JSC 114.2 115.4 1.2 1.0%

Algeria (incl. LNG) 24.6 21.8 -2.8 -11.5%

Qatar 17.9 19.9 2.0 11.0%

Iran 6.8 6.5 -0.3 -4.5%

Lybia (incl. LNG) 4.8 5.7 0.9 19.2%

Deliveries by Major Exporters

2013 2014 Changes, bcm Changes,

%

Norway* 82.4 90.2 7.8 9.4%

Netherlands 43.3 37.2 -6.1 -14.1%

United Kingdom 30.6 32.2 1,6 5.2%

Bcm

Bcm Deliveries by Major Indigenous Producers

Sources: Bloomberg, IEA, Eurostat, National Statistical Agencies, Estimates by Gazprom Export LLC as of October 2015

* Including pipeline and LNG supply of Norway to the European market, but not supply to Asia and America

6

© ZMB

Mid-Term Gas Demand Forecasts

Gazprom Gas Deliveries to Europe*

7

* European countries including Turkey except for CIS and Baltics

Mid-Term Forecasts of Gas Consumption in Europe

~156-160

bcma

Largely driven by weather conditions Gazprom’s mid-term (2016-2018) estimate of gas deliveries to Europe is 156-160 bcma.

138.6 150.0

138.8

161.5 146.6

159-160

$303

$373 $397

$383

$345

$237-240

225

275

325

375

425

475

525

0

40

80

120

160

200

2010 2011 2012 2013 2014 2015

bcm

$/mcm

Source: Annual Reports of PJSC Gazprom

Source: CERA, PIRA, IEA

100.0

90.1

81.0

87.3 89.6 90.3 88.3

92.8 95.2

84.6

87.4 87.8

78

84

89

95

100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% 2006-2014 actual

CERA (Nov-2014)

CERA (Jul-2014)

PIRA (Oct-2014)

PIRA (Jul-2014)

IEA (May-2014)

IEA (May-2015)

28 93 162

176 0 0

223 223 223

37 121 213

151 192 237

241 185 89

Asian Price Premium

8

NBP «Month-Ahead» Prices versus Japanese LNG Prices

Sources: Bloomberg, METI, Platts, Customs Statistics of South Korea and Japan

Asian Premium dropped to $0.8 MMBTU compared to $5.7 MMBTU a year earlier. Oil-Indexed LNG Prices were $9.9 MMBTU in August 2015 compared to $16.9 MMBTU in August 2014.

*JKM

© ZMB 9 9

LNG Deliveries to Europe

LNG Deliveries to Europe by Country

3Q 2014 3Q 2015 Changes, bcm Changes, %

Qatar 17.9 19.9 2.0 11.0%

Algeria 10.7 9.6 -1.2 -11.4%

Nigeria 4.3 5.2 1.0 22.9%

Norway 1.7 2.2 0.5 28.0

Trinidad and Tobago 2.3 1.4 -0.9 -39.8%

Peru 0.9 1.1 0.2 -18.3%

Yemen 0.0 0.1 0.1

Oman 0.0 0.1 0.1

Equatorial Guinea 0.1 0.0 -0.1 -100.0%

Total 38.0 39.6 1.5 4.0%

Sources: Bloomberg, Estimates by Gazprom Export LLC

© ZMB 10

Hypothetical LNG Prices Based on Futures Prices: Full Costs of North American LNG are Higher than European Hub Prices

180

200

220

240

260

280

300

320

340

360

380

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

Sep

-17

Dec

-17

Mar

-18

Jun

-18

Sep

-18

Dec

-18

Mar

-19

Jun

-19

Sep

-19

Dec

-19

Mar

-20

Jun

-20

Sep

-20

Dec

-20

Mar

-21

Jun

-21

Sep

-21

Dec

-21

Mar

-22

Henry Hub-Based Cost-Plus Price Range NBP forward curve

$/mcm

Sources: Bloomberg, Wood McKenzie, Platts, PIRA * P = HH forwards * 115% + X, where X is cost of delivering to Europe

Full costs of US LNG delivered to Europe are higher than European hubs’ prices on a forward curve. Sales to Europe will not compensate full costs of the off-taker from the US LNG terminals.

28 93 162

176 0 0

223 223 223

37 121 213

151 192 237

241 185 89

Long Term European Natural Gas Consumption

According to consensus forecast for 2025 and 2035, demand could be 23% and 27% higher compared to 2014

11

28 93 162

176 0 0

223 223 223

37 121 213

151 192 237

241 185 89

Natural Gas European Demand and Production Gap

Due to falling indigenous production European demand for additional gas imports could be 149 bcm by 2025 and 195 bcm by 2035, according to consensus forecast 12

© ZMB 13

OECD Europe Power Generation Forecast by Type of Fuel

Source: IEA

0

100

200

300

400

500

600

700

800

2013 2020 2025 2030 2035

Other renewables

Bioenergy

Hydro

Nuclear

Gas

Oil

Coal

Mtoe

15,7% 17,9% 20,7%

21,9% 23,6%

© ZMB 14

OECD Europe Residential and Commercial Sector Energy Consumption Forecast by Type of Fuel

Source: IEA

0

100

200

300

400

500

600

2013 2020 2025 2030 2035

Other renewables

Bioenergy

Heat

Electricity

Gas

Oil

Coal

Mtoe

35,3% 35,5% 37,7%

35,7% 35,5%

© ZMB 15

OECD Europe Energy Consumption in Industry by

Type of Fuel

Source: IEA

0

50

100

150

200

250

300

350

2013 2020 2025 2030 2035

Other renewables

Bioenergy

Heat

Electricity

Gas

Oil

Coal

Mtoe

31,5% 28,5% 27,9%

27,3% 26,8%

© ZMB 16

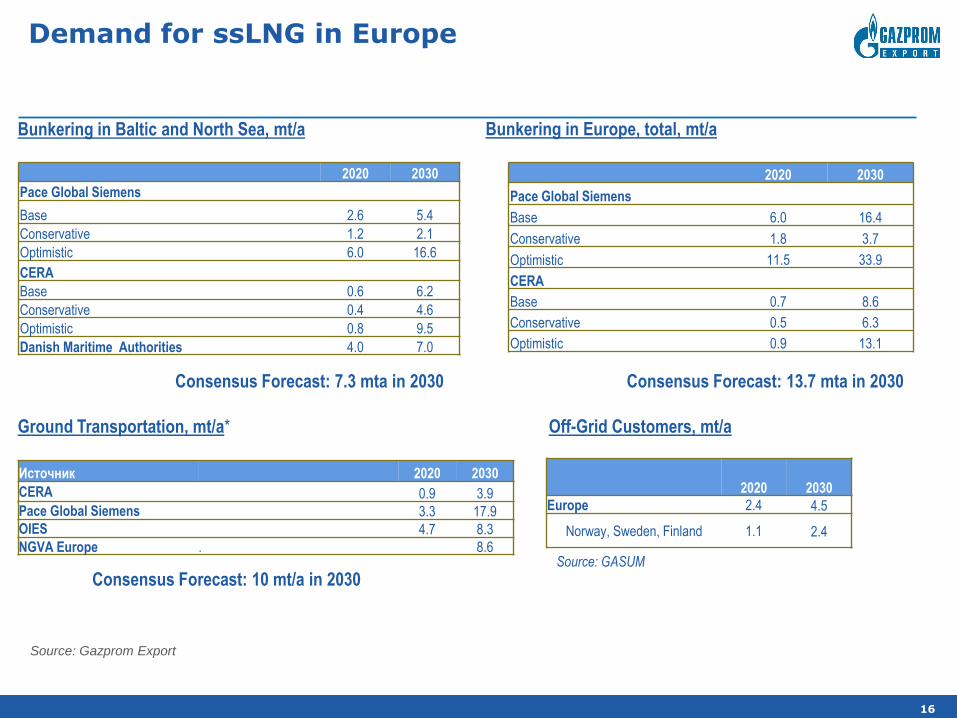

2020 2030

Pace Global Siemens

Base 2.6 5.4

Conservative 1.2 2.1

Optimistic 6.0 16.6

CERA

Base 0.6 6.2

Conservative 0.4 4.6

Optimistic 0.8 9.5

Danish Maritime Authorities 4.0 7.0

Bunkering in Baltic and North Sea, mt/a Bunkering in Europe, total, mt/a

2020 2030

Pace Global Siemens

Base 6.0 16.4

Conservative 1.8 3.7

Optimistic 11.5 33.9

CERA

Base 0.7 8.6

Conservative 0.5 6.3

Optimistic 0.9 13.1

Consensus Forecast: 7.3 mta in 2030 Consensus Forecast: 13.7 mta in 2030

Ground Transportation, mt/a*

Источник 2020 2030

CERA 0.9 3.9

Pace Global Siemens 3.3 17.9

OIES 4.7 8.3

NGVA Europe . 8.6

Demand for ssLNG in Europe

Consensus Forecast: 10 mt/a in 2030

2020 2030

Europe 2.4 4.5

Norway, Sweden, Finland 1.1 2.4

Off-Grid Customers, mt/a

Source: GASUM

Source: Gazprom Export

© ZMB 17

Schematic Hub-Price Behavior in Different Hybrid Pricing Models

100

150

200

250

300

350

400

Liquid Hubs

Oil-indexed LTC

Liquid Hubs

$/mcm

100

150

200

250

300

350

400

Illiquid Hubs

Oil-indexed LTC

Illiquid Hubs

$/mcm

The difference between the two hybrids is in liquidity of hubs measured by the

degree of financialization by the importers/intermediaries of their take-or-pay

obligations from the long-term oil-indexed contracts.

© ZMB 18

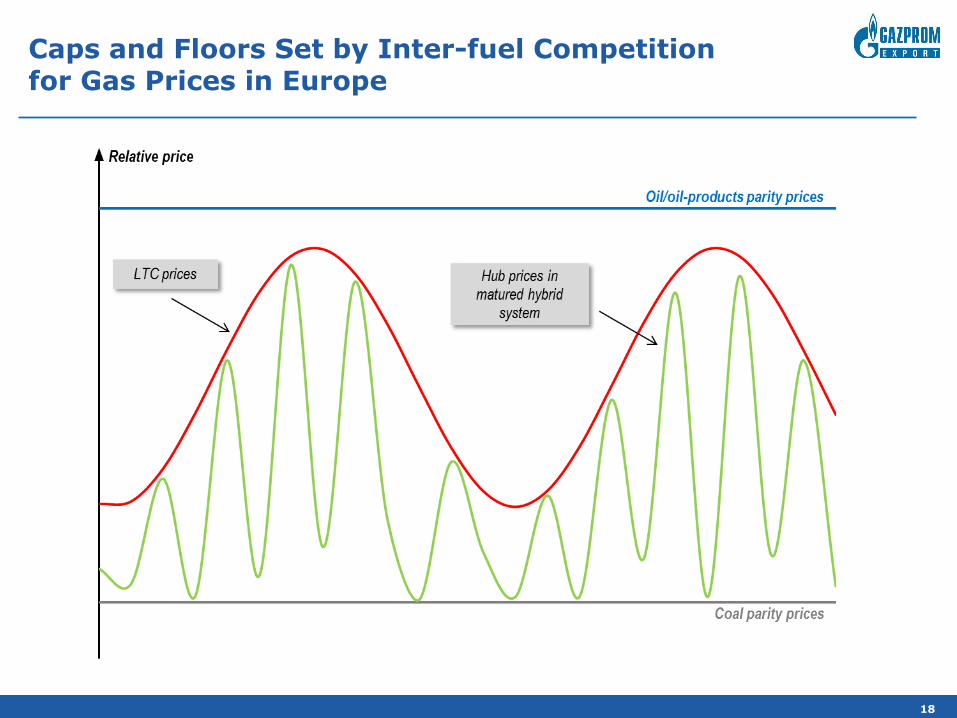

Caps and Floors Set by Inter-fuel Competition for Gas Prices in Europe

© ZMB 19

Caps and Floors Set by Inter-fuel Competition for Gas Prices (2)

© ZMB 20 20

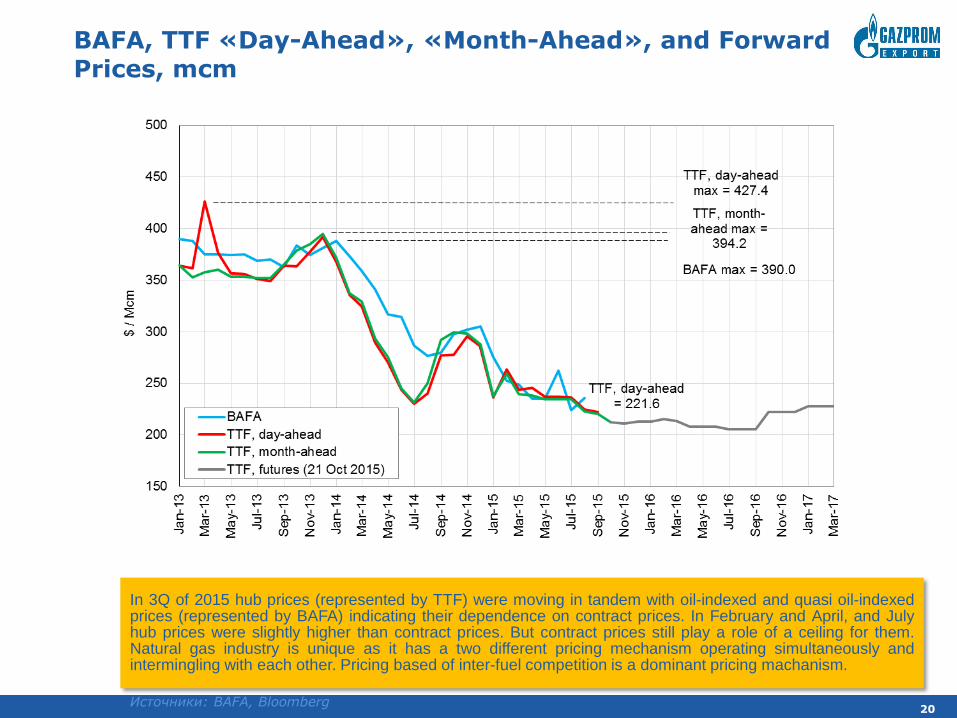

BAFA, TTF «Day-Ahead», «Month-Ahead», and Forward Prices, mcm

Источники: BAFA, Bloomberg

In 3Q of 2015 hub prices (represented by TTF) were moving in tandem with oil-indexed and quasi oil-indexed prices (represented by BAFA) indicating their dependence on contract prices. In February and April, and July hub prices were slightly higher than contract prices. But contract prices still play a role of a ceiling for them. Natural gas industry is unique as it has a two different pricing mechanism operating simultaneously and intermingling with each other. Pricing based of inter-fuel competition is a dominant pricing machanism.

© ZMB 21

Overblown Gas Demand Expectations in Europe in the Past Resulted in Market Overcontraction

Source: Purvin and Gerts 1998 Forecast for 2015, Gazprom Export calculations

© ZMB 22

There is Need to Rebalance Market by Eliminating Paper and Physical Gas Disconnect

Source: Gazprom Export

Midstreamers LTC Contracts

End-users

Hub

Year-ahead contract

Portfolio

optimization

Sell Q1 volume on

hubs under a

forward contract

that equals to

MAQ+

Buy back Q2

volume of paper

gas that equals to

physical demand

by the end-users

Under current market conditions:

Q1 > Q2

THANK YOU FOR YOUR ATTENTION!

![Energy Consumption and Greenhouse Gas Emissions 1998_ifa_marrakech_kongshaug[1]](https://img.pdfslide.net/doc/110x75/577d1e951a28ab4e1e8ecdc9/energy-consumption-and-greenhouse-gas-emissions-1998ifamarrakechkongshaug1.jpg)