Embed Size (px)

Citation preview

European Healthcare Sector

Post-summer prescription

September 2015

Generally smooth sailing through the recent market correction

Buying opportunities: Merck KGaA, Gerresheimer, Rhön Klinikum

DR. MARCUS WIEPRECHT

+49-69-78808 221 | [email protected] MARKUS GOLA

+49-69-78808-233 | [email protected]

For important disclosure information please see Appendix section at the end of this report.

2 / 44

This page is intentionally left blank.

11 SEPTEMBER 2015 3 / 44

For important disclosure information please see Appendix section at the end of this report

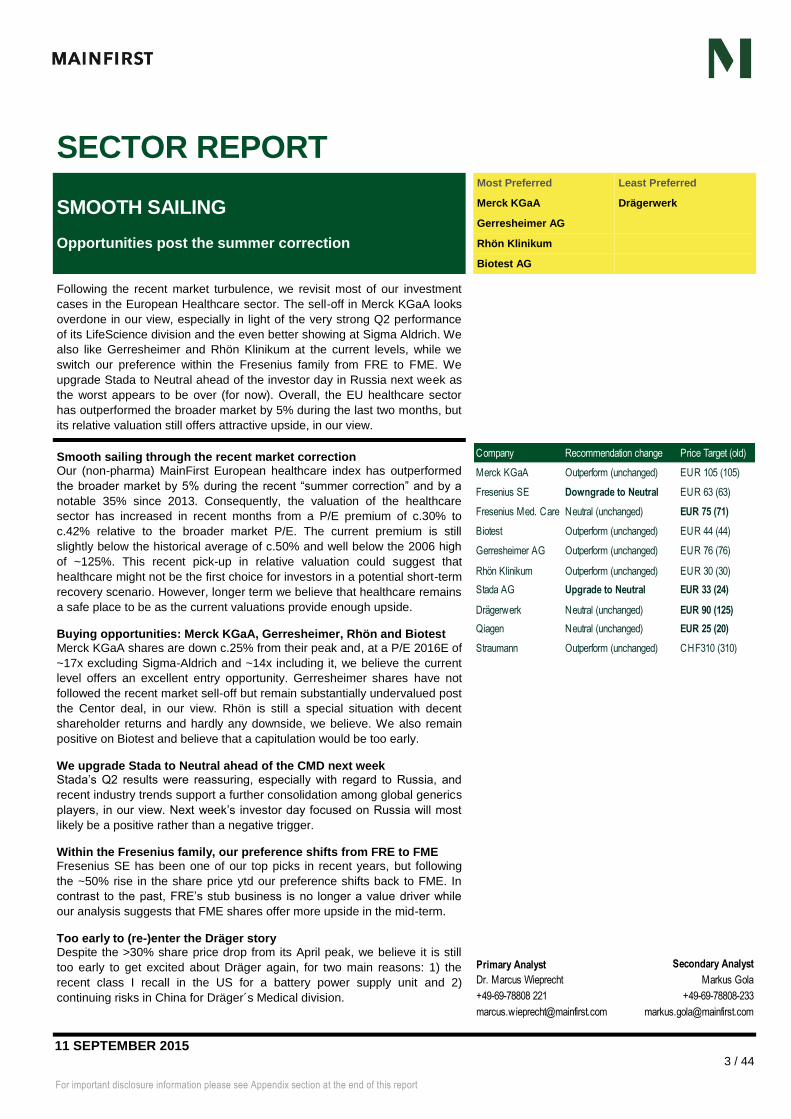

SECTOR REPORT

SMOOTH SAILING

Opportunities post the summer correction

Most Preferred Least Preferred

Merck KGaA Drägerwerk

Gerresheimer AG

Rhön Klinikum

Biotest AG

Following the recent market turbulence, we revisit most of our investment

cases in the European Healthcare sector. The sell-off in Merck KGaA looks

overdone in our view, especially in light of the very strong Q2 performance

of its LifeScience division and the even better showing at Sigma Aldrich. We

also like Gerresheimer and Rhön Klinikum at the current levels, while we

switch our preference within the Fresenius family from FRE to FME. We

upgrade Stada to Neutral ahead of the investor day in Russia next week as

the worst appears to be over (for now). Overall, the EU healthcare sector

has outperformed the broader market by 5% during the last two months, but

its relative valuation still offers attractive upside, in our view.

Smooth sailing through the recent market correction Our (non-pharma) MainFirst European healthcare index has outperformed

the broader market by 5% during the recent “summer correction” and by a

notable 35% since 2013. Consequently, the valuation of the healthcare

sector has increased in recent months from a P/E premium of c.30% to

c.42% relative to the broader market P/E. The current premium is still

slightly below the historical average of c.50% and well below the 2006 high

of ~125%. This recent pick-up in relative valuation could suggest that

healthcare might not be the first choice for investors in a potential short-term

recovery scenario. However, longer term we believe that healthcare remains

a safe place to be as the current valuations provide enough upside.

Buying opportunities: Merck KGaA, Gerresheimer, Rhön and Biotest

Merck KGaA shares are down c.25% from their peak and, at a P/E 2016E of

~17x excluding Sigma-Aldrich and ~14x including it, we believe the current

level offers an excellent entry opportunity. Gerresheimer shares have not

followed the recent market sell-off but remain substantially undervalued post

the Centor deal, in our view. Rhön is still a special situation with decent

shareholder returns and hardly any downside, we believe. We also remain

positive on Biotest and believe that a capitulation would be too early.

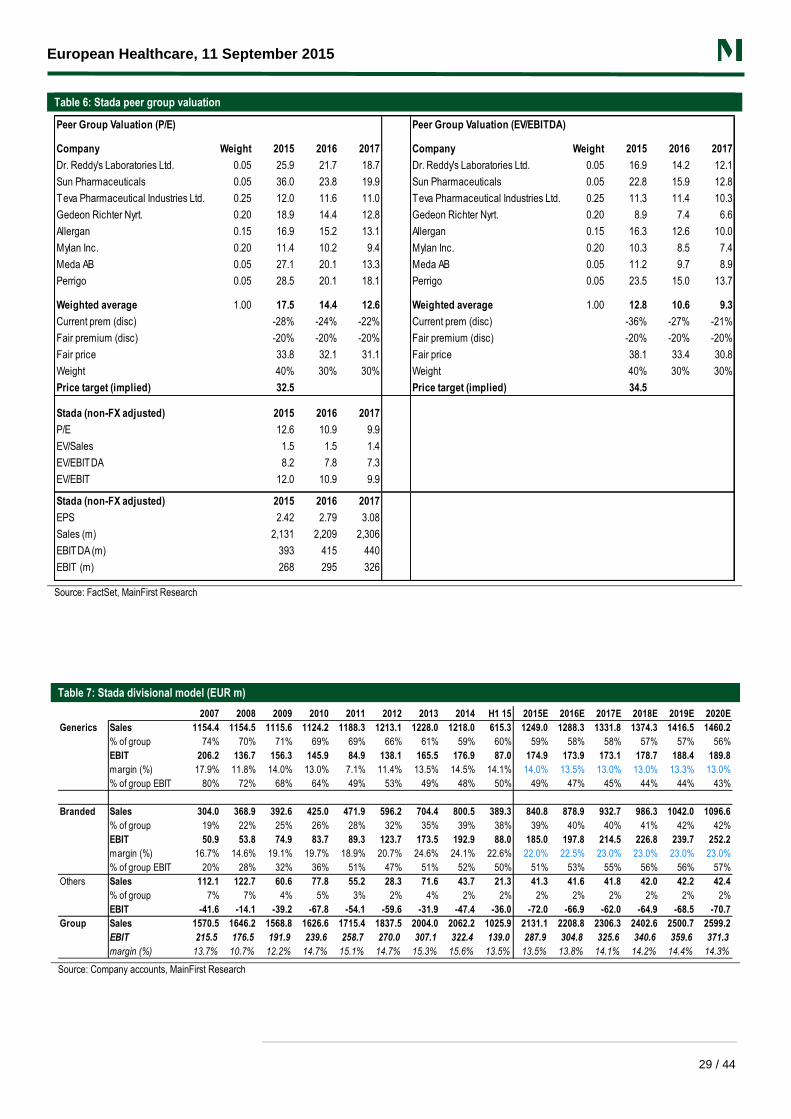

We upgrade Stada to Neutral ahead of the CMD next week Stada’s Q2 results were reassuring, especially with regard to Russia, and

recent industry trends support a further consolidation among global generics

players, in our view. Next week’s investor day focused on Russia will most

likely be a positive rather than a negative trigger.

Within the Fresenius family, our preference shifts from FRE to FME

Fresenius SE has been one of our top picks in recent years, but following

the ~50% rise in the share price ytd our preference shifts back to FME. In

contrast to the past, FRE’s stub business is no longer a value driver while

our analysis suggests that FME shares offer more upside in the mid-term.

Too early to (re-)enter the Dräger story Despite the >30% share price drop from its April peak, we believe it is still

too early to get excited about Dräger again, for two main reasons: 1) the

recent class I recall in the US for a battery power supply unit and 2)

continuing risks in China for Dräger´s Medical division.

Company Recommendation change Price Target (old)

Merck KGaA Outperform (unchanged) EUR 105 (105)

Fresenius SE Downgrade to Neutral EUR 63 (63)

Fresenius Med. Care Neutral (unchanged) EUR 75 (71)

Biotest Outperform (unchanged) EUR 44 (44)

Gerresheimer AG Outperform (unchanged) EUR 76 (76)

Rhön Klinikum Outperform (unchanged) EUR 30 (30)

Stada AG Upgrade to Neutral EUR 33 (24)

Drägerwerk Neutral (unchanged) EUR 90 (125)

Qiagen Neutral (unchanged) EUR 25 (20)

Straumann Outperform (unchanged) CHF310 (310)

Primary Analyst Secondary Analyst

Dr. Marcus Wieprecht Markus Gola

+49-69-78808 221 +49-69-78808-233

European Healthcare, 11 September 2015

4 / 44

Table of Contents

Bigger picture post the market correction.................................................................... 5 Healthcare outperformed during the recent market correction ..................................... 5 Relative sector valuation still below historical average ................................................. 5

Key takeaways for our universe .................................................................................... 7 Buying opportunities in Merck KGaA, Gerresheimer, Rhön and Biotest .................. 7

We upgrade Stada to Neutral ahead of the CMD next week ................................... 7

Within the Fresenius family, our preference shifts from FRE to FME ...................... 7

Too early to (re-)enter the Dräger story ................................................................... 7

Merck KGaA (MRK GY / MRCG.DE) ............................................................................... 9

Fresenius SE (FRE GY / FREG.DE) .............................................................................. 13

Fresenius Medical Care (FME GY / FMEG.DE) ............................................................ 15

Gerresheimer AG (GXI GY / GXIG.DE) ......................................................................... 17

Rhön Klinikum (RHK GY / RHKG.DE) .......................................................................... 19

Biotest AG (BIO3 GR / BIOG_p.DE) ............................................................................. 21

Stada AG (SAZ GY / STAGn.DE) .................................................................................. 23 This is why we turn less negative, but… .................................................................... 25 Q2 results painted a slightly better picture ................................................................. 25 Recent industry trends support further consolidation… .............................................. 25 …but major risks remain unchanged .......................................................................... 27 Balance sheet risks .................................................................................................... 27 Russian consumer and currency risks ....................................................................... 27 Valuation still attractive, even excluding FX adjustments ........................................... 28

Drägerwerk (DRW3 GR / DRW3.F) ............................................................................... 31

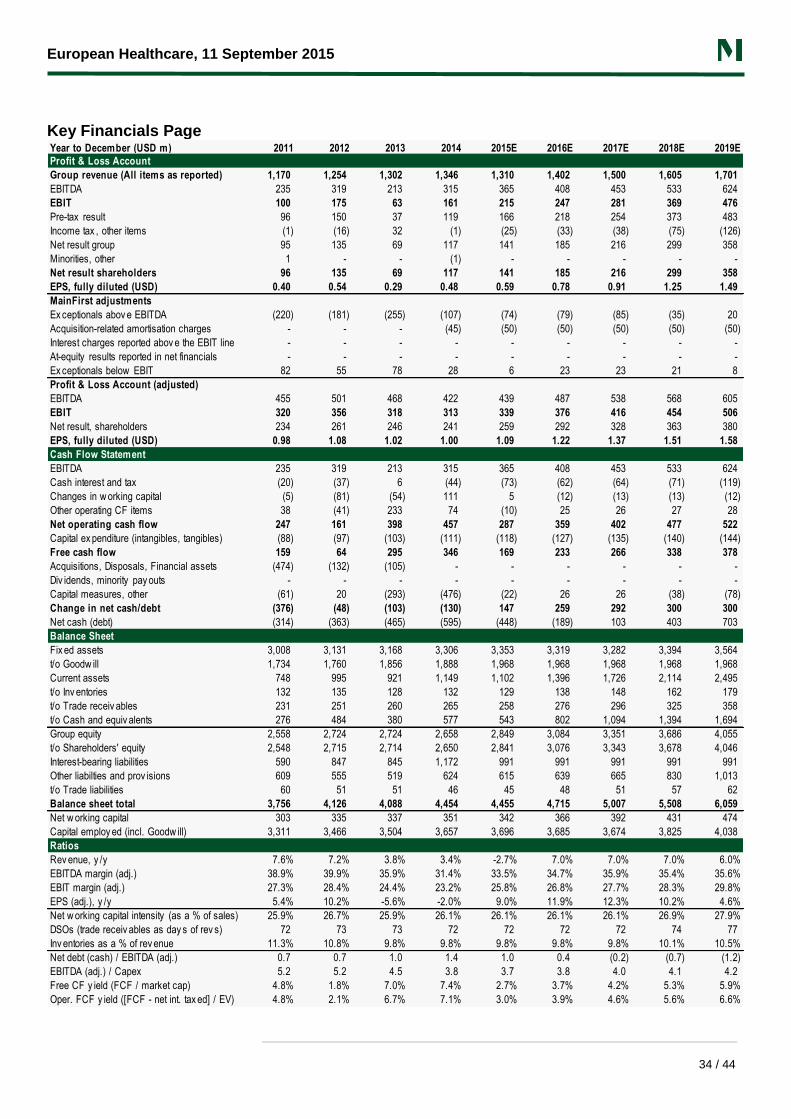

Qiagen (QIA GY / QGENF.DE) ...................................................................................... 33

Straumann (STMN SW / STMN.SW) ............................................................................. 35

Appendix: Regulatory Disclosures and Disclaimer ................................................... 37

European Healthcare, 11 September 2015

5 / 44

Bigger picture post the market correction

Healthcare outperformed during the recent market correction

The slowdown of emerging market economies and the unexpected currency moves in

China increased fears of a downturn in global GDP, leading to plummeting equities

around the world last month. Chinese equities in particular saw an extraordinary

meltdown. On 4th

September 2015, the Chinese central bank released a statement in

which Mr Zhou, the governor of the central bank, said that “the correction in the stock

market is almost done” and that the situation in China was back under control. Whether

this is in fact the case remains to be seen. In any event, we believe this is a good point in

time to take a closer look at our European healthcare universe and to identify investment

opportunities arising from the recent sell-off.

Our proprietary “MainFirst Healthcare Index”, which includes non-pharma healthcare/

medtech companies, indicates that the recent correction resulted in a further

outperformance of the healthcare sector compared to the broader market. Since 2013,

healthcare has outperformed the broader market by c.35% (around +60% versus circa

+25%) and by 5% in August alone, owing to its more defensive nature and lower

exposure to emerging markets relative to other sectors.

Chart 1: Healthcare sector perf. vs broader market: Long term Chart 2: …Short-term view

Source: FactSet, MainFirst Research Source: FactSet, MainFirst Research

The companies included in our healthcare sector index are: Coloplast A/S Class B,

DiaSorin S.p.A., Elekta AB Class B, Draegerwerk AG & Co. KGaA Pref, Essilor

International SA, Eurofins Scientific Société Européenne, Fagron NV, Fresenius SE &

Co. KGaA, Fresenius Medical Care AG & Co. KGaA, Galenica AG, Gerresheimer AG,

Getinge AB Class B, GN Store Nord A/S, Grifols, S.A. Class A, Korian-Medica SA,

Merck KGaA, Oriola-KD Oyj Class B, Orpea SA, Qiagen NV, Rhön-Klinikum AG, Smith &

Nephew plc, Sonova Holding AG, Sorin S.p.A., Stada Arzneimittel AG, Straumann

Holding AG, Synergy Health plc, Tecan Trading AG, and William Demant Holding A/S.

Relative sector valuation still below historical average

The healthcare sector’s valuation has seen a substantial multiple expansion since 2012,

from c.15x forward P/E to 23x a few months ago. During the recent market correction,

the sector P/E dropped back to c.20x (see following chart). However, the current level is

still below the 30x forward P/E peak seen in 2006, but well above the lows of around 13x

forward P/E hit in 2008. While the sector’s multiple expansion over the last 3.5 years

may look impressive, we would point out that the relative picture looks clearly less

outstanding. Relative to the broader market, the healthcare sector trades at a premium of

~42%, which is still slightly below the long run average (01/2002 – 09/2015) of c.50%

and substantially below the record high of ~125% reached in early 2006.

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014 2015

MainFirst Health Care Index STOXX Europe 600

90

100

110

120

130

140

150

160

170

180

01/13 03/13 05/13 07/13 09/13 11/13 01/14 03/14 05/14 07/14 09/14 11/14 01/15 03/15 05/15 07/15 09/15

MainFirst Health Care Index STOXX Europe 600

Our (non-pharma) European

healthcare index has outperformed

the broader market by 35% since

2013 and by 5% in the recent market

correction since early August

Due to the higher valuation, we focus

on stocks that were unjustifiably hit

by the sell-off or investment cases

not fully recognised by the market

European Healthcare, 11 September 2015

6 / 44

The pick-up in relative valuation in recent months may suggest that in a short-term

recovery scenario, healthcare might not be the first choice for investors. However, longer

term, we believe that the sector is still a very safe place to be and current valuations

provide enough upside to remain positive on the sector.

Chart 3: Historical P/E valuation of European Healthcare Sector

Source: FactSet, MainFirst Research

Chart 4: Historical P/E valuation of Healthcare relative to the broader STOXX Europe 600 index

Source: FactSet, MainFirst Research

0

5

10

15

20

25

30

35

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

12m

fo

rwar

d P

E

MainFirst Health Care Index

1

1.25

1.5

1.75

2

2.25

2.5

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Rel

ativ

e P

/E p

rem

ium

MainFirst Health Care Index/STOXX Europe 600

European Healthcare, 11 September 2015

7 / 44

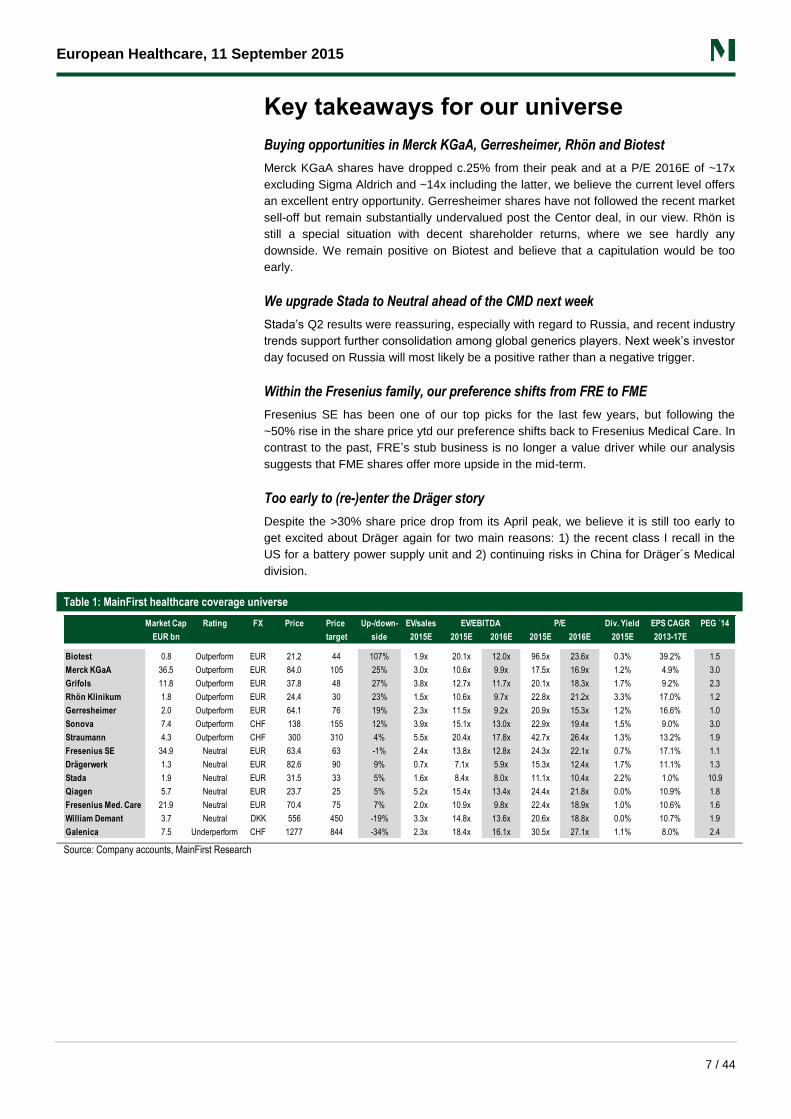

Key takeaways for our universe

Buying opportunities in Merck KGaA, Gerresheimer, Rhön and Biotest

Merck KGaA shares have dropped c.25% from their peak and at a P/E 2016E of ~17x

excluding Sigma Aldrich and ~14x including the latter, we believe the current level offers

an excellent entry opportunity. Gerresheimer shares have not followed the recent market

sell-off but remain substantially undervalued post the Centor deal, in our view. Rhön is

still a special situation with decent shareholder returns, where we see hardly any

downside. We remain positive on Biotest and believe that a capitulation would be too

early.

We upgrade Stada to Neutral ahead of the CMD next week

Stada’s Q2 results were reassuring, especially with regard to Russia, and recent industry

trends support further consolidation among global generics players. Next week’s investor

day focused on Russia will most likely be a positive rather than a negative trigger.

Within the Fresenius family, our preference shifts from FRE to FME

Fresenius SE has been one of our top picks for the last few years, but following the

~50% rise in the share price ytd our preference shifts back to Fresenius Medical Care. In

contrast to the past, FRE’s stub business is no longer a value driver while our analysis

suggests that FME shares offer more upside in the mid-term.

Too early to (re-)enter the Dräger story

Despite the >30% share price drop from its April peak, we believe it is still too early to

get excited about Dräger again for two main reasons: 1) the recent class I recall in the

US for a battery power supply unit and 2) continuing risks in China for Dräger´s Medical

division.

Table 1: MainFirst healthcare coverage universe

Source: Company accounts, MainFirst Research

Market Cap Rating FX Price Price Up-/down- EV/sales Div. Yield EPS CAGR PEG ´14

EUR bn target side 2015E 2015E 2016E 2015E 2016E 2015E 2013-17E

Biotest 0.8 Outperform EUR 21.2 44 107% 1.9x 20.1x 12.0x 96.5x 23.6x 0.3% 39.2% 1.5

Merck KGaA 36.5 Outperform EUR 84.0 105 25% 3.0x 10.6x 9.9x 17.5x 16.9x 1.2% 4.9% 3.0

Grifols 11.8 Outperform EUR 37.8 48 27% 3.8x 12.7x 11.7x 20.1x 18.3x 1.7% 9.2% 2.3

Rhön Klinikum 1.8 Outperform EUR 24.4 30 23% 1.5x 10.6x 9.7x 22.8x 21.2x 3.3% 17.0% 1.2

Gerresheimer 2.0 Outperform EUR 64.1 76 19% 2.3x 11.5x 9.2x 20.9x 15.3x 1.2% 16.6% 1.0

Sonova 7.4 Outperform CHF 138 155 12% 3.9x 15.1x 13.0x 22.9x 19.4x 1.5% 9.0% 3.0

Straumann 4.3 Outperform CHF 300 310 4% 5.5x 20.4x 17.8x 42.7x 26.4x 1.3% 13.2% 1.9

Fresenius SE 34.9 Neutral EUR 63.4 63 -1% 2.4x 13.8x 12.8x 24.3x 22.1x 0.7% 17.1% 1.1

Drägerwerk 1.3 Neutral EUR 82.6 90 9% 0.7x 7.1x 5.9x 15.3x 12.4x 1.7% 11.1% 1.3

Stada 1.9 Neutral EUR 31.5 33 5% 1.6x 8.4x 8.0x 11.1x 10.4x 2.2% 1.0% 10.9

Qiagen 5.7 Neutral EUR 23.7 25 5% 5.2x 15.4x 13.4x 24.4x 21.8x 0.0% 10.9% 1.8

Fresenius Med. Care 21.9 Neutral EUR 70.4 75 7% 2.0x 10.9x 9.8x 22.4x 18.9x 1.0% 10.6% 1.6

William Demant 3.7 Neutral DKK 556 450 -19% 3.3x 14.8x 13.6x 20.6x 18.8x 0.0% 10.7% 1.9

Galenica 7.5 Underperform CHF 1277 844 -34% 2.3x 18.4x 16.1x 30.5x 27.1x 1.1% 8.0% 2.4

EV/EBITDA P/E

European Healthcare, 11 September 2015

8 / 44

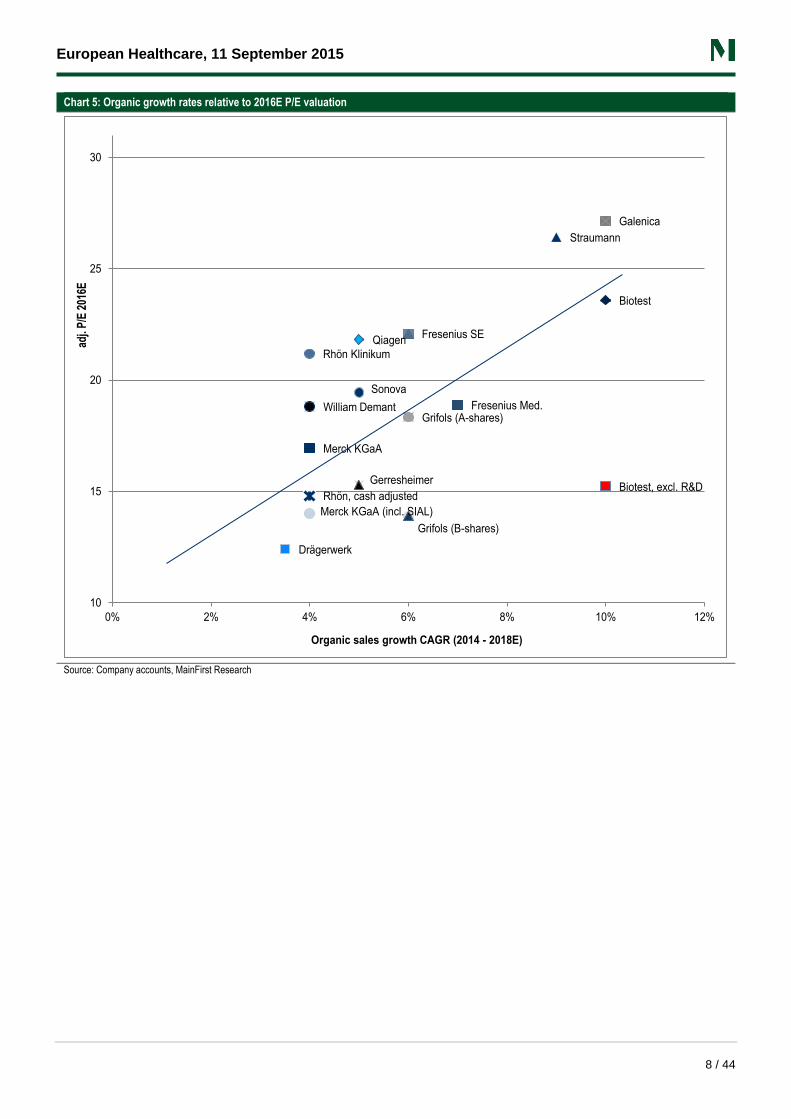

Chart 5: Organic growth rates relative to 2016E P/E valuation

Source: Company accounts, MainFirst Research

Biotest

Biotest, excl. R&D

Fresenius Med.

Fresenius SE

Galenica

Gerresheimer

Grifols (A-shares)

Grifols (B-shares)

Merck KGaA

Qiagen

Rhön Klinikum

Straumann

William Demant

Rhön, cash adjusted

Sonova

Drägerwerk

Merck KGaA (incl. SIAL)

10

15

20

25

30

0% 2% 4% 6% 8% 10% 12%

adj.

P/E

201

6E

Organic sales growth CAGR (2014 - 2018E)

European Healthcare, 11 September 2015

11 SEPTEMBER 2015 9 / 44

For important disclosure information please see Appendix section at the end of this report

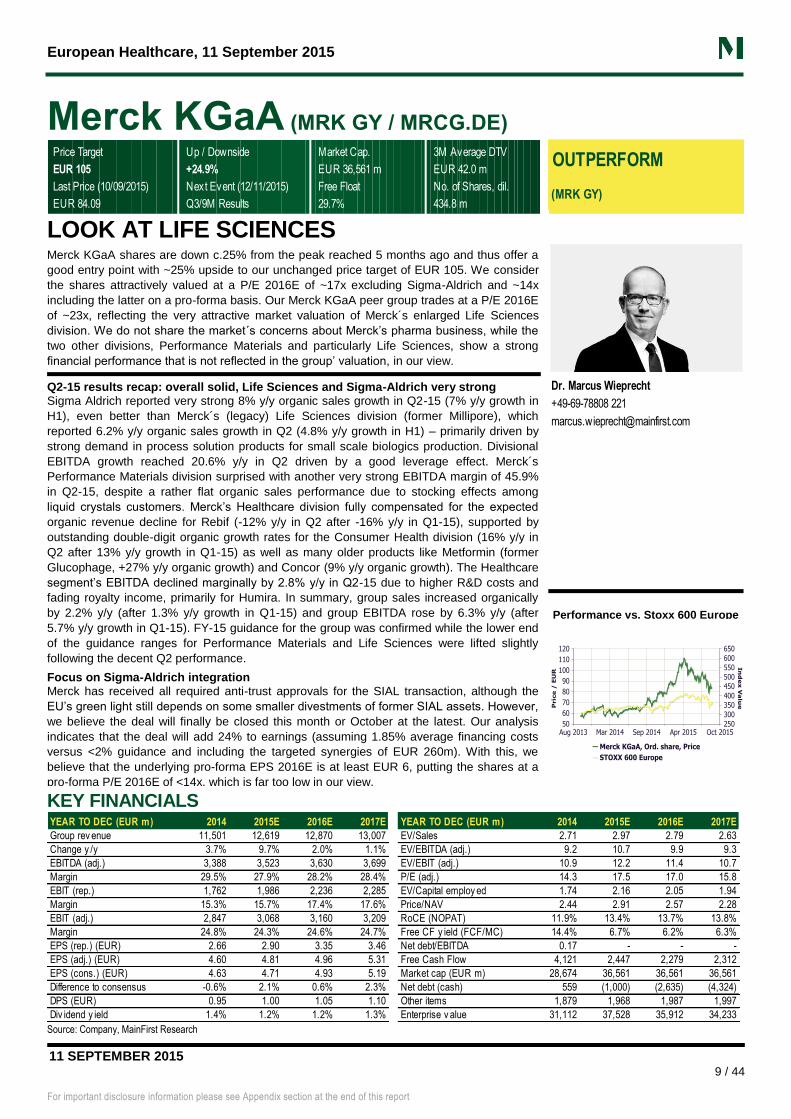

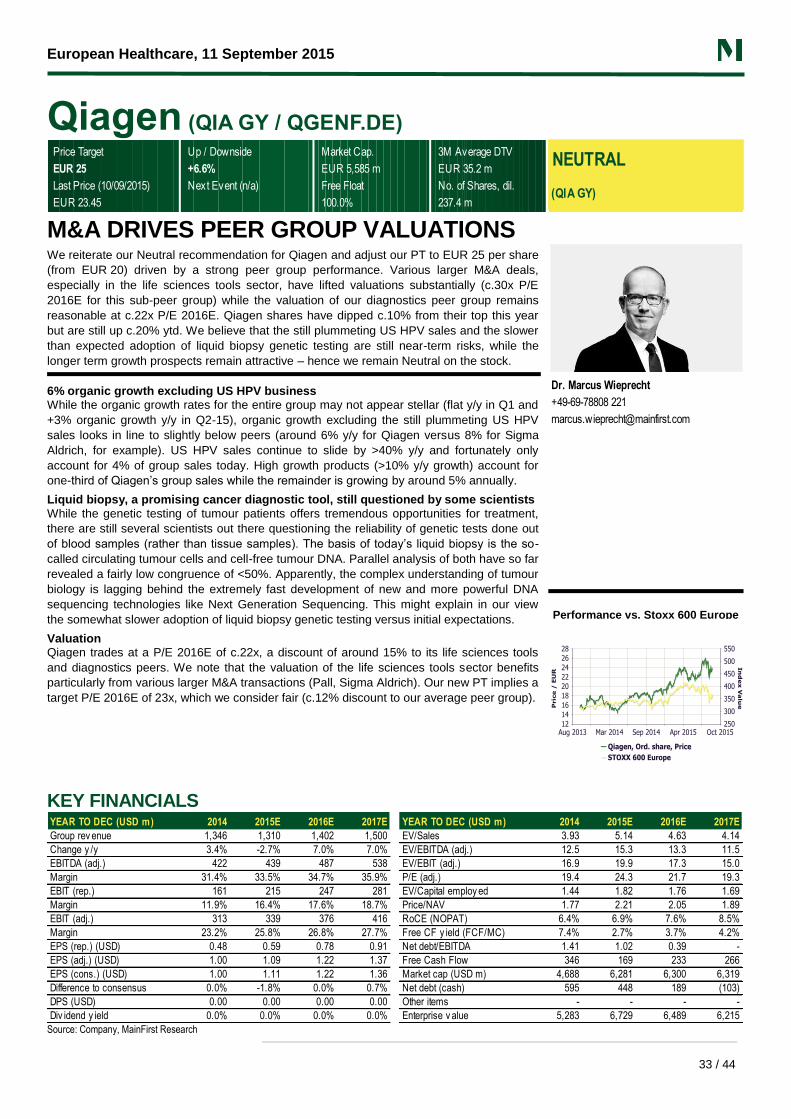

Merck KGaA (MRK GY / MRCG.DE)

Price Target Up / Downside Market Cap. 3M Average DTV

EUR 105 +24.9% EUR 36,561 m EUR 42.0 m

Last Price (10/09/2015) Next Event (12/11/2015) Free Float No. of Shares, dil.

EUR 84.09 Q3/9M Results 29.7% 434.8 m

OUTPERFORM

(MRK GY)

LOOK AT LIFE SCIENCES Merck KGaA shares are down c.25% from the peak reached 5 months ago and thus offer a

good entry point with ~25% upside to our unchanged price target of EUR 105. We consider

the shares attractively valued at a P/E 2016E of ~17x excluding Sigma-Aldrich and ~14x

including the latter on a pro-forma basis. Our Merck KGaA peer group trades at a P/E 2016E

of ~23x, reflecting the very attractive market valuation of Merck´s enlarged Life Sciences

division. We do not share the market´s concerns about Merck’s pharma business, while the

two other divisions, Performance Materials and particularly Life Sciences, show a strong

financial performance that is not reflected in the group’ valuation, in our view.

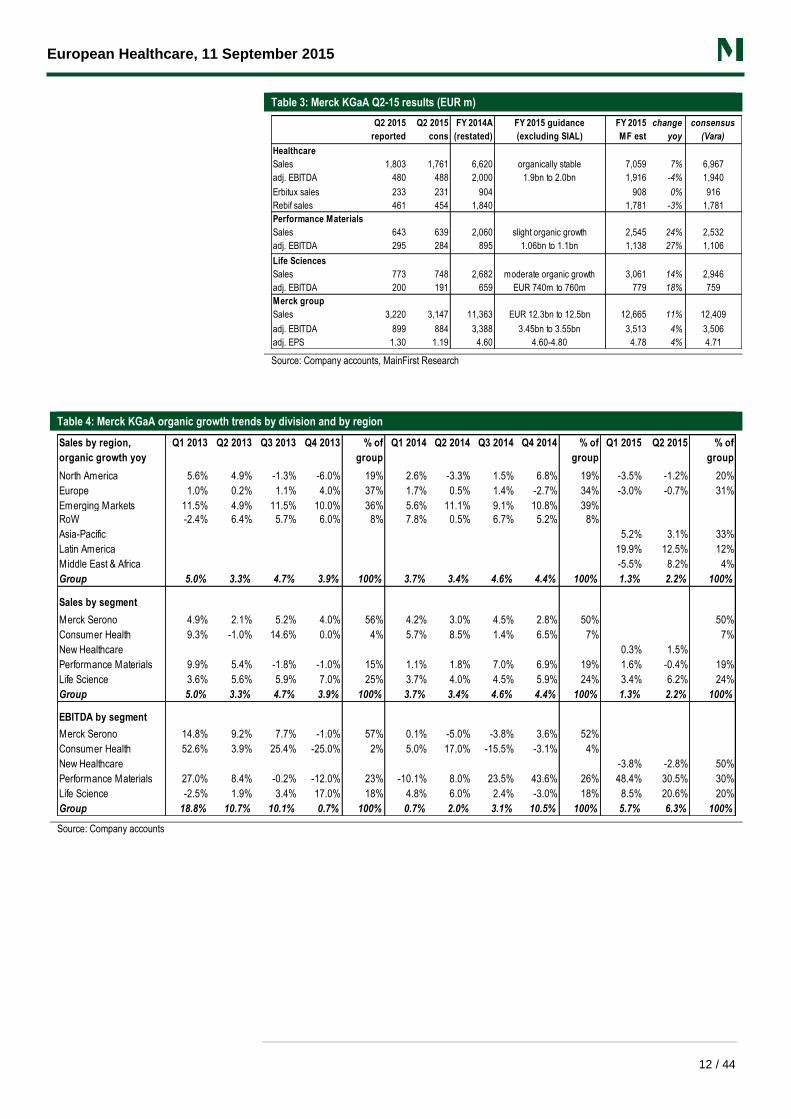

Q2-15 results recap: overall solid, Life Sciences and Sigma-Aldrich very strong Sigma Aldrich reported very strong 8% y/y organic sales growth in Q2-15 (7% y/y growth in

H1), even better than Merck´s (legacy) Life Sciences division (former Millipore), which

reported 6.2% y/y organic sales growth in Q2 (4.8% y/y growth in H1) – primarily driven by

strong demand in process solution products for small scale biologics production. Divisional

EBITDA growth reached 20.6% y/y in Q2 driven by a good leverage effect. Merck´s

Performance Materials division surprised with another very strong EBITDA margin of 45.9%

in Q2-15, despite a rather flat organic sales performance due to stocking effects among

liquid crystals customers. Merck’s Healthcare division fully compensated for the expected

organic revenue decline for Rebif (-12% y/y in Q2 after -16% y/y in Q1-15), supported by

outstanding double-digit organic growth rates for the Consumer Health division (16% y/y in

Q2 after 13% y/y growth in Q1-15) as well as many older products like Metformin (former

Glucophage, +27% y/y organic growth) and Concor (9% y/y organic growth). The Healthcare

segment’s EBITDA declined marginally by 2.8% y/y in Q2-15 due to higher R&D costs and

fading royalty income, primarily for Humira. In summary, group sales increased organically

by 2.2% y/y (after 1.3% y/y growth in Q1-15) and group EBITDA rose by 6.3% y/y (after

5.7% y/y growth in Q1-15). FY-15 guidance for the group was confirmed while the lower end

of the guidance ranges for Performance Materials and Life Sciences were lifted slightly

following the decent Q2 performance.

Focus on Sigma-Aldrich integration Merck has received all required anti-trust approvals for the SIAL transaction, although the

EU’s green light still depends on some smaller divestments of former SIAL assets. However,

we believe the deal will finally be closed this month or October at the latest. Our analysis

indicates that the deal will add 24% to earnings (assuming 1.85% average financing costs

versus <2% guidance and including the targeted synergies of EUR 260m). With this, we

believe that the underlying pro-forma EPS 2016E is at least EUR 6, putting the shares at a

pro-forma P/E 2016E of <14x, which is far too low in our view.

Dr. Marcus Wieprecht

+49-69-78808 221

Performance vs. Stoxx 600 Europe

KEY FINANCIALS

Source: Company, MainFirst Research

YEAR TO DEC (EUR m) 2014 2015E 2016E 2017E YEAR TO DEC (EUR m) 2014 2015E 2016E 2017E

Group rev enue 11,501 12,619 12,870 13,007 EV/Sales 2.71 2.97 2.79 2.63

Change y /y 3.7% 9.7% 2.0% 1.1% EV/EBITDA (adj.) 9.2 10.7 9.9 9.3

EBITDA (adj.) 3,388 3,523 3,630 3,699 EV/EBIT (adj.) 10.9 12.2 11.4 10.7

Margin 29.5% 27.9% 28.2% 28.4% P/E (adj.) 14.3 17.5 17.0 15.8

EBIT (rep.) 1,762 1,986 2,236 2,285 EV/Capital employ ed 1.74 2.16 2.05 1.94

Margin 15.3% 15.7% 17.4% 17.6% Price/NAV 2.44 2.91 2.57 2.28

EBIT (adj.) 2,847 3,068 3,160 3,209 RoCE (NOPAT) 11.9% 13.4% 13.7% 13.8%

Margin 24.8% 24.3% 24.6% 24.7% Free CF y ield (FCF/MC) 14.4% 6.7% 6.2% 6.3%

EPS (rep.) (EUR) 2.66 2.90 3.35 3.46 Net debt/EBITDA 0.17 - - -

EPS (adj.) (EUR) 4.60 4.81 4.96 5.31 Free Cash Flow 4,121 2,447 2,279 2,312

EPS (cons.) (EUR) 4.63 4.71 4.93 5.19 Market cap (EUR m) 28,674 36,561 36,561 36,561

Difference to consensus -0.6% 2.1% 0.6% 2.3% Net debt (cash) 559 (1,000) (2,635) (4,324)

DPS (EUR) 0.95 1.00 1.05 1.10 Other items 1,879 1,968 1,987 1,997

Div idend y ield 1.4% 1.2% 1.2% 1.3% Enterprise v alue 31,112 37,528 35,912 34,233

European Healthcare, 11 September 2015

11 SEPTEMBER 2015 10 / 44

For important disclosure information please see Appendix section at the end of this report

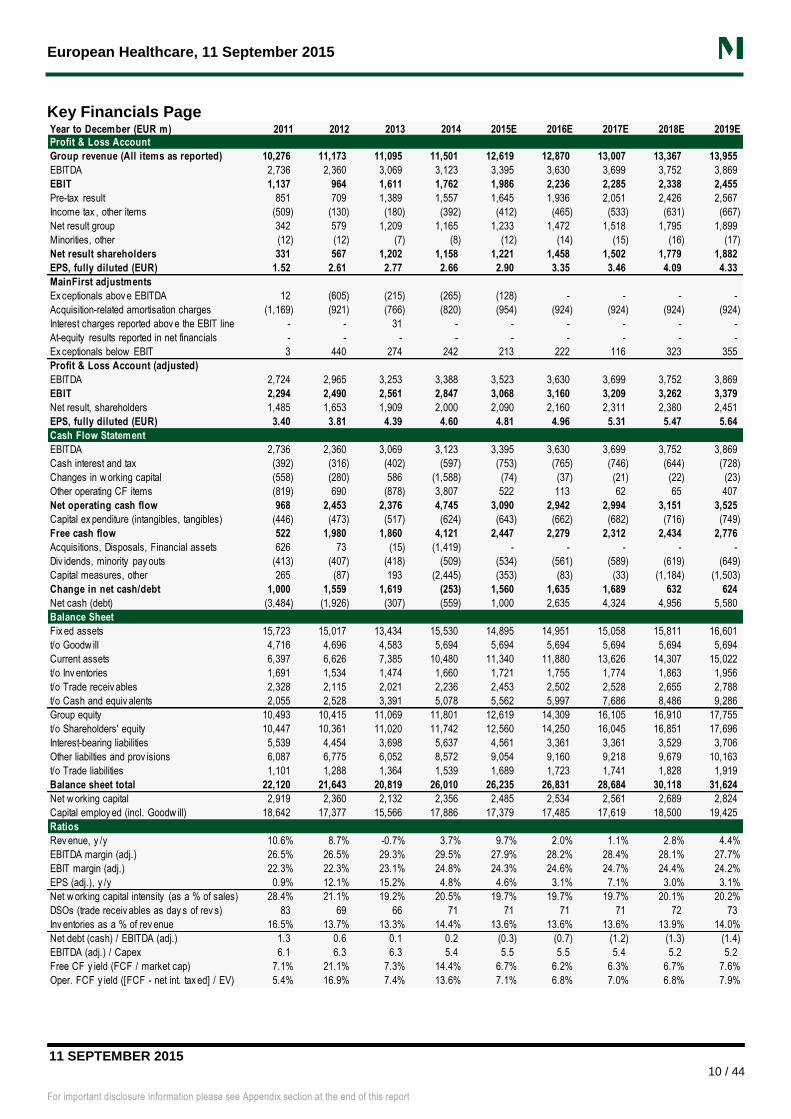

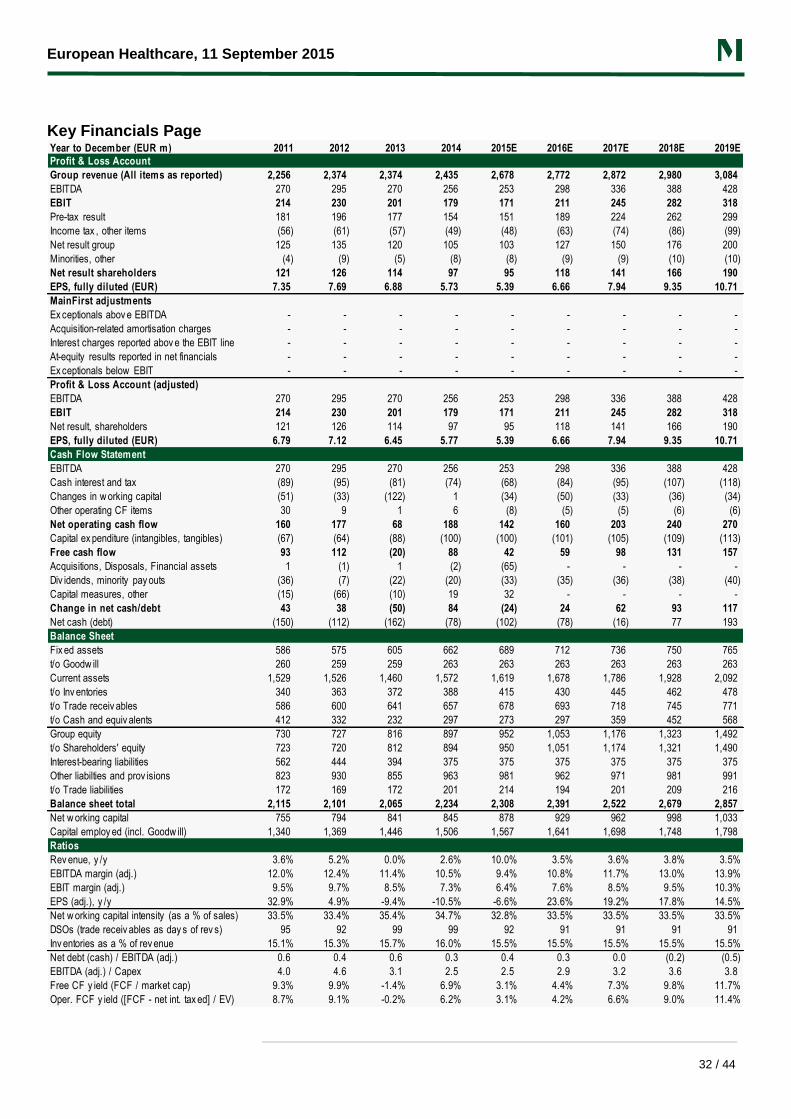

Key Financials Page

Year to December (EUR m) 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Profit & Loss Account

Group revenue (All items as reported) 10,276 11,173 11,095 11,501 12,619 12,870 13,007 13,367 13,955

EBITDA 2,736 2,360 3,069 3,123 3,395 3,630 3,699 3,752 3,869

EBIT 1,137 964 1,611 1,762 1,986 2,236 2,285 2,338 2,455

Pre-tax result 851 709 1,389 1,557 1,645 1,936 2,051 2,426 2,567

Income tax , other items (509) (130) (180) (392) (412) (465) (533) (631) (667)

Net result group 342 579 1,209 1,165 1,233 1,472 1,518 1,795 1,899

Minorities, other (12) (12) (7) (8) (12) (14) (15) (16) (17)

Net result shareholders 331 567 1,202 1,158 1,221 1,458 1,502 1,779 1,882

EPS, fully diluted (EUR) 1.52 2.61 2.77 2.66 2.90 3.35 3.46 4.09 4.33

MainFirst adjustments

Ex ceptionals abov e EBITDA 12 (605) (215) (265) (128) - - - -

Acquisition-related amortisation charges (1,169) (921) (766) (820) (954) (924) (924) (924) (924)

Interest charges reported abov e the EBIT line - - 31 - - - - - -

At-equity results reported in net financials - - - - - - - - -

Ex ceptionals below EBIT 3 440 274 242 213 222 116 323 355

Profit & Loss Account (adjusted)

EBITDA 2,724 2,965 3,253 3,388 3,523 3,630 3,699 3,752 3,869

EBIT 2,294 2,490 2,561 2,847 3,068 3,160 3,209 3,262 3,379

Net result, shareholders 1,485 1,653 1,909 2,000 2,090 2,160 2,311 2,380 2,451

EPS, fully diluted (EUR) 3.40 3.81 4.39 4.60 4.81 4.96 5.31 5.47 5.64

Cash Flow Statement

EBITDA 2,736 2,360 3,069 3,123 3,395 3,630 3,699 3,752 3,869

Cash interest and tax (392) (316) (402) (597) (753) (765) (746) (644) (728)

Changes in w orking capital (558) (280) 586 (1,588) (74) (37) (21) (22) (23)

Other operating CF items (819) 690 (878) 3,807 522 113 62 65 407

Net operating cash flow 968 2,453 2,376 4,745 3,090 2,942 2,994 3,151 3,525

Capital ex penditure (intangibles, tangibles) (446) (473) (517) (624) (643) (662) (682) (716) (749)

Free cash flow 522 1,980 1,860 4,121 2,447 2,279 2,312 2,434 2,776

Acquisitions, Disposals, Financial assets 626 73 (15) (1,419) - - - - -

Div idends, minority pay outs (413) (407) (418) (509) (534) (561) (589) (619) (649)

Capital measures, other 265 (87) 193 (2,445) (353) (83) (33) (1,184) (1,503)

Change in net cash/debt 1,000 1,559 1,619 (253) 1,560 1,635 1,689 632 624

Net cash (debt) (3,484) (1,926) (307) (559) 1,000 2,635 4,324 4,956 5,580

Balance Sheet

Fix ed assets 15,723 15,017 13,434 15,530 14,895 14,951 15,058 15,811 16,601

t/o Goodw ill 4,716 4,696 4,583 5,694 5,694 5,694 5,694 5,694 5,694

Current assets 6,397 6,626 7,385 10,480 11,340 11,880 13,626 14,307 15,022

t/o Inv entories 1,691 1,534 1,474 1,660 1,721 1,755 1,774 1,863 1,956

t/o Trade receiv ables 2,328 2,115 2,021 2,236 2,453 2,502 2,528 2,655 2,788

t/o Cash and equiv alents 2,055 2,528 3,391 5,078 5,562 5,997 7,686 8,486 9,286

Group equity 10,493 10,415 11,069 11,801 12,619 14,309 16,105 16,910 17,755

t/o Shareholders' equity 10,447 10,361 11,020 11,742 12,560 14,250 16,045 16,851 17,696

Interest-bearing liabilities 5,539 4,454 3,698 5,637 4,561 3,361 3,361 3,529 3,706

Other liabilties and prov isions 6,087 6,775 6,052 8,572 9,054 9,160 9,218 9,679 10,163

t/o Trade liabilities 1,101 1,288 1,364 1,539 1,689 1,723 1,741 1,828 1,919

Balance sheet total 22,120 21,643 20,819 26,010 26,235 26,831 28,684 30,118 31,624

Net w orking capital 2,919 2,360 2,132 2,356 2,485 2,534 2,561 2,689 2,824

Capital employ ed (incl. Goodw ill) 18,642 17,377 15,566 17,886 17,379 17,485 17,619 18,500 19,425

Ratios

Rev enue, y /y 10.6% 8.7% -0.7% 3.7% 9.7% 2.0% 1.1% 2.8% 4.4%

EBITDA margin (adj.) 26.5% 26.5% 29.3% 29.5% 27.9% 28.2% 28.4% 28.1% 27.7%

EBIT margin (adj.) 22.3% 22.3% 23.1% 24.8% 24.3% 24.6% 24.7% 24.4% 24.2%

EPS (adj.), y /y 0.9% 12.1% 15.2% 4.8% 4.6% 3.1% 7.1% 3.0% 3.1%

Net w orking capital intensity (as a % of sales) 28.4% 21.1% 19.2% 20.5% 19.7% 19.7% 19.7% 20.1% 20.2%

DSOs (trade receiv ables as day s of rev s) 83 69 66 71 71 71 71 72 73

Inv entories as a % of rev enue 16.5% 13.7% 13.3% 14.4% 13.6% 13.6% 13.6% 13.9% 14.0%

Net debt (cash) / EBITDA (adj.) 1.3 0.6 0.1 0.2 (0.3) (0.7) (1.2) (1.3) (1.4)

EBITDA (adj.) / Capex 6.1 6.3 6.3 5.4 5.5 5.5 5.4 5.2 5.2

Free CF y ield (FCF / market cap) 7.1% 21.1% 7.3% 14.4% 6.7% 6.2% 6.3% 6.7% 7.6%

Oper. FCF y ield ([FCF - net int. tax ed] / EV) 5.4% 16.9% 7.4% 13.6% 7.1% 6.8% 7.0% 6.8% 7.9%

European Healthcare, 11 September 2015

11 / 44

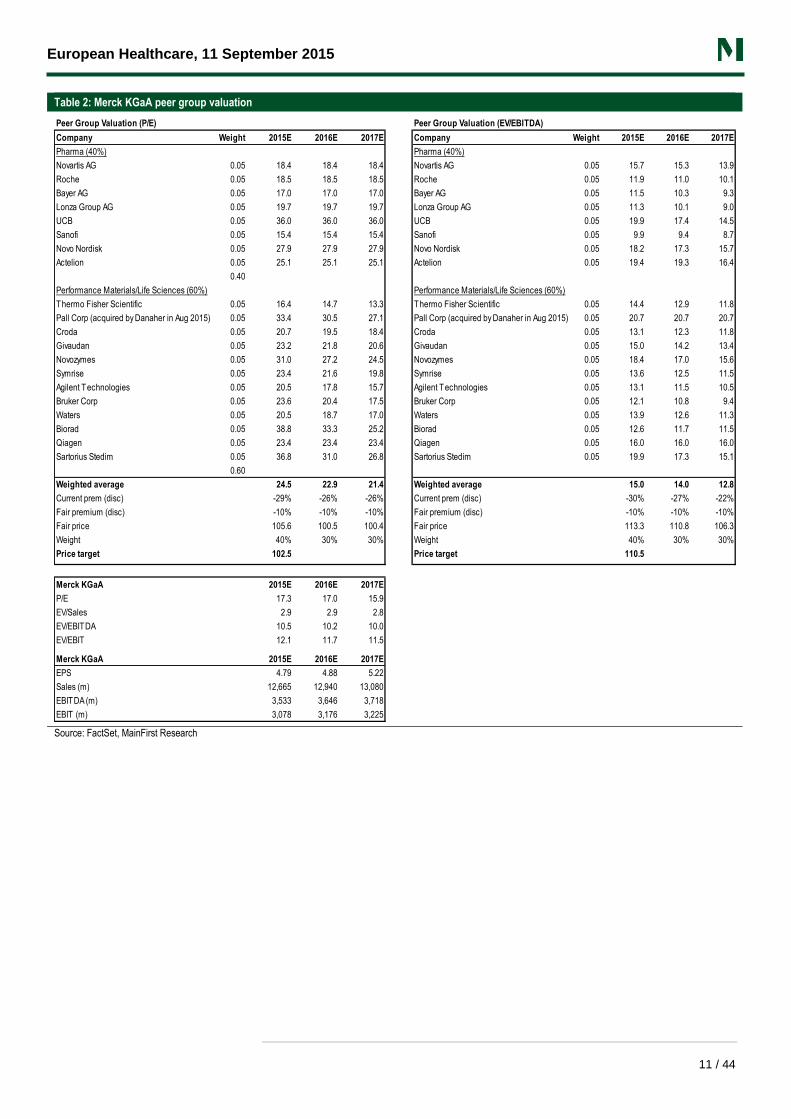

Table 2: Merck KGaA peer group valuation

Source: FactSet, MainFirst Research

Peer Group Valuation (P/E) Peer Group Valuation (EV/EBITDA)

Company Weight 2015E 2016E 2017E Company Weight 2015E 2016E 2017E

Pharma (40%) Pharma (40%)

Novartis AG 0.05 18.4 18.4 18.4 Novartis AG 0.05 15.7 15.3 13.9

Roche 0.05 18.5 18.5 18.5 Roche 0.05 11.9 11.0 10.1

Bayer AG 0.05 17.0 17.0 17.0 Bayer AG 0.05 11.5 10.3 9.3

Lonza Group AG 0.05 19.7 19.7 19.7 Lonza Group AG 0.05 11.3 10.1 9.0

UCB 0.05 36.0 36.0 36.0 UCB 0.05 19.9 17.4 14.5

Sanofi 0.05 15.4 15.4 15.4 Sanofi 0.05 9.9 9.4 8.7

Novo Nordisk 0.05 27.9 27.9 27.9 Novo Nordisk 0.05 18.2 17.3 15.7

Actelion 0.05 25.1 25.1 25.1 Actelion 0.05 19.4 19.3 16.4

0.40

Performance Materials/Life Sciences (60%) Performance Materials/Life Sciences (60%)

Thermo Fisher Scientific 0.05 16.4 14.7 13.3 Thermo Fisher Scientific 0.05 14.4 12.9 11.8

Pall Corp (acquired by Danaher in Aug 2015) 0.05 33.4 30.5 27.1 Pall Corp (acquired by Danaher in Aug 2015) 0.05 20.7 20.7 20.7

Croda 0.05 20.7 19.5 18.4 Croda 0.05 13.1 12.3 11.8

Givaudan 0.05 23.2 21.8 20.6 Givaudan 0.05 15.0 14.2 13.4

Novozymes 0.05 31.0 27.2 24.5 Novozymes 0.05 18.4 17.0 15.6

Symrise 0.05 23.4 21.6 19.8 Symrise 0.05 13.6 12.5 11.5

Agilent Technologies 0.05 20.5 17.8 15.7 Agilent Technologies 0.05 13.1 11.5 10.5

Bruker Corp 0.05 23.6 20.4 17.5 Bruker Corp 0.05 12.1 10.8 9.4

Waters 0.05 20.5 18.7 17.0 Waters 0.05 13.9 12.6 11.3

Biorad 0.05 38.8 33.3 25.2 Biorad 0.05 12.6 11.7 11.5

Qiagen 0.05 23.4 23.4 23.4 Qiagen 0.05 16.0 16.0 16.0

Sartorius Stedim 0.05 36.8 31.0 26.8 Sartorius Stedim 0.05 19.9 17.3 15.1

0.60

Weighted average 24.5 22.9 21.4 Weighted average 15.0 14.0 12.8

Current prem (disc) -29% -26% -26% Current prem (disc) -30% -27% -22%

Fair premium (disc) -10% -10% -10% Fair premium (disc) -10% -10% -10%

Fair price 105.6 100.5 100.4 Fair price 113.3 110.8 106.3

Weight 40% 30% 30% Weight 40% 30% 30%

Price target 102.5 Price target 110.5

Merck KGaA 2015E 2016E 2017E

P/E 17.3 17.0 15.9

EV/Sales 2.9 2.9 2.8

EV/EBITDA 10.5 10.2 10.0

EV/EBIT 12.1 11.7 11.5

Merck KGaA 2015E 2016E 2017E

EPS 4.79 4.88 5.22

Sales (m) 12,665 12,940 13,080

EBITDA (m) 3,533 3,646 3,718

EBIT (m) 3,078 3,176 3,225

European Healthcare, 11 September 2015

12 / 44

Table 3: Merck KGaA Q2-15 results (EUR m)

Source: Company accounts, MainFirst Research

Table 4: Merck KGaA organic growth trends by division and by region

Source: Company accounts

Q2 2015

reported

Q2 2015

cons

FY 2014A

(restated)

FY 2015 guidance

(excluding SIAL)

FY 2015

MF est

change

yoy

consensus

(Vara)

Healthcare

Sales 1,803 1,761 6,620 organically stable 7,059 7% 6,967

adj. EBITDA 480 488 2,000 1.9bn to 2.0bn 1,916 -4% 1,940

Erbitux sales 233 231 904 908 0% 916

Rebif sales 461 454 1,840 1,781 -3% 1,781

Performance Materials

Sales 643 639 2,060 slight organic growth 2,545 24% 2,532

adj. EBITDA 295 284 895 1.06bn to 1.1bn 1,138 27% 1,106

Life Sciences

Sales 773 748 2,682 moderate organic growth 3,061 14% 2,946

adj. EBITDA 200 191 659 EUR 740m to 760m 779 18% 759

Merck group

Sales 3,220 3,147 11,363 EUR 12.3bn to 12.5bn 12,665 11% 12,409

adj. EBITDA 899 884 3,388 3.45bn to 3.55bn 3,513 4% 3,506

adj. EPS 1.30 1.19 4.60 4.60-4.80 4.78 4% 4.71

Sales by region,

organic growth yoy

Q1 2013 Q2 2013 Q3 2013 Q4 2013 % of

group

Q1 2014 Q2 2014 Q3 2014 Q4 2014 % of

group

Q1 2015 Q2 2015 % of

group

North America 5.6% 4.9% -1.3% -6.0% 19% 2.6% -3.3% 1.5% 6.8% 19% -3.5% -1.2% 20%

Europe 1.0% 0.2% 1.1% 4.0% 37% 1.7% 0.5% 1.4% -2.7% 34% -3.0% -0.7% 31%

Emerging Markets 11.5% 4.9% 11.5% 10.0% 36% 5.6% 11.1% 9.1% 10.8% 39%

RoW -2.4% 6.4% 5.7% 6.0% 8% 7.8% 0.5% 6.7% 5.2% 8%

Asia-Pacific 5.2% 3.1% 33%

Latin America 19.9% 12.5% 12%

Middle East & Africa -5.5% 8.2% 4%

Group 5.0% 3.3% 4.7% 3.9% 100% 3.7% 3.4% 4.6% 4.4% 100% 1.3% 2.2% 100%

Sales by segment

Merck Serono 4.9% 2.1% 5.2% 4.0% 56% 4.2% 3.0% 4.5% 2.8% 50% 50%

Consumer Health 9.3% -1.0% 14.6% 0.0% 4% 5.7% 8.5% 1.4% 6.5% 7% 7%

New Healthcare 0.3% 1.5%

Performance Materials 9.9% 5.4% -1.8% -1.0% 15% 1.1% 1.8% 7.0% 6.9% 19% 1.6% -0.4% 19%

Life Science 3.6% 5.6% 5.9% 7.0% 25% 3.7% 4.0% 4.5% 5.9% 24% 3.4% 6.2% 24%

Group 5.0% 3.3% 4.7% 3.9% 100% 3.7% 3.4% 4.6% 4.4% 100% 1.3% 2.2% 100%

EBITDA by segment

Merck Serono 14.8% 9.2% 7.7% -1.0% 57% 0.1% -5.0% -3.8% 3.6% 52%

Consumer Health 52.6% 3.9% 25.4% -25.0% 2% 5.0% 17.0% -15.5% -3.1% 4%

New Healthcare -3.8% -2.8% 50%

Performance Materials 27.0% 8.4% -0.2% -12.0% 23% -10.1% 8.0% 23.5% 43.6% 26% 48.4% 30.5% 30%

Life Science -2.5% 1.9% 3.4% 17.0% 18% 4.8% 6.0% 2.4% -3.0% 18% 8.5% 20.6% 20%

Group 18.8% 10.7% 10.1% 0.7% 100% 0.7% 2.0% 3.1% 10.5% 100% 5.7% 6.3% 100%

European Healthcare, 11 September 2015

13 / 44

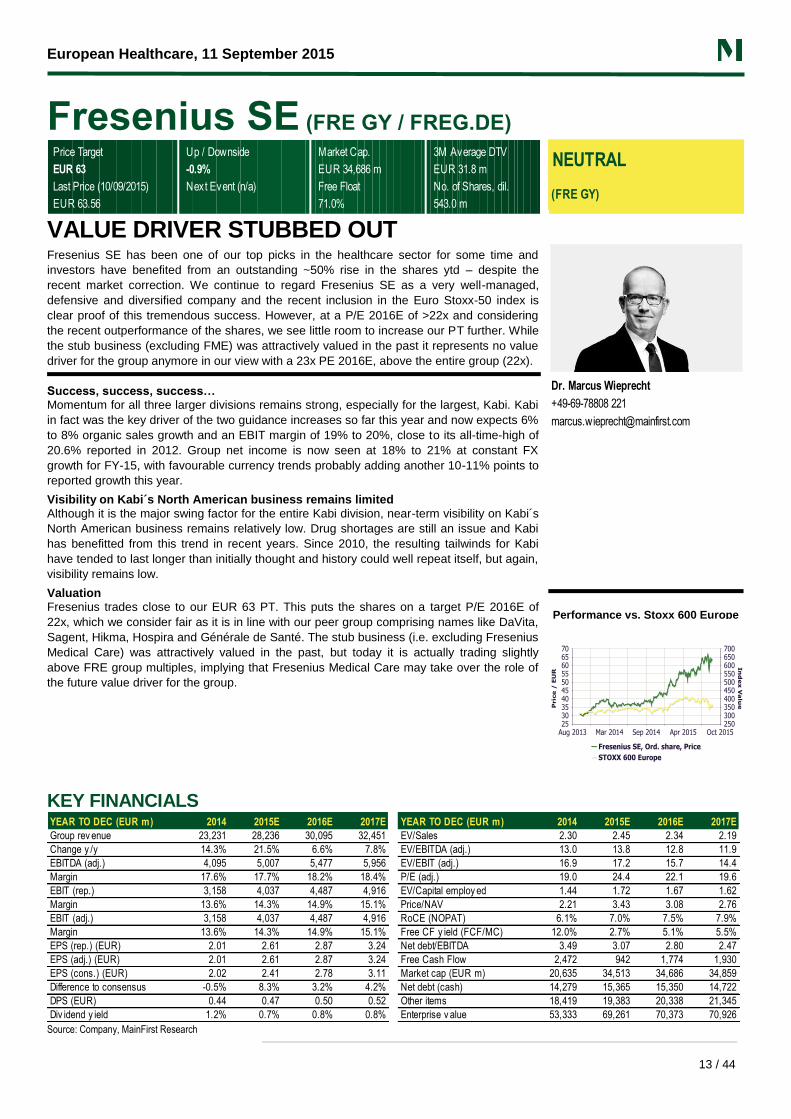

Fresenius SE (FRE GY / FREG.DE)

Price Target Up / Downside Market Cap. 3M Average DTV

EUR 63 -0.9% EUR 34,686 m EUR 31.8 m

Last Price (10/09/2015) Next Event (n/a) Free Float No. of Shares, dil.

EUR 63.56 71.0% 543.0 m

NEUTRAL

(FRE GY)

VALUE DRIVER STUBBED OUT Fresenius SE has been one of our top picks in the healthcare sector for some time and

investors have benefited from an outstanding ~50% rise in the shares ytd – despite the

recent market correction. We continue to regard Fresenius SE as a very well-managed,

defensive and diversified company and the recent inclusion in the Euro Stoxx-50 index is

clear proof of this tremendous success. However, at a P/E 2016E of >22x and considering

the recent outperformance of the shares, we see little room to increase our PT further. While

the stub business (excluding FME) was attractively valued in the past it represents no value

driver for the group anymore in our view with a 23x PE 2016E, above the entire group (22x).

Success, success, success… Momentum for all three larger divisions remains strong, especially for the largest, Kabi. Kabi

in fact was the key driver of the two guidance increases so far this year and now expects 6%

to 8% organic sales growth and an EBIT margin of 19% to 20%, close to its all-time-high of

20.6% reported in 2012. Group net income is now seen at 18% to 21% at constant FX

growth for FY-15, with favourable currency trends probably adding another 10-11% points to

reported growth this year.

Visibility on Kabi´s North American business remains limited

Although it is the major swing factor for the entire Kabi division, near-term visibility on Kabi´s

North American business remains relatively low. Drug shortages are still an issue and Kabi

has benefitted from this trend in recent years. Since 2010, the resulting tailwinds for Kabi

have tended to last longer than initially thought and history could well repeat itself, but again,

visibility remains low.

Valuation Fresenius trades close to our EUR 63 PT. This puts the shares on a target P/E 2016E of

22x, which we consider fair as it is in line with our peer group comprising names like DaVita,

Sagent, Hikma, Hospira and Générale de Santé. The stub business (i.e. excluding Fresenius

Medical Care) was attractively valued in the past, but today it is actually trading slightly

above FRE group multiples, implying that Fresenius Medical Care may take over the role of

the future value driver for the group.

Dr. Marcus Wieprecht

+49-69-78808 221

Performance vs. Stoxx 600 Europe

KEY FINANCIALS

Source: Company, MainFirst Research

YEAR TO DEC (EUR m) 2014 2015E 2016E 2017E YEAR TO DEC (EUR m) 2014 2015E 2016E 2017E

Group rev enue 23,231 28,236 30,095 32,451 EV/Sales 2.30 2.45 2.34 2.19

Change y /y 14.3% 21.5% 6.6% 7.8% EV/EBITDA (adj.) 13.0 13.8 12.8 11.9

EBITDA (adj.) 4,095 5,007 5,477 5,956 EV/EBIT (adj.) 16.9 17.2 15.7 14.4

Margin 17.6% 17.7% 18.2% 18.4% P/E (adj.) 19.0 24.4 22.1 19.6

EBIT (rep.) 3,158 4,037 4,487 4,916 EV/Capital employ ed 1.44 1.72 1.67 1.62

Margin 13.6% 14.3% 14.9% 15.1% Price/NAV 2.21 3.43 3.08 2.76

EBIT (adj.) 3,158 4,037 4,487 4,916 RoCE (NOPAT) 6.1% 7.0% 7.5% 7.9%

Margin 13.6% 14.3% 14.9% 15.1% Free CF y ield (FCF/MC) 12.0% 2.7% 5.1% 5.5%

EPS (rep.) (EUR) 2.01 2.61 2.87 3.24 Net debt/EBITDA 3.49 3.07 2.80 2.47

EPS (adj.) (EUR) 2.01 2.61 2.87 3.24 Free Cash Flow 2,472 942 1,774 1,930

EPS (cons.) (EUR) 2.02 2.41 2.78 3.11 Market cap (EUR m) 20,635 34,513 34,686 34,859

Difference to consensus -0.5% 8.3% 3.2% 4.2% Net debt (cash) 14,279 15,365 15,350 14,722

DPS (EUR) 0.44 0.47 0.50 0.52 Other items 18,419 19,383 20,338 21,345

Div idend y ield 1.2% 0.7% 0.8% 0.8% Enterprise v alue 53,333 69,261 70,373 70,926

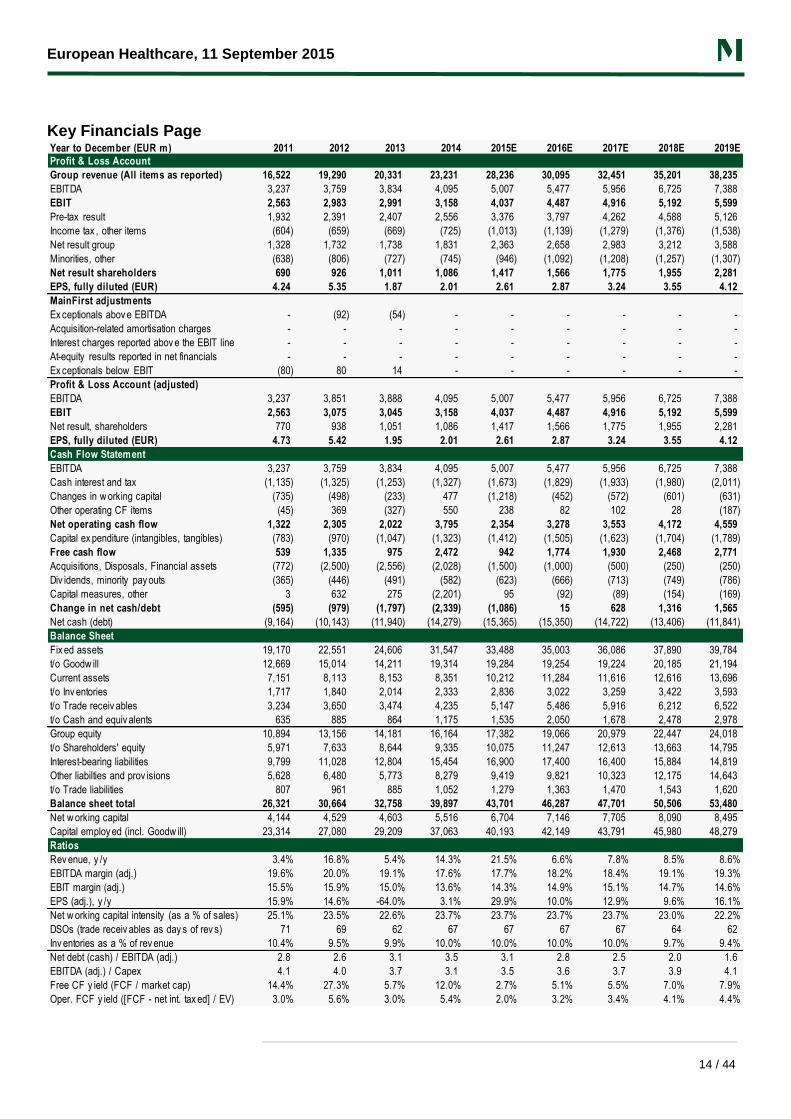

European Healthcare, 11 September 2015

14 / 44

Key Financials Page

Year to December (EUR m) 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Profit & Loss Account

Group revenue (All items as reported) 16,522 19,290 20,331 23,231 28,236 30,095 32,451 35,201 38,235

EBITDA 3,237 3,759 3,834 4,095 5,007 5,477 5,956 6,725 7,388

EBIT 2,563 2,983 2,991 3,158 4,037 4,487 4,916 5,192 5,599

Pre-tax result 1,932 2,391 2,407 2,556 3,376 3,797 4,262 4,588 5,126

Income tax , other items (604) (659) (669) (725) (1,013) (1,139) (1,279) (1,376) (1,538)

Net result group 1,328 1,732 1,738 1,831 2,363 2,658 2,983 3,212 3,588

Minorities, other (638) (806) (727) (745) (946) (1,092) (1,208) (1,257) (1,307)

Net result shareholders 690 926 1,011 1,086 1,417 1,566 1,775 1,955 2,281

EPS, fully diluted (EUR) 4.24 5.35 1.87 2.01 2.61 2.87 3.24 3.55 4.12

MainFirst adjustments

Ex ceptionals abov e EBITDA - (92) (54) - - - - - -

Acquisition-related amortisation charges - - - - - - - - -

Interest charges reported abov e the EBIT line - - - - - - - - -

At-equity results reported in net financials - - - - - - - - -

Ex ceptionals below EBIT (80) 80 14 - - - - - -

Profit & Loss Account (adjusted)

EBITDA 3,237 3,851 3,888 4,095 5,007 5,477 5,956 6,725 7,388

EBIT 2,563 3,075 3,045 3,158 4,037 4,487 4,916 5,192 5,599

Net result, shareholders 770 938 1,051 1,086 1,417 1,566 1,775 1,955 2,281

EPS, fully diluted (EUR) 4.73 5.42 1.95 2.01 2.61 2.87 3.24 3.55 4.12

Cash Flow Statement

EBITDA 3,237 3,759 3,834 4,095 5,007 5,477 5,956 6,725 7,388

Cash interest and tax (1,135) (1,325) (1,253) (1,327) (1,673) (1,829) (1,933) (1,980) (2,011)

Changes in w orking capital (735) (498) (233) 477 (1,218) (452) (572) (601) (631)

Other operating CF items (45) 369 (327) 550 238 82 102 28 (187)

Net operating cash flow 1,322 2,305 2,022 3,795 2,354 3,278 3,553 4,172 4,559

Capital ex penditure (intangibles, tangibles) (783) (970) (1,047) (1,323) (1,412) (1,505) (1,623) (1,704) (1,789)

Free cash flow 539 1,335 975 2,472 942 1,774 1,930 2,468 2,771

Acquisitions, Disposals, Financial assets (772) (2,500) (2,556) (2,028) (1,500) (1,000) (500) (250) (250)

Div idends, minority pay outs (365) (446) (491) (582) (623) (666) (713) (749) (786)

Capital measures, other 3 632 275 (2,201) 95 (92) (89) (154) (169)

Change in net cash/debt (595) (979) (1,797) (2,339) (1,086) 15 628 1,316 1,565

Net cash (debt) (9,164) (10,143) (11,940) (14,279) (15,365) (15,350) (14,722) (13,406) (11,841)

Balance Sheet

Fix ed assets 19,170 22,551 24,606 31,547 33,488 35,003 36,086 37,890 39,784

t/o Goodw ill 12,669 15,014 14,211 19,314 19,284 19,254 19,224 20,185 21,194

Current assets 7,151 8,113 8,153 8,351 10,212 11,284 11,616 12,616 13,696

t/o Inv entories 1,717 1,840 2,014 2,333 2,836 3,022 3,259 3,422 3,593

t/o Trade receiv ables 3,234 3,650 3,474 4,235 5,147 5,486 5,916 6,212 6,522

t/o Cash and equiv alents 635 885 864 1,175 1,535 2,050 1,678 2,478 2,978

Group equity 10,894 13,156 14,181 16,164 17,382 19,066 20,979 22,447 24,018

t/o Shareholders' equity 5,971 7,633 8,644 9,335 10,075 11,247 12,613 13,663 14,795

Interest-bearing liabilities 9,799 11,028 12,804 15,454 16,900 17,400 16,400 15,884 14,819

Other liabilties and prov isions 5,628 6,480 5,773 8,279 9,419 9,821 10,323 12,175 14,643

t/o Trade liabilities 807 961 885 1,052 1,279 1,363 1,470 1,543 1,620

Balance sheet total 26,321 30,664 32,758 39,897 43,701 46,287 47,701 50,506 53,480

Net w orking capital 4,144 4,529 4,603 5,516 6,704 7,146 7,705 8,090 8,495

Capital employ ed (incl. Goodw ill) 23,314 27,080 29,209 37,063 40,193 42,149 43,791 45,980 48,279

Ratios

Rev enue, y /y 3.4% 16.8% 5.4% 14.3% 21.5% 6.6% 7.8% 8.5% 8.6%

EBITDA margin (adj.) 19.6% 20.0% 19.1% 17.6% 17.7% 18.2% 18.4% 19.1% 19.3%

EBIT margin (adj.) 15.5% 15.9% 15.0% 13.6% 14.3% 14.9% 15.1% 14.7% 14.6%

EPS (adj.), y /y 15.9% 14.6% -64.0% 3.1% 29.9% 10.0% 12.9% 9.6% 16.1%

Net w orking capital intensity (as a % of sales) 25.1% 23.5% 22.6% 23.7% 23.7% 23.7% 23.7% 23.0% 22.2%

DSOs (trade receiv ables as day s of rev s) 71 69 62 67 67 67 67 64 62

Inv entories as a % of rev enue 10.4% 9.5% 9.9% 10.0% 10.0% 10.0% 10.0% 9.7% 9.4%

Net debt (cash) / EBITDA (adj.) 2.8 2.6 3.1 3.5 3.1 2.8 2.5 2.0 1.6

EBITDA (adj.) / Capex 4.1 4.0 3.7 3.1 3.5 3.6 3.7 3.9 4.1

Free CF y ield (FCF / market cap) 14.4% 27.3% 5.7% 12.0% 2.7% 5.1% 5.5% 7.0% 7.9%

Oper. FCF y ield ([FCF - net int. tax ed] / EV) 3.0% 5.6% 3.0% 5.4% 2.0% 3.2% 3.4% 4.1% 4.4%

European Healthcare, 11 September 2015

15 / 44

Fresenius Medical Care (FME GY / FMEG.DE)

Price Target Up / Downside Market Cap. 3M Average DTV

EUR 75 +6.5% EUR 21,733 m EUR 70.4 m

Last Price (10/09/2015) Next Event (29/10/2015) Free Float No. of Shares, dil.

EUR 70.41 Q3/9M Results 69.0% 308.1 m

NEUTRAL

(FME GY)

PREFERENCE SHIFTING FROM FRE TO FME We slightly increase our PT, by EUR 4 per share or 5%, to EUR 75 (implying a target P/E

2016E of 20x) but keep our Neutral recommendation for Fresenius Medical Care. FME

shares have lost c.15% from their peak, far more than its parent FRE, which has dipped just

c.4% from its high. Ytd, FME shares are still up by around 13% (versus c.50% for FRE

shares), which is slightly better than the broader Dax-30 performance of around +5% ytd. As

discussions on reimbursement cuts in the US seem to be off the agenda for the time being,

FME can focus on its global efficiency program, integrating recent acquisitions in the US and

the patient switch to Mircera.

Mircera deal is clearly positive for 2016 earnings The recent supply agreement for Roche’s Mircera in the US through FME’s JV with Galenica

is clearly positive for FME from 2016 onwards. Mircera is a long-acting EPO and the first

cheaper EPO alternative for dialysis providers in the US, ahead of first EPO biosimilars,

which are expected to come to the US market from 2016 onwards. We estimate that FME

will be able to save an extra ~USD 100m in costs (Mircera costs ~25% less, 50% of patients

switched, on a total estimated USD 750m EPO bill for FME´s US clinics) on top of the

targeted USD 300m cost savings from its Global Efficiency Program launched early last

year. However, these estimated Mircera cost savings are already included in FME’s FY-16

guidance for 15% to 20% net income growth following more muted growth in FY-15. Roche´s

production capacity for Mircera is somewhat limited, implying that Mircera will primarily be

used only in FME’s own dialysis clinics (37% market share in the US).

Japanese dialysis service market opening up: big numbers, difficult to consolidate While the story has been around for many years already, there seems to be some progress

now in Japan as foreign companies are now allowed to run dialysis clinics. The Japanese

market offers a huge opportunity for global dialysis players given the large numbers of

patients (c.326,000, 13% of global dialysis patients) with very high reimbursement levels,

creating a USD 20bn market opportunity. The downside, however, is that around 85% of the

market is highly fragmented (i.e. independent clinics), making it very difficult for any global

dialysis player to consolidate its position.

New CMS/government reimbursement discussions unlikely in the next few years While reimbursement discussions are a regular occurrence in the US every few years

(especially when certain costs like those for renal drugs are plunging), FME does not see

any new discussions coming up until the end of this decade. However, once cheaper renal

drugs like Mircera or EPO biosimilars have been on the market for a few years, a new

discussion on dialysis reimbursement for Medicare patients is foreseeable.

Dr. Marcus Wieprecht

+49-69-78808 221

Performance vs. Stoxx 600 Europe

KEY FINANCIALS

Source: Company, MainFirst Research

YEAR TO DEC (USD m) 2014 2015E 2016E 2017E YEAR TO DEC (USD m) 2014 2015E 2016E 2017E

Group rev enue 15,832 17,218 18,606 20,367 EV/Sales 1.76 2.01 1.88 1.71

Change y /y 8.4% 8.8% 8.1% 9.5% EV/EBITDA (adj.) 9.4 11.0 9.8 8.9

EBITDA (adj.) 2,968 3,163 3,561 3,928 EV/EBIT (adj.) 12.3 14.4 12.6 11.4

Margin 18.7% 18.4% 19.1% 19.3% P/E (adj.) 16.9 22.6 19.0 16.9

EBIT (rep.) 2,255 2,391 2,746 3,057 EV/Capital employ ed 1.24 1.50 1.47 1.44

Margin 14.2% 13.9% 14.8% 15.0% Price/NAV 1.79 2.37 2.27 2.16

EBIT (adj.) 2,269 2,406 2,761 3,073 RoCE (NOPAT) 6.9% 7.0% 7.8% 8.5%

Margin 14.3% 14.0% 14.8% 15.1% Free CF y ield (FCF/MC) 5.2% 4.0% 4.8% 4.6%

EPS (rep.) (USD) 3.46 3.52 4.18 4.69 Net debt/EBITDA 2.89 2.80 2.47 2.17

EPS (adj.) (USD) 3.46 3.52 4.18 4.69 Free Cash Flow 929 974 1,178 1,141

EPS (cons.) (USD) 3.48 3.74 4.27 4.70 Market cap (USD m) 17,978 24,393 24,515 24,637

Difference to consensus -0.6% -5.9% -2.1% -0.2% Net debt (cash) 8,563 8,846 8,807 8,511

DPS (USD) 0.78 0.80 0.85 0.90 Other items 1,279 1,444 1,603 1,772

Div idend y ield 1.3% 1.0% 1.1% 1.1% Enterprise v alue 27,819 34,683 34,924 34,921

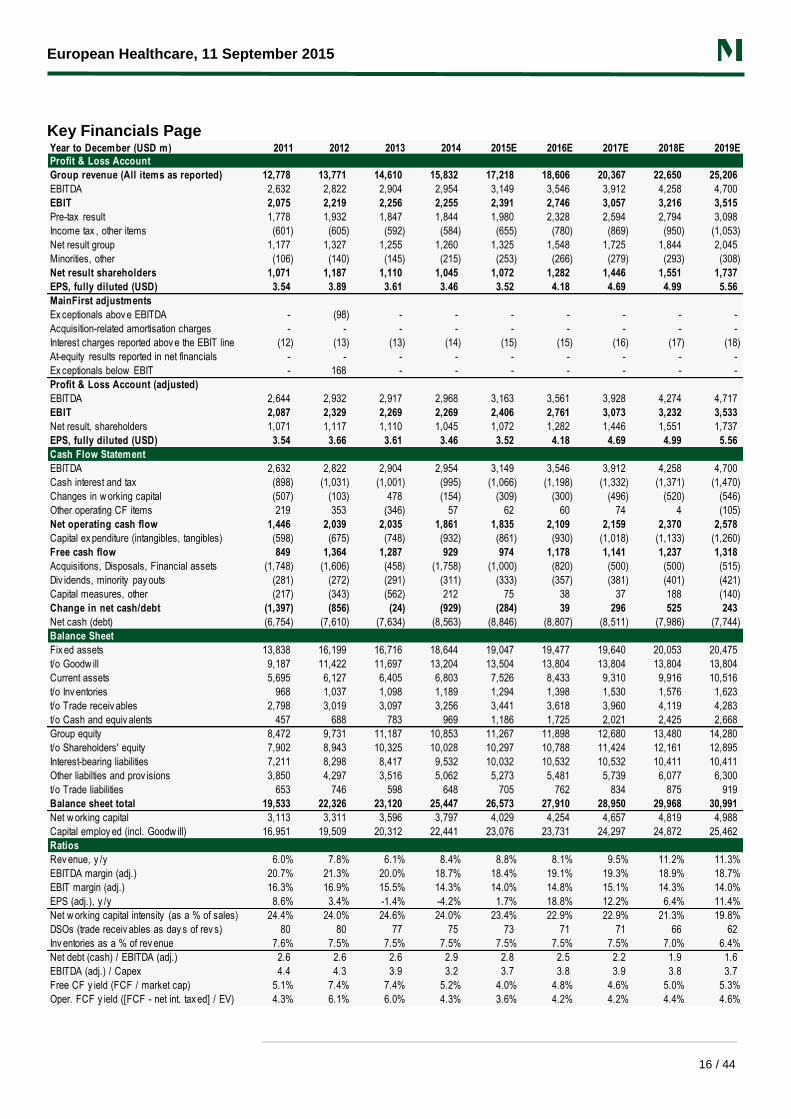

European Healthcare, 11 September 2015

16 / 44

Key Financials Page

Year to December (USD m) 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Profit & Loss Account

Group revenue (All items as reported) 12,778 13,771 14,610 15,832 17,218 18,606 20,367 22,650 25,206

EBITDA 2,632 2,822 2,904 2,954 3,149 3,546 3,912 4,258 4,700

EBIT 2,075 2,219 2,256 2,255 2,391 2,746 3,057 3,216 3,515

Pre-tax result 1,778 1,932 1,847 1,844 1,980 2,328 2,594 2,794 3,098

Income tax , other items (601) (605) (592) (584) (655) (780) (869) (950) (1,053)

Net result group 1,177 1,327 1,255 1,260 1,325 1,548 1,725 1,844 2,045

Minorities, other (106) (140) (145) (215) (253) (266) (279) (293) (308)

Net result shareholders 1,071 1,187 1,110 1,045 1,072 1,282 1,446 1,551 1,737

EPS, fully diluted (USD) 3.54 3.89 3.61 3.46 3.52 4.18 4.69 4.99 5.56

MainFirst adjustments

Ex ceptionals abov e EBITDA - (98) - - - - - - -

Acquisition-related amortisation charges - - - - - - - - -

Interest charges reported abov e the EBIT line (12) (13) (13) (14) (15) (15) (16) (17) (18)

At-equity results reported in net financials - - - - - - - - -

Ex ceptionals below EBIT - 168 - - - - - - -

Profit & Loss Account (adjusted)

EBITDA 2,644 2,932 2,917 2,968 3,163 3,561 3,928 4,274 4,717

EBIT 2,087 2,329 2,269 2,269 2,406 2,761 3,073 3,232 3,533

Net result, shareholders 1,071 1,117 1,110 1,045 1,072 1,282 1,446 1,551 1,737

EPS, fully diluted (USD) 3.54 3.66 3.61 3.46 3.52 4.18 4.69 4.99 5.56

Cash Flow Statement

EBITDA 2,632 2,822 2,904 2,954 3,149 3,546 3,912 4,258 4,700

Cash interest and tax (898) (1,031) (1,001) (995) (1,066) (1,198) (1,332) (1,371) (1,470)

Changes in w orking capital (507) (103) 478 (154) (309) (300) (496) (520) (546)

Other operating CF items 219 353 (346) 57 62 60 74 4 (105)

Net operating cash flow 1,446 2,039 2,035 1,861 1,835 2,109 2,159 2,370 2,578

Capital ex penditure (intangibles, tangibles) (598) (675) (748) (932) (861) (930) (1,018) (1,133) (1,260)

Free cash flow 849 1,364 1,287 929 974 1,178 1,141 1,237 1,318

Acquisitions, Disposals, Financial assets (1,748) (1,606) (458) (1,758) (1,000) (820) (500) (500) (515)

Div idends, minority pay outs (281) (272) (291) (311) (333) (357) (381) (401) (421)

Capital measures, other (217) (343) (562) 212 75 38 37 188 (140)

Change in net cash/debt (1,397) (856) (24) (929) (284) 39 296 525 243

Net cash (debt) (6,754) (7,610) (7,634) (8,563) (8,846) (8,807) (8,511) (7,986) (7,744)

Balance Sheet

Fix ed assets 13,838 16,199 16,716 18,644 19,047 19,477 19,640 20,053 20,475

t/o Goodw ill 9,187 11,422 11,697 13,204 13,504 13,804 13,804 13,804 13,804

Current assets 5,695 6,127 6,405 6,803 7,526 8,433 9,310 9,916 10,516

t/o Inv entories 968 1,037 1,098 1,189 1,294 1,398 1,530 1,576 1,623

t/o Trade receiv ables 2,798 3,019 3,097 3,256 3,441 3,618 3,960 4,119 4,283

t/o Cash and equiv alents 457 688 783 969 1,186 1,725 2,021 2,425 2,668

Group equity 8,472 9,731 11,187 10,853 11,267 11,898 12,680 13,480 14,280

t/o Shareholders' equity 7,902 8,943 10,325 10,028 10,297 10,788 11,424 12,161 12,895

Interest-bearing liabilities 7,211 8,298 8,417 9,532 10,032 10,532 10,532 10,411 10,411

Other liabilties and prov isions 3,850 4,297 3,516 5,062 5,273 5,481 5,739 6,077 6,300

t/o Trade liabilities 653 746 598 648 705 762 834 875 919

Balance sheet total 19,533 22,326 23,120 25,447 26,573 27,910 28,950 29,968 30,991

Net w orking capital 3,113 3,311 3,596 3,797 4,029 4,254 4,657 4,819 4,988

Capital employ ed (incl. Goodw ill) 16,951 19,509 20,312 22,441 23,076 23,731 24,297 24,872 25,462

Ratios

Rev enue, y /y 6.0% 7.8% 6.1% 8.4% 8.8% 8.1% 9.5% 11.2% 11.3%

EBITDA margin (adj.) 20.7% 21.3% 20.0% 18.7% 18.4% 19.1% 19.3% 18.9% 18.7%

EBIT margin (adj.) 16.3% 16.9% 15.5% 14.3% 14.0% 14.8% 15.1% 14.3% 14.0%

EPS (adj.), y /y 8.6% 3.4% -1.4% -4.2% 1.7% 18.8% 12.2% 6.4% 11.4%

Net w orking capital intensity (as a % of sales) 24.4% 24.0% 24.6% 24.0% 23.4% 22.9% 22.9% 21.3% 19.8%

DSOs (trade receiv ables as day s of rev s) 80 80 77 75 73 71 71 66 62

Inv entories as a % of rev enue 7.6% 7.5% 7.5% 7.5% 7.5% 7.5% 7.5% 7.0% 6.4%

Net debt (cash) / EBITDA (adj.) 2.6 2.6 2.6 2.9 2.8 2.5 2.2 1.9 1.6

EBITDA (adj.) / Capex 4.4 4.3 3.9 3.2 3.7 3.8 3.9 3.8 3.7

Free CF y ield (FCF / market cap) 5.1% 7.4% 7.4% 5.2% 4.0% 4.8% 4.6% 5.0% 5.3%

Oper. FCF y ield ([FCF - net int. tax ed] / EV) 4.3% 6.1% 6.0% 4.3% 3.6% 4.2% 4.2% 4.4% 4.6%

European Healthcare, 11 September 2015

17 / 44

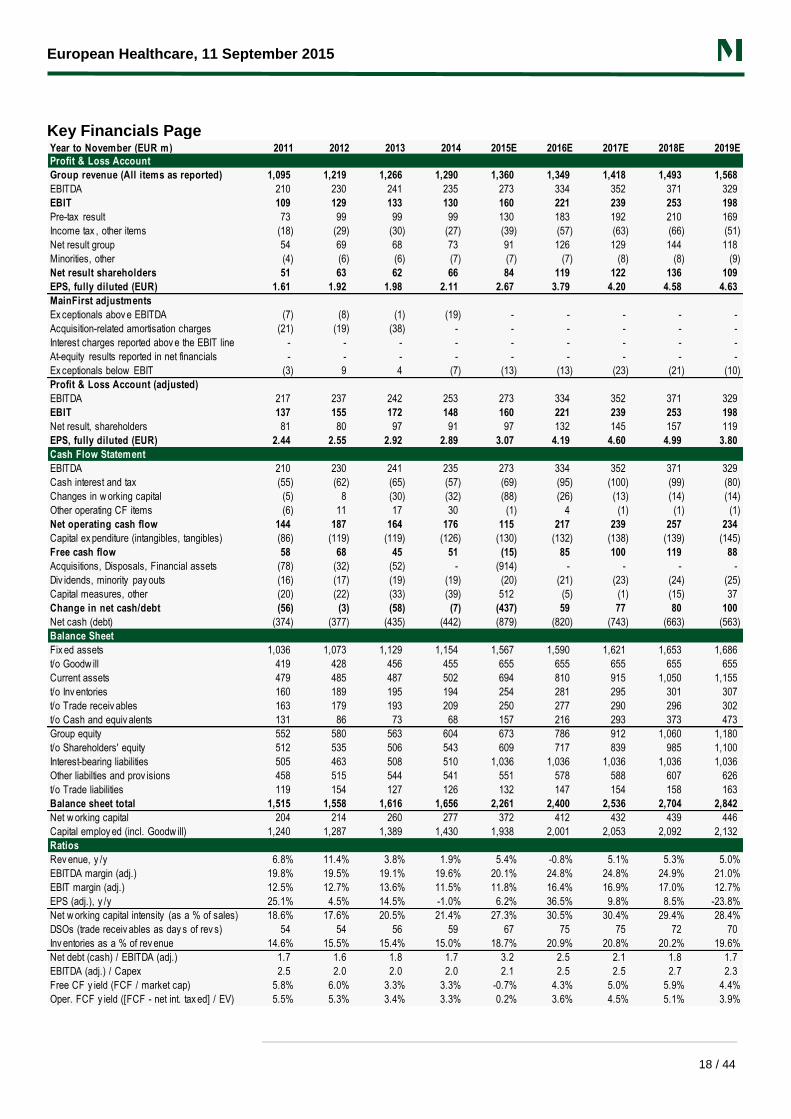

Gerresheimer AG (GXI GY / GXIG.DE)

Price Target Up / Downside Market Cap. 3M Average DTV

EUR 76 +19.3% EUR 2,000 m EUR 6.4 m

Last Price (10/09/2015) Next Event (n/a) Free Float No. of Shares, dil.

EUR 63.71 100.0% 31.4 m

OUTPERFORM

(GXI GY)

SHARES ~20% UNDERVALUED POST THE CENTOR DEAL Gerresheimer shares sailed smoothly through the stormy markets last month, having lost

~6% since the peak of EUR 68 reached shortly after the Centor acquisition at the end of

July. We believe this deal is not yet fully reflected in Gerresheimer´s valuation as Centor fits

strategically as well as financially for shareholders, adding a high-margin US-based plastics

business and thus improving group margins substantially. Having sold a more capex-

intensive glass business earlier this year (Tubing Glass to Corning) and replacing those

assets with far less capex-intensive ones (Centor), the group’s cash flows and return ratios

should improve. We reiterate our OPF recommendation and EUR 76 PT.

What we like: Centor is a strong player in a high-margin niche market According to Gerresheimer’s management, the attractions of the Centor business are: 1) it is

a market leader with a >50% share of a niche pharmacy supply market with historically very

stable revenue growth and margin trends; 2) 85% of Centor’s group sales are generated by

the two key flagship products “1-Clic” and “Screw.Loc”, which are widely known by patients

in the US; 3) 54 of the top 60 retailers are exclusively supplied by Centor in the US; 4)

Centor is expected to grow at least in line with the US prescription retail market, which is

forecast to grow by more than 2% until 2019 (IMS estimates); 5) Centor’s business metrics

are similar to the GXI plastics business, with contracts lasting for 2-3 years, including some

price escalation clauses so that rising raw material costs can be passed on to customers; 6)

the Centor products account for less than 0.1% of total pharmacy revenues, i.e. a small

portion; and 7) EBITDA margins are currently around 44%, with a very high cash conversion

rate (41% for GXI standalone, 48% for GXI plus Centor).

A low risk deal in our view In view of the above, the risks entailed by this deal seem fairly low. Neither is there any

integration risk as the acquired business is a pure add-on to GXI´s plastics business,

bringing a completely new sales channel (i.e. to pharmacies). According to CEO Röhrhoff,

Centor’s management has an outstanding track record in delivering on financial targets and

he sees no reason for this to change. Furthermore, the financing of the deal is locked in with

bridge financing of up to 18 months in place.

Valuation While we would not argue for a substantial multiple expansion for GXI shares following the

Centor deal, we consider a target 2016E P/E of 18x fair using our pro-forma EPS estimates

forming the basis for our EUR 76 price target. Our healthcare/packaging peer group trades

at a weighted 2016/2017 P/E of 20x and 18x, respectively, implying some incremental

upside in a blue-sky scenario.

Dr. Marcus Wieprecht

+49-69-78808 221

Performance vs. Stoxx 600 Europe

KEY FINANCIALS

Source: Company, MainFirst Research

YEAR TO NOV (EUR m) 2014 2015E 2016E 2017E YEAR TO NOV (EUR m) 2014 2015E 2016E 2017E

Group rev enue 1,290 1,360 1,349 1,418 EV/Sales 1.73 2.30 2.27 2.10

Change y /y 1.9% 5.4% -0.8% 5.1% EV/EBITDA (adj.) 8.8 11.4 9.2 8.5

EBITDA (adj.) 253 273 334 352 EV/EBIT (adj.) 15.1 19.5 13.9 12.5

Margin 19.6% 20.1% 24.8% 24.8% P/E (adj.) 17.1 20.8 15.2 13.9

EBIT (rep.) 130 160 221 239 EV/Capital employ ed 1.56 1.61 1.53 1.45

Margin 10.1% 11.8% 16.4% 16.9% Price/NAV 2.85 3.29 2.79 2.38

EBIT (adj.) 148 160 221 239 RoCE (NOPAT) 7.6% 5.8% 7.6% 8.0%

Margin 11.5% 11.8% 16.4% 16.9% Free CF y ield (FCF/MC) 3.3% -0.7% 4.3% 5.0%

EPS (rep.) (EUR) 2.11 2.67 3.79 4.20 Net debt/EBITDA 1.75 3.22 2.45 2.11

EPS (adj.) (EUR) 2.89 3.07 4.19 4.60 Free Cash Flow 51 (15) 85 100

EPS (cons.) (EUR) 2.83 3.05 3.42 3.87 Market cap (EUR m) 1,551 2,000 2,000 2,000

Difference to consensus 2.1% 0.7% 22.5% 18.9% Net debt (cash) 442 879 820 743

DPS (EUR) 0.75 0.79 0.83 0.87 Other items 245 243 242 241

Div idend y ield 1.5% 1.2% 1.3% 1.4% Enterprise v alue 2,238 3,123 3,063 2,984

European Healthcare, 11 September 2015

18 / 44

Key Financials Page

Year to November (EUR m) 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Profit & Loss Account

Group revenue (All items as reported) 1,095 1,219 1,266 1,290 1,360 1,349 1,418 1,493 1,568

EBITDA 210 230 241 235 273 334 352 371 329

EBIT 109 129 133 130 160 221 239 253 198

Pre-tax result 73 99 99 99 130 183 192 210 169

Income tax , other items (18) (29) (30) (27) (39) (57) (63) (66) (51)

Net result group 54 69 68 73 91 126 129 144 118

Minorities, other (4) (6) (6) (7) (7) (7) (8) (8) (9)

Net result shareholders 51 63 62 66 84 119 122 136 109

EPS, fully diluted (EUR) 1.61 1.92 1.98 2.11 2.67 3.79 4.20 4.58 4.63

MainFirst adjustments

Ex ceptionals abov e EBITDA (7) (8) (1) (19) - - - - -

Acquisition-related amortisation charges (21) (19) (38) - - - - - -

Interest charges reported abov e the EBIT line - - - - - - - - -

At-equity results reported in net financials - - - - - - - - -

Ex ceptionals below EBIT (3) 9 4 (7) (13) (13) (23) (21) (10)

Profit & Loss Account (adjusted)

EBITDA 217 237 242 253 273 334 352 371 329

EBIT 137 155 172 148 160 221 239 253 198

Net result, shareholders 81 80 97 91 97 132 145 157 119

EPS, fully diluted (EUR) 2.44 2.55 2.92 2.89 3.07 4.19 4.60 4.99 3.80

Cash Flow Statement

EBITDA 210 230 241 235 273 334 352 371 329

Cash interest and tax (55) (62) (65) (57) (69) (95) (100) (99) (80)

Changes in w orking capital (5) 8 (30) (32) (88) (26) (13) (14) (14)

Other operating CF items (6) 11 17 30 (1) 4 (1) (1) (1)

Net operating cash flow 144 187 164 176 115 217 239 257 234

Capital ex penditure (intangibles, tangibles) (86) (119) (119) (126) (130) (132) (138) (139) (145)

Free cash flow 58 68 45 51 (15) 85 100 119 88

Acquisitions, Disposals, Financial assets (78) (32) (52) - (914) - - - -

Div idends, minority pay outs (16) (17) (19) (19) (20) (21) (23) (24) (25)

Capital measures, other (20) (22) (33) (39) 512 (5) (1) (15) 37

Change in net cash/debt (56) (3) (58) (7) (437) 59 77 80 100

Net cash (debt) (374) (377) (435) (442) (879) (820) (743) (663) (563)

Balance Sheet

Fix ed assets 1,036 1,073 1,129 1,154 1,567 1,590 1,621 1,653 1,686

t/o Goodw ill 419 428 456 455 655 655 655 655 655

Current assets 479 485 487 502 694 810 915 1,050 1,155

t/o Inv entories 160 189 195 194 254 281 295 301 307

t/o Trade receiv ables 163 179 193 209 250 277 290 296 302

t/o Cash and equiv alents 131 86 73 68 157 216 293 373 473

Group equity 552 580 563 604 673 786 912 1,060 1,180

t/o Shareholders' equity 512 535 506 543 609 717 839 985 1,100

Interest-bearing liabilities 505 463 508 510 1,036 1,036 1,036 1,036 1,036

Other liabilties and prov isions 458 515 544 541 551 578 588 607 626

t/o Trade liabilities 119 154 127 126 132 147 154 158 163

Balance sheet total 1,515 1,558 1,616 1,656 2,261 2,400 2,536 2,704 2,842

Net w orking capital 204 214 260 277 372 412 432 439 446

Capital employ ed (incl. Goodw ill) 1,240 1,287 1,389 1,430 1,938 2,001 2,053 2,092 2,132

Ratios

Rev enue, y /y 6.8% 11.4% 3.8% 1.9% 5.4% -0.8% 5.1% 5.3% 5.0%

EBITDA margin (adj.) 19.8% 19.5% 19.1% 19.6% 20.1% 24.8% 24.8% 24.9% 21.0%

EBIT margin (adj.) 12.5% 12.7% 13.6% 11.5% 11.8% 16.4% 16.9% 17.0% 12.7%

EPS (adj.), y /y 25.1% 4.5% 14.5% -1.0% 6.2% 36.5% 9.8% 8.5% -23.8%

Net w orking capital intensity (as a % of sales) 18.6% 17.6% 20.5% 21.4% 27.3% 30.5% 30.4% 29.4% 28.4%

DSOs (trade receiv ables as day s of rev s) 54 54 56 59 67 75 75 72 70

Inv entories as a % of rev enue 14.6% 15.5% 15.4% 15.0% 18.7% 20.9% 20.8% 20.2% 19.6%

Net debt (cash) / EBITDA (adj.) 1.7 1.6 1.8 1.7 3.2 2.5 2.1 1.8 1.7

EBITDA (adj.) / Capex 2.5 2.0 2.0 2.0 2.1 2.5 2.5 2.7 2.3

Free CF y ield (FCF / market cap) 5.8% 6.0% 3.3% 3.3% -0.7% 4.3% 5.0% 5.9% 4.4%

Oper. FCF y ield ([FCF - net int. tax ed] / EV) 5.5% 5.3% 3.4% 3.3% 0.2% 3.6% 4.5% 5.1% 3.9%

European Healthcare, 11 September 2015

19 / 44

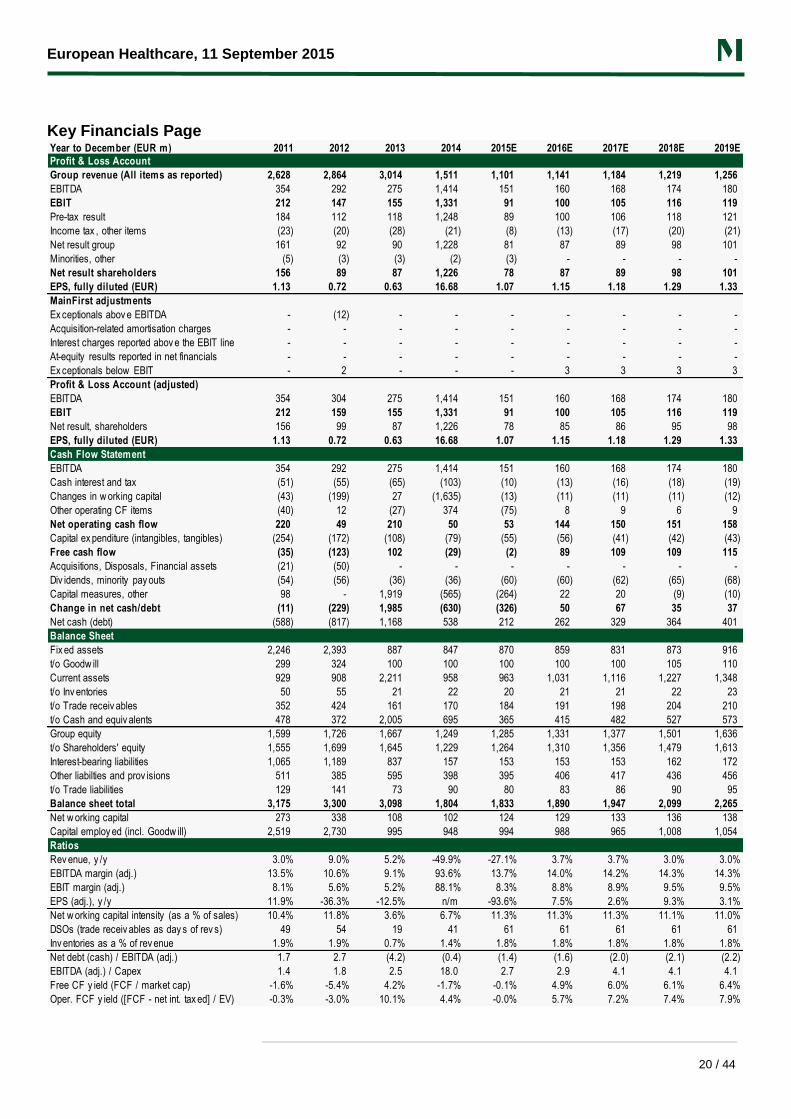

Rhön Klinikum (RHK GY / RHKG.DE)

Price Target Up / Downside Market Cap. 3M Average DTV

EUR 30 +22.3% EUR 1,802 m EUR 12.3 m

Last Price (10/09/2015) Next Event (n/a) Free Float No. of Shares, dil.

EUR 24.53 87.5% 73.5 m

OUTPERFORM

(RHK GY)

DECENT RETURNS, LIMITED DOWNSIDE

Although Rhön shares have slipped by ~8% from the peak reached at the end of May, they

are still up by ~3% ytd, so the overall volatility of the shares remains very low. We continue

to like the Rhön investment case for the following reasons: 1) strong shareholder return

potential (higher dividend payout ratio and further share buybacks); 2) a massively

underestimated underlying, fully-leveraged earnings potential implying >20% upside for the

shares mid-term with hardly any downside risk; and 3) a still valid M&A story with larger

shareholders likely to take control within the next five years, in our view. We retain our

Outperform rating and EUR 30 price target.

EUR 511m net cash position leaves multiple options Rhön currently has EUR 511m net cash on its balance sheet (as per June 2015), giving the

company multiple options for decent shareholder returns. Around EUR 180m will be used for

another c.10% share buyback starting Sept 11 and ending Oct 8 while c.EUR 200m will be

used to expand capacity in Bad Neustadt (we estimate a c.17% capacity expansion), Rhön’s

most profitable (>20% EBITDA margin) but oldest hospital. The remaining c.EUR 100m net

cash could be leveraged up to around EUR 500m (implying 2-3x net debt/EBITDA) for future

acquisitions in the German specialised hospital market.

Rhön unlikely to remain independent in 5 years in our view We continue to believe that Rhön will not remain independent mid-term, given that the

founder and current head of the supervisory board Eugen Münch will have to leave the

supervisory board at the age of 75 at the latest (he is now 70). This should pave the way for

other larger shareholders (like Asklepios/Dr. gr. Broermann, who owns 15.25% today and/or

B. Braun, who currently holds 18%) to gradually take over control, in our view. Even Sana

(non-listed German hospital chain) has expressed interest in some Rhön assets.

Valuation: Underlying P/E is very attractive ~13x Optically, Rhön shares may appear fully valued at a P/E 2016E of ~21x. However, we

believe that the underlying EPS potential for Rhön is at least 50% higher than our 2016E

EPS of EUR 1.15. More share buybacks already this year and a better leveraging of the

strong net cash position via earnings-accretive acquisitions as well as the planned capacity

expansion in Bad Neustadt should lead to a further EPS expansion, which we and

consensus have not yet built into our models. We calculate an underlying mid-term EPS

potential of around EUR 1.80, taking the underlying P/E of Rhön shares today to just ~13x.

Our price target of EUR 30 implies a target P/E of ~16.5x, which we still consider

conservative.

Dr. Marcus Wieprecht

+49-69-78808 221

Performance vs. Stoxx 600 Europe

KEY FINANCIALS

Source: Company, MainFirst Research

YEAR TO DEC (EUR m) 2014 2015E 2016E 2017E YEAR TO DEC (EUR m) 2014 2015E 2016E 2017E

Group rev enue 1,511 1,101 1,141 1,184 EV/Sales 0.79 1.46 1.37 1.26

Change y /y -49.9% -27.1% 3.7% 3.7% EV/EBITDA (adj.) 0.8 10.7 9.8 8.9

EBITDA (adj.) 1,414 151 160 168 EV/EBIT (adj.) 0.9 17.7 15.6 14.2

Margin 93.6% 13.7% 14.0% 14.2% P/E (adj.) 1.4 22.9 21.3 20.8

EBIT (rep.) 1,331 91 100 105 EV/Capital employ ed 1.26 1.62 1.58 1.55

Margin 88.1% 8.3% 8.8% 8.9% Price/NAV 1.39 1.43 1.38 1.33

EBIT (adj.) 1,331 91 100 105 RoCE (NOPAT) 138.0% 8.3% 8.8% 9.1%

Margin 88.1% 8.3% 8.8% 8.9% Free CF y ield (FCF/MC) -1.7% -0.1% 4.9% 6.0%

EPS (rep.) (EUR) 16.68 1.07 1.15 1.18 Net debt/EBITDA - - - -

EPS (adj.) (EUR) 16.68 1.07 1.15 1.18 Free Cash Flow (29) (2) 89 109

EPS (cons.) (EUR) 16.68 1.06 1.18 1.29 Market cap (EUR m) 1,712 1,802 1,802 1,802

Difference to consensus 0.0% 0.9% -2.5% -8.5% Net debt (cash) (538) (212) (262) (329)

DPS (EUR) 6.67 0.80 0.81 0.82 Other items 21 22 22 22

Div idend y ield 28.6% 3.3% 3.3% 3.4% Enterprise v alue 1,195 1,612 1,562 1,495

European Healthcare, 11 September 2015

20 / 44

Key Financials Page

Year to December (EUR m) 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Profit & Loss Account

Group revenue (All items as reported) 2,628 2,864 3,014 1,511 1,101 1,141 1,184 1,219 1,256

EBITDA 354 292 275 1,414 151 160 168 174 180

EBIT 212 147 155 1,331 91 100 105 116 119

Pre-tax result 184 112 118 1,248 89 100 106 118 121

Income tax , other items (23) (20) (28) (21) (8) (13) (17) (20) (21)

Net result group 161 92 90 1,228 81 87 89 98 101

Minorities, other (5) (3) (3) (2) (3) - - - -

Net result shareholders 156 89 87 1,226 78 87 89 98 101

EPS, fully diluted (EUR) 1.13 0.72 0.63 16.68 1.07 1.15 1.18 1.29 1.33

MainFirst adjustments

Ex ceptionals abov e EBITDA - (12) - - - - - - -

Acquisition-related amortisation charges - - - - - - - - -

Interest charges reported abov e the EBIT line - - - - - - - - -

At-equity results reported in net financials - - - - - - - - -

Ex ceptionals below EBIT - 2 - - - 3 3 3 3

Profit & Loss Account (adjusted)

EBITDA 354 304 275 1,414 151 160 168 174 180

EBIT 212 159 155 1,331 91 100 105 116 119

Net result, shareholders 156 99 87 1,226 78 85 86 95 98

EPS, fully diluted (EUR) 1.13 0.72 0.63 16.68 1.07 1.15 1.18 1.29 1.33

Cash Flow Statement

EBITDA 354 292 275 1,414 151 160 168 174 180

Cash interest and tax (51) (55) (65) (103) (10) (13) (16) (18) (19)

Changes in w orking capital (43) (199) 27 (1,635) (13) (11) (11) (11) (12)

Other operating CF items (40) 12 (27) 374 (75) 8 9 6 9

Net operating cash flow 220 49 210 50 53 144 150 151 158

Capital ex penditure (intangibles, tangibles) (254) (172) (108) (79) (55) (56) (41) (42) (43)

Free cash flow (35) (123) 102 (29) (2) 89 109 109 115

Acquisitions, Disposals, Financial assets (21) (50) - - - - - - -

Div idends, minority pay outs (54) (56) (36) (36) (60) (60) (62) (65) (68)

Capital measures, other 98 - 1,919 (565) (264) 22 20 (9) (10)

Change in net cash/debt (11) (229) 1,985 (630) (326) 50 67 35 37

Net cash (debt) (588) (817) 1,168 538 212 262 329 364 401

Balance Sheet

Fix ed assets 2,246 2,393 887 847 870 859 831 873 916

t/o Goodw ill 299 324 100 100 100 100 100 105 110

Current assets 929 908 2,211 958 963 1,031 1,116 1,227 1,348

t/o Inv entories 50 55 21 22 20 21 21 22 23

t/o Trade receiv ables 352 424 161 170 184 191 198 204 210

t/o Cash and equiv alents 478 372 2,005 695 365 415 482 527 573

Group equity 1,599 1,726 1,667 1,249 1,285 1,331 1,377 1,501 1,636

t/o Shareholders' equity 1,555 1,699 1,645 1,229 1,264 1,310 1,356 1,479 1,613

Interest-bearing liabilities 1,065 1,189 837 157 153 153 153 162 172

Other liabilties and prov isions 511 385 595 398 395 406 417 436 456

t/o Trade liabilities 129 141 73 90 80 83 86 90 95

Balance sheet total 3,175 3,300 3,098 1,804 1,833 1,890 1,947 2,099 2,265

Net w orking capital 273 338 108 102 124 129 133 136 138

Capital employ ed (incl. Goodw ill) 2,519 2,730 995 948 994 988 965 1,008 1,054

Ratios

Rev enue, y /y 3.0% 9.0% 5.2% -49.9% -27.1% 3.7% 3.7% 3.0% 3.0%

EBITDA margin (adj.) 13.5% 10.6% 9.1% 93.6% 13.7% 14.0% 14.2% 14.3% 14.3%

EBIT margin (adj.) 8.1% 5.6% 5.2% 88.1% 8.3% 8.8% 8.9% 9.5% 9.5%

EPS (adj.), y /y 11.9% -36.3% -12.5% n/m -93.6% 7.5% 2.6% 9.3% 3.1%

Net w orking capital intensity (as a % of sales) 10.4% 11.8% 3.6% 6.7% 11.3% 11.3% 11.3% 11.1% 11.0%

DSOs (trade receiv ables as day s of rev s) 49 54 19 41 61 61 61 61 61

Inv entories as a % of rev enue 1.9% 1.9% 0.7% 1.4% 1.8% 1.8% 1.8% 1.8% 1.8%

Net debt (cash) / EBITDA (adj.) 1.7 2.7 (4.2) (0.4) (1.4) (1.6) (2.0) (2.1) (2.2)

EBITDA (adj.) / Capex 1.4 1.8 2.5 18.0 2.7 2.9 4.1 4.1 4.1

Free CF y ield (FCF / market cap) -1.6% -5.4% 4.2% -1.7% -0.1% 4.9% 6.0% 6.1% 6.4%

Oper. FCF y ield ([FCF - net int. tax ed] / EV) -0.3% -3.0% 10.1% 4.4% -0.0% 5.7% 7.2% 7.4% 7.9%

European Healthcare, 11 September 2015

21 / 44

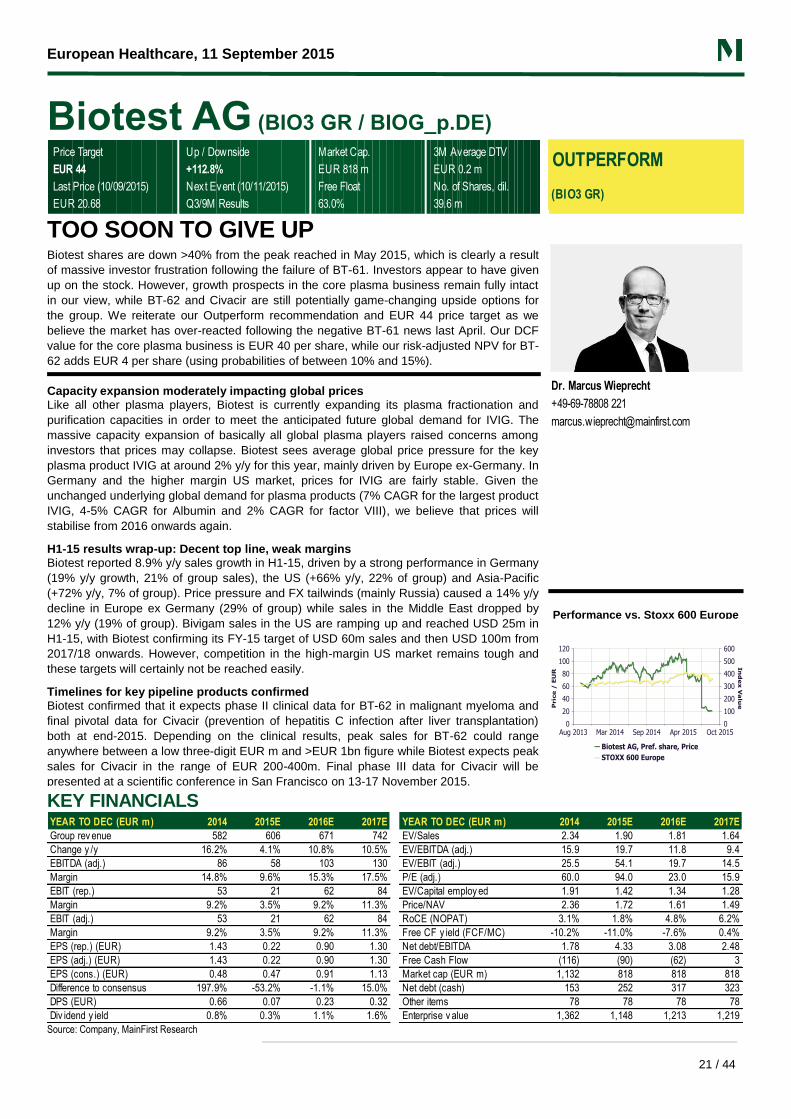

Biotest AG (BIO3 GR / BIOG_p.DE)

Price Target Up / Downside Market Cap. 3M Average DTV

EUR 44 +112.8% EUR 818 m EUR 0.2 m

Last Price (10/09/2015) Next Event (10/11/2015) Free Float No. of Shares, dil.

EUR 20.68 Q3/9M Results 63.0% 39.6 m

OUTPERFORM

(BIO3 GR)

TOO SOON TO GIVE UP Biotest shares are down >40% from the peak reached in May 2015, which is clearly a result

of massive investor frustration following the failure of BT-61. Investors appear to have given

up on the stock. However, growth prospects in the core plasma business remain fully intact

in our view, while BT-62 and Civacir are still potentially game-changing upside options for

the group. We reiterate our Outperform recommendation and EUR 44 price target as we

believe the market has over-reacted following the negative BT-61 news last April. Our DCF

value for the core plasma business is EUR 40 per share, while our risk-adjusted NPV for BT-

62 adds EUR 4 per share (using probabilities of between 10% and 15%).

Capacity expansion moderately impacting global prices Like all other plasma players, Biotest is currently expanding its plasma fractionation and

purification capacities in order to meet the anticipated future global demand for IVIG. The

massive capacity expansion of basically all global plasma players raised concerns among

investors that prices may collapse. Biotest sees average global price pressure for the key

plasma product IVIG at around 2% y/y for this year, mainly driven by Europe ex-Germany. In

Germany and the higher margin US market, prices for IVIG are fairly stable. Given the

unchanged underlying global demand for plasma products (7% CAGR for the largest product

IVIG, 4-5% CAGR for Albumin and 2% CAGR for factor VIII), we believe that prices will

stabilise from 2016 onwards again.

H1-15 results wrap-up: Decent top line, weak margins Biotest reported 8.9% y/y sales growth in H1-15, driven by a strong performance in Germany

(19% y/y growth, 21% of group sales), the US (+66% y/y, 22% of group) and Asia-Pacific

(+72% y/y, 7% of group). Price pressure and FX tailwinds (mainly Russia) caused a 14% y/y

decline in Europe ex Germany (29% of group) while sales in the Middle East dropped by

12% y/y (19% of group). Bivigam sales in the US are ramping up and reached USD 25m in

H1-15, with Biotest confirming its FY-15 target of USD 60m sales and then USD 100m from

2017/18 onwards. However, competition in the high-margin US market remains tough and

these targets will certainly not be reached easily.

Timelines for key pipeline products confirmed Biotest confirmed that it expects phase II clinical data for BT-62 in malignant myeloma and

final pivotal data for Civacir (prevention of hepatitis C infection after liver transplantation)

both at end-2015. Depending on the clinical results, peak sales for BT-62 could range

anywhere between a low three-digit EUR m and >EUR 1bn figure while Biotest expects peak

sales for Civacir in the range of EUR 200-400m. Final phase III data for Civacir will be

presented at a scientific conference in San Francisco on 13-17 November 2015.

Dr. Marcus Wieprecht

+49-69-78808 221

Performance vs. Stoxx 600 Europe

KEY FINANCIALS

Source: Company, MainFirst Research

YEAR TO DEC (EUR m) 2014 2015E 2016E 2017E YEAR TO DEC (EUR m) 2014 2015E 2016E 2017E

Group rev enue 582 606 671 742 EV/Sales 2.34 1.90 1.81 1.64

Change y /y 16.2% 4.1% 10.8% 10.5% EV/EBITDA (adj.) 15.9 19.7 11.8 9.4

EBITDA (adj.) 86 58 103 130 EV/EBIT (adj.) 25.5 54.1 19.7 14.5

Margin 14.8% 9.6% 15.3% 17.5% P/E (adj.) 60.0 94.0 23.0 15.9

EBIT (rep.) 53 21 62 84 EV/Capital employ ed 1.91 1.42 1.34 1.28

Margin 9.2% 3.5% 9.2% 11.3% Price/NAV 2.36 1.72 1.61 1.49

EBIT (adj.) 53 21 62 84 RoCE (NOPAT) 3.1% 1.8% 4.8% 6.2%

Margin 9.2% 3.5% 9.2% 11.3% Free CF y ield (FCF/MC) -10.2% -11.0% -7.6% 0.4%

EPS (rep.) (EUR) 1.43 0.22 0.90 1.30 Net debt/EBITDA 1.78 4.33 3.08 2.48

EPS (adj.) (EUR) 1.43 0.22 0.90 1.30 Free Cash Flow (116) (90) (62) 3

EPS (cons.) (EUR) 0.48 0.47 0.91 1.13 Market cap (EUR m) 1,132 818 818 818

Difference to consensus 197.9% -53.2% -1.1% 15.0% Net debt (cash) 153 252 317 323

DPS (EUR) 0.66 0.07 0.23 0.32 Other items 78 78 78 78

Div idend y ield 0.8% 0.3% 1.1% 1.6% Enterprise v alue 1,362 1,148 1,213 1,219

European Healthcare, 11 September 2015

22 / 44

Key Financials Page

Year to December (EUR m) 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Profit & Loss Account

Group revenue (All items as reported) 422 440 501 582 606 671 742 823 916

EBITDA 72 76 86 86 58 103 130 162 193

EBIT 42 45 54 53 21 62 84 111 138

Pre-tax result 29 36 48 47 13 52 74 101 128

Income tax , other items (10) (13) (16) (28) (4) (16) (22) (30) (38)

Net result group 19 23 32 19 9 36 52 71 89

Minorities, other (2) - - - - - - - -

Net result shareholders 17 23 32 19 9 36 51 70 89

EPS, fully diluted (EUR) 3.95 2.82 2.54 1.43 0.22 0.90 1.30 1.78 2.25

MainFirst adjustments

Ex ceptionals abov e EBITDA - - - - - - - - -

Acquisition-related amortisation charges - - - - - - - - -

Interest charges reported abov e the EBIT line - - - - - - - - -

At-equity results reported in net financials - - - - - - - - -

Ex ceptionals below EBIT - - - - - - - - -

Profit & Loss Account (adjusted)

EBITDA 72 76 86 86 58 103 130 162 193

EBIT 42 45 54 53 21 62 84 111 138

Net result, shareholders 17 23 32 19 9 36 51 70 89

EPS, fully diluted (EUR) 1.44 1.94 2.54 1.43 0.22 0.90 1.30 1.78 2.25

Cash Flow Statement

EBITDA 72 76 86 86 58 103 130 162 193

Cash interest and tax (23) (23) (23) (34) (12) (25) (32) (40) (48)

Changes in w orking capital 13 (9) (78) (77) (8) (41) (43) (56) (63)

Other operating CF items 10 (10) 8 14 6 6 6 6 6

Net operating cash flow 72 35 (7) (11) 44 41 60 71 87

Capital ex penditure (intangibles, tangibles) (27) (35) (43) (104) (133) (103) (57) (62) (65)

Free cash flow 45 - (50) (116) (90) (62) 3 8 22

Acquisitions, Disposals, Financial assets 49 5 10 1 - - - - -

Div idends, minority pay outs (6) (5) (6) (8) (9) (3) (9) (13) (18)

Capital measures, other - 1 74 (3) (1) - - - -

Change in net cash/debt 87 1 28 (125) (100) (65) (6) (4) 4

Net cash (debt) (56) (55) (27) (153) (252) (317) (323) (327) (323)

Balance Sheet

Fix ed assets 305 301 306 340 436 498 509 521 531

t/o Goodw ill - - - - - - - - -

Current assets 378 381 581 693 595 571 607 659 727

t/o Inv entories 153 184 227 246 248 275 304 338 375

t/o Trade receiv ables 121 96 119 182 182 195 208 231 256

t/o Cash and equiv alents 83 57 204 179 80 15 9 5 9

Group equity 347 369 461 480 477 508 548 603 673

t/o Shareholders' equity 347 369 461 480 477 508 548 603 672

Interest-bearing liabilities 139 112 232 332 332 332 332 332 332

Other liabilties and prov isions 197 200 194 221 223 229 236 244 253

t/o Trade liabilities 35 47 51 56 58 64 71 79 87

Balance sheet total 683 682 887 1,033 1,031 1,069 1,116 1,180 1,258

Net w orking capital 239 233 294 372 372 406 441 490 544

Capital employ ed (incl. Goodw ill) 544 534 600 712 808 904 950 1,010 1,076

Ratios

Rev enue, y /y 2.3% 4.3% 13.8% 16.2% 4.1% 10.8% 10.5% 11.0% 11.2%

EBITDA margin (adj.) 17.2% 17.3% 17.1% 14.8% 9.6% 15.3% 17.5% 19.7% 21.0%

EBIT margin (adj.) 9.8% 10.1% 10.7% 9.2% 3.5% 9.2% 11.3% 13.5% 15.0%

EPS (adj.), y /y -1.4% 34.7% 30.9% -43.7% -84.6% n/m 44.4% 36.9% 26.4%

Net w orking capital intensity (as a % of sales) 56.7% 53.0% 58.7% 63.9% 61.5% 60.5% 59.5% 59.5% 59.5%

DSOs (trade receiv ables as day s of rev s) 105 80 86 114 110 106 102 102 102

Inv entories as a % of rev enue 36.2% 41.9% 45.3% 42.3% 41.0% 41.0% 41.0% 41.0% 41.0%

Net debt (cash) / EBITDA (adj.) 0.8 0.7 0.3 1.8 4.3 3.1 2.5 2.0 1.7

EBITDA (adj.) / Capex 2.6 2.2 2.0 0.8 0.4 1.0 2.3 2.6 2.9

Free CF y ield (FCF / market cap) 9.1% 0.0% -7.0% -10.2% -11.0% -7.6% 0.4% 1.0% 2.6%

Oper. FCF y ield ([FCF - net int. tax ed] / EV) 9.0% 1.0% -5.6% -8.3% -7.3% -4.5% 0.8% 1.3% 2.3%

European Healthcare, 11 September 2015

23 / 44

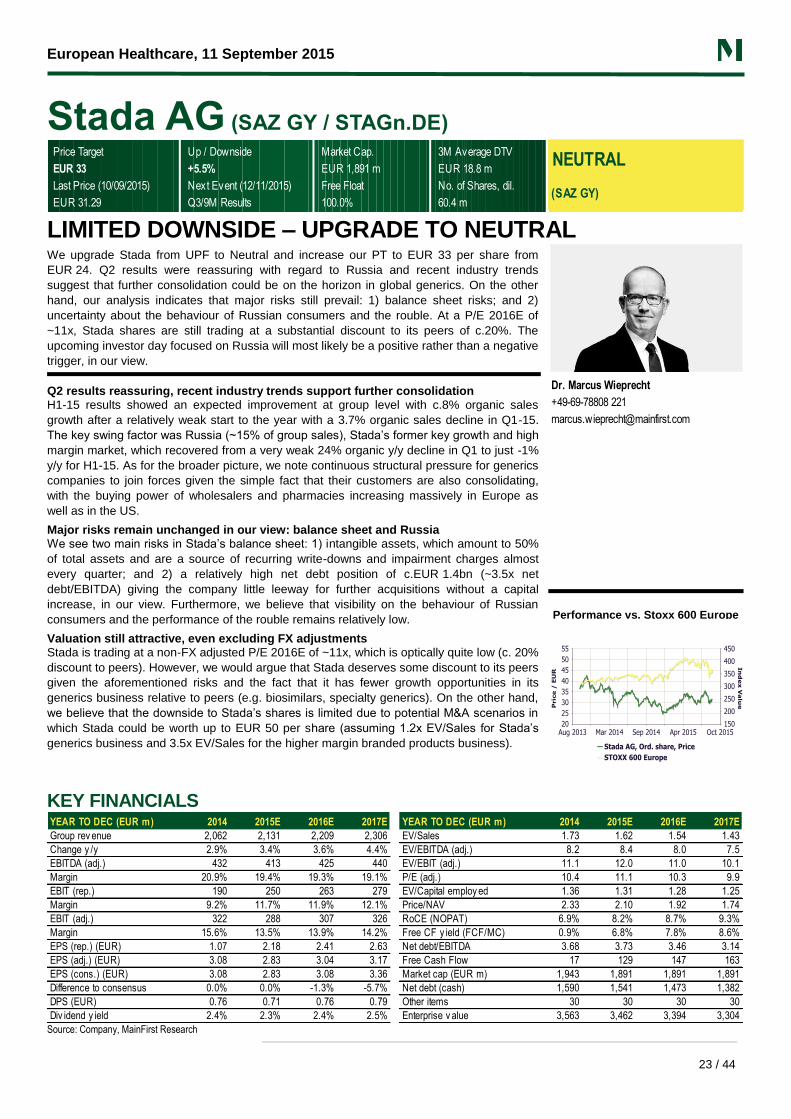

Stada AG (SAZ GY / STAGn.DE)

Price Target Up / Downside Market Cap. 3M Average DTV

EUR 33 +5.5% EUR 1,891 m EUR 18.8 m

Last Price (10/09/2015) Next Event (12/11/2015) Free Float No. of Shares, dil.

EUR 31.29 Q3/9M Results 100.0% 60.4 m

NEUTRAL

(SAZ GY)

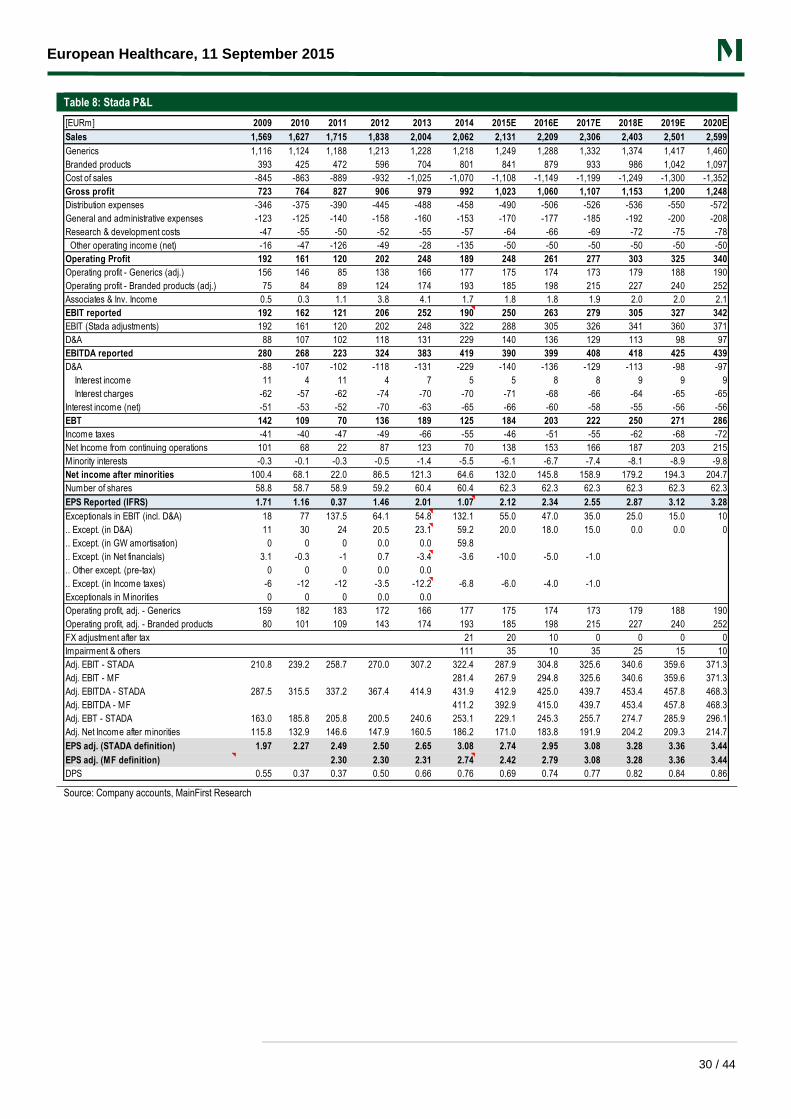

LIMITED DOWNSIDE – UPGRADE TO NEUTRAL We upgrade Stada from UPF to Neutral and increase our PT to EUR 33 per share from

EUR 24. Q2 results were reassuring with regard to Russia and recent industry trends

suggest that further consolidation could be on the horizon in global generics. On the other

hand, our analysis indicates that major risks still prevail: 1) balance sheet risks; and 2)

uncertainty about the behaviour of Russian consumers and the rouble. At a P/E 2016E of

~11x, Stada shares are still trading at a substantial discount to its peers of c.20%. The

upcoming investor day focused on Russia will most likely be a positive rather than a negative

trigger, in our view.

Q2 results reassuring, recent industry trends support further consolidation H1-15 results showed an expected improvement at group level with c.8% organic sales

growth after a relatively weak start to the year with a 3.7% organic sales decline in Q1-15.

The key swing factor was Russia (~15% of group sales), Stada’s former key growth and high

margin market, which recovered from a very weak 24% organic y/y decline in Q1 to just -1%

y/y for H1-15. As for the broader picture, we note continuous structural pressure for generics

companies to join forces given the simple fact that their customers are also consolidating,

with the buying power of wholesalers and pharmacies increasing massively in Europe as

well as in the US.

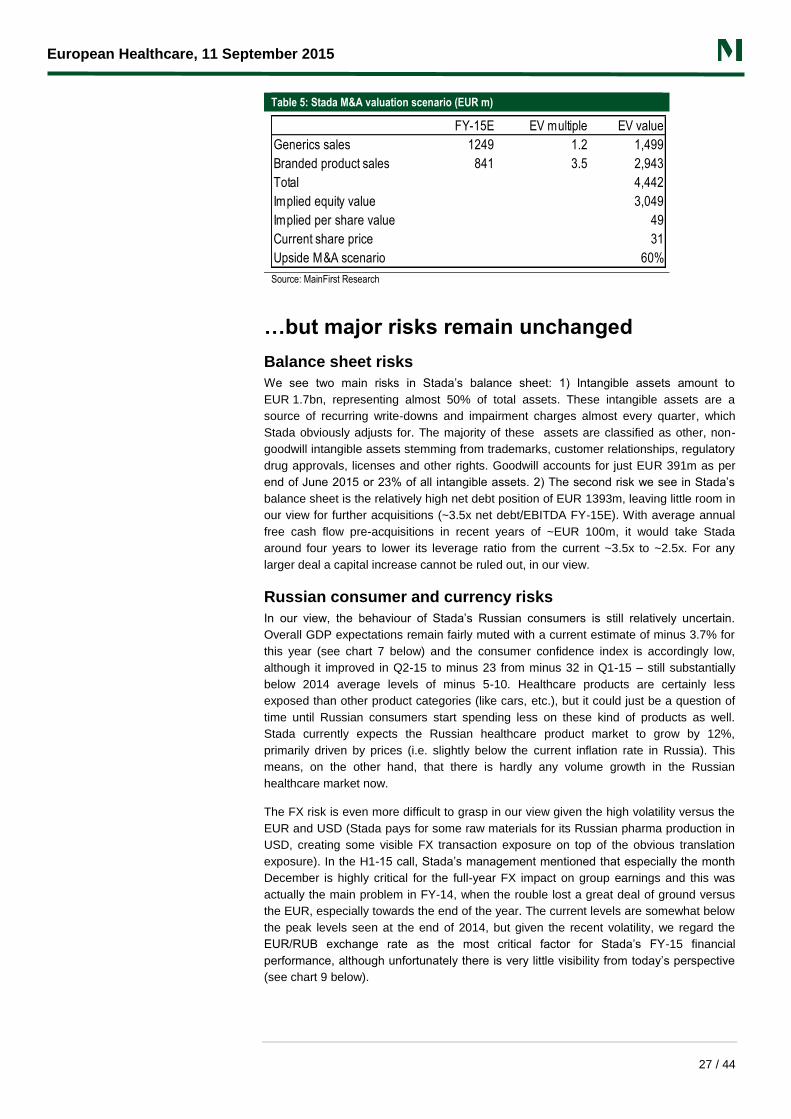

Major risks remain unchanged in our view: balance sheet and Russia We see two main risks in Stada’s balance sheet: 1) intangible assets, which amount to 50%

of total assets and are a source of recurring write-downs and impairment charges almost

every quarter; and 2) a relatively high net debt position of c.EUR 1.4bn (~3.5x net

debt/EBITDA) giving the company little leeway for further acquisitions without a capital

increase, in our view. Furthermore, we believe that visibility on the behaviour of Russian

consumers and the performance of the rouble remains relatively low.

Valuation still attractive, even excluding FX adjustments Stada is trading at a non-FX adjusted P/E 2016E of ~11x, which is optically quite low (c. 20%

discount to peers). However, we would argue that Stada deserves some discount to its peers

given the aforementioned risks and the fact that it has fewer growth opportunities in its

generics business relative to peers (e.g. biosimilars, specialty generics). On the other hand,

we believe that the downside to Stada’s shares is limited due to potential M&A scenarios in