Embed Size (px)

Citation preview

1

European Road Show June 2006

O I L S E A R C H L I M I T E D

2

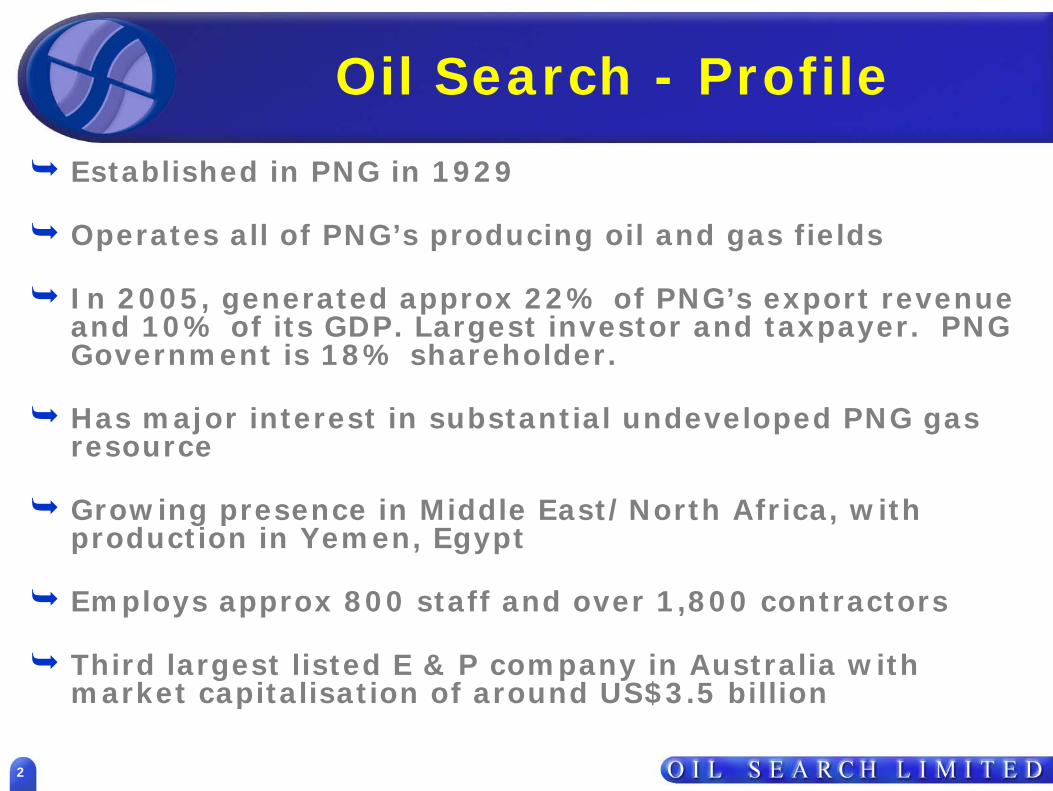

Oil Search - Profile

Established in PNG in 1929

Operates all of PNG’s producing oil and gas fields

In 2005, generated approx 22% of PNG’s export revenue and 10% of its GDP. Largest investor and taxpayer. PNG Government is 18% shareholder.

Has major interest in substantial undeveloped PNG gas resource

Growing presence in Middle East/North Africa, with production in Yemen, Egypt

Employs approx 800 staff and over 1,800 contractors

Third largest listed E & P company in Australia with market capitalisation of around US$3.5 billion

3

Oil SearchWhere We Operate

4

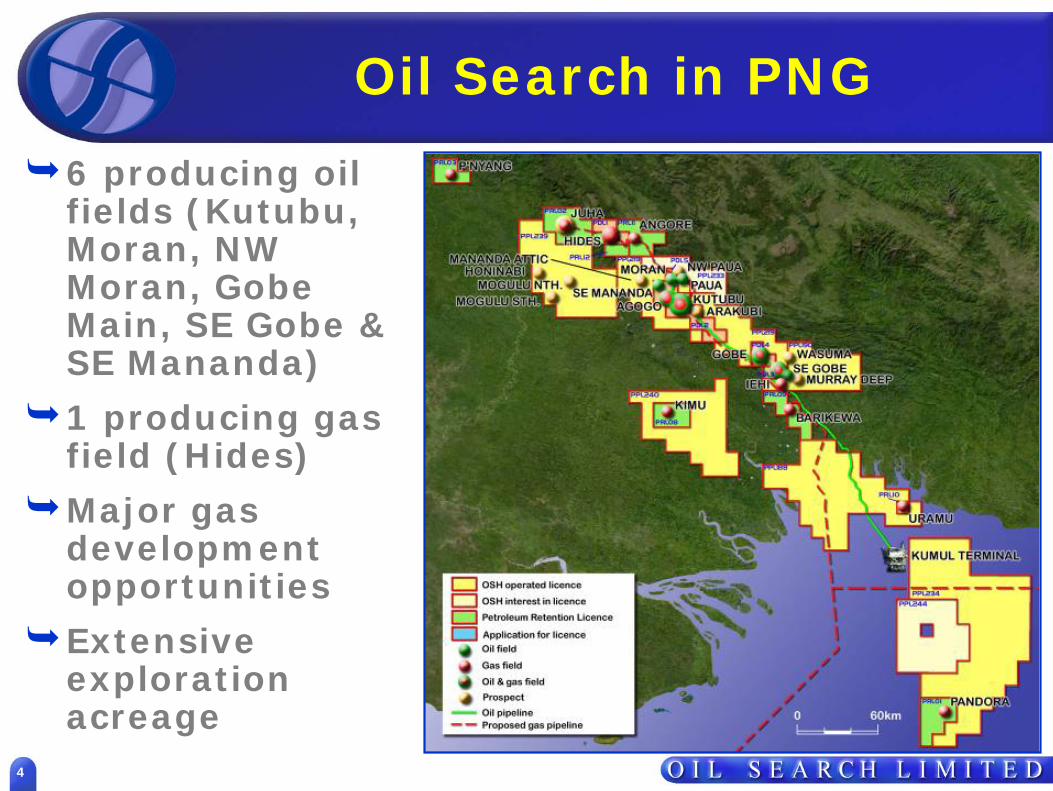

Oil Search in PNG

6 producing oil fields (Kutubu, Moran, NW Moran, Gobe Main, SE Gobe & SE Mananda)

1 producing gas field (Hides)

Major gas development opportunities

Extensive exploration acreage

5

Oil SearchWhere We Operate

6

Oil Search in Yemen

1 producing oil field (Nabrajah, Block 43)Nabrajah Basement development6 concession areas (5 as Operator)

7

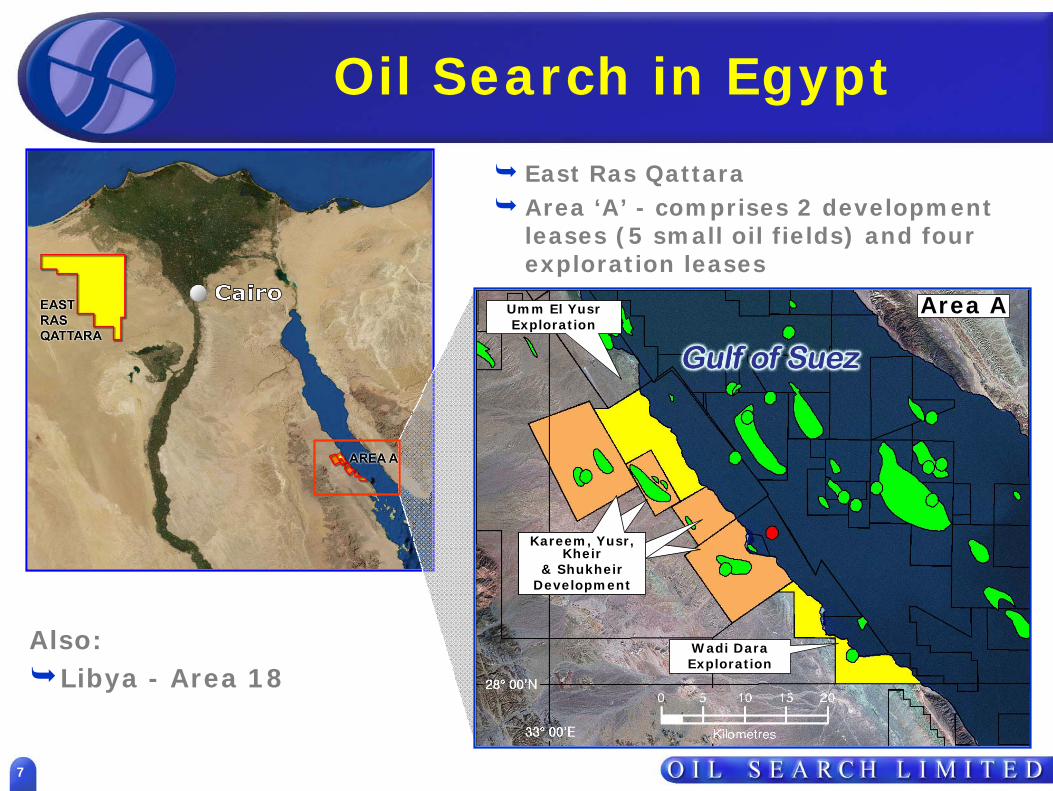

Oil Search in Egypt

Also:Libya - Area 18

East Ras Qattara Area ‘A’ - comprises 2 development leases (5 small oil fields) and four exploration leases

Area A

Wadi DaraExploration

Kareem, Yusr, Kheir

& ShukheirDevelopment

Kareem, Yusr, Kheir

& ShukheirDevelopment

Kareem, Yusr, Kheir

& ShukheirDevelopment

Kareem, Yusr, Kheir

& ShukheirDevelopment

Umm El YusrExploration

8

Core Expertise

Developing country specialistAbility to work co-operatively with host governments and local communitiesCulturally sensitive and diverseExperienced in operating in challenging environmentsLow cost, innovative, regionally significant operator

9

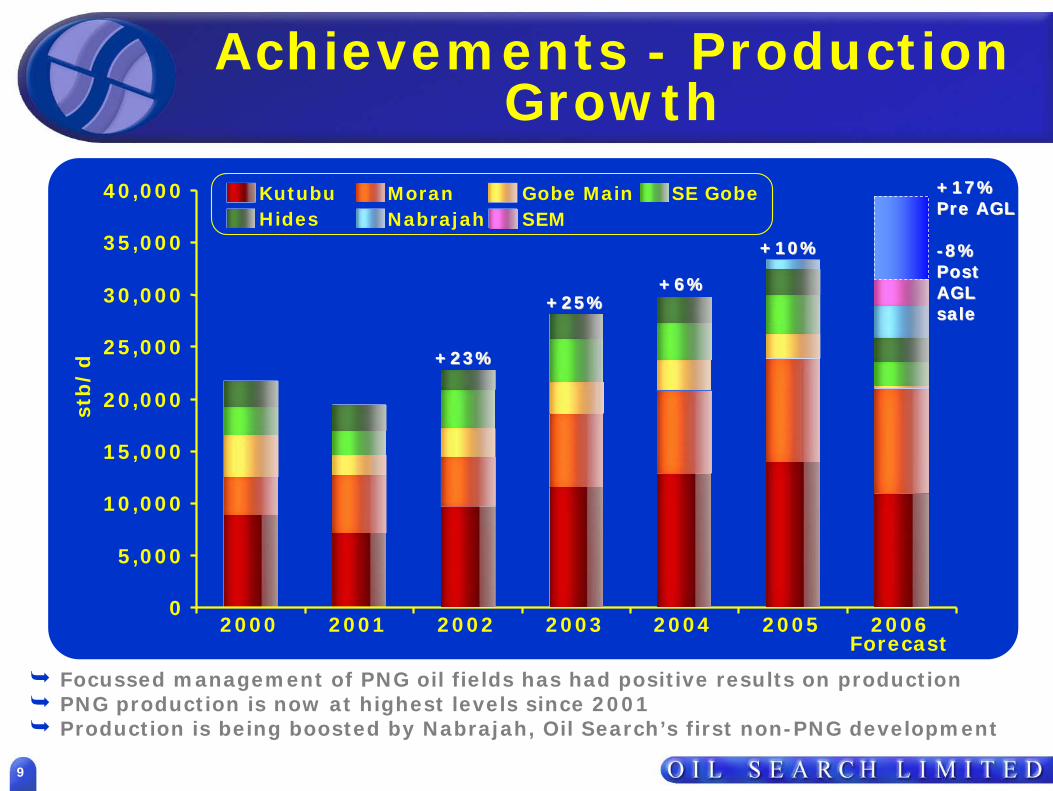

Achievements - Production Growth

Focussed management of PNG oil fields has had positive results on productionPNG production is now at highest levels since 2001Production is being boosted by Nabrajah, Oil Search’s first non-PNG development

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

stb

/d

Kutubu Moran Gobe Main SE GobeHides Nabrajah SEM

2000 2001 2002 2003 2004 2005Forecast

+23%+23%

+25%+25%+6%+6%

+10%+10%

2006

+17%+17%Pre AGLPre AGL

--8% 8% PostPostAGL AGL salesale

10

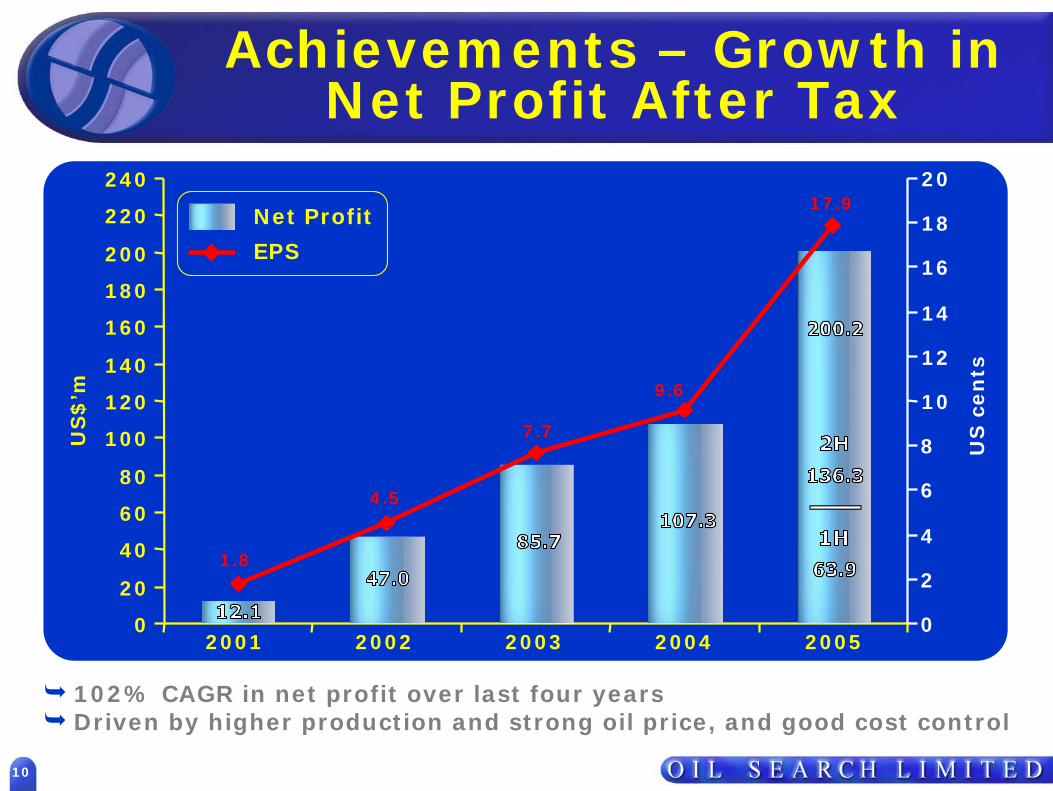

Achievements – Growth in Net Profit After Tax

102% CAGR in net profit over last four yearsDriven by higher production and strong oil price, and good cost control

US

cen

ts

US

$’m

0

20

40

60

80

100

120

140

160

180

200

220

240

2001 2002 2003 2004 20050

2

4

6

8

10

12

14

16

18

20

4.5

17.9

9.6

7.7

1.8

Net Profit

EPS

11

Achievements - Top Quartile Total Shareholder Returns

0

20

40

60

80

100

120

2003 2004 2005

%

8th out ofASX 150

5th out ofASX 150

4th out ofASX 150

Four fold increase in Market Capitalisation since 2003

12

Growth - The Next Phase

Strategic Review in 2002Five year plan to double market capitalisation, and to generate top quartile returnsDelivered : operating control of core business

: significant production increase: operating cost reductions: major steps towards commercialising

discovered gas resource: development of quality exploration

portfolio: very strong balance sheet

All key objectives have been achieved

13

Growth - The Next Phase

New Strategic Review underway

Objective to more than double market capitalisation by 2010

Starting from a position of strengthExcellent asset base, with large discovered gas resource and quality exploration portfolioCapture of latent value potential will deliver target

Focus on gas commercialisationIncreased explorationContinued production optimisation

14

Growth - The Next Phase

Business in a New EnvironmentOil prices around/above US$50/bblUnprecedented demand for gas (especially Asia-Pacific) delivering new price environmentShortage of equipment, services and people cost escalation and pressures on timely delivery

Essential to Drive Business to Manage these Influences

15

Growth - The Next Phase

Oil Search positioning itself to take advantage of opportunities created by the new market fundamentals

Key part of Strategic ReviewTargeted value extraction in producing fieldsTight cost controlsProcurement and services alliancingEquipment ownership to control costs and availability and people

16

Growth - The Next Phase

Focus for GrowthDeliver Value

Substantial remaining potential in PNG oil fieldsFurther Yemen developmentsCost controls and improved profitability

Extract ValueCommercialise our 1.1 billion boe gas and liquids resource

PNG Gas ProjectLNG / Petrochemical

Create ValueAcceleration of exploration activity in PNG and Middle East / North AfricaMix of low risk moderate impact, higher risk high impact programme

17

Vision for 2011

Market capitalisation above US$7 billion

Continuation of world class health, safety and environment performance

Oil production growth through PNG and Middle East optimisation and new developments

Development of multiple gas offtake projects

Strong Balance Sheet / Active Capital Management

18

DELIVER VALUE

19

PNG Oil Production Outlook

SummaryProgrammes post-operatorship change have been successfulCurrent gross PNG production

At 2001 levelsDouble the level predicted by previous Operator for 2006

Opportunities exist, with continuous programme for the foreseeable future

3 drilling rigs in 2006 4 drilling rigs in 2007

PNG Gross Production History 2000-2005and Forecast 2006

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2000

2001

2002

2003

2004

2005

2006

STB/D

Forecast

Trend BeforeOil Search

Operatorship

20

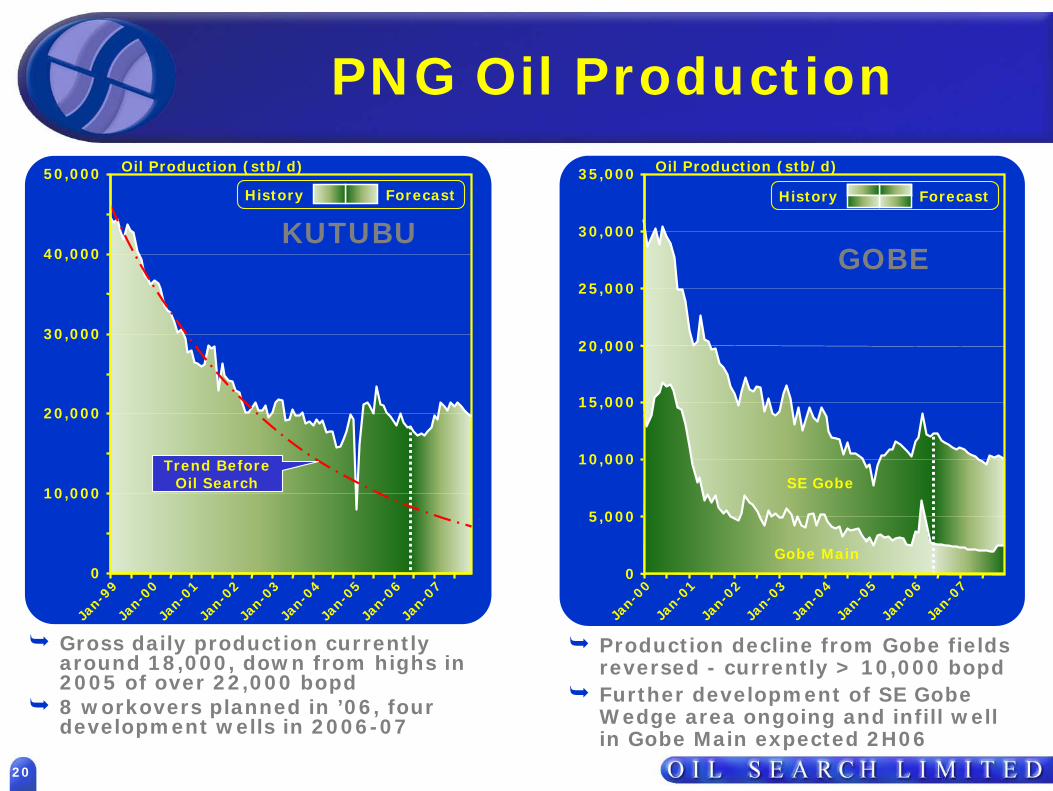

PNG Oil Production

Gross daily production currently around 18,000, down from highs in 2005 of over 22,000 bopd8 workovers planned in ’06, four development wells in 2006-07

Production decline from Gobe fields reversed - currently > 10,000 bopdFurther development of SE Gobe Wedge area ongoing and infill well in Gobe Main expected 2H06

0

10,000

20,000

30,000

40,000

50,000

Jan-

99Ja

n-00

Jan-

01Ja

n-02

Jan-

03Ja

n-04

Jan-

05Ja

n-06

Jan-

07

Oil Production (stb/d)

Trend BeforeOil Search

ForecastHistory

KUTUBU

Jan-

00Ja

n-01

Jan-

02Ja

n-03

Jan-

04Ja

n-05

Jan-

06Ja

n-07

5,000

10,000

15,000

20,000

25,000

30,000

35,000 Oil Production (stb/d)

ForecastHistory

GOBE

0

SE Gobe

Gobe Main

21

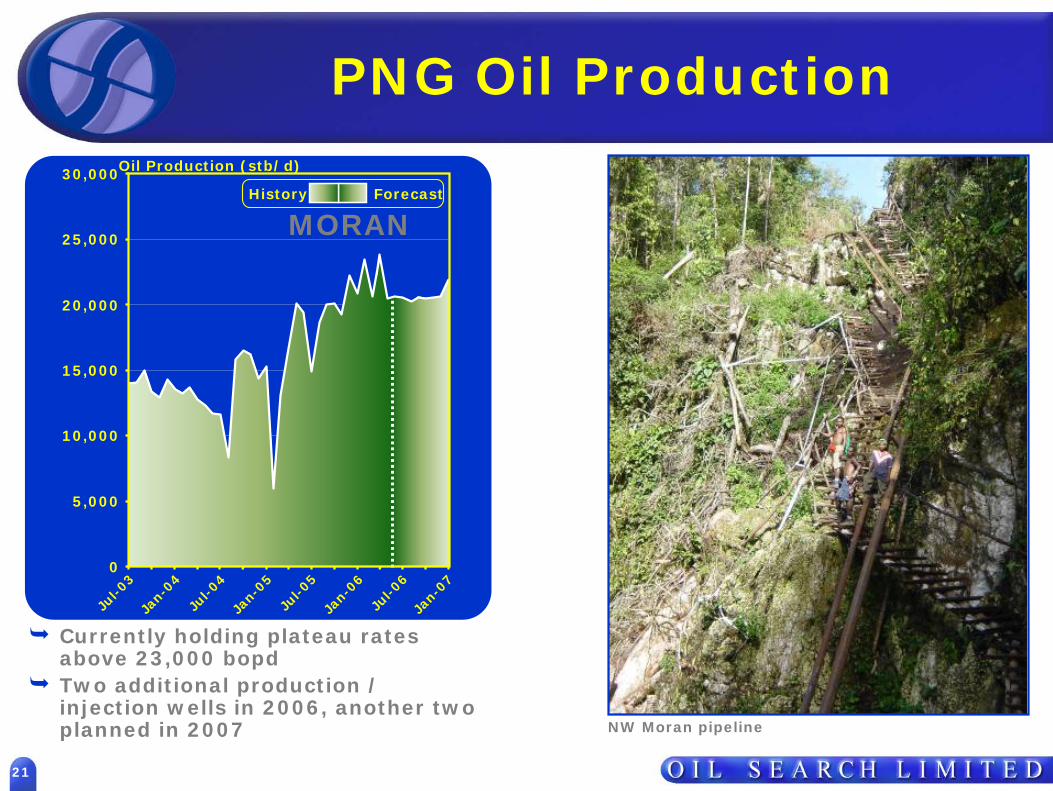

PNG Oil Production

Currently holding plateau rates above 23,000 bopd Two additional production / injection wells in 2006, another two planned in 2007

0

5,000

10,000

15,000

20,000

25,000

30,000

Jul-0

3Ja

n-04

Jul-0

4Ja

n-05

Jul-0

5Ja

n-06

Jul-0

6

Oil Production (stb/d)

MORANForecastHistory

NW Moran pipeline

Jan-

07

22

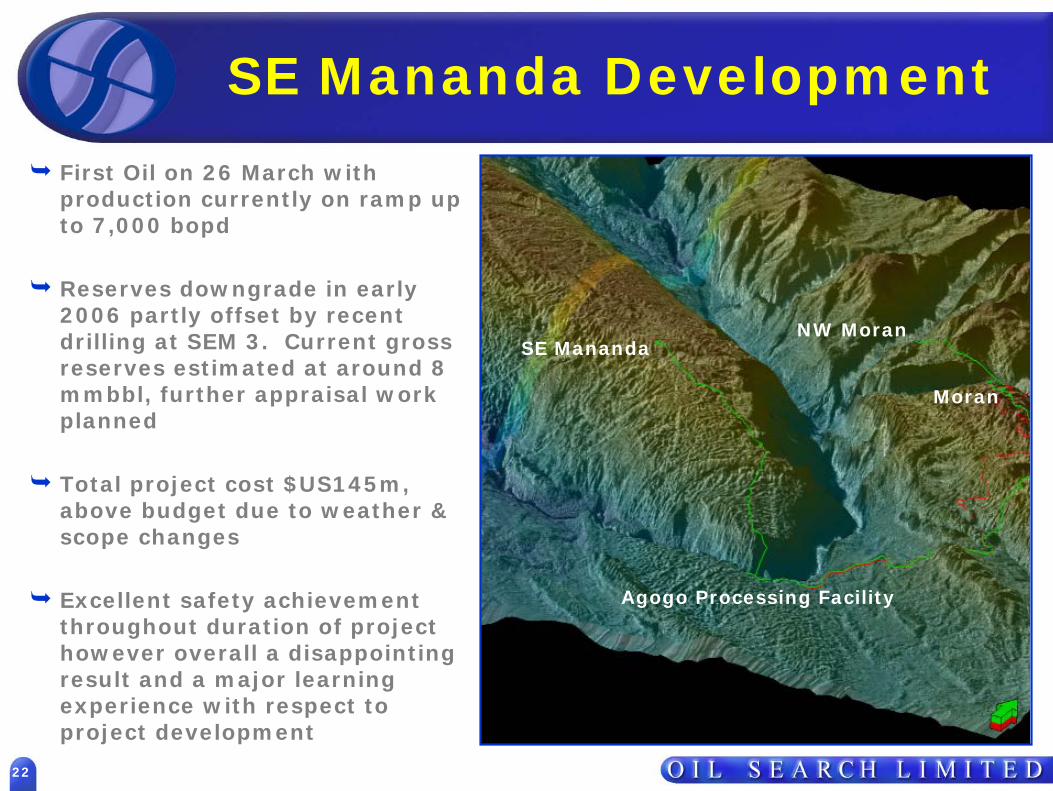

SE Mananda Development

First Oil on 26 March with production currently on ramp up to 7,000 bopd

Reserves downgrade in early 2006 partly offset by recent drilling at SEM 3. Current gross reserves estimated at around 8 mmbbl, further appraisal work planned

Total project cost $US145m, above budget due to weather & scope changes

Excellent safety achievement throughout duration of project however overall a disappointing result and a major learning experience with respect to project development

SE Mananda

Moran

Agogo Processing Facility

NW Moran

23

SE Mananda Bridge

24

SE Mananda Bridge

25

Yemen Production -Nabrajah

Nabrajah gross production currently averaging around 9,000 bopdFacilities expansion to 25,000 bopd nearing completionField still under appraisal – Nab-10 testing underwayFollowing completion of Nab-10, will drill Nab-11, 1km west of Nab-5 in same terraceDrilling will re-commence 2H 06, post interpretation of 3D seismic -2400

-2200

-2000

-1800

-1600

-1400

-1200

-1000

Nabrajah-8Nabrajah-10

Top Qishn

Top Saar

Top Qishn S2

Top Basement

DEPTH (m)

0 500 m500

Possible fractured Basement

“Naifa”Reservoir

Nabrajah 10

Nabrajah 11

Surface locationTop Basement location

DNO mapping

Nabrajah 2

Nabrajah 9

Nabrajah 8

26

EXTRACT VALUE

27

Gas Commercialisation

Oil Search has over 1 billion boe of proven and probable uncontracted gas and associated liquids

Resource is of considerable potential value, as world prices continue to climb

Approximately 40% of resource dedicated to PNG Gas Project – low Australian gas prices an anomaly in the developed world

Considerable new interest in PNG’s static gas resources

Strategic approach designed to capture phased value in new market regime

28

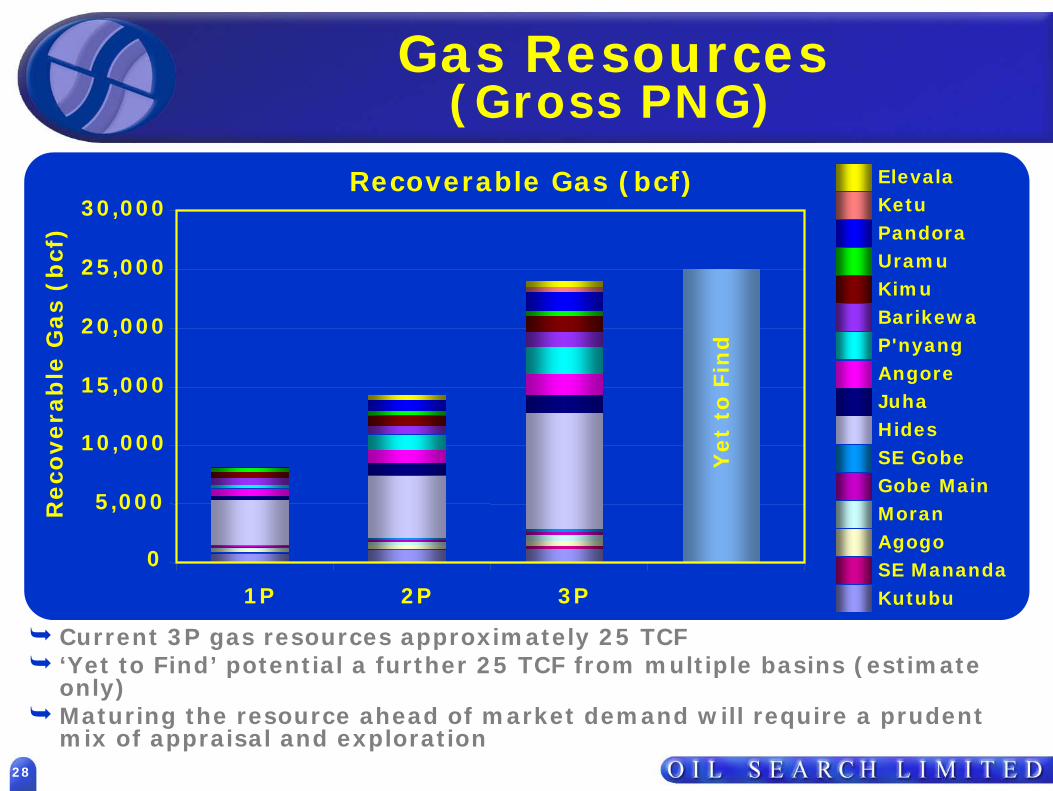

Gas Resources(Gross PNG)

Current 3P gas resources approximately 25 TCF‘Yet to Find’ potential a further 25 TCF from multiple basins (estimate only)Maturing the resource ahead of market demand will require a prudent mix of appraisal and exploration

Recoverable Gas (bcf) ElevalaKetuPandoraUramuKimuBarikewaP'nyangAngoreJuhaHidesSE GobeGobe MainMoranAgogoSE ManandaKutubu

0

5,000

10,000

15,000

20,000

25,000

30,000

1P 2P 3P

Reco

vera

ble

Gas

(bcf

)

Yet

to F

ind

29

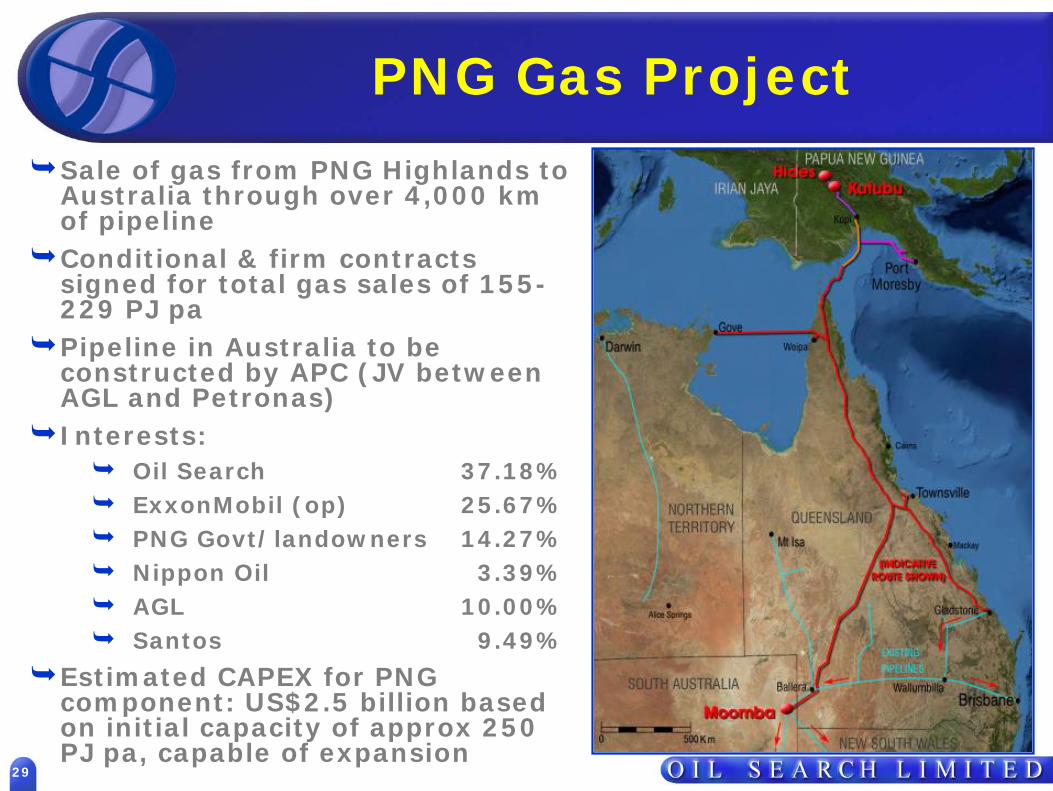

PNG Gas Project

Sale of gas from PNG Highlands to Australia through over 4,000 km of pipelineConditional & firm contracts signed for total gas sales of 155-229 PJ paPipeline in Australia to be constructed by APC (JV between AGL and Petronas)Interests:

Oil Search 37.18%ExxonMobil (op) 25.67%PNG Govt/landowners 14.27%Nippon Oil 3.39%AGL 10.00%Santos 9.49%

Estimated CAPEX for PNG component: US$2.5 billion based on initial capacity of approx 250 PJ pa, capable of expansion

30

PNG Gas Project Status

Markets are largely underwritten. Likely to be close to/at initial build plant capacity. Not actively seeking additional markets

Government/landowner agreements - substantial activities in PNG to finalise regulatory and landowner agreements with unanimous support from all partiesProgress being made on tariff negotiations with APC –critical path itemBankable finance plan – IM to be released shortlyEnvironmental management plan well advanced

Discussions with Santos progressing to positive conclusion

Mid-year 2006 target for project sanction is aggressive, more likely to be second half, project participants pushing ahead aggressively

Still targeting late 2009 for first gas

31

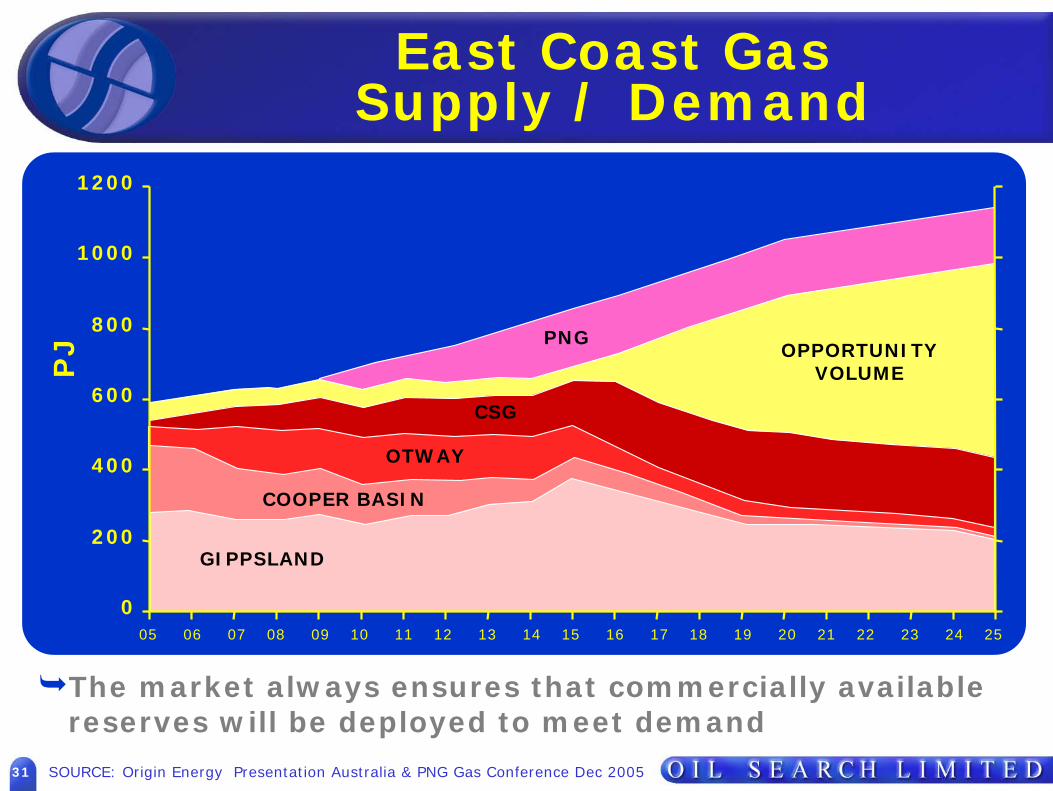

East Coast GasSupply / Demand

The market always ensures that commercially available reserves will be deployed to meet demand

05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

0

200

400

600

800

1000

1200

PJ

SOURCE: Origin Energy Presentation Australia & PNG Gas Conference Dec 2005

GIPPSLAND

COOPER BASIN

OTWAY

CSG

OPPORTUNITYVOLUME

PNG

32

Gas Commercialisation –Phase 2

PNG Gas Project commercialises significant volume of reserves and delivers major infrastructure spine

Opens way for further gas development in PNG, for in-country projects and LNG

New initiative recognising world market realities –substantial price differentials, strong demand

Significant interest for petrochemicals, GtL, fertiliser and new LNG developments

Targeting higher returns and reviewing opportunities to get involved in more points of value chain

Requires resource conversion to contractable gas

33

Phase 2 Gas Strategy

Aiming for 150 PJ pa initial market load in Port Moresby, growing to over 300 PJ paFEED on pipeline from Kopi to Port Moresby underwayFlexible gas supply options but to include potential development of:

Juha (OSH 31.5%)Barikewa (OSH 42.6%)Kimu (OSH 44.6%)Uramu (OSH 49.5%)

Subject to further appraisal success -accelerated appraisal programme seeking to convert 4-8 tcf into contractable status in 3 years

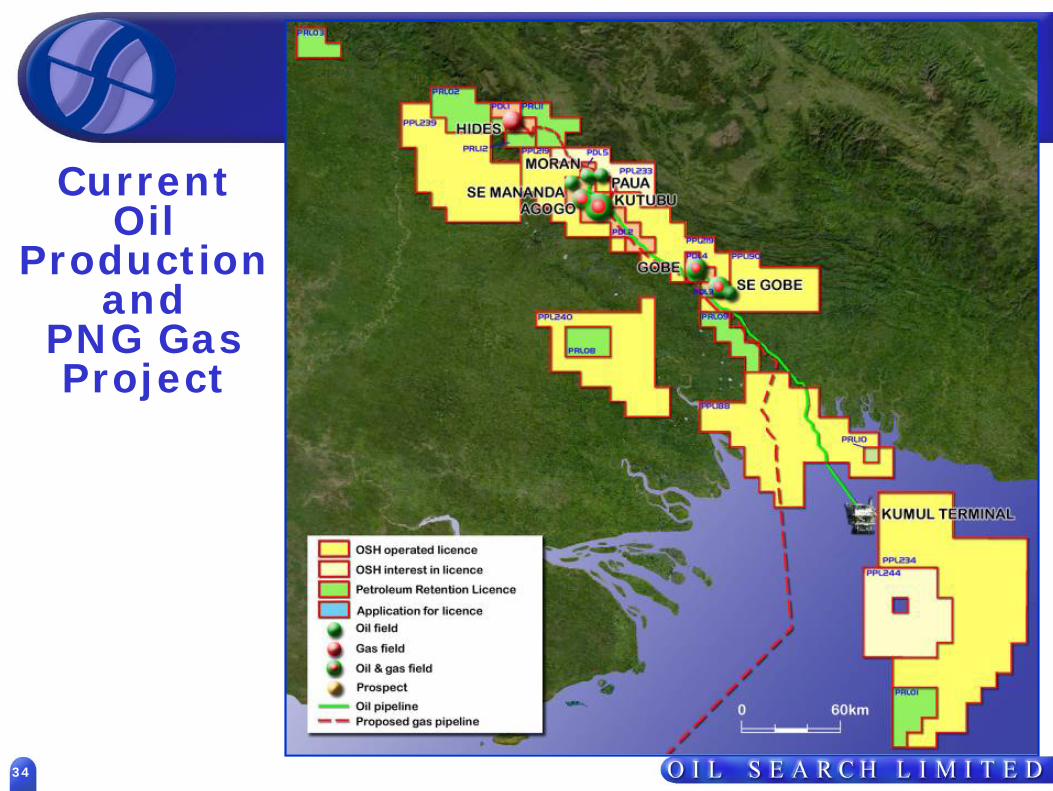

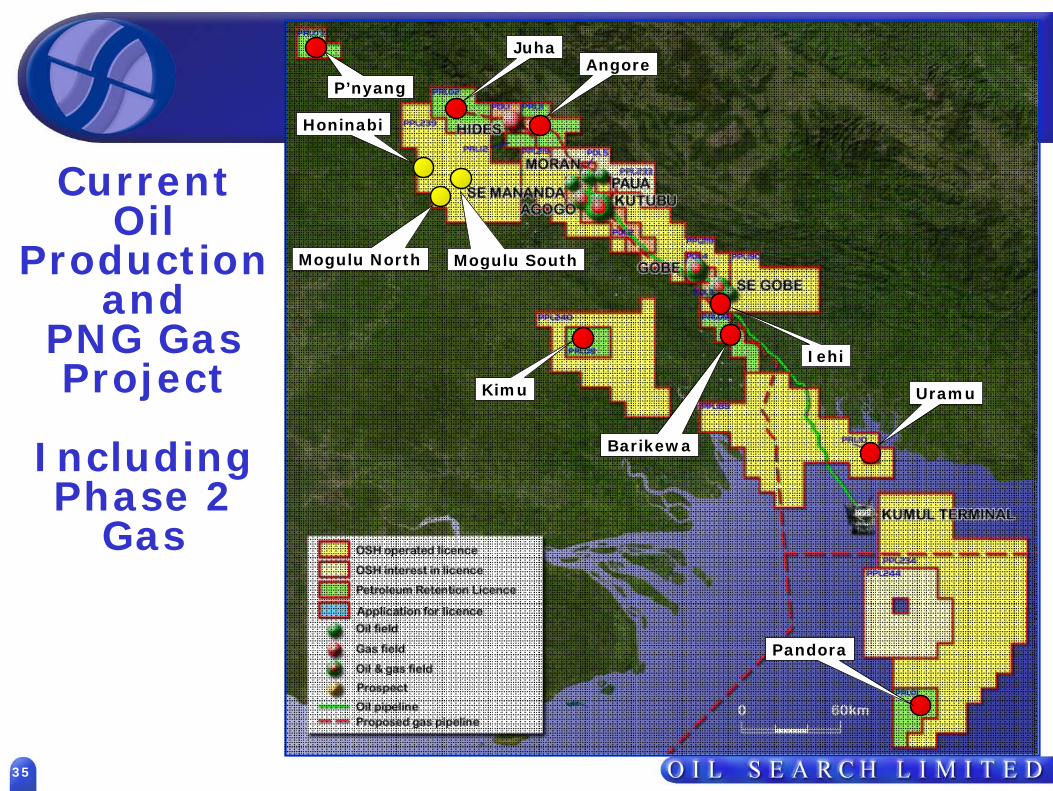

34

CurrentOil

Production and

PNG Gas Project

35

CurrentOil

Production and

PNG Gas Project

IncludingPhase 2

Gas

Angore

Barikewa

Uramu

Pandora

Juha

P’nyang

Kimu

Iehi

Honinabi

Mogulu North Mogulu South

36

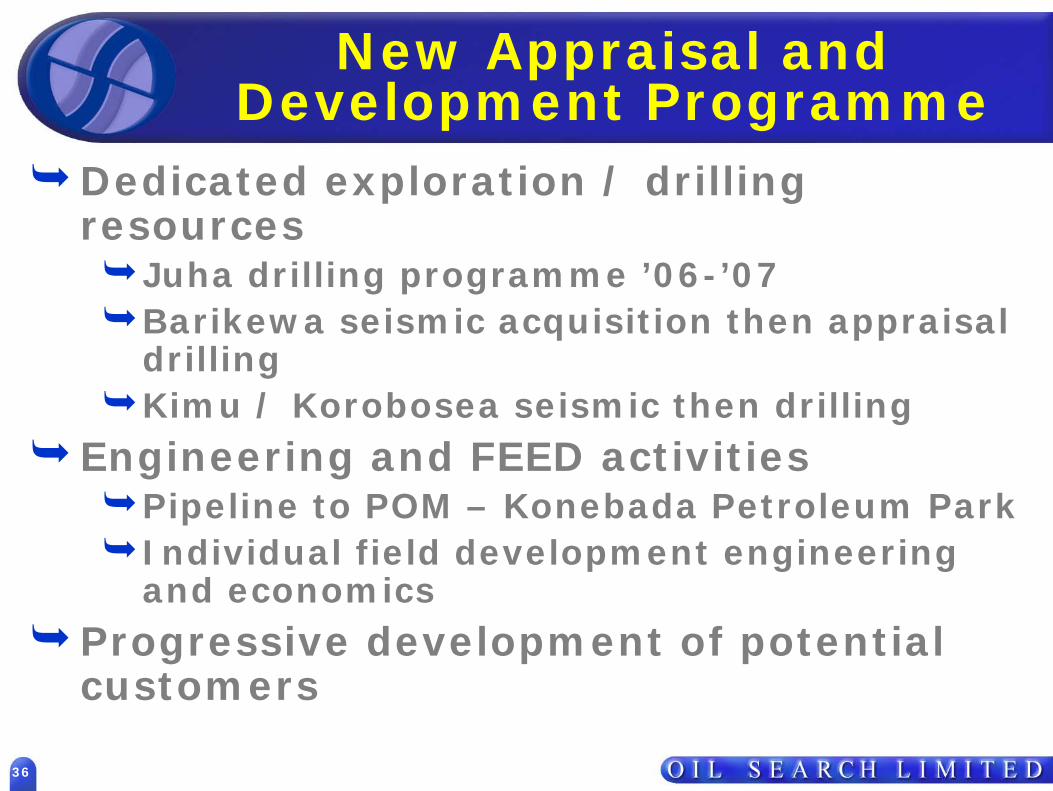

New Appraisal and Development Programme

Dedicated exploration / drilling resources

Juha drilling programme ’06-’07Barikewa seismic acquisition then appraisal drillingKimu / Korobosea seismic then drilling

Engineering and FEED activitiesPipeline to POM – Konebada Petroleum ParkIndividual field development engineering and economics

Progressive development of potential customers

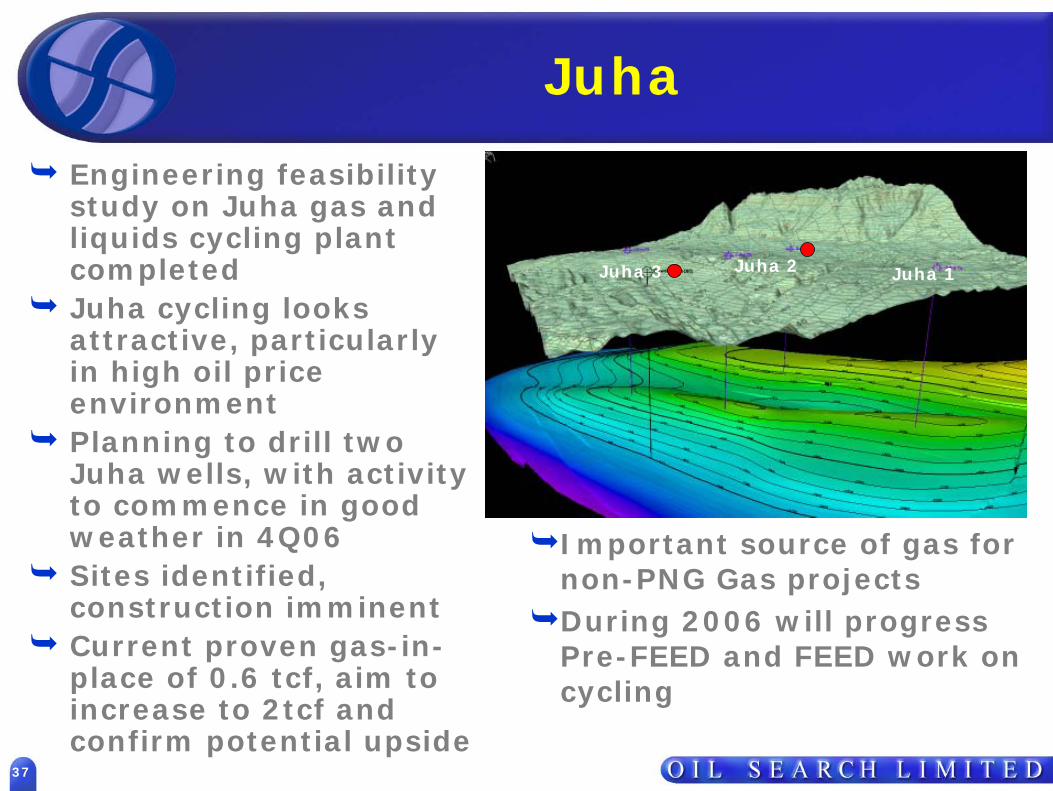

37

Juha

Engineering feasibility study on Juha gas and liquids cycling plant completed Juha cycling looks attractive, particularly in high oil price environment Planning to drill two Juha wells, with activity to commence in good weather in 4Q06Sites identified, construction imminentCurrent proven gas-in-place of 0.6 tcf, aim to increase to 2tcf and confirm potential upside

Important source of gas for non-PNG Gas projectsDuring 2006 will progress Pre-FEED and FEED work on cycling

Juha 3 Juha 2 Juha 1

38

CREATE VALUE

39

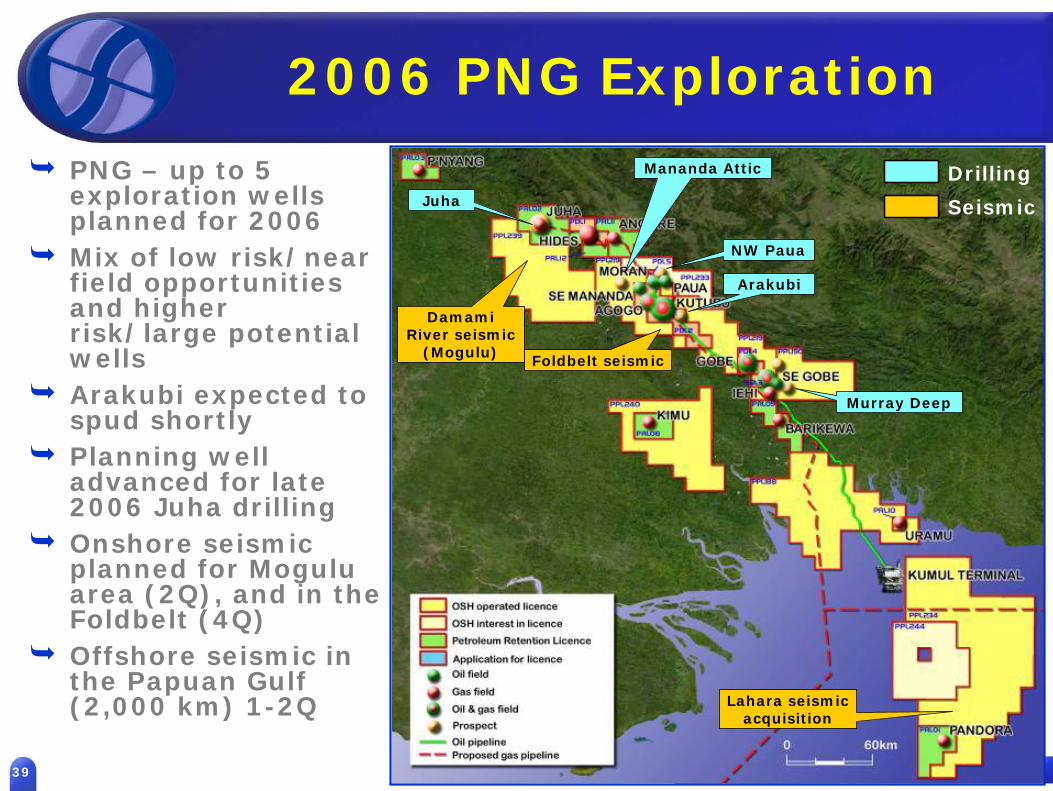

2006 PNG Exploration

PNG – up to 5 exploration wells planned for 2006Mix of low risk/near field opportunities and higher risk/large potential wellsArakubi expected to spud shortlyPlanning well advanced for late 2006 Juha drillingOnshore seismic planned for Moguluarea (2Q), and in the Foldbelt (4Q)Offshore seismic in the Papuan Gulf (2,000 km) 1-2Q

Juha

DamamiRiver seismic

(Mogulu)

NW Paua

Mananda Attic

Murray Deep

Arakubi

Lahara seismic acquisition

Foldbelt seismic

Drilling

Seismic

40

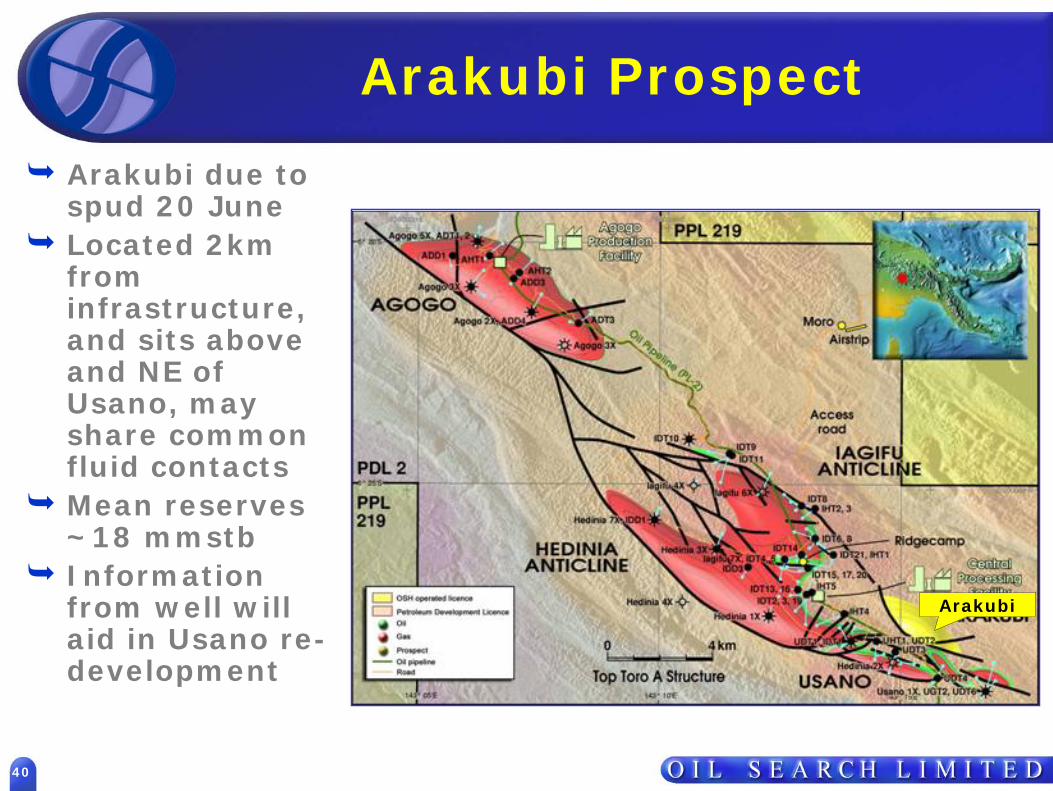

Arakubi Prospect

Arakubi due to spud 20 JuneLocated 2km from infrastructure, and sits above and NE of Usano, may share common fluid contactsMean reserves ~18 mmstbInformation from well will aid in Usano re-development

Arakubi

41

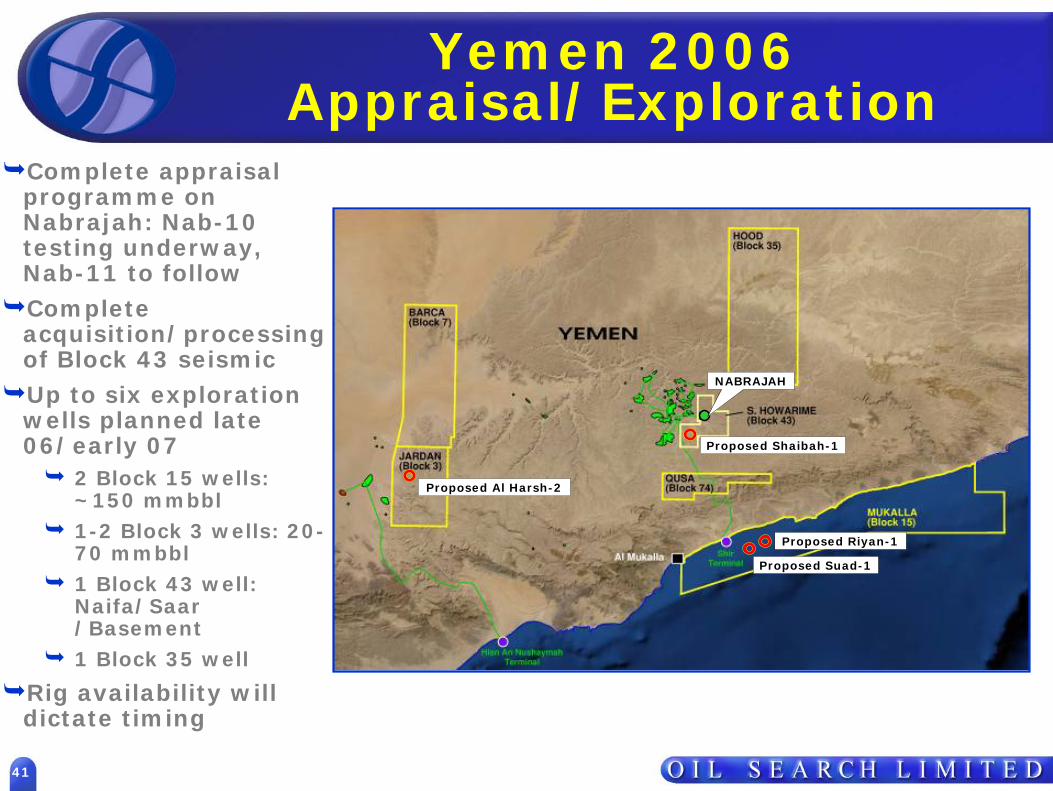

Yemen 2006Appraisal/Exploration

Proposed Al Harsh-2

Proposed Shaibah-1

Proposed Riyan-1

Proposed Suad-1

NABRAJAH

Complete appraisal programme on Nabrajah: Nab-10 testing underway, Nab-11 to followComplete acquisition/processing of Block 43 seismicUp to six exploration wells planned late 06/early 07

2 Block 15 wells: ~150 mmbbl 1-2 Block 3 wells: 20-70 mmbbl1 Block 43 well: Naifa/Saar /Basement1 Block 35 well

Rig availability will dictate timing

42

Egypt & Libya

Egypt - East Ras Qattara3D has substantially increased block potential2 wells commencing 3Q06

Egypt - Area ‘A’15 well/3 years committed development /exploration programmeExploration commences early 2007Focus on prolific Nubian play

Libya - Area 18 : Seismic acquisition during2006, drilling 2007

Further growth optionsbeing pursued in bothEgypt and Libya during2006

Two Wells

Area A

Wadi DaraExploration

Kareem, Yusr, Kheir& Shukheir

Development

Kareem, Yusr, Kheir& Shukheir

Development

Kareem, Yusr, Kheir& Shukheir

Development

Kareem, Yusr, Kheir& Shukheir

Development

Umm El YusrExploration

43

Production Outlook (net)

PNG Gas Project gas

PNG GasProject liquids

Hides

Area 'A', Egypt

Nabrajah Yemen

MoranGobe + SEG

SEM

Kutubu

06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

0

4

8

12

16

20

24

mm

bo

e

Upside from further gas developments 2011 onwards

44

Summary

Capturing latent value in existing portfolio will deliver material growth

Strategic review will set the scene for growth over the next five yearsContinue to optimise existing producing assets, recognising challenges and opportunities presented by high oil price environmentGas – priority is to deliver PNG Gas Project and progress next phase of gas developmentsExploration – mix of low risk/near field opportunities and higher risk/large potential exploration wells, in PNG and Middle East / North Africa. Unhedged exposure to high oil pricesFinancially very strong, with cash of nearly US$500 million

45

O I L S E A R C H L I M I T E D