Embed Size (px)

Citation preview

European Semester Country Report for Greece

European Commission – IOBE conference:

Integrating Greece into the European Semester Policy Framework: Priorities for sustainable growth and

competitiveness

Wednesday, 20 March 2019

Acropolis Museum, Athens

Declan Costello

Mission Chief for Greece

DG ECFIN

Barbara Kauffmann

Director, Employment & Social Governance

DG EMPLCopyright rests with the author. All rights reserved

Outline

2

• 1. European Semester process

• 2. Country Report on Greece (27 Feb)

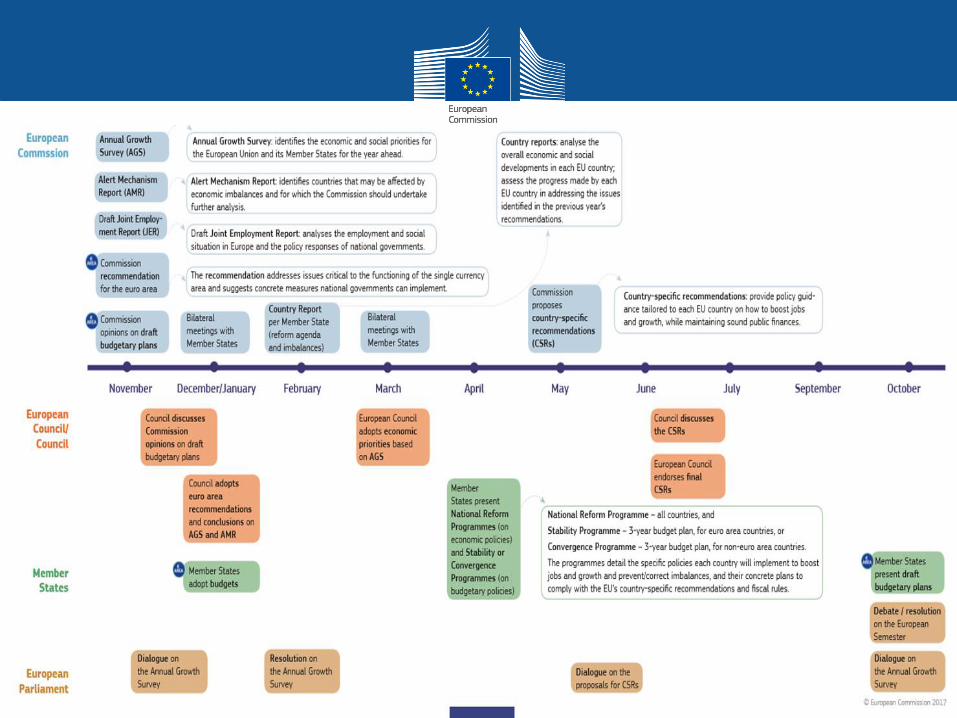

The European Semester: why and how

3

- Introduced in 2010

- Framework that enables EU member countries to:

-A) coordinate their economic policies throughout the year

-B) address the economic challenges facing the EU.

Goals of the European Semester

• ensuring sound public finances

• preventing excessive macroeconomic imbalances in the EU

• supporting structural reforms to create more growth, jobsand social inclusion

• boosting investment

4

21 November 2018 Autumn Package (Annual Growth Survey)

27 February 2019 Winter package (Country reports)

18-22 March 2019 Bilateral meetings with MS

Mid-April 2019 EL presents National Reform Programme

5 June 2019 Spring package (COM adopts CSRs)

Second half of June Discussion on CSRs (EPC, EMCO, EFCA, EFC)

July 2019 Council adopts CSRs

N.B. Dates for adoption of the various packages are indicative

Milestones

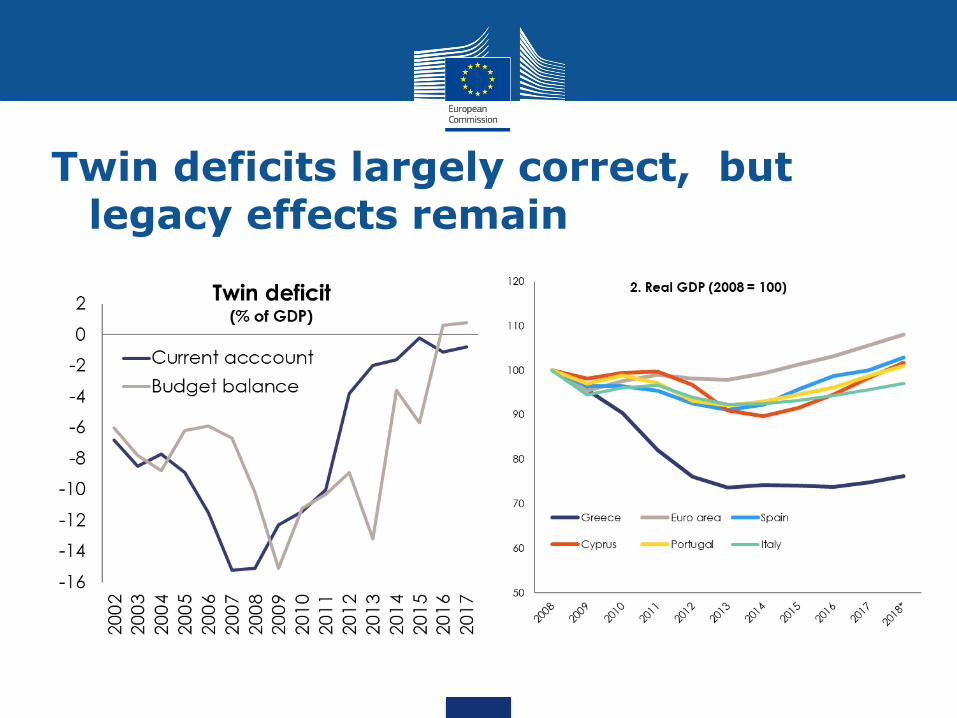

European Semester Winter Package: Main conclusions for the EU (1)

6

Challenges vary significantly across countriesand call for appropriate and determined policyaction:

Some good news… …but challenges ahead

Growing European economy, although at a more moderate pace

Subdued productivity levels

Employment at record high / unemployment at record low

Youth unemployment still unacceptably high in some MSs

Improving public finances overall, though still high debt in some MSs

Intensifying population ageing

Real household income below pre-crisis levels in some MSs

European Semester Winter Package: Main conclusions per Member State

7

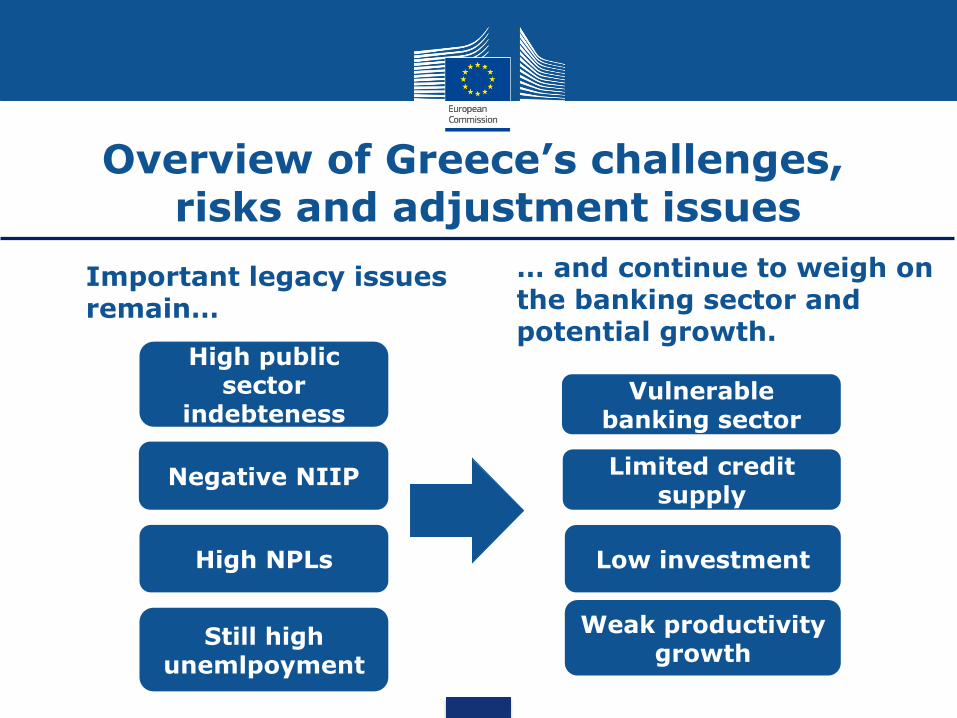

Twin deficits largely correct, but legacy effects remain

Overview of Greece’s challenges, risks and adjustment issues

Important legacy issues remain…

… and continue to weigh on the banking sector and potential growth.

Low investment

Weak productivity growth

High NPLs

High public sector

indebteness

Limited credit supply

Negative NIIP

Vulnerablebanking sector

Still high unemlpoyment

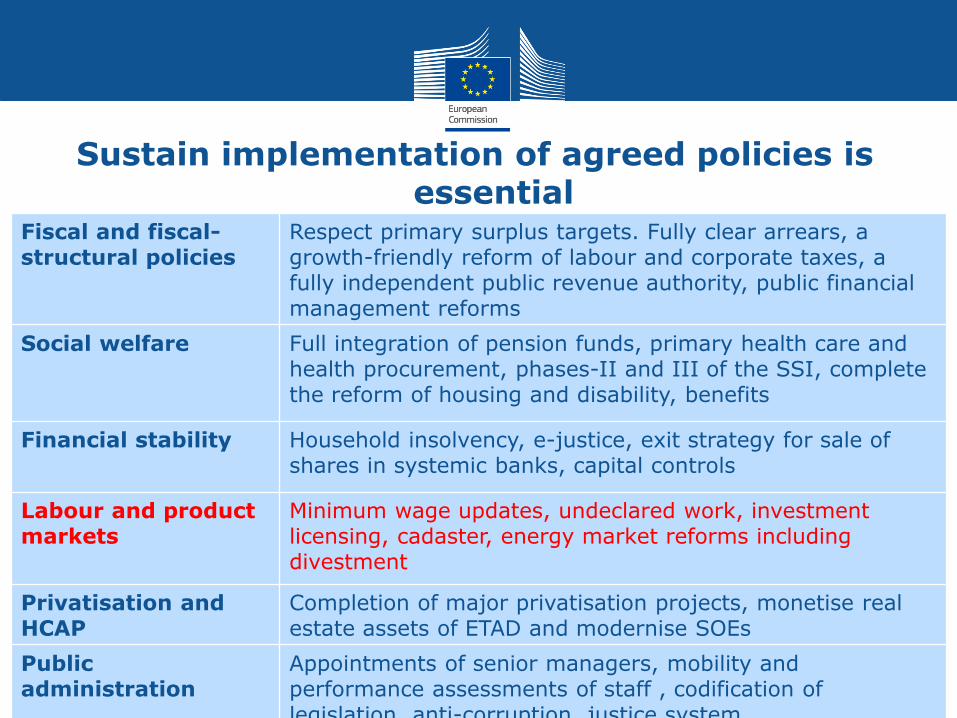

Sustain implementation of agreed policies is essential

10

Fiscal and fiscal-structural policies

Respect primary surplus targets. Fully clear arrears, agrowth-friendly reform of labour and corporate taxes, afully independent public revenue authority, public financial management reforms

Social welfare Full integration of pension funds, primary health care and health procurement, phases-II and III of the SSI, complete the reform of housing and disability, benefits

Financial stability Household insolvency, e-justice, exit strategy for sale of shares in systemic banks, capital controls

Labour and product markets

Minimum wage updates, undeclared work, investment licensing, cadaster, energy market reforms includingdivestment

Privatisation and HCAP

Completion of major privatisation projects, monetise real estate assets of ETAD and modernise SOEs

Public administration

Appointments of senior managers, mobility and performance assessments of staff , codification of legislation, anti-corruption, justice system

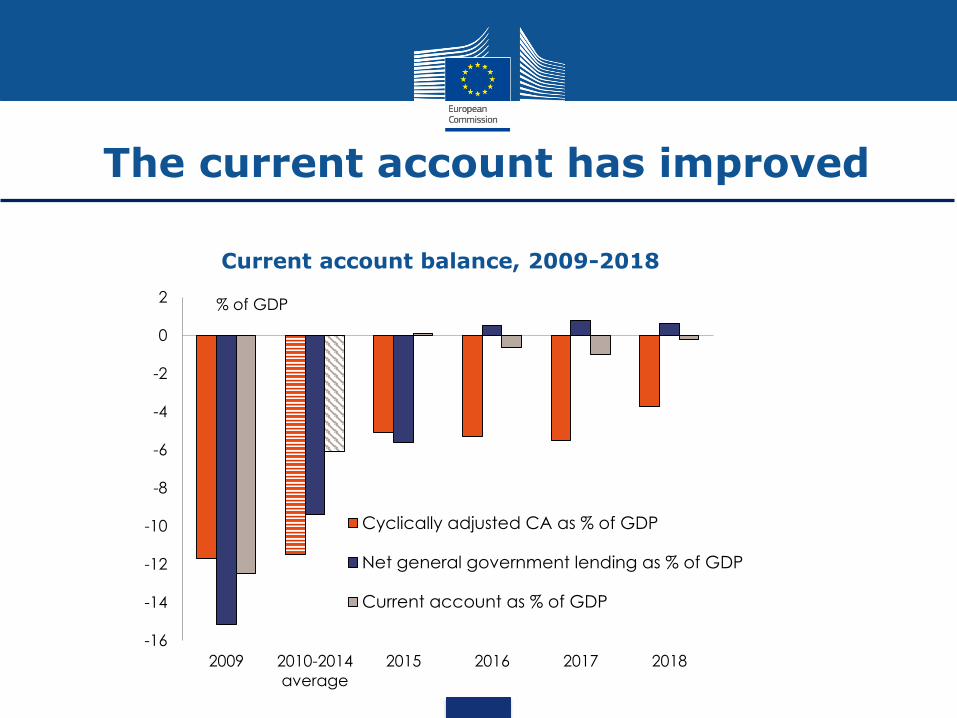

The current account has improved

Current account balance, 2009-2018

-16

-14

-12

-10

-8

-6

-4

-2

0

2

2009 2010-2014

average

2015 2016 2017 2018

% of GDP

Cyclically adjusted CA as % of GDP

Net general government lending as % of GDP

Current account as % of GDP

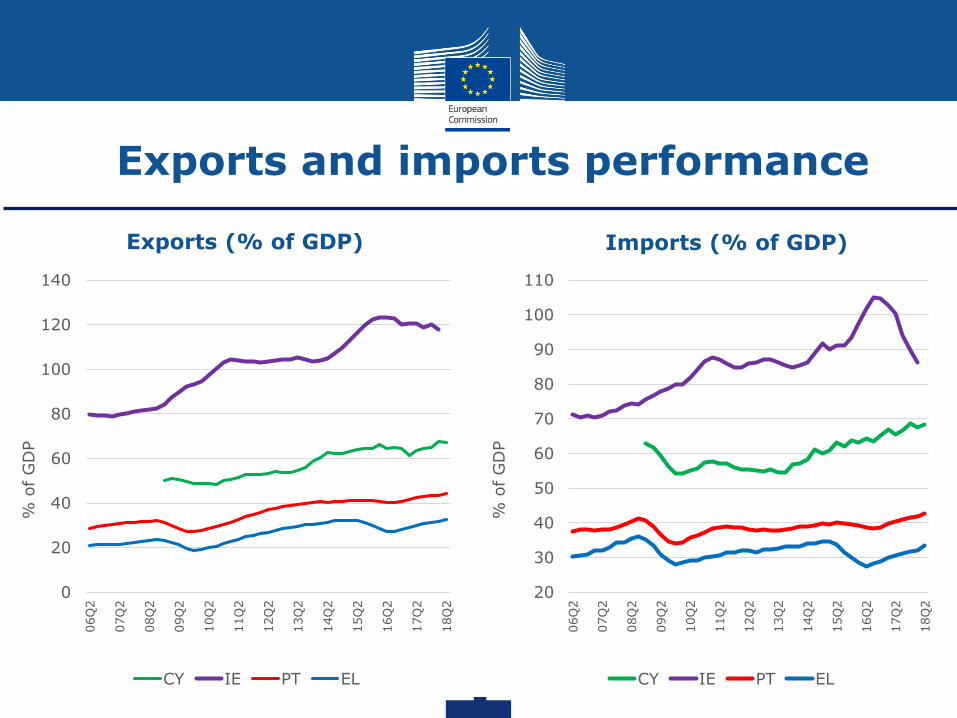

Exports and imports performance

Exports (% of GDP) Imports (% of GDP)

20

30

40

50

60

70

80

90

100

110

06Q

2

07Q

2

08Q

2

09Q

2

10Q

2

11Q

2

12Q

2

13Q

2

14Q

2

15Q

2

16Q

2

17Q

2

18Q

2

% o

f G

DP

CY IE PT EL

0

20

40

60

80

100

120

140

06Q

2

07Q

2

08Q

2

09Q

2

10Q

2

11Q

2

12Q

2

13Q

2

14Q

2

15Q

2

16Q

2

17Q

2

18Q

2

% o

f G

DP

CY IE PT EL

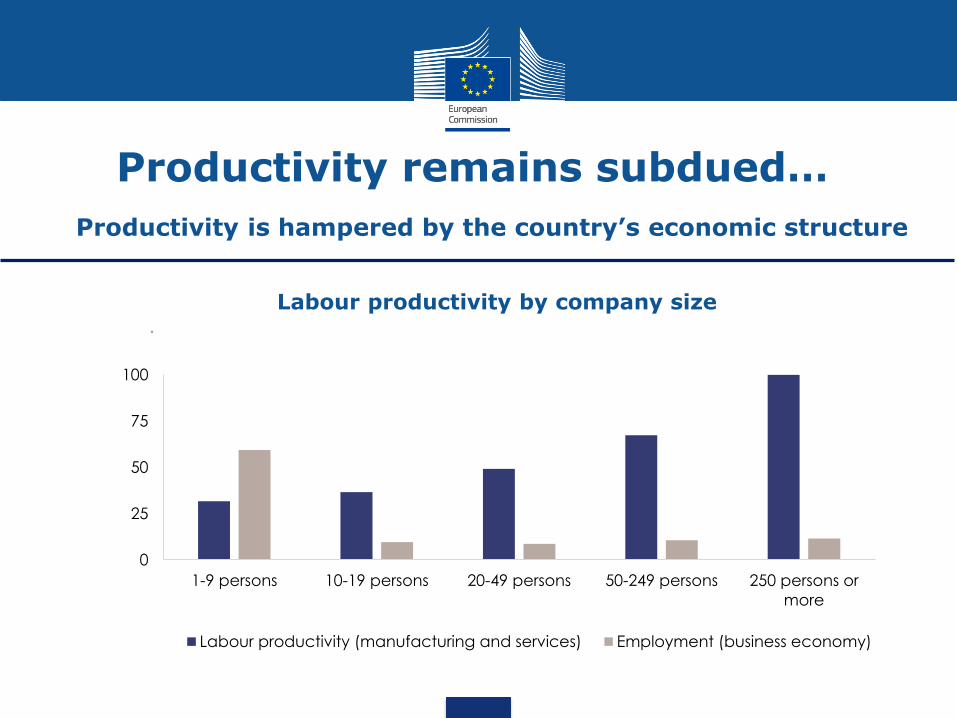

Productivity remains subdued…

13

Labour productivity by company size

Productivity is hampered by the country’s economic structure

0

25

50

75

100

1-9 persons 10-19 persons 20-49 persons 50-249 persons 250 persons or

more

*

Labour productivity (manufacturing and services) Employment (business economy)

14

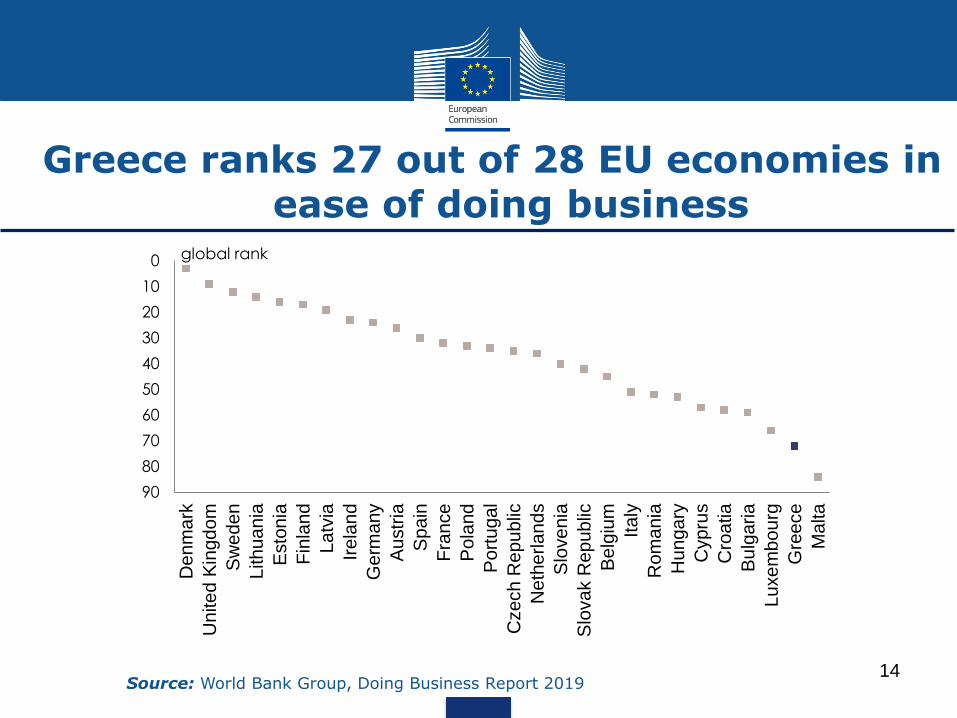

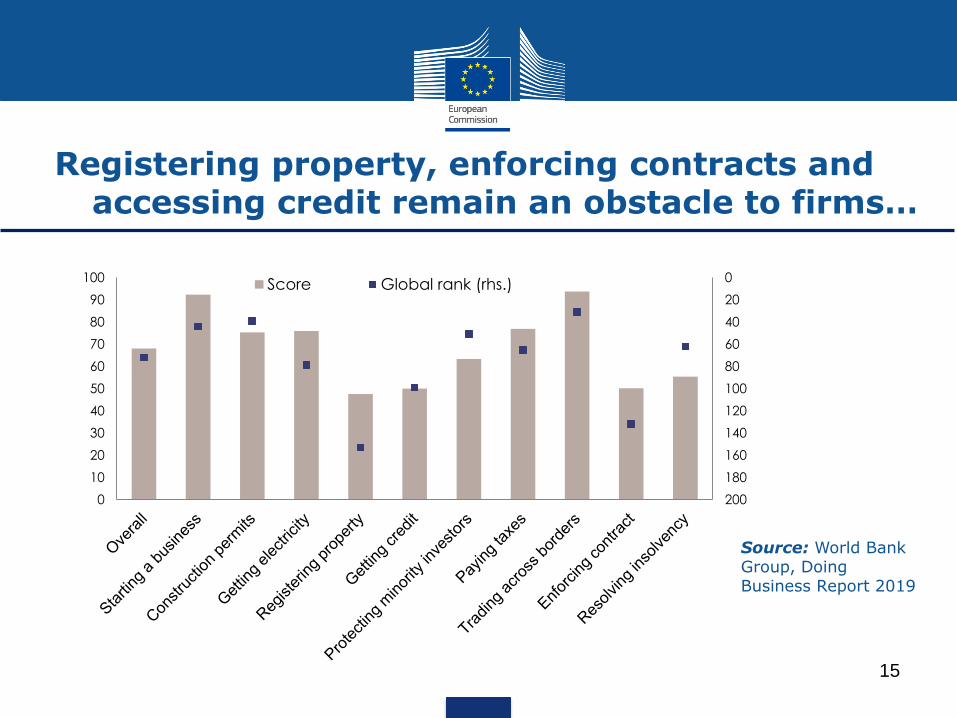

Greece ranks 27 out of 28 EU economies in ease of doing business

0

10

20

30

40

50

60

70

80

90

De

nm

ark

Un

ite

d K

ing

do

m

Sw

ed

en

Lith

ua

nia

Esto

nia

Fin

lan

d

La

tvia

Ire

lan

d

Germ

any

Au

str

ia

Spain

Fra

nce

Po

land

Port

ugal

Czech

Re

pu

blic

Ne

the

rla

nd

s

Slo

ve

nia

Slo

va

k R

ep

ub

lic

Be

lgiu

m

Ita

ly

Ro

ma

nia

Hu

ng

ary

Cypru

s

Cro

atia

Bu

lgaria

Lu

xe

mb

ou

rg

Gre

ece

Ma

lta

global rank

Source: World Bank Group, Doing Business Report 2019

15

Source: World Bank Group, Doing Business Report 2019

0

20

40

60

80

100

120

140

160

180

2000

10

20

30

40

50

60

70

80

90

100Score Global rank (rhs.)

Registering property, enforcing contracts and accessing credit remain an obstacle to firms…

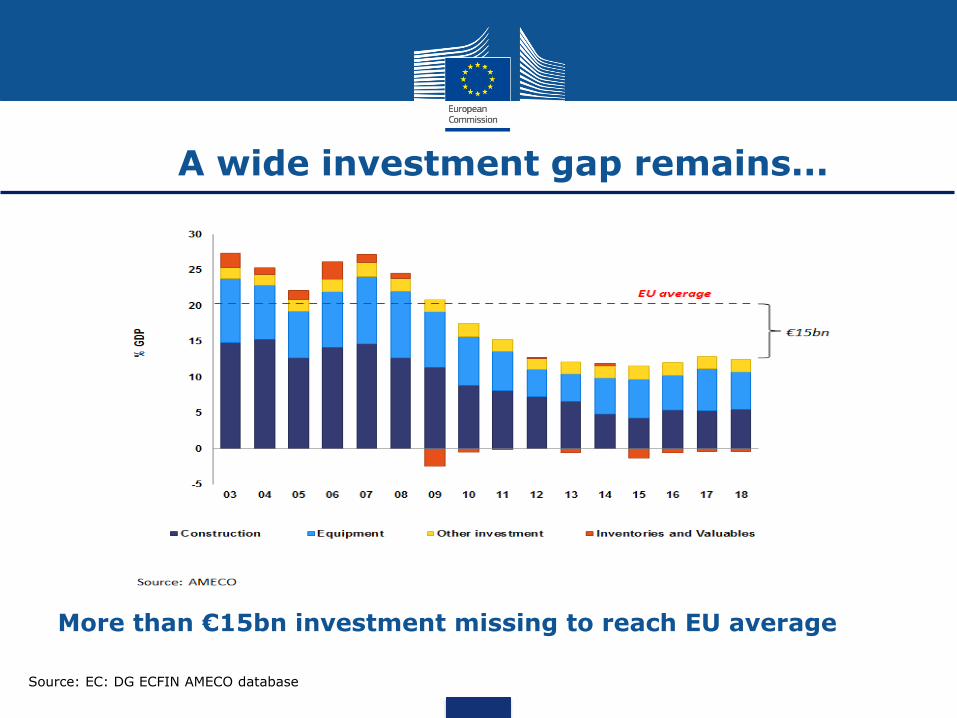

More than €15bn investment missing to reach EU average

Source: EC: DG ECFIN AMECO database

A wide investment gap remains...

Investment opportunities

17

• Investment needs are high & support to growth enablers is needed

• Transport and logistics: ports, completion of the railway axis Patras-Athens-Thessalonica, small port infrastructures, coastal shipping routes

• Energy market: generation, transmission, energy efficiency, innovation

• Public infrastructure: climate adaptation, environmental challenges

• Skills and employability: education, social inclusion, public employmentservice, childcare and long-term care

• Build-up of competitive advantage: agro-food, tourism, health, R&D

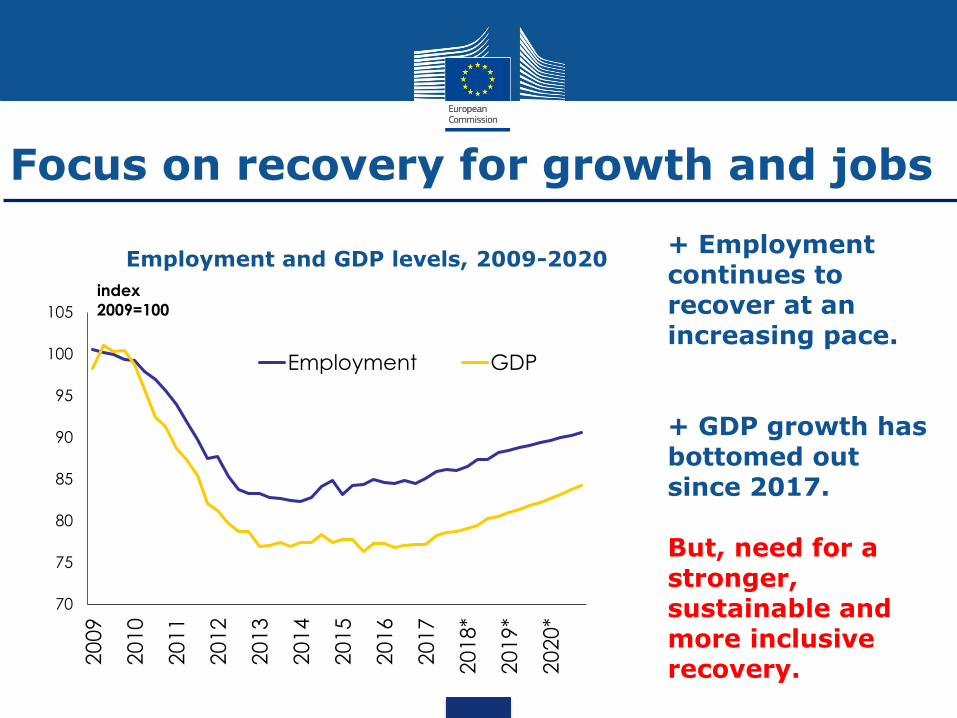

Focus on recovery for growth and jobs

Employment and GDP levels, 2009-2020+ Employment continues to recover at an increasing pace.

+ GDP growth has bottomed out since 2017.

But, need for a stronger, sustainable and more inclusive recovery.

70

75

80

85

90

95

100

105

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

*

20

19

*

20

20

*

index

2009=100

Employment GDP

Source: ELSTAT

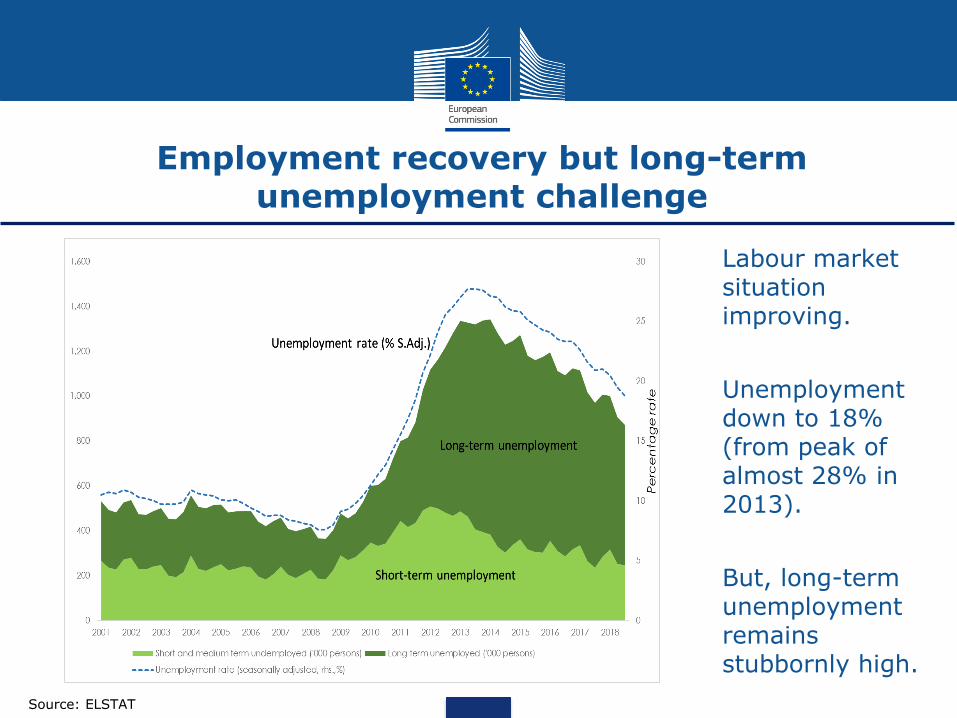

Employment recovery but long-term unemployment challenge

Labour market situation improving.

Unemployment down to 18% (from peak of almost 28% in 2013).

But, long-term unemployment remains stubbornly high.

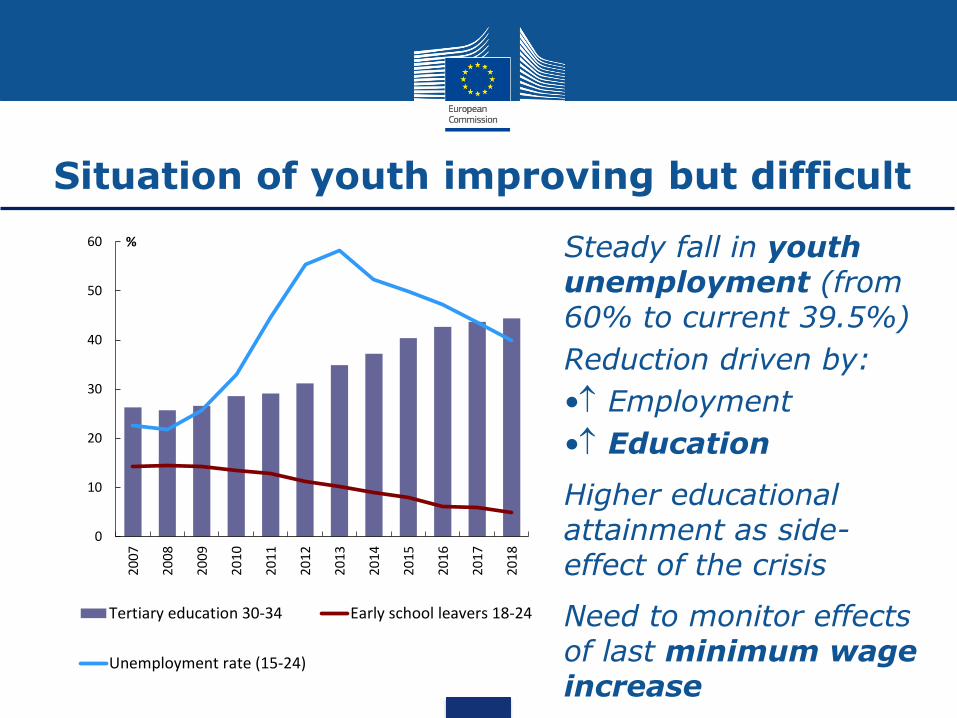

Situation of youth improving but difficult

Steady fall in youth unemployment (from 60% to current 39.5%)

Reduction driven by:

• Employment

• Education

Higher educational attainment as side-effect of the crisis

Need to monitor effects of last minimum wage increase

0

10

20

30

40

50

60

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

%

Tertiary education 30-34 Early school leavers 18-24

Unemployment rate (15-24)

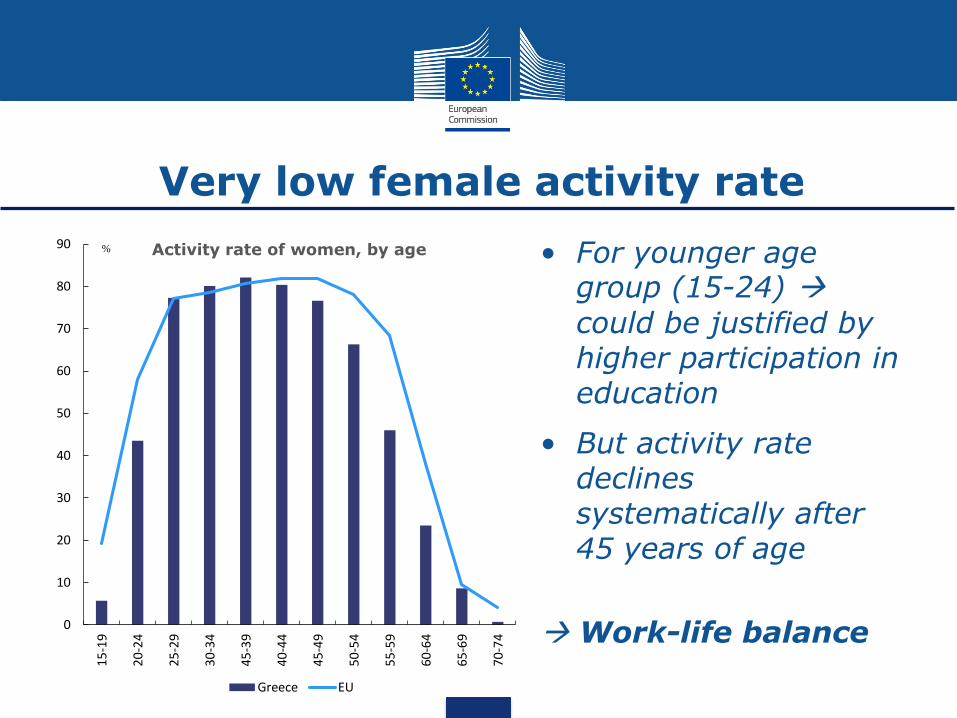

Very low female activity rate

• For younger age group (15-24)

could be justified by higher participation in education

• But activity rate declines systematically after 45 years of age

Work-life balance0

10

20

30

40

50

60

70

80

90

15-1

9

20-2

4

25-2

9

30-3

4

45-3

9

40-4

4

45-4

9

50-5

4

55-5

9

60-6

4

65-6

9

70-7

4

Activity rate of women, by age

Greece EU

%

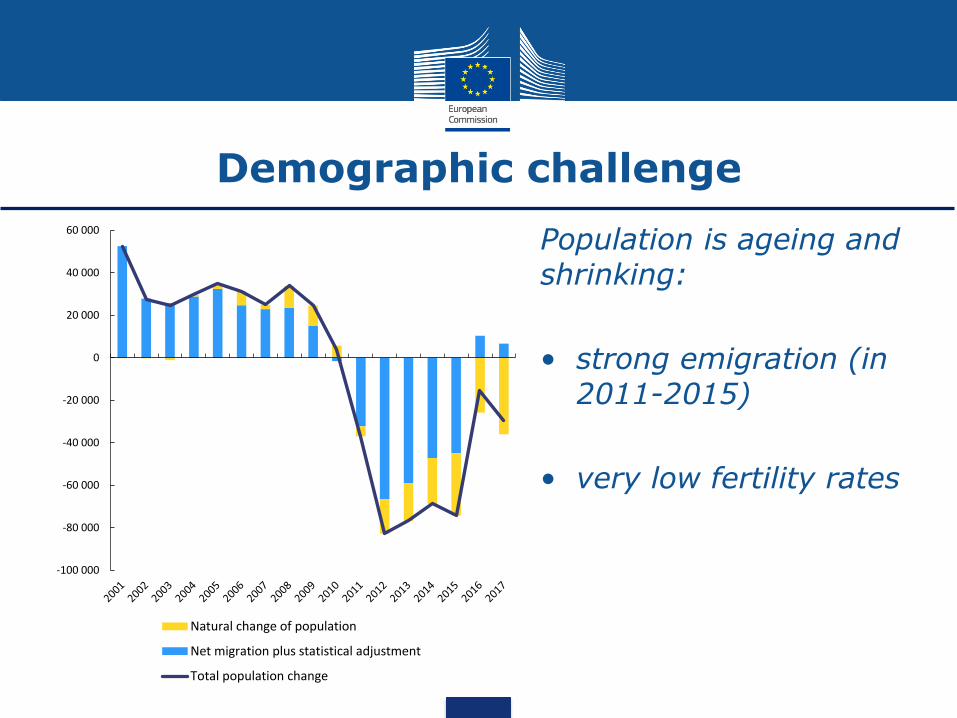

Demographic challenge

Population is ageing and shrinking:

• strong emigration (in 2011-2015)

• very low fertility rates

-100 000

-80 000

-60 000

-40 000

-20 000

0

20 000

40 000

60 000

Natural change of population

Net migration plus statistical adjustment

Total population change

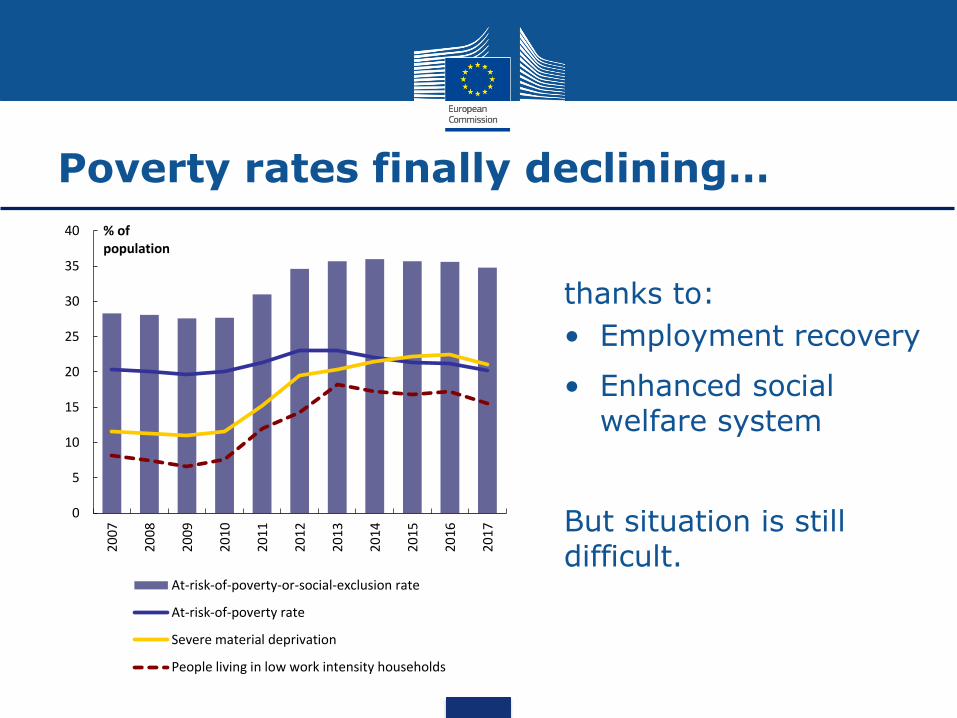

Poverty rates finally declining…

thanks to:

• Employment recovery

• Enhanced social welfare system

But situation is still difficult.

0

5

10

15

20

25

30

35

40

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

% of population

At-risk-of-poverty-or-social-exclusion rate

At-risk-of-poverty rate

Severe material deprivation

People living in low work intensity households

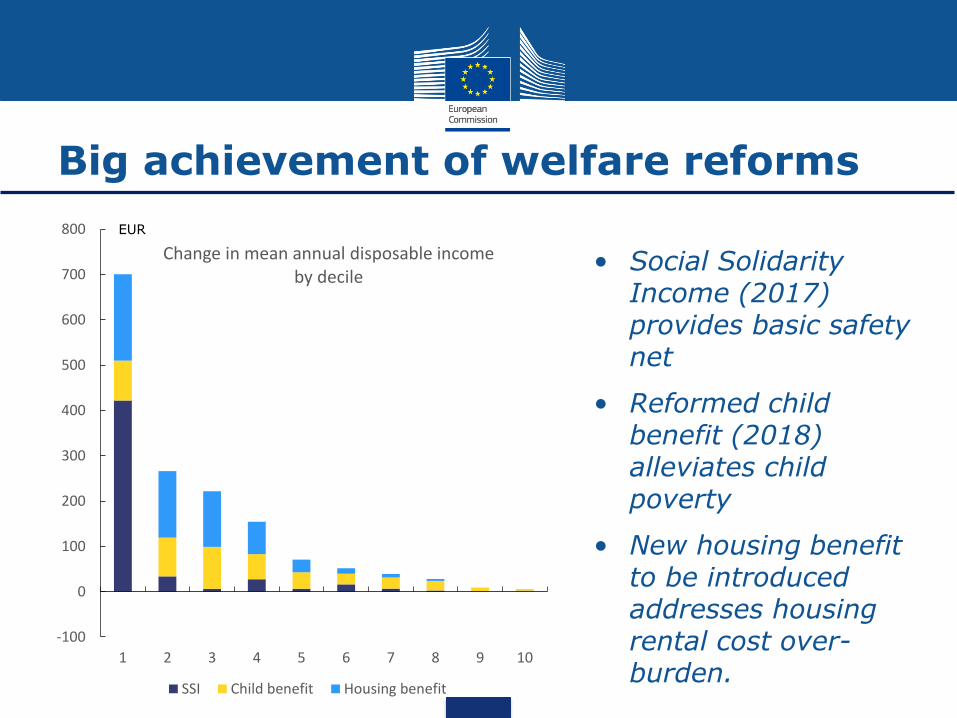

Big achievement of welfare reforms

• Social Solidarity Income (2017) provides basic safety net

• Reformed child benefit (2018) alleviates child poverty

• New housing benefit to be introduced addresses housing rental cost over-burden.

-100

0

100

200

300

400

500

600

700

800

1 2 3 4 5 6 7 8 9 10

Change in mean annual disposable incomeby decile

SSI Child benefit Housing benefit

EUR

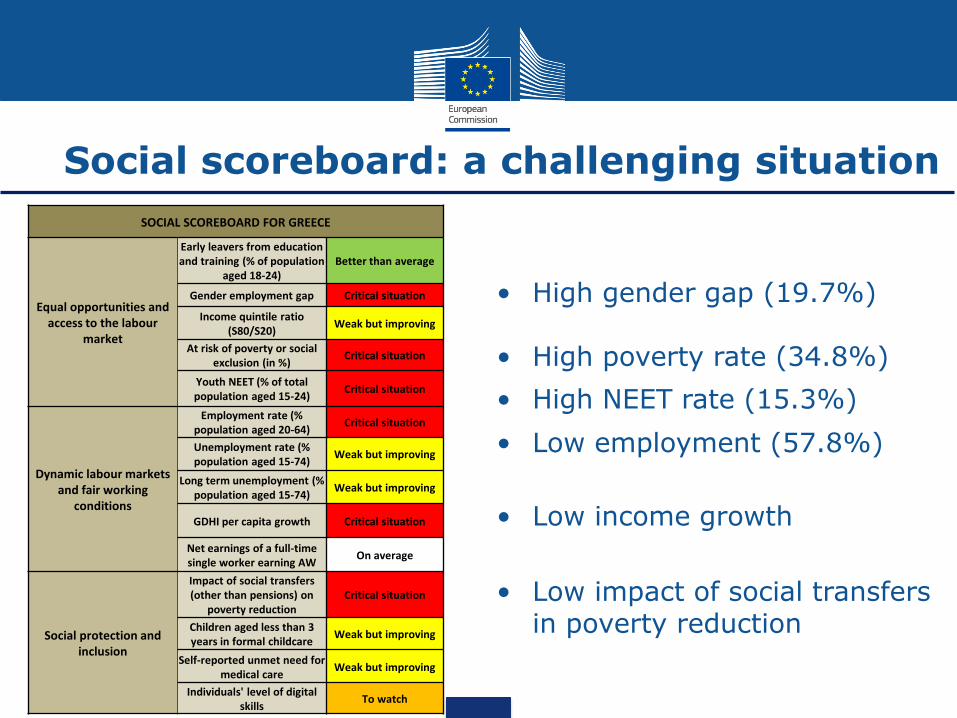

Social scoreboard: a challenging situation

SOCIAL SCOREBOARD FOR GREECE

Equal opportunities and access to the labour

market

Early leavers from education and training (% of population

aged 18-24)Better than average

Gender employment gap Critical situation

Income quintile ratio (S80/S20)

Weak but improving

At risk of poverty or social exclusion (in %)

Critical situation

Youth NEET (% of total population aged 15-24)

Critical situation

Dynamic labour markets and fair working

conditions

Employment rate (% population aged 20-64)

Critical situation

Unemployment rate (% population aged 15-74)

Weak but improving

Long term unemployment (% population aged 15-74)

Weak but improving

GDHI per capita growth Critical situation

Net earnings of a full-time single worker earning AW

On average

Social protection and inclusion

Impact of social transfers (other than pensions) on

poverty reductionCritical situation

Children aged less than 3 years in formal childcare

Weak but improving

Self-reported unmet need for medical care

Weak but improving

Individuals' level of digital skills

To watch

• High gender gap (19.7%)

• High poverty rate (34.8%)

• High NEET rate (15.3%)

• Low employment (57.8%)

• Low income growth

• Low impact of social transfers in poverty reduction

More effective labour market policies

Favourable environment for growth and job creation:

• Well-functioning collective bargaining

• Contrast informality and undeclared work

• Investment in human capital

Policies improving employability and participation:

• Individualised services by the PES, job-matching

• Increased labour market relevance of education

• Improved availability and attractiveness of VET

Proper involvement of social partners in national policymaking needs to be ensured

Concrete actions in line with commitments

Improved support for the unemployed

Modernisation of public employment service

More effective design and delivery of active labour market policies

Full implementation of Action plan to fight undeclared work

On-going modernisation of the social welfaresystem

Completion of setup of single pension fund EFKA

Completion of primary health care system

Completion of the disability benefits

Ευχαριστώ!

28