Embed Size (px)

Citation preview

EuropeanVoice

Sponsored by

Payments: at the heart of the digital economy

CONTENTS

Growing trends...........................................P3Non-cash payments...................................P4Innovation in the payments sector...........P5Interchange fees.....................................P6-7Reform proposals...................................P8-9State of legislation.....................................P9Revision of the payments services directive..................................... P10Security and sharing confidential data..P10Fraud and security.....................................P11SEPA...........................................................P12Financial inclusion....................................P13Conclusions...............................................P14

Publication of this report has been made possible byMasterCard. The sponsor has no control over the content, for which European Voice retains full editorial responsibility.

ACRONYMS

EMV Europay MasterCard Visa – standards for chip and PIN cards

EPC European Payments Council – association of banks and payment service providers responsible for implementing the Single European Payments Area

HAC Honour all cards rule – merchants are required to accept all cards within the same brand regardless of the level of fees

MIF Multilateral interchange fees – fees paid by the merchant’s payment service provider to the cardholder’s payment service provider

MSC Merchant services charge – fee paid by the merchants for use of a payment service provider’s payment services

NFC Near field communication – system which allows contactless payment

NDR No discrimination rule – rule which prevents retailers guiding consumers towards the use of certain payment methods through surcharging, rebates or other methods

PIN Personal identification number – number used to authenticate a user’s identity

PSD Payment services directive – 2007 legislation on creatinga level playing field for payments services

PSDII Term referring to proposals for revision of payment services directive

PSP Payment services provider – company offering payments by credit or debit card, normally a bank

SEPA Single Euro Payments Area – area in which the cost of making transfers in euro is the same for domestic and non-domestic transactions

TPP Third party payment provider – organisation offering payments services which does not directly service the user’s account

Written by Simon TaylorImages: iStock

3

PAYMENTS: AT THE HEART OF THE DIGITAL ECONOMY

Growing trendsMaking payments electronically has become a normal part ofpeople’s everyday lives. Businesses and consumers rely on theability to make payments safely, conveniently and reliably withouthaving to handle notes and coins.

The average value of each card payment transaction in the European Union in 2013 was €49.40; the total value of card payments reached €2.2 trillion in 2013. Electronic payments nowaccount for a growing share of the value of transactions. In the EU,card payments represented 16.5% of all transactions in 2013, according to figures from the European Central Bank (ECB). TheUnited Kingdom, Portugal and Sweden were at the top of theleague, but even in Sweden and Norway, which have the aim of becoming cashless societies, cash is still the most common meansof making payments. In Germany, card payments account for only8% of transactions. The use of cash remains very popular there because of the historical experience of hyperinflation and a fear ofdebt. This tradition comes at a price: a study conducted by Steinbeis University in Berlin estimated that the cost to the German economy of producing and handling cash was €8 billion a year.

In recent years, payments via the internet have grown rapidly as more and more consumers make purchases online. Developments in mobile phone technology and growth in the

ownership of smartphones have boosted mobile-based payments(m-payments), which is the fastest growing payments sector. The value of m-payments worldwide is expected to pass the $234 billion (€186bn) mark this year. In Europe, 23% of electronicpayments were made using smartphones or tablets in the secondquarter of 2014, according to figures from payments processorAyden. In the United States the figure was 17%.

Several companies have emerged in recent years to provide newpayment services offering quick and convenient ways to settletransactions in the digital economy. PayPal was launched in 1998. Itquickly gained popularity as a way of making payments on eBay,the online auction site. It has grown into a company with annualrevenues of $145bn (€116bn); eBay is planning to spin off PayPal asa standalone company this year, reflecting the popularity of itsservice. This year Apple, the consumer electronics company,launched Apple Pay, a payments service on its iPhones.

The proliferation of card-based, internet and mobile systemsdemonstrates the importance of fast, efficient and trustworthypayment systems for the global digital economy. This report examines innovation in the payments sector and assesses howthe regulatory environment in the EU affects the development ofcompetitive services.

GreeceBulgaria Romania

Lithuania HungaryPoland

Germany

ItalyCzech Republic

SpainAustriaCroatia

Eurozone Slovenia

Latvia Malta

LuxembourgSlovakia

EU Netherlands

IrelandBelgiumCyprusEstoniaFinlandFrance

DenmarkSwedenPortugal

United Kingdom 34.77

33.89

24.72

22.14

20.2920.47

21.28

16.60

16.84

18.6919.39

13.4613.77

14.46

14.64

15.2916.49

13.19

8.22

10.62

10.66

12.04

4.42

7.998.00

8.16

8.17

8.31

3.16

4.34

Value of transactions as a ratio to GDP(percentages; total for the period)

Source: ECB

4

E-payments and m-payments: M-payments are expected to register rapid growth as people makegreater use of tablets and smartphones to manage transactions.According to the World Payments Report 2014, m-payments areforecast to grow by 60.8% in 2015. The growth rate in e-payments(payments made in the e-commerce market) will be lower at 15.9%,partly because of a migration of e-payments to mobile devices.

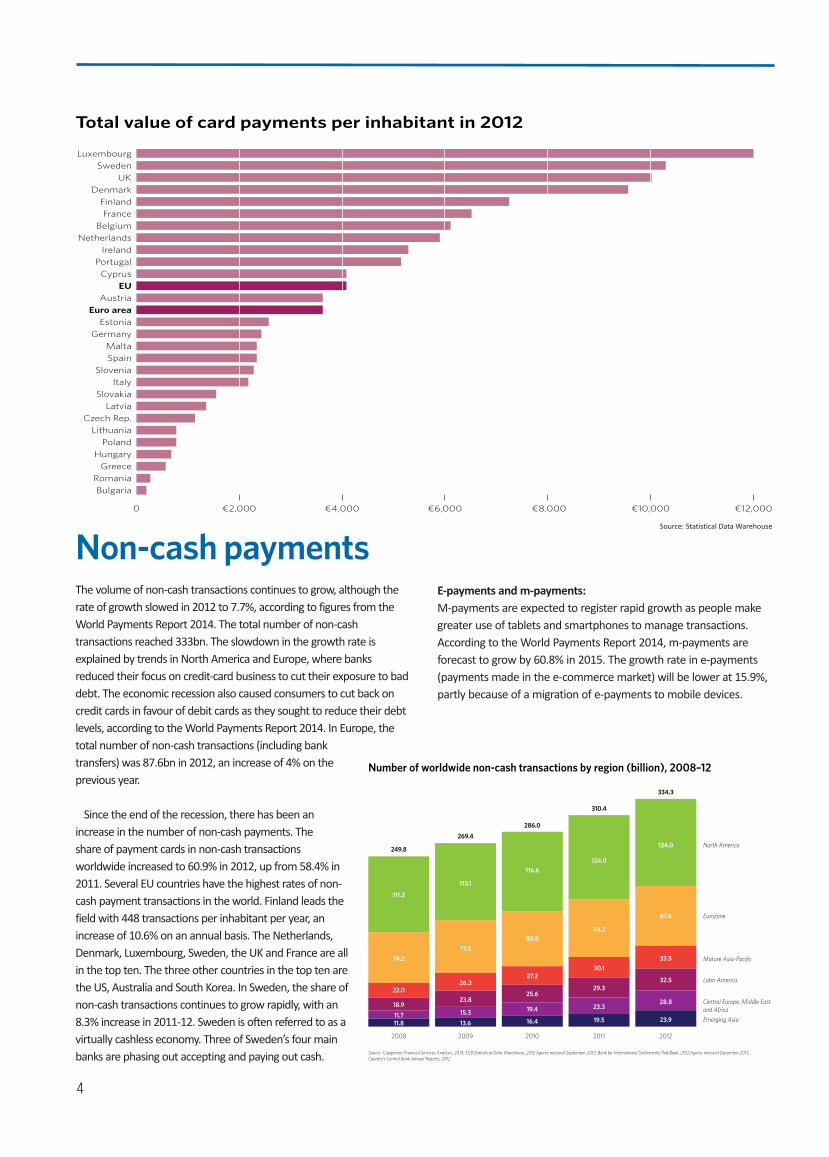

The volume of non-cash transactions continues to grow, although therate of growth slowed in 2012 to 7.7%, according to figures from theWorld Payments Report 2014. The total number of non-cashtransactions reached 333bn. The slowdown in the growth rate isexplained by trends in North America and Europe, where banksreduced their focus on credit-card business to cut their exposure to baddebt. The economic recession also caused consumers to cut back oncredit cards in favour of debit cards as they sought to reduce their debtlevels, according to the World Payments Report 2014. In Europe, thetotal number of non-cash transactions (including banktransfers) was 87.6bn in 2012, an increase of 4% on theprevious year.

Since the end of the recession, there has been anincrease in the number of non-cash payments. The share of payment cards in non-cash transactionsworldwide increased to 60.9% in 2012, up from 58.4% in2011. Several EU countries have the highest rates of non-cash payment transactions in the world. Finland leads thefield with 448 transactions per inhabitant per year, anincrease of 10.6% on an annual basis. The Netherlands,Denmark, Luxembourg, Sweden, the UK and France are allin the top ten. The three other countries in the top ten arethe US, Australia and South Korea. In Sweden, the share ofnon-cash transactions continues to grow rapidly, with an8.3% increase in 2011-12. Sweden is often referred to as avirtually cashless economy. Three of Sweden’s four mainbanks are phasing out accepting and paying out cash.

Non-cash payments

Total value of card payments per inhabitant in 2012

LuxembourgSweden

UKDenmark

FinlandFrance

BelgiumNetherlands

IrelandPortugal

CyprusEU

AustriaEuro area

EstoniaGermany

MaltaSpain

SloveniaItaly

SlovakiaLatvia

Czech Rep.Lithuania

PolandHungary

GreeceRomaniaBulgaria

0 ¤2,000 ¤4,000 ¤6,000 ¤8,000 ¤10,000 ¤12,000

Number of worldwide non-cash transactions by region (billion), 2008–12

11.811.7

18.9

22.0

74.2

111.2

13.6

15.3

23.8

26.3

77.2

113.1

16.4

19.4

25.6

27.2

80.8

116.6

19.5

23.3

29.3

30.1

84.2

124.0

23.9

28.8

32.5

33.5

87.6

124.0249.8

269.4

286.0

310.4

334.3

2008 2009 2010 2011 2012

North America

Eurozone

Mature Asia-Pacific

Latin America

Central Europe, Middle Eastand AfricaEmerging Asia

Source: Capgemini Financial Services Analysis, 2014; ECB Statistical Data Warehouse, 2012 figures released September 2013; Bank for International Settlements Red Book, 2012 figures released December 2013,Country’s Central Bank Annual Reports, 2012

Source: Statistical Data Warehouse

5

PAYMENTS: AT THE HEART OF THE DIGITAL ECONOMY

In the past ten years, the market for electronic payments hasseen an explosion in the development of new services, largelydriven by the growth in e-commerce and the need to makeonline payments. There were 25.4bn e-commerce transactionsworldwide in 2012 and this number is forecast to increase to38.5bn in 2015, according to the World Payments Report 2014.

One of the best-known payment services that has emerged inresponse to the e-commerce boom is PayPal. It was developed in1998 by a group of software designers who were working onsecurity for handheld devices and were looking for a securemeans of transferring funds electronically. PayPal was bought byonline auction site eBay in 2002 and last year it generated 41%of eBay’s revenue, handling €6.6bn in transactions. It has nowmoved into offline payments by offering its payment services inshops, and this year eBay is planning to spin off PayPal as astandalone company. The popularity of the service has beendriven by its electronic wallet function, by which users add fundsto their PayPal account from a credit card or bank account anduse the funds stored with PayPal to pay for online transactionswithout having to enter bank account or credit card details eachtime.

In recent years, a number of other companies have developedelectronic wallet services. One example is Google Wallet, whichwas launched in 2011. It enjoyed an initial surge in users butstruggled to expand its share of the market, partly because ofconsumer concerns about the security of mobile payments.

The next stage of innovation was the development ofcontactless payments that allow card holders to authorisepayments to retailers by passing their cards over a reader ratherthan having to insert the card and type in a personalidentification number. This is known in the US as ‘tap and pay’and works using near-field communication (NFC) technology.One of the challenges for Google Wallet and other earlycontactless systems was that only a limited number of retailersin the US – 220,000, around 10% of all retailers – have had NFCreaders installed, limiting the scheme’s usefulness forconsumers.

Apple Pay, Apple’s payments system, which was launched inthe US on 20 October, is expected to gain a large share of thepayments market in a short time. Apple Pay will benefit from thehuge numbers of Apple product owners and the trust that usershave in the company to win a major share of the electronicpayments market. It is available on iPhone 6, the latest model,Apple Watch and the forthcoming new version of the iPad, givingthe system a potential market of 200 million Apple consumersworldwide. It offers the option of making contactless payments.The scheme is accepted by a number of major US retail chains,including McDonald’s, Walgreens and Subway, although some

Innovation in the payments sector

chains – for example, Walmart, 7-Eleven and Best Buy – havesaid they will not operate the system. According to press reports,Apple Pay is expected to launch in Europe in 2015. Apple isnotoriously coy about the launch dates of its products.

In order to ensure that Apple Pay achieves rapid marketpenetration, Apple has struck deals with the three main creditcard companies, MasterCard, Visa and American Express, tointeroperate with Apple Pay. The companies cover 83% of allcredit card purchases in the US.

PayPal, Google Wallet and Apple Pay have been built on theexisting payment infrastructure established by the major cardcompanies. Carsten Sørensen, a reader in the department ofmanagement at the London School of Economics and PoliticalScience and an expert on digital innovation, says that nopayment scheme can be successful unless it involves cardcompanies. Companies offering payment services prefer to linkup with established payment providers and build their serviceson the back of existing payment infrastructures. Sørensen saysthat Apple Pay will be able to leverage the popularity of Apple’sconsumer products and reinforce their desirability. “It will beanother reason to want to own an iPhone,” he says, referring toApple Pay. The usability of the system will be crucial to its take-up by consumers, as ease of use is the determining factorfor users, he says. He notes that Apple has a track record in“making things easier to use for consumers”.

6

Interchange feesMultilateral interchange fees (MIFs) are central to the card payments industry. They are a major source of revenue for banksissuing payment cards together with annual user fees and the interest earned on credit cards.

Every time a consumer makes a purchase from a retailer using a creditor debit card, the retailer pays a fee to its bank called the merchantservice charge (MSC). The MSC is made up of different elements, whichis determined by banks accepting card payments, such as:

the interchange fee, which is paid by the retailer’s bank to theconsumer’s bank;

a fee paid by the retailer’s bank to the card scheme (Visa orMasterCard or domestic schemes such as Bancontact in Belgium)for using the card;

a fee paid by the retailer to the retailer’s bank for the paymentprocessing services of the retailer’s bank.

The consumer’s bank pays the retailer the price of the itembought minus the interchange fee. The main element of the MSC

is the interchange fee, which is set by the card companies. Banksearn a percentage of the value of each transaction so they havean incentive for the fees to be as high as the market can bear. Ifthey are too high, retailers will refuse to accept card payments.

These arrangements are known as four-party schemes as they involve two banks (the consumer’s bank and the retailer’s bank),the consumer and the retailer. The card companies operate thescheme and make their revenue in fees from banks based on thenumber of cards issued, the volume and value of transactionsmade using the cards.

Three-party cards also exist, where one organisation offers payment services to both the consumer and retailers. This is thestructure used by American Express and Diner’s Club.

In the EU, the level of MIFs varies from member state to member state. In the UK, for example, the rates are around 0.95% of the value of the transaction for a credit-card purchase,according to Europe Economics. Fees in Denmark, Belgium andthe Netherlands are some of the lowest in the EU at around 0.2%for a debit-card payment.

How MIFs work

Source: BEUC* Usually, consumers also pay an annual fee to their bank for using the card – the cardholder fee

A multilateral interchange fee (MIF) is a fee a retailer’s bank must pay to a consumer’s bank for each card payment. MIFs typically involve four parties:

1

23

For every individual card payment the retailer pays a charge to its bank called a Merchant Service Charge (MSC)…

Retailer Retailer’sbank

Customer Customer’sbank

… most of which the retailer’s bank passes on to the consumer’s bank under the name of an MIF

As a result, the final amount received by the retailer is less than the

amount paid by the consumer*

7

PAYMENTS: AT THE HEART OF THE DIGITAL ECONOMY

Retailers complain that MIFs prevent competition in the payments sector by fixing a minimum price for the cost of handling card transactions and by posing obstacles to new entrants. Ruth Milligan, at Eurocommerce, says that when creditcards were first introduced, the interchange fees functioned as incentives to consumers to obtain and use cards. Part of thesefees were used to pay for cardholder rewards such as air miles.“But now everyone has a credit or debit card. The current interchange fee business model has run its course”, she says.

Interchange fees are set by the card companies, and retailersare not able to negotiate to have them lowered. The banks whoissue payment cards have a financial incentive to keep MIFs ashigh as the market can bear and therefore less incentive to workwith other payment-service companies that pay lower fees, retailers argue.

Retailers claim that they would pass on the benefits of lowercosts to consumers in lower prices, although this view is challenged by the card companies who say there is little evidencethat this has happened in countries that have capped fees.

BEUC, the European consumers’ organisation, says that MIFsare a “barrier to competition”. “Several national debit schemeshave disappeared,” says Farid Aliyev, BEUC’s financial services officer, and banks in many countries are reluctant to adopt otherpayment solutions that generate less revenue.

MIFs are a barrier to competition.Several national debit schemeshave disappeared. Banks in many

countries are reluctant to adopt other payment solutions that generate less revenue

Farid Aliyev, financial services officerBEUC, the European consumers’ organisation

Some consumer groups such as BEUC argue that the cost ofMIFs is borne by all consumers, even those who do not havecards, because retailers pass on the cost in the form of higherprices. The card companies argue that interchange fees spreadthe costs of providing payment services among all parties involved: card companies, banks, retailers and consumers. Interchange fees also cover the cost of other services that are essential if consumers are to trust payment systems, such as security precautions and insurance against fraud.

The card companies argue that costs may even rise for consumers if fees are capped, as banks would have to replace the revenue from interchange fees with higher user charges or interest rate increase.

8

include cases where the card-scheme operator used a fourthparty, such as a bank, to market its cards and paid a fee to thebank for doing so. The Commission argues that these aredisguised interchange fees and should therefore be covered bythe caps on fees.

The regulation on interchange fees was published at the sametime as changes were proposed to the EU’s payment servicesdirective, originally agreed in 2007, which aim to foster thecreation of an effective single market for payment services in theEU. The proposed changes would extend existing requirementson security and consumer protection to new payment serviceproviders (see page 10).

The European Commission argued that interchange feesrestricted competition because banks, which issue credit anddebit cards, had no incentive to support new payments schemes.Announcing the proposals in July 2013, Joaquín Almunia, at thetime the European commissioner for competition, said:“Breaking up this cosy system between banks and card schemes

The European Commission investigated interchange fees aspart of an inquiry into retail banking in 2005. After a two-year investigation, the Commission concluded that the feeslimited competition and were a barrier to other paymentservices. Using EU competition law, it ordered credit-cardcompanies to cap the fees at a relatively low level.

MasterCard contested the Commission’s decisions in theEU’s General Court. But the court ruled in 2012 in favour ofthe Commission’s analysis and upheld the decision to capthe level of interchange fees.

In July 2013, the Commission followed up the rulings witha proposed regulation – legislation that is directly legallyenforceable in the EU’s member states – cappinginterchange fees at 0.3% of the transaction value for creditcards and 0.2% for debit cards. The Commission said thatthe caps would save consumers €730 million a year. Three-party schemes would be exempt from the caps on feesunless they resembled four-party schemes. This would

Reform proposals

Use of payment instruments in the EU

Sources: ECB and Statistical Data Warehouse

All cardsCompound annualgrowth rate: 10.2%

Credit transfersCompound annualgrowth rate: 5.1%

Direct debitsCompound annualgrowth rate: 5.5%

ChequesCompound annualgrowth rate -6%

E-moneyCompound annualgrowth rate: 23.1%

40,000

30,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

20,000

10,000

0

9

PAYMENTS: AT THE HEART OF THE DIGITAL ECONOMY

will allow new providers to enter the market.” The Commissionargues that banks and card companies want consumers to usecards with high fees. The cost of these fees is then passed on toconsumers through higher retail prices as retailers seek torecoup the cost of the fees.

Credit-card companies have criticised the proposals for a lackof supporting data to justify capping interchange fees at thelevels proposed and have brought a court case to get theCommission to publish its studies. The Commission has not yetdone so. MasterCard cited a study by the Brattle Group, a macro-economic consultancy, which found that the Commissionhad overstated the degree to which fees should be capped.

The Brattle Group argued that fees should be well over 1%. Daniele Condorelli, an economist at the University of Essex,who has studied interchange fees on behalf of MasterCard, says that the Commission has no empirical evidence thatcapping interchange fees will benefit consumers. “You want to regulate something if there is a market failure. But there is no empirical evidence that the market is notworking well and no evidence capping will work,” he says.Condorelli says that the payments market is highly competitive,as the emergence of services such as BitCoin, PayPal and Apple Pay illustrates.

The Spanish consumer rights organisation ADICAE is alsocritical of the Commission’s approach. Fernando Herrero,ADICAE’s director of communications, points out that cappinginterchange fees does not automatically lower costs forconsumers. He cites the example of Spain, where the cost ofusing credit cards rose in 2005-10 when the governmentbrought in caps on interchange fees. “We saw that the impactof the regulation of interchange fees has consequences: highercosts for consumers for credit and debit cards in the annualfees and the interest rate.” He says the Commission’s proposalsshould have been accompanied by additional measures to limitbanks’ potential to increase other charges.

ADICAE has sent studies of the Spanish situation to theCommission, arguing that there should be measures to preventbanks increasing annual fees and the interest rate charged. TheCommission has responded by saying that because there waslittle competition in the Spanish market for credit and debitcards, it was easier for banks to increase fees charged toconsumers.

Retailers and online merchants such as airlines have sought torecoup some of the cost of interchange fees by adding onsurcharges that are passed on to the consumer. With thecapping of interchange fees, the practice of surcharging will bebanned for all cards covered by the caps.

The Council of Ministers and the European Parliament havebeen examining the Commission’s proposals. The EuropeanParliament has backed the Commission’s approach to capfees, but voted to exclude all three-party schemes from thescope of the regulation that were below a certain marketshare.

The Council also supports the Commission’s approach andexcludes three-party schemes and commercial cards from thescope of the caps unless they are acting like four-partyschemes. Member states can also exclude these schemes ifthey have less than a 5% market share. This would meanAmerican Express would be exempt as it has around 3% ofthe EU cards market and would gain a significant competitiveadvantage over rivals, such as Visa and MasterCard.

MasterCard and Visa argue that three-party schemesshould be covered by the fee caps. Otherwise the number ofthree-party schemes using four-party models would increase.As they tend to have higher fees and charges, the cost toconsumers of using cards will rise, undermining the intendedresult of the regulation. Javier Perez, president of MasterCardEurope, said in June that the proposals “risk playing directlyinto the hands of the most expensive market players”.

Retailers also argue for three-party schemes to be coveredby the regulation. Eurocommerce and the European RetailRoundtable say that exempting these schemes would allowthem to market themselves aggressively as low-cost in termsof upfront fees, but with high hidden fees. Merchants wouldcome under pressure to accept them and their share of themarket would increase, even if their fees are higher thanfour-party schemes covered by the cap.

The Council of Ministers and MEPs aim to reconcile thedifferences between their positions so that the regulationcan be adopted next year.

State of legislation

10

Revision of the payments services directiveThe European Commission published in July 2013 a proposal toupdate the existing law on payment services to take account ofdevelopments in the payments sector, in particular to regulatenew kinds of payment-service providers that have emerged. Themain targets of the proposals are third-party payment providers(TPPs) that provide access to payment accounts indirectly. They include payment-initiation services – such as iDeal, based inthe Netherlands, SOFORT in Germany and Trustly in Sweden –that offer a means of paying for goods and services onlinewithout a debit or credit card. These providers arrange a credittransfer from a user’s bank account to the account of the e-commerce retailer.

When consumers want to make a payment online, they arepresented with a choice of payment service providers. If they opt

When consumers use third-party payment providers, they send information about their bank accounts through those providers.The proposal from the Commission to revise the payment services directive states that “sensitive payment data or personalised security credentials” should not be stored by thethird-party payment provider. The aim is to guard against possible security breaches that would give criminals access todata about clients.

The way in which data is shared with third-party serviceproviders is the subject of heated debate while changes to thepayment services directive are being negotiated.

The European Payments Council (EPC), a body that representsthe European banking industry on payments issues, says thatconsumers should not share their confidential data with a thirdparty, ie, organisations that arenot banks. In the case of iDEAL,an online banking system developed and owned by Dutchbanks, consumers provide theirauthentification data within thebanks’ own online banking system. In iDeal’s view, thisarrangement means that usersdo not have to provide confiden-tial information to a third party.

But not all TPPs conform to thisbank-owned model. Indeed, in2011 the European Commissionlaunched an investigation intowhether the EPC, which draws up

Security and sharing account data

21.3bn

Note: E-commerce includes retail sales, travel sales, digital downloads purchased via any digital channel and sales from businesses that occur over primarily CSource: Capgemini Financial Services Analysis, 2014

2011

25.4bn

2012

29.3bn

2013

34.1bn

2014

38.5bn

2015

Forecast Forecast Forecast

Number of global e-commerce transactions (billions), 2011–15

for a TPP it will use its software interfaces to link banks’ onlinefacilities. To make a purchase, consumers enter their onlinebanking credentials (eg passwords and/or personal identificationnumbers) to approve payment transfers.

The proposals to revise the payment services directive would place TPPs under a legal obligation to meet standards ofsecurity that already apply to traditional payment-serviceproviders. They will be required to guarantee a range ofconsumer rights, including the right to refunds, disputesettlement rules and complaints procedures. The revision alsoproposes standard rules on who has liability in the case offraudulent payments and data breaches. The customer’s firstclaim would be on the banks, which may in turn make claims onthe TPPs.

the rule-books for payment service providers, was trying to exclude competition in the payments sector with a requirementthat all payments systems should be linked to banks. The inquiryhad been triggered by a complaint from SOFORT, a TPP based inGermany. The EPC dropped the requirement in 2013 during thecourse of the Commission’s investigation.

Georg Schardt, deputy chief executive of SOFORT, argues that, even before TPPs come under the remit of the paymentservices directive, his company’s system of security protection is high. Personal authentification data such as log-in details haveto be entered anew by the consumer for each transaction and are not stored by SOFORT. What is stored are the transaction details – IBAN and/or Bic numbers, names, references, amounts.The authentification data are encrypted by SOFORT before beingtransmitted to the consumer’s bank for approval.

Note: E-commerce includes retail sales, travel sales, digital downloads purchased via any digital channel and salesfrom businesses that occur over primarily C2C platformsSource: Capgemini Financial Services Analysis, 2014

11

PAYMENTS: AT THE HEART OF THE DIGITAL ECONOMY

Fraud and security One of the major incentives for consumers and businesses tomake electronic payments is that they avoid the need to handlecash, which carries the risk of loss or theft. But electronic payments are also a target for criminals. Card fraud is a majorproblem for the payments sector and the level of fraud is increasing for online payments. This year criminals hacked thecustomer databases at US retailers Home Depot and Target, andgained access to credit card details of 56 million and 40 millioncustomers respectively. The data breaches are estimated to havecost the companies hundreds of millions of dollars for measuresto protect customers. At Target, CEO Gregg Steinhafel lost his jobover the handling of the breach.

According to figures compiled by the European Central Bank,the level of card fraud within the Single Euro Payments Area(SEPA) increased in 2012 for the first time since 2008, mainly because of higher levels of internet fraud. The total value of cardfraud reached €1.33 billion in 2012, an increase of 14.8% compared to 2011. In 2012, €1 in every €2,635 spent on creditand debit cards issued within SEPA was lost to fraud. That represented 0.038% of the total €3.5 trillion value of transactions,up from 0.036% in 2011. Fraud in cases where the card was notphysically present (ie, for telephone or internet payments) accounted for 60% of the total value of fraud, an increase on 56%in 2011. The volume of payments where the card is not presenthas been increasing in the past few years and rose by 15%-20% ayear from 2008-12.

Ajay Bhalla, president, enterprise safety and security at MasterCard, says: “Not only are retailer data breaches rising, butthey are becoming larger in scale.” He points out that technologymaking fraud possible is becoming more sophisticated and criminals are using it. Retailers are working more closely withbanks to tackle fraud, he says.

Johannes Kleis, a spokesman at BEUC, the European consumers’association, says: “Card payments over the internet are a huge security issue.” Fears about fraud and the safety of online payments are deterring consumers from making more purchasesonline. A Eurobarometer opinion poll carried out for the EuropeanCommission in May-June 2013 on cyber-security found that themisuse of personal data and the security of online payments werethe two biggest concerns of people making online purchases.

Fraud involving cards being used in shops and in cash dispensers has declined because of technological changes in recent years. Magnetic strips in cards have been replaced by chips, and cardholders are required to enter personal identification numbers (PINs) to validate transactions. Chip andPIN technology has been developed using the EMV standard,which refers to the consortium of three card companies responsible (Europay, MasterCard and Visa). By the end of 2010,

around 90% of all transactions in retailers and 80% of all payments cards in the EU were EMV-compliant. Fraud in caseswhere the card was present (ie, in cash machines and in shops)fell in 2012 compared to the year before, according to the ECB.Fraud involving cards is higher in the US because the chip and PINsystem is not as common as in Europe.

Ensuring that consumers feel that they can make online payments without fear of fraud is crucial if the e-commerce sector is to continue to grow. To improve security of online payments, banks and card scheme operators have introduced additional measures such as requiring extra forms of authentication like text messages or a card reader that generatesan encrypted authentication code. However, often this means atrade-off between ease of use and higher security measures. Ifthe additional security measures slow down the paymentprocess, consumers will be put off.

Biometric technologies offer one way to improve security protection while ensuring that payments remain quick and easy.Zwipe, a Norwegian company, has developed a fingerprint readerthat can be incorporated into payment cards or attached to payment terminals in shops. The system is currently being tested inNorway and the company hopes that it will become operational in2015. The system’s great advantage is that it is quicker than the existing chip and PIN system: it takes three to four seconds to approve a payment compared to 30 seconds for chip cards.

12

The Single Euro Payments Area (SEPA)The introduction of the euro in 1999 was meant to deliver savingsfor business and consumers as they would no longer have to paytransaction costs for making payments and transfers within theeurozone. But the architects of the euro realised that consumersand businesses would not enjoy these savings if banks and otherfinancial institutions continued to charge more for non-domestictransactions than for domestic equivalents.

From 2003, EU legislation banned banks from charging more forcross-border transactions than they would charge for domesticones.

To make the process of making transfers and payments withinthe EU as simple as possible, the EU has created a Single EuroPayments Area (SEPA). The deadline for ensuring that credittransfers and direct debits comply with SEPA rules was put back

Number of card payments per inhabitant in 2012

Source: Statistical Data Warehouse

SwedenDenmark

FinlandUK

EstoniaNetherlandsLuxembourg

FrancePortugalBelgium

EUIreland

EurozoneLatvia

SloveniaAustria

SpainCyprus

LithuaniaGermany

MaltaPoland

SlovakiaCzech Rep.

ItalyHungaryRomania

GreeceBulgaria

230224

213167

159158

156129

115111

7978

7063

6258

5248

4439

383232

3028

2777

4

to August this year after it became clear that the initial February2014 deadline would not be met. The later deadline has beenmet.

The ECB is concentrating on implementing SEPA for cards. A report published by the ECB in April showed that there is potential for growth in card use in the EU. This is illustrated bythe wide discrepancy between the use of cards in different EUcountries. The average Swede makes 230 card payments a yearwhile Bulgarians, Romanians and Greeks make on average fewerthan ten payments.

The ECB has supported the European Commission’s proposalson interchange fees and the revision of the payments services directive as a way of harmonising the rules for payment servicesand the business practices of payment service providers.

13

PAYMENTS: AT THE HEART OF THE DIGITAL ECONOMY

Financial inclusionAs the European economy relies less and less on cash, the abilityto make electronic payments becomes ever more essential if people are to participate fully in society. To take one example, inSweden, which has become a virtually cashless society, most public toilets require an electronic payment card.

There are an estimated 2.5 billion people worldwide who donot have access to bank accounts – 44 million in the US alone.Electronic payments offer a means of bringing financial servicesto people who do not usually have access to banks and bank accounts. In African countries, the M-Pesa system, launched byVodafone and Safaricom, provides banking and payment servicesvia mobile phones. Users register their phones at a mobile phoneshop or retailer and top the phone up with funds by exchangingcash for electronic money. The funds can be sent by mobilephone and the recipient can redeem the electronic money forcash at an M-Pesa agent.

The scheme – launched in Kenya in 2007 (pesa is the Swahiliword for money) and since extended to Tanzania, Afghanistan,

South Africa and India – has 18 million users. This year M-Pesahas been introduced in Romania, its first incursion into Europe.

Pre-paid cards are another means of providing payment services to people who do not have access to bank accounts.Funds such as welfare benefits and pension payments are transferred from governments directly onto cards and can thenbe used to pay bills and perform other financial transactions thatrequire electronic payment. The use of these cards helps to ensure that social payments are spent appropriately.

The EU has approved legislation to give all citizens access topayment accounts. The rules, approved in April, aim to ensurethat, even if they are not citizens of the country in which theylive, people have access to accounts that can be used for basic financial services, such as receiving salaries, pensions and welfarepayments and paying utility bills.

The rules include requirements on the transparency of fees sothat people can choose the best-value provider.

14

PAYMENTS: AT THE HEART OF THE DIGITAL ECONOMY

Conclusions The degree of technological innovation in the payments sector overthe past ten years has been phenomenal. Where once shoppers had to run their credit cards through a card-reader and sign a slip of paper, the advent of chips in cards led first to the use of personalised identification numbers. Near-Field Communicationtechnology now means that payments can be made by passingcards over a card-reader. Buying goods and services online has beenmade quick and convenient by the development of systems such asPayPal and Amazon’s One-Click functionality.

The crucial elements for successful payments systems are security,ease of use and availability. Consumers need to know that their accounts are protected from attempts to defraud. They need to beable to make payments in what they consider a reasonable periodof time. And they need to be able to use the payment methodwherever they are.

Modern electronic payment systems go a long way to meet thesecriteria. The launch of Apple Pay in the US and its probable launch inEurope next year will probably lead to further improvements in userexperience.

But in the EU, the reality of a single payments market for retailtransactions is still some way off. Consumers stick with domesticpayment schemes that they know and trust. Popular national payment schemes include Bancontact in Belgium, Giro in Germanyand Dankort in Denmark. The goal of EU-wide competition amongpayments systems is still to be achieved. In some countries,schemes have had a hard time dislodging domestic services. In others, domestic schemes have withered.

The EU has taken steps to boost competition in the payments sector and to create a level playing-field among the different typesof payment providers. One of its main targets has been interchangefees, which are set by card companies or domestic schemes andwhich generate revenue for the banks issuing credit and debit cards.The Commission argues that interchange fees prevent competitionamong payment service providers because banks have limited

incentive to work with low-cost schemes and lose the income frominterchange fees.

The card companies argue that capping fees will not necessarilylead to lower costs for consumers. Charges may even rise if certaintypes of cards, such as American Express, are excluded from thecaps and the cost of using cards in the form of user fees and interestcharges increases.

Interchange fees have proved to be a reliable source of income forthe card companies. In some EU countries, such as the Netherlandsand Denmark, non-card payment schemes have built up a large shareof the domestic market. This is because they are cheap or free to use,convenient and reliable. Few of these have managed to expand theirservices outside their home market. This suggests that there is not yeta competitive single market for payment services in the EU.

The European Central Bank estimated that processing retail payments can cost as much as 1% of gross domestic product or€130 billion a year. A competitive payment sector would have significant economic benefits and would contribute significantly toexploiting the potential of e-commerce and the digital economy.The Commission estimates that capping interchange fees will saveconsumers €730 million a year.

The emergence in the payments sector of new services and technological innovations has, over recent years, been striking. Inthe context of the arguments over card fees, that innovation hasbeen cited as evidence that the European market is competitive,but the card-fees discussion perhaps poses the wrong questions, orthe right questions in the wrong order. The truth is that the European market is still in formation. For the most part, the marketsare still national and some of them are still dominated by nationalpayment schemes, while others are more open to new entrants. Ifthe benefits of technological innovation are to be taken up and applied across the EU, and if European consumers are to avail themselves of a richer variety of services, then Europe needs bothmore competition and greater market integration.

EuropeanVoiceEuropean Voice.Dénomination sociale: EUROPEAN VOICE SA. Forme sociale: société anonyme. Siège social: Rue de la Loi 155, 1040 Bruxelles. Numéro d’entreprise: 0526.900.436 RPM Bruxelles.

© 2014 European Voice All rights reserved.

Neither this publication nor any part of it may be reproduced, stored in a retrieval system, ortransmitted in any form by any means, electronic, mechanical, photocopying, recording orotherwise, without prior permission. Whilst every effort has been taken to verify the accuracy of this information, neitherEuropean Voice nor its affiliates can accept any responsibility or liability for reliance by anyperson on this information.