Embed Size (px)

Citation preview

Evaluating Employee Benefits

Presented by William HallTaylor Insurance Services

March 18th, 2008

Proprietary and Confidential, Taylor Insurance Services

Goals and Agenda

1. Section 125 Administration2. Open Enrollment Practices3. Supplemental Insurance

Section 125 Plans

Proprietary and Confidential, Taylor Insurance Services

Section 125 Plan Employer Savings

Section 125 of the IRS code allows employers to deduct certain insurance premiums on a pre-tax basis, thus lowering the federal, state and local income taxes for both the employer and the employee. These tax savings can help defray the cost of insurance premiums.

Employer SavingsAvg Monthly Pre-tax Deductions $ 300.00# of Employees 300Total Pre-tax Deductions $90,000.00Employer FICA rate 7.65%Total Pre-tax Employer Savings $ 6876.00Total Employer Annual Savings $82,512.00

Proprietary and Confidential, Taylor Insurance Services

Section 125 Plan Employee Savings

Employee Savings After tax Pre Tax

Gross Monthly Salary $ 3,000.00 $3,000.00

Avg Monthly Pre-tax Deductions $ - $ 300.00

Taxable Monthly Salary $ 3,000.00 $2,700.00

State and Federal Income Tax @ 28% $ 840.00 $ 756.00

FICA Tax @ 7.65% $ 230.00 $ 207.00

Gross Take-Home pay $ 1,930.00 $1,737.00

After Tax Deductions $ 300.00 $ -

Net Take Home Pay $ 1,630.00 $1,737.00

Monthly employee increase in net pay $ - $ 107.00

Proprietary and Confidential, Taylor Insurance Services

Section 125 Plan Administration

1. Do you currently have your Section 125 Summary Plan Documents at your office?

2. Are you currently distributing Section 125 Summary Plan Descriptions to all employees during new employee orientations and open enrollments?

3. Are you completing discrimination testing on an annual basis?

4. Do you currently have on file (electronic or paper) signed documents (deduction election forms, choose not to participate, etc.) for all employees?

Open Enrollments

Proprietary and Confidential, Taylor Insurance Services

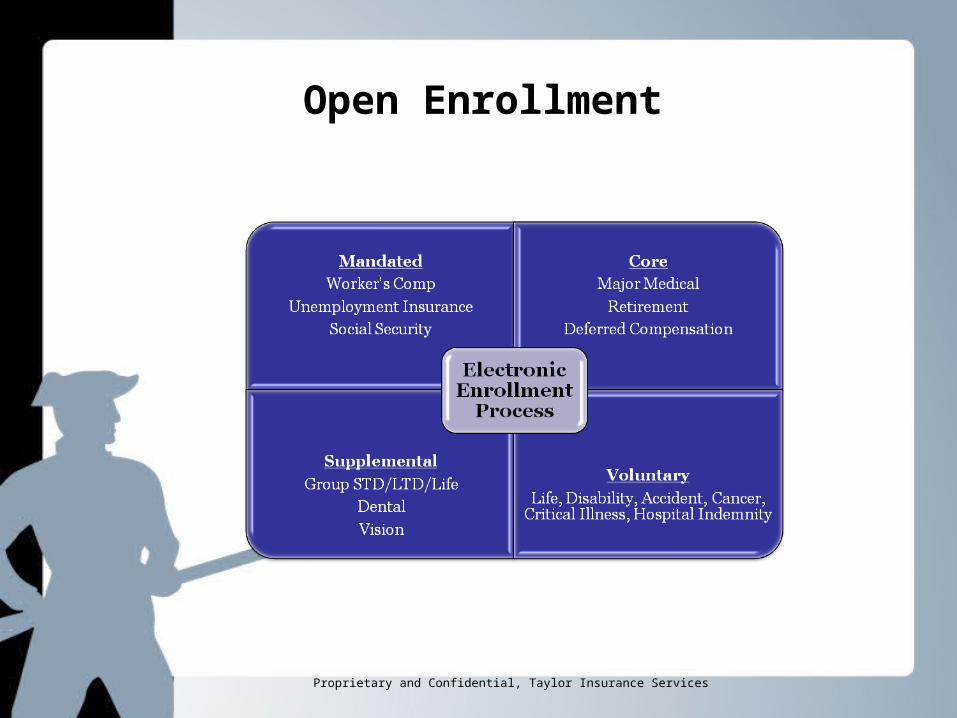

Open Enrollment

The enrollment process is designed around the Circle of Benefits: mandated, core, supplemental and voluntary. The Circle is designed to communicate to your employees the importance of a well-rounded benefits package. It is also designed to help your employees learn about the financial contribution the company is making towards their welfare.

When employees understand the value of a well-rounded benefits package, they are better equipped to make informed decisions. The open enrollment/benefit communication process is designed to show your employees how to protect the most valuable asset they have: their lives.

The enrollment process is recommended for all new employees during employee orientation and annually during open enrollment.

Proprietary and Confidential, Taylor Insurance Services

Open Enrollment

Proprietary and Confidential, Taylor Insurance Services

Electronic Enrollments

Your Electronic Enrollment should have unlimited flexibility to perform the following tasks:

Enrollment SetupSupport open

enrollment, new hire enrollment or

qualified status changes.

Administrator Tools

Monitor enrollment status and history; EOI

tracking and mgmt; customizable reports; 24

hour online access.

EmployeeComplete printout of

“Hidden Paycheck” and “Benefits Summary”

BrandingCan be branded and

customized according to employer’s specs, including logo’s.

Data IntegrationRegularly updates

employee information to most back office

HRIS/payroll systems.

Proprietary and Confidential, Taylor Insurance Services

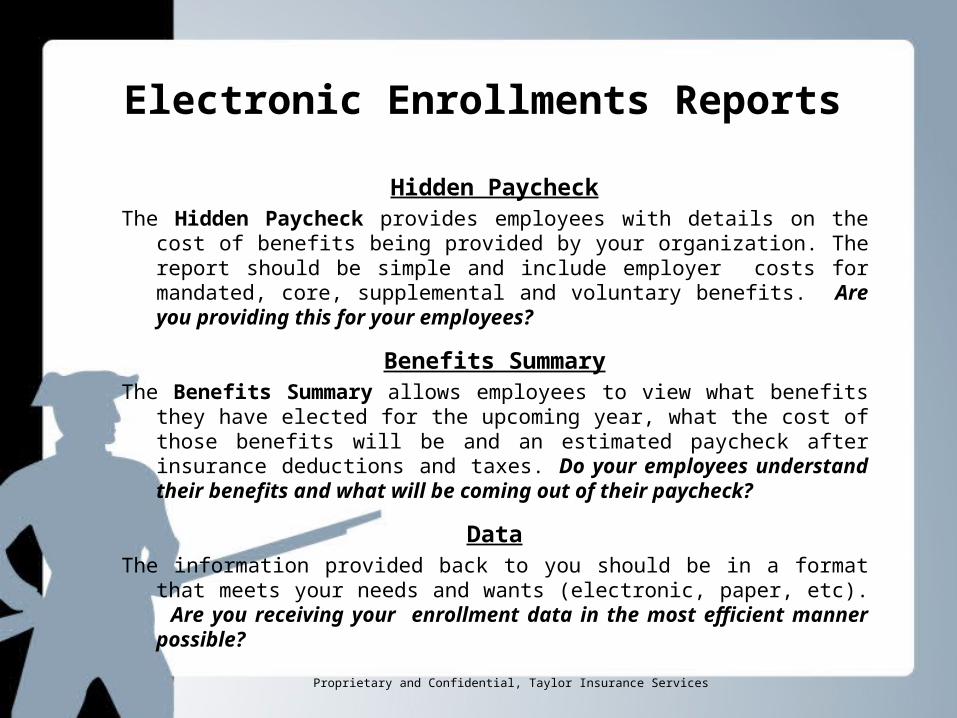

Electronic Enrollments Reports

Hidden PaycheckThe Hidden Paycheck provides employees with details on the cost

of benefits being provided by your organization. The report should be simple and include employer costs for mandated, core, supplemental and voluntary benefits. Are you providing this for your employees?

Benefits SummaryThe Benefits Summary allows employees to view what benefits

they have elected for the upcoming year, what the cost of those benefits will be and an estimated paycheck after insurance deductions and taxes. Do your employees understand their benefits and what will be coming out of their paycheck?

DataThe information provided back to you should be in a format that

meets your needs and wants (electronic, paper, etc). Are you receiving your enrollment data in the most efficient manner possible?

Proprietary and Confidential, Taylor Insurance Services

Make Open Enrollment Fun

Benefit fairs and/or employee appreciation days are a great way to kick off your annual open enrollment. They create a festive mood for employees who may be experiencing low morale due to market changes, economic downturns, anxiety over potential layoffs, etc.

Employee Benefits

Proprietary and Confidential, Taylor Insurance Services

Supplemental Insurance

Supplemental insurance: Innovative, voluntary insurance products that typically pay benefits directly to insured independently of any other benefits.

Why does supplemental coverage exist? Because employees want first dollar coverage but employers can no longer afford to give first dollar, comprehensive coverage to all employees. The result is a pleasant compromise where employees buy what they need, and the employer makes it available to them.

As with any type of insurance, the first rule for supplemental insurance is to choose a reputable carrier. Use AM Best or Standard and Poor’s to check the financial stability of a company.

The second rule is to customize your benefits package to meet your employee’s needs.

Proprietary and Confidential, Taylor Insurance Services

Group vs. Individual

Individual– Fully underwritten;– Plans are typically modular…customizable to meet individuals

needs;– Always portable without rate increases.– Can be offered under Contingent Guaranteed Issue

underwriting.

Group– Guaranteed issue upon first enrollment;– Rates are typically lower due to standardization of benefits and

pricing associated with a specific group of people;– Benefits are usually not portable but if they are, there is usually

a rate increase;– Group benefits always seek to coordinate with other benefits,

so that the coverage you think you are buying may not be what actually pays out.

Proprietary and Confidential, Taylor Insurance Services

Individual Supplemental Insurance

Permanent Life

Insurance

CancerInsurance

Term Life Insurance

Critical Illness

Insurance

Hospital Indemnity Insurance

Heart/Stroke

Insurance

Disability Insurance

Accident Insurance

Proprietary and Confidential, Taylor Insurance Services

Group Supplemental Insurance

Group Life Insurance

Group LTD

Dental VisionLong Term

Care

Mini-medical

Group STD

Proprietary and Confidential, Taylor Insurance Services

Group Life Insurance

• Group Life Insurance– Typically offered as employer paid or employee paid or both and

is guaranteed issue. • Can be offered as a multiplication of the employee’s salary

(anywhere from 2x to 5x income) with a ceiling for the guaranteed issue benefit. Can also be offered as a set amount ($20,000, $30,000, etc).

• Is usually inexpensive coverage but rates increase as the insured get’s older

• Coverage can made available for spouses and dependants.

Proprietary and Confidential, Taylor Insurance Services

Individual Life Insurance

• Designed to supplement the group life insurance that is usually offered by employers. Based on models offered by government after 9/11, most Americans are under-insured. The current recommended model is 5-10 times annual income.

• May be offered on a Contingent Guaranteed Issue basis, allowing employees to enjoy the guarantee issue underwriting features on an individual, portable policy.

Proprietary and Confidential, Taylor Insurance Services

Individual Life Insurance

• Whole Life Insurance: Equity is developed in the policy by diverting a portion of the premiums into a cash fund that can be used as collateral for a loan. Policy typically endows at age 100. Expensive policies where rates can be guaranteed to age 100. Inflexible death benefit.

• Universal Life Insurance: Equity is built in the policy by investing a portion of premiums in managed investments with a guaranteed minimum return on investment from 3-5.5%. Death benefit is flexible. Rates can be guaranteed. This is designed to change with a person as their needs change throughout their life while providing certain of guaranteed features.

• Term: Equivalent to renting a house because you have no equity in the policy. You buy coverage for a certain period of time (10, 20 or 30 years). Very inexpensive and premiums are guaranteed during the term of the policy, however, rates will increase when the insured renews after the Term period.

Proprietary and Confidential, Taylor Insurance Services

Disability

• Why?– Disability is designed to protect the most valuable asset that

we have:

Your Ability To Earn An Income

• Types– Short Term Disability: Income protection that will cover up

to 60% of an employee’s income. Shorter elimination periods with benefit periods typically up to two years. Can be offered under a group or individual basis.

– Long Term Disability: Income protection that will cover up to 60% of an employee’s income. Elimination periods start at 3 months and can last to age 65. Typically offered under group coverage.

Proprietary and Confidential, Taylor Insurance Services

Specified Disease

• Why?– Cardiovascular Disease is the #1 killer of Americans.– 1 out of 2 men and 1 out of 3 women will be diagnosed

with cancer in their lifetime.

• Cancer– Typical policy pays an initial diagnosis up to $20,000

plus indemnifies the insured for specific occurrences.• $100 annual wellness benefit• Hospital confinement, surgery, chemo/radiation, blood

transfusions, new & experimental drugs, ICU, stem cell transplants, etc.

• Critical Illness– Can have a guaranteed issue feature;– Provide up to $50,000 lump sum benefit;– Provides a lump sum payment for heart attack, stroke,

cancer, Alzheimer’s, By-pass surgery & Renal failure.

Proprietary and Confidential, Taylor Insurance Services

Accident

• Why?– One in 8 people in the US sought treatment for an injury in 2007.

• Features:– Indemnifies the insured for “First dollar expenses” associated

with unforeseen accidents. There are a variety of reimbursement features including initial medical expenses, short term disability, broken bone benefits, surgical benefits, hospital confinement, ambulance charges and more.

– Can be used to supplement the increasing deductibles and co-pays that are a result of increasing major medical costs.

Proprietary and Confidential, Taylor Insurance Services

Hospital Indemnity

• Why?– The average for 1 day in the hospital in the US is $3,700. With a

$500 deductible and 80/20 plan, the employee’s portion of costs would be an average of $1140.

• Features:– Indemnifies the insured for “First dollar expenses” associated

with a hospital.– Typically provides initial hospitalization benefit, in and out

patient surgery benefits, doctor visits and daily room and board benefits.

– Typically covers maternity.

Proprietary and Confidential, Taylor Insurance Services

Dental / Vision• In some cases, dental and vision are included in major medical.

– Restricts the flexibility for an employee to customize their benefits.– Benefits are typically not as rich as individual plans.– Numerous “hidden costs” can adversely affect major medical rates.

• Dental– Covers dental charges up to and including exams, x-rays, extraction,

dentures, surgery and orthodontics. Provider networks are available but the insured can typically use any dentist that they choose. Can feature a combination of co-pays and deductibles plus co-insurance.

• Typically has the highest employee satisfaction rating of all supplemental benefits.

• Recent innovations have enhanced this benefit include Dental rewards

• Vision– Covers vision charges up to and including exams, lenses, frames,

contacts and can sometimes offer discounts for laser surgery. True vision plans are typically offered with a provider network but there are reimbursement plans available. Can feature a combination of co-pays and deductibles plus co-insurance.

• Very high satisfaction rating from employees.

Proprietary and Confidential, Taylor Insurance Services

Supplemental Insurance

Allstate Products UnderwritingIn addition to flexible products, Taylor Insurance Services was

instrumental in the development of the Simplified Contingent Guaranteed Issue underwriting program at Allstate. Basically, this program allows almost all of our Individual Supplemental Benefits to be issued based on 3 questions:

1. Do you work at least 20 hours per week?2. Have you been diagnosed with Aids/HIV?3. Have you been hospitalized in the last 6 months?

Questions?