Embed Size (px)

Citation preview

Evasion of Revenue

in State of Assam

O/o Pr. Accountant General (A&E), Assam

At Guwahati on Feb. 2, 2015

Our Treasury Inspection Mandate

Art. 149 of Constitution

S. 18 (1)(a)

CAG’s (DPC) Act

Challan

The Portions of a Challan Form

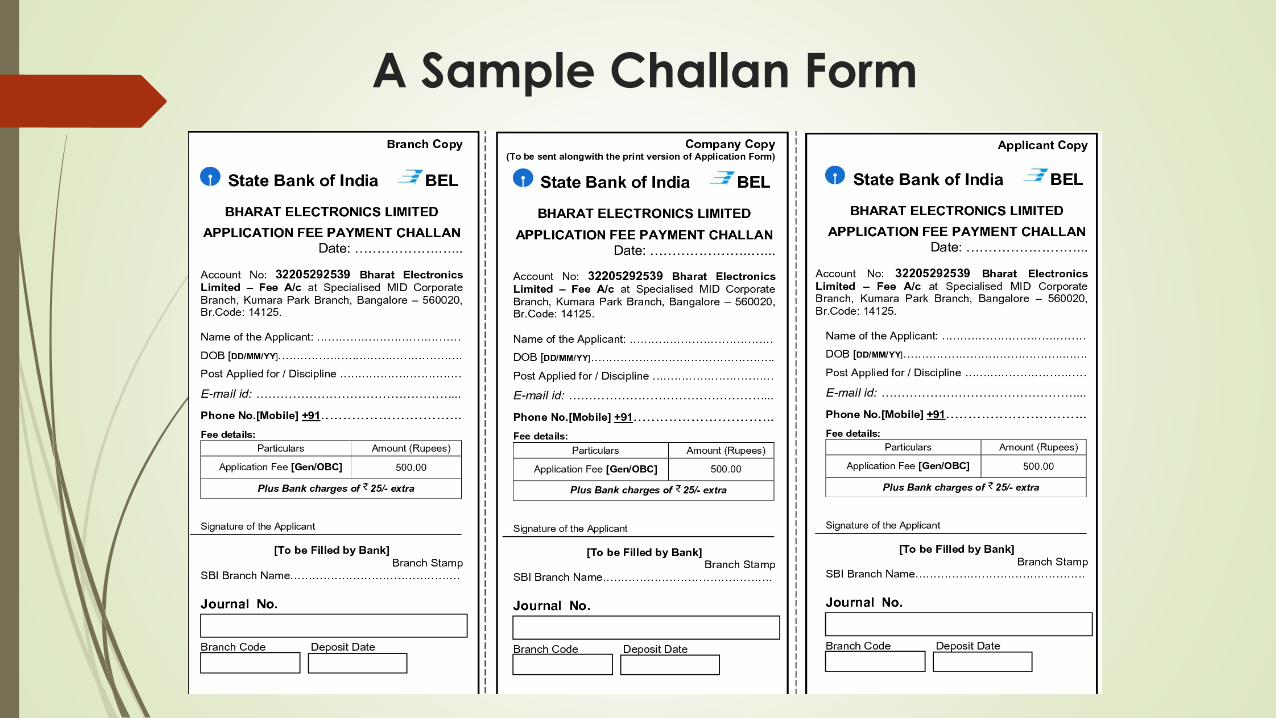

A Sample Challan Form

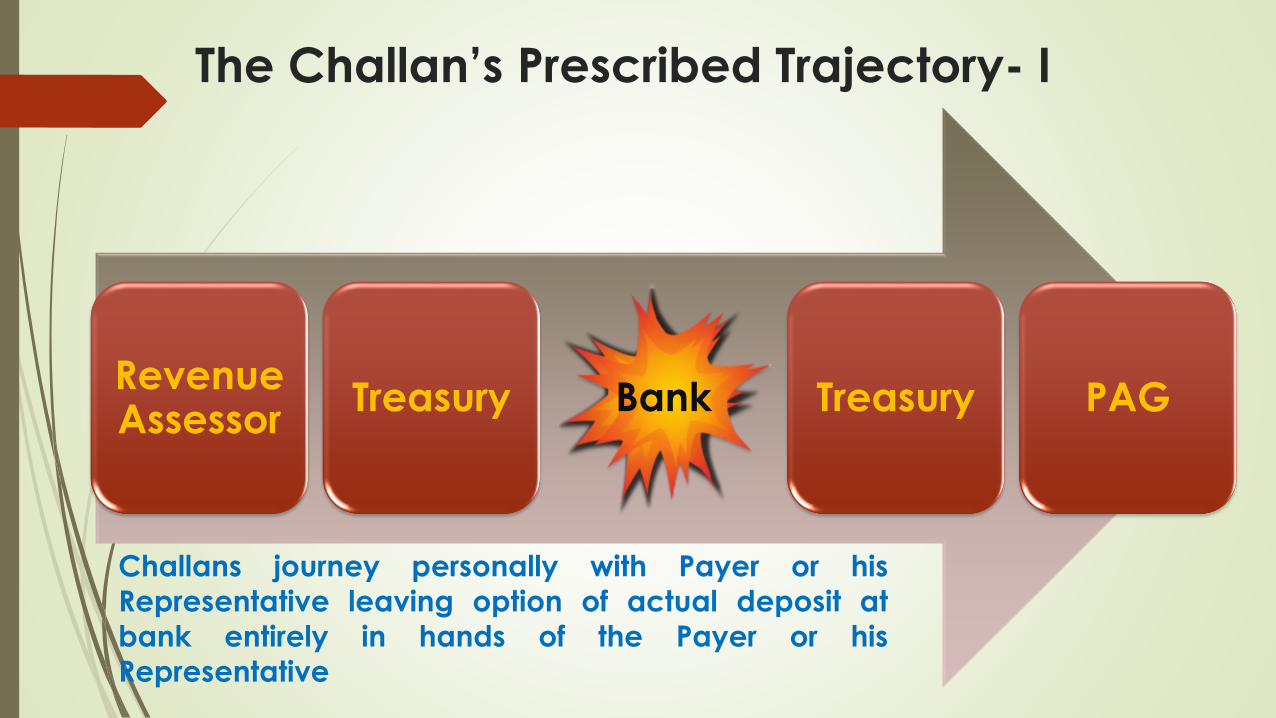

The Challan’s Prescribed Trajectory- I

Revenue Assessor

Treasury Bank Treasury PAG

Challans journey personally with Payer or his

Representative leaving option of actual deposit at

bank entirely in hands of the Payer or his

Representative

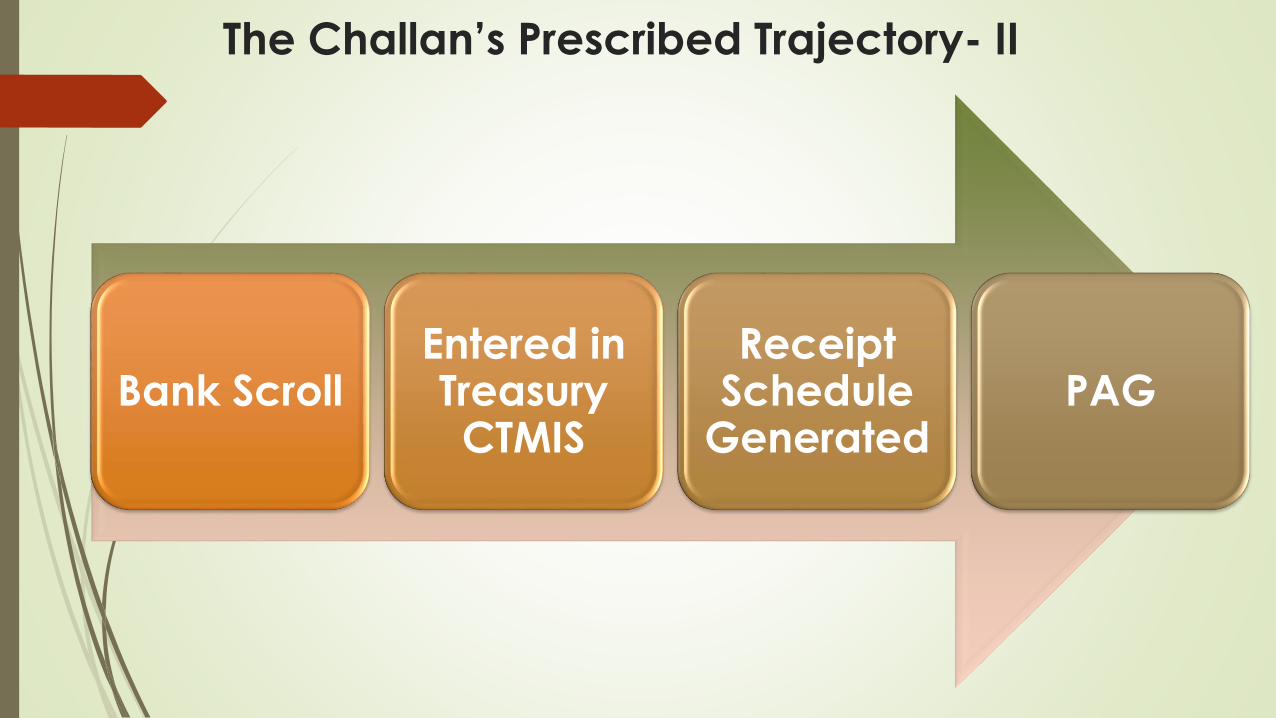

Bank ScrollEntered in Treasury CTMIS

Receipt Schedule

GeneratedPAG

The Challan’s Prescribed Trajectory- II

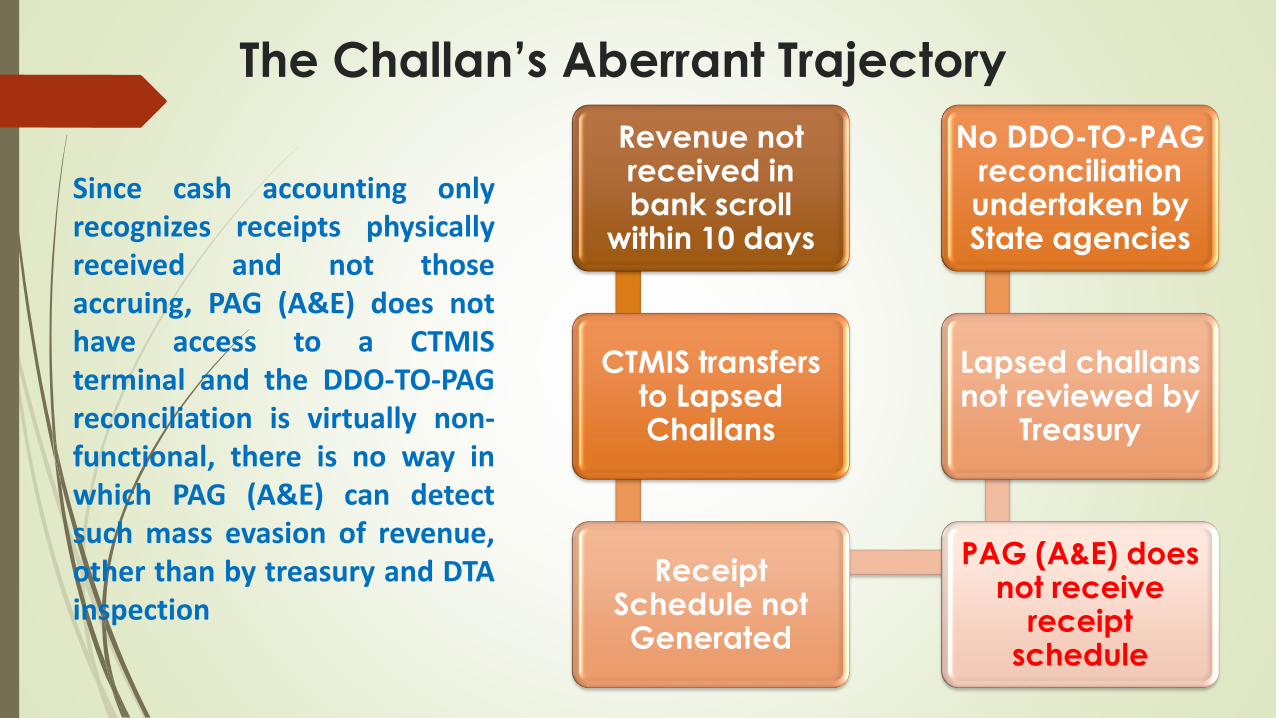

Revenue not received in bank scroll

within 10 days

CTMIS transfers to Lapsed Challans

Receipt Schedule not Generated

PAG (A&E) does not receive

receipt schedule

Lapsed challansnot reviewed by

Treasury

No DDO-TO-PAG reconciliation undertaken by State agencies

The Challan’s Aberrant Trajectory

Since cash accounting onlyrecognizes receipts physicallyreceived and not thoseaccruing, PAG (A&E) does nothave access to a CTMISterminal and the DDO-TO-PAGreconciliation is virtually non-functional, there is no way inwhich PAG (A&E) can detectsuch mass evasion of revenue,other than by treasury and DTAinspection

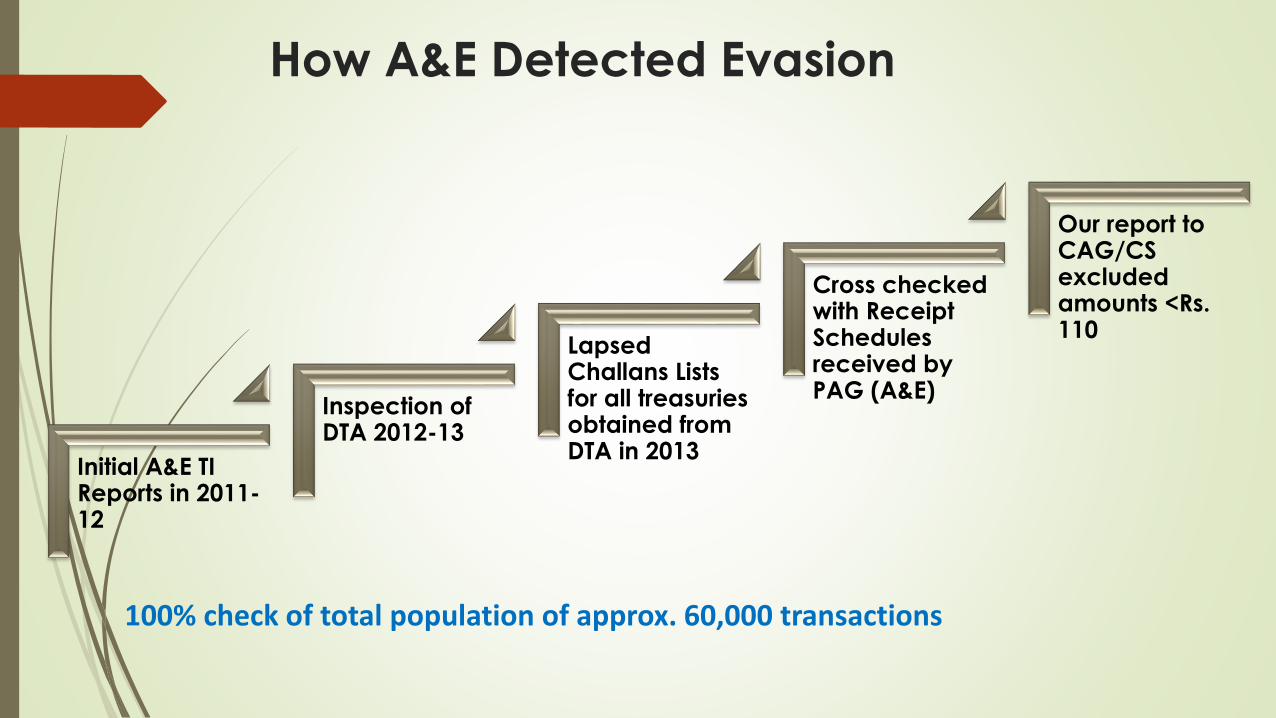

How A&E Detected Evasion

Initial A&E TI Reports in 2011-12

Inspection of DTA 2012-13

Lapsed Challans Lists for all treasuries obtained from DTA in 2013

Cross checked with Receipt Schedules received by PAG (A&E)

Our report to CAG/CS excluded amounts <Rs. 110

100% check of total population of approx. 60,000 transactions

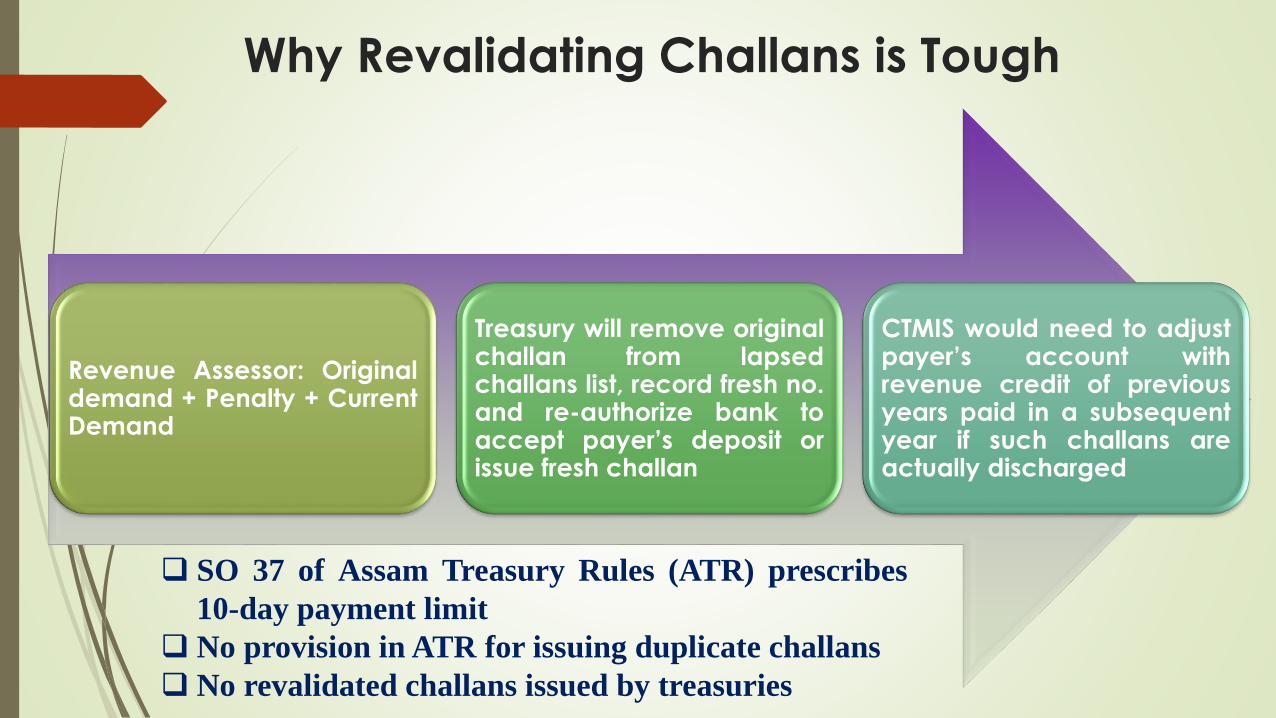

Why Revalidating Challans is Tough

Revenue Assessor: Originaldemand + Penalty + CurrentDemand

Treasury will remove originalchallan from lapsedchallans list, record fresh no.and re-authorize bank toaccept payer’s deposit orissue fresh challan

CTMIS would need to adjustpayer’s account withrevenue credit of previousyears paid in a subsequentyear if such challans areactually discharged

SO 37 of Assam Treasury Rules (ATR) prescribes

10-day payment limit

No provision in ATR for issuing duplicate challans

No revalidated challans issued by treasuries

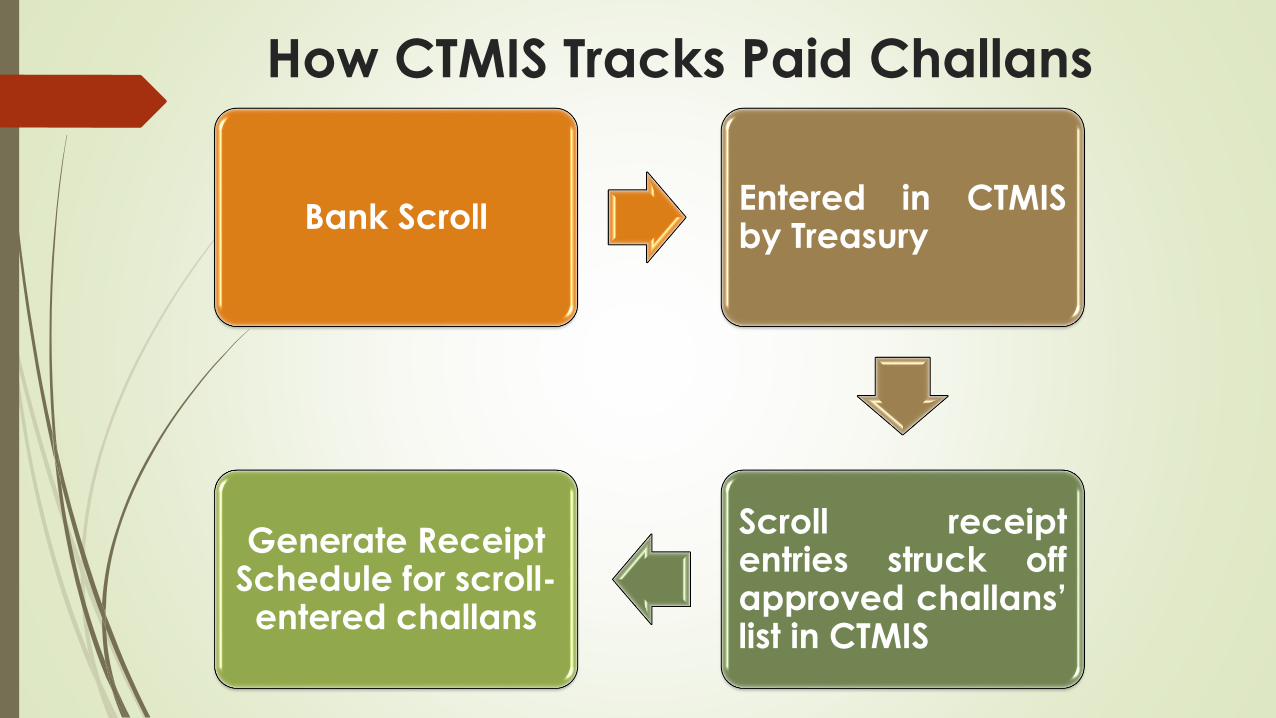

How CTMIS Tracks Paid Challans

Bank ScrollEntered in CTMISby Treasury

Scroll receiptentries struck offapproved challans’list in CTMIS

Generate Receipt Schedule for scroll-entered challans

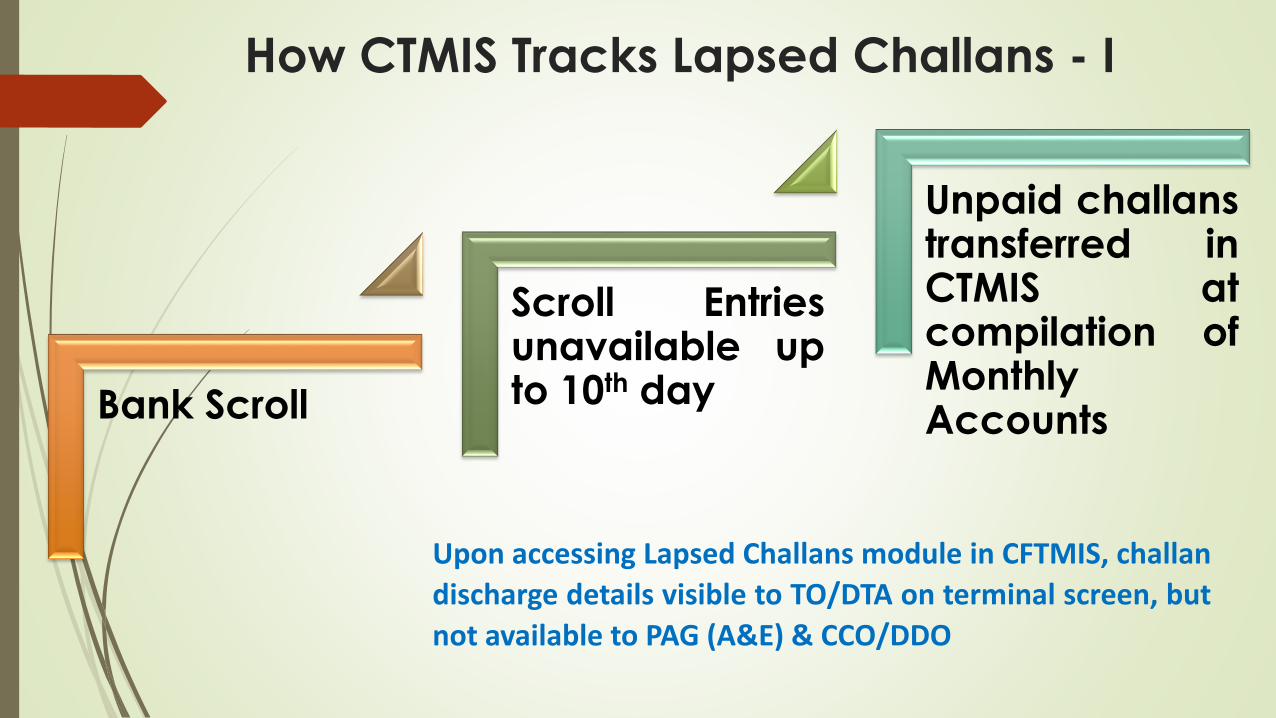

How CTMIS Tracks Lapsed Challans - I

Bank Scroll

Scroll Entriesunavailable upto 10th day

Unpaid challanstransferred inCTMIS atcompilation ofMonthlyAccounts

Upon accessing Lapsed Challans module in CFTMIS, challan

discharge details visible to TO/DTA on terminal screen, but

not available to PAG (A&E) & CCO/DDO

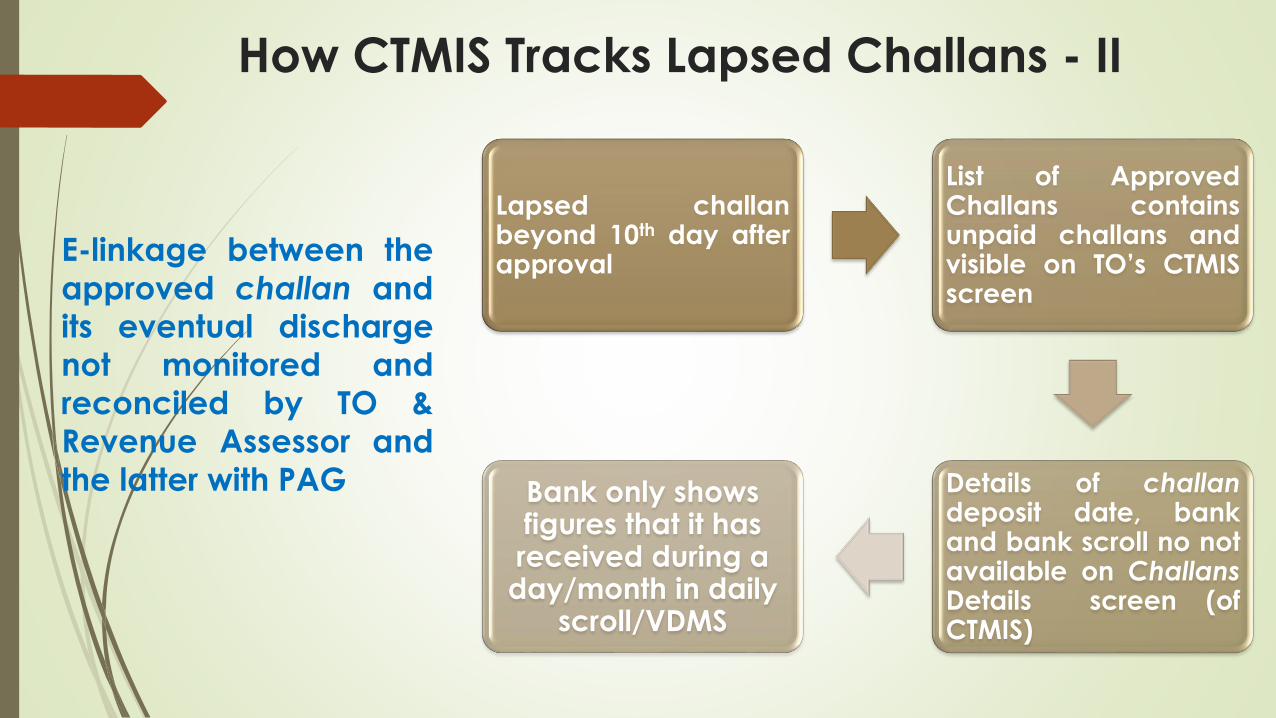

How CTMIS Tracks Lapsed Challans - II

Lapsed challanbeyond 10th day afterapproval

List of ApprovedChallans containsunpaid challans andvisible on TO’s CTMISscreen

Details of challandeposit date, bankand bank scroll no notavailable on ChallansDetails screen (ofCTMIS)

Bank only shows figures that it has received during a

day/month in daily scroll/VDMS

E-linkage between the

approved challan andits eventual discharge

not monitored and

reconciled by TO &

Revenue Assessor and

the latter with PAG

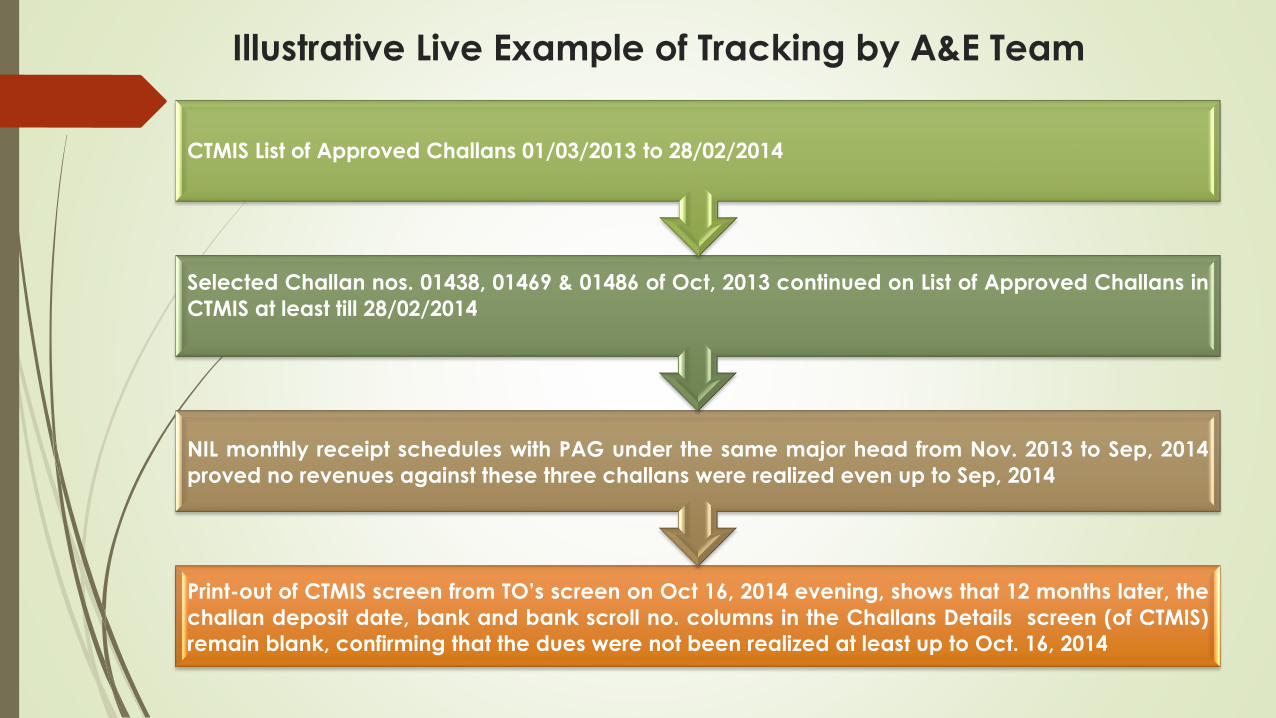

Illustrative Live Example of Tracking by A&E Team

Print-out of CTMIS screen from TO’s screen on Oct 16, 2014 evening, shows that 12 months later, the

challan deposit date, bank and bank scroll no. columns in the Challans Details screen (of CTMIS)

remain blank, confirming that the dues were not been realized at least up to Oct. 16, 2014

NIL monthly receipt schedules with PAG under the same major head from Nov. 2013 to Sep, 2014

proved no revenues against these three challans were realized even up to Sep, 2014

Selected Challan nos. 01438, 01469 & 01486 of Oct, 2013 continued on List of Approved Challans in

CTMIS at least till 28/02/2014

CTMIS List of Approved Challans 01/03/2013 to 28/02/2014

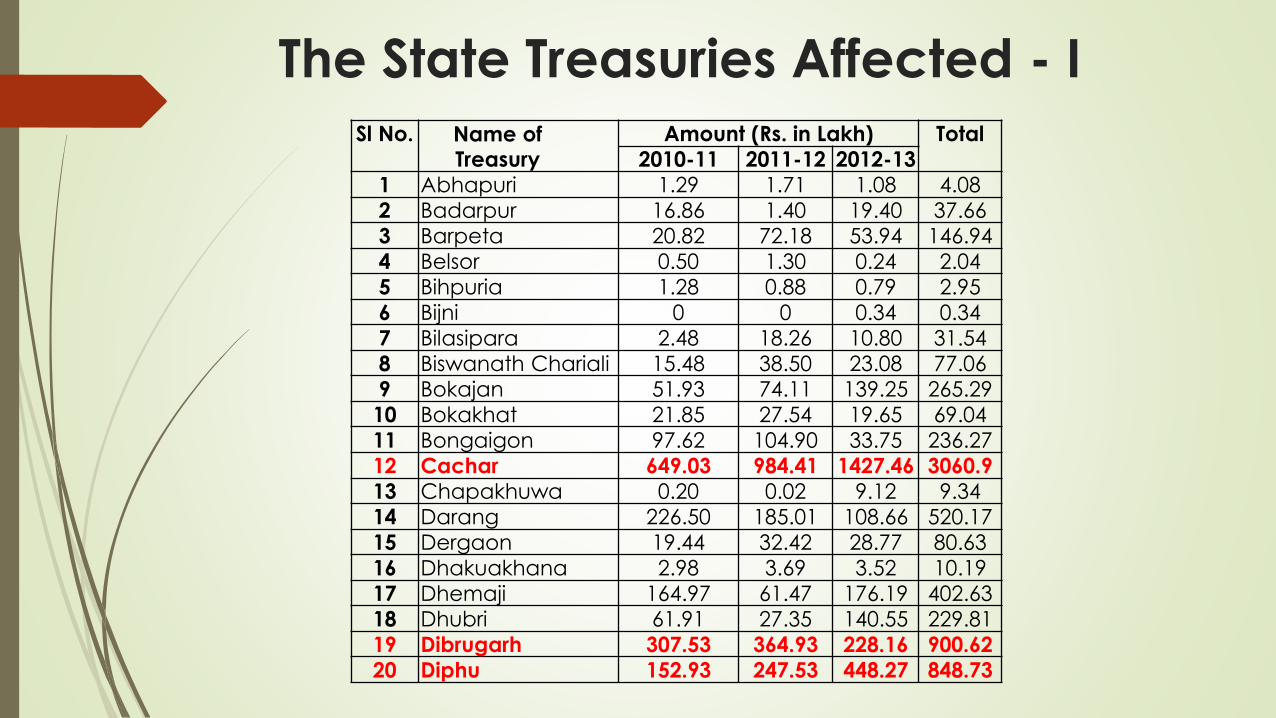

The State Treasuries Affected - I

Sl No. Name of Treasury

Amount (Rs. in Lakh) Total

2010-11 2011-12 2012-13

1 Abhapuri 1.29 1.71 1.08 4.08

2 Badarpur 16.86 1.40 19.40 37.66

3 Barpeta 20.82 72.18 53.94 146.94

4 Belsor 0.50 1.30 0.24 2.04

5 Bihpuria 1.28 0.88 0.79 2.95

6 Bijni 0 0 0.34 0.34

7 Bilasipara 2.48 18.26 10.80 31.54

8 Biswanath Chariali 15.48 38.50 23.08 77.06

9 Bokajan 51.93 74.11 139.25 265.29

10 Bokakhat 21.85 27.54 19.65 69.04

11 Bongaigon 97.62 104.90 33.75 236.27

12 Cachar 649.03 984.41 1427.46 3060.9

13 Chapakhuwa 0.20 0.02 9.12 9.34

14 Darang 226.50 185.01 108.66 520.17

15 Dergaon 19.44 32.42 28.77 80.63

16 Dhakuakhana 2.98 3.69 3.52 10.19

17 Dhemaji 164.97 61.47 176.19 402.63

18 Dhubri 61.91 27.35 140.55 229.81

19 Dibrugarh 307.53 364.93 228.16 900.62

20 Diphu 152.93 247.53 448.27 848.73

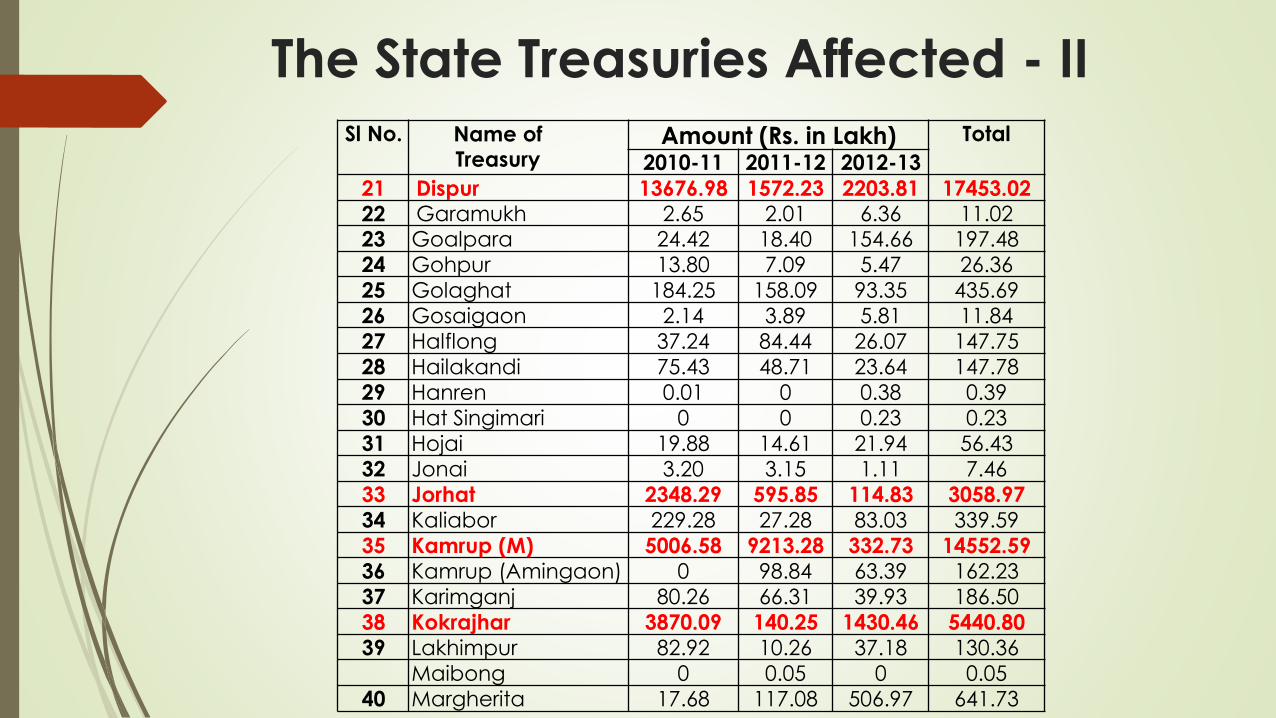

The State Treasuries Affected - II

Sl No. Name of Treasury

Amount (Rs. in Lakh) Total

2010-11 2011-12 2012-13

21 Dispur 13676.98 1572.23 2203.81 17453.02

22 Garamukh 2.65 2.01 6.36 11.0223 Goalpara 24.42 18.40 154.66 197.48

24 Gohpur 13.80 7.09 5.47 26.36

25 Golaghat 184.25 158.09 93.35 435.69

26 Gosaigaon 2.14 3.89 5.81 11.84

27 Halflong 37.24 84.44 26.07 147.75

28 Hailakandi 75.43 48.71 23.64 147.78

29 Hanren 0.01 0 0.38 0.39

30 Hat Singimari 0 0 0.23 0.23

31 Hojai 19.88 14.61 21.94 56.43

32 Jonai 3.20 3.15 1.11 7.46

33 Jorhat 2348.29 595.85 114.83 3058.97

34 Kaliabor 229.28 27.28 83.03 339.59

35 Kamrup (M) 5006.58 9213.28 332.73 14552.59

36 Kamrup (Amingaon) 0 98.84 63.39 162.23

37 Karimganj 80.26 66.31 39.93 186.50

38 Kokrajhar 3870.09 140.25 1430.46 5440.80

39 Lakhimpur 82.92 10.26 37.18 130.36

Maibong 0 0.05 0 0.05

40 Margherita 17.68 117.08 506.97 641.73

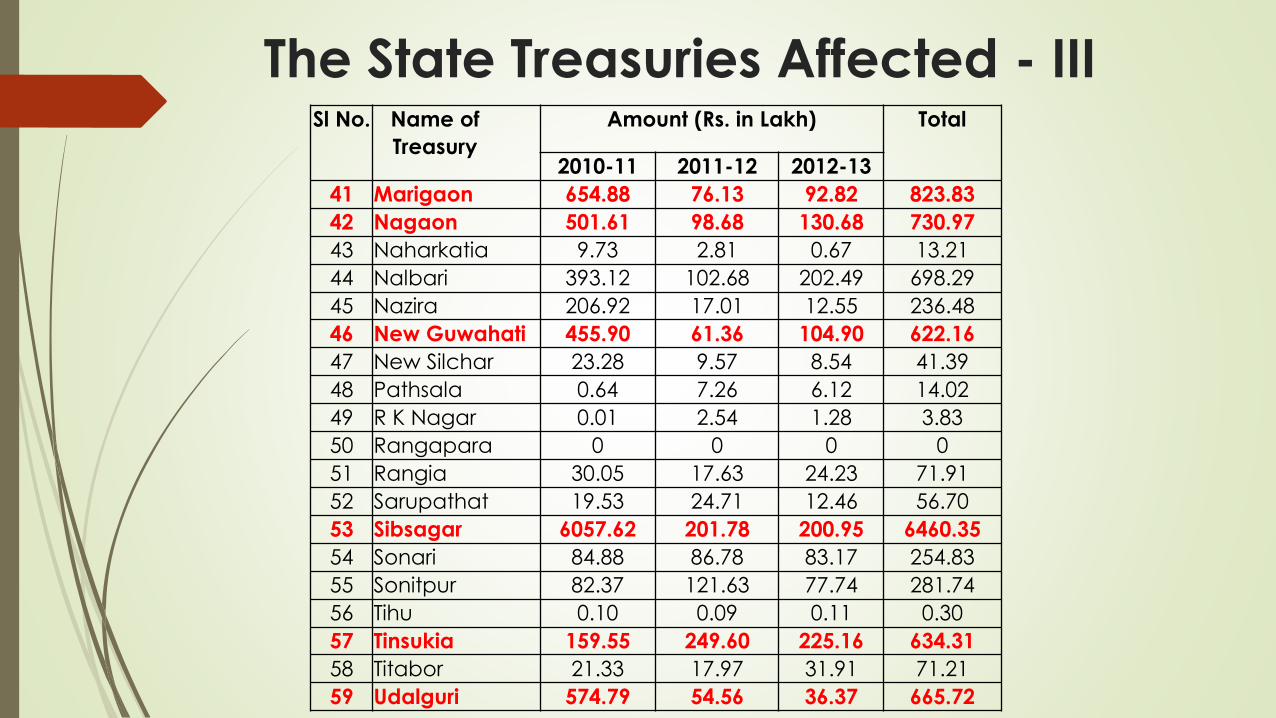

The State Treasuries Affected - IIISl No. Name of

Treasury

Amount (Rs. in Lakh) Total

2010-11 2011-12 2012-13

41 Marigaon 654.88 76.13 92.82 823.83

42 Nagaon 501.61 98.68 130.68 730.97

43 Naharkatia 9.73 2.81 0.67 13.21

44 Nalbari 393.12 102.68 202.49 698.29

45 Nazira 206.92 17.01 12.55 236.48

46 New Guwahati 455.90 61.36 104.90 622.16

47 New Silchar 23.28 9.57 8.54 41.39

48 Pathsala 0.64 7.26 6.12 14.02

49 R K Nagar 0.01 2.54 1.28 3.83

50 Rangapara 0 0 0 0

51 Rangia 30.05 17.63 24.23 71.91

52 Sarupathat 19.53 24.71 12.46 56.70

53 Sibsagar 6057.62 201.78 200.95 6460.35

54 Sonari 84.88 86.78 83.17 254.83

55 Sonitpur 82.37 121.63 77.74 281.74

56 Tihu 0.10 0.09 0.11 0.30

57 Tinsukia 159.55 249.60 225.16 634.31

58 Titabor 21.33 17.97 31.91 71.21

59 Udalguri 574.79 54.56 36.37 665.72

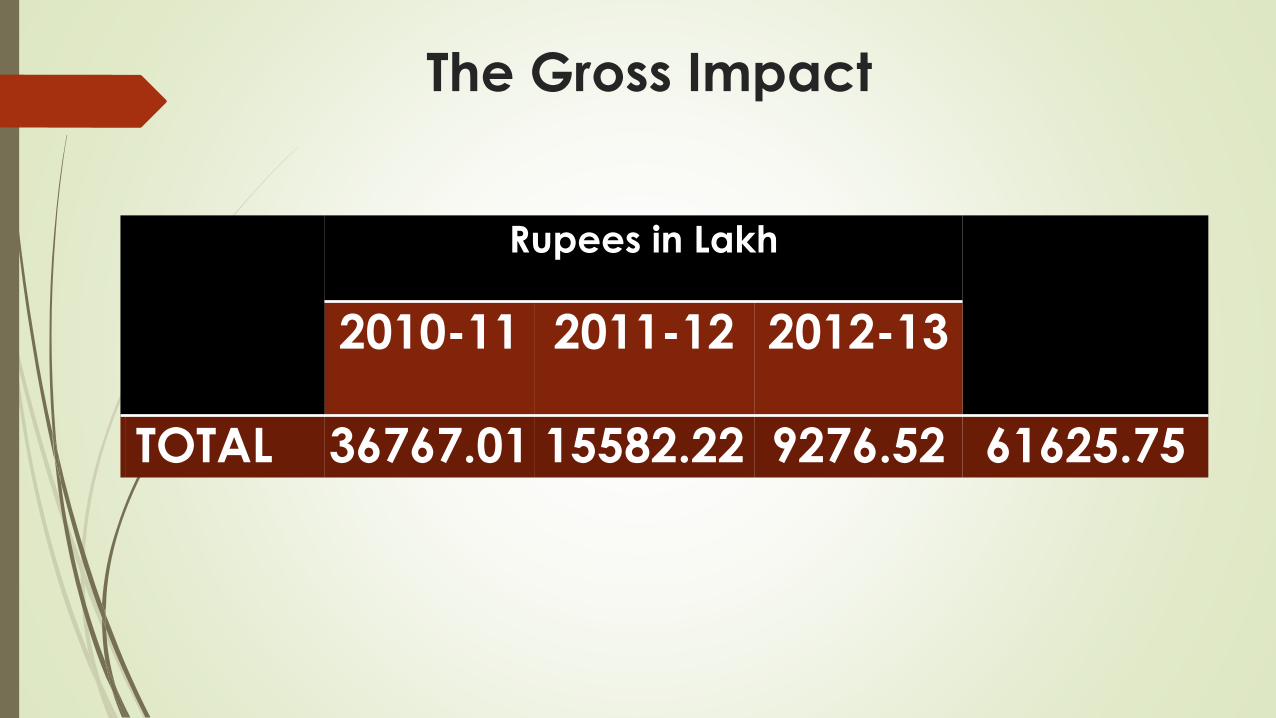

The Gross Impact

Rupees in Lakh

2010-11 2011-12 2012-13

TOTAL 36767.01 15582.22 9276.52 61625.75

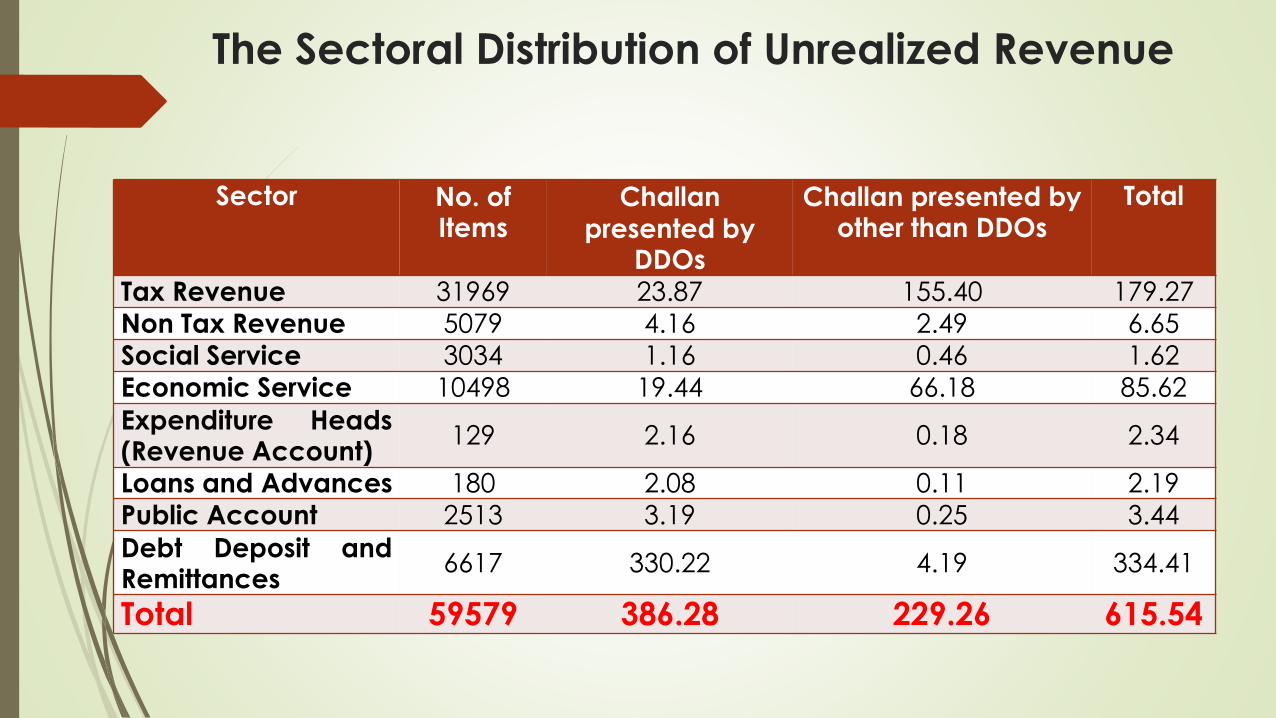

The Sectoral Distribution of Unrealized Revenue

Sector No. of Items

Challan

presented by DDOs

Challan presented by other than DDOs

Total

Tax Revenue 31969 23.87 155.40 179.27

Non Tax Revenue 5079 4.16 2.49 6.65

Social Service 3034 1.16 0.46 1.62Economic Service 10498 19.44 66.18 85.62

Expenditure Heads(Revenue Account)

129 2.16 0.18 2.34

Loans and Advances 180 2.08 0.11 2.19

Public Account 2513 3.19 0.25 3.44

Debt Deposit andRemittances

6617 330.22 4.19 334.41

Total 59579 386.28 229.26 615.54

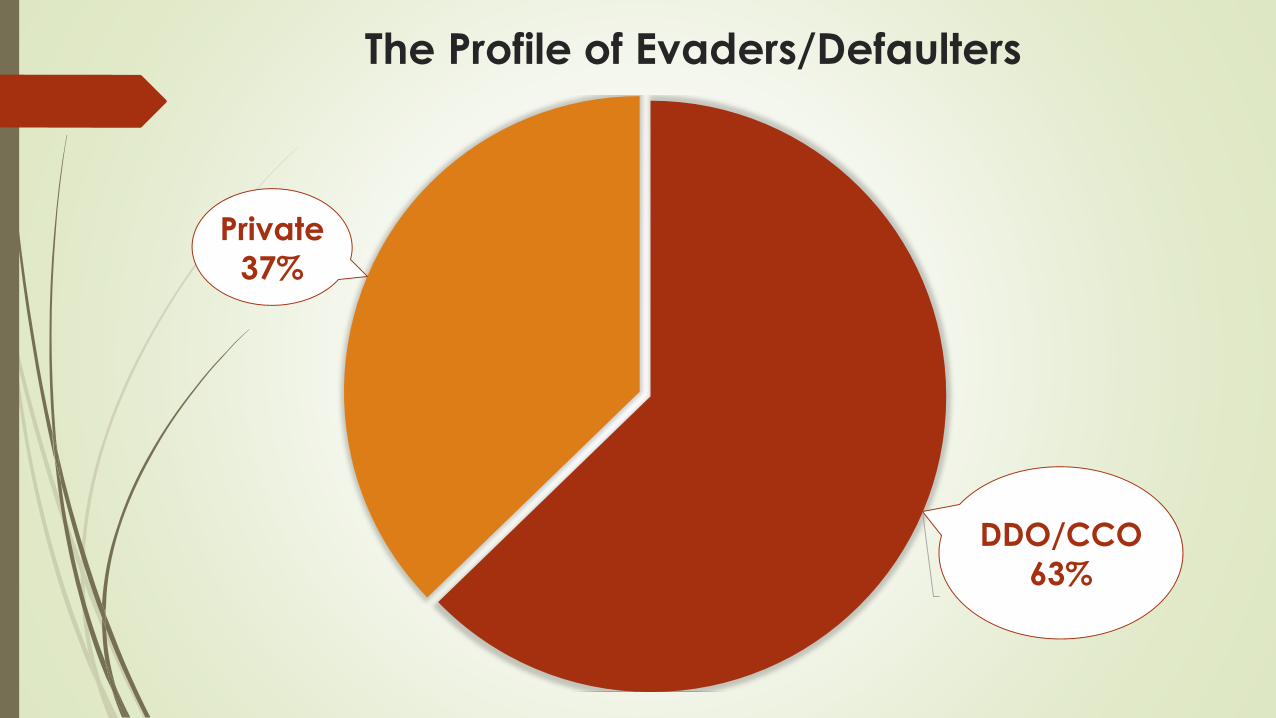

The Profile of Evaders/Defaulters

DDO/CCO

63%

Private

37%

Some Major Deprived Revenue Budget Heads

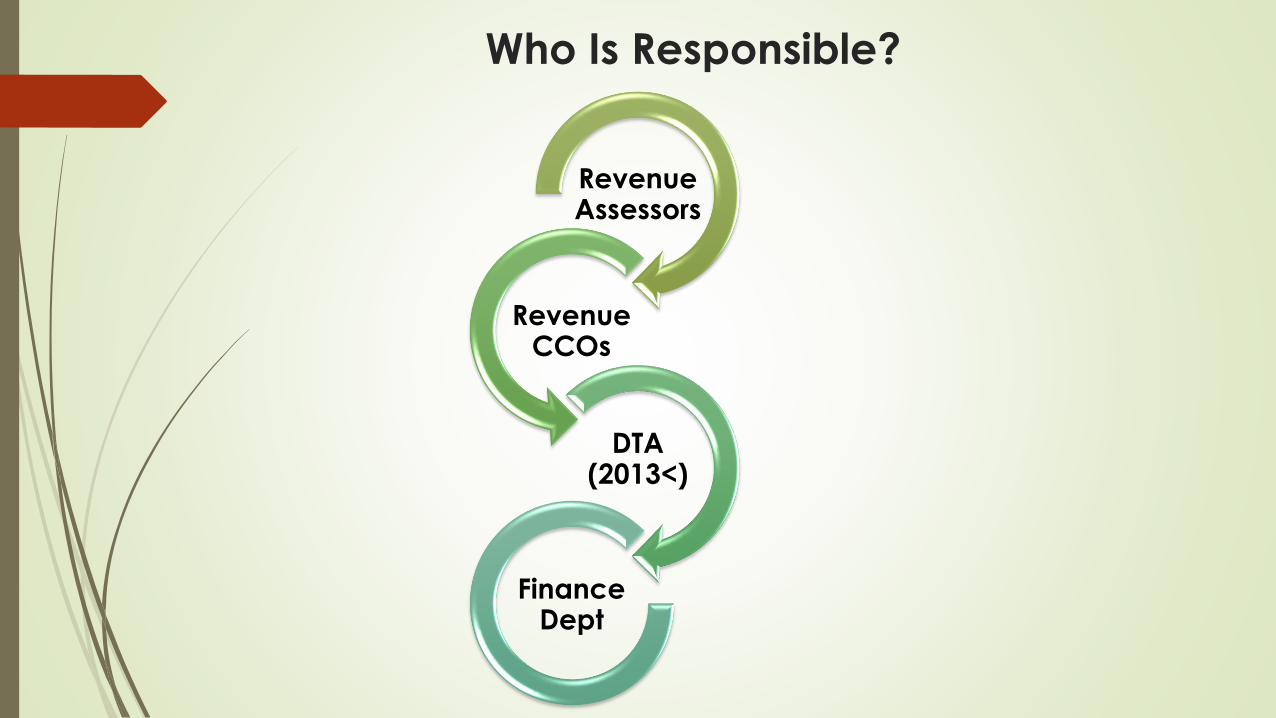

Who Is Responsible?

Revenue Assessors

Revenue CCOs

DTA (2013<)

Finance Dept

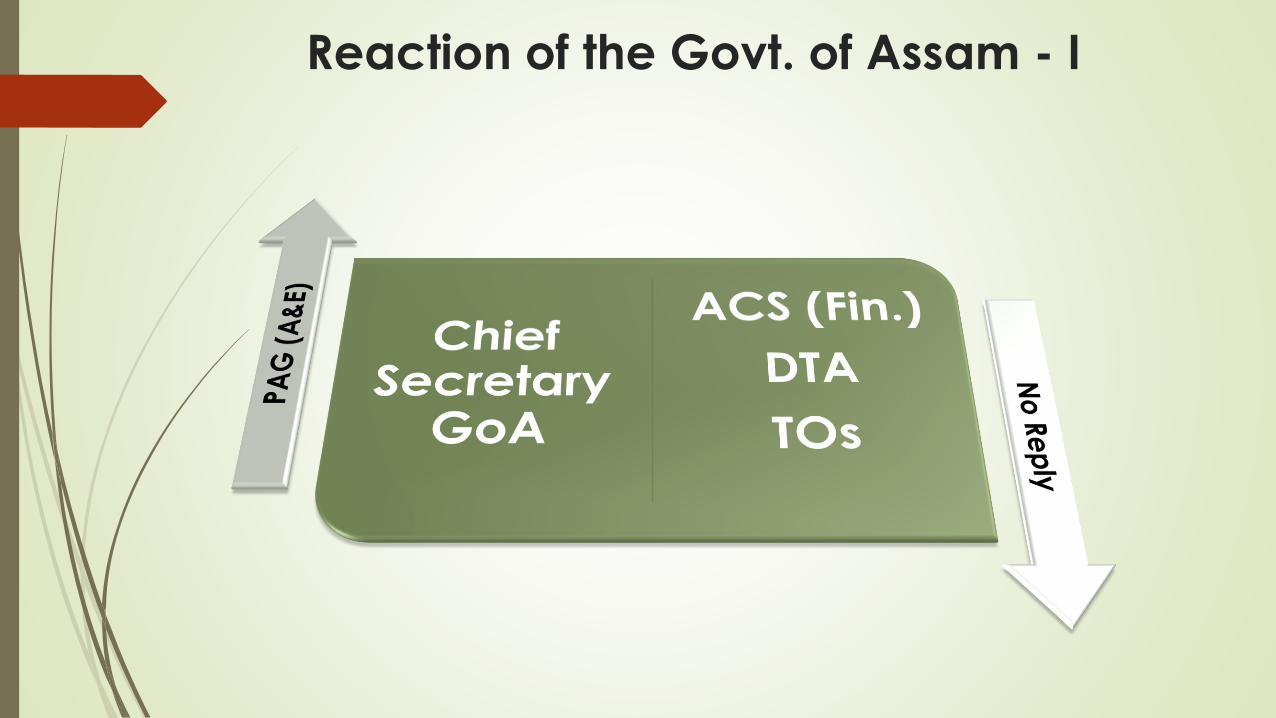

Reaction of the Govt. of Assam - I

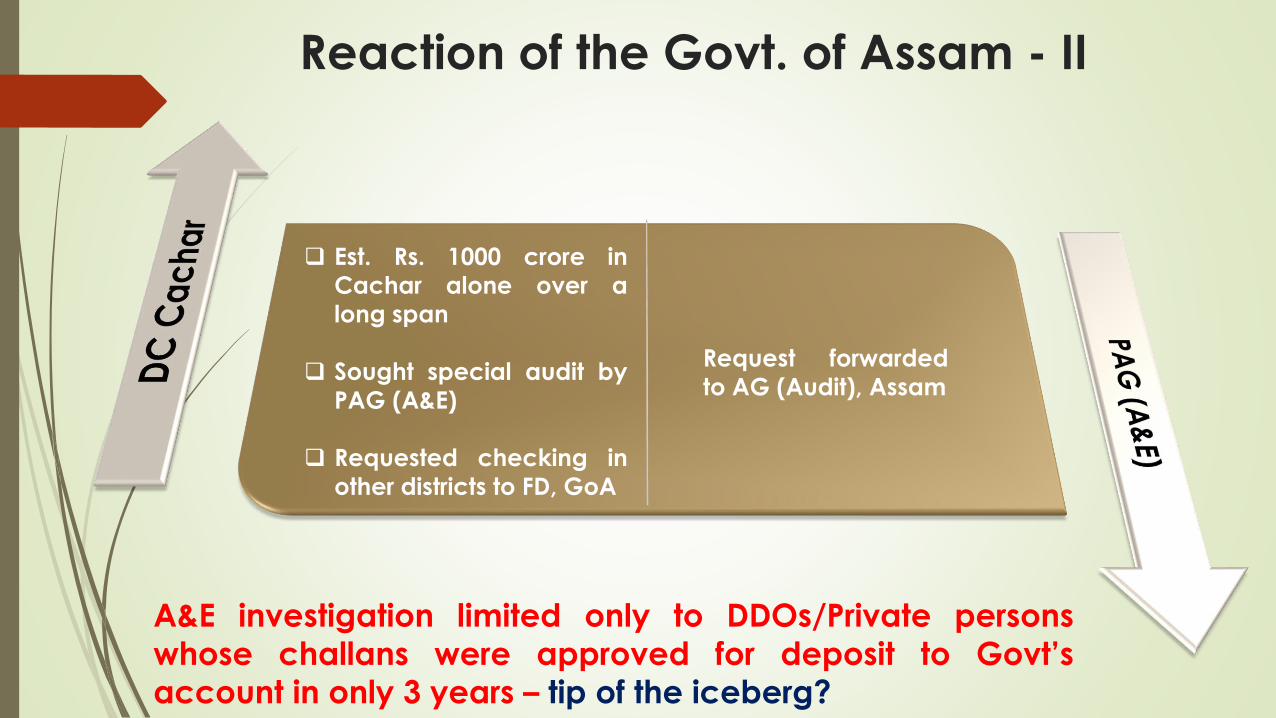

Reaction of the Govt. of Assam - II

Est. Rs. 1000 crore in

Cachar alone over a

long span

Sought special audit by

PAG (A&E)

Requested checking in

other districts to FD, GoA

Request forwarded

to AG (Audit), Assam

A&E investigation limited only to DDOs/Private persons

whose challans were approved for deposit to Govt’s

account in only 3 years – tip of the iceberg?

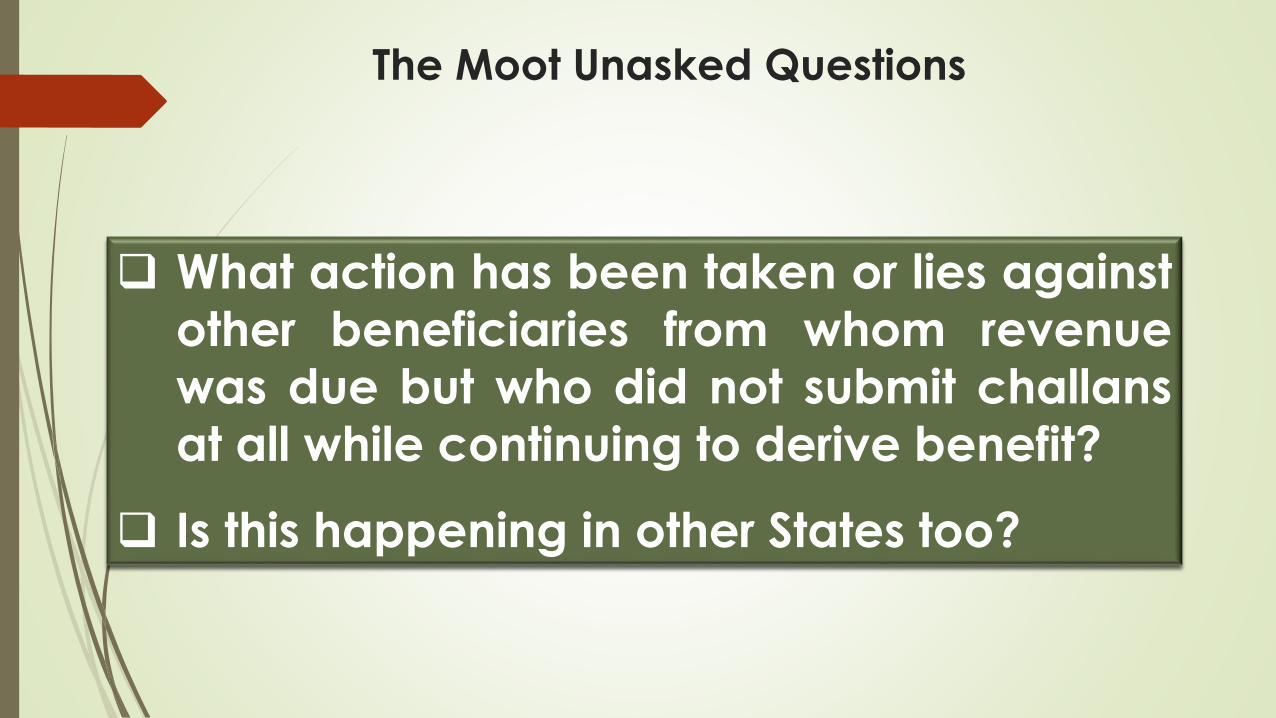

The Moot Unasked Questions

What action has been taken or lies against

other beneficiaries from whom revenue

was due but who did not submit challans

at all while continuing to derive benefit?

Is this happening in other States too?

© Devised and Presented by

O/o Pr. Accountant General (A&E), Assam

Guwahati

Feb 2, 2015