Embed Size (px)

Citation preview

Ex-ante Impacts of Agricultural Insurance: Evidence

from a Field Experiment in Mali

Ghada Elabed* & Michael R Carter**

*Mathematica Policy Research**University of California, Davis & NBER

BASIS Assets & Market Access Research Program &I4 Index Insurance Innovation Initiative

http://basis.ucdavis.edu.

Annual Global Development Conference, Casablanca

13 June 2015

Elabed & Carter Impacts of Insurance in Mali

Uninsured Risk Is Costly

Risk is costly:

Makes Households Poor when it leads them to adopt less risky,but lower returning activitiesKeeps Households Poor not only when it de-capitalizes them inthe wake of a shock, but also when it leads them to accumulateunproductive 'bu�er' assets in anticipation of shocks

Can insurance have real development impacts?

Not just ex post smoothing e�ects (see previous work)But allowing farmers to ex ante prudentially invest more andincrease their average incomes

This presentation looks at the investment and income impactsof index insurance for cotton farmers in Mali

Elabed & Carter Impacts of Insurance in Mali

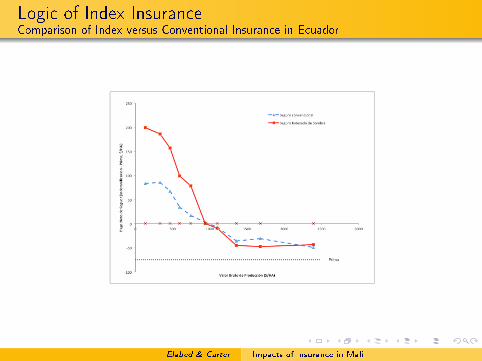

Logic of Index Insurance

Conventional insurance (based on individual loss adjustment)has a dismal record

Costly to verify losses for smallholdersMoral hazard if do not/cannot reliably verify lossesAdverse selection

Index insurance does not pay based on (veri�ed) individuallosses, but instead based on a cheap to measure 'index' that iscorrelated with individual losses (e.g., average yields in a zone,or rainfall)

Cuts costsEliminates moral hazard & adverse selection

Elabed & Carter Impacts of Insurance in Mali

Cotton Production in Mali

Most farmers are smallholders and grow a mix of subsistencecrops and cotton

Cotton is their main (and often only) source of cash

Cotton is a pro�table, but risky crop

Production organized in cooperatives

Cotton is controlled by the Compagnie malienne pour ledéveloppement du textile (CMDT), a parastatal

CMDT provides input loans and buys the harvest at a priceannounced before planting

Elabed & Carter Impacts of Insurance in Mali

Risk and Capital Constraints in Mali

Farmers access credit via group loans:

Amount of loan is on average 95,000CFA/ha, and the netrevenue from cotton is 105,000CFA/haIf the cooperative yield falls below 750 kg/ha, loan repaymentis tenuousP(yield < 750) = 10%Consequences of default are substantial (informal collateral)

The collateral risk of default appears to discourage farmersfrom growing as much cotton as they otherwise might�classicexample of risk rationing

Output can be taxed away to pay for others in the group

Elabed & Carter Impacts of Insurance in Mali

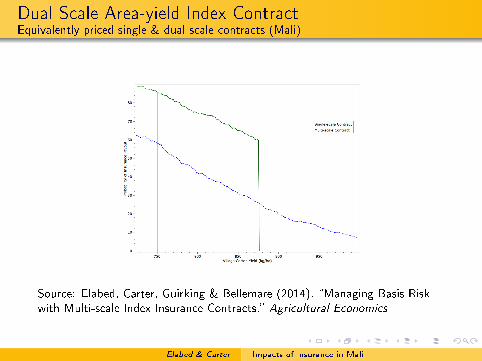

Dual Scale Area-yield Index Contract

To address these issues, developed an area-yield insurancecontract

Can do this easily because monopsony buyer (CMDT) alreadymeasures area and output

Insured unit is the cooperative (as it holds the joint liabilitydebt for all farmers in the village)

Payouts based on the average yield of the cooperative and ofthe �ZPA� grouping (an agglomeration of 10-15 villagecooperatives)

This dual scale area-yield contract has a low level of basis risk:Conditional on a loss, the probability of getting a payment is80%, and the probability that net proceeds are less than thevalue of 750 kg of cotton per-hectare drops to 2%

Elabed & Carter Impacts of Insurance in Mali

The Mali Pilot Project

In cooperation with PlaNet Guarantee implemented arandomized control trial for the 2011/12 year

87 cooperatives: 59 were randomly selected for treatment(o�ered insurance), 28 served as control

An encouragement design: reduced the price of contract to50%, 75%, or 100% of the actuarially fair premium

Decisions to buy the insurance made in May 2011 (plantingseason)

30% of the treated cooperatives purchased the insurancecontract

Elabed & Carter Impacts of Insurance in Mali

The Mali Pilot Project

Note that the insurance purchase decision was a joint decisionby co-op

Creates the possibility that an individual farmer may not knows/he is insured (e.g., if missed meeting)

Ex ante e�ects can of course only occur if farmers know theyare insured

In the analysis to follow, we will both look at the impacts ofbeing insured (co-op purchased insurance) and also impact iffarmer reports that s/he is insured.

Elabed & Carter Impacts of Insurance in Mali

Research design

Unfortunately, we discovered �aws in roll-out (not all treatedco-ops were actually o�ered insurance)

Fortunately, we had audit questions that allowed us to �gureout what really happened

But only 22.5% of the treated households believed they wereinsured (and 10% of non-treated households!)

Results shown here use the audit-based reclassi�cation oftreatment and control areas

Paper includes all results�similar estimated impacts but lessprecise

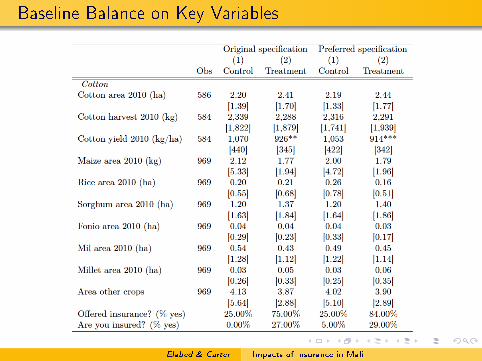

Audit-adjusted treatment & control groups are balanced interms of observable covariates

Let's focus now on key outcome variables

Elabed & Carter Impacts of Insurance in Mali

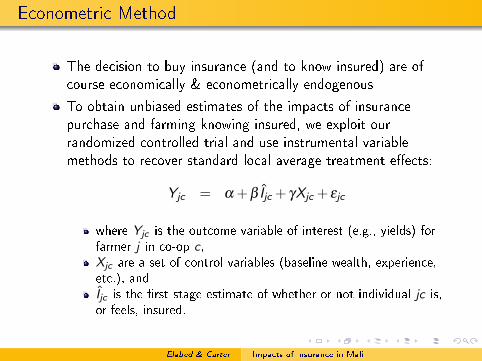

Econometric Method

The decision to buy insurance (and to know insured) are ofcourse economically & econometrically endogenous

To obtain unbiased estimates of the impacts of insurancepurchase and farming knowing insured, we exploit ourrandomized controlled trial and use instrumental variablemethods to recover standard local average treatment e�ects.

Elabed & Carter Impacts of Insurance in Mali

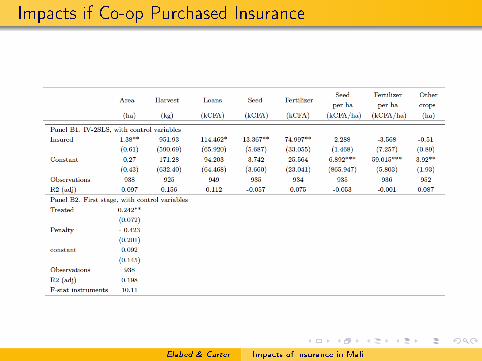

Impacts if Co-op Purchased Insurance

Elabed & Carter Impacts of Insurance in Mali

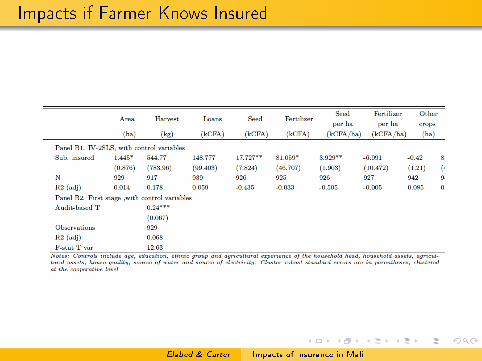

Impacts if Farmer Knows Insured

Elabed & Carter Impacts of Insurance in Mali

Conclusion

Impact of insurance are substantial at the extensive margin:

Area in cotton rose by 1.3 to 1.4 hectares (a 60% increase)Matching increases in loans and inputsNo impacts on input intensity, nor any impact on reduction inother ag activityOutput (and income) increases are estimated to be about40%, but this �gure is not signi�cant (noisy outcome measure)

We thus see that insurance can have substantial developmentimpact

New pilot in Burkina Faso�stay tuned!

Elabed & Carter Impacts of Insurance in Mali

Extra Material

Elabed & Carter Impacts of Insurance in Mali

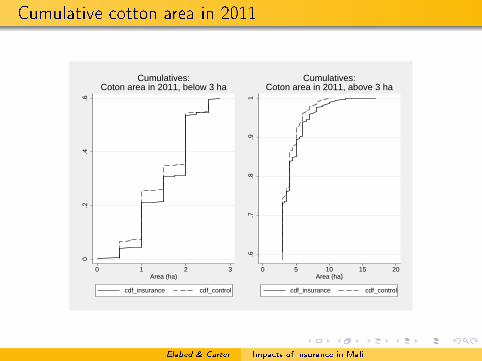

Cumulative cotton area in 2011

0.2

.4.6

0 1 2 3Area (ha)

cdf_insurance cdf_control

Cumulatives:Coton area in 2011, below 3 ha

.6.7

.8.9

1

0 5 10 15 20Area (ha)

cdf_insurance cdf_control

Cumulatives:Coton area in 2011, above 3 ha

Elabed & Carter Impacts of Insurance in Mali

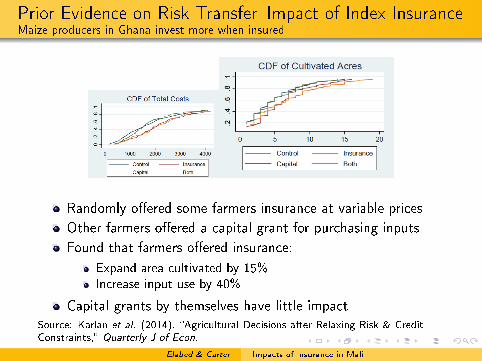

Prior Evidence on Risk Transfer�Impact of Index InsuranceMaize producers in Ghana invest more when insured

Randomly o�ered some farmers insurance at variable prices

Other farmers o�ered a capital grant for purchasing inputs

Found that farmers o�ered insurance:

Expand area cultivated by 15%Increase input use by 40%

Capital grants by themselves have little impactSource: Karlan et al. (2014). �Agricultural Decisions after Relaxing Risk & CreditConstraints,� Quarterly J of Econ.

Elabed & Carter Impacts of Insurance in Mali

Logic of Index InsuranceComparison of Index versus Conventional Insurance in Ecuador

Elabed & Carter Impacts of Insurance in Mali

Dual Scale Area-yield Index ContractEquivalently priced single & dual-scale contracts (Mali)

Source: Elabed, Carter, Guirking & Bellemare (2014). �Managing Basis Riskwith Multi-scale Index Insurance Contracts,� Agricultural Economics

Elabed & Carter Impacts of Insurance in Mali

Risk Rationing and Cotton Production

Loans come with a binding joint liability clause

Consequences of default are substantial (informal collateral)

Survey in 2006: 32% of the farmers growing cotton haddi�culty with their loan repayment

38% had to sell their assets4% sent one of their children to work for another farmerSome saw their credit line reduced and faced exclusion fromthe credit group

The collateral risk of default appears to discourage farmersfrom growing as much cotton as they otherwise might�classicexample of risk rationing

Elabed & Carter Impacts of Insurance in Mali

Research question and Research Strategy

There is modest but growing evidence that risk transfer (viainsurance) & risk reduction (via stress tolerant varieties) haseconomically notable impacts

Protecting current and future assets: Janzen and Carter (2014)Relaxing risk and capital constraints: Karlan et al (2014)Incentivizing technology adoption: Mobarak and Rosenzweig(2012)

Use the remainder of our time to look at the investment andincome impacts of insurance for cotton farmers in Mali

We designed an insurance contract for cotton cooperatives inMali

We randomly o�ered insurance to 87 cotton cooperatives

Elabed & Carter Impacts of Insurance in Mali

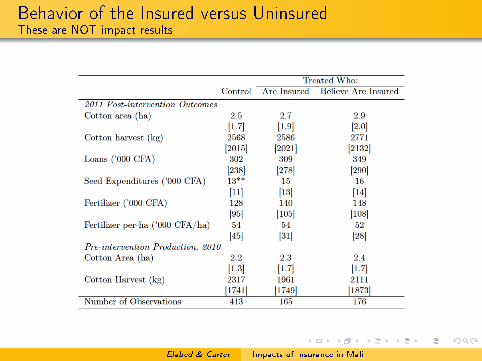

Behavior of the Insured versus UninsuredThese are NOT impact results

Elabed & Carter Impacts of Insurance in Mali

Risk Rationing and Cotton Production

Loans come with a binding joint liability clause

Consequences of default are substantial (informal collateral)

Survey in 2006: 32% of the farmers growing cotton haddi�culty with their loan repayment

38% had to sell their assets4% sent one of their children to work for another farmerSome saw their credit line reduced and faced exclusion fromthe credit group

The collateral risk of default appears to discourage farmersfrom growing as much cotton as they otherwise might�classicexample of risk rationing

Elabed & Carter Impacts of Insurance in Mali

Dual Scale Area-yield Index Contract

To address these issues, developed an area-yield insurancecontract

Can do this easily because monopsony buyer (CMDT) alreadymeasures area and output

Insured unit is the cooperative (as it holds the joint liabilitydebt for all farmers in the village)

But at what scale set the trigger or strikepoint that determinespayment?

If take average across a larger area, basis risk increasesIf take average across too small an area, collusion and moralhazard possible

Elabed & Carter Impacts of Insurance in Mali

Dual Scale Area-yield Index Contract

Rather than face the tradeo� between a village level yieldtrigger (moral hazard) versus a yield trigger based on a larger�ZPA� grouping (an agglomeration of 10-15 villagecooperatives), designed a dual scale contract

Payouts based on the average yield of the cooperative AND ofthe ZPA

Can think of the ZPA trigger as an audit rule�only believevillage yields are low due to nature if neighboring villages arealso showing some signs of stress

Conditional on a loss, the probability of getting a payment is80%, and the probability that net proceeds are less than thevalue of 750 kg of cotton per-hectare drops to 2%

Elabed & Carter Impacts of Insurance in Mali

Logic of Index Insurance

Conventional insurance (based on individual loss adjustment)has a dismal record

Costly to verify losses for smallholdersMoral hazard if do not/cannot reliably verify lossesAdverse selection

Index insurance does not pay based on (veri�ed) individuallosses, but instead based on a cheap to measure 'index' that iscorrelated with individual losses (e.g., average yields in a zone,or rainfall)

Cuts costsEliminates moral hazard & adverse selection

Elabed & Carter Impacts of Insurance in Mali

Baseline Balance on Key Variables

Elabed & Carter Impacts of Insurance in Mali

Econometric Method

The decision to buy insurance (and to know insured) are ofcourse economically & econometrically endogenous

To obtain unbiased estimates of the impacts of insurancepurchase and farming knowing insured, we exploit ourrandomized controlled trial and use instrumental variablemethods to recover standard local average treatment e�ects:

Yjc = α +β Ijc + γXjc + εjc

where Yjc is the outcome variable of interest (e.g., yields) forfarmer j in co-op c ,Xjc are a set of control variables (baseline wealth, experience,etc.), andIjc is the �rst stage estimate of whether or not individual jc is,or feels, insured.

Elabed & Carter Impacts of Insurance in Mali

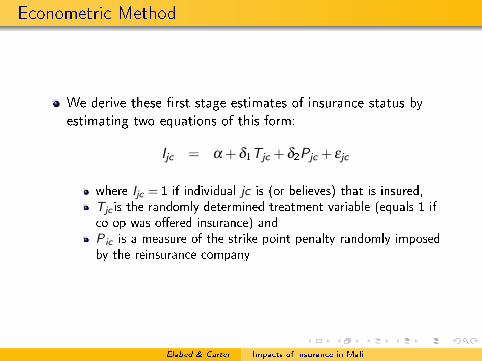

Econometric Method

We derive these �rst stage estimates of insurance status byestimating two equations of this form:

Ijc = α +δ1Tjc +δ2Pjc + εjc

where Ijc = 1 if individual jc is (or believes) that is insured,Tjc is the randomly determined treatment variable (equals 1 ifco-op was o�ered insurance) andP ic is a measure of the strike point penalty randomly imposedby the reinsurance company

Elabed & Carter Impacts of Insurance in Mali

Strikepoint Penalty

Research team designed & then priced the contract under theassumption that yields for di�erent co-ops in the same area aredriven by a common parametric probability structure

Structure was allowed to parametrically shift with each co-op'saverage long-term yields

Resulted in a set of spatially stable prices

Elabed & Carter Impacts of Insurance in Mali

Strikepoint Penalty

Reinsurance partner rejected this approach and priced eachco-op separately using burn rates based on the short timeseries available on each co-op

Resulted in often radical downward shift in strike points, withneighboring co-ops sometimes o�ered radically di�erentcontracts

Also resulted in no contracts being o�ered to more than halfthe co-ops in pilot area

Because these strike point di�erences were driven byrandomness (did one co-op happen to have an especially badyear in its time series, whereas its neighbor did not), a measureof this strike point penalty should serve as a statistically validand strong instrument to explain insurance purchase

Elabed & Carter Impacts of Insurance in Mali

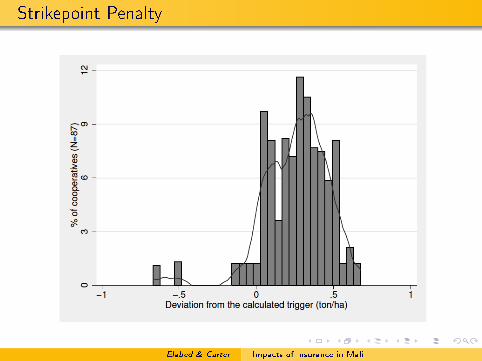

Strikepoint Penalty

Elabed & Carter Impacts of Insurance in Mali