Embed Size (px)

Citation preview

EXAMINING SACHS AND WARNER’S MODEL OF NATURAL RESOURCE CURSE: IMPLICATIONS AND LESSONS FOR NATURAL RESOURCE-RICH

COUNTRIES

A Thesis submitted to the Faculty of the

Graduate School of Arts & Sciences in partial fulfillment of the requirements for

the degree of Master of Public Policy in the Georgetown Public Policy Institute

By

Anne Hong, A.B.

Washington, D.C. April 8, 2009

ii

EXAMINING SACHS AND WARNER’S MODEL OF NATURAL RESOURCE CURSE: IMPLICATIONS AND LESSONS FOR NATURAL RESOURCE-RICH COUNTRIES

Anne Hong, A.B.

Thesis Advisor: Tobias Pfutze, Ph.D.

ABSTRACT

This thesis explores the model of natural resource curse proposed by Jeffrey Sachs and

Andrew Warner (1995) in two parts. First, it re-creates the model to determine if the results are

time-specific. In other words, by extending the time period beyond 1970 to 1989, this thesis will

attempt to ascertain whether natural resource exports do, in fact, result, in slowed growth, as

measured by GDP in a cross-country analysis. Secondly, it will attempt to develop arguments for

why differences in time-specific results are produced, testing theories regarding human capital

investment, debt overhang, and country size effects on the so-called “resource curse.”

Essentially, the theory behind Dutch Disease and natural resource curse has two

purported effects that limit growth. One hypothesis argues that natural resources result in trade

shocks because commodity markets are naturally volatile. Consequently, appreciation in

exchange rates leaves the natural resource economy in a depressed state following such boom and

bust cycles. A second hypothesis is that the investment in the booming sector (natural resource

sector) produces small contributions to overall growth as lagging sector resources move to the

booming sector.

Prior research has demonstrated that the effects of a “natural resource curse” do, to some

extent, exist, however, the defined time period by which such a curse persists (or the time period

in which it can be overcome) has never really been defined. Emulating the original model as

closely possible, this thesis attempts to ascertain whether Dutch Disease is a temporary problem

or one that persists over longer time periods. The question becomes, then, whether countries

iii

learn to correct for the problems of over-investment in the booming sector as well as rent-seeking

over time. While the period that Sachs and Warner (1995) examine is comprehensive (measuring

about 19 years of data), the effects for a recent time period (1990 to 2003) and for an extended

time period (1970 to 2003), demonstrate the effects of the natural resource curse are not, in fact,

constant. While the extended time model demonstrates a substantial effect of primary resource

exports on GDP growth, the most recent time period model does not. With this in mind, what are

the policy implications of natural resource curse? Is it a time-specific curse that can only be

observed over specific time periods? Or is there something inherent in the economy of the 1990s

that addresses why share of exports in natural resources is not statistically significant for growth?

In addition to attempting to ascertain the reasons behind time-specific results for natural

resource curse, the thesis will examine three potential theories: the argument that export

concentration is the cause of natural resource curse (as opposed to actual natural resources

serving as the root cause of the problem), the argument that human capital investment can often

mitigate the negative effects of natural resource dependence, and finally, debt overhang as the

causal mechanism behind the resource curse.

With these theories in mind, this thesis will attempt to answer some of the questions

about policy-making in light of Dutch Disease and Natural Resource Curse if it is, in fact, an

intractable problem.

iv

TABLE OF CONTENTS

I. Introduction........................................................................................................................1-5

II. Background and Literature Review.................................................................................5-14

III. Conceptual Framework and Hypothesis.........................................................................14-16

IV. Data and Methods...........................................................................................................16-17

V. Summary Statistics.........................................................................................................17-19

VI. Regression Results.........................................................................................................20-28

VII. Discussion and Conclusion............................................................................................28-31

VIII. References......................................................................................................................32-34

1

I. Introduction

This thesis explores the phenomenon known as Dutch Disease by utilizing the model of

Jeffrey Sachs and Andrew Warner (1995) as a basis for understanding potential theories

surrounding Dutch Disease and Natural Resource Curse. The concept of the Dutch Disease

gained momentum following the post-World War II era as numerous Latin American countries

suffered from economic problems following slumps in commodity prices. While there is cursory

evidence of this “curse” (as a brief examination of a scatter plot of commodity-rich countries and

GDP growth generally plots a negative relationship), this thesis utilizes an econometric model

developed by Sachs and Warner (1995) in addressing the time conundrum of the curse, that is to

say, to discern whether the findings hold up for a different time period altogether and whether the

effects of slow growth are not as significant when dealing with longer time periods than that

which was originally utilized in their study. Upon emulating the model and subsequently testing

it for the time period 1970 to 2003 and 1990 to 2003, one finds that the results are not statistically

significant for the 1990 to 2003 period. With this said, there may be implications for re-assessing

the original Sachs and Warner (1995) model and testing additional variables to explain the tested

effects.

In attempting to determine why the discussed effects are significant for 1970 to 2003 and

not for 1990 to 2003, three possible arguments are examined: human capital investment as a

policy measure to fight the resource curse, natural resource as a measure of export concentration,

and natural resource curse as debt overhang.

Specifically, because unsatisfactory growth performance is often associated with low

levels of human capital as well as high risk (which limits public and private investment), the

model should go beyond simply controlling for “rule of law” and also employ human capital

indicators to ascertain whether a high proportion of natural resource exports does contribute to

2

slower growth when controlling for those factors which often accompany the macroeconomic

environments of Less Developed Countries (LDCs).

Birdsall, Pinckney, and Sabot (2001) have argued that countries can achieve equitable

growth through investments in human capital as it has positive effects on investments in savings,

investments, and increases productivity. Of course, the direction of causality, a priori, is not

entirely clear. Cross-country growth regressions show a general positive relationship between

educational attainment and growth rates. The problem, with resource-rich economies, then, is

that because resource rents are controlled by only a few firms, those owners (whether they are

private or public) capture rents rather than investing them. Secondly, because income is

concentrated in the booming sector, incomes for other tradables fall, reducing the incentives for

educational attainment.

Sachs and Warner (1995) do not fully examine the effects of human capital investment on

GDP growth; and while it is unlikely that the addition of such a variable could have a hugely

dramatic impact on the model’s results, it is a question which has important policy implications.

Consequently, the addition of the variable for human capital seems to be theoretically supported.

The Sachs and Warner (1995) model evinces additional questions regarding the effects of

Dutch Disease on large versus small countries. From a non-causal perspective, it is clear that

agriculture and natural resource exports comprise a declining proportion of GDP as GNP per

capita increases. Syrquin and Chenery (1975, 1989) conducted exhaustive studies to determine

the relationships between several sectors (manufacturing, services, agriculture, and utilities) and

GDP and GNP per capita. In examining the structure of value added in GDP by country resource

endowment (large country with manufacturing sector, small country with primary sector, large

country with primary sector, and small country with manufacturing sector), the relationships for

the sectors and share of GDP hold across the different country samples. In general, as GNP per

3

capita increases (from USD 250 to 4,000), the share of GDP for agricultural sector declines while

the share for utilities, manufacturing, and services increases, albeit at differing rates.1 What these

relationships indicate, generally, is that the benefits of primary exports decrease as GNP per

capita increases; and furthermore, it indicates that development of the manufacturing and/or

services sector is more beneficial relative to other sectors for overall economic growth.

A secondary implication of the Syrquin and Chenery (1975, 1989) study is that country

size may matter. Auty and Kiiski (2001) bolster the argument, purporting that large resource-

abundant countries have “two advantages over the small ones for sustaining economic growth.

First, the probability of depending on one or two primary exports is lower for large countries than

for small ones...second, trade accounts for a smaller share of GDP in large economies so that they

are more self-contained and therefore less vulnerable to external shocks.”2 It may be argued,

then, that the effects of Dutch Disease are not constant; in other words, it affects countries with

fewer exports in a negatively more dramatic way and furthermore, that price shocks then have far

more detrimental effects on GDP growth for smaller countries. As such, this thesis will build on

the initial Sachs and Warner (1995) model to ascertain a better understanding of how natural

resources can impact growth and if it is environment-specific (i.e. when commodity price

fluctuations are high versus low, etc.)

A final and third concern of the thesis involves the question of natural resources as a

proxy for debt overhang. If results are time-specific, what can we glean from environmental

impacts and the effects on this natural resource curse phenomenon? The 1970s were marked by

high commodity prices which then underwent a bust in the 1980s. In contrast, the 1990s were

marked by similar boom and bust but on a substantially smaller scale (with less volatility). If that

1 Auty, R.M. and S. Kiiski. “Natural Resources and Welfare.” Resource Abundance and Economic Development. Ed. R.M. Auty. Oxford: Oxford University Press, 2001, 21. 2 Auty, Kiiski, 28-29.

4

is the case, then perhaps the Dutch Disease phenomenon is actually the result of a separate causal

mechanism: because countries use natural resources as collateral, the volatility in prices reduces

a countries ability to pay external debt when bust cycles occur. If this is assumed, the Dutch

Disease can only be observed over periods of time in which the real price appreciation increases

were dramatic and volatile (perhaps more so than those observed in the 1990s.)

Of the studies conducted on Dutch Disease, one might ask why, specifically, the model of

Sachs and Warner was chosen. While a very simple regression study demonstrates that negative

relationships exist between natural resource endowments and GDP growth, Sachs and Warner do

have some hesitations in accepting models of other authors. The study of Doppelhofer et al.

(2000), for example, has omitted variable bias, as it did not control for a number of other possible

factors which might have explained the negative relationship between natural resource

endowments and growth. An illustration of this concern, as pointed out by Sachs and Warner,

was geography. Paul Collier and other economic development theorists have argued that there is

some relationship between geography and growth (especially with countries that are land-locked),

and Sachs and Warner tackle this issue through their liberal use of other trade “openness” factors

which can serve as indicators for such non-quantifiable factors such as geography.

Furthermore, Sachs and Warner were the first to confirm the theory of Dutch Disease on

a comparative, worldwide level.3 Given that it is the most comprehensive econometric study, to

date, with regard to the natural resource curse, this thesis will utilize the model and methods as a

basis for determining the effects of natural resource exportation for a period of time beyond 20

years.

3 Sachs, Jeffrey and Andrew Warner. “Natural Resource Abundance and Economic Growth.” Center for International Development and Harvard Institute for International Development, Working Paper. Harvard University, November 1997, 3.

5

Counterexamples have not been particularly compelling in providing substantial

econometric evidence to refute the study of Sachs and Warner, though some authors have pointed

out that countries such as Finland, Sweden, and Canada continue to rely heavily on natural

resource exports but do not suffer from economic stagnation. While these studies do serve as

strong counter-examples of natural resource exports and GDP growth, they do not, in and of

themselves, wholly produce robust enough findings to generally refute the theory of Dutch

Disease.

II. Background and Literature Review

The Natural Resource Curse is characterized, primarily, by the theory of Dutch Disease

which expounds upon the chief problems associated with high concentration in exports in the

natural resource sector. The term Dutch Disease refers to the adverse effects on Dutch

manufacturing following the natural gas discoveries in the 1960s. The increase in natural gas

exports led to appreciation of the Dutch real exchange rate from high earnings from the export of

gas; but that increase in exchange rate was subsequently deleterious to the previously competitive

exporters. Production of non-gas exports thereby decreased, resulting in slowed economic

growth overall.

The core model of Dutch Disease assumed by this thesis is presented by Corden and

Neary (1982) as a Booming Sector Model, in which three assumed sectors, namely, the Booming

Sector (B), Lagging Sector (L) and Non-Tradeables (N), produce goods facing world prices. The

resource boom then results in three effects: a spending effect, a relative price effect, and a

resource movement effect. Output is determined by economic inputs and labor. With regard to

the spending effect, a boom raises aggregate incomes of the factors initially employed (the causes

of the boom being either technical, windfall discoveries, or exogenous price increases). This

6

boom, then, subsequently results in a spending effect as the extra income from sector B is

invested directly or indirectly. Following from this, provided the income elasticity of demand for

N is elastic, the price of N relative to the prices of tradables will rise. This effect is known as real

appreciation.4 From drawing resources out of B and L and into N and drawing demand to B and

L.

In addition to the spending effect and real price appreciation, there is a resource

movement effect.5 As demand in labor in sector B increases, labor moves from L and N to B.

This result lowers output of the lagging sector, resulting in de-industrialization. These two effects

can have substantial impacts on the economies of primary export countries.

Finally, the third effect, the relative price effect, results as there is an appreciation in the

currency resulting from the boom. This effect reduces the domestic prices of exports and of

imports, which are competing with domestic output, reducing the rents of the booming sector.

The domestic prices of non-tradables rise with increased demand, so resources shift from

tradables to non-tradables, with a consequent reduction in exports and an increase in imports.6

The Dutch Disease phenomenon has become commonplace in economic development

literature, as numerous countries that have been heavily dependent on commodity exports have

experienced stagnated or stunted development. A cursory examination of heavy commodity-

exporting countries may seem to legitimate the claim, but a more thorough examination of the

effects of primary exports over a substantial period of time is crucial to understanding the impact

of commodity exports on GDP.

4 Corden, W.M. “Booming Sector and Dutch Disease Economics: Survey and Consolidation.” Oxford Economic Papers. New Series, Vol. 36, No. 3., (Nov., 1984), 360. 5 Ibid. 6 Auty, R.M. Resource Abundance and Economic Development. Ed. R.M. Auty. Oxford: Oxford University Press, 2001, 7.

7

Fluctuations in international primary markets, resulting from high levels of natural

resource exports, make investment, both in the public and private sector, relatively difficult.

Secondly, the “secular movements in the terms of trade” of many primary products can leave

producers in a weak position.7 While manufactured goods have increasingly comprised a higher

percentage of total good traded, those countries that do trade primary sector goods tend to have

higher percentage of total trade in primary goods. As a result, there are concerns about the effects

that such high levels of commodity exporting can have on those respective economies. For

countries with a large share of exports in natural resources, the combination of these effects has a

compounding effect to produce a lessened future potential for exporting manufactured goods and

diversifying the production base.8

Sachs and Warner (1995 and 2001) effectively summarize the “curse of natural

resources” through a country-level econometric study that utilizes share of primary exports as a

key independent variable to determine effects on GDP growth over a nearly twenty year period.

Sachs and Warner summarize the studies of Auty (1990), Gelb (1988), and Sachs and Warner

(1995 and 1999) to show alternative studies in demonstrating the effect of natural resource

exports on economic growth and find that the inclusion of alternative variables and methods

supports the “natural resource curse” theory.

So, then, with the aforementioned problems with natural resource exports, what are the

potential treatments for mitigating the negative impact of resource endowment(s)? In dealing

with the question of savings, Collier and Gunning (1999) do a cross-country examination of a

handful of studies, examining disparities in results from private savings versus public savings and

the length of the specific commodity price booms in question. While they theorize that public 7 Abrams, F. Gerard and Jere R. Behrman. Commodity Exports and Economic Development. Lexington: Lexington Books, 1982, 3. 8 Murshed, S.M. “Contrasting Natural Resource Endowments.” Resource Abundance and Economic Development. Ed. R.M. Auty. Oxford: Oxford University Press, 2001, 115.

8

savings may help mitigate the effects of trade shocks, a corresponding outcome would then be

that Dutch Disease effects would be mitigated. The problem with examining the effects of

savings rates in numerous natural resource-rich countries is that many of those countries,

particularly in Africa, lack the infrastructure, transparency, and accountability to ensure that the

windfall gains benefit the entire population as opposed to just government officials. Windfall

gains in these countries have been wasted in many cases, but the development of a Stabilization

Account, through the help of the World Bank, has been heralded as a potential solution for the

misuse of windfall gains.9 While one cannot econometrically test the effects of an externally

created savings account (for lack of data and relative youth of the institution of such programs),

the examination of domestic savings in light of price shock expectations may be an important

variable to control for, given that it has been theorized to help smooth production cycles and price

volatility in commodity markets. Many economists point to the case of Norway as a government

that successfully instituted transparency and savings to overcome the effects of the natural

resource curse; and if this is the case, perhaps the question is not whether natural resource curses

are intrinsically linked to poor growth but whether the treatment of such endowments results in

poor economic results.

Having considered the limitations of including the effects of specific Stabilization

Accounts on GDP growth (because of a paucity of data in adequately measuring those effects),

the thesis will accept the Sachs and Warner (1995) model’s inclusion of domestic investment as a

proxy for potentially measuring the effects of investment on natural resource export

concentration.

9 Jerome, Afeikhana. “Unit 1: Practical Proposals for Lifting the Oil Curse in Nigeria.” Africa – Commodty Dependence, Resource Curse, and Export Diversification. Ed. Karl Wohlmuth, Chicot Eboue, Achim Ugtowski, Afeikhena Jerome, Tobias Knedlik, Mareike Meyn, Touna Mama. New Brunswick: Transaction Publishers, 2007, 105.

9

The comprehensive inclusion of variables (rule of law, domestic investment, trade

openness, and terms of trade) that Sachs and Warner (1995) employ provided a compelling

reason to use the Sachs and Warner (1995) model as a basis for this thesis. The model was

chosen for its comprehensive scope and full inclusion of variables that had previously not been

included in such a panel study. However, what Sachs and Warner (1995 and 2001) do not answer

is how long the effect of Dutch Disease really takes in terms of time. Is it a phenomena that is

eventually ‘recoverable’ in some sense? Or are countries that suffer from such a disease destined

to continue down the path of stagnated growth? The question of time is an important one, as it

may have substantial policy effects. For countries suffering from Dutch Disease, is a concerted

effort away from natural resources sector the solution? Or can stagnated growth be expected for a

temporary period of time and eventually, the country will compensate for those losses in other

areas? By extending the time period and also replicating the study in a more recent period, this

thesis will attempt to ascertain what Dutch Disease effects are in terms of time.

Additionally, while the Sachs and Warner model is effective in addressing trade openness

and domestic investment in the economy, it does not address three policy questions that have

implications for Dutch Disease theory, namely, human capital investment, country size, and

environmental influences of commodity price volatility. This thesis will address the theory by

examining ideas posited by a number of authors with regard to attempts to “correct” for Dutch

Disease through policies aimed to mitigate the effects of the curse.

Human Capital Investment as a Mitigating Factor for Natural Resource Curse

An interesting theory with regard to the theory of Dutch Disease and natural resource

curse is that it may not be the natural resource sector itself that is the problem, but rather, the

macro-economic and societal ways in which natural resource abundance is handled. Having said

this, controlling for such factors that would mitigate certain effects of the “curse,” namely,

10

education and savings rates as well as country size, could lead to some insights about how to

handle such situations. Furthermore, as Botswana has often been cited as an example that has

escaped the curse, to some degree, and coincidentally has higher levels of investment in human

capital, there could be lessons gleaned from the non-fiscal policy treatment of the curse. While

countries have aggressively pursued attempts at protectionism, liberalization, tariffs, and

openness to help deter Dutch Disease effects, case studies regarding the use of savings to smooth

production or investment in education have not been exhausted by any means.

Going beyond the application of economics, society itself can manage some of the

negative aspects of the natural resource curse. As argued by Wohlmuth, natural resources can

enhance growth, but only if “negative effects on corruption on investment on openness to trade

and on human capital formation can be controlled.”10 While Sachs and Warner do effectively

address trade openness and corruption through the use of a Rule of Law Index, they do not

acknowledge the productivity or employment effect, that is to say, the resource sector will

employ labor and may often build an incentive to draw labor from other sectors (specifically in

service sectors or manufacturing) so incentives for education may then decrease. Additionally,

this result could potentially be offset by the development of technology in the natural resource

sector, increasing productivity and thereby producing incentives for human capital and education.

The problem, however, is that either way, the Sachs and Warner (1995) model does not control

for this variable. While Manzano and Rigobon (2001) have added human capital to a fixed-

effects model of Sachs and Warner, simply adding it to a non fixed-effects model may also

produce differing results from that which was originally produced.

10 Wolhmuth, Karl. “An Introduction: Abundance of Natural Resources and Vulnerability to Crises.” Africa – Commodity Dependence, Resource Curse and Export Diversification. Ed. Karl Wohlmuth, Chicot Eboue, Achim Gutowski, Afeikhena Jerome, Tobias Knedlik, Mareike Meyn, Touna Mama. New Brunswick: Transaction Publishers, 2007, 11.

11

Gylfason (2001) also explores the relationship between large natural resource

endowments and education, arguing that natural resource abundance has been theorized to reduce

public and private incentives to improve human capital because of high levels of non-wage

income. On the other hand, there are cases such as Botswana, where the rents from natural

resources have resulted in high education expenditures. Despite conflicting cases that do serve as

anomalies, the general trend is that across countries, public expenditures on education relative to

national income “are all inversely related to natural resource abundance.”11 Sachs and Warner

(1995) do not effectively examine this variable – and the consequential policy implications that

investment in education could have over particularly extended time periods (such as that

examined in this thesis), could be extremely enlightening in determining how to mitigate the

curse. Gylfason (2001) does preliminary cross-country examinations of public expenditures on

education and natural resource abundance, but does not extend the analysis to a full econometric

model that controls for a host of other variables. His argument hinges on a four-part effects

model of natural resource curse, arguing that the exchange rate effects, rent seeking, and

overconfidence produces stagnations in economic development, but additionally, that public and

private incentives for human capital are reduced.

Country Size and Dutch Disease: the “Staple Trap”

Large resource-abundant countries have been demonstrated to have certain advantages

over the smaller countries with regard to sustaining economic growth. First, the likelihood of

staple dependence (that is, dependence on a few exports) is smaller for larger countries and

secondly, because large countries likely have more diversified natural resources, it may have a

higher likelihood of diversifying into the manufacturing sector because large markets allow for

11 Gylfason, Thorvaldur. “Lessons from Dutch Disease: Causes, Treatments, and Cures.” The Paradox of Plenty (STATOIL- ECON conference volume), 22 March 2001. http://www3.hi.is/~gylfason/pdf/statoil22.pdf

12

economies of scale. Additionally, trade accounts for a smaller share of GDP in large economies

and thus, they are less vulnerable to trade shocks. Syrquin and Chenery (1989) did an extensive

study on the effects of agriculture as a share of GDP in large countries versus smaller countries

and found that the share of agriculture in GDP declined more slowly in large countries than in

any other endowment category.12

In addition to the increased susceptibility of smaller countries to trade shocks as well as

the lack of diversification in exports, smaller countries also have been observed, historically, to

take a longer time to diversify into production and manufactured goods. While Syrquin and

Chenery (1989) specifically explore the differences in trends between different primary exports

(agricultural products versus mineral products), this thesis does not differentiate between the

different sectors. Rather, it will attempt to address this issue of country size as a potential control

variable for the effects of Dutch Disease.

Lederman and Maloney (2006) argue that export concentration is the reason behind

econometric models that have demonstrated the effect of this resource curse. As such, this

concentration “of export revenues reduces growth by hampering productivity and...[export

concentration], rather than natural resources, per se, drives...[the] negative impact of natural

resource exports over total exports, a proxy that we, in the end see as measuring concentration.”13

Dependence on a single export, which is usually the case for resource-rich countries, can thereby

make a country increasingly susceptible to sharp declines in terms of trade. Using estimation

techniques that use differing methods of natural resource endowments (specifically Leamer’s

calculation of net natural resource exports per worker) shows significance but positive

relationship with growth as opposed to negative. 12 Auty, R.M. and S. Kiiski, 29. 13 Lederman, Daniel and William F. Maloney. “Trade Structure and Growth.” Natural Resources: Neither Curse nor Destiny. Ed. Daniel Lederman and William F. Maloney. Palo Alto: Stanford University Press, 2007, 16.

13

Natural Resource Curse as a mechanism of Debt Overhang

A third, and relatively newer theory, questioning the natural resource curse is that

proposed by Manzano and Rigobon (2007). Manzano and Rigobon do not attempt to refute the

natural resource curse in its entirety, but rather, attempt to describe a specific causal mechanism

that may be producing the results found in the Sachs and Warner (1995) study that could be

operating outside of simply the Dutch Disease phenomenon.

Manzano and Rigobon (2007) complete both fixed-effects and cross-sectional models and

find that the natural resource curse effect persists in cross-sectional studies but not in those using

fixed effects. So, then, in an attempt to determine omitted variables that may be causing such

results, they pinpoint credit constraints and debt overhang as a possible explanation. In showing

debt growth and its correlation with resource abundance, the relationship is relatively strongly

positive. And interestingly, those countries with very negative growth and high level of resources

also demonstrated large jumps in debt-to GDP ratios.

However, this relationship between debt and natural resources is not uni-dimensional.

Examining the commodity prices in the 1970s and 1980s, Manzano and Rigobon make a

compelling argument that perhaps large swings in nominal commodity prices of coal, copper,

iron, and oil all experienced great booms in the early part of the period between 1970 and 1990

only to suffer large drops by the 1980s (all of them as much as 30%). Given such price volatility,

the findings result in disparate results when dividing the regression between 1970-1980 and 1980-

1990. With the addition of credit constraints as a variable on a sliding scale of debt to GNP, the

authors find that non-agricultural exports (the variable of interest) becomes insignificant and the

debt variable becomes strongly significant.

Manzano and Rigobon (2007) do take liberty in altering the core structure of the model;

and as such, this thesis will attempt to maintain the core of the Sachs and Warner (1995) model

14

rather than altering the calculation of natural resource endowment or model specification, and

instead, attempt to address why the results of the Sachs and Warner (1995) study are, in fact, time

dependent.

With these three primary theoretical questions in mind, this thesis will proceed as

follows: emulating the original Sachs and Warner (1995) model to ensure sound econometric

methods of emulation, then extending the time period beyond 1989 to 2003 and subsequently

testing for the period 1990 to 2003 along with a re-examination of the original model utilizing

additional variables.

III. Conceptual Framework and Hypothesis

The question of Dutch Disease and natural resource curse is an interesting one with

regard to development; moreover, it is crucial to understand whether its effects are real, in the

sense that so much of the developing world is rich in commodities, and yet, so many of these

countries have been unable to harness the advantages of booming commodity prices (especially in

oil), to create sustainable development and economic growth. Consequently, the research

question poses the question first posed by Sachs/Warner in that it asks whether Dutch Disease

does, in fact, exist.

The hypothesis, then, is do the effects of Dutch Disease continue beyond 20 years? Or

more specifically, does natural resource abundance have a stagnating effect on economic

development over a time period as long as 33 years (1970 to 2003)? In addition, while this

natural resource curse has been evident for historical periods, is it still relevant when examining

natural resource endowments from the period 1990 to 2003?

Furthermore, the question of the combination of macroeconomic factors as well as

societal and governance factors need to be controlled for in order to ascertain exactly what the

15

effects of natural resource endowments are. Specifically, the problem with some empirical

studies that do not involve econometric models have adequately demonstrated that numerous

LDCs lack development and growth despite large natural resource endowments; however, many

of those countries have been enmeshed in civil war or have extremely corrupt governments that

do not handle the windfall gains from natural resources in an effective manner. With that said,

the conceptual framework will examine the different sort of factors that could result in explaining

natural resource curse by controlling for such things as human capital, rule of law, terms of trade,

etc.

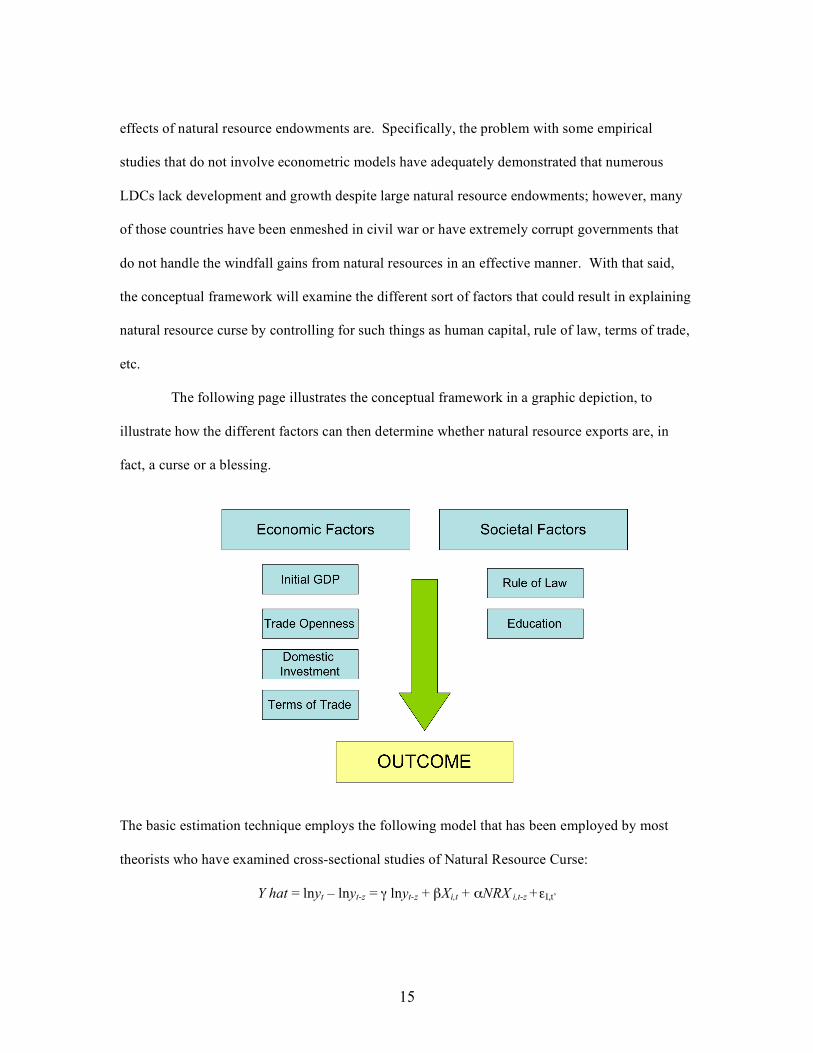

The following page illustrates the conceptual framework in a graphic depiction, to

illustrate how the different factors can then determine whether natural resource exports are, in

fact, a curse or a blessing.

The basic estimation technique employs the following model that has been employed by most

theorists who have examined cross-sectional studies of Natural Resource Curse:

Y hat = lnyt – lnyt-z = γ lnyt-z + βXi,t + αNRX i,t-z +εI,t’

16

This stylized model utilizes growth rate of GDP per capita as the dependent variable. This is

measured as the differences in the natural logarithms of income per capita between the year t and

the initial year t-z. Utilizing the Barro (1991) specification, Sachs and Warner (1995) regress this

on the initial log of income per capita.

While this model has incited criticism from Lederman and Maloney (2006) among others

for endogeneity problems, specifically with regard to the initial level of income and its high

correlation with growth and the interdependence of growth-related variables, as pointed out by

Knight, Loayza, and Villanueva (1993), the core model did theoretically support the purported

theory of Natural Resource Curse. And because this thesis is essentially testing time effects of

the original Sachs and Warner (1995) model, the fundamental OLS model will not be altered,

save for the addition of new independent variables.

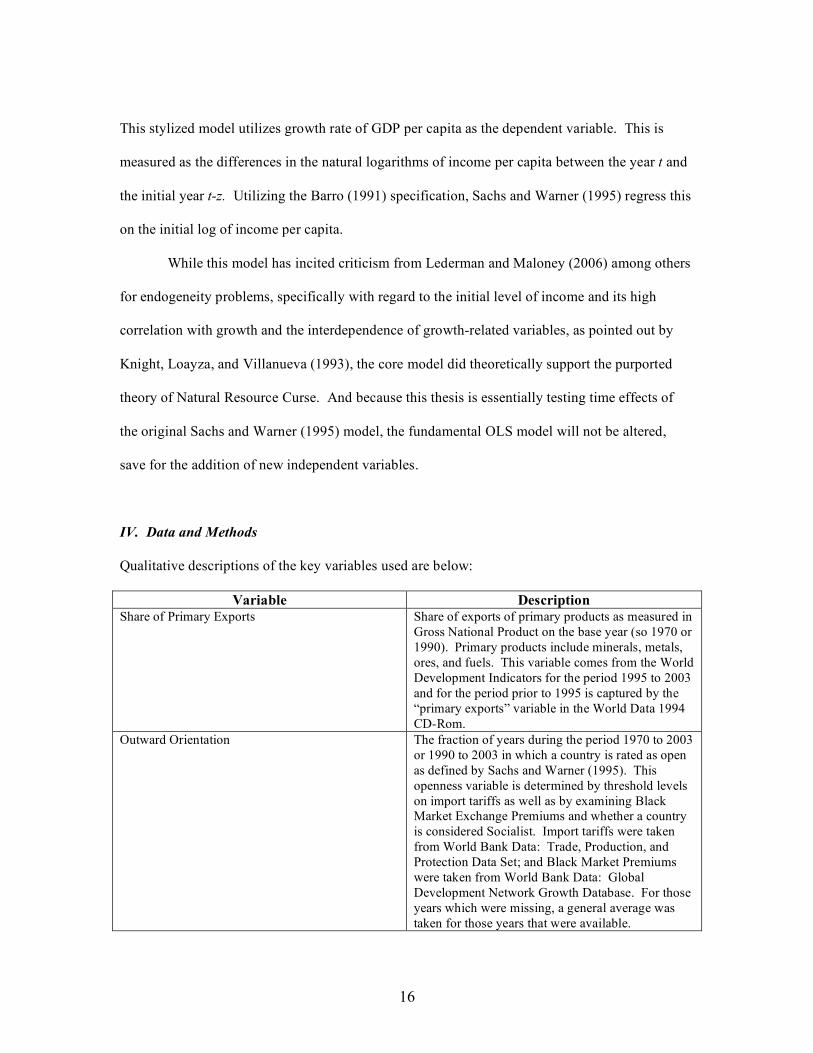

IV. Data and Methods Qualitative descriptions of the key variables used are below:

Variable Description Share of Primary Exports Share of exports of primary products as measured in

Gross National Product on the base year (so 1970 or 1990). Primary products include minerals, metals, ores, and fuels. This variable comes from the World Development Indicators for the period 1995 to 2003 and for the period prior to 1995 is captured by the “primary exports” variable in the World Data 1994 CD-Rom.

Outward Orientation The fraction of years during the period 1970 to 2003 or 1990 to 2003 in which a country is rated as open as defined by Sachs and Warner (1995). This openness variable is determined by threshold levels on import tariffs as well as by examining Black Market Exchange Premiums and whether a country is considered Socialist. Import tariffs were taken from World Bank Data: Trade, Production, and Protection Data Set; and Black Market Premiums were taken from World Bank Data: Global Development Network Growth Database. For those years which were missing, a general average was taken for those years that were available.

17

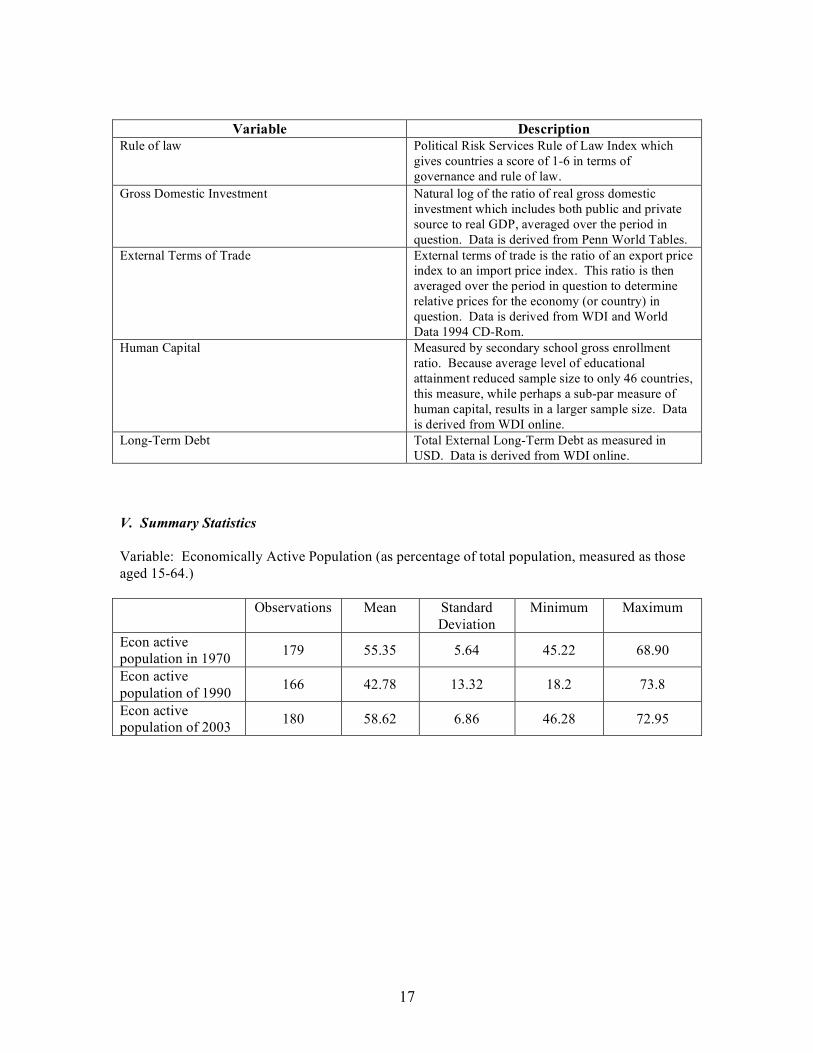

Variable Description Rule of law Political Risk Services Rule of Law Index which

gives countries a score of 1-6 in terms of governance and rule of law.

Gross Domestic Investment Natural log of the ratio of real gross domestic investment which includes both public and private source to real GDP, averaged over the period in question. Data is derived from Penn World Tables.

External Terms of Trade External terms of trade is the ratio of an export price index to an import price index. This ratio is then averaged over the period in question to determine relative prices for the economy (or country) in question. Data is derived from WDI and World Data 1994 CD-Rom.

Human Capital Measured by secondary school gross enrollment ratio. Because average level of educational attainment reduced sample size to only 46 countries, this measure, while perhaps a sub-par measure of human capital, results in a larger sample size. Data is derived from WDI online.

Long-Term Debt Total External Long-Term Debt as measured in USD. Data is derived from WDI online.

V. Summary Statistics Variable: Economically Active Population (as percentage of total population, measured as those aged 15-64.)

Observations Mean Standard Deviation

Minimum Maximum

Econ active population in 1970 179 55.35 5.64 45.22 68.90

Econ active population of 1990

166 42.78 13.32 18.2 73.8

Econ active population of 2003 180 58.62 6.86 46.28 72.95

18

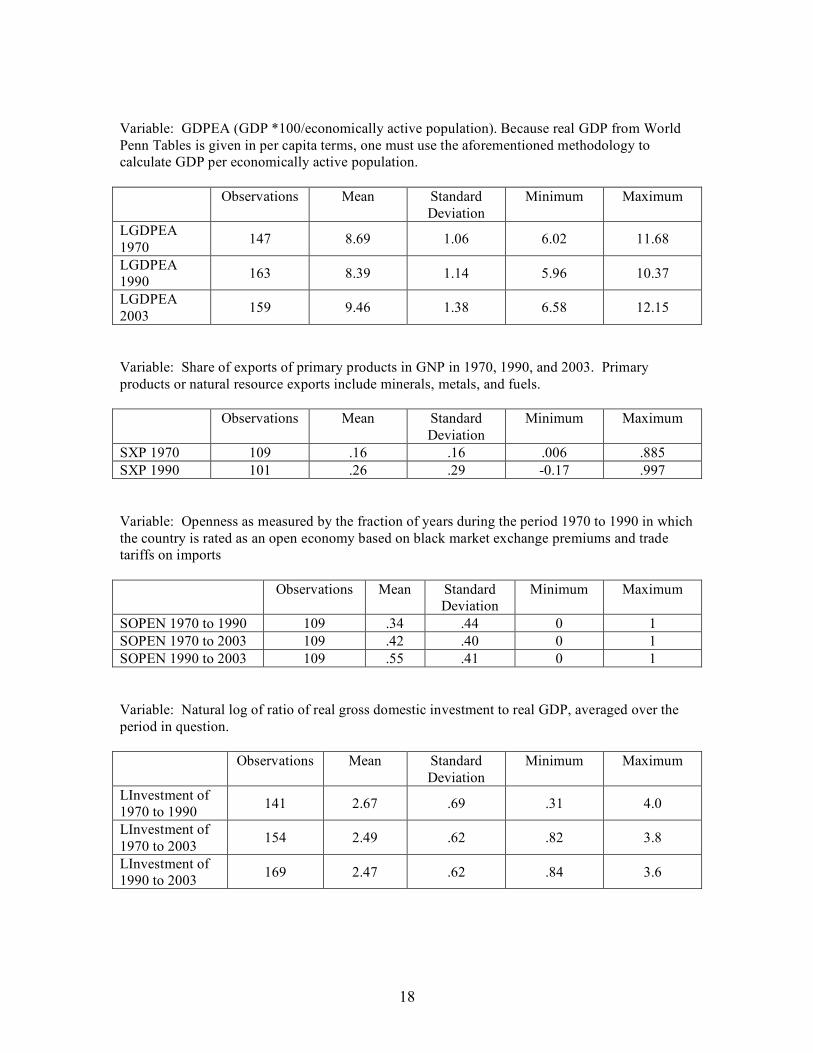

Variable: GDPEA (GDP *100/economically active population). Because real GDP from World Penn Tables is given in per capita terms, one must use the aforementioned methodology to calculate GDP per economically active population.

Observations Mean Standard Deviation

Minimum Maximum

LGDPEA 1970

147 8.69 1.06 6.02 11.68

LGDPEA 1990 163 8.39 1.14 5.96 10.37

LGDPEA 2003

159 9.46 1.38 6.58 12.15

Variable: Share of exports of primary products in GNP in 1970, 1990, and 2003. Primary products or natural resource exports include minerals, metals, and fuels.

Observations Mean Standard Deviation

Minimum Maximum

SXP 1970 109 .16 .16 .006 .885 SXP 1990 101 .26 .29 -0.17 .997 Variable: Openness as measured by the fraction of years during the period 1970 to 1990 in which the country is rated as an open economy based on black market exchange premiums and trade tariffs on imports

Observations Mean Standard Deviation

Minimum Maximum

SOPEN 1970 to 1990 109 .34 .44 0 1 SOPEN 1970 to 2003 109 .42 .40 0 1 SOPEN 1990 to 2003 109 .55 .41 0 1 Variable: Natural log of ratio of real gross domestic investment to real GDP, averaged over the period in question.

Observations Mean Standard Deviation

Minimum Maximum

LInvestment of 1970 to 1990 141 2.67 .69 .31 4.0

LInvestment of 1970 to 2003

154 2.49 .62 .82 3.8

LInvestment of 1990 to 2003 169 2.47 .62 .84 3.6

19

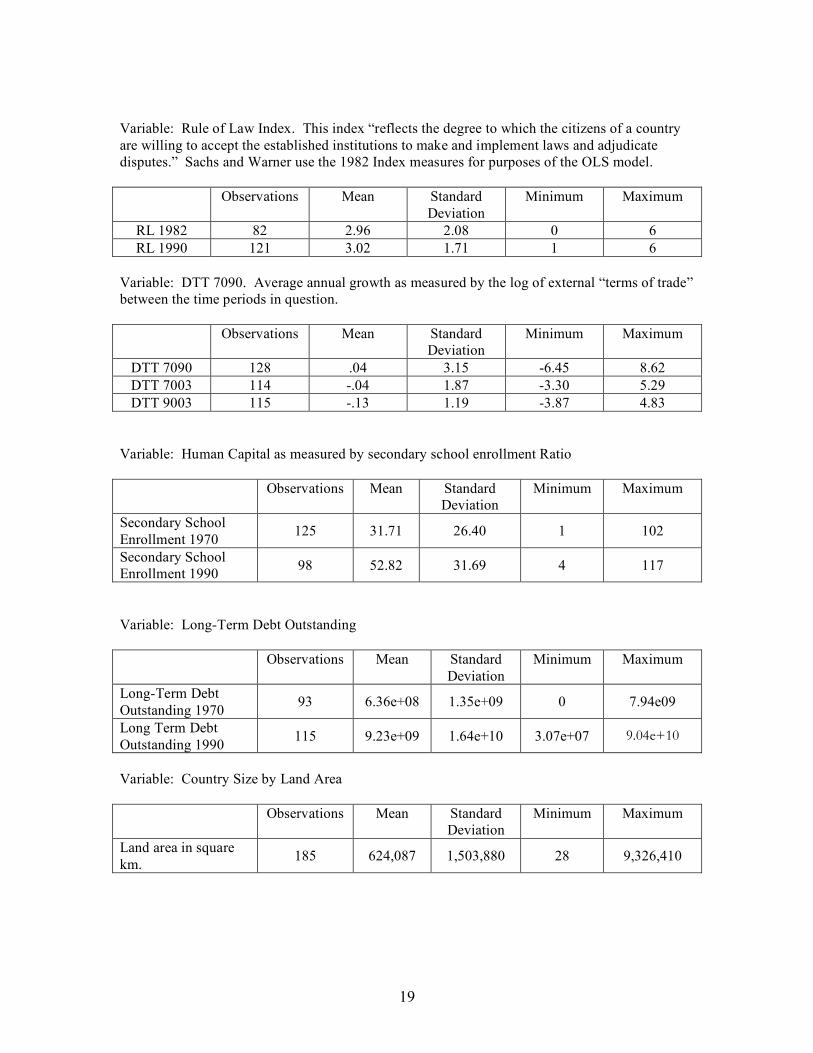

Variable: Rule of Law Index. This index “reflects the degree to which the citizens of a country are willing to accept the established institutions to make and implement laws and adjudicate disputes.” Sachs and Warner use the 1982 Index measures for purposes of the OLS model.

Observations Mean Standard Deviation

Minimum Maximum

RL 1982 82 2.96 2.08 0 6 RL 1990 121 3.02 1.71 1 6

Variable: DTT 7090. Average annual growth as measured by the log of external “terms of trade” between the time periods in question.

Observations Mean Standard Deviation

Minimum Maximum

DTT 7090 128 .04 3.15 -6.45 8.62 DTT 7003 114 -.04 1.87 -3.30 5.29 DTT 9003 115 -.13 1.19 -3.87 4.83

Variable: Human Capital as measured by secondary school enrollment Ratio

Observations Mean Standard Deviation

Minimum Maximum

Secondary School Enrollment 1970

125 31.71 26.40 1 102

Secondary School Enrollment 1990 98 52.82 31.69 4 117

Variable: Long-Term Debt Outstanding

Observations Mean Standard Deviation

Minimum Maximum

Long-Term Debt Outstanding 1970

93 6.36e+08 1.35e+09 0 7.94e09

Long Term Debt Outstanding 1990

115 9.23e+09 1.64e+10 3.07e+07 9.04e+10

Variable: Country Size by Land Area

Observations Mean Standard Deviation

Minimum Maximum

Land area in square km. 185 624,087 1,503,880 28 9,326,410

20

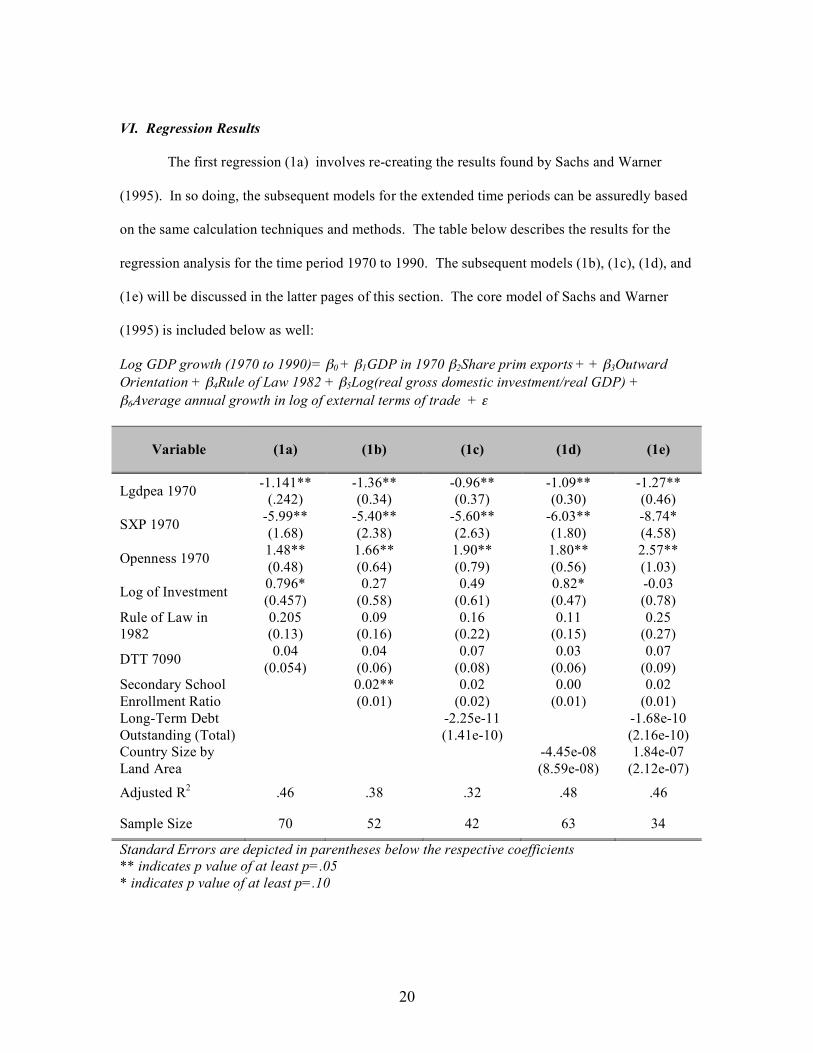

VI. Regression Results

The first regression (1a) involves re-creating the results found by Sachs and Warner

(1995). In so doing, the subsequent models for the extended time periods can be assuredly based

on the same calculation techniques and methods. The table below describes the results for the

regression analysis for the time period 1970 to 1990. The subsequent models (1b), (1c), (1d), and

(1e) will be discussed in the latter pages of this section. The core model of Sachs and Warner

(1995) is included below as well:

Log GDP growth (1970 to 1990)= β0 + β1GDP in 1970 β2Share prim exports + + β3Outward Orientation + β4Rule of Law 1982 + β5Log(real gross domestic investment/real GDP) + β6Average annual growth in log of external terms of trade + ε

Variable (1a) (1b) (1c) (1d) (1e)

Lgdpea 1970 -1.141** (.242)

-1.36** (0.34)

-0.96** (0.37)

-1.09** (0.30)

-1.27** (0.46)

SXP 1970 -5.99** (1.68)

-5.40** (2.38)

-5.60** (2.63)

-6.03** (1.80)

-8.74* (4.58)

Openness 1970 1.48** (0.48)

1.66** (0.64)

1.90** (0.79)

1.80** (0.56)

2.57** (1.03)

Log of Investment 0.796* (0.457)

0.27 (0.58)

0.49 (0.61)

0.82* (0.47)

-0.03 (0.78)

Rule of Law in 1982

0.205 (0.13)

0.09 (0.16)

0.16 (0.22)

0.11 (0.15)

0.25 (0.27)

DTT 7090 0.04 (0.054)

0.04 (0.06)

0.07 (0.08)

0.03 (0.06)

0.07 (0.09)

Secondary School Enrollment Ratio 0.02**

(0.01) 0.02

(0.02) 0.00

(0.01) 0.02

(0.01) Long-Term Debt Outstanding (Total) -2.25e-11

(1.41e-10) -1.68e-10 (2.16e-10)

Country Size by Land Area -4.45e-08

(8.59e-08) 1.84e-07

(2.12e-07)

Adjusted R2 .46 .38 .32 .48 .46

Sample Size 70 52 42 63 34

Standard Errors are depicted in parentheses below the respective coefficients ** indicates p value of at least p=.05 * indicates p value of at least p=.10

21

Per the specification of the Sachs and Warner (1995) model, the significant variables are

share of exports and log of initial gdp. For purposes of this thesis, the SXP is the variable which

is of utmost concern. Share of exports (SXP) is measured as a share of GDP; and thus, based on

the regression results, one can argue that a one unit increase in share of exports as a percentage of

GDP decreases GDP growth by 5.99% in real GDP. This effect is statistically significant at the

p=.001 level. In terms of other statistically significant factors, the degree of trade openness is

statistically significant at the p=.003 level. Its coefficient implies that an increase of one unit in

the fraction of years a country is considered “open to trade” (or 1/20 in this case, as it is captured

over a 20 year time period), implies a 1.48% increase in GDP.

Concerns:

Given the differences in the regression results between the model above and those

produced by Sachs and Warner (1995), a comparison of summary statistics was produced to

determine if the calculations involved in measuring certain variables was, in fact, disparate. The

comparisons with the Sachs and Warner (1995) summary statistics reveal that the general

summary statistics are, in fact, for the most part, akin to those of the authors. Consequently,

differences in data calculation and sources are not likely. Rather, their inclusion of several

countries using alternative data sources, namely, for Bangladesh, Bahrain, Botswana, Cape

Verde, China, Cyprus, Jordan, Iran, Myanmar, Taiwan, South Africa, Uganda, Singapore,

Trinidad, Zimbabwe, may be responsible for the different outcomes.

Because the level of significance matches the original Sachs and Warner, the model is

extended for the time period 1970-2003 in model (2a) to determine whether the results indicate

similar levels of significance for the variables in question.

22

Log GDP growth (1970 to 2003) = β0 + β1Share prim exports + β2GDP in 1970 + β3Outward Orientation + β4Rule of Law + β5Log(real gross domestic investment/real GDP) + β6Average annual growth in log of external terms of trade + ε

Variable (2a) (2b) (2c) (2d) (2e)

Lgdpea 1970 -0.90** (2.78)

-1.07** (0.33)

-1.04** (0.38)

-1.03** (0.33)

-1.04** (0.39)

SXP 1970 -7.74** (2.06)

-7.52** (2.19)

-6.63** (2.95)

-7.92** (2.21)

-6.65** (3.00)

Openness 1970 1.71** (0.72)

1.77** (0.82)

1.32 (1.01)

1.69** (0.81)

1.30 (1.03)

Log of Investment

1.29** (0.47)

1.24** (0.49)

0.73 (0.64)

1.30** (0.49)

0.75 (0.65)

Rule of Law in 1982

0.065 (0.14)

-0.04 (0.17)

0.25 (0.26)

-0.003 (0.17)

0.26 (0.27)

DTT 7090 0.149 (0.11)

0.14 (0.11)

0.20 (0.13)

0.13 (0.11)

0.20 (0.14)

Secondary School Enrollment Ratio

0.01 (0.01)

0.04* (0.02)

0.01 (0.01)

0.04* (0.02)

Long-Term Debt Outstanding (Total)

-5.19e-11 (1.59e-10) -3.25e-11

(1.98)e-10

Country Size by Land Area -1.27e-07

(1.03e-07) -4.01e-08 (2.34e-07)

Adjusted R2 .47 .48 .49 .49 .34

Sample Size 64 58 40 58 40

Standard Errors are depicted in parentheses below the respective coefficients ** indicates p value of at least p=.05 * indicates p value of at least p=.10

Based on the results from the regression above, openness, share of primary exports, and

log of initial GDP remain statistically significant. Thus, it may be implied that the Sachs and

Warner (1995) model is not time-specific.

Finally, a third time-specific model is examined for the period 1990 to 2003, model (3a).

Here, the same variables produced in the former two models are included, with the exception of

23

the years in question for the share of exports, Rule of Law Index, the original GDP, the terms of

trade, the log of domestic investment, and fraction of years of openness.

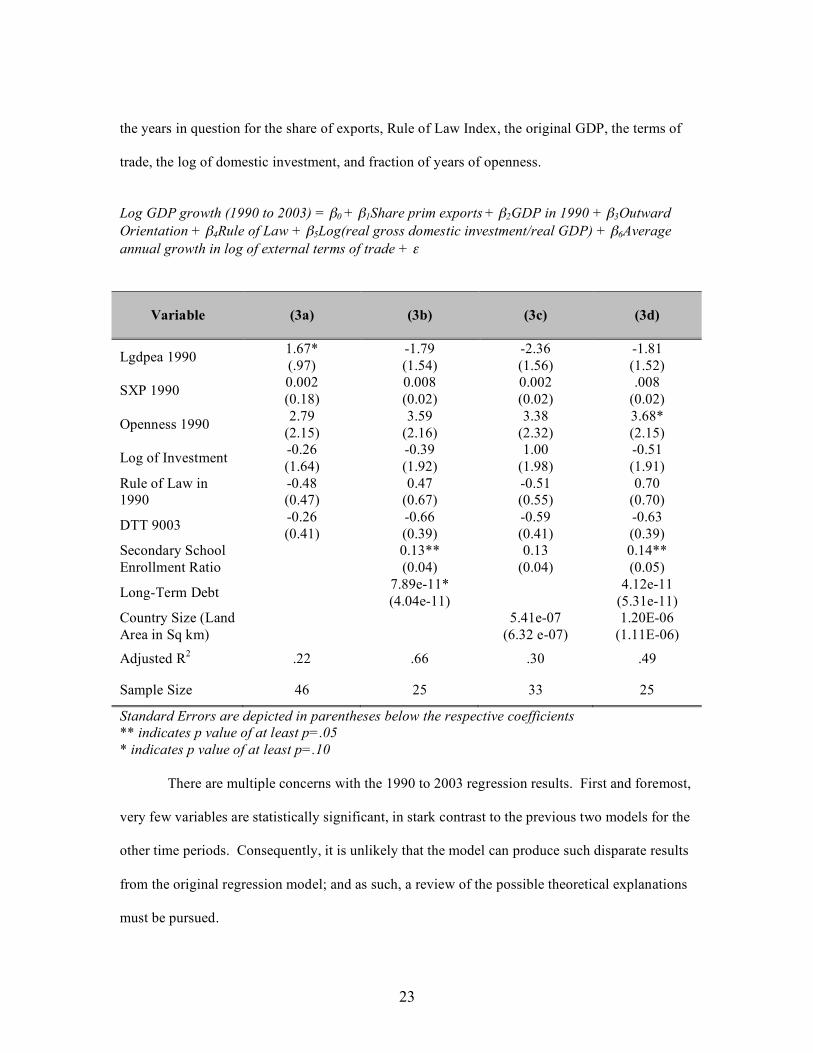

Log GDP growth (1990 to 2003) = β0 + β1Share prim exports + β2GDP in 1990 + β3Outward Orientation + β4Rule of Law + β5Log(real gross domestic investment/real GDP) + β6Average annual growth in log of external terms of trade + ε

Variable (3a) (3b) (3c) (3d)

Lgdpea 1990 1.67* (.97)

-1.79 (1.54)

-2.36 (1.56)

-1.81 (1.52)

SXP 1990 0.002 (0.18)

0.008 (0.02)

0.002 (0.02)

.008 (0.02)

Openness 1990 2.79 (2.15)

3.59 (2.16)

3.38 (2.32)

3.68* (2.15)

Log of Investment -0.26 (1.64)

-0.39 (1.92)

1.00 (1.98)

-0.51 (1.91)

Rule of Law in 1990

-0.48 (0.47)

0.47 (0.67)

-0.51 (0.55)

0.70 (0.70)

DTT 9003 -0.26 (0.41)

-0.66 (0.39)

-0.59 (0.41)

-0.63 (0.39)

Secondary School Enrollment Ratio 0.13**

(0.04) 0.13

(0.04) 0.14** (0.05)

Long-Term Debt 7.89e-11* (4.04e-11) 4.12e-11

(5.31e-11) Country Size (Land Area in Sq km) 5.41e-07

(6.32 e-07) 1.20E-06

(1.11E-06)

Adjusted R2 .22 .66 .30 .49

Sample Size 46 25 33 25

Standard Errors are depicted in parentheses below the respective coefficients ** indicates p value of at least p=.05 * indicates p value of at least p=.10

There are multiple concerns with the 1990 to 2003 regression results. First and foremost,

very few variables are statistically significant, in stark contrast to the previous two models for the

other time periods. Consequently, it is unlikely that the model can produce such disparate results

from the original regression model; and as such, a review of the possible theoretical explanations

must be pursued.

24

Possible Explanations:

It is possible that the notion of natural resource curse is time-dependent. Going back in

history, R. M. Auty has pointed out that natural resources, in the nineteenth century, were not

considered ‘curses’ for development; and that up until the 1960s, those countries that were rich in

natural resources, in fact, experienced higher average GDP than countries not-resource rich. In

effect, this presents a very real quagmire in relation to the theory of Dutch Disease and natural

resource curse: Is it time-specific? In other words, is it environment-specific? Given the oil

shocks of the 1970s, it is possible that the natural resource curse model of Sachs and Warner

(1995) is adequately demonstrating repercussions from the global oil shocks of the 1970s and

early 1980s rather than an inherent tendency for natural-resource countries to truly suffer from a

‘curse’ of sorts.

In recent years, the growth trajectory of resource-abundant countries has been positive,

with sustained rapid economic growth. What is interesting is that the effects of natural resources

on GDP are not equal across the sample of countries. Auty argues that smaller countries tend to

suffer from the effects of “natural resource curse” more so than larger countries. This effect

results as larger countries tend to have less dependency on just one or two primary exports

whereas smaller ones are more vulnerable to collapses.14 Per Auty, the effects of smaller

countries that have natural resources as a primary export may be dependent on only a handful of

exports whereas larger countries have more diverse exports.

In models (1d) and (1e) for the 1970 to 1990 period and models, (2d) and (2e) for the

1970 to 2003 period, an attempt to control for country size is made by including the land area in

square miles for the data set. The significance of the key variable, SXP, does not change given

the addition of the control. 14 Auty, R.M. Resource Abundance and Economic Development. Ed. R.M. Auty. Oxford: Oxford University Press, 2001, 7.

25

Other theorists have posited that demographic cycles play a substantial role in

determining outcomes of growth. Changing dependency ratios have been argued to accompany

changes in the demographic transition, which then, have implications for economic growth and

domestic investment and savings. The problem with this theory, however, is that a cursory

examination of demographic transitions and country-level GDP may, in fact, demonstrate such a

relationship, however, it is a difficult concept to prove causation in terms of direction of causality.

Looking at other potential policy explanations, there is a growing volume of literature

which argues that human capital investment plays a substantial role in lowering the growth rates

of resource-abundant countries. While Lederman and Maloney (working paper, 2002), have

addressed the question of human capital in a fixed-effects model, the addition of human capital

and risk index measures to the basic Sachs and Warner model (1995) may lead to differing results

when controlling for those variables. Birdsall, Pinckney, and Sabot make the astute observation

that resource-abundant countries tend to invest less in education. Governments in resource-rich

countries may attempt to increase education efforts, but because the labor market in such

countries do not reward education, there is likely little investment beyond the natural resource

sector.15 Consequently, raising the rates of return for human capital can induce higher savings

and more investment, in addition to increased productivity. Many point to the investment in

human capital as one of the key factors in aiding the rapid growth of the Asian Tigers.

Determining the direction of causality with regard to education and GDP growth has been

a challenge. Barro-style cross-country regressions regarding growth have generally demonstrated

that education has significant impacts on growth rates; education increases wages but it

importantly also increases productivity (in resources sectors and otherwise). In addition to the

15 Birdsall, Nancy, Thomas Pinckney and Richard Scott. “Natural Resources, Human Capital, and Growth.” Resource Abundance and Economic Development. Ed. R.M. Auty. Oxford: Oxford University Press, 2001, 58.

26

direct impact that education has on output, it also has an indirect effect. Education generally

reduces inequality, which subsequently perpetuates growth. Education has also been

demonstrated to improve child health, which can then aid a country to transition to a different

demographic transition with lower fertility rates and increased savings and investment.

With this concept in mind, an additional regression was run utilizing the human capital as

measured by secondary school enrollment ratios (models (1b), (1c), (1d), (1d), (2b), (2c), (2d),

and (2e)). The problem with the primary school enrollment values was that the sample size was

reduced substantially when the secondary school enrollment ratio was included in the regression

model. As a result, this variable was included as an alternative to school enrollment rates.

It is clear from the results in regression 1 and 2 that the addition of the human capital

variable does not change the results dramatically for the original Sachs and Warner (1995) model

or the extended model from 1970 to 2003. The education variable is, however, statistically

significant, which demonstrates some effect of educational attainment on GDP growth. However,

because the sample size is reduced when adding the education variable, there is some concern that

the model may be biased because of small sample size.

So, then, how can one explain these curious results from 1990 to 2003? One thought is

that commodity prices underwent a boom and bust cycle between 1970 and 1990 as well as 1970

to 2003 that was less drastic or not present during the latter time period in the 1990s. However,

between 1990 to 2003, commodity prices did experience a boom and slight bust effect.

Consequently, it may be possible that fluctuations in commodity prices could provide a key to

determining why the resource curse existed from 1970 to 1990 and not between 1990 and 2003.

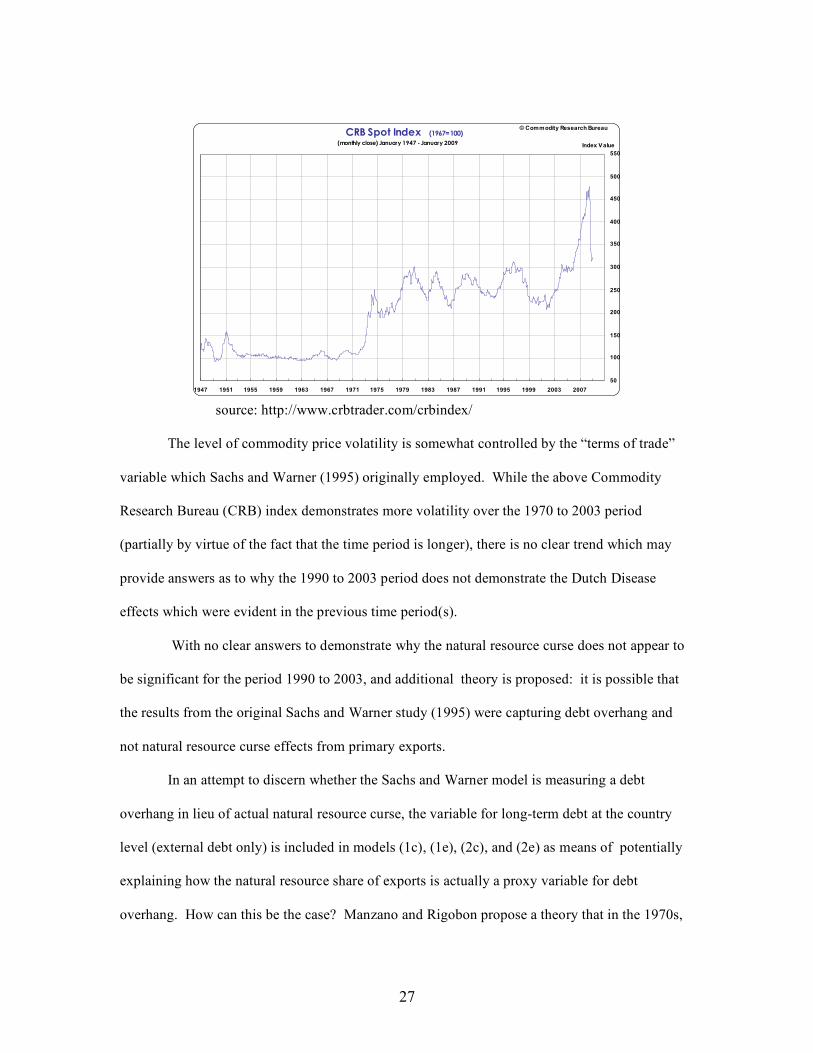

A cursory examination of the CRB commodity spot price index does not seem to hold any

answers.

27

CRB Spot Index (1967=100)

(monthly close) January 1947 - January 2009

50

100

150

200

250

300

350

400

450

500

550

1947 1951 1955 1959 1963 1967 1971 1975 1979 1983 1987 1991 1995 1999 2003 2007

© Commodity Research Bureau

Index Value

source: http://www.crbtrader.com/crbindex/

The level of commodity price volatility is somewhat controlled by the “terms of trade”

variable which Sachs and Warner (1995) originally employed. While the above Commodity

Research Bureau (CRB) index demonstrates more volatility over the 1970 to 2003 period

(partially by virtue of the fact that the time period is longer), there is no clear trend which may

provide answers as to why the 1990 to 2003 period does not demonstrate the Dutch Disease

effects which were evident in the previous time period(s).

With no clear answers to demonstrate why the natural resource curse does not appear to

be significant for the period 1990 to 2003, and additional theory is proposed: it is possible that

the results from the original Sachs and Warner study (1995) were capturing debt overhang and

not natural resource curse effects from primary exports.

In an attempt to discern whether the Sachs and Warner model is measuring a debt

overhang in lieu of actual natural resource curse, the variable for long-term debt at the country

level (external debt only) is included in models (1c), (1e), (2c), and (2e) as means of potentially

explaining how the natural resource share of exports is actually a proxy variable for debt

overhang. How can this be the case? Manzano and Rigobon propose a theory that in the 1970s,

28

the high commodity prices led to developing countries to utilize those commodities as collateral

for debt. When those prices fell in the 1980s, the significant fall left a majority of countries with

a considerable debt overhang. After exhaustive re-evaluation of the original Sachs and Warner

model using fixed effects models with panel data, the authors find that the natural resource curse

disappears. A plausible explanation for this result is that there is correlation with omitted

variables – and they propose this to be those with high debt (incidentally, those countries with the

most negative growth and large natural resources were those that also had significant increases in

their debt-to-GDP ratio between 1975 and 1985.16) While the models ((1c), (1e), (2c), and (2e))

utilized in this thesis did not seem to eradicate the negative significance of the SXP variable,

given the addition of the long-term debt variable, it differs from the Manzano and Rigobon (2007)

study in that regular cross-sectional analysis was used (in lieu of the panel data and models which

they employed). The model was based upon the original Sachs and Warner (1995) structure with

the addition of Long-Term Debt Outstanding.

These curious results lead us to question whether there is some intrinsic, inherent factor

that was present in the 1970s which allowed for natural resources to negatively impact GDP

growth that was not present at later periods of time. The possible answers, namely, education,

country size, and debt, do not seem to hold answers to this enigma. With that said, the following

section will delve more into theories to help ascertain what makes this model time-specific.

VII. Discussion and Conclusion

The curious results from the 1990 to 2003 period indicate that perhaps natural resource

curse is time specific. Lederman and Maloney test the results for historical periods prior to 1970

16 Manzano, Ozmel and Roberto Rigobon. “Resource Curse or Debt Overhang?” Natural Resources: Neither Curse nor Destiny. Ed. Daniel Lederman and William F. Maloney. Palo Alto: Stanford University Press, 2007, 41.

29

and find that the results do not hold up when looking at other time periods. Utilizing a simplified

version of the Sachs and Warner (1995) model, Lederman and Maloney find that the share of

natural resources as a percentage of exports actually has a positive effect for 1820 to 1870 (they

did not include all other variables given lack of data) and also for 1913 to 1950.17

An interesting theory proposed by Basedau (2005) is that the type of resource may

matter. In other words, “the banana curse is different from the oil curse.”18 Moreover,

macroeconomic vulnerability and the likelihood of susceptibility to price fluctuations differ from

resource to resource. Historically, metals, for example, have been demonstrated to be less

volatile in prices than oil. Secondly, Basedau points out that location and the manner of

exploitation are two other crucial factors in explaining the effects of natural resource exports.

Furthermore, certain resources can be easily smuggled (such as diamonds), which could produce

high prices on the global market as a result of the nature of the illegality of the resource in

question. “When rebel groups are willing to cooperate with criminal networks or run their

networks abroad, they can greatly benefit from this trade. On the other hand, governments will

rather try to avoid illicit commodities as a source of income since most of them are concerned

with their public image.”19 Consequently, grouping natural resources as a “share of total exports”

as was done in the aforementioned models may not be representative of the actual natural

resource abundance a country may have. Furthermore, grouping them into one category may also

confuse the effects that such exports have on the overall GDP growth.

17 Lederman, Daniel and William Maloney. “Open Questions about the Linke between Natural Resources and Economic Growth: Sachs and Warner Revisited.” Central Bank of Chile Working Paper. No. 141, February 2002. 18 Basedau, Matthias. “Context Matters – Rethinking the Resource Curse in Sub-Saharan Africa.” Working Paper: Global and Area Studies. German Oversease Institute Responsible Unit: Institute of African Affairs, May 2005. www.duei.de/workingpapers, 24. 19 Ibid, 25.

30

Given this quagmire of trying to make sense of differing results, a number of policy

implications are clear: natural resources cannot be definitively thought of as a “curse” as a whole

and secondly, resources should not be used as collateral for debt. There are few definitive

answers that may be gleaned from the results discussed herein; however, repeated studies by

Lederman and Maloney and Manzano and Rigobon have demonstrated that when fixed-effects

models are utilized, the negative impact of such a natural resource “curse” are mitigated, if not

eradicated. So, then, one must approach the issue of Dutch Disease (and the curse) with caution.

Domestic savings and investment have not been demonstrated to necessarily eradicate the curse

but the question of time is important. Perhaps the 1990 to 2003 period is too short a time period

to adequately measure the negative (or positive) impacts of natural resource abundance. Without

much fluctuation in commodity prices, the effects of any real exchange rate appreciation and

subsequent bust effects may be difficult to discern. Furthermore, the debt overhang question may

be useful in creating policies to avoid using commodities as collateral wherever possible.

Further research regarding the time effect of Dutch Disease must be studied. Perhaps a

better evaluation of the time effect would be to study individual commodities within the model

along with a commodity index price volatility measure that could better account for how much

the boom and busts can impact a country’s growth. Without more specific information on the

extent to which commodity prices fluctuate, it is difficult to definitively argue that the curse is

non-existent, and therefore, the conclusion is that context matters. Aside from investments in

human capital and rule of law, domestic savings/investments and openness to trade can all help to

alleviate the effects of a potential curse, but those measures have a dynamic interplay with the

type of resource in question as well as the global commodity market(s) itself. Attempting to

simplify such a curse in a cross-sectional study does not aid in formulating specific policies to

prevent such deleterious effects; however, they do aid policy-makers in understanding that

31

generalizations regarding commodities can be dangerous, as fixed-effects models by other authors

have demonstrated. Country context beyond those measurable factors, as well as the role of

illegal markets, global commodity price volatility and demand are crucial to understanding how

natural resources can affect a given economy.

Perhaps the overarching conclusion is that a country-level study of Dutch Disease may be

dangerous in that it generalizes a problem that involves far more inputs than just those variables

captured in the original Sachs and Warner (1995) model. Subsequent studies which account for

commodity price levels as well as volatility must be evaluated to understand the economic aspects

of the phenomenon.

32

VIII. References

Abrams, F. Gerard and Jere R. Behrman. Commodity Exports and Economic Development. Lexington: Lexington Books, 1982.

Adams, F. Gerard and Jere R. Behrman. Commodity Exports and Economic Development.

Philadelphia: Lexington Books, 1983. Asiedu, Elizabeth. “On the Determinants of Foreign Direct Investment to Developing

Countries: Is Africa Different.?” World Development Vol. 30, No.1, (2002), 107-119. Auty, Richard M. and Sampsa Kiiski. “Natural Resources, Ccapital Accumulation, Structural

Change, and Welfare.” Resource Abundance and Economic Development. Ed R.M. Auty. New York: Oxford University Press, 2001, 19-35.

Auty, Richard M. and Alan H. Gelb. “Political Economy of Resource-Abundant States.”

Resource Abundance and Economic Development. Ed R.M. Auty. New York: Oxford University Press, 2001, 126-143.

Basedau, Matthias. “Context Matters – Rethinking the Resource Curse in Sub-Saharan

Africa.” German Overseas Institute. Responsible Unit: Institute of African Affairs. Working Papers: Global and Area Studies. www.duei.de/workingpapers.

Birdsall, Nancy, Thomas Pinckney and Richard Sabot. “Natural Resources, Human Capital

and Growth.” Resource Abundance and Economic Development. Ed R.M. Auty. New York: Oxford University Press, 2001, 58-75.

Bresinger, Clemens and James Thurlow. “Asian-Driven Resource Booms in Africa:

Rethinking the Impacts Development.” International Food Policy Research Institute: Discussion Paper 00747. January 2008.

Corden, W.M. “Booming Sector and Dutch Disease Economics: Survey and

Consolidation.” Oxford Economic Papers, New Series, Vol. 36, NO. 3 (Nov., 1984), 359-380.

Collier, Paul and Jan Willem Gunning and Associates. Trade Shocks in Developing Countries –

Volume 1: Africa. Oxford: Oxford University Press, 1999. Deaton, Agnus. “Commodity Prices and Growth in Africa.” Journal of Economic Perspectives.

Vol. 13. No. 3 (Summer, 1999), 23-40. De Gregorio, Jose. “The Role of Foreign Direct Investment and Natural Resources in

Economic Development.” Central Bank of Chile Working Papers. No. 196, Enero 2003. http://www.bcentral.cl/estudios/documentos-trabajo/pdf/dtbc196.pdf

33

Manzano, Ozmel and Roberto Rigobon. “Resource Curse or Debt Overhang?” Natural Resources: Neither Curse nor Destiny. Ed. Daniel Lederman and William F. Maloney. Palo Alto: Stanford University Press, 2007, 41-70.

MacBean, Alasdair I. and D.T. Nguyen. Commodity Policies: Problems and Prospects. New York:

Croom Helm, 1987. Murshed, S.M. “Contrasting Natural Resource Endowments.” Resource Abundance and

Economic Development. Ed. R.M. Auty. Oxford: Oxford University Press, 2001. Gylfason, Thorvaldur. “Lessons from Dutch Disease: Causes, Treatments, and Cures.” The

Paradox of Plenty (STATOIL- ECON conference volume), 22 March 2001. http://www3.hi.is/~gylfason/pdf/statoil22.pdf

Lederman, Daniel and William F. Maloney. “Neither Curse nor Destiny: Introduction to

Natural Resources and Development.” Natural Resources: Neither Curse nor Destiny. Ed. Daniel Lederman William F. Maloney. Palo Alto: Stanford University Press, 2007, 1-11.

Lederman, Daniel and William F. Maloney. “Open Questions about the Link between

Natural Resources and Economic Growth: Sachs and Warner Revisited.” Central Bank of Chile, Working Papers. No. 141, February 2002.

Ridgway, James. It’s All for Sale: The control of Global Resources. Durham: Duke University

Press, 2004.

Rodriguez, Francisco and Jeffrey D. Sachs. “Why do Resrouce-Abundant Economies Grow More Slowly?” Journal of Economic Growth, 4. September 1999, 277-303.

Sachs, Jeffrey D. and Andrew M. Warner. “Natural Resources and Economic Development:

The curse of natural resources.” European Economic Review. 45 (2001) 827-838. Sachs, Jeffrey D. and Andrew M. Warner. “Natural Resource Abundance and Economic

Growth.” Working Paper for Center for International Development and Harvard Institute for International Development. (November 1997).

Sachs, Jeffrey D. and Andrew M. Warner. “Sources of Slow Growth in African

Economics.” Journal of African Economies. December 1997, Volume 6, Number 3, 335-376.

Sachs, Jeffrey D. and Francisco Rodriguez. “Why do Resource-Abundant Economies grow

more Slowly?” Journal of Economic Growth. 4 (September 1999), 277-303. Stocker, Herbert. “Growth Effects of FDI – Myth or Reality?” Foreign Direct Investment. Ed

John-ren Chen. New York: St. Martin’s Press, 2000.

34

Wijnbergen, Sweder van. “The ‘Dutch Disease’ After All?” The Economic Journal. Vol. 94,

N0. 373, March 1984, 41-55. Wolhmuth, Karl. “An Introduction: Abundance of Natural Resources and Vulnerability to

Crises.” Africa – Commodity Dependence, Resource Curse and Export Diversification. Ed. Karl Wohlmuth, Chicot Eboue, Achim Gutowski, Afeikhena Jerome, Tobias Knedlik, Mareike Meyn, Touna Mama. New Brunswick: Transaction Publishers, 2007.