Embed Size (px)

Citation preview

Examining the latest developments in Russian refining

and possible implications for Europe and other regions

Platts Middle Distillates 2015

January 2015

2

Important Notice

The information contained herein has been prepared by the Company. The opinions presented herein are based on general

information gathered at the time of writing and are subject to change without notice. The Company relies on information obtained

from sources believed to be reliable but does not guarantee its accuracy or completeness.

These materials contain statements about future events and expectations that are forward-looking statements. Any statement in

these materials that is not a statement of historical fact is a forward-looking statement that involves known and unknown risks,

uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from

any future results, performance or achievements expressed or implied by such forward-looking statements. We assume no

obligations to update the forward-looking statements contained herein to reflect actual results, changes in assumptions or

changes in factors affecting these statements.

This presentation does not constitute an offer or invitation to sell, or any solicitation of any offer to subscribe for or purchase any

securities and nothing contained herein shall form the basis of any contract or commitment whatsoever. No reliance may be

placed for any purposes whatsoever on the information contained in this presentation or on its completeness, accuracy or

fairness. The information in this presentation is subject to verification, completion and change. The contents of this presentation

have not been verified by the Company. Accordingly, no representation or warranty, express or implied, is made or given by or on

behalf of the Company or any of its shareholders, directors, officers or employees or any other person as to the accuracy,

completeness or fairness of the information or opinions contained in this presentation. None of the Company nor any of its

shareholders, directors, officers or employees nor any other person accepts any liability whatsoever for any loss howsoever

arising from any use of this presentation or its contents or otherwise arising in connection therewith.

3

Russian Government has proclaimed 3 key goals for Russian refining industry

upgrade campaign by 2020 and uses 4 levers to achieve them

Increase lights yield (conversion) 1

• Key focus is on meeting demand for

gasoline

Lights yield, %

Higher fuel standards in Russia Replace refineries old units and

increase HSE standards

2 3

Euro <5

Euro 5

2020

0%

100%

2012

70%

30%

Diesel and gasoline production,

MTPA

• Increased motor fuel production and

Euro-5 compliance remains in focus in

nearest years

• It is estimated that 70% of Russian

refining units have already exceed

their expected lifetime

• Key replacement goals:

−High health, safety and

environmental standards

−Operational integrity

−Maximization of refinery utilization

−Increase in labor productivity due to

automation & technology

4 party agreement between Government (FAS, Rosstandart, Rostehnadzor) and oil companies

Each oil company is obliged to upgrade refineries to agreed configuration and to produce a certain amount of motor fuels meeting technical

Regulation specifications

Differentiation of excise taxes

Russia excise tax for higher specification

fuel is smaller, incentivizing quality

improvement

Introduction of technical regulation

Motor fuels non-compliant to norms are

prohibited from sale on domestic market

•Minimum Euro 4 in 2015

•Minimum Euro 5 from 2016

2020

66%

2012

55%

Source: Minenergo, Skolkovo business school, Rosneft

Differentiation of export duties

Significant export duty advantage for light

products compared to dark products

B

A

C

D

4

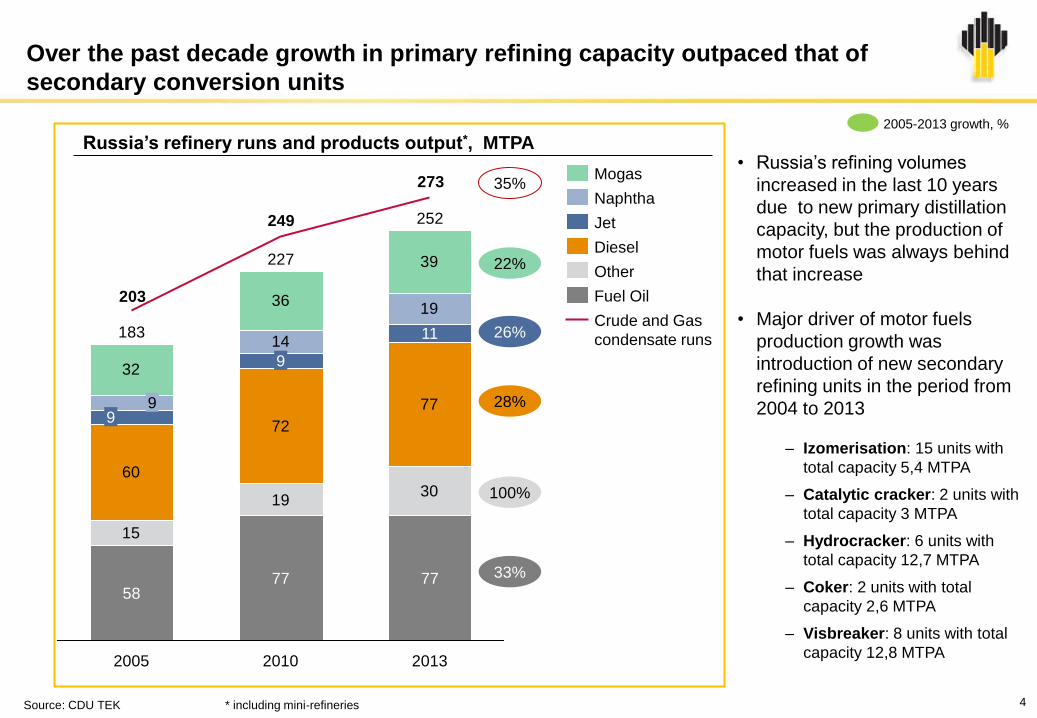

Over the past decade growth in primary refining capacity outpaced that of

secondary conversion units

Russia’s refinery runs and products output*, MTPA

15

1930

60

72

14

19

32

36

39

77

203

249

273

2013

252

2010

227

2005

183

9 9

58

9

77

11

77

Naphtha

Diesel

Other

Fuel Oil

Mogas

Crude and Gas

condensate runs

Jet

• Russia’s refining volumes

increased in the last 10 years

due to new primary distillation

capacity, but the production of

motor fuels was always behind

that increase

• Major driver of motor fuels

production growth was

introduction of new secondary

refining units in the period from

2004 to 2013

– Izomerisation: 15 units with

total capacity 5,4 MTPA

– Catalytic cracker: 2 units with

total capacity 3 MTPA

– Hydrocracker: 6 units with

total capacity 12,7 MTPA

– Coker: 2 units with total

capacity 2,6 MTPA

– Visbreaker: 8 units with total

capacity 12,8 MTPA

Source: CDU TEK * including mini-refineries

22%

2005-2013 growth, %

28%

100%

33%

26%

35%

5

Existing refinery modernization projects will lead to substantial

increase of gasoline and diesel supply

Additional production of motor fuels after modernization*, MTPA

0,4 0,5

3,0

0,5

1,7

3,6

Gasoline: +10 MTPA by 2021

2020

2,7 3,0

2015 2016 2019

3,1

2017

8,3

6,7

2014

1,1

2018

3,3

Diesel:

+30 MPTA by 2021

Source: Rosneft * Upon completion of on-going projects

Slavneft TAIF

Antipinsky

Gazprom

Surgutneftegaz TANEKO GazpromNeft

Bashneft

Lukoil

Rosneft Aliance

Gazprom:

Hydrotreatment ,

izomerization

(Astrakhan);

Gazpromneft:

hydrotreatment,

izomerization

(Мoscow);

Surgutneftegaz.:

hydrocracker (Kirishi);

Аntipinsky.: AT

Aliance:

hydrotreatment and

hydrocracker

Gazprom:

izomerization

(Salavat);

Lukoil : AVT

(Volgograd);

TANEKO:

hydrocracker;

Antipinsky:

hydrotreatment

Gazprom: izomerization

(Surgut);

Gazpromneft: АТ (Omsk);

Lukoil: izomerization,

hydrocracker (Volgograd),

Coker (Perm), izomerization,

catcracker (NNovgorod);

Rosneft: Hydrocracker

(Komsomolsk.), catcracker

(Samara), Coker (Аchinsk);

Аntipinsky: Coker

Аntipinsky:

izomerization, reformer;

Gazprom: catcracker

(Salavat);

Rosneft.: Hydrocracker,

izomerization, reformer

(Tuapse), hydrocracker,

coker (Samara),

hydrocracker (Achinsk);

Bashneft: hydrocracker

Gazprom: alkylation

(Salavat);

Rosneft.: flexicoking

(Тuapse),

hydrotreatment

(Ryazan);

Gazpromneft: coker

(Omsk)

Bashneft: coker,

Gazpromneft: hydrocracker (Omsk);

Antipinsky: Hydrocracker

Lukoil: hydrocracker

(NNovgorod);

Rosneft: hydrocracker

(Ryazan);

Slavneft:

hydrocracker

6

Tax maneuver will level the duties for crude and dark products, while increasing

the tax advantage for light products

46

72

98

182

2014 2015 2016

155

275

147

-34%

205

179 182

154 154

2017

-70%

0%

Crude Dark products Light products

• Significant tax gap

between crude and

products

• Equal tax for dark

and light products

• Equal tax for crude

and dark products

• Significant tax gap

between dark and

light products

Crude

2015

36%

2016

42%

2017

30% 30%

2019 2018

30%

2014

59%

Export duties after tax maneuver, USD/t @ 85 USD/bbl Brent New tax maneuver export duties, %

Dark products

2014 2016

82% 100% 100%

2018

100%

2019 2017 2015

76% 66%

Light products

30%

2019

30%

2017

30%

2016

40%

61%

2015

48%

78%

2018 2014

65%

90% Gasoline Diesel

Source: Rosneft

7

Tax maneuver impact on refining: worse margins for simple refineries and

stable margins for complex refineries

59

30 24

6052

23

2015

2

2017 2016

-27

2014

104

-15 -3

-12

• Profitability of sophisticated

refineries remains stable

• Simple refineries in Russia

become uneconomical at

Brent 50$ /bbl and marginal

at 85 $ /bbl

• Potential shut-down of

unprofitable simple refineries

will not impact domestic fuels

market, but may release

additional 20-30 MTPA of

crude for exports

50 $/b 100 $/b 85 $/b

Simple refinery margin*, $/t

9176 82 86

17

2016

127

18

135

2017 2015

16

119

143

2014

19

85 $/b 100 $/b 50 $/b

Complex refinery margin*, $/t

Source: Rosneft * Simple - refinery has a visbreaker without VGO conversion. Complex – refinery with VGO conversion units. Location – Central Russia

8

There is no risk of gasoline deficit on domestic market in short term.

Surplus expected in the long term.

0

10

20

30

40

50

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Rosneft TNK-BP Lukoil

GazpromNeft Gazprom Bashneft

Slavneft Surgutneftegaz Other

Risk group Loss-making Consumption (low case)

Consumption (base case)

• Historically gasoline balance

in Russia has been tight, with

seasonal deficit covered by

imports from Belarus

• Implementation of refineries

conversion projects in Russia

will lead to gasoline surplus

starting from 2017

• Slower demand growth in

2015-2016 minimizes risks of

deficit before launch of most

refinery conversion units

• Possible closure of

unprofitable refineries is

unlikely to generate deficit on

domestic market even in

2015

Russia gasoline supply/demand balance, MTPA

Source: demand forecast – Wood Mackenzie, actual data - Petromarket, production forecast – Rosneft assumptions, actual data – CDU TEK

9

Russia will become a net exporter of gasoline, primarily in European direction

-2,3-1,7-2,5-1,9

-0,9-1,4-1,3-1,0

-0,7-0,1-2,3-2,4

4,6

12,2 12,6 12,0 -1,3-1,2-1,2-1,5

2,02,32,42,4

-1,7-1,6-1,5-1,4

1,6

North-West

Center

South

Volga

Ural region

Siberia

Far East *

Far East region deficit is

covered by Siberia

supplies «on route» to

export ports

6,94,8

-2,4

8,2

25 20 16 2012

Kirishi

2,3 MTPA

Tuapse

2,4

MTPA

0,80,91,0 0,41,6

2012 20 25 16

Total «East» *

Regional gasoline supply/ demand balances in Russia, MTPA (base case)

• Volga region refineries will close

the gasoline deficit in nearby

regions

• Surplus gasoline production

from Siberia region will cover

the deficit in Far East

• Main export refineries will be the

ones located in or near

exporting ports:

− Kirishi in North-West region

exporting to North West

Europe hub (production 2,3

MTPA after 2016)

− Tuapse on the Black sea

shore exporting to the

Mediterranean (production 2,1

MTPA after 2016)

Tuapse will be an export oriented refinery –

South region deficit will be covered by Volga

region supplies «on route» to export ports

FEPCO

FEPCO

Total «West»

Source: Rosneft * inc. FEPCO 1,6 MTPA

10

Diesel export volumes will increase as production growth outpaces

demand growth

• Russia has the potential for a

higher dieselization:

– Diesel quality compliant

with modern engine

requirements

– Sufficient capacities for

winter diesel production

• Production of diesel

increases faster than

demand, exports to remain

above 50% of production in

the coming 10 years

• Possible closure of

unprofitable refineries and

refineries in risk group is

unlikely to have major

influence on balances

Russia diesel supply/demand balance, MTPA*

Source: demand forecast – Wood Mackenzie, actual data - Petromarket, production forecast – Rosneft assumptions, actual data – CDU TEK

0

20

40

60

80

100

120

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Rosneft TNK-BP Lukoil

GazpromNeft Gazprom Bashneft

Slavneft Surgutneftegaz Other

Risk group Loss-making Consumption (low case)

Consumption (base case)

11

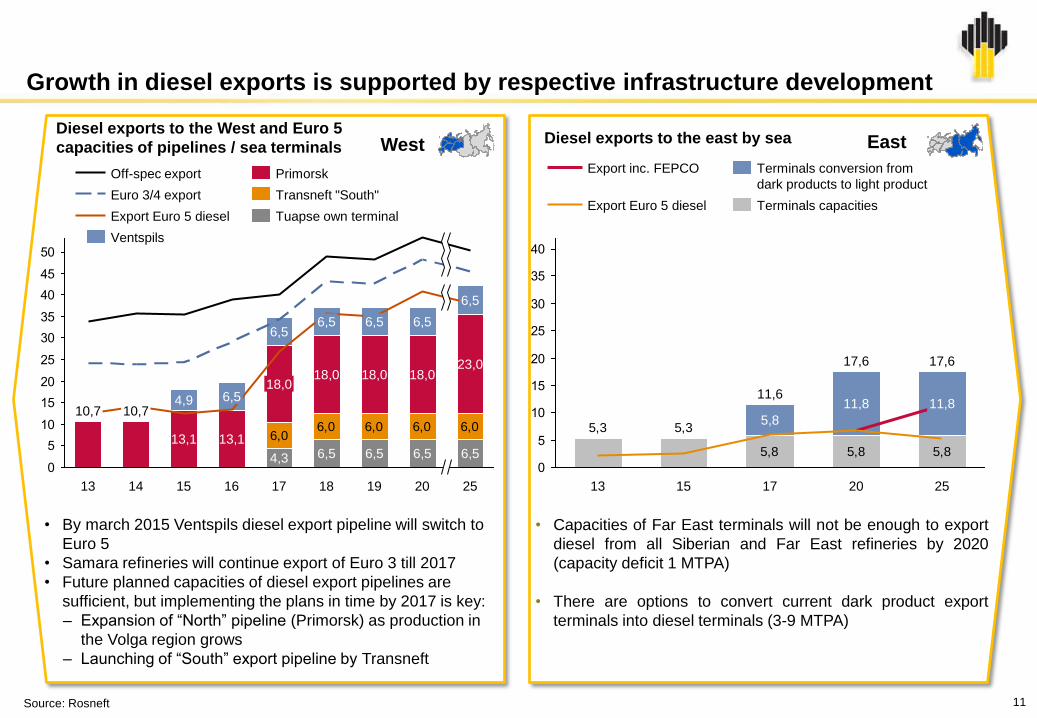

Growth in diesel exports is supported by respective infrastructure development

Diesel exports to the east by sea

6,06,0 6,0 6,0 6,0

0

5

10

15

20

25

30

35

40

45

50

6,5 4,9

16 17

4,3

18,0

6,5 6,5

13

10,7

14

13,1

15

13,1

10,7

18,0

6,5

20

6,5

6,5

18,0

6,5

6,5

19

23,0

6,5

25

18,0

18

6,5

Tuapse own terminal Export Euro 5 diesel

Transneft "South"

Off-spec export

Euro 3/4 export

Primorsk

Ventspils

Diesel exports to the West and Euro 5

capacities of pipelines / sea terminals East West

• Capacities of Far East terminals will not be enough to export

diesel from all Siberian and Far East refineries by 2020

(capacity deficit 1 MTPA)

• There are options to convert current dark product export

terminals into diesel terminals (3-9 MTPA)

• By march 2015 Ventspils diesel export pipeline will switch to

Euro 5

• Samara refineries will continue export of Euro 3 till 2017

• Future planned capacities of diesel export pipelines are

sufficient, but implementing the plans in time by 2017 is key:

– Expansion of “North” pipeline (Primorsk) as production in

the Volga region grows

– Launching of “South” export pipeline by Transneft

Source: Rosneft

5,8 5,8 5,8

5,35,3

0

5

10

15

20

25

30

35

40

15 13

5,8

11,8 11,8

17

11,6

25

17,6 17,6

20

Export Euro 5 diesel

Terminals conversion from

dark products to light product

Terminals capacities

Export inc. FEPCO

12

Jet production capacities to exceed demand significantly, leading to growing

export of jet or diesel depending on logistics solutions

Jet supply / demand balance

Jet supply / demand balance East

West

▪ Russia historically had a tight balance for jet

fuel, but will have a surplus starting from 2015.

▪ Share of jet export can increase significantly

after 2015-16 and by 2020 can achieve

30-40% of production.

▪ Increase of jet prices due to tax maneuver can

lead to lower sales to international airlines on

domestic market which account for 15-25% of

the market.

▪ Logistical solutions need to be developed to

export surplus jet fuel (or conversion into

diesel at refineries)

12,912,111,9

10,410,28,97,67,4

9,28,17,87,67,4

7,35,9

2013

7,6 7,4

2012

7,2

2014

2015

2017

2016

2018 2025

Production*

Demand (low)

Demand (base)

4,14,13,82,92,82,82,8 0,81,81,91,9

2013

2012

1,8

2015

2016

2014

1,9 1,9

4,9

2018

2,0 2,2

4,1

2025

**

2017

Demand (low)

Demand (base)

Production*

FEPCO

* In case of jet oversupply it can be converted to diesel ** inc. FEPCO 0,8 MTPA

13

Fuel oil export in the Western direction will remain significant at 35 MTPA, while

in the East a 2 MTPA deficit may occur

2030

42,1

5,8

2025

42,2

6,5

2020

44,6

7,5

2013

64,3

11,8

2010

62,4

10,9

2005

50,3

14,5

Demand (excluding

transit bunkering)

Production

Fuel oil production Fuel oil production

2030

-2,5

2025

-2,1

2020

-2,1

2013

4,6

2010

7,7

2005

4,5

Fuel oil export

51,3

34,4

16,8

2005

35,7

24,3

11,4

2030

34,9

19,9

15,0

2025

34,0

19,3

14,8

2020

35,2

19,9

15,3

2013

52,4

24,5

27,9

2010

other Baltic Russia

Fuel oil export

East West

• Higher fuel oil prices due to tax maneuver leads to lower

transit bunkering volumes (40-50% market share).

• In case of higher transit bunkering volumes, fuel oil will be

shipped from western Russia, by rail or sea depending on

economics.

• Even after Russian refineries modernization, fuel oil export to

the west will remain significant – around 35 MTPA

• Tightening of emissions regulation limits the usage of fuel oil

in maritime bunkering in Europe

2013 2030

2,8 2,8 2,8

2025 2020

10,9

2010

12,3

2005

9,8

Demand (excluding transit bunkering)

Production

Some fuel oil deficit may occur

following decrease in fuel oil

production

14

Share of high quality products in Russia exports to Europe, Mediterranean and

Asia is and will continue to grow

52 35 34

1333

30

78

1077

12

2025

88

4

2020

93

4

2013

84

-2

5 5

Diesel Euro 5

Jet (base case)

Gasoline (base case)

Fuel oil

Diesel Euro3/4

Diesel off-spec

Export of refined products, MTPA West

725

5

7

-2

2020 2025

6

1 2 -2

2013

2

7

Fuel oil

Diesel Jet (base case)

Gasoline (base case)

East Export of refined products, MTPA

• Refined products export volumes to the West will be relatively

stable at 80-90 MTPA, but the structure of products exported

will change significantly:

– Volume of fuel oil will decrease

– Both volume and more important quality of diesel will

increase

– Exports of gasoline and jet fuel begin, adding to the

diversity

• Export to the East will remain low at 6-7 MTPA:

– Export of fuel oil will stop as production decreases.

Depending on demand a deficit is possible

– High quality diesel exports will increase following refinery

upgrades