Embed Size (px)

Citation preview

Exchange rate, output & macro policies in the short run. The fixed exchange rate.

The Mundell-Fleming model, part 2.

Gabriela Grotkowska & Joanna Siwińska-GorzelakWNE UW

Introduction: Central Bank’s Interventions in Foreign Exchange Markets

• Central banks usually have foreign currency reserves in the event that they should desire to conduct interventions on their own account.

• If central banks intervene in foreign exchange markets on their own behalf, then they do so using their own reserves of assets denominated in foreign currencies.

• Note that under the fixed exchange rate regime, the CB declares that it will keep the exchange rate fixed (constant), hence it will be forced to intervene

Introduction: Central Bank’s Interventions in Foreign Exchange Markets

• We can distinguish between foreign intervention that does or does not change the monetary base.

• The former type is called unsterilized intervention (no additional, accompanying change in the monetary base) while the latter is referred to as sterilized intervention (the CB simultaneously & additionally changes the monetary base).

• Unsterilized intervention: when a monetary authority buys (sells) foreign exchange, its own monetary base increases (decreases) by the amount of the purchase (sale).

• Many central banks routinely sterilize foreign exchange operations—that is, they reverse the effect of the foreign exchange operation on the domestic monetary base other moneymarket operations.

Foreign Exchange Interventions and the Domestic Money Supply

• Central banks conduct their interventions through the banking system & in case of unsterilized interventions :

– changing the monetary base and thereby altering the money stock

– when the central banks intervenes and buys foreign currency, domestic money supply goes up

• Conclusion: unsterilized foreign exchange interventions influence the domestic money stock

Sterilization of Interventions

• Sterilization of the sale of foreign exchange reserves requires an equal-sized expansion of domestic credit, perhaps via a central bank open-market purchase, that would maintain an unchanged monetary base.

• STERILIZATION A central bank policy of altering domestic credit in an equal and opposite direction relative to any variation in foreign exchange reserves so as to prevent the monetary base from changing.

• Conclusions: sterilized foreign exchange interventions do NOT influence the domestic money stock

Monetary Policy and the BoP with Imperfect Capital Mobility

• Exchange rate is fixed (of course) • Assume a monetary expansion (the short run!):• As a result the real interest rate declines and income

increases • A rise in real income stimulates an increase in imports and

thereby causes a trade deficit to occur (CU deficit) • The equilibrium interest rate declines, but because capital

mobility is not perfect, a limited amount of financial capital flows out of the country (FA deficit)

• As a result, a monetary expansion generates a balance-of-payments deficit.

• Since exchange rate cannot change, the central bank has to step in again…

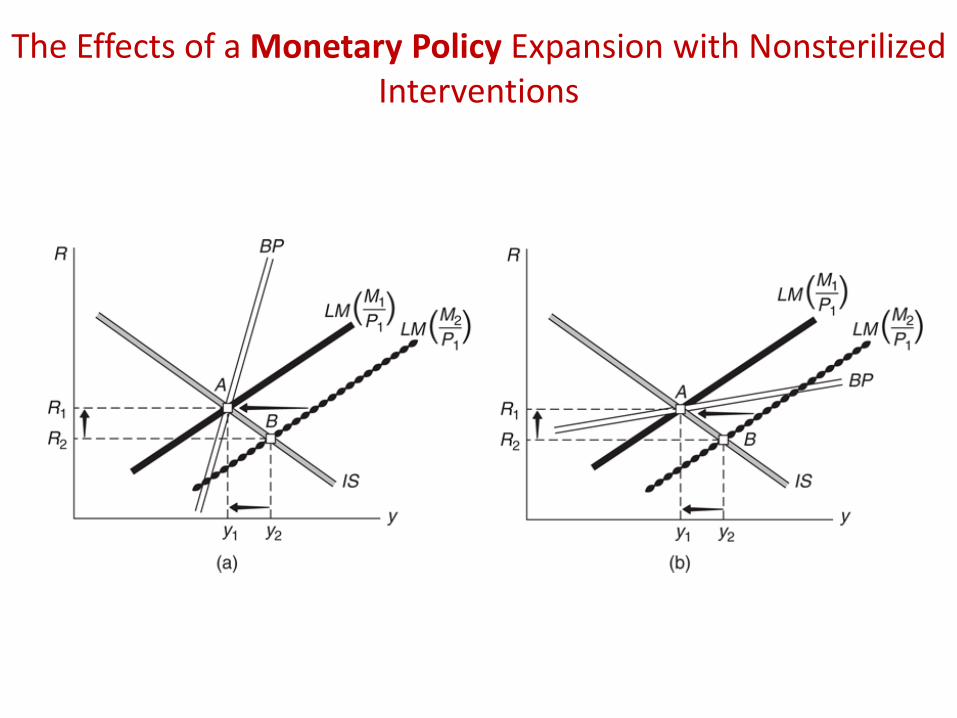

The Effects of a Monetary Policy Expansion with NonsterilizedInterventions

Monetary Policy in MF model (fixed exchange rate)

• As a result of monetary expansion, there is a pressure for the balance-of-payments to turn ito a deficit & a downward pressure on the nation’s currency value.

• To keep the value of its currency from declining, a central bank hass to sell some of its foreign exchange reserves, and buy domestic currency. Thisimplies a decline in some of its money liabilities in circulation. Hence, the domestic money stock falls back to the old level.

• A nonsterilized monetary expansion with a fixed exchange rate leads to an eventual contraction of the money stock.

• As long as no other factors change, the economy then would re-attain its initial equilibrium real income level and interest rate, leading to the return to the original balance-of-payments equilibrium.

• Monetary policy is ineffective!

Sterilized Monetary Policy

• An increase in M causes a BoP deficit.

• If a nation experiences a balance-of-payments deficit, there would be downward pressure on the nation’s currency value.

• To keep the value of its currency from declining, a central bank would have to sell some of its foreign exchange reserves, which would require a decline in some of its money liabilities in circulation. Hence, the domestic money stock would begin to fall.

• To keep this from happening, the central bank would have to add sufficient domestic assets—which would be a sterilized intervention.

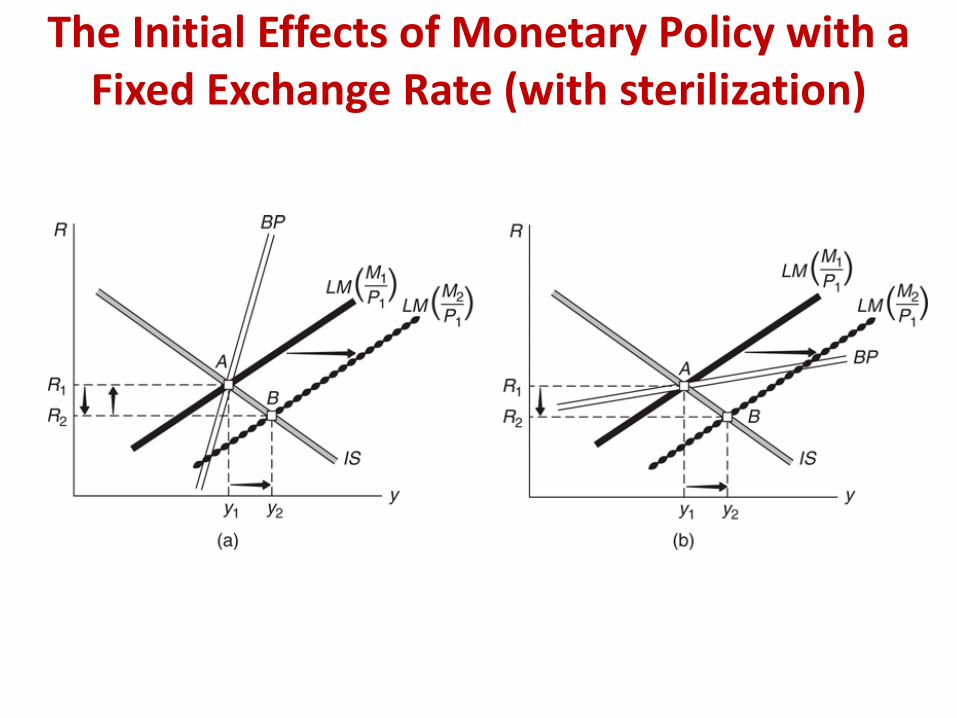

The Initial Effects of Monetary Policy with a Fixed Exchange Rate (with sterilization)

Sterilized Monetary Policy

• Note however, that this situation cannot hold forever, as eventually the C.B. will loose all of its reserves.

• Hence, eventually the C.B will be forced to reverse its policy

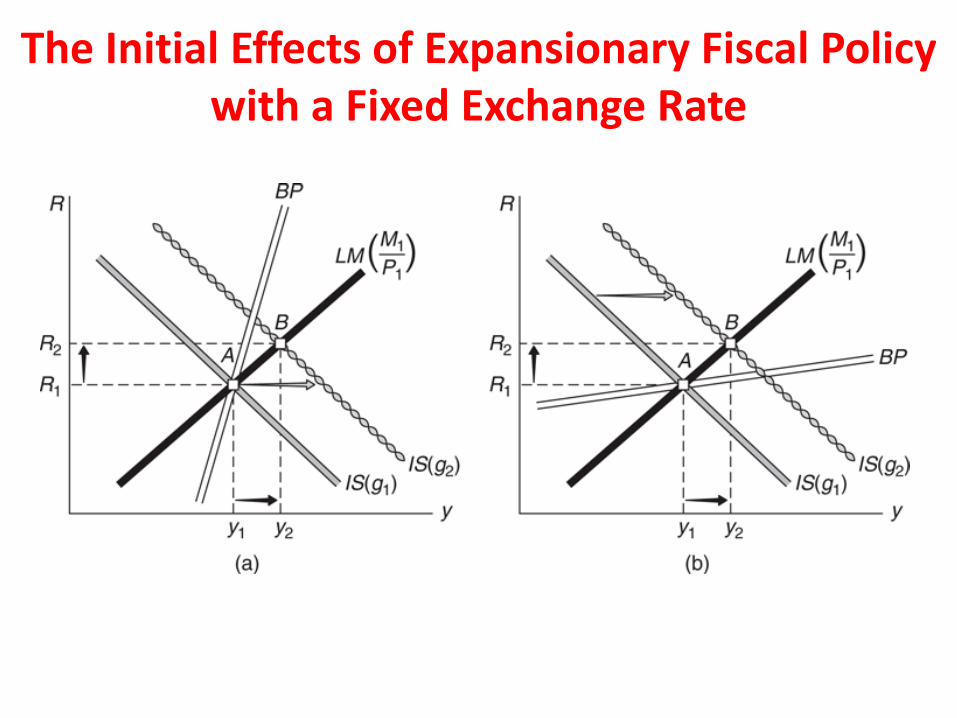

Fiscal Policy and the BoP with Imperfect Capital Mobility

• Assume a fiscal expansion & resulting increase in Y and r:

• A rise in equilibrium real income induces a rise in imports that causes the nation to experience a trade deficit.

• The rise in the equilibrium interest rate (r) generates an inflow of financial resources from other nations

• With low capital mobility this inflow is not very significant. Thus, on net there is a balance-of-payments deficit.

• If capital mobility is big, the same increase in government spending results in a balance-of-payments surplus.

The Initial Effects of Expansionary Fiscal Policy with a Fixed Exchange Rate

The Effects of Fiscal Policy Actions with and without Monetary Sterilization

• Under a fixed exchange rate, fiscal policy actions force a central bank to respond to international payments imbalances by reducing or accumulating foreign exchange reserves.

• The real income effects of fiscal policy actions hinge on central bank decisions about whether to sterilize and on the degree of capital mobility.

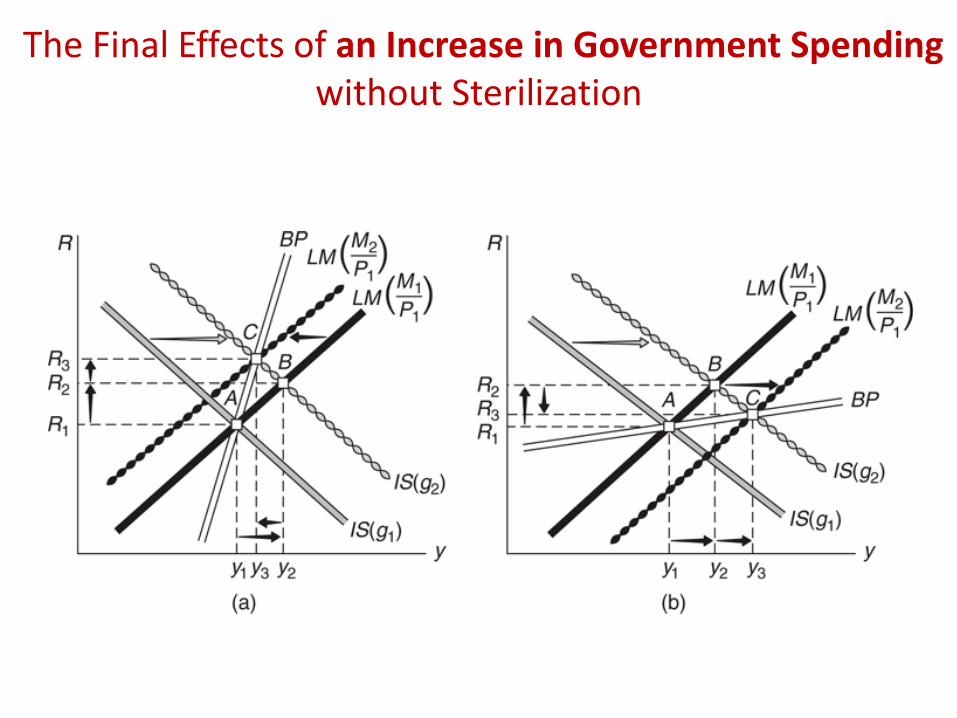

The Final Effects of an Increase in Government Spending without Sterilization

The Final Effects of an Increase in Government Spending with Sterilization

• If the CB sterilises that the country can remain in point B for some time, but eventually the C.B will have to stop the sterilization

• Due to a change in money supply, the new equilibrium will be in C.

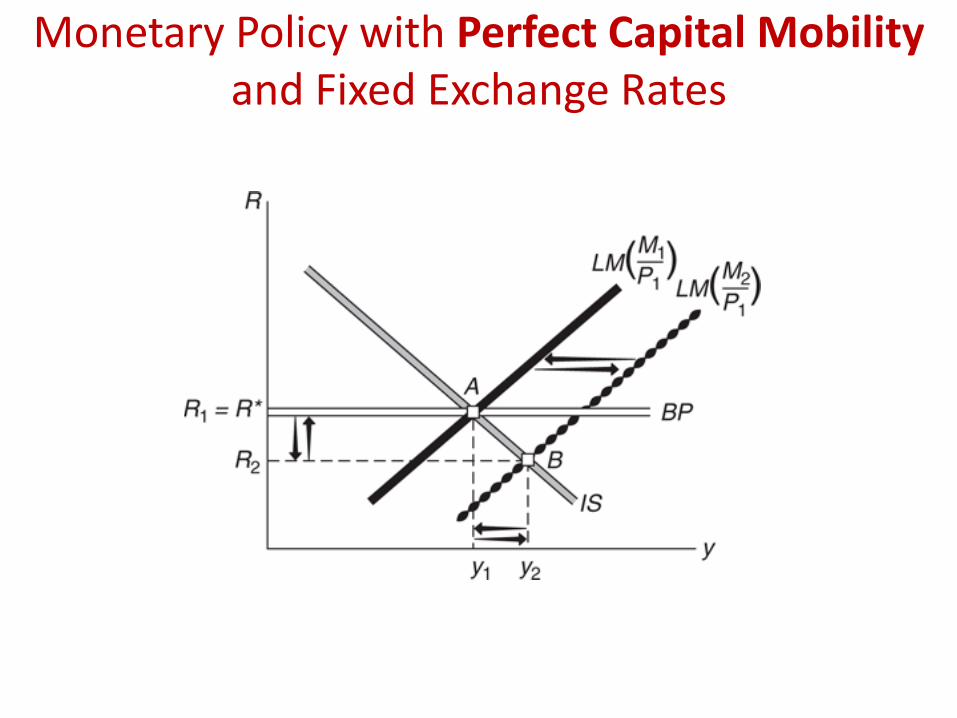

Monetary Policy with Perfect Capital Mobility and Fixed Exchange Rates

Monetary Policy under a Fixed Exchange Rate

• An expansionary monetary policy action ultimately has no effect on real income when the central bank maintains a fixed exchange rate.

• Because it must intervene in the foreign exchange market to keep the exchange rate from changing, the central bank effectively must “undo” its own policies.

• No sterilization is possible, as the capital inflow (outflow) is huge.

• From that we can formulate a very important statement on the impossible trinity

Impossible trinity

• A macroeconomic policy trilemma, also called the impossible trinity.

• A country must choose between free capital mobility, exchange-rate management and an independent monetary policy.

• Only two of the three are possible.

• If a country chooses free capital mobility and wants monetary autonomy, it has to allow its currency to float. That is the two-from-three combination that most modern economies choose.

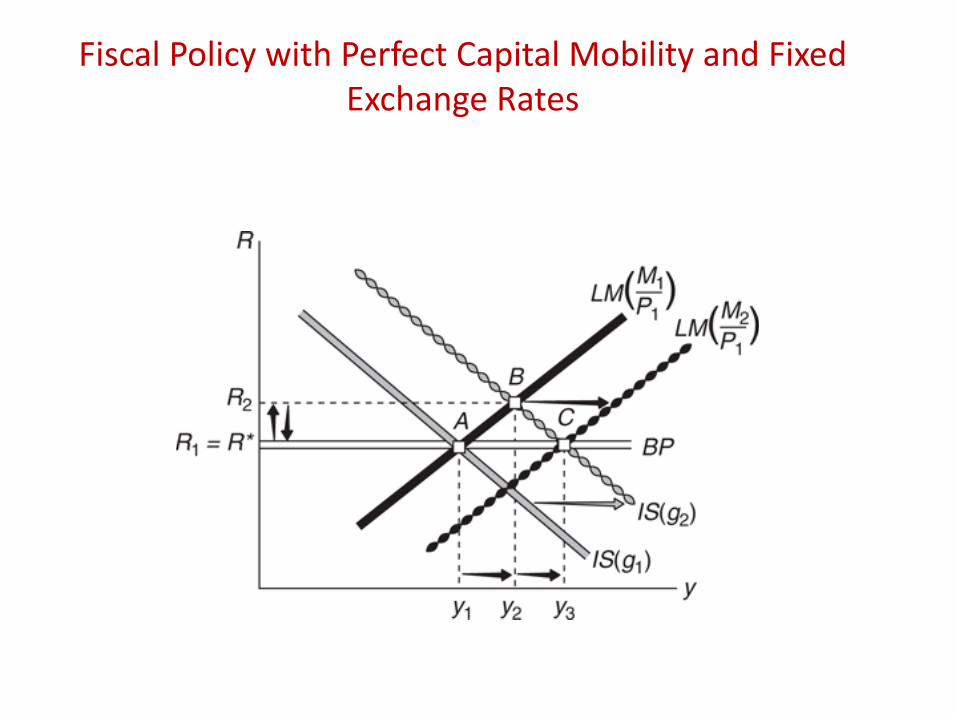

Fiscal Policy with Perfect Capital Mobility and Fixed Exchange Rates

Fiscal Policy and a Fixed Exchange Rate

• The extent to which fiscal policy actions can influence real income under a fixed exchange rate are enlarged if capital is completely mobile.

• Fiscal policy has its greatest possible effect on equilibrium real income when capital is perfectly mobile.

A devaluation/revaluation

• Note that „depreciation” and „appreciation” refer to changes in the value of a currency due to market changes.

• Devaluation refers to a change in a fixed exchange rate caused by the central bank.

• A unit of domestic currency is made less valuable, so that more units must be exchanged for 1 unit of foreign currency.

• Revaluation is also a change in a fixed exchange rate caused by the central bank.

• A unit of domestic currency is made more valuable, so that fewer units need to be exchanged for 1 unit of foreign currency.

A devaluation/revaluation

• If the central bank devalues the domestic currency

so that the new fixed exchange rate is E1, it buys

foreign assets, increasing the money supply,

decreasing the interest rate and increasing output

• This has the same implication as depreciation

under flexible exchange rate regime – IS and BP

lines shift to the right, as a result of expansionary

monetary policy

• The final results is higher output, and higher NX

Summary - policies under the Fixed versus Floating Exchange Rates

1. (With perfectly mobile capital), monetary policy actions have minimal effects on equilibrium real income in a small open economy if the exchange rate is fixed

2. With perfect capital mobility, fiscal policy actions exert their largest feasible effects on equilibrium real income in a small open economy if the exchange is fixed.