Embed Size (px)

Citation preview

1

Exchange rates in the

long run (Purchasing

Power Parity: PPP)

Jan J. Michalek

The law of one price:

i – for a product i;

PiPL = EPLN/€ * PiG

Or equivalently:

EPLN/€ = PiPL / PiG

Idea: The same product should have the same

price at competitive markets (no trade barriers

and low transport costs)

but there are many reservations

JJ Michalek

2

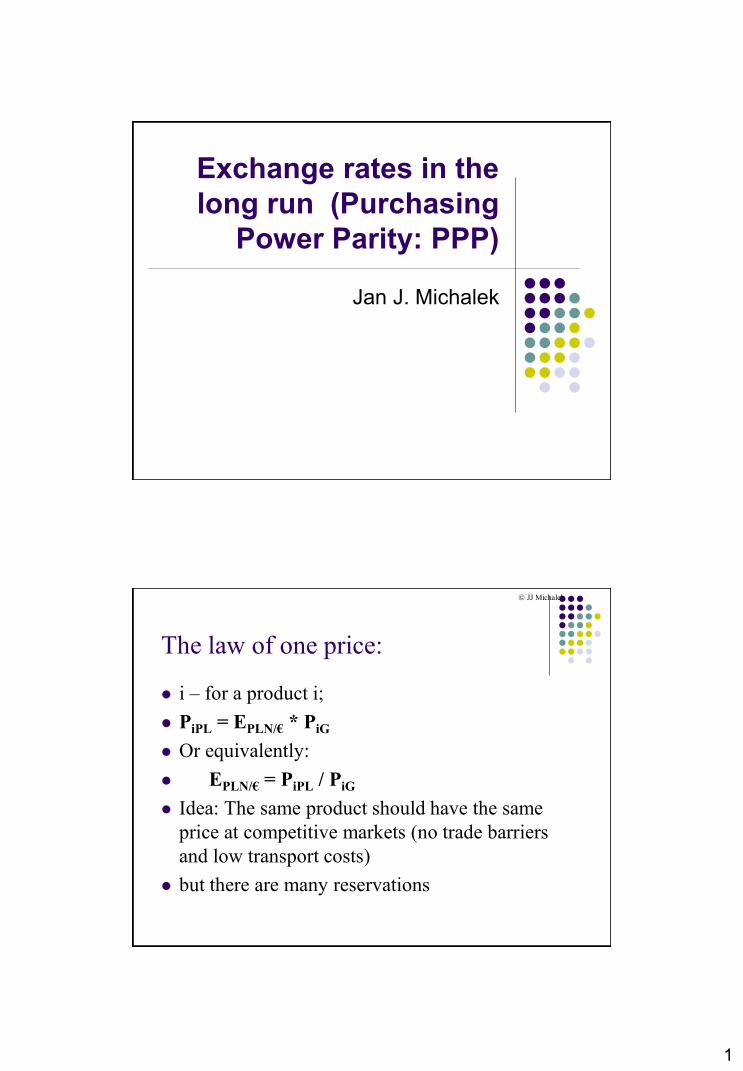

Empirical verification of law of one

price: butter

Empirical analysis of law of one price: price in

grams of silver per hectoliter f charcoal

3

PPP theory: absolute version

Theory of PPP: Purchasing power parity (PPP): the exchange rate is equal to

relations of purchasing power among analyzed countries

If PPL: Prices in Poland

PG: Prices in Germany

Then PPP foresees that:

EPLN/€ = PPL / PG or more general: E=P/P*

According to PPP: rise in domestic price level leads to the proportional

depreciation of domestic currency.

Another notation:

PPL = EPLN/€ *PG

JJ Michalek

PPP theory: relative version

Exchange rates equals to relative prices

Relative PPP theory: percentage change in the exchange rate =

difference in the percentage changes in relative prices:

wheret is the rate of inflation in time t.: t = (Pt-Pt-1)/Pt-1

*

11 / ttttt EEE

JJ Michalek

4

Purchasing Power Parity: once

again in two versions

Purchasing power parity comes in 2 forms:

Absolute PPP: purchasing power parity that has already

been discussed. Exchange rates equal price levels across

countries.

EPLN/€ = PPL/PEU

Relative PPP: changes in exchange rates equal changes in

prices (inflation) between two periods:

(EPLN/€,t - EPLN/€, t –1)/EPLN/€, t –1 = PL, t - EU, t

where t = inflation rate from period t-1 to t

Model based on PPP:

monetary approach

PPL = MsPL/L(RPLN,YPL); and the same abroad;

Where L(RPLN,YPL) is the real aggregate demand for money.

Fundamental equation of the monetary approach:

PLPLN

Gs

G

S

PLGPLPLN YRL

YRLM

MPPE

,,

//

long run changes in the ex-rate is fully determined by the relative supplies of

those monies an the relative real demand for them

Or in the abbreviated form::

PLGPLNS

G

S

PLPLN YYRR

MM

E ,/

where: (.) is the relative aggregate demand for monies in Germany in relation to

Poland.

JJ Michalek

5

Monetary Approach

to Exchange Rates

To the degree that PPP holds and to the degree that

prices adjust to equate real money supply with real

money demand, we have the following prediction:

The exchange rate is determined in the long run by

prices, which are determined by the relative supply

of money across countries and the relative real

demand of money across countries.

Monetary Approach

to Exchange Rates (cont.)

Predictions about changes in:

1. Money supply: a permanent rise in the domestic money supply

causes a proportional increase in the domestic price level,

causing a proportional depreciation in the domestic currency (through PPP).

same prediction as long run model without PPP

2. Interest rates: a rise in the domestic interest rate

lowers domestic money demand,

increasing the domestic price level,

causing a proportional depreciation of the domestic currency (through PPP).

6

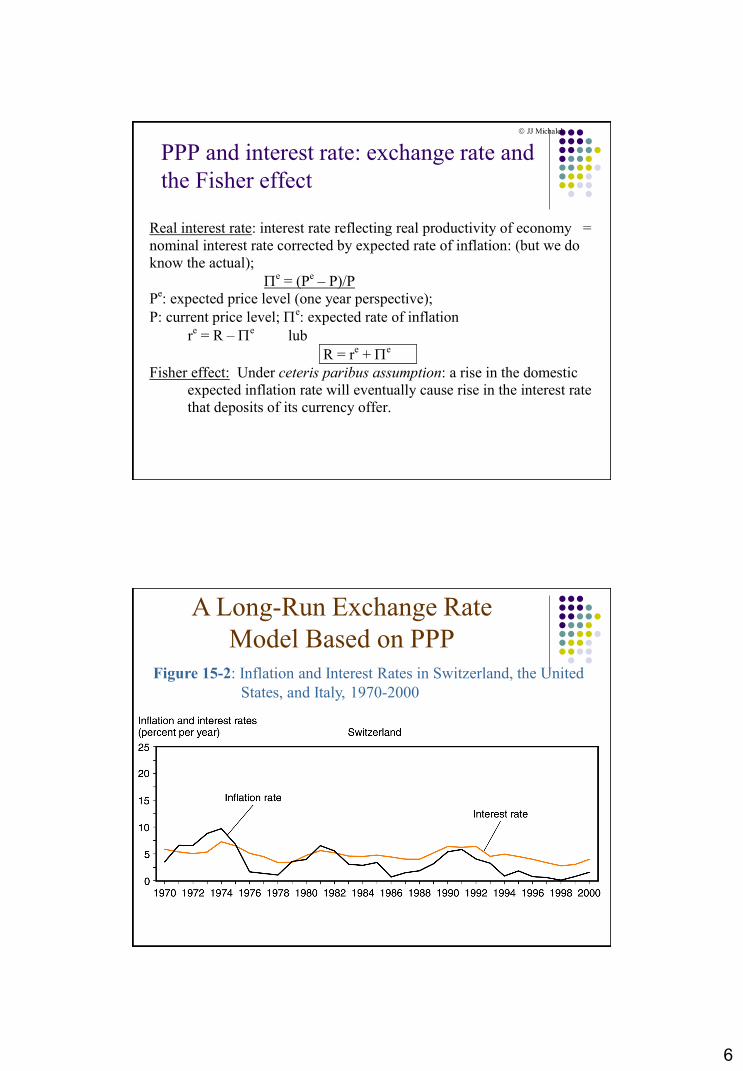

PPP and interest rate: exchange rate and

the Fisher effect

Real interest rate: interest rate reflecting real productivity of economy =

nominal interest rate corrected by expected rate of inflation: (but we do

know the actual);

e = (P

e – P)/P

Pe: expected price level (one year perspective);

P: current price level; e: expected rate of inflation

re = R –

e lub

R = re +

e

Fisher effect: Under ceteris paribus assumption: a rise in the domestic

expected inflation rate will eventually cause rise in the interest rate

that deposits of its currency offer.

JJ Michalek

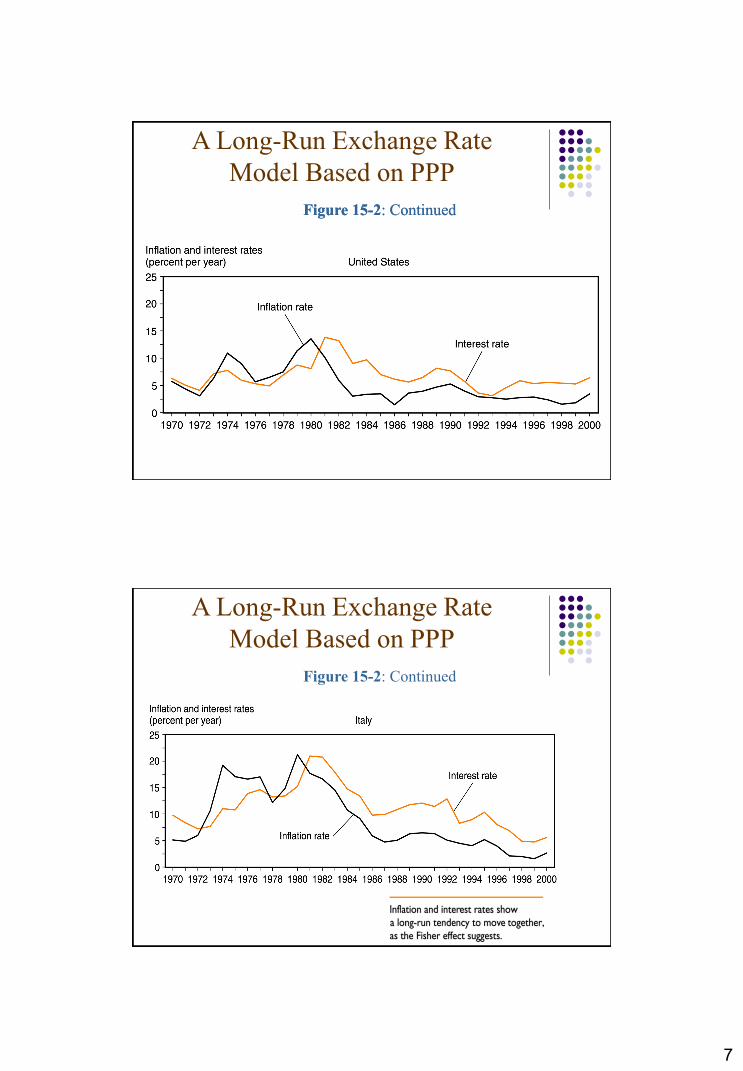

Figure 15-2: Inflation and Interest Rates in Switzerland, the United

States, and Italy, 1970-2000

A Long-Run Exchange Rate

Model Based on PPP

7

Figure 15-2: Continued

A Long-Run Exchange Rate

Model Based on PPP

Figure 15-2: Continued

A Long-Run Exchange Rate

Model Based on PPP

Figure 15-2: Continued

8

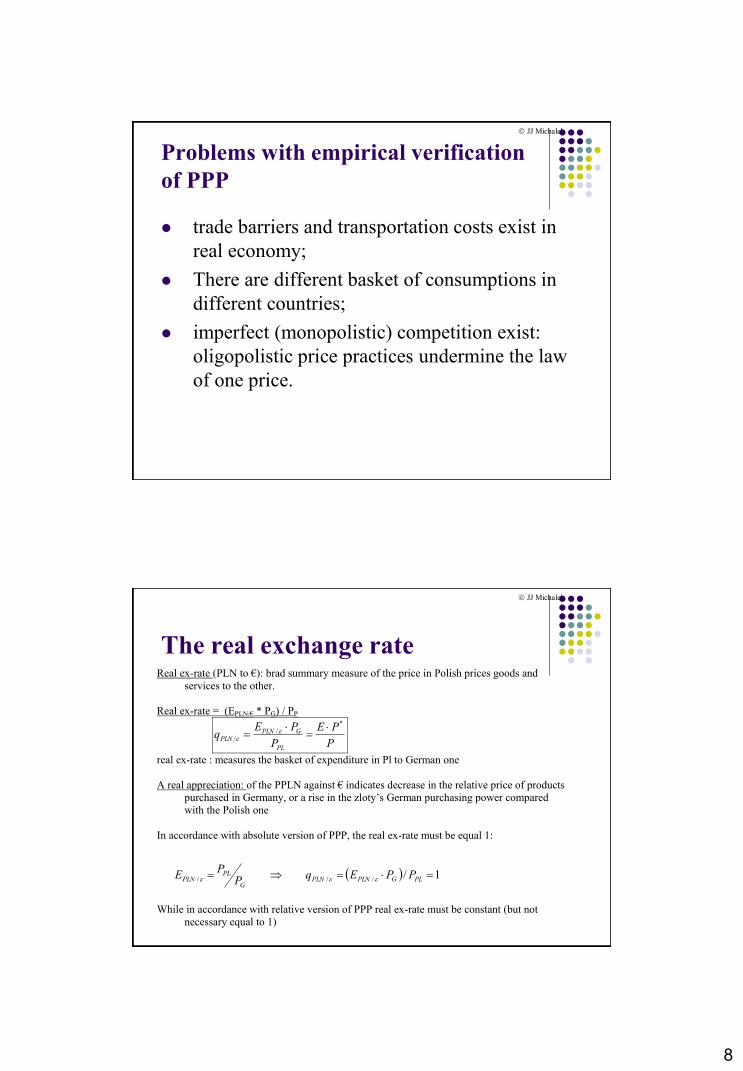

Problems with empirical verification

of PPP

trade barriers and transportation costs exist in

real economy;

There are different basket of consumptions in

different countries;

imperfect (monopolistic) competition exist:

oligopolistic price practices undermine the law

of one price.

JJ Michalek

The real exchange rate Real ex-rate (PLN to €): brad summary measure of the price in Polish prices goods and

services to the other.

Real ex-rate = (EPLN/€ * PG) / PP

P

PE

P

PEq

PL

GPLNPLN

*

/

real ex-rate : measures the basket of expenditure in Pl to German one

A real appreciation: of the PPLN against € indicates decrease in the relative price of products

purchased in Germany, or a rise in the zloty’s German purchasing power compared

with the Polish one

In accordance with absolute version of PPP, the real ex-rate must be equal 1:

While in accordance with relative version of PPP real ex-rate must be constant (but not

necessary equal to 1)

1//// PLGPLNPLNG

PLPLN PPEq

PP

E

JJ Michalek

9

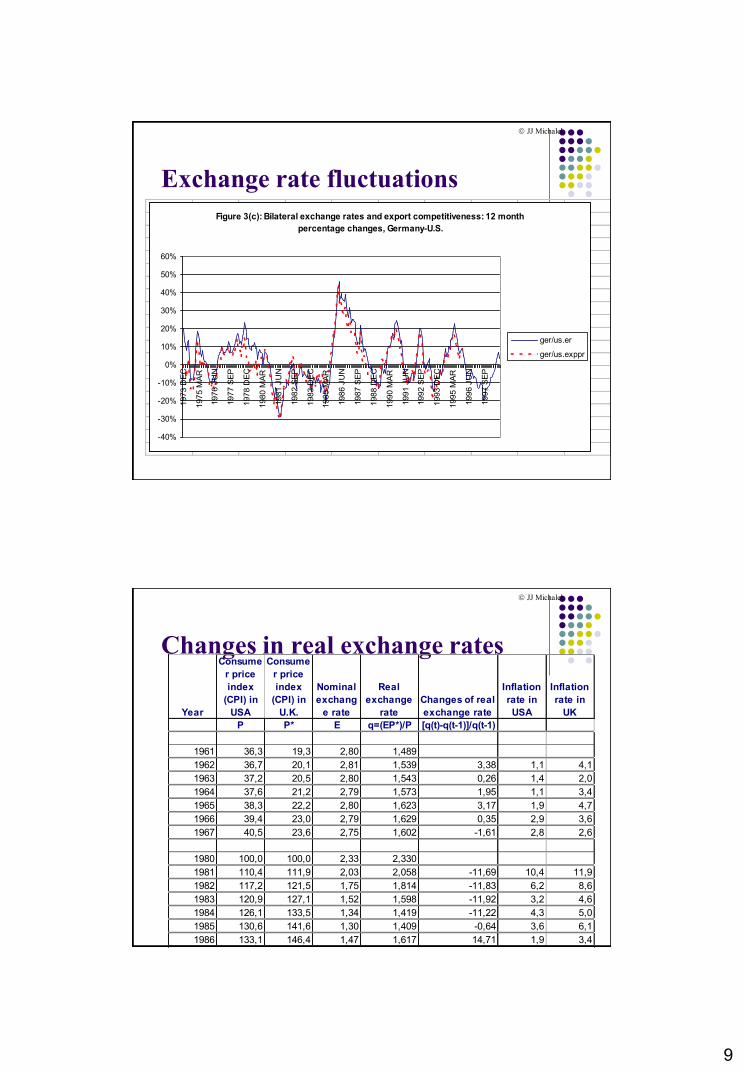

Exchange rate fluctuations

Figure 3(c): Bilateral exchange rates and export competitiveness: 12 month

percentage changes, Germany-U.S.

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1973 D

EC

1975 M

AR

1976 J

UN

1977 S

EP

1978 D

EC

1980 M

AR

1981 J

UN

1982 S

EP

1983 D

EC

1985 M

AR

1986 J

UN

1987 S

EP

1988 D

EC

1990 M

AR

1991 J

UN

1992 S

EP

1993 D

EC

1995 M

AR

1996 J

UN

1997 S

EP

ger/us.er

ger/us.exppr

JJ Michalek

Changes in real exchange rates

Year

Consume

r price

index

(CPI) in

USA

Consume

r price

index

(CPI) in

U.K.

Nominal

exchang

e rate

Real

exchange

rate

Changes of real

exchange rate

Inflation

rate in

USA

Inflation

rate in

UK

P P* E q=(EP*)/P [q(t)-q(t-1)]/q(t-1)

1961 36,3 19,3 2,80 1,489

1962 36,7 20,1 2,81 1,539 3,38 1,1 4,1

1963 37,2 20,5 2,80 1,543 0,26 1,4 2,0

1964 37,6 21,2 2,79 1,573 1,95 1,1 3,4

1965 38,3 22,2 2,80 1,623 3,17 1,9 4,7

1966 39,4 23,0 2,79 1,629 0,35 2,9 3,6

1967 40,5 23,6 2,75 1,602 -1,61 2,8 2,6

1980 100,0 100,0 2,33 2,330

1981 110,4 111,9 2,03 2,058 -11,69 10,4 11,9

1982 117,2 121,5 1,75 1,814 -11,83 6,2 8,6

1983 120,9 127,1 1,52 1,598 -11,92 3,2 4,6

1984 126,1 133,5 1,34 1,419 -11,22 4,3 5,0

1985 130,6 141,6 1,30 1,409 -0,64 3,6 6,1

1986 133,1 146,4 1,47 1,617 14,71 1,9 3,4

JJ Michalek

10

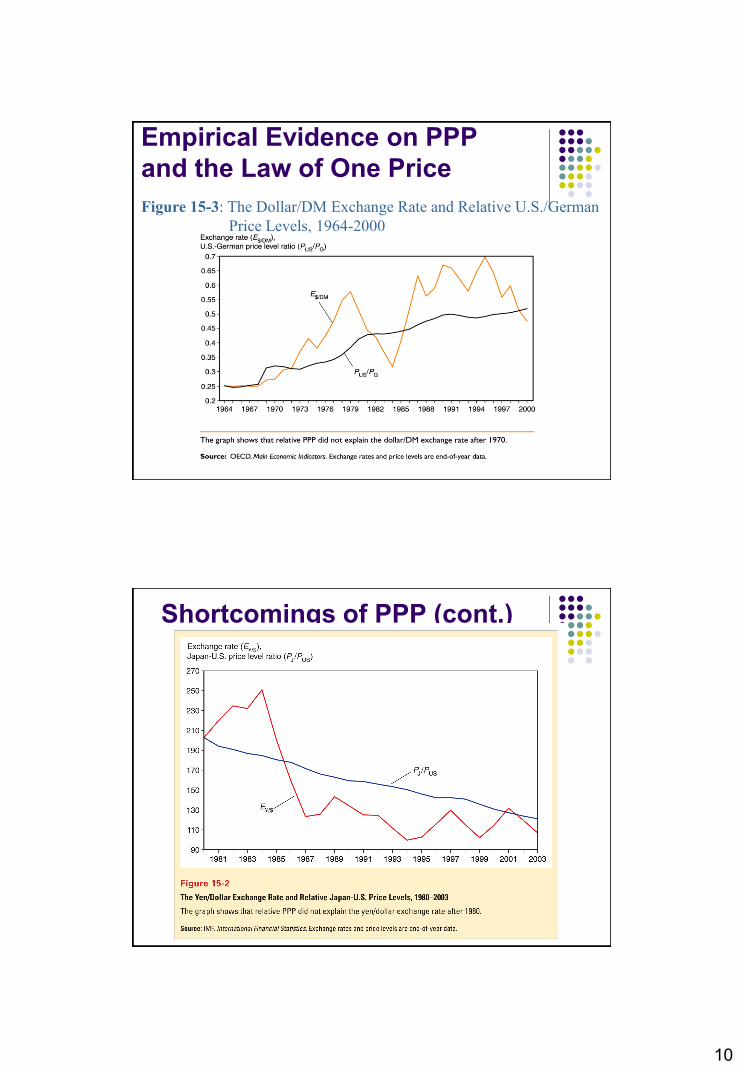

Empirical Evidence on PPP

and the Law of One Price

Figure 15-3: The Dollar/DM Exchange Rate and Relative U.S./German

Price Levels, 1964-2000

Shortcomings of PPP (cont.)

11

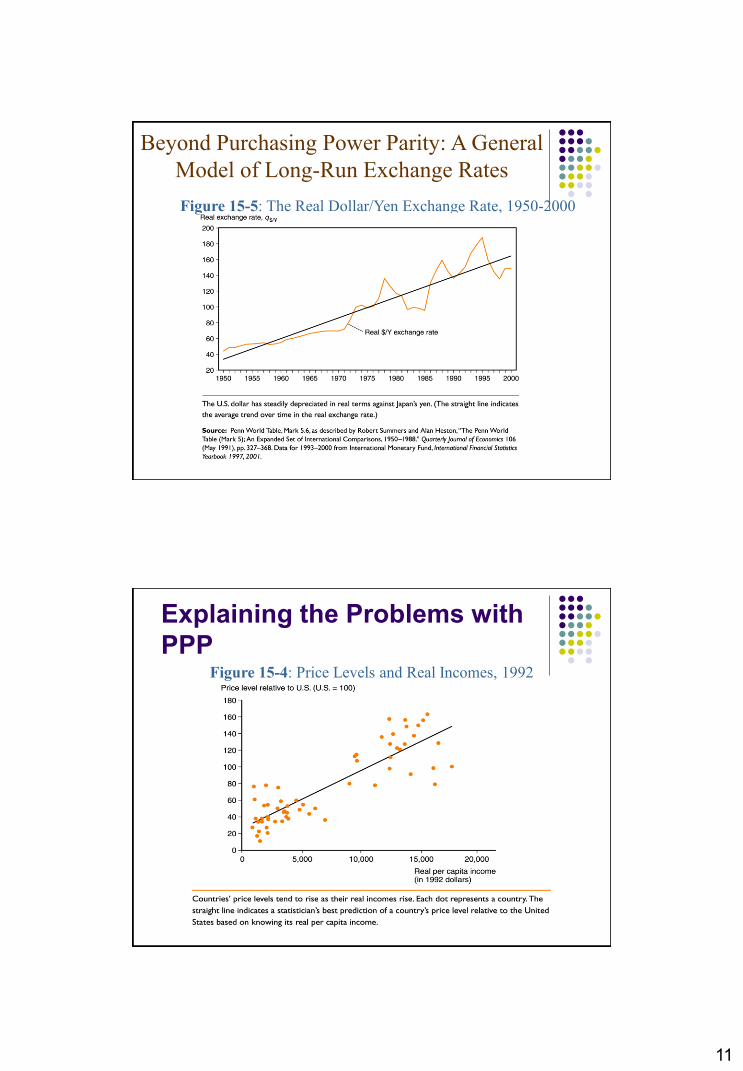

Beyond Purchasing Power Parity: A General

Model of Long-Run Exchange Rates

Figure 15-5: The Real Dollar/Yen Exchange Rate, 1950-2000

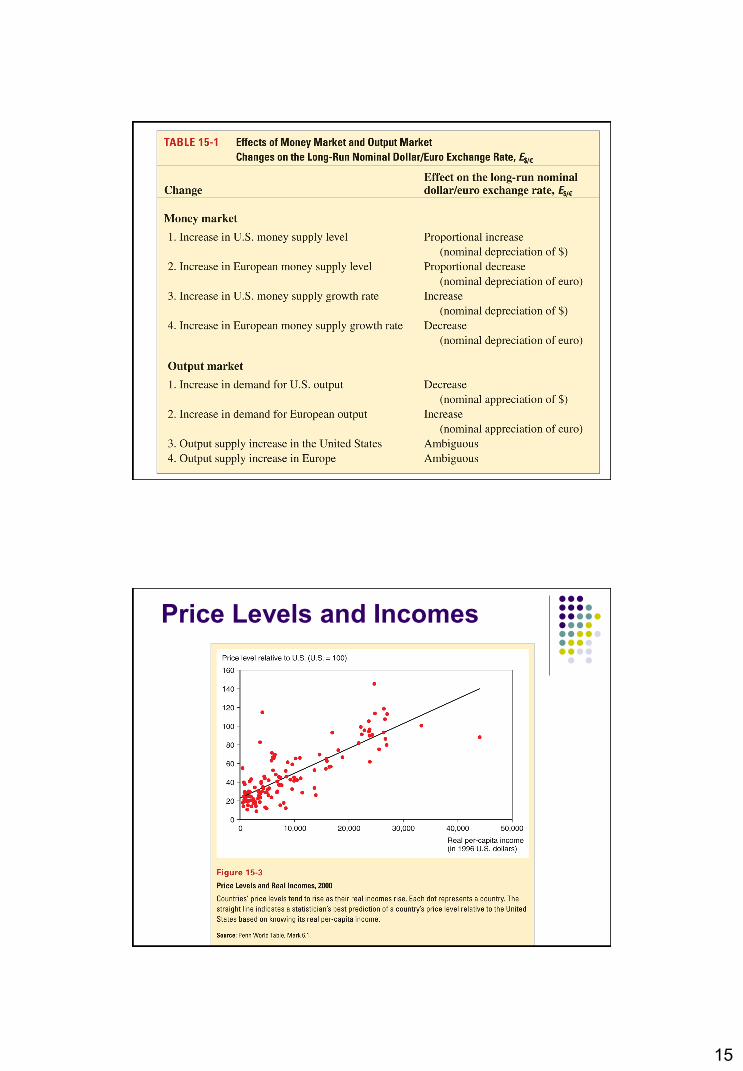

Explaining the Problems with

PPP Figure 15-4: Price Levels and Real Incomes, 1992

12

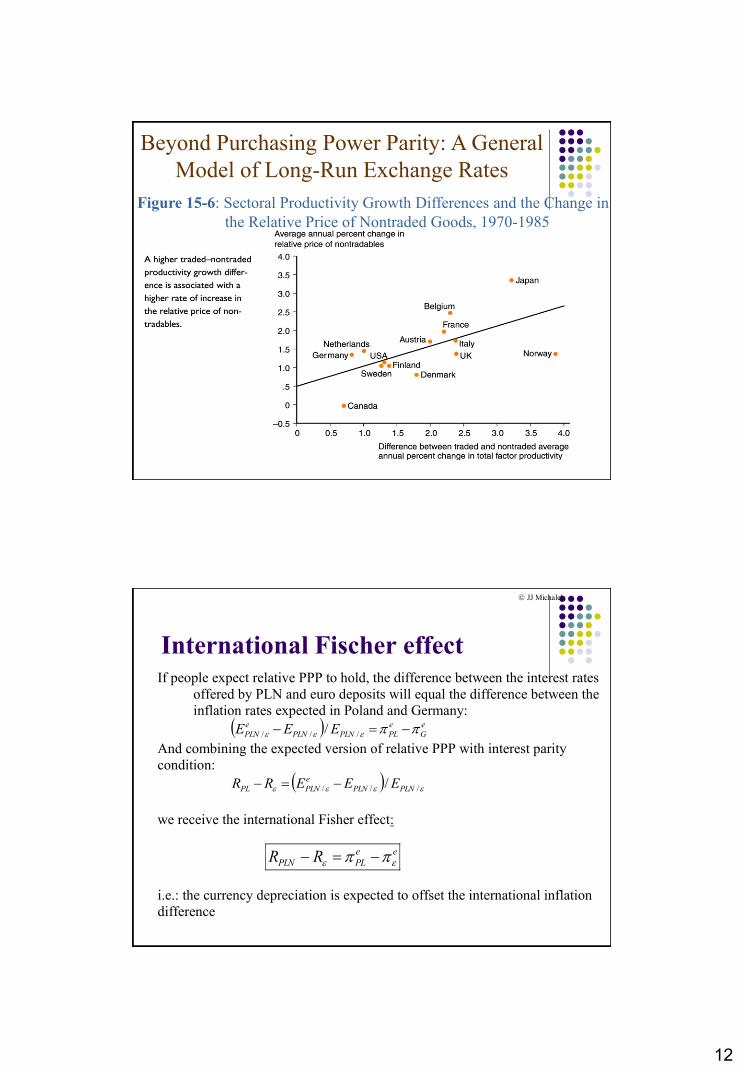

Figure 15-6: Sectoral Productivity Growth Differences and the Change in

the Relative Price of Nontraded Goods, 1970-1985

Beyond Purchasing Power Parity: A General

Model of Long-Run Exchange Rates

International Fischer effect If people expect relative PPP to hold, the difference between the interest rates

offered by PLN and euro deposits will equal the difference between the

inflation rates expected in Poland and Germany:

e

G

e

PLPLNPLN

e

PLN EEE /// /

And combining the expected version of relative PPP with interest parity

condition:

/// / PLNPLN

e

PLNPL EEERR

we receive the international Fisher effect:

ee

PLPLN RR

i.e.: the currency depreciation is expected to offset the international inflation

difference

JJ Michalek

13

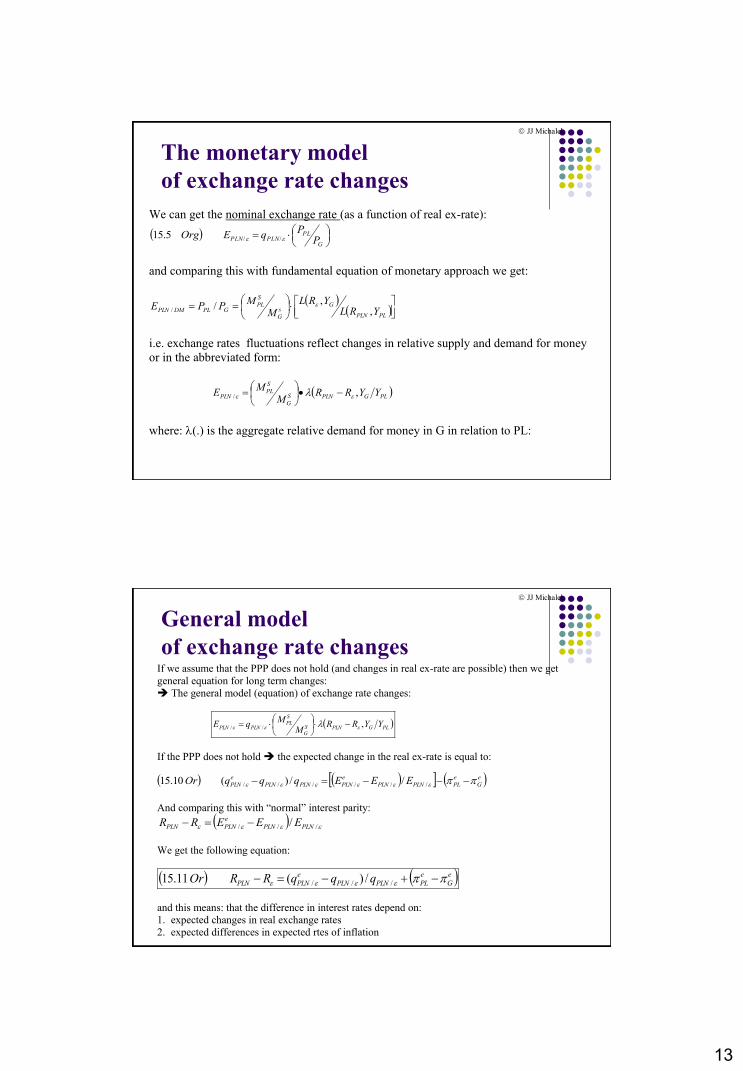

The monetary model

of exchange rate changes

We can get the nominal exchange rate (as a function of real ex-rate):

G

PLPLNPLN P

PqEOrg //5.15

and comparing this with fundamental equation of monetary approach we get:

PLPLN

Gs

G

S

PLGPLDMPLN YRL

YRLM

MPPE

,,

//

i.e. exchange rates fluctuations reflect changes in relative supply and demand for money

or in the abbreviated form:

PLGPLNS

G

S

PLPLN YYRR

MM

E ,/

where: (.) is the aggregate relative demand for money in G in relation to PL:

JJ Michalek

General model

of exchange rate changes If we assume that the PPP does not hold (and changes in real ex-rate are possible) then we get

general equation for long term changes:

The general model (equation) of exchange rate changes:

PLGPLNS

G

S

PLPLNPLN YYRR

MM

qE ,//

If the PPP does not hold the expected change in the real ex-rate is equal to:

And comparing this with “normal” interest parity:

We get the following equation:

eGe

PLPLNPLN

e

PLNPLN qqqRROr /// /)(11.15

and this means: that the difference in interest rates depend on:

1. expected changes in real exchange rates

2. expected differences in expected rtes of inflation

eGe

PLPLNPLN

e

PLNPLNPLN

e

PLN EEEqqqOr ////// //)(10.15

/// / PLNPLN

e

PLNPLN EEERR

JJ Michalek

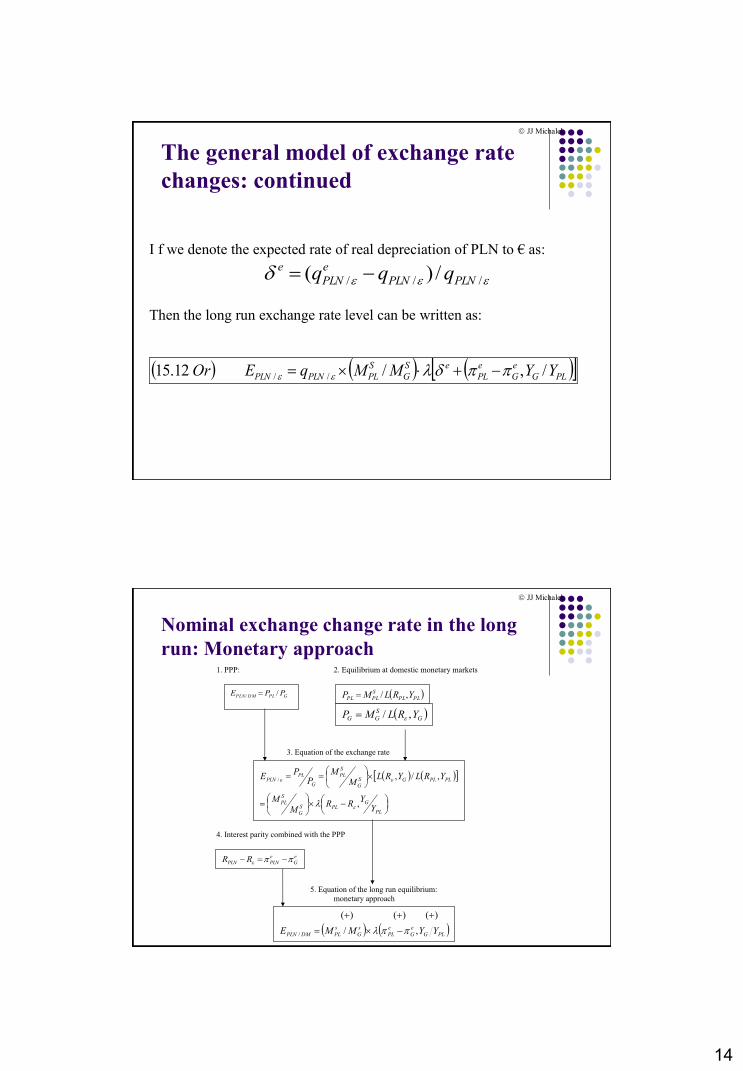

14

The general model of exchange rate

changes: continued

I f we denote the expected rate of real depreciation of PLN to € as:

/// /)( PLNPLN

e

PLN

e qqq

Then the long run exchange rate level can be written as:

PLG

e

G

e

PL

eS

G

S

PLPLNPLN YYMMqEOr /,/12.15 //

JJ Michalek

Nominal exchange change rate in the long

run: Monetary approach 1. PPP: 2. Equilibrium at domestic monetary markets

3. Equation of the exchange rate

4. Interest parity combined with the PPP

5. Equation of the long run equilibrium:

monetary approach

GPLDMPLN PPE // PLPL

S

PLPL YRLMP ,/

GS

GG YRLMP ,/

PL

GPLS

G

S

PL

PLPLGS

G

S

PL

G

PLPLN

YY

RRM

M

YRLYRLM

MP

PE

,

,/,/

e

G

e

PLNPLN RR

PLG

e

G

e

PL

s

G

s

PLDMPLN YYMME ,/

)()()(

/

JJ Michalek

15

Price Levels and Incomes

16

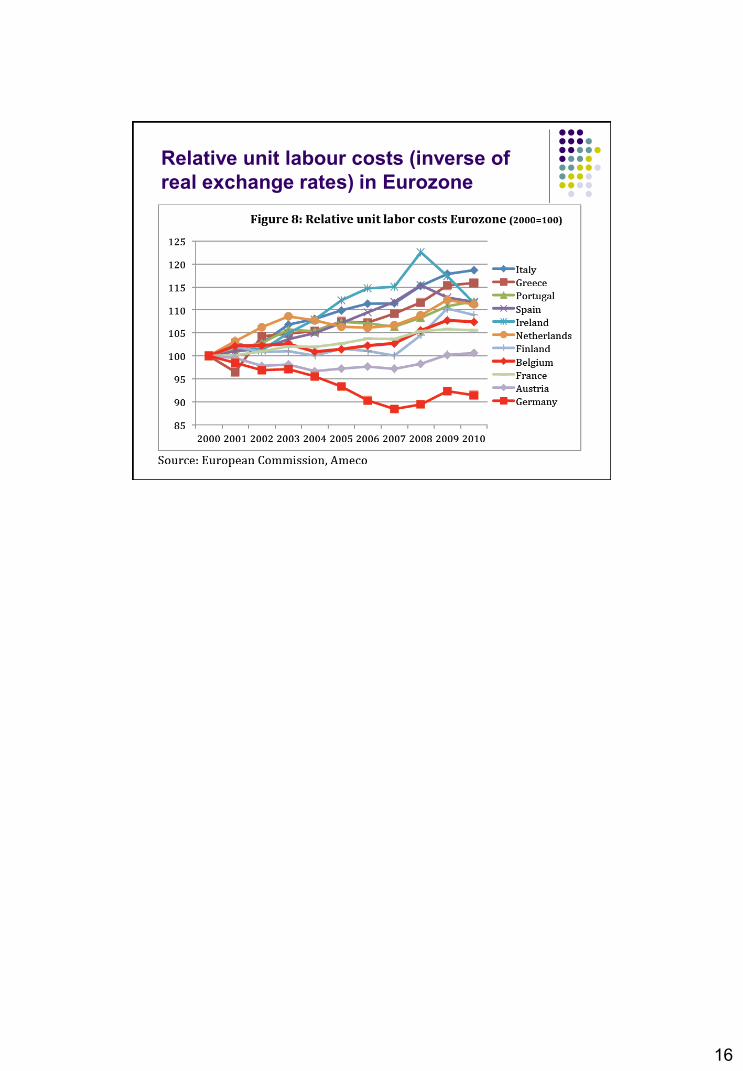

Relative unit labour costs (inverse of

real exchange rates) in Eurozone