Embed Size (px)

Citation preview

Updated March 2015 1

Derivatives Market Fees

BM&FBOVESPA S.A.

v.1. Julho/2014

Exchange-Traded

Derivatives

Exchange Fee

March 2015

Updated March 2015 2

Derivatives Market Fees

CALCULATION METHODOLOGY

The rules for the calculation of the exchange fees are

defined per group of products that present similar

features or purposes according to the tables below.

In this calculation, formulas or fixed values expressed

in Brazilian Reals or in a different reference unit may

be applied. In the case of fixed values expressed in a

reference unit different from Brazilian Reals, these

values must be converted into Brazilian Reals through

the application of an exchange rate or a market price.

A base factor of the exchange fee is defined to be

used in the calculation of exchange fees for each

group of products

The base factor of the exchange fee may be subject

to a discount depending on the average volume

traded by the customer applied to a tiered fee

schedule.

Applying the Tiered Fee Schedule – valid only to

exchange-traded products. The Exchange publishes a

tiered fee schedule for each contract or group of

contracts with the same underlying asset. Each tiered

fee schedule is composed of two volume limit-values

that determine the boundaries of the interval to be

considered as volume tier and one value that applies

to the exchange fee calculation formula.

The volume tier of a customer is obtained by

calculating the average volume traded in the contract

over a period of 21 consecutive trading sessions

immediately preceding and including the calculation

date. This calculation will be performed on the last

business day of each week and the average unit cost

per contract obtained through the application of the

volume to the tiered fee schedule will apply to all the

transactions with the given product that are carried

out during the week following the calculation.

For the purpose of calculating the number of traded

contracts, the aggregate volume traded by a customer

through all the brokerage houses with which the

customer holds an account must be considered. To

this end, the traded volume will be aggregated by

individual taxpayer’s number (CPF), corporate

taxpayer’s number (CNPJ) or capital markets

regulatory agency’s (CVM) number, thereby

increasing the tier discounts and allowing customers

the right to choose their brokerage houses.

The average unit value will be given by the following

formula:

The exchange fee refers to trading services. The exchange fee will be charged in the following

situations:

• The trading of a contract (opening or closing a position before the expiration date);

• The exercise of options;

• The procedure for assignment of rights.

For transactions with origin in direct market access (DMA), a 10% discount, cumulative with

volume discounts, will be granted. The exchange fees will be charged on the first business day

subsequent to the day its generating factor occurs.

EXCHANGE FEE

Where:

𝑴 = the aggregate volume traded in the contract by a customer through all the brokerage houses

with which that customer holds an account;

𝑸 𝟏 = M or the maximum volume for the first tier, whichever is the lowest;

𝑽 𝟏 = the value for the first tier;

𝑸 𝒊 = the maximum volume for the i-th tier, which exceeds the volume for the first tier, or zero, if M is

less than the minimum volume for the i-th tier;

𝑽 𝒊 = the value for i-th tier.

𝑨𝒗𝒆𝒓𝒂𝒈𝒆 𝑽𝒂𝒍𝒖𝒆 (𝒑) = 𝑸 𝟏 ∗ 𝑽 𝟏 + ⋯ + 𝑸 𝒊 − 𝑸 𝒊 − 𝟏 ∗ 𝑽 𝒊 + 𝑴 − 𝑸[𝒊 − 𝟏]) ∗ 𝑽[𝒊 + 𝟏]

Updated March 2015 3

Derivatives Market Fees

Group of products

Real-denominated interest rate

U.S. Dollar-denominated interest rate

Inflation-indexed interest rate

Inflation indexes

Gold

Stock indexes

Sovereign debt

Exchange rate

Commodities

EXCHANGE FEE

Updated March 2015 4

Derivatives Market Fees

Base contract for the average: DI futures

Applicable contracts:

• DI Futures Contract (One-day Interbank Deposit Futures Contract)

• Call and Put Option on DI Futures Contract

• Structured DI forward rate volatility transaction (VTF)

• Call and Put Option on Average One-Day Interbank Deposit Rate Index (IDI)

• Structured DI spot rate volatility transaction (VID)

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝟏𝟎𝟎. 𝟎𝟎𝟎 ∗ 𝟏 +𝒑

𝟏𝟎𝟎

𝒕𝒆𝒓𝒎𝟐𝟓𝟐

− 𝟏

Where:

𝒑 = the factor calculated by using the rule set forth in the Application of the Tiered Fee Schedule, or

the base factor if the customer does not have a previously calculated average value;

𝒕𝒆𝒓𝒎 = term of the operation, in reserve days, limited to a minimum of 1 and maximum of 105 days. The

value of the unit cost of the contracts based on Real-denominated interest rates is calculated based

on the number of basis points as a consequence of the put to par effect found in these contracts,

similarly to the calculation methodology for fixed income securities.

Options

30% of the unit cost of the exchange fee for the futures contract.

Day Trade (futures & options)

Futures = 35% of the unit cost of the exchange fee for a regular trade.

Options = 50% of the unit cost of the exchange fee for a regular trade.

REAL-DENOMINATED INTEREST RATE

Volume of Contracts Exchange Fee

From To %

1 100 0.0012022

101 1,260 0.0011421

1,261 2,800 0.0010218

2,801 7,300 0.0009618

7,301 47,900 0.0009016

Above 47,900 0.0007815

Application of the average value of the tier

Updated March 2015 5

Derivatives Market Fees

Base contract for the average: OC1 futures

Applicable contracts:

• OC1 Futures Contract

• Call and Put Option on ITC

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝟏𝟎𝟎. 𝟎𝟎𝟎 ∗ 𝟏 +𝒑

𝟏𝟎𝟎

𝒕𝒆𝒓𝒎𝟐𝟓𝟐

− 𝟏

Where:

𝒑 = the average value calculated after the application of the discount policy by volume traded in the

table above, expressed in annual percentage and rounded to the seventh decimal place;

𝒕𝒆𝒓𝒎 = term of the operation, in reserve days, limited to a minimum of 1 and maximum of 105 days.

Options

30% of the calculated value of the unit cost of the exchange fee and of the variable registration fee of

the futures contract.

Day Trade

Futures = 35% of the unit cost of the exchange fee for a regular trade.

Options = 50% of the unit cost of the exchange fee for a regular trade.

REAL-DENOMINATED INTEREST RATE

Volume of Contracts Exchange Fee

From To %

1 100 0.0012022

101 1,260 0.0011421

1,261 2,800 0.0010218

2,801 7,300 0.0009618

7,301 47,900 0.0009016

Above 47,900 0.0007815

Application of the average value of the tier

Updated March 2015 6

Derivatives Market Fees

Base contracts for the average: Forward rate agreement (FRA) on the DI x U.S. Dollar spread (FRC)

and DI x US Dollar Spread Futures Contract

Applicable contracts:

• DI x US Dollar Spread Futures Contract

• FRA on the DI x U.S. Dollar Spread

• DI x U.S. Dollar Swap with Reset (SCC)

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝟓𝟎. 𝟎𝟎𝟎 ∗𝒑

𝟏𝟎𝟎∗

𝒕𝒆𝒓𝒎

𝟑𝟔𝟎∗ 𝒅𝒐𝒍𝒍𝒂𝒓

Where:

𝒑 = average value calculated after the application of the discount policy by volume traded in the table

above, expressed in annual percentage and rounded to the seventh decimal place;

𝒕𝒆𝒓𝒎 = term of the operation, in calendar days, limited to a minimum of 30 and maximum of 270 days. For

the FRC the term of the operation is given by difference between the term at the long and the short

end of the contract;

𝒅𝒐𝒍𝒍𝒂𝒓 = the offered PTAX foreign exchange rate on the last day of the month prior to that of the transaction.

The value of the unit cost of the exchange fee of the contracts based on Real-denominated interest rates is

calculated based on the number of basis points as a consequence of the put to par effect found in these

contracts, similarly to the calculation methodology for fixed income securities.

Day Trade

50% of the unit cost of the exchange fee for a regular trade.

U.S. DOLLAR-DENOMINATED INTEREST RATE

Volume of Contracts Exchange Fee

From To % Annual

1 100 0.0016816

101 1,000 0.0015135

1,001 1,400 0.0014574

1,401 3,400 0.0013453

3,401 14,850 0.0012892

Above 14,850 0.0011771

Application of the average value of the tier

Updated March 2015 7

Derivatives Market Fees

Base contracts for the average: Forward rate agreement (FRA) on the OC1 x US Dollar Spread (FRO)

and OC1 x US Dollar Spread Futures Contract

Applicable contracts:

• OC1 x US Dollar Spread Futures Contract

• FRA on the OC1 x U.S. Dollar Spread (FRO)

• OC1 x U.S. Dollar Swap with Reset (SCS)

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝟓𝟎. 𝟎𝟎𝟎 ∗𝒑

𝟏𝟎𝟎∗

𝒕𝒆𝒓𝒎

𝟑𝟔𝟎∗ 𝒅𝒐𝒍𝒍𝒂𝒓

Where:

𝒑 = average value calculated after the application of the discount policy by volume traded in the table

above, expressed in annual percentage and rounded to the seventh decimal place;

𝒕𝒆𝒓𝒎 = term of the operation, in calendar days, limited to a minimum of 30 and maximum of 270 days. For

the FRC the term of the operation is given by difference between the term at the long and the short

end of the contract;

𝒅𝒐𝒍𝒍𝒂𝒓 = the offered PTAX foreign exchange rate on the last day of the month prior to that of the transaction.

The value of the unit cost of the exchange fee of the contracts based on Real-denominated interest rates is

calculated based on the number of basis points as a consequence of the put to par effect found in these

contracts, similarly to the calculation methodology for fixed income securities.

Day Trade

50% of the unit cost of the exchange fee for a regular trade.

U.S. DOLLAR-DENOMINATED INTEREST RATE

Volume of Contracts Exchange Fee

From To % Annual

1 100 0.0016816

101 1,000 0.0015135

1,001 1,400 0.0014574

1,401 3,400 0.0013453

3,401 14,850 0.0012892

Above 14,850 0.0011771

Application of the average value of the tier

Updated March 2015 8

Derivatives Market Fees

Base contracts for the average: DI x IGP-M Spread Futures Contract and DI x IPCA Spread Futures

Contract

Applicable contracts:

• DI x IGP-M Spread Futures Contract

• FRA on the DI x IGP-M Spread

• DI x IPCA Spread Futures Contract

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝟏𝟎𝟎. 𝟎𝟎𝟎 ∗ 𝑴 ∗ 𝒍 ∗ 𝟏 +𝒑

𝟏𝟎𝟎

𝒕𝒆𝒓𝒎𝟐𝟓𝟐

− 𝟏

Where:

𝒑 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated

average value;

𝒕𝒆𝒓𝒎 = term of the operation, in reserve days, limited to a minimum of 1 and maximum of 105 days. For

the FRM the term of the operation is given by difference between the term at the long and the short

end of the contract;

𝑴 = the contract multiplier to the value of BRL 0.005 for the DI x IGP-M spread and the FRA on the DI x

IGP-M spread, and to the value of BRL 0.0005 for the DI x IPCA spread;

𝒍 = inflation index number (IGP-M or IPCA, depending on the contract) announced for the month

previous to the calculation.

The value of the unit cost of the contracts based on Real-denominated interest rates is calculated based on

the number of basis points as a consequence of the put to par effect found in these contracts, similarly to the

calculation methodology for fixed income securities.

Day Trade

50% of the unit cost of the exchange fee for a regular trade.

INFLATION-INDEXED INTEREST RATE

Volume of Contracts Exchange Fee

From To %

1 10 0.0009016

11 50 0.0008415

51 130 0.0007815

131 150 0.0007213

151 300 0.0006612

Above 300 0.0006011

Application of the average value of the tier

Updated March 2015 9

Derivatives Market Fees

a) IGP-M

Base contracts for the average: IGP-M Futures Contract and FRA on the IGP-M

Applicable contracts:

• IGP-M Futures Contract

The unit value of each fee shall be calculated individually the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝑴 ∗ 𝒍

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated

average value;

𝑴 = the contract multiplier to the value of BRL 500,00;

𝒍 = inflation index number (IGP-M) announced for the month previous to the calculation.

Day Trade

50% of the unit cost of the exchange fee for a regular trade.

INFLATION INDEXES

Volume of Contracts Exchange Fee

From To Points

1 10 0.0000027

11 50 0.0000026

51 130 0.0000024

131 150 0.0000023

151 300 0.0000022

Above 300 0.0000019

Application of the average value of the tier

Updated March 2015 10

Derivatives Market Fees

b) IPCA

Base contracts for the average: IPCA Futures Contract and FRA on the IPCA

Applicable contracts:

• IPCA Futures Contract

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝑴 ∗ 𝒍

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated

average value;

𝑴 = the contract multiplier to the value of BRL 50,00;

𝒍 = inflation index number (IPCA) announced for the month previous to the calculation.

Day Trade

50% of the unit cost of the exchange fee for a regular trade.

INFLATION INDEXES

Volume of Contracts Exchage Fee

From To Points

1 10 0.0000024

11 50 0.0000023

51 130 0.0000022

131 150 0.0000021

151 300 0.0000020

Above 300 0.0000017

Application of the average value of the tier

Updated March 2015 11

Derivatives Market Fees

Base contracts for the average: Gold Spot Contract (250g) and Gold Futures Contract (250g)

Applicable contracts:

• Gold Spot Contract (250g)

• Gold Spot Contract (10g)

• Gold Spot Contract (0.225g)

• Gold Futures Contract (250g)

• Call and Put Options on Gold Spot Contract (250g)

• Gold Forward Contract (250g)

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝑴 ∗ 𝒅𝒐𝒍𝒍𝒂𝒓

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tieres Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝑴 = the contract multiplier to the equivalent of 250g, of which 0.04 to OZ2 and 0.0009 to OZ3;

𝒅𝒐𝒍𝒍𝒂𝒓 = the offered PTAX foreign exchange rate on the last day of the month prior to that of the transaction.

Options

30% of the unit cost of the exchange fee for the futures contract.

Day Trade (futures and options)

50% of the unit cost of the exchange fee for a regular trade.

GOLD

Volume of Contracts Exhange Fee

From To USD

1 10 0.33

11 50 0.31

51 130 0.29

131 150 0.28

151 300 0.27

Above 300 0.24

Application of the average value of the tier

Updated March 2015 12

Derivatives Market Fees

a) Ibovespa

Base contracts for the average: Ibovespa Futures Contract, Mini Ibovespa Futures Contract,

Structured Ibovespa Rollover Transaction and Brazil Index- 50 Futures Contract.

Applicable contracts:

• Ibovespa Futures Contract

• Forward Points on Ibovespa Futures Transaction (FWI)

• Call and Put Options on Ibovespa Futures Contract (American-style and European-style)

• Structured Ibovespa Volatility Transaction (VOI)

• Mini Ibovespa Futures Contract

• Structured Ibovespa Rollover Transaction (IR1)

• Brazil Index-50 Futures Contract (IBrX-50). In the case of the IBrX-50 Futures Contract, seeking to

promote liquidity, the values of the unit cost of the exchange fee and of the variable registration fee have

been reduced, and this product is now included in the group of Ibovespa Futures products.

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value.

Options

100% of the unit cost of the exchange fee for the futures contract.

Mini contract

12% of the unit cost of the exchange fee for the standard futures contract.

Day Trade (futures, options and mini contracts)

Futures = 30% of the unit cost of the exchange fee for a regular trade.

Options = 30% of the unit cost of the exchange fee for a regular trade.

Mini contracts = 50% of the unit cost of the exchange fee for a regular trade.

STOCK INDEXES

Volume of Contracts Exhange Fee

From To BRL

1 10 0.91

11 50 0.81

51 100 0.78

101 190 0.73

191 2,000 0.68

Above 2,000 0.64

Application of the average value of the tier

Updated March 2015 13

Derivatives Market Fees

b) S&P 500

Base contracts for the average: BVMFS&P 500 Index Futures Contract and Structured Rollover

Transaction of the BVMF S&P 500 Index Futures Contract

Applicable contracts:

• BVMF S&P 500 Index Futures Contract

• Structured Rollover Transaction of the BVMF S&P 500 Index Futures Contract

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝒅𝒐𝒍𝒍𝒂𝒓

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝒅𝒐𝒍𝒍𝒂𝒓 = the offered PTAX foreign exchange rate on the last day of the month prior to that of the transaction.

STOCK INDEXES

Volume of Contracts Exhange Fee

From To USD

1 190 0.60

191 2000 0.45

Above 2,000 0.24

Application of the average value of the tier

Updated March 2015 14

Derivatives Market Fees

c) Indexes Futures Contracts with Cash Settlement Denominated in Points of Indexes:

• SENSEX Index

• FTSE/JSE Top 40 Index

• Hang Seng Index

• MICEX Index

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value.

Day Trade

50% of the unit cost of the exchange fee for a regular trade.

STOCK INDEXES

Volume of Contracts Exchange Fee

From To BRL

1 10 0.16

11 50 0.15

51 100 0.14

101 190 0.13

191 2,000 0.12

Above 2,000 0.11

Application of the average value of the tier

Updated March 2015 15

Derivatives Market Fees

Base contracts for the average: Global Bond Futures Contract, A-Note 2018 Futures Contract, Ten-

Year U.S. Treasury Note Futures Contract

Applicable contracts:

• Global Bond Futures Contract

• A-Note 2018 Futures Contract

• Ten-Year U.S. Treasury Note Futures Contract (T10)

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝒅𝒐𝒍𝒍𝒂𝒓

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝒅𝒐𝒍𝒍𝒂𝒓 = the offered PTAX foreign exchange rate on the last day of the month prior to that of the transaction.

Day Trade

50% of the unit cost of the exchange fee for a regular trade.

SOVEREIGN DEBT

Volume of Contracts Exhange Fee

From To USD

1 25 0.53

26 50 0.50

51 200 0.45

201 250 0.42

251 400 0.39

Above 400 0.34

Application of the average value of the tier

Updated March 2015 16

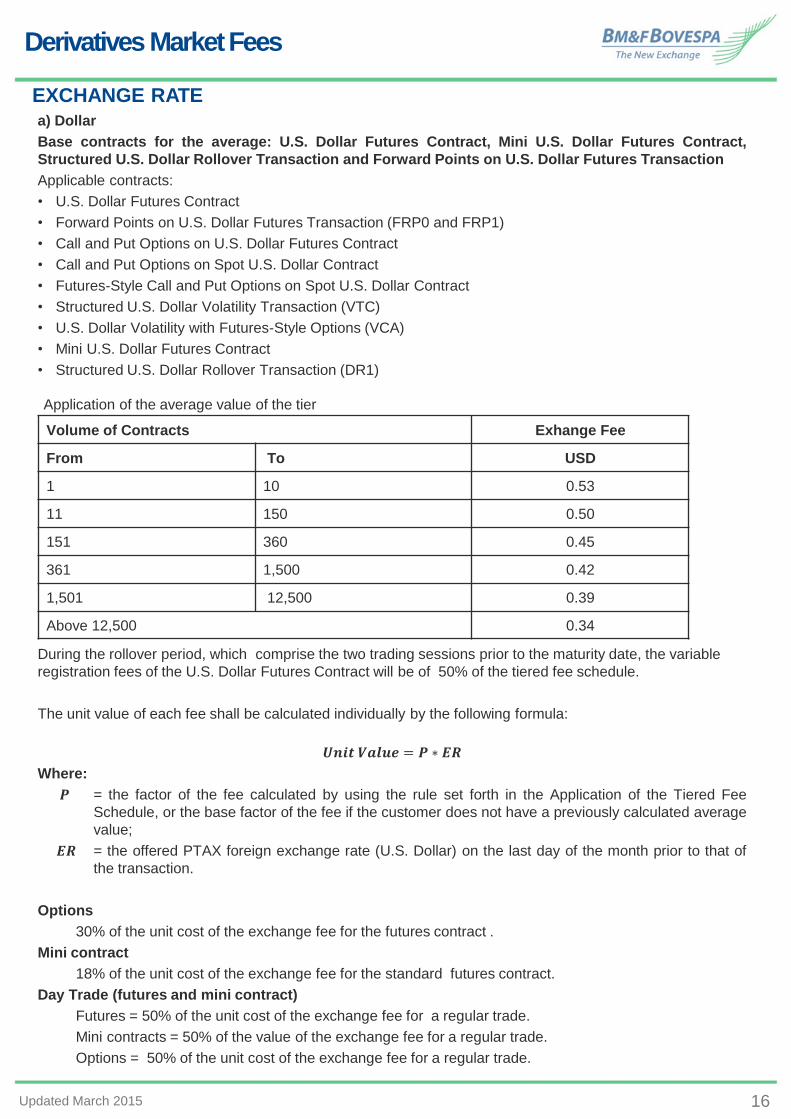

Derivatives Market Fees

a) Dollar

Base contracts for the average: U.S. Dollar Futures Contract, Mini U.S. Dollar Futures Contract,

Structured U.S. Dollar Rollover Transaction and Forward Points on U.S. Dollar Futures Transaction

Applicable contracts:

• U.S. Dollar Futures Contract

• Forward Points on U.S. Dollar Futures Transaction (FRP0 and FRP1)

• Call and Put Options on U.S. Dollar Futures Contract

• Call and Put Options on Spot U.S. Dollar Contract

• Futures-Style Call and Put Options on Spot U.S. Dollar Contract

• Structured U.S. Dollar Volatility Transaction (VTC)

• U.S. Dollar Volatility with Futures-Style Options (VCA)

• Mini U.S. Dollar Futures Contract

• Structured U.S. Dollar Rollover Transaction (DR1)

During the rollover period, which comprise the two trading sessions prior to the maturity date, the variable

registration fees of the U.S. Dollar Futures Contract will be of 50% of the tiered fee schedule.

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝑬𝑹

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝑬𝑹 = the offered PTAX foreign exchange rate (U.S. Dollar) on the last day of the month prior to that of

the transaction.

Options

30% of the unit cost of the exchange fee for the futures contract .

Mini contract

18% of the unit cost of the exchange fee for the standard futures contract.

Day Trade (futures and mini contract)

Futures = 50% of the unit cost of the exchange fee for a regular trade.

Mini contracts = 50% of the value of the exchange fee for a regular trade.

Options = 50% of the unit cost of the exchange fee for a regular trade.

EXCHANGE RATE

Volume of Contracts Exhange Fee

From To USD

1 10 0.53

11 150 0.50

151 360 0.45

361 1,500 0.42

1,501 12,500 0.39

Above 12,500 0.34

Application of the average value of the tier

Updated March 2015 17

Derivatives Market Fees

b) Euro

Base contracts for the average: Euro Futures Contracts (EUR and EBR).

Applicable contracts:

• Euro Futures Contract (EUR)

• Euro Futures Contract (EBR)

• Mini Euro Futures Contract

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝑬𝑹

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝑬𝑹 = the offered PTAX foreign exchange rate (Euro) on the last day of the month prior to that of the

transaction.

Mini contract

18% of the unit cost of the exchange fee for the standard futures contract .

Day Trade (futures and mini contract)

Futures = 50% of the unit cost of the exchange fee for a regular trade.

Mini contracts = 50% of the unit cost of the exchange fee for a regular trade.

EXCHANGE RATE

Volume of Contracts Exhange Fee

From To EUR

1 20 0.55

21 50 0.53

51 130 0.47

131 150 0.44

151 1,000 0.41

Above 1,000 0.36

Application of the average value of the tier

Updated March 2015 18

Derivatives Market Fees

c) Other currencies

Base contracts for the average: Australian Dollar Futures Contract (AUD), Canadian Dollar Futures

Contract (CAD), Japanese Yen Futures Contract (JPY), Pound Sterling Futures Contract (GBP),

Mexican Peso Futures Contract (MXN), New Zeland Futures Contract (NZD), Swiss Franc Futures

Contract (CHF), Chinese Yuan Futures Contract (CNY), Turkish Lira Futures Contracts (TRY), Chilean

Peso Futures Contract (CLP), South African Rand Futures Contract (ZAR)

Applicable contracts:

• Australian Dollar Futures Contract (AUD)

• Canadian Dollar Futures Contract (CAD)

• Japanese Yen Futures Contract (JPY)

• Pound Sterling Futures Contract (GBP)

• Mexican Peso Futures Contract (MXN)

• New Zeland Futures Contract (NZD)

• Swiss Franc Futures Contract (CHF)

• Chinese Yuan Futures Contract (CNY)

• Turkish Lira Futures Contracts (TRY)

• Chilean Peso Futures Contract (CLP)

• South African Rand Futures Contract (ZAR)

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝑬𝑹

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝑬𝑹 = the offered PTAX foreign exchange rate (U.S. Dollar) on the last day of the month prior to that of

the transaction .

Day Trade (futures)

Futures = 50% of the unit cost of the exchange fee for a regular trade.

EXCHANGE RATE

Volume of Contracts Exhange Fee

From To USD

1 20 0.53

21 50 0.50

51 130 0.45

131 150 0.42

151 1,000 0.39

Above 1,000 0.34

Application of the average value of the tier

Updated March 2015 19

Derivatives Market Fees

a) Sugar

Base contracts for the average: Crystal Sugar Futures Contract and Maturity Rollover for Cash Settled

Crystal Sugar Futures Contract

Applicable contracts:

• Crystal Sugar Futures Contract

• Call and Put Options on Crystal Sugar Futures Contract

• Maturity Rollover for Cash Settled Crystal Sugar Futures Contract

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value.

Options

30% of the unit cost of the exchange fee for the futures contract.

Day Trade (futures and options)

50% of the unit cost of the exchange fee for a regular trade.

COMMODITIES

Volume of Contracts Exhange Fee

From To BRL

1 25 0.82

26 50 0.80

51 85 0.73

86 120 0.70

121 250 0.65

Above 251 0.58

Application of the average value of the tier

Updated March 2015 20

Derivatives Market Fees

b) Live Cattle

Base contracts for the average: Real-denominated Live Cattle Futures Contract and Structured Live

Cattle Rollover Transaction.

Applicable contracts:

• Real-denominated Live Cattle Futures Contract

• Call and Put Options on Real-denominated Live Cattle Futures Contract

• Structured Live Cattle Rollover Transaction

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value.

Options

30% of the unit cost of the exchange fee for the futures contract.

Day Trade (futures and options)

30% of the unit cost of the exchange fee for a regular trade.

COMMODITIES

Volume of Contracts Exhange Fee

From To BRL

1 5 1,27

6 10 1,21

11 20 1,14

21 30 1,08

31 150 1,00

Above 150 0,93

Application of the average value of the tier

Updated March 2015 21

Derivatives Market Fees

c) Arabica Coffee

Base contracts for the average: 4/5 and 6/7 Arabica Coffee Futures Contract and Structured 4/5 and

6/7 Arabica Coffee Rollover Transaction

Applicable contracts:

• 4/5 Arabica Coffee Futures Contract

• Option on 4/5 Arabica Coffee Futures

• Structured 4/5 Arabica Coffee Rollover Transaction

• 6/7 Arabica Coffee Futures Contract

• Option on 6/7 Arabica Coffee Futures

• Structured 6/7 Arabica Coffee Rollover Transaction

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝒅𝒐𝒍𝒍𝒂𝒓

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝒅𝒐𝒍𝒍𝒂𝒓 = the offered PTAX foreign exchange rate on the last day of the month prior to that of the transaction.

Options

4/5 Coffee Options = 30% of the unit cost of the exchange fee for the futures contract.

6/7 Coffee Options = 50% of the unit cost of the exchange fee for the futures contract

Day Trade (futures and options)

4/5 and 6/7 Futures = 30% of the unit cost calculated for the Exchange Fee

4/5 Coffee Options = 30% of the Unit Cost calculated for the Exchange Fee.

6/7 Coffee Options = 50% of the Unit Cost calculated for the Exchange Fee

COMMODITIES

Volume of Contracts Exhange Fee

From To USD

1 5 0.41

6 10 0.39

11 20 0.37

21 100 0.35

101 200 0.33

Above 200 0.28

Application of the average value of the tier

Updated March 2015 22

Derivatives Market Fees

d) Anhydrous Fuel Ethanol

Base contract for the average: Anhydrous Fuel Ethanol Futures Contract

Applicable contract:

• Anhydrous Fuel Ethanol Futures Contract

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value.

Day Trade

50% of the unit cost of the exchange fee for a regular trade.

COMMODITIES

Volume of Contracts Exhange Fee

From To BRL

1 5 1.67

6 25 1.59

26 65 1.50

66 75 1.42

76 100 1.33

Above 100 1.26

Application of the average value of the tier

Updated March 2015 23

Derivatives Market Fees

e) Hydrous Ethanol

Base contract for the average: Hydrous Ethanol Futures Contract

Applicable contracts:

• Hydrous Ethanol Futures Contract

• Call and Put Options on Cash Settled Hydrous Ethanol Futures Contract

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value.

Options

30% of the unit cost of the exchange fee for the futures contract.

Day Trade (futures and options)

Futures and options = 30% of the unit cost of the exchange fee for a regular trade.

COMMODITIES

Volume of Contracts Exhange Fee

From To BRL

1 5 1.67

6 25 1.59

26 65 1.50

66 75 1.42

76 100 1.33

Above 100 1.26

Application of the average value of the tier

Updated March 2015 24

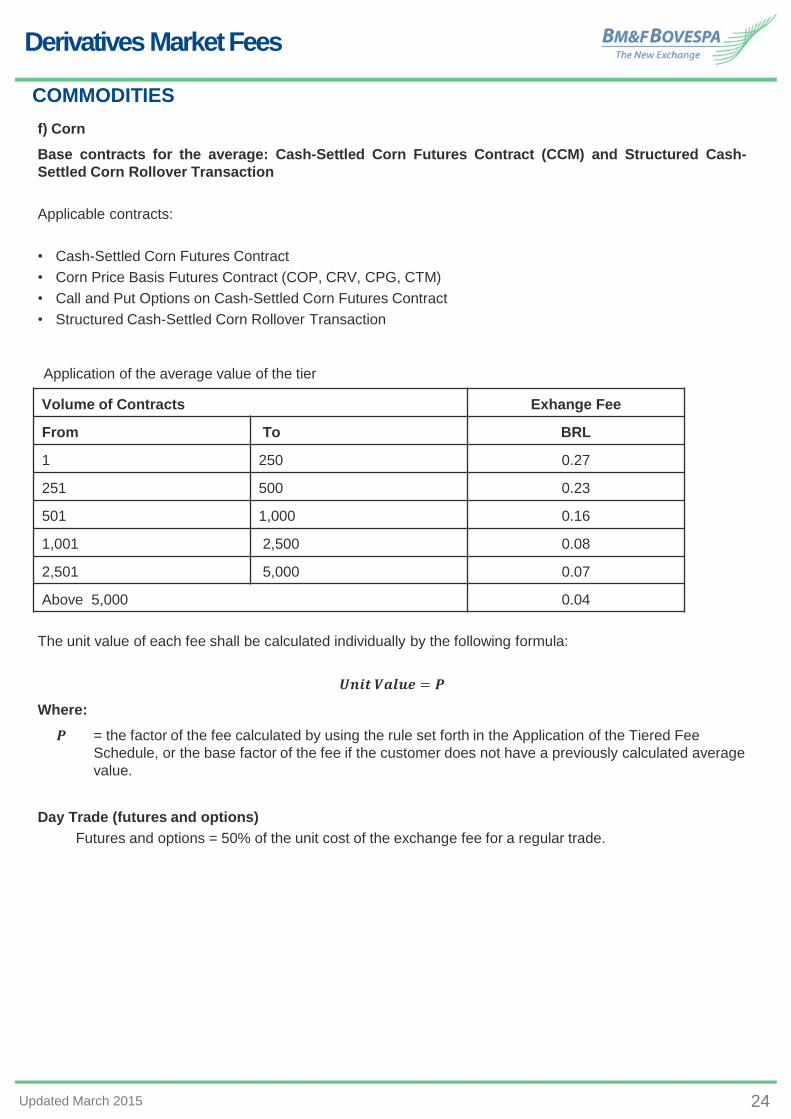

Derivatives Market Fees

f) Corn

Base contracts for the average: Cash-Settled Corn Futures Contract (CCM) and Structured Cash-

Settled Corn Rollover Transaction

Applicable contracts:

• Cash-Settled Corn Futures Contract

• Corn Price Basis Futures Contract (COP, CRV, CPG, CTM)

• Call and Put Options on Cash-Settled Corn Futures Contract

• Structured Cash-Settled Corn Rollover Transaction

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value.

Day Trade (futures and options)

Futures and options = 50% of the unit cost of the exchange fee for a regular trade.

COMMODITIES

Volume of Contracts Exhange Fee

From To BRL

1 250 0.27

251 500 0.23

501 1,000 0.16

1,001 2,500 0.08

2,501 5,000 0.07

Above 5,000 0.04

Application of the average value of the tier

Updated March 2015 25

Derivatives Market Fees

g) Cash-Settled Soybean (SFI)

Base contract for the average: Cash-Settled Soybean Futures

Applicable contracts:

• The Cash-Settled Soybean Futures Contract

• Call and Put Options on the Cash-Settled Soybean Futures Contract

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝒅𝒐𝒍𝒍𝒂𝒓

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝒅𝒐𝒍𝒍𝒂𝒓 = the offered PTAX (U.S. Dollar) on the last day of the month prior to that of the transaction.

Options

50% of the unit cost of the exchange fee for the futures contract.

Day Trade (futures and options)

50% of the unit cost of the exchange fee for a regular trade.

COMMODITIES

Volume of Contracts Exhange Fee

From To USD

1 250 0.20

251 500 0.17

501 1,000 0.12

1,001 2,500 0.09

2,501 5,000 0.06

Above 5,000 0.04

Application of the average value of the tier

Updated March 2015 26

Derivatives Market Fees

h) Cash-Settled Soybean of CME Group (SJC)

The unit value of each fee shall be calculated individually by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝒅𝒐𝒍𝒍𝒂𝒓

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝒅𝒐𝒍𝒍𝒂𝒓 = the offered PTAX (U.S. Dollar) on the last day of the month prior to that of the transaction.

N = Number of contracts negotiated bigger than 1 .

Day Trade

It will not be attributed a special fee scheme for day trade transactions.

COMMODITIES

Volume of Contracts Exhange Fee

From To USD

1 N 0.30

Application of the average value of the tier

Updated March 2015 27

Derivatives Market Fees

i) Cash-Settled Mini Crude Oil Futures Contract (WTI)

Base contracts for the average: Cash-Settled Mini Crude Oil Futures Contract (WTI)

The unit value of each fee shall be calculated by the following formula:

𝑼𝒏𝒊𝒕 𝑽𝒂𝒍𝒖𝒆 = 𝑷 ∗ 𝒅𝒐𝒍𝒍𝒂𝒓

Where:

𝑷 = the factor of the fee calculated by using the rule set forth in the Application of the Tiered Fee

Schedule, or the base factor of the fee if the customer does not have a previously calculated average

value;

𝒅𝒐𝒍𝒍𝒂𝒓 = the offered PTAX (U.S. Dollar) on the last day of the month prior to that of the transaction.

N = Number of contracts negotiated bigger than 1 .

Day Trade

It will not be attributed a special fee scheme for day trade transactions with the Cash-Settled Mini

Crude Oil Futures Contract, being applicable the values described above.

COMMODITIES

Volume of Contracts Exhange Fee

From To USD

1 N 0.52

Application of the average value of the tier

Updated March 2015 28

Derivatives Market Fees