Embed Size (px)

Citation preview

i

EXECUTIVE SUMMARY

1. Introduction

The Autonomous Region in Muslim Mindanao (ARMM) was created pursuant to

Republic Act No. 6734, otherwise known as the Organic Act Providing for the Establishment

of an Autonomous Region in Muslim Mindanao. This was strengthened by RA 9054 which

expands the Organic Act for the Autonomous Region in Muslim Mindanao, amending RA

6734.

The Autonomous Regional Government (ARG) of ARMM shall have the power to

create its own sources of revenues and levy taxes, fees, and charges. It shall have fiscal

autonomy, not only in generating but also in budgeting its own sources of revenue, its share

from the internal revenue taxes, and grants and subsidies received from the National

Government (NG). Despite its autonomous nature, the ARMM’s operation is funded by the

NG through the general appropriations acts.

The ARG is headed by MUJIV S. HATAMAN, elected Regional Governor in

ARMM, who is the chief executive of the ARG and have control of all the regional executive

commissions, agencies, boards, bureaus, and offices except those provided for in R.A. No.

9054. The Office of the Regional Governor (ORG-ARMM) serves as conduit of all releases to

the entire region, to include its 26 Regional Government Agencies (RGAs) funded by the

National Government and 20 Locally Created Offices which are attached to ORG and other

Regional Government Agencies with no fiscal autonomy are all funded out of the ARG Local

Fund Budget.

The 26 RGAs and Offices of the ARG covered by this report are the following:

1. Office of the Regional Governor (ORG)

2. Office of the Regional Vice-Governor (ORVG)

3. Cooperative Development Authority (CDA)

4. Commission on Higher Education (CHED)

5. Department of Agriculture and Fisheries (DAF)

6. Department of Agrarian Reform (DAR)

7. Department of Environment and Natural Resources (DENR)

8. Department of Education (DEPED)

9. Department of Interior and Local Government (DILG)

10. Department of Health (DOH)

11. Department of Labor and Employment (DOLE)

12. Department of Science and Technology (DOST)

13. Department of Tourism (DOT)

14. Department of Transportation and Communication (DOTC)

15. Department of Public Works and Highways (DPWH)

16. Department of Social Welfare and Development (DSWD)

17. Department of Trade and Industry (DTI)

ii

18. Housing and Land Use Regulatory Board (HLURB)

19. Office of the Regional Treasury (ORT)

20. Office for Southern Cultural Communities (OSCC)

21. Regional Board of Investment (RBOI)

22. Regional Planning and Development Office (RPDO)

23. Regional Tripartite Wages and Productivity Board (RTWPB)

24. Technical Education and Skills Development Authority (TESDA)

25. Regional Human Rights Commission (RHRC)

26. Bureau of Fisheries and Aquatic Resources (BFAR)

Also, pursuant to Section 19, Article VI of R.A. No. 9054, the ARG had Locally

Created Offices funded out of the Local Fund Budget.

1. Regional Budget and Management Office (RBMO)

2. ARMM Development Academy (ADA)

3. Bureau of Cultural Heritage (BCH)

4. Coordinating Development Office, Bangsamoro Youth Affairs (CDO-BYA)

5. Regional Commission on Bangsamoro Women (RCBW)

6. Regional Reconciliation and Unification Commision (RRUC)

7. Regional Sports Coordinating Office (RSCO)

8. Southern Philippne Development Authority (SPDA)

9. ARMM Regional Library (ARL)

10. Joint Peace and Development Monitoring Committee (JPDMC)

11. ARMM Humanitarian Emergency Assistance Response Team (A-HEART)

12. Office of the Attorney General (OAG)

13. Bureau of Public Information (BPI)

14. Regional Housing and Rural Development Authority- Project Management Office

(RHRDA-PMO)

15. Regional Economic Zone Authority (REZA)

16. Regional Ports Management Authority. (RRMA)

17. Regional Economic Zone Authority – Polloc Freeport (REZA-PF)

18. Bureau of Madaris Education (BME)

19. Regional Madrasah Graduate Academy (RMGA)

20. Regional Darul Ifta (RDI)

Audit Scope:

The audit covered the operations and financial transactions of the Autonomous Regional

Government, ARMM for calendar year 2015.

2. Financial Highlights

The ARG-ARMM consolidated financial condition, results of operations for the

calendar year 2015, to include the General Fund, Local Fund and Trust Fund is presented as

follows:

iii

Financial Condition:

Particulars CY 2015

Assets P9,996,995,284.44

Liabilities 3,123,907,791.25

Equity P6,873,087,493.19

Results of Operations;

Particulars CY 2015

Total Income P26,337,745,975.07

Total Expenses 22,518,186,011.16

Excess of Income over Expenses P3,819,559,963.91

3. Opinion of the auditor on the fairness of presentation of the financial statements.

The Auditor rendered a Qualified opinion on the fairness of presentation of the

financial statements of the Regional Government Agencies in ARMM as of December 31,

2015 in view of the deficiencies noted in the accounts and non-compliance with the existing

laws, rules and regulations as stated in the Independent Auditor’s Report and discussed in

detail in Part II of this report.

4. Summary of Significant Observations and Recommendations:

4.1 120 school buildings with a contract cost totaling P177,632,862.31 under the

DepEd School Building Program (SBP) for CY 2011 implemented by the Office

of the Regional Governor (ORG-ARMM) and 682 classrooms totaling

P501,902,166.19 under SBP for CY 2012 implemented by DepEd-ARMM

remained unfinished as of December 31, 2015 in violation of the provisions of the

signed Contract Agreement between the Contractors and the ORG-ARMM.

Conduct inspection/evaluation on the uncompleted projects to determine their present existing conditions and status whether the projects are being utilized or not

indicating the reasons for non-utilization.

Explore all the possibilities on how to make use of the projects to recover part of its cost to prevent the projects from further deterioration and damage.

If delay cannot be fully justified, impose liquidated damages and terminate or

rescind the contracts and enforce appropriate legal action against the concerned

contractors.

iv

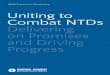

4.2 Fund transfers from ORG, DA, DSWD, DILG, DPWH and ORT to various

Implementing Agencies (IA) total P2,853,879,155.59 remained unliquidated as

of year-end contrary to COA Circular No. 94-013 dated December 13, 1994 and

COA Circular No. 2012-01 dated June 14, 2012.

Require the concerned RGAs, Local Government Units (LGUs), OUs, and NGO/POs to direct their respective Accountants to submit the RCI and RD

certified correct by the Accountant, approved by the Head of the IA, and duly

audited by the Auditor of the IA; Copy of Credit Notice issued by the Auditor of

the IA and Copy of OR issued for the refund of unexpended/unutilized balance of

fund transferred to the Accounting Unit in pursuant to item 3.1.3 of COA Circular

2012-001 dated June 14, 2012 and items Nos. 4.6 and 5.4 of COA Circular No.

94-013 dated December 13, 1994, respectively.

Further, issue demand letters to the IAs and require them to submit Reports of

Expenditures relative to the disbursements of funds duly verified by the Auditor

and to strengthens the monitoring and control collaborating closely with the IA to

effectively enforce the liquidation of outstanding balances for the proper

administration of the program or projects funds

For DSWD-ARMM, require the managing director of the Habitat for Humanity

Foundation Incorporated to liquidate the fund transferred and/or return the

undisbursed fund to the DSWD-ARMM, in accordance with the COA Circular No.

94-013 dated December 13, 1994, COA Circular No.2012 dated June 14, 2012 and

the MOA.

4.3 Fund transfers from DA-OSEC, Central Office, Quezon City, totaling

P278,516,311.21 remained unliquidated as of December 31, 2014 in the books of

DA-OSEC- Central Office.

We recommend to DAF-ARMM that, since the funds is part of the Disbursement

Acceleration Program (DAP) which was declared unconstitutional by the Supreme

Court, to comply to COA Memorandum No. 2015-005 dated March 30, 2015 for

the immediate liquidation of the fund transfers totaling P273,646,377.17 (per DA-

OSEC, records, as of December 31, 2014) and immediately refund/return the

unutilized and/or unobligated balance out of the fund transfers to Bureau of

Treasury.

4.4 The Fund transfers by ORG-ARMM to LGUs and DPWH-ARMM for the

construction Women Peace Centers funded out of the OPAPP, Disbursement

Acceleration Program (DAP) totaling P14,021,838.66 remained unliquidated as

of December 31, 2015.

Since the project fund is part of the DAP which was declared unconstitutional by the Supreme Court, we recommended to require the Provincial Government of

Lanao del Sur and DPWH-ARMM to comply to COA Memorandum No. 2015-

005 dated March 30, 2015 for the immediate liquidation of the fund transfers and

v

for the ORG-ARMM to immediately refund/return the unutilized and/or

unobligated balance out of the fund transfers to Bureau of Treasury.

4.5 The unutilized/unobligated balances of DAP fund and other funds of DSWD-

ARMM and BFAR-ARMM totaling to P781,403.82 and P2,362,088.50,

respectively, remained un-remitted to the Bureau of Treasury as of December

31, 2015 contrary to COA Memorandum No. 2015-005 dated March 30, 2015.

We recommended that BFAR-ARMM and DSWD-ARMM immediately refund/return the unutilized and/or unobligated balance out of the fund transfers to

Bureau of Treasury.

4.6 Amount utilized totaling P48,121,063.54 for Gender and Development (GAD)

program by at least 14 RGAs is less than the prescribed 5% of their 2015

budget to implement GAD plans contrary to Section 34 (2) of the General

Provisions of the 2015 General Appropriations Act and paragraph 6.1 of PCW-

NEDA-DBM Joint Circular No. 2012-01 thus, depriving the intended

beneficiaries of the benefits due to them.

We recommend to formulate GAD plan designed to address gender issues within their concerned sectors or mandate and allocate at least five percent (5%) of their

budget pursuant to Section 34 of the General provision of 2015 GAA and

Paragraph (6.1) of PCW-NEDA-DBM Joint Circular No. 2012-01 and ensure that

the utilization of GAD Budget are in accordance with the GAD Plans and

evaluated based on the GAD performance indicators identified by said agencies.

4.7 Cash Advances totaling P32,113,102.20 remained unliquidated as of December

31, 2015 in violation to Section 89 of PD No. 1445 and Item 5.8 of COA

Circular No. 97-002.

Require all concerned accountable officers to immediately settle their accounts and

strictly comply with the provisions of Section 89 of P.D. No. 1445 and Item 5.8 of

COA Circular No. 97-002;

Exhaust all possible means to locate the whereabouts of officials and employees who are no longer connected with the Auditee and require them to immediately

liquidate and/or refund their unliquidated cash advances.

Require the liquidation of outstanding cash advances by retired/separated employees prior to and as a condition to the payment of any claim or issuance of

the clearance.

Desist from paying honoraria and allowances of detailed government officials out

of your cash advances. Authorized honoraria and allowances shall be remitted to

their mother agency to make the payments.

vi

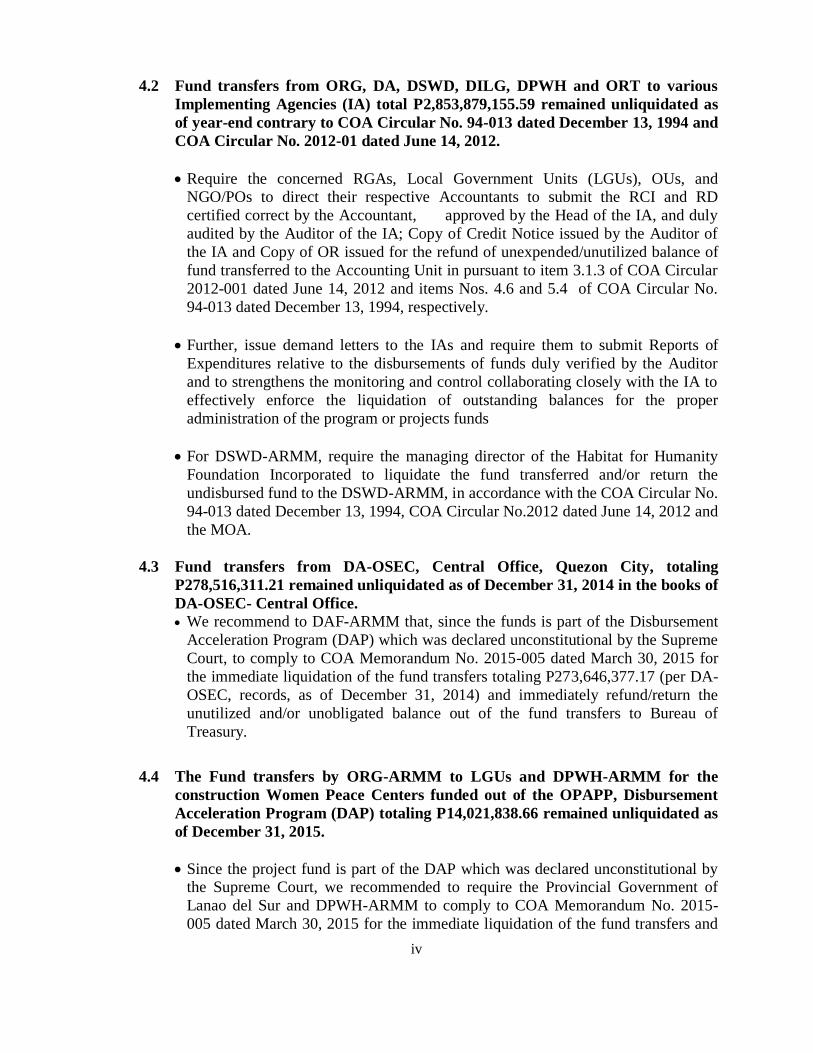

Require the Accountant of DAF-ARMM to make the necessary adjustments to correct the balance of the account – Advances to Special Disbursing Officers in the

financial statement.

4.8 The accuracy of the reported balance of Cash in Bank – Local Currency,

Current Account, totaling P210,980,979.34 as of December 31, 2015 cannot be

ascertained due to the absence/delayed submission of Bank Reconciliation

Statement (BRS), in violation to Section 74 of P.D. 1445, COA Circular 96-011

dated October 2, 1996,COA Circular No. 92-125 A dated March 4, 1992.and

DOF-DBM Joint Circular No. 1-90.

We recommend that the management should require the accountant to prepare and

submit the monthly bank reconciliation statement to the office of the auditor to

ensure the correctness of the cash in bank, LLCA account balance of the agency in

compliance with Section 74 of P.D 1445, COA Circular 96-011 dated October 2,

1996, COA Circular No. 92-125 A dated March 4, 1992 and DOF/DBM Joint

Circular No. 1-90.

4.9 The DOLE-ARMM declared an accounts payable totaling P607,582.21 which

represents obligated allotment not yet covered by notice of cash allocation for

payment of various creditors of DOLE-ARMM, but the unpaid disbursement

vouchers (DVs) in support of such claims were not yet submitted to our office

for verification, in violation to Sections 4 and 59 of P.D.1445 and pertinent

provisions of PPSAS 29.

We recommended that management instruct the accountant to submit to the

Auditor the unpaid DVs and the corresponding supporting documents in support of

the Accounts Payable totaling P607,582.21, the earliest time possible for our

verification, pursuant to Sections 4 and 59 of P.D. 1445 and PPSAS 29.

4.10 The BFAR-ARMM failed to recognize procured PPE totaling P2,072,099.00 in

violation of Section 63 of PD 1445.

The concerned staff should take up in the books all property and equipment acquired/received by the agency immediately upon receipt and issues the

corresponding Acknowledgment Receipt of Equipment (ARE) to the responsible

receiving officer or employee. Prompt entries should be made to recognize the

acquisition cost or appraised value of PPE, and their accumulated depreciations.

Committee on PPE Count should be created to conduct the physical count of PPE,

reclassification of serviceable and unserviceable items. The result hereof will be

the basis of the accountant in recording PPE in the books.

4.11 DPWH-1ST

and 2nd

Maguindanao Engineering Districts Supply Officers and

Accountants’ cash basis and outright expense method of recording for

procurement of construction supplies and materials acquired for distribution

totaling P751,258,726.03 were directly recorded to the Construction-in-Progress

vii

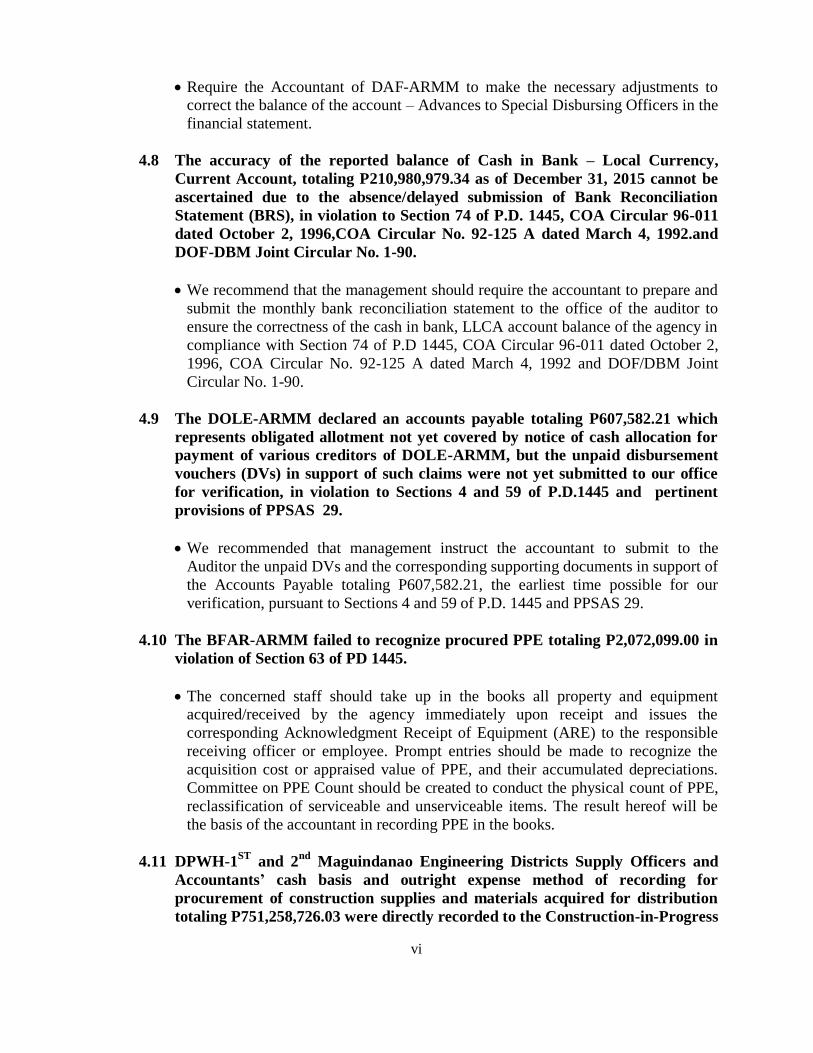

(CIP)-Infrastructure Assets account instead of Construction Materials

Inventory account as stated in COA Circular 2015-007 thereby resulting to

overstatement of PPE account and understatement of inventory and liability

accounts.

Instruct the Accountant to Book ensuing purchases of construction materials to the Construction Materials Inventory account, maintain Stock Ledger Card (SLC);

Reclassify any unissued inventories to its respective accounts; and

Require the concerned Supply Officer to submit the monthly RSMIs to the Accountant for recording and to maintain and update the Stock Cards (SC) for

each item in stock.

4.12 DPWH-Maguindanao Area Equipment Services’ (AES) Supply Officer and

Accountant’s cash basis and outright expense method of recording for

procurement of spare parts to be utilized in the repairs and maintenance of

various service vehicles and heavy equipments amounting to P2,718,297.33 is

not in line with the provisions of COA Circular 2015-007 thereby understating

the asset and the liability account.

We recommend for the Area Equipment Engineer to instruct the Accountant and the Supply Officer: a) to use the accrual basis of accounting for the purchase,

receipt, and payment of spare parts inventory, b) to post adjusting entries to

recognize the inventory and liability account upon purchase and the recognition of

expense account or PPE account for minor and major repair, respectively. c) to

implement the inventory accounting system for spare parts on hand, including the

use of SLC and SC the Accounting Unit and Supplies Office, respectively.

4.13 DPWH-ARMM failed to record the cost of completed

rehabilitation/improvement of the old office building and other ground

development in the DPWH-ARMM totaling P4,279,438.92.

Request the DPWH-MED to transfer the cost of the project to DPWH-ARMM for proper recording in the books. Prepare the necessary JEV to record the asset

account.

4.14 The DPWH-ARMM failed to provide for the CY 2015 depreciation on the land

improvements implemented by DPWH-MED within the DPWH-ARMM

compound costing P777,560.00 thereby, overstating its assets and understating

the expenses.

Compute for the depreciation of the land improvement effective from the time the

project was completed and prepare the necessary JEV to record the same.

4.15 The DPWH-ARMM remitted twice the 1% Contractor’s Tax totaling

P596,621.79, while a total of P10,291,240.89 of the 1% Contractor’s Tax

viii

withheld remained unremitted as of December 31, 2015 contrary to Section 100

of Muslim Mindanao Autonomy Act (MMA) No. 049.

For the withholding taxes, which were remitted twice, inquire with the Office of the Regional Treasurer (ORT)-ARMM if these could still be refunded or if the

agency could have it offset against future remittances of contractor’s tax.

Henceforth, care should be taken in remitting taxes so as to avoid the same

situation.

As for the unremitted taxes, have these remitted the soonest and to strictly comply

with the due date on the remittance of the Contractor’s Tax as per Section 100 of

MMA Act No. 049.

4.16 DPWH-ARMM failed to remit to the BIR as of December 31, 2015, either

through Tax Remittance Advice (TRA) or check payments, withholding taxes

totaling P76,316,875.48 contrary to existing BIR regulations on remittance of

withholding tax.

Remit these taxes the soonest possible time and henceforth, to strictly comply with the due date on the remittance of these taxes as per BIR regulations.

4.17 DEPED-ARMM has 14 bank accounts with total balance of P4,842,688.63,

which remained dormant for over five years, were not yet closed and remitted

to the Bureau of Treasury (BTr), thus, contrary to EO No. 338 and Section 4. 2

and 4.6 of Joint Circular No. 9-81 dated October 19, 1981.

We recommended that the Regional Secretary direct the Cashier to immediately communicate to the concerned bank to close the dormant bank accounts and the

Accountant to conduct a thorough examination thereof and prepare the necessary

adjustments, if warranted to come up with the correct cash account balances.

4.18 DTI, CHED, DOT, DA, and TESDA, all of ARMM, have dormant accounts and

still remain in the Books Contrary to COA Circular No. 97-001.

We recommended that the Accountant shall settle these accounts in accordance with COA Circular No. 97-001 dated February 5, 1997.

Further, the accountant and other concerned personnel should initiate the

verification of the origin, nature or purpose of all accounts that remain non-moving

for over five years and exert effort to gather the necessary documents to support

the account balance and be guided with the provisions of EO No. 109 and Joint

DBM-COA Circular No. 99-6 dated November 13, 1999 and Section IIIA.10 of

COA Circular 97-001 dated February 5, 1997.

Accounts which become dormant for over five years shall be reviewed, analyzed and reconciled together with the other related accounts in the trial balance and

ix

determine which accounts are fully depreciated and reclassify them into other

assets if the same are functional, or dispose them if otherwise, and make the

necessary adjusting entries to that effect.

Require the Accountant to locate the vouchers/schedules and that would support the recorded balances on dormant accounts. If in case, it cannot be found despite

all efforts, a request shall be brought to COA for proper disposition. If an authority

is obtained from COA for the write off of the dormant accounts, it shall be

effected by a debit to the account “Impairment Loss- Other Receivables and shall

be close to Income and Expense Summary Account and/ or debit memo to the

account “Loss of Accounts” and the accounts to be written off shall then be

transferred to the Registry of Accounts Written off. (RAWO).

4.19 The accuracy and reliability of the Inventory accounts of DepEd, DOTC,

DILG, DPWH-Maguindanao Area Equipment Services (AES), and DOH, all of

ARMM, with total balance of P 23,728,380.50 as of December 31, 2015 were

doubtful due to failure of management to conduct physical count of inventories

at year end pursuant to Section 65 of MNGAS, Volume II. Hence, the reliability

of reported balances at year end of inventory accounts are doubtful

The Supply Officer to conduct physical count of all items of inventories every six months in order to determine the actual existence and condition of supplies on

stock as required under Section 62 of MNGAS, Vol. II.

the Accountant to ensure that inventories are properly classified and recorded in

the books of accounts as well as all the RSMI submitted by the Property Office;

the Property Officer to prepare the RSMI in accordance with the provisions of Section 62 of the MNGAS, Volume II; and

the Accounting Office and the Property Office to maintain the Supplies Ledger Cards and Stock Cards, respectively, and to reconcile periodically their records in

accordance with Section 43 of MNGAS, Volume I.

Prepare and submit RPCI in accordance with the format prescribed in Appendix 62

of MNGAS Vol. II, copy furnished the Auditor;

For the Area Equipment Engineer to see to it that the internal control policies defined by the government shall be strictly adhered to. He shall direct the Chief,

Finance and Management Services Division to see to it that a) the necessary

subsidiary ledgers to support the general ledger accounts are maintained and kept

up to date; b) Maintain close coordination with the Accounting and Property Unit

in reconciling the PPE account

4.20 The accuracy and existence of the Other Assets account of RTWPB-ARMM,

included in the Non-Current Assets of the agency and valued in the Statement

of Financial Position as at December 31, 2015 at P533,168.00 cannot be

ascertained, because of the non-preparation and submission of the Year End

physical count Report by management, contrary to Section 4.3 of COA

Circular No. 97-005 dated July 10, 1997. Further, the agency should have

x

determined at the end of the year whether the Other Assets were subject for

impairment, as provided under PPSAS 21.

Instruct the Acting Supply Officer to conduct a Year End Inventory of PPE and to include the Other Assets account totaling to P533,168.00, pursuant to the provision

of Section 4.3 of COA Circular No. 97-005 dated July 10, 1997.

A periodic reconciliation of the PPELC maintained by the accountant with that of

the Property Cards maintained by the Supply Officer should be regularly made to

promptly detect any discrepancies and appropriate adjustments in both records

should be out rightly recorded and reflected in the book of accounts.

Assess at each reporting date whether there is any indication that the Other Assets may be impaired. If any such indication exists, the entity shall estimate the

recoverable service amount of the asset, as provided under PPSAS 21.

4.21 The validity and accuracy of the Property, Plant and Equipment (PPE)

accounts of ORVG, CDA, OSCC, DAR, DAR-MAG and DOLE, all of the

ARMM, with total book value of P 3,201,365.89 (net of depreciation) cannot

be ascertained, due to the non-submission of Physical Count Report for PPE

accounts as of December 31, 2015 in violation to existing rules and regulations.

Further, the Notes to Financial Statements does not disclose the estimated

useful life of the assets for the accurate computation of the annual depreciation,

in violation to Section 4.3 of COA Circular No. 97-005 dated July 10, 1997 and

pertinent provisions of PPSAS 17.

We recommend that Report on the Physical Count of Property, Plant and equipment (RPCPPE) be submitted to the Auditor as prescribed. Should there be

no physical count conducted, then require the creation of an Inventory Committee

to conduct physical count of PPE and to submit the RPCPPE. Further, the

Accounting Unit should maintain and make a timely update of the Property, Plant

and Equipment Ledger Card (PPELC).

A periodic reconciliation of the PPELC maintained by the accountant with that of the Property Cards maintained by the Supply Officer should be regularly made to

promptly detect any discrepancies and appropriate adjustments in both records

should be out rightly recorded and reflected in the book of accounts.

4.22 The DAR-ARMM has an outstanding obligations to the GSIS, PAG-IBIG and

PHILHEALTH totaling to P473,217.18 which remained unsettled as at

December 31, 2015, in violation to Section 6 (a) of PD 1146.

We recommend that the Cashier and Accountant remit the mandatory obligations

withheld due to the GSIS, Pag-ibig and Philhealth amounting to P466,047.38,

P6,632,.93, and P536.87, respectively, or for a total of P473,217.18.

xi

4.23 An estimated P11,236,284.00 Personal Services expenses of DEPED-ARMM

was overstated due to the misstatement of salary steps of teachers.

We recommend the following to the Regional Secretary:

Create a committee to conduct investigation and immediately impose the appropriate penalties to those committed this particular violation of existing laws;

Create a committee to work on the reconciliation of the PSIIPOP and payroll to

come with the correct salary steps of DepEd-ARMM official and employees;

Establish office guidelines on the updating and changing of salary steps to avoid misstatements thereof;

After establishing the correct salary steps, impose a refund to the employees with overpayment.

After thorough investigation, instruct the Regional Accountant to prepare and book the necessary adjustments in the books of the agency correct the deficiencies

discovered.

4.24 TESDA, CHED, DPWH-Lanao del Sur Engineering District II, ORVG and

CDA, all of the ARMM, failed to submit Mandatory Reports in violation of

Sections 38, 40 (b), 40 (d) of GAM, Section 122, 100 and 107 of PD 1445, Section

98 of GAAM, Volume 1, Sections 22 & 57 of the Manual on National

Government Accounting System (MNGAS) and Section 69, PD 1445.

The management should create a working committee to act on the physical count

of PPE once every year, as well as on the disposal of unserviceable PPE.

Determine which PPE are fully depreciated and unserviceable and drop them from

the books pursuant to Sec. 79, PD 1445.

The accountant and other concerned officer/s should prepare and submit journals on or before 5

th day of the following month. Familiarize themselves with the

Philippine Public Sector Accounting Standards (PPSAS), including the different

journals, forms and reports under the GAM.

Further, we recommend that Report of Accountability for Accountable Forms (RAAF) be submitted on monthly basis by concerned Accountable Officer

pursuant to Section 98 of GAAM, Volume 1 and require the Cashier to submit

promptly the RCD as well as the receipts and supporting documents to the

Auditor, in accordance with the above cited rules and regulations.

4.25 TESDA, DPWH-RO, DA, OSCC, DOT, ORVG, DSWD, RPDO, CHED, DAR

and DILG, all of ARMM were delayed in the submission of Disbursement

Vouchers with supporting documents and other reports Contrary to Sec. 39,

100 and 122 PD 1445, Section 7.2.1.(a) of COA Circular No. 2009 dated Sept.

xii

15, 2009 and 122 of PD 1445, thereby resulting to the delay in the verification

and audit of the transactions.

Submit the paid DVs together with their supporting documents without waiting for others to submit their liquidation papers, especially if it warrants a cause of delay;

Promptly notify those officers or employees concerned for the immediate process

and submission of their liquidation papers; and/

Augment support staff, if necessary, to assist in the facilitation of the liquidation papers

Adopt a system to be able to comply with the prompt submission of the DVs. The Audit Team does not expect to receive the DVs on or before the 5

th day of the

following month, but a month or two is enough for the agency to comply with the

submission.

Prepare daily the Report of Checks Issued (RCI) and furnished the Accounting Section, especially if numerous checks were issued in a day.

Both the Cash Section and the Accounting Section must have a close coordination

and find ways to comply with the prompt submission of the transactions.

Prepare JEVs and attach to each DV for easier verification.

The accountants, cashiers and other concerned responsible officials submit the required reports and liquidations of fund transfers and comply strictly with the

provisions of Section 100 and 122 of PD 1445 to enable the auditor to conduct

timely audit and ensure validity and accuracy of recorded transactions.

4.26 BFAR-ARMM failed to submit on time copies of MOA for the receipt of funds

from BFAR-CO and/ ORG-ARMM, contrary to Sec. 39 (1) of P.D. 1445

The personnel concerned should submit without delay to the Auditor all

documents necessary for the conduct of audit in order to have comprehensive

review and analysis of accounts and to determine the reliability of the

management’s assertion on the existence and/occurrence, validity, accuracy and

completeness of the recorded transactions.

4.27 DPWH-ARMM fund transfers to LGUs and NGAs, and payments to various

suppliers and contractors totaling P356,895,154.02 were supported with Official

Receipts (OR) that are either undated, incorrect, double, while others were not

supported by OR at all contrary to COA Circular 2012-001.

For the ORs without date, verify with the payees on when these were actually received and have these properly filled up.

xiii

For those without OR, require from them the submission of the corresponding OR.

For those with the wrong amount in the OR, verify with the payees the actual

amount received by them, and make the appropriate action based on the

verification made.

For those issued with two ORs, determine which are accurate, and also verify the reason for the issuance of another OR for the same transaction.

4.28 DTI, RBOI, BFAR, DOST, DTI, DPWH, CHED, DPWH-LDS-II and DPWH-

1ST

MED, all of ARMM, failed to furnish copies of perfected contracts/purchase

orders for procurement and their supporting documents within five (5) days

upon perfection thereof preventing the timely evaluation and review contrary

to COA Circular No. 96-010, COA Circular No. 2009-001 and Sec. 39 (1) of PD

1445.

We recommend that copy of contract, purchase order, notice of delivery, inspection and acceptance report and their supporting documents be submitted to

the audit team within the period prescribed, under COA Circular No. 2009-001

dated February 12, 2009 and the concerned officials must comply with the above-

mentioned Circular.

The BAC and the accounting personnel should design an effective internal control

to secure all the contracts and purchase orders with supporting documents and

make them readily available for submission to the office of the auditor for his

review within the prescribed period.

The concerned personnel should see to it that all funds received be supported with legal documents authorizing the disbursement of said funds; immediately furnish

the auditor’s office copy of MOA/NCA/NFT, and comply with the terms and

conditions set forth in said documents.

4.29 For CY 2015 the total Notices of Suspensions (NS) amounted to P

1,086,211,177.13 and disallowances of P 666,107,898.53 which are still

outstanding and unsettled even at the end of the year, contrary to Sec. 7.1.1,

COA Circular No. 2009-006 dated September 15, 2009, Rules and Regulations

on the Settlement of Accounts (RRSA) thus, may end up with court suit or a

waste of government monies.

We recommend that concerned employees be directed immediately to settle in full, their audit suspensions and disallowances in accordance with Sections 5.4 and

7.1.1 of the Rules and Regulations on the Settlement of Accounts (RRSA).

Henceforth, ensure that government auditing rules and regulations are strictly

xiv

complied with before processing claims/effecting payments to minimize

suspensions and disallowances in audit.

We recommended that the management direct the head of accounting division to enforce immediate settlement of the audit suspensions totaling P 39,163,728.73

within the reglementary period to avoid maturing into disallowance, pursuant

to Section 7.1.1 and 9.3 of COA Circular No. 2009-006 dated September

15, 2009.

4.30 DPWH-Maguindanao 1st and 2

nd EDs failed to provide the Audit Team with the

list of all on-going government projects/programs/activities (PPA) contrary to

COA Circular No. 2013-004 dated January 13, 2013.

We recommend that at the beginning of the year management shall provide the

audit team with the list of all on-going government PPA pursuant to COA Circular

No. 2013-004.

VALUE FOR MONEY

4.31 The DepEd-ARMM failed to achieve the targeted completion of the 1,032

classroom buildings due to the delay and failure of the Contractors to execute

properly the terms and condition of the contracts, thus the intended purpose of

increasing delivery of good quality education was not achieved.

We recommend that the Management shall formulate and adopt effective

guidelines for the review, monitoring, inspection and reporting of program

implementation of the school buildings and other infrastructure projects in order to

prevent delays and non-implementation of projects, hence the needs the objective

of serving the needs of the increasing student population in the Agency’s area of

jurisdiction were be responded. If warranted, mandated liquidated damages maybe

charged against defaulting contractors.

4.32 Out of the P186,121,960.00 received by BFAR-ARMM from BFAR-CO in

CY2015 for fishery and aquatic projects, only P80,589,985.97 was disbursed

and liquidated, leaving a total unutilized amount of P105,531,975.16. Also, out

of the P40,850,000.00 received from ORG-ARMM for ARMM HELPS projects,

only P10,288,477.00 was utilized, while the remaining P30,561,523.00 was

reverted to the Bureau of Treasury due to lack of adequate time since funds

were received only last week of December 2015. Hence, the intended

beneficiaries were deprived of the benefits.

The Agency should be diligent to make sure that all projects allotted with funds are fully implemented within the timeframe prescribed by law. Exert effective

coordination with the source agency for the immediate release of the approved

budgets in order to avoid delayed implementation of projects.

xv

4.33 Farm Equipment found in DAF-ARMM compound costing P12,326,236.00

remain undistributed as of the year-end, thus defeated the purpose of acquiring

the equipment for the immediate needs of the farmers of ARMM.

We recommend that the management should store these units intended for rescue operation under a roofed building so as not to expose the said items to wear and

tear. We recommend further, that the coordinator of any agri-pinoy program

should identify first the relevance of farm machineries before including the said

items in their proposals to avoid wastage of government funds. Distribute to the

intended beneficiaries the foregoing machineries the soonest possible time to

maximize the objectives of the program.

5. Statement on the quantity/number of recommendations implemented, partially

implemented and not implemented in the current year for the unimplemented prior

years audit recommendations.

The status of implementation of prior year’s audit recommendations is summarized below

and shown in detail in Part III of this report.

Status of Implementation No. of

Recommendations

Percentage as to

total

Fully Implemented 50 36%

Partially implemented 74 53%

On-going 3 2%

Not Implemented 12 9%

Total 139 100%

We enjoin the Management to ensure full implementation of all partially and not

implemented prior year’s audit recommendations to improve operational as well as

financial efficiency of the agency.

![Food security and nutrition: building a global narrative ... · EXECUTIVE SUMMARY EXECUTIVE SUMMARY EXECUTIVE SUMMARY EXECUTIVE SUMMAR Y [ 2 ] This document contains the Summary and](https://img.pdfslide.net/doc/110x75/5ff5433612d22125fb06e6b5/food-security-and-nutrition-building-a-global-narrative-executive-summary-executive.jpg)