Embed Size (px)

Citation preview

brownstoneresearch.com

1E X P O N E N T I A L T E C H I N V E S T O R

HOW TO 5X YOUR MONEY IN THE BOOMING CLOUD INDUSTRY

brownstoneresearch.com

2

On September 27, 2016, I sent out an urgent alert to my Exponential Tech subscribers…

I recommended purchasing shares in a lit-tle-known enterprise software company focused on hybrid cloud computing technology.

It was a Tuesday. And the initial public offering (IPO) was scheduled for that Friday, September 30, 2016.

There wasn’t much time. But it was a great in-vestment opportunity. I remember practically pulling an all-nighter to get the research and analysis done in order to feel confident in the recommendation.

At the time, the company was tiny with only $846 million in annual revenue in its current fis-cal year and an enterprise value (EV) of just $2.2 billion at the time of the IPO. That was an EV/sales ratio of just 2.6 for a super high-growth, high-margin software company. Crazy.

I knew the company well. And I saw that the un-derwriters – the investment banks – of the IPO were underpricing the deal. Their mistake was our opportunity.

At the time, I wrote:

I believe that with [this company’s] lead-ing-edge technology, combined with the fact that it will be valued more like a soft-ware company, we have the opportunity for a massive gain.

We were able to build a position at $16 a share, and 11 days later, we closed out the position at $32.01 for a 100.1% gain. While Exponential Tech Investor is not a trading service, we certainly won’t complain about those kinds of quick gains.

One reader, Peggy G., wrote to me and said:

Hello Jeff Brown. Thank you for the ur-gent IPO alert – I made a bundle on it!

I was thrilled to hear that my readers were able to make a great return in only a few days.

2016 feels like a long time ago. I almost feel nos-talgic for those days. The markets have changed dramatically since then, especially for technology IPOs. The chance for normal investors to gain ac-cess to shares in high-quality technology IPOs at or around the IPO offer price is pretty much gone.

But that doesn’t mean that there isn’t an appetite for quality research in this space. Here’s reader Peggy G. again…

Has [your publisher] ever considered offering an advisory service in IPOs? Es-pecially the kind you can buy at IPO or at least on the first day of open market, and sell quickly thereafter for a nice profit on the trade? If you ever decide to offer such a service, I would love to be in on the beta testing!

Sadly, for Peggy and all retail investors, it is nearly impossible to get into a great IPO at a reasonable

How to 5X Your Money in the Booming Cloud IndustryBy Jeff Brown, Editor, Exponential Tech Investor

brownstoneresearch.com

3

valuation. That is why I steer my subscribers away from overvalued IPOs. Investing in them is a sure-fire way to lose a lot of hard-earned money.

As a perfect example, Snowflake (SNOW), an-other cloud software company, went public in September of 2020. It was the largest software IPO in history. Snowflake’s shares were priced at $120, putting the IPO valuation at an incredible $33 billion.

But that’s not the end of the story.

Snowflake’s share price opened at $245 a share, a bit more than double the $120 offer price. Sadly, normal investors had no chance to invest anywhere between $120 and $245. There liter-ally was no window to get in. Only institutions and very high-net-worth individuals were able to get allocations of shares in this exciting new cloud company.

On the first day of trading, the stock closed at $254 a share, resulting in a $71.4 billion valua-tion. That’s incredible. But here’s where it gets even nuttier.

Snowflake’s fiscal year sales forecast back then was about $403 million. That’s less than half the fiscal year revenue of the company I recommend-ed in Exponential Tech Investor back in 2016.

Now Snowflake trades at an EV/sales ratio of 88. That’s a value equivalent to 88 years of revenue (not profit). Insane.

This is precisely why we aren’t going to invest in Snowflake in this report.

But we are going to take advantage of a mispric-ing in the market… a flashback to 2016.

In this report, we’re going to take a position in Nutanix (NTNX) and make even more money

than we did the first time around… I also believe that an acquisition is likely, which would be an added kicker to our returns. I’ll explain more about that a bit later.

A Flashback to 2016

My name is Jeff Brown. You’ve picked a great time to join us. If this is your first time reading my research, then allow me to introduce myself.

For nearly 30 years, I’ve worked at the executive level for some of the world’s most dominant tech-nology firms like Qualcomm, NXP Semiconduc-tors, and Juniper Networks. I’m also an active an-gel investor in early stage technology companies.

I’ve invested in dozens of private deals over the years with incredible success. In short, working with, studying, and investing in bleeding-edge technology has been my life’s work. And these days, I use my technology and investing expertise to share the best technology investments with readers like you.

In Exponential Tech Investor, we invest in small- and sometimes micro-capitalization technology companies on the verge of exponen-tial growth. As I said, we’ll be revisiting an old friend in this report.

The last time we invested in Nutanix, we made 100.1% returns in a matter of days. This time, we won’t settle for “just” doubling our money. I believe we stand to make 5X on this investment the second time around.

But first, let’s spend just a little time on Nutanix, its technology, and where it fits into the informa-tion technology (IT) and cloud services industries.

As a reminder, cloud-based services simply mean that an organization’s data is housed off-site at a data center somewhere. Software programs are

brownstoneresearch.com

4

run remotely. Users can simply log on to those software applications through their web browser and use the software hosted in the cloud.

If we’ve ever used Google’s intuitive Google Docs… shopped on Amazon… streamed a movie from Netflix… or uploaded and stored files on Dropbox, then we’ve already used and benefited from cloud technology.

Nutanix was born in late 2009 after the financial crisis. It was an interesting period in the technol-ogy industry. Cloud-based services were in a na-scent stage, and much of the industry was heavily driven by Amazon’s Web Services division. After all, Amazon Web Services had only launched a modern version of its cloud-based storage and computing service in 2006.

Nutanix understood early the importance of cloud-based services and the value the technolo-gy would bring to corporations and governments around the world.

Nutanix knew that there wasn’t a one-size-fits-all approach to building out an IT infrastructure. Every organization would have different needs, which would require different architectures. And Nutanix also knew that it would be a multivendor environment for cloud services.

In other words, Amazon Web Services would be the powerhouse, but there would also be several other strong players.

The company’s product strategy anticipated an environment where organizations would manage their data storage and computing resources in some form of hybrid architecture.

As a simple example, a company might choose to have 20% of its software running on-site for mission-critical applications that it needs to con-trol, 50% running on Amazon Web Services, and

the remaining 30% running on Google’s Cloud Platform.

And Nutanix became a pioneer in a technology that would facilitate this type of network archi-tecture design.

Hyper-Converged Infrastructure

Nutanix specialized in something called hy-per-converged infrastructure (HCI). It is an exciting space but a bit of a dry topic. So here is a simple explanation of the technology…

The key is to use a “hypervisor,” a piece of soft-ware that can run on pretty much any kind of server. The hypervisor may be installed on thousands of servers. And it is the underlying technology that allows a corporation to design its data storage and computing architecture… no matter where it is physically located in the world. Whatever the software architecture is, it runs on top of and across all the hypervisor software installed on servers around the world.

The ability to employ this kind of hybrid net-work at multiple locations is important because an organization’s IT requirements become more complex every year with even higher demands for improved performance.

A simple example is the number of software ap-plications an average business uses. In 2015, that number was “just” 31. In 2020, the average was 127, which represents more than a 4X increase in just five years.

And for multinational corporations, the com-plexities become even more difficult to manage. In many countries, due to data privacy laws or compliance issues, data can only be stored and used in-country. This requires specially designed IT infrastructure for support.

brownstoneresearch.com

5

This is what Nutanix does. It simpli-fies all of these complexities and helps organizations greatly reduce overall IT operational costs, on average, by 62% over a five-year period.

Its scope includes the hypervisor soft-ware, management software, compliance and security software, data storage soft-ware, backup and data recovery soft-ware, database management, software orchestration tools, and even software that enables organizations to create virtual desktops to support remote work, which has become particularly relevant this year during the pandemic.

Given the breadth of its product offerings, Nu-tanix is competing in one of the largest market opportunities in the world. The broad cloud ser-vice and technology industry is worth more than $250 billion this year alone.

A Competitive Picture

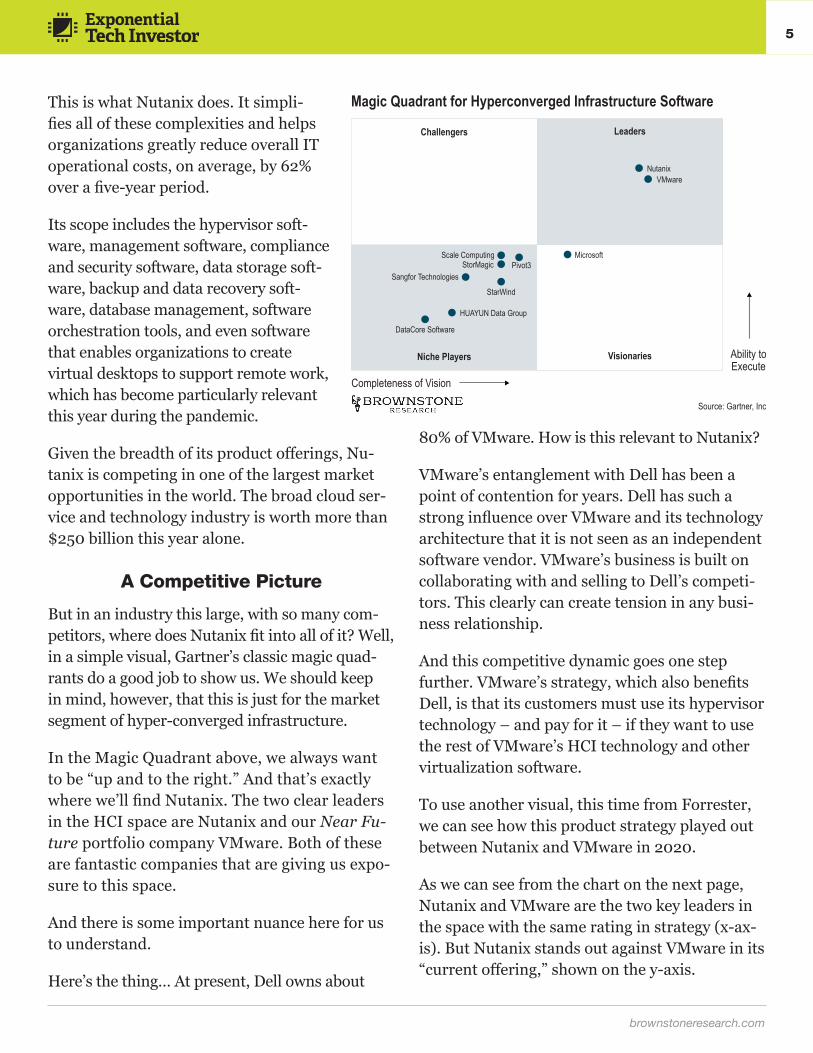

But in an industry this large, with so many com-petitors, where does Nutanix fit into all of it? Well, in a simple visual, Gartner’s classic magic quad-rants do a good job to show us. We should keep in mind, however, that this is just for the market segment of hyper-converged infrastructure.

In the Magic Quadrant above, we always want to be “up and to the right.” And that’s exactly where we’ll find Nutanix. The two clear leaders in the HCI space are Nutanix and our Near Fu-ture portfolio company VMware. Both of these are fantastic companies that are giving us expo-sure to this space.

And there is some important nuance here for us to understand.

Here’s the thing… At present, Dell owns about

80% of VMware. How is this relevant to Nutanix?

VMware’s entanglement with Dell has been a point of contention for years. Dell has such a strong influence over VMware and its technology architecture that it is not seen as an independent software vendor. VMware’s business is built on collaborating with and selling to Dell’s competi-tors. This clearly can create tension in any busi-ness relationship.

And this competitive dynamic goes one step further. VMware’s strategy, which also benefits Dell, is that its customers must use its hypervisor technology – and pay for it – if they want to use the rest of VMware’s HCI technology and other virtualization software.

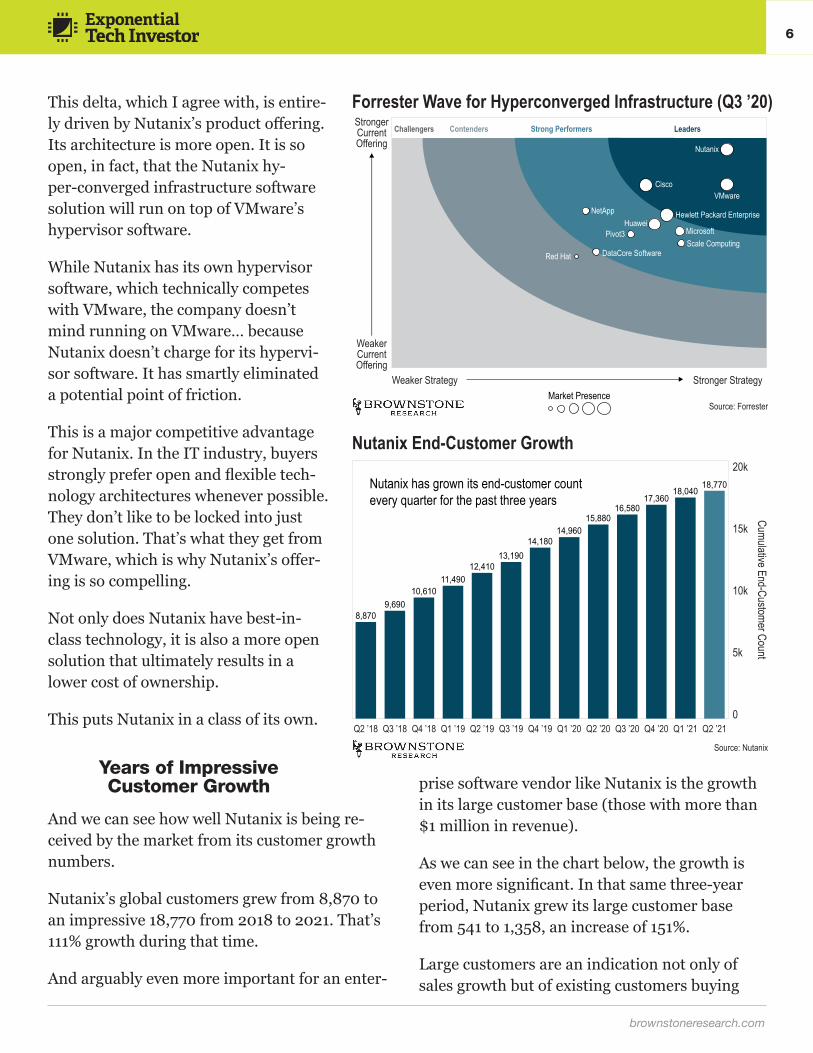

To use another visual, this time from Forrester, we can see how this product strategy played out between Nutanix and VMware in 2020.

As we can see from the chart on the next page, Nutanix and VMware are the two key leaders in the space with the same rating in strategy (x-ax-is). But Nutanix stands out against VMware in its “current offering,” shown on the y-axis.

Magic Quadrant for Hyperconverged Infrastructure Software

Source: Gartner, Inc

Ability to Execute

Completeness of Vision

LeadersChallengers

VisionariesNiche Players

DataCore Software

StarWind

Pivot3StorMagicScale Computing

Sangfor Technologies

HUAYUN Data Group

Microsoft

VMwareNutanix

brownstoneresearch.com

6

This delta, which I agree with, is entire-ly driven by Nutanix’s product offering. Its architecture is more open. It is so open, in fact, that the Nutanix hy-per-converged infrastructure software solution will run on top of VMware’s hypervisor software.

While Nutanix has its own hypervisor software, which technically competes with VMware, the company doesn’t mind running on VMware… because Nutanix doesn’t charge for its hypervi-sor software. It has smartly eliminated a potential point of friction.

This is a major competitive advantage for Nutanix. In the IT industry, buyers strongly prefer open and flexible tech-nology architectures whenever possible. They don’t like to be locked into just one solution. That’s what they get from VMware, which is why Nutanix’s offer-ing is so compelling.

Not only does Nutanix have best-in-class technology, it is also a more open solution that ultimately results in a lower cost of ownership.

This puts Nutanix in a class of its own.

Years of Impressive Customer Growth

And we can see how well Nutanix is being re-ceived by the market from its customer growth numbers.

Nutanix’s global customers grew from 8,870 to an impressive 18,770 from 2018 to 2021. That’s 111% growth during that time.

And arguably even more important for an enter-

prise software vendor like Nutanix is the growth in its large customer base (those with more than $1 million in revenue).

As we can see in the chart below, the growth is even more significant. In that same three-year period, Nutanix grew its large customer base from 541 to 1,358, an increase of 151%.

Large customers are an indication not only of sales growth but of existing customers buying

Forrester Wave for Hyperconverged Infrastructure (Q3 ’20)

Source: Forrester

Weaker Current Offering

Stronger Current Offering

Red Hat

Pivot3Huawei

NetApp

CiscoVMware

Nutanix

DataCore SoftwareScale ComputingMicrosoft

Hewlett Packard Enterprise

Challengers Contenders Strong Performers Leaders

Weaker Strategy Stronger StrategyMarket Presence

Nutanix End-Customer Growth

Cumulative End-Customer Count

0

5k

10k

15k

20kNutanix has grown its end-customer count every quarter for the past three years

Source: Nutanix

Q2 ’18

8,870

Q3 ’18

9,690

Q4 ’18

10,610

Q1 ’19

11,490

Q2 ’19

12,410

Q3 ’19

13,190

Q4 ’19

14,180

Q1 ’20

14,960

Q2 ’20

15,880

Q3 ’20

16,580

Q4 ’20

17,360

Q1 ’21

18,040

Q2 ’21

18,770

brownstoneresearch.com

7

more of Nutanix’s products. If that is happening, we know that Nutanix has a great product market fit and happy cus-tomers, and it is delivering technology on which its customers become reliant.

The Nuance in Nutanix

Things get a lot more interesting when we take a look at revenue and cash flow numbers. Context is so important in an investment thesis. Understanding the key drivers behind the numbers is criti-cal in the case of Nutanix.

They don’t look perfect, but there is a perfectly good reason for the short-term slowdown in growth and the negative free cash flow. In the case of Nutanix, the nuance is very important in this story.

As I mentioned earlier, Nutanix oper-ates in the enterprise software space, which requires a lot of in-person pre-sales efforts, especially for larger deals. Needless to say, this kind of sale was tough to do amid the global pandemic and travel restrictions of the last year.

In the fiscal year revenue chart to the right, we can see the impact on the numbers. Nutanix’s fiscal year ends on July 31 each year. We can see that its fiscal year 2020 showed moderate growth around 5.6% compared to the prior fiscal year. That isn’t surprising considering the impact of the pandemic from March through July of 2020 (five months).

The current forecast for fiscal year 2021 is also conservative. But I do believe that we’ll see a sur-prise to the upside this fiscal year based on my outlook for economic recovery for 2021.

And there was another dynamic at play that con-tributed to the slowdown in revenue growth in fiscal years 2019, 2020, and 2021…

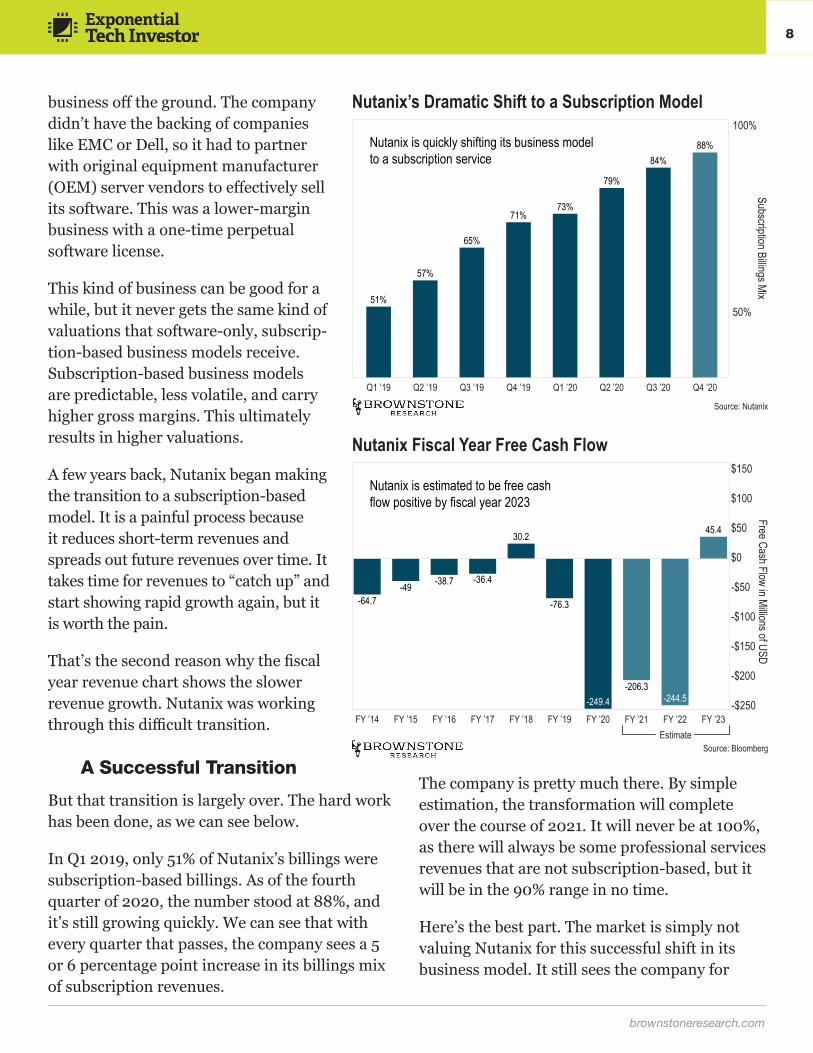

Nutanix has been going through a major busi-ness transformation away from hardware and perpetual software licenses to a subscrip-tion-based software model.

In the early years, Nutanix had to pursue a more hardware-centric product strategy to get its

Nutanix Large Customer Growth

Cumulative Large Customer Count

0

500

1k

1.5kNutanix has grown its number of large customers (more than $1 million) every quarter for three years

Source: Nutanix

Q2 ’18

541

Q3 ’18

593

Q4 ’18

645

Q1 ’19

714

Q2 ’19

779

Q3 ’19

848

Q4 ’19

921

Q1 ’20

990

Q2 ’20

1,060

Q3 ’20

1,122

Q4 ’20

1,207

Q1 ’21

1,276

Q2 ’21

1,358

Nutanix Fiscal Year Revenue

Fiscal Year Revenue in Millions of USD$100

$0

$500

$1k

$1.5k

$2.5k

$2k

Nutanix is projected to continue to grow its yearly revenue through FY 2023

Source: Bloomberg

127.1241.4

503.4

845.91155.5

1235.11305 1310.8

1499.6

1823.8

FY ’14 FY ’15 FY ’16 FY ’17 FY ’18 FY ’19 FY ’20 FY ’21 FY ’22 FY ’23Estimate

brownstoneresearch.com

8

business off the ground. The company didn’t have the backing of companies like EMC or Dell, so it had to partner with original equipment manufacturer (OEM) server vendors to effectively sell its software. This was a lower-margin business with a one-time perpetual software license.

This kind of business can be good for a while, but it never gets the same kind of valuations that software-only, subscrip-tion-based business models receive. Subscription-based business models are predictable, less volatile, and carry higher gross margins. This ultimately results in higher valuations.

A few years back, Nutanix began making the transition to a subscription-based model. It is a painful process because it reduces short-term revenues and spreads out future revenues over time. It takes time for revenues to “catch up” and start showing rapid growth again, but it is worth the pain.

That’s the second reason why the fiscal year revenue chart shows the slower revenue growth. Nutanix was working through this difficult transition.

A Successful Transition

But that transition is largely over. The hard work has been done, as we can see below.

In Q1 2019, only 51% of Nutanix’s billings were subscription-based billings. As of the fourth quarter of 2020, the number stood at 88%, and it’s still growing quickly. We can see that with every quarter that passes, the company sees a 5 or 6 percentage point increase in its billings mix of subscription revenues.

The company is pretty much there. By simple estimation, the transformation will complete over the course of 2021. It will never be at 100%, as there will always be some professional services revenues that are not subscription-based, but it will be in the 90% range in no time.

Here’s the best part. The market is simply not valuing Nutanix for this successful shift in its business model. It still sees the company for

Nutanix’s Dramatic Shift to a Subscription Model

Subscription Billings Mix

50%

100%Nutanix is quickly shifting its business model to a subscription service

Source: Nutanix

51%

Q1 ’19

57%

Q2 ’19

65%

Q3 ’19

71%

Q4 ’19

73%

Q1 ’20

79%

Q2 ’20

84%

Q3 ’20

88%

Q4 ’20

Source: Bloomberg

Nutanix Fiscal Year Free Cash Flow

Free Cash Flow in Millions of USD

-$200

-$250

-$150

-$100

$0

-$50

$50

$100

$150Nutanix is estimated to be free cash flow positive by fiscal year 2023

-64.7 -76.3

-206.3-249.4 -244.5

-49 -38.7 -36.4

30.2 45.4

FY ’14 FY ’15 FY ’16 FY ’17 FY ’18 FY ’19 FY ’20 FY ’21 FY ’22 FY ’23Estimate

brownstoneresearch.com

9

what it used to be, not as it is today.

And there is something else that I’m even more excited about. It is related to how the company is spending its money. Please stick with me here. Just like with the revenue charts, it is not what it seems.

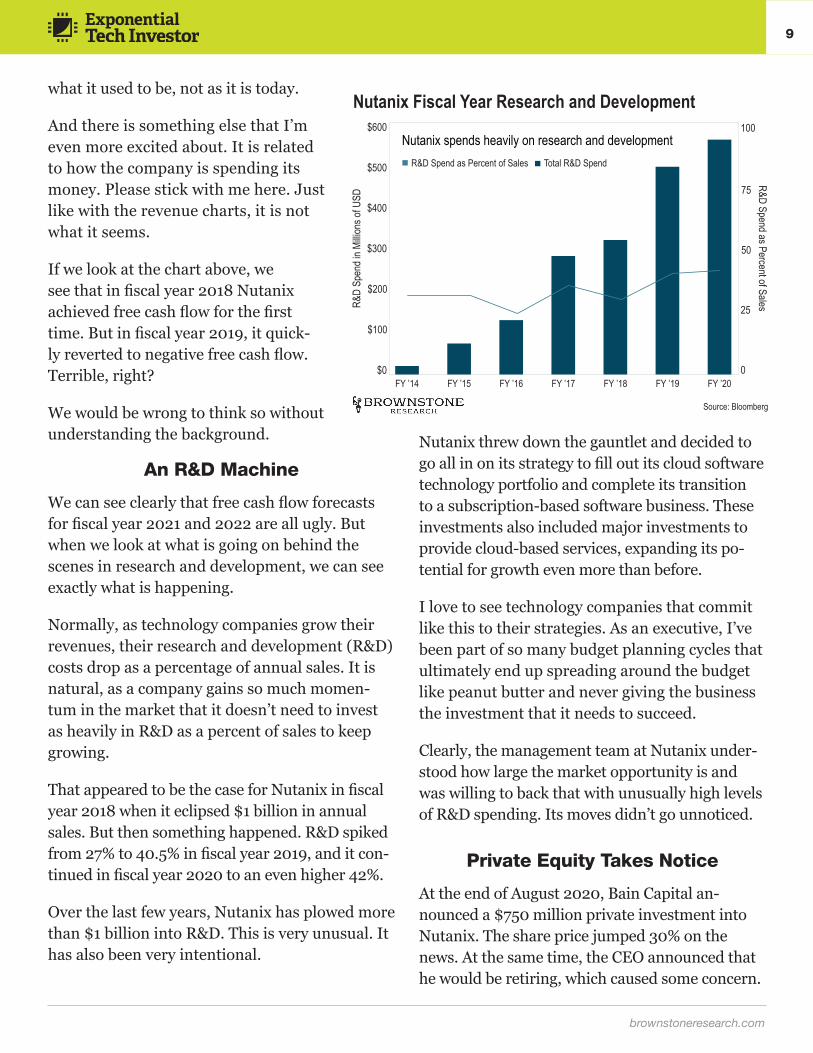

If we look at the chart above, we see that in fiscal year 2018 Nutanix achieved free cash flow for the first time. But in fiscal year 2019, it quick-ly reverted to negative free cash flow. Terrible, right?

We would be wrong to think so without understanding the background.

An R&D Machine

We can see clearly that free cash flow forecasts for fiscal year 2021 and 2022 are all ugly. But when we look at what is going on behind the scenes in research and development, we can see exactly what is happening.

Normally, as technology companies grow their revenues, their research and development (R&D) costs drop as a percentage of annual sales. It is natural, as a company gains so much momen-tum in the market that it doesn’t need to invest as heavily in R&D as a percent of sales to keep growing.

That appeared to be the case for Nutanix in fiscal year 2018 when it eclipsed $1 billion in annual sales. But then something happened. R&D spiked from 27% to 40.5% in fiscal year 2019, and it con-tinued in fiscal year 2020 to an even higher 42%.

Over the last few years, Nutanix has plowed more than $1 billion into R&D. This is very unusual. It has also been very intentional.

Nutanix threw down the gauntlet and decided to go all in on its strategy to fill out its cloud software technology portfolio and complete its transition to a subscription-based software business. These investments also included major investments to provide cloud-based services, expanding its po-tential for growth even more than before.

I love to see technology companies that commit like this to their strategies. As an executive, I’ve been part of so many budget planning cycles that ultimately end up spreading around the budget like peanut butter and never giving the business the investment that it needs to succeed.

Clearly, the management team at Nutanix under-stood how large the market opportunity is and was willing to back that with unusually high levels of R&D spending. Its moves didn’t go unnoticed.

Private Equity Takes Notice

At the end of August 2020, Bain Capital an-nounced a $750 million private investment into Nutanix. The share price jumped 30% on the news. At the same time, the CEO announced that he would be retiring, which caused some concern.

FY ’14 FY ’15 FY ’16 FY ’17 FY ’18 FY ’19 FY ’20

Nutanix Fiscal Year Research and Development

Nutanix spends heavily on research and development

Source: Bloomberg

R&D Spend as Percent of Sales Total R&D Spend

R&D Spend as Percent of Sales

0

25

50

75

100$600

$500

$0

$100

$200

$300

$400

R&D

Spen

d in M

illion

s of U

SD

brownstoneresearch.com

10

But this was a great move. The CEO had a great run. He has been effecting a major transition in the business that is largely done and announced a $750 million influx in cash last year.

This was much-needed cash to carry the com-pany to positive free cash flow and to fund more rapid growth. The company is still in this essen-tial phase of growth. New CEO Rajiv Ramaswa-mi can take the company from $1 billion to $5 billion in revenue or more.

But the other reason that private equity like Bain Capital jumped into Nutanix, and why the compa-ny hired a new CEO, is that the company is a key acquisition target. It is the stand-alone gem in the HCI segment… and it is the best in its business.

And the last four and a half years of heavy R&D spending are about to pay off in a major way. Nu-tanix has hit an incredible inflection point in its history. This stock is now one of the most incred-ible deals in the tech sector right now.

Nutanix is trading around $26 a share, just 62% above its IPO price back in 2016.

Far more important than the nominal share price, Nutanix is trading at an enterprise value to sales (EV/sales) ratio of 3.9. I find this absolutely crazy. VMware is trading at 5.5, and its valuation has always suffered due to its ownership by Dell.

Or compare this to Snowflake – the company I mentioned early on – which is trading at an EV/sales of 88. That’s right. On a valuation basis, Nutanix is nearly 23 times “cheaper” than the largest software IPO in history. And while Nuta-nix isn’t growing as quickly as SNOW, its reve-nues are more than two times that of SNOW. Its gross margins are about 23 points higher than SNOW’s 56%.

Nutanix has nearly 80% gross margins and will

return to high-revenue growth mode by next fiscal year. Right now, large-capitalization sub-scription-based software firms are trading at EV/sales ratios of more than 20, yet Nutanix is trading at 3.9. Talk about mispricing the value of a company…

In a technology market like we are seeing now, a company like Nutanix – which is a leader in one of the hottest technology sectors, cloud software solutions – should be trading at least at an EV/sales of 12 sometime over the next 24 months.

This year, the success of Nutanix’s business tran-sition to subscription-based billing will be clear, as will the value of its major R&D investments. The company will also be able to clearly demonstrate that it will return to generating free cash flow in fiscal year 2023, which begins on August 1, 2022.

Based on my assumptions and the expected reve-nues of $1.8 billion in fiscal year 2023, within the next two years, Nutanix has 5X return potential. This is exactly why we’re going to invest in Nuta-nix (to make a bunch of money) instead of in-vesting in Snowflake, where we’d be sure to lose most of what we put in.

This is what makes us different from 99% of re-tail investors. Most investors will chase overval-ued, overhyped stocks like Snowflake. And they will inevitably suffer losses.

But we know better. Valuation matters. Rather than chasing the next “hot” tech stock we see on CNBC, we’ll do the smart thing and invest in an exciting company like Nutanix trading at a bar-gain valuation.

And we have the added excitement of a poten-tial acquisition in that same time frame. In fact, I’ll be amazed if an acquisition doesn’t happen. There is too much value, potential growth, and

brownstoneresearch.com

11

To contact us, call toll free Domestic/International: 1-888-512-0726, Mon-Fri: 9am-5pm ET or email [email protected].

© 2021 Brownstone Research, 55 NE 5th Avenue, Delray Beach, FL 33483. All rights reserved. Any reproduction, copying, or redistribution, in whole or in part, is prohibited without written permission from the publisher.

Information contained herein is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your personal situation—we are not financial advisors nor do we give personalized advice. The opinions expressed herein are those of the publisher and are subject to change without notice. It may become outdated and there is no obligation to update any such information.

Recommendations in Brownstone Research publications should be made only after consulting with your advisor and only after reviewing the prospectus or financial statements of the company in question. You shouldn’t make any decision based solely on what you read here.

Brownstone Research writers and publications do not take compensation in any form for covering those securities or commodities.

Brownstone Research expressly forbids its writers from owning or having an interest in any security that they recommend to their readers. Furthermore, all other employees and agents of Brownstone Research and its affiliate companies must wait 24 hours before following an initial recommendation published on the Internet, or 72 hours after a printed publication is mailed.

future profits at Nutanix for this company to remain independent. It’s too good to pass up at these levels, which show that Nutanix is clearly mispriced in the market.

In a market that overprices a cloud software company like Snowflake at 88 times annual sales, we’re not going to go wrong buying into Nutanix at an EV/sales of 3.9.

Let’s make sure we don’t miss this opportunity.

Action to Take: Please refer to our model portfolio for the most current recommended buy-up-to price for Nutanix (NTNX). Be sure to use a limit order when placing trades. For the time being, we will hold NTNX with no stop loss. Always remember to use rational position sizing.

Risk Management: I recommend holding Nutanix without a stop loss for the time being. So let’s remember to keep our position sizing rational. Small-cap stocks can be volatile. And remember, I never recommend going “all in” on any one investment.

Regards,

Jeff Brown Editor, Exponential Tech Investor