Embed Size (px)

Citation preview

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 1/40

Infrastructural Support SystemInfrastructural Support System

& Regulatory Framework& Regulatory FrameworkPresented byPresented by

Ram PujariRam Pujari

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 2/40

Export Incentive ProgrammesExport Incentive Programmes

Concessive Export CreditConcessive Export Credit Speedy, need based finance for up to 3 years at a stretchSpeedy, need based finance for up to 3 years at a stretch

Pre and Post Shipment FinancePre and Post Shipment Finance

Concessive Interest rate regimeConcessive Interest rate regime

In Rupee or Foreign CurrencyIn Rupee or Foreign Currency

Tax breaksTax breaks

Exim Policy IncentivesExim Policy Incentives

Special Processing ZonesSpecial Processing Zones

Duty Draw-back schemesDuty Draw-back schemes

Special RebatesSpecial Rebates

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 3/40

Exim Policy InitiativesExim Policy Initiatives

Special Economic Zones (SEZs)Special Economic Zones (SEZs)

Offshore Banking Units (OBUs) shall be permitted inOffshore Banking Units (OBUs) shall be permitted inSEZs.SEZs.

Units in SEZ can hedge commodity price risks, providedUnits in SEZ can hedge commodity price risks, providedthey are undertaken on stand-alone basis. This willthey are undertaken on stand-alone basis. This will

impart security to the returns of the unit.impart security to the returns of the unit.

ECBs for a tenure of less than 3 years can be raisedECBs for a tenure of less than 3 years can be raised

these units. Access to working capital loan atthese units. Access to working capital loan atinternationally competitive rates facilitatedinternationally competitive rates facilitated

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 4/40

Exim…. Employment OrientedExim…. Employment Oriented

AgricultureAgriculture

Registration & packaging restrictions are removed on Butter, Wheat andRegistration & packaging restrictions are removed on Butter, Wheat andWheat products, Coarse Grains, Groundnut Oil and Cashew to Russia .Wheat products, Coarse Grains, Groundnut Oil and Cashew to Russia .

Quantitative and packaging restrictions on wheat and its products, Butter,Quantitative and packaging restrictions on wheat and its products, Butter,

Pulses, grain and flour of Barley, Maize, Bajra, Ragi and Jowar alreadyPulses, grain and flour of Barley, Maize, Bajra, Ragi and Jowar alreadybeen removed.been removed.

Restrictions on export of all cultivated (other than wild) varieties of seed,Restrictions on export of all cultivated (other than wild) varieties of seed,except Jute and Onion, removed.except Jute and Onion, removed.

To promote export of agro and agro based products, 20 Agri export zonesTo promote export of agro and agro based products, 20 Agri export zoneshave been notified.have been notified.

In order to promote diversification of agriculture, transport subsidy for exportIn order to promote diversification of agriculture, transport subsidy for exportof fruits, vegetables, floriculture, poultry and dairy products is given.of fruits, vegetables, floriculture, poultry and dairy products is given.

3% special DEPB rate for primary & processed foods exported in retail3% special DEPB rate for primary & processed foods exported in retailpackaging of 1 kg or less.packaging of 1 kg or less.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 5/40

Exim…. Cottage & HandicraftsExim…. Cottage & Handicrafts

Cottage Sector & HandicraftsCottage Sector & Handicrafts

Rs. 5 crore earmarked under Market Access Initiative (MAI) for Rs. 5 crore earmarked under Market Access Initiative (MAI) for promoting cottage sector exports coming under the KVIC.promoting cottage sector exports coming under the KVIC.

Handicrafts sector can also access funds from MAI scheme for Handicrafts sector can also access funds from MAI scheme for development of website for virtual exhibition of their product.development of website for virtual exhibition of their product.

Under EPCG, units need not maintain average level of exports,Under EPCG, units need not maintain average level of exports,while calculating the Export Obligation.while calculating the Export Obligation.

Entitled to Export House status on achieving lower average exportEntitled to Export House status on achieving lower average exportperformance of Rs.5 crore as against Rs. 15 crore for others; andperformance of Rs.5 crore as against Rs. 15 crore for others; and

Entitled to duty free imports of an enlarged list of items asEntitled to duty free imports of an enlarged list of items asembellishments upto 3% of FOB value of their exports.embellishments upto 3% of FOB value of their exports.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 6/40

Exim …. SSIExim …. SSI

In centres of economic and export excellence such as Tirupur for In centres of economic and export excellence such as Tirupur for hosiery, woollen blanket in Panipat, woollen knitwear in Ludhiana,hosiery, woollen blanket in Panipat, woollen knitwear in Ludhiana,the following are available to small scale sector:the following are available to small scale sector:

Common service providers in these areas shall be entitled for facility of Common service providers in these areas shall be entitled for facility of

EPCG scheme.EPCG scheme. The recognised associations of units in these areas will be able toThe recognised associations of units in these areas will be able to

access the funds under the Market Access Initiative scheme for access the funds under the Market Access Initiative scheme for creating focused technological services and marketing abroad.creating focused technological services and marketing abroad.

Such areas will receive priority for assistance for identified criticalSuch areas will receive priority for assistance for identified critical

infrastructure gaps from the scheme on Central Assistance to Statesinfrastructure gaps from the scheme on Central Assistance to States Entitlement for Export House status at Rs. 5 crore instead of Rs. 15Entitlement for Export House status at Rs. 5 crore instead of Rs. 15

crore for others.crore for others.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 7/40

Leather IndustryLeather Industry

Duty free imports of trimmings and embellishments uptoDuty free imports of trimmings and embellishments upto3% of the FOB value hitherto confined to leather 3% of the FOB value hitherto confined to leather garments extended to all leather products.garments extended to all leather products.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 8/40

Exim…. TextilesExim…. Textiles

Sample fabrics permitted duty free within the 3% limitSample fabrics permitted duty free within the 3% limitfor trimmings and embellishments.for trimmings and embellishments.

10% variation in GSM be allowed for fabrics under 10% variation in GSM be allowed for fabrics under Advance Licence.Advance Licence.

Additional items such as zip fasteners, inlay cards,Additional items such as zip fasteners, inlay cards,eyelets, rivets, eyes, toggles, velcro tape, cord and cordeyelets, rivets, eyes, toggles, velcro tape, cord and cordstopper included in input output norms.stopper included in input output norms.

Duty Entitlement Passbook (DEPB) rates for all kinds of Duty Entitlement Passbook (DEPB) rates for all kinds of

blended fabrics permitted. Such blended fabrics to haveblended fabrics permitted. Such blended fabrics to havethe lowest rate as applicable to different constituentthe lowest rate as applicable to different constituentfabrics.fabrics.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 9/40

Exim… Gems & JewelleryExim… Gems & Jewellery

Gem & JewelleryGem & Jewellery

Customs duty on import of rough diamonds is being reduced to 0%.Customs duty on import of rough diamonds is being reduced to 0%.Import of rough diamonds is already freely allowed. LicensingImport of rough diamonds is already freely allowed. Licensing

regime for rough diamond is being abolished. This should help theregime for rough diamond is being abolished. This should help the

country emerge as a major international centre for diamonds.country emerge as a major international centre for diamonds. Value addition norms for export of plain jewellery reduced fromValue addition norms for export of plain jewellery reduced from

10% to 7%. Export of all mechanised unstudded jewellery allowed10% to 7%. Export of all mechanised unstudded jewellery allowedat a value addition of 3 % only. Having already achieved leadershipat a value addition of 3 % only. Having already achieved leadershipposition in diamonds, now efforts will be made for achievingposition in diamonds, now efforts will be made for achieving

quantum jump on jewellery exports as well.quantum jump on jewellery exports as well. Personal carriage of jewellery allowed through Hyderabad andPersonal carriage of jewellery allowed through Hyderabad and

Jaipur airport as well.Jaipur airport as well.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 10/40

Exim… Technology OrientedExim… Technology Oriented

a) Electronic hardwarea) Electronic hardware

The Electronic Hardware Technology Park (EHTP)The Electronic Hardware Technology Park (EHTP)scheme is being modified to enable the sector to facescheme is being modified to enable the sector to facethe zero duty regime under ITA(Information Technologythe zero duty regime under ITA(Information Technology

Agreement)-1. The units shall be entitled to followingAgreement)-1. The units shall be entitled to followingfacility:facility:

Net Foreign Exchange as a Percentage of ExportsNet Foreign Exchange as a Percentage of Exports(NFEP) positive in 5 years.(NFEP) positive in 5 years.

No other export obligation for units in EHTP.No other export obligation for units in EHTP. Supplies of ITA I items having zero duty in the domesticSupplies of ITA I items having zero duty in the domestic

market to be eligible for counting of export obligation.market to be eligible for counting of export obligation.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 11/40

b) Chemicals and Pharmaceuticalsb) Chemicals and Pharmaceuticals

All pesticides formulations to have 65% of DEPB rate of All pesticides formulations to have 65% of DEPB rate of such pesticides.such pesticides.

Free export of samples without any limit.Free export of samples without any limit.

Reimbursement of 50% of registration fees for Reimbursement of 50% of registration fees for registration of drugs.registration of drugs.

c) Projectsc) Projects Free import of equipment and other goods used abroadFree import of equipment and other goods used abroad

for more than one year.for more than one year.

Exim… Technology OrientedExim… Technology Oriented

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 12/40

Exim… Growth OrientedExim… Growth Oriented

a) Strategic Package for Status Holdersa) Strategic Package for Status Holders

Status holders are eligible for the following new/ special facilities:Status holders are eligible for the following new/ special facilities:

Licence/Certificate/Permissions and Customs clearances for bothLicence/Certificate/Permissions and Customs clearances for bothimports and exports on self-declaration basis.imports and exports on self-declaration basis.

Fixation of Input-Output norms on priority;Fixation of Input-Output norms on priority; Priority Finance for medium and long term capital requirement asPriority Finance for medium and long term capital requirement as

per conditions notified by RBI;per conditions notified by RBI;

Exemption from compulsory negotiation of documents throughExemption from compulsory negotiation of documents throughbanks. The remittance, however, would continue to be receivedbanks. The remittance, however, would continue to be received

through banking channels;through banking channels; 100% retention of foreign exchange in Exchange Earners’ Foreign100% retention of foreign exchange in Exchange Earners’ Foreign

Currency (EEFC) account;Currency (EEFC) account;

Enhancement in repatriation period from 180 days to 360 days.Enhancement in repatriation period from 180 days to 360 days.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 13/40

Exim… Growth orientedExim… Growth oriented

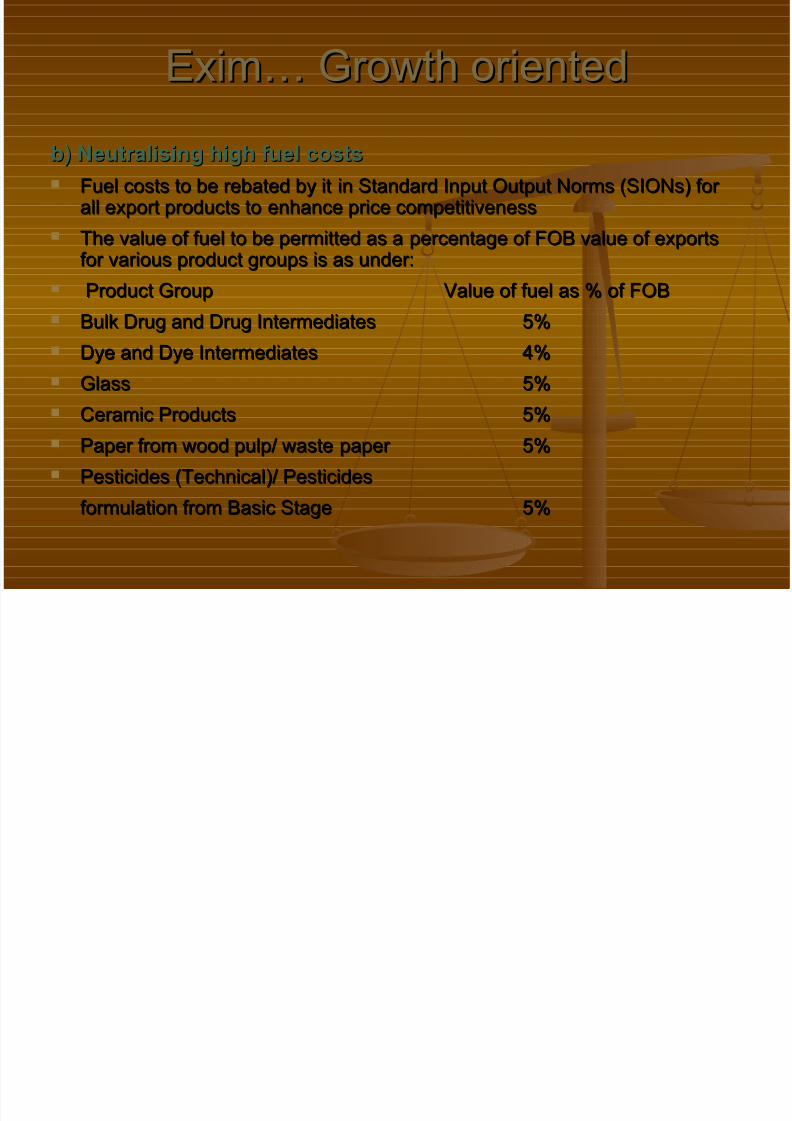

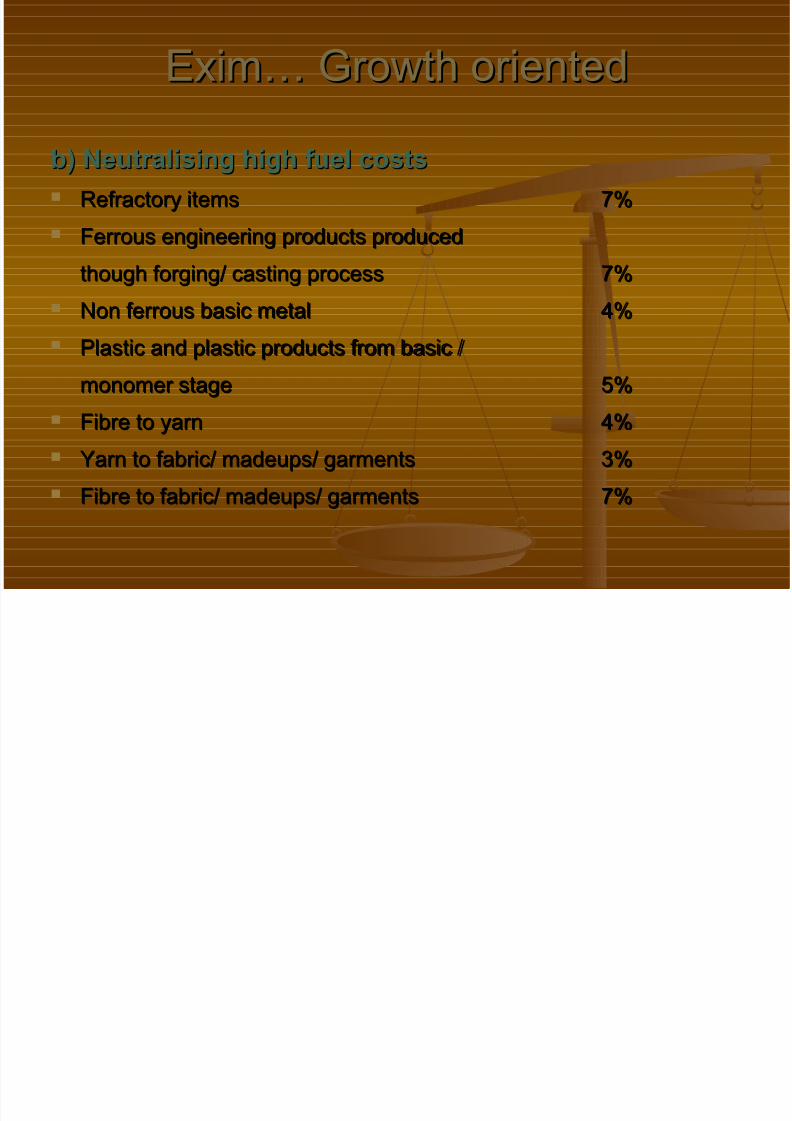

b) Neutralising high fuel costsb) Neutralising high fuel costs

Fuel costs to be rebated by it in Standard Input Output Norms (SIONs) for Fuel costs to be rebated by it in Standard Input Output Norms (SIONs) for all export products to enhance price competitivenessall export products to enhance price competitiveness

The value of fuel to be permitted as a percentage of FOB value of exportsThe value of fuel to be permitted as a percentage of FOB value of exportsfor various product groups is as under:for various product groups is as under:

Product GroupProduct Group Value of fuel as % of FOBValue of fuel as % of FOB

Bulk Drug and Drug IntermediatesBulk Drug and Drug Intermediates 5%5%

Dye and Dye IntermediatesDye and Dye Intermediates 4%4%

GlassGlass 5%5%

Ceramic ProductsCeramic Products 5%5% Paper from wood pulp/ waste paper Paper from wood pulp/ waste paper 5%5%

Pesticides (Technical)/ PesticidesPesticides (Technical)/ Pesticides

formulation from Basic Stageformulation from Basic Stage 5%5%

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 14/40

b) Neutralising high fuel costsb) Neutralising high fuel costs

Refractory itemsRefractory items 7%7%

Ferrous engineering products producedFerrous engineering products produced

though forging/ casting processthough forging/ casting process 7%7% Non ferrous basic metalNon ferrous basic metal 4%4%

Plastic and plastic products from basic /Plastic and plastic products from basic /

monomer stagemonomer stage 5%5%

Fibre to yarnFibre to yarn 4%4%

Yarn to fabric/ madeups/ garmentsYarn to fabric/ madeups/ garments 3%3%

Fibre to fabric/ madeups/ garmentsFibre to fabric/ madeups/ garments 7%7%

Exim… Growth orientedExim… Growth oriented

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 15/40

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 16/40

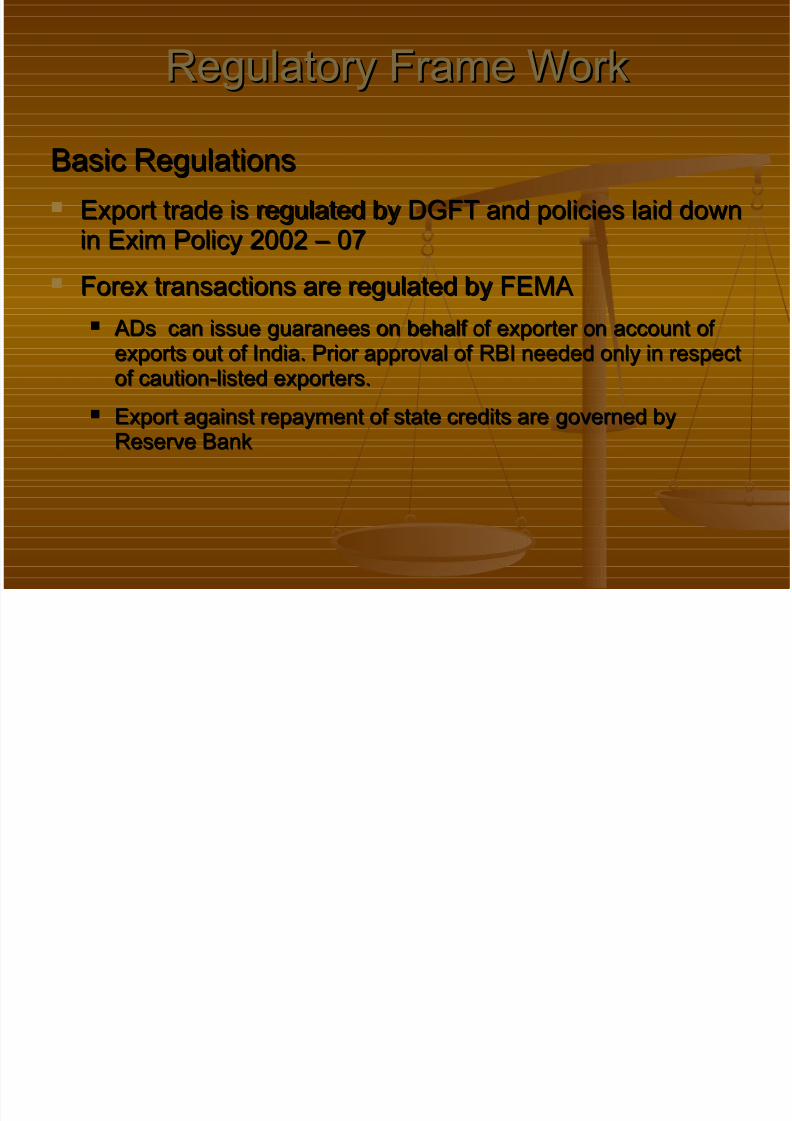

Regulatory Frame WorkRegulatory Frame Work

Basic RegulationsBasic Regulations

Export trade is regulated by DGFT and policies laid downExport trade is regulated by DGFT and policies laid downin Exim Policy 2002 – 07in Exim Policy 2002 – 07

Forex transactions are regulated by FEMAForex transactions are regulated by FEMA ADs can issue guaranees on behalf of exporter on account of ADs can issue guaranees on behalf of exporter on account of

exports out of India. Prior approval of RBI needed only in respectexports out of India. Prior approval of RBI needed only in respectof caution-listed exporters.of caution-listed exporters.

Export against repayment of state credits are governed byExport against repayment of state credits are governed byReserve BankReserve Bank

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 17/40

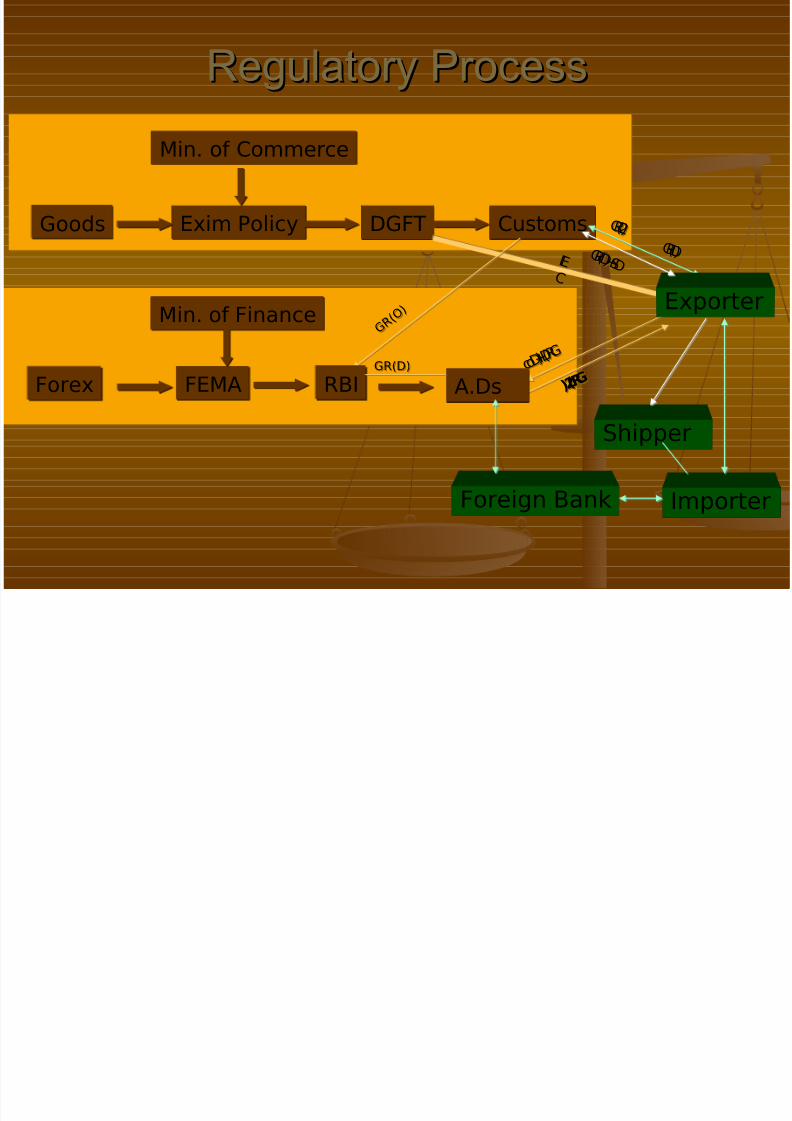

Regulatory ProcessRegulatory Process

ForexForex FEMAFEMA

Min. of FinanceMin. of Finance

GoodsGoods Exim PolicyExim Policy

Min. of CommerceMin. of Commerce

DGFTDGFT CustomsCustoms

I E

C

I E

C

G R ( 2 )G R ( 2 )

G R ( 2 ) G R ( 2 )

G R ( D ) G R ( D )

G R ( D ) + D o c G R ( D ) + D o c

G R ( O )

G R ( O )

RBIRBI A.DsA.Ds

Exporter

Importer

G R ( D ) + S D G R ( D ) + S D

Shipper

Foreign Bank

GR(D)GR(D)

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 18/40

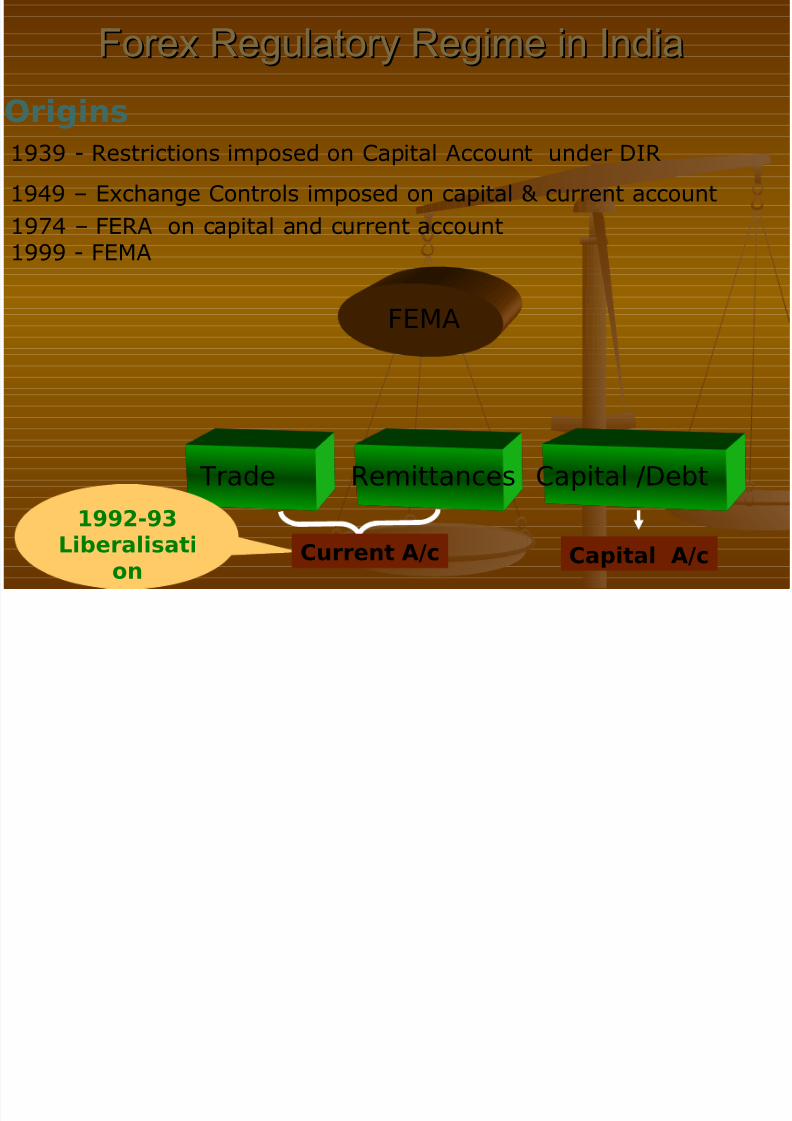

Forex Regulatory Regime in IndiaForex Regulatory Regime in India

Origins

1939 - Restrictions imposed on Capital Account under DIR

1949 – Exchange Controls imposed on capital & current account

1974 – FERA on capital and current account1999 - FEMA

FEMA

Trade Capital /DebtRemittances

1992-93

Liberalisation Current A/c Capital A/c

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 19/40

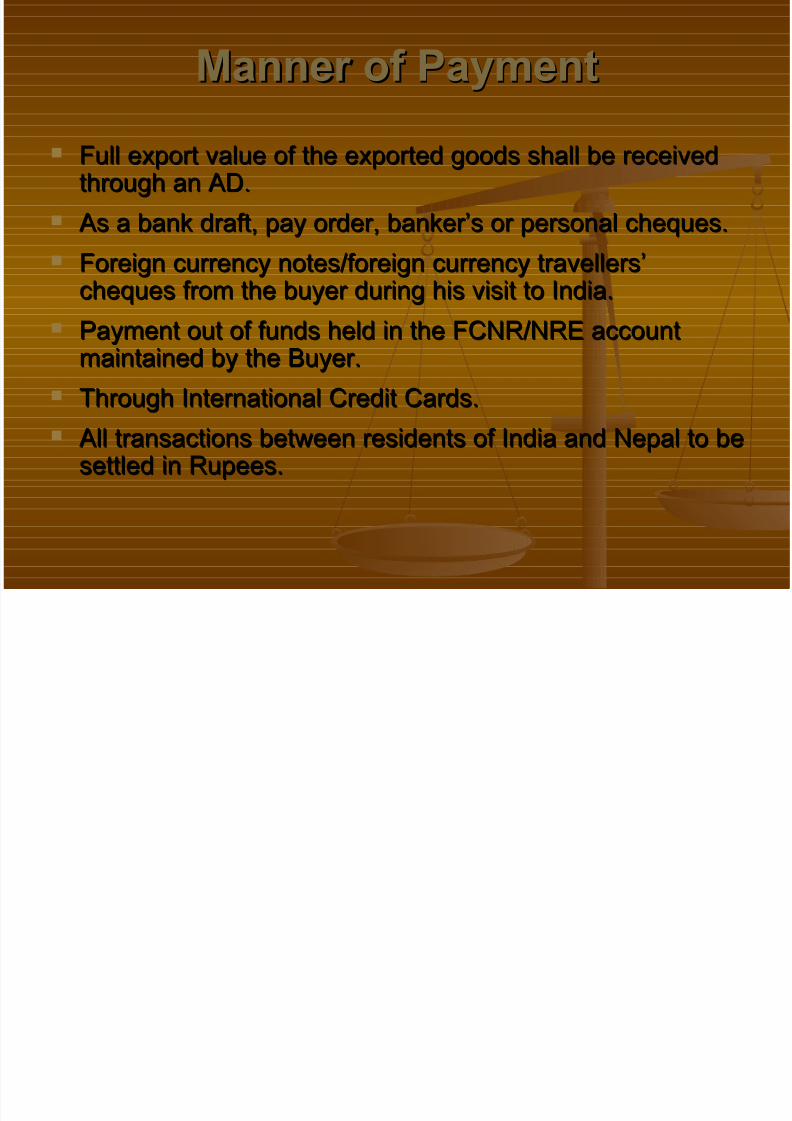

Manner of PaymentManner of Payment

Full export value of the exported goods shall be receivedFull export value of the exported goods shall be receivedthrough an AD.through an AD.

As a bank draft, pay order, banker’s or personal cheques.As a bank draft, pay order, banker’s or personal cheques.

Foreign currency notes/foreign currency travellers’Foreign currency notes/foreign currency travellers’cheques from the buyer during his visit to India.cheques from the buyer during his visit to India.

Payment out of funds held in the FCNR/NRE accountPayment out of funds held in the FCNR/NRE accountmaintained by the Buyer.maintained by the Buyer.

Through International Credit Cards.Through International Credit Cards.

All transactions between residents of India and Nepal to beAll transactions between residents of India and Nepal to besettled in Rupees.settled in Rupees.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 20/40

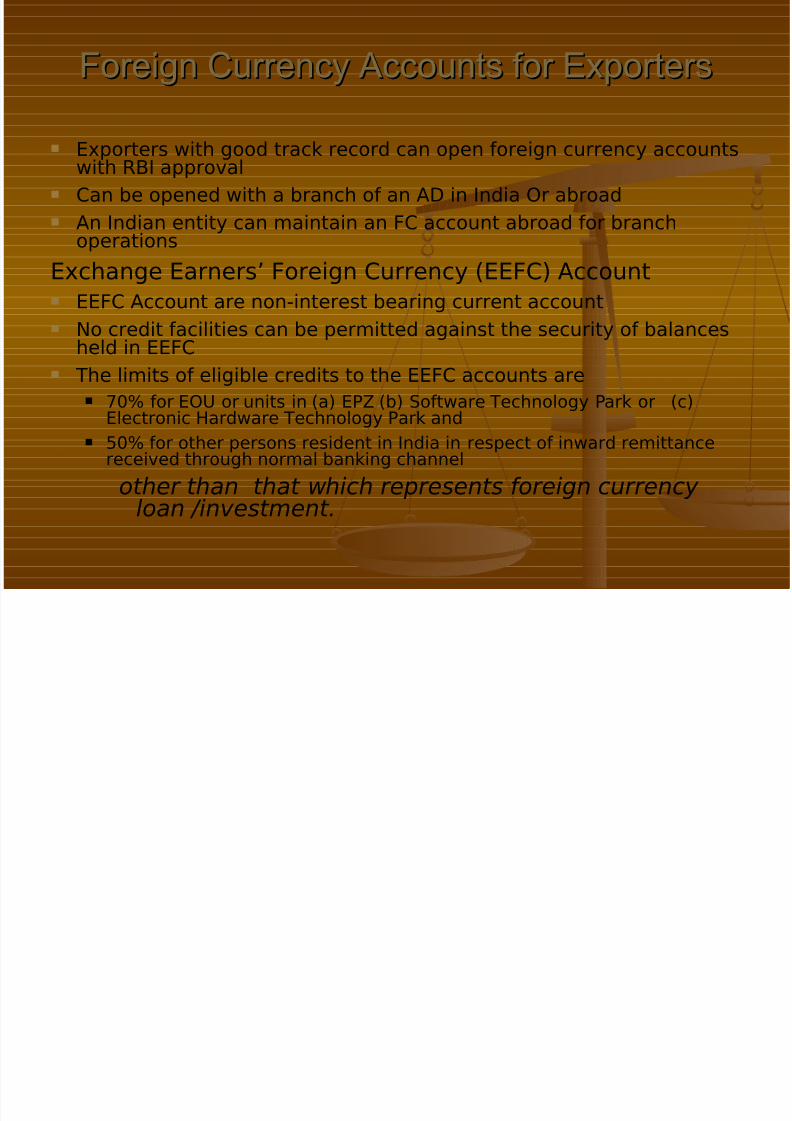

Foreign Currency Accounts for ExportersForeign Currency Accounts for Exporters

Exporters with good track record can open foreign currency accountswith RBI approval

Can be opened with a branch of an AD in India Or abroad

An Indian entity can maintain an FC account abroad for branchoperations

Exchange Earners’ Foreign Currency (EEFC) Account EEFC Account are non-interest bearing current account

No credit facilities can be permitted against the security of balancesheld in EEFC

The limits of eligible credits to the EEFC accounts are 70% for EOU or units in (a) EPZ (b) Software Technology Park or (c)

Electronic Hardware Technology Park and 50% for other persons resident in India in respect of inward remittance

received through normal banking channel

other than that which represents foreign currency loan /investment.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 21/40

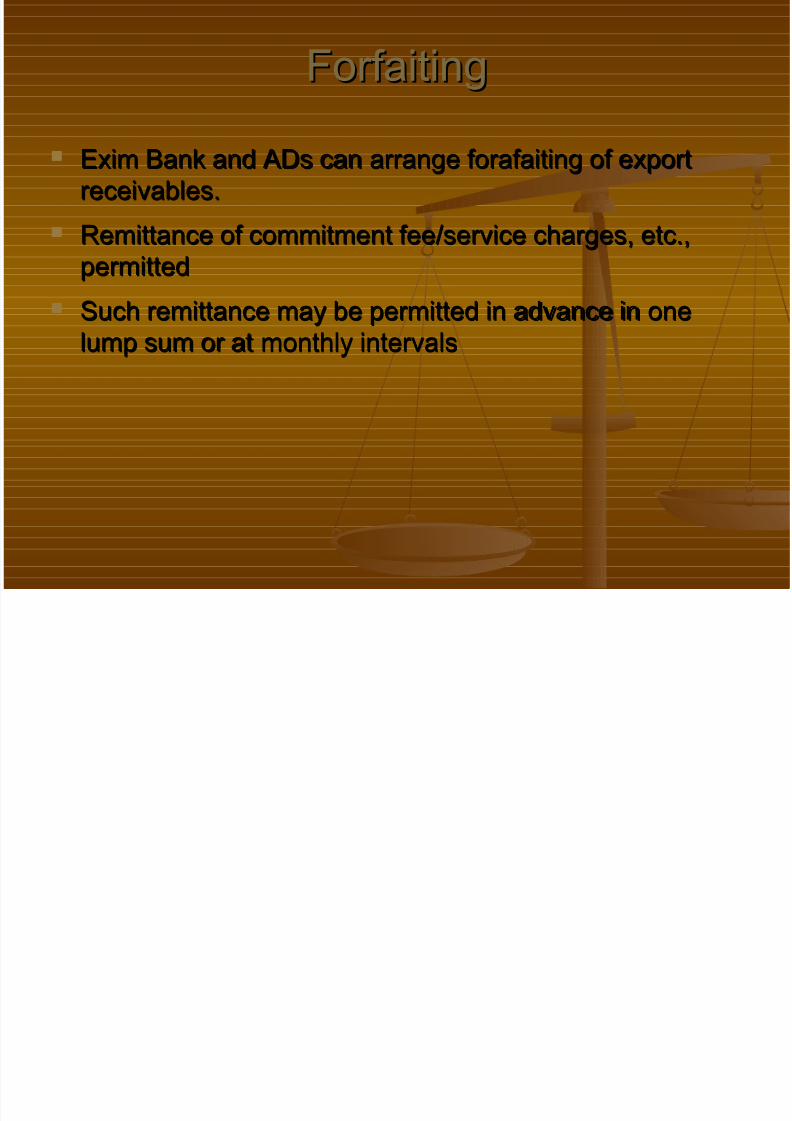

ForfaitingForfaiting

Exim Bank and ADs can arrange forafaiting of exportExim Bank and ADs can arrange forafaiting of exportreceivables.receivables.

Remittance of commitment fee/service charges, etc.,Remittance of commitment fee/service charges, etc.,

permittedpermitted Such remittance may be permitted in advance in oneSuch remittance may be permitted in advance in one

lump sum or at monthly intervalslump sum or at monthly intervals

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 22/40

Export Declarations – GRs, etcExport Declarations – GRs, etc Completed GR forms, in dupli-cate, should be submitted to the Customs at theCompleted GR forms, in dupli-cate, should be submitted to the Customs at the

port of shipment along with the shipping bill.port of shipment along with the shipping bill.

Customs will certify the value declared on both copies, record the assessed valueCustoms will certify the value declared on both copies, record the assessed valueand return the duplicate copy to the exporter and return the duplicate copy to the exporter

Duplicate GR +shipping documents should be resubmitted to CustomsDuplicate GR +shipping documents should be resubmitted to Customs

After examination, Customs will return it for submission to the authorised dealer for After examination, Customs will return it for submission to the authorised dealer for negotiation or collection of export bills.negotiation or collection of export bills.

Authorised dealer will report the export transaction to Reserve Bank and retainAuthorised dealer will report the export transaction to Reserve Bank and retainduplicate GR together with a copy of invoice till full export proceeds are receivedduplicate GR together with a copy of invoice till full export proceeds are received

After receipt of payment AD submits the duplicate GR to Reserve Bank.After receipt of payment AD submits the duplicate GR to Reserve Bank.

Where duplicate GR is misplaced or lost, another copy duly certified by CustomsWhere duplicate GR is misplaced or lost, another copy duly certified by Customsis acceptable.is acceptable.

Where Customs offices process shipping bills electronically, SDF forms should beWhere Customs offices process shipping bills electronically, SDF forms should be

submittedsubmitted In case of exports by barges/country craft/road trans-port, the form should beIn case of exports by barges/country craft/road trans-port, the form should be

presented at the Customs station at the border presented at the Customs station at the border

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 23/40

Check list for security formsCheck list for security forms Number on the duplicate copy of a GR is the same as the oneNumber on the duplicate copy of a GR is the same as the one

recorded on the Bill of Lading/Shipping Billrecorded on the Bill of Lading/Shipping Bill Bill of Lading issued on ‘freight prepaid’ basis is OK if it is a f.o.b.,Bill of Lading issued on ‘freight prepaid’ basis is OK if it is a f.o.b.,

f.a.s. etc. provided freight has been included in the invoice and the bill.f.a.s. etc. provided freight has been included in the invoice and the bill.

In the case of c.i.f., c.& f. etc. contracts whose freight is sought to beIn the case of c.i.f., c.& f. etc. contracts whose freight is sought to bepaid at destination, deduction can only be up to the extent of freightpaid at destination, deduction can only be up to the extent of freightdeclared on GR/SDF form or the actual amount of freight indicated ondeclared on GR/SDF form or the actual amount of freight indicated on

the Bill of Lading/Airway Bill, whichever is less.the Bill of Lading/Airway Bill, whichever is less. Likewise, where the marine insurance is taken by the exporters onLikewise, where the marine insurance is taken by the exporters on

buyer’s account, authorised dealer should verify that the actualbuyer’s account, authorised dealer should verify that the actualamount paid is received from the buyer through invoice and the bill.amount paid is received from the buyer through invoice and the bill.

The documents submitted do not reveal any materialThe documents submitted do not reveal any material inter seinter se

discrepancies in regard to description of goods export-ed, export valuediscrepancies in regard to description of goods export-ed, export valueor country of destination.or country of destination.

Export realizable value may be more than the declared to/acceptedExport realizable value may be more than the declared to/acceptedvalue by Customs where the contract provides for reimbursement of value by Customs where the contract provides for reimbursement of freight increase or devaluationfreight increase or devaluation

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 24/40

Drawing Bills under ExportDrawing Bills under Export

Trade DiscountTrade Discount

Accepted only if the discount has been declared on relative GR/SDFAccepted only if the discount has been declared on relative GR/SDFform at the time of shipment and accepted by Customs.form at the time of shipment and accepted by Customs.

Part DrawingsPart Drawings

In certain lines of export trade, it is the practice to leave a small part of In certain lines of export trade, it is the practice to leave a small part of

the invoice value undrawn for payment after adjustment due tothe invoice value undrawn for payment after adjustment due todifferences in weight, quality, etc. to be ascertained after arrival anddifferences in weight, quality, etc. to be ascertained after arrival andinspection, weighment or analysis of the goods.inspection, weighment or analysis of the goods.

the amount of undrawn balance is normal in line, subject to a maximumthe amount of undrawn balance is normal in line, subject to a maximumof 10 per cent of the full export value; andof 10 per cent of the full export value; and

an undertaking is obtained from exporter on the duplicate of an undertaking is obtained from exporter on the duplicate of

GR/SDF/PP forms that he will surrender/account for the balanceGR/SDF/PP forms that he will surrender/account for the balanceproceeds within the period prescribed for realisation.proceeds within the period prescribed for realisation.

If exporter is unable to repatriate undrawn balance in spite of bestIf exporter is unable to repatriate undrawn balance in spite of bestefforts, AD, on being satisfied with theefforts, AD, on being satisfied with the bona fidesbona fides of the case, mayof the case, maysubmit duplicate copies of GR/PP/SDF formssubmit duplicate copies of GR/PP/SDF forms

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 25/40

Consignment ExportsConsignment Exports

AD will instruct his overseas branch/correspondent to deliver AD will instruct his overseas branch/correspondent to deliver documents only against trust receipt/undertaking to deliver saledocuments only against trust receipt/undertaking to deliver saleproceeds by a specified dateproceeds by a specified date

The agents/consignees may deduct from sale proceeds of theThe agents/consignees may deduct from sale proceeds of the

goods expenses normally incurred towards receipt, storage and salegoods expenses normally incurred towards receipt, storage and saleof the goods, such as landing charges, warehouse rent, handlingof the goods, such as landing charges, warehouse rent, handlingcharges, etc. and remit the net proceeds to the exporter charges, etc. and remit the net proceeds to the exporter

The account sales received from the Agent/Consignee should beThe account sales received from the Agent/Consignee should beverified by the authorised dealer before it is sent to Reserve Bankverified by the authorised dealer before it is sent to Reserve Bank

along with the relative dupli-cate GR/SDF/PP forms.along with the relative dupli-cate GR/SDF/PP forms. Deductions in Account Sales should be supported by bills/receipts inDeductions in Account Sales should be supported by bills/receipts in

original except in case of petty items like postage/cable charges,original except in case of petty items like postage/cable charges,stamp duty etc.stamp duty etc.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 26/40

Despatch of Shipping DocumentsDespatch of Shipping Documents

Authorised dealers should normally despatch shipping documentsAuthorised dealers should normally despatch shipping documentsto their overseas branches/correspondents expeditiously.to their overseas branches/correspondents expeditiously.

Where advance payment has been received or an irrevocable LCWhere advance payment has been received or an irrevocable LCpermits, shipping documents can be dispatched direct to thepermits, shipping documents can be dispatched direct to theconsignees or their agentsconsignees or their agents

In other cases if the exporter is a regular customer and theIn other cases if the exporter is a regular customer and theauthorised dealer is satisfied, direct dispatch is OKauthorised dealer is satisfied, direct dispatch is OK

`Status Holder Exporters' (as defined in the EXIM Policy) may`Status Holder Exporters' (as defined in the EXIM Policy) maydespatch the export documents to the consignees outside Indiadespatch the export documents to the consignees outside Indiasubject to the terms and conditions thatsubject to the terms and conditions that

the export proceeds are repatriated through the authorised dealer the export proceeds are repatriated through the authorised dealer named in the GR Form andnamed in the GR Form and

the duplicate copy of the GR form is submitted to the Authorisedthe duplicate copy of the GR form is submitted to the AuthorisedDealer for monitoring purposes, by the exporters within 21 daysDealer for monitoring purposes, by the exporters within 21 daysfrom the date of export.from the date of export.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 27/40

Reduction in value of export duesReduction in value of export duesReduction in invoice value on account of prepayment of usance billsReduction in invoice value on account of prepayment of usance bills

Cash discount to the extent of proportionate interest on the unexpired period of Cash discount to the extent of proportionate interest on the unexpired period of usance, at interest rate stipulated in the contract or at prime rate/LIBOR if notusance, at interest rate stipulated in the contract or at prime rate/LIBOR if notstipulated in the contract.stipulated in the contract.

Reduction in ValueReduction in Value

Can be reduced, if AD is satis-fied about genuineness of the request:Can be reduced, if AD is satis-fied about genuineness of the request:

the reduction does not exceed 10% of invoice value,the reduction does not exceed 10% of invoice value,

it does not relate to export of commodities subject to floor price stipulations,it does not relate to export of commodities subject to floor price stipulations,

the exporter is not on the exporters’ caution list of Reserve Bank, andthe exporter is not on the exporters’ caution list of Reserve Bank, and

the exporter is advised to surrender proportionate export incentives availedthe exporter is advised to surrender proportionate export incentives availedof, if any.of, if any.

The ceiling does not apply to exporters to the their track record beingThe ceiling does not apply to exporters to the their track record being

satisfactory,satisfactory, i.e.,i.e., the export outstandings do not exceed 5% of the averagethe export outstandings do not exceed 5% of the averageannual export realisation during preceding three calendar years.annual export realisation during preceding three calendar years.

outstandings in respect of exports made to countries facing externalisationoutstandings in respect of exports made to countries facing externalisation problems may be ignored provided the payments have been made by the problems may be ignored provided the payments have been made by thebuyers in the local currency.buyers in the local currency.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 28/40

Advance PaymentsAdvance Payments

Advance Payments against ExportsAdvance Payments against Exports

Exporters may receive advance payments (with or withoutExporters may receive advance payments (with or withoutinterest) from their overseas buyers.interest) from their overseas buyers.

Shipments made against the advance payments need to beShipments made against the advance payments need to bemonitored by AD.monitored by AD.

Appropriations made against every ship ment must beAppropriations made against every ship ment must beendorsed on the original copy of the inward remit tanceendorsed on the original copy of the inward remit tancecertificate issued for advance remittance.certificate issued for advance remittance.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 29/40

Part DrawingsPart Drawings

In certain lines, a part of invoice value is left undrawn for paymentIn certain lines, a part of invoice value is left undrawn for paymentafter adjustment due to differences in weight, quality, etc. to beafter adjustment due to differences in weight, quality, etc. to beascertained after arrival and inspection, weighment or analysis of ascertained after arrival and inspection, weighment or analysis of the goods.the goods.

the amount of undrawn balance is normal in line, subject to athe amount of undrawn balance is normal in line, subject to amaximum of 10 per cent of the full export value; andmaximum of 10 per cent of the full export value; and

an undertaking is obtained from exporter on the duplicate of an undertaking is obtained from exporter on the duplicate of GR/SDF/PP forms that he will surrender/account for the balanceGR/SDF/PP forms that he will surrender/account for the balanceproceeds within the period prescribed for realisation.proceeds within the period prescribed for realisation.

If exporter is unable to repatriate undrawn balance in spite of bestIf exporter is unable to repatriate undrawn balance in spite of bestefforts, AD, on being satisfied with theefforts, AD, on being satisfied with the bona fidesbona fides of the case, mayof the case, maysubmit duplicate copies of GR/PP/SDF formssubmit duplicate copies of GR/PP/SDF forms

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 30/40

Change of buyer/consigneeChange of buyer/consignee

Change of Buyer Change of Buyer

Can be done freely providedCan be done freely provided

the reduction in value, if any, involved does not exceedthe reduction in value, if any, involved does not exceed

10% and10% and the realisation of export proceeds is not delayed beyondthe realisation of export proceeds is not delayed beyond

the period of six months from the date of export.the period of six months from the date of export.

Export on Elongated Credit Terms permissible with RBI Export on Elongated Credit Terms permissible with RBI

approval approval

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 31/40

Extension of Time LimitExtension of Time Limit

Normally to be realized within six months from the date of export Extension of time needs RBI’s approval.

ADs can permit time extension beyond 6 months where invoicevalue does not exceed US $ 1,00,000 subject to followingconditions; Reasons for delay is beyond exporter’s control Exporter declares that he will realise proceeds during extended period.

Up to 3 months at a time - beyond one year from the date of export thetotal export outstandings of the exporter should not be more than 10%of the average of export realisations during the preceding 3 financialyears.

As a temporary measure w.e.f. September 1, 2001, 360 days from thedate of shipment is allowed for realisation for exports to certainspecified countries.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 32/40

Shipments lost in TransitShipments lost in Transit

When shipments for which payment has not are lost in transit,When shipments for which payment has not are lost in transit,insurance claim should be made as soon as the loss is known. Theinsurance claim should be made as soon as the loss is known. Theduplicate copy of GR/SDF/PP form should be forwarded to Reserveduplicate copy of GR/SDF/PP form should be forwarded to ReserveBank with following particulars :Bank with following particulars :

Amount for which shipment was insured.Amount for which shipment was insured. Name and address of insurance company.Name and address of insurance company.

Place where claim is payable.Place where claim is payable.

In cases where claim is payable abroad, AD must collect the fullIn cases where claim is payable abroad, AD must collect the full

amount through overseas branch/correspondent and forward theamount through overseas branch/correspondent and forward theduplicate copy of GR/SDF/PP form to Reserve Bank only after theduplicate copy of GR/SDF/PP form to Reserve Bank only after theamount has been collected. A certificate for the amount of claimamount has been collected. A certificate for the amount of claimreceived should be furnished on the reverse of the duplicate copy.received should be furnished on the reverse of the duplicate copy.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 33/40

Payment by ECGCPayment by ECGC

Where ECGC settles a claim, the exporter is statutoryWhere ECGC settles a claim, the exporter is statutoryobliged to realise proceeds within prescribed period. Inobliged to realise proceeds within prescribed period. Insuch cases, exporter should, in consultation with ECGC,such cases, exporter should, in consultation with ECGC,

take all necessary steps for realising the proceeds.take all necessary steps for realising the proceeds.

Authorised dealers should also continue to hold theAuthorised dealers should also continue to hold theduplicate copies of GR/SDF/PP forms in their custodyduplicate copies of GR/SDF/PP forms in their custodyand initiate follow-up measures in the normal manner.and initiate follow-up measures in the normal manner.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 34/40

Trade Discounts …Trade Discounts …

Trade DiscountTrade Discount

Accepted only if the discount has been declared onAccepted only if the discount has been declared onrelative GR/SDF form at the time of shipment andrelative GR/SDF form at the time of shipment andaccepted by Customs.accepted by Customs.

Export ClaimsExport Claims Eexport claims may be remitted, provided the relativeEexport claims may be remitted, provided the relative

export proceeds have already been realised andexport proceeds have already been realised andrepatriated to India and the exporter is not on the cautionrepatriated to India and the exporter is not on the cautionlist of Reserve Bank.list of Reserve Bank.

In all such cases of remittances, the exporter shouldIn all such cases of remittances, the exporter shouldsurrender proportionate export incentive, if any, receivedsurrender proportionate export incentive, if any, receivedby him.by him.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 35/40

Write off of unrealised billsWrite off of unrealised bills

(i) If an exporter is not able to realise the export dues(i) If an exporter is not able to realise the export duesdespite best efforts, the unrealised portion can be writtendespite best efforts, the unrealised portion can be writtenoff:off:

The relevant amount has remained outstanding for one year or The relevant amount has remained outstanding for one year or

more;more;

The aggregate amount of write off allowed by the autho-risedThe aggregate amount of write off allowed by the autho-riseddealer during a calendar year does not exceed 10% of the totaldealer during a calendar year does not exceed 10% of the totalexport proceeds realised through the concerned authorisedexport proceeds realised through the concerned authoriseddealer during the previous calendar year;dealer during the previous calendar year;

Satisfactory documentary evidence is furnished in support of theSatisfactory documentary evidence is furnished in support of theexporter having made all efforts to realise the dues;exporter having made all efforts to realise the dues;

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 36/40

Acceptable circumstancesAcceptable circumstances The overseas buyer ‘s insolvency certified by official liquidator The overseas buyer ‘s insolvency certified by official liquidator

The overseas buyer is not traceable over a reasonably long period of time;The overseas buyer is not traceable over a reasonably long period of time;

The goods exported have been auctioned or destroyed by theThe goods exported have been auctioned or destroyed by thePort/Customs/Health authorities in the importing country;Port/Customs/Health authorities in the importing country;

The unrealised amount represents the balance due in a case settledThe unrealised amount represents the balance due in a case settledthrough the intervention of the Indian Embassy, Foreign Chamber of through the intervention of the Indian Embassy, Foreign Chamber of

Commerce, etc.Commerce, etc. The unrealised amount represents the undrawn balance of an export billThe unrealised amount represents the undrawn balance of an export bill

(not exceeding 10% of the invoice value) remained outstanding and turned(not exceeding 10% of the invoice value) remained outstanding and turnedout to be unrealisable despite all efforts made by the exporter;out to be unrealisable despite all efforts made by the exporter;

The cost of resorting to legal action would be dispro-portionate or whereThe cost of resorting to legal action would be dispro-portionate or wherethe exporter even after winning the Court case against the over-seas buyer the exporter even after winning the Court case against the over-seas buyer could not execute the Court decreecould not execute the Court decree

Bills were drawn for the difference between the letter of credit value andBills were drawn for the difference between the letter of credit value andactual export value or between the provisional and the actual freightactual export value or between the provisional and the actual freightcharges but the amount has remained unrealised consequent on dishonour charges but the amount has remained unrealised consequent on dishonour of the bills by the overseas buyer of the bills by the overseas buyer

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 37/40

Exporters’ Caution ListExporters’ Caution List

Authorised dealers should not accept for Authorised dealers should not accept for negotiation/collection shipping documents coveringnegotiation/collection shipping documents coveringexports de-clared on GR/SDF/PP forms completed byexports de-clared on GR/SDF/PP forms completed by

such exporters nor coun-tersign PP forms completed bysuch exporters nor coun-tersign PP forms completed by

them unless the GR/SDF/PP forms bear approval of them unless the GR/SDF/PP forms bear approval of Reserve Bank.Reserve Bank.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 38/40

Agency CommissionAgency Commission

(i)(i) Payment of commission, either by remittance or byPayment of commission, either by remittance or bydeduction from invoice value, is permitted :deduction from invoice value, is permitted :

Amount has been declared on GR/SDF/PP/SOFTEX form andAmount has been declared on GR/SDF/PP/SOFTEX form andaccepted by Customs authorities or Ministry of Informationaccepted by Customs authorities or Ministry of Information

Technology, Government of India / EPZ authorities as the caseTechnology, Government of India / EPZ authorities as the casemay be.may be.

If not declared on GR/SDF/PP/SOFTEX form, remittance may beIf not declared on GR/SDF/PP/SOFTEX form, remittance may beallowed if reasons adduced for not declaring are satisfactoryallowed if reasons adduced for not declaring are satisfactoryprovided a valid agreement/written understanding between theprovided a valid agreement/written understanding between the

exporter and/or beneficiary for payment of commission subsists.exporter and/or beneficiary for payment of commission subsists.

The relative shipment has already been made.The relative shipment has already been made.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 39/40

Agency …..Agency …..

(ii)(ii) Payment of commission, in respect of exports under counter tradePayment of commission, in respect of exports under counter tradethrough Escrow Accounts designated in U.S.dollar, subject to thethrough Escrow Accounts designated in U.S.dollar, subject to thefollowing conditions :following conditions :

The payment of commission satisfies the conditions as at (a) and (b)The payment of commission satisfies the conditions as at (a) and (b)

stipulated in paragraph above.stipulated in paragraph above.

The commission is not payable to Escrow Account holders themselves.The commission is not payable to Escrow Account holders themselves.

The commission should not be allowed by deduction from the invoiceThe commission should not be allowed by deduction from the invoice

value.value.

NOTE : Payment of commission is prohibited on exports made byNOTE : Payment of commission is prohibited on exports made byIndian Partners towards equity participation in an overseas jointIndian Partners towards equity participation in an overseas jointventure / wholly owned subsidiary as also exports under Rupeeventure / wholly owned subsidiary as also exports under RupeeCredit Route.Credit Route.

8/4/2019 Export Finance Options

http://slidepdf.com/reader/full/export-finance-options 40/40

Refund of Export ProceedsRefund of Export Proceeds

Refund of export proceeds may be allowed by ADsRefund of export proceeds may be allowed by ADsthrough whom the proceeds were originally received,through whom the proceeds were originally received,provided such goods are re-imported into India onprovided such goods are re-imported into India on

account of poor quality etc. and evidence of re-importaccount of poor quality etc. and evidence of re-import

has been submitted.has been submitted. In all such cases, exporters should be advised toIn all such cases, exporters should be advised to

surrender the propor-tionate incentives availed of, if any,surrender the propor-tionate incentives availed of, if any,against the relevant export.against the relevant export.