Embed Size (px)

Citation preview

EXPORT FINANCING AND MULTINATIONAL

TAX STRUCTURE

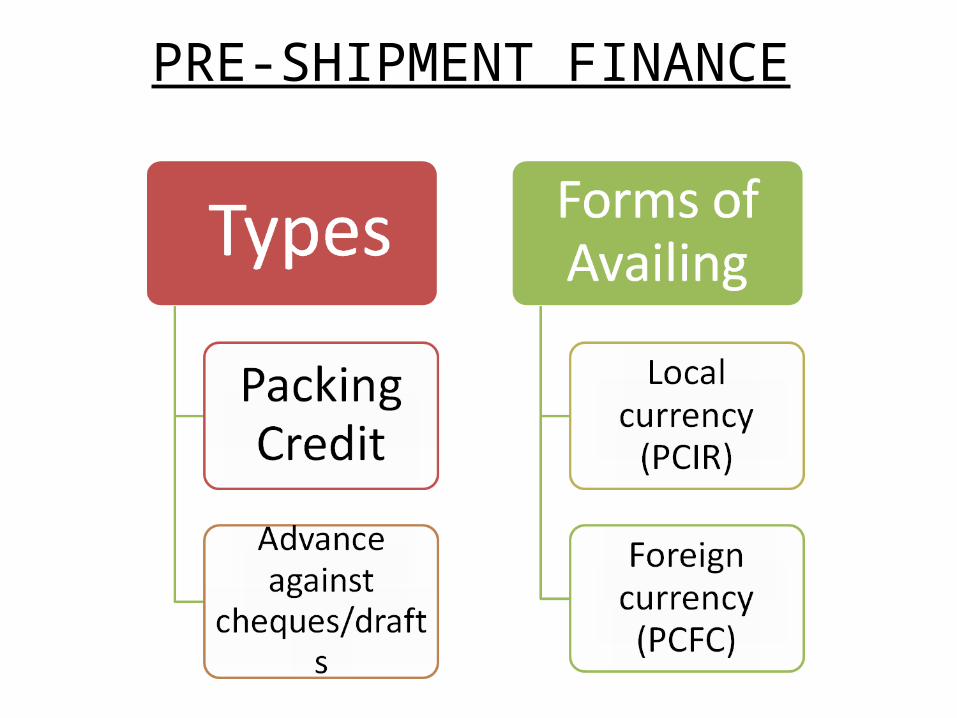

PRE-SHIPMENT FINANCE

PACKING CREDIT (Domestic Currency)

• Purpose • Requirement for getting packing credit• Eligibility• Quantum of finance• Procedure

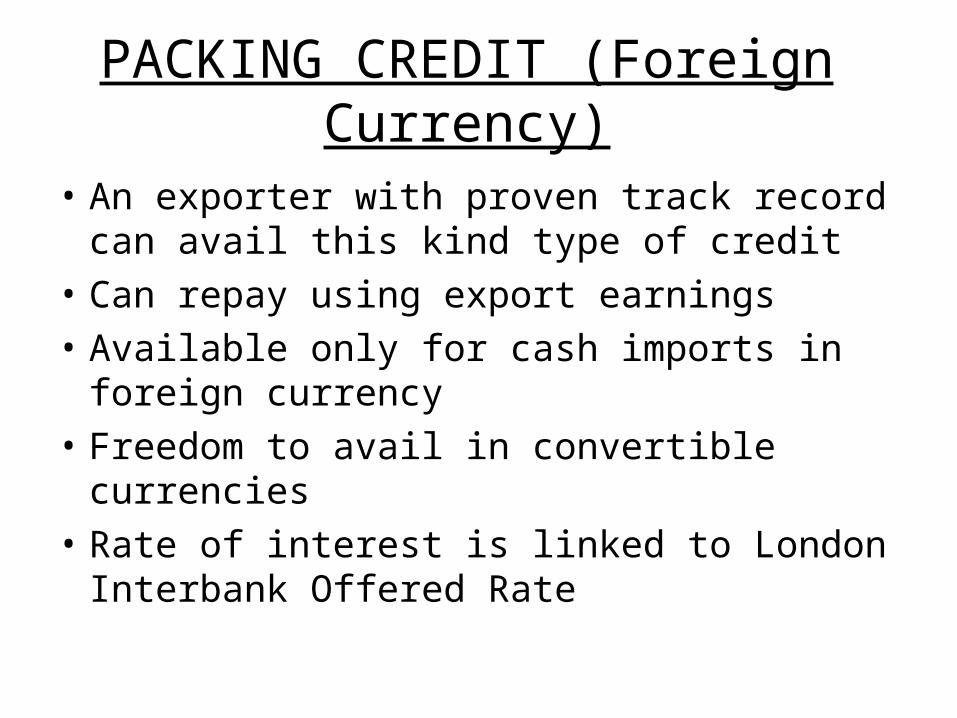

PACKING CREDIT (Foreign Currency)

• An exporter with proven track record can avail this kind type of credit

• Can repay using export earnings• Available only for cash imports in foreign

currency• Freedom to avail in convertible currencies• Rate of interest is linked to London Interbank

Offered Rate

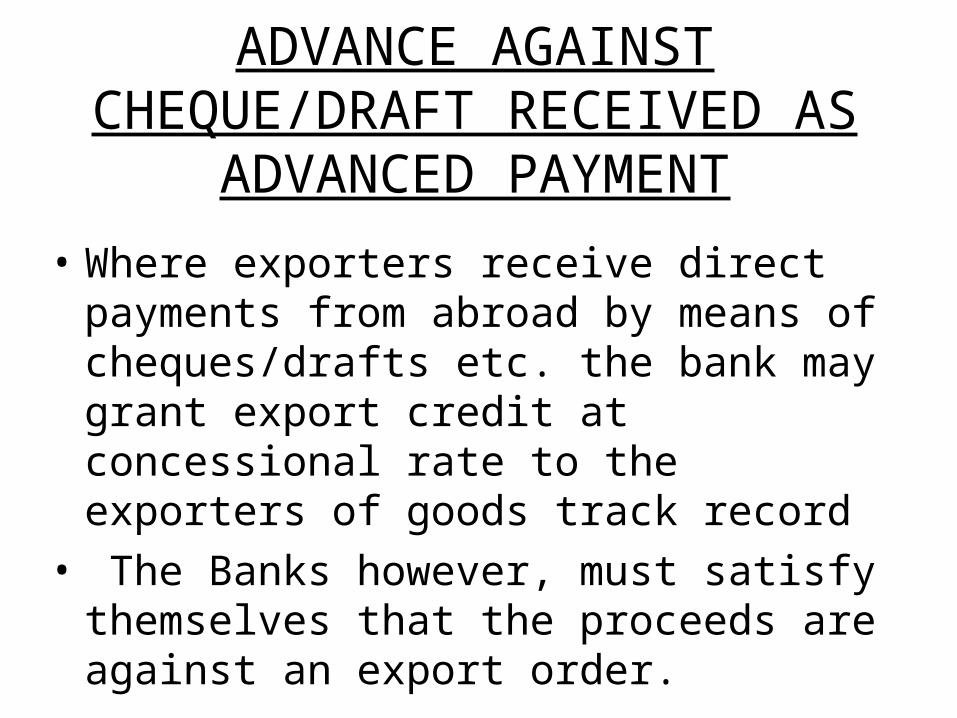

ADVANCE AGAINST CHEQUE/DRAFT RECEIVED AS

ADVANCED PAYMENT

• Where exporters receive direct payments from abroad by means of cheques/drafts etc. the bank may grant export credit at concessional rate to the exporters of goods track record

• The Banks however, must satisfy themselves that the proceeds are against an export order.

Post Shipment FinanceWhat is a Post Shipment Finance?Post-shipment finance is a loan or advance granted by a bank to an exporter of goods from India. This facility is available to an exporter subsequent to the date of shipment of goods up to the date of realization of export proceedsWho is eligible for post-shipment finance?Post-shipment finance is extended to the actual exporter who has exported the goods or to an exporter in whose name the export documents are transferred. Basic Features.1.Purpose of Finance2.Basis of Finance3.Types of Finance4.Quantum of Finance5.Period of Finance

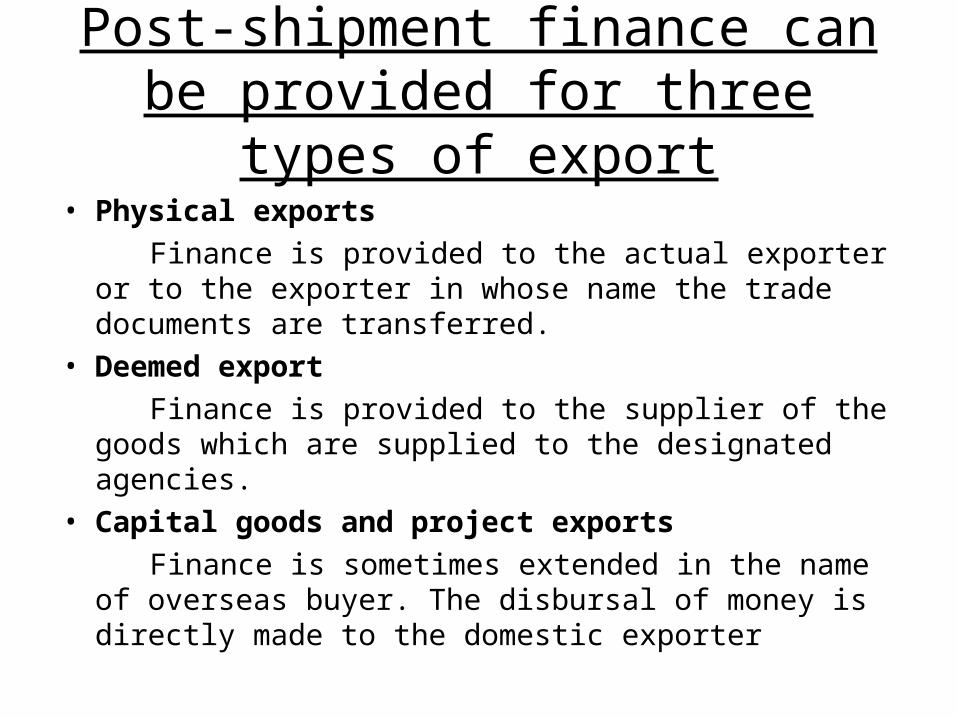

Post-shipment finance can be provided for three types of export

• Physical exports

Finance is provided to the actual exporter or to the exporter in whose name the trade documents are transferred.

• Deemed export

Finance is provided to the supplier of the goods which are supplied to the designated agencies.

• Capital goods and project exports

Finance is sometimes extended in the name of overseas buyer. The disbursal of money is directly made to the domestic exporter

Types of Post Shipment Finance

The post shipment finance can be classified as :1.Export Bills purchased/discounted Export bills (Non L/C Bills) is used in terms of sale contract/ order may be discounted or purchased by the banks. It is used in indisputable international trade transactions and the proper limit has to be sanctioned to the exporter for purchase of export bill facility

2. Export Bills negotiated. The risk of payment is less under the LC, as the issuing bank makes sure the payment. The risk is further reduced, if a bank guarantees the payments by confirming the LC However, this arises two major risk factors for the banks The risk of nonperformance by the exporter The bank also faces the documentary risk where the issuing bank refuses to honour its commitment

3. Advance against export bills sent on collection basis.

Bills can only be sent on collection basis, if the bills drawn under LC have some discrepancies. Banks may allow advance against these collection bills to an exporter with a concessional rates of interest depending upon the transit period in case of DP Bills and transit period plus usance period in case of usance bill

4. Advance against export on consignment basis

Bank may choose to finance when the goods are exported on consignment basis at the risk of the exporter for sale and eventual payment of sale proceeds to him by the consignee

5. Advance against undrawn balance on exports.

It is a very common practice in export to leave small part undrawn for payment after adjustment due to difference in rates, weight, quality etc.

6. Advance against claims of Duty Drawback.

Duty Drawback is a type of discount given to the exporter in his own country. This discount is given only, if the in-house cost of production is higher in relation to international price. This type of financial support helps the exporter to fight successfully in the international markets.

Post-shipment Credit

• Sight Bills - Not more than 10%

• Upto 90 days - Not more than 10%

• 91 days upto 6 months - 12%

TRADE FINANCE METHODS

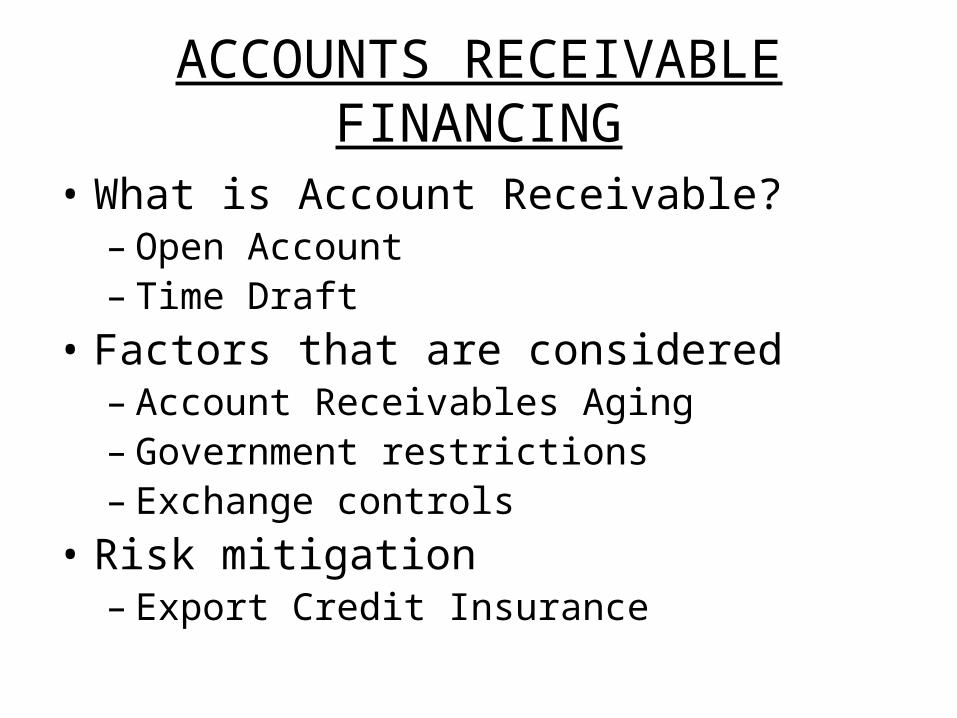

ACCOUNTS RECEIVABLE FINANCING

• What is Account Receivable?– Open Account– Time Draft

• Factors that are considered– Account Receivables Aging– Government restrictions– Exchange controls

• Risk mitigation– Export Credit Insurance

FACTORING- THE PROCESSYOU

Deliver Goods or Services and generate an invoice/receivable

YOU consider selling the invoice to the factor(At a DISCOUNT) per factoring contract

Factor performs its own credit approval process before purchasing the receivable/invoice

20% is held in the Reserve Account

Factor funds you 80% of the amount immediately

Factor collects payment on the invoice from your customer

Factor rebates YOU 20% reserve minus fee

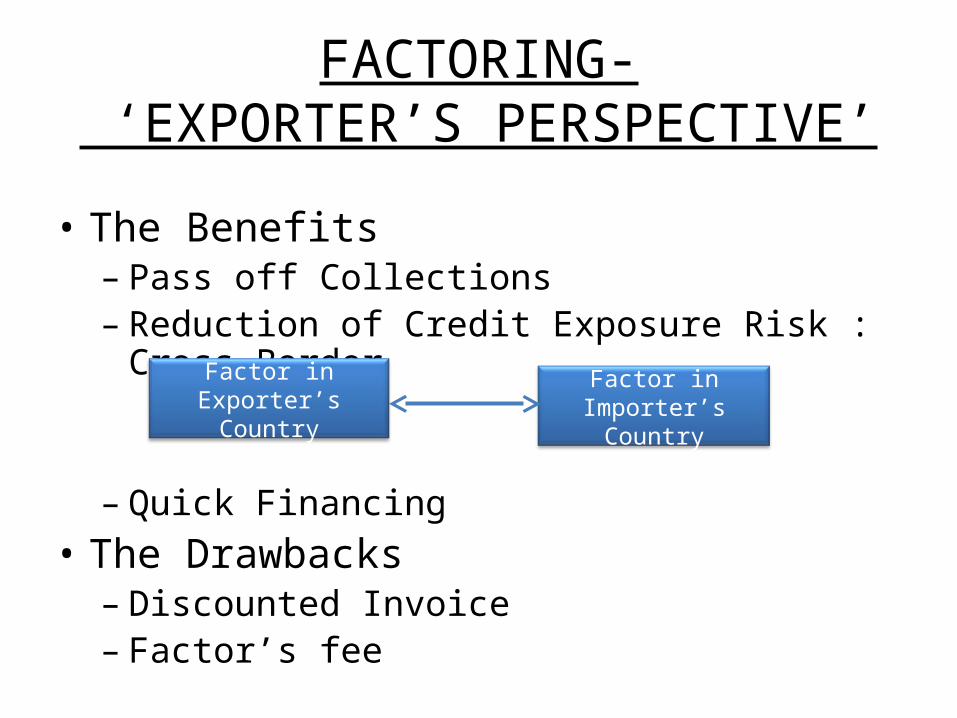

FACTORING- ‘EXPORTER’S PERSPECTIVE’

• The Benefits– Pass off Collections– Reduction of Credit Exposure Risk : Cross Border

– Quick Financing

• The Drawbacks– Discounted Invoice– Factor’s fee

Factor in Exporter’s Country

Factor in Importer’s Country

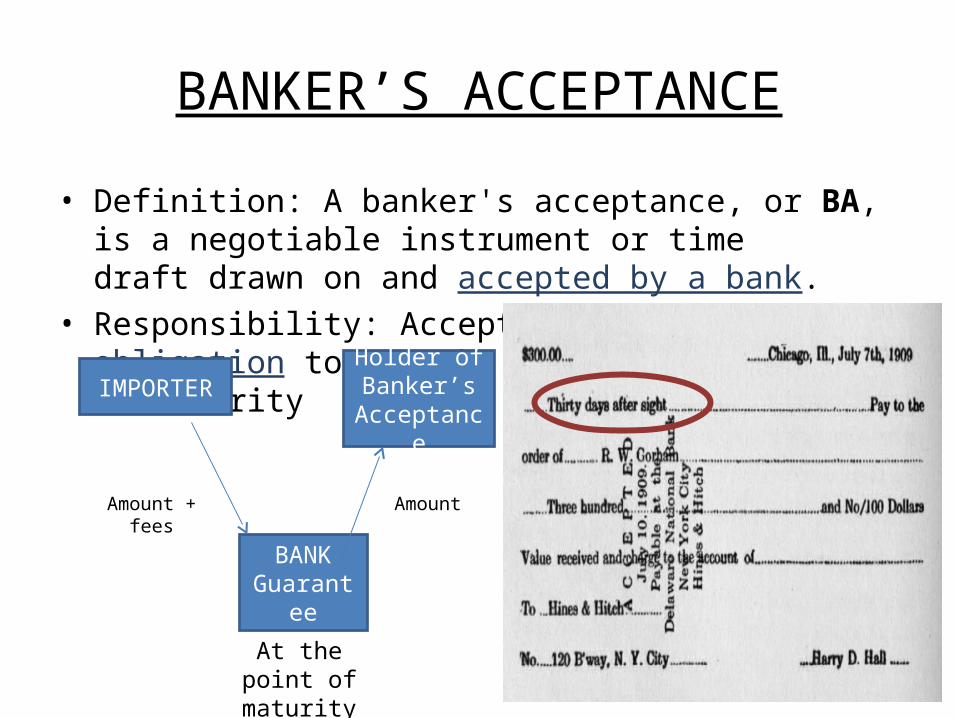

BANKER’S ACCEPTANCE

• Definition: A banker's acceptance, or BA, is a negotiable instrument or time draft drawn on and accepted by a bank.

• Responsibility: Accepting bank’s obligation to pay the holder of the draft at maturity

IMPORTERHolder of Banker’s

Acceptance

BANKGuarantee

At the point of maturity

Amount + fees

Amount

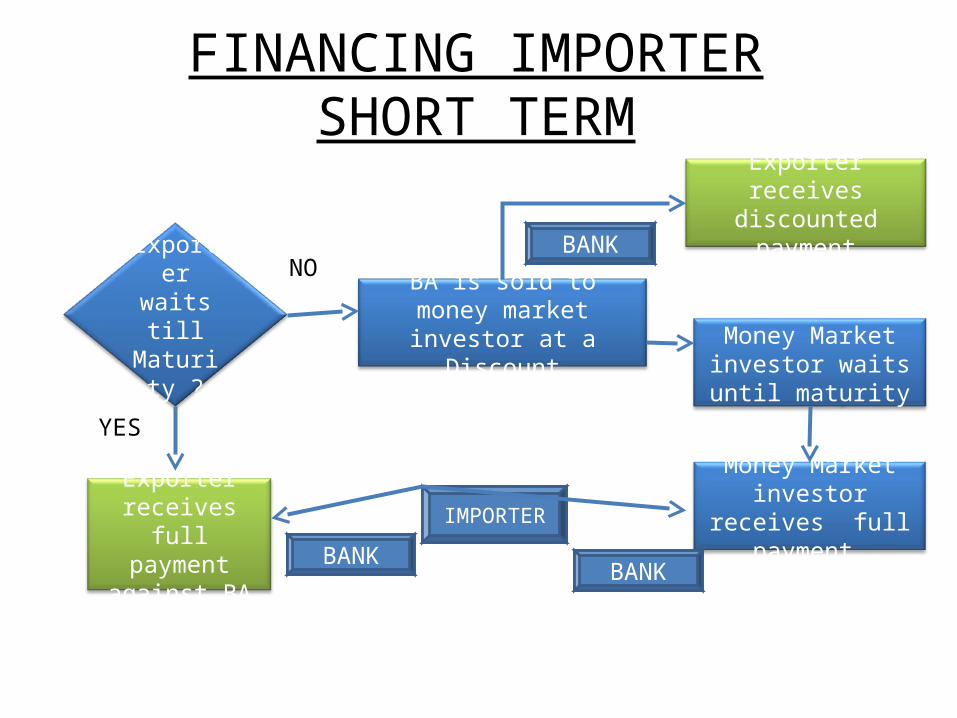

FINANCING IMPORTERSHORT TERM

Exporter waits till Maturity

?

BA is sold to money market investor at a

Discount

Exporter receives discounted payment

Money Market investor waits until

maturity

Money Market investor receives full

payment

Exporter receives full

payment against BA

IMPORTER

NO

YES

BANK

BANK

BANK

WORKING CAPITAL FINANCING

Raw Materials

Work In Progress

Finished Goods

Receivables

Cash

OPERATING CYCLE

WC financing in INTERNATIONAL TRADE??

WC financing in domestic business

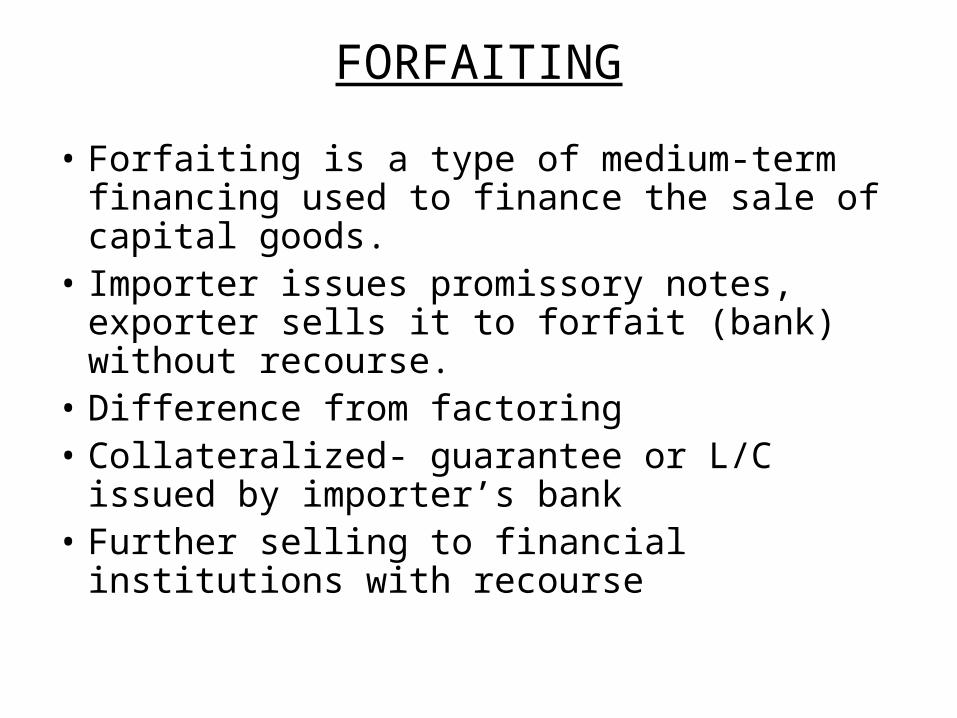

FORFAITING

• Forfaiting is a type of medium-term financing used to finance the sale of capital goods.

• Importer issues promissory notes, exporter sells it to forfait (bank) without recourse.

• Difference from factoring• Collateralized- guarantee or L/C issued by

importer’s bank• Further selling to financial institutions with

recourse

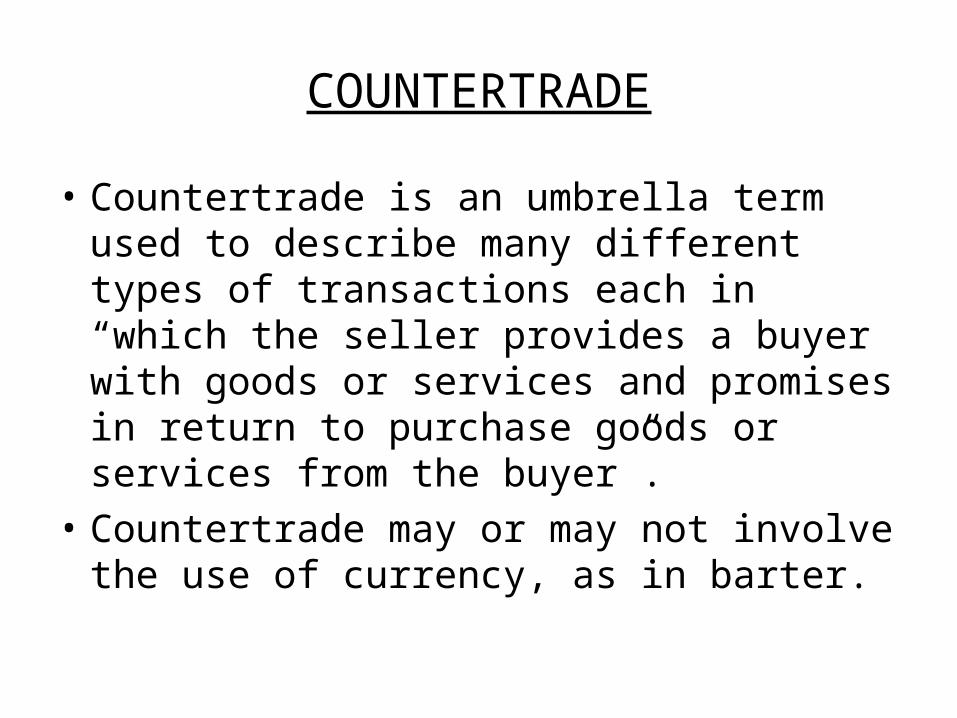

COUNTERTRADE

• Countertrade is an umbrella term used to describe many different types of transactions each in “which the seller provides a buyer with goods or services and promises in return to purchase goods or services from the buyer”.

• Countertrade may or may not involve the use of currency, as in barter.

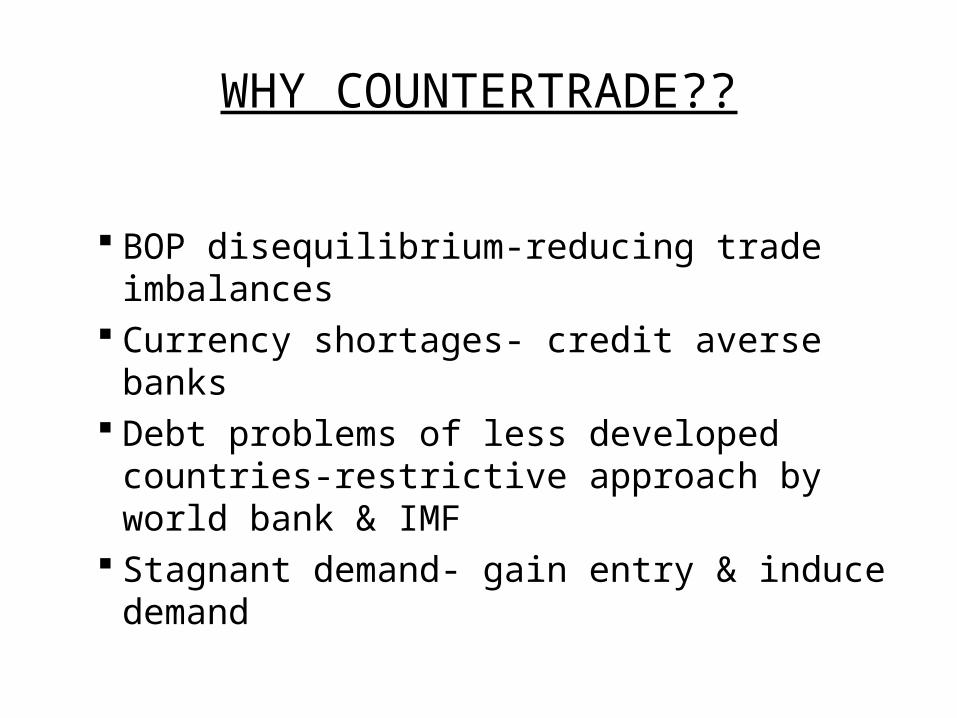

WHY COUNTERTRADE??

BOP disequilibrium-reducing trade imbalances

Currency shortages- credit averse banks Debt problems of less developed countries-

restrictive approach by world bank & IMF Stagnant demand- gain entry & induce

demand

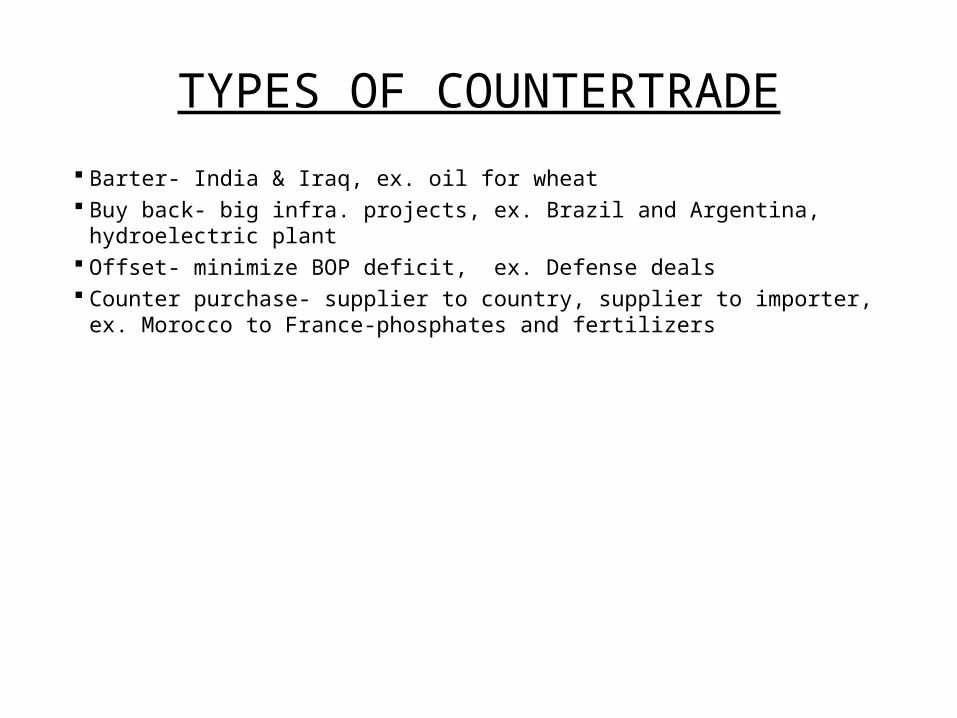

TYPES OF COUNTERTRADE

Barter- India & Iraq, ex. oil for wheat Buy back- big infra. projects, ex. Brazil and Argentina, hydroelectric plant Offset- minimize BOP deficit, ex. Defense deals Counter purchase- supplier to country, supplier to importer, ex. Morocco to

France-phosphates and fertilizers

INTERNATIONAL TAX STRUCTURE

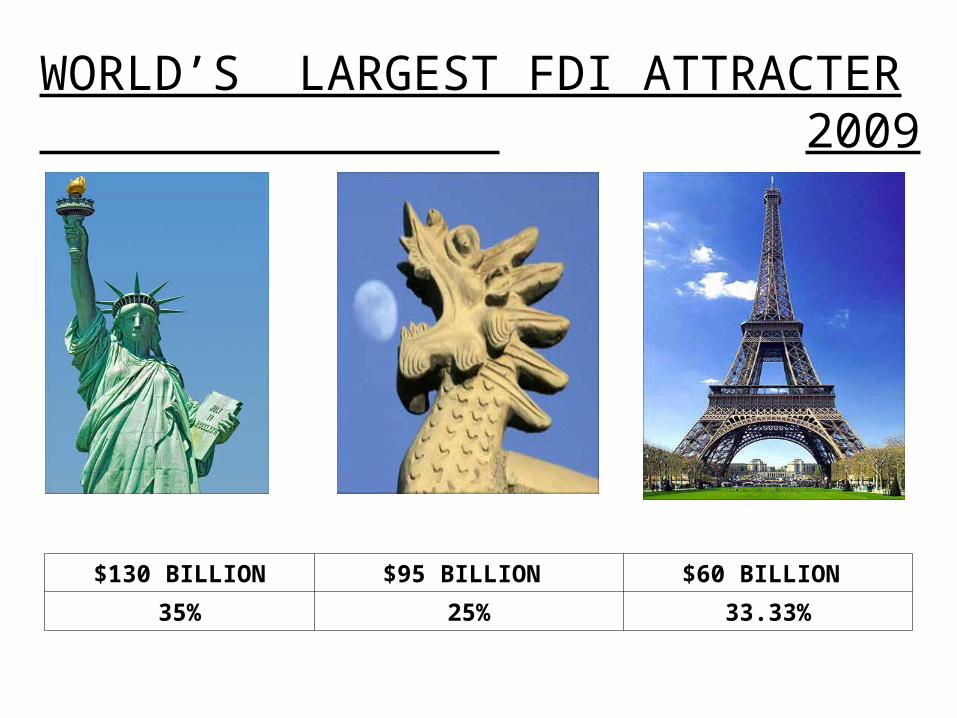

WORLD’S LARGEST FDI ATTRACTER 2009

$130 BILLION $95 BILLION $60 BILLION

35% 25% 33.33%

$48 BILLION $46 BILLION $39 BILLION

16.5% 28% 20%

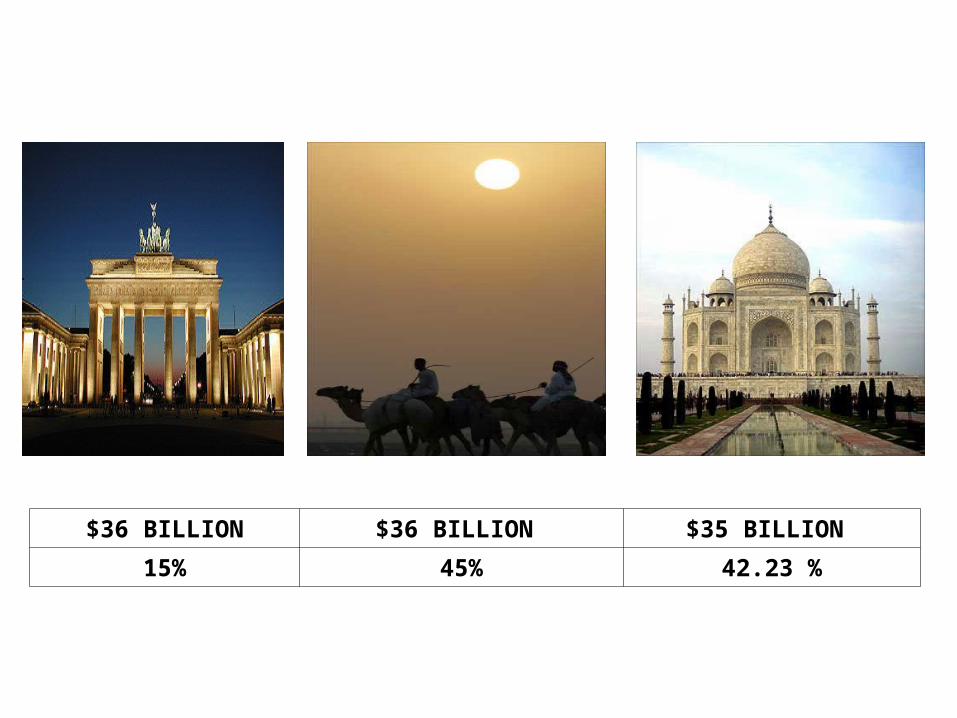

$36 BILLION $36 BILLION $35 BILLION

15% 45% 42.23 %

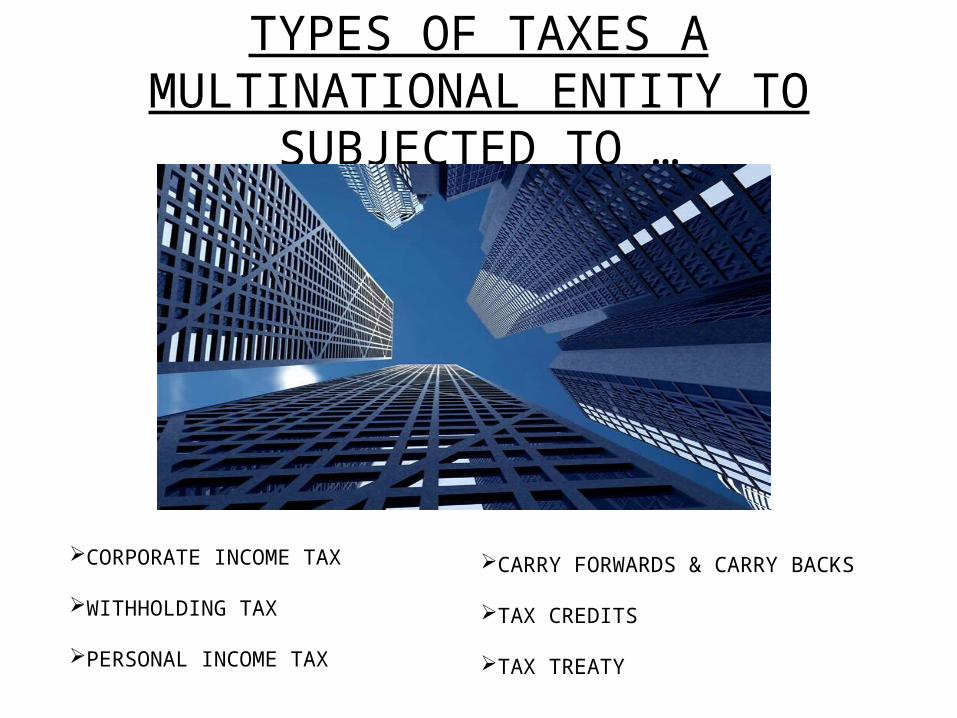

TYPES OF TAXES A MULTINATIONAL ENTITY TO

SUBJECTED TO …

CORPORATE INCOME TAX

WITHHOLDING TAX

PERSONAL INCOME TAX

CARRY FORWARDS & CARRY BACKS

TAX CREDITS

TAX TREATY

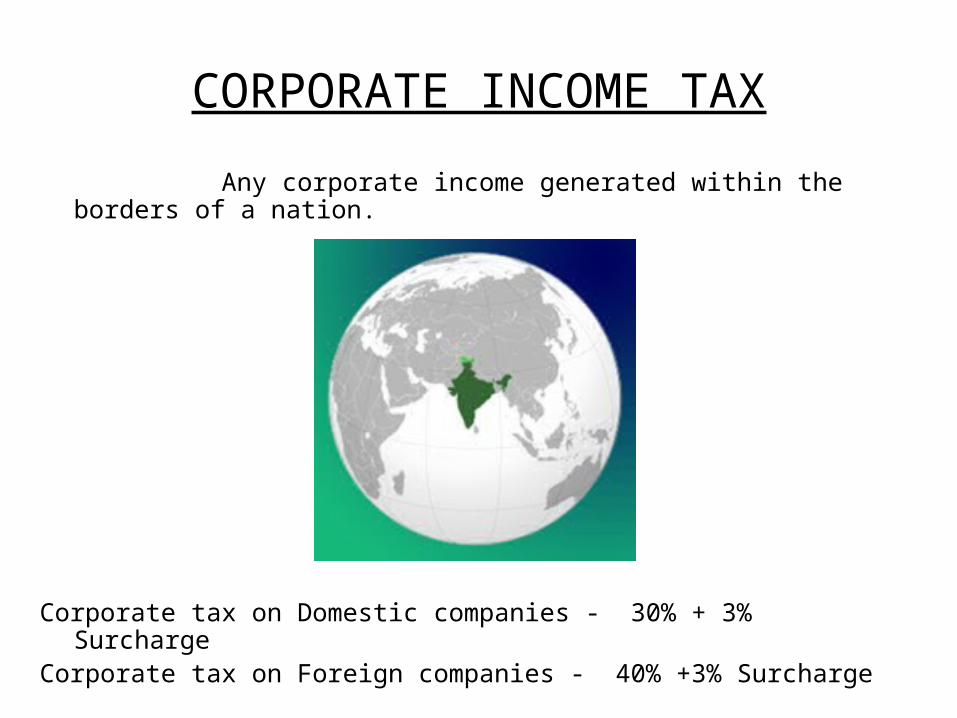

CORPORATE INCOME TAX

Any corporate income generated within the borders of a nation.

Corporate tax on Domestic companies - 30% + 3% SurchargeCorporate tax on Foreign companies - 40% +3% Surcharge

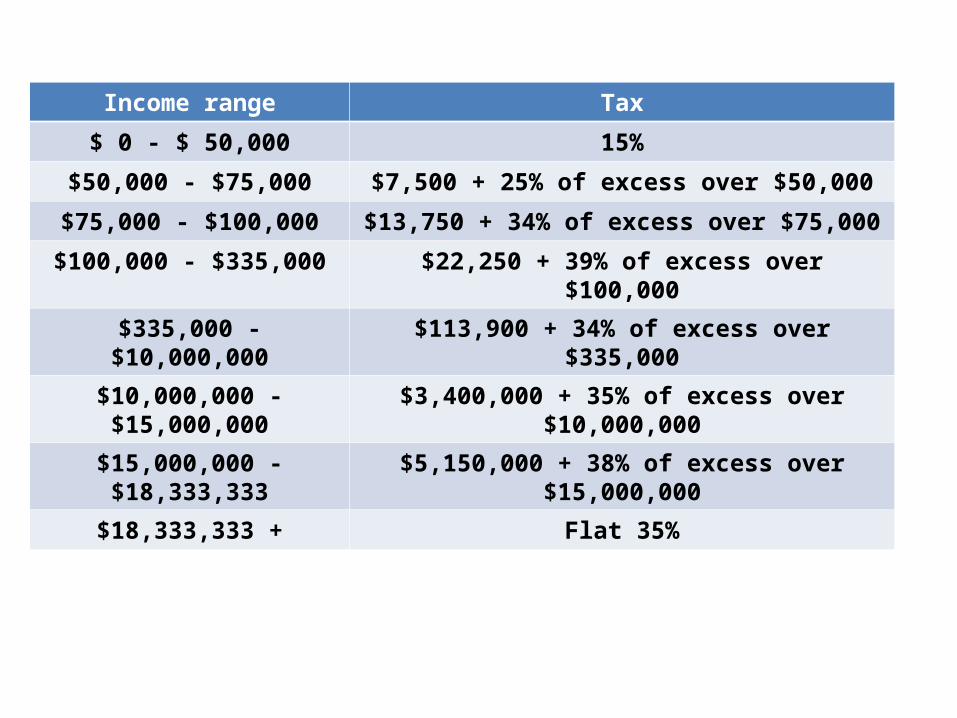

Income range Tax

$ 0 - $ 50,000 15%

$50,000 - $75,000 $7,500 + 25% of excess over $50,000

$75,000 - $100,000 $13,750 + 34% of excess over $75,000

$100,000 - $335,000 $22,250 + 39% of excess over $100,000

$335,000 - $10,000,000 $113,900 + 34% of excess over $335,000

$10,000,000 - $15,000,000 $3,400,000 + 35% of excess over $10,000,000

$15,000,000 - $18,333,333 $5,150,000 + 38% of excess over $15,000,000

$18,333,333 + Flat 35%

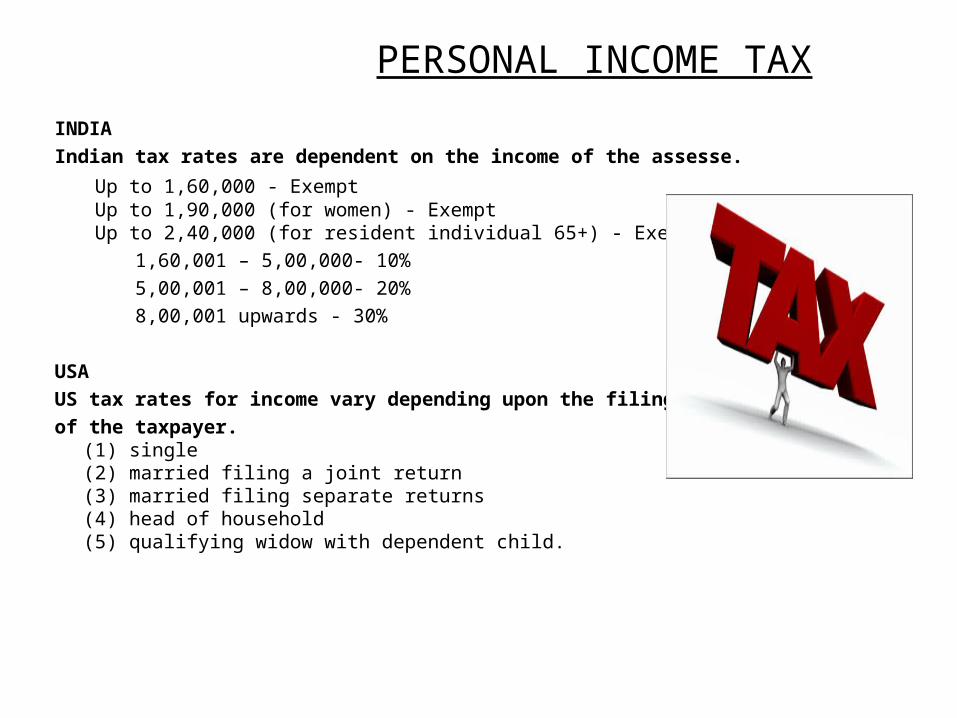

PERSONAL INCOME TAX INDIA

Indian tax rates are dependent on the income of the assesse.

Up to 1,60,000 - Exempt Up to 1,90,000 (for women) - Exempt Up to 2,40,000 (for resident individual 65+) - Exempt

1,60,001 – 5,00,000- 10% 5,00,001 – 8,00,000- 20% 8,00,001 upwards - 30%

USA

US tax rates for income vary depending upon the filing status of the taxpayer.

(1) single(2) married filing a joint return(3) married filing separate returns(4) head of household(5) qualifying widow with dependent child.

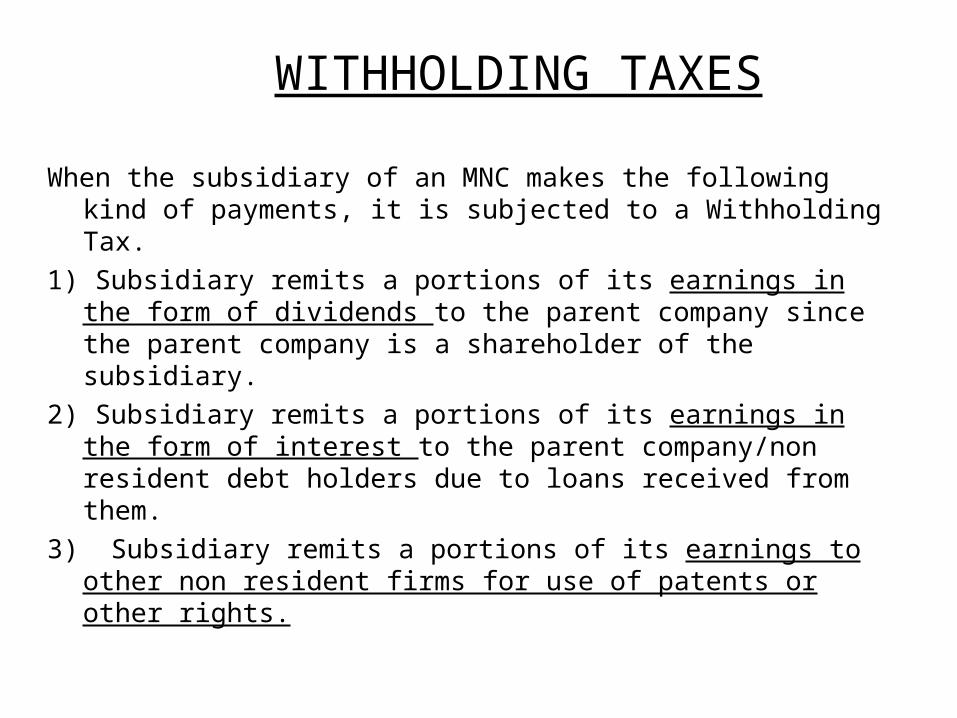

WITHHOLDING TAXES

When the subsidiary of an MNC makes the following kind of payments, it is subjected to a Withholding Tax.

1) Subsidiary remits a portions of its earnings in the form of dividends to the parent company since the parent company is a shareholder of the subsidiary.

2) Subsidiary remits a portions of its earnings in the form of interest to the parent company/non resident debt holders due to loans received from them.

3) Subsidiary remits a portions of its earnings to other non resident firms for use of patents or other rights.

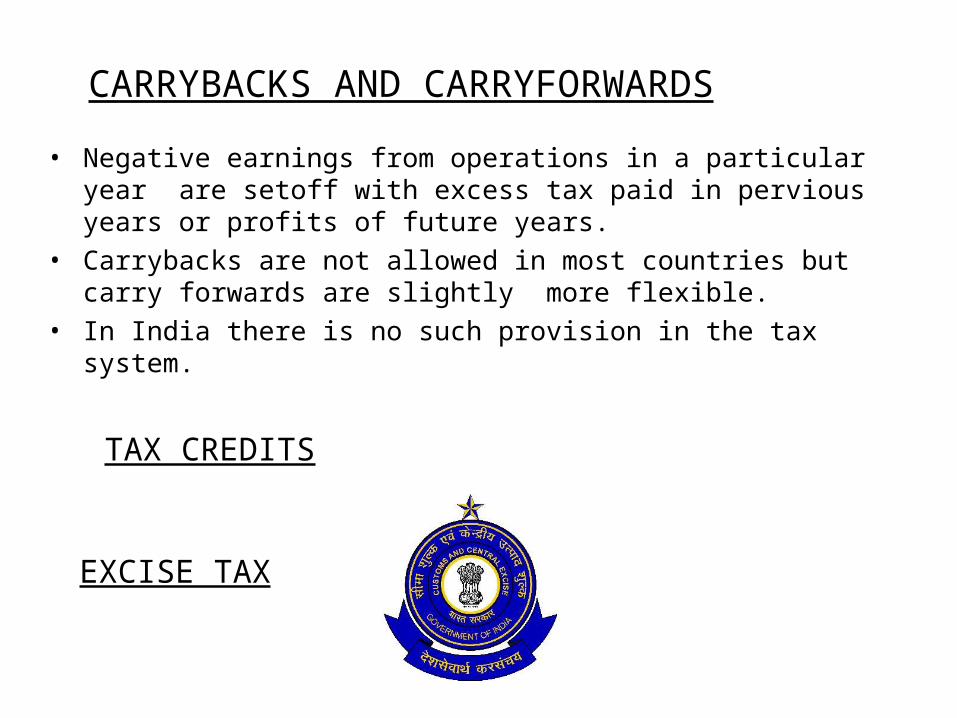

CARRYBACKS AND CARRYFORWARDS

• Negative earnings from operations in a particular year are setoff with excess tax paid in pervious years or profits of future years.

• Carrybacks are not allowed in most countries but carry forwards are slightly more flexible.

• In India there is no such provision in the tax system.

TAX CREDITS

EXCISE TAX

Tax TreatyTreaties -

• Define which taxes are covered and who is a resident and eligible for benefits,

• Reduce the amounts of tax withheld from interest, dividends, and royalties paid by a resident of one country to residents of the other country.

• Reduction of double taxation, eliminating tax evasion, and encouraging cross-border trade efficiency.

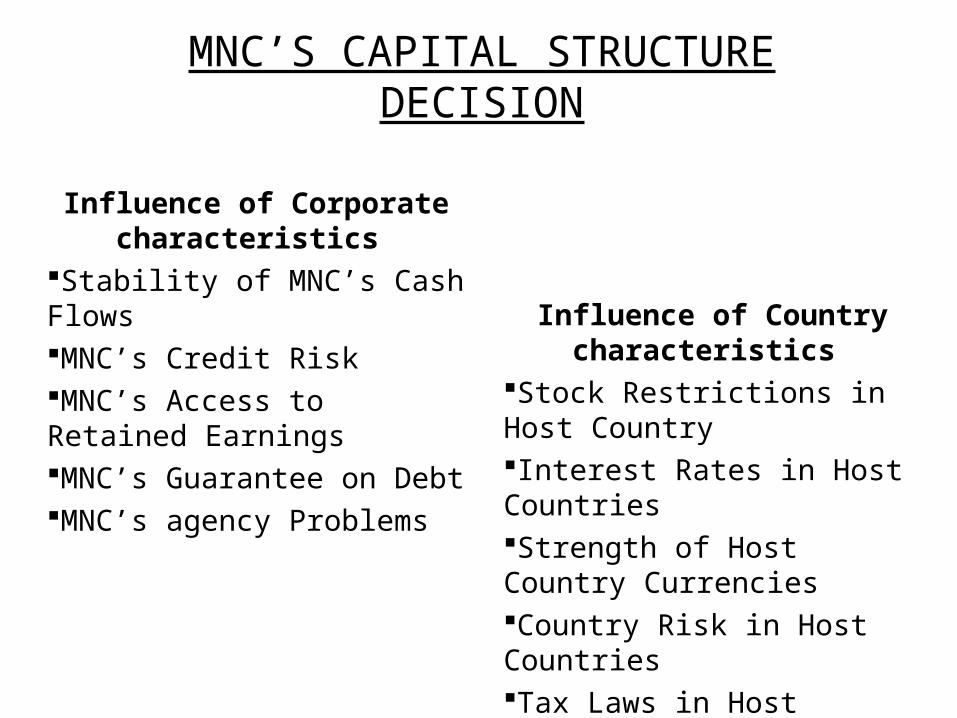

MNC’S CAPITAL STRUCTURE DECISION

Influence of Corporate characteristics

Stability of MNC’s Cash FlowsMNC’s Credit RiskMNC’s Access to Retained EarningsMNC’s Guarantee on DebtMNC’s agency Problems

Influence of Country characteristics

Stock Restrictions in Host CountryInterest Rates in Host CountriesStrength of Host Country CurrenciesCountry Risk in Host CountriesTax Laws in Host Countries