Embed Size (px)

Citation preview

REACHING THE WORLD THROUGH PRIVATE

SECTOR INITIATIVE: SERVICE EXPORTS FROM THE PHILIPPINES

June, 2011

Soonhwa Yi

The World Bank

Roadmap

• Pattern of Services Exports• Which services sector has performed well in

exporting and which one has lagged?• What are the characteristics of the sectors

with relatively strong or weak performance?– BPO vs Tourism

• What strategies, fundamentals, and policies contributed to, or failed to, boost exports? – BPO vs Tourism

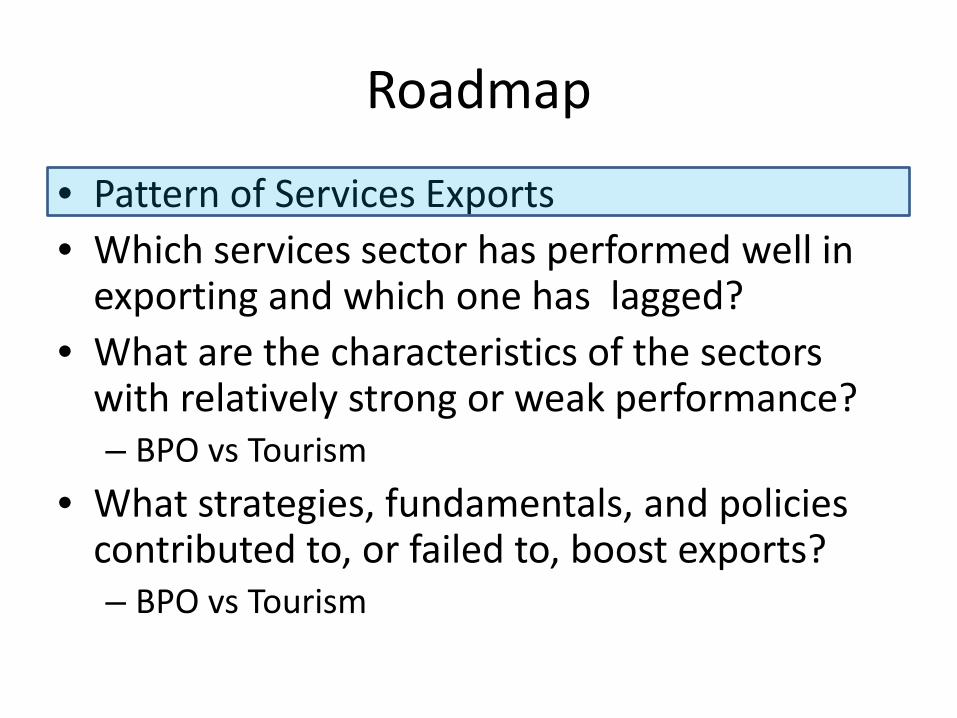

Cross-border services exports growing faster than goods

-50

0

50

100

150

200

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Goods Services

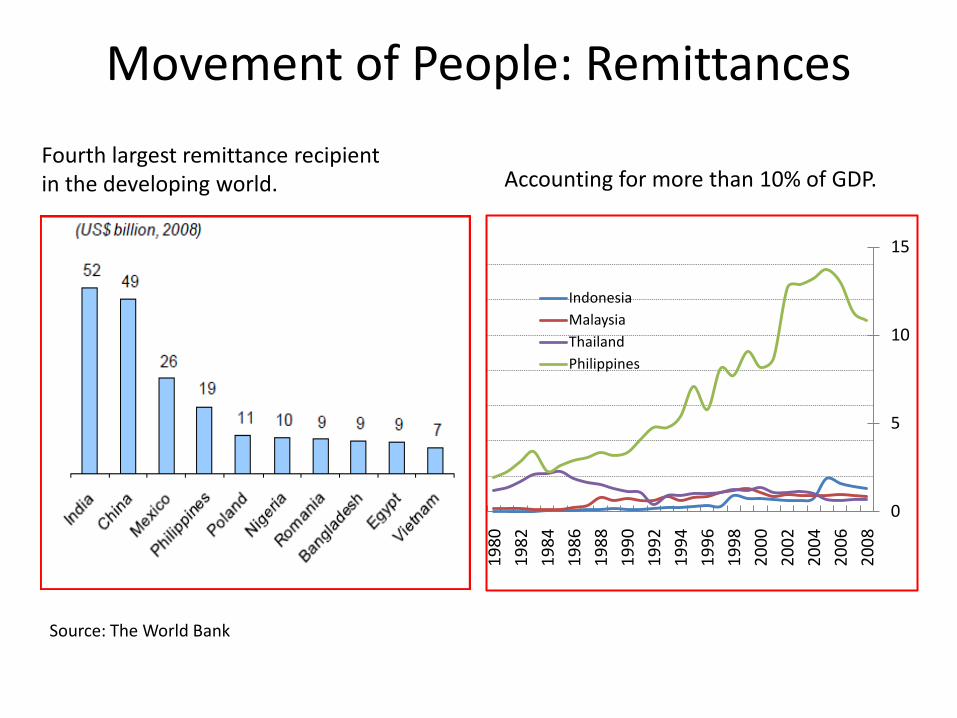

Movement of People: Remittances

0

5

10

15

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

IndonesiaMalaysiaThailandPhilippines

Source: The World Bank

Accounting for more than 10% of GDP.Fourth largest remittance recipient in the developing world.

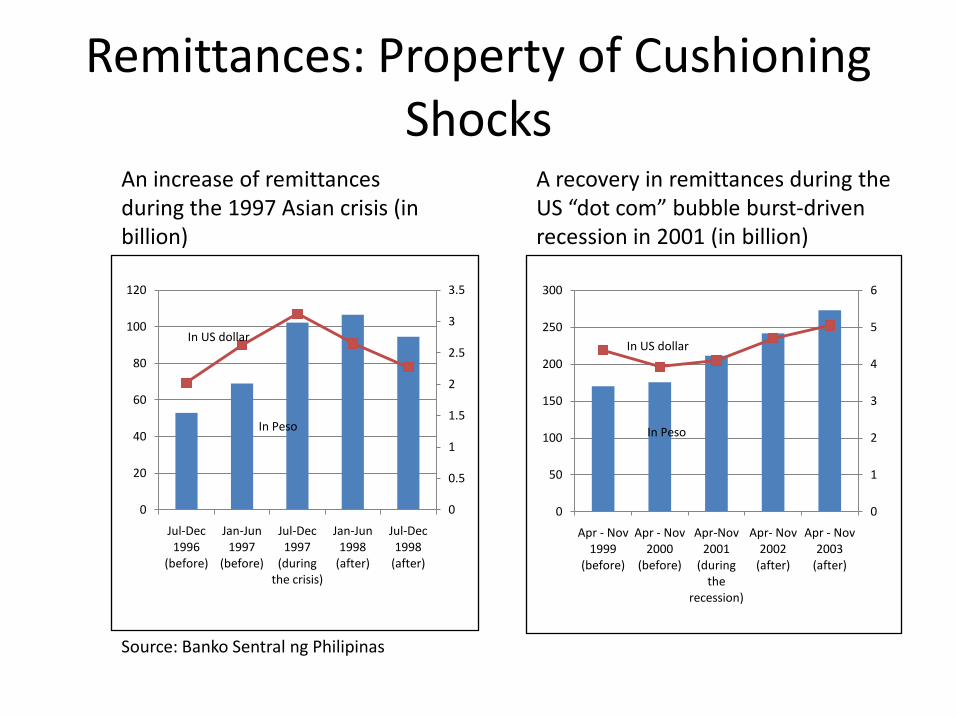

Remittances: Property of Cushioning Shocks

In Peso

In US dollar

0

0.5

1

1.5

2

2.5

3

3.5

0

20

40

60

80

100

120

Jul-Dec 1996

(before)

Jan-Jun 1997

(before)

Jul-Dec 1997

(during the crisis)

Jan-Jun 1998

(after)

Jul-Dec 1998

(after)

In Peso

In US dollar

0

1

2

3

4

5

6

0

50

100

150

200

250

300

Apr - Nov 1999

(before)

Apr - Nov 2000

(before)

Apr-Nov 2001

(during the

recession)

Apr- Nov 2002

(after)

Apr - Nov 2003

(after)

Source: Banko Sentral ng Philipinas

An increase of remittances during the 1997 Asian crisis (in billion)

A recovery in remittances during the US “dot com” bubble burst-driven recession in 2001 (in billion)

Roadmap

• Pattern of Services Exports• Which services sector has performed well in

exporting and which one has lagged?• What are the characteristics of the sectors

with relatively strong or weak performance?– BPO vs Tourism

• What strategies, fundamentals, and policies contributed to, or failed to, boost exports? – BPO vs Tourism

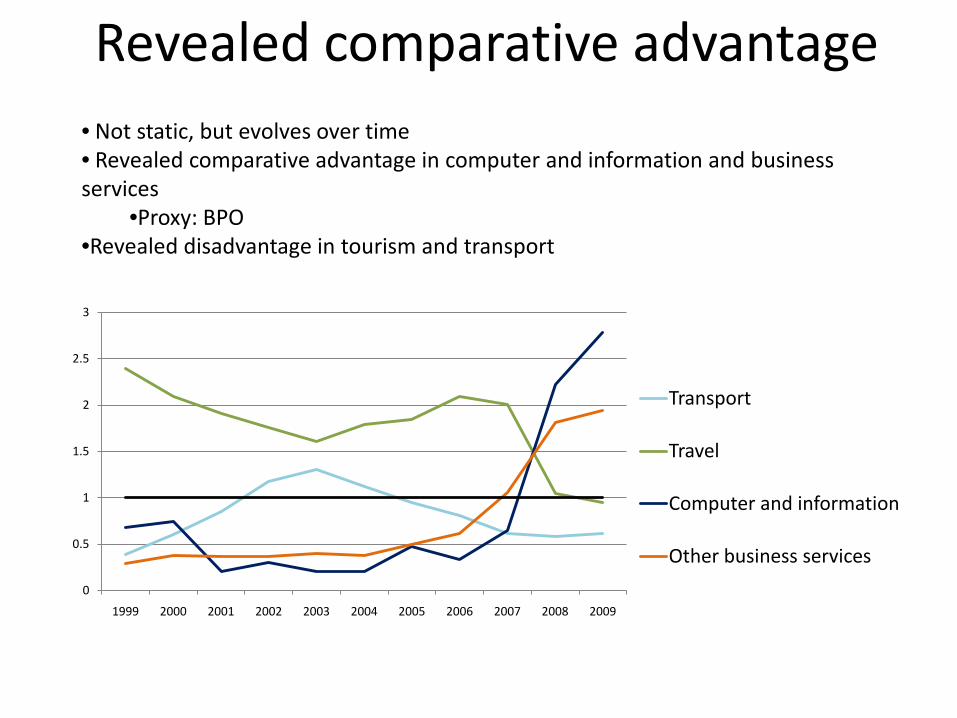

Revealed comparative advantage• Not static, but evolves over time• Revealed comparative advantage in computer and information and business services

•Proxy: BPO•Revealed disadvantage in tourism and transport

0

0.5

1

1.5

2

2.5

3

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Transport

Travel

Computer and information

Other business services

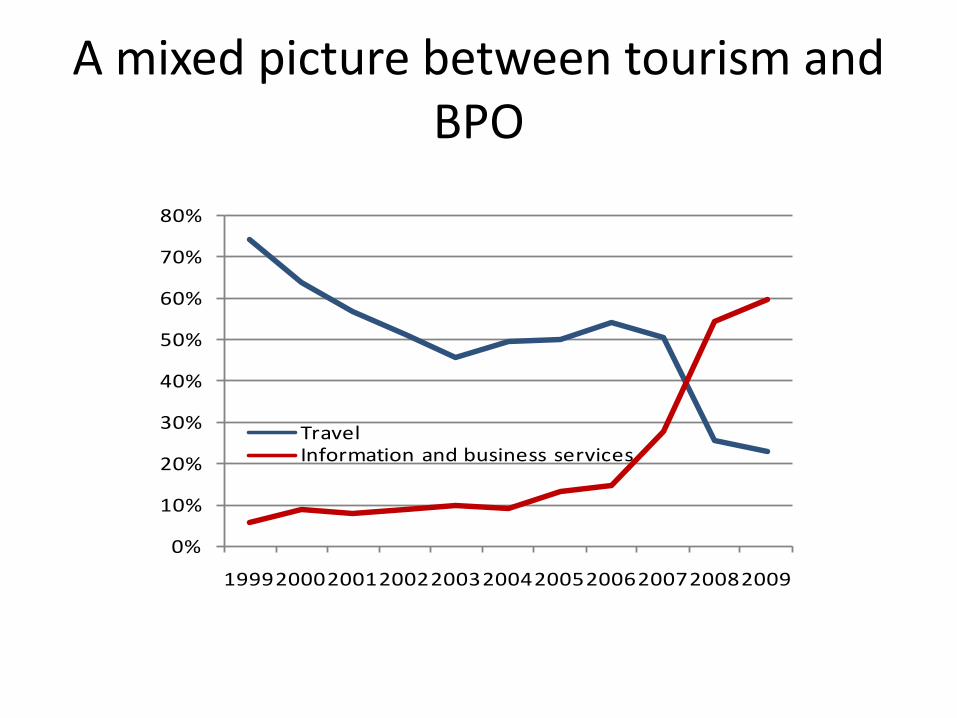

A mixed picture between tourism and BPO

0%

10%

20%

30%

40%

50%

60%

70%

80%

19992000200120022003200420052006200720082009

TravelInformation and business services

Roadmap

• Pattern of Services Exports• Which services sector has performed well in

exporting and which one has lagged?• What are the characteristics of the sector with

relatively strong performance?– BPO

• What strategies, fundamentals, and policies contributed to, or failed to, boost exports? – BPO vs Tourism

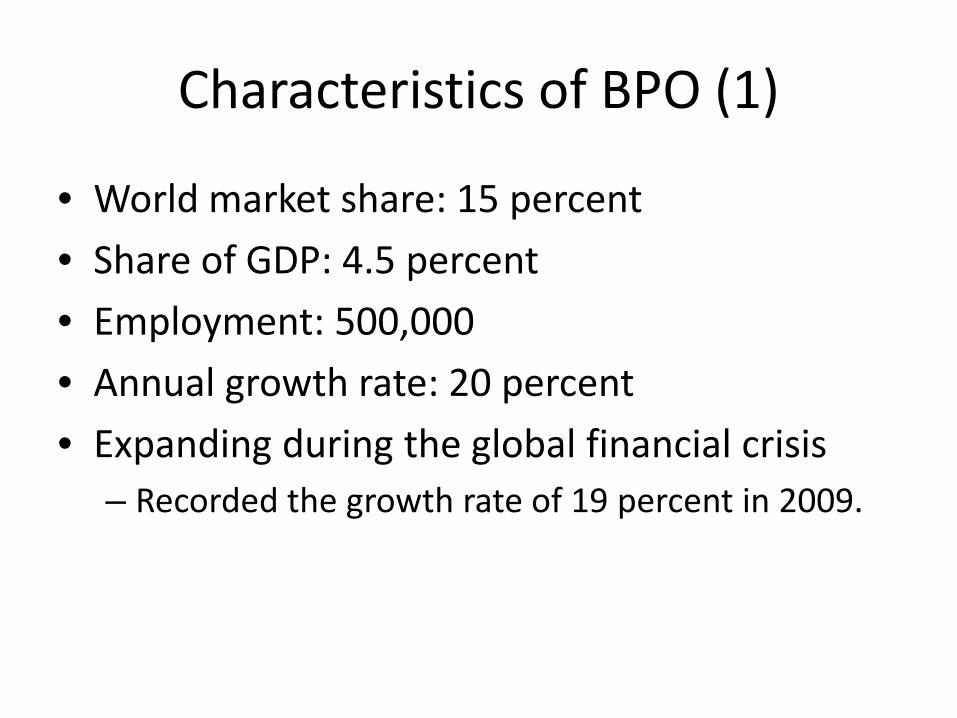

Characteristics of BPO (1)

• World market share: 15 percent

• Share of GDP: 4.5 percent

• Employment: 500,000

• Annual growth rate: 20 percent

• Expanding during the global financial crisis– Recorded the growth rate of 19 percent in 2009.

• Key subsector – Contact/call centers: 70 percent of the total BPO

output

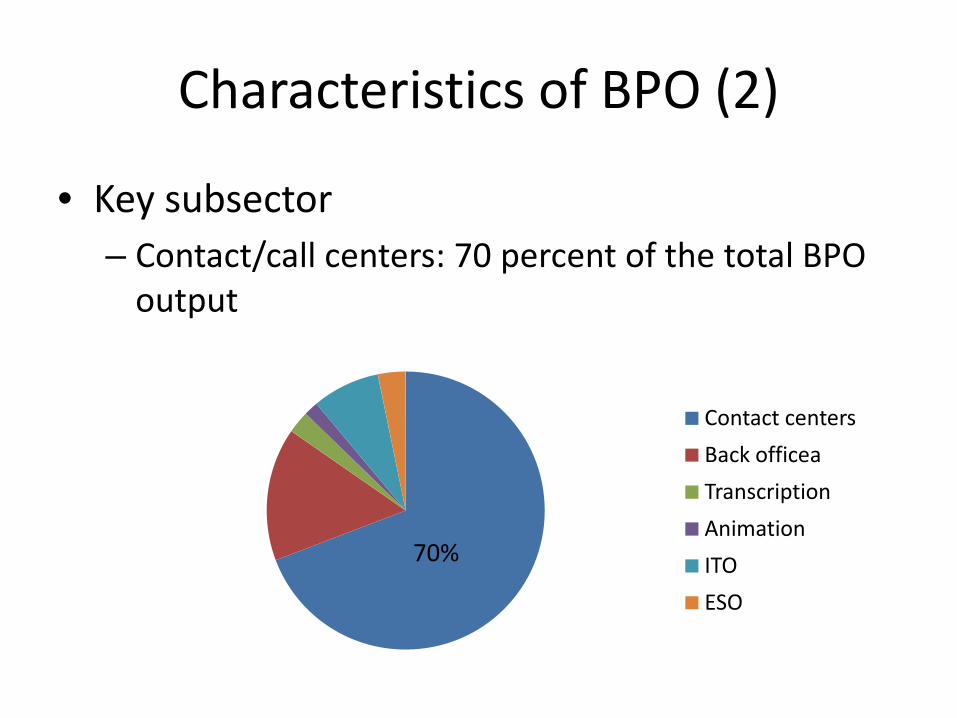

Characteristics of BPO (2)

70%

Contact centers

Back officea

Transcription

Animation

ITO

ESO

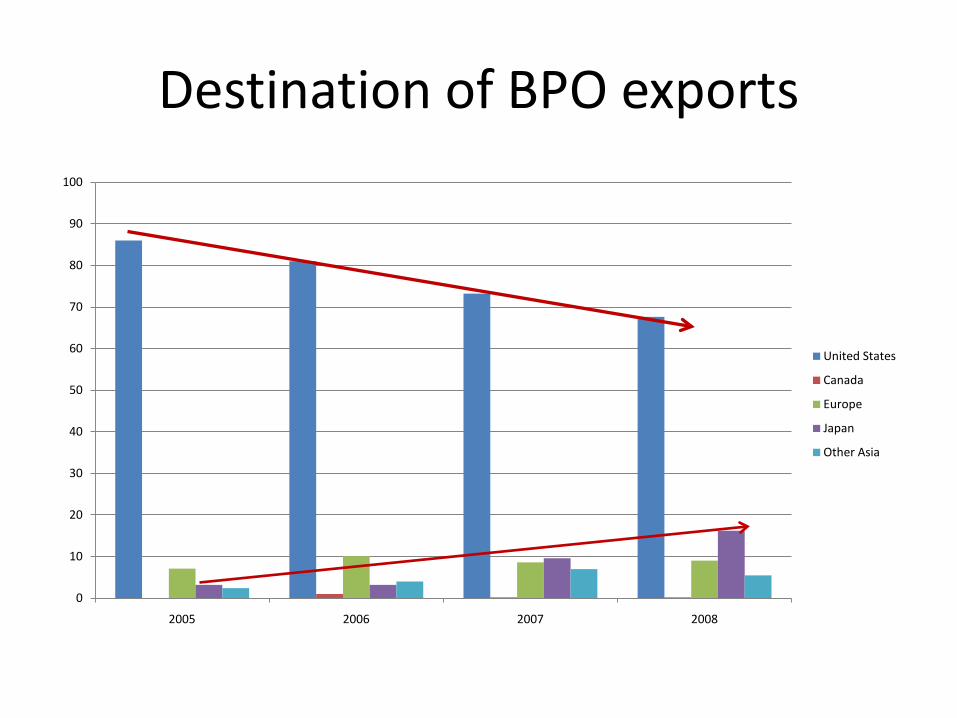

Destination of BPO exports

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008

United States

Canada

Europe

Japan

Other Asia

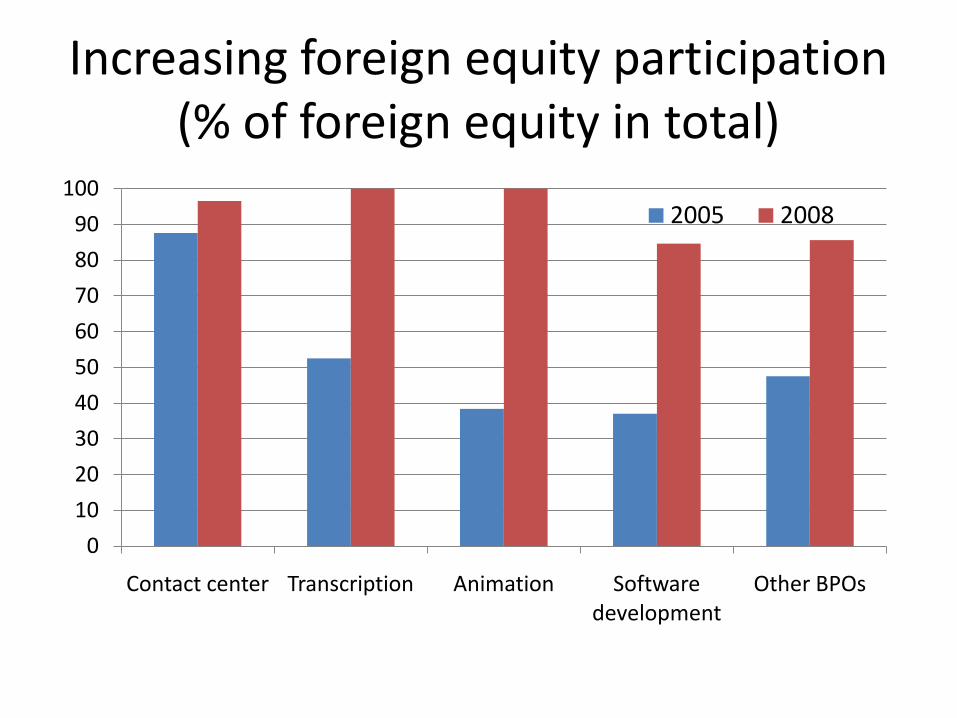

Increasing foreign equity participation(% of foreign equity in total)

0

10

20

30

40

50

60

70

80

90

100

Contact center Transcription Animation Software development

Other BPOs

2005 2008

Roadmap

• Pattern of Services Exports• Which services sector has performed well in

exporting and which one has lagged?• What are the characteristics of the sectors

with relatively strong or weak performance?– BPO vs Tourism

• What strategies, fundamentals, and policies contributed to boost exports? – BPO

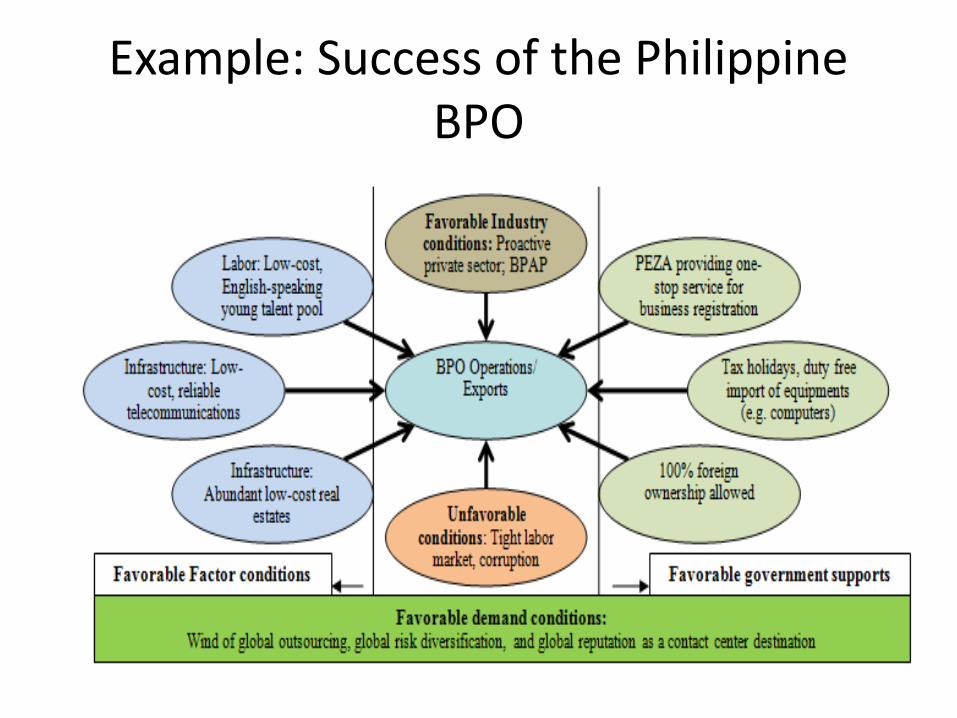

Example: Success of the Philippine BPO

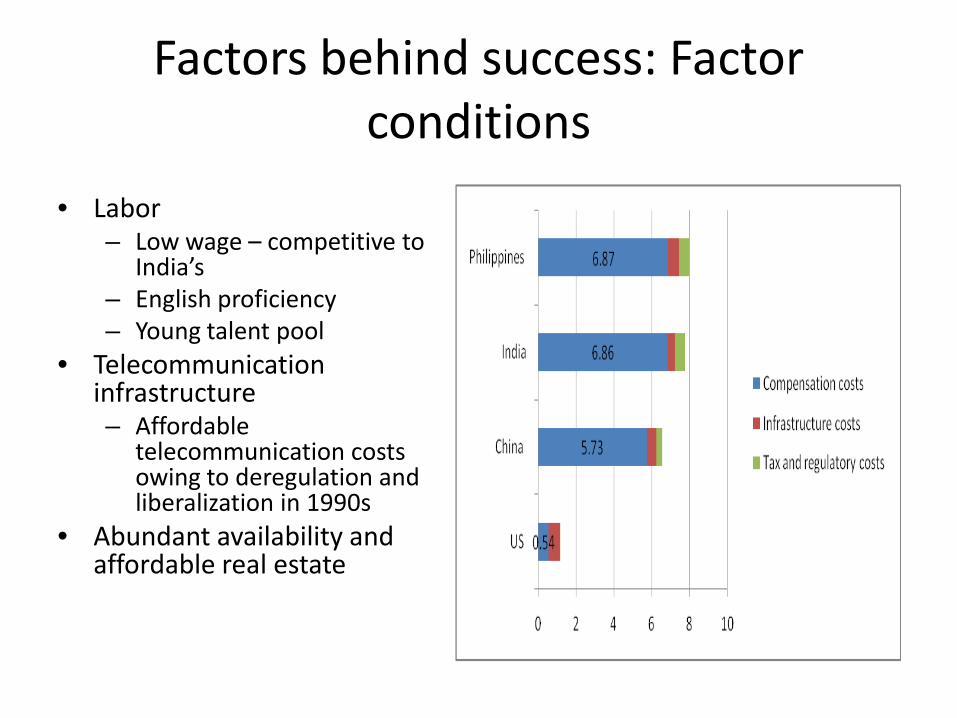

Factors behind success: Factor conditions

• Labor – Low wage – competitive to

India’s– English proficiency– Young talent pool

• Telecommunication infrastructure– Affordable

telecommunication costs owing to deregulation and liberalization in 1990s

• Abundant availability and affordable real estate

Factors behind success: Government’s support

• Tax incentives

• Foreign ownership allowed to 100 percent.

• PEZA has lowered the minimum space requirements to be declared as a PEZA IT park or building

• PEZA creates a more business-conducive environment

Proactive private sector

• Adopted an early strategic plan led by industry players

• BPAP, the umbrella BPO organization, plays a leading role in supporting and promoting the BPO industry– Prepared the blueprint, Roadmap 2010

• Setting out goals and specific action items to obtain success– In 2009, produced the “Next Wave Cities” scorecard

• Providing tools to help both investors and local governments assess readiness and develop working capacities.

– Prepared another blueprint, Roadmap 2016.

Roadmap

• Pattern of Services Exports• Which services sector has performed well in

exporting and which one has lagged?• What are the characteristics of the sector with

relatively weak performance?– Tourism

• What strategies, fundamentals, and policies contributed to, or failed to, boost exports? – BPO vs Tourism

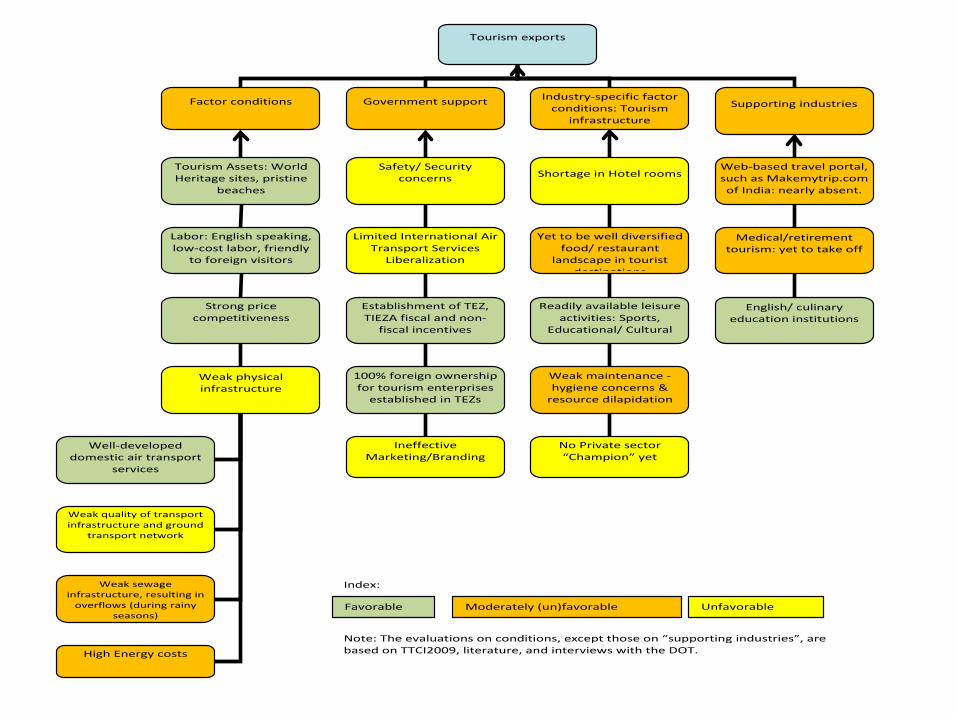

Tourism exports

Factor conditions Government support

Tourism Assets: World Heritage sites, pristine

beaches

Labor: English speaking, low-cost labor, friendly

to foreign visitors

Strong price competitiveness

Industry-specific factor conditions: Tourism

infrastructure

Weak physical infrastructure

Well-developed domestic air transport

services

Weak quality of transport infrastructure and ground

transport network

Weak sewage infrastructure, resulting in

overflows (during rainy seasons)

High Energy costs

Safety/ Security concerns

Limited International Air Transport Services

Liberalization

Establishment of TEZ, TIEZA fiscal and non-

fiscal incentives

Ineffective Marketing/Branding

Shortage in Hotel rooms

Yet to be well diversified food/ restaurant

landscape in tourist destinations

Readily available leisure

activities: Sports, Educational/ Cultural

Weak maintenance -hygiene concerns &

resource dilapidation

No Private sector “Champion” yet

Supporting industries

Web-based travel portal, such as Makemytrip.com of India: nearly absent.

Medical/retirement tourism: yet to take off

English/ culinary education institutions

100% foreign ownership for tourism enterprises

established in TEZs

Favorable Moderately (un)favorable Unfavorable

Index:

Note: The evaluations on conditions, except those on “supporting industries”, are based on TTCI2009, literature, and interviews with the DOT.

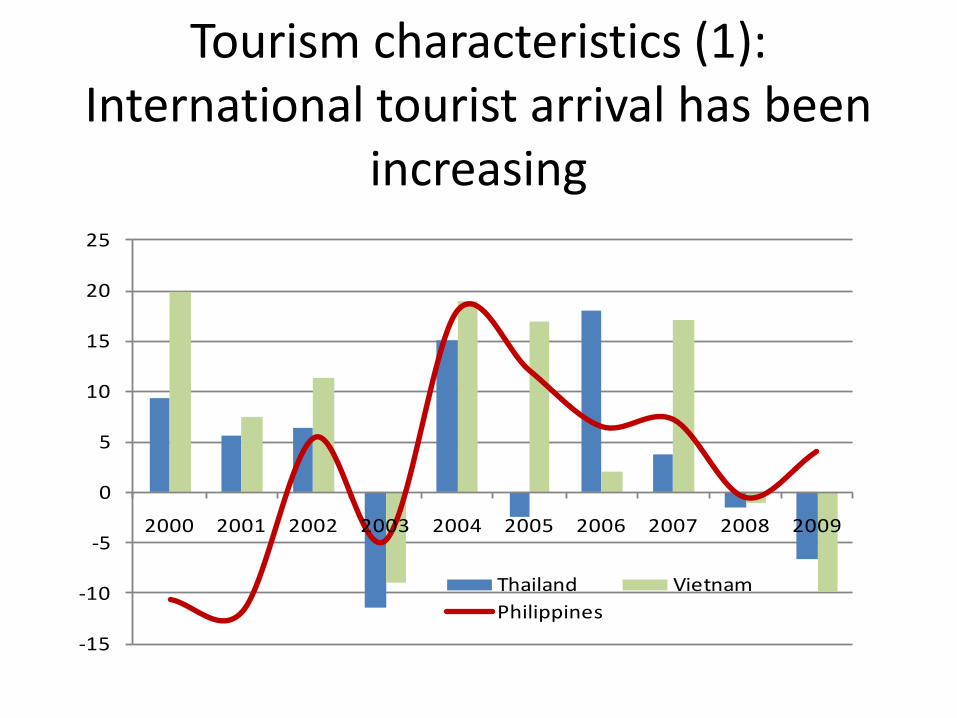

Tourism characteristics (1): International tourist arrival has been

increasing

-15

-10

-5

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Thailand VietnamPhilippines

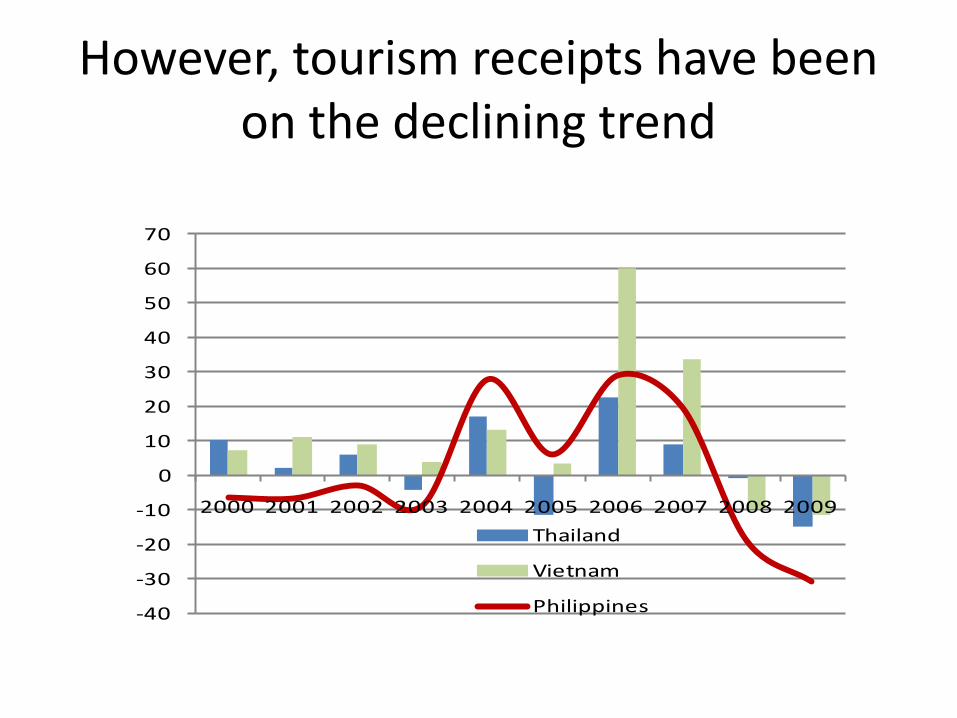

However, tourism receipts have been on the declining trend

-40

-30

-20

-10

0

10

20

30

40

50

60

70

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Thailand

Vietnam

Philippines

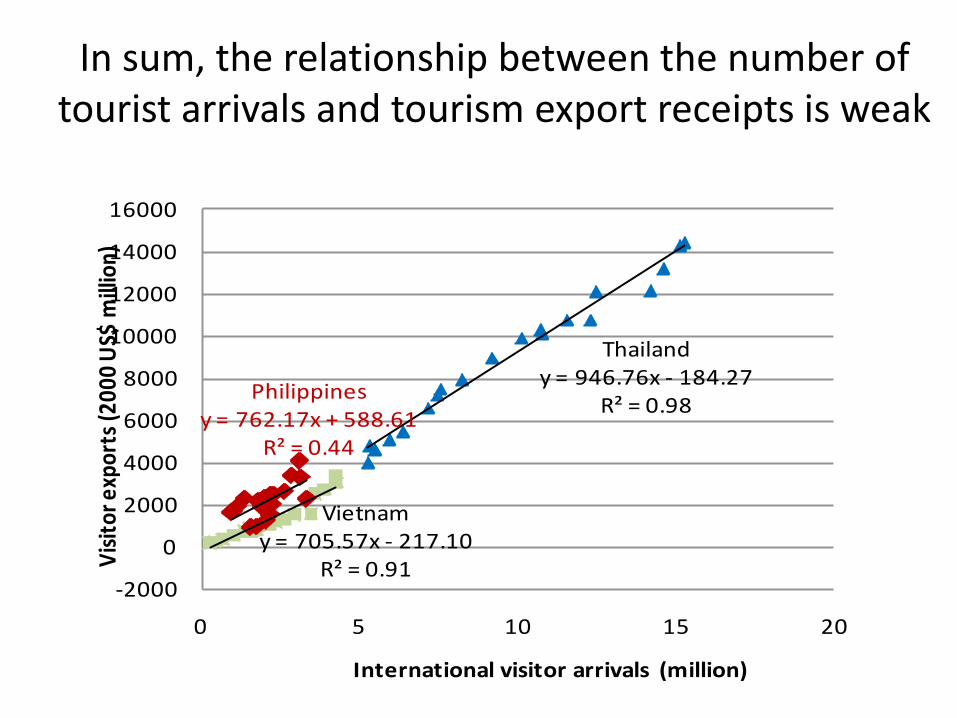

In sum, the relationship between the number of tourist arrivals and tourism export receipts is weak

Thailandy = 946.76x - 184.27

R² = 0.98

Vietnamy = 705.57x - 217.10

R² = 0.91

Philippines y = 762.17x + 588.61

R² = 0.44

-2000

0

2000

4000

6000

8000

10000

12000

14000

16000

0 5 10 15 20

Visit

or e

xpor

ts (2

000

US$

mill

ion)

International visitor arrivals (million)

Roadmap

• Pattern of Services Exports• Which services sector has performed well in

exporting and which one has lagged?• What are the characteristics of the sector with

relatively strong or weak performance?– BPO vs Tourism

• What strategies, fundamentals, and policies failed to boost exports? – Tourism

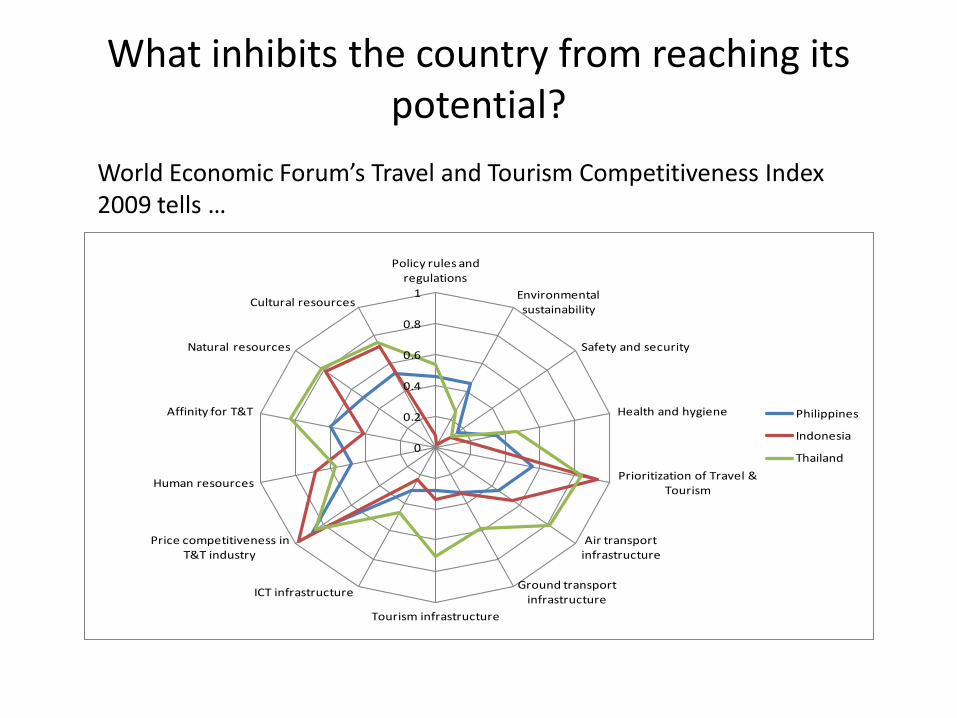

What inhibits the country from reaching its potential?

0

0.2

0.4

0.6

0.8

1

Policy rules and regulations

Environmental sustainability

Safety and security

Health and hygiene

Prioritization of Travel & Tourism

Air transport infrastructure

Ground transport infrastructure

Tourism infrastructure

ICT infrastructure

Price competitiveness in T&T industry

Human resources

Affinity for T&T

Natural resources

Cultural resources

Philippines

Indonesia

Thailand

World Economic Forum’s Travel and Tourism Competitiveness Index 2009 tells …

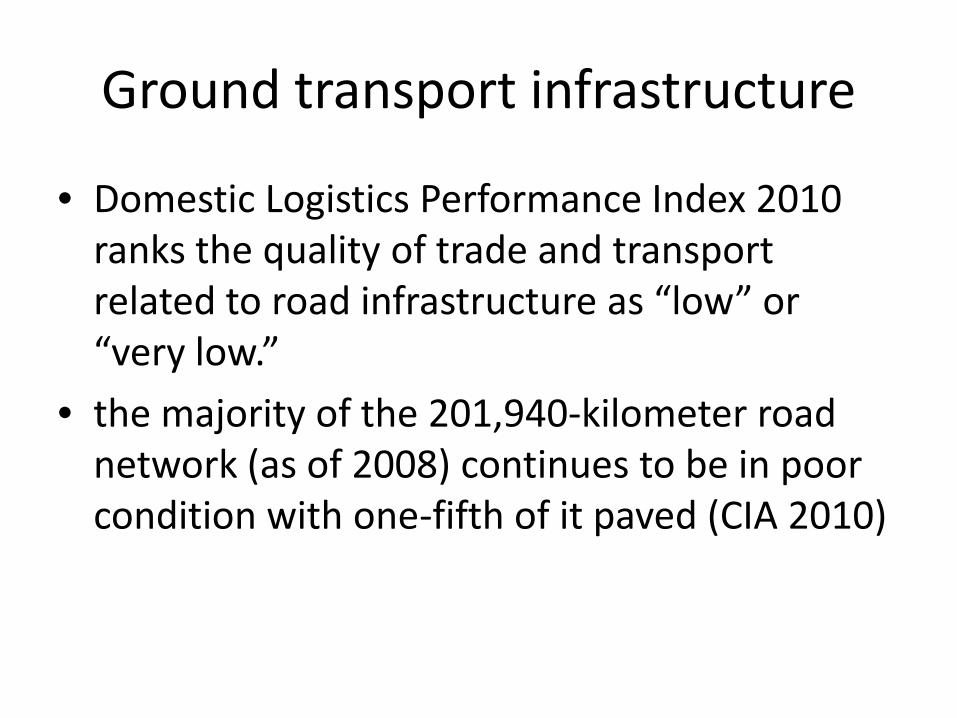

Ground transport infrastructure

• Domestic Logistics Performance Index 2010 ranks the quality of trade and transport related to road infrastructure as “low” or “very low.”

• the majority of the 201,940-kilometer road network (as of 2008) continues to be in poor condition with one-fifth of it paved (CIA 2010)

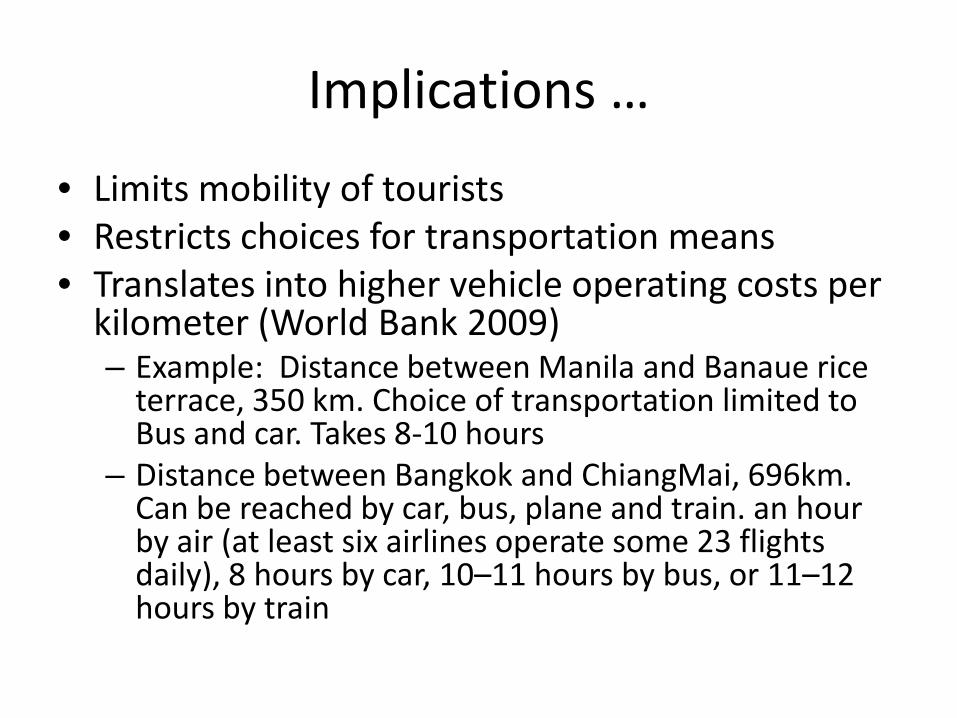

Implications …

• Limits mobility of tourists• Restricts choices for transportation means• Translates into higher vehicle operating costs per

kilometer (World Bank 2009) – Example: Distance between Manila and Banaue rice

terrace, 350 km. Choice of transportation limited to Bus and car. Takes 8-10 hours

– Distance between Bangkok and ChiangMai, 696km. Can be reached by car, bus, plane and train. an hour by air (at least six airlines operate some 23 flights daily), 8 hours by car, 10–11 hours by bus, or 11–12 hours by train

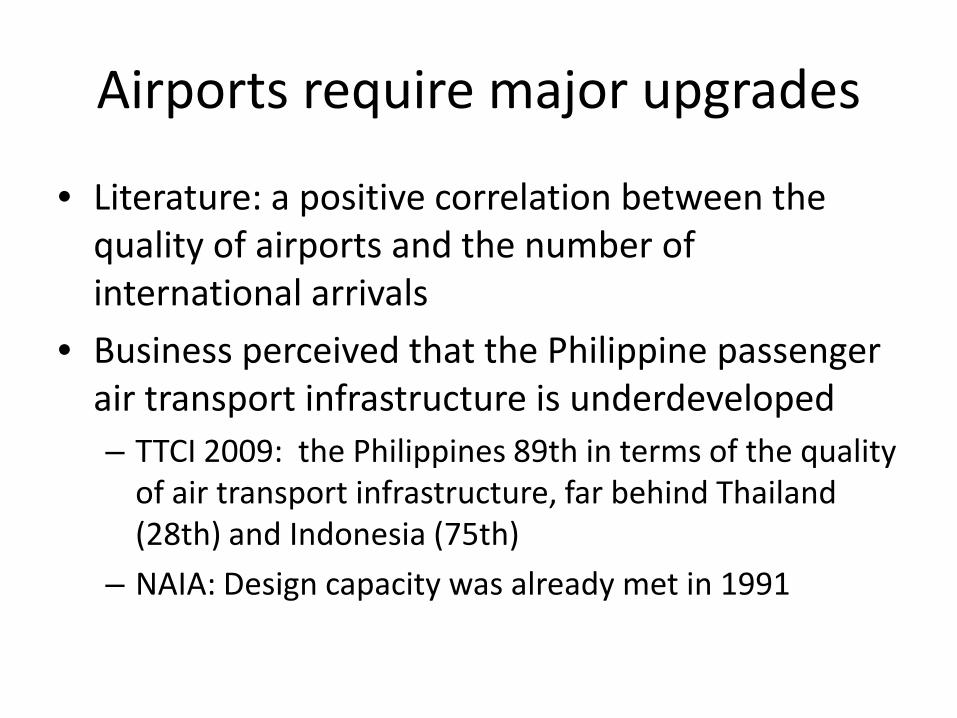

Airports require major upgrades

• Literature: a positive correlation between the quality of airports and the number of international arrivals

• Business perceived that the Philippine passenger air transport infrastructure is underdeveloped– TTCI 2009: the Philippines 89th in terms of the quality

of air transport infrastructure, far behind Thailand (28th) and Indonesia (75th)

– NAIA: Design capacity was already met in 1991

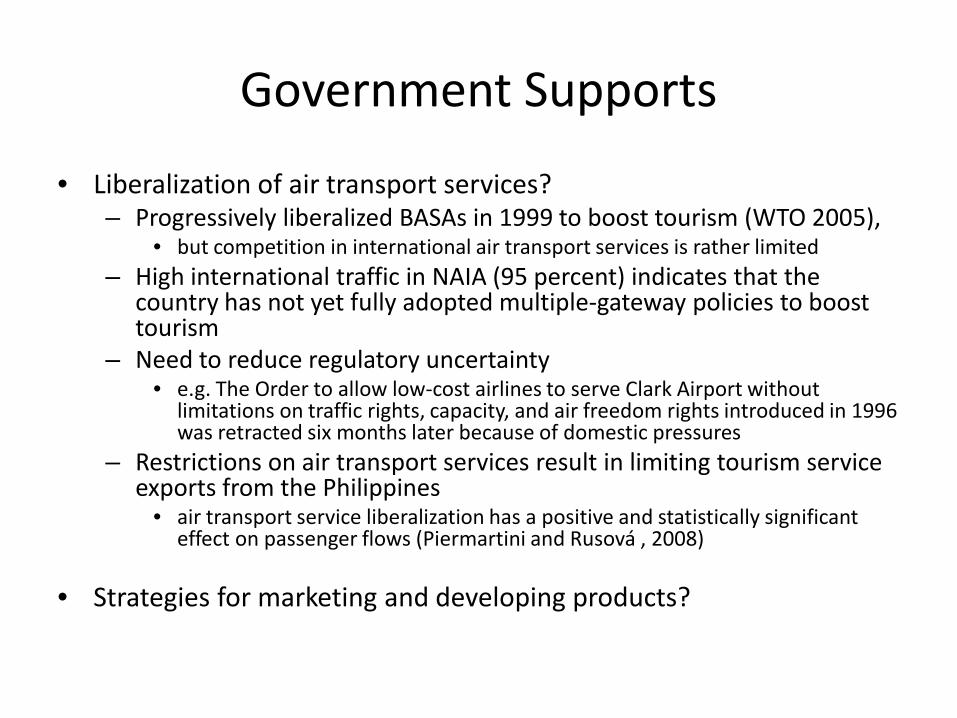

Government Supports

• Liberalization of air transport services? – Progressively liberalized BASAs in 1999 to boost tourism (WTO 2005),

• but competition in international air transport services is rather limited– High international traffic in NAIA (95 percent) indicates that the

country has not yet fully adopted multiple-gateway policies to boost tourism

– Need to reduce regulatory uncertainty• e.g. The Order to allow low-cost airlines to serve Clark Airport without

limitations on traffic rights, capacity, and air freedom rights introduced in 1996 was retracted six months later because of domestic pressures

– Restrictions on air transport services result in limiting tourism service exports from the Philippines

• air transport service liberalization has a positive and statistically significant effect on passenger flows (Piermartini and Rusová , 2008)

• Strategies for marketing and developing products?

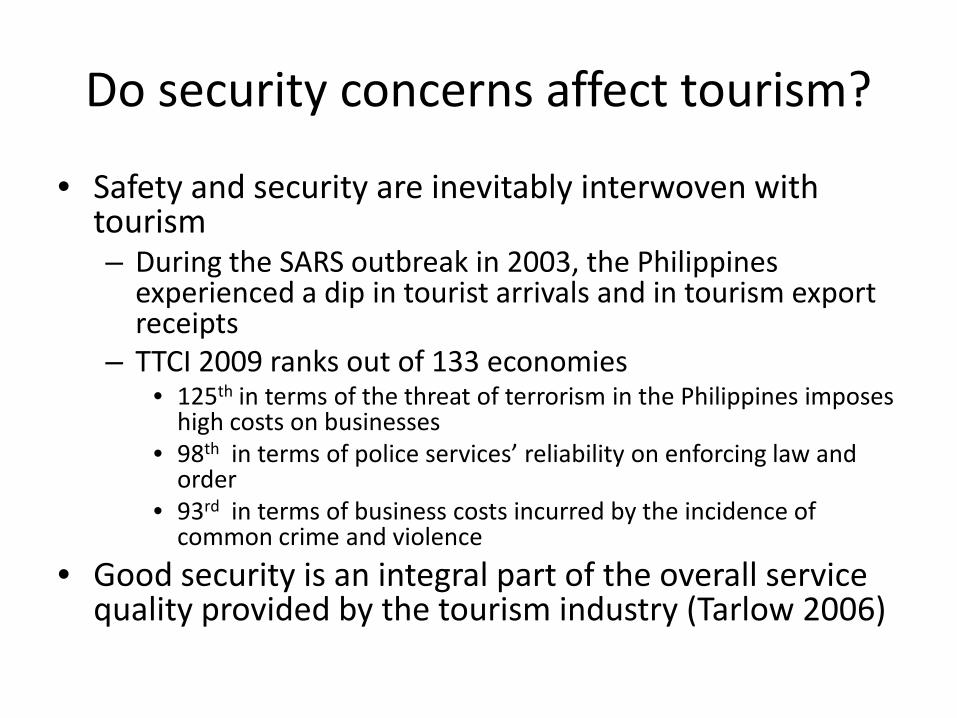

Do security concerns affect tourism?

• Safety and security are inevitably interwoven with tourism– During the SARS outbreak in 2003, the Philippines

experienced a dip in tourist arrivals and in tourism export receipts

– TTCI 2009 ranks out of 133 economies• 125th in terms of the threat of terrorism in the Philippines imposes

high costs on businesses • 98th in terms of police services’ reliability on enforcing law and

order • 93rd in terms of business costs incurred by the incidence of

common crime and violence

• Good security is an integral part of the overall service quality provided by the tourism industry (Tarlow 2006)

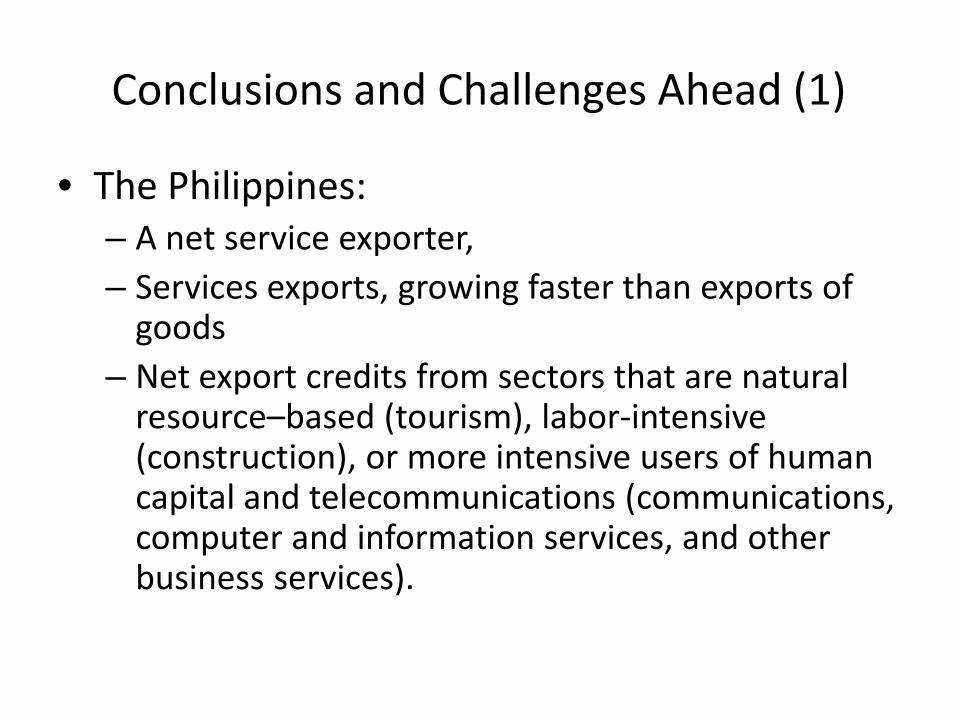

Conclusions and Challenges Ahead (1)

• The Philippines:– A net service exporter, – Services exports, growing faster than exports of

goods– Net export credits from sectors that are natural

resource–based (tourism), labor-intensive (construction), or more intensive users of human capital and telecommunications (communications, computer and information services, and other business services).

• BPO – How to shift the gear to high value-added sub-sector?– Comprehensive data protection law in place?– Quality control, especially in the area of medical

transcription?

• Tourism– PPP in infrastructure– More conducive business environment– Proactive private sector’s role in developing tourism

products

Conclusions and Challenges Ahead (2)