Embed Size (px)

Citation preview

Extensions to Consumer theory

Inter-temporal choiceUncertainty

Revealed preferences

Extensions to Consumer theory

We now know how a consumer chooses the most satisfying bundle out of the ones it can afford From observing changes in choice that follow

changes in price, we can derive the demand function.

But how useful (and realistic) is this theory? We assumed that agents have no savings... Does the theory still stand under uncertainty ? We assume that stable preferences just “exist”.

Extensions to Consumer theory

Inter-temporal choice

Uncertainty

Revealed preferences

Inter-temporal choice

The typical agents spreads his consumption over several periods of time: immediate consumption, savings, borrowing, etc.

Consume today / consume tomorrow Current preferences between goods are convex. Seems this is also the case for inter-temporal choices

We need to define : Inter-temporal preferences Inter-temporal budget constraint

Inter-temporal preferences

Preference for current consumption A unit of consumption today is “worth” more than a

unit of consumption tomorrow I’d rather receive 100 € today than 100 € next week !

If I give up some current consumption , I expect to receive a return (r) in compensation.

There must exist a value of (r), a psychological interest rate, for which I am indifferent between current and future consumption Would you rather receive 100 € today or 101 € next

week ? What about 120 € ?

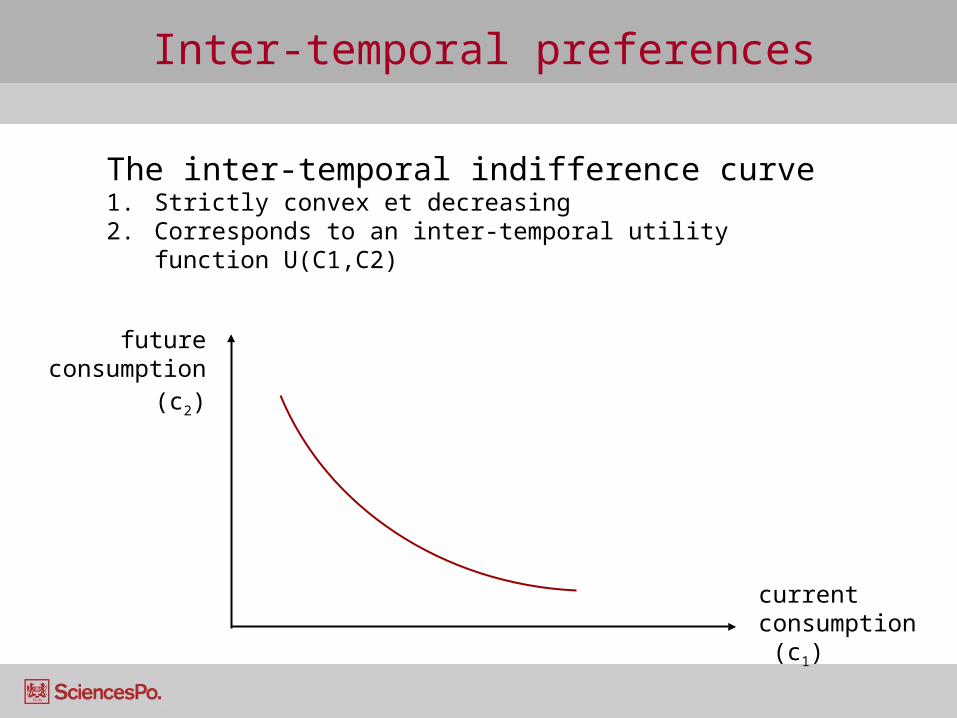

Inter-temporal preferences

future consumption

(c2)

current consumption (c1)

The inter-temporal indifference curve1. Strictly convex et decreasing 2. Corresponds to an inter-temporal utility function

U(C1,C2)

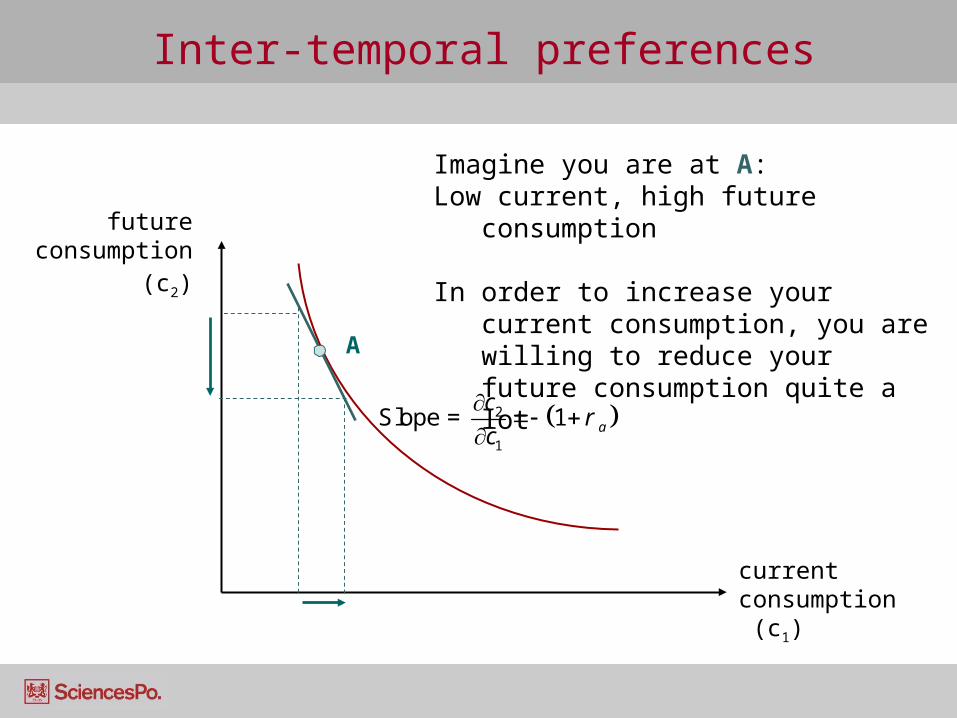

Inter-temporal preferences

A

2

1

1 a

cr

c

Slope =

Imagine you are at A:Low current, high future

consumption

In order to increase your current consumption, you are willing to reduce your future consumption quite a lot

future consumption

(c2)

current consumption (c1)

Inter-temporal preferences

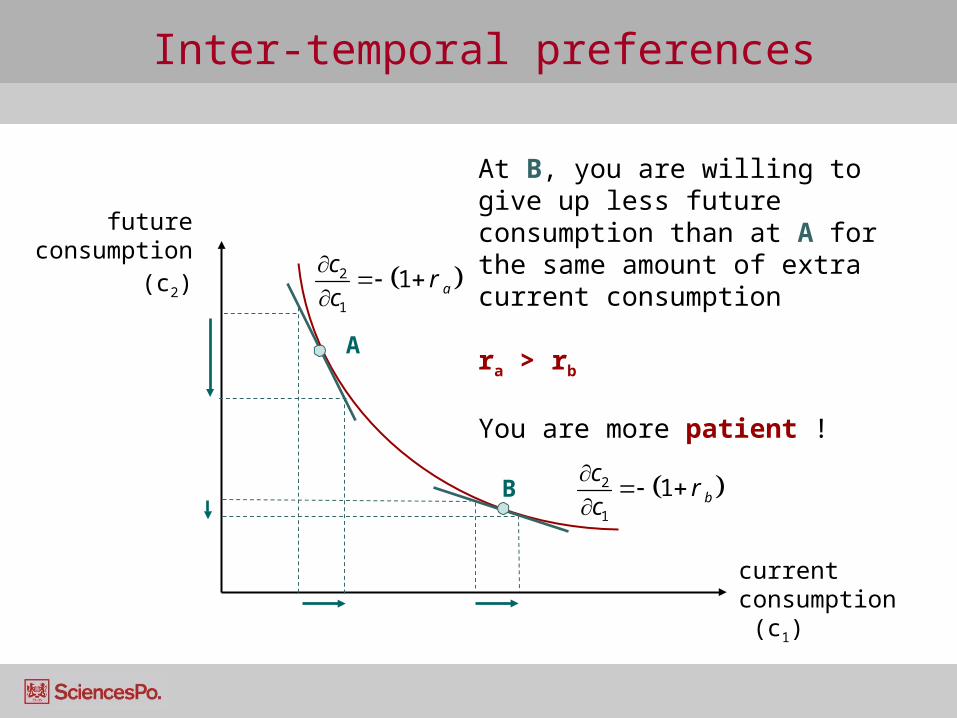

A

At B, you are willing to give up less future consumption than at A for the same amount of extra current consumption

ra > rb

You are more patient !

B

future consumption

(c2)

current consumption (c1)

2

1

1 b

cr

c

2

1

1 a

cr

c

Inter-temporal preferences

A

B

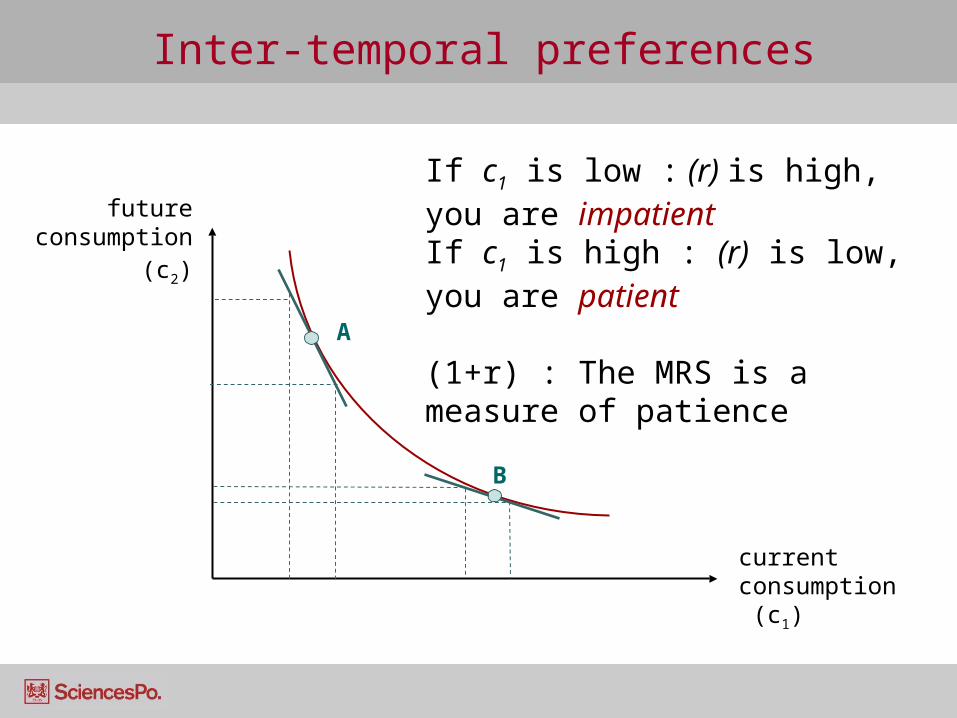

If c1 is low : (r) is high, you are impatientIf c1 is high : (r) is low, you are patient

(1+r) : The MRS is a measure of patience

future consumption

(c2)

current consumption (c1)

Inter-temporal budget constraint

Let’s see what happens if your savings earn interest over time.

A sum Mt invested in t is worth Mt+1=Mt×(1+i) after 1 year 01/08 : I invest 100 € 12/08 : I will receive 100 × (1+i) € If i = 0,05 (5%); Mt+1=100 × (1,05) =105 €

A invested sum Mt+1 was worth Mt=Mt+1(1+i) a year earlier 12/08 : I receive 525 € 01/08 : I invested 525 (1+i) € If i = 0,05 (5%); Mt = 525(1,05)= 500 €

Inter-temporal budget constraint

Simplification: invariable price p1 = p2 = 1 Explicit interest rate: i Consumption : c Budget : b Two periods : 1 and 2

Inter-temporal budget constraint

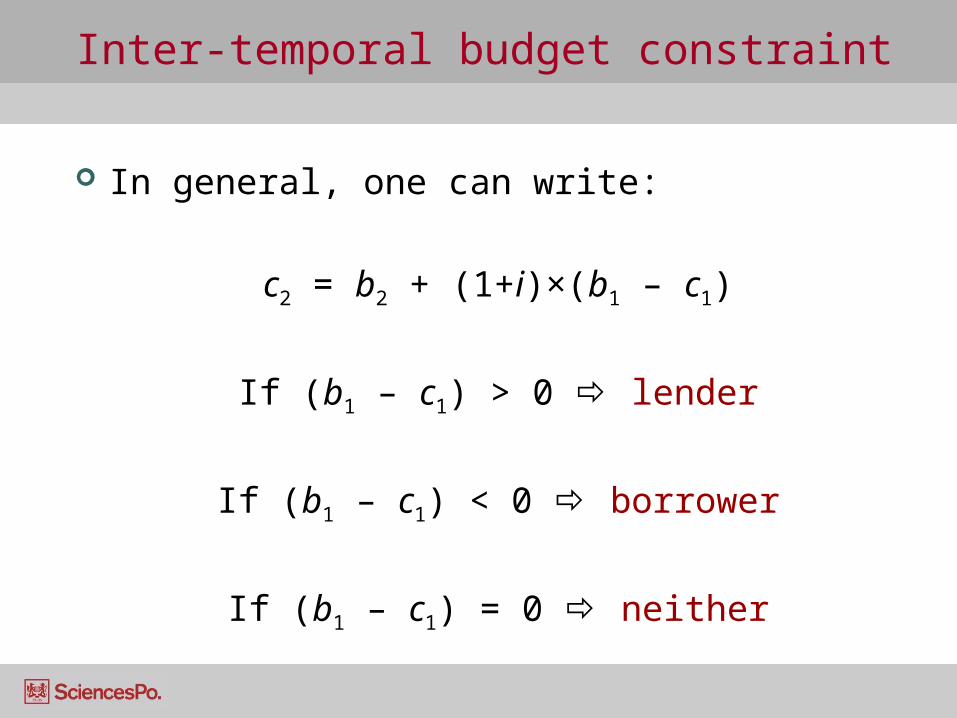

In general, one can write:

c2 = b2 + (1+i)×(b1 – c1)

If (b1 – c1) > 0 lender

If (b1 – c1) < 0 borrower

If (b1 – c1) = 0 neither

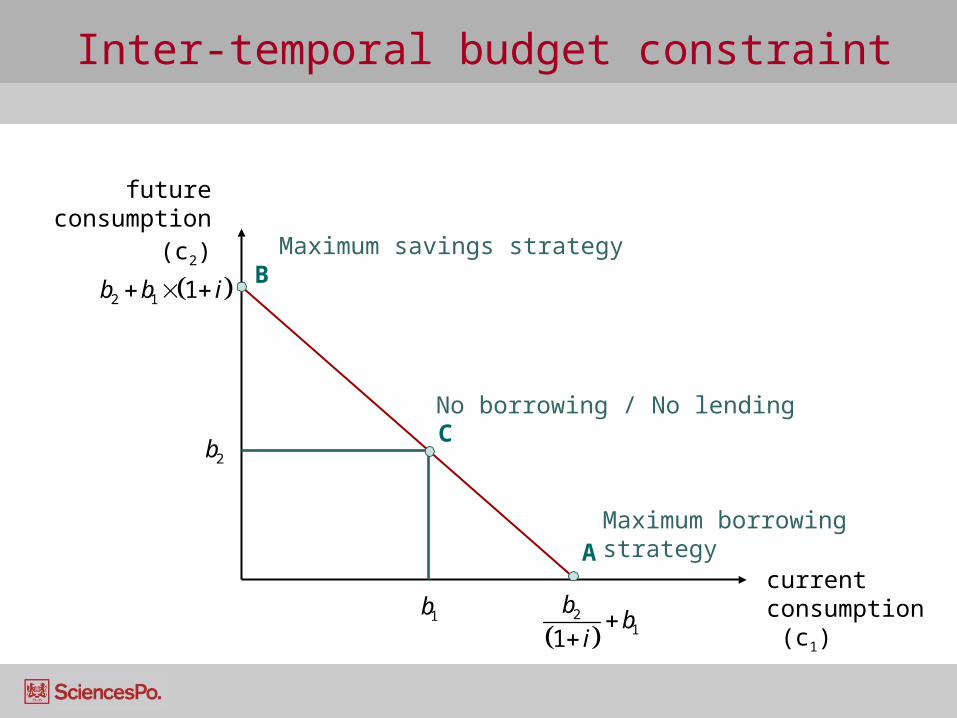

Inter-temporal budget constraint

Current Value Future value

B

C

21 (1 )

bb

i

21 (1 )

cc

i

1 2(1 )b i b

1 2(1 )c i c

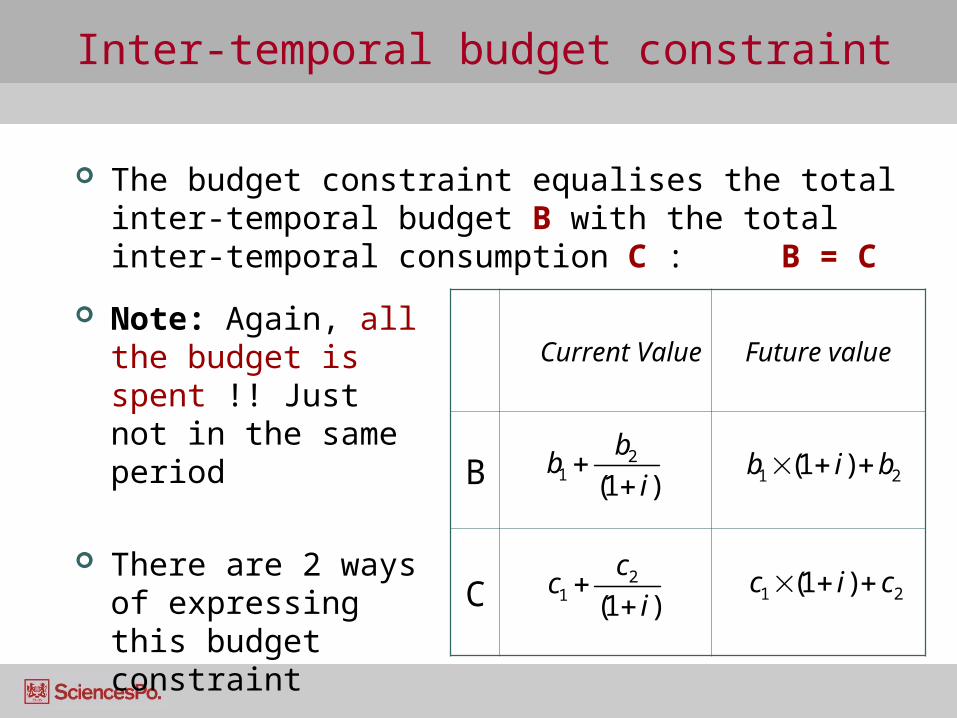

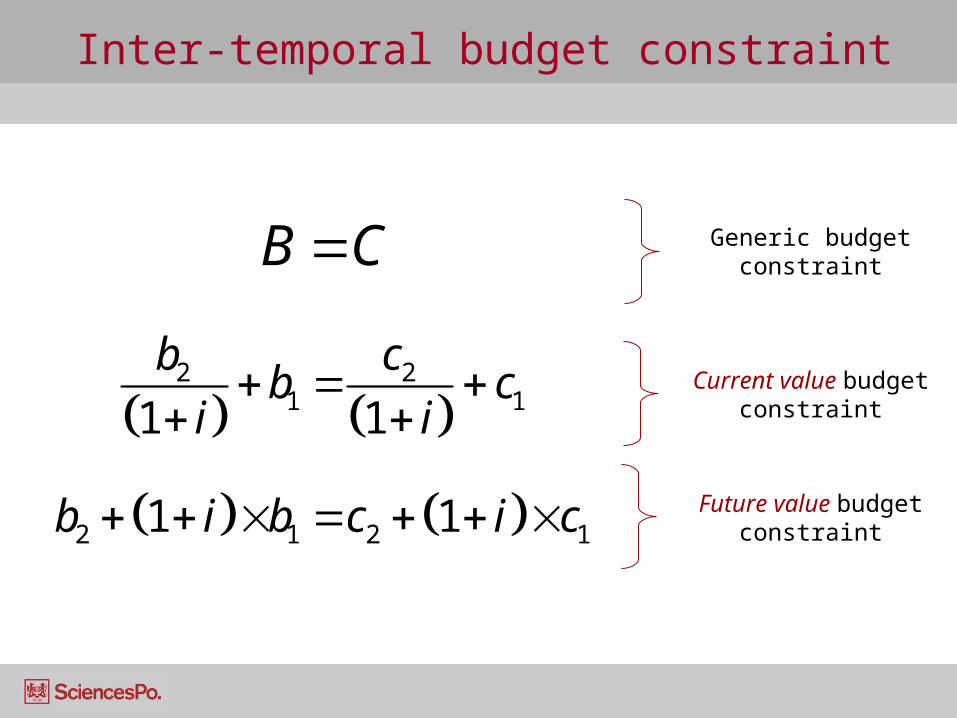

The budget constraint equalises the total inter-temporal budget B with the total inter-temporal consumption C : B = C

Note: Again, all the budget is spent !! Just not in the same period

There are 2 ways of expressing this budget constraint

Inter-temporal budget constraint

2 21 1

2 1 2 1

1 1

1 1

b cb c

i i

b i b c i c

Current value budget constraint

Future value budget constraint

Generic budget constraintB C

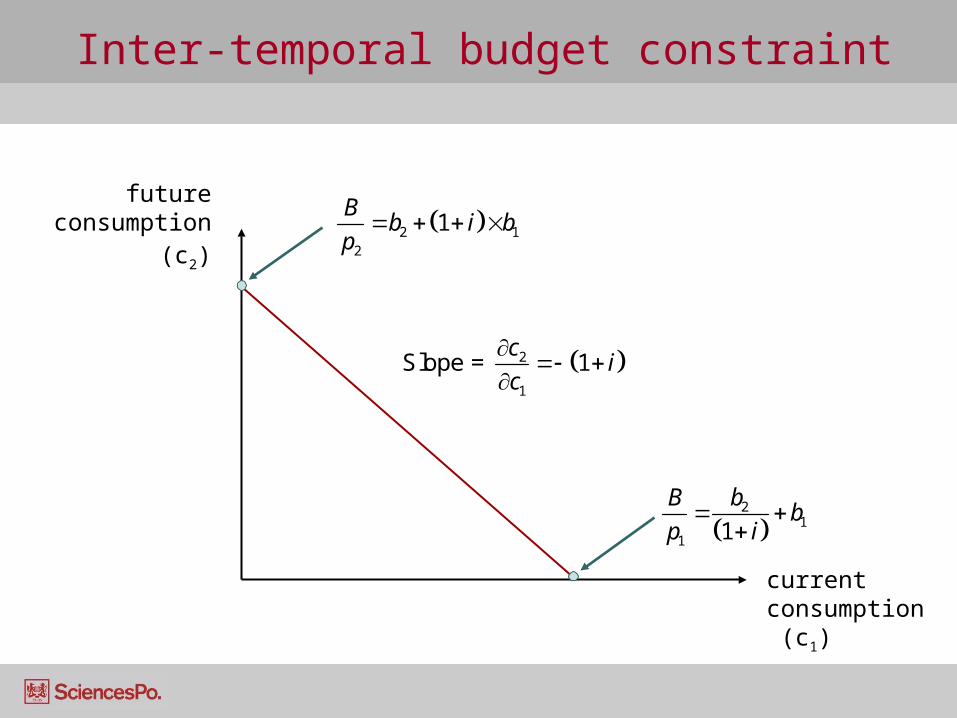

Inter-temporal budget constraint

2 12

1B

b i bp

2

11 1

bBb

p i

2

1

1c

ic

Slope =

future consumption

(c2)

current consumption (c1)

Inter-temporal budget constraint

2

11

bb

i

2 1 1b b i

A

B

1b

2bC

Maximum savings strategy

Maximum borrowing strategy

No borrowing / No lending

future consumption

(c2)

current consumption (c1)

Inter-temporal budget constraint

2

11

bb

i

2 1 1b b i

A

B

1b

2bC

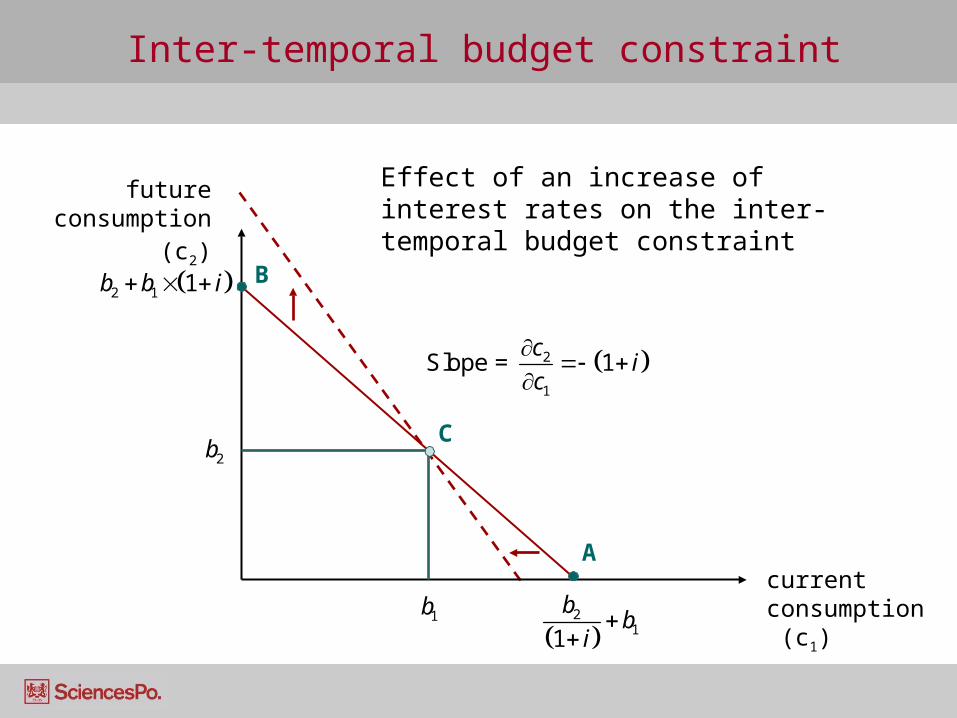

future consumption

(c2)

current consumption (c1)

Effect of an increase of interest rates on the inter-temporal budget constraint

2

1

1c

ic

Slope =

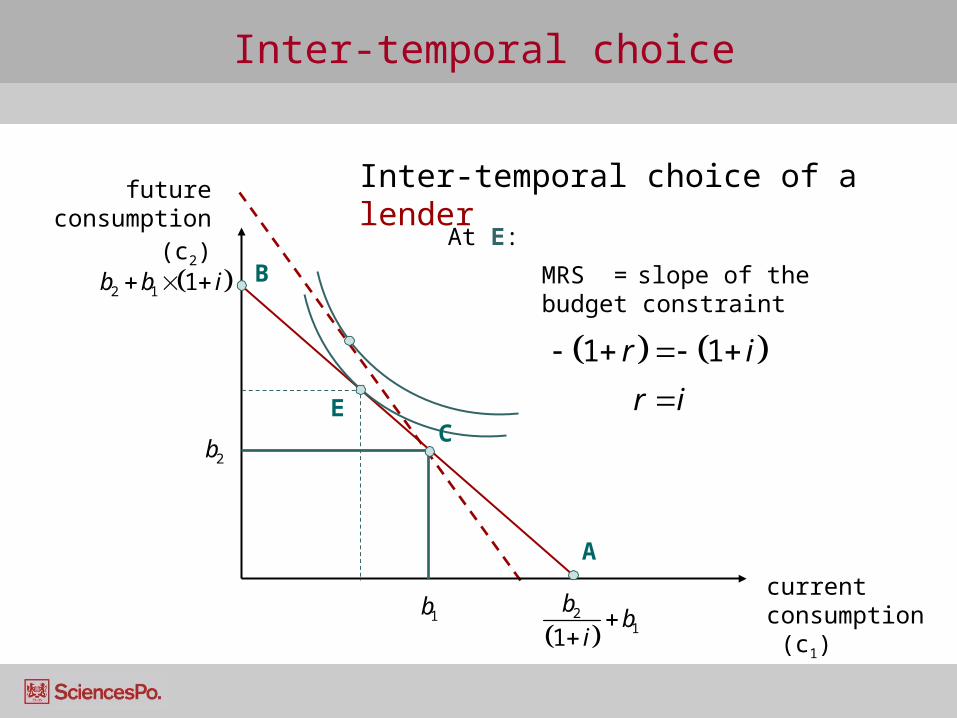

Inter-temporal choice

2

11

bb

i

2 1 1b b i

A

B

E

Inter-temporal choice of a lenderfuture consumption

(c2)

current consumption (c1)

1b

2bC

At E:

1 1r i

r i

MRS = slope of the budget constraint

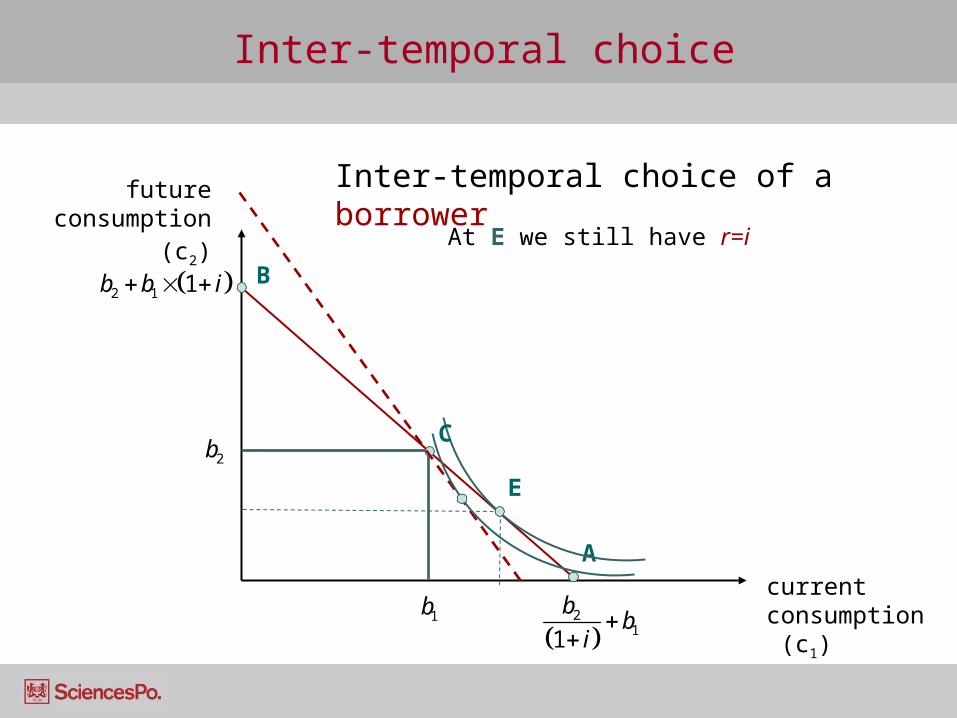

Inter-temporal choice

2

11

bb

i

2 1 1b b i

A

B

E

Inter-temporal choice of a borrower

1b

2bC

future consumption

(c2)

current consumption (c1)

At E we still have r=i

Extensions to Consumer theory

Inter-temporal choice

Uncertainty

Revealed preferences

Uncertainty

How do we calculate the utility of an agent when there is uncertainty about which bundle will be consumed?

Example: You’re trying to decide if you want to buy a raffle ticket. What determines the potential utility of buying this ticket? The amount of prizes and their value The amount on tickets on sale

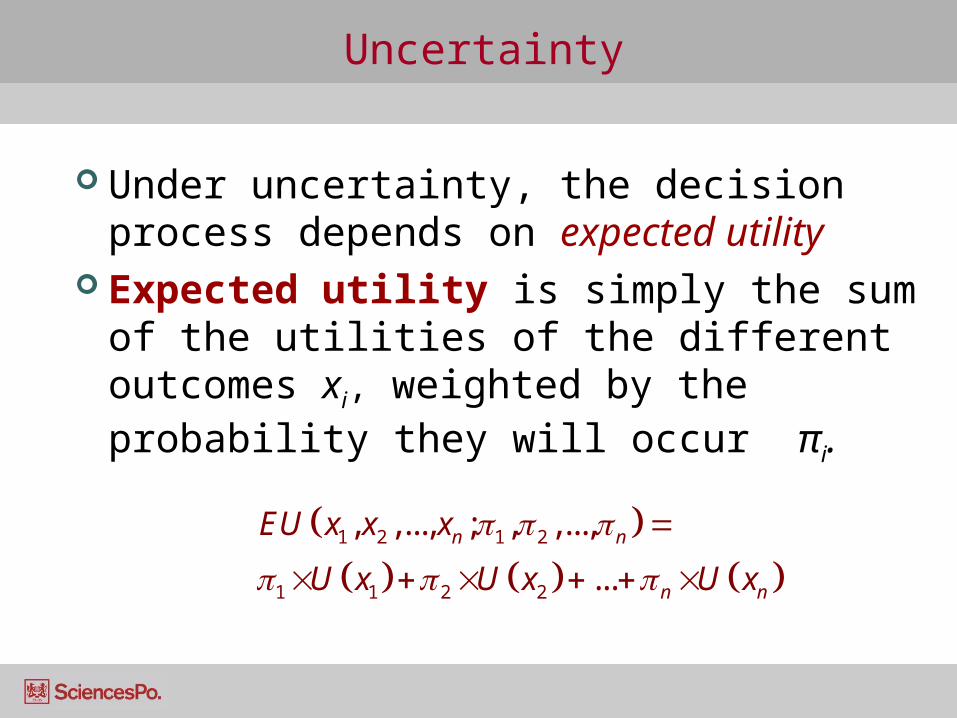

Uncertainty

Under uncertainty, the decision process depends on expected utility

Expected utility is simply the sum of the utilities of the different outcomes xi, weighted by the probability they will occur πi.

1 2 1 2

1 1 2 2

, ,..., ; , ,...,

...

n n

n n

EU x x x

U x U x U x

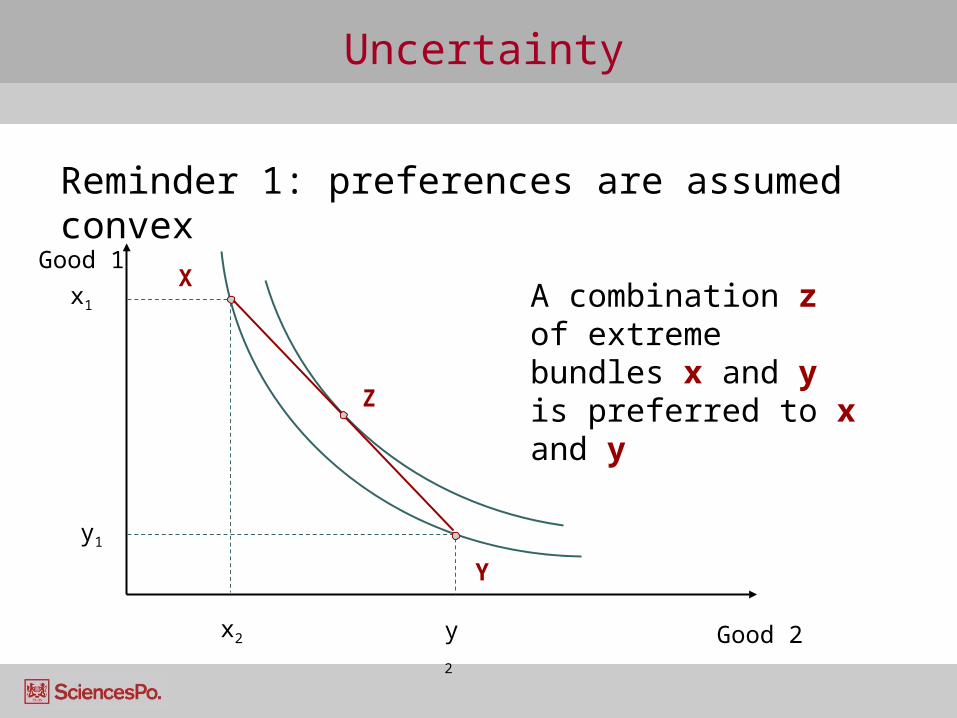

Uncertainty

Reminder 1: preferences are assumed convex

Good 1

Good 2

y1

y2

Y

x1

x2

XA combination z of extreme bundles x and y is preferred to x and yZ

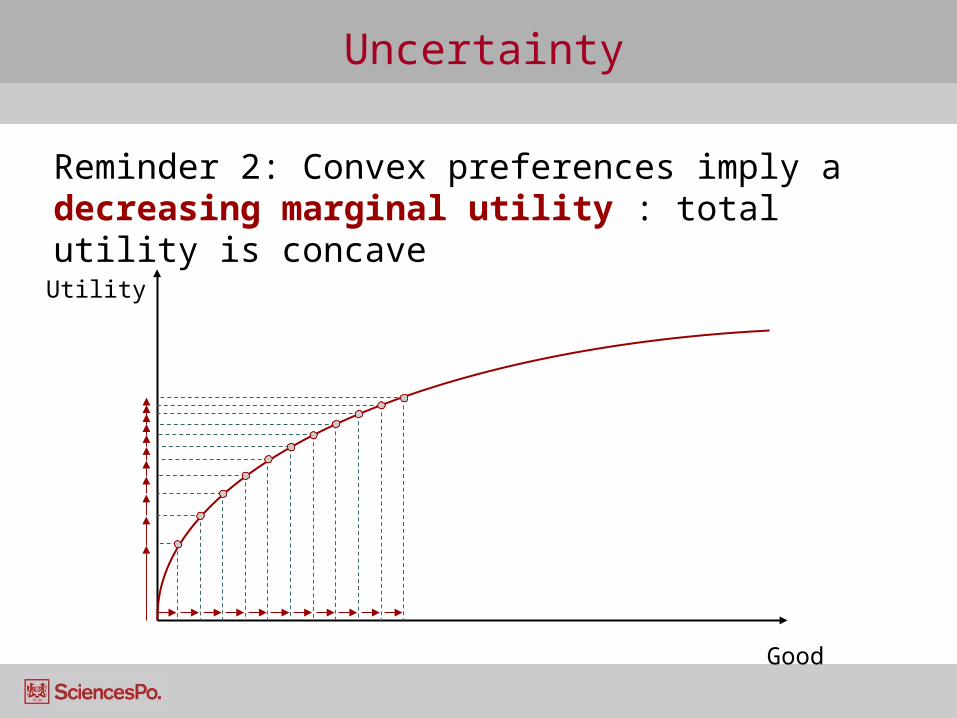

Uncertainty

Good

Utility

Reminder 2: Convex preferences imply a decreasing marginal utility : total utility is concave

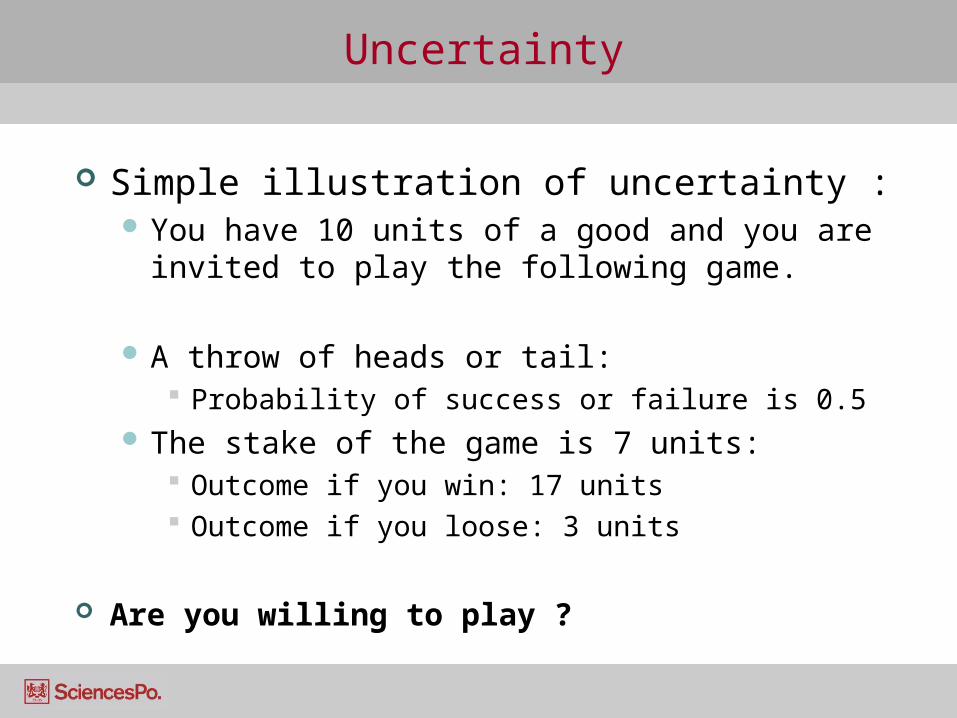

Uncertainty

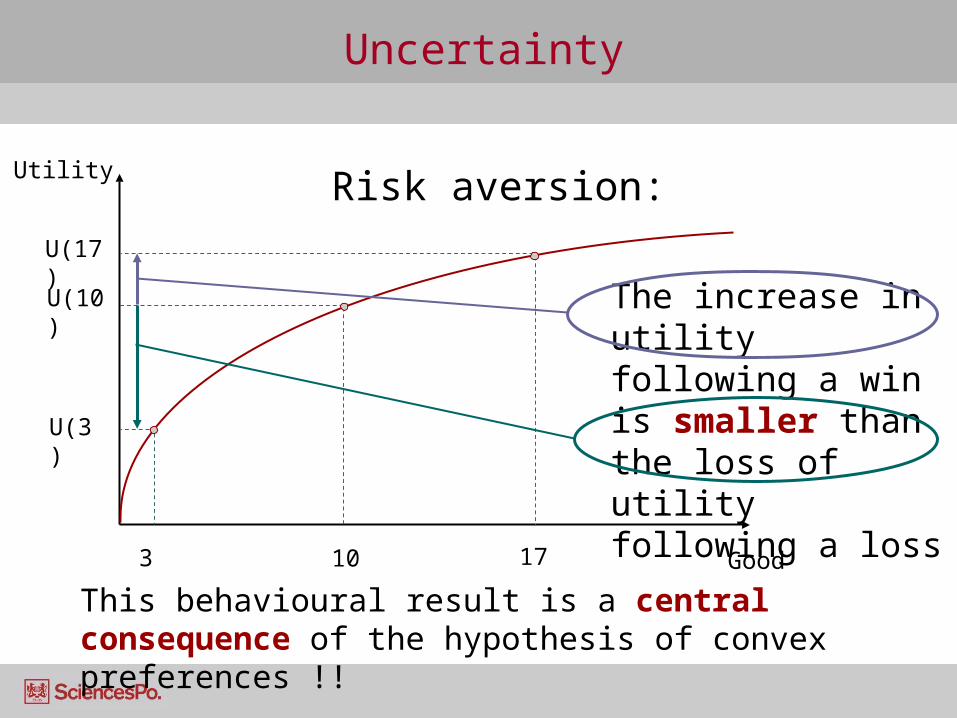

Simple illustration of uncertainty : You have 10 units of a good and you are invited

to play the following game.

A throw of heads or tail: Probability of success or failure is 0.5

The stake of the game is 7 units: Outcome if you win: 17 units Outcome if you loose: 3 units

Are you willing to play ?

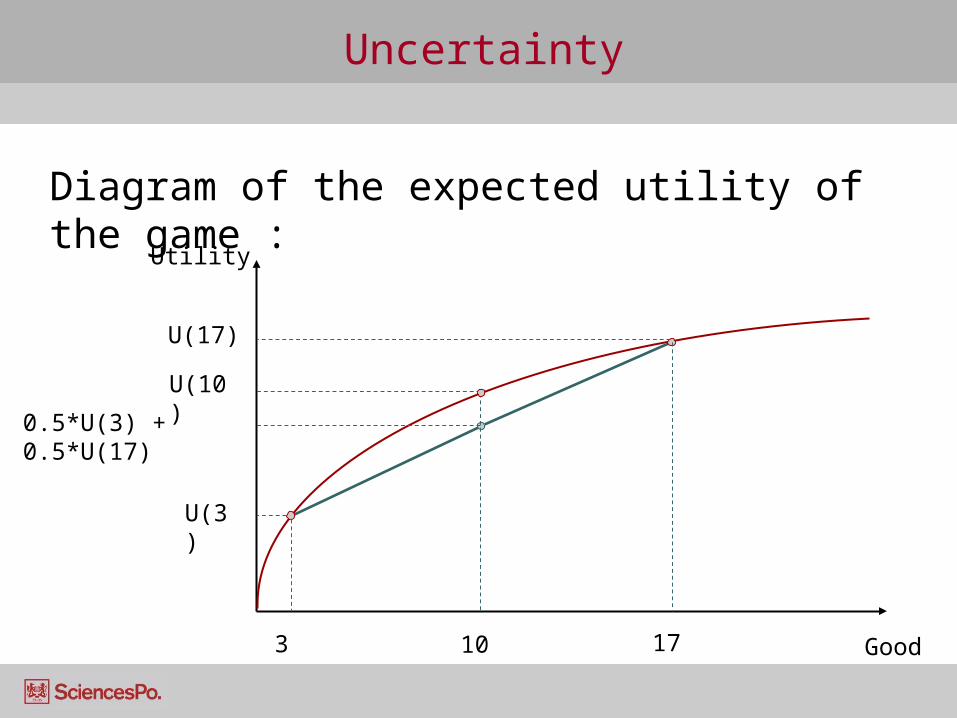

Uncertainty

Good

Utility

Diagram of the expected utility of the game :

3

U(3)

10

U(10)

17

U(17)

0.5*U(3) + 0.5*U(17)

Uncertainty

In this example, the expected result does not change the expected endowment of the agent.The player starts with 10 units and the net

expected gain is 0.

Even though the expected outcome is the same as the initial situation, the mere existence of the game reduces the utility of the agent.

Why is that ?

Uncertainty

Good

Utility

3

U(3)

10

U(10)

17

U(17)

The increase in utility following a win is smaller than the loss of utility following a loss

This behavioural result is a central consequence of the hypothesis of convex preferences !!

Risk aversion:

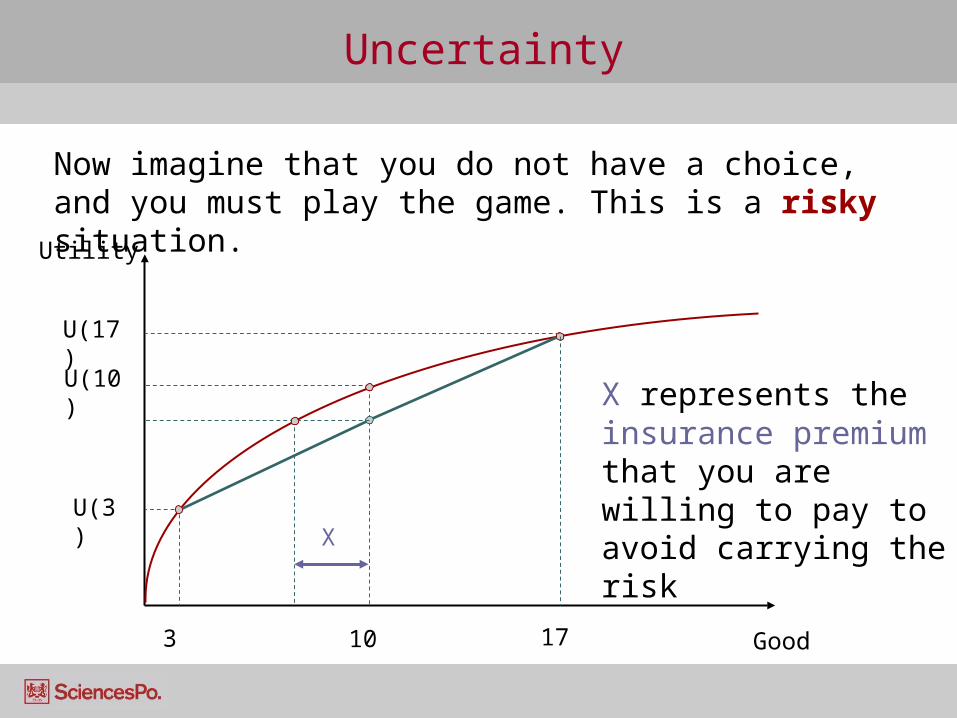

Uncertainty

Now imagine that you do not have a choice, and you must play the game. This is a risky situation.

Good

Utility

3

U(3)

10

U(10)

17

U(17)

X represents the insurance premium that you are willing to pay to avoid carrying the riskX

Adapting to Uncertainty/risk

Insurance: Agents are willing to accept a smaller endowment to mitigate

the presence of risk A risky outcome, however, does not impact all agents.

Insurance spreads this risk over all the agents: This is known as the mutualisation of risk.

Diversification behaviour: Imagine you sell umbrellas: your income depends on the

weather, so your future income is uncertain. How can you make your income more certain? Sell some ice-

creams on the side !! Financial markets:

Spread the risk over many assets instead of concentrating it on a few.

You can “sell” your risk to agents that are willing to carry it, against a payment. But beware of information problems !!

Extensions to Consumer theory

Inter-temporal choice

Uncertainty

Revealed preferences

Revealed preferences

Up until now we have assumed that preferences and indifference curves are given, and are stable This assumption was required for the purpose of

developing a theory of choice ! But we’ve never directly observed them. How do

we know we’re right?

We can reverse the theory: we work backwards from the optimal bundle and the budget constraint to get to the indifference curve.

Past choices/decisions reveal your preferences

Revealed preferences

If we have information on the bundles chosen by consumers in the past,

If we have information on the changes in prices and incomes for the duration of the period,

Then we can determine the indifference curves of the agent and verify if preferences are stable through time.

The process of revealed preferences: Gives us information on the indifference curves Allows us to check the realism of the assumptions

behind consumer theory and the test the coherence of consumers when they make choices.

Revealed preferences

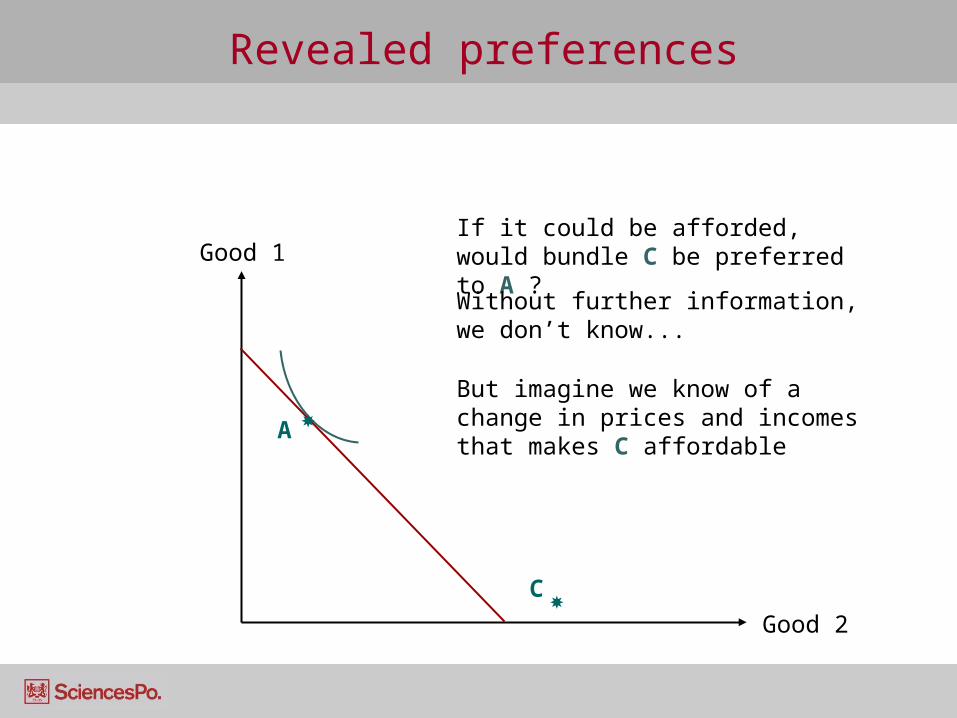

A

If it could be afforded, would bundle C be preferred to A ?

C

Good 1

Good 2

Without further information, we don’t know...

But imagine we know of a change in prices and incomes that makes C affordable

Revealed preferences

Good 2

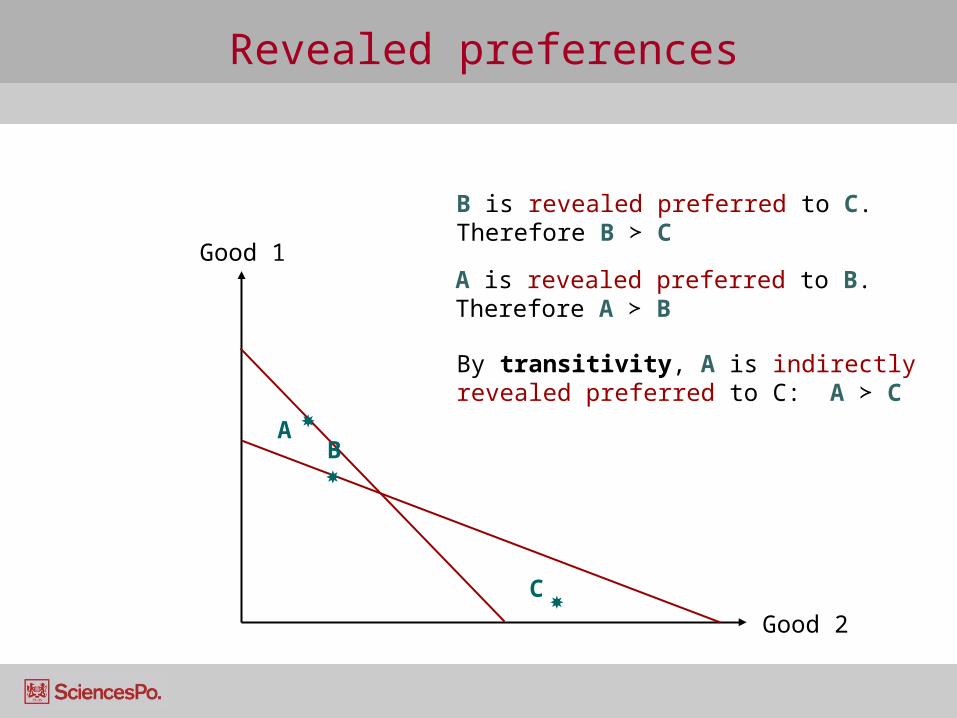

B is revealed preferred to C. Therefore B ≻ C

C

A is revealed preferred to B. Therefore A ≻ B

By transitivity, A is indirectly revealed preferred to C: A ≻ C

B

Good 1

A

Revealed preferences

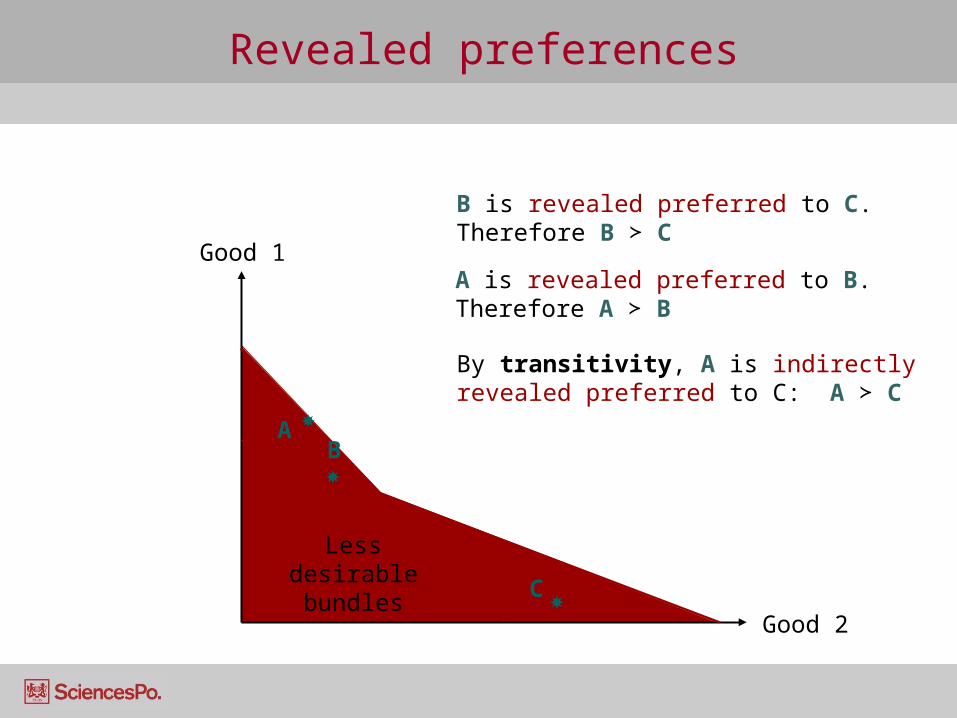

Less desirable bundles

Good 1

Good 2

C

B

A

B is revealed preferred to C. Therefore B ≻ C

A is revealed preferred to B. Therefore A ≻ B

By transitivity, A is indirectly revealed preferred to C: A ≻ C

Revealed preferences

Good 1

Good 2

C

A

B

Y

Z

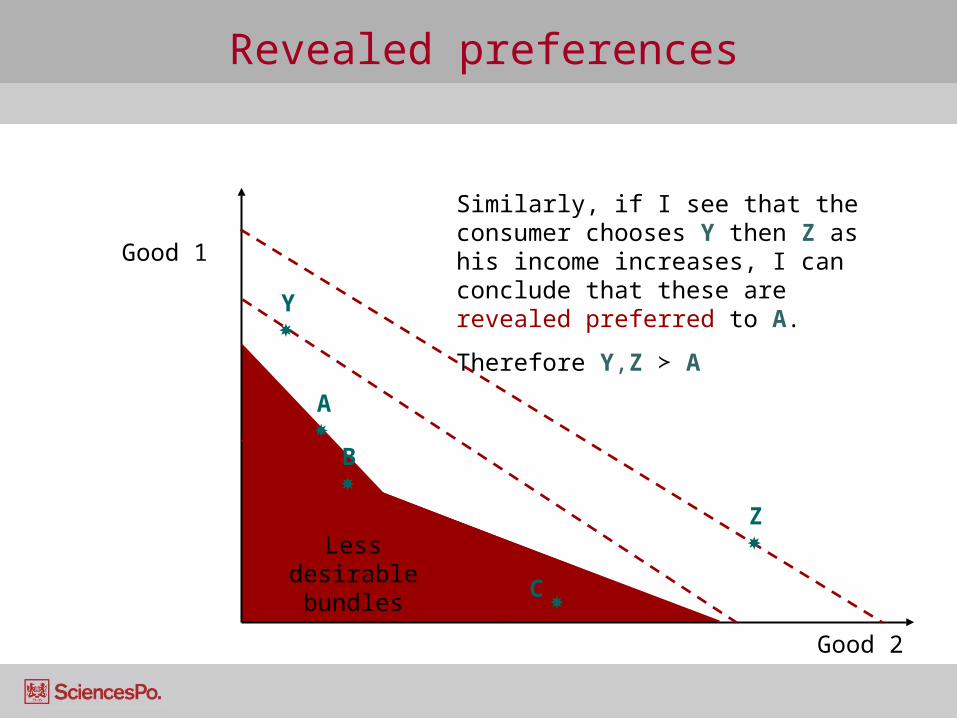

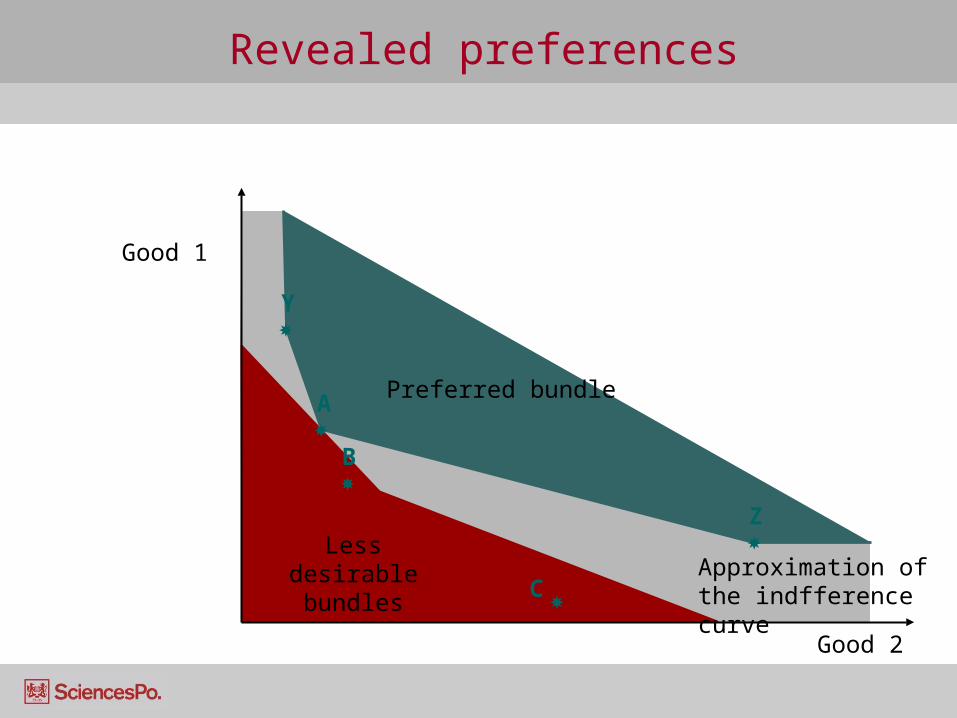

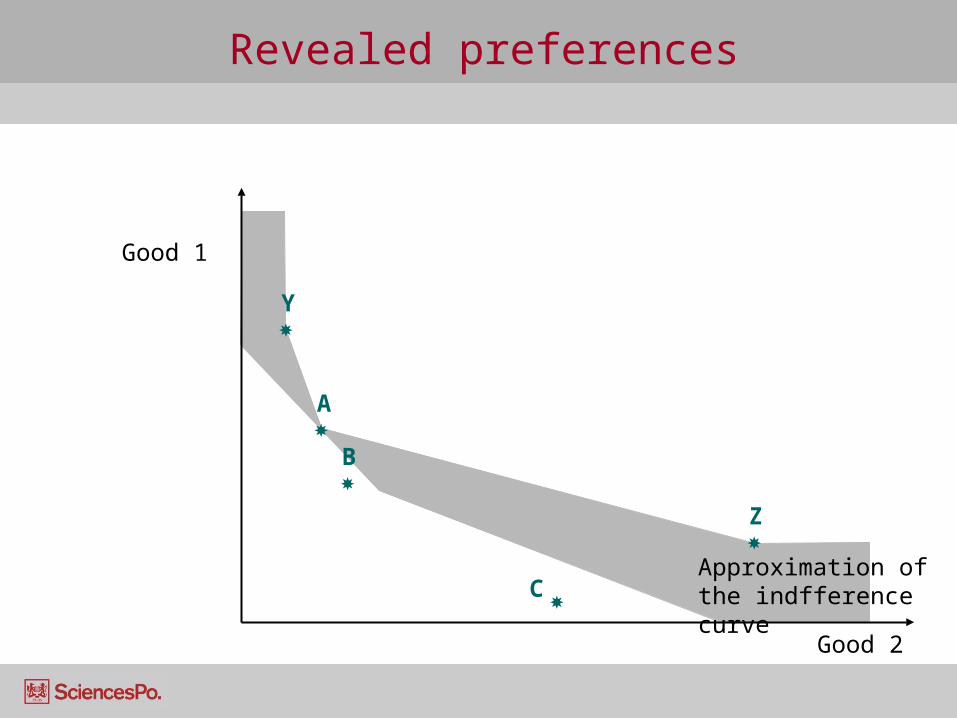

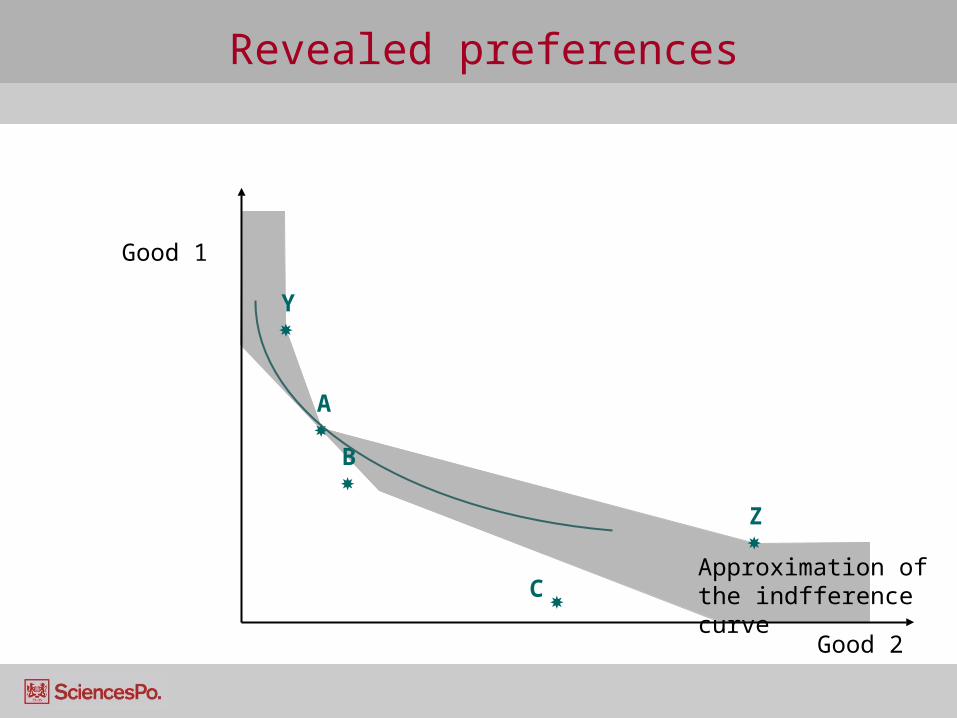

Similarly, if I see that the consumer chooses Y then Z as his income increases, I can conclude that these are revealed preferred to A.

Therefore Y,Z ≻ A

Less desirable bundles

Revealed preferences

Good 2

C

A

B

Y

Z

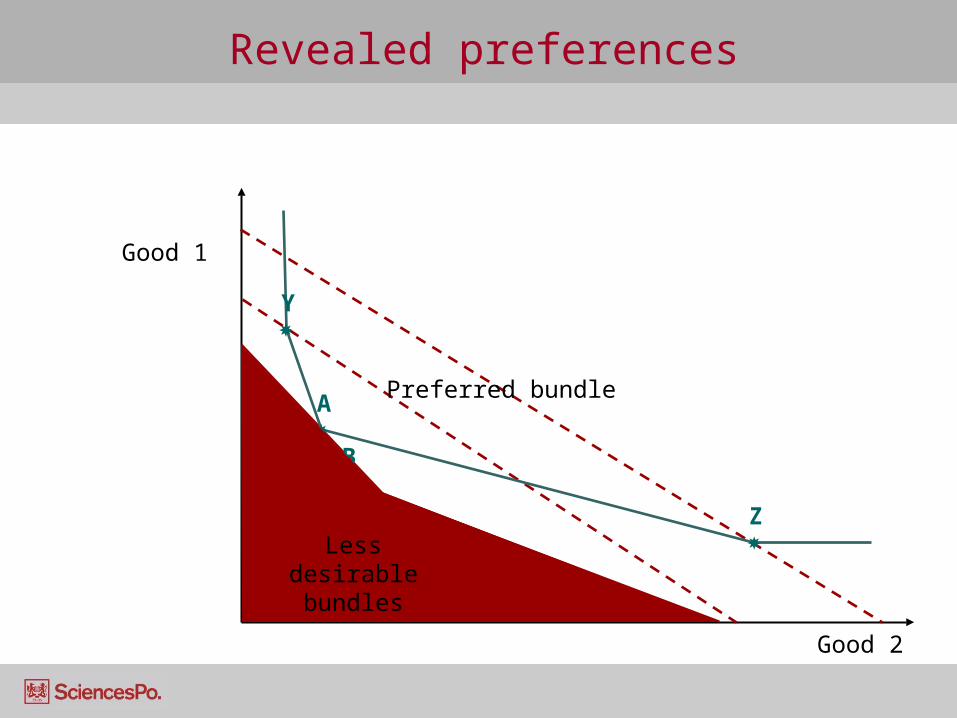

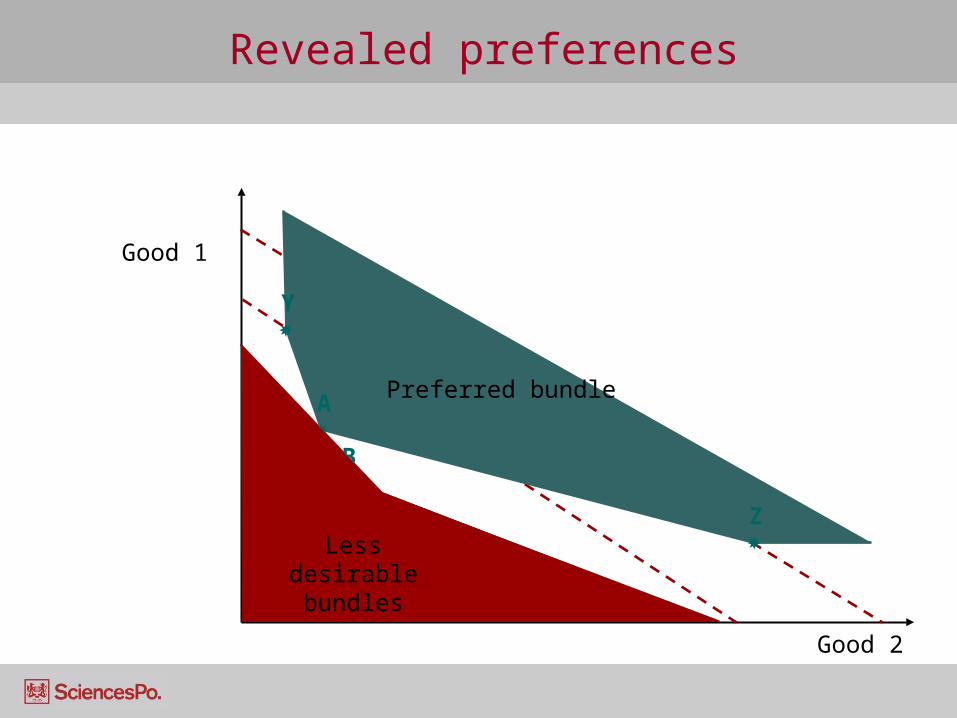

Preferred bundle

Good 1

Less desirable bundles

Revealed preferences

Good 2

C

A

B

Y

Z

Good 1

Preferred bundle

Less desirable bundles

Revealed preferences

Good 2

C

A

B

Y

Z

Preferred bundle

Approximation of the indfference curve

Good 1

Less desirable bundles

Revealed preferences

Good 2

C

A

B

Y

Z

Approximation of the indfference curve

Good 1

Revealed preferences

Good 2

C

A

B

Y

Z

Approximation of the indfference curve

Good 1