Embed Size (px)

Citation preview

Exchange Rates Determination

Jamshed uz Zaman

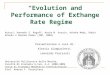

he exchange rate is the domestic price of a unit of foreign currency. This price is set by demand and supply of goods, and services. The demand generally rises because of increased claims by foreigners and supply rises

because of increased claims by foreigners and supply rises because of higher local claims on foreign countries. If demand exceeds supply the exchange rate rises. If supply increases

T

020406080

100120140160

40 41 42 43 44 45

Demand Supply

with no change in demand the rate falls. It is in equilibrium when there is no pressure to change. The overall situation in a nation’s balance of payments determines whether or not the rate will change. The rate can be manipulated, and such manipulation, or lack of it, has given rise to several exchange rate systems.

Exchange Rate System

Freely Fluctuating rates vary with demand and supply without limits; adjust automatically;

Fixed Rates such as the pure gold standard, move over a narrow range, with the upper and lower points known. It places burden on the domestic economy.

Flexible Rates allow market to set rates within prescribed limits are reached. It allows automatic adjustment but relieves the domestic economy of the burden. IMF prefers and encourages members to peg its currency, within limits, to the dollar.

Floating Rates are employed as temporary measures; rates are allowed to seek their own level in the market to establish what the new official rate should be.

Exchange Control rates are set by the government, which has direct control over both demand and supply. A multiple rate system is often concomitant with rate being set in line with a specific government program.

Exchange Rate Regimes: IMF Type explanation

1. Exchange Arrangement with No Separate Legal Tender: The currency of another country circulates as the sole legal tender or the member belongs to a monetary or currency union in which the members of the Union share the same legal tender.

2. Currency Board Arrangements: A monetary regime based on an implicit legislative commitment to exchange domestic currency for a specified foreign currency at a fixed exchange rate, combined with restrictions on the issuing authority to ensure the fulfillment of its legal obligation. [Dollarization]

3. Conventional Arrangements:

Absolute Purchasing Power Parity Theory

There are several theories dealing with the question why exchange rate changes. The basic answer is that, in short run, the exchange rate is influenced by comparative interest rates and expectation about the future, while in long run, exchange rate depends on comparative price levels. In short, exchange rate between two countries is equal to the ratio of price levels of them. This is absolute Purchasing Power Parity (PPP) theory, which may be denoted by,

e PP

d fd

f,

Improved version of the absolute PPP theory states that the spot exchange rate is determined by the relative prices of similar baskets of goods.

Relative Purchasing Power Parity Theory The absolute PPP was ultimately revised to relative PPP theory, which asserts that percentage change in exchange rate between two countries is equal to the difference of percentage changes in their price level,

( ) ( ) ( ),e e

eP P

PP P

Pt t

td f

t t

td

t t

tf

1

1

1

1

1

1

This equation holds under the condition that there exist no transport cost, no tariff and markets are competitive.

Fisher Effect, named after Irving Fisher, states that nominal interest rates in each country are equal to the required real rate of return plus compensation for expected inflation.i = r + π i$ = r$ + π$ , i¥ = r¥ + π¥

i= nominal interest rate, r = real interest rate and π is the expected inflation

International Fisher Effect or Fisher-Open states that the spot exchange rate should change in an amount equal to but in opposite direction of the difference in interest rates between two countries.i$-i¥ = r$ + π$ - r¥ - π¥ = π$ - π¥ = 100x (S t-1 - S t)/ S t .... (approx.)

The Theory of Interest Rate Parity (IRP) states that the difference in the national interest rates for securities of similar risk and maturity should be equal to, but opposite in sign to, the forward rate discount or premium for the foreign currency, except for transaction costs.

When spot and forward exchange markets are not in equilibrium, as described by interest rate parity, the potential for ‘risk less’ or arbitrage profit exists. This is called Covered Interest Arbitrage (CIA).

Forecasting: Forward rate is the best estimator. Time series forecasting considering all variables are also efficient. The Asset Approach considers both relative interest rates and country’s outlook for economic growth and profitability.

Bangladesh :Immediately before

Independence: Pakistani Rupee was pegged with Pound Sterling.

Up to December 31, 1971 £1=Rs. 13.33From January 1, 1972 : £1 = Tk. 18.98. Pegged to a single currency,

namely Pound Sterling.May, 1975 : £1 = Tk.30Since 1976 : Re-fixed 18 occasions during 26 April 1976- 13

August 1979August 1979 : Pegged to multiple currencies, i.e., Trade

Weighted Basket Method, 4 Currencies: £, $, DM, ¥. £ being intervention currency

11 January 1983 : Trade Weighted Basket Method with 6 currencies, Intervention currency US $.

July 1989 : Trade Weighted Basket Method with 10 currencies

1990 : Single Rate, Trade Weighted Basket, daily monitoring through calculation of REER to maintain purchasing power parity.

:

From 1971 to 1990 multiple exchange rates were allowed through different names of Export benefits like, Export Bonus Scheme, XPL, XPB, Home Remittance Scheme etc. Since 1983 Bangladesh continued to pursue a pegged to a basket exchange rate policy keeping in view the need for strengthening the country's competitiveness in international trade: improving the current account position and maintaining the stability of the value of Taka. This was ensured through monitoring REER, calculated on the basis of a basket containing currencies of 10/15 countries. Up to 31 December 1991, a Secondary Exchange Market existed in Bangladesh where rates were used to be determined considering the forces of demand for and supply of foreign exchange. The SEM rate and the Official rates have been unified from 1 January, 1992. Since 17 July, 1993, first step towards currency convertibility was taken. Convertibility on current transactions was adopted in July 1993. Forex rates were used to be calculated everyday on the basis of previous day’s REER of the 15 currencies, dollar being the intervention currency. Convertibility on capital accounts is not under consideration.

Bangladesh Taka was floated since May 2003 without any trouble.

Bangladesh Bank determined FOREX rate in the following way:

REERIndex b

i

Wi

ERIxCPIERIxCPI

( )( )

or,( )

log[ (log log )]ERIxCPI

Anti w CPI ERIb

i Where ERI = Exchange Rate and CPI = Consumer Price Index, i = particular country and B ids for Bangladesh.An Example

(Imaginary)Country Tk /

Currency

Tk./$ ER ERI CPI logCPI +

logERI= Y

Weights (w)

wY

USA 40 40 1 100 103 4.013 0.30 1.2UK 70 40 1.7 85 104 3.946 0.20 0.79Germany 24 40 0.6 95 105 3.999 0.20 0.80Japan 0.50 40 0.1 101 100 4.004 0.30 1.20Bangladesh

1 40 0.03 98 99 1

wY=3.99

Since antilog of 3.99 = 9867.806REER Index =(98)(99)(100)/9867.1 = 98As we want to make the Index of REER = 100 we proceed this way

Index 100 when $1 is equal to Tk. 40 .. 1 .. $1 ... ... ... Tk. 40/100 .. 98 .. $1 ... ... ... Tk. (40x98)/100 = 39.2.

For Index Number, Price Level, Weights etc. read any text book on Statistics

Bangladesh: Balance of Payments(In million US dollar)

FY 98

FY 99

FY 00

FY 01

FY 02

FY 03

FY 04

FY 05

Trade Balance -1669 -1934 -1865 -2011 -1768 -2207 -2319 -3297 Exports, fob (including EPZ) 1/ 5103 5283 5701 6419 5929 6492 7521 8573

Imports, cif (including EPZ) 2/ -6772 -7217 -7566 -8430 -7697 -8699 -9840 -11870

Services (net) -570 -603 -645 -914 -499 -688 874 -870 Receipts 707 707 849 759 865 887 924 1177

Payments -1277 -1310 -1494 -1673 -1364 -1575 -1798 -2047

Income (net) -100 -135 -221 -264 -319 -195 -374 -641 Receipt 91 91 97 97 50 64 63 115

Payments -191 -226 -318 -361 -369 -259 -437 -756

Current transfers 3/ 1876 2195 2394 2171 2826 3418 3743 4290 Official 126 220 165 72 69 60 61 37

Private 1750 1975 2229 2099 2757 3358 3682 4253

of which Worker's remittances 1525 3372 3851

Current Account Balance -463 -477 -337 -1018 240 328 176 -518Capital account (net) 445 387 561 432 410 392 196 163 Capital transfers 445 387 561 432 410 392 196 163

Financial account 237 -395 -185 407 71 302 78 744 Direct investment 4/ 249 198 194 174 65 92 385 540

Portfolio investment 3 -6 0 0 -6 2 6 0

Other investment -15 -587 -379 233 12 208 -313 204 MLT loans 706 821 806 790 733 937 544 940

MLT amortization payments -308 -341 -396 -416 -421 -431 -397 -449

Other long term loans (net) -47 -41 127 -13 -42 -20 -41 -46

Other short term loans (net) 168 -78 56 86 20 226 13 241

Other Assets -41 -58 -55 -68 -52 -81 -125 -155

Trade Credit (net) -522 -829 -641 -260 -253 -494 -321 -127

Commercial Banks' (net) 29 -61 -276 114 27 71 14 -200 Assets -19 -31 -161 147 -90 217 86 -91

Liabilities 48 -30 -115 -33 117 -146 -72 -109

Errors and omissions 5/ -88 267 125 -47 -356 -123 -279 -228 OVERALL BALANCE 131 -218 164 -226 365 899 171 161Reserve Assets -131 218 -164 226 -365 -899 -171 -161 Bangladesh Bank 6/ -131 218 -164 226 -365 -899 -171 -161

Assets -14 205 -79 302 -276 -887 -235 -319

Liabilities -117 13 -85 -76 -89 -12 64 158

Source: Statistics Department, Bangladesh BankP = Provisional1/ On the basis of shipment. Includes goods procured in ports and repairs on goods.2/ On the basis of exchange records. Includes goods procured in ports, repairs on goods.3/ Food and commodity grants including Technical Assistance.4/ Only cash flow through banking channel. From 1997-98 it also includes investment in the form of cash and equipment under gas and electricity5/ Including excess of shipment over actual receipt from exports.6/ Consistent with monetary survey data, including NFCD account.