Embed Size (px)

Citation preview

B190

01no

EY Norwegian Cloud Maturity Survey 2019 Current and planned adoption of cloud services

2 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

Contents

01 Cloud maturity 4

02 Drivers and challenges 6

03 Current usage 10

04 Future plans 16

05 About the survey 22

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 3

Introduction

Cloud adoption in Norway is increasing; but a lack of cloud expertise and the complexity in migrating legacy applications are still holding the adoption back.

Reduced time-to-market with new digital solutions is driving cloud adoptionThe most important business driver for cloud adoption is reduced time-to-market with new digital solutions. Cost savings are less important among the respondents this year; hence being able to release new digital services faster with the support of a scalable cloud platform seems to be more important than costs.

The lack of cloud expertise and the complexity in migrating legacy applications are holding cloud adoption back The percentage of respondents that considers the lack of cloud expertise as a challenge related to using cloud services has increased significantly since last year’s survey. The complexity in migrating legacy applications is still a barrier for large-scale adoption of cloud services. This indicates that Norway is still immature when it comes to cloud computing and that more experienced people within the domain are required to handle the current cloud transformation.

DevOps and serverless are mainstreamThe number of respondents that are applying DevOps methods has increased significantly this year. About 39% of the respondents are using serverless PaaS cloud services. These findings indicate that these methods and services are now mainstream in the Norwegian market.

Multi-cloud is the new blackAbout 74% of the respondents are using two or more IaaS or PaaS providers — indicating that a multi-cloud strategy is popular among the largest organizations in Norway.

Compared to 2018, there is an increasing focus on executing on cloud initiatives rather than developing cloud strategiesAbout 32% of the respondents have even planned to start the migration of all their datacenters to Infrastructure as a Service (IaaS) and Platform as a Service (PaaS) in 2019, showing that many large Norwegian organizations have decided to embrace the cloud fully.

4 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

01 Cloud maturity

01 Cloud maturity

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 5

01 Cloud maturity

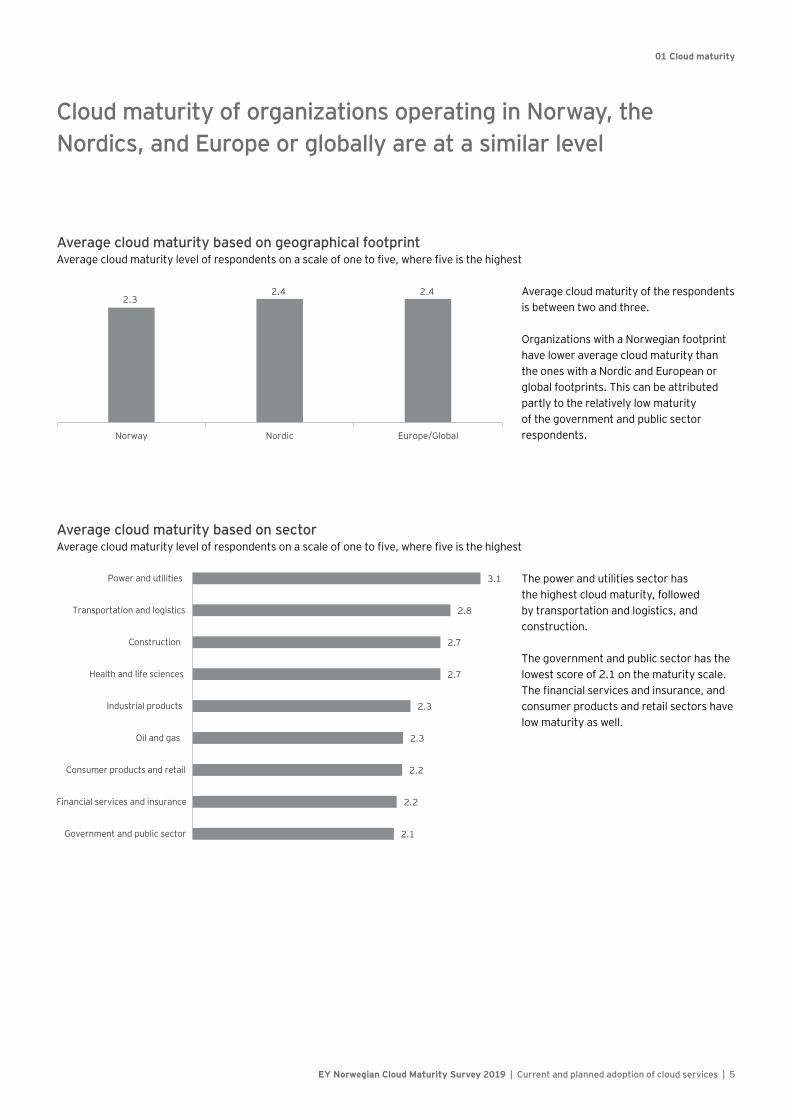

Cloud maturity of organizations operating in Norway, the Nordics, and Europe or globally are at a similar level

Average cloud maturity of the respondents is between two and three.

Organizations with a Norwegian footprint have lower average cloud maturity than the ones with a Nordic and European or global footprints. This can be attributed partly to the relatively low maturity of the government and public sector respondents.

Average cloud maturity based on geographical footprintAverage cloud maturity level of respondents on a scale of one to five, where five is the highest

The power and utilities sector has the highest cloud maturity, followed by transportation and logistics, and construction.

The government and public sector has the lowest score of 2.1 on the maturity scale. The financial services and insurance, and consumer products and retail sectors have low maturity as well.

Average cloud maturity based on sectorAverage cloud maturity level of respondents on a scale of one to five, where five is the highest

2.3 2.4 2.4

Norway Nordic Europe/Global

2.1

2.2

2.2

2.3

2.3

2.7

2.7

2.8

3.1

Government and public sector

Financial services and insurance

Consumer products and retail

Oil and gas

Industrial products

Health and life sciences

Construction

Transportation and logistics

Power and utilities

6 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

02 Drivers and challenges

02 Drivers and challenges

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 7

02 Drivers and challenges

Reduced time-to-market with new digital solutions is driving cloud adoption; but the lack of cloud expertise is holding companies back

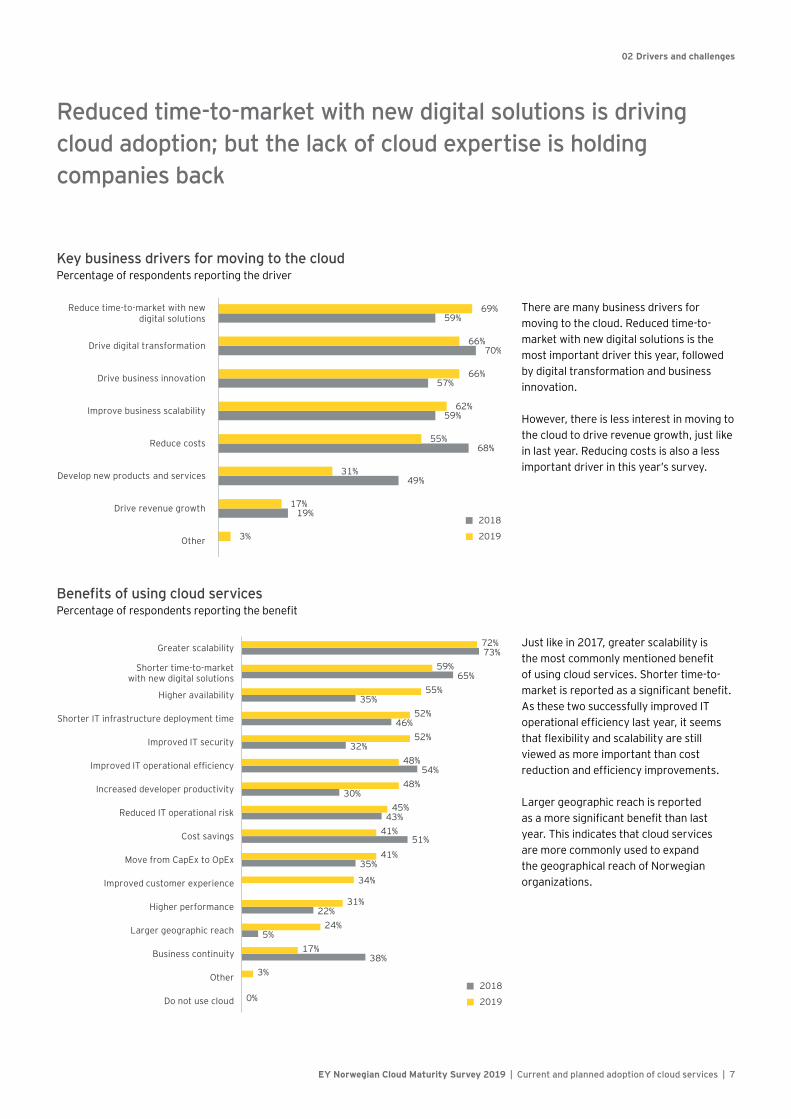

There are many business drivers for moving to the cloud. Reduced time-to-market with new digital solutions is the most important driver this year, followed by digital transformation and business innovation.

However, there is less interest in moving to the cloud to drive revenue growth, just like in last year. Reducing costs is also a less important driver in this year’s survey.

Key business drivers for moving to the cloudPercentage of respondents reporting the driver

Just like in 2017, greater scalability is the most commonly mentioned benefit of using cloud services. Shorter time-to-market is reported as a significant benefit. As these two successfully improved IT operational efficiency last year, it seems that flexibility and scalability are still viewed as more important than cost reduction and efficiency improvements.

Larger geographic reach is reported as a more significant benefit than last year. This indicates that cloud services are more commonly used to expand the geographical reach of Norwegian organizations.

Benefits of using cloud servicesPercentage of respondents reporting the benefit

2019

201819%

49%

68%

59%

57%

70%

59%

3%

17%

31%

55%

62%

66%

66%

69%

Other

Drive revenue growth

Develop new products and services

Reduce costs

Improve business scalability

Drive business innovation

Drive digital transformation

Reduce time-to-market with newdigital solutions

2019

2018

38%

5%

22%

35%

51%

43%

30%

54%

32%

46%

35%

65%

73%

0%

3%

17%

24%

31%

34%

41%

41%

45%

48%

48%

52%

52%

55%

59%

72%

Do not use cloud

Other

Business continuity

Larger geographic reach

Higher performance

Improved customer experience

Move from CapEx to OpEx

Cost savings

Reduced IT operational risk

Increased developer productivity

Improved IT operational efficiency

Improved IT security

Shorter IT infrastructure deployment time

Higher availability

Shorter time-to-market with new digital solutions

Greater scalability

8 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

02 Drivers and challenges

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 9

02 Drivers and challenges

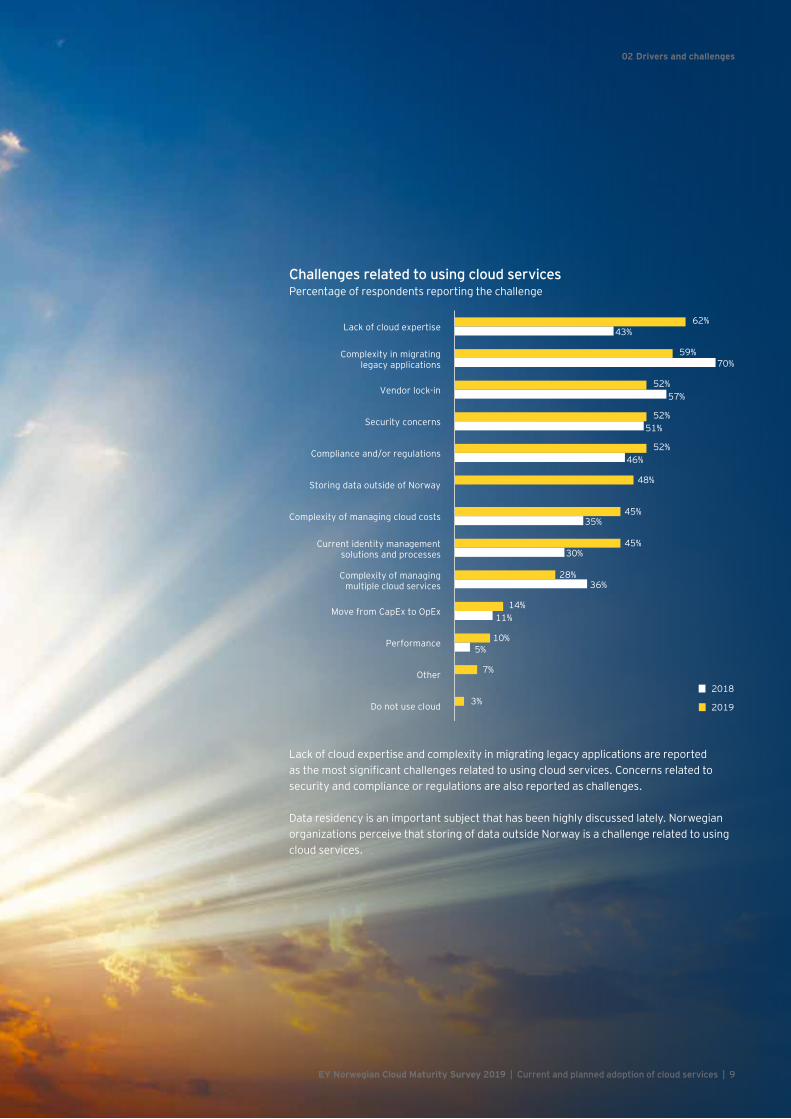

Lack of cloud expertise and complexity in migrating legacy applications are reported as the most significant challenges related to using cloud services. Concerns related to security and compliance or regulations are also reported as challenges.

Data residency is an important subject that has been highly discussed lately. Norwegian organizations perceive that storing of data outside Norway is a challenge related to using cloud services.

Challenges related to using cloud servicesPercentage of respondents reporting the challenge

2019

2018

5%

11%

36%

30%

35%

46%

51%

57%

70%

43%

3%

7%

10%

14%

28%

45%

45%

48%

52%

52%

52%

59%

62%

Do not use cloud

Other

Performance

Move from CapEx to OpEx

Complexity of managing multiple cloud services

Current identity management solutions and processes

Complexity of managing cloud costs

Storing data outside of Norway

Compliance and/or regulations

Security concerns

Vendor lock-in

Complexity in migrating legacy applications

Lack of cloud expertise

10 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

03 Current usage

03 Current usage

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 11

03 Current usage

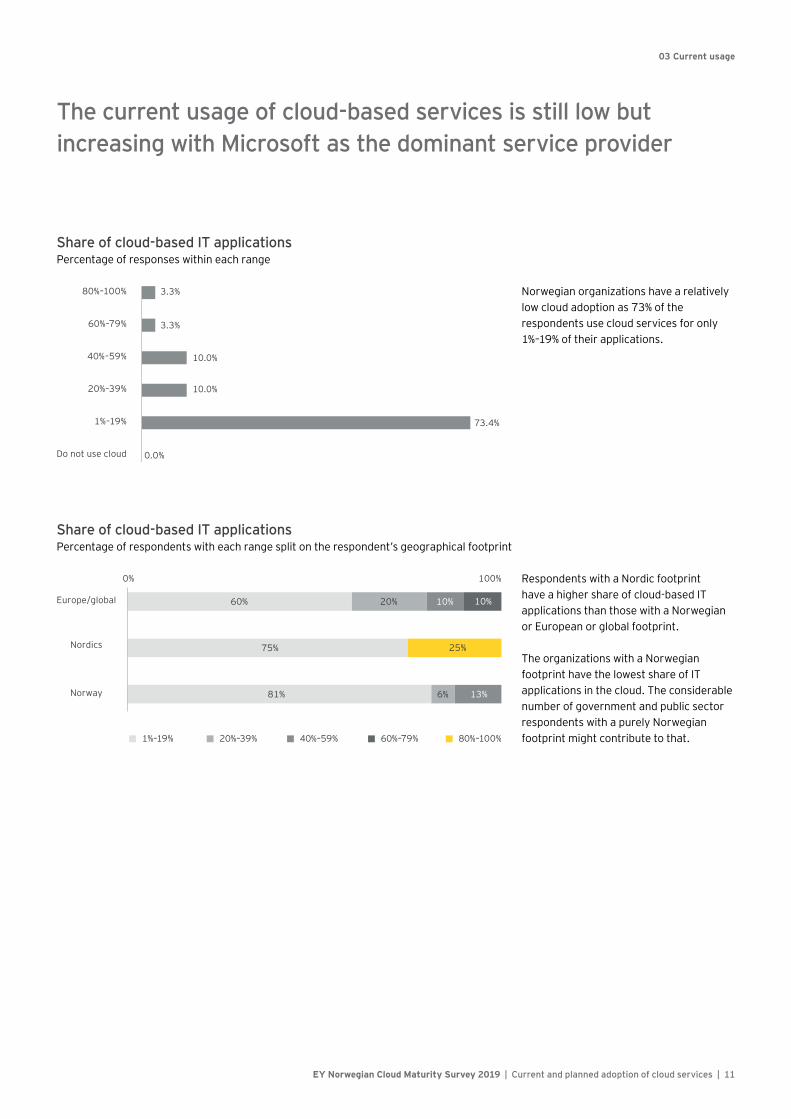

The current usage of cloud-based services is still low but increasing with Microsoft as the dominant service provider

Norwegian organizations have a relatively low cloud adoption as 73% of the respondents use cloud services for only 1%–19% of their applications.

Share of cloud-based IT applications Percentage of responses within each range

Respondents with a Nordic footprint have a higher share of cloud-based IT applications than those with a Norwegian or European or global footprint.

The organizations with a Norwegian footprint have the lowest share of IT applications in the cloud. The considerable number of government and public sector respondents with a purely Norwegian footprint might contribute to that.

Share of cloud-based IT applications Percentage of respondents with each range split on the respondent’s geographical footprint

0.0%

73.4%

10.0%

10.0%

3.3%

3.3%

Do not use cloud

1%–19%

20%–39%

40%–59%

60%–79%

80%–100%

81%

75%

60%

6%

20%

13%

10% 10%

25%

0% 100%

Norway

Nordics

Europe/global

1%–19% 20%–39% 40%–59% 60%–79% 80%–100%

12 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

03 Current usage

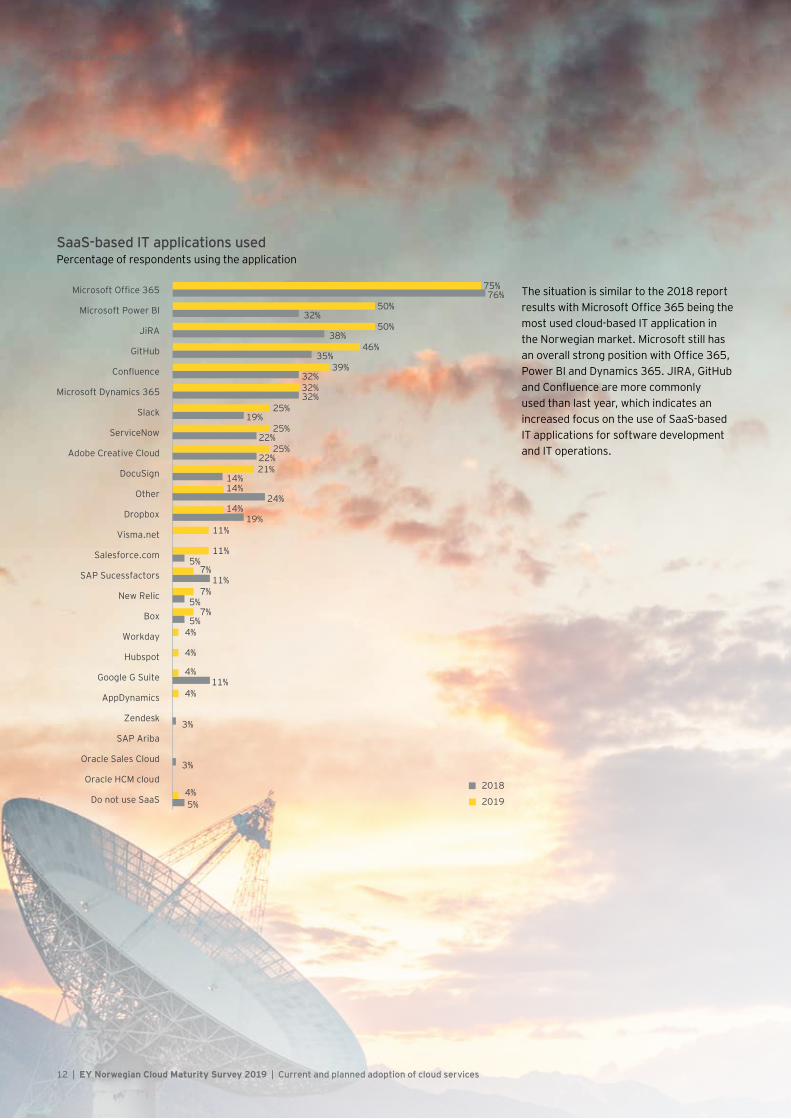

The situation is similar to the 2018 report results with Microsoft Office 365 being the most used cloud-based IT application in the Norwegian market. Microsoft still has an overall strong position with Office 365, Power BI and Dynamics 365. JIRA, GitHub and Confluence are more commonly used than last year, which indicates an increased focus on the use of SaaS-based IT applications for software development and IT operations.

SaaS-based IT applications usedPercentage of respondents using the application

2019

2018

5%

3%

3%

11%

5%

5%

11%

5%

19%

24%

14%

22%

22%

19%

32%

32%

35%

38%

32%

76%

4%

4%

4%

4%

4%

7%

7%

7%

11%

11%

14%

14%

21%

25%

25%

25%

32%

39%

46%

50%

50%

75%

Do not use SaaS

Oracle HCM cloud

Oracle Sales Cloud

SAP Ariba

Zendesk

AppDynamics

Google G Suite

Hubspot

Workday

Box

New Relic

SAP Sucessfactors

Salesforce.com

Visma.net

Dropbox

Other

DocuSign

Adobe Creative Cloud

ServiceNow

Slack

Microsoft Dynamics 365

Confluence

GitHub

JiRA

Microsoft Power BI

Microsoft Office 365

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 13

03 Current usage

About 93% of the respondents have below 40% of their IT infrastructure in the cloud. The share of cloud-based IT infrastructure is significantly lower than the share of cloud-based IT applications, which indicate that Norwegian organizations currently are adopting SaaS based IT applications faster than IaaS/PaaS cloud-based IT infrastructure.

Share of cloud-based IT infrastructure Percentage of responses within each range

The majority of the respondents use two or more IaaS or PaaS providers, and 28% uses three or more providers. The low level of respondents using only one provider indicates the popularity of a multi-cloud strategy in the Norwegian market.

Number of IaaS or PaaS providers usedPercentage of respondents within each category

10.0%

66.7%

16.7%

3.3%

3.3%

Do not use cloud

1%–19%

20%–39%

40%–59%

60%–79%

80%–100%

0.0%

14.3%10.7%

46.4%

21.4%

7.2%

None One Two Three Four or more

14 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

03 Current usage

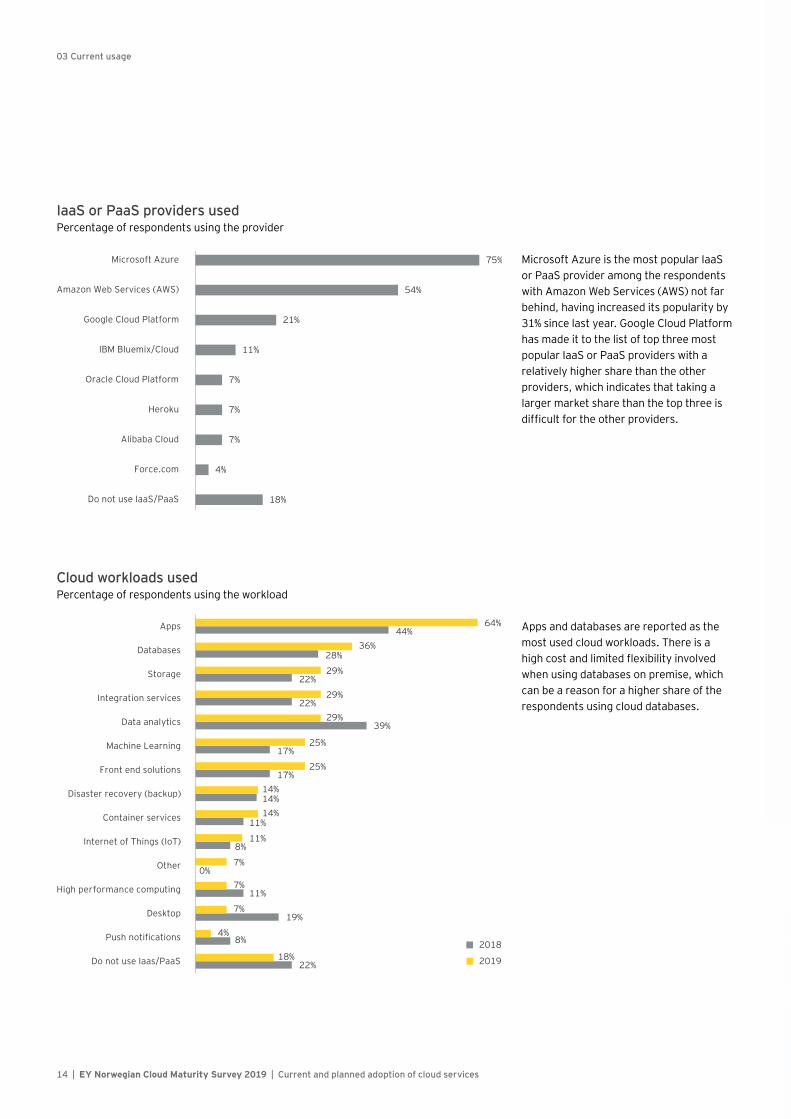

Microsoft Azure is the most popular IaaS or PaaS provider among the respondents with Amazon Web Services (AWS) not far behind, having increased its popularity by 31% since last year. Google Cloud Platform has made it to the list of top three most popular IaaS or PaaS providers with a relatively higher share than the other providers, which indicates that taking a larger market share than the top three is difficult for the other providers.

IaaS or PaaS providers usedPercentage of respondents using the provider

Apps and databases are reported as the most used cloud workloads. There is a high cost and limited flexibility involved when using databases on premise, which can be a reason for a higher share of the respondents using cloud databases.

Cloud workloads usedPercentage of respondents using the workload

18%

4%

7%

7%

7%

11%

21%

54%

75%

Do not use IaaS/PaaS

Force.com

Alibaba Cloud

Heroku

Oracle Cloud Platform

IBM Bluemix/Cloud

Google Cloud Platform

Amazon Web Services (AWS)

Microsoft Azure

2019

2018

22%

8%

19%

11%

0%

8%

11%

14%

17%

17%

39%

22%

22%

28%

44%

18%

4%

7%

7%

7%

11%

14%

14%

25%

25%

29%

29%

29%

36%

64%

Do not use Iaas/PaaS

Push notifications

Desktop

High performance computing

Other

Internet of Things (IoT)

Container services

Disaster recovery (backup)

Front end solutions

Machine Learning

Data analytics

Integration services

Storage

Databases

Apps

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 15

03 Current usage

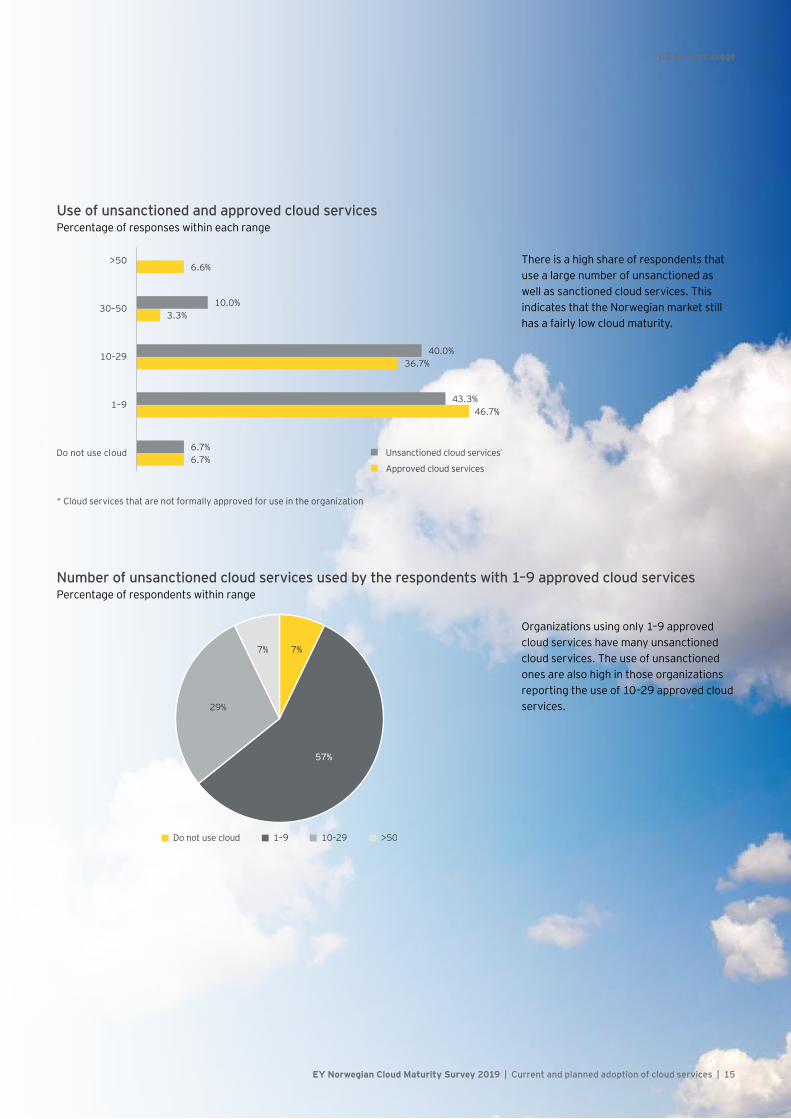

There is a high share of respondents that use a large number of unsanctioned as well as sanctioned cloud services. This indicates that the Norwegian market still has a fairly low cloud maturity.

Use of unsanctioned and approved cloud services Percentage of responses within each range

Organizations using only 1–9 approved cloud services have many unsanctioned cloud services. The use of unsanctioned ones are also high in those organizations reporting the use of 10–29 approved cloud services.

Number of unsanctioned cloud services used by the respondents with 1–9 approved cloud servicesPercentage of respondents within range

6.7%

46.7%

36.7%

3.3%

6.6%

6.7%

43.3%

40.0%

10.0%

Do not use cloud

1–9

10–29

30–50

>50

Unsanctioned cloud services*

Approved cloud services

* Cloud services that are not formally approved for use in the organization

7%

57%

29%

7%

Do not use cloud 1–9 10–29 >50

16 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

04 Future plans

04 Future plans

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 17

04 Future plans

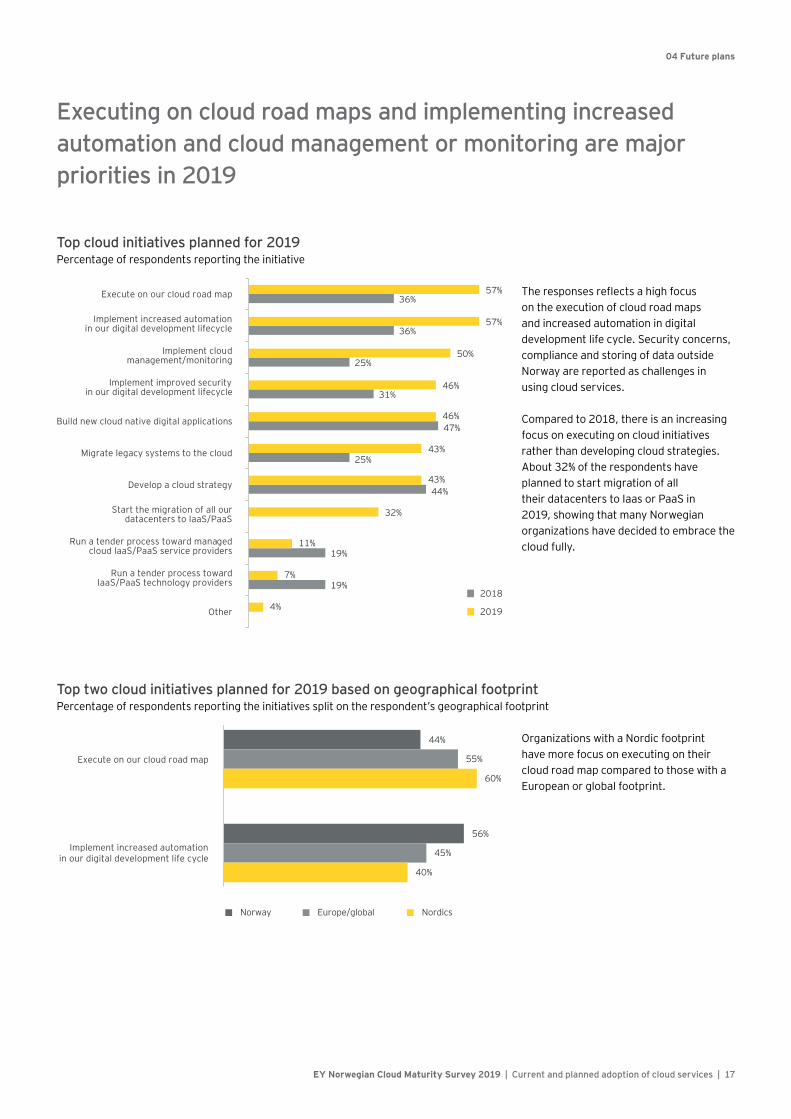

Executing on cloud road maps and implementing increased automation and cloud management or monitoring are major priorities in 2019

The responses reflects a high focus on the execution of cloud road maps and increased automation in digital development life cycle. Security concerns, compliance and storing of data outside Norway are reported as challenges in using cloud services.

Compared to 2018, there is an increasing focus on executing on cloud initiatives rather than developing cloud strategies. About 32% of the respondents have planned to start migration of all their datacenters to Iaas or PaaS in 2019, showing that many Norwegian organizations have decided to embrace the cloud fully.

Top cloud initiatives planned for 2019Percentage of respondents reporting the initiative

Organizations with a Nordic footprint have more focus on executing on their cloud road map compared to those with a European or global footprint.

Top two cloud initiatives planned for 2019 based on geographical footprintPercentage of respondents reporting the initiatives split on the respondent’s geographical footprint

2019

201819%

19%

44%

25%

47%

31%

25%

36%

36%

4%

7%

11%

32%

43%

43%

46%

46%

50%

57%

57%

Other

Run a tender process toward IaaS/PaaS technology providers

Run a tender process toward managedcloud IaaS/PaaS service providers

Start the migration of all our datacenters to IaaS/PaaS

Develop a cloud strategy

Migrate legacy systems to the cloud

Build new cloud native digital applications

Implement improved securityin our digital development lifecycle

Implement cloudmanagement/monitoring

Implement increased automationin our digital development lifecycle

Execute on our cloud road map

44%

56%

55%

45%

60%

40%

Execute on our cloud road map

Implement increased automation in our digital development life cycle

Norway Europe/global Nordics

18 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

04 Future plans

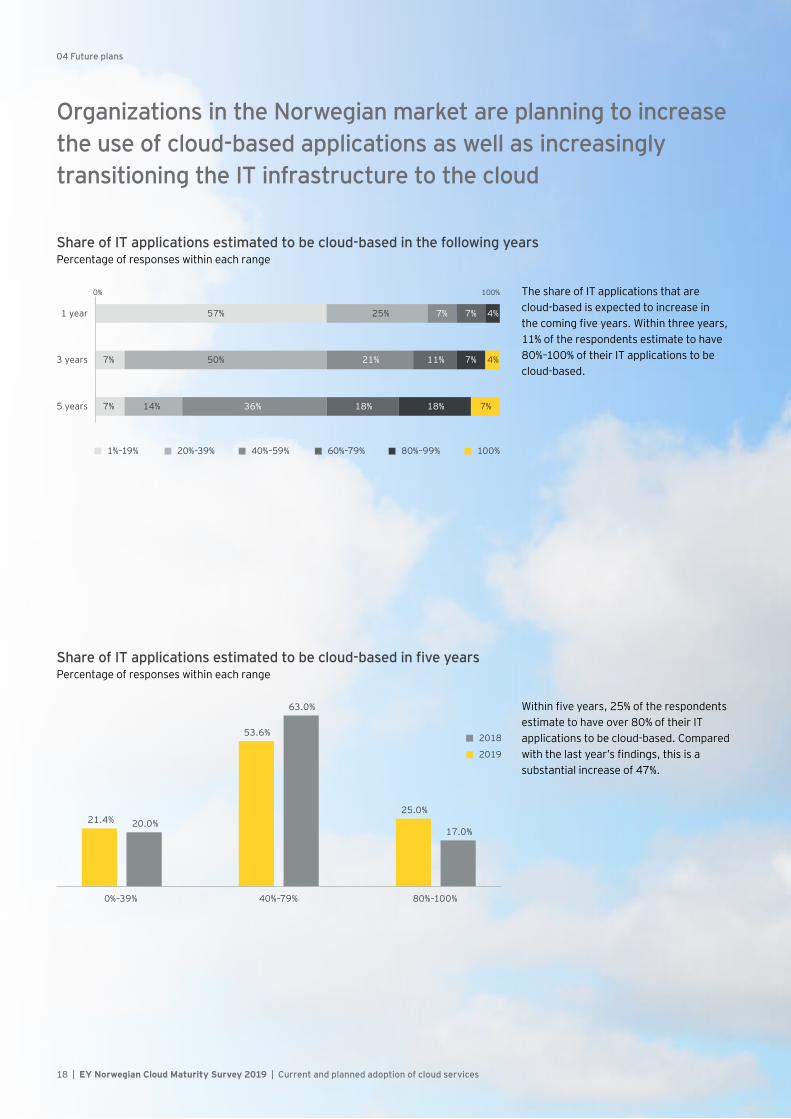

Organizations in the Norwegian market are planning to increase the use of cloud-based applications as well as increasingly transitioning the IT infrastructure to the cloud

The share of IT applications that are cloud-based is expected to increase in the coming five years. Within three years, 11% of the respondents estimate to have 80%–100% of their IT applications to be cloud-based.

Share of IT applications estimated to be cloud-based in the following yearsPercentage of responses within each range

Within five years, 25% of the respondents estimate to have over 80% of their IT applications to be cloud-based. Compared with the last year’s findings, this is a substantial increase of 47%.

Share of IT applications estimated to be cloud-based in five yearsPercentage of responses within each range

1%–19% 20%–39% 40%–59% 60%–79% 100%

57%

7%

7%

25%

50%

14%

7%

21%

36%

7%

11%

18%

4%

7%

18%

4%

7%

0% 100%

1 year

3 years

5 years

80%–99%

21.4%

53.6%

25.0%20.0%

63.0%

17.0%

0%–39% 40%–79% 80%–100%

2019

2018

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 19

04 Future plans

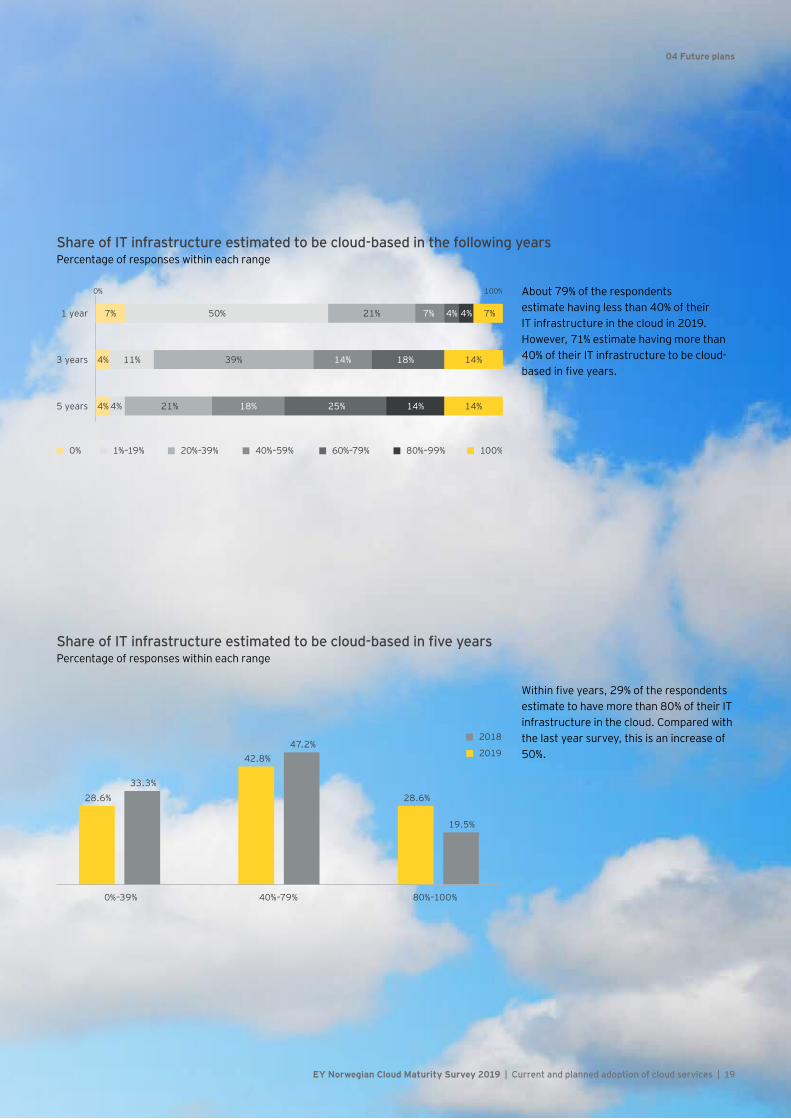

About 79% of the respondents estimate having less than 40% of their IT infrastructure in the cloud in 2019. However, 71% estimate having more than 40% of their IT infrastructure to be cloud-based in five years.

Share of IT infrastructure estimated to be cloud-based in the following yearsPercentage of responses within each range

Within five years, 29% of the respondents estimate to have more than 80% of their IT infrastructure in the cloud. Compared with the last year survey, this is an increase of 50%.

Share of IT infrastructure estimated to be cloud-based in five yearsPercentage of responses within each range

1%–19% 20%–39% 40%–59% 60%–79% 100%

0% 100%

1 year

3 years

5 years

80%–99%

7%

4%

4%

50%

11%

4%

21%

39%

21%

7%

14%

18%

4%

18%

25%

4%

14%

7%

14%

14%

0%

2019

2018

28.6%

42.8%

28.6%33.3%

47.2%

19.5%

0%–39% 40%–79% 80%–100%

20 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

04 Future plans

The IT department is taking a larger responsibility for cloud-based technology

Defining cloud security policy and deciding or advising on which applications to implement in the cloud are reported as two most important roles of the IT department with regard to cloud. In addition, managing cloud contracts and deciding on policies for cloud use are also of high priority. This is supported by the findings on the challenges related to cloud services with respect to security concerns and compliance.

The role of IT department with regard to cloudPercentage of respondents reporting the role

Almost all respondents report GDPR compliance as the most important IT security requirement they have for cloud providers. Data processing agreements (DPAs) and location of the customer data are also considered as important requirements. This is supported by the findings on the challenges related to cloud services with respect to security concerns and compliance.

Important IT security requirements for the cloud provider Percentage of respondents reporting the requirement

4%

54%

54%

75%

75%

79%

82%

Do not use cloud

Manage all cloud deployments

Manage/optimize costs of cloud

Set policies for cloud use

Manage cloud service contracts

Decide/advise on which applications to implement in the cloud

Define cloud security policy

4%

36%

39%

50%

68%

86%

96%

Other

ISAE3402/SOC 1 Report

SOC 2 Report on GDPR/Privacy or similar

Visibility of all the parties involved in the service delivery

Where your data is located

Data processing agreement (DPA)

GDPR compliance

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 21

04 Future plans

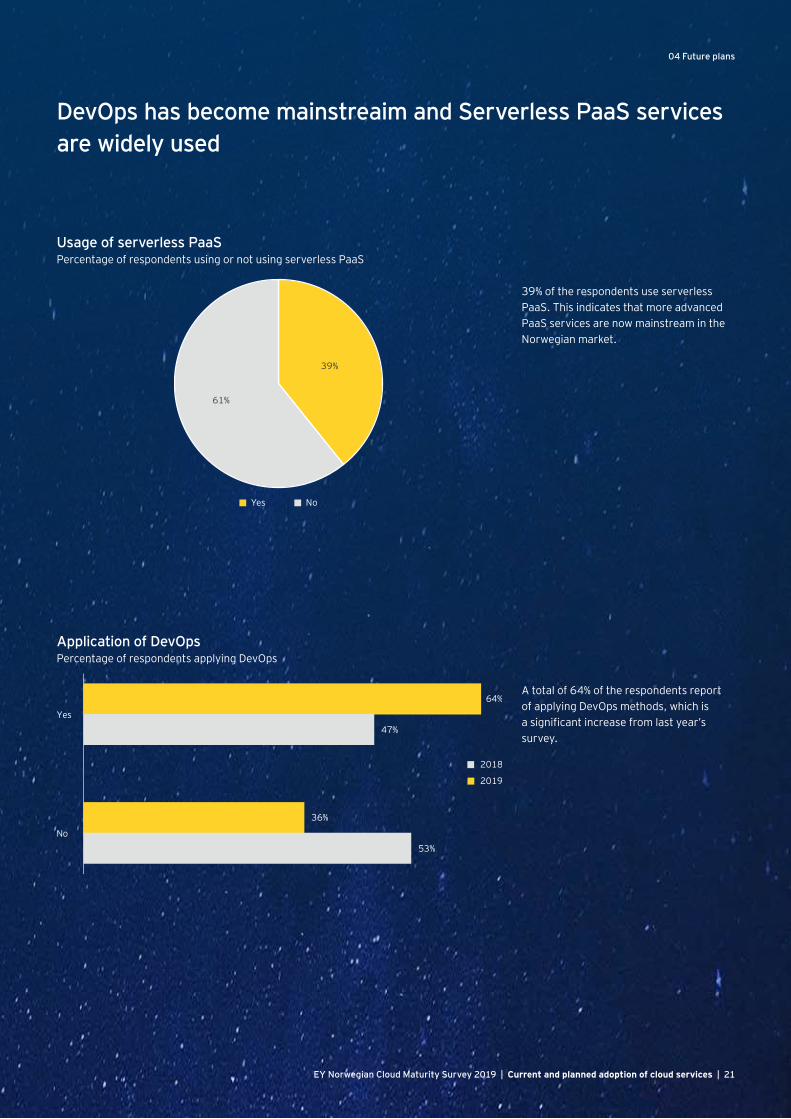

DevOps has become mainstreaim and Serverless PaaS services are widely used

39% of the respondents use serverless PaaS. This indicates that more advanced PaaS services are now mainstream in the Norwegian market.

Usage of serverless PaaSPercentage of respondents using or not using serverless PaaS

A total of 64% of the respondents report of applying DevOps methods, which is a significant increase from last year’s survey.

Application of DevOpsPercentage of respondents applying DevOps

39%

61%

Yes No

2019

2018

64%

36%

47%

53%

Yes

No

22 | EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services

05 About the survey

05 About the survey

EY Norwegian Cloud Maturity Survey 2019 | Current and planned adoption of cloud services | 23

05 About the survey

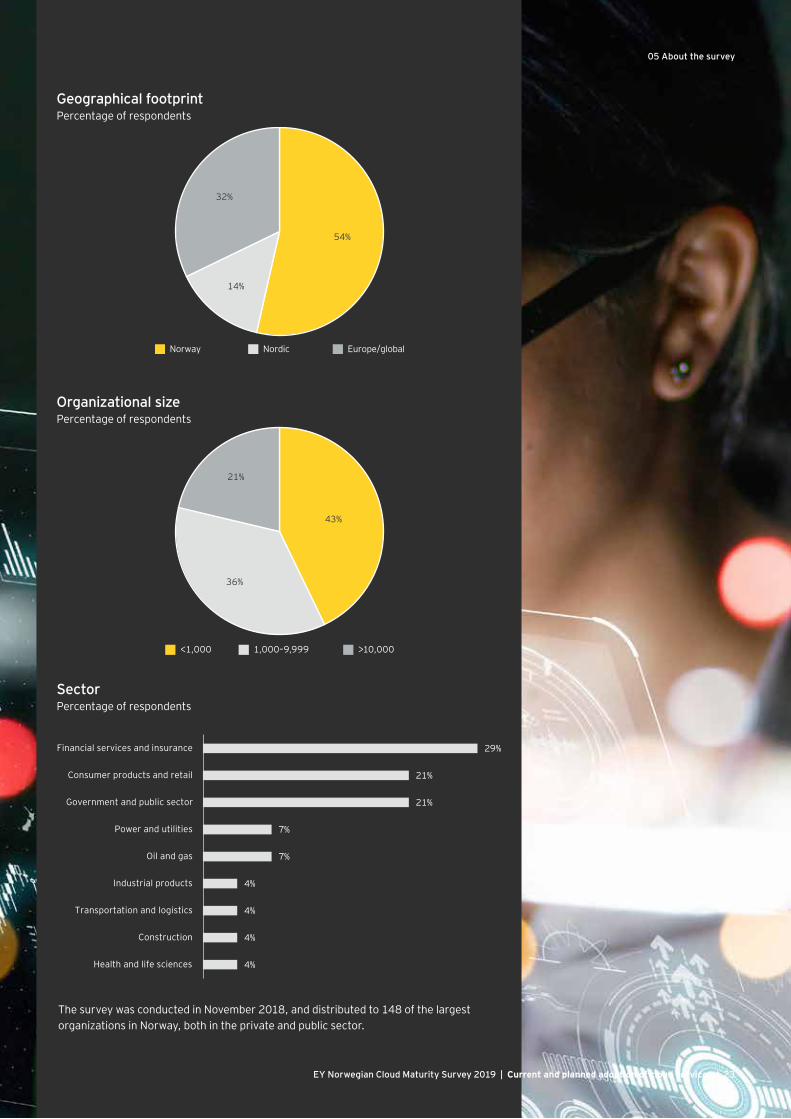

Geographical footprintPercentage of respondents

SectorPercentage of respondents

54%

14%

32%

Norway Nordic Europe/global

Organizational sizePercentage of respondents

43%

36%

21%

<1,000 1,000–9,999 >10,000

4%

4%

4%

4%

7%

7%

21%

21%

29%

Health and life sciences

Construction

Transportation and logistics

Industrial products

Oil and gas

Power and utilities

Government and public sector

Consumer products and retail

Financial services and insurance

The survey was conducted in November 2018, and distributed to 148 of the largest organizations in Norway, both in the private and public sector.

B190

01no

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2019 EYGM Limited. All Rights Reserved.

EYG no. 000028-19Gbl ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com

EY contacts

Christian MjaanesPartner Ernst & Young AS | Advisory | Technology Consulting+47 951 50 088 [email protected]

Sophus SlaattaDirector | Cloud ComputingErnst & Young AS | Advisory | Technology Consulting+47 408 56 [email protected]