Embed Size (px)

Citation preview

F5 Revision Test

Introduction

This revision test is made up of two documents:

1. This interactive PDF, which will allow you to answer section A and B questions presented in a similar format to the live exam

2. Aseparatespreadsheetand/orwordprocessingfile,whichwillallowyoutoanswersectionCquestionspresented in a similar format to the live exam

3. These two documents can be saved and then submitted together for marking.

Some important points to note are as follows:

• These documents cannot replicate the exact functionality of the live exam environment but will provide a similar exam experience

• The questions are presented in a way which closely mirrors, but is not the same as the live exam• If you have not done so already, please refer to the full specimen exam and other resources available at

www.accaglobal.com/uk/en/student/exam-support-resources.html• ThefullspecimenexamhasbeenpreparedbyACCA’sexaminingteamandreflectstheliveexamexperience

in terms of its structure, range of questions and functionality, and these resources should be a key part of your preparation for the exam.

The content for this F5 revision test has been provided by BPP Learning Media.

Instructions Section A

This section of the exam contains 15 objective test (OT) questions.

Each question is worth 2 marks and is compulsory.

This exam section is worth 30 marks in total.

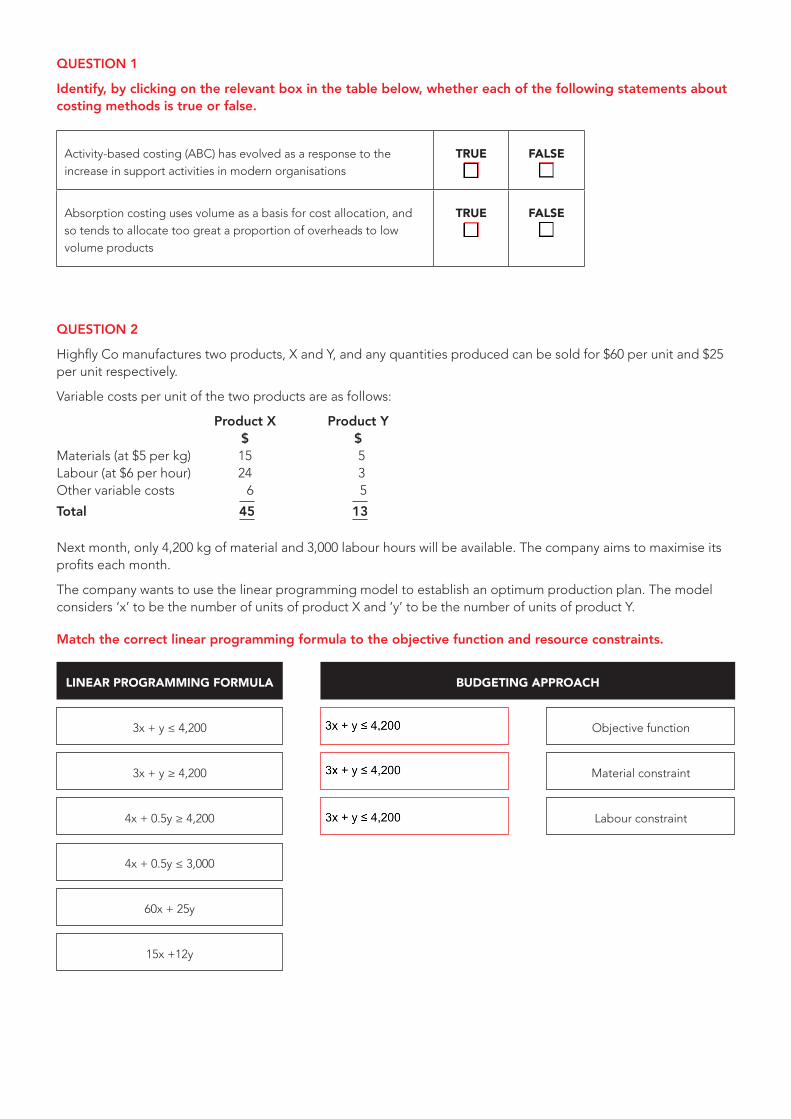

QUESTION 1

Identify, by clicking on the relevant box in the table below, whether each of the following statements about costing methods is true or false.

QUESTION 2

HighflyComanufacturestwoproducts,XandY,andanyquantitiesproducedcanbesoldfor$60perunitand$25per unit respectively.

Variable costs per unit of the two products are as follows:

Product X Product Y $ $Materials(at$5perkg) 15 5Labour(at$6perhour) 24 3Othervariablecosts 6 5

Total 45 13

Nextmonth,only4,200kgofmaterialand3,000labourhourswillbeavailable.Thecompanyaimstomaximiseitsprofitseachmonth.

The company wants to use the linear programming model to establish an optimum production plan. The model considers‘x’tobethenumberofunitsofproductXand‘y’tobethenumberofunitsofproductY.

Match the correct linear programming formula to the objective function and resource constraints.

Activity-basedcosting(ABC)hasevolvedasaresponsetotheincrease in support activities in modern organisations

TRUE FALSE

Absorption costing uses volume as a basis for cost allocation, and so tends to allocate too great a proportion of overheads to low volume products

TRUE FALSE

LINEAR PROGRAMMING FORMULA BUDGETING APPROACH

3x+y≤4,200

3x+y≥4,200

4x+0.5y≥4,200

4x+0.5y≤3,000

60x+25y

15x+12y

Objective function

Material constraint

Labour constraint

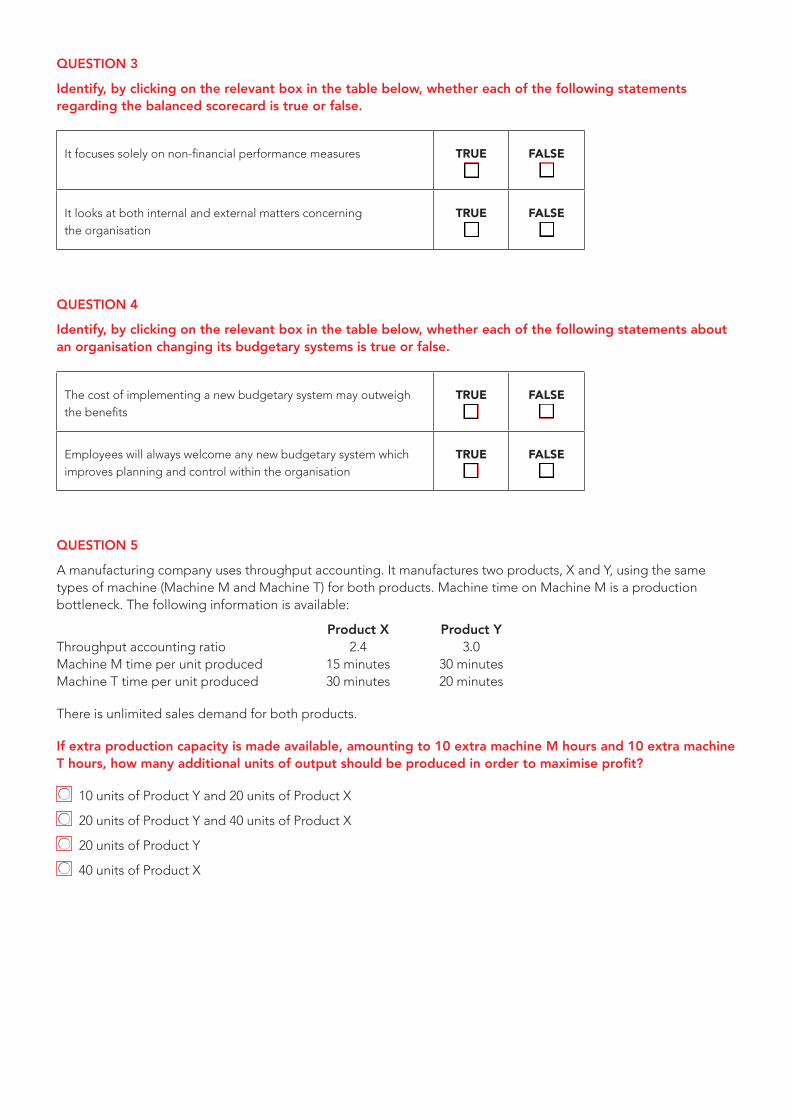

QUESTION 3

Identify, by clicking on the relevant box in the table below, whether each of the following statements regarding the balanced scorecard is true or false.

QUESTION 4

Identify, by clicking on the relevant box in the table below, whether each of the following statements about an organisation changing its budgetary systems is true or false.

QUESTION 5

Amanufacturingcompanyusesthroughputaccounting.Itmanufacturestwoproducts,XandY,usingthesametypes of machine (Machine M and Machine T) for both products. Machine time on Machine M is a production bottleneck. The following information is available:

Product X Product YThroughputaccountingratio 2.4 3.0MachineMtimeperunitproduced 15minutes 30minutesMachineTtimeperunitproduced 30minutes 20minutes

There is unlimited sales demand for both products.

If extra production capacity is made available, amounting to 10 extra machine M hours and 10 extra machine T hours, how many additional units of output should be produced in order to maximise profit?

10unitsofProductYand20unitsofProductX

20unitsofProductYand40unitsofProductX

20unitsofProductY

40unitsofProductX

Itfocusessolelyonnon-financialperformancemeasures TRUE FALSE

It looks at both internal and external matters concerning the organisation

TRUE FALSE

The cost of implementing a new budgetary system may outweigh thebenefits

TRUE FALSE

Employees will always welcome any new budgetary system which improves planning and control within the organisation

TRUE FALSE

QUESTION 6

A company has entered two different new markets.

In market A, it is initially charging low prices so as to gain rapid market share while demand is relatively elastic.

In market B, it is initially charging high prices so as to earn maximum profits while demand is relatively inelastic.

Which price strategy is the company using in each market?

Penetration pricing in market A and price skimming in market B

Price discrimination in market A and penetration pricing in market B

Price skimming in market A and penetration pricing in market B

Price skimming in market A and price discrimination in market B

QUESTION 7

Which TWO of the following are controls which help to ensure the security of highly confidential information?

Data encryption

Mandatory fields

Hierarchical passwords

Range checks

QUESTION 8

Total production costs in a month where 900 units are produced are $58,200 and total production costs in a month

where 1,200 units are produced are $66,600.

The variable cost per unit is constant up to a production level of 2,000 units per month. A step up of $6,000 occurs

in total fixed costs when production reaches 1,100 units per month.

What is the total production cost for a month when 1,000 units are produced?

$

QUESTION 9

S Company is a manufacturer of multiple products and uses target costing. It has been noted that Product Pcurrently has a target cost gap and the company wishes to close this gap.

Which of the following may be used to close the target cost gap for product P?

Use overtime to complete work ahead of the planned schedule

Substitute current materials with cheaper alternatives of the same quality

Increase the selling price of Product P

Negotiate a cheaper rent agreement for S Company’s premises

QUESTION 10

Identify, by clicking on the relevant box in the table below, whether each of the following statements about management information systems (MIS) is true or false.

QUESTION 11

The following are some of the areas which require control within a division.

(i) Generation of revenues(ii) Investment in non-current assets(iii) Investment in working capital(iv) Apportionedheadofficecosts

Which of the above does the manager have control over in an investment centre?

i, ii and iii only

ii, iii and iv only

i, ii and iv only

All of the above

QUESTION 12

Aninvestmentcentreinamanufacturinggroupproducedthefollowingresultsinthepreviousfinancialyear:

$’000Operatingprofit 360Capitalemployed:non-currentassets 1,500Currentassets 100

For the purpose of performance measurement, non-current assets are valued at cost. The investment centre is consideringanewinvestmentthatwillincreaseannualoperatingprofitby$25,000,andwillrequireaninvestmentof$100,000inanon-currentassetandanadditional$30,000inworkingcapital.

Will the performance measurement criteria of (1) return on investment (ROI) and (2) residual income (RI) motivate the centre manager to undertake the investment? Assume a notional capital charge of 18% on divisional capital.

ROI RI

Yes Yes

Yes No

No Yes

No No

They are designed to report on existing operations TRUE FALSE

They will have an external focus TRUE FALSE

QUESTION 13

For a charitable organisation providing relief services to under-developed economies, which one of the following performance measures would be the most suitable measurement of the effectiveness in the use of the charity’s aid funds?

Percentage of funds spent on frontline activities

Ratio of volunteer helpers to full-time employees in the organisation

Size of operating surplus (fund income less expenditure)

Total spending by the charity on its operations

QUESTION 14

A company introduced Product C to the market 12 months ago and is now about to enter the maturity stage ofits life cycle. The maturity stage is expected to last for three months. The Director of Sales and Marketing has suggested four possible prices that the company could charge during the next three months. The following table shows the results of some market research into the level of weekly demand at alternative prices:

Selling price per unit $300 $255 $240 $225 Weekly demand (units) 1,800 2,400 3,600 4,200

Each unit of product C has a variable cost of $114 and takes one standard hour to produce.

Which selling price will maximise the weekly profit during this stage of the product life cycle?

Select:

QUESTION 15

A company has received a special order for which it is considering the use of material B which it has held in its inventory for some time. This inventory of 945 kg was bought at $4.50 per kg. The special order requires 1,500 kg ofmaterial B. If the inventory is not used for this order, it would be sold for $2.75 per kg. The current price of materialB is $4.25 per kg.

What is the total relevant cost of material B for the special order (to 2 decimal places)?

$

Section B

This section of the exam contains three OT cases.

Each OT case contains a scenario which relates to five OT questions.

Each question is worth 2 marks and is compulsory.

This exam section is worth 30 marks in total.

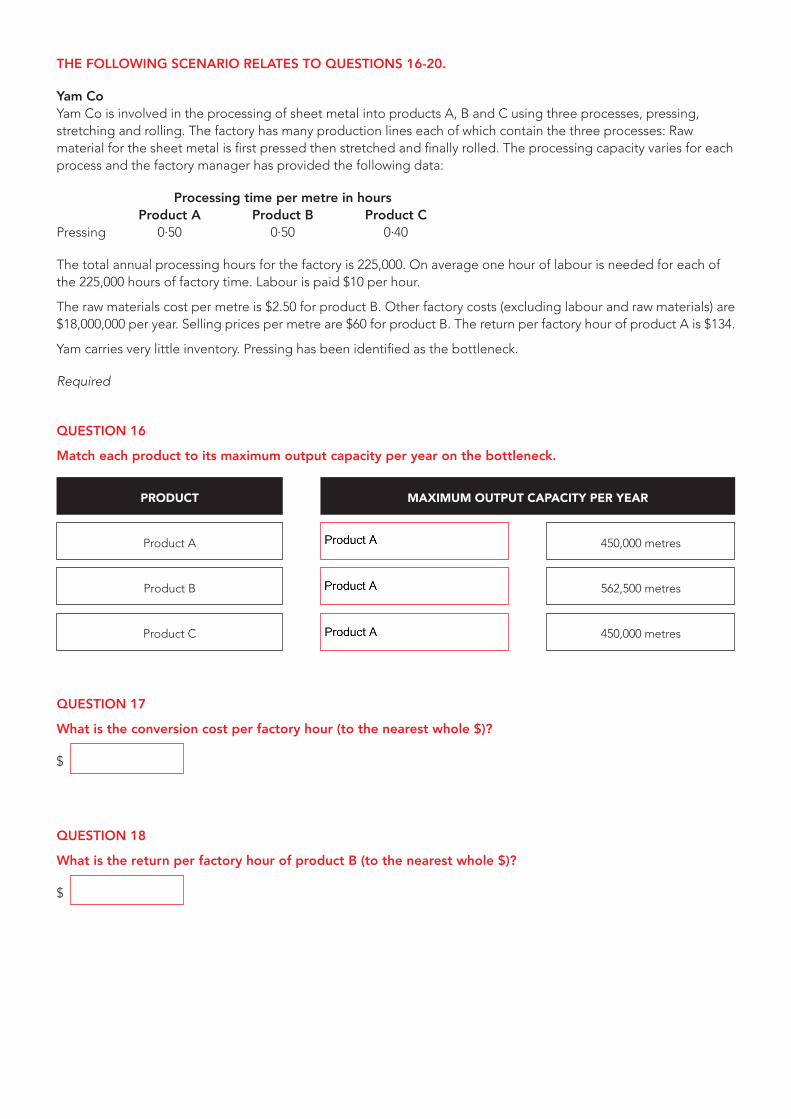

THE FOLLOWING SCENARIO RELATES TO QUESTIONS 16-20.

Yam Co YamCoisinvolvedintheprocessingofsheetmetalintoproductsA,BandCusingthreeprocesses,pressing,stretching and rolling. The factory has many production lines each of which contain the three processes: Raw materialforthesheetmetalisfirstpressedthenstretchedandfinallyrolled.Theprocessingcapacityvariesforeachprocess and the factory manager has provided the following data:

Processing time per metre in hours Product A Product B Product CPressing 0·50 0·50 0·40

Thetotalannualprocessinghoursforthefactoryis225,000.Onaverageonehouroflabourisneededforeachofthe225,000hoursoffactorytime.Labourispaid$10perhour.

Therawmaterialscostpermetreis$2.50forproductB.Otherfactorycosts(excludinglabourandrawmaterials)are$18,000,000peryear.Sellingpricespermetreare$60forproductB.ThereturnperfactoryhourofproductAis$134.

Yamcarriesverylittleinventory.Pressinghasbeenidentifiedasthebottleneck.

Required

QUESTION 16

Match each product to its maximum output capacity per year on the bottleneck.

QUESTION 17

What is the conversion cost per factory hour (to the nearest whole $)?

$

QUESTION 18

What is the return per factory hour of product B (to the nearest whole $)?

$

PRODUCT MAXIMUM OUTPUT CAPACITY PER YEAR

Product A

Product B

ProductC

450,000metres

562,500metres

450,000metres

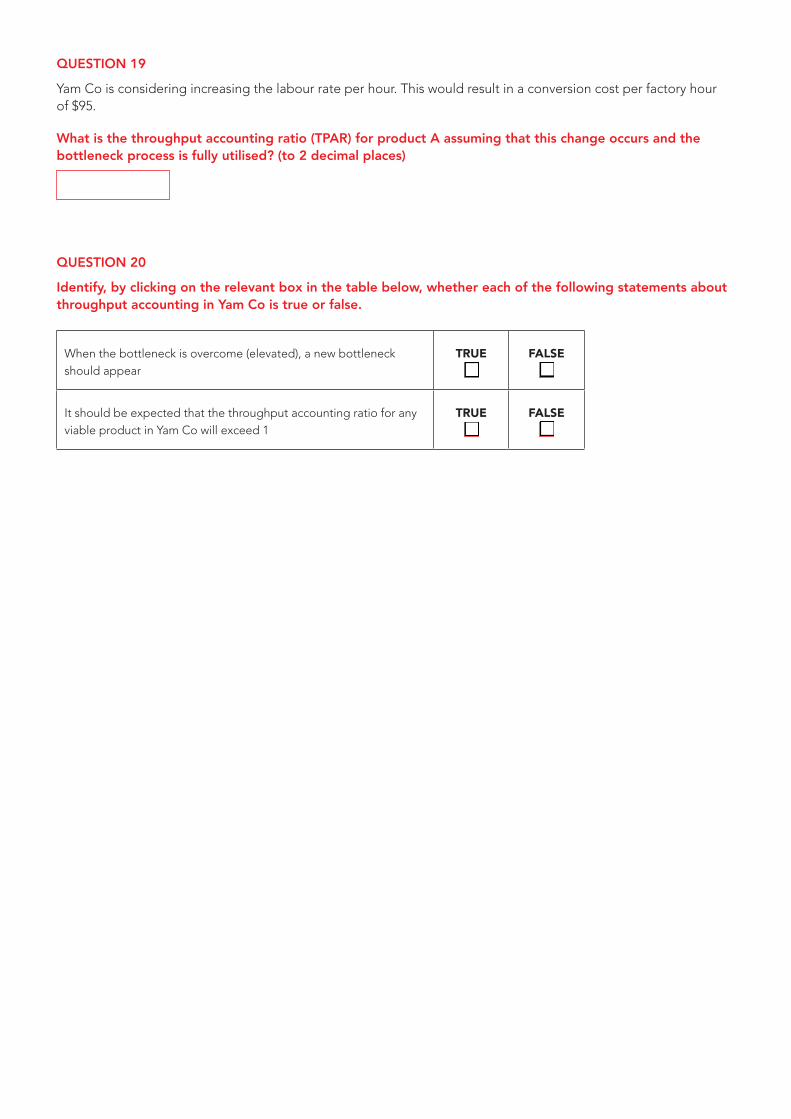

QUESTION 19

YamCoisconsideringincreasingthelabourrateperhour.Thiswouldresultinaconversioncostperfactoryhour of$95.

What is the throughput accounting ratio (TPAR) for product A assuming that this change occurs and the bottleneck process is fully utilised? (to 2 decimal places)

QUESTION 20

Identify, by clicking on the relevant box in the table below, whether each of the following statements about throughput accounting in Yam Co is true or false.

When the bottleneck is overcome (elevated), a new bottleneck should appear

TRUE FALSE

It should be expected that the throughput accounting ratio for any viableproductinYamCowillexceed1

TRUE FALSE

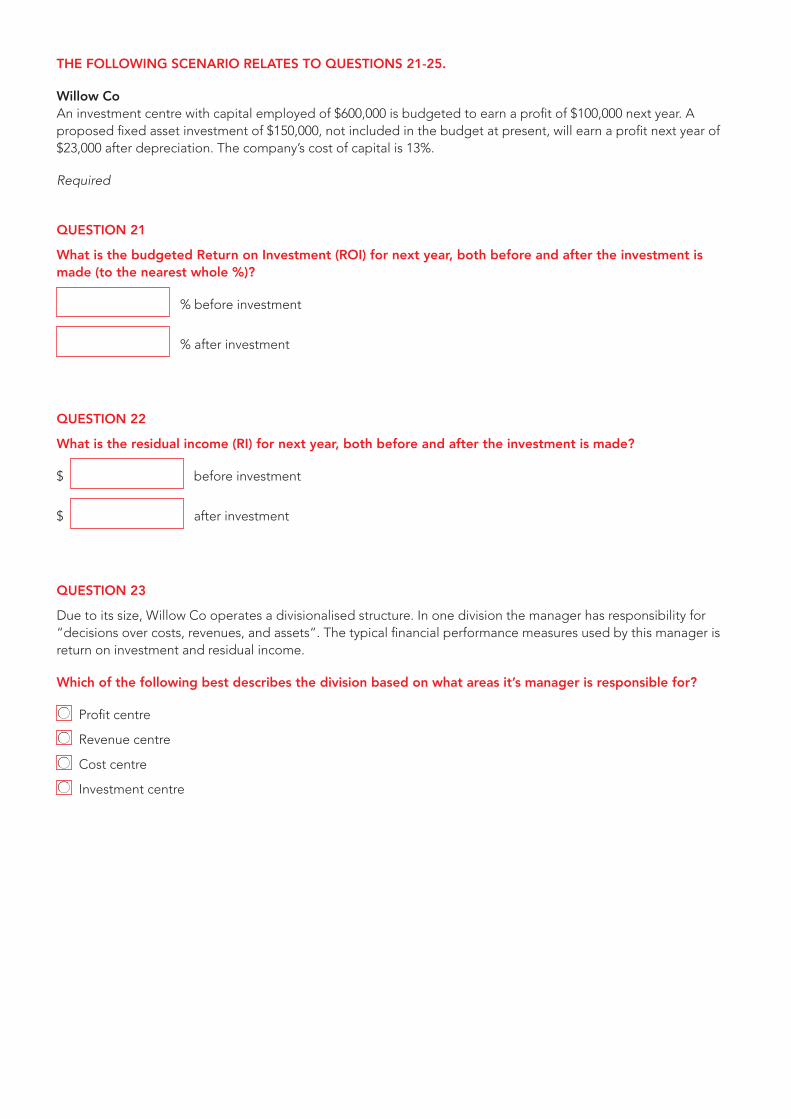

THE FOLLOWING SCENARIO RELATES TO QUESTIONS 21-25.

Willow Co

An investment centre with capital employed of $600,000 is budgeted to earn a profit of $100,000 next year. Aproposed fixed asset investment of $150,000, not included in the budget at present, will earn a profit next year of$23,000 after depreciation. The company’s cost of capital is 13%.

Required

QUESTION 21

What is the budgeted Return on Investment (ROI) for next year, both before and after the investment is made (to the nearest whole %)?

% before investment

% after investment

QUESTION 22

What is the residual income (RI) for next year, both before and after the investment is made?

$ before investment

$ after investment

QUESTION 23

Due to its size, Willow Co operates a divisionalised structure. In one division the manager has responsibility for“decisions over costs, revenues, and assets”. The typical financial performance measures used by this manager isreturn on investment and residual income.

Which of the following best describes the division based on what areas it’s manager is responsible for?

Profit centre

Revenue centre

Cost centre

Investment centre

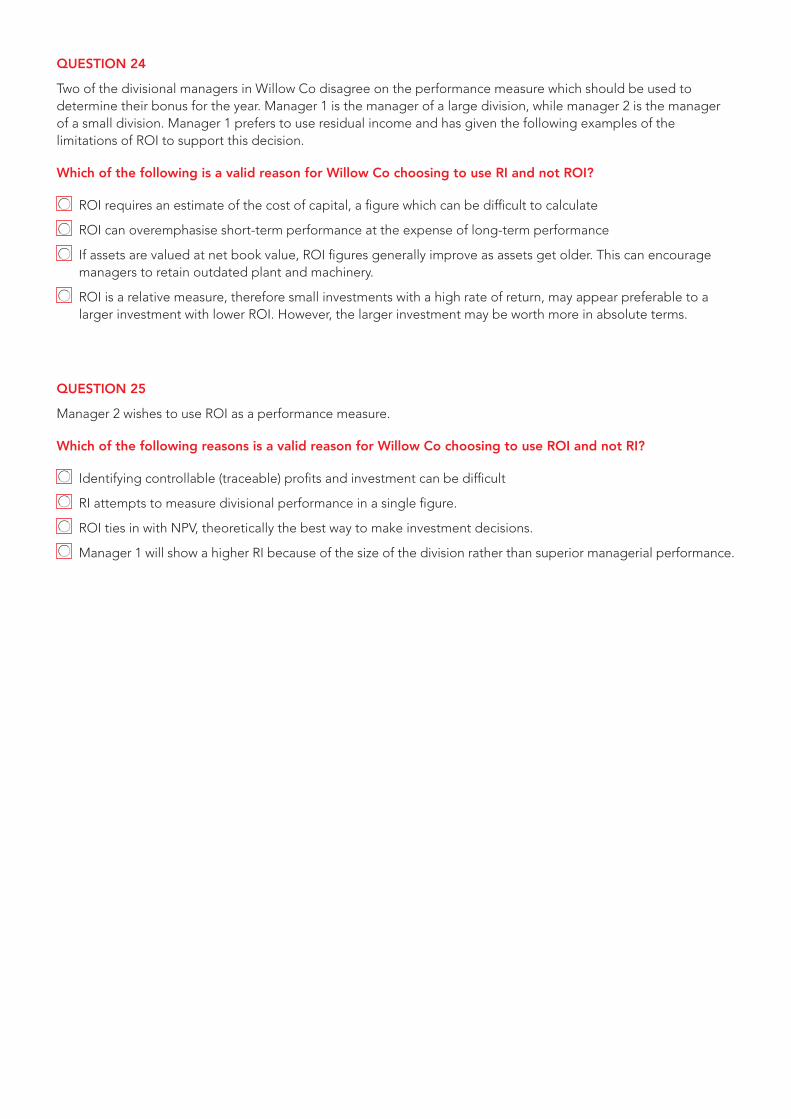

QUESTION 24

Two of the divisional managers in Willow Co disagree on the performance measure which should be used todetermine their bonus for the year. Manager 1 is the manager of a large division, while manager 2 is the manager of a small division. Manager 1 prefers to use residual income and has given the following examples of the limitations of ROI to support this decision.

Which of the following is a valid reason for Willow Co choosing to use RI and not ROI?

ROI requires an estimate of the cost of capital, a figure which can be difficult to calculate

ROI can overemphasise short-term performance at the expense of long-term performance

If assets are valued at net book value, ROI figures generally improve as assets get older. This can encouragemanagers to retain outdated plant and machinery.

ROI is a relative measure, therefore small investments with a high rate of return, may appear preferable to a larger investment with lower ROI. However, the larger investment may be worth more in absolute terms.

QUESTION 25

Manager 2 wishes to use ROI as a performance measure.

Which of the following reasons is a valid reason for Willow Co choosing to use ROI and not RI?

Identifying controllable (traceable) profits and investment can be difficult

RI attempts to measure divisional performance in a single figure.

ROI ties in with NPV, theoretically the best way to make investment decisions.

Manager 1 will show a higher RI because of the size of the division rather than superior managerial performance.

THE FOLLOWING SCENARIO RELATES TO QUESTIONS 26-30.

Kiss Co KissCohasdevelopedanewproduct.Thefirstbatchof200unitswilltake3,500labourhourstoproduce.Therewillbean75%learningcurvethatwillcontinueuntil4,800unitshavebeenproduced.Batchesafterthislevelwilleachtakethesameamountoftimeasthe24thbatch.Thebatchsizewillalwaysbe200units.

Note.Thelearningindexforan75%learningcurveis-0.415

Ignore the time value of money.

QUESTION 26

Calculate the time taken for the 24th batch (to the nearest hour).

QUESTION 27

Thetotaltimeforthefirst16batchesofunitswas22,000hours.

What was the actual learning rate (to the nearest whole %)?

QUESTION 28

KissComakesanotherproduct,theLyco.Thelearningeffectstoppedafterthe16thbatchoftheproduct,whichwaswhena‘steadystate’wasreached.WorkersinKissCoreceived$15perhour.ThefirstbatchofLycotook0.75hourstoproduce.The16thbatchofLycotook0.5hours,andthestandardcostwasrevisedtothisfigureoncethe‘steadystate’wasreached.KissCoproduced10,000batchesofLycoduringtheyear.

What is the favourable labour efficiency planning variance?

$

QUESTION 29

Identify, by clicking on the relevant box in the table below, whether each of the following statements made about Kiss Co is true or false.

QUESTION 30

In which of the following ways might an operational manager in Kiss Co try to improve labour efficiency and achieve favourable labour efficiency variances?

Increase output volumes

Increase inspection and testing of products

Provide workers with training

Arrange for overtime working

Asaresultofthelearningeffect,thelabourefficiencyplanningvariance of Lyco should always be favourable

TRUE FALSE

A standard labour cost should only be established when a ‘steady state’isreached

TRUE FALSE

Section C

Please now refer to the separate spreadsheet and/or word processing file to complete Section C questions.