Embed Size (px)

Citation preview

2

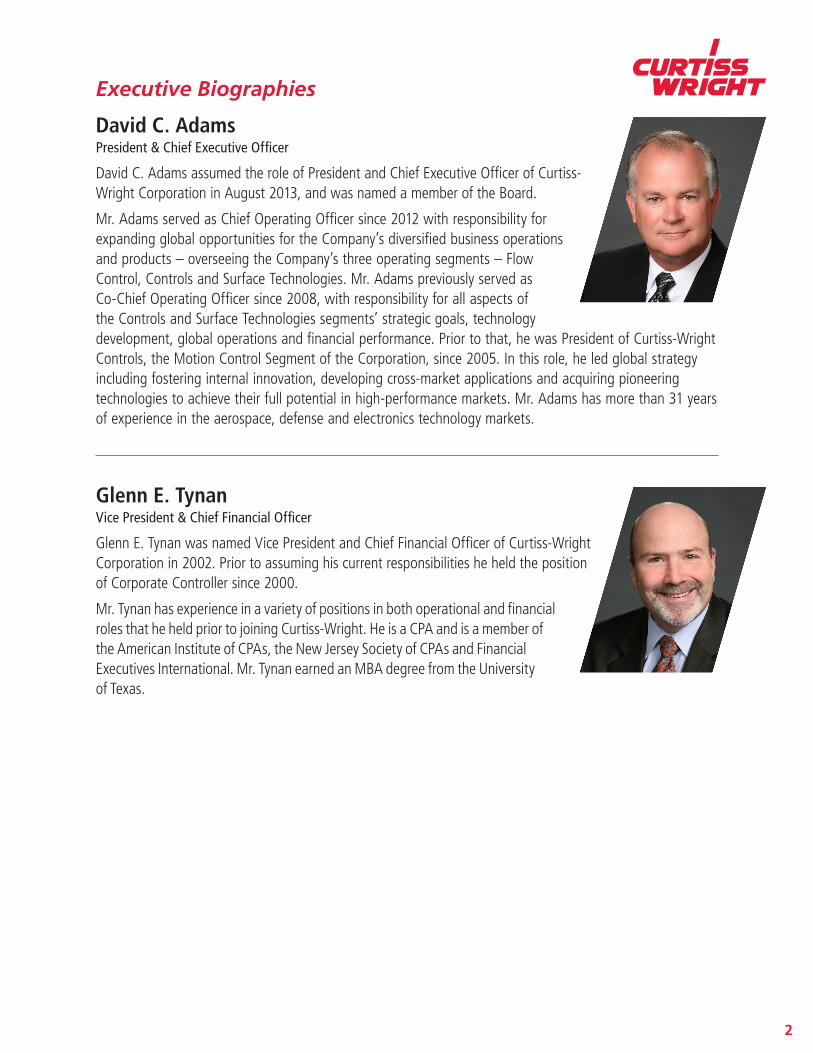

Executive Biographies

David C. AdamsPresident & Chief Executive Officer

David C. Adams assumed the role of President and Chief Executive Officer of Curtiss-Wright Corporation in August 2013, and was named a member of the Board.

Mr. Adams served as Chief Operating Officer since 2012 with responsibility for expanding global opportunities for the Company’s diversified business operations and products – overseeing the Company’s three operating segments – Flow Control, Controls and Surface Technologies. Mr. Adams previously served as Co-Chief Operating Officer since 2008, with responsibility for all aspects of the Controls and Surface Technologies segments’ strategic goals, technology development, global operations and financial performance. Prior to that, he was President of Curtiss-Wright Controls, the Motion Control Segment of the Corporation, since 2005. In this role, he led global strategy including fostering internal innovation, developing cross-market applications and acquiring pioneering technologies to achieve their full potential in high-performance markets. Mr. Adams has more than 31 years of experience in the aerospace, defense and electronics technology markets.

Glenn E. TynanVice President & Chief Financial Officer

Glenn E. Tynan was named Vice President and Chief Financial Officer of Curtiss-Wright Corporation in 2002. Prior to assuming his current responsibilities he held the position of Corporate Controller since 2000.

Mr. Tynan has experience in a variety of positions in both operational and financial roles that he held prior to joining Curtiss-Wright. He is a CPA and is a member of the American Institute of CPAs, the New Jersey Society of CPAs and Financial Executives International. Mr. Tynan earned an MBA degree from the University of Texas.

3

Certain statements made in this informational packet, including statements about future revenue, financial performance guidance, quarterly and annual revenue, net income, operating income growth, future business opportunities, cost saving initiatives, the successful integration of our acquisitions, and future cash flow from operations, are forwardlooking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements present management’s expectations, beliefs, plans and objectives regarding future financial performance, and assumptions or judgments concerning such performance. Any discussions contained in this informational packet, except to the extent that they contain historical facts, are forward-looking and accordingly involve estimates, assumptions, judgments and uncertainties. Such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those expressed or implied. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Such risks and uncertainties include, but are not limited to: a reduction in anticipated orders; an economic downturn; changes in competitive marketplace and/ or customer requirements; a change in government spending; an inability to perform customer contracts at anticipated cost levels; and other factors that generally affect the business of aerospace, defense contracting, electronics, marine, and industrial companies. Such factors are detailed in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2012, and subsequent reports filed with the Securities and Exchange Commission.

Forward Looking Statements

4

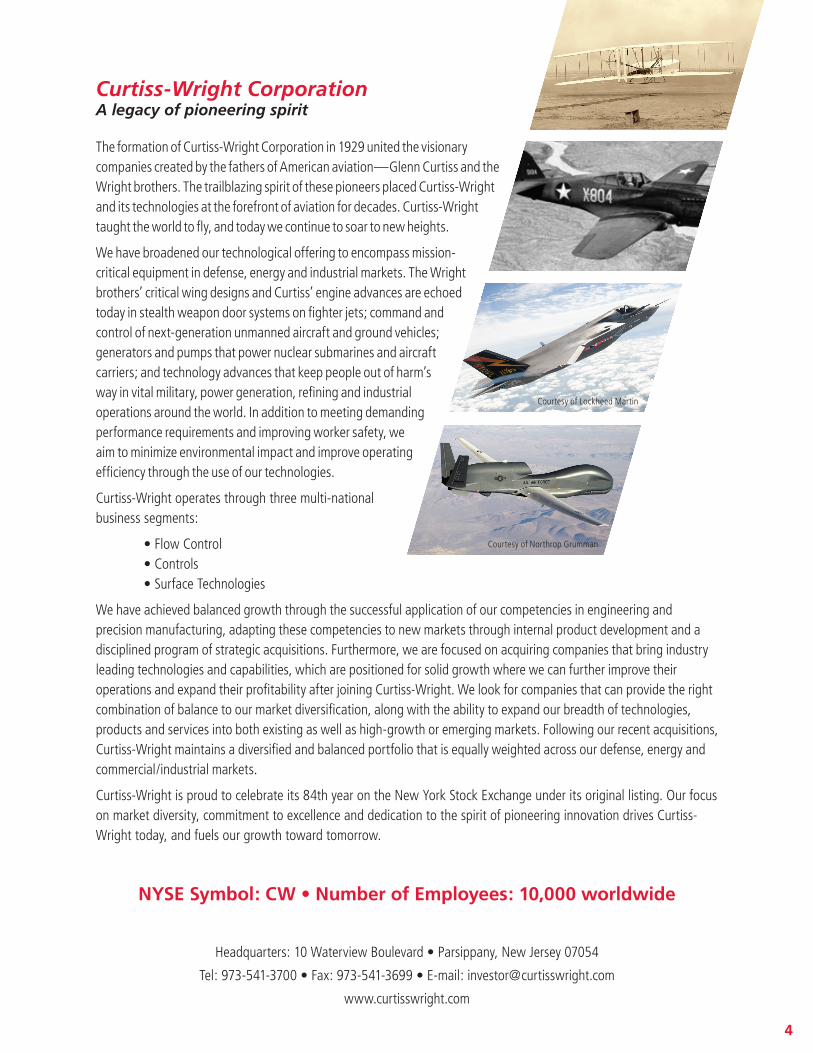

Curtiss-Wright CorporationA legacy of pioneering spirit

The formation of Curtiss-Wright Corporation in 1929 united the visionary companies created by the fathers of American aviation—Glenn Curtiss and the Wright brothers. The trailblazing spirit of these pioneers placed Curtiss-Wright and its technologies at the forefront of aviation for decades. Curtiss-Wright taught the world to fly, and today we continue to soar to new heights.

We have broadened our technological offering to encompass mission-critical equipment in defense, energy and industrial markets. The Wright brothers’ critical wing designs and Curtiss’ engine advances are echoed today in stealth weapon door systems on fighter jets; command and control of next-generation unmanned aircraft and ground vehicles; generators and pumps that power nuclear submarines and aircraft carriers; and technology advances that keep people out of harm’s way in vital military, power generation, refining and industrial operations around the world. In addition to meeting demanding performance requirements and improving worker safety, we aim to minimize environmental impact and improve operating efficiency through the use of our technologies.

Curtiss-Wright operates through three multi-national business segments:

• Flow Control• Controls• Surface Technologies

We have achieved balanced growth through the successful application of our competencies in engineering and precision manufacturing, adapting these competencies to new markets through internal product development and a disciplined program of strategic acquisitions. Furthermore, we are focused on acquiring companies that bring industry leading technologies and capabilities, which are positioned for solid growth where we can further improve their operations and expand their profitability after joining Curtiss-Wright. We look for companies that can provide the right combination of balance to our market diversification, along with the ability to expand our breadth of technologies, products and services into both existing as well as high-growth or emerging markets. Following our recent acquisitions, Curtiss-Wright maintains a diversified and balanced portfolio that is equally weighted across our defense, energy and commercial/industrial markets.

Curtiss-Wright is proud to celebrate its 84th year on the New York Stock Exchange under its original listing. Our focus on market diversity, commitment to excellence and dedication to the spirit of pioneering innovation drives Curtiss-Wright today, and fuels our growth toward tomorrow.

NYSE Symbol: CW • Number of Employees: 10,000 worldwide

Headquarters: 10 Waterview Boulevard • Parsippany, New Jersey 07054

Tel: 973-541-3700 • Fax: 973-541-3699 • E-mail: [email protected]

www.curtisswright.com

Courtesy of Lockheed Martin

Courtesy of Northrop Grumman

5

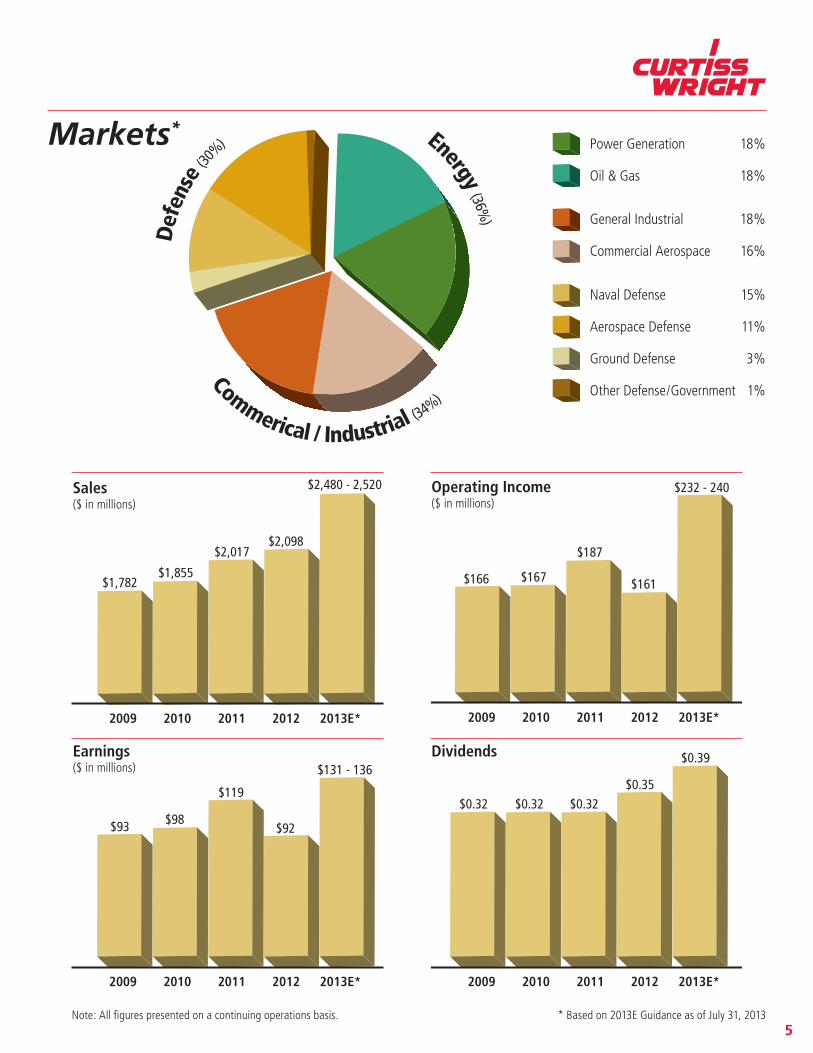

Markets*

Note: All figures presented on a continuing operations basis.

Def

ense

(30

%)

Energy (36%)

Commerical / Industrial (34%)

$2,098

$2,480 - 2,520

$1,855$1,782

$2,017

2012 2013E*20102009 2011

Sales($ in millions)

2012 2013E*20102009 2011

Earnings($ in millions)

$92

$131 - 136

$98$93

$119

$161

$232 - 240

$167$166

$187

2012 2013E*20102009 2011

Operating Income($ in millions)

2012 2013E*20102009 2011

Dividends

$0.35

$0.39

$0.32 $0.32 $0.32

Naval Defense 15%

Aerospace Defense 11%

Ground Defense 3%

Other Defense/Government 1%

Power Generation 18%

Oil & Gas 18%

General Industrial 18%

Commercial Aerospace 16%

* Based on 2013E Guidance as of July 31, 2013

6

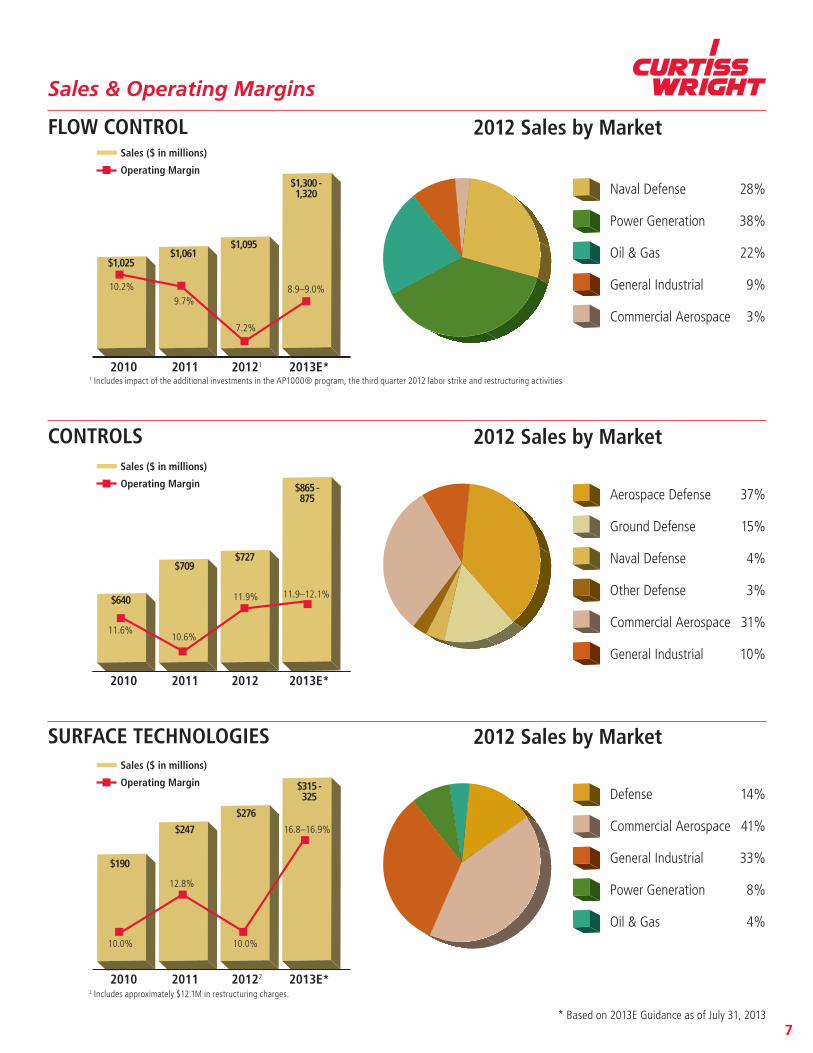

Curtiss-Wright Business Segments — At a Glance

FLOW CONTROLOur Flow Control segment designs and manufactures highly engineered, critical-function products that

manage the flow of liquids and gases, generate power, provide electronic operating systems and monitor or provide vital functions. Products include:

• High-performance pumps, motors, generators, power conditioning electronics, electronic control integration and protection solutions for defense, power generation, oil and gas and general industrial markets.

• Engineered solutions supporting critical components, systems integration and qualification/ dedication for operating nuclear reactors and for new plant construction. Customers include the global power generation industry, original equipment manufacturers, nuclear steam supply system suppliers, engineering-procurement-construction firms and the U.S. Department of Energy.

• Specialized valves, heavy-wall pressure vessels, valve automation and control systems, coke unheading systems and fluidic catalytic cracking unit components for the oil and gas refining and petrochemical industries. Production, processing and environmental equipment and solutions serving upstream oil and gas, and fracking operations.

• Shipboard helicopter and cable handling systems for naval defense, and ground support vehicles for commercial aviation.

• Electronic instrumentation and control equipment for naval defense and commercial processing.

CONTROLSOur Controls segment integrates complex elements for use in flight control, actuation and drive systems,

sensing and electronic computing system applications. Products include:

• Rugged deployed commercial off-the-shelf (COTS) open standards based electronics boards and subsystems for demanding computing, networking and data processing applications, as well as custom software design and hardware manufacturing for aerospace, ground and naval defense markets.

• Integrated electronics for defense, aerospace and general industrial applications including motion control, network-centric computing, vehicle management, sensor management, power management, high-speed data recording and storage and electro-mechanical solutions.

• Programmable controllers and drives for electric-powered vehicles operating in industrial and medical markets. Sensors, electronic throttle controls and joysticks for on- and off-highway vehicles and heavy trucks.

• Electro-mechanical, electro-hydraulic and hydro-mechanical actuation control components and systems for defense and commercial aerospace applications such as trailing and leading-edge flap actuators for passenger aircraft, weapons handling systems, weapons bay door drive systems, lead edge flight controls and canopy actuators for military fighter aircraft.

• Position, pressure and temperature sensors; smoke and ice detection sensors; solenoids and solenoid valves; air data computers; flight data recorders and joysticks for defense and commercial aerospace, along with general industrial markets.

SURFACE TECHNOLOGIESOur Surface Technologies segment provides highly technical services that enhance the performance and

extend the life of critical components in the commercial aerospace, general industrial, energy and defense markets. Services include:

• Shot and laser peening processes impart beneficial stresses to metal components to increase resistance to fatigue and stress failure.

• Specialty coatings provide a range of end-use properties tailored to a component’s operating environment.

• Materials testing confirms physical and metallurgical properties during the design phase of the manufacturing cycle, as well as quality assurance and finished goods testing during the production phase. Our expertise in failure analysis aids customers in identifying and solving surface treatment issues.

For more information, visit: www.cwfc.com

For more information, visit: www.cwcontrols.com

For more information, visit: www.cwst.com

7

Sales & Operating Margins

1 Includes impact of the additional investments in the AP1000® program, the third quarter 2012 labor strike and restructuring activities

2 Includes approximately $12.1M in restructuring charges.

FLOW CONTROL

CONTROLS

SURFACE TECHNOLOGIES

Sales ($ in millions)

Operating Margin

20121 2013E*2010 2011

10.2%9.7%

7.2%

8.9–9.0%

$1,095

$1,300 - 1,320

$1,025$1,061

Sales ($ in millions)

Operating Margin

2012 2013E*2010 2011

11.6%10.6%

11.9% 11.9–12.1%

$727

$865 - 875

$640

$709

Sales ($ in millions)

Operating Margin

10.0% 10.0%

16.8–16.9%

12.8%

20122 2013E*2010 2011

$276

$315 - 325

$190

$247

Naval Defense 28%

Power Generation 38%

Oil & Gas 22%

General Industrial 9%

Commercial Aerospace 3%

Aerospace Defense 37%

Ground Defense 15%

Naval Defense 4%

Other Defense 3%

Commercial Aerospace 31%

General Industrial 10%

Defense 14%

Commercial Aerospace 41%

General Industrial 33%

Power Generation 8%

Oil & Gas 4%

2012 Sales by Market

2012 Sales by Market

2012 Sales by Market

* Based on 2013E Guidance as of July 31, 2013

8

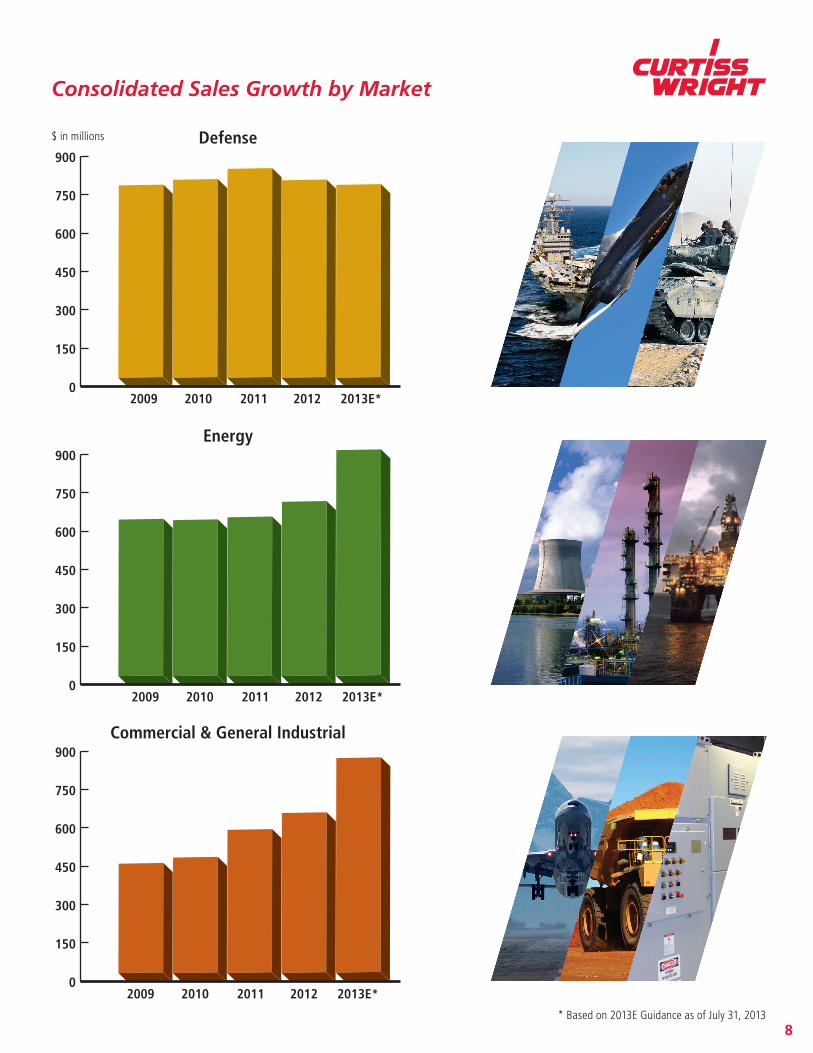

Consolidated Sales Growth by Market

Commercial & General Industrial

Energy

Defense

0

150

300

450

600

750

900

2012 2013E*2010 20112009

0

150

300

450

600

750

900

2012 2013E*2010 20112009

0

150

300

450

600

750

900

2012 2013E*2010 20112009

$ in millions

* Based on 2013E Guidance as of July 31, 2013