Embed Size (px)

Citation preview

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

The views expressed in this presentation are those of the presenter. Official positions of the FASB are reached only after extensive due process and deliberations

FASB Update Russ Golden, FASB Chairman

May 11, 2018 University of Washington Financial Reporting Conference

Revenue Recognition: Implementation Progress

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Technical inquiries & TRG activities

Advisory group discussions (status/efforts, look-backs)

Engagement with external committees, regulators, and stakeholders

Various educational activities: webcasts/podcasts targeting preparers, auditors, and investors

Rev Rec: Implementation Support

3

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

MARCH 20 MEETING: Focused on initial/recurring costs of public co. transition

FEEDBACK: Some preparers/practitioners, initial level of effort to apply:

- Need to review all contracts or revenue streams - Some costs minimized because the information technology

systems did not need to be modified.

FASAC Post-Effective Date Assessment of Cost-Benefits

4

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Ongoing discussions with: PCC (informal meetings and 4 formal meetings a year)

AICPA PCPS Technical Issues Committee – we have a liaison meeting with them at least once a year and the staff is talks to them every time they convene for a meeting (~5 times a year).

Private Company Town Halls (2-3 Town Halls per year).

Webcasts

Rev Rec Monitoring/Implementation: Private Companies

5

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Monitoring Diversity

Post-Effective Date Assessment of Costs - One-Time Transition Costs - Ongoing Costs

Post-Effective Date Assessment of Benefits

Future Plans

6

Leases

77

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Leases: Transition

24

Current Transition

Feedback

New Transition Added

• Recognize leases on balance sheet for all periods • Provide new lease disclosures for all periods • Some relief provided with “run-off” approach for existing leases

• Unanticipated costs and complexity related to comparative periods • Examples: disclosures, tracking of FX rates

• Initially apply new leases guidance at effective date • Still gets leases on balance sheet at effective date • Changes when new leases guidance is initially applied,

not how

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Leases: Practical Expedients

24

Example existing practical expedients

New practical expedients coming…

Short-term lease practical expedient

Lessee practical expedient on not separating lease and nonlease components

Lessor practical expedient on not separating lease and nonlease components

Land easements transition practical expedient

PURPOSE: Provide relief from application of leases guidance when appropriate (i.e., costs versus benefits)

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Leases: Other Issues

Exclude from consideration taxes imposed on and concurrent with a specific revenue-producing transaction that are collected by the lessor from a lessee

Exclude certain lessor costs (e.g., insurance) from variable consideration when lessor costs are paid by lessees and uncertainty in amount paid will not be resolved

Lessor issues – practical expedients coming…(consistent with Topic 606)

10

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

SAB 74 disclosures on possible impact of application

FASB available for implementation questions

Leases Timeline

1/19 2/16

Standard issued Mandatory effective date

11

Credit Losses

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Presentations to preparers & practitioners at events

FASB sponsored webcast – July 2016

Educational presentations in association with regulator staff/ constituent training

Participation in webcasts sponsored by other organizations (example: American Banker)

Quarterly meetings with federal banking agencies and Conference of State Bank Supervisors, along with presentations at training sessions

Participation in industry meetings or seminars with credit risk managers

Credit Losses: Education

13

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Convened in early 2016, before final standard issued Effort to improve confusing words and phrases before issued Should reduce need for technical corrections

PURPOSE: Solicit, analyze, and discuss stakeholder issues arising from implementation of new guidance Inform the FASB about those implementation issues

Help Board determine what, if any, action will be needed to address those issues

Provide forum for stakeholders to learn about new guidance from others involved with implementation

Credit Losses: Transition Resource Group

14

Next TRG meeting: Monday, June 11, 8:30 a.m. – 4 p.m. EDT

Disclosure Framework

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Improving the effectiveness of notes requires both:

16

Disclosure Framework: Two Components

Appropriate exercise of discretion by reporting entities when

assessing disclosure requirements

Phase II: Entity’s Decision Process

Consistent considerations by the Board in each standard-setting

activity

Phase I: Board’s Decision Process

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

In the coming months, FASB will issue four final documents intended to improve the effectiveness of disclosures in notes to financial statements. They include:

A new chapter in the FASB’s conceptual framework on disclosures

An update to an existing chapter of the conceptual framework that aligns the FASB’s definition of materiality with other definitions in the financial reporting system

An update to Fair Value Measurement disclosure requirements.

An update to Defined Benefit Plan disclosure requirements.

Next steps

17

1

2

3

4

Agenda Consultation

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Segment Reporting

Financial Performance Reporting

Liabilities/Equity

New Projects Added to Agenda

19

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Segment Reporting: ITC Feedback

20

2016 Agenda Consultation • Users rated segment reporting as a high priority in need of improvement. • Preparers rated it a low priority but acknowledged that improvements are

warranted.

Many support making improvements, but do not consider this a major financial reporting issue:

• Segment disclosures are limited and reconciliations can be difficult to tie out. • Aggregation criteria is subjective and questions continue to arise in practice. • Other topics take priority, but continued focus on segments is warranted.

Others do not support making improvements: • Segments are not a major concern and changes are unnecessary. • Management perspective is sound. • Post-implementation review noted that the standard is effective. • It is not possible to force better disclosures under the management approach.

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Potential alternatives

(1) Segment disclosure requirements: • Adding items to the list of required segment disclosures • Requiring information to be reported in a table

(2) Aggregation criteria • Current criteria is very judgmental • Remove some of the cost from the system • Clarify when aggregation can occur

Segment Reporting: Potential Improvements

21

August 2017 – Staff undertaken outreach with preparers, users, regulators and audit firms to understand the impact of the different alternatives

September 2017 - The Board decided to add a project will focus these areas

February 2018 – Discussed issues related to the aggregation criteria

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

To better understand the impact and costs associated with different alternatives, we plan to undertake field testing.

Seeking small & large preparers from a variety of industries

Please contact [email protected] if you would be interested in participating

Segment Reporting—Field Testing

22

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Financial Performance Reporting: Background

23

Objective of research is to identify & evaluate alternatives for improving financial performance reporting

FASB directed staff to perform research on a financial statement presentation project in January 2014

Re-scoped from the previous financial statement presentation project, which went inactive in 2011

RESEARCH

RE-SCOPE

IDENTIFY & EVALUATE

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Reasons for Undertaking FPR Project

24

Ranked as top priority across stakeholders in 2015 FASAC agenda survey

Stakeholders continue to raise concern – McKinsey

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

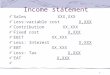

Income Statement Net Revenue XXX

Cost of Sales (XXX)

Gross Profit XXX Selling, General and Administrative Expenses (XXX)

Impairment charge (XXX)

Amortization of intangible assets (XXX)

Operating profit XXX Interest Expense (XXX)

Interest Income XXX

Income before income tax XXX Income tax expense (XXX)

Net Income XXX

Example: Consumer Goods Company

25

82% of respondents to a 2013 CFA survey think financial statement presentation, with improved disaggregation, to be very important Enhanced disaggregation of the income statement can reduce need for certain Non-GAAP measures

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Income Statement: Perceived Issues

26

Aggregation of earnings into only a few line items • Entities are only required to present certain lines • SG&A and COGS comprise lots of dissimilar items

No requirement to prepare a structured income statement • Use of Non-GAAP metrics suggests that some performance

measures, in addition to net income, are important

Limited transparency of items that are useful in making future earnings predictions

• Nonrecurring items aren’t clearly communicated • Users rely on Non-GAAP measures to provide greater transparency

of performance • Adjustments and nonrecurring items may not be consistent over time

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

FPR: Two Work Streams

27

Disaggregation of Performance Information

Structure of the Performance Statement

1

2

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

At its September 2017 meeting, the FASB: - Discussed improving structure of income

statement by developing an operating performance measure

- Decided to prioritize disaggregation of performance information

- Would retain this issue on the research agenda

Issue now appears as a separate research project in the technical agenda

FPR—Structure

28

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

29

FPR - Disaggregation

Established a Project Resource Group Focused on COGS and SG&A lines Planning outreach to understand what capabilities are used to roll up information into COGS and SG&A lines

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Liabilities/Equity: Background High volume of SEC comment letters

Leading cause of financial statement restatements

Stakeholder Feedback on

Guidance

Complex

Difficult to Navigate

Rules-based and path

dependent

Internally inconsistent

30

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

The Board added a project to its agenda on distinguishing liabilities from equity (including convertible debt) with the following objectives:

1. Reduce cost and complexity in financial reporting associated with:

a) Convertible Instruments b) Scope exception to derivative accounting (Subtopic 815-40)

I. Indexation criterion (formerly EITF 07-5) II. Equity classification criterion (formerly EITF 00-19)

2. Maintain or improve the quality of information reported to financial statement users.

L/E: Project Objectives

31

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Current GAAP: Five Models Initial Measurement Attribute

Model Host Instrument Conversion Option

1) Embedded Derivative Residual Fair Value

2) Cash Conversion Fair Value w/o conversion option

Residual

3) Beneficial Conversion Feature Residual Intrinsic Value

4) Substantial Premium Cost* Residual

5) Traditional Convertible Debt No separation – entire instrument carried at amortized cost.

∗ Cost refers to the carrying amount of the liability after the premium is removed.

Convertible Debt

32

Objective: Simplification

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Indexation Criterion

• Indexed to an entity’s own stock • 20 illustrative examples applied by analogy

Equity Classification

Criterion (Settlement)

• Additional criteria for equity classification • Difficult interpretation of 8 strict rules

Derivatives Scope Exception

33

Objective: Simplification

Other Projects

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Cloud Computing

Nonemployee Share-based Payments

Consolidations

Income Taxes

Other Projects of Note

35

Customer’s Accounting for a Cloud Computing Arrangement That Is Considered a Service Contract EITF Issue 17-A

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Implementation costs of CCAs that are service contracts would be accounted for in accordance with the guidance in Subtopic 350-40 on internal-use software

EITF Consensus-for-exposure

37

For example: configuration costs incurred during the application development stage of implementation would be capitalized, whereas costs incurred during the preliminary project and postimplementation stages would be expensed

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

The amortization period of the capitalized implementation costs would include periods covered by renewal options of the CCA that are reasonably certain to be exercised

The amortization of the capitalized implementation costs would be recorded in the same line item on the income statement as the fees for the CCA

Proposed Accounting Standards Update released on 3/1/18; comments were due 4/30/18

EITF Consensus-for-exposure

38

Nonemployee Stock Compensation

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Will expand scope of Topic 718, Compensation—Stock Compensation to also include share-based awards granted to nonemployees in exchange for goods and services to be used in a grantor’s own operations.

• Topic 718 currently only includes share-based awards granted to employees

Will substantially align accounting for nonemployee and employee share-based awards. - Will supersede Subtopic 505-50, Equity—Equity Based

Payments to Non-Employees.

New ASU: Non-Employee Stock Compensation (Expected 2Q 2018)

40

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Accounting for nonemployee share-based awards was identified as an area for simplification through:

- Ideas submitted to the FASB as part of simplification initiative

- The Private Company Council’s (PCC) ongoing dialogue about

making improvements to accounting for share-based awards

- The Post-Implementation Review of FASB Statement No.

123(R), Share-Based Payment.

Non-Employee Stock Compensation: Why?

41

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Effective for public business entities for fiscal years beginning after December 15, 2018, including interim periods within that fiscal year.

For all other entities, the amendments are effective for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020. Early adoption is permitted, but no earlier than an entity’s adoption date of Topic 606 (Revenue Recognition).

Non-Employee Stock Compensation: Effective Dates

42

Consolidations

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Consolidations: Background

44

Stakeholders requested that Board address certain areas of the VIE guidance for related parties under common control.

Stakeholder feedback indicates that current consolidation guidance in Topic 810 is difficult to navigate and, thus, apply.

Private company stakeholders continue to express difficulty applying variable interest entity (VIE) guidance to common control arrangements.

DIFFICULT TO NAVIGATE

DIFFICULTY APPLYING VIE

VIE GUIDANCE

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Project: Consolidation: Reorganization & Targeted Improvements

45

Reorganize consolidation guidance in Topic 810 into a new Topic – Topic 812

Separate Subtopics for VIEs and voting interest entities

Controlled by contract guidance moved to Topic 958: Not-for-Profit Entities

Not expecting change to current outcomes reached under 810

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Project—Consolidation: Targeted Improvements to Related Party Guidance for VIEs

46

Private companies have alternative to not apply VIE guidance to common control arrangements

Indirect interests through a related party under common control considered on proportionate basis for determining whether decision-making fee is a variable interest

When evaluating whether a related party under common control must consolidate a VIE: • Require consolidation when substantially all activities of a VIE are

conducted on behalf of that related party. • Provide criteria for a reporting entity to consider when determining

whether it must consolidate the VIE • Removes required consolidation in all cases at commonly controlled

entity level

Tax Cuts and Jobs Act and Income Tax Reporting Staff Q&As and Update 2018-02, Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

On December 22, 2017, U.S. Congress enacted tax bill, H.R. 1, An Act to Provide for Reconciliation Pursuant to Titles II and V of the Concurrent Resolution on the Budget for Fiscal Year 2018 (Tax Cuts and Jobs Act). Upon enactment, stakeholders requested feedback on: Whether private companies and not-for-profit entities can apply U.S.

Securities and Exchange Commission (SEC) Staff Accounting Bulletin (SAB) No. 118, Income Tax Accounting Implications of the Tax Cuts and Jobs Act

Whether to discount the tax liability on deemed repatriation Whether to discount alternative minimum tax credits that become refundable Accounting for the base erosion anti-abuse tax Accounting for global intangible low-taxed income.

In response, FASB staff issued five Staff Q&A documents.

Staff Q&As: Topic 740, Income Taxes

48

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

GAAP Requirements - Effect recognized at date of enactment. - Measurement of current and deferred taxes is based on provisions of the

enacted tax law. - The tax effect of a retroactive change in enacted tax rates on current and

deferred taxes is determined at the date of enactment using temporary differences and currently taxable income existing as of the date of enactment.

- The effect of adjusting deferred taxes for a change in tax rate is included in income from continuing operations for the period that includes the enactment date.

This means that, as the tax laws or rates were enacted in 2017, the effects are reported in 2017.

Financial Reporting Implications—Timing of Enactment

49

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Update 2018-02—Main Provisions

50

Allows option to elect to reclassify from accumulated other comprehensive income to retained earnings for stranded tax effects resulting from the Tax Cuts and Jobs Act.

If election made to reclassify stranded tax effects, the amount of that reclassification should include: Effect of change in the U.S. federal corporate income tax rate Other income tax effects of the Tax Cuts and Jobs Act that entity

elects to reclassify.

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Update 2018-02

51

Transition Apply amendments either: At beginning of annual or interim period in which

amendments are adopted Retrospectively to each period (or periods) in

which the income tax effects of the Tax Cuts and Jobs Act related to items remaining in accumulated other comprehensive income are recognized.

Effective Date For all entities for fiscal years beginning after

December 15, 2018, and interim periods within those fiscal years.

Early adoption permitted

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

FASB Implementation Web Portal

52

www.fasb.org/implementation

Copyright 2018 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Questions or Comments? www.fasb.org

53