Embed Size (px)

Citation preview

Global Equity Research – India Indian Retail Sector

April 2008

1 Global Equity Research – India

Fasten your seatbelts-organized retail to treble in 5 years

The Indian Super Bazaar, which is the fifth largest retail destination

globally, according to industry estimates is estimated to grow from the

US$ 330 billion in 2007 to US$ 440 billion by 2010 and $650 billion by

2015. The organized retail market is expected to grow at nearly 28%

CAGR from an estimated Rs.690 billion in 2006-2007 to around

Rs.2400 billion by 2012.

The main factors contributing to this robust growth will be –

(1) Rising disposable income;

(2) Demographic changes;

(3) Growing consumerism;

(4) Growing retail malls, infrastructure, etc.

Organized retail comprises various verticals including Food & beverage,

Clothing & textiles, Household appliances, Home Décor & furnishing,

Beauty, personal and health care, Footwear, Equipment, Stationery &

paper.

Domestic big corporate houses and International major retailers are

exploring various formats and options to capture the market share and

ride high on the growth trajectory of Indian Retail market.

Profitably and long term viability in all the above verticals is directly

related to 3 major factors

- Focus in terms of products and target customer,

- Economies of scale, and

- Share of Private Labels

Market study and our research indicate that apparels enjoy maximum

gross margins, followed by food & grocery and household appliances.

However apparels also witness the highest overhead costs due to

massive selling & advertising costs and high lease rentals.

To capture the high retail growth trajectory, we initiate coverage on

Vishal Retail and Koutons Retail – the 2 major players that have

build up a good retail business model and are honing their strategies to

capture higher share in the growing organized retail.

Vishal retail now intends to adopt the franchisee model for its

Epitome Global Services Pvt. Ltd 7th Floor, “A” wing Prism Towers Mindspace, Goregaon (w) Mumbai - 400 062 Tel: (022) 4001.6600 Fax: (022) 4001.6666 Analysts: Anandh Baheti 91 22 4001 6612 Hiral Susania 91 22 4001 6613 Sector: Retail/Buy Date: 11th April 2008

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

2 Global Equity Research – India

specialist retail formats seeing the tremendous leverage it offers in

terms of scale whereas Koutons now plans to open its own large

format stores which was so far operating on the franchisee model.

Thus, the two companies are trying to strike a strategic balance

between own stores and franchise operated stores.

Though the two companies have various differences such as format,

size and product portfolio, the common thing that belies in the two

companies is the importance given to entrepreneurship spirit and the

target potential customer group.

Vishal retail now intends to adopt the franchisee model for its

speciality retail formats seeing the tremendous leverage it offers in

terms of scale whereas Koutons now plans to open its own large

format stores which was so far operating on the franchisee model.

Thus, the two companies are trying to strike a strategic balance

between own stores and franchise operated stores.

Retailing – revolutionizing the way Indians shop

India has one of the largest numbers of retail outlets in the world. Of

the 13 million retail outlets in the country, nearly 5 million sell only

food and grocery related products. At present, organized retail

accounts for only 4 per cent of the total retail market, offering huge

growth potential.

Key Characteristics

■ Total Private Consumption Expenditure in India –approx 400

Billion USD

■ Retail Sale – 225 Billion USD

■ Organized Retail – 7 Billion USD (3.2%)

■ Retailing – 35% of GDP

■ Format – Only 6% larger than 500 sq. Ft.

India has topped AT Kearney's annual Global Retail Development

Index (GRDI) for the third consecutive year, maintaining its position

as the most attractive market for retail investment.

The Indian retail market, which is the fifth largest retail destination

globally, according to industry estimates is projected to grow from

US$ 330 billion in 2007 to US$ 450 billion by 2010 and US$ 640

billion by 2015.

* Whereas organized retail

which presently accounts only

for 5 per cent of the total

market is likely to increase its

share to 12 – 15 per cent by

2010. I.e. 67.5 billion

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

3 Global Equity Research – India

As the income growth rolls across Indian population, like their

Western counterparts, a new generation of urban Indians has started

realizing the convenience and choice offered by Hypermarkets &

Malls. They are also increasingly using credit cards — the share of

Indians who use plastic money has quadrupled over last 4-5 years.

330450

640

0

200

400

600

800

2007 2010e 2015e

High growth Retail Sector

The Indian retail sector has entered into a fast-paced growth phase.

Increased job creation, high spending power and a pervasive

economic climate have lent further impetus to this sector.

Retail is now being heralded as the next sunrise sector after IT, with

the potential to contribute significantly to the country's GDP and

create new job opportunities, going further.

Spokes of Growth Cycle

A number of policy developments and market changes have re-

aligned the structure of the Indian retail sector. This has made it

immensely attractive for domestic as well as international retailers.

A colossal shift is taking place from spending on necessities such as

food and clothing to discretionary spending on household appliances,

entertainment, premium apparels and restaurants. According to an

estimate, households that can afford choice-based consumption will

grow from 8-9 million to 85-90 million by 2025.

Numerous Indian retail chains like Pantaloons, Shopper's Stop and

also large business groups such as Reliance, Tata, ITC, AV Birla

Group and Bharti have chalked out aggressive expansion plans and

are venturing into multiple retail formats.

Key Characteristics

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

4 Global Equity Research – India

Visible Investments in the Industry

■ Reliance Retail is going ahead with plans worth an investment of

US$ 6.25 billion for setting up over 5000 stores in various

formats.

■ Spencer's is also planning to set up 500 more stores within a year

with an investment of nearly US$ 25 million.

■ Hypercity is planning to set up 250 Express-city stores in the

convenience store format across the country in the next five

years.

■ Wadhawan Food Retail promoted "Spinach" chain of retail stores

plans to have 1,500 establishments by 2011.

■ DLF plans to invest US$ 4.02 billion over four years to develop

about 20 large shopping malls across the country.

■ Big Shopping centers and US-based Lehman Brothers' wholly-

owned special purpose vehicle BIG Mauritius Holdings to invest

US$ 2.4 billion for setting up shopping malls in the next ten years

■ Israeli mall developer Plaza Center NV plans to invest US$ 1.25

billion over the next five-seven years to set up 50 malls in India

■ Bharti Enterprises had announced US$ 2.5 billion retail plans and

has inked a 50:50 joint venture with Walmart; plans to announce

final plans by April’08

The home-bred retailers, with their intrinsic knowledge of the Indian

Markets, are expected to capture a major share of the retailing pie

before foreign retailers make their big bang entry.

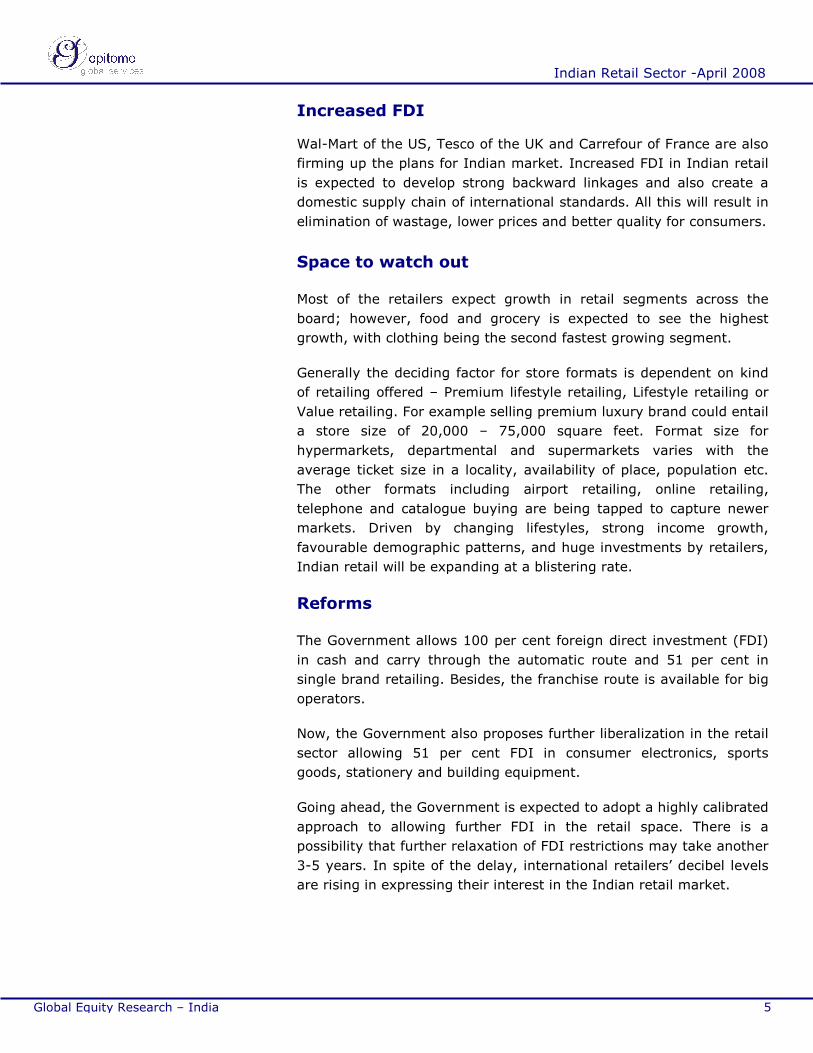

Key drivers for the sector

Positive demographics The purchasing power- rising Income levels

42%

39%

26%

27%

22%

23%

11%

12%

0% 20% 40% 60% 80% 100%

2006

2010E

0-19 Yrs 20-34 Yrs 35-54 Yrs 55+ Yrs

`

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

5 Global Equity Research – India

Increased FDI

Wal-Mart of the US, Tesco of the UK and Carrefour of France are also

firming up the plans for Indian market. Increased FDI in Indian retail

is expected to develop strong backward linkages and also create a

domestic supply chain of international standards. All this will result in

elimination of wastage, lower prices and better quality for consumers.

Space to watch out

Most of the retailers expect growth in retail segments across the

board; however, food and grocery is expected to see the highest

growth, with clothing being the second fastest growing segment.

Generally the deciding factor for store formats is dependent on kind

of retailing offered – Premium lifestyle retailing, Lifestyle retailing or

Value retailing. For example selling premium luxury brand could entail

a store size of 20,000 – 75,000 square feet. Format size for

hypermarkets, departmental and supermarkets varies with the

average ticket size in a locality, availability of place, population etc.

The other formats including airport retailing, online retailing,

telephone and catalogue buying are being tapped to capture newer

markets. Driven by changing lifestyles, strong income growth,

favourable demographic patterns, and huge investments by retailers,

Indian retail will be expanding at a blistering rate.

Reforms

The Government allows 100 per cent foreign direct investment (FDI)

in cash and carry through the automatic route and 51 per cent in

single brand retailing. Besides, the franchise route is available for big

operators.

Now, the Government also proposes further liberalization in the retail

sector allowing 51 per cent FDI in consumer electronics, sports

goods, stationery and building equipment.

Going ahead, the Government is expected to adopt a highly calibrated

approach to allowing further FDI in the retail space. There is a

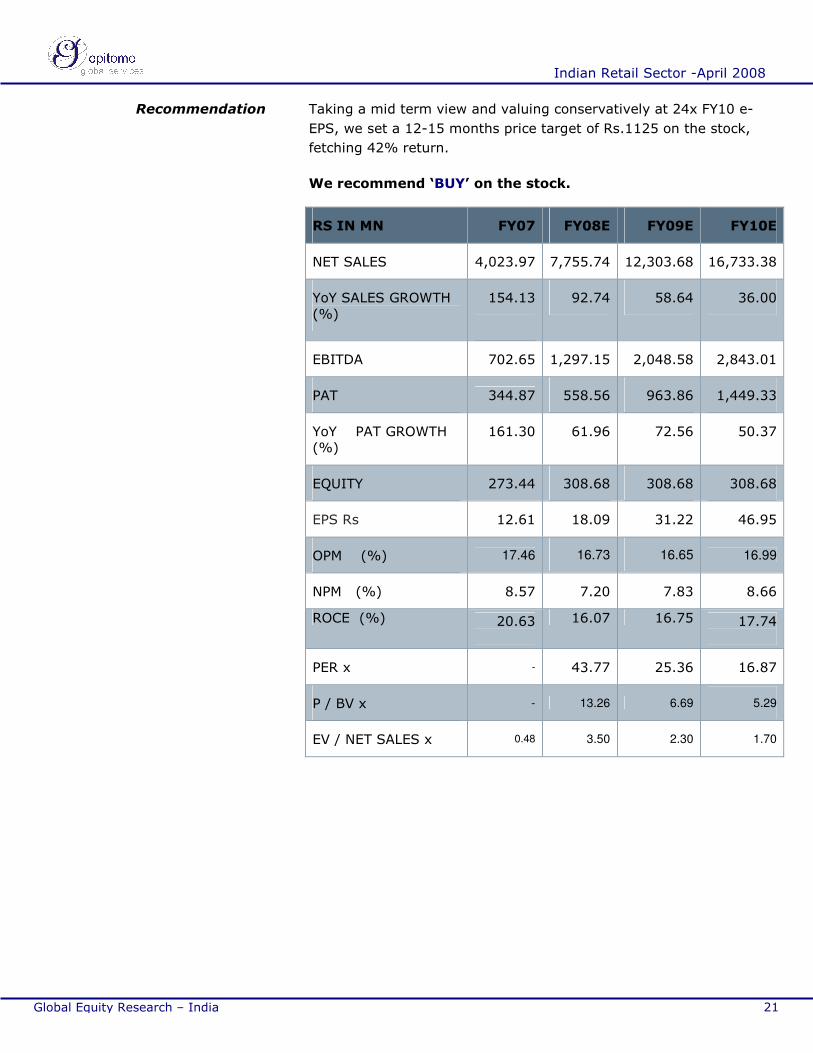

possibility that further relaxation of FDI restrictions may take another

3-5 years. In spite of the delay, international retailers’ decibel levels

are rising in expressing their interest in the Indian retail market.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

6 Global Equity Research – India

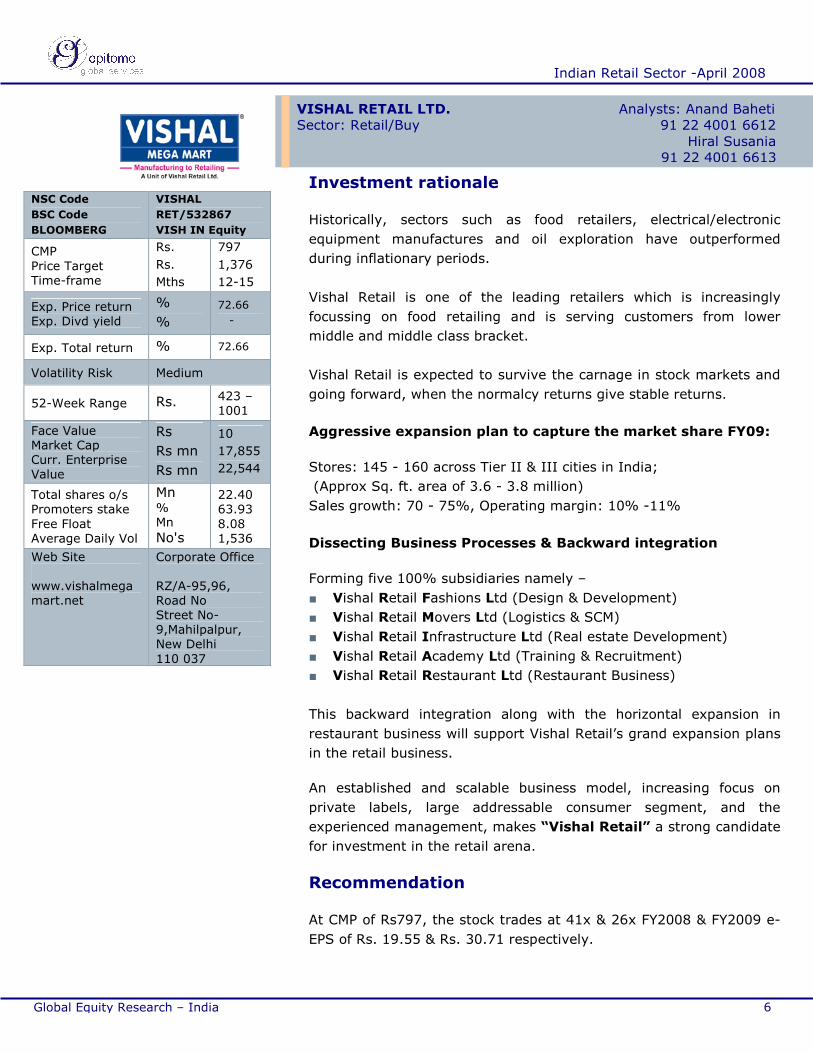

NSC Code

BSC Code

BLOOMBERG

VISHAL

RET/532867

VISH IN Equity

CMP Price Target Time-frame

Rs.

Rs.

Mths

797

1,376

12-15

Exp. Price return Exp. Divd yield

%

%

72.66

-

Exp. Total return % 72.66

Volatility Risk Medium

52-Week Range Rs. 423 – 1001

Face Value Market Cap Curr. Enterprise Value

Rs

Rs mn

Rs mn

10

17,855

22,544

Total shares o/s Promoters stake Free Float Average Daily Vol

Mn % Mn No's

22.40 63.93 8.08 1,536

Web Site www.vishalmegamart.net

Corporate Office RZ/A-95,96, Road No Street No-9,Mahilpalpur, New Delhi 110 037

VISHAL RETAIL LTD. Analysts: Anand Baheti Sector: Retail/Buy 91 22 4001 6612 Hiral Susania

91 22 4001 6613

Investment rationale

Historically, sectors such as food retailers, electrical/electronic

equipment manufactures and oil exploration have outperformed

during inflationary periods.

Vishal Retail is one of the leading retailers which is increasingly

focussing on food retailing and is serving customers from lower

middle and middle class bracket.

Vishal Retail is expected to survive the carnage in stock markets and

going forward, when the normalcy returns give stable returns.

Aggressive expansion plan to capture the market share FY09:

Stores: 145 - 160 across Tier II & III cities in India;

(Approx Sq. ft. area of 3.6 - 3.8 million)

Sales growth: 70 - 75%, Operating margin: 10% -11%

Dissecting Business Processes & Backward integration

Forming five 100% subsidiaries namely –

■ Vishal Retail Fashions Ltd (Design & Development)

■ Vishal Retail Movers Ltd (Logistics & SCM)

■ Vishal Retail Infrastructure Ltd (Real estate Development)

■ Vishal Retail Academy Ltd (Training & Recruitment)

■ Vishal Retail Restaurant Ltd (Restaurant Business)

This backward integration along with the horizontal expansion in

restaurant business will support Vishal Retail’s grand expansion plans

in the retail business.

An established and scalable business model, increasing focus on

private labels, large addressable consumer segment, and the

experienced management, makes “Vishal Retail” a strong candidate

for investment in the retail arena.

Recommendation

At CMP of Rs797, the stock trades at 41x & 26x FY2008 & FY2009 e-

EPS of Rs. 19.55 & Rs. 30.71 respectively.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

7 Global Equity Research – India

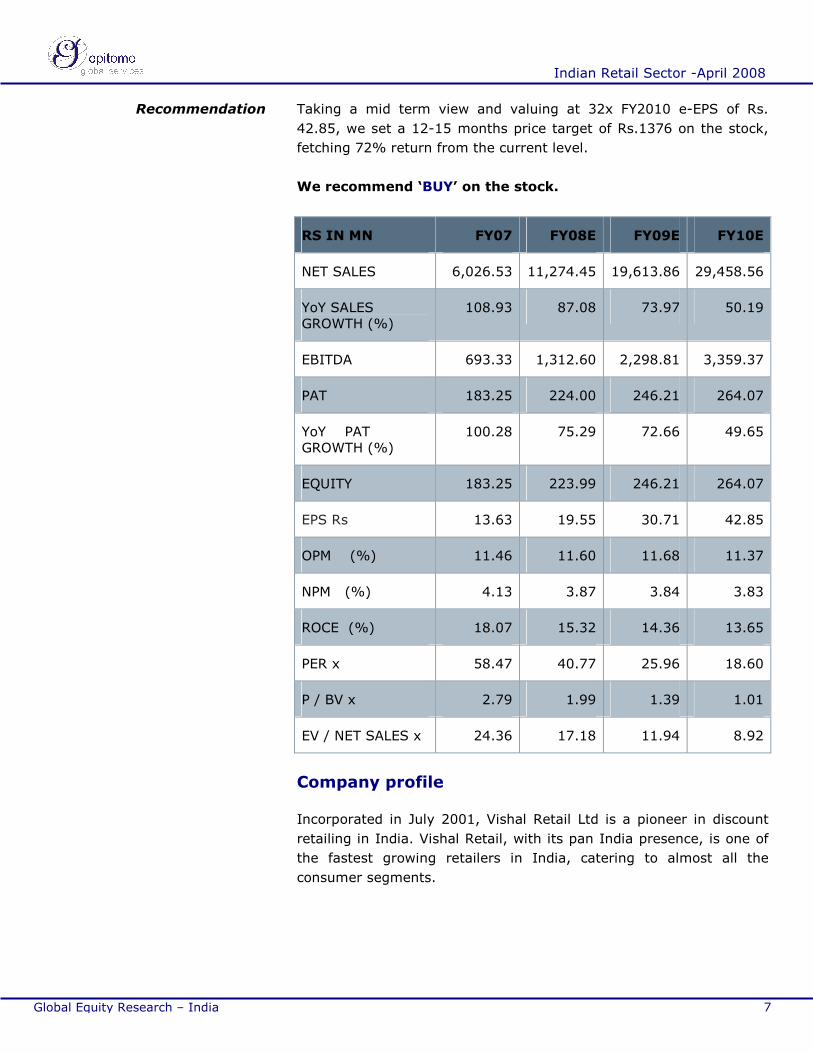

Taking a mid term view and valuing at 32x FY2010 e-EPS of Rs.

42.85, we set a 12-15 months price target of Rs.1376 on the stock,

fetching 72% return from the current level.

We recommend ‘BUY’ on the stock.

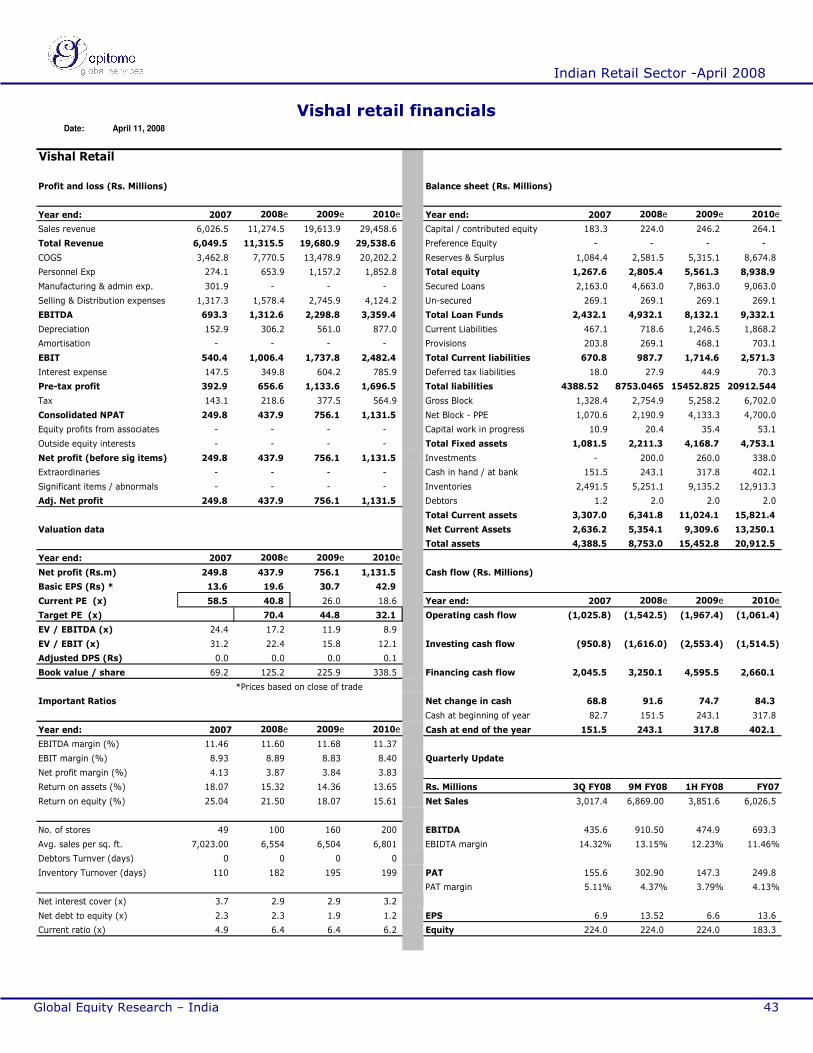

RS IN MN FY07 FY08E FY09E FY10E

NET SALES 6,026.53 11,274.45 19,613.86 29,458.56

YoY SALES GROWTH (%)

108.93 87.08 73.97 50.19

EBITDA 693.33 1,312.60 2,298.81 3,359.37

PAT 183.25 224.00 246.21 264.07

YoY PAT GROWTH (%)

100.28 75.29 72.66 49.65

EQUITY 183.25 223.99 246.21 264.07

EPS Rs 13.63 19.55 30.71 42.85

OPM (%) 11.46 11.60 11.68 11.37

NPM (%) 4.13 3.87 3.84 3.83

ROCE (%) 18.07 15.32 14.36 13.65

PER x 58.47 40.77 25.96 18.60

P / BV x 2.79 1.99 1.39 1.01

EV / NET SALES x 24.36 17.18 11.94 8.92

Company profile

Incorporated in July 2001, Vishal Retail Ltd is a pioneer in discount

retailing in India. Vishal Retail, with its pan India presence, is one of

the fastest growing retailers in India, catering to almost all the

consumer segments.

Recommendation

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

8 Global Equity Research – India

The growth magnitude of Vishal Retail is visible from the following

numbers –

Jan 1986 - 1 store

(An independent enterprise)

March 2008 – 100 stores

(67Cities 20 States; covering area of 2,130,000 Sq. Ft approx)

Though the growth looks a bit of non-starter, the fact that actual

growth has started ticking only after 2001 will definitely give a

high.

Vishal primarily caters to the bulging middle and lower middle class

consumer bracket, which forms approx. 60% of India’s total

purchasing power. The Company is operating a chain of low cost

hypermarkets, focused on Tier II and III towns and cities, across the

country.

The philosophy behind value retailing is - cost benefits that are

derived from the large central purchase of goods and services are

passed on to the consumer. Vishal’s hypermarket showrooms have

over 85,000 products which fulfil all the household needs and also

offer affordable family fashion at prices suiting every section of the

society.

Vishal has differentiated itself with its strong focus on private labels

manufactured in-house, and quasi-private labels sourced from low-

cost manufacturers. This also helps Vishal in improving revenue

streams and margins.

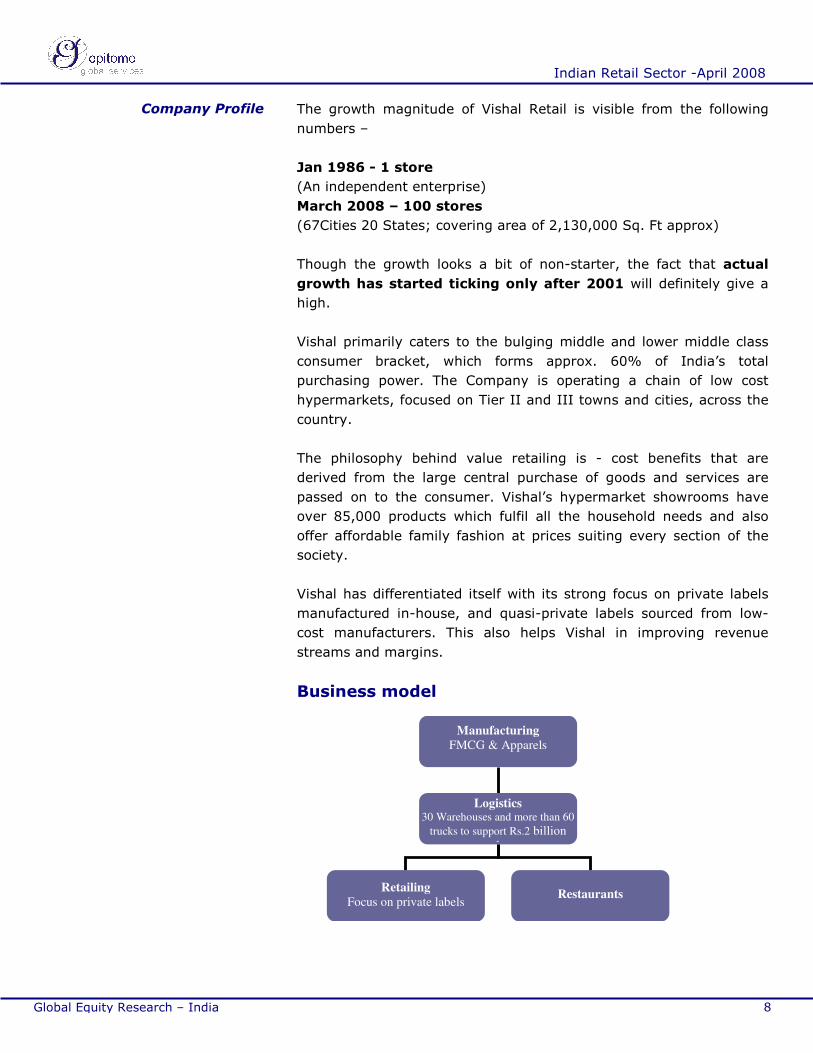

Business model

Manufacturing

FMCG & Apparels

Logistics 30 Warehouses and more than 60

trucks to support Rs.2 billion

sales

Retailing

Focus on private labels Restaurants

Restaurants

Company Profile

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

9 Global Equity Research – India

Strategy

It has an ambitious rollout plan to reach a total of 150 stores

covering approx 3.80 million sq. Ft. of retail space by FY09. The

Company is also focusing on integration and towards this end has

initiated backward integration in the field of high fashion by setting

up a state of the art manufacturing facility to support its high-end /

premium retailing.

With more than 80% of its stores located in Tier II & III cities, the

company is gaining first mover advantage and a competitive edge by

acquiring/leasing real estate at lower prices, and is also achieving

critical mass. During 9M FY08, the average rentals per square feet

per month stood at Rs. 31.

With its basics firmly in place, Vishal is now focusing on de-risking its

business model by diversifying in Restaurants, Jewellery and

medicine retailing, by strengthening its management team and

upgrading its technology and supply chain efficiencies. This will help

support scalability and derive efficiency gains.

On pilot basis the Company opened Vishal Fashion Mart and Vishal

Jewel Mart in New Delhi to tap the speciality market. These formats

are much smaller in size ranging from 1,500-2,500 square feet. The

Company already has close to 20 Vishal Fashion Mart and is also

considering to enter various other formats including convenience,

apparel, restaurants, consumer durables, IT, footwear, lifestyle and

home in the next one years time.

For these speciality formats, the Company plans to take up the

franchise route to control its fixed costs and overcome the talent

crunch which the industry is facing. Apart from this, the Company

plans to foray in the cash-and-carry business in a year’s time.

Vishal has also focused on its backward integration into garment

manufacturing as a key margin improvement factor for the company.

In FY07, Private labels (in-house manufacturing) contributed to 10%

of turnover and the quasi-private labels (products sourced from

unbranded manufacturer suppliers) contributed over 60% to its

revenue.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

10 Global Equity Research – India

To support this high decibel growth they have decided to form

separate project implementation teams. Also, the implementation of

SAP will enable the company to scale without any hiccups.

As the Company generates 61 % of its revenue form its Apparel

business, the VRFL will provide the stores with latest designs and

trend in the market which can eventually be manufactured as private

or quasi-private labels.

VRML will provide complete logistic solution to the Company stores.

These resources can eventually be used to cater to the needs of the

other retailers, thus making optimum utilization of available

resources.

Normally, the king-size formats of Vishal retail stores are of around

25,000 sq. Ft. That automatically increase the per square feet rates

of the surrounding area. Vishal retail, which has big plans of covering

an area of approx. 10 million sq ft. In next 5-6 years, can tap this

potential increase in realty prices by developing the stores and the

surrounding area through VRIL.

The big store size also allows the Company to expand horizontally

and generate additional stream of revenues from its restaurant

business. The Company already has 40 (QSR) Quick Service

Restaurants that generate a very healthy gross margin of 60%

(excluding only the raw material costs). The Company plans to have

restaurants in all the stores that are more than 20,000 square feet in

size.

The Company with the existing headcount of 12,500 employees is

facing a high attrition rate of 15%. VRAL will be a training institute

for the aspirants seeking a career in retail and feeder to Vishal Retail

Ltd. Initially, this will cater only to the needs of the Company at both

the front-end and the backend level and eventually will cater to the

overall retail sector.

Thus, the Company’s strategy of moving backwards from its business

will not only help the Company to capitalize on its retail expansion

but also tap the potential opportunities available in the logistics,

training and development and real estate infrastructure which is

geared-up by the boom in the retail industry.

Strategy

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

11 Global Equity Research – India

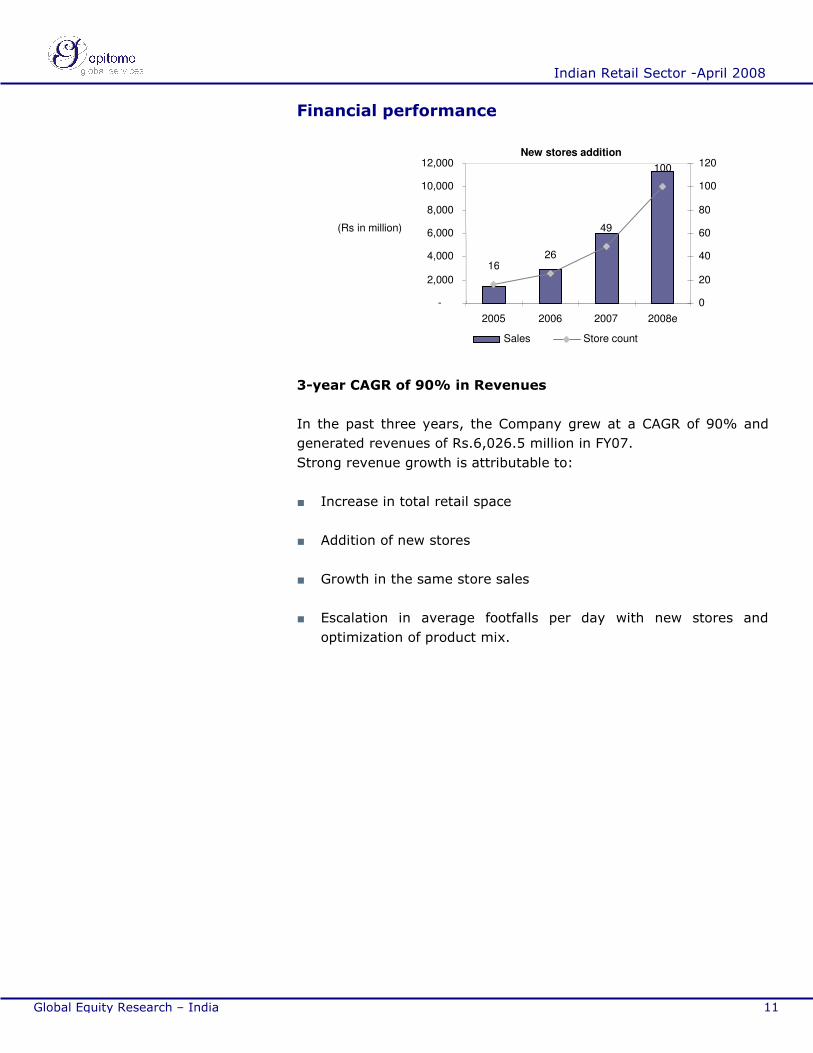

Financial performance

New stores addition

26

100

49

16

-

2,000

4,000

6,000

8,000

10,000

12,000

2005 2006 2007 2008e 0

20

40

60

80

100

120

Sales Store count

(Rs in million)

3-year CAGR of 90% in Revenues

In the past three years, the Company grew at a CAGR of 90% and

generated revenues of Rs.6,026.5 million in FY07.

Strong revenue growth is attributable to:

■ Increase in total retail space

■ Addition of new stores

■ Growth in the same store sales

■ Escalation in average footfalls per day with new stores and

optimization of product mix.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

12 Global Equity Research – India

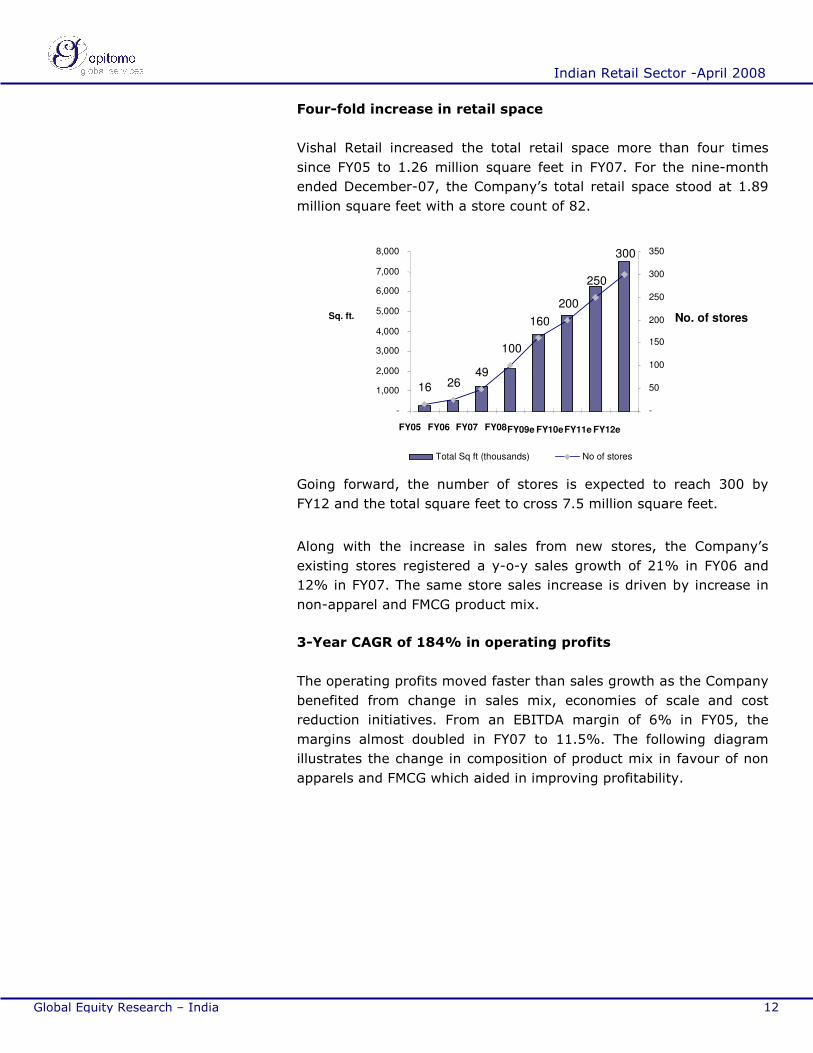

Four-fold increase in retail space

Vishal Retail increased the total retail space more than four times

since FY05 to 1.26 million square feet in FY07. For the nine-month

ended December-07, the Company’s total retail space stood at 1.89

million square feet with a store count of 82.

16 2649

100

200

250

300

160

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY05 FY06 FY07 FY08 FY09e FY10e FY11e FY12e

Sq. ft.

-

50

100

150

200

250

300

350

Total Sq ft (thousands) No of stores

No. of stores

Going forward, the number of stores is expected to reach 300 by

FY12 and the total square feet to cross 7.5 million square feet.

Along with the increase in sales from new stores, the Company’s

existing stores registered a y-o-y sales growth of 21% in FY06 and

12% in FY07. The same store sales increase is driven by increase in

non-apparel and FMCG product mix.

3-Year CAGR of 184% in operating profits

The operating profits moved faster than sales growth as the Company

benefited from change in sales mix, economies of scale and cost

reduction initiatives. From an EBITDA margin of 6% in FY05, the

margins almost doubled in FY07 to 11.5%. The following diagram

illustrates the change in composition of product mix in favour of non

apparels and FMCG which aided in improving profitability.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

13 Global Equity Research – India

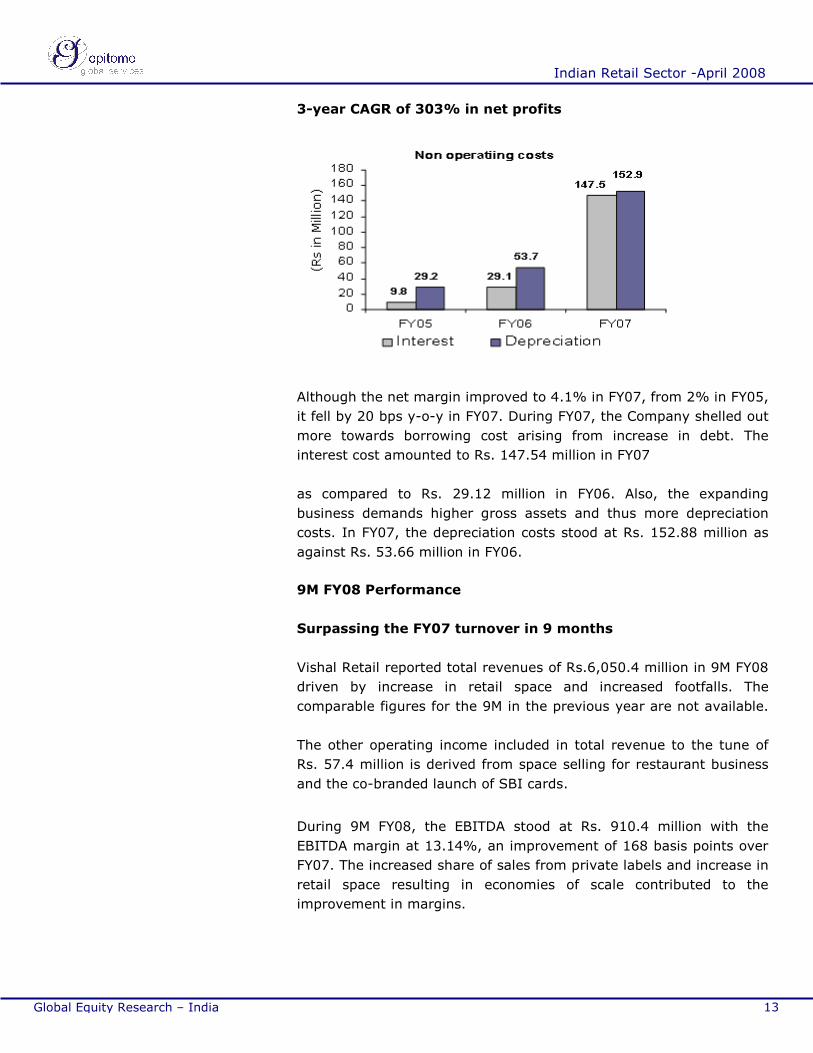

3-year CAGR of 303% in net profits

Although the net margin improved to 4.1% in FY07, from 2% in FY05,

it fell by 20 bps y-o-y in FY07. During FY07, the Company shelled out

more towards borrowing cost arising from increase in debt. The

interest cost amounted to Rs. 147.54 million in FY07

as compared to Rs. 29.12 million in FY06. Also, the expanding

business demands higher gross assets and thus more depreciation

costs. In FY07, the depreciation costs stood at Rs. 152.88 million as

against Rs. 53.66 million in FY06.

9M FY08 Performance

Surpassing the FY07 turnover in 9 months

Vishal Retail reported total revenues of Rs.6,050.4 million in 9M FY08

driven by increase in retail space and increased footfalls. The

comparable figures for the 9M in the previous year are not available.

The other operating income included in total revenue to the tune of

Rs. 57.4 million is derived from space selling for restaurant business

and the co-branded launch of SBI cards.

During 9M FY08, the EBITDA stood at Rs. 910.4 million with the

EBITDA margin at 13.14%, an improvement of 168 basis points over

FY07. The increased share of sales from private labels and increase in

retail space resulting in economies of scale contributed to the

improvement in margins.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

14 Global Equity Research – India

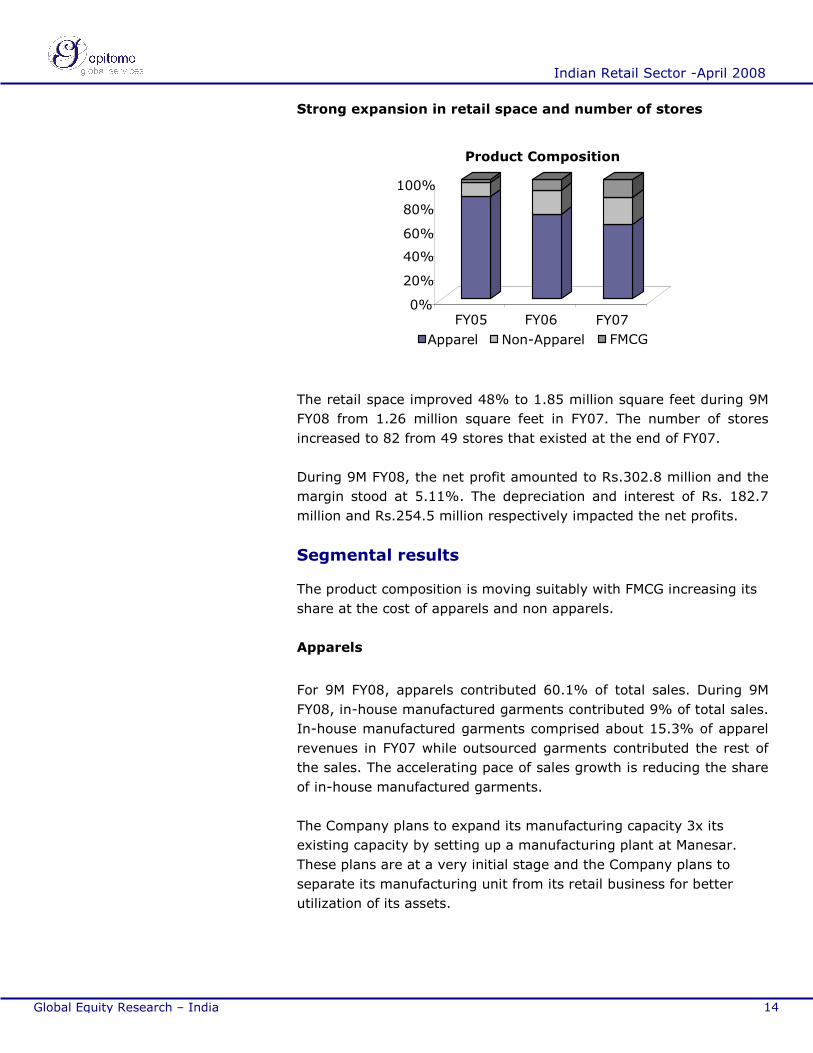

Strong expansion in retail space and number of stores

0%

20%

40%

60%

80%

100%

FY05 FY06 FY07

Product Composition

Apparel Non-Apparel

FMCG

The retail space improved 48% to 1.85 million square feet during 9M

FY08 from 1.26 million square feet in FY07. The number of stores

increased to 82 from 49 stores that existed at the end of FY07.

During 9M FY08, the net profit amounted to Rs.302.8 million and the

margin stood at 5.11%. The depreciation and interest of Rs. 182.7

million and Rs.254.5 million respectively impacted the net profits.

Segmental results

The product composition is moving suitably with FMCG increasing its

share at the cost of apparels and non apparels.

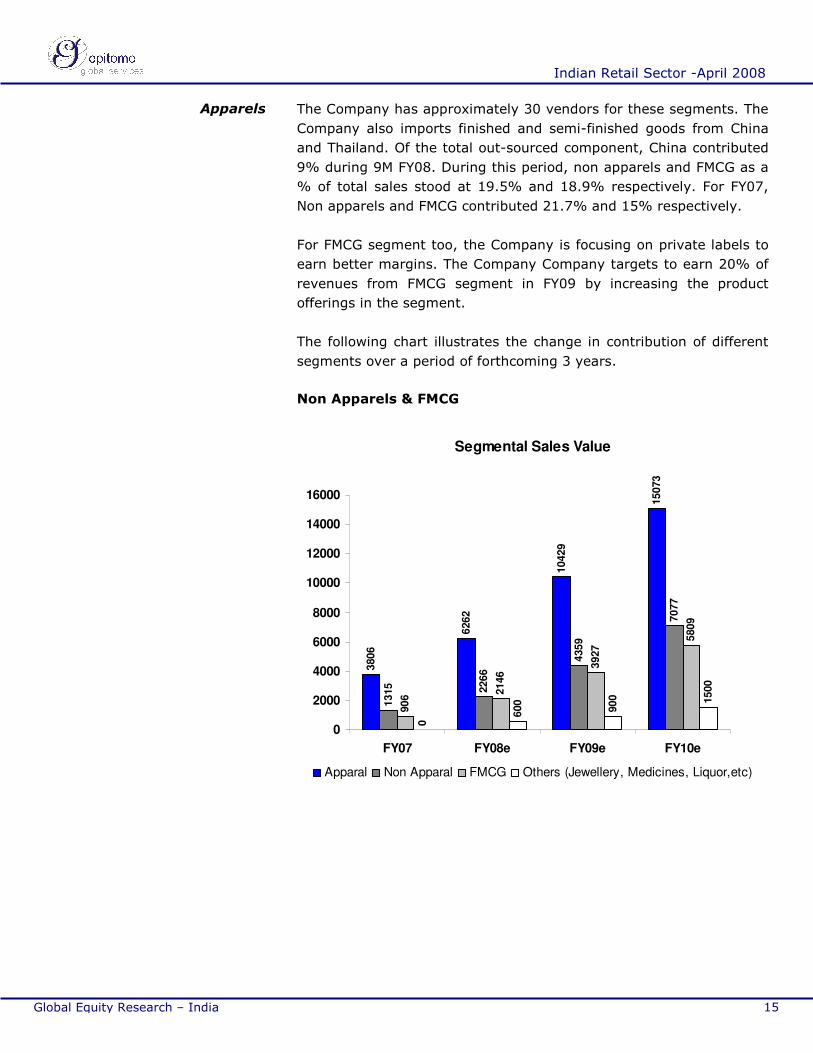

Apparels

For 9M FY08, apparels contributed 60.1% of total sales. During 9M

FY08, in-house manufactured garments contributed 9% of total sales.

In-house manufactured garments comprised about 15.3% of apparel

revenues in FY07 while outsourced garments contributed the rest of

the sales. The accelerating pace of sales growth is reducing the share

of in-house manufactured garments.

The Company plans to expand its manufacturing capacity 3x its

existing capacity by setting up a manufacturing plant at Manesar.

These plans are at a very initial stage and the Company plans to

separate its manufacturing unit from its retail business for better

utilization of its assets.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

15 Global Equity Research – India

The Company has approximately 30 vendors for these segments. The

Company also imports finished and semi-finished goods from China

and Thailand. Of the total out-sourced component, China contributed

9% during 9M FY08. During this period, non apparels and FMCG as a

% of total sales stood at 19.5% and 18.9% respectively. For FY07,

Non apparels and FMCG contributed 21.7% and 15% respectively.

For FMCG segment too, the Company is focusing on private labels to

earn better margins. The Company Company targets to earn 20% of

revenues from FMCG segment in FY09 by increasing the product

offerings in the segment.

The following chart illustrates the change in contribution of different

segments over a period of forthcoming 3 years.

Non Apparels & FMCG

Segmental Sales Value

3806

6262

10429

15073

1315 2266

4359

7077

906

2146

3927

5809

0

600

900 1500

0

2000

4000

6000

8000

10000

12000

14000

16000

FY07 FY08e FY09e FY10e

Apparal Non Apparal FMCG Others (Jewellery, Medicines, Liquor,etc)

Apparels

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

16 Global Equity Research – India

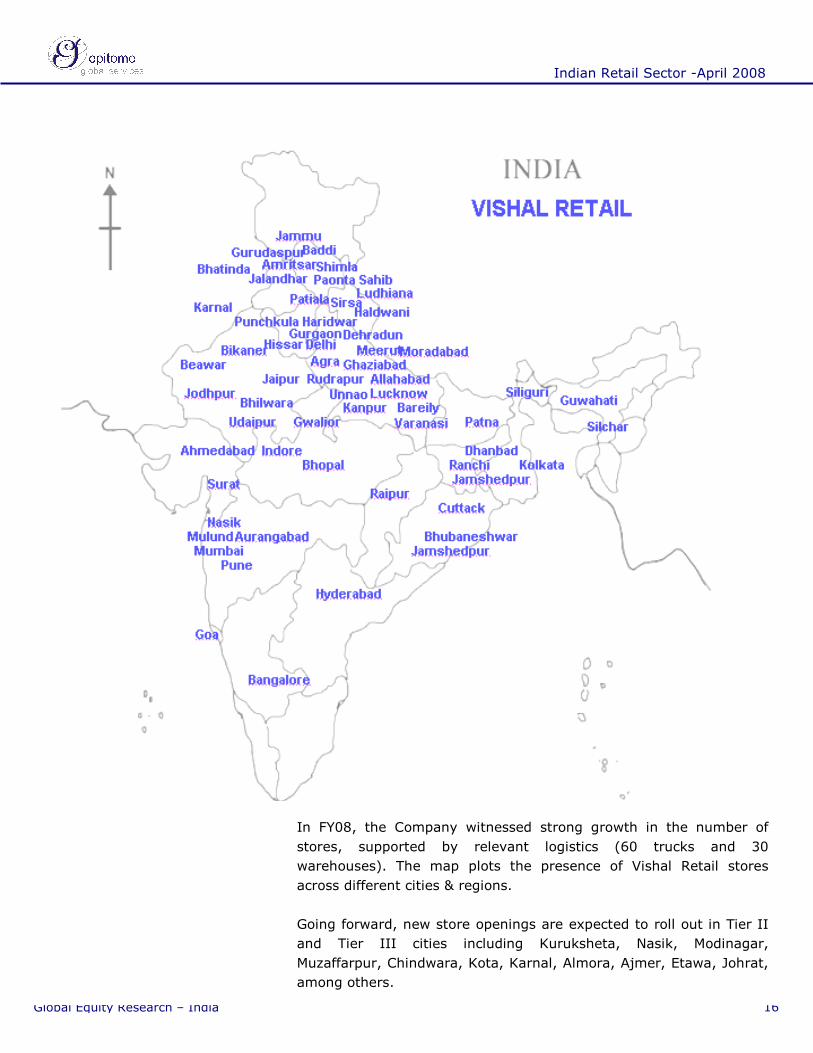

In FY08, the Company witnessed strong growth in the number of

stores, supported by relevant logistics (60 trucks and 30

warehouses). The map plots the presence of Vishal Retail stores

across different cities & regions.

Going forward, new store openings are expected to roll out in Tier II

and Tier III cities including Kuruksheta, Nasik, Modinagar,

Muzaffarpur, Chindwara, Kota, Karnal, Almora, Ajmer, Etawa, Johrat,

among others.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

17 Global Equity Research – India

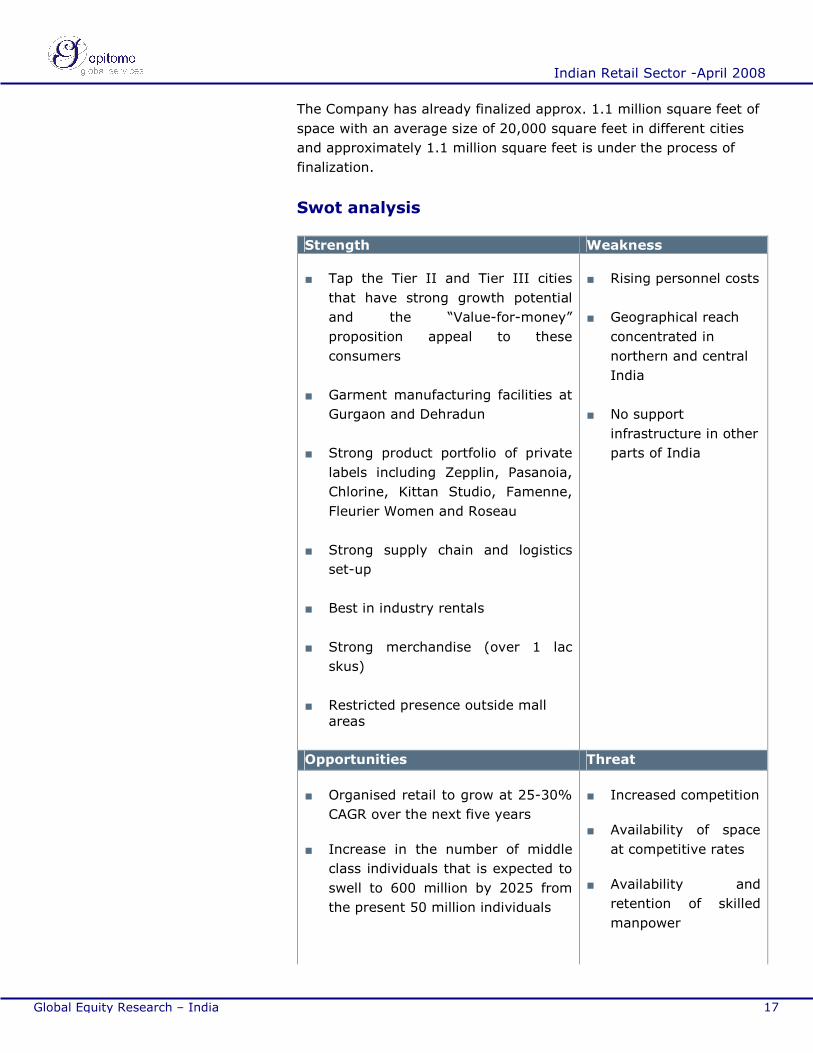

The Company has already finalized approx. 1.1 million square feet of

space with an average size of 20,000 square feet in different cities

and approximately 1.1 million square feet is under the process of

finalization.

Swot analysis

Strength Weakness

■ Tap the Tier II and Tier III cities

that have strong growth potential

and the “Value-for-money”

proposition appeal to these

consumers

■ Garment manufacturing facilities at

Gurgaon and Dehradun

■ Strong product portfolio of private

labels including Zepplin, Pasanoia,

Chlorine, Kittan Studio, Famenne,

Fleurier Women and Roseau

■ Strong supply chain and logistics

set-up

■ Best in industry rentals

■ Strong merchandise (over 1 lac

skus)

■ Restricted presence outside mall areas

■ Rising personnel costs

■ Geographical reach

concentrated in

northern and central

India

■ No support

infrastructure in other

parts of India

Opportunities Threat

■ Organised retail to grow at 25-30%

CAGR over the next five years

■ Increase in the number of middle

class individuals that is expected to

swell to 600 million by 2025 from

the present 50 million individuals

■ Increased competition

■ Availability of space

at competitive rates

■ Availability and

retention of skilled

manpower

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

18 Global Equity Research – India

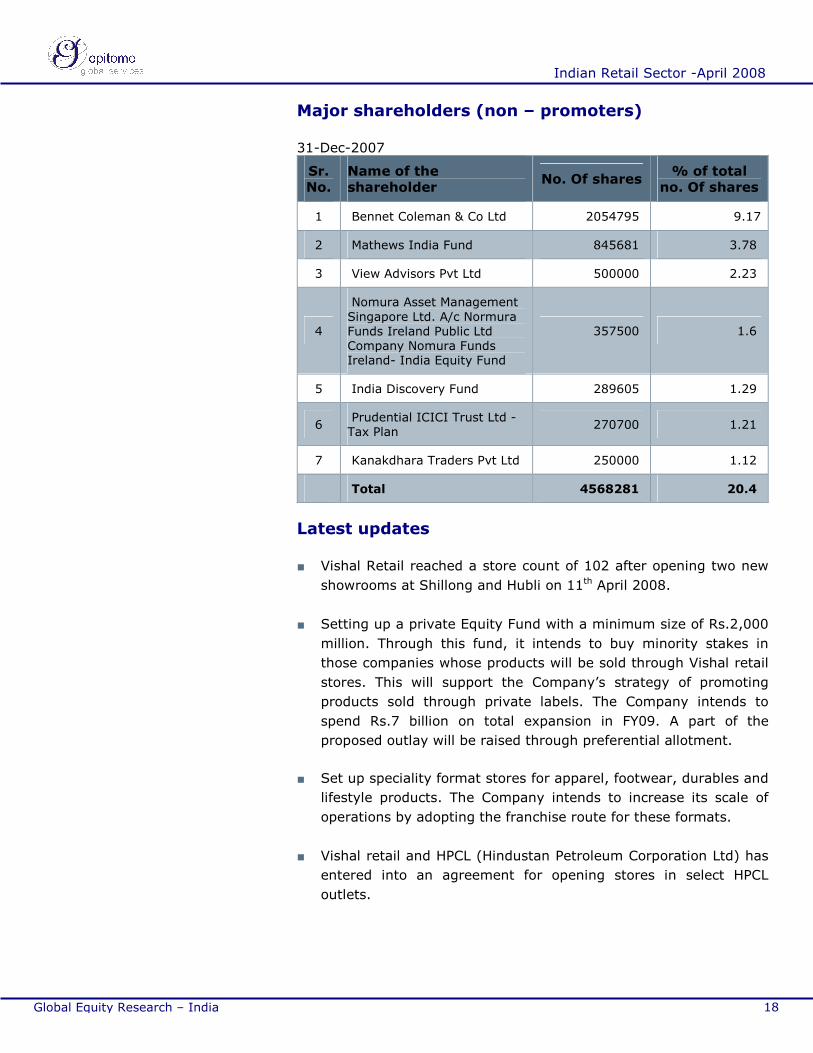

Major shareholders (non – promoters)

31-Dec-2007

Sr.

No.

Name of the

shareholder No. Of shares

% of total

no. Of shares

1 Bennet Coleman & Co Ltd 2054795 9.17

2 Mathews India Fund 845681 3.78

3 View Advisors Pvt Ltd 500000 2.23

4

Nomura Asset Management Singapore Ltd. A/c Normura Funds Ireland Public Ltd Company Nomura Funds Ireland- India Equity Fund

357500 1.6

5 India Discovery Fund 289605 1.29

6 Prudential ICICI Trust Ltd -Tax Plan

270700 1.21

7 Kanakdhara Traders Pvt Ltd 250000 1.12

Total 4568281 20.4

Latest updates

■ Vishal Retail reached a store count of 102 after opening two new

showrooms at Shillong and Hubli on 11th April 2008.

■ Setting up a private Equity Fund with a minimum size of Rs.2,000

million. Through this fund, it intends to buy minority stakes in

those companies whose products will be sold through Vishal retail

stores. This will support the Company’s strategy of promoting

products sold through private labels. The Company intends to

spend Rs.7 billion on total expansion in FY09. A part of the

proposed outlay will be raised through preferential allotment.

■ Set up speciality format stores for apparel, footwear, durables and

lifestyle products. The Company intends to increase its scale of

operations by adopting the franchise route for these formats.

■ Vishal retail and HPCL (Hindustan Petroleum Corporation Ltd) has

entered into an agreement for opening stores in select HPCL

outlets.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

19 Global Equity Research – India

■ HPCL has 8,000 retail outlets and the Company intends to either

open stores or use them for the purpose of warehouse.

■ Like Koutons retail, the Company intends to capitalize on the

benefits of franchise model. Accordingly, the kirana outlets that

were facing the heat of organised retail will join hands with Vishal

under the franchise route. This will be a win-win situation for both

parties. The kirana stores will benefit from Vishal’s merchandising

expertise, technology, promotional schemes and supply chain

management. Besides, they will be offered minimum guarantee so

they do not lose out on their opportunity cost. While Vishal retail

will have a strong support of the army of kirana stores – so far

disgruntled with organised retail -- that exist in the country. This

will help the company in facing the competition from large players

like Reliance, Future and Bharti Retail.

Latest updates

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

20 Global Equity Research – India

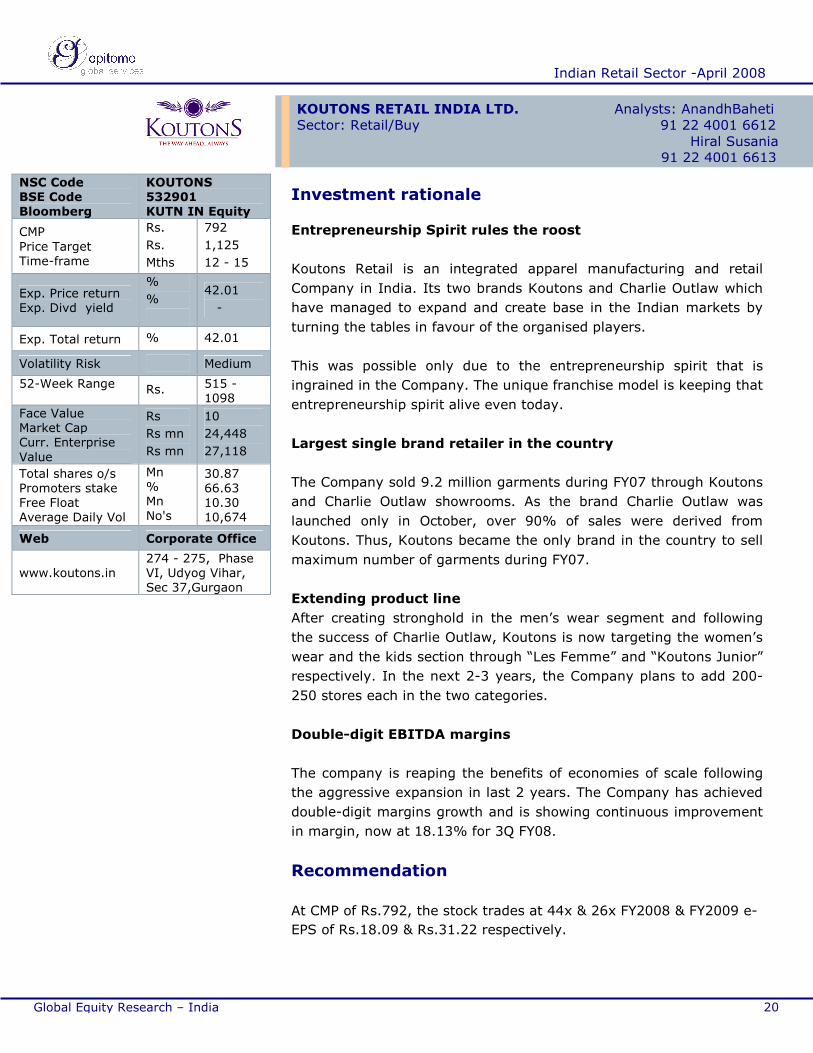

NSC Code BSE Code Bloomberg

KOUTONS 532901 KUTN IN Equity

CMP Price Target Time-frame

Rs.

Rs.

Mths

792

1,125

12 - 15

Exp. Price return Exp. Divd yield

%

%

42.01

-

Exp. Total return % 42.01

Volatility Risk Medium

52-Week Range

Rs. 515 - 1098

Face Value Market Cap Curr. Enterprise Value

Rs

Rs mn

Rs mn

10

24,448

27,118

Total shares o/s Promoters stake Free Float Average Daily Vol

Mn % Mn No's

30.87 66.63 10.30 10,674

Web Corporate Office

www.koutons.in 274 - 275, Phase VI, Udyog Vihar, Sec 37,Gurgaon

Investment rationale

Entrepreneurship Spirit rules the roost

Koutons Retail is an integrated apparel manufacturing and retail

Company in India. Its two brands Koutons and Charlie Outlaw which

have managed to expand and create base in the Indian markets by

turning the tables in favour of the organised players.

This was possible only due to the entrepreneurship spirit that is

ingrained in the Company. The unique franchise model is keeping that

entrepreneurship spirit alive even today.

Largest single brand retailer in the country

The Company sold 9.2 million garments during FY07 through Koutons

and Charlie Outlaw showrooms. As the brand Charlie Outlaw was

launched only in October, over 90% of sales were derived from

Koutons. Thus, Koutons became the only brand in the country to sell

maximum number of garments during FY07.

Extending product line

After creating stronghold in the men’s wear segment and following

the success of Charlie Outlaw, Koutons is now targeting the women’s

wear and the kids section through “Les Femme” and “Koutons Junior”

respectively. In the next 2-3 years, the Company plans to add 200-

250 stores each in the two categories.

Double-digit EBITDA margins

The company is reaping the benefits of economies of scale following

the aggressive expansion in last 2 years. The Company has achieved

double-digit margins growth and is showing continuous improvement

in margin, now at 18.13% for 3Q FY08.

Recommendation

At CMP of Rs.792, the stock trades at 44x & 26x FY2008 & FY2009 e-

EPS of Rs.18.09 & Rs.31.22 respectively.

KOUTONS RETAIL INDIA LTD. Analysts: AnandhBaheti Sector: Retail/Buy 91 22 4001 6612

Hiral Susania 91 22 4001 6613

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

21 Global Equity Research – India

Taking a mid term view and valuing conservatively at 24x FY10 e-

EPS, we set a 12-15 months price target of Rs.1125 on the stock,

fetching 42% return.

We recommend ‘BUY’ on the stock.

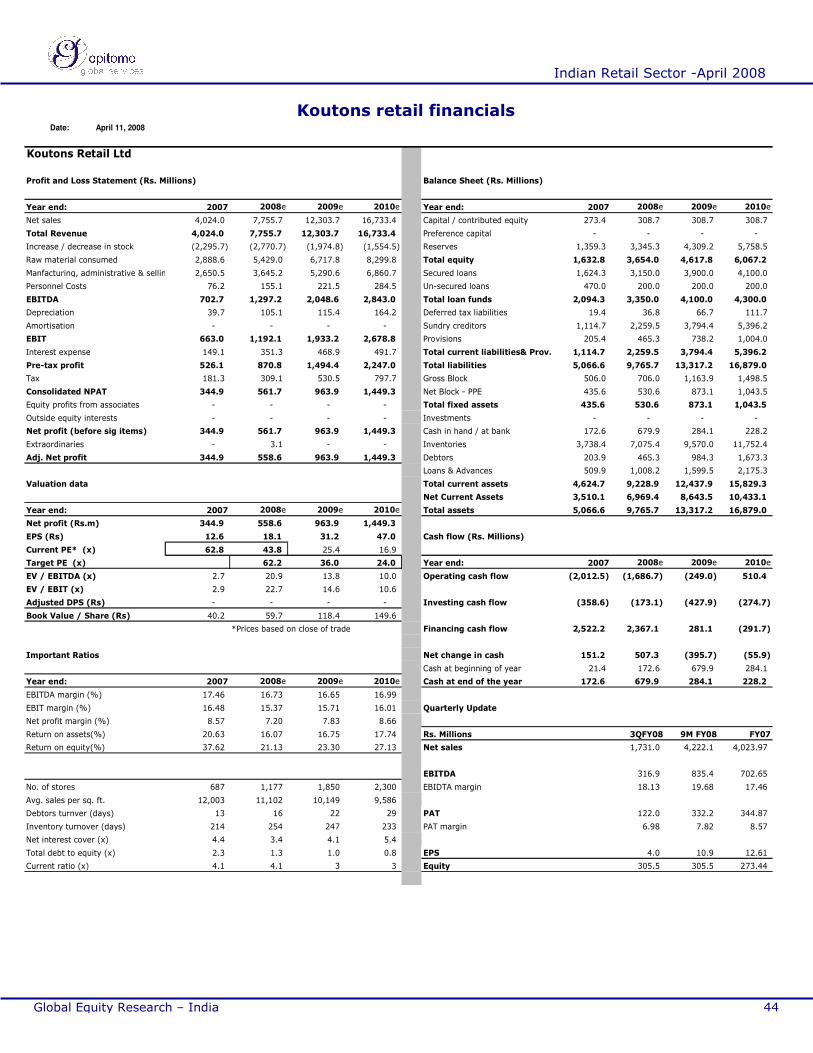

RS IN MN FY07 FY08E FY09E FY10E

NET SALES 4,023.97 7,755.74 12,303.68 16,733.38

YoY SALES GROWTH (%)

154.13

92.74 58.64 36.00

EBITDA 702.65 1,297.15 2,048.58 2,843.01

PAT 344.87 558.56 963.86 1,449.33

YoY PAT GROWTH (%)

161.30

61.96 72.56 50.37

EQUITY 273.44 308.68 308.68 308.68

EPS Rs 12.61 18.09 31.22 46.95

OPM (%) 17.46 16.73 16.65 16.99

NPM (%) 8.57 7.20 7.83 8.66

ROCE (%) 20.63

16.07 16.75 17.74

PER x - 43.77 25.36 16.87

P / BV x - 13.26 6.69 5.29

EV / NET SALES x 0.48 3.50 2.30 1.70

Recommendation

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

22 Global Equity Research – India

Company overview

Koutons was incorporated in 1994 as Charlie Creations Private Ltd.

The name was later changed to Koutons Retail Private Limited in

February 2006 and Koutons Retail India Limited from June 2006.

Koutons Retail has emerged as an integrated apparel manufacturing

and retailing company. It undertakes designing, manufacturing and

retailing of apparel under the Koutons, Charlie Outlaw, Upper Class,

Les Femme, and Koutons Junior brands.

The Company’s major focus area has been to target men’s apparel

range including denim and non-denim trousers, formal and casual

shirts, t-shirts, suits, blazers, sweat shirts, cargos in the middle to

high fashion segment predominantly through the Company’s ebos

(Exclusive brand outlets).

To address a broader customer base, the Company has recently

introduced a line of women’s wear under the “Les femme” brand and

the “Koutons Junior” brand that targets the children.

The Company sold 9.2 million garments during FY07 through Koutons

and Charlie Outlaw showrooms. As the brand Charlie Outlaw was

launched only in October; over 90% of sales were derived from

Koutons. Thus, Koutons became the only brand in the country to sell

maximum number of garments during FY07.

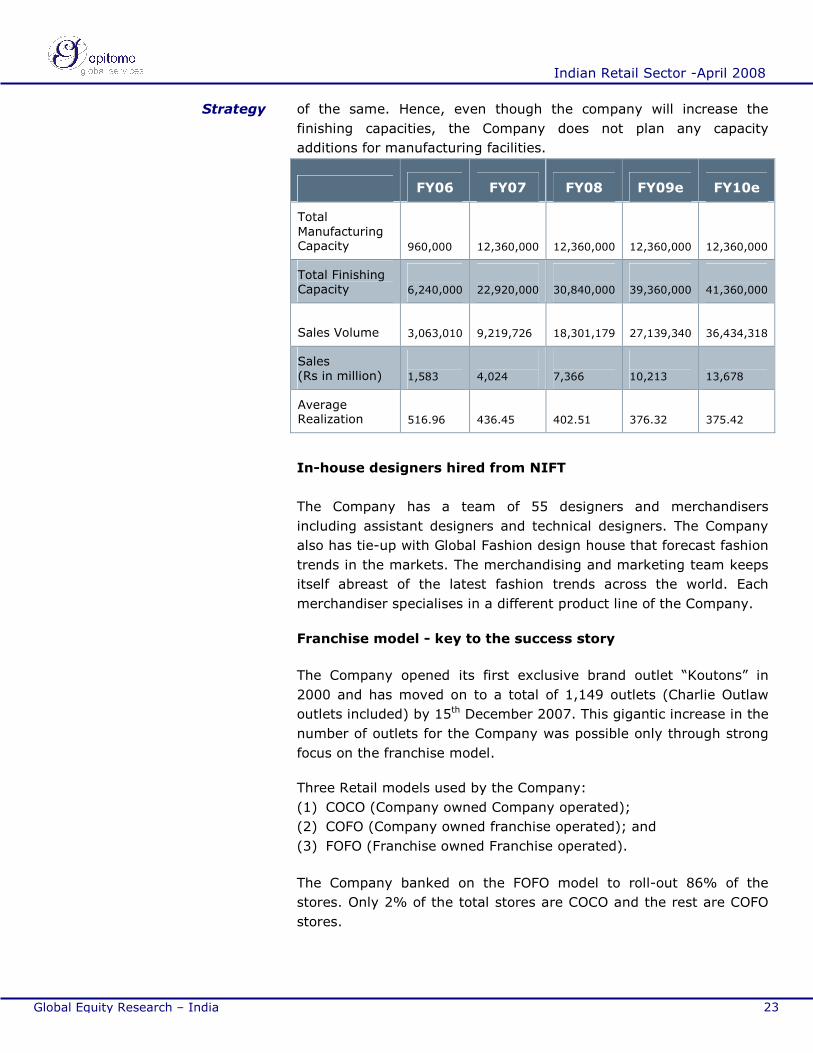

Strategy

Integrated Manufacturing Facilities

The Company presently has 18 manufacturing units (1 Owned and

rest leased for a period of 5-7 years) and 14 warehouses located in

and around Gurgaon. An integrated manufacturing unit at Gurgaon,

Haryana will be set-up on the 13,000 square feet of land allotted to

the Company by the Government and commissioned by December

2008. The Company will shift 7-8 of the existing units to this location

which will improve efficiencies and lower the lease rental costs to that

extent for the Company.

In the appreciating rupee scenario, a lot of domestic manufacturing

capacities and those in Bangladesh are lying idle which is available for

domestic retailers. And the Company plans to take full advantage

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

23 Global Equity Research – India

of the same. Hence, even though the company will increase the

finishing capacities, the Company does not plan any capacity

additions for manufacturing facilities.

FY06 FY07 FY08 FY09e FY10e

Total Manufacturing Capacity

960,000

12,360,000

12,360,000

12,360,000

12,360,000

Total Finishing Capacity

6,240,000

22,920,000

30,840,000

39,360,000

41,360,000

Sales Volume 3,063,010

9,219,726

18,301,179

27,139,340

36,434,318

Sales (Rs in million)

1,583

4,024

7,366

10,213

13,678

Average Realization

516.96

436.45

402.51

376.32

375.42

In-house designers hired from NIFT

The Company has a team of 55 designers and merchandisers

including assistant designers and technical designers. The Company

also has tie-up with Global Fashion design house that forecast fashion

trends in the markets. The merchandising and marketing team keeps

itself abreast of the latest fashion trends across the world. Each

merchandiser specialises in a different product line of the Company.

Franchise model - key to the success story

The Company opened its first exclusive brand outlet “Koutons” in

2000 and has moved on to a total of 1,149 outlets (Charlie Outlaw

outlets included) by 15th December 2007. This gigantic increase in the

number of outlets for the Company was possible only through strong

focus on the franchise model.

Three Retail models used by the Company:

(1) COCO (Company owned Company operated);

(2) COFO (Company owned franchise operated); and

(3) FOFO (Franchise owned Franchise operated).

The Company banked on the FOFO model to roll-out 86% of the

stores. Only 2% of the total stores are COCO and the rest are COFO

stores.

Strategy

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

24 Global Equity Research – India

Under COFO/FOFO model, the Company bears only the promotion

and advertising expenses and the rest of the expenses including,

operating and staffing expenses, taxation returns etc are borne by

the franchisee.

The franchisee has to pay security deposit (Rs.5 – Rs.10 Lakh) to the

Company for obtaining the rights to open the retail outlet.The

Company is liable to pay interest on the security deposit. Depending

on the volume of sales generated, the franchisee receives commission

or minimum guarantee whichever is higher as consideration. The

company has nine-year franchise agreement where the franchisees

are disallowed to exit for the said period. However, the Company can

close the stores at its own discretion.

Coco store plans

Going forward, the Company plans to increase the share of the COCO

stores as it plans to add larger format flagship stores in 38 cities.

Over the next two years, 120 such stores will be added with store

sizes ranging from 3,000-5,000 square feet. These stores will act as a

one stop shop for the entire family as it will include all the products

range of the Company.

To save on paying higher rentals, the Company plans to open

different stores in the same shopping mall. For example, the ground

floor could be booked for women’s wear while the first floor for Men’s

wear and the basement for kids wear. This would average out the

rental costs of the Company as rentals vary on different floors.

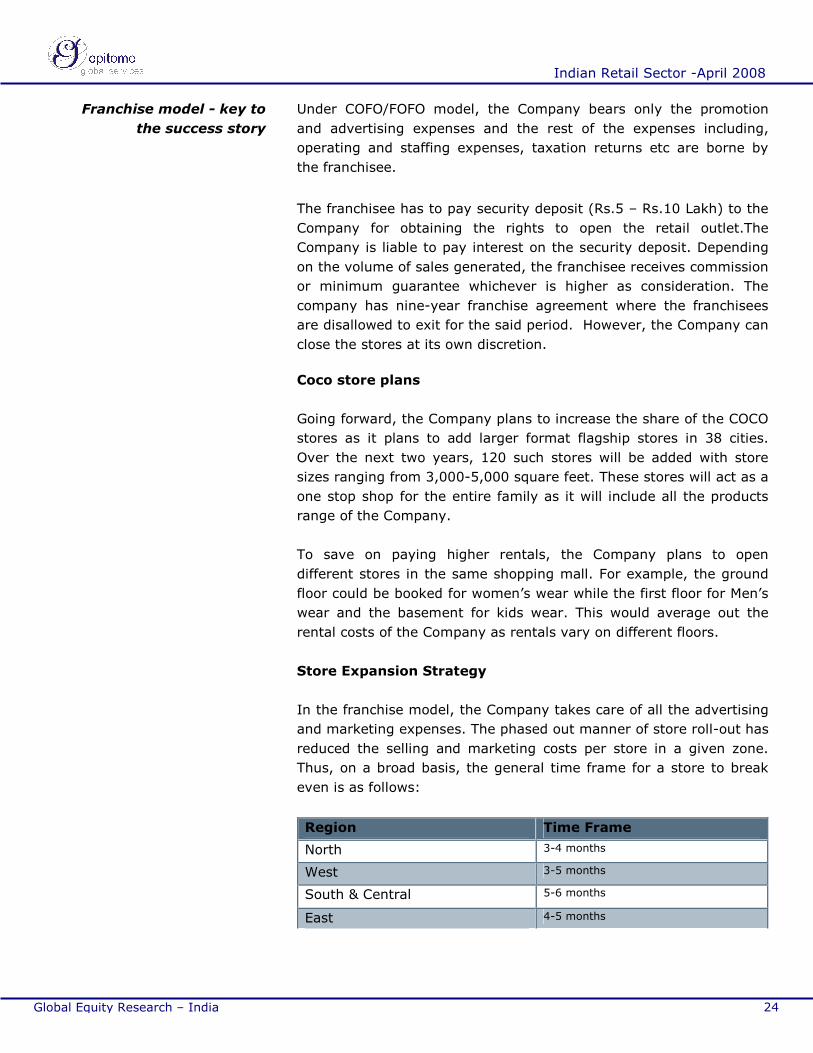

Store Expansion Strategy

In the franchise model, the Company takes care of all the advertising

and marketing expenses. The phased out manner of store roll-out has

reduced the selling and marketing costs per store in a given zone.

Thus, on a broad basis, the general time frame for a store to break

even is as follows:

Region Time Frame

North 3-4 months

West 3-5 months

South & Central 5-6 months

East 4-5 months

Franchise model - key to

the success story

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

25 Global Equity Research – India

The break even point for a Franchise operated store is at the level

when the Company is able to recover the minimum guarantee

payment made on a monthly basis and the selling and advertising

expenses for a region.

In the rising rental costs scenario to keep the franchisees motivated,

the company either increases the minimum guarantee to incorporate

increased rentals or creates sales target slabs which offer incremental

commission rate.

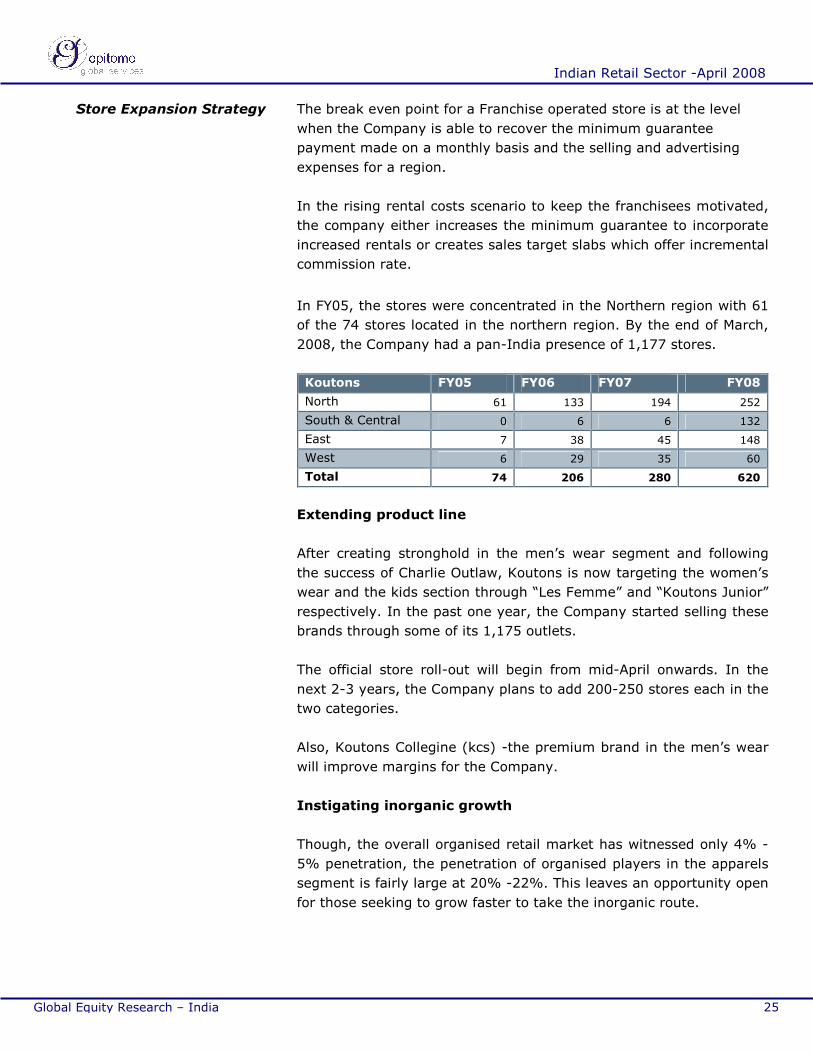

In FY05, the stores were concentrated in the Northern region with 61

of the 74 stores located in the northern region. By the end of March,

2008, the Company had a pan-India presence of 1,177 stores.

Koutons FY05 FY06 FY07 FY08

North 61 133 194 252

South & Central 0 6 6 132

East 7 38 45 148

West 6 29 35 60

Total 74 206 280 620

Extending product line

After creating stronghold in the men’s wear segment and following

the success of Charlie Outlaw, Koutons is now targeting the women’s

wear and the kids section through “Les Femme” and “Koutons Junior”

respectively. In the past one year, the Company started selling these

brands through some of its 1,175 outlets.

The official store roll-out will begin from mid-April onwards. In the

next 2-3 years, the Company plans to add 200-250 stores each in the

two categories.

Also, Koutons Collegine (kcs) -the premium brand in the men’s wear

will improve margins for the Company.

Instigating inorganic growth

Though, the overall organised retail market has witnessed only 4% -

5% penetration, the penetration of organised players in the apparels

segment is fairly large at 20% -22%. This leaves an opportunity open

for those seeking to grow faster to take the inorganic route.

Store Expansion Strategy

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

26 Global Equity Research – India

Koutons capitalised on one such opportunity available to acquire 51%

stake in Delhi-based Upper Class through its 100% subsidiary DBG

retail. Upper Class has strong presence in the ladies apparel segment.

This acquisition goes well with overall strategy of the Company

wherein the Company recently targeted the women’s segment. This

acquisition is expected to add Rs.170 million at the top line and 7 –

8% at net margin level.

The Upper Class has close to two decades of experience in the

women’s premium apparel segment. In the domestic market, Upper

Class has its own brand outlets in New Delhi, Jaipur, Ludhiana and

Vadodara. And it is available in multi brand outlets (mbos) such as

Globus, Piramyd, Shoppers Stop and Pantaloons.

In the export market, Upper Class supplies apparels to leading brands

in Europe such as Armand, Thiery, Class, F Ferra, Alcorpe English,

and is available in stores such as Splash and Lullu Center in the

Middle East under its signature brand Upper class.

Koutons plans to increase the domestic presence of Upper Class to

400 retail outlets by 2010. The Company’s pan-India presence and

franchising experience will facilitate Upper Class in procuring material

from domestic as well as international markets at reasonable prices.

Brand strategy

The Koutons stores are positioned for men’s formal wear range

targeting the 22-45 years age group. The average per store size

varies between 1,000-1,500 square feet. These stores are largely

located in Tier-I cities (roughly corresponding to state capitals and

important cities and Tier-II (roughly corresponding to district

headquarters) cities. At the end of March 2008, the store cont stood

at 620. The Company on an average earns 18%-18.5% margin on

Koutons stores with per store generating approximately Rs.1.2 crore

of revenues.

The Charlie Outlaw stores are positioned for casual wear that target

the 14-25 years of age group. The average per store size varies from

500-700 square feet. These stores are located in Tier II cities

(roughly corresponding to sub-district headquarters), Tier III cities

and Tier IV cities. This small format size of the stores helped the

Company in rolling out stores at an accelerated pace. Since the

launch of 104 stores in a single day in October 2006, the store count

now stands at 557 at the end of March 2008. On an average one

Instigating inorganic growth

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

27 Global Equity Research – India

Charlie outlaw

Store generates Rs. 0.5 – Rs. 0.6 million of revenue and margins

stands at 17% -18%

SCM

Both in the domestic and the international market, the Company

operates through intermediaries.

The Company procures raw materials from India, China, Taiwan and

Italy through third-party suppliers. In the next two years, the

Company plans to set-up offices at Hong Kong and Singapore to

eliminate the intermediaries.

In FY07, out of the total raw material procured, 28% was imported

and the rest was procured from domestic sources. The decision

making process of procuring raw materials is real time / live delayed

as Mr. B.S. Sawhney-Managing Director is involved in procurement of

raw materials.

For the movement of apparels from the warehouse to the ebos, the

Company is dependent on road transport and relies completely on

third-party transporters. In terms of costing and specialisation, the

regional transport companies are more competent and hence the

Company relies on them.

Considering the scale of operations, the Company is able to book

truckloads instead of booking the number of cartons. This reduces the

cost per carton for the Company.

For example, if the Company books place in the truck on the basis of

carton it would cost them around Rs.50 per carton while a truck with

a capacity of 1000 cartons would cost only Rs.22,000. Thus, cost per

carton comes down to Rs.22.

Brand strategy

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

28 Global Equity Research – India

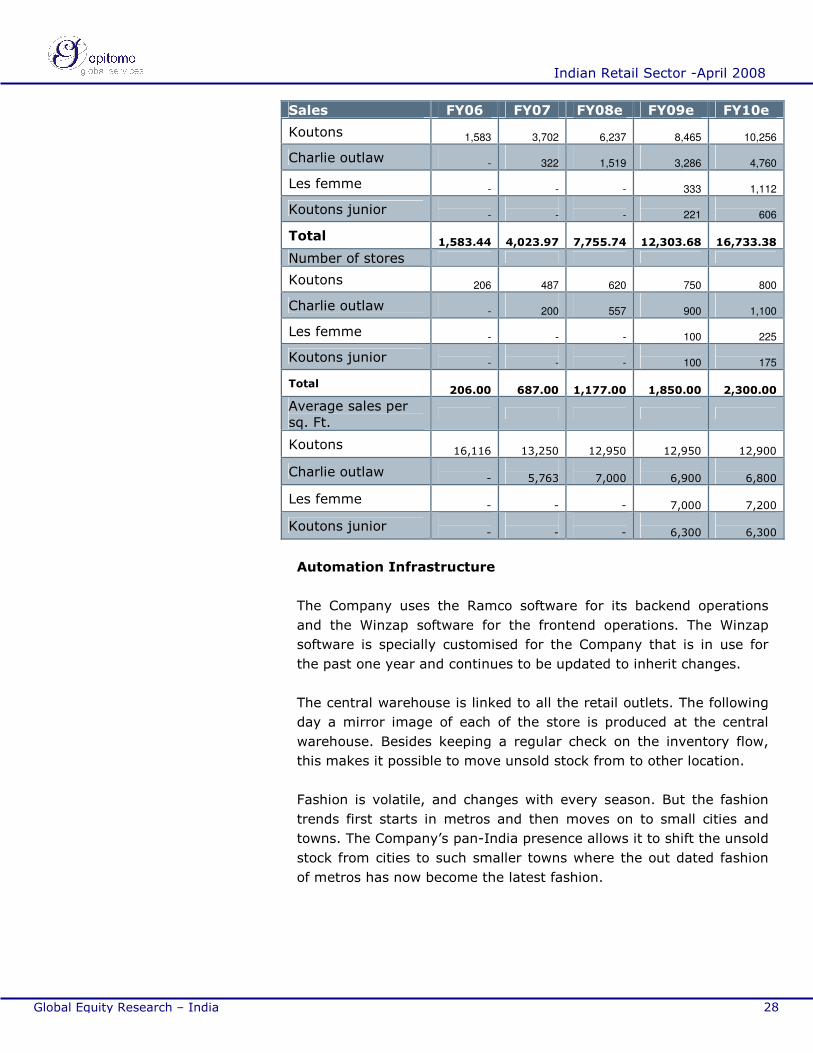

Sales FY06 FY07 FY08e FY09e FY10e

Koutons

1,583

3,702

6,237

8,465

10,256

Charlie outlaw

-

322

1,519

3,286

4,760

Les femme

-

-

-

333

1,112

Koutons junior

-

-

-

221

606

Total

1,583.44

4,023.97

7,755.74

12,303.68

16,733.38

Number of stores

Koutons

206

487

620

750

800

Charlie outlaw

-

200

557

900

1,100

Les femme

-

-

-

100

225

Koutons junior

-

-

-

100

175

Total

206.00

687.00

1,177.00

1,850.00

2,300.00

Average sales per sq. Ft.

Koutons

16,116

13,250

12,950

12,950

12,900

Charlie outlaw -

5,763

7,000

6,900

6,800

Les femme -

-

-

7,000

7,200

Koutons junior -

-

-

6,300

6,300

Automation Infrastructure

The Company uses the Ramco software for its backend operations

and the Winzap software for the frontend operations. The Winzap

software is specially customised for the Company that is in use for

the past one year and continues to be updated to inherit changes.

The central warehouse is linked to all the retail outlets. The following

day a mirror image of each of the store is produced at the central

warehouse. Besides keeping a regular check on the inventory flow,

this makes it possible to move unsold stock from to other location.

Fashion is volatile, and changes with every season. But the fashion

trends first starts in metros and then moves on to small cities and

towns. The Company’s pan-India presence allows it to shift the unsold

stock from cities to such smaller towns where the out dated fashion

of metros has now become the latest fashion.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

29 Global Equity Research – India

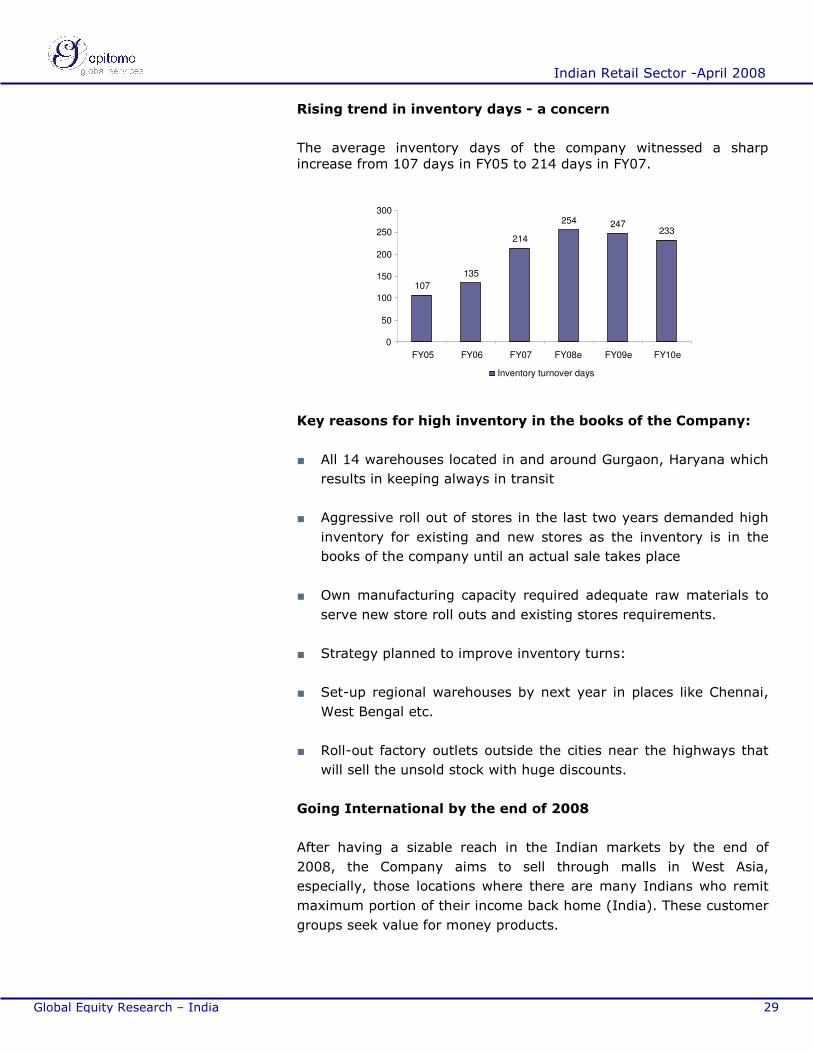

Rising trend in inventory days - a concern

The average inventory days of the company witnessed a sharp increase from 107 days in FY05 to 214 days in FY07.

107 135

214

254 247 233

0

50

100

150

200

250

300

FY05 FY06 FY07 FY08e FY09e FY10e

Inventory turnover days

Key reasons for high inventory in the books of the Company:

■ All 14 warehouses located in and around Gurgaon, Haryana which

results in keeping always in transit

■ Aggressive roll out of stores in the last two years demanded high

inventory for existing and new stores as the inventory is in the

books of the company until an actual sale takes place

■ Own manufacturing capacity required adequate raw materials to

serve new store roll outs and existing stores requirements.

■ Strategy planned to improve inventory turns:

■ Set-up regional warehouses by next year in places like Chennai,

West Bengal etc.

■ Roll-out factory outlets outside the cities near the highways that

will sell the unsold stock with huge discounts.

Going International by the end of 2008

After having a sizable reach in the Indian markets by the end of

2008, the Company aims to sell through malls in West Asia,

especially, those locations where there are many Indians who remit

maximum portion of their income back home (India). These customer

groups seek value for money products.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

30 Global Equity Research – India

Also, “Upper Class” already has presence in Europe and Middle East.

The Company initially plan to supply to other stores – both to test the

markets and to create brand visibility and eventually open their

stores in those areas.

In India, the Company has booked space for 240 stores in mall areas

with an average carpet area of 800-900 sq.ft. The Company will open

200 stores of all formats during April 15-May 15.

Financial performance

Strong Revenue growth – 135% CAGR in 3 years

In the past three years, the Company grew at a CAGR of 134.85%

and generated revenues of Rs.4,023.97 million in FY07. This growth

is largely attributable to aggressive expansion strategy adopted by

the Company. The region-wise contribution to percentage sales

growth is depicted from the following table:

Zonal Break-up (%) FY06 FY07 FY08

North 174.75 84.43 32.15

South & Central - 197.95 185.11

East 1074.85 264.60 58.23

West 304.00 285.00 45.84

*No comparable data available for FY06

This clearly implies that the growth in the Northern region is

maturing. The other regions continue to show high growth backed by

increased penetration.

In the Southern and Central region the store count has significantly

moved up from 6 to 132 which support the triple-digit sales growth.

Growth in store and total Square feet

Going forward, we expect the store count to grow from 1170 in FY08

to 2300 in FY10 with the corresponding space increase from 0.8

million to 1.9 million.

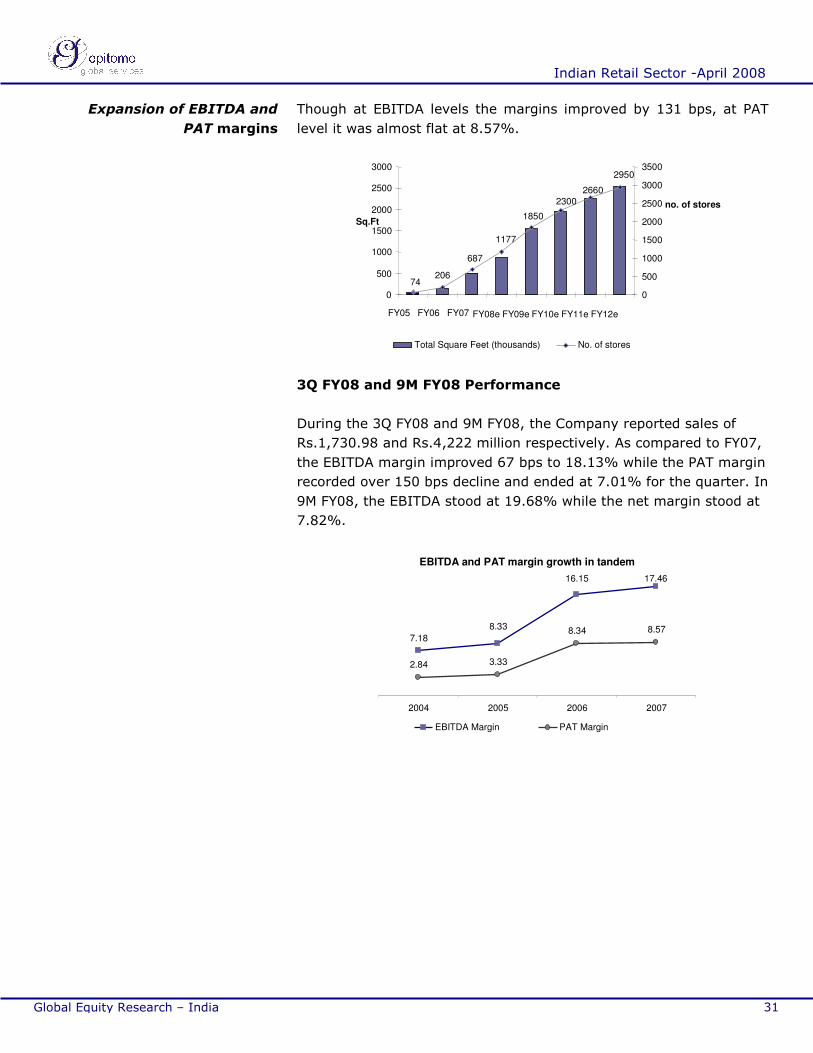

Expansion of EBITDA and PAT margins

During FY06, the Company saw huge margin expansion due to

benefits of economies of scale and in FY07, margins have maintained

at around same level. As seen from the chart, the EBITDA and PAT

margins stood at 16.15% and 8.34% respectively in FY06.

Going International by

the end of 2008

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

31 Global Equity Research – India

Though at EBITDA levels the margins improved by 131 bps, at PAT

level it was almost flat at 8.57%.

74 206 687

1177

1850

2950 2660

2300

0

500

1000

1500

2000

2500

3000

FY05 FY06 FY07 FY08e FY09e FY10e FY11e FY12e

Sq.Ft

0

500

1000

1500

2000

2500

3000

3500

no. of stores

Total Square Feet (thousands) No. of stores

3Q FY08 and 9M FY08 Performance

During the 3Q FY08 and 9M FY08, the Company reported sales of

Rs.1,730.98 and Rs.4,222 million respectively. As compared to FY07,

the EBITDA margin improved 67 bps to 18.13% while the PAT margin

recorded over 150 bps decline and ended at 7.01% for the quarter. In

9M FY08, the EBITDA stood at 19.68% while the net margin stood at

7.82%.

EBITDA and PAT margin growth in tandem

7.18 8.33

16.15

2.84 3.33

8.34 8.57

17.46

2004 2005 2006 2007

EBITDA Margin PAT Margin

Expansion of EBITDA and

PAT margins

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

32 Global Equity Research – India

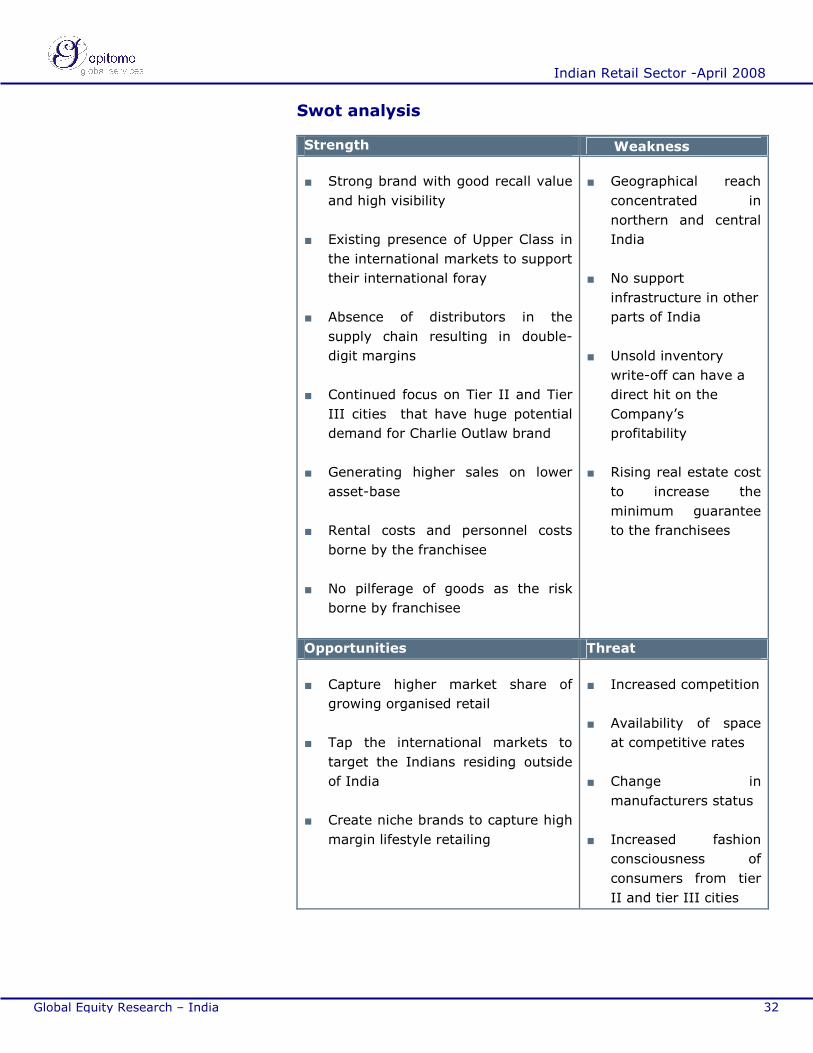

Swot analysis

Strength Weakness

■ Strong brand with good recall value

and high visibility

■ Existing presence of Upper Class in

the international markets to support

their international foray

■ Absence of distributors in the

supply chain resulting in double-

digit margins

■ Continued focus on Tier II and Tier

III cities that have huge potential

demand for Charlie Outlaw brand

■ Generating higher sales on lower

asset-base

■ Rental costs and personnel costs

borne by the franchisee

■ No pilferage of goods as the risk

borne by franchisee

■ Geographical reach

concentrated in

northern and central

India

■ No support

infrastructure in other

parts of India

■ Unsold inventory

write-off can have a

direct hit on the

Company’s

profitability

■ Rising real estate cost

to increase the

minimum guarantee

to the franchisees

Opportunities Threat

■ Capture higher market share of

growing organised retail

■ Tap the international markets to

target the Indians residing outside

of India

■ Create niche brands to capture high

margin lifestyle retailing

■ Increased competition

■ Availability of space

at competitive rates

■ Change in

manufacturers status

■ Increased fashion

consciousness of

consumers from tier

II and tier III cities

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

33 Global Equity Research – India

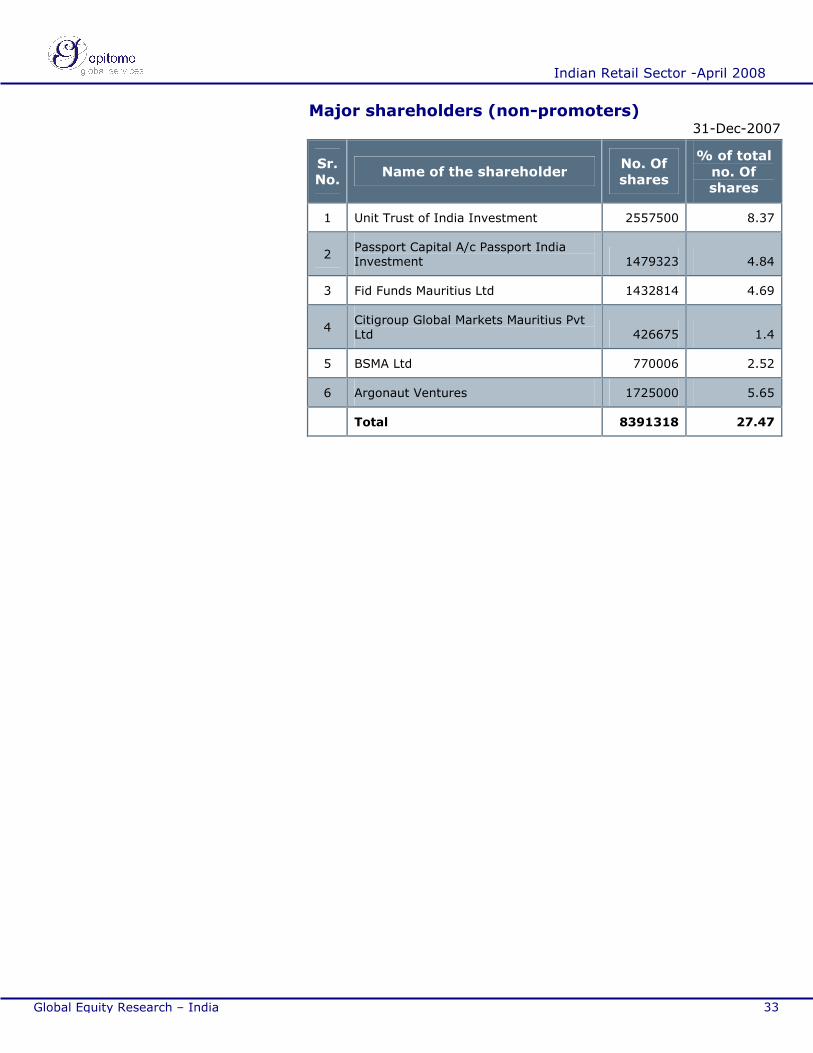

Major shareholders (non-promoters) 31-Dec-2007

Sr.

No. Name of the shareholder

No. Of

shares

% of total

no. Of shares

1 Unit Trust of India Investment 2557500 8.37

2 Passport Capital A/c Passport India Investment 1479323 4.84

3 Fid Funds Mauritius Ltd 1432814 4.69

4 Citigroup Global Markets Mauritius Pvt Ltd 426675 1.4

5 BSMA Ltd 770006 2.52

6 Argonaut Ventures 1725000 5.65

Total 8391318 27.47

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

34 Global Equity Research – India

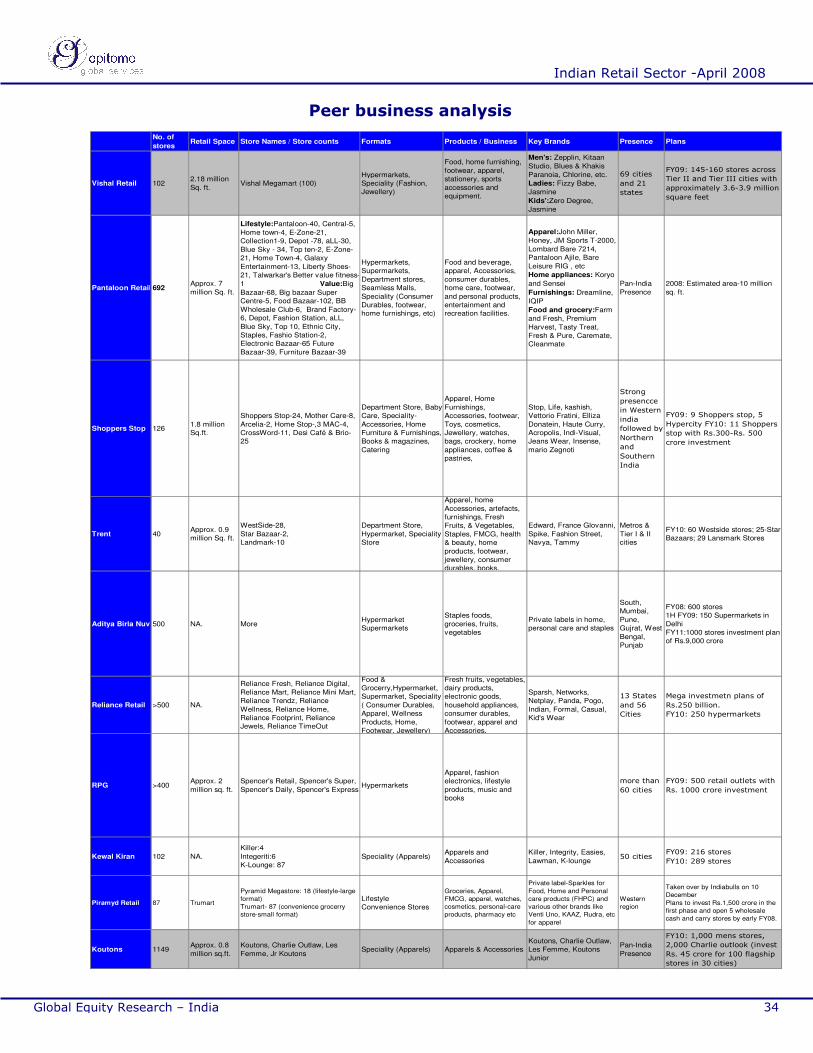

Peer business analysis

No. of

storesRetail Space Store Names / Store counts Formats Products / Business Key Brands Presence Plans

Vishal Retail 1022.18 million

Sq. ft.Vishal Megamart (100)

Hypermarkets,

Speciality (Fashion,

Jewellery)

Food, home furnishing,

footwear, apparel,

stationery, sports

accessories and

equipment.

Men's: Zepplin, Kitaan

Studio, Blues & Khakis

Paranoia, Chlorine, etc.

Ladies: Fizzy Babe,

Jasmine

Kids':Zero Degree,

Jasmine

69 cities

and 21

states

FY09: 145-160 stores across

Tier II and Tier III cities with

approximately 3.6-3.9 million

square feet

Pantaloon Retail 692Approx. 7

million Sq. ft.

Lifestyle:Pantaloon-40, Central-5,

Home town-4, E-Zone-21,

Collection1-9, Depot -78, aLL-30,

Blue Sky - 34, Top ten-2, E-Zone-

21, Home Town-4, Galaxy

Entertainment-13, Liberty Shoes-

21, Talwarkar's Better value fitness-

1 Value:Big

Bazaar-68, Big bazaar Super

Centre-5, Food Bazaar-102, BB

Wholesale Club-6, Brand Factory-

6, Depot, Fashion Station, aLL,

Blue Sky, Top 10, Ethnic City,

Staples, Fashio Station-2,

Electronic Bazaar-65 Future

Bazaar-39, Furniture Bazaar-39

Hypermarkets,

Supermarkets,

Department stores,

Seamless Malls,

Speciality (Consumer

Durables, footwear,

home furnishings, etc)

Food and beverage,

apparel, Accessories,

consumer durables,

home care, footwear,

and personal products,

entertainment and

recreation facilities.

Apparel:John Miller,

Honey, JM Sports T-2000,

Lombard Bare 7214,

Pantaloon Ajile, Bare

Leisure RIG , etc

Home appliances: Koryo

and Sensei

Furnishings: Dreamline,

IQIP

Food and grocery:Farm

and Fresh, Premium

Harvest, Tasty Treat,

Fresh & Pure, Caremate,

Cleanmate

Pan-India

Presence

2008: Estimated area-10 million

sq. ft.

Shoppers Stop 1261.8 million

Sq.ft.

Shoppers Stop-24, Mother Care-8,

Arcelia-2, Home Stop-,3 MAC-4,

CrossWord-11, Desi Café & Brio-

25

Department Store, Baby

Care, Speciality-

Accessories, Home

Furniture & Furnishings,

Books & magazines,

Catering

Apparel, Home

Furnishings,

Accessories, footwear,

Toys, cosmetics,

Jewellery, watches,

bags, crockery, home

appliances, coffee &

pastries,

Stop, Life, kashish,

Vettorio Fratini, Elliza

Donatein, Haute Curry,

Acropolis, Indi-Visual,

Jeans Wear, Insense,

mario Zegnoti

Strong

presencce

in Western

india

followed by

Northern

and

Southern

India

FY09: 9 Shoppers stop, 5

Hypercity FY10: 11 Shoppers

stop with Rs.300-Rs. 500

crore investment

Trent 40Approx. 0.9

million Sq. ft.

WestSide-28,

Star Bazaar-2,

Landmark-10

Department Store,

Hypermarket, Speciality

Store

Apparel, home

Accessories, artefacts,

furnishings, Fresh

Fruits, & Vegetables,

Staples, FMCG, health

& beauty, home

products, footwear,

jewellery, consumer

durables, books,

Edward, France Glovanni,

Spike, Fashion Street,

Navya, Tammy

Metros &

Tier I & II

cities

FY10: 60 Westside stores; 25-Star

Bazaars; 29 Lansmark Stores

Aditya Birla Nuvo500 NA. MoreHypermarket

Supermarkets

Staples foods,

groceries, fruits,

vegetables

Private labels in home,

personal care and staples

South,

Mumbai,

Pune,

Gujrat, West

Bengal,

Punjab

FY08: 600 stores

1H FY09: 150 Supermarkets in

Delhi

FY11:1000 stores investment plan

of Rs.9,000 crore

Reliance Retail >500 NA.

Reliance Fresh, Reliance Digital,

Reliance Mart, Reliance Mini Mart,

Reliance Trendz, Reliance

Wellness, Reliance Home,

Reliance Footprint, Reliance

Jewels, Reliance TimeOut

Food &

Grocerry,Hypermarket,

Supermarket, Speciality

( Consumer Durables,

Apparel, Wellness

Products, Home,

Footwear, Jewellery)

Fresh fruits, vegetables,

dairy products,

electronic goods,

household appliances,

consumer durables,

footwear, apparel and

Accessories,

Sparsh, Networks,

Netplay, Panda, Pogo,

Indian, Formal, Casual,

Kid's Wear

13 States

and 56

Cities

Mega investmetn plans of

Rs.250 billion.

FY10: 250 hypermarkets

RPG >400Approx. 2

million sq. ft.

Spencer's Retail, Spencer's Super,

Spencer's Daily, Spencer's ExpressHypermarkets

Apparel, fashion

electronics, lifestyle

products, music and

books

more than

60 cities

FY09: 500 retail outlets with

Rs. 1000 crore investment

Kewal Kiran 102 NA.

Killer:4

Integeriti:6

K-Lounge: 87

Speciality (Apparels)Apparels and

Accessories

Killer, Integrity, Easies,

Lawman, K-lounge50 cities

FY09: 216 stores

FY10: 289 stores

Piramyd Retail 87 Trumart

Pyramid Megastore: 18 (lifestyle-large

format)

Trumart- 87 (convenience grocerry

store-small format)

Lifestyle

Convenience Stores

Groceries, Apparel,

FMCG, apparel, watches,

cosmetics, personal-care

products, pharmacy etc

Private label-Sparkles for

Food, Home and Personal

care products (FHPC) and

various other brands like

Venti Uno, KAAZ, Rudra, etc

for apparel

Western

region

Taken over by Indiabulls on 10

December

Plans to invest Rs.1,500 crore in the

first phase and open 5 wholesale

cash and carry stores by early FY08.

Koutons 1149Approx. 0.8

million sq.ft.

Koutons, Charlie Outlaw, Les

Femme, Jr KoutonsSpeciality (Apparels) Apparels & Accessories

Koutons, Charlie Outlaw,

Les Femme, Koutons

Junior

Pan-India

Presence

FY10: 1,000 mens stores,

2,000 Charlie outlook (invest

Rs. 45 crore for 100 flagship

stores in 30 cities)

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

35 Global Equity Research – India

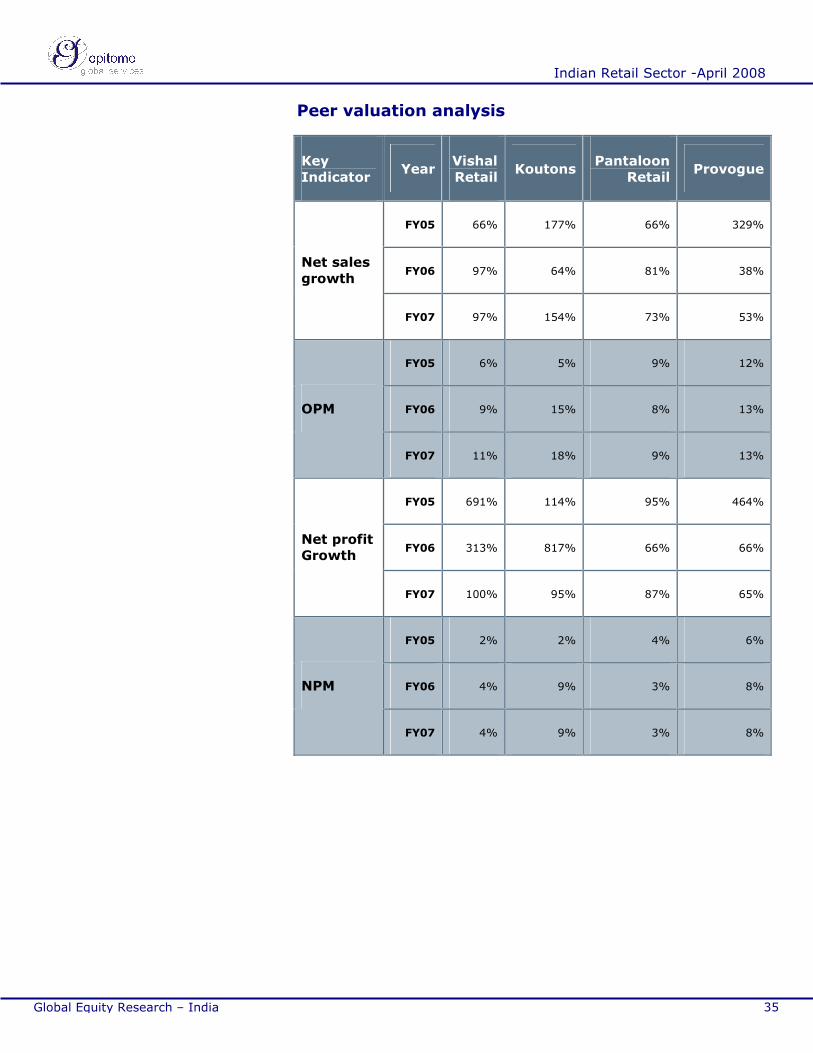

Peer valuation analysis

Key

Indicator Year

Vishal

Retail Koutons

Pantaloon

Retail Provogue

FY05 66% 177% 66% 329%

FY06 97% 64% 81% 38% Net sales

growth

FY07 97% 154% 73% 53%

FY05 6% 5% 9% 12%

FY06 9% 15% 8% 13% OPM

FY07 11% 18% 9% 13%

FY05 691% 114% 95% 464%

FY06 313% 817% 66% 66% Net profit

Growth

FY07 100% 95% 87% 65%

FY05 2% 2% 4% 6%

FY06 4% 9% 3% 8% NPM

FY07 4% 9% 3% 8%

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

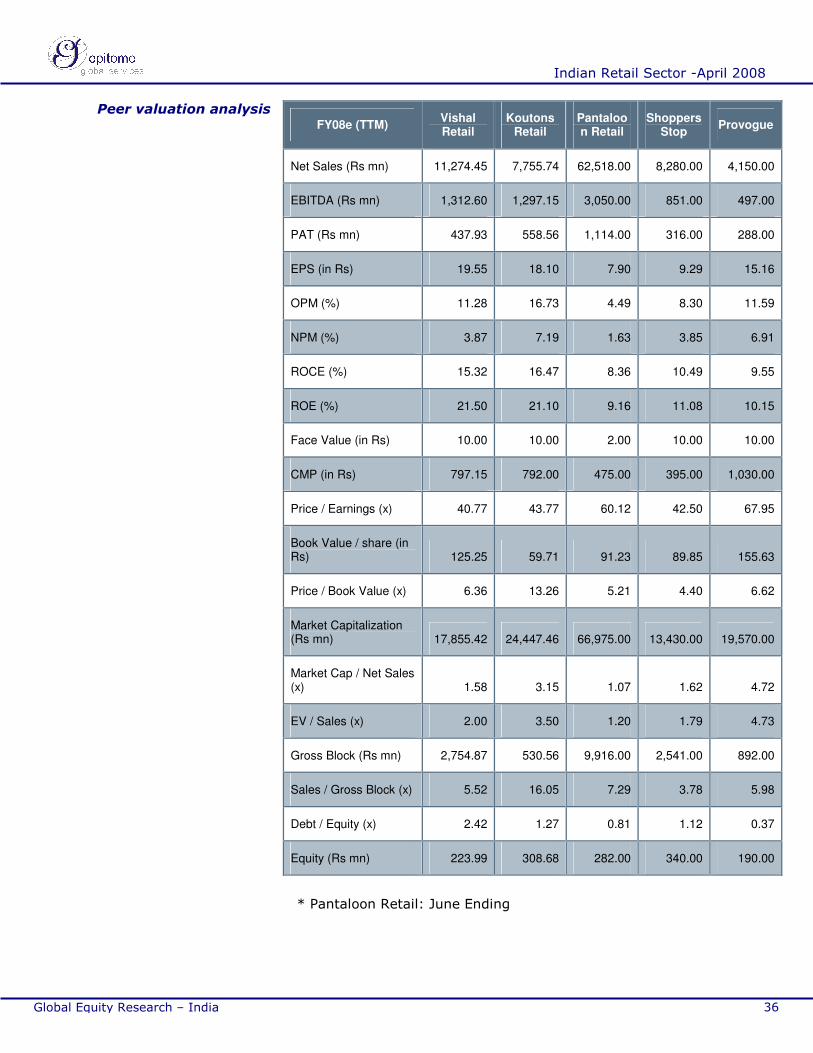

36 Global Equity Research – India

FY08e (TTM) Vishal Retail

Koutons Retail

Pantaloon Retail

Shoppers Stop

Provogue

Net Sales (Rs mn) 11,274.45 7,755.74 62,518.00 8,280.00 4,150.00

EBITDA (Rs mn) 1,312.60 1,297.15 3,050.00 851.00 497.00

PAT (Rs mn) 437.93 558.56 1,114.00 316.00 288.00

EPS (in Rs) 19.55 18.10 7.90 9.29 15.16

OPM (%) 11.28 16.73 4.49 8.30 11.59

NPM (%) 3.87 7.19 1.63 3.85 6.91

ROCE (%) 15.32 16.47 8.36 10.49 9.55

ROE (%) 21.50 21.10 9.16 11.08 10.15

Face Value (in Rs) 10.00 10.00 2.00 10.00 10.00

CMP (in Rs) 797.15 792.00 475.00 395.00 1,030.00

Price / Earnings (x) 40.77 43.77 60.12 42.50 67.95

Book Value / share (in Rs) 125.25 59.71 91.23 89.85 155.63

Price / Book Value (x) 6.36 13.26 5.21 4.40 6.62

Market Capitalization (Rs mn) 17,855.42 24,447.46 66,975.00 13,430.00 19,570.00

Market Cap / Net Sales (x) 1.58 3.15 1.07 1.62 4.72

EV / Sales (x) 2.00 3.50 1.20 1.79 4.73

Gross Block (Rs mn) 2,754.87 530.56 9,916.00 2,541.00 892.00

Sales / Gross Block (x) 5.52 16.05 7.29 3.78 5.98

Debt / Equity (x) 2.42 1.27 0.81 1.12 0.37

Equity (Rs mn) 223.99 308.68 282.00 340.00 190.00

* Pantaloon Retail: June Ending

Peer valuation analysis

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

37 Global Equity Research – India

Though Pantaloon Retails’ sales dwarf the sales of both Vishal retail

and Koutons it clearly suggests the kind of potential growth

opportunity available in India.

Leveraging on the strength of the franchise model, Koutons retail has

been able to generate the highest margins both at the operating and

net levels.

Vishal Retail’s operating level margin compares well with Provogue

but the product offering in the FMCG and non apparel categories

along with massive investment lined up by the company puts

pressure on net margins that stand at lower-single digit levels.

However, ROCE and ROE for both Vishal Retail and Koutons makes

them a promising investment opportunity.

Koutons price to book value and sales to gross block is the highest

among its peers as the company derives its sales on a very low asset

base of rs.705.98 million.

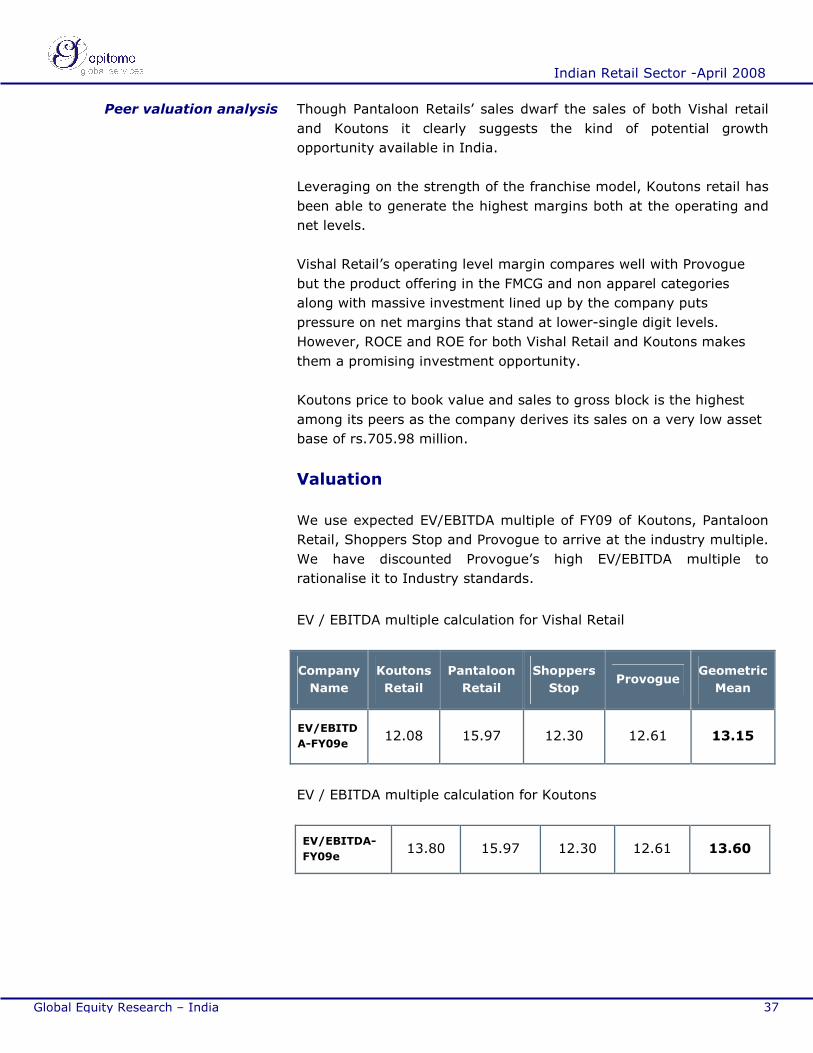

Valuation

We use expected EV/EBITDA multiple of FY09 of Koutons, Pantaloon

Retail, Shoppers Stop and Provogue to arrive at the industry multiple.

We have discounted Provogue’s high EV/EBITDA multiple to

rationalise it to Industry standards.

EV / EBITDA multiple calculation for Vishal Retail

Company

Name

Koutons

Retail

Pantaloon

Retail

Shoppers

Stop Provogue

Geometric

Mean

EV/EBITD

A-FY09e 12.08 15.97 12.30 12.61 13.15

EV / EBITDA multiple calculation for Koutons

EV/EBITDA-

FY09e 13.80 15.97 12.30 12.61 13.60

Peer valuation analysis

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

38 Global Equity Research – India

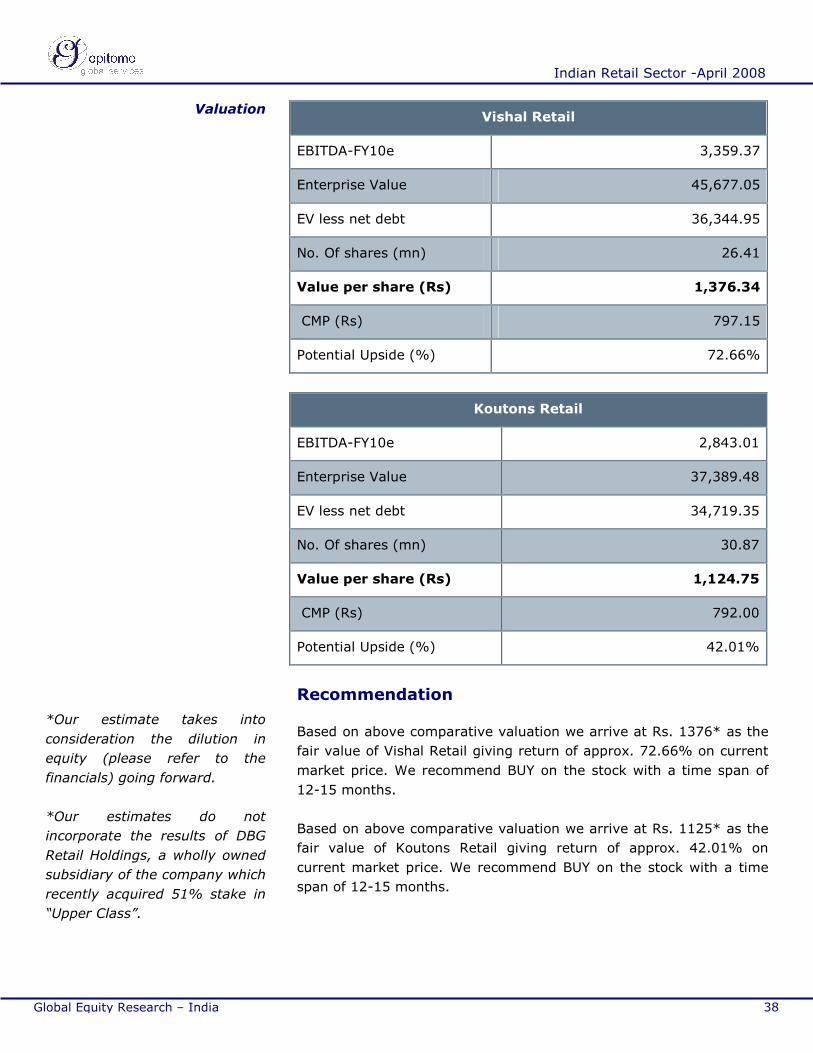

Vishal Retail

EBITDA-FY10e 3,359.37

Enterprise Value 45,677.05

EV less net debt 36,344.95

No. Of shares (mn) 26.41

Value per share (Rs) 1,376.34

CMP (Rs) 797.15

Potential Upside (%) 72.66%

Koutons Retail

EBITDA-FY10e 2,843.01

Enterprise Value 37,389.48

EV less net debt 34,719.35

No. Of shares (mn) 30.87

Value per share (Rs) 1,124.75

CMP (Rs) 792.00

Potential Upside (%) 42.01%

Recommendation

Based on above comparative valuation we arrive at Rs. 1376* as the

fair value of Vishal Retail giving return of approx. 72.66% on current

market price. We recommend BUY on the stock with a time span of

12-15 months.

Based on above comparative valuation we arrive at Rs. 1125* as the

fair value of Koutons Retail giving return of approx. 42.01% on

current market price. We recommend BUY on the stock with a time

span of 12-15 months.

*Our estimate takes into

consideration the dilution in

equity (please refer to the

financials) going forward.

*Our estimates do not

incorporate the results of DBG

Retail Holdings, a wholly owned

subsidiary of the company which

recently acquired 51% stake in

“Upper Class”.

Valuation

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

39 Global Equity Research – India

Risk & concerns

Vishal retail

Competition risk

The huge investments being planned in the booming retail sector will

result in increased competition. Although the organized retail

presently accounts for only 4% of total retail, their strong presence in

Tier I cities and now their expansion in smaller cities will beef-up

competition.

As a matter of fact, Reliance and Big Bazaar have big plans to

increase the number of stores in NCR region where Vishal retail have

strong presence.

In FY07, the Company derived 62% of its revenues from the Northern

block.

This can affect the same store sales and profitability of the Company

as the existing and potential customers have more choice and the

winner will eventually be the one who is closer to the consumer and

sells at competitive prices.

Execution risk

During FY08, the Company has been able to shore up its store count

to 100 from 49 in FY07.

Also, alone in the March quarter the Company added 18 stores to

meet the targeted store roll-out of 100 for FY08. However going

forward, the store openings may be delayed due to lack of suitable

space and infrastructure bottlenecks.

Supply chain management risk

The Company’s aggressive store roll-out strategy demands a strong

logistics and distribution facilities in place.

So far the Company has been able to post strong performance thanks

to fleet of 60 trucks owned by the Company and 30 warehouses in 9

cities.

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

40 Global Equity Research – India

Also, the Company’s wholly owned subsidiary “Vishal Retail Movers

Ltd” for which the Company already has set-up a team will be an

added advantage.

Fashion risk

The Company generated 63% of its revenue during FY07 through

Apparels. Thus, any change in fashion has its direct impact on the

sales for the Company.

Vishal retail can mitigate this risk by manufacturing the apparels in its

manufacturing plants at Delhi and Dehradun. The Company also has

an in-house team of 40-50 designers.

Rising rental costs

For a retail chain, lease rentals normally accounts for 7 – 8% of

revenue. The location of the Vishal retail stores away from mall areas

in standalone buildings has kept their lease rentals low. In FY07, the

rentals as a percent of sales stood at 5.4%.

The Company continues to maintain focus in tier III cities like

Haldwani, Patiala, Jalandhar, Jammu, Panchkula, Hissar, Bhilwara,

Bikaner, Baddi etc, where rentals per sq. Ft. Is comparatively lower.

This strategy mitigates the risk of high rentals for the Company.

Koutons retail

Execution risk

The Company’s execution capabilities can be easily gauged from the

fact that the number of stores in each of the Koutons and Charlie

Outlaw Brand has grown manifold. From a modest store count of 74

in FY05, the number of stores has grown to 1,177 in FY08.

Any delay in the store roll out can directly impact the future revenues

of the Company.

Competition risk

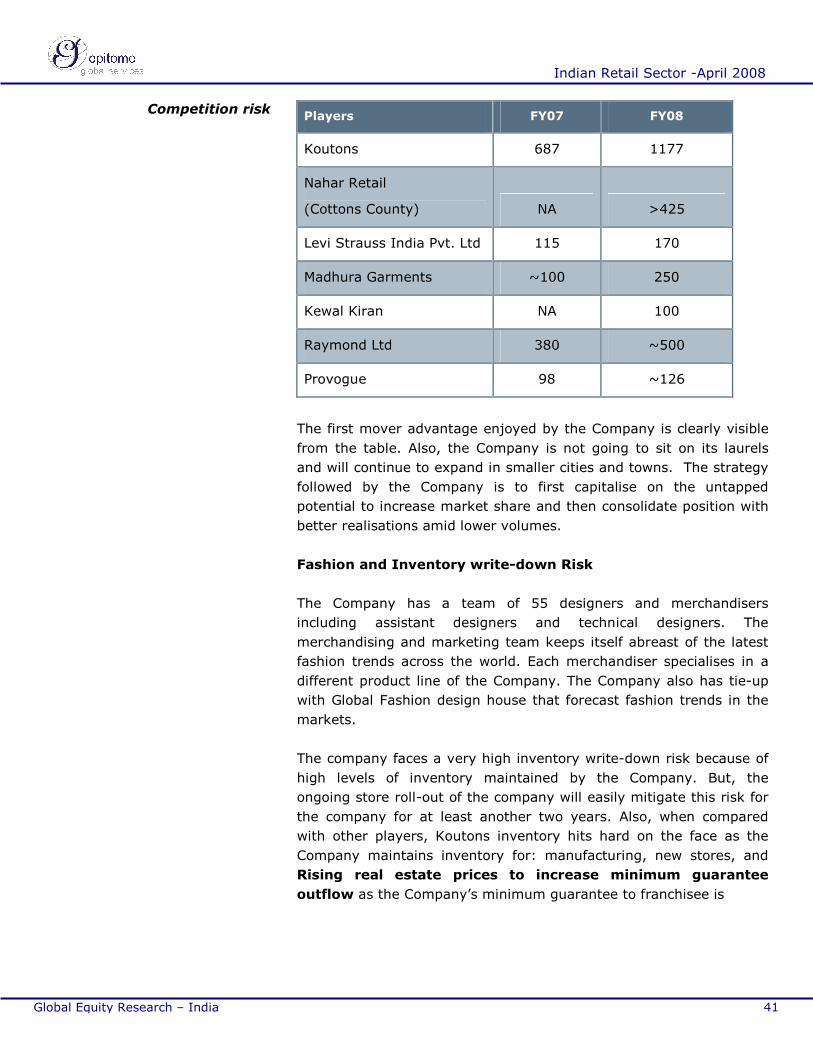

Koutons lead the race in terms of store count. The kind of competition

faced by the Company is visible from the following table:

Supply chain

management risk

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

41 Global Equity Research – India

Players FY07 FY08

Koutons 687 1177

Nahar Retail

(Cottons County) NA >425

Levi Strauss India Pvt. Ltd 115 170

Madhura Garments ~100 250

Kewal Kiran NA 100

Raymond Ltd 380 ~500

Provogue 98 ~126

The first mover advantage enjoyed by the Company is clearly visible

from the table. Also, the Company is not going to sit on its laurels

and will continue to expand in smaller cities and towns. The strategy

followed by the Company is to first capitalise on the untapped

potential to increase market share and then consolidate position with

better realisations amid lower volumes.

Fashion and Inventory write-down Risk

The Company has a team of 55 designers and merchandisers

including assistant designers and technical designers. The

merchandising and marketing team keeps itself abreast of the latest

fashion trends across the world. Each merchandiser specialises in a

different product line of the Company. The Company also has tie-up

with Global Fashion design house that forecast fashion trends in the

markets.

The company faces a very high inventory write-down risk because of

high levels of inventory maintained by the Company. But, the

ongoing store roll-out of the company will easily mitigate this risk for

the company for at least another two years. Also, when compared

with other players, Koutons inventory hits hard on the face as the

Company maintains inventory for: manufacturing, new stores, and

Rising real estate prices to increase minimum guarantee

outflow as the Company’s minimum guarantee to franchisee is

Competition risk

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

42 Global Equity Research – India

dependent on the overall costs borne by the franchisee including the

rentals and salary payable to employees, the increase in real estate

costs has a direct impact on rentals payable by franchisee.

To mitigate this risk, the commission received by the franchisee is

made volume driven. Also, once a store is opened the company has

nine-year franchise agreement where the franchisees are disallowed

to exit for the said period. However, the Company can close the

stores at its own discretion.

Fashion and Inventory

write-down Risk

Indian Retail Research Report

June 19, 2008

Indian Retail Sector -April 2008

43 Global Equity Research – India

Vishal Retail

Profit and loss (Rs. Millions) Balance sheet (Rs. Millions)

Year end: 2007 2008e 2009e 2010e Year end: 2007 2008e 2009e 2010e

Sales revenue 6,026.5 11,274.5 19,613.9 29,458.6 Capital / contributed equity 183.3 224.0 246.2 264.1

Total Revenue 6,049.5 11,315.5 19,680.9 29,538.6 Preference Equity - - - -

COGS 3,462.8 7,770.5 13,478.9 20,202.2 Reserves & Surplus 1,084.4 2,581.5 5,315.1 8,674.8

Personnel Exp 274.1 653.9 1,157.2 1,852.8 Total equity 1,267.6 2,805.4 5,561.3 8,938.9

Manufacturing & admin exp. 301.9 - - - Secured Loans 2,163.0 4,663.0 7,863.0 9,063.0

Selling & Distribution expenses 1,317.3 1,578.4 2,745.9 4,124.2 Un-secured 269.1 269.1 269.1 269.1

EBITDA 693.3 1,312.6 2,298.8 3,359.4 Total Loan Funds 2,432.1 4,932.1 8,132.1 9,332.1

Depreciation 152.9 306.2 561.0 877.0 Current Liabilities 467.1 718.6 1,246.5 1,868.2