Embed Size (px)

Citation preview

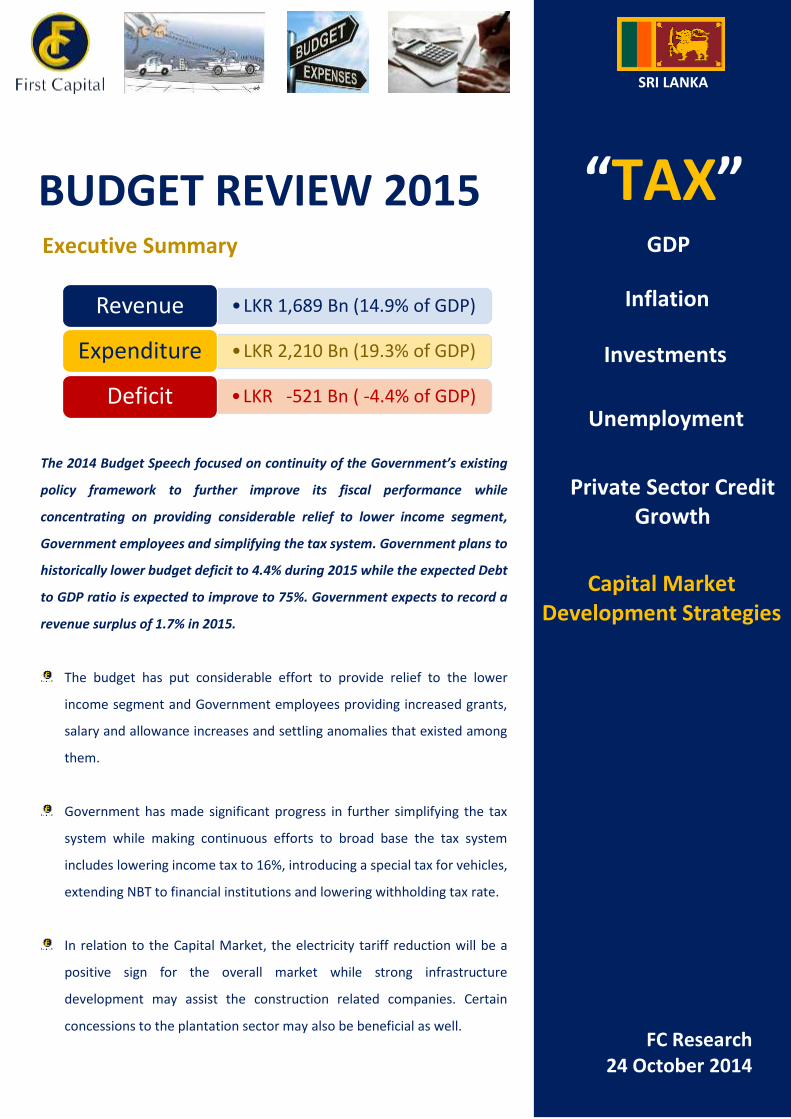

BUDGET REVIEW 2015

The 2014 Budget Speech focused on continuity of the Government’s existing

policy framework to further improve its fiscal performance while

concentrating on providing considerable relief to lower income segment,

Government employees and simplifying the tax system. Government plans to

historically lower budget deficit to 4.4% during 2015 while the expected Debt

to GDP ratio is expected to improve to 75%. Government expects to record a

revenue surplus of 1.7% in 2015.

The budget has put considerable effort to provide relief to the lower

income segment and Government employees providing increased grants,

salary and allowance increases and settling anomalies that existed among

them.

Government has made significant progress in further simplifying the tax

system while making continuous efforts to broad base the tax system

includes lowering income tax to 16%, introducing a special tax for vehicles,

extending NBT to financial institutions and lowering withholding tax rate.

In relation to the Capital Market, the electricity tariff reduction will be a

positive sign for the overall market while strong infrastructure

development may assist the construction related companies. Certain

concessions to the plantation sector may also be beneficial as well.

Executive Summary

Inflation

Unemployment

Private Sector Credit Growth

GDP

Investments

Capital Market Development Strategies

“TAX”

FC Research 24 October 2014

SRI LANKA

•LKR 1,689 Bn (14.9% of GDP)Revenue

•LKR 2,210 Bn (19.3% of GDP)Expenditure

•LKR -521 Bn ( -4.4% of GDP)Deficit

FC Research

2

Budget Review - 2015

Table of Contents

1.0 FISCAL STRATEGY .................................................................................................. 3

BUDGET SUMMARY FOR 2015 .................................................................................. 4

JAN – SEP 2014 FISCAL OUTLOOK ............................................................................. 4

2.0 BUDGET AND THE STOCK MARKET ......................................................................... 5

CAPITAL MARKET DEVELOPMENTS .............................................................................. 5

BUDGET 2014 & LISTED SECURITIES ........................................................................... 5

FC Research

3

Budget Review - 2015

1.0 FISCAL STRATEGY

The Government expects to continue its prime objective to support the country’s growth

prospects in the medium to long run via further strengthening its fiscal position. The fiscal position

is expected to be improved through higher Government revenue and a controlled expenditure

management. Government Revenue is expected reach a surplus of 1.7% of GDP in 2015. Budget

deficit is anticipated to be reduced to 4.4% with Debt to GDP ratio expected to fall to 75.0%.

The Government plans to grow revenue to 14.9% of GDP to LKR 1,689 Bn for 2015 with 84% of the

revenue expected through taxes, with VAT projecting to take the top slot contributing 5.5% of tax

revenue. Non-tax revenue is forecasted to be 10.3% of the total expected government revenue.

The total planned expenditure for 2015 is LKR 2,210 Bn maintained at 19.3% of GDP, which is

slightly below compared to 2014 estimated reach of 19.4% of GDP. Recurrent expenditure is

forecasted to be controlled at 69% of total expenditure constituting 12.9% of GDP significantly

lower from the 2014 planned figure of 13.8% of GDP mainly driven by the support of the declining

interest payments. Salaries and interest payments are expected to be the largest components of

recurrent expenditure amounting to 37% and 28% of recurrent expenditure respectively.

Government plans to grow public investments to 6.5% of GDP with the largest investment

continuing to be for highways where 2.0% of GDP (32% of public investments) is expected to be

spent.

FC Research

4

Budget Review - 2015

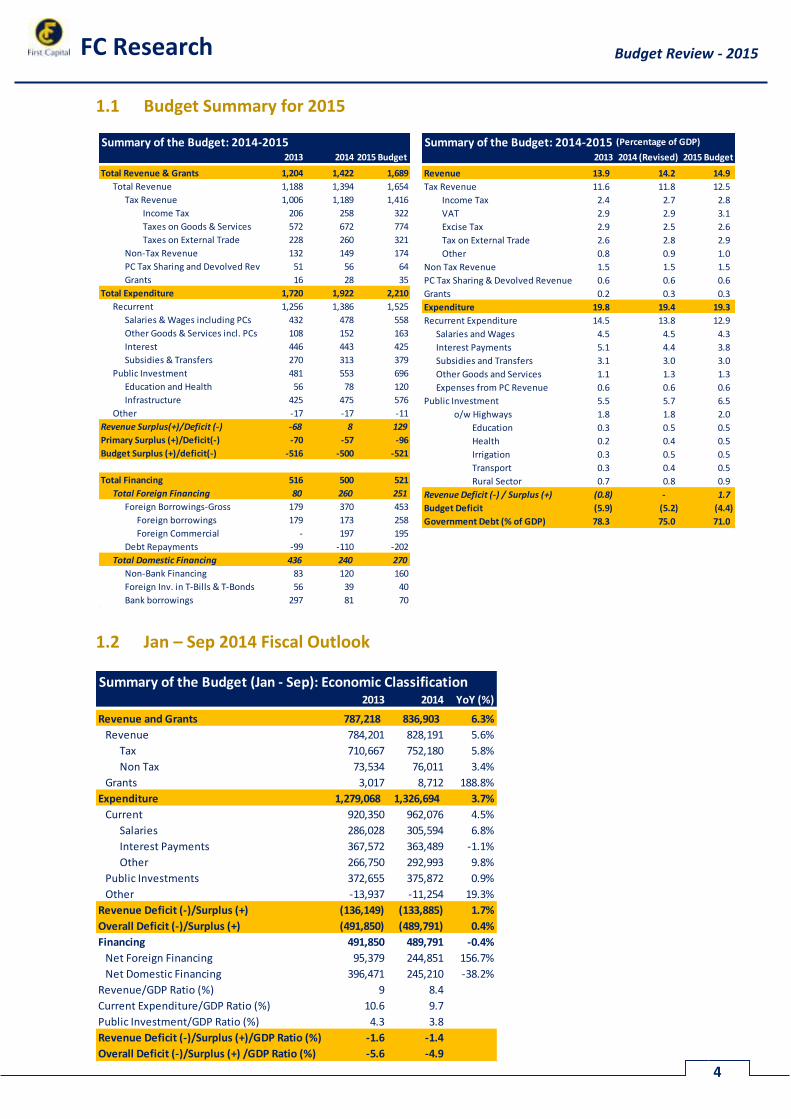

1.1 Budget Summary for 2015

1.2 Jan – Sep 2014 Fiscal Outlook

Summary of the Budget (Jan - Sep): Economic Classification2013 2014 YoY (%)

Revenue and Grants 787,218 836,903 6.3%

Revenue 784,201 828,191 5.6%

Tax 710,667 752,180 5.8%

Non Tax 73,534 76,011 3.4%

Grants 3,017 8,712 188.8%

Expenditure 1,279,068 1,326,694 3.7%

Current 920,350 962,076 4.5%

Salaries 286,028 305,594 6.8%

Interest Payments 367,572 363,489 -1.1%

Other 266,750 292,993 9.8%

Public Investments 372,655 375,872 0.9%

Other -13,937 -11,254 19.3%

Revenue Deficit (-)/Surplus (+) (136,149) (133,885) 1.7%

Overall Deficit (-)/Surplus (+) (491,850) (489,791) 0.4%

Financing 491,850 489,791 -0.4%

Net Foreign Financing 95,379 244,851 156.7%

Net Domestic Financing 396,471 245,210 -38.2%

Revenue/GDP Ratio (%) 9 8.4

Current Expenditure/GDP Ratio (%) 10.6 9.7

Public Investment/GDP Ratio (%) 4.3 3.8

Revenue Deficit (-)/Surplus (+)/GDP Ratio (%) -1.6 -1.4

Overall Deficit (-)/Surplus (+) /GDP Ratio (%) -5.6 -4.9

Summary of the Budget: 2014-2015 (Percentage of GDP)

2013 2014 (Revised) 2015 Budget

Revenue 13.9 14.2 14.9

Tax Revenue 11.6 11.8 12.5

Income Tax 2.4 2.7 2.8

VAT 2.9 2.9 3.1

Excise Tax 2.9 2.5 2.6

Tax on External Trade 2.6 2.8 2.9

Other 0.8 0.9 1.0

Non Tax Revenue 1.5 1.5 1.5

PC Tax Sharing & Devolved Revenue 0.6 0.6 0.6

Grants 0.2 0.3 0.3

Expenditure 19.8 19.4 19.3

Recurrent Expenditure 14.5 13.8 12.9

Salaries and Wages 4.5 4.5 4.3

Interest Payments 5.1 4.4 3.8

Subsidies and Transfers 3.1 3.0 3.0

Other Goods and Services 1.1 1.3 1.3

Expenses from PC Revenue 0.6 0.6 0.6

Public Investment 5.5 5.7 6.5

o/w Highways 1.8 1.8 2.0

Education 0.3 0.5 0.5

Health 0.2 0.4 0.5

Irrigation 0.3 0.5 0.5

Transport 0.3 0.4 0.5

Rural Sector 0.7 0.8 0.9

Revenue Deficit (-) / Surplus (+) (0.8) - 1.7

Budget Deficit (5.9) (5.2) (4.4)

Government Debt (% of GDP) 78.3 75.0 71.0

Summary of the Budget: 2014-20152013 2014 2015 Budget

Total Revenue & Grants 1,204 1,422 1,689

Total Revenue 1,188 1,394 1,654

Tax Revenue 1,006 1,189 1,416

Income Tax 206 258 322

Taxes on Goods & Services 572 672 774

Taxes on External Trade 228 260 321

Non-Tax Revenue 132 149 174

PC Tax Sharing and Devolved Rev 51 56 64

Grants 16 28 35

Total Expenditure 1,720 1,922 2,210

Recurrent 1,256 1,386 1,525

Salaries & Wages including PCs 432 478 558

Other Goods & Services incl. PCs 108 152 163

Interest 446 443 425

Subsidies & Transfers 270 313 379

Public Investment 481 553 696

Education and Health 56 78 120

Infrastructure 425 475 576

Other -17 -17 -11

Revenue Surplus(+)/Deficit (-) -68 8 129

Primary Surplus (+)/Deficit(-) -70 -57 -96

Budget Surplus (+)/deficit(-) -516 -500 -521

Total Financing 516 500 521

Total Foreign Financing 80 260 251

Foreign Borrowings-Gross 179 370 453

Foreign borrowings 179 173 258

Foreign Commercial - 197 195

Debt Repayments -99 -110 -202

Total Domestic Financing 436 240 270

Non-Bank Financing 83 120 160

Foreign Inv. in T-Bills & T-Bonds 56 39 40

Bank borrowings 297 81 70

FC Research

5

Budget Review - 2015

2.0 BUDGET & THE STOCK MARKET 2.1 Capital Market Developments

No Development Proposals

2.2 Budget 2014 & Listed Securities

Budgetary Move Counters Affected Impact

Extend the 2% NBT applicable to the banking sector to all

banks and financial institutions.

BFI Sector NBT is a broad based turnover tax which is likely

to have a negative impact on the bottom line of

the counters in the BFI sectors.

12% annual interest rate for deposits of pensioners and

elders, who maintain their deposits in State Banks and

commercial banks will exempt the statutory reserve

requirement on individual deposits maintained by the

elderly people. Further, Central Bank has also permitted

Finance Companies to pay 11% interest on such deposits.

BFI Sector This would have an impact on competitiveness

of private commercial banks due to shifting

deposits from private banks to state banks.

However this would depend on the amount by

which they are going to increase and/or

pensioners FDs.

The present withholding tax regime applicable to

individuals and charitable institutions will be revised by

introducing a single withholding tax rate of 2.5%

irrespective of the amount of interest.

BFI Sector This would promote savings of the country due

to standardization of WHT.

Increase deposit insurance by 50% to provide greater

security to deposit holders of the banks.

Banking Sector Banks will have a minor hit on their bottomlines

Profits and income arising or accruing to any Unit Trust

from investments made on or after January 1, 2015, in US

Dollar deposits or US Dollar denominated securities

listed in any foreign Stock Exchange will be exempted

from tax.

BFI Sector and Investment

Management Companies

This is likely to promote foreign investment

flows to the country due to lower tax regime.

Electricity tariff reduction of 15% for all other industries

from November 2014.

Manufacturing, Hotel and F&B

Sectors

Margin enhancement due to lowering cost will

reflect on future performance.

Provide lands on long term leases to set up 300 factories

in every divisional secretary area in the background of

improved prospects for export and import competing

industries. Provisions will be made to permit lump sum

depreciation for the importation of plant and machinery

in addition to exempting them from dividend tax and

providing a half tax holiday for a period of 3 years.

Manufacturing Sector Incentives to expand export-import based

businesses further due to tax and other

concessions.

Investors undertaking new investments in excess of LKR

500 mn will be given a 7 year half tax holiday provided

such investments are registered with the Inland Revenue

Department before end of 2015.

Manufacturing Sector Incentives to start large scale projects.

Revised Customs tariffs effective from today will

facilitate a further expansion of value creating, import

competing industries. Quality standards will be enforced

on imports and exports to promote competitive

industries. An anti-dumping legislation will be placed

before Parliament shortly to ensure fair practices in

external trade.

Manufacturing Sector, Trading

Sector

This will safeguard domestic manufacturers

against low cost imported substitutes. Trading

companies that import may face tighter

regulation.

FC Research

6

Budget Review - 2015

Budgetary Move Counters Affected Impact

Sri Lankan expats to be granted dual citizenship or 5 year

work visas and the facility to import a vehicle worth 60%

of the total annual foreign revenue they bring into the

country, inclusive of tax concessions.

Motor Sector Demand enhancement due to lower tax regime

Taxes on all electric cars will be reduced to 25%. Motor Sector Boost in demand

Impose Excise Special Provision tax on motor vehicle

imports tax in lieu of all multiple taxes at the point of

import.

Motor sector This may boost demand for motor vehicles

Several expressways to be completed by 2017 including

Ruwanpura highway and Northern highways.

Construction Sector and Cement

Manufacturers

Local contacters may get direct or indirect

opportunities to contribute to these projects by

catering their services and suppling raw

materials.

500 small buses to be imported. Lanka Ashok Leyland PLC Boost the topline and bottom-line of the

company.

Cess tax on rubber imports to be increased by LKR 10/Kg. Rubber Related Manufacturing

Sector

Local tire manufactures are likely to benenifit

from the cess.

Price of yoghurt and milk powder by local manufacturers

to be dropped by LKR 3 and LKR 100 respectively.

Lucky Lanka Milk Processing

Company Limited

Lanka Milk Foods PLC

NP margins may decline further

Reduce the duty on importation of gold by exporters

using their foreign currency accounts for the purpose of

exports to 3.5% by way of a 50% duty waiver, to

encourage jewellery exports and reduce the service fee

imposed by the Gem and Jewellery Authority to 0.25% of

FOB value of exports.

Blue Diamonds Jewellery

Worldwide PLC

Possible margin expansion due to lowering of

tariff and incentives for exports.

Entrepreneurs who started industries in Sri Lanka even

before the opening of the economy in 1977 give a 10%

discount on taxes payable.

All Sectors Positive Impact for the relevant business

Introduce a credit scheme at 6% interest to encourage

investments in new buses by private bus owners who

have operated for at least for 5 years.

BFI and Motor Sectors This may likely to improve demand for leases

on buses from banks and finance companies.

In order to assist SME suppliers, super market's margins

should not be more than 25% of the maximum retail

price marked on domestically supplied products and ask

to reduce prices of all essential goods by at least 10% in

view of the reduction in VAT by 1%, electricity by 15% to

25% and lending rates of banks by significant margins.

Retail and Diversified Sector There will be a hit on supermarket's

profitability due to lower margins.

Raise the minimum wage of the private sector

employees to Rs. 10,000 per month from January 2015

and to increase all minimum wages above that threshold

at least by Rs. 500 per month and increase the employer

contribution to EPF by 2% to 14%.

All Sectors All counters will have a 2% increase in

personnel cost due to EPF adjustment.

The interest or discount accruing or arising to any person

from any investment made on or after January 1, 2015 in

any Corporate Debt Security, issued by the Urban

Development Authority will be exempted from tax.

Investment Management

Companies

This will help gain access to alternative

investment opportunities.

The present rate of VAT of 12% will be reduced to 11%. All Sectors This will bring benefit across all sectors.

Tax rate applicable for gross collection betting and

gaming will be revised to 10%.

JKH (Proposed Integrated Resort

Development Project)

An entry fee of US$ 100 will be charged per person who

enters casino entertainment.

JKH (Proposed Integrated Resort

Development Project)

May reduce demand from low income segment

Implement a pension scheme for employees in the

apparel industry.

Apparel Sector - TJL, MGT This is likely to increase cost of Apparel

companies although it may reduce labour

turnover.

Enforce the payment of 7.5 percent or 15 percent tax and

other provisions contained in the Act for foreigners who

have access to state and private land through long lease

arrangements.

For companies with a large

foreign stake

This would likely to escalate cost for companies

with larger foreign stakes.

FC Research

7

Budget Review - 2015

Budgetary Move Counters Affected Impact

Credit scheme with an 8-year maturity at 6 percent

interest to all well performing companies that will

commit, on an agreed area for planting and replanting,

for social development of plantation workers and to

increase the volume of value added tea exports. This

facility will not be extended to plantation companies,

which have not paid due lease rental value to the

Government.

Tea Plantation Companies Enhancement of GP margins due to higher value

addition to the final products.

Increase new and replanting subsidy for coconut from

LKR 7,000 to LKR 10,000 per acre and the subsidy for the

rehabilitation of coconut land from LKR 15,000 to LKR

20,000 per acre. Proposal to increase Kapruka investment

loan up to LKR 3 million to cover soil improvement and

water retention in coconut lands. I propose to increase

the planting subsidy for minor export crops by 25 percent

and accordingly increase the allocation by Rs. 250 million

to the Department of Agricultural Exports. It is proposed

to increase the subsidy granted for the cultivation of

fruits and vegetables as well as operating dairy farms by

50 percent.

Agri Exporters This may improve coconut supply of the country

and in turn, this will help lower the coconut

price

Continue the LKR 5,000 per acre grant assistance to

support land preparation towards water retention, soil

conservation, the use of organic fertilizer for smallholder

tea cultivation to increase production. The subsidized

price of LKR 1,250 per 50/kg bag will also be continued for

all these crops. The prevailing high taxes on edible oil,

coconut oil and palm oil at the point of customs will be

maintained in the long-term interest of coconut

plantation.

Tea Plantation Companies and

Coconut estates

Cost maintenance

Provision of maize at a subsidized price of LKR 40 per kg

to small poultry farms and provide export incentives for

chicken and eggs.

Poultry Sector This is likely to improve margins in companies

operating in the poultry industry since maize is

their main input of production.

No.1, Lake Crescent,

Colombo 2

Sales Desk: +94 11 2145 000

Fax: +94 11 2145 050

HEAD OFFICE BRANCHES

No.1, Lake Crescent, Matara Negombo

Colombo 2 No. 24, Mezzanine Floor, No.72A, 2/1,

Sales Desk: +94 11 2145 000 E.H. Cooray Building, Old Chilaw Road,

Fax: +94 11 2145 050 Anagarika Dharmapala Mw, Negombo

Matara

Tel: +94 41 2237 636 Tel: +94 31 2233 299

SALES BRANCHES

CEO Jaliya Wijeratne +94 71 5329 602 Negombo

Priyanka Anuruddha +94 76 6910 035

Priyantha Wijesiri +94 76 6910 036

Colombo

Nishantha Mudalige +94 76 6910 041 Matara

Anushka Buddhika +94 77 9553 613 Sumeda Jayawardana +94 76 6910 038

Gamini Hettiarachchi +94 76 6910 039

Thushara Abeyratne +94 76 6910 037

Nishani Prasangi +94 76 6910 033

Ishanka Wickramanayaka +94 77 7611 200

RESEARCH

Dimantha Mathew +94 11 2145 016

Reshan Wediwardana +94 11 2145 017

Nandika Fonseka +94 11 2145 018

FIRST CAPITAL GROUP

HEAD OFFICE BRANCHES

No. 2, Deal Place, Matara Kurunegala Kandy

Colombo 3 No. 24, Mezzanine Floor, No. 6, 1st Floor, No.213-215,

Tel: +94 11 2576 878 E.H. Cooray Building, Union Assurance Building, Peradeniya Road,

Anagarika Dharmapala Mawatha, Rajapihilla Mawatha, Kandy

Matara Kurunegala

Tel: +94 41 2222 988 Tel: +94 37 2222 930 Tel: +94 81 2236 010

Disclaimer:

This Review is prepared and issued by First Capital Equities (Pvt) Ltd. based on information in the public domain, internally developed and other sources, believed to be

correct. Although all reasonable care has been taken to ensure the contents of the Review are accurate, First Capital Equities (Pvt) Ltd and/or its Directors,

employees, are not responsible for the correctness, usefulness, reliability of same. First Capital Equities (Pvt) Ltd may act as a Broker in the investments which are the

subject of this document or related investments and may have acted on or used the information contained in this document, or the research or analysis on which it is

based, before its publication. First Capital Equities (Pvt) Ltd and/or its principal, their respective Directors, or Employees may also have a position or be otherwise interested

in the investments referred to in this document. This is not an offer to sell or buy the investments referred to in this document. This Review may contain data which are

inaccurate and unreliable. You hereby waive irrevocably any rights or remedies in law or equity you have or may have against First Capital Equities (Pvt) Ltd with respect to

the Review and agree to indemnify and hold First Capital Equities (Pvt) Ltd and/or its principal, their respective directors and employees harmless to the fullest extent

allowed by law regarding all matters related to your use of this Review. No part of this document may be reproduced, distributed or published in whole or in part by any

means to any other person for any purpose without prior permission.

First Capital Equities (Pvt) Ltd