Embed Size (px)

Citation preview

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 1/20

Foreign Currency Convertible Bond

FCCB

ITM ( Capital Market )

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 2/20

Convertible Bond

It is a typ e o f bond that the hol der can con vert in to sharesof com mon stock in the is suing comp any or cas h of equa lvalue, at an ag ree d-u pon pr ice. I t is a hyb ri d secu rit y withdebt- and equ ity-l ik e f ea tu res .

• Low coup on ra te, the in stru ment carri es ad di tio nal valueth rou gh the op tion to con vert th e bond to stock, and th ereb ypartici pate i n fu rth er grow th in th e comp any's equity val ue.

• From th e issuer's perspectiv e, th e k ey benefit of rais ingmon ey by sell ing conv ertib le bon ds is a r educed cas hinteres t pay me nt.

• Benefit of redu ce d interes t payments , th e value ofsharehol der's eq ui ty i s redu ce d due to the stock dilu tionex pect ed when bo nd ho ld ers conv ert th eir bond s i nt o n ewshares.

ITM ( Capital Market )

Key Benefits

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 3/20

ABC of FCCB• Al so referred as FCCN Foreig n Cur re ncy Con verti ble Note s

• Foreig n Cur re ncy Con verti ble Bon ds (FCCB ) are d ebtinstrum ents is sued in a cur re ncy dif ferent than the issuer’sdomes ti c cu rrency with an op tion to con vert th em incommon shares of th e i ssuer com pany .

• It’s a qu as i debt ins trum ent t o r aise foreig n curren cy fu nd sat attractiv e r ate.

• Acts lik e a bond by maki ng reg ul ar cou pon and pri nci palpaymen ts and al so gi ves th e bon dh ol der an op tion to con vertth e bond into stock .

• Inv es tors rece ive the safety of guarantee d payments on thebon d and are also ab le to tak e adv antag e of an y larg epri ce app reciatio n in th e comp any's stock

ITM ( Capital Market )

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 4/20

Guide line s

• Company can issue FCCB only upto value of USD 500 million in asingle year. However issue of FCCBs exceeding USD 500 mn subjectto approval of RBI.

• Should be listed on BSE and NSE and minimum net worth during the

previous three years should not be less than 500 crore

• Minimum average maturity shall be 3 years for borrowing upto US$20 million and 5 years in case it exceeds US $20 million.

• Cab be raised through two route Automatic and RBI approval Theautomatic route is available to real sector i.e. Industrial sector,specially infrastructure sector-in India, while all other sectors have totake RBI approval

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 5/20

????How Different

Equ ity

• Immed iate Eq ui tydilution

• Div idend Distri bu tion

ITM ( Capital Market )

Debt

• High interest rates in borrowings• High coupon in bonds

• ECB limited to capital goods, overseasacquisitions, Capacity augmentation

FCCB

1.Low coupon interes t com pa re to debt2. No immedi ate di lu tion of equ ity

3. No ca sh pa ym ent in good ma rk et con di tion4. All tr ansact ion s in forei gn curren cy

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 6/20

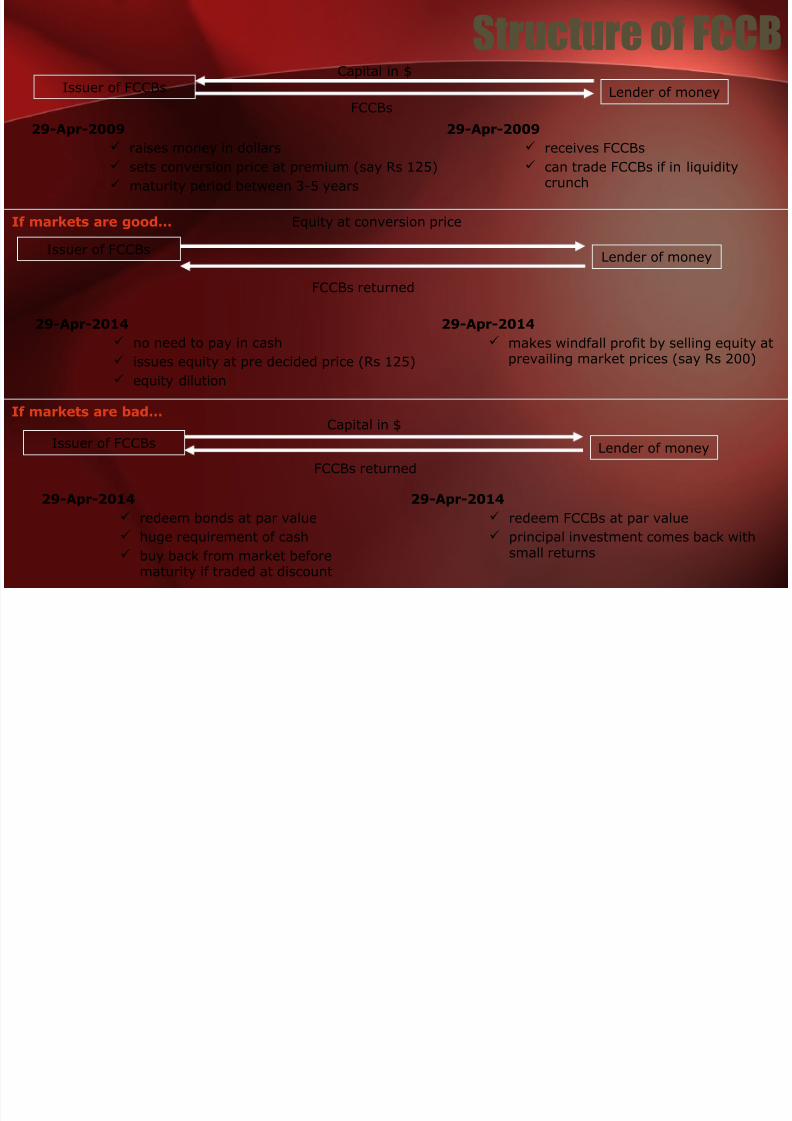

Structure of FCCBIssuer of FCCBs Lender of money

Capital in $

FCCBs

29-Apr-2009

raises money in dollars

sets conversion price at premium (say Rs 125)

maturity period between 3-5 years

29-Apr-2009

receives FCCBs

can trade FCCBs if in liquiditycrunch

If markets are good…

Issuer of FCCBsLender of money

Equity at conversion price

FCCBs returned

29-Apr-2014

no need to pay in cash

issues equity at pre decided price (Rs 125)

equity dilution

29-Apr-2014

makes windfall profit by selling equity atprevailing market prices (say Rs 200)

Issuer of FCCBs Lender of money

Capital in $

FCCBs returned

29-Apr-2014

redeem bonds at par value

huge requirement of cash

buy back from market beforematurity if traded at discount

29-Apr-2014

redeem FCCBs at par value

principal investment comes back with

small returns

If markets are bad…

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 7/20

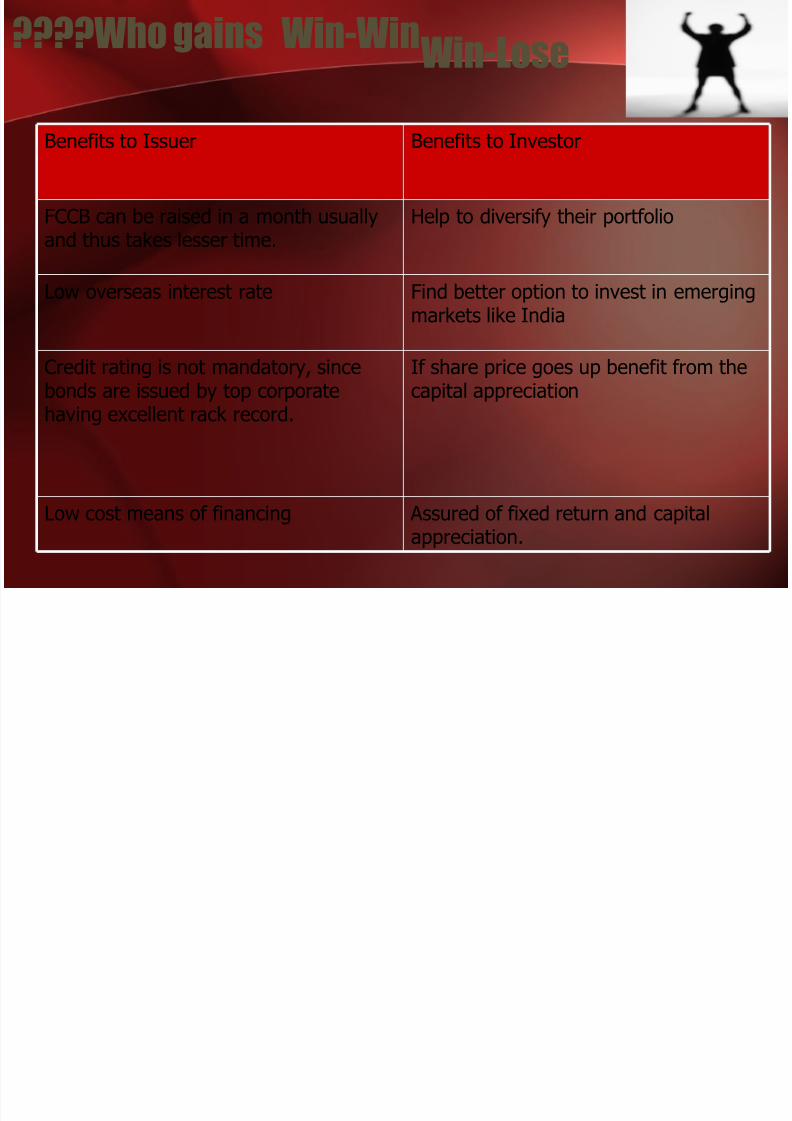

????Who gains Win-WinWin-Lose

Assured of fixed return and capitalappreciation.

Low cost means of financing

If share price goes up benefit from thecapital appreciation

Credit rating is not mandatory, sincebonds are issued by top corporate

having excellent rack record.

Find better option to invest in emergingmarkets like India

Low overseas interest rate

Help to diversify their portfolioFCCB can be raised in a month usuallyand thus takes lesser time.

Benefits to InvestorBenefits to Issuer

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 8/20

????WHY FCCB

•FCCB become a pop ul ar tool for rai sing fu nds f rom ov erse asmark et .

•Hig h rid ing in th e mark et res ili ence seen in th e second arymark ets .

•The tota l amo un t r aised f rom FCCB s dur in g th e las t t hreeyears sta rtin g 2006 on ward s amoun te d to $15bn .

• Comp ani es went in for the FCCB ro ute to fun d theirex pans ion /ac quisiti on p lans.

•Sim pl y bec au se shorter lead ti mes associate d with th eproce ss as we ll as fo r the fact th at comp ani es gain edex pos ure in to a gl ob al inv estor bas e.

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 9/20

Wockhardt’s Big Plans

• Board meeting of Q2, 2004 - Wockhardt launched its maiden FCCB issueof US $ 100 Mn with a Greenshoe option of US $10 Mn

• 5 year, zero coupon bond with a 50 per cent premium

Purpose:• To expand reach in Europe through the inorganic route –acquired two

companies in Europe and established its own sales and marketingorganization in the US

• Setup of a SEZ in the Shendra Industrial Park near Aurangabad,Maharashtra, which will house the company’s R&D and manufacturingfacilities

• Targeted a big-ticket acquisition in end 2006 - early bidder for betapharm, a generic drug firm in Germany which was later acquired byDr Reddy’s Laboratories Limited

• Acquired 3 major companies for $453 million in the last 30 months(Ireland based Pinewood Laboratories for $150 million, NegmaLaboratories of France for $265 million and Morton GrovePharmaceuticals of US for $38 million)`

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 10/20

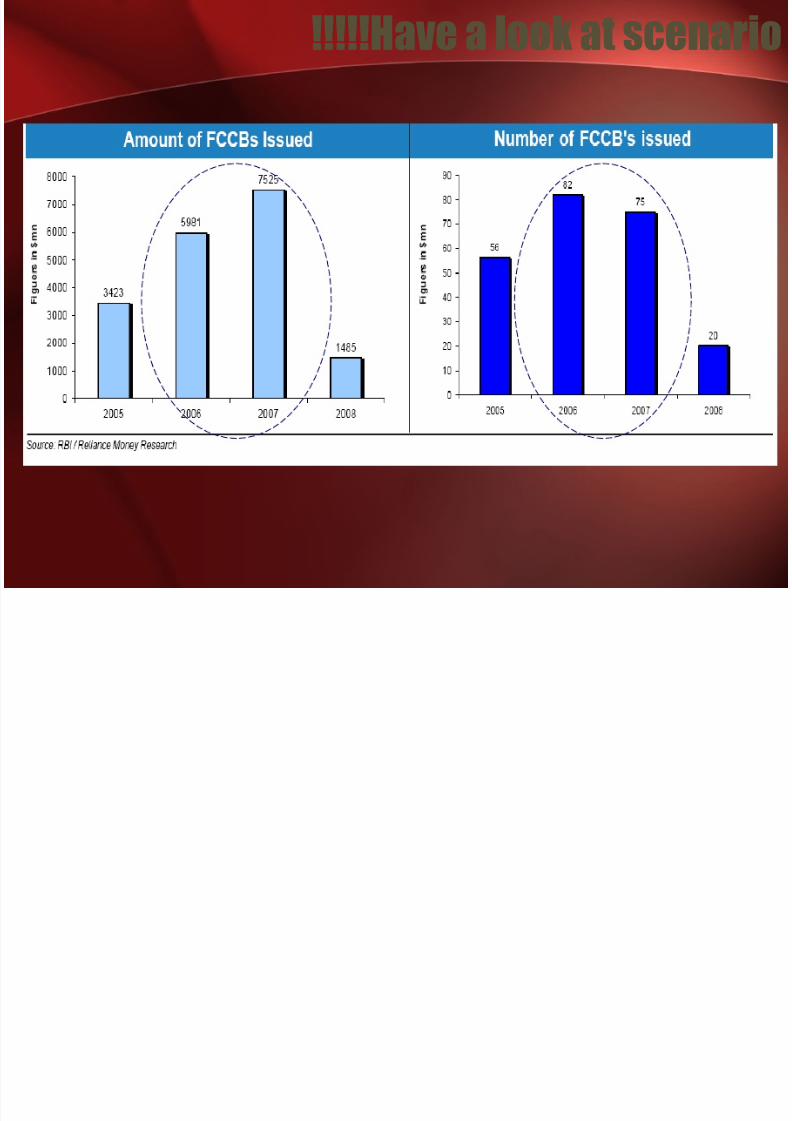

!!!!!Have a look at scenario

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 11/20

BIG B’s Of FCCB

598.95961450 USDJun, 2012Tata Motors

268.80231150 USDJan, 2010Tata Chemicals

306.60476500 USDMay,2011

Reliance

Communication

360.10716440 USDMar,2011Ranbaxy

174.35486110 USDSept,2009Wockhardt

91.4054675 USDJun, 2012Moser Baer

181.15465120 USDFeb, 2011Bajaj Hindusthan

677.051014150 USDMay,2011Aurbindo Pharma

Share price

as on

Sept 18,2009

Conversio

n

price at

maturity

(Rs)

Issue Size

(Mn)

Maturity

PeriodCompany

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 12/20

????? What to do ?????

I n tod ay’s f i nanci al do wn tu rn …

• Con vers ion p ri ce of FCCBs h as gone severa l tim es hig herth an their curren t mark et p ri ce .

• pri ce s of In dian shares have fall en sharp ly com pared to th econv ers ion pri ce of th e b on ds in to equi ty .

• Inv es tors disin te res ted i n con verti ng th eir bond s intoequ ity as they do no t see o pp ortu ni ty to con vert such bond sinto eq ui ties .

• Rupee at l ow , hig h IN R pay me nt awa iti ng • Reset the conv ersion clause , to br in g it clos er to rea lity -

Potenti al dil uti on of share hol din gs

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 13/20

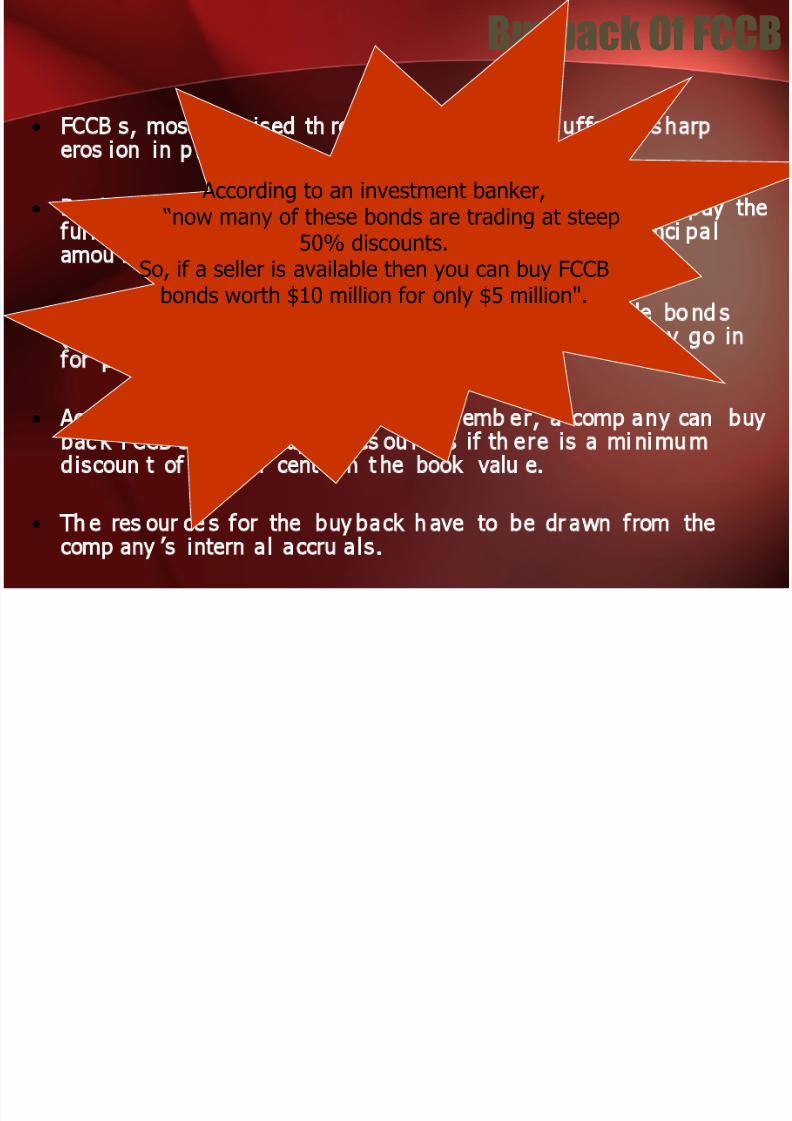

Buyback Of FCCB

• FCCB s, most ly r aised th rou gh bond s, have s uffered s harperos ion in p ri ce s.

• Buybac k is a chea per op tion as promoters wil l have to pay theful l coupon (i nte res t rate on the face value) an d pri nci palamou nt if th ey wait for the bonds to mat ure.

• Prom oters or i ssuers of foreig n cu rrency con verti ble bo nd s(FCCB s) may be al low ed to bu y b ac k the bond s if th ey go infor pre paym ent.

• Accord ing to RBI ann ou nced in D ec emb er, a comp any can buybac k FCCB s out of r up ee res ou rce s if th ere is a mi ni mu mdiscoun t of 25 per cent on t he book valu e.

• Th e res our ce s for the buyback h ave to be dr awn from the

comp any ’s intern al accru als.

According to an investment banker, “now many of these bonds are trading at steep

50% discounts.

So, if a seller is available then you can buy FCCBbonds worth $10 million for only $5 million".

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 14/20

• Th e RBI permi tted Indian comp anies to buy back FCC Bs upto max imu m $50 mil lion to 100 mil li on u nd er th e app rov alroute, if i t is d on e at a mi ni mu m dis cou nt of 25% on thebook v alu e.

• Ma ndated t hat t he fu nd s used for the buy back woul d h ave

to be ou t of ex isti ng fo reign cu rre ncy funds held ei ther inIndia.

• It coul d also be ou t of fres h ECB , rais ed i n con fo rmity withprev alent ECB norm s.

• Th e FCCB s bought bac k or repu rch ased fro m the h ol ders

mu st be cancell ed and shoul d n ot be re-iss ued or re- sold .• Th e buy back shou ld not have any eff ec t on the bond hol dersnot op ting for the buy back or o n the no n-p artici pati ng bondhold ers of comp an ies opti ng for th e buy back .

• Prep ayment of FC CB is perm itted upto US $200 Mi lli onsubject to comp li ance of min imum averag e matur ity

perio d.For hig her prep ayment amoun t, RBI ap prov al i sneeded.

Guide line s

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 15/20

What spee ds up Mah in dr a &

Mah indr a F CC B bu yback • M&M had comp leted a $ 200 mil l ion F CCB i ss ue i n 2006 invest ors from Euro pe

and Asi a.

• Wi th ma turit y of 5 -y ea r p lus one d ay.

• Fac e val ue of $ 100,000 per bond , and an ini tial co nversi on pri ce of Rs 9 22.04

per sha re.

• M&M exp ect ed bond-hol ders to conv ert these bonds int o e quit y. But wit h t hedownt urn in the g lob al equit y mark et, these b ond s are no w pri ced muc hhi gher than t he company 's stock price.

• If not co nvert ed , woul d have t o rep ay the deb t a t t he t ime of mat uri ty, whic hwo ul d increase the financi al burd en of the cash-st rap ped fi rm s.

• M&M has re purchased 65 zero coup on FC CBs due 2011 ,a gg re gat ing to $6 .5million

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 16/20

• Indian comp anies now faci ng some hars h re al ity . As mos tof the bo nd s are up for redemp ti on in th e next year whi chcou ld hav e a n eg ati ve im pact o n the ca pita l stru ct ure ofth ese comp ani es.

• A basket of aroun d 1 56 comp ani es which h ad is sued FCCB sbetw ee n 2006 to 2008 are lik ely to tak e adv antag e of t hi smeas ure ann oun ce d by th e RBI .

• Larg e ru pee d ep re ci ation and th e s harp stoc k price fall swhi ch have crea ted larg e los ses on both FCC Bs and ECBs .

• For rep ayin g thes e FCCBs lik ely to in vol ve fre sh debt fu ndsat hi gher rate s whi ch coul d fu rth er p ut strain o n the ca shflo ws goin g ah ead .

ITM ( Capital Market )

A sob story today….

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 17/20

FC CB

A T ICKI N G T IM E BO MB

(Exp lode i f fa il to pa y)

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 18/20

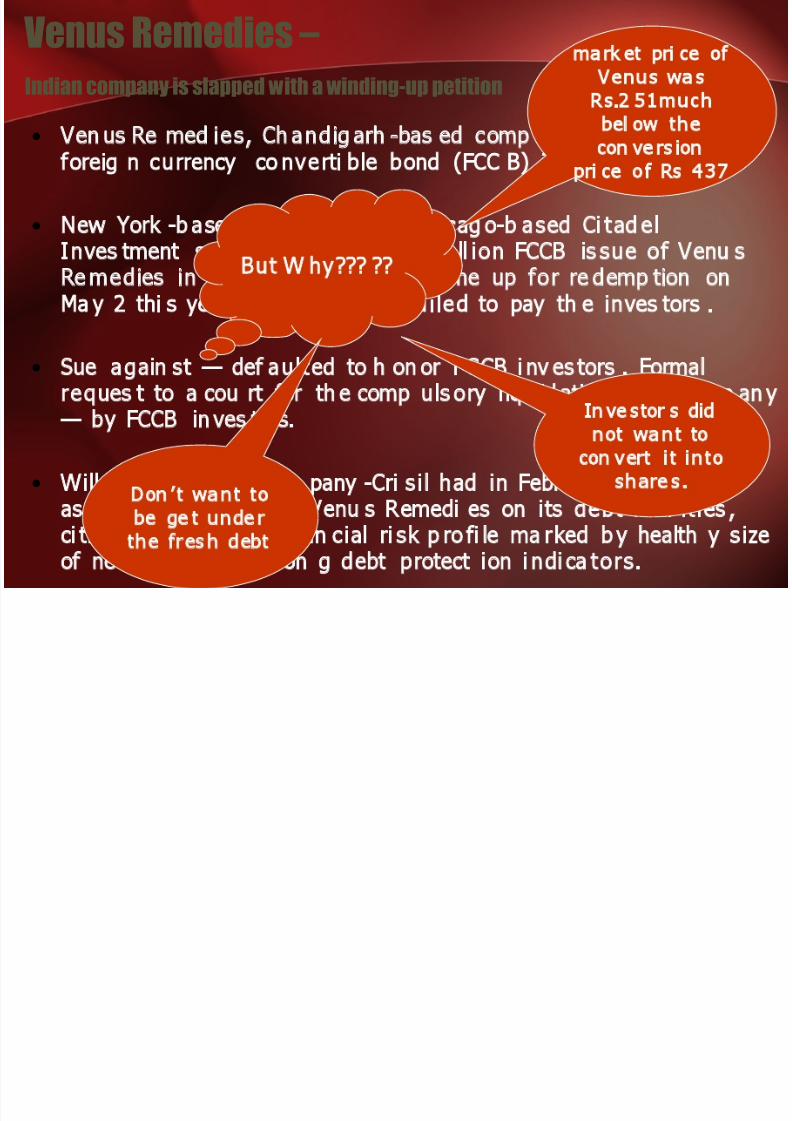

Venus Remedies –

Indian company is slapped with a winding-up petition

• Ven us Re med ies, Ch andig arh -bas ed comp an y defaul te d on aforeig n currency co nverti ble bond (FCC B) issue.

• New York -b ase d DE Sh aw an d C hi cag o-b ased Ci tad elInves tment sub scri bed to a $12-mi ll ion FCCB is sue of Venu s

Re medies in May 2006 whi ch is ca me up for re demp tion onMa y 2 thi s yea r, b ut co mpan y failed to pay th e inves tors .

• Sue again st — def aulted to h on or FCCB i nv es tors . Formalreques t to a cou rt for th e comp uls ory liq uid ation of a comp an y

— by FCCB in ves tors.

• Will ful def aul t b y com pany -Cri sil had in Febr uary 2009as signed A -rati ng to Venu s Remedi es on its debt facil ities ,ci tin g comf ortab le fi nan cial ri sk p ro fi le marked b y health y size

of net worth and stron g debt protect ion i ndi ca tors .

But W hy??? ??

ma rk et pri ce ofVenus was

Rs.2 51muchbel ow the

con ve rs ionpri ce of Rs 437

In ve stor s didnot want tocon vert it into

shares.Don’t want tobe get under

the fresh debt

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 19/20

Another way Out……. CREDIT- LINKED NOTES

• CLN is a credit derivative linked to foreign currency convertible

bonds (FCCBs).

• Protection from Credit Risk.

• Indian bank overseas wings bank buys CLN.

• No Default by FCCB issuer the bank makes money on this.

• Syndicating foreign banks exit after offloading the CLN in the

secondary market.

• Lapped up by Indian banks as they earn a coupon of 50-60 basispoint.

8/14/2019 Fccb Group 1

http://slidepdf.com/reader/full/fccb-group-1 20/20

Thank You