Embed Size (px)

Citation preview

Feasibility Study for the

Replacement of Waterworld

20 January 2015

Version Control 2

Version No Date Comments Author Reviewed by Issued to

1 20/01/2015 Final report for client review Tom Pinnington Simon Molden Lawrence Istead

Disclaimer

This document and its contents have been prepared and are intended solely for the client’s information and use on the Feasibility Study for the

Replacement of Waterworld only. Atkins, The Sports Consultancy and AFLS&P assume no responsibility to any other party in respect of or arising out of

or in connection with this document and/or its contents

It is not possible for Atkins and The Sports Consultancy to guarantee the fulfilment of any estimates or forecasts contained within this report, although

they have been conscientiously prepared on the basis of our research and information made available to us at the time of the study.

Neither Atkins, The Sports Consultancy or AFLS&P nor the authors will be held liable to any party for any direct or indirect losses, financial or otherwise,

associated with any contents of this report. We have relied in a number of areas on information provided by the client, and have not undertaken

additional independent verification of this information. Where applicable, assumptions have been agreed with the client’s representatives and have been

clearly stated.

Contents 3

Contents Page Number

Executive Summary 4

Introduction and Background 13

Needs Analysis 15

Site Options Appraisal 22

Facility Options 27

Capital Costs 29

Revenue Projections 32

Funding & Affordability 36

Recommended Option 44

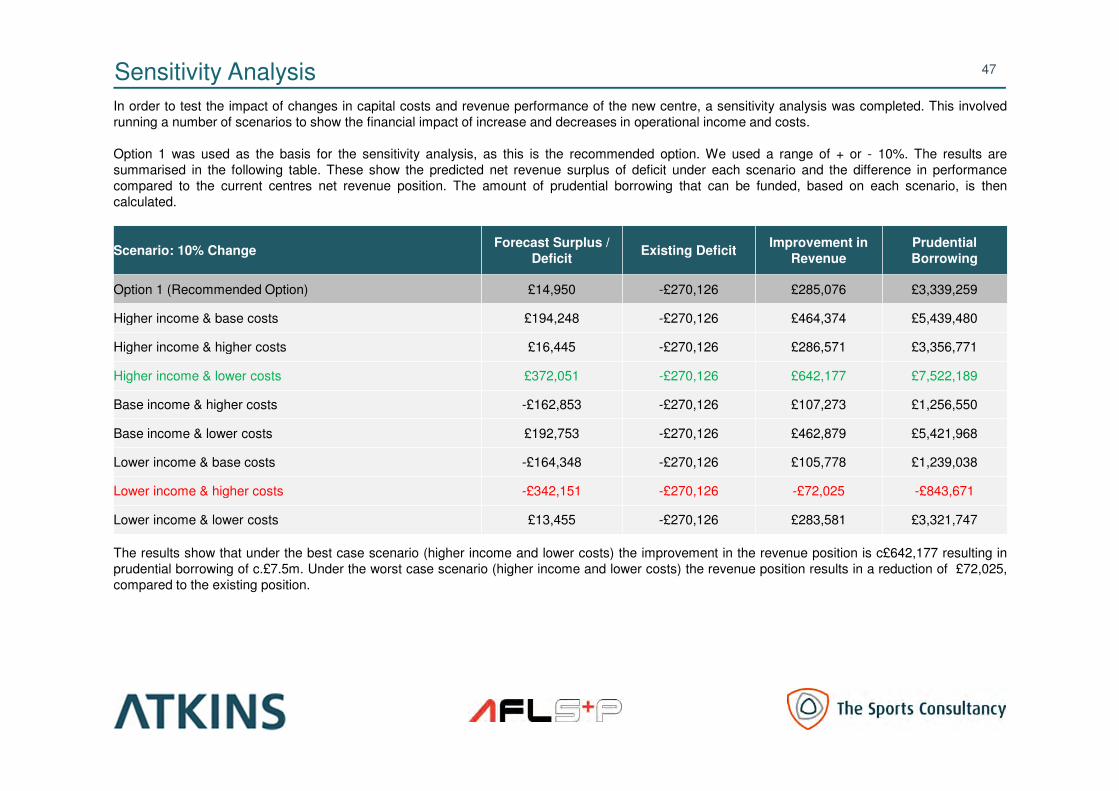

Sensitivity Analysis 46

Outline Project Programme 48

Procurement Options 50

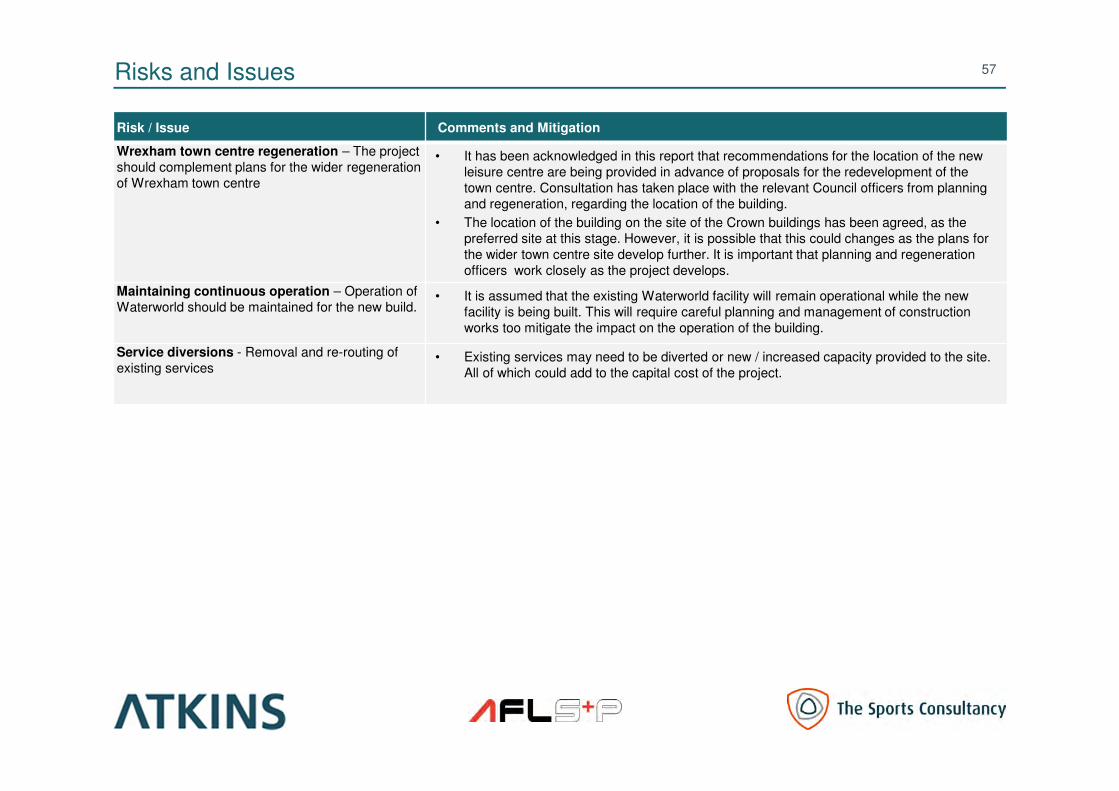

Risks and Issues 55

Conclusions and Recommendation 58

Appendices

Appendix 1 – Latent Demand Report

Appendix 2 – Initial Capital Cost Estimates

Appendix 3 – Income and Expenditure Projections

Appendix 4 – Concept Sketch Plans

Appendix 5 – Town Centre Sites

Executive Summary

4

Executive Summary

Introduction

Atkins (incorporating subsidiary Faithful & Gould), in partnership with The Sports Consultancy and AFLS+P Architects, was appointed by Wrexham

County Borough Council (the Council) in September 2014, to complete a feasibility study for a new main leisure centre, in central Wrexham. The new

centre is intended to provide a long-term replacement for Waterworld but to serve the County Borough as a whole. The outputs from the study will be

used by the Council as the basis of decisions on whether, and how best, to proceed with the development of a new leisure centre. The agreed scope of

work included the following:

• A feasibility study for a new leisure centre to serve Wrexham and the wider catchment of the County Borough, taking into consideration competing

facilities (existing and planned).

• Assessment of the capital and revenue implications of the proposed facility mix options, including variants, and identification of which is the most

financially beneficial. This assessment should be set in the context of the current financial constraints affecting the Council.

• A review of the financial impact of the sensitivity analysis (i.e. under performance or over performance).

• Above all, a recommendation as to which facility option is the most financially viable and an assessment of how the scheme could be funded

including prudential borrowing.

• Recommendation of the most cost and time effective manner to procure the delivery of the new facility.

• Recommendation of the most financially beneficial approach to financing the capital delivery of the proposed facility.

Needs Analysis

The Sports Consultancy was appointed by Wrexham County Borough Council (the Council), in May 2013, to conduct an options evaluation study to

investigate the options for the replacement of Plas Madoc Leisure and Activity Centre (Plas Madoc) and Waterworld Leisure and Activity Centre

(Waterworld). This study was completed in November 2013 and forms the basis of the brief for this feasibility study. During the options evaluation study

a range wide ranging needs analysis was completed. This resulted in the following facility mix being recommended for the replacement of Waterworld in

Wrexham town centre:

• 8 lane 25 metre pool (17m x 25m) to ASA County standard

• Spectator seating for 250 people

• Learner pool

• Leisure water area (one flume/feature)

• 120 station health and fitness; includes weights area

• Dance/fitness studios; 2 x 30 person & storage.

The options evaluation study recommended the site of the Council offices, Crown buildings, as the preferred location. This feasibility uses the results of

the previous options evaluation study and develops them further in a feasibility study.

5

Executive Summary

Re-opening of Total Fitness

The club closed in 2011, after increased rental costs and a failure to secure sufficient membership income meant the site was no longer financially

viable. It is understood that Total Fitness is investing over £1m to upgrade existing facilities. Membership fees will be slightly lower than previously, with

full adult membership at £40 per month compared to circa £45 previously. Concessionary membership fees are being advertised at £30 per month. We

understand that the previous club operated with membership of between 4,000 and 4,500 members. As the site has not yet re-opened, there is no

information available on future membership numbers. The local market has undergone some changes since 2011, with DW Fitness benefitting from

displaced members from the former Total Fitness site and the emergence of Simply Gym at the budget end of the market. However, Total Fitness clearly

sees an opportunity to attract sufficient membership numbers to justify investment and re-opening of the site.

Plas Madoc Leisure Centre

Plas Madoc Leisure Centre was transferred to a community led trust to operate in 2014 and re-opened in December 2014 under the new name Splash

Magic. It continues to operate a gym with circa 48 stations of equipment. We understand that current (January 2015) membership numbers are between

200 and 250 members. This compares with circa 700 members the centre had before it closed in April 2014. We would expect the majority of this

reduced membership to be drawn from a more local catchment than was previously the case. Full, single adult membership fees are now £26 per month,

positioning the gym towards the lower end of the market in terms of cost. Given that Splash Magic has been operating for only two months at the time of

writing this report it is not clear whether it will be financially viable and sustainable in the long-term.

Impact of the re-opening of Total Fitness on the Business Case for Waterworld

It is recognised that the impact of the re-opening of Total Fitness and Splash Magic pose a risk to the business case for a replacement of Waterworld.

Previously, both facilities were not financially viable and were closed. It is not possible to provide a definitive view on whether these sites, or indeed

others such as Simply Gym or DW Fitness, will be viable in the future. However, this study does take account of the impact of both facilities on the

business case for Waterworld. The principal risk relates to the impact on membership projections for Waterworld, from increased competition. Revenue

generated from health and fitness membership is the foundation of the business case. Therefore, any reduction to this will have a detrimental effect on

the net revenue position and on the affordability of the project. In order to provide as much clarity as possible of the impact of the re-opening of these

facilities updated health and fitness membership forecasts were commissioned from The Leisure Database Company. They made a number of

reasonable assumptions based on information available on the two facilities and adjusted their previous predictions in light of the findings.

The results of the revised membership projections for Waterworld show that future membership projections would be reduced from c.3,100 (assuming

Splash Magic and Total Fitness were closed) to 2,565 (assuming they re-open and remain operational). We believe that this represents a realistic

assessment of the likely membership numbers that could be achieved by a good operator at Waterworld and we have used the reduced membership

projection as the basis for all business planning work. However, it should be noted that there will inevitably be other changes in the local market over

time as other providers enter and exit the market. Therefore, these projections can only provide a snapshot based on what is currently known. Longer

term, other risks and opportunities will inevitably arise.

6

Executive Summary

The Options

The needs analysis work, completed during the previous study, informed the development of four facility options. These were developed to understand

the likely capital, revenue and funding implications of a range of options that meet the current and future needs of the catchment population, to a lesser

or greater extent. A summary of the options is contained in the following. A cross indicates facilities that are included in each option.

* The term leisure water refers to a separate shallow beached pool area, similar to the sloping pool at Plas Madoc. Alternatively this area could also be

utilised for toddler splash/confidence water area. The cost of including a single flume has also been allowed for in leisure water options.

50 metre Competition Pool Option

The option of a 50 metre pool was discounted during the previous Options Evaluation Study, as the results of supply and demand modelling work

commissioned by Sport Wales did not support that level of provision. The proposed 8 Lane 25m pool will result in a shortfall of provision across the

County Borough equivalent to 4 x 25m lanes, which is only half of what would be required to increase provision to an 8 lane 50m competition pool.

The results of the supply and demand modelling suggest that if an 8 lane 50m pool was provided this is likely to be under utilised. However, consultation

with Swim Wales suggests that this would provide a valuable facility for swimming clubs in North Wales. In financial terms, the provision of an 8-lane

50m pool have a negative impact on the net revenue position and is likely to add circa £3m to the capital cost of the project. The reduced revenue

position and increased capital cost would make the project significantly leas affordable. Therefore, the 50m pool option was discounted on the grounds

of insufficient need and the negative impact on financial viability.

7

Option 1 Option 2 Option 3 Option 4

Activity Areas8 Lane Pool - No

Leisure Water

8 Lane Pool - With

Leisure Water

6 Lane Pool - No

Leisure Water

6 Lane Pool - With

Leisure Water

6 Lane 25m pool (full disabled access) X X

8 lane 25 metre pool (17m x 25m) to ASA County

standard (full disabled access)X X

Spectator seating for 240 people X X X X

Learner pool with moveable floor (full disabled access) X X X X

120 station health and fitness; includes weights area X X X X

Dance/fitness studios; 2 x 30 person & storage X X X X

Leisure water area (one flume/feature)* X X

Executive Summary

Site Options Appraisal

Council officers provided a number of possible locations to ensure that the potential sites considered are as accessible as possible for the largest number

of pool users. The sites that were appraised are listed below and described in the following paragraphs:

• Site 1 - Western Gateway

• Site 2 – Total Fitness

• Site 3 - Memorial Hall

• Site 4 – Waterworld

• Site 5 – Former Wrexham Town Centre Police Station

• Site 6 - Crown Buildings (currently Council offices).

The review of the sites concluded that the Crown Buildings site remained the preferred location for development of the new leisure centre. The principal

benefits of the Crown Buildings site are:

• It is in central location in Wrexham town, close to the existing leisure centre.

• There is adequate site available to accommodate the new development, with the existing car park on the adjacent site and possibly on some of the

Waterworld site, if required.

• It is currently in Council ownership with good accessibility.

• Development of this site could be completed while the existing pool continues to operate.

• Use of the Crown buildings could also enable the existing Waterworld site to be disposed of to generate a capital receipt to contribute towards the new

centre. This is important in terms of the affordability of the development.

• The exact location of the new centre will be defined following development of the town centre master planning.

8

Executive Summary

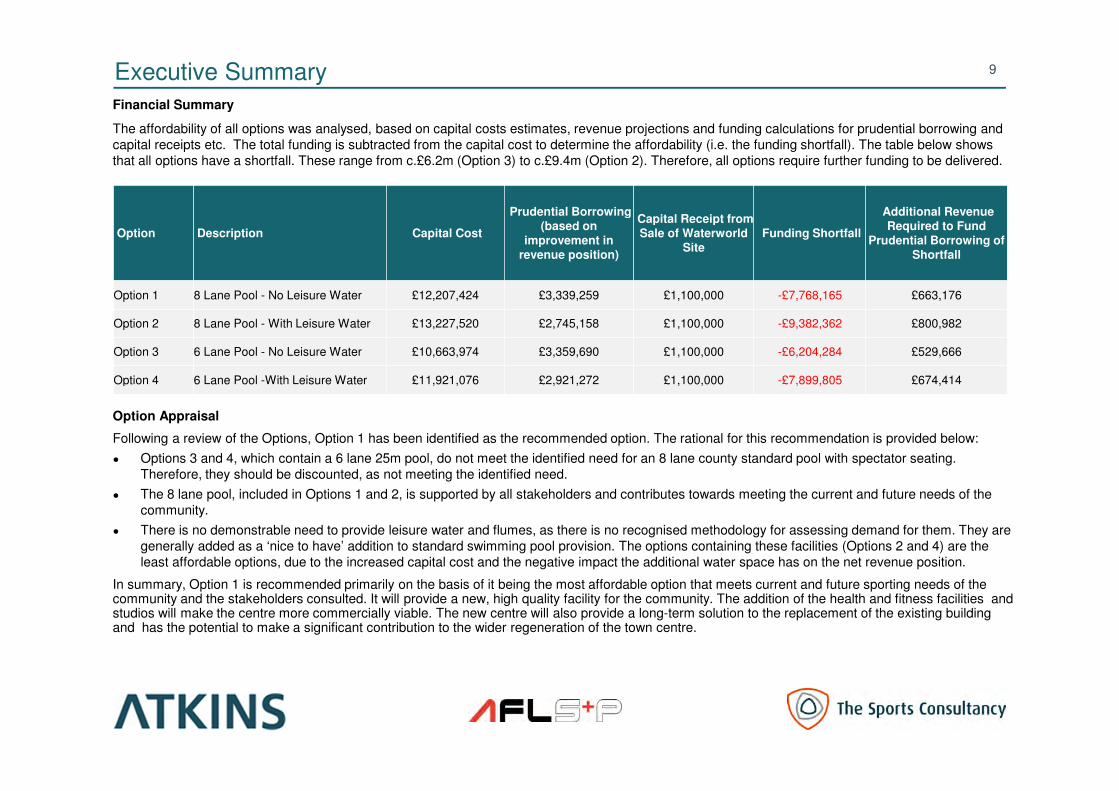

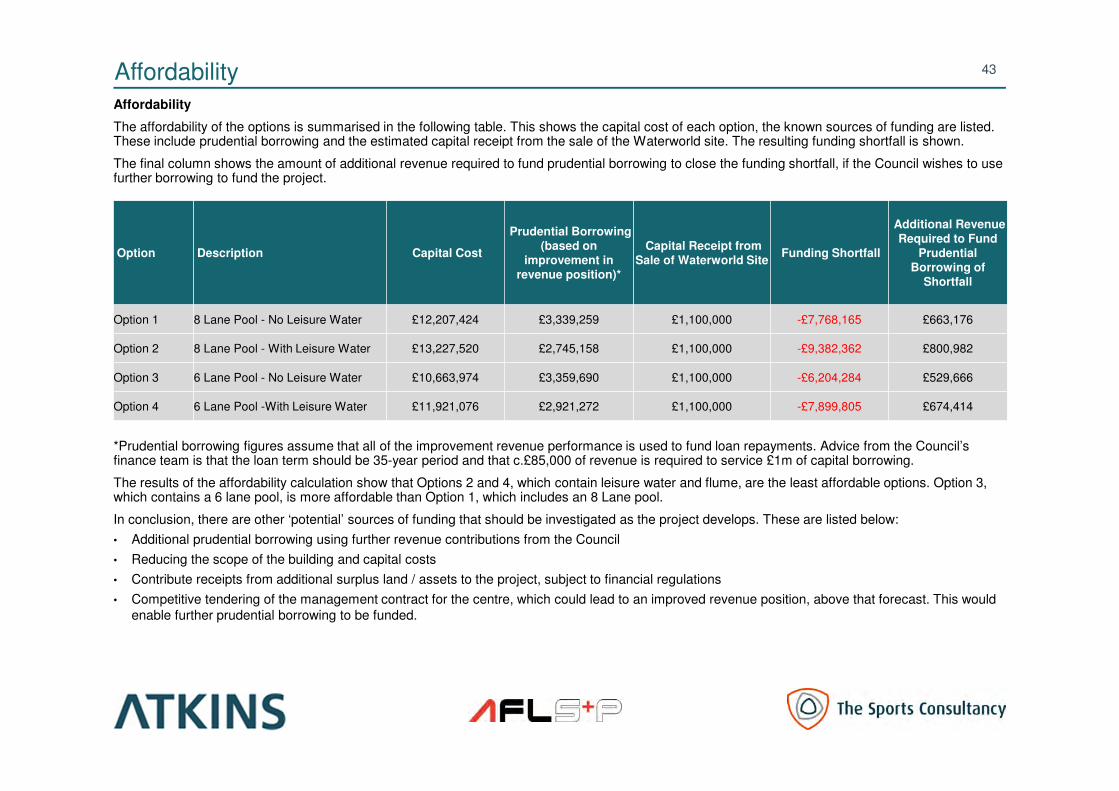

Financial Summary

The affordability of all options was analysed, based on capital costs estimates, revenue projections and funding calculations for prudential borrowing and

capital receipts etc. The total funding is subtracted from the capital cost to determine the affordability (i.e. the funding shortfall). The table below shows

that all options have a shortfall. These range from c.£6.2m (Option 3) to c.£9.4m (Option 2). Therefore, all options require further funding to be delivered.

Option Appraisal

Following a review of the Options, Option 1 has been identified as the recommended option. The rational for this recommendation is provided below:

● Options 3 and 4, which contain a 6 lane 25m pool, do not meet the identified need for an 8 lane county standard pool with spectator seating.

Therefore, they should be discounted, as not meeting the identified need.

● The 8 lane pool, included in Options 1 and 2, is supported by all stakeholders and contributes towards meeting the current and future needs of the

community.

● There is no demonstrable need to provide leisure water and flumes, as there is no recognised methodology for assessing demand for them. They are

generally added as a ‘nice to have’ addition to standard swimming pool provision. The options containing these facilities (Options 2 and 4) are the

least affordable options, due to the increased capital cost and the negative impact the additional water space has on the net revenue position.

In summary, Option 1 is recommended primarily on the basis of it being the most affordable option that meets current and future sporting needs of the community and the stakeholders consulted. It will provide a new, high quality facility for the community. The addition of the health and fitness facilities and studios will make the centre more commercially viable. The new centre will also provide a long-term solution to the replacement of the existing building and has the potential to make a significant contribution to the wider regeneration of the town centre.

9

Option Description Capital Cost

Prudential Borrowing

(based on improvement in

revenue position)

Capital Receipt from Sale of Waterworld

Site

Funding Shortfall

Additional Revenue

Required to Fund Prudential Borrowing of

Shortfall

Option 1 8 Lane Pool - No Leisure Water £12,207,424 £3,339,259 £1,100,000 -£7,768,165 £663,176

Option 2 8 Lane Pool - With Leisure Water £13,227,520 £2,745,158 £1,100,000 -£9,382,362 £800,982

Option 3 6 Lane Pool - No Leisure Water £10,663,974 £3,359,690 £1,100,000 -£6,204,284 £529,666

Option 4 6 Lane Pool -With Leisure Water £11,921,076 £2,921,272 £1,100,000 -£7,899,805 £674,414

Executive Summary

Funding Options

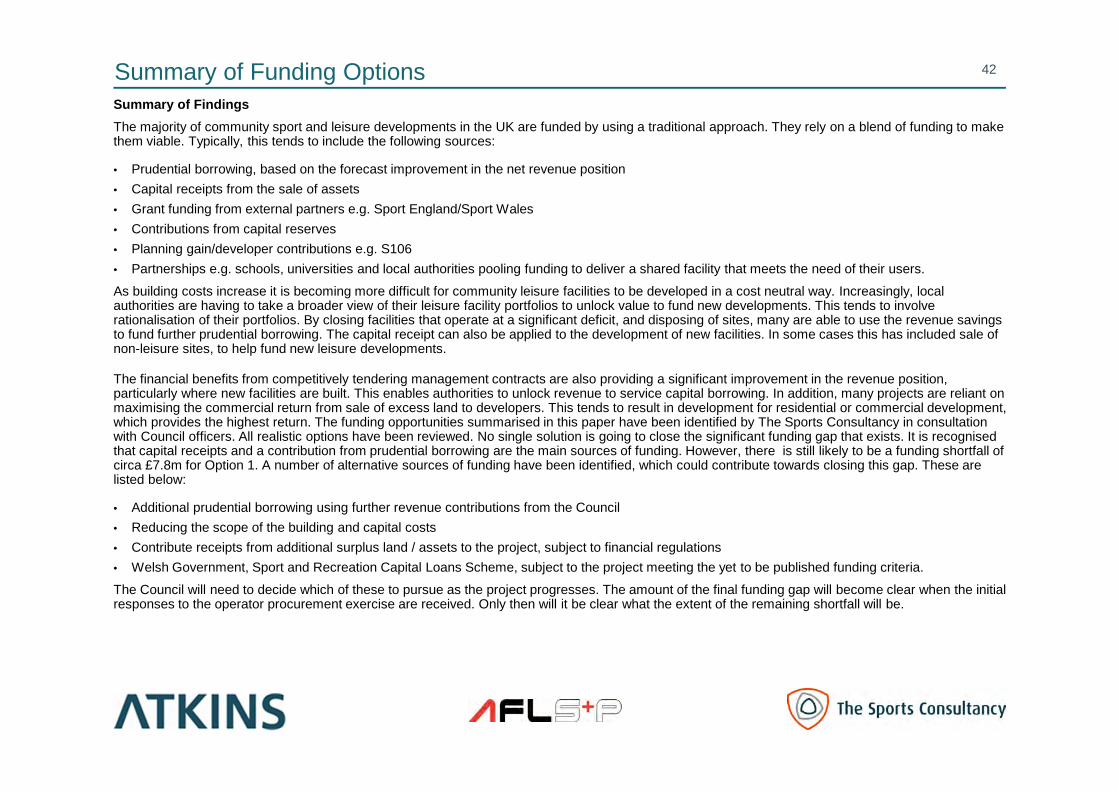

The majority of community sport and leisure developments in the UK are funded by using a traditional approach. They rely on a blend of funding to make them viable. Typically, this tends to include the following sources:

• Prudential borrowing, based on the forecast improvement in the net revenue position

• Capital receipts from the sale of assets

• Grant funding from external partners e.g. Sport England/Sport Wales

• Contributions from capital reserves

• Planning gain/developer contributions e.g. S106

• Partnerships e.g. schools, universities and local authorities pooling funding to deliver a shared facility that meets the need of their users.

As building costs increase it is becoming more difficult for community leisure facilities to be developed in a cost neutral way. Increasingly, local authorities are having to take a broader view of their leisure facility portfolios to unlock value to fund new developments. This tends to involve rationalisation of their portfolios. By closing facilities that operate at a significant deficit, and disposing of sites, many are able to use the revenue savings to fund further prudential borrowing. The capital receipt can also be applied to the development of new facilities. In some cases this has included sale of non-leisure sites, to help fund new leisure developments.

The financial benefits from competitively tendering management contracts are also providing a significant improvement in the revenue position, particularly where new facilities are built. This enables authorities to unlock revenue to service capital borrowing. In addition, many projects are reliant on maximising the commercial return from sale of excess land to developers. This tends to result in development for residential or commercial development, which provides the highest return. The funding opportunities summarised in this paper have been identified by The Sports Consultancy in consultation with Council officers. All realistic options have been reviewed. No single solution is going to close the significant funding gap that exists. It is recognised that capital receipts and a contribution from prudential borrowing are the main sources of funding. However, there is still likely to be a funding shortfall of circa £7.8 for Option 1. A number of alternative sources of funding have been identified, which could contribute towards closing this gap. These are listed below:

• Additional prudential borrowing using further revenue contributions from the Council

• Reducing the scope of the building and capital costs (including Sport England’s Affordable Models)

• Contribute receipts from additional surplus land / assets to the project, subject to financial regulations

• Welsh Government, Sport and Recreation Capital Loans Scheme (subject to the project meeting the funding criteria).

The Council will need to decide which of these to pursue, as the project progresses. The amount of the final funding gap will become clear when the initial responses to the operator procurement exercise are received. Only then will it be clear what the extent of the remaining shortfall will be.

10

Executive Summary

Project Programme

An outline programme has been developed to show the key stages in the development of the project and the timescales associated with these. The

programme is based on the Royal Institution of British Architects (RIBA) stages of work. It shows that the new centre could be completed by Qtr 2 2018.

This programme assumes that there are no long delays in Council approvals or in the procurement of consultants and contractors.

Next Steps

The work completed during this study represents the initial feasibility stage. It includes capital and revenue estimates and the outline business case for

the initial options to enable the Council to decide whether to proceed with the development of the preferred option. However, it should be noted that all

capital and revenue costs will be subject to change as the options are developed and refined. If the Council decides to proceed with the project, the next

stage should involve completion of RIBA Stage 2 (Concept Design) based on the preferred option. This includes:

• Preparing more detailed designs for the preferred option

• Proposals for structural design

• Proposals for building services systems

• Development of the project cost plan

• Review of the delivery strategy and programme

• Finalise project brief

• Prepare sustainability, health and safety, operational, procurement and construction strategies and plans

• Review and develop the project risk register

• Complete relevant site surveys and investigations

• Review and development of the business case.

The cost of taking the project forward through the next stages of work are included in the professional fees within the capital costs estimates contained in

this report.

11

Executive Summary

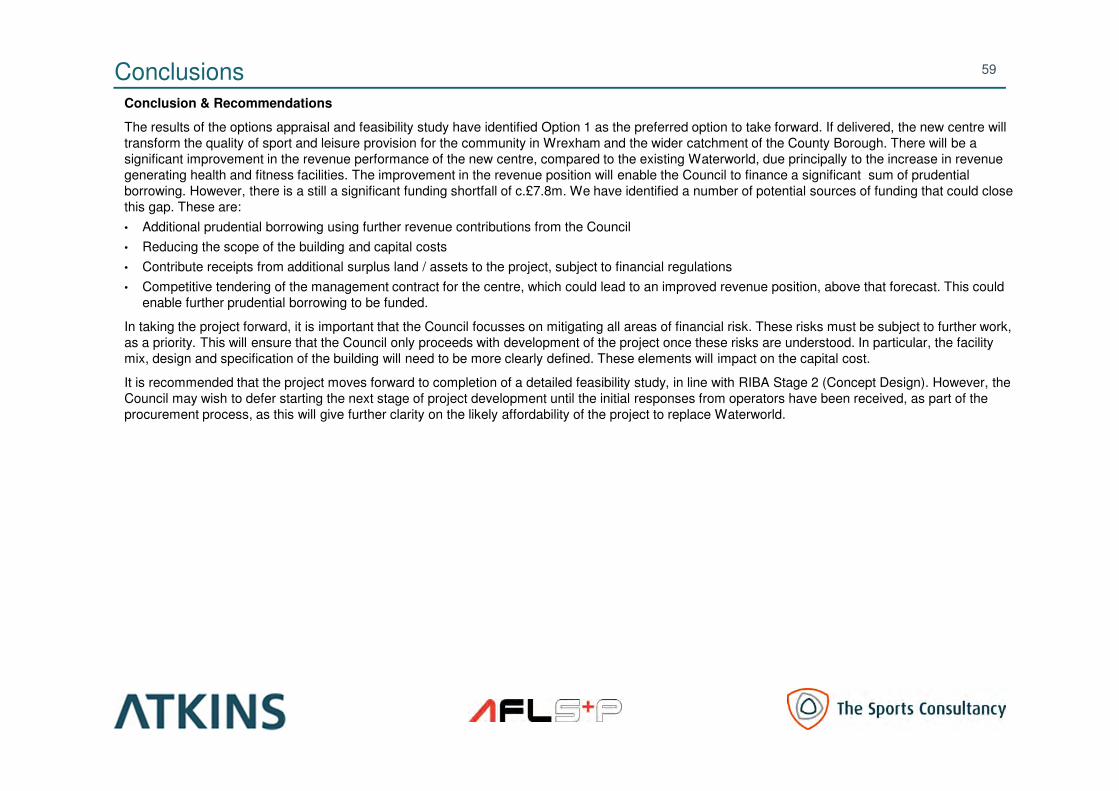

Conclusion & Recommendations

The results of the options appraisal and feasibility study have identified Option 1 as the preferred option to take forward. If delivered, the new centre will

transform the quality of sport and leisure provision for the community in Wrexham and the wider catchment of the County Borough. There will be a

significant improvement in the revenue performance of the new centre, compared to the existing Waterworld, due principally to the increase in revenue

generating health and fitness facilities. The improvement in the revenue position will enable the Council to finance a significant sum of prudential

borrowing. However, there is a still a significant funding shortfall of c.£7.8m. We have identified a number of potential sources of funding that could close

this gap. These are:

• Additional prudential borrowing using further revenue contributions from the Council

• Reducing the scope of the building and capital costs

• Contribute receipts from additional surplus land / assets to the project, subject to financial regulations

• Competitive tendering of the management contract for the centre, which could lead to an improved revenue position, above that forecast. This could

enable further prudential borrowing to be funded.

In taking the project forward, it is important that the Council focusses on mitigating all areas of financial risk. These risks must be subject to further work,

as a priority. This will ensure that the Council only proceeds with development of the project once these risks are understood. In particular, the facility

mix, design and specification of the building will need to be more clearly defined. These elements will impact on the capital cost.

It is recommended that the project moves forward to completion of a detailed feasibility study, in line with RIBA Stage 2 (Concept Design). However, the

Council may wish to defer starting the next stage of project development until the initial responses from operators have been received, as part of the

procurement process, as this will give further clarity on the likely affordability of the project to replace Waterworld.

12

Introduction and Background

13

Introduction

Atkins (incorporating subsidiary Faithful & Gould), in partnership with The Sports Consultancy and AFLS+P Architects, was appointed by Wrexham

County Borough Council (the Council) in September 2014, to complete a feasibility study for a new main leisure centre, in central Wrexham, to serve the

County Borough. The new centre is intended to provide a long term replacement for Waterworld. The outputs from the study will be used by the Council

as the basis of decisions on whether, and how best, to proceed with the development of a new leisure centre. The agreed scope of work included the

following:

• A feasibility study for a new leisure centre to serve Wrexham and the wider catchment of the County Borough, taking into consideration competing

facilities (existing and planned).

• Assessment of the capital and revenue implications of the proposed facility mix options, including variants, and identification of which is the most

financially beneficial. This assessment should be set in the context of the current financial constraints affecting the Council.

• A review of the financial impact of the sensitivity analysis (i.e. under performance or over performance).

• Above all, a recommendation as to which facility option is the most financially viable and an assessment of how the scheme could be funded

including prudential borrowing.

• Recommendation of the most cost and time effective manner to procure the delivery of the new facility.

• Recommendation of the most financially beneficial approach to financing the capital delivery of the proposed facility.

The outputs from the study will be used by the Council as the basis of decisions on whether, and how best, to proceed with the development of a new

leisure centre.

Stages of work completed

The key stages of work completed were:

• Stage 1 - Project Initiation

• Stage 2 - Needs Analysis and external consultation work

• Stage 3 - Options Development

• Stage 4 - Options Appraisal and Refinement

• Stage 5 - Conclusions and Recommendations.

The results of the study are contained in this summary report and appendices.

14

Needs Analysis

15

Needs Analysis

Existing Facilities

Waterworld is located in Wrexham town centre. It opened in 1970 and was significantly refurbished in 1998. The facility is now 43 years old. There are

issues affecting the structure and fabric of the Waterworld swimming pool. The building is likely to require replacement during the term of the proposed

management contract, which is why a decision on its future is required. Waterworld contains the following activity areas:

• Main swimming pool - 6 lane 33m pool with moveable boom to create separate pool (7m x 12.5m)

• Leisure pool - Separate flume area (former diving pool)

• Teaching pool - 6m x 12.5m

• Health suite - Sauna and steam room

• Health and fitness - Circa 40 stations of equipment

• Dance studio - 1 studio.

Recommendation from the Leisure Strategy (2013) and Options Appraisal Study

In 2013, the Council commissioned an Options Evaluation Study to investigate the options for the replacement of Plas Madoc Leisure and Activity Centre

(Plas Madoc) and Waterworld Leisure and Activity Centre (Waterworld). The Options Evaluation Study was linked to the Council’s wider Leisure

Strategy, also completed in 2013. One of the key recommendations of this study was that Plas Madoc Leisure and Activity Centre should be closed and

that the Council should conduct an initial feasibility study to define and assess the options for the replacement of Waterworld in central Wrexham. Plas

Madoc has recently been transferred to a community based trust, SPLASH, which is now operating the centre which has been re-branded Splash Magic.

The Council is facing significant financial challenges with at least £45m savings required over the next few years. A clear decision is now required

regarding the long-term future of Waterworld, to identify more efficient delivery models, whilst at the same time maintaining the services provided to the

local community.

The wider Leisure Strategy included an appraisal of the management options available to the Council for the remaining portfolio of facilities. This

concluded that the most efficient and financially viable option for the future management of the Council’s facilities is to contract the management to an

external (not for profit) trust operator. As the Council intends to externalise the management contract, it is critical that it is in a position to tell the market

what its strategy is at the outset of the procurement process (and how this strategy is going to be funded and implemented). This study is intended to

inform the subsequent operator procurement. The Options Evaluation Study recommended that the following facility mix should be the focus of the

feasibility study:

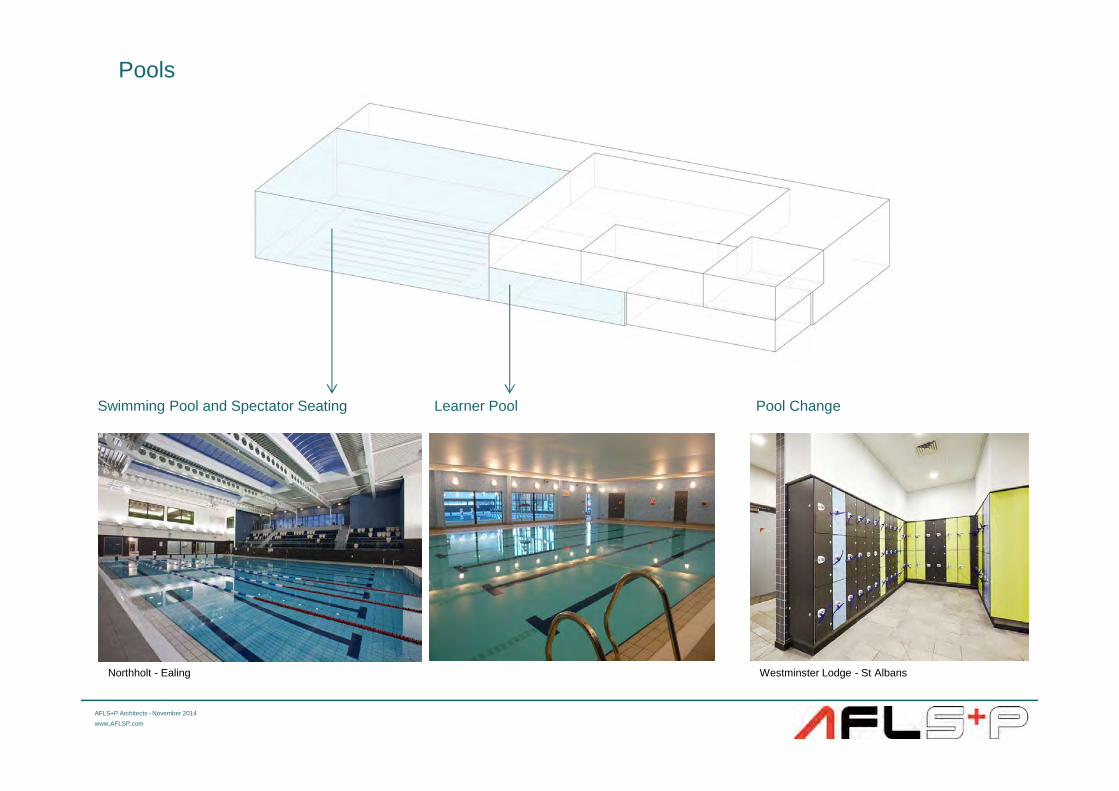

• 8 lane 25 metre swimming pool (17m x 25m) to ASA County standard spectator seating for 250 people

• Learner pool

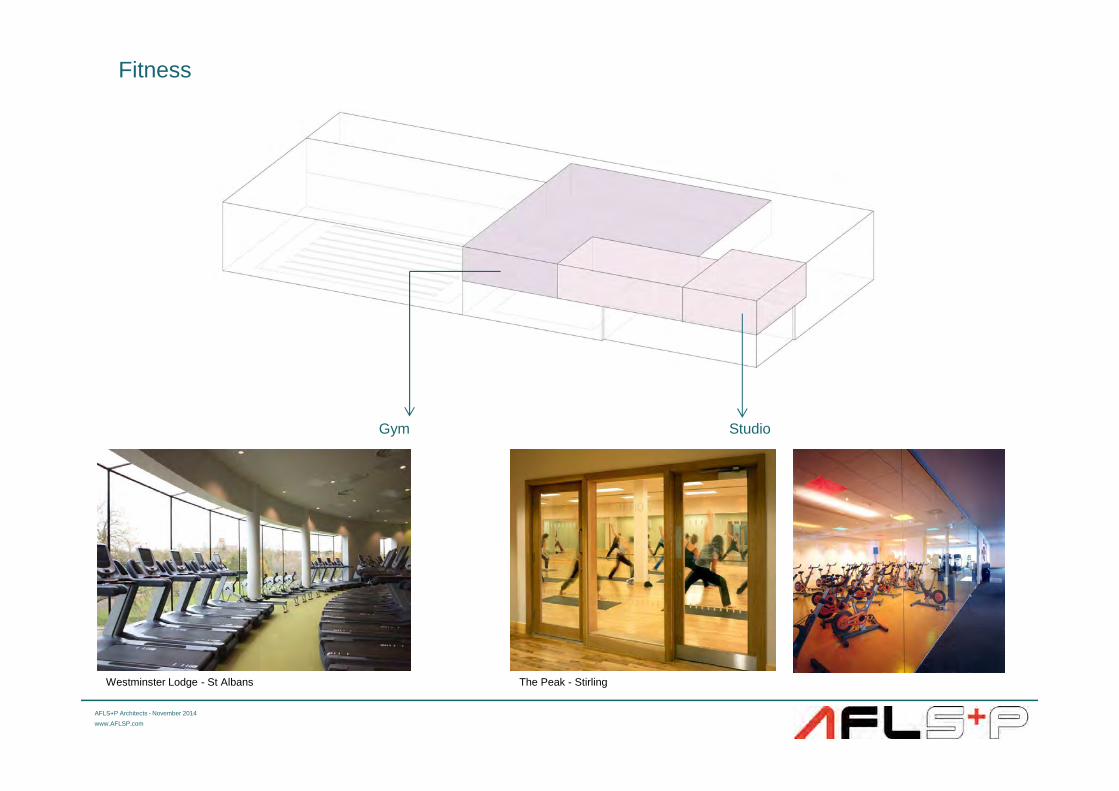

• 120 station health and fitness; includes weights area

• Dance/fitness studios; 2 x 30 person & storage

In addition, it was recommended that a Leisure water area (one flume/feature) should be considered as an option, to replace the flume at the existing

Waterworld site.

16

Needs Analysis

Stakeholder Consultation

Over 60 clubs and organisations were contacted during the consultation stage of the Leisure Strategy. In particular, this included their views on facility

requirements for Waterworld. A summary of the key findings from the consultation is provided below:

• The current building is beyond its designed life. There is very limited scope for expansion, due to site restrictions and the structure of the building. A

replacement should be considered in the short to medium-term

• The facility is well used, with significant excess demand for health and fitness and studio use, in particular. This is demonstrated by the need to use

the nearby Memorial Hall to accommodate many of these activities that cannot be accommodated in the Waterworld building.

• The current lack of health and fitness facilities at Waterworld means the Council is forgoing potential income from health and fitness membership.

Increasing the health and fitness areas will increase throughput and revenue, resulting in reduced financial support from the Council. This should be a

priority for the Council

• Waterworld is situated in a central ‘town centre’ location, with a lack of comparable, swimming facilities in the area

• Leisure water/flumes could be included as part of a replacement facility to offset the loss of leisure water/flumes at the current pool

• The Council and stakeholders have aspirations for a county standard pool to be provided in Wrexham. This is to meet the needs of swimming and

also to reflect Wrexham’s status as the third largest settlement in Wales, below, Cardiff and Swansea.

In addition to the consultation completed during the Leisure Strategy, further consultation was conducted with a number of potential partners. The results

are summarised in the following paragraphs:

Sport Wales - Sport Wales Senior Officer

Sport Wales advises that input from the National Governing Body (Swim Wales) is critical. It already has an established working partnership with

Wrexham County Borough Council in terms of an annual investment into their Local Sport Plan, part of which includes swimming and recreational dry

side activities with targeted groups. This would continue as part of their CORE programme funding arrangement and would include any new facilities

developed. Sport Wales doesn’t currently operate a Capital lottery investment programme, all investment is revenue based. Therefore, it has no capital

funding to contribute towards the project.

Swim Wales - Regional Business Manager (North)

Swim Wales states that whilst the proposed facility would be an improvement on the existing, and perhaps is the best that can be hoped for in the current

climate, it could be missing an opportunity. If, as is likely, leisure facilities in Wrexham move to Trust or management company there could be potential

for a wide range of stakeholders to come together and justify a 50m facility, something that North Wales is in dire need of. As a point for discussion, an 8

lane 50metre pool with moveable floor could provide the desired facility mix, whilst providing a much needed resource and additional income from hire of

50m lanes. However, Swim Wales has no funding to support the project.

17

Needs Analysis

Coleg Cambria

The colleges commented that the proposed facility would be an excellent resource for the area. It also supports the development of a county standard

competition pool. A health and fitness suite and multi-activity studios will provide facilities which could potentially attract large numbers of users and

provide a good income stream. The College would be interested in exploring opportunities to work in partnership with the Council to deliver activities at

the site. This could include the involvement of learners, particularly those on courses related to sports and leisure or other associated areas. Further

discussion would be required to develop options further. The College would certainly be interested in promoting the use of the facilities for staff and

students as part of its overall approach to wellbeing.

Any funding contribution would be a decision for the College's Governing Body. The College has an ambitious estate strategy which sets out a

framework of potential developments over the next 10 years and this will require significant funding. The College, like other public sector organisations,

is likely to experience significant funding cuts over the next few years and all funding decision will need to be prioritised. Therefore, at this point the

College is unable to commit capital funding towards the project.

Glyndŵr University Wrexham - Director of Operations

The University is very supportive of the Council in seeking to provide for a County standard swimming facility within the area. The University states that

with its existing financial commitment to its own sports facilities it is unable to contribute capital funding towards the swimming pool project. Student

numbers and associated student needs analysis undertaken in sports facility provision do not justify such a spend. The University has good links with

Wrexham Swimming Club and would look to use the new facilities to strengthen these links further.

Betsi Cadwalader University Health Board

Betsi Cadwalader University Health Board was contacted on several occasions but does not have resources to contribute towards the project.

Summary

Generally, the comments support the need for improved facilities for swimming to replace the existing Waterworld. The key issue is that a county

standard pool should be provided to deliver the local needs and those of competition swimmers in the wider catchment of north Wales. The request from

Swim Wales to consider a 50m pool was reviewed during the options appraisal study and was discounted on the grounds of affordability.

While all of the organisations consulted are supportive of the proposals, and are keen to work in partnership with the Council, none of them are able to

commit capital funding towards the project at this stage.

18

Needs Analysis

Supply and Demand Analysis for Swimming Pools

Detailed supply and demand analysis has been completed for swimming pools, using Sport Wales’ Facility Planning Model (FPM). This provides a

robust, industry recognised, assessment of supply and demand for these facility types. It also takes account of the impact of significant forecast

population growth and the impact this will have on future demand. According to the 2011 census the population of the Wrexham County Borough Council

was c.135,000. Projections from Info Base Cymru suggest that by 2031 the population will increase by to approximately 158,000.

The following conclusions can be drawn from analysis of the findings from the FPM modelling:

• Overall summary – The proposed 8 lane 25m pool is preferable, in terms of meeting the identified demand, as it includes greater provision of pool

space. It would result in an increase in utilisation and throughput at a replacement for Waterworld. This would need to be carefully managed by the

operator, particularly during peak periods.

• Any provision less than the proposed 8 lane 25m pool at Waterworld would result in a more significant reduction in supply and is likely to be more

problematic, in terms of meeting demand for swimming in the County Borough. This supports the need for an 8 lane county standard pool.

• The option of a 50 metre pool was discounted during the previous Options Evaluation Study, as the results of supply and demand modelling work

commissioned by Sport Wales did not support that level of provision. The proposed 8 Lane 25m pool will result in a shortfall of provision across the

County Borough equivalent to 4 x 25m lanes, which is only half of what would be required to increase provision to an 8 lane 50m competition pool.

The results of the supply and demand modelling suggest that if an 8 lane 50m pool was provided this is likely to be under utilised. However, consultation

with Swim Wales suggests that this would provide a valuable facility for swimming clubs in North Wales. In financial terms, the provision of an 8-lane

50m pool have a negative impact on the net revenue position and is likely to add c.£3m to the capital cost of the project. The reduced revenue position

and increased capital cost would make the project significantly leas affordable. Therefore, the 50m pool option was discounted on the grounds of

insufficient need and the negative impact on financial viability.

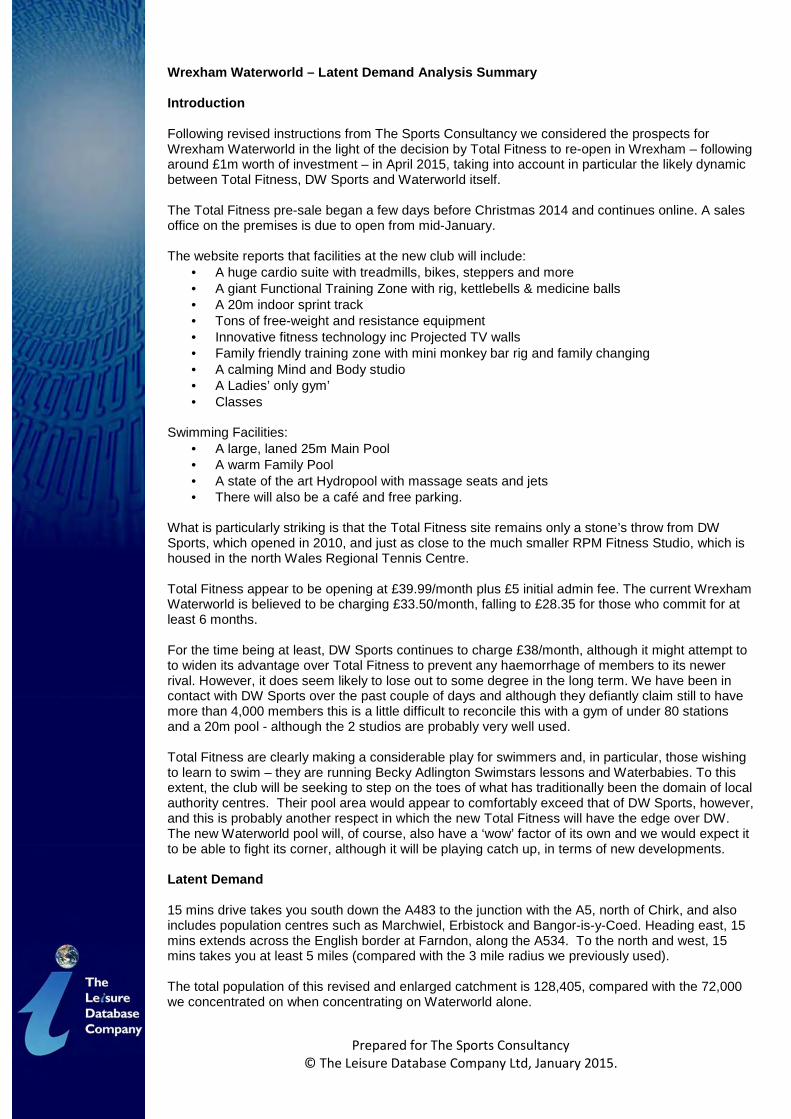

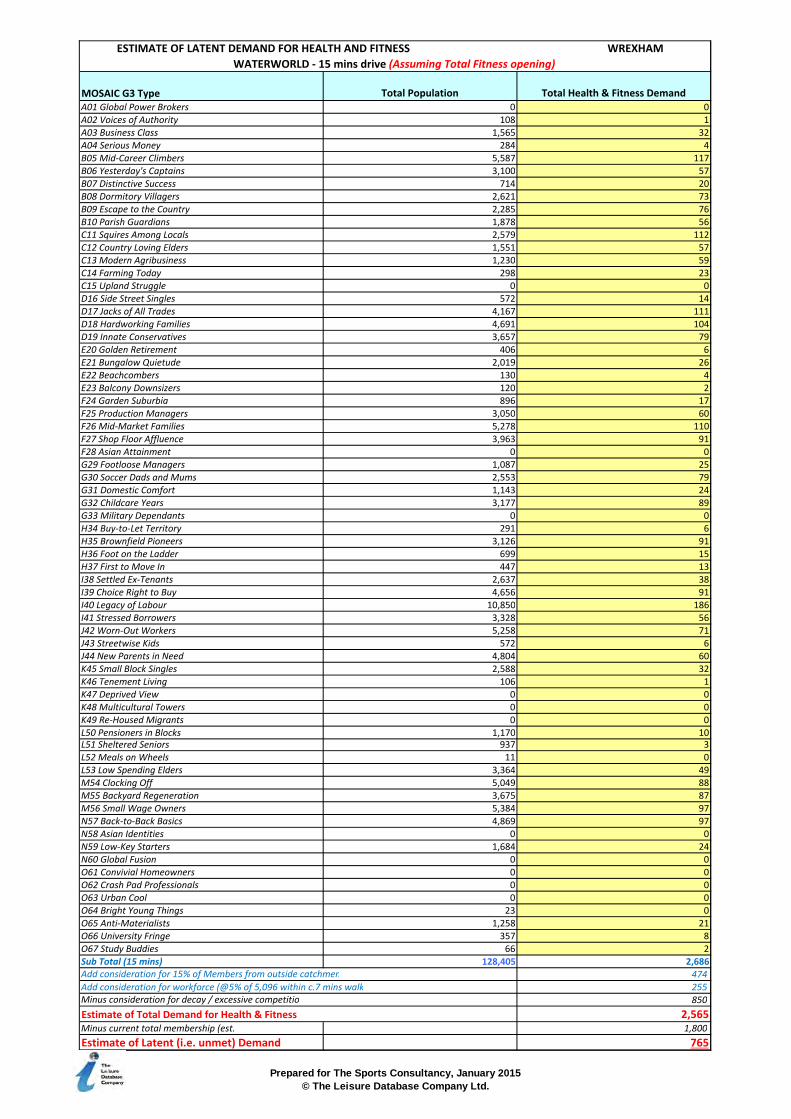

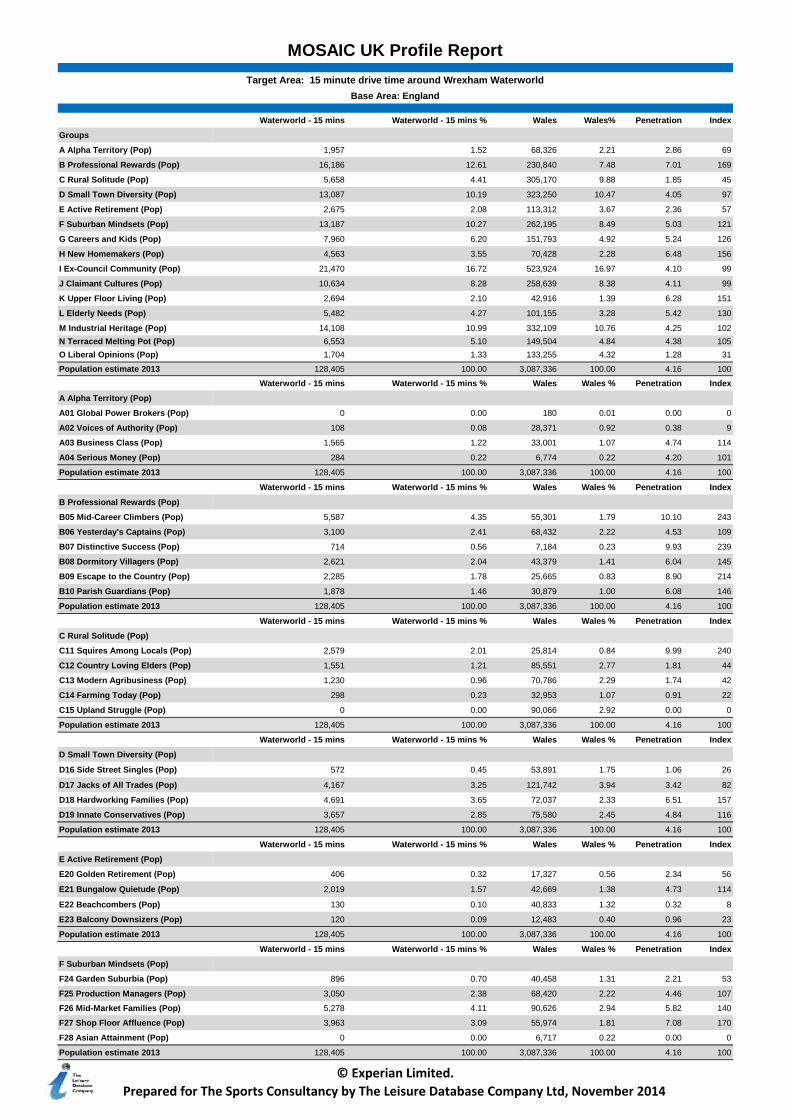

Review of the findings from a latent demand report for health and fitness membership

The Sports Consultancy commissioned a latent demand report from The Leisure Database Company Ltd. The latent demand report provides a detailed

analysis of consumer demographics, using Experian’s MOSAIC consumer profiling, for a defined core catchment area of a 15-minute drive time. The

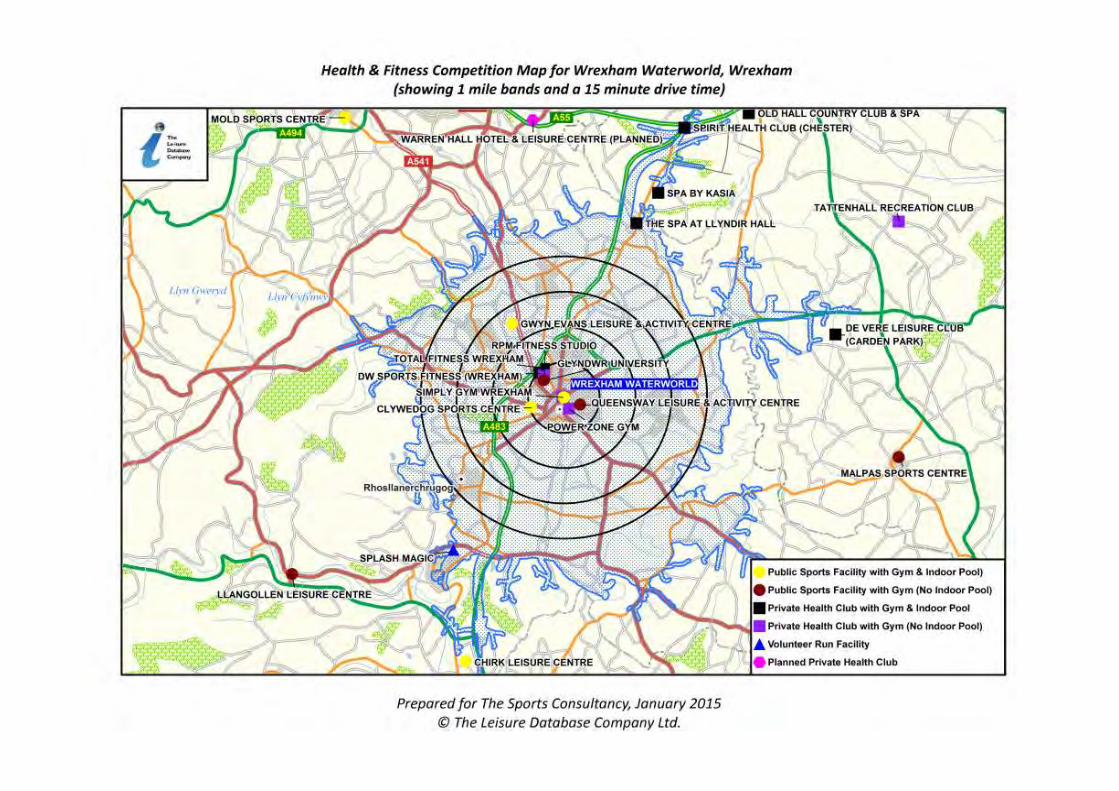

report identifies the profile of consumers on a postcode basis and their propensity to join a health and fitness club. It identifies competing facilities within

the catchment area and their current membership numbers. This enables a detailed estimate of latent demand to be produced and the likely overall

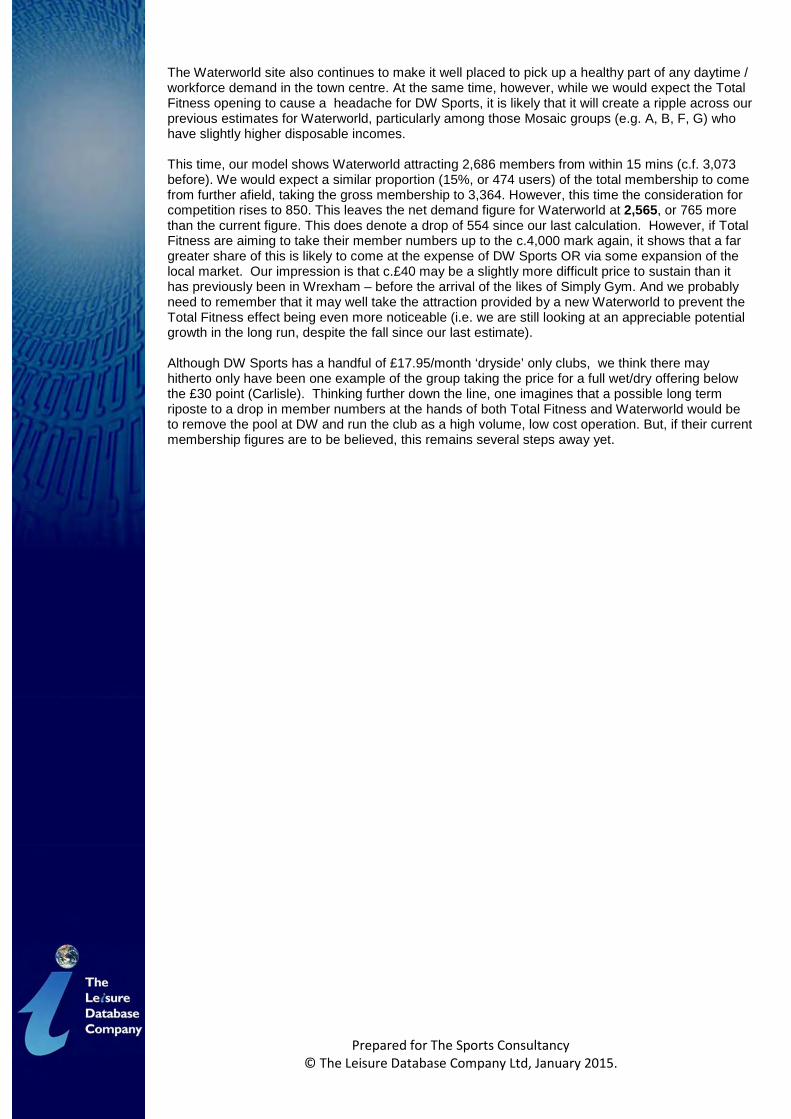

membership targets to be defined. The latent demand report for the proposed Waterworld site identifies a potential membership of 2,565. This takes

account of the impact of the re-opening of Plas Madoc and the planned re-opening of Total Fitness Wrexham.

These reports are accurate and are used by most major commercial health and fitness operators when making decisions on the location for new gym

developments. As such, they provide a robust, but relatively conservative, estimate of membership numbers - a key income generator in the business

plan. This is a robust and well tested methodology for forecasting membership numbers and the resulting income. The full results of the demand analysis

is contained in Appendix 1.

19

Needs AnalysisUsing a typical ratio of 25 members per health and fitness station, new health and fitness facilities should be designed to accommodate c.100 stations of

equipment. We have allowed additional capacity for 20 further stations, to allow for changes in the local population and further membership growth

above that forecast in the latent demand analysis. This area could comfortably accommodate up to c.4,500, if a higher ratio of members per station is

required.

Re-opening of Total Fitness

The club closed in 2011, after increased rental costs and a failure to secure sufficient membership income meant the site was no longer financially

viable. It is understood that Total Fitness is investing over £1m, to upgrade existing facilities. Membership fees will be slightly lower than previously, with

full adult membership at £40 per month compared to circa £45 previously. Concessionary membership fees are being advertised at £30 per month. We

understand that the previous club operated with membership of between 4,000 and 4,500 members. As the site has not yet re-opened, there is no

information available on future membership numbers. The local market has undergone some changes since 2011, with DW Fitness benefitting from

displaced members from the former Total Fitness site and the emergence of Simply Gym at the budget end of the market. However, Total Fitness clearly

sees an opportunity to attract sufficient membership numbers to justify investment and re-opening of the site.

Plas Madoc Leisure Centre

Plas Madoc Leisure Centre was transferred to a community led trust to operate in 2014 and re-opened in December 2014 under the new name Splash

Magic. It continues to operate a gym with circa 48 stations of equipment. We understand that current (January 2015) membership numbers are between

200 and 250 members. This compares with circa 700 members the centre had before it closed in April 2014. We would expect the majority of this

reduced membership to be drawn from a more local catchment than was previously the case. Full, single adult membership fees are now £26 per month,

positioning the gym towards the lower end of the market in terms of cost. Given that Splash Magic has been operating for only two months at the time of

writing this report it is not clear whether it will be financially viable and sustainable in the long-term.

Impact of the re-opening of Total Fitness on the Business Case for Waterworld

It is recognised that the impact of the re-opening of Total Fitness and Splash Magic pose a risk to the business case for a replacement of Waterworld.

Previously, both facilities were not financially viable and were closed. It is not possible to provide a definitive view on whether these sites, or indeed

others such as Simply Gym or DW Fitness, will be viable in the future. However, this study does take account of the impact of both facilities on the

business case for Waterworld. The principal risk relates to the impact on membership projections for Waterworld, from increased competition. Revenue

generated from health and fitness membership is the foundation of the business case. Therefore, any reduction to this will have a detrimental effect on

the net revenue position and on the affordability of the project. In order to provide as much clarity as possible of the impact of the re-opening of these

facilities updated health and fitness membership forecasts were commissioned from The Leisure Database Company. They made a number of

reasonable assumptions based on information available on the two facilities and adjusted their previous predictions in light of the findings.

The results of the revised membership projections for Waterworld show that future membership projections would be reduced from c.3,100 (assuming

Splash Magic and Total Fitness were closed) to 2,565 (assuming they re-open and remain operational). We believe that this represents a realistic

assessment of the likely membership numbers that could be achieved by a good operator at Waterworld and we have used the reduced membership

projection as the basis for all business planning work. However, it should be noted that there will inevitably be other changes in the local market over

time as other providers enter and exit the market. Therefore, these projections can only provide a snapshot based on what is currently known. Longer

term, other risks and opportunities will inevitably arise.

20

Needs Analysis

Summary of the Needs Analysis

The findings from the needs analysis completed during the options appraisal stage, and updated as part of this feasibility study, support the provision of

the following facilities in a replacement of Waterworld:

* The term leisure water refers to a separate shallow beached pool area, similar to the sloping pool at Plas Madoc. Alternatively, this area could also be

utilised for toddler splash/confidence water area. The cost of including a single flume has also been allowed for in leisure water options.

21

Activity Area Notes

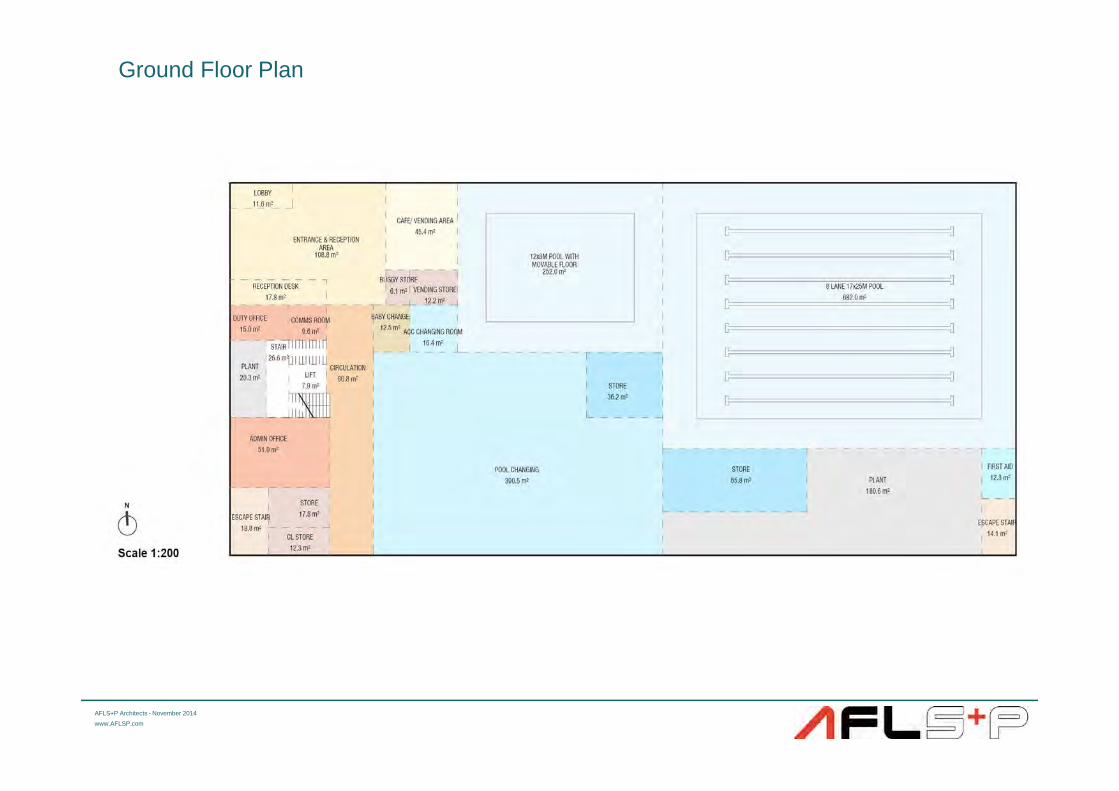

8 lane 25 metre pool (17m x 25m) to ASA

County standard

At least an 8 lane 25m pool should be provided to meet current and future needs. The pool will provide

full access for people with disabilities.

Spectator seating for 240 peopleSpectator seating for 240 spectators must be provided if the pool is to be able to host county standard

competition

Learner pool with moveable floor with full

disabled access

The learner pool must be provided to meet the need for learn to swim and school swimming

programmes. The pool will have a moveable floor for maximum flexibility of use and revenue

generation. It will also provide full disabled access.

120 station health and fitness; includes

weights area

The latent demand analysis supports provision of a 120 station health and fitness suite to meet the

local demand and to generate revenue for the centre. The area for the health and fitness suite should

be based on 5m2 per station, which provides scope to accommodate up to 133 stations at 4.5m2.

Dance/fitness studios; 2 x 30 person &

storage

Given the scale of the proposed health and fitness provision, we recommend that 2 x studios are

included in the facility mix to provide flexible activity spaces for group based activities.

Leisure water area (one flume/feature)*

Leisure water is not an essential facility. There is no demonstrable need to provide leisure water and

flumes, as there is no recognised methodology for assessing demand for them. They are generally

added as a ‘nice to have’ addition to standard swimming pool provision.

Site Options Appraisal

22

Site Options Appraisal

Site Options

During the Options Evaluation Study a number of potential sites, identified by the Council, were assessed to provide a recommendation on which should

be used to accommodate the replacement of Waterworld. This involved completion of site analysis and a scoring exercise to help establish the preferred

option.

Council officers provided a number of possible locations, to ensure that all potential sites had been considered, through a site options appraisal. The

sites considered are listed below and described briefly in the following paragraphs:

• Site 1 - Western Gateway

• Site 2 – Total Fitness

• Site 3 - Memorial Hall

• Site 4 – Waterworld

• Site 5 – Former Wrexham Town Centre Police Station

• Site 6 - Crown Buildings (currently Council offices).

1 - Western Gateway

The Western Gateway site is located to the west of Wrexham town, close to the junction between the A483 and A525. The site area is 16.5 hectares.

The site has been acquired by the Council with the long-term objective of building out Wrexham Technology Park into its third phase, focussing on

businesses that can help drive the Wrexham County Borough Council economy and improve sustainability through, for example, the creation of new and

better-paid jobs. It is likely that it will also deliver a significant number of new, high quality, homes. Much of the site is restricted to B1, B2 and B8 uses.

This site was discounted during the Options Evaluation Study.

2 - Total Fitness

The Total Fitness site is located to approximately half a mile north west of Wrexham town centre. It contains a former health and fitness club which

closed in September 2011, after the chain failed to agree terms with the landlord and decided to withdraw from the site. The site, including parking

measures 1.6 Hectares. We understand that the site has recently been acquired by Total Fitness. It is being re-furbished and is planned to re-open in

April 2015, therefore it is no longer available for development of a new leisure centre and was therefore discounted.

3 - Memorial Hall

The Memorial Hall site is located on a site close to Waterworld in Wrexham town centre. It is owned by the Council and measures approximately 0.2

Hectares. The Hall offers a range of facilities which can accommodate events such as exhibitions, conferences, seminars, concerts, dinner dances,

discos and a variety of health and fitness classes and meetings.

23

Site Options Appraisal

4 – Waterworld

The Waterworld site is located in Wrexham town centre. It is owned by the Council and measures approximately 0.8 Hectares.

5 – Former Wrexham Town Centre Police Station

The former police station site is located next to the existing Waterworld site. It is understood that the Police service is seeking to dispose of the site for

development in order to generate a capital receipt to help contribute towards the cost of developing a new police station on an alternative site. While it is

possible that the site could accommodate a new leisure centre, it is likely that the Council would be required to purchase the site at the market value,

thereby increasing the cost of the project. As a result of the likely impact on the financial viability of the project this site was discounted.

6 - Crown Buildings (currently Council offices)

The Crown Buildings site is located next to the Waterworld site in the Town Centre. It is an office building owned by the Council and measures

approximately 0.6 Hectares. It currently houses a number of Council departments.

Conclusions

Following completion of the site analysis and selection process, the preferred location was identified as the Crown Buildings. This site scored highest

compared to other locations. It is in central location in Wrexham town, close to the existing leisure centre. There is adequate site available to

accommodate the new development, with the existing car park on the adjacent site and possibly on some of the current Waterworld site. It is currently in

Council ownership with good accessibility. Development of this site could be completed while the existing pool continues to operate, thereby minimising

disruption in service to existing users. Once the new building is completed the current Waterworld site can be vacated and disposed of to generate a

capital receipt to contribute towards the new centre

24

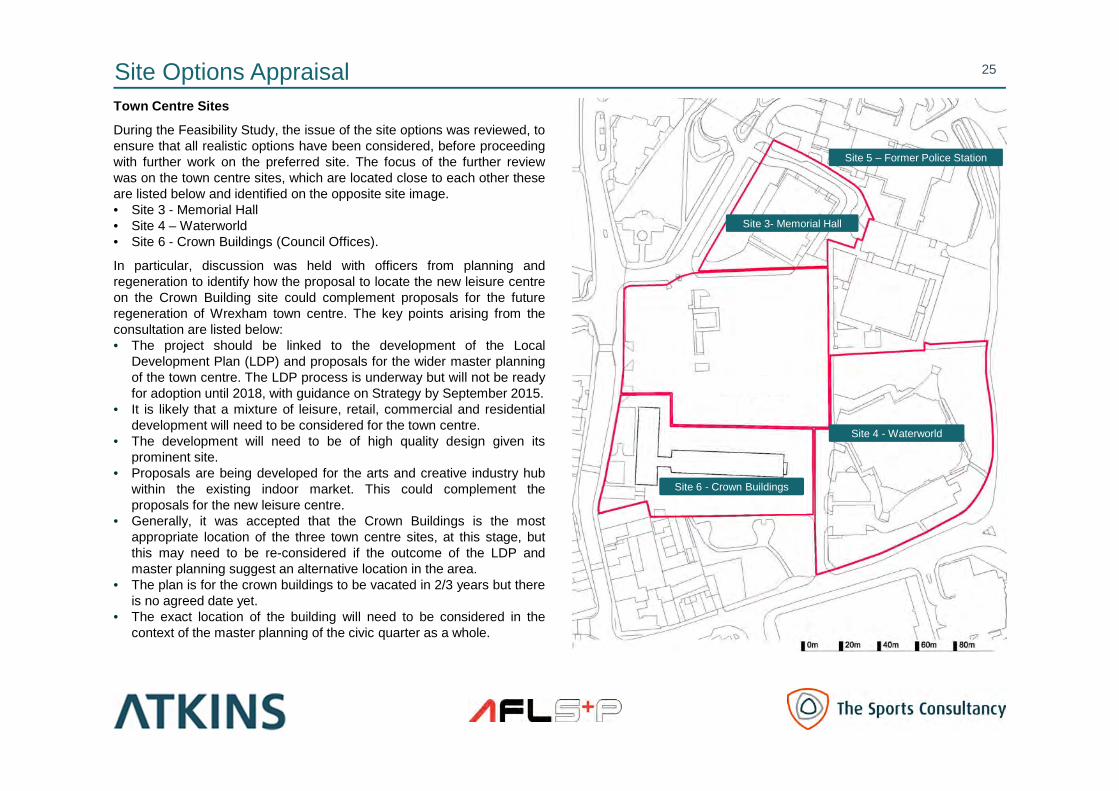

Site Options AppraisalTown Centre Sites

During the Feasibility Study, the issue of the site options was reviewed, toensure that all realistic options have been considered, before proceedingwith further work on the preferred site. The focus of the further reviewwas on the town centre sites, which are located close to each other theseare listed below and identified on the opposite site image.• Site 3 - Memorial Hall• Site 4 – Waterworld• Site 6 - Crown Buildings (Council Offices).

In particular, discussion was held with officers from planning andregeneration to identify how the proposal to locate the new leisure centreon the Crown Building site could complement proposals for the futureregeneration of Wrexham town centre. The key points arising from theconsultation are listed below:• The project should be linked to the development of the Local

Development Plan (LDP) and proposals for the wider master planningof the town centre. The LDP process is underway but will not be readyfor adoption until 2018, with guidance on Strategy by September 2015.

• It is likely that a mixture of leisure, retail, commercial and residentialdevelopment will need to be considered for the town centre.

• The development will need to be of high quality design given itsprominent site.

• Proposals are being developed for the arts and creative industry hubwithin the existing indoor market. This could complement theproposals for the new leisure centre.

• Generally, it was accepted that the Crown Buildings is the mostappropriate location of the three town centre sites, at this stage, butthis may need to be re-considered if the outcome of the LDP andmaster planning suggest an alternative location in the area.

• The plan is for the crown buildings to be vacated in 2/3 years but thereis no agreed date yet.

• The exact location of the building will need to be considered in thecontext of the master planning of the civic quarter as a whole.

25

Site 3- Memorial Hall

Site 4 - Waterworld

Site 6 - Crown Buildings

Site 3- Memorial Hall

Site 5 – Former Police Station

Site Options Appraisal

Conclusions

• The review of the Crown Buildings site concluded that it remained the preferred location for development of the new leisure centre, as was the case

during the previous Options Evaluation Study.

• The principal benefits of the Crown Buildings site are:

• It is in a central location in Wrexham town, close to the existing leisure centre.

• There is adequate site available to accommodate the new development, with the existing car park on the adjacent site and possibly on some of

the Waterworld site, if needed. It is currently in Council ownership with good accessibility.

• Development of this site could be completed while the existing pool at Waterworld continues to operate.

• Use of the Crown buildings site would enable the existing Waterworld site to be disposed of to generate a capital receipt (estimated at £1.1m) to

contribute towards the new centre, thereby improving affordability.

• It is important that the exact location of the new centre is considered in the context of the potential development of the wider town centre site.

Planning and regeneration officers from the Council should continue to be consulted as the design develops. This will ensure that the potential of the

leisure centre to contribute towards town centre regeneration is maximised.

26

Facility Options

27

Facility Options

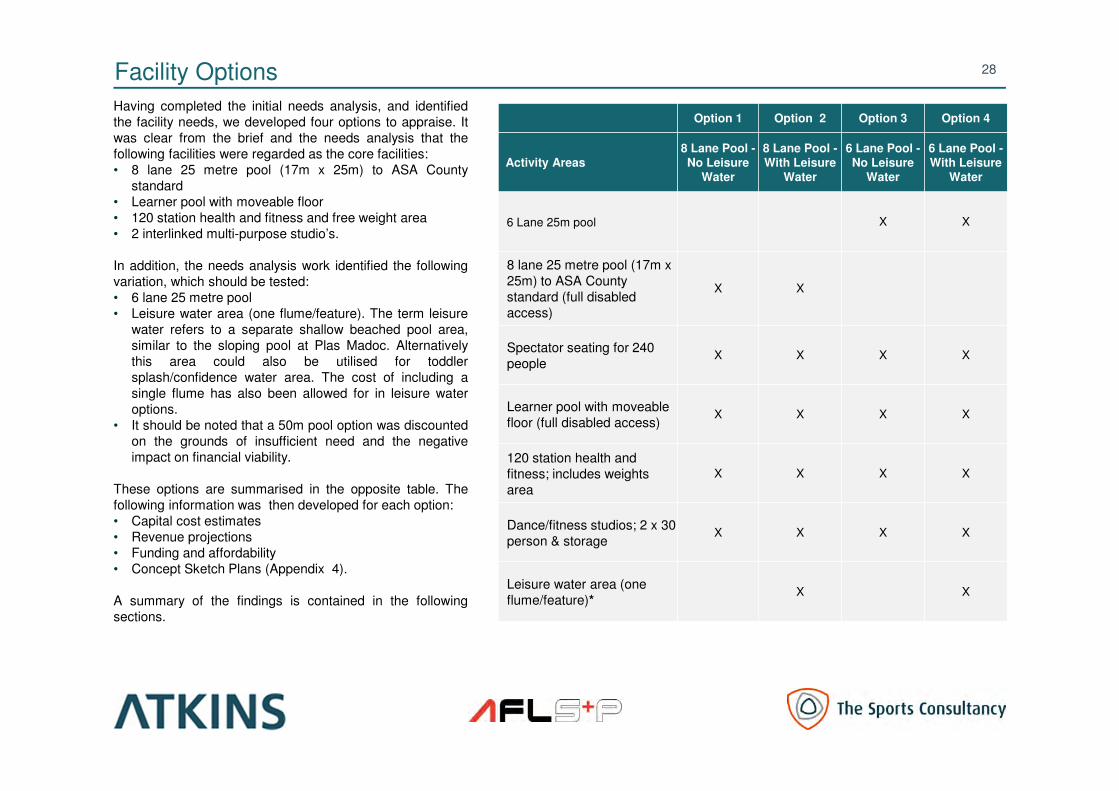

Having completed the initial needs analysis, and identified

the facility needs, we developed four options to appraise. It

was clear from the brief and the needs analysis that the

following facilities were regarded as the core facilities:

• 8 lane 25 metre pool (17m x 25m) to ASA County

standard

• Learner pool with moveable floor

• 120 station health and fitness and free weight area

• 2 interlinked multi-purpose studio’s.

In addition, the needs analysis work identified the following

variation, which should be tested:

• 6 lane 25 metre pool

• Leisure water area (one flume/feature). The term leisure

water refers to a separate shallow beached pool area,

similar to the sloping pool at Plas Madoc. Alternatively

this area could also be utilised for toddler

splash/confidence water area. The cost of including a

single flume has also been allowed for in leisure water

options.

• It should be noted that a 50m pool option was discounted

on the grounds of insufficient need and the negative

impact on financial viability.

These options are summarised in the opposite table. The

following information was then developed for each option:

• Capital cost estimates

• Revenue projections

• Funding and affordability

• Concept Sketch Plans (Appendix 4).

A summary of the findings is contained in the following

sections.

28

Option 1 Option 2 Option 3 Option 4

Activity Areas

8 Lane Pool -

No Leisure Water

8 Lane Pool -

With Leisure Water

6 Lane Pool -

No Leisure Water

6 Lane Pool -

With Leisure Water

6 Lane 25m pool X X

8 lane 25 metre pool (17m x

25m) to ASA County

standard (full disabled

access)

X X

Spectator seating for 240

peopleX X X X

Learner pool with moveable

floor (full disabled access)X X X X

120 station health and

fitness; includes weights

area

X X X X

Dance/fitness studios; 2 x 30

person & storageX X X X

Leisure water area (one

flume/feature)*X X

Initial Capital Cost Estimates

29

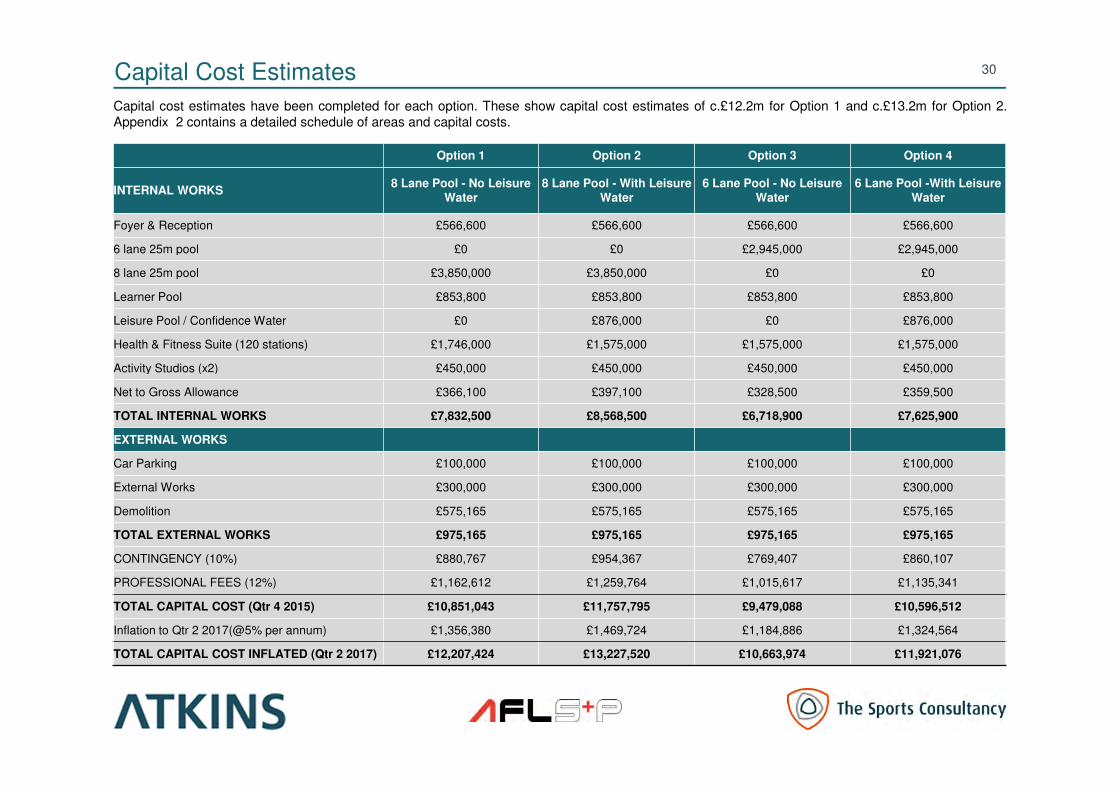

Capital Cost Estimates

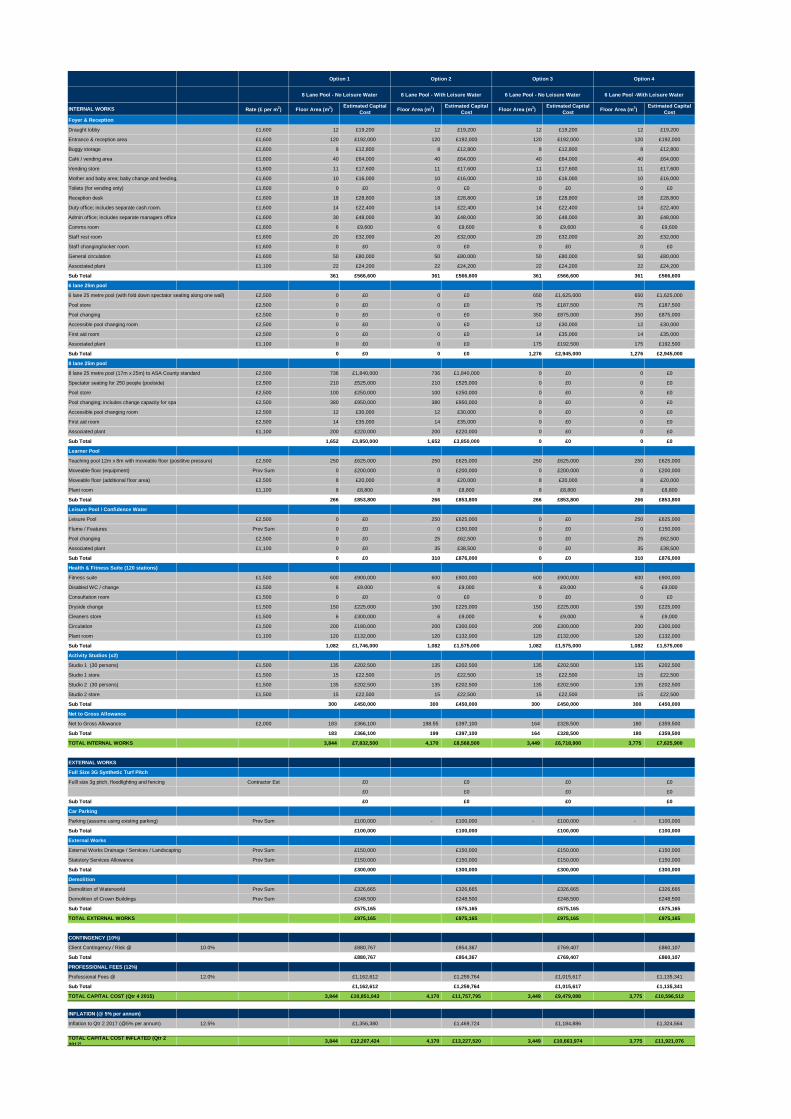

Capital cost estimates have been completed for each option. These show capital cost estimates of c.£12.2m for Option 1 and c.£13.2m for Option 2.

Appendix 2 contains a detailed schedule of areas and capital costs.

30

Option 1 Option 2 Option 3 Option 4

INTERNAL WORKS8 Lane Pool - No Leisure

Water

8 Lane Pool - With Leisure

Water

6 Lane Pool - No Leisure

Water

6 Lane Pool -With Leisure

Water

Foyer & Reception £566,600 £566,600 £566,600 £566,600

6 lane 25m pool £0 £0 £2,945,000 £2,945,000

8 lane 25m pool £3,850,000 £3,850,000 £0 £0

Learner Pool £853,800 £853,800 £853,800 £853,800

Leisure Pool / Confidence Water £0 £876,000 £0 £876,000

Health & Fitness Suite (120 stations) £1,746,000 £1,575,000 £1,575,000 £1,575,000

Activity Studios (x2) £450,000 £450,000 £450,000 £450,000

Net to Gross Allowance £366,100 £397,100 £328,500 £359,500

TOTAL INTERNAL WORKS £7,832,500 £8,568,500 £6,718,900 £7,625,900

EXTERNAL WORKS

Car Parking £100,000 £100,000 £100,000 £100,000

External Works £300,000 £300,000 £300,000 £300,000

Demolition £575,165 £575,165 £575,165 £575,165

TOTAL EXTERNAL WORKS £975,165 £975,165 £975,165 £975,165

CONTINGENCY (10%) £880,767 £954,367 £769,407 £860,107

PROFESSIONAL FEES (12%) £1,162,612 £1,259,764 £1,015,617 £1,135,341

TOTAL CAPITAL COST (Qtr 4 2015) £10,851,043 £11,757,795 £9,479,088 £10,596,512

Inflation to Qtr 2 2017(@5% per annum) £1,356,380 £1,469,724 £1,184,886 £1,324,564

TOTAL CAPITAL COST INFLATED (Qtr 2 2017) £12,207,424 £13,227,520 £10,663,974 £11,921,076

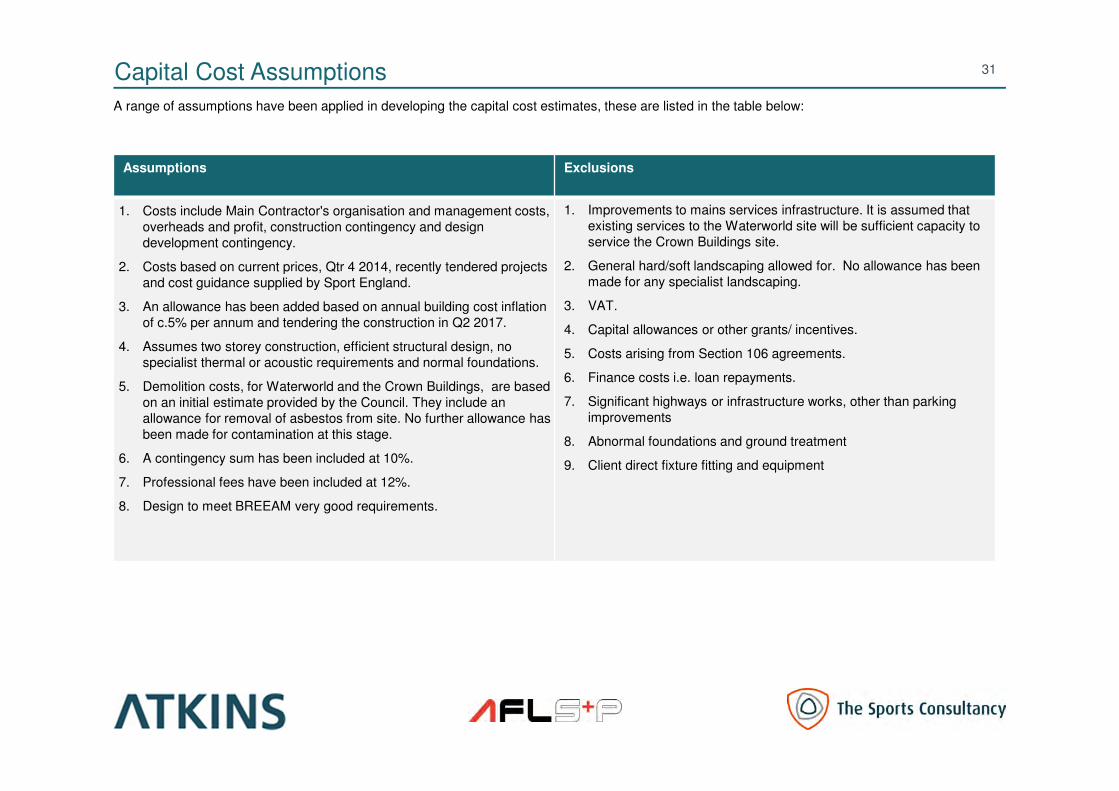

Capital Cost Assumptions

A range of assumptions have been applied in developing the capital cost estimates, these are listed in the table below:

31

Assumptions Exclusions

1. Costs include Main Contractor's organisation and management costs,

overheads and profit, construction contingency and design

development contingency.

2. Costs based on current prices, Qtr 4 2014, recently tendered projects

and cost guidance supplied by Sport England.

3. An allowance has been added based on annual building cost inflation

of c.5% per annum and tendering the construction in Q2 2017.

4. Assumes two storey construction, efficient structural design, no

specialist thermal or acoustic requirements and normal foundations.

5. Demolition costs, for Waterworld and the Crown Buildings, are based

on an initial estimate provided by the Council. They include an

allowance for removal of asbestos from site. No further allowance has

been made for contamination at this stage.

6. A contingency sum has been included at 10%.

7. Professional fees have been included at 12%.

8. Design to meet BREEAM very good requirements.

1. Improvements to mains services infrastructure. It is assumed that

existing services to the Waterworld site will be sufficient capacity to

service the Crown Buildings site.

2. General hard/soft landscaping allowed for. No allowance has been

made for any specialist landscaping.

3. VAT.

4. Capital allowances or other grants/ incentives.

5. Costs arising from Section 106 agreements.

6. Finance costs i.e. loan repayments.

7. Significant highways or infrastructure works, other than parking

improvements

8. Abnormal foundations and ground treatment

9. Client direct fixture fitting and equipment

Revenue Projections

32

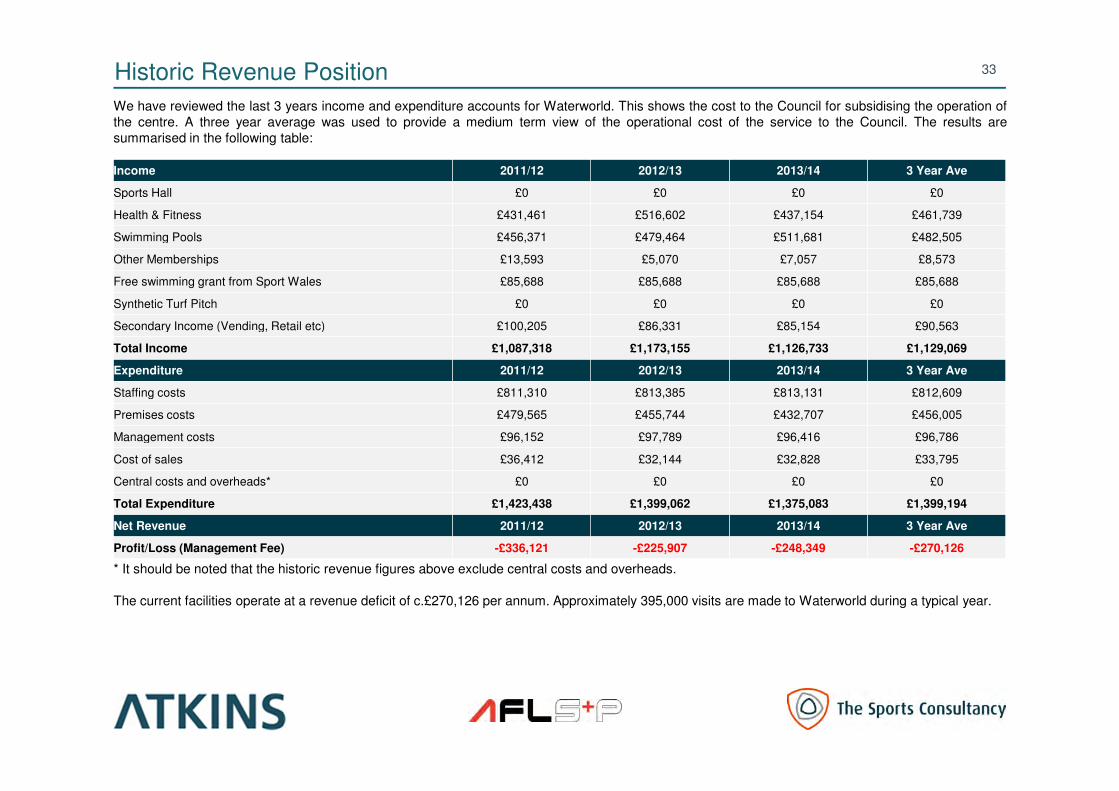

Historic Revenue Position

We have reviewed the last 3 years income and expenditure accounts for Waterworld. This shows the cost to the Council for subsidising the operation of

the centre. A three year average was used to provide a medium term view of the operational cost of the service to the Council. The results are

summarised in the following table:

* It should be noted that the historic revenue figures above exclude central costs and overheads.

The current facilities operate at a revenue deficit of c.£270,126 per annum. Approximately 395,000 visits are made to Waterworld during a typical year.

33

Income 2011/12 2012/13 2013/14 3 Year Ave

Sports Hall £0 £0 £0 £0

Health & Fitness £431,461 £516,602 £437,154 £461,739

Swimming Pools £456,371 £479,464 £511,681 £482,505

Other Memberships £13,593 £5,070 £7,057 £8,573

Free swimming grant from Sport Wales £85,688 £85,688 £85,688 £85,688

Synthetic Turf Pitch £0 £0 £0 £0

Secondary Income (Vending, Retail etc) £100,205 £86,331 £85,154 £90,563

Total Income £1,087,318 £1,173,155 £1,126,733 £1,129,069

Expenditure 2011/12 2012/13 2013/14 3 Year Ave

Staffing costs £811,310 £813,385 £813,131 £812,609

Premises costs £479,565 £455,744 £432,707 £456,005

Management costs £96,152 £97,789 £96,416 £96,786

Cost of sales £36,412 £32,144 £32,828 £33,795

Central costs and overheads* £0 £0 £0 £0

Total Expenditure £1,423,438 £1,399,062 £1,375,083 £1,399,194

Net Revenue 2011/12 2012/13 2013/14 3 Year Ave

Profit/Loss (Management Fee) -£336,121 -£225,907 -£248,349 -£270,126

Revenue Projections (10-Year Average)

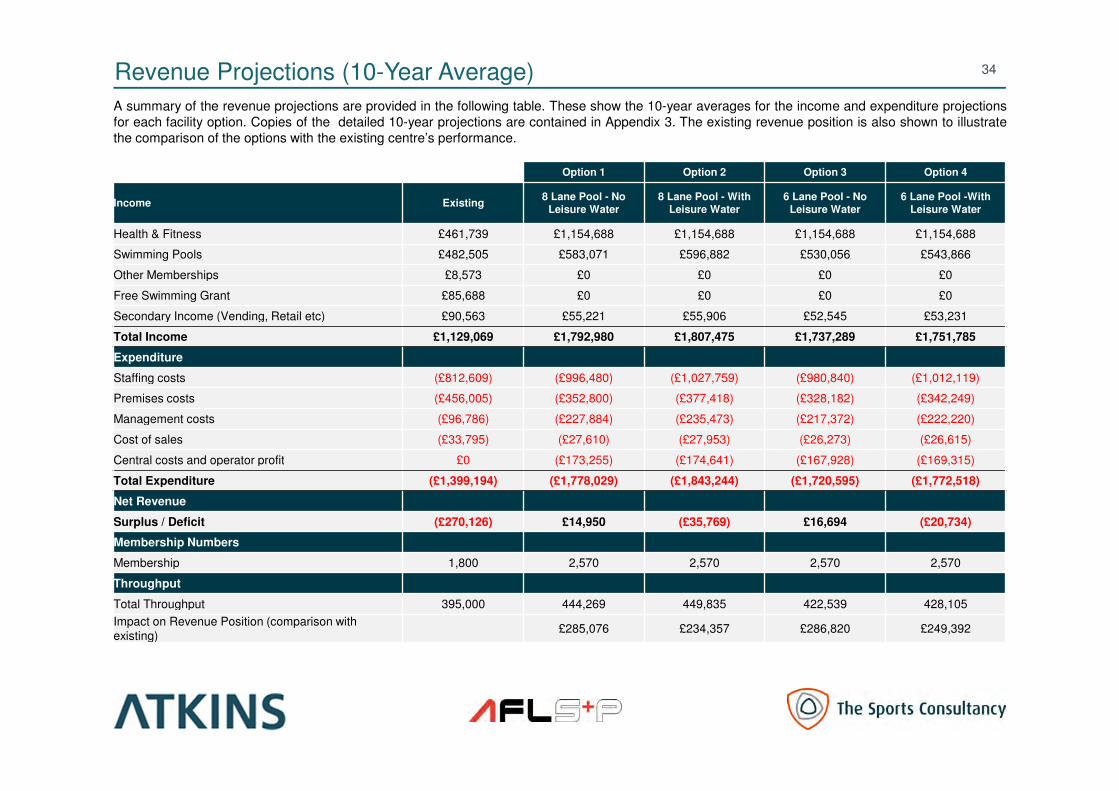

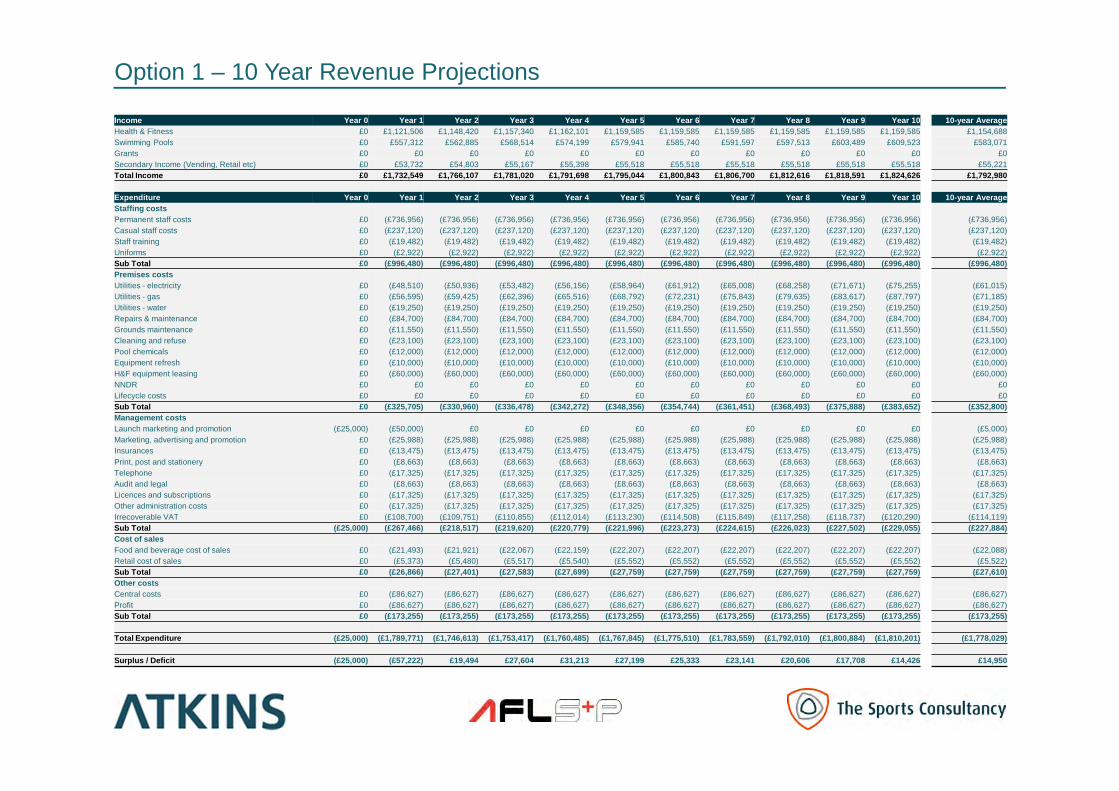

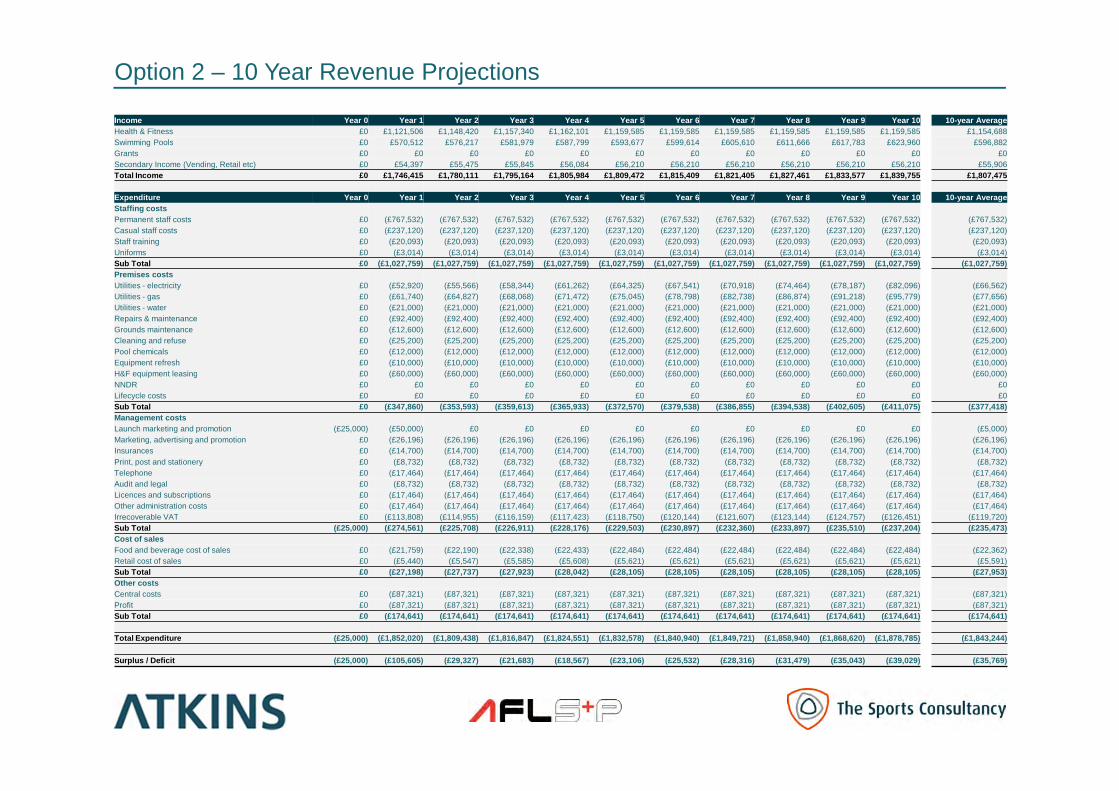

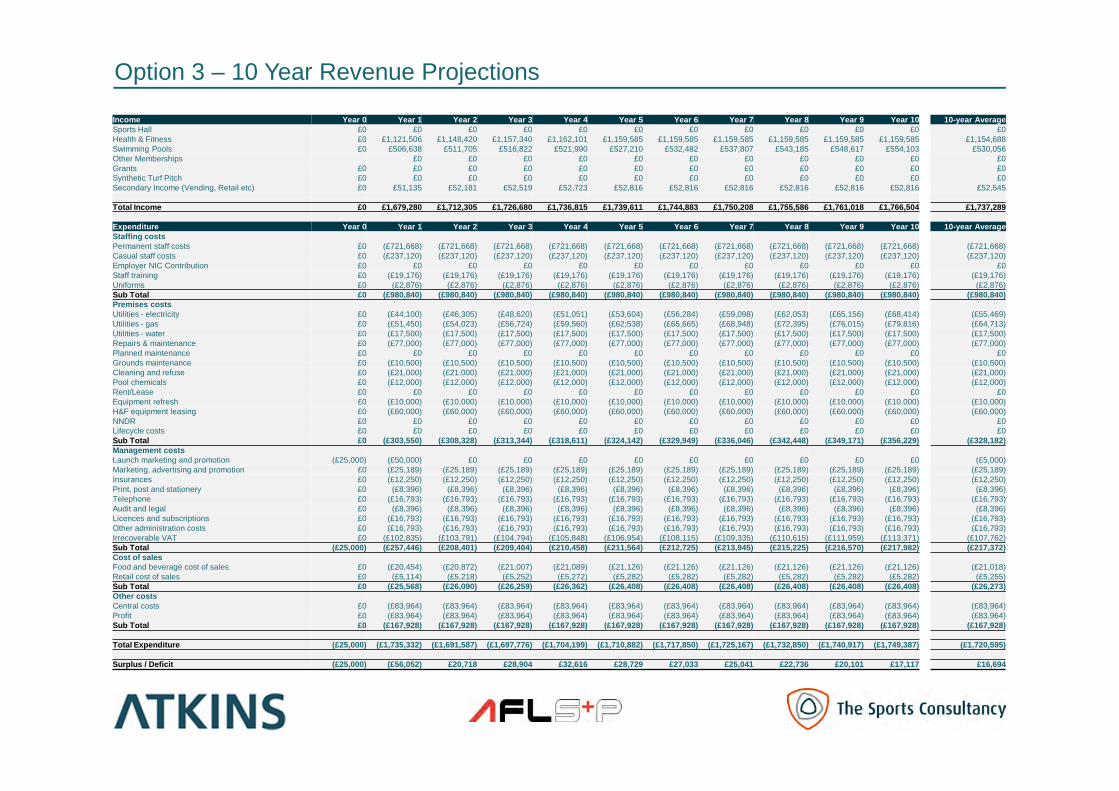

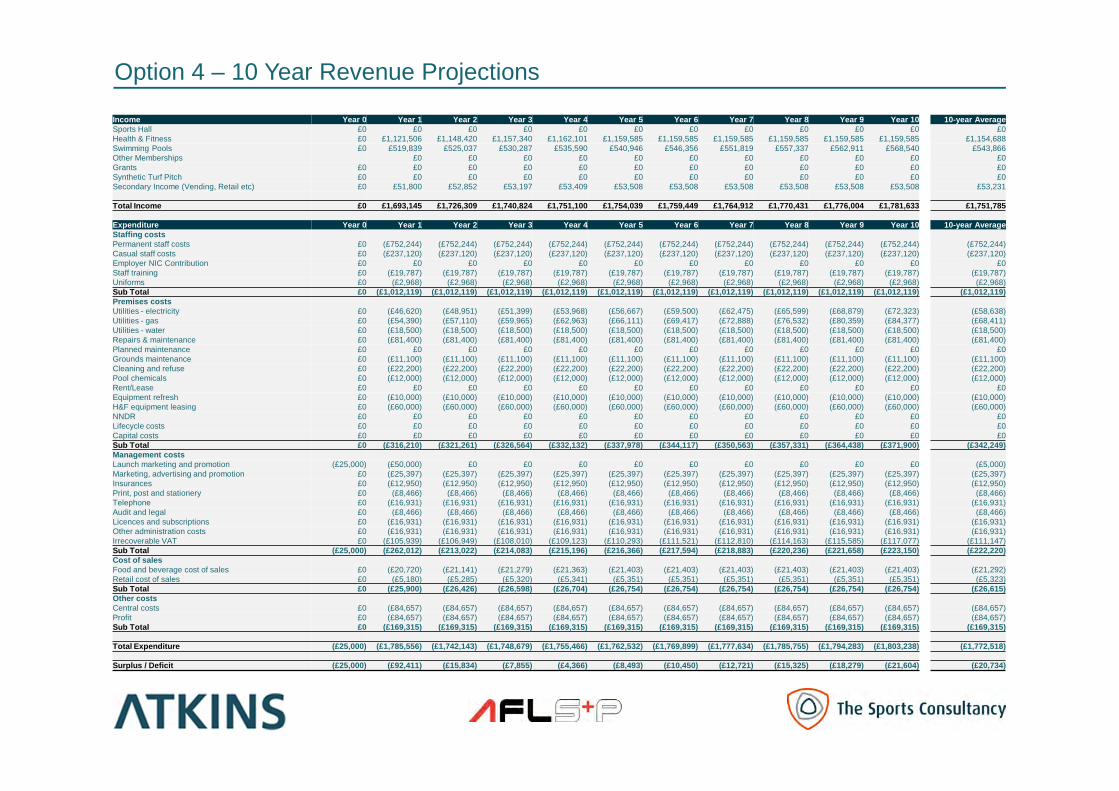

A summary of the revenue projections are provided in the following table. These show the 10-year averages for the income and expenditure projections

for each facility option. Copies of the detailed 10-year projections are contained in Appendix 3. The existing revenue position is also shown to illustrate

the comparison of the options with the existing centre’s performance.

34

Option 1 Option 2 Option 3 Option 4

Income Existing8 Lane Pool - No

Leisure Water8 Lane Pool - With

Leisure Water6 Lane Pool - No

Leisure Water6 Lane Pool -With

Leisure Water

Health & Fitness £461,739 £1,154,688 £1,154,688 £1,154,688 £1,154,688

Swimming Pools £482,505 £583,071 £596,882 £530,056 £543,866

Other Memberships £8,573 £0 £0 £0 £0

Free Swimming Grant £85,688 £0 £0 £0 £0

Secondary Income (Vending, Retail etc) £90,563 £55,221 £55,906 £52,545 £53,231

Total Income £1,129,069 £1,792,980 £1,807,475 £1,737,289 £1,751,785

Expenditure

Staffing costs (£812,609) (£996,480) (£1,027,759) (£980,840) (£1,012,119)

Premises costs (£456,005) (£352,800) (£377,418) (£328,182) (£342,249)

Management costs (£96,786) (£227,884) (£235,473) (£217,372) (£222,220)

Cost of sales (£33,795) (£27,610) (£27,953) (£26,273) (£26,615)

Central costs and operator profit £0 (£173,255) (£174,641) (£167,928) (£169,315)

Total Expenditure (£1,399,194) (£1,778,029) (£1,843,244) (£1,720,595) (£1,772,518)

Net Revenue

Surplus / Deficit (£270,126) £14,950 (£35,769) £16,694 (£20,734)

Membership Numbers

Membership 1,800 2,570 2,570 2,570 2,570

Throughput

Total Throughput 395,000 444,269 449,835 422,539 428,105

Impact on Revenue Position (comparison with

existing)£285,076 £234,357 £286,820 £249,392

Assumptions Applied in the Revenue Projections

To support the capital cost estimation, and to provide the Council with an understanding of the long-term financial implications of the new centre, 10-year

revenue projections were developed. The projections are based on The Sports Consultancy’s benchmark model, which generates the required outputs

through performance indicators from our Operational Database. This contains over 700 records of financial and throughput information from over 300

operational leisure facilities across the United Kingdom. As such, it is a ‘high-level’ model which depends on results from other, similar facilities, rather

than specific programmes of usage and local pricing. The database generates a range of benchmark levels (e.g. mean, upper quartile, lower quartile)

and in choosing the benchmarks to use, it is important to consider the specific local context and current facility performance. For this study we applied

the upper quartile data, as this will be a new facility in an area with significant existing and potential demand. We have also reviewed historic income

and expenditure data for the existing facilities at Waterworld to provide a local perspective.

The following approach was adopted in selecting the benchmarks:

• Income - this took into account the performance of the existing centre, the fact that the new centre will be designed to a higher specification than is

currently the case and the need for the business plan to be relatively prudent

• Expenditure - this took into account the expenditure levels at the existing centre and the fact that the facilities will be new and more efficient than the

existing one

• Throughput - this took into account the throughput levels at the existing centre and the likely increase due to the opening of a new facility.

The operational analysis includes a number of key expenditure areas, which are listed below:

• Staffing costs - based on an appropriate staffing structure and costs for similar facilities

• Utilities - based on benchmark rates for similar new wet and dry leisure facilities

• Repairs and maintenance - based on benchmark rates for similar facilities

• Rates (NNDR) - it is assumed that a trust operator will benefit from 100% rate relief, although it should be noted that 20% of this is discretionary relief

• Cleaning - based on benchmark rates for similar facilities

• Insurances - based on benchmark rates for similar facilities

• Cost of sales - based on benchmark rates for similar facilities

• Operator profit - at 5% of income at year 1

• Overheads and central costs - at 5% of income at year 1

• Full price health and fitness membership at £35 per month, with an average of 2,570 members over 10 years.

Lifecycle costs, for the periodic refurbishment and replacement of facilities, have been excluded from the revenue projections at this stage. This is to

allow a like for like comparison with the existing revenue position, which does not include an allowance for these costs. However, lifecycle costs should

be considered going forward to ensure the facilities are kept in good condition and that income does not diminish over time, due to deteriorating facilities.

A typical allowance equal to 1.6% of the build costs (excluding fees and contingencies) should be allowed for on an annual basis.

35

Funding & Affordability

36

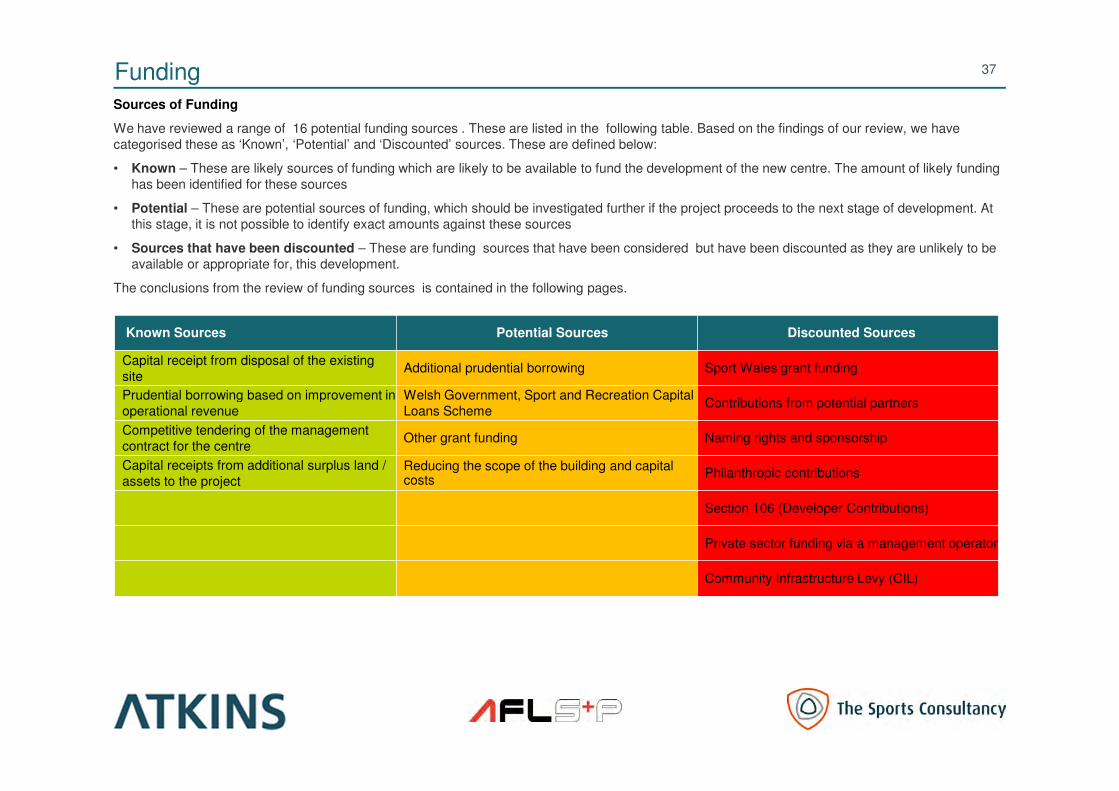

Funding

Sources of Funding

We have reviewed a range of 16 potential funding sources . These are listed in the following table. Based on the findings of our review, we have

categorised these as ‘Known’, ‘Potential’ and ‘Discounted’ sources. These are defined below:

• Known – These are likely sources of funding which are likely to be available to fund the development of the new centre. The amount of likely funding

has been identified for these sources

• Potential – These are potential sources of funding, which should be investigated further if the project proceeds to the next stage of development. At

this stage, it is not possible to identify exact amounts against these sources

• Sources that have been discounted – These are funding sources that have been considered but have been discounted as they are unlikely to be

available or appropriate for, this development.

The conclusions from the review of funding sources is contained in the following pages.

37

Known Sources Potential Sources Discounted Sources

Capital receipt from disposal of the existing

siteAdditional prudential borrowing Sport Wales grant funding

Prudential borrowing based on improvement in

operational revenue

Welsh Government, Sport and Recreation Capital

Loans SchemeContributions from potential partners

Competitive tendering of the management

contract for the centreOther grant funding Naming rights and sponsorship

Capital receipts from additional surplus land /

assets to the projectReducing the scope of the building and capital costs

Philanthropic contributions

Section 106 (Developer Contributions)

Private sector funding via a management operator

Community Infrastructure Levy (CIL)

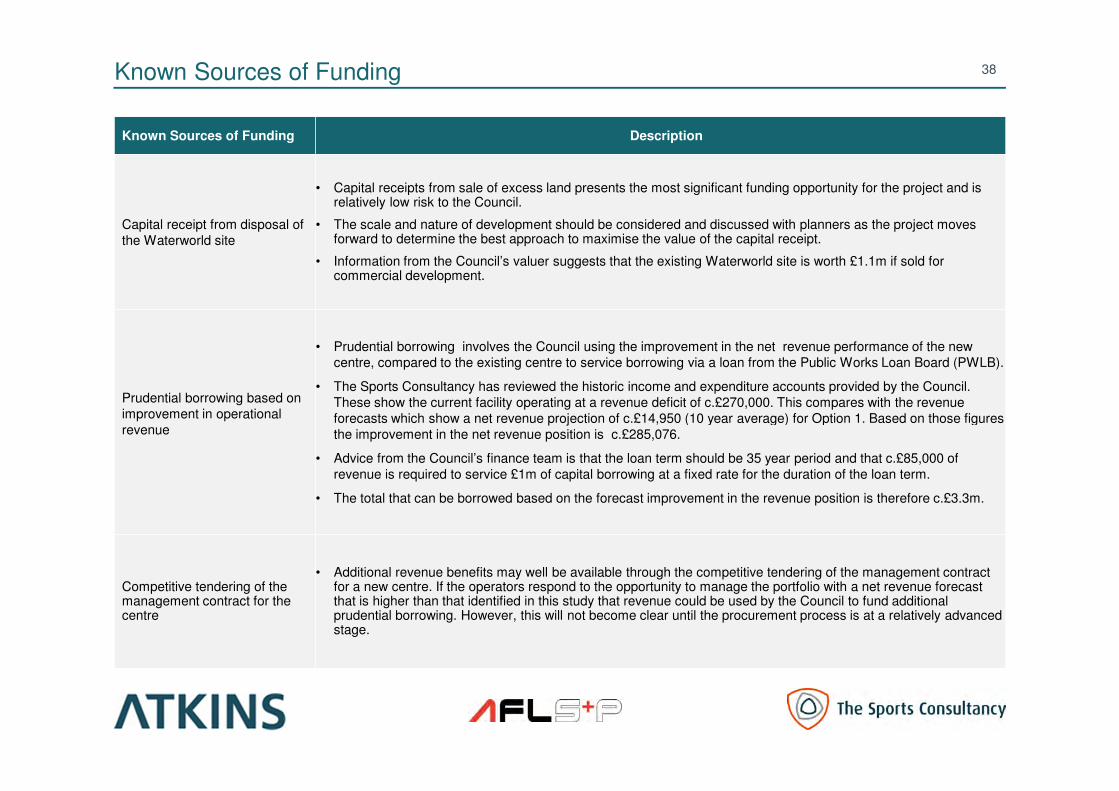

Known Sources of Funding 38

Known Sources of Funding Description

Capital receipt from disposal of

the Waterworld site

• Capital receipts from sale of excess land presents the most significant funding opportunity for the project and is relatively low risk to the Council.

• The scale and nature of development should be considered and discussed with planners as the project moves forward to determine the best approach to maximise the value of the capital receipt.

• Information from the Council’s valuer suggests that the existing Waterworld site is worth £1.1m if sold for commercial development.

Prudential borrowing based on

improvement in operational

revenue

• Prudential borrowing involves the Council using the improvement in the net revenue performance of the new

centre, compared to the existing centre to service borrowing via a loan from the Public Works Loan Board (PWLB).

• The Sports Consultancy has reviewed the historic income and expenditure accounts provided by the Council.

These show the current facility operating at a revenue deficit of c.£270,000. This compares with the revenue

forecasts which show a net revenue projection of c.£14,950 (10 year average) for Option 1. Based on those figures

the improvement in the net revenue position is c.£285,076.

• Advice from the Council’s finance team is that the loan term should be 35 year period and that c.£85,000 of

revenue is required to service £1m of capital borrowing at a fixed rate for the duration of the loan term.

• The total that can be borrowed based on the forecast improvement in the revenue position is therefore c.£3.3m.

Competitive tendering of the management contract for the centre

• Additional revenue benefits may well be available through the competitive tendering of the management contract for a new centre. If the operators respond to the opportunity to manage the portfolio with a net revenue forecast that is higher than that identified in this study that revenue could be used by the Council to fund additional prudential borrowing. However, this will not become clear until the procurement process is at a relatively advanced stage.

Potential Sources of Funding 39

Potential Sources Description

Additional prudential borrowing• The Council could borrow additional funding via the Public Works Loan Board to contribute towards the funding

shortfall. It would need to fund c.£85k revenue per annum to borrow each additional £1m, based on a 35 year loan term.

Welsh Government, Sport and

Recreation Capital Loans

Scheme (subject to the project

meeting the funding criteria).

• The Welsh Government has announced that it will shortly launch an interest free loan scheme aimed at helping local authorities fund capital projects aimed at increasing participation in sport and physical activity. It is not yet clear what the funding priorities and criteria are. The total amount of funding available for distribution is understood to be £5m.

Other grant funding• We are not aware of any other significant grant funding opportunities for a project of this type in this location.

However, there may be relatively small amounts available from local grant funding trust or foundations.

Reducing the scope of the building and capital costs

• Reducing the scale and scope of the building is an option for the Council and it could help reduce the funding gap. However, any departure from the agreed specification would diminish ability of the Council to meet the sporting needs of the local community and the needs of other stakeholder organisations.

• We recognise that the preferred option for the Council includes an 8 lane 25m pool. The only further reduction in the scope is providing a 6 lane pool as opposed to the 8 lane pool. This is unlikely to be acceptable to the Council and partners. However, it may need to be considered if the funding gap cannot be covered by funding from other sources.

Contribute receipts from additional surplus land / assets to the project

• Many recent community leisure developments have been facilitated by rationalisation of facilities across a portfolio (leisure and other facilities). This has helped unlock capital receipts and revenue savings that have been used to finance borrowing costs.

• The Council should consider whether there are any further opportunities to dispose of assets to contribute towards the shortfall for the replacement of Waterworld.

• It is noted that the recommendations of the Options Evaluation Study included using the revenue saving the withdrawal from Plas Madoc to help fully fund the replacement of Waterworld. However, this revenue saving is not now available to contribute towards the new leisure centre.

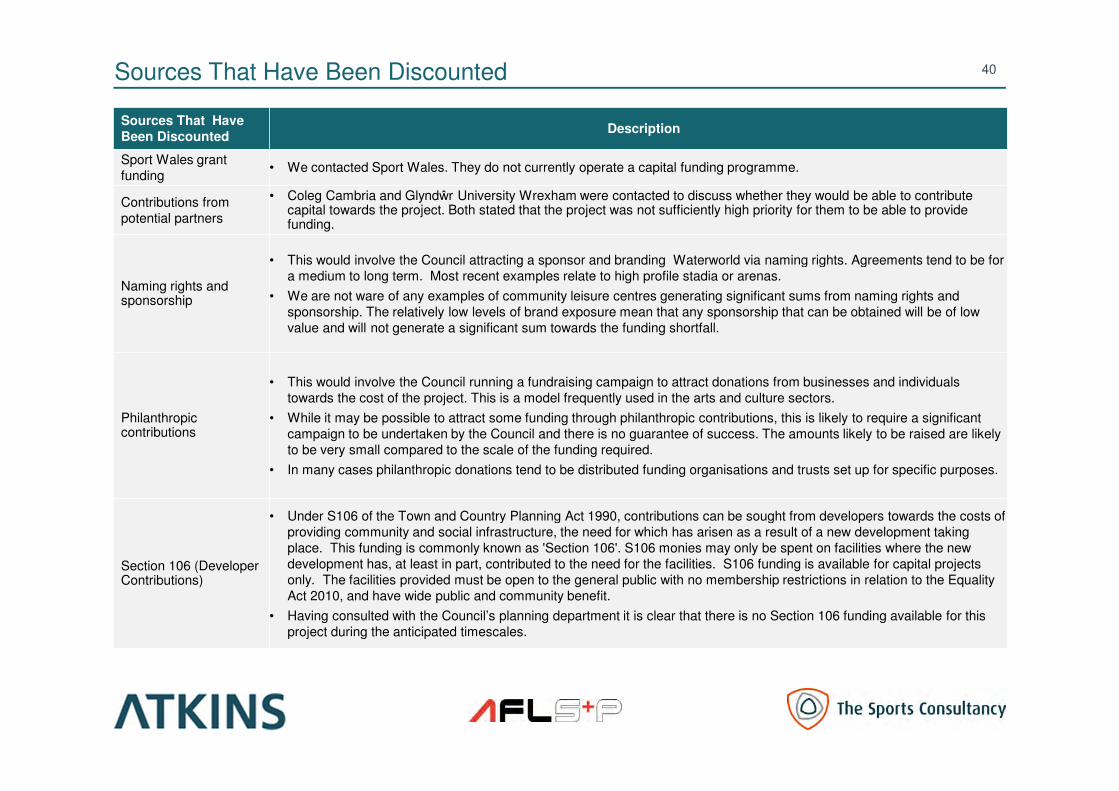

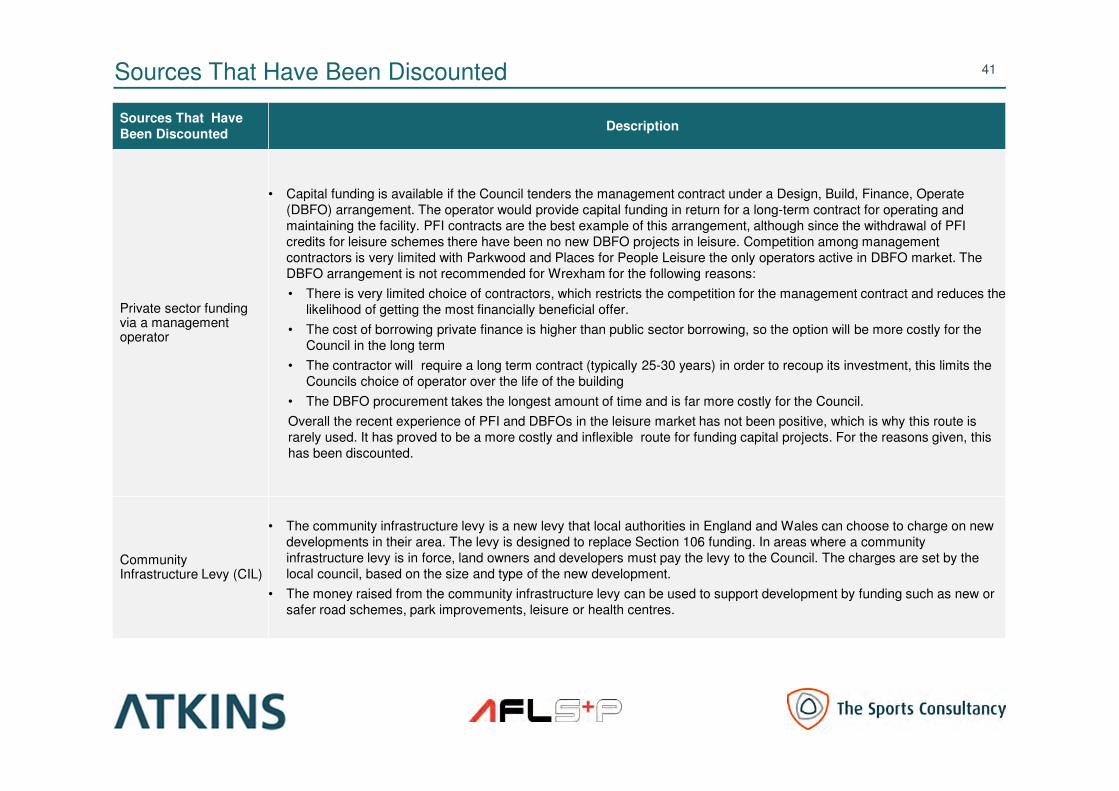

Sources That Have Been Discounted 40

Sources That Have

Been DiscountedDescription

Sport Wales grant

funding• We contacted Sport Wales. They do not currently operate a capital funding programme.

Contributions from

potential partners

• Coleg Cambria and Glyndŵr University Wrexham were contacted to discuss whether they would be able to contribute capital towards the project. Both stated that the project was not sufficiently high priority for them to be able to provide funding.

Naming rights and sponsorship

• This would involve the Council attracting a sponsor and branding Waterworld via naming rights. Agreements tend to be for

a medium to long term. Most recent examples relate to high profile stadia or arenas.

• We are not ware of any examples of community leisure centres generating significant sums from naming rights and

sponsorship. The relatively low levels of brand exposure mean that any sponsorship that can be obtained will be of low

value and will not generate a significant sum towards the funding shortfall.

Philanthropic contributions

• This would involve the Council running a fundraising campaign to attract donations from businesses and individuals

towards the cost of the project. This is a model frequently used in the arts and culture sectors.

• While it may be possible to attract some funding through philanthropic contributions, this is likely to require a significant

campaign to be undertaken by the Council and there is no guarantee of success. The amounts likely to be raised are likely

to be very small compared to the scale of the funding required.

• In many cases philanthropic donations tend to be distributed funding organisations and trusts set up for specific purposes.

Section 106 (Developer Contributions)

• Under S106 of the Town and Country Planning Act 1990, contributions can be sought from developers towards the costs of

providing community and social infrastructure, the need for which has arisen as a result of a new development taking

place. This funding is commonly known as 'Section 106'. S106 monies may only be spent on facilities where the new

development has, at least in part, contributed to the need for the facilities. S106 funding is available for capital projects

only. The facilities provided must be open to the general public with no membership restrictions in relation to the Equality

Act 2010, and have wide public and community benefit.

• Having consulted with the Council’s planning department it is clear that there is no Section 106 funding available for this

project during the anticipated timescales.

Sources That Have Been Discounted 41

Sources That Have

Been DiscountedDescription

Private sector funding via a management operator

• Capital funding is available if the Council tenders the management contract under a Design, Build, Finance, Operate

(DBFO) arrangement. The operator would provide capital funding in return for a long-term contract for operating and

maintaining the facility. PFI contracts are the best example of this arrangement, although since the withdrawal of PFI

credits for leisure schemes there have been no new DBFO projects in leisure. Competition among management

contractors is very limited with Parkwood and Places for People Leisure the only operators active in DBFO market. The

DBFO arrangement is not recommended for Wrexham for the following reasons:

• There is very limited choice of contractors, which restricts the competition for the management contract and reduces the

likelihood of getting the most financially beneficial offer.

• The cost of borrowing private finance is higher than public sector borrowing, so the option will be more costly for the

Council in the long term

• The contractor will require a long term contract (typically 25-30 years) in order to recoup its investment, this limits the

Councils choice of operator over the life of the building

• The DBFO procurement takes the longest amount of time and is far more costly for the Council.

Overall the recent experience of PFI and DBFOs in the leisure market has not been positive, which is why this route is

rarely used. It has proved to be a more costly and inflexible route for funding capital projects. For the reasons given, this

has been discounted.

Community Infrastructure Levy (CIL)

• The community infrastructure levy is a new levy that local authorities in England and Wales can choose to charge on new

developments in their area. The levy is designed to replace Section 106 funding. In areas where a community

infrastructure levy is in force, land owners and developers must pay the levy to the Council. The charges are set by the

local council, based on the size and type of the new development.

• The money raised from the community infrastructure levy can be used to support development by funding such as new or

safer road schemes, park improvements, leisure or health centres.

Summary of Funding Options 42

Summary of Findings