Embed Size (px)

Citation preview

Level 5, 2 Bligh Street Sydney NSW 2000 Australia Tel: +61-2-8252-9223 Fax+61-2-9475-5435

www.pilbaraminerals.com.au

ACN 112-425-788 ASX ANNOUCEMENT 18th February 2014

FEASIBILITY STUDY RESULTS - TABBA TABBA TANTALUM PROJECT

ROBUST AND VIABLE WITH LOW CAPITAL AND MINING COSTS

KEY FINANCIAL HIGHLIGHTS OF FEASIBILITY STUDY:

Project Revenue $30.2M

EBITDA $16M with Project NPV of $14.4M at an IRR of 162%.

Capital Cost of $3.9M ($1.5M already spent, plant capital items already 90% completed).

Life-of-mine (LOM) off-take agreement in place with world-leading tantalum producer, Global Advanced Metals Wodgina Pty Ltd (GAMW).

First full year production (2014-15) operating costs forecast at $34.74/lb.

PROJECT HIGHLIGHTS:

Maiden JORC Ore Reserve of 133,000 tonnes at 1,290ppm Ta2O5.

Total LOM production of 364,000 lbs of Ta2O5.

Production of 256,000 lbs of Ta2O5 in first full year of operations.

All government approvals necessary to commence production are well advanced, and Pilbara Minerals and its Joint Venture partner Nagrom intend to fast-track construction subject to completion of financing.

FUTURE GROWTH OPPORTUNITIES:

The Tabba Tabba orebodies are open along strike and at depth – upside exists for the identification of further resources within and adjacent to the immediate pit area.

Plant throughput rate is based on conservative assumptions.

Additional production potential from processing lower grade stockpiles, or through the development of the nearby Strelley Project also secured under the Pilbara Minerals/Nagrom JV.

ASX Release cont. Page | 2

Page 2

Pilbara Minerals Ltd (ASX: PLS) is pleased to announce that it has completed its Feasibility Study on the advanced Tabba Tabba Tantalum Project, located 84km by road from Port Hedland in Western Australia, with the results demonstrating robust project viability through low capital and mining costs. The successful completion of the Feasibility Study puts Pilbara Minerals on track to join the ranks of junior miners, with first production forecast for the third quarter of CY 2014 subject to project funding.

The Feasibility Study has defined an initial mine life of 19 months producing approximately 365,000 pounds (lbs) of tantalum pentoxide (Ta2O5), within a minimum 5% Ta2O5 concentrate, delivering EBITDA (earnings before interest, tax, depreciation and amortisation) of $16 million.

Pilbara Minerals Executive and Chief Geologist John Young said “The completion of the Feasibility Study is a significant milestone, with the positive results clearly demonstrating that the Tabba Tabba Project’s high grade and quality concentrate will deliver a technically and financially robust project.” “Based on the results of the Study, Pilbara Minerals and its Joint Venture partner, Nagrom, intend to fast-track the development of the Tabba Tabba Project, subject to the completion of project financing. Tabba Tabba will deliver a steady source of cash flow for at least the next two to three years, with potential for future growth from a number of sources, including the development of the nearby Strelley Project,” Mr Young said. Pilbara Minerals entered into a 50/50 joint venture agreement with Nagrom in October 2013 to evaluate, develop and mine the Tabba Tabba Project. Nagrom are world renowned metallurgical and gravity processing specialists. Pilbara and Nagrom intend to develop a boutique open cut mining and processing operation capable of generating attractive cash flows and returns for a small capital outlay. The Tabba Tabba Project, acquired from world-leading global tantalum producer, Global Advanced Metals Wodgina Pty Ltd (GAMW), will be developed under a five-year mining and off-take agreement with GAMW, providing price certainty and underpinning the development. Feasibility Study Summary The Feasibility Study (FS) proposes mining and processing 118,000 tonnes of ore per annum from a single pit at the Tabba Tabba Project. The study incorporates the development of the site infrastructure, mining, processing facility and rehabilitation. The FS establishes a robust financial model, with projected payback of the entire capital cost in month six of operations. It estimates that over the LOM, 364,000lbs of Ta2O5 will be recovered at an average operating cost of $34.74/lb. The financial results reported are based on a commercially sensitive 5-year fixed sales price with Global Advanced Metals Wodgina Pty Ltd (GAMW), subject to annual CPI adjustments. Total EBITDA is estimated to be $16 million with an estimated Net Present Value (NPV) of $14.4 million over the initial mine life of 19 months. The pre-start-up capital cost is estimated at $3.9 million, of which approximately $1.5 million has been spent to date. The FS was compiled and completed by Pilbara Minerals, Nagrom Pty Ltd with input from a number of industry consultants. Nagrom completed the metallurgy, process design and the various infrastructure requirements. Resource work was completed by Mitchell River Group Pty Ltd. Life of Mine (LOM) planning and reserve was completed by Croeser Pty Ltd and supported by Dempers and Seymour for the Geotechnical work. A full list of consultants is listed later in this announcement.

ASX Release cont. Page | 3

Page 3

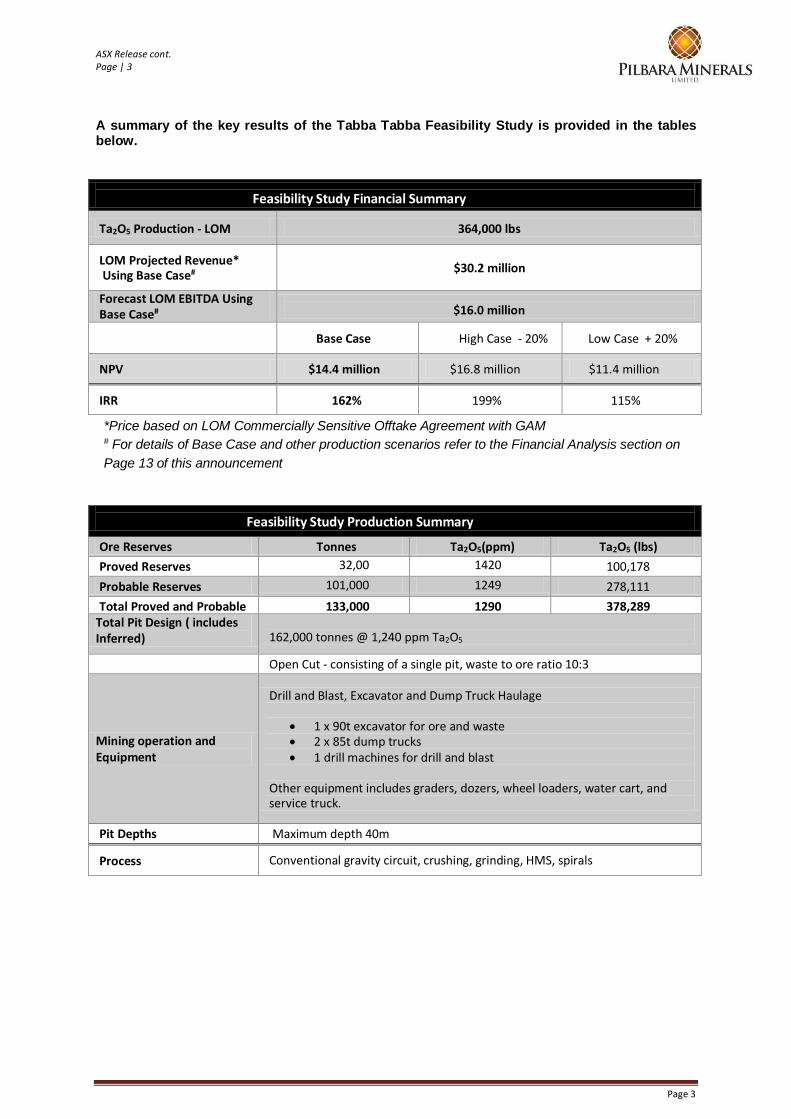

A summary of the key results of the Tabba Tabba Feasibility Study is provided in the tables below.

Feasibility Study Financial Summary

Ta2O5 Production - LOM 364,000 lbs

LOM Projected Revenue* Using Base Case#

$30.2 million

Forecast LOM EBITDA Using Base Case#

$16.0 million

Base Case High Case - 20% Low Case + 20%

NPV $14.4 million $16.8 million $11.4 million

IRR 162% 199% 115%

*Price based on LOM Commercially Sensitive Offtake Agreement with GAM # For details of Base Case and other production scenarios refer to the Financial Analysis section on

Page 13 of this announcement

Feasibility Study Production Summary

Ore Reserves Tonnes Ta2O5(ppm) Ta2O5 (lbs)

Proved Reserves 32,00 1420 100,178

Probable Reserves 101,000 1249 278,111

Total Proved and Probable 133,000 1290 378,289 Total Pit Design ( includes Inferred)

162,000 tonnes @ 1,240 ppm Ta2O5

Open Cut - consisting of a single pit, waste to ore ratio 10:3

Mining operation and Equipment

Drill and Blast, Excavator and Dump Truck Haulage

1 x 90t excavator for ore and waste 2 x 85t dump trucks 1 drill machines for drill and blast

Other equipment includes graders, dozers, wheel loaders, water cart, and service truck.

Pit Depths Maximum depth 40m Process Conventional gravity circuit, crushing, grinding, HMS, spirals

ASX Release cont. Page | 4

Page 4

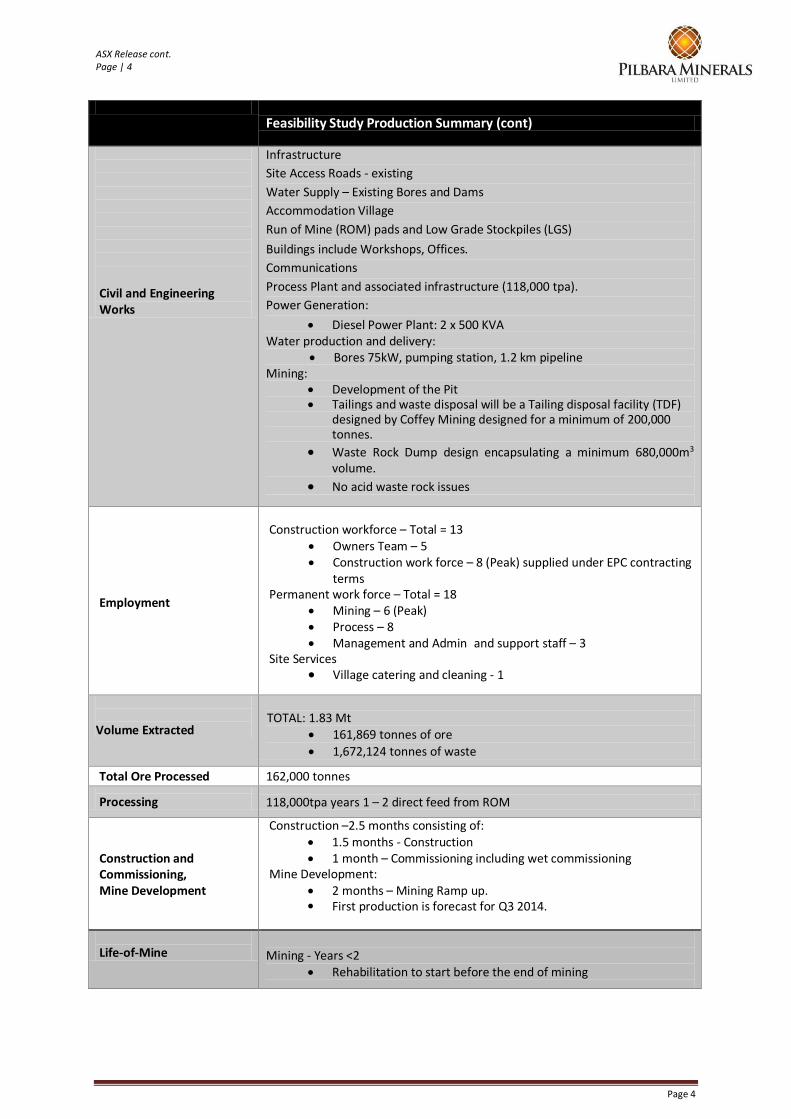

Feasibility Study Production Summary (cont)

Civil and Engineering Works

Infrastructure

Site Access Roads - existing

Water Supply – Existing Bores and Dams

Accommodation Village

Run of Mine (ROM) pads and Low Grade Stockpiles (LGS)

Buildings include Workshops, Offices.

Communications

Process Plant and associated infrastructure (118,000 tpa).

Power Generation:

Diesel Power Plant: 2 x 500 KVA Water production and delivery:

Bores 75kW, pumping station, 1.2 km pipeline Mining:

Development of the Pit Tailings and waste disposal will be a Tailing disposal facility (TDF)

designed by Coffey Mining designed for a minimum of 200,000 tonnes.

Waste Rock Dump design encapsulating a minimum 680,000m3 volume.

No acid waste rock issues

Employment

Construction workforce – Total = 13

Owners Team – 5 Construction work force – 8 (Peak) supplied under EPC contracting

terms Permanent work force – Total = 18

Mining – 6 (Peak) Process – 8 Management and Admin and support staff – 3

Site Services Village catering and cleaning - 1

Volume Extracted

TOTAL: 1.83 Mt

161,869 tonnes of ore

1,672,124 tonnes of waste

Total Ore Processed 162,000 tonnes Processing 118,000tpa years 1 – 2 direct feed from ROM

Construction and Commissioning, Mine Development

Construction –2.5 months consisting of: 1.5 months - Construction 1 month – Commissioning including wet commissioning

Mine Development: 2 months – Mining Ramp up. First production is forecast for Q3 2014.

Life-of-Mine

Mining - Years <2

Rehabilitation to start before the end of mining

ASX Release cont. Page | 5

Page 5

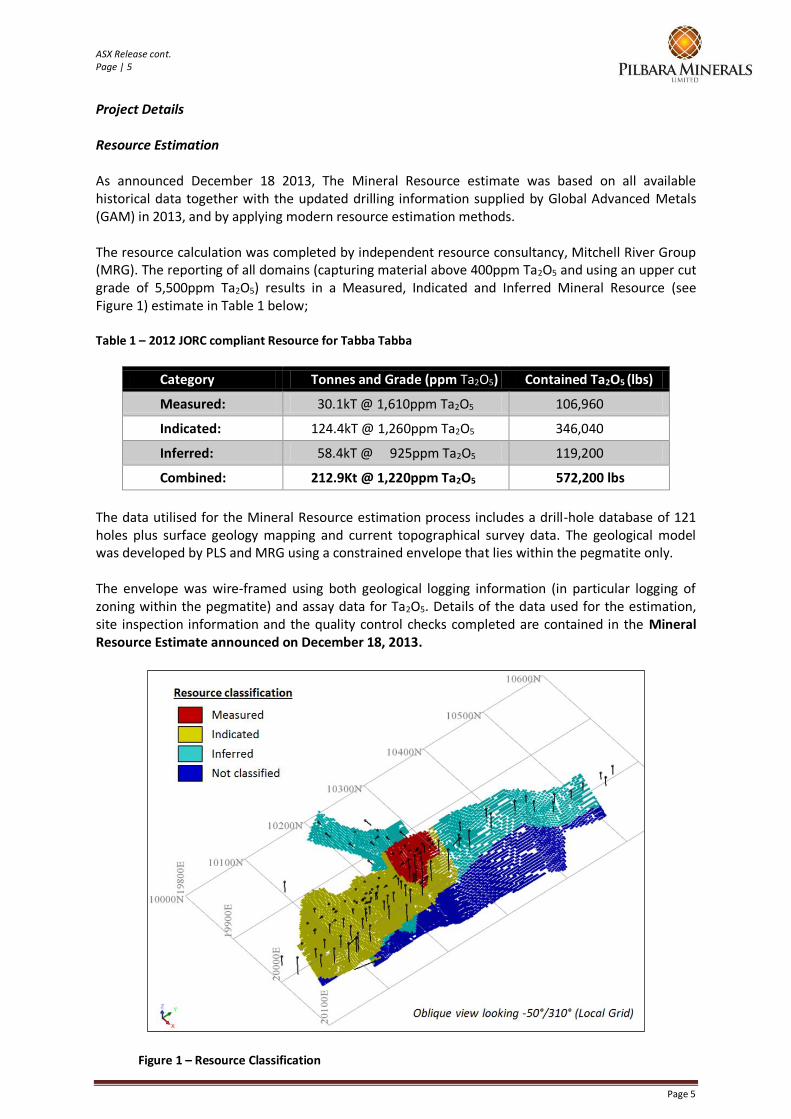

Project Details Resource Estimation As announced December 18 2013, The Mineral Resource estimate was based on all available historical data together with the updated drilling information supplied by Global Advanced Metals (GAM) in 2013, and by applying modern resource estimation methods. The resource calculation was completed by independent resource consultancy, Mitchell River Group (MRG). The reporting of all domains (capturing material above 400ppm Ta2O5 and using an upper cut grade of 5,500ppm Ta2O5) results in a Measured, Indicated and Inferred Mineral Resource (see Figure 1) estimate in Table 1 below; Table 1 – 2012 JORC compliant Resource for Tabba Tabba

Category Tonnes and Grade (ppm Ta2O5) Contained Ta2O5 (lbs)

Measured: 30.1kT @ 1,610ppm Ta2O5 106,960

Indicated: 124.4kT @ 1,260ppm Ta2O5 346,040

Inferred: 58.4kT @ 925ppm Ta2O5 119,200

Combined: 212.9Kt @ 1,220ppm Ta2O5 572,200 lbs

The data utilised for the Mineral Resource estimation process includes a drill-hole database of 121 holes plus surface geology mapping and current topographical survey data. The geological model was developed by PLS and MRG using a constrained envelope that lies within the pegmatite only. The envelope was wire-framed using both geological logging information (in particular logging of zoning within the pegmatite) and assay data for Ta2O5. Details of the data used for the estimation, site inspection information and the quality control checks completed are contained in the Mineral Resource Estimate announced on December 18, 2013.

Figure 1 – Resource Classification

ASX Release cont. Page | 6

Page 6

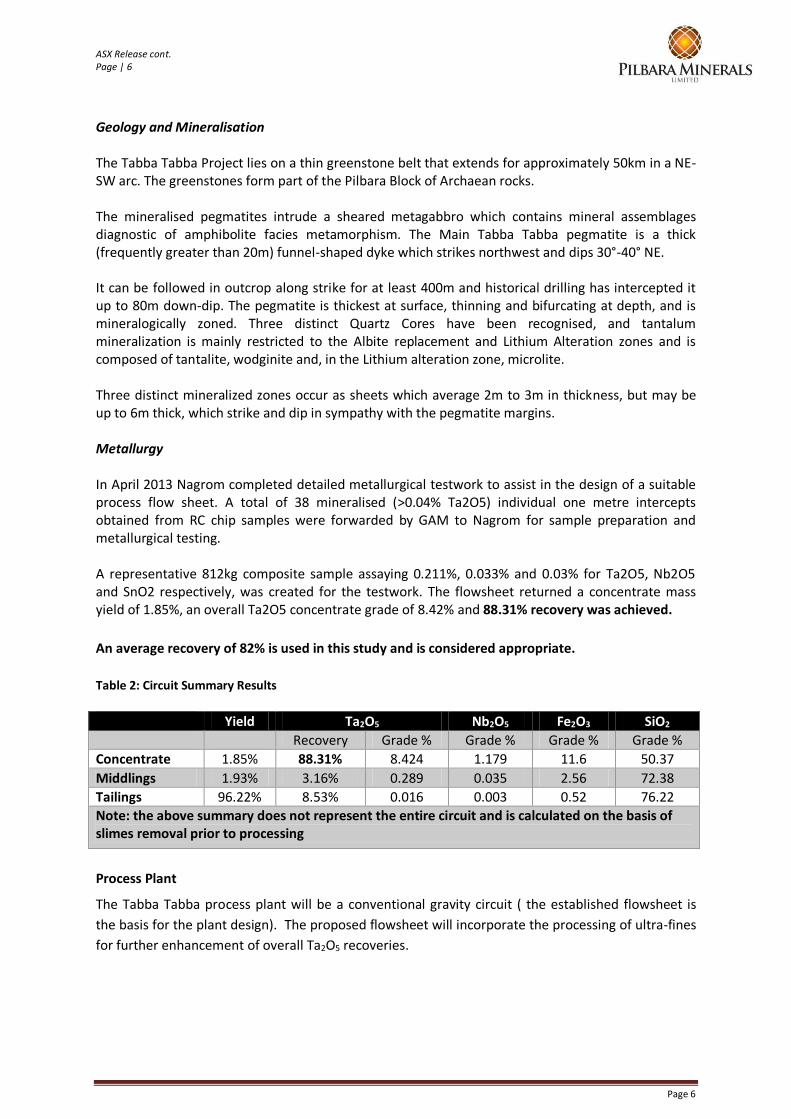

Geology and Mineralisation The Tabba Tabba Project lies on a thin greenstone belt that extends for approximately 50km in a NE-SW arc. The greenstones form part of the Pilbara Block of Archaean rocks. The mineralised pegmatites intrude a sheared metagabbro which contains mineral assemblages diagnostic of amphibolite facies metamorphism. The Main Tabba Tabba pegmatite is a thick (frequently greater than 20m) funnel-shaped dyke which strikes northwest and dips 30°-40° NE. It can be followed in outcrop along strike for at least 400m and historical drilling has intercepted it up to 80m down-dip. The pegmatite is thickest at surface, thinning and bifurcating at depth, and is mineralogically zoned. Three distinct Quartz Cores have been recognised, and tantalum mineralization is mainly restricted to the Albite replacement and Lithium Alteration zones and is composed of tantalite, wodginite and, in the Lithium alteration zone, microlite. Three distinct mineralized zones occur as sheets which average 2m to 3m in thickness, but may be up to 6m thick, which strike and dip in sympathy with the pegmatite margins. Metallurgy In April 2013 Nagrom completed detailed metallurgical testwork to assist in the design of a suitable process flow sheet. A total of 38 mineralised (>0.04% Ta2O5) individual one metre intercepts obtained from RC chip samples were forwarded by GAM to Nagrom for sample preparation and metallurgical testing. A representative 812kg composite sample assaying 0.211%, 0.033% and 0.03% for Ta2O5, Nb2O5 and SnO2 respectively, was created for the testwork. The flowsheet returned a concentrate mass yield of 1.85%, an overall Ta2O5 concentrate grade of 8.42% and 88.31% recovery was achieved.

An average recovery of 82% is used in this study and is considered appropriate.

Table 2: Circuit Summary Results

Yield Ta2O5 Nb2O5 Fe2O3 SiO2

Recovery Grade % Grade % Grade % Grade %

Concentrate 1.85% 88.31% 8.424 1.179 11.6 50.37

Middlings 1.93% 3.16% 0.289 0.035 2.56 72.38

Tailings 96.22% 8.53% 0.016 0.003 0.52 76.22

Note: the above summary does not represent the entire circuit and is calculated on the basis of slimes removal prior to processing

Process Plant The Tabba Tabba process plant will be a conventional gravity circuit ( the established flowsheet is

the basis for the plant design). The proposed flowsheet will incorporate the processing of ultra-fines

for further enhancement of overall Ta2O5 recoveries.

ASX Release cont. Page | 7

Page 7

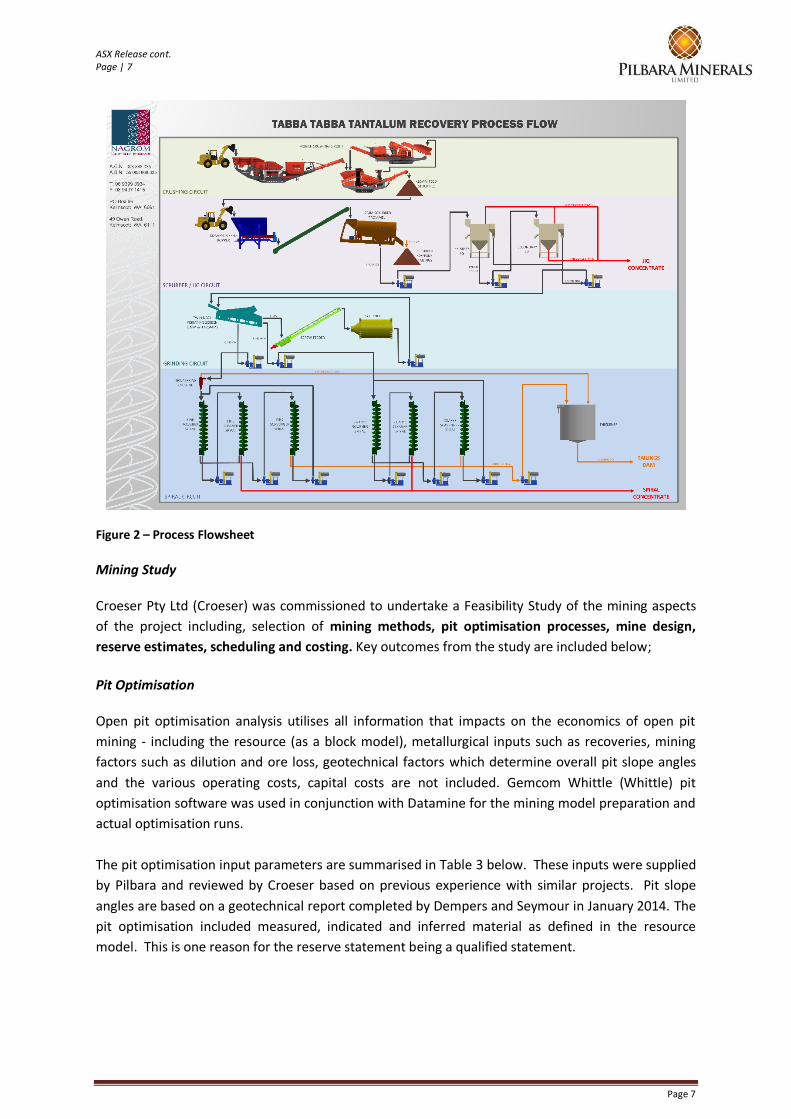

Figure 2 – Process Flowsheet

Mining Study Croeser Pty Ltd (Croeser) was commissioned to undertake a Feasibility Study of the mining aspects

of the project including, selection of mining methods, pit optimisation processes, mine design,

reserve estimates, scheduling and costing. Key outcomes from the study are included below;

Pit Optimisation Open pit optimisation analysis utilises all information that impacts on the economics of open pit

mining - including the resource (as a block model), metallurgical inputs such as recoveries, mining

factors such as dilution and ore loss, geotechnical factors which determine overall pit slope angles

and the various operating costs, capital costs are not included. Gemcom Whittle (Whittle) pit

optimisation software was used in conjunction with Datamine for the mining model preparation and

actual optimisation runs.

The pit optimisation input parameters are summarised in Table 3 below. These inputs were supplied

by Pilbara and reviewed by Croeser based on previous experience with similar projects. Pit slope

angles are based on a geotechnical report completed by Dempers and Seymour in January 2014. The

pit optimisation included measured, indicated and inferred material as defined in the resource

model. This is one reason for the reserve statement being a qualified statement.

ASX Release cont. Page | 8

Page 8

Table 3: Summary of pit optimisation inputs

Tabba Tabba Project

Summary of pit optimisation inputs Note: All currency in AUD

Metal price Units Amount

Ta2O5 $/lb LOM Offtake

Operating costs Units Amount

General & Administration $/t ore 15.32

Processing $/t ore 18.19

Incremental ore mining cost $/t ore 0.14

Subtotal $/t ore 33.65

Mining costs Units Amount

Average mining cost $/t rock 3.33

Whittle schedule parameters

Ore production rate (tpa) 118,000

Annual discount rate 10%

Pit slope angle, footwall - degrees 34

Pit slope angle, hangingwall - degrees 41

Mining dilution 15.0%

Mining recovery factor 95.0%

Metallurgical recovery % Overall

Ta2O5 82.0%

Optimisation Results Pit shell number 15 (162,000 tonnes @ 1235ppm Ta2O5) is the pit shell with the highest undiscounted cashflow of $16.75M. These results were the final option of a number of runs and were used as the base case for the final pit design Ore Reserve

Reserves are based on the final limits pit design. Ore recovery of 95% and dilution of 15% was

assumed for the reserve statement. Reserves are summarised in Table 4. Material classified as

measured in the resource model was classified as proved in the reserve and indicated was classified

as probable. In addition to the numbers stated there is 29,000 tonnes (at an average grade of

1038ppm Ta2O5 ) of inferred material included in the designed pit.

Table 4: Tabba Tabba Ore Reserves

Reserves Tonnes Ta2O5 ppm Nb2O5

Proved 32,000 1,420 294

Probable 101,000 1,249 292

Total 133,000 1,290 292

ASX Release cont. Page | 9

Page 9

In the opinion of Croeser these reserves are JORC compliant. In the opinion of Croeser these

reserves are JORC compliant with qualifications, as follows:

1. Inferred material was used in the pit optimisation and in the final financial assessment.

2. Approvals to proceed with mining have not been completed.

Pit Design

A final limits pit design was completed based on pit shell 15 (See Table 5) of the base case pit optimisation as detailed above. The footwall (West wall) follows the orebody. The highwall (East wall) is 34 m at the highest point. The deepest point in the pit is at 67.5mRL and the ramp exit is at 105mRL. The pit design guide lines used are as follows:

Two way access ramp widths of 18m from ramp exit at 105mRL to 97.5mRL

One way access ramp widths of 12m from 95mRL to 67.5mRL

From the 97.5mRL to the 95mRL the ramp transitions from 18m wide to 12m wide

Ramp gradient of 1 in 10 everywhere

Berm widths of 4m on the footwall and 5m on the hangingwall

Batter angles are mostly 50 degrees on the footwall and 65 degrees on the hangingwall

Batter slope angles and berm widths were designed according to the guidelines supplied by Dempers and Seymour in their geotechnical report.

Figure 3 West East section showing the pit design outline and the resource model block greater than

150ppm Ta2O5

ASX Release cont. Page | 10

Page 10

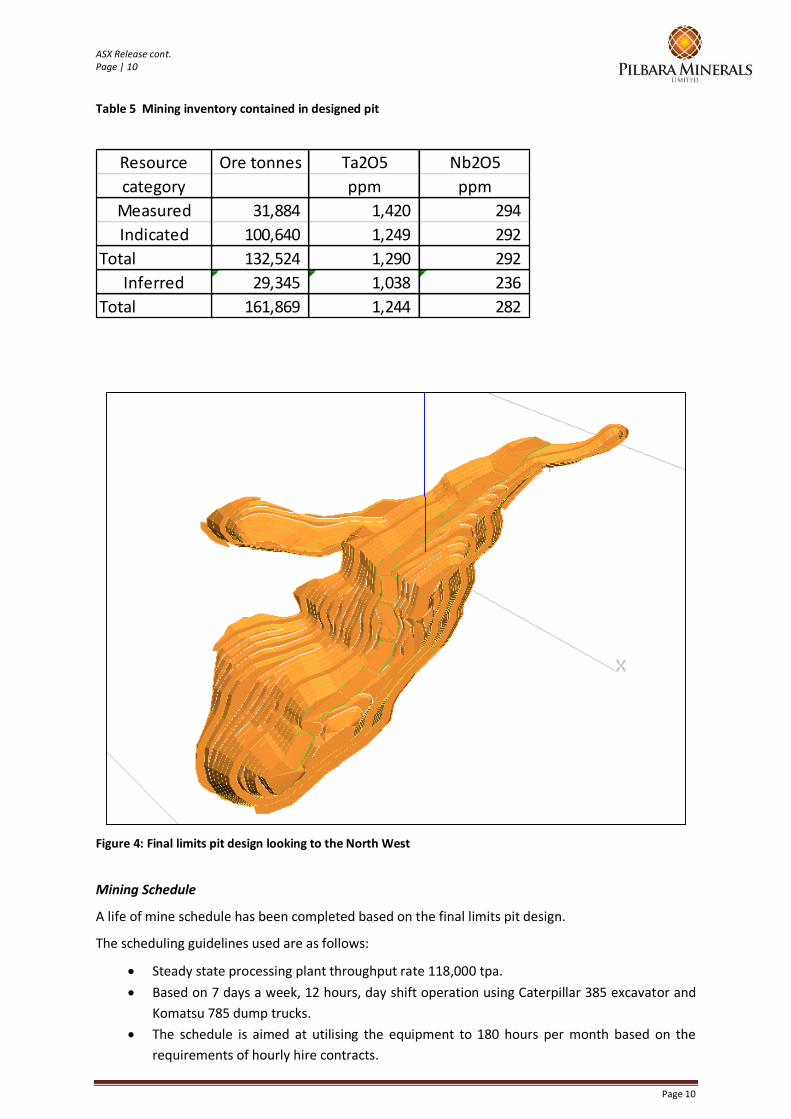

Table 5 Mining inventory contained in designed pit

Figure 4: Final limits pit design looking to the North West

Mining Schedule

A life of mine schedule has been completed based on the final limits pit design.

The scheduling guidelines used are as follows:

Steady state processing plant throughput rate 118,000 tpa.

Based on 7 days a week, 12 hours, day shift operation using Caterpillar 385 excavator and

Komatsu 785 dump trucks.

The schedule is aimed at utilising the equipment to 180 hours per month based on the

requirements of hourly hire contracts.

Resource Ore tonnes Ta2O5 Nb2O5

category ppm ppm

Measured 31,884 1,420 294

Indicated 100,640 1,249 292

Total 132,524 1,290 292

Inferred 29,345 1,038 236

Total 161,869 1,244 282

ASX Release cont. Page | 11

Page 11

The schedule allows for two months of pre-strip.

The schedule extends over 17 months.

The largest stockpile is 17,000 tonnes at the end of month 16.

Features of the life of mine schedule as completed:

The schedule (See Figure 4) was adapted to suit the best case cost scenario using an hourly

hire fleet.

It is not known at this stage when mining may commence, but the schedule maintains

sufficient stockpile to keep the plant operating in the case of a major weather event.

The mine fleet is under trucked to make the best use of two 90 tonne dump trucks and one

backhoe excavator. This fleet is very cost effective.

Figure 4: Life of mine schedule graph

Mining Cost Estimates

Mining costs for the project are based on a number of written quotations submitted by independent contractors for load and Haul (wet hourly hire rates) and contract Drill and Blast. There submissions were based on the mining schedule. Mining costs are detailed in operating costs and expressed as $/per tonne of ore.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

20,000

40,000

60,000

80,000

100,000

120,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Ta2O

5 p

pm

To

nn

es m

ined

Periods - months

Schedule graph

Ore tonnes mined

Waste tonnes mined

Ta2O5 ppm

ASX Release cont. Page | 12

Page 12

Capital Cost Estimate The capital cost estimate for the Project has been calculated at $3.9 million as outlined in table 6. Table 6 – Capital Cost Estimate

Cost Centre Detail Cost

Process Plant Feeder $120,000

Trommel $290,864

Jigs $260,000

Spirals $180,000

Triple Deck Screen $180,000

Ball Mill/Starter $150,000

Crush/Screen Plant $750,000

Thickener $200,000

Tools $15,000

Services Bore, Gen & Dam Pumps $150,000

Generators x2 (Plant) $230,00

Generator (Backup) $50,000

Generator (camp) $14000

Communications $12,000

Vehicles All Terrain Fork $35,000

Front End Loader $209,000

Vehicles (3) $70,000

Infrastructure Accommodation $250,000

Electrical Infrastructure $350,000

Mess/Office (2) $10,000

Workshop and Tools $35,000

Contingency at 10% $356000

Total: $3,900,864

The capital cost estimate is based upon a plant design of 30tph (or 118,000tpa with a 90% availability) and includes construction and commissioning of the process plant, power supply, accommodation village, mine office-infrastructure and water bore field. The estimate is based principally on a series of quotes on plant and infrastructure components either as tenders or submissions received by Nagrom Pty Ltd (see Appendix 1 for Site Photographs). The parties providing the tenders and quotes on supply have current or prior experience in building and operating in the Pilbara region of Western Australia.

ASX Release cont. Page | 13

Page 13

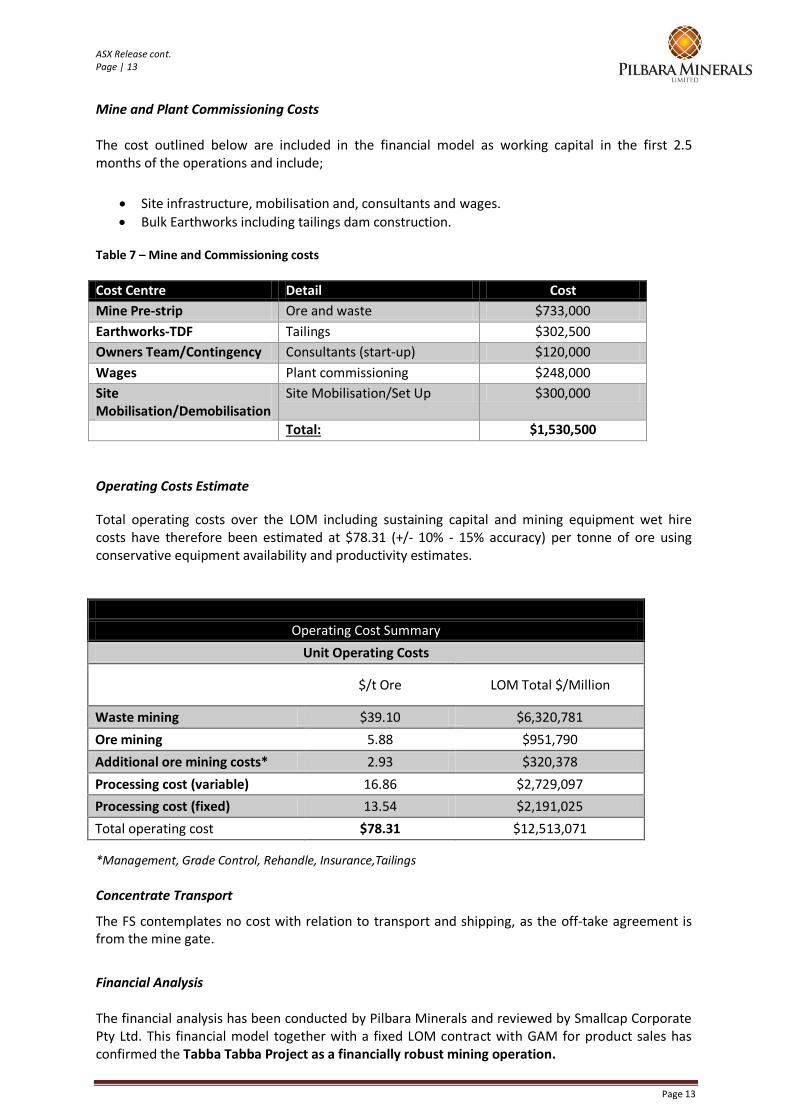

Mine and Plant Commissioning Costs The cost outlined below are included in the financial model as working capital in the first 2.5 months of the operations and include;

Site infrastructure, mobilisation and, consultants and wages.

Bulk Earthworks including tailings dam construction. Table 7 – Mine and Commissioning costs

Cost Centre Detail Cost

Mine Pre-strip Ore and waste $733,000

Earthworks-TDF Tailings $302,500

Owners Team/Contingency Consultants (start-up) $120,000

Wages Plant commissioning $248,000

Site Mobilisation/Demobilisation

Site Mobilisation/Set Up $300,000

Total: $1,530,500

Operating Costs Estimate Total operating costs over the LOM including sustaining capital and mining equipment wet hire costs have therefore been estimated at $78.31 (+/- 10% - 15% accuracy) per tonne of ore using conservative equipment availability and productivity estimates.

Operating Cost Summary

Unit Operating Costs

$/t Ore LOM Total $/Million

Waste mining $39.10 $6,320,781

Ore mining 5.88 $951,790

Additional ore mining costs* 2.93 $320,378

Processing cost (variable) 16.86 $2,729,097

Processing cost (fixed) 13.54 $2,191,025

Total operating cost $78.31 $12,513,071 *Management, Grade Control, Rehandle, Insurance,Tailings

Concentrate Transport The FS contemplates no cost with relation to transport and shipping, as the off-take agreement is from the mine gate. Financial Analysis The financial analysis has been conducted by Pilbara Minerals and reviewed by Smallcap Corporate Pty Ltd. This financial model together with a fixed LOM contract with GAM for product sales has confirmed the Tabba Tabba Project as a financially robust mining operation.

ASX Release cont. Page | 14

Page 14

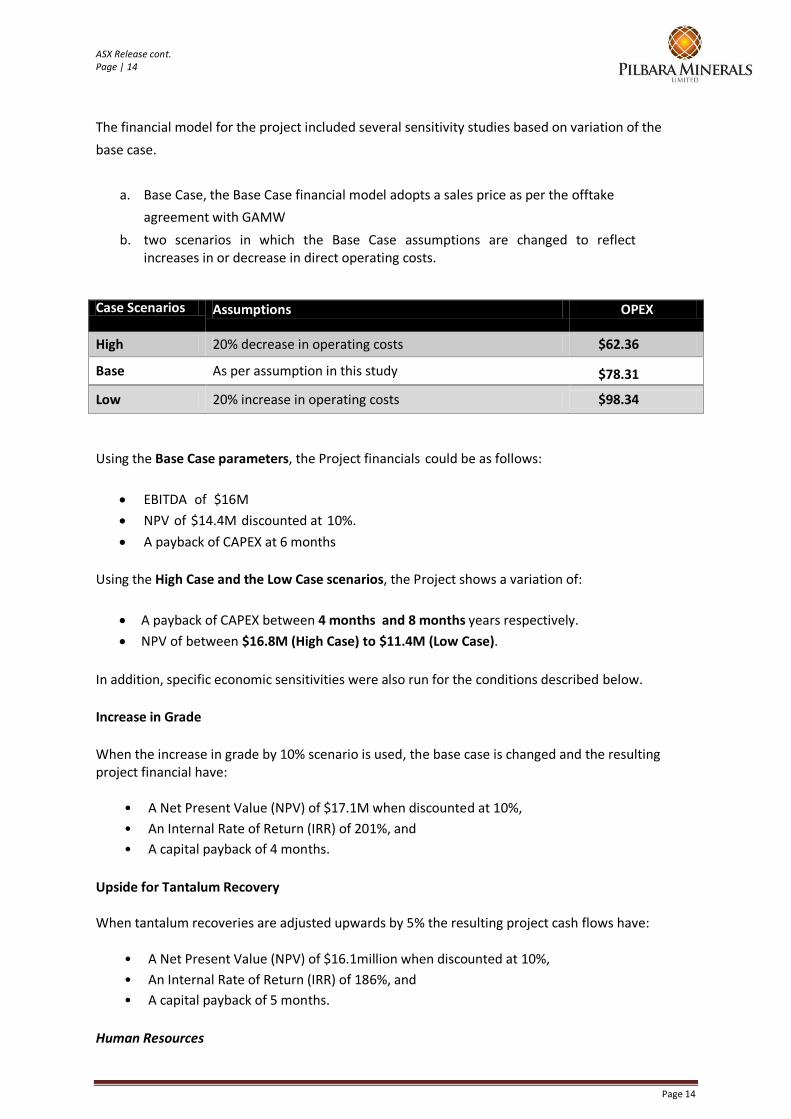

The financial model for the project included several sensitivity studies based on variation of the

base case.

a. Base Case, the Base Case financial model adopts a sales price as per the offtake

agreement with GAMW

b. two scenarios in which the Base Case assumptions are changed to reflect increases in or decrease in direct operating costs.

Case Scenarios Assumptions OPEX

High 20% decrease in operating costs $62.36

Base As per assumption in this study

$78.31

Low 20% increase in operating costs $98.34

Using the Base Case parameters, the Project financials could be as follows:

EBITDA of $16M

NPV of $14.4M discounted at 10%.

A payback of CAPEX at 6 months

Using the High Case and the Low Case scenarios, the Project shows a variation of:

A payback of CAPEX between 4 months and 8 months years respectively.

NPV of between $16.8M (High Case) to $11.4M (Low Case).

In addition, specific economic sensitivities were also run for the conditions described below.

Increase in Grade

When the increase in grade by 10% scenario is used, the base case is changed and the resulting project financial have:

• A Net Present Value (NPV) of $17.1M when discounted at 10%,

• An Internal Rate of Return (IRR) of 201%, and

• A capital payback of 4 months.

Upside for Tantalum Recovery When tantalum recoveries are adjusted upwards by 5% the resulting project cash flows have:

• A Net Present Value (NPV) of $16.1million when discounted at 10%,

• An Internal Rate of Return (IRR) of 186%, and

• A capital payback of 5 months.

Human Resources

ASX Release cont. Page | 15

Page 15

The FS contemplates a total peak construction workforce of 18 persons comprising:

Owners Team – 6

Construction work force – 12 (Peak) Post construction, the permanent peak work force is envisaged at 14 persons comprising:

Mining – 6 (Peak)

Process – 4

Management and Admin and support staff – 3

Village catering and cleaning – 1 Future Growth and Opportunities Pilbara Minerals sees numerous opportunities for future growth outside of the existing parameters considered by the Feasibility Study. Firstly, the Feasibility Study is based on currently known ore reserves with all ore bodies remaining open along strike and at depth. Significant upside exists for further discoveries along the host pegmatites which have been mapped adjacent to the pit area and within the mining licenses. Plant throughput rate is also based on conservative assumptions. To access high grade ores in the first few months, the mining rate has been planned to be at a rate higher than the plant throughput rate of 0.118Mtpa such that mining will be completed in approximately 1.4 years. In addition, the Strelley Deposit, is located just 15kms north-east of Tabba Tabba. Strelley was historically mined for eluvial tin (Sn) and Ta2O5 however has never been systematically explored or RC drilled. This project has significant potential to extend production at the Tabba Tabba Plant site. GAM has agreed to include this project in the current offtake and mining agreement. FS Contributors

The FS is based upon extensive drilling, analysis, QA/QC analysis and review, geological modelling,

mineralogical studies, metallurgical test work, geotechnical drilling and studies and mine planning

studies. Additional studies have been conducted on process water, environmental and social issues,

legal approvals, and land tenure.

The external organisations that contributed to the development of the FS include:

Mitchell River Group Pty Ltd - Resource Estimation

Roeselt Croeser – Mine Design and Reserves, Pit optimisation, Mine schedule and plan.

PLS/Smallcap Corporate Pty Ltd - Financial Analysis

Dempers and Seymour Pty Ltd - Geotechnical Report

Coffey Mining Limited - Tailings Storage Facility

Nagrom - Metallurgical sampling and testwork

Nagrom - Plant and Infrastructure Design & fabrication

K Lindbeck & Associates – Environmental assessment

Australasian Ecological Services - Fauna Study Level 1

PEK Enviro - Flora Study Level 1

Rockwater Pty Ltd - Subterranean Study

Yamatji Marlpa AC -Njamal Archaeological & Ethnographic Site Identification & Work

Area Clearance Heritage Survey of Tabba Tabba Project Area

ASX Release cont. Page | 16

Page 16

SUMMARY OF ORE RESERVE ESTIMATE AND REPORTING CRITERIA

As per ASX Listing Rule 5.9.1 and the 2012 JORC reporting guidelines, a summary of the material information used to estimate the Ore Reserve is detailed below (for more detail please refer to Table 1- Section 4, Sections 1 to 3 that relate to the resource estimate released to the ASX on the 18th of December have not materially changed.) Mineral Resource

The mineral resource model is documented in Technical Report for Tabba Tabba Tantalum Deposit, Pilbara Region, Western Australia, dated 18th December 2013 and was prepared by L.A. Barnes, J. Young, I. Algar and A. McDonald. This document describes the resource modelling process and covers all the requirements according to the JORC code. Site Visits

The competent person has not been for any site visits. All necessary information has been made available electronically and there were no issues that required clarification from a site visit. Study Status

This ore reserve and Feasibility study has been completed to a Feasibility level. The author considers that with the supplied and available information the project is viable. The project is sensitive to mining cost due to the high strip ratio. For this reason the author ensured that a rigorous check of mining costs was completed. The project is also sensitive to the inferred material that has been included in the mine plan and financial assessment of the project. For this reason the reserve statement will qualify this as one of the conditions.

Cut-off parameters

The cut-off grade was determined based on the input parameters as listed in table 3. The value of 278 ppm Ta2O5 was used for the reserve estimate.

Mine Factors and Assumptions

The method used to convert Mineral Resource to Ore Reserve is based upon a pit optimisation identifying an economic shell within which practical mining design has been applied. The various inputs have been supplied by appropriately qualified consultants. Selected mining methods such as truck and shovel are industry standard and are considered appropriate for the project. The mining method is conventional using equipment of Caterpillar 385 excavator and Komatsu 785 dump trucks, these are capable of mining to within centimetres of the grade control lines. It is assumed that there will be some blasting dilution and displacement. It is assumed that spotters will be used to direct the digging of ore contacts as and when required. The mining dilution was assumed to be 15%, while the mining recovery (ore loss 5%) was assumed to be 95%. These two factors together reflect the nature of the mineralised portion of the orebody which is typically 2m to 3m thick and up to 6m thick in places. The mineralisation occurs as sheets and is fairly continuous. The resource report discusses the existence of low grade halos around the higher grade mineralised envelopes. These halos have been modelled but were not included in the resource statement. Visible control is likely to be limited. It is assumed that grade control practices

ASX Release cont. Page | 17

Page 17

will be suitable. Drilling samples for grade control will be taken at 1m intervals from the blast hole rig when drilling is within the pegmatite only. Samples will be prepped on site, with a LM5 mill and a subsample of 200gms taken and transported to Perth at Nagrom for XRF analysis. The minimum mining width was assumed to be 10m. This allows enough room for proposed equipment to operate. The pit will be mined as a single stage so the minimum mining width will only apply at the bottom of the pit and in a small section of the pit which cuts into the side of a small hill. Inferred material has been used in the pit optimisation and in the mine schedule. This is stated clearly in the qualifications of the reserve statement. A pit optimisation based on measured and indicated material only showed 31,000 tonnes less in ore and $2.21M less in cashflow. This represents 19% of the ore in the pit optimisation used for this statement and 13% of the cashflow. The mineralised material in the designed pit is listed in Table 4 showing 29,000 tonnes of inferred material included in the mine plan. The site will require haul road establishment, provision of water and power, semi portable mine office and workshop.

Metallurgical Factors Assumptions

A dedicated process plant is planned. The metallurgical report by Nagrom discusses the metallurgical test work completed in detail. The author accepts the recovery numbers supplied by Nagrom Pty Ltd and not been made aware of any deleterious elements or potential metallurgical problems. The proposed flowsheet for processing is considered appropriate and ore specifications for sale can be met.

Environmental

All soil and waste characterisation and flora-fauna studies, water assessments have been completed, there have been no native title objections to any of the tenements and miscellaneous licences have been granted. There have been no site of significant impacts identified. All mining approval documents are in draft form, mining approval should be given 3 months from submittal. Waste rock characterisation studies have been completed and their no potential for acid rock drainage problems. Tailings Storage facilities have been designed (Coffey Mining) and soil testwork completed with no issues. No water applications have been submitted as pump tests are incomplete, no issues are expected with water supply. Field studies and monitoring of rehabilitation will be ongoing to continually improve the knowledge of the area to allow successful rehabilitation outcomes. Infrastructure The infrastructure required for the mining operation includes access roads, offices, haul roads, heavy equipment workshop, tailings facility and waste rock dump. Fuel will be transported on site and stored in a facility supplied by the fuel contractor. The proximity to Port Hedland ensures easy access to labour and site maintenance services.

Costs

There were no capital costs assumed in the mining study. The mining operating costs were derived from written hourly hire quotes. A number of quotes were received from contractors and the submission from Bluestone Mining was accepted as the primary basis for the mining cost estimate.

ASX Release cont. Page | 18

Page 18

The costs were built up using a fixed and variable method. The time line was dictated by the mining schedule. Equipment hire charges were based either on the scheduled equipment hours or on the minimum monthly hours specified by the contractors. Capital costs for the project facilities were developed by NAGROM, with individual capital items quoted and priced from equipment suppliers and is based upon costing the process design work. The CCE is expressed in Australian dollars. The expected cost includes a contingency of 10%. The estimate is likely to have an accuracy range of +/-15% centred on the expected cost. No allowance has been made for the government royalty as this is the responsibility of Global Advanced Metal Limited the mining lease holder. Revenue Factors

Head grade and metal content are derived from the Mineral Resource Estimate and the modifying factors described above. Revenue from the product sales is based on the supply of a +5% Ta2O5 concentrate at mine gate to Global Advanced Metals

Market

Market changes for the product are not applicable as sales of the product are fixed for a minimum 5 year period.

Economic

Inputs to the economic analysis include the factors described above including ore waste, and metal quantities from the mining and processing schedule, recovery factors, estimated processing costs, cost quotes and estimates and sale prices as per the offtake agreement. A range of NPVs are provided based on variations in operating costs, grade and recovery.

Social

All native title and pastoral agreements are in place

Governmental Approvals

All draft documents are ready for submittal to the Western Australian Department of Mines , there is no reason to suggest that mine approval will not be given.

Competent Person’s Statement The Company confirms it is not aware of any new information or data that materially affects the information included in the December 18, 2013 Mineral Resource Estimate and that all material assumptions and technical parameters underpinning the estimate continue to apply and have not materially changed when referring to its maiden resource announcement made on December 18, 2013. The information in this report that relates to Mineral Ore Reserves is based on and fairly represents information and supporting documentation prepared by Mr. Roselt Croeser who is a full time employee of Croeser Pty Ltd. Mr. Croeser has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the Joint Ore Reserves Committee (JORC) ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr. Croeser consents to the inclusion in this report of the matters based on his information in the form and context in which it appears.

Level 5, 2 Bligh Street Sydney NSW 2000 Australia Tel: +61-2-8252-9223 Fax+61-2-9475-5435

www.pilbaraminerals.com.au

ACN 112-425-788

Table1

Section 4 Estimation and Reporting of Ore Reserves

(Criteria listed in section 1, and where relevant in sections 2 and 3, also apply to this section, these have been reported on and included in the December 18, 2013 Mineral

Resource Estimate)

Criteria JORC Code explanation Commentary

Mineral Resource estimate for conversion to Ore Reserves

Description of the Mineral Resource estimate used as a basis for the conversion to an Ore Reserve.

Clear statement as to whether the Mineral Resources are reported additional to, or inclusive of, the Ore Reserves.

The mineral resource model is documented in Technical Report for Tabba Tabba Tantalum Deposit, Pilbara Region, Western Australia, dated December 2013 and was prepared by L.A. Barnes, J. Young, I. Algar and A. McDonald. This document describes the resource modelling process and covers all the requirements according to the JORC code. The author has reviewed the model with the principal author. The author is satisfied that the resource model is suitable.

The resource statement is inclusive of the reserves.

Site visits Comment on any site visits undertaken by the Competent Person and the outcome of those visits.

If no site visits have been undertaken indicate why this is the case.

The competent person has not been for any site visits. All necessary information has been made available electronically and there were no issues that required clarification from a site visit

Study status The type and level of study undertaken to enable Mineral Resources to be converted to Ore Reserves.

The Code requires that a study to at least Pre-Feasibility Study level has been undertaken to convert Mineral Resources to Ore Reserves. Such studies will have been carried out and will have determined a mine plan that is technically achievable and economically viable, and

This ore reserve and Feasibility study has been completed to a Feasibility level. The author considers that with the supplied and available information the project is viable. The project is sensitive to mining cost due to the high strip ratio. For this reason the author ensured that a rigorous check of mining costs was completed. The project is also sensitive to the inferred material that has been included

ASX Release cont. Page | 20

Page 20

Criteria JORC Code explanation Commentary

that material Modifying Factors have been considered. in the mine plan and financial assessment of the project. For this reason the reserve statement will qualify this as one of the conditions.

Cut-off parameters

The basis of the cut-off grade(s) or quality parameters applied. The cut-off grade was determined based on the input parameters as listed in table 3. The value of 278 ppm Ta2O5 was used for the reserve estimate.

Mining factors or assumptions

The method and assumptions used as reported in the Pre-Feasibility or Feasibility Study to convert the Mineral Resource to an Ore Reserve (i.e. either by application of appropriate factors by optimisation or by preliminary or detailed design).

The choice, nature and appropriateness of the selected mining method(s) and other mining parameters including associated design issues such as pre-strip, access, etc.

The assumptions made regarding geotechnical parameters (eg pit slopes, stope sizes, etc), grade control and pre-production drilling.

The major assumptions made and Mineral Resource model used for pit and stope optimisation (if appropriate).

The mining dilution factors used.

The mining recovery factors used.

Any minimum mining widths used.

The manner in which Inferred Mineral Resources are utilised in mining studies and the sensitivity of the outcome to their inclusion.

The infrastructure requirements of the selected mining methods.

The method used to convert Mineral Resource to Ore Reserve is based upon a pit optimisation identifying an economic shell within which practical mining design has been applied.

The various inputs have been supplied by appropriately qualified consultants. Selected mining methods such as truck and shovel are industry standard and are considered appropriate for the project.

The mining method is conventional using equipment of Caterpillar 385 excavator and Komatsu 785 dump trucks, these are capable of mining to within centimetres of the grade control lines. It is assumed that there will be some blasting dilution and displacement. It is assumed that spotters will be used to direct the digging of ore contacts as and when required

The mining dilution was assumed to be 15%, while the mining recovery (ore loss 5%) was assumed to be 95%. These two factors together reflect the nature of the mineralised portion of the orebody which is typically 2m to 3m thick and up to 6m thick in places. The mineralisation occurs as sheets and is fairly continuous. The resource report discusses the existence of low grade halos around the higher grade mineralised envelopes. These halos have been modelled but were not included in the resource statement. Visible control is likely to be limited. It is assumed that grade control practices will be suitable.

ASX Release cont. Page | 21

Page 21

Criteria JORC Code explanation Commentary

Drilling samples for grade control will be taken at 1m intervals from the blast hole rig when drilling is within the pegmatite only. Samples will be prepped on site, with a LM5 mill and a subsample of 200gms taken and transported to Perth at Nagrom for XRF analysis.

The minimum mining width was assumed to be 10m. This allows enough room for proposed equipment to operate. The pit will be mined as a single stage so the minimum mining width will only apply at the bottom of the pit and in a small section of the pit which cuts into the side of a small hill.

Inferred material has been used in the pit optimisation and in the mine schedule. This is stated clearly in the qualifications of the reserve statement. A pit optimisation based on measured and indicated material only showed 31,000 tonnes less in ore and $2.21M less in cashflow. This represents 19% of the ore in the pit optimisation used for this statement and 13% of the cashflow. The mineralised material in the designed pit is listed in Table 4 showing 29,000 tonnes of inferred material included in the mine plan.

The site will require haul road establishment, provision of water and power, semi portable mine office and workshop.

Metallurgical factors or assumptions

The metallurgical process proposed and the appropriateness of that process to the style of mineralisation.

Whether the metallurgical process is well-tested technology or novel in nature.

The nature, amount and representativeness of metallurgical test work undertaken, the nature of the metallurgical domaining applied and the corresponding metallurgical recovery factors applied.

Any assumptions or allowances made for deleterious elements.

The existence of any bulk sample or pilot scale test work and the degree to which such samples are considered representative of the

A dedicated process plant is planned. The metallurgical report by Nagrom discusses the metallurgical test work completed in detail. The author accepts the recovery numbers supplied by Nagrom Pty Ltd and not been made aware of any deleterious elements or potential metallurgical problems. The proposed flowsheet for processing is considered appropriate and ore specifications for sale can be met.

ASX Release cont. Page | 22

Page 22

Criteria JORC Code explanation Commentary

orebody as a whole.

For minerals that are defined by a specification, has the ore reserve estimation been based on the appropriate mineralogy to meet the specifications?

Environmental The status of studies of potential environmental impacts of the mining and processing operation. Details of waste rock characterisation and the consideration of potential sites, status of design options considered and, where applicable, the status of approvals for process residue storage and waste dumps should be reported.

All soil and waste characterisation and flora-fauna studies, water assessments have been completed, there have been no native title objections to any of the tenements and miscellaneous licences have been granted. There have been no site of significant impacts identified.

All mining approval documents are in draft form, mining approval should be given 3 months from submittal. Waste rock characterisation studies have been completed and their no potential for acid rock drainage problems. Tailings Storage facilities have been designed (Coffey Mining) and soil testwork completed with no issues. No water applications have been submitted as pump tests are incomplete, no issues are expected with water supply.

Field studies and monitoring of rehabilitation will be ongoing to continually improve the knowledge of the area to allow successful rehabilitation outcomes.

Infrastructure The existence of appropriate infrastructure: availability of land for plant development, power, water, transportation (particularly for bulk commodities), labour, accommodation; or the ease with which the infrastructure can be provided, or accessed.

The infrastructure required for the mining operation includes access roads, offices, haul roads, heavy equipment workshop, tailings facility and waste rock dump. Fuel will be transported on site and stored in a facility supplied by the fuel contractor.

The proximity to Port Hedland ensures easy access to labour and site maintenance services

Costs The derivation of, or assumptions made, regarding projected capital costs in the study.

The methodology used to estimate operating costs.

Allowances made for the content of deleterious elements.

The source of exchange rates used in the study.

Derivation of transportation charges.

There were no capital costs assumed in the mining study. The mining operating costs were derived from written hourly hire quotes. A number of quotes were received from contractors and the submission from Bluestone Mining was accepted as the primary basis for the mining cost estimate. The costs were built up using a fixed and

ASX Release cont. Page | 23

Page 23

Criteria JORC Code explanation Commentary

The basis for forecasting or source of treatment and refining charges, penalties for failure to meet specification, etc.

The allowances made for royalties payable, both Government and private.

variable method. The time line was dictated by the mining schedule. Equipment hire charges were based either on the scheduled equipment hours or on the minimum monthly hours specified by the contractors.

Capital costs for the project facilities were developed by NAGROM, with individual capital items quoted and priced from equipment suppliers and is based upon costing the process design work. The CCE is expressed in Australian dollars. The expected cost includes a contingency of 10%. The estimate is likely to have an accuracy range of +/-15% centred on the expected cost.

No allowance has been made for the government royalty as this is the responsibility of Global Advanced Metal Limited the mining lease holder.

Revenue factors

The derivation of, or assumptions made regarding revenue factors including head grade, metal or commodity price(s) exchange rates, transportation and treatment charges, penalties, net smelter returns, etc.

The derivation of assumptions made of metal or commodity price(s), for the principal metals, minerals and co-products.

Head grade and metal content are derived from the Mineral Resource Estimate and the modifying factors described above.

Revenue from the product sales is based on the supply of a +5% Ta2O5 concentrate at mine gate to Global Advanced Metals Wodgina Pty Ltd.

Market assessment

The demand, supply and stock situation for the particular commodity, consumption trends and factors likely to affect supply and demand into the future.

A customer and competitor analysis along with the identification of likely market windows for the product.

Price and volume forecasts and the basis for these forecasts.

For industrial minerals the customer specification, testing and acceptance requirements prior to a supply contract.

Market changes for the product are not applicable as sales of the product are fixed for a minimum 5 year period.

Economic The inputs to the economic analysis to produce the net present value (NPV) in the study, the source and confidence of these economic inputs including estimated inflation, discount rate, etc.

NPV ranges and sensitivity to variations in the significant

Inputs to the economic analysis include the factors described above including ore waste, and metal quantities from the mining and processing schedule, recovery factors, estimated processing costs, cost quotes and estimates and sale prices as per the offtake

ASX Release cont. Page | 24

Page 24

Criteria JORC Code explanation Commentary

assumptions and inputs. agreement. A range of NPVs are provided based on variations in operating costs, grade and recovery.

Social The status of agreements with key stakeholders and matters leading to social licence to operate.

All native title and pastoral agreements are in place

Other To the extent relevant, the impact of the following on the project and/or on the estimation and classification of the Ore Reserves:

Any identified material naturally occurring risks.

The status of material legal agreements and marketing arrangements.

The status of governmental agreements and approvals critical to the viability of the project, such as mineral tenement status, and government and statutory approvals. There must be reasonable grounds to expect that all necessary Government approvals will be received within the timeframes anticipated in the Pre-Feasibility or Feasibility study. Highlight and discuss the materiality of any unresolved matter that is dependent on a third party on which extraction of the reserve is contingent.

All draft documents are ready for submittal to the Western Australian Department of Mines, there is no reason to suggest that mine approval will not be given within the timeframes anticipated in the Feasibility Study.

Classification The basis for the classification of the Ore Reserves into varying confidence categories.

Whether the result appropriately reflects the Competent Person’s view of the deposit.

The proportion of Probable Ore Reserves that have been derived from Measured Mineral Resources (if any).

Measured and indicated resources have been converted to Proven and Probable Reserves

The estimated Ore reserves and mining method are appropriate in the opinion of the competent person appropriate for this style of deposit

Audits or reviews

The results of any audits or reviews of Ore Reserve estimates. All inputs to the estimation of ore reserves have been subject to internal reviews.

Discussion of relative accuracy/ confidence

Where appropriate a statement of the relative accuracy and confidence level in the Ore Reserve estimate using an approach or procedure deemed appropriate by the Competent Person. For example, the application of statistical or geostatistical procedures to quantify the relative accuracy of the reserve within stated confidence limits, or, if such an approach is not deemed appropriate, a qualitative discussion of the factors which could affect the relative accuracy and confidence of the estimate.

The statement should specify whether it relates to global or local

The assessment of the relative accuracy using statistical or geostatistical techniques is not considered appropriate.

There are no additional factors or areas of uncertainty remaining to be disclosed which could have material adverse impacts on project viability

ASX Release cont. Page | 25

Page 25

Criteria JORC Code explanation Commentary

estimates, and, if local, state the relevant tonnages, which should be relevant to technical and economic evaluation. Documentation should include assumptions made and the procedures used.

Accuracy and confidence discussions should extend to specific discussions of any applied Modifying Factors that may have a material impact on Ore Reserve viability, or for which there are remaining areas of uncertainty at the current study stage.

It is recognised that this may not be possible or appropriate in all circumstances. These statements of relative accuracy and confidence of the estimate should be compared with production data, where available.

Level 5, 2 Bligh Street Sydney NSW 2000 Australia Tel: +61-2-8252-9223 Fax+61-2-9475-5435

www.pilbaraminerals.com.au

ACN 112-425-788 More Information:

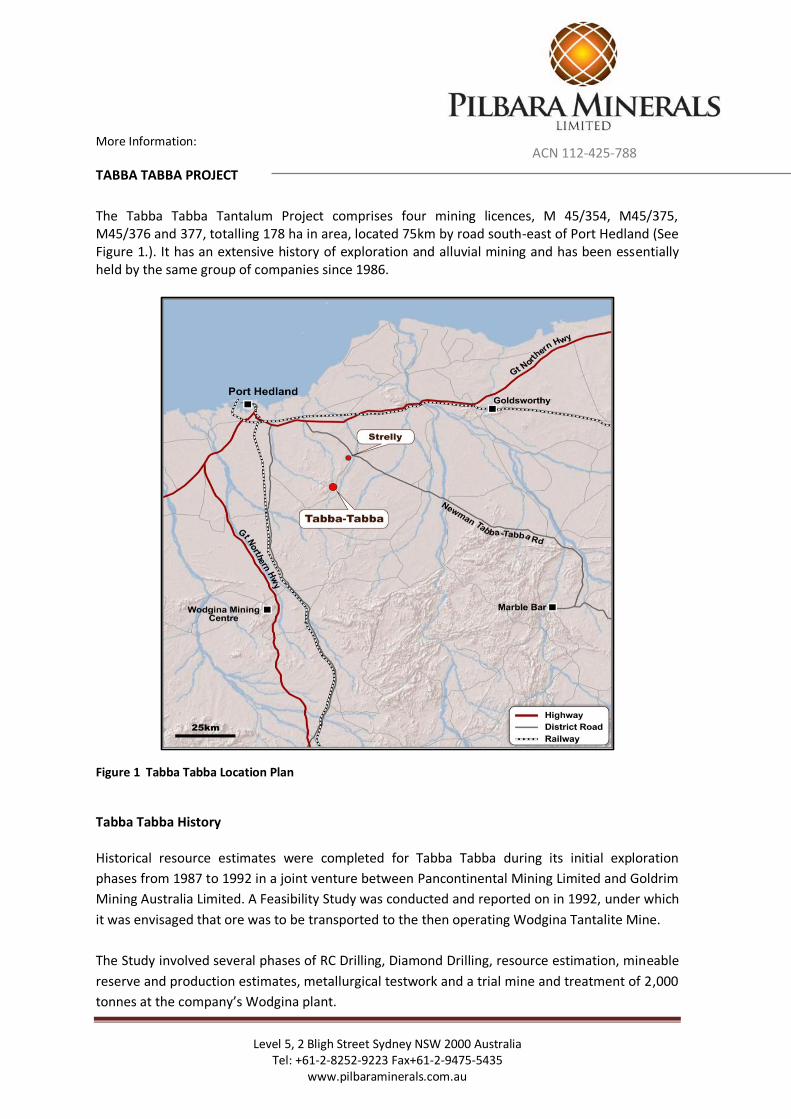

TABBA TABBA PROJECT

The Tabba Tabba Tantalum Project comprises four mining licences, M 45/354, M45/375, M45/376 and 377, totalling 178 ha in area, located 75km by road south-east of Port Hedland (See Figure 1.). It has an extensive history of exploration and alluvial mining and has been essentially held by the same group of companies since 1986.

Figure 1 Tabba Tabba Location Plan

Tabba Tabba History Historical resource estimates were completed for Tabba Tabba during its initial exploration

phases from 1987 to 1992 in a joint venture between Pancontinental Mining Limited and Goldrim

Mining Australia Limited. A Feasibility Study was conducted and reported on in 1992, under which

it was envisaged that ore was to be transported to the then operating Wodgina Tantalite Mine.

The Study involved several phases of RC Drilling, Diamond Drilling, resource estimation, mineable

reserve and production estimates, metallurgical testwork and a trial mine and treatment of 2,000

tonnes at the company’s Wodgina plant.

ASX Release cont. Page | 27

Page 27

As announced December 18, 2013 the initial work by Pilbara Minerals has involved the estimation

of a maiden 2012 JORC compliant mineral resource using all historic data plus the updated drilling

information supplied by GAM. The 2013 calculation which has provided an Inferred Resource was

carried out by independent resource consultancy Mitchell River Group (MRG). The reporting of all

domains (capturing material above 0.04% Ta2O5) and using an upper cut grade of 0.55% Ta2O5,

results in an Inferred Mineral Resource estimate of 211,000 tonnes @ 0.124% Ta2O5 containing

575,000 lb of Ta2O5.

Late in 2013, Pilbara Minerals set about upgrading the resource by completing geotechnical

studies for mine design, including bulk density analysis of ore and waste. This work has now been

finalised and makes up critical components of the 2014 Feasibility Study.

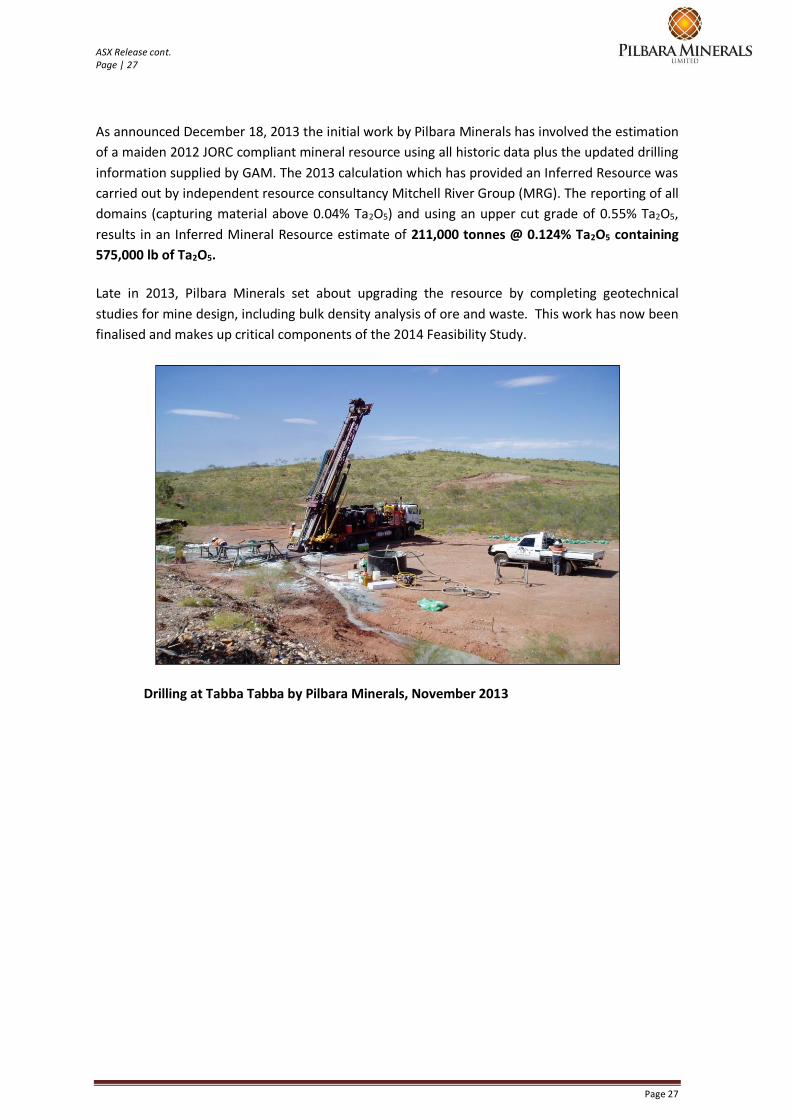

Drilling at Tabba Tabba by Pilbara Minerals, November 2013

ASX Release cont. Page | 28

Page 28

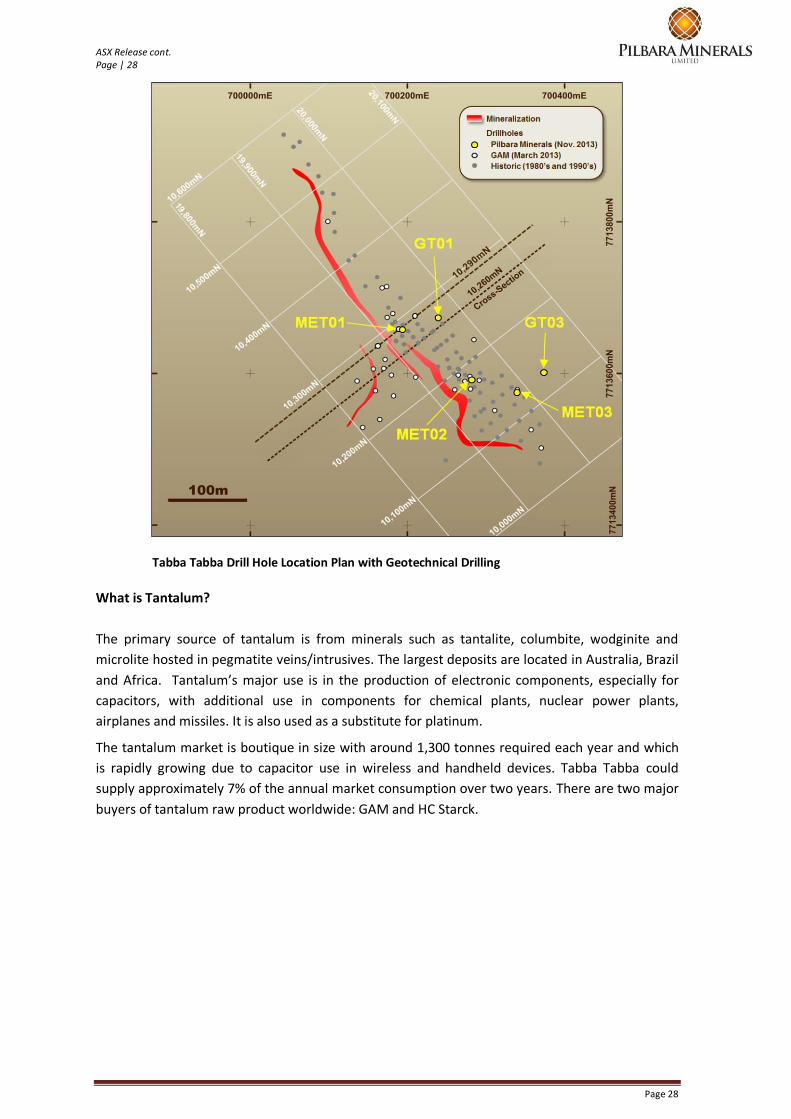

Tabba Tabba Drill Hole Location Plan with Geotechnical Drilling

What is Tantalum?

The primary source of tantalum is from minerals such as tantalite, columbite, wodginite and

microlite hosted in pegmatite veins/intrusives. The largest deposits are located in Australia, Brazil

and Africa. Tantalum’s major use is in the production of electronic components, especially for

capacitors, with additional use in components for chemical plants, nuclear power plants,

airplanes and missiles. It is also used as a substitute for platinum.

The tantalum market is boutique in size with around 1,300 tonnes required each year and which

is rapidly growing due to capacitor use in wireless and handheld devices. Tabba Tabba could

supply approximately 7% of the annual market consumption over two years. There are two major

buyers of tantalum raw product worldwide: GAM and HC Starck.

ASX Release cont. Page | 29

Page 29

APPENDIX 1 Site Photographs

Photograph 1: Looking south from proposed Waste Dump.

Photograph 2: Looking south from hole TTRC1310.

ASX Release cont. Page | 30

Page 30

.

Photograph 3: Proposed plant site.

Photograph 4: Proposed water supply dam.

ASX Release cont. Page | 31

Page 31

Photograph 5: Drilling looking along strike of pegmatite outcrop.

Photograph 6: Drilling looking north-west across pegmatite outcrop.