Embed Size (px)

Citation preview

Islamic Finance Bulletin

February 2014

lums.lancs.ac.uk/research/centres/golcer

Gulf One Lancaster Centre For Economic Research

Page 2

From the Editor

Half-way through the first quarter of this year, markets across the world had swung both ways, profoundly

unsure still of the strength of global economy recovery.

How the US Federal Reserve in particular would react, having begun to taper its prolonged stimulus programme,

was a key concern, mixed with (i) the uncertainties of the state of the Chinese economy, (ii) the ability of

emerging markets in Asia to recover from recent capital flight, and (iii) the condition of sovereigns and corporates

in the West to emerge convincingly from the post-crisis period.

Bonds continued to suffer from the selling pressure of late 2013, but thereupon responded to investors’ search

for safe havens once stocks wondered whether the easy money era was drawing towards an end. Gold was

bought upon the same motivation, while oil and copper indicated that a lack of fundamental direction was the

underlying truth.

On the sukuk side, these instruments initially felt the triple effects of emerging-market turbulence, oil-price

fragility, and weakened fixed-income sentiment generally. However, in the Gulf arena both local and overseas

investors were evidently awaiting their next opportunity to capture yield, welcoming renewed issuance.

In this edition we once again document those key trends, besides sampling news and comment on the expansion

of Islamic finance, this time featuring Asia especially.

Viewpoints are provided by voices from the multilateral bodies the World Bank and the Asian Development

Bank, addressing financial exclusion and poverty alleviation -- also the scope that Islamic microfinance has to

break through barriers and improve the lives of those who are currently under-banked and need support.

Following last month’s item on Indonesia, in this issue we feature Pakistan, and its own vast potential for Shariah-

compliant finance to make inroads into existing markets, as well as make a key-turning difference to millions of

Muslim customers and entrepreneurs.

ContentsHIGHLIGHTS (p.3)

RECENT DEVELOPMENTS (p.4)

VIEWPOINT (p.7)

VIEWPOINT (p.9)

FEATURE (p.11)

STOCK MARKETS (p.14)

COMMODITIES (p.17)

BOND AND CDS MARKETS (p.18)

PERSPECTIVE (p.21)

DIARY (p.22)

Page 3

Islamic Finance and Asia: The Asia region contains

vast potential not only to advance Shariah-compliance

across financial and non-financial sectors, but to utilize

its methods for poverty alleviation and microfinance

projects. Equally, those are matters both of natural

demand, in terms of hitherto under-served Muslim

populations, and promoting and enabling supply by

official policy means. The issues of financial exclusion

and distribution of wealth are pervasive concerns that

Islamic mechanisms can be employed particularly to

address.

Pakistan: As the world’s sixth most populous country,

Pakistan has an ample base among its own citizenry

to exercise the potential of the various strands of the

Islamic economy. Following initial attempts to develop

this dimension of economic growth and development in

previous decades, a newfound emphasis has been brought

to advance the cause of Islamic finance, especially by

the central bank’s strategic plan. Claiming an enhanced

share of banking business, and taking responsibility for

agricultural financing, feature on the agenda.

MENA Markets: Both the stock and bond markets of

the GCC states have performed relatively well in recent

weeks and months, compared with both developed

and emerging counterparts. Confidence has grown

not only in the region’s financial standing, but also in its

attempts to extend cyclical rebound, elements which

to some extent are missing among other blocs. Dubai’s

resurgence has been the star turn in this show, while the

lingering political tensions in Egypt have been ignored

by investors attracted to signs of solidity returning to the

economy.

Highlights

Recent Developments in the Islamic Finance Industry

UK moves forward with Islamic finance plansThe UK government has chosen HSBC to handle and

advise on its debut Islamic bond planned for as early as

this year. Other banks are to be mandated closer to the

time of the issuance. Law firm Linklaters is expected to

provide legal support for the sukuk, including its tax and

real estate implications. The timing of the sale will depend

both on market conditions and the required preparation.

In addition, the government has launched a new venture

seeking to bolster London’s position as a centre for Islamic

finance by extending its ‘Help to Buy’ mortgage scheme

to loans that comply with Islamic law. Help to Buy was

launched last year, and offers banks insurance against the

risk of lending to home-buyers who cannot afford large

mortgage deposits. Britain’s finance ministry announced

that property finance plans that cater for Islam’s bar on

interest payments would now be eligible in the same way

as standard mortgages. Islamic mortgages are to be

provided by the Islamic Bank of Britain, which is owned by

Qatar’s Masraf Al Rayan.

Source: Bloomberg, January 31st & ArabianBusiness.com,

February 11th

GOLCER finds these initiatives to be active steps following

the UK’s recent official announcements of becoming the

first non-Muslim nation to support the Islamic finance

industry and sell sukuk. Last October Prime Minister

Cameron announced the plan to sell £200m ($330m)

in securities that comply with Islam’s ban on interest, a

development reflecting the “pragmatism and political

will” that has been pronounced. The issuance of sukuk

will bring a series of benefits to the UK, helping to

establish a “fresh global capital” for Islamic finance

alongside Dubai and Kuala Lumpur. According to

PricewaterhouseCoopers, the industry is growing 17% a

year, and expected to be valued at $2.7trn by 2017.

Islamic finance in Italy might need Gulf supportBankers in Italy are putting efforts towards developing

Islamic finance in the country. Campaigns have been

launched which seek to benefit from growing economic

links between the Gulf countries and the eurozone’s third

largest economy. Italy’s trade ties with the Gulf are

booming, with exports to the UAE reaching 5.5 billion

euros in 2012, a 16.7% rise from 2011, according to

government data. This month Kuwait’s sovereign

wealth fund has announced that it will invest 500

million euros ($685m) in Italian companies, in

coordination with the Italian government’s own

strategic investment fund, in line with a similar deal

with Qatar last year. Only about 2% of Italy’s

population of 61m are Muslim; yet both bankers

and academics hope that as Gulf companies and

investors increase their activities in Italy, Islamic

finance will follow.

Source: ArabianBusiness.com February 20th

GOLCER perceives that while there has been minor, marginal progress in the industry in continental Europe, witnessed mainly in France and Germany, it seems that Italy is seeking trade and investment with wealthy GCC states through Islamic finance instruments as a way to solve its substantial debt problems. Italian firms raising loans could use Islamic structures to attract Islamic banks from the Gulf through, for example, bonds and equities if they were certified as Shariah-compliant. Political and legislative hurdles remain an issue for this attempted boost to the sector.

Takaful seen struggling in KuwaitKuwait’s takaful firms are said to be struggling still

in a crowded market with intense competition. This

perception is borne out by stagnant growth and

persistent losses for those firms, though operating in

one of the world’s richest countries on a per capita

basis. That reality has caused doubts to be raised

about the sector’s long-term viability. Kuwaiti takaful

firms posted a combined 47.4m dinars ($167.7m)

in premiums in 2012, an 18.7% share of the total.

However, this figure was spread across 11 locally-

incorporated takaful firms, with many companies in

the sector having failed to post consistent profits. In

Page 4

Recent Developments in the Islamic Finance Industry

a market with 32 insurers, takaful firms have said they are

facing disadvantages relative to their conventional peers,

which have been running their businesses in the country for

decades, allowing them to build solid customer bases and

large financial surpluses.

Kuwait’s landscape in this regard seems to be quite

different from the situation in Bahrain, where the central

bank will release a new regulatory framework for takaful

this quarter. The new rules, developed after two years of

consultation with the industry, cover the operations and

solvency of takaful firms. They call for a new formulas to

calculate capital and replace free loans (qarad Hassan)

with capital injections. Under the proposed rules, total

capital would include both the available capital of the

shareholders’ fund and the net admissible assets of the

policyholders’ funds.

Source: Reuters, January 31st & February 11th

GOLCER thinks that Kuwait’s takaful sector could even

shrink in the coming years, facing a critical position,

with reduced profit margins. Takaful firms are required

to distribute excess profits to policyholders, unlike

conventional firms, which account for such surpluses

as profits. The relative underperformance may also be

attributed to the lack of a supervisory body, which made

the takaful industry -- not only in Kuwait but worldwide

-- vulnerable to sensitive performance results, as well as to

uncompetitive practices.

Saudi Arabia and Malaysia bourses link boostedThe stock exchanges of Saudi Arabia and Malaysia have signed an agreement to foster closer ties between them, with the aim to promote Islamic finance. The deal is likely to enhance areas such as equities, mutual funds and sukuk, and to build on sharing expertise and developing human capital. Saudi Arabia’s stock exchange hosts the largest Islamic banks in the world, while the exchange of Malaysia has the largest and most liquid market for trading sukuk. Saudi Arabia’s exchange has already addressed, but not yet signed, similar agreements with its Abu Dhabi and Bahrain counterparts.

Source: Khaleej Times, February 21st

GOLCER finds that this initiative is one of the important Islamic finance tie-ups during 2014, in reaction to the increased competition among many countries contemplating cross-border activity in the industry. According to Thomson Reuters data, the two countries represent the largest Islamic finance markets globally, holding a combined $682bn in Islamic banking assets. Still, however, there could be some challenges to face, given the traditional differences in the design and implementation of Shariah-compliant financial products between the two countries. (See Focus.)

Morocco intends funds for Islamic financeMorocco, the only North African nation with an investment-grade rating at Standard & Poor’s, has announced plans to allow Islamic banking for the first time, proposing to invest in the industry. The country approved a draft Islamic finance law on January 16th. This document offers a framework to regulate Islamic banks, and allows for sukuk sales. It awaits parliamentary approval, but is expected to be enacted by the middle of this year. The Moroccan Association of Participative Financiers estimates total investment in Shariah-compliant products to reach $7bn by 2018 if the law comes into effect.

Source: Bloomberg, January 31st

GOLCER sees the Islamic finance industry clearly responding to the accelerating demand worldwide for financing that complies with Islamic law. By 2018 Islamic banking assets are expected to climb to $3.4trn from about $1.7trn in 2013, according to Ernst & Young. Morocco has slowly joined the race, with more than 95% of its population of 34 million supporting the introduction of banking that adheres to Shariah.

Islamic finance body IILM plans further issuance

The Malaysia-based International Islamic Liquidity Management Corp (IILM) announced its plans to

Page 5

Page 6

issue a $490m three-month Islamic bond by the end of February, after expanding its issuance programme to $1.35bn in January. The auction of the sukuk is rated A-1 by Standard and Poor’s, according to a filing lodged with Malaysia’s central bank. The IILM has already sold $860m of three-month paper this year, aiming to meet a shortage of highly-liquid, investment-grade financial instruments which Islamic banks can trade to manage their short-term funding needs. Shareholders of the IILM are the central banks of Indonesia, Kuwait, Luxembourg, Malaysia, Mauritius, Nigeria, Qatar, Turkey and the UAE, as well as the Jeddah-based Islamic Development Bank.

Source: Reuters, January 31st

GOLCER views the IILM’s programme as being still in its early stages, and has doubts about the successful, active trading of its sukuk, and even the reasons behind issuing these additional sukuk, as the primary dealers have held on to the IILM instruments after auction and there has been little, if any, secondary market trade in them.

Focus: Gulf-Asia co-operationIn October 2013 the Central Bank of the UAE announced it had

signed an MoU with Central Bank of Malaysia on the sidelines

of the annual IMF/WB meetings, aimed at co-operation,

exchange of information and expertise, and training. It would

contribute to the realisation of a sound financial system in

the UAE and Malaysia, and represents a trend to stronger

ties between Islamic finance centres in the Arabian Gulf and

Southeast Asian regions, despite traditional differences in the

design and implementation of Shariah-compliant financial

products.

Source: Khaleej Times, Reuters, November 2013

New Malaysian standards for Shariah-compliant equities

that are expected to attract more Islamic investment funds

from the Gulf countries were introduced last November by the

Malaysian Securities Commission. An improved screening

methodology is used that encompasses quantitative filters

such as benchmarks for financial ratios, moving closer to the

approach generally used in the Gulf. The change is widely

expected to help further internationalise Malaysia’s Islamic

finance industry.

The methodology had previously included only qualitative

screens; for example, banning companies involved

in sectors such as tobacco, alcohol, weapons and

gambling. Islamic fund managers in Malaysia now have

six months to drop securities that are excluded from the

list, which currently has a total of 653 Shariah-compliant

stocks out of 914 listed on the Bursa Malaysia.

In another move, the Philippine Stock Exchange said it

would designate its first Shariah-compliant companies,

in a bid to keep Muslims’ money in the country. Another

strengthening player in the sector is Singapore, [whose]

government has undertaken initiatives in areas such as

taxation, capital markets, REITs, takaful insurance and

Islamic equity indexes in order to improve Singapore’s

attractiveness for Islamic finance.

Source: Arno Maierbrugger, investvine.com, Inside

Investor, December 2013

The Malaysia-Gulf Cooperation Council (GCC)

framework agreement signed in January 2011 was

intended to enhance bilateral economic links. Instead,

co-operation grew at a disappointingly slow pace, [but

now] appears to be gaining momentum. Generous tax

incentives to encourage commercial banks operating in

Malaysia to establish Islamic banking subsidiaries and

foreign companies have been drawing in a number of

GCC banks to establish operations in Malaysia (e.g.

Kuwait Finance House). Conversely, the GCC economies

are attractive potential targets for Malaysian investment.

Another interesting shift is that Arab countries are now

looking to Malaysia to enhance halal standards and

promote related products. Until recently, meat and halal

products have been largely imported by the GCC from

Australia, New Zealand, Ireland, Brazil, Canada, and the

US. Although Malaysia had taken the lead in developing

and modernizing this sector, it has essentially lost out to

these competitors in the past. With the Gulf changing

its focus to Asia, the food and chemicals industries in

Malaysia that are largely bound by halal laws command

an edge over other regional manufacturers.

Source: Evelyn Davadason, University of Malaya, June

2013 for Middle East Institute

What level of impact could be expected from the growth of Islamic finance (IF) in the region, in terms of bringing basic banking facilities to lower-income groups, and plans for development and poverty alleviation?

ADB regards Islamic finance to have great potential in the fight against poverty in Asia. There is a sizable part of the population in the Asia & Pacific region, especially in rural areas, that for religious, cultural or moral reasons sees Islamic finance as the only method by which to access financial services which would otherwise result in their financial exclusion.Apart from being a viable alternative to the conventional interest-based financial system, which is prone to extreme risks, the risk-sharing solutions offered by Islamic finance may assist in restoring equilibrium, as it encourages and facilitates investment in real economic activity and societal welfare, while prohibiting investment in socially-harmful ventures such as gaming, alcohol and adult entertainment, or risky financial products such as highly-speculative derivative contracts, of the kind which led to the 2008 sub-prime crisis.In addition to the important complementary role that Islamic finance can play in global finance, the sector provides an exciting opportunity to expand the accessibility to finance which can play a more positive role in eradicating poverty. It can address the issue of financial inclusion from two directions: one through promoting risk-sharing contracts which provide a viable alternative to conventional debt-based financing, and the other through emphasizing the socially-responsible principles of transparency and prohibition of speculation and exploitation.

Is the ADB promoting or simply facilitating the development of the IF sector? Can you give details of how that is being done?

Asian Development Bank (ADB) has 14 member countries that have a majority Muslim population, as well as other members with a sizeable Muslim component (including India, PRC, the Philippines, Sri Lanka and Thailand). ADB’s Developing Member Countries (DMCs) represent approximately 80% of the world’s Muslim population. A number of these DMCs have developed relatively sophisticated Shariah-compliant finance (SCF) industries which complement their conventional financial services sectors.As the premier development institution of Asia, ADB is well placed to play a catalytic role in the development of SCF in the region. We can assist in the development of best practice for prudential standards and corporate governance rules for central banks and securities regulators, to enable them to properly and fairly regulate Islamic financial institutions (IIFIs). ADB can also play a catalytic role in helping to meet the nascent demand for SCF from the private sector, that is becoming evident in certain DMCs.ADB’s participation in SCF will assist the development of the SCF industry during its formative early stages in DMCs, an involvement which will ensure that SCF is being undertaken using best international standards.

Islamic Finance and the fight against poverty in Asia

Interview with Ashraf Mohammed, Asian Development Bank

Viewpoint

Page 7

Page 8

ADB’s significant role in the development of Shariah-compliant finance in Asia has included:

• Supporting the development of international best practice in prudential standards and corporate governance for IIFIs, by assisting through technical assistance (TA) and co-operation, standards-setting organizations such as the Islamic Financial Services Board (IFSB), and through knowledge-dissemination activities, e.g. workshops and conferences.• Advising and assisting DMCs, through TAs and loans, in capital markets development for Islamic financial institutions, including development of appropriate supervisory and regulatory laws and frameworks• Promoting the use of SCF through co-financing opportunities with IIFIs such as the Islamic Development Bank, and developing and participating in innovative financing structures such as the Islamic Infrastructure Fund and the International Islamic Liquidity Management Corporation • Providing credit enhancement in SCF non-sovereign transactions such as Pakistan’s Fauji Wind Power Project

How do you perceive the relative roles of the public and private sectors in the regional growth of the IF industry?

Public sector institutions have an enormous role to play in the promotion and development of Islamic finance in their countries. Anecdotal evidence would suggest that those counties that have progressive regulatory and supervisory authorities providing the necessary legal and regulatory framework to establish a level playing-field for Islamic finance to take hold and expand are the ones which have benefited the most in terms of the contribution that Islamic finance makes to the economy.Among the developed Islamic banking jurisdictions in Asia are Malaysia, Indonesia, Pakistan and Brunei. Malaysia is one of the global leaders for Islamic financial services, and held an estimated 9% share of the global Islamic banking assets in 2013. Comparatively, Indonesia, Pakistan and Brunei

have smaller shares, but their growth and regulatory developments in recent years have enabled them to be en route to expanding on their volume of Shariah-compliant banking assets. These countries have demonstrated that if government takes the trouble of developing an effective strategy and supports that strategy to create an enabling environment, then they will derive a huge dividend from private sector participation.

It has been suggested that Islamic finance promotes economic or financial stability per se. Does your research on the Asian region support that stance?

The linkage of financial development with economic development has already been established. However, a high level of financial development in a country is not necessarily any indication of alleviation of poverty in that country. There is growing realization that, in addition to financial development, there should be emphasis to promote financial stability, which in turn should assist to expand the accessibility to finance which can play a more positive role in eradicating poverty. Enhancing the access to and the quality of basic financial services -- such as availability of finance, mobilization of savings, insurance and risk management -- can facilitate sustainable growth and productivity, particularly for micro, small and medium-scale enterprises.It can be argued that the core principles of Islam lay great emphasis on social justice, inclusion, and the sharing of resources between different strata of society, thus reinforcing financial stability. Islamic finance further supports financial stability and equity through specific instruments of redistribution of wealth amongst society as whole, such as Zakat and Waqf.

Ashraf Mohammed is Assistant General Counsel, Practice Leader in Islamic Finance at the Asian Development Bank (ADB). The opinions expressed are his own.

About 700 million of the world’s poor live in predominantly Muslim-populated countries. In recent years, there has been growing interest in Islamic finance as a tool to increase financial inclusion among Muslim populations.

The main issue relates to the fact that many Muslim-headed households and micro, small, and medium enterprises may voluntarily exclude themselves from formal financial markets because of Shariah requirements.

Islamic legal systems, among other characteristics, prohibit predefined interest-bearing loans. They also require financial providers to share in the risks of the business activities for which they provide financial services (profit and loss sharing). Given these requirements, most conventional financial services

are not relevant for religiously-minded Muslim individuals and firms in need of financing.

Based on a 2010 Gallup poll, about 90% of the adults residing in Organization of Islamic Cooperation (OIC) member countries consider religion an important part of their daily lives (Crabtree 2010). This may help explain why only about 25% of adults in OIC member countries have an account in formal financial institutions, which is below the global average of about 50%.

Muslim countries are far from uniform in terms of financial inclusion. For example, 34% of the unbanked Afghan population cite religious reasons for not having an account in a formal financial institution, while only 0.1% of Malaysians do so, although both countries have similarly high Gallup

Islamic Finance and Financial Inclusion: the World Bank’s view

Viewpoint

Page 9

Page 10

religiosity indexes (97% and 96% respectively).

This can be traced to the extent to which Islamic financial institutions are present in a given country. An analysis suggests that the size of Islamic assets per adult population is negatively correlated with the share of adults citing religious reasons for not having an account. This correlation is particularly strong if one focuses on the group of OIC countries and, even more, on those OIC countries that show a religiosity index exceeding 85%.

Based on the Global Findex [Financial Inclusion Index], for religious reasons, some 51 million adults in the OIC countries do not have accounts in a formal financial institution. Given that a majority of the OIC population lives in poverty, Islamic microfinance could be particularly attractive.

Global surveys on Islamic microfinance completed by the Consultative Group to Assist the Poor (CGAP) in 2007 and 2012 provide some initial insights into the rapidly growing Islamic microfinance industry.

The 2007 CGAP survey found fewer than 130 Islamic microfinance institutions (MFIs) and 500,000 customers respectively. Within five years, these figures more than doubled, reaching 256 MFIs and 1.3 million active clients. These figures are on the conservative side because they are based on data for 16 of the 57 OIC member countries (excluding economies such as the Islamic Republic of Iran, Malaysia, and Turkey, which have active Islamic finance industries).

In short, the estimated unmet demand for Shariah-compliant financial products, in conjunction with the rapid growth of Islamic MFIs, as well as the astonishing growth of the overall Islamic finance industry, all point to the growing attractiveness of Shariah-compliant financial products and the supply shortage of such products.

Religiosity also has an impact on the access of firms to finance in OIC countries. The number of Islamic banks per 100,000 adults is negatively correlated with the

proportion of firms identifying access to finance as a major constraint. The negative correlation is greater if one focuses on OIC countries and greater still if one focuses on a subset of OIC countries with a religiosity index above 85%.

These findings, which are mainly driven by small firms, suggest that increasing the number of Shariah-compliant financial institutions can make a positive difference in the operations of small firms (0–20 employees) in Muslim-populated countries by reducing the access barriers to formal financial services.

Efforts to increase financial inclusion in jurisdictions with Muslim populations require sustainable mechanisms to provide Shariah-compliant financial services to all residents, especially the Muslim poor, people who are living on less than $2 per day.

One obstacle is the lack of transparency and the absence of a broadly-accepted standardized process for assessing the compliance of financial institutions with Shariah guidelines, which makes it difficult for many individuals to distinguish between financial institutions that are operating based on Shariah specifications and institutions that are not. Another difficulty has been the lack of information and training on Islamic finance.

Finally, in their infancy and smaller in scale, Islamic financial products tend to be more expensive than their conventional counterparts, reducing their attractiveness.

This article is an abridged version of Box 1.4 in the Global Financial Development Report 2014: Financial Inclusion, Washington, DC, 2014

Islamic finance report card: Pakistan

by Rachel Latham and Andrew Shouler

Feature

Page 11

Amidst all the talk of Islamic finance hubs inter-nationally -- whether in the Middle East or the Far East or Europe -- there remains much yet to be achieved on purely a domestic basis in certain, key countries.

Indeed, can there be a nation that offers great-er potential for the growth of Islamic finance (IF) than Pakistan, which essentially needs to look no further than its own people for the realiza-tion of the sector’s critical objective of mutual development across society?

Pakistan has a population of 180 million (mak-ing it the world’s sixth most populous country), and is the second largest Muslim nation in the world (representing around 97% of its total population). Additionally, the large rural share, 63% of total, is evidently under-banked. Ac-cording to a 2011 World Bank study, roughly 90% of the entire population do not have an

account at a formal financial institution.

While, not surprisingly, Pakistan was among the pioneers of Islamic finance, progress in the 1980s and 1990s “met with limited success, largely due to slippages at the implementation and execution stage,” Mr Yaseen Anwar, then governor of the State Bank of Pakistan, admit-ted at a conference earlier this year.

Asian Development Bank’s Islamic Finance Team Leader Ashraf Mohammed refers to research citing an inadequate infrastructure in that era, and insufficiently trained human resources, factors that were rectified in the subsequent period by “a more practical and gradual approach”.

The re-launched official effort in 2001 envis-aged Islamic and conventional banks co-ex-isting, and enabling consumers to do banking

Page 12

within the system of their choice, which opened the way for the IF sector to succeed, based on demand-driven impulses.

With an annual growth rate of over 30% over the last five years, Shariah-compliant banking is now spread across 80 districts of the country, with a network of 1200 branches, and Islamic banking assets currently constitute 8-10% of both assets and deposits, according to data last year produced by State Bank of Pakistan (SBP), the central bank.

Key to this advancement has been the crucial role played by the SBP, with its introduction and application of key regulatory reforms and pru-dential measures to ensure financial stability and provide a comprehensive, multi-tiered frame-work to ensure the Shariah conformity of Islamic banks’ operations.

Today, the IF industry in Pakistan includes five fully-fledged Islamic banks and five takaful firms, with an additional twelve conventional banks offering services through Islamic windows. The central bank is also at an “advanced stage” towards issuing a detailed Shariah governance framework, which would outline roles for direc-tors, management and Shariah boards.

In the opinion of the Jeddah-based Islamic Development Bank (IDB), Islamic finance is “growing fast” in Pakistan, though facing “chal-lenges and constraints”, with demand “driven by multiple factors such as a faith-based appeal for the Muslim population, the potential to aug-ment financial engineering by blending it with socially- and ethically-responsive financing; [also to] service high-net-worth clients (whether Muslim or non-Muslim), and attract cross-border oil revenue surpluses”.

The IDB has noted the “pro-active policy” of the country’s central bank in this regard. Pledg-

ing itself to align its regulatory framework with international standards and best practices, SBP says it regularly reviews and evaluates the output of the IFSB, AAOIFI, and IIFM for potential use, keeping in view local circumstances and norms.

Recently the SBP adopted a global standard, from Bahrain-based AAOIFI, for Islamic bonds, to help issuers attract investors from the Gulf and elsewhere. The number of individual sukuk issues in Pakistan has eased in recent years, despite the rapid growth of issuance globally.

Now the SBP has developed a five-year Strate-gic Plan (2014-18) in consultation with all rel-evant parties in the IF sector, to take the industry to its next level of growth and development.

Part of this initiative involves a mass-media campaign to raise awareness of Islamic finance among consumers. “There still prevails a signifi-cant population that is either unaware of Islamic banking or has confusions and misconceptions about its current paradigm,” said then governor Anwar at the campaign’s initiation last year.

Meanwhile, the Ministry of Finance has set up a committee to explore areas to promote Islamic banking, including studying the conversion of conventional banks onto an IF basis, to submit recommendations by this year-end. Propos-als involving Islamic money markets, and issues of secondary market liquidity and maximizing equity-based financing rather than debt-based financing, will also be explored.

Collectively, the authorities’ aim is to expand Islamic banks’ share of the total banking sector to 15% by 2017.

Commenting on the nature, opportunity and out-look of the IF sector in Pakistan, London-based Edbiz Consulting has argued that the same strict-ness that has characterised the country’s view of

Page 13

Shariah compliance should enable it to become a global ‘centre of excellence’ for Islamic bank-ing and finance, by ensuring the authenticity of financial products. Chairman and CEO Humayon Dar has assessed that, in order to achieve parity of market share with conventional counterparts by 2025, Pakistan’s Islamic banks will have to grow by at least the recent rate of 35% per annum for the intervening period. “This is certainly a steep task, but a realistic target,” he says, and currently “the momentum is in the right direction”.

Besides the scale of the sector’s potential, one particular dimension that seems to hold promise and most immediate relevance is microfinance, which is especially attuned to the poverty allevia-tion aspect of Islamic finance, as well as focusing on the social and ethical concerns of self-respect, self-reliance and support for women and the most vulnerable members of society (see box).

The SBP’s governor, describing Islamic microfi-nance as a confluence of two industries, has said that financial inclusion is a key strategic goal of the central bank, and stressed that the industry should develop capacity to aid agriculture and SMEs particularly, both for participants in those sectors and for the economy as a whole, with “every sup-port and facilitation” from the central bank.

These options include the establishment of fully-fledged Islamic microfinance banks, Islamic mi-crofinance services by fully-fledged Islamic banks, and Islamic microfinance divisions in conventional microfinance banks. Allied with the institution’s inherent checks on the use of funds, the prospect for this segment of IF activity is “positive”, the governor stated.

Mr Anwar’s recent, acting successor at the State Bank of Pakistan, Mr Ashraf Wathra, has further underlined agri-financing as a policy priority, and indeed invited all key stakeholders to be on board

for Islamic finance’s overall, further growth and development.

Trends in Islamic Micro Finance (MF)

Islamic microfinance currently constitutes less than 1% of the microfinance industry globally, which has 126 institutions in fourteen countries, led by a 36% share located in the GCC.

In Pakistan microfinance and Islamic banking were initiated at the same time, in 2001, and subse-quently have grown significantly, although Islamic MF lags quite far behind broader Islamic finance.

While several institutions have launched Islamic microfinance products in Pakistan over the past few years, two providers offer a fully Shariah-compliant product line, one being Akhuwat, op-erating primarily on the disbursement of interest-free loans through donations, the other being the Wasil Foundation, which offers a range of Islamic finance services designed to encourage enterprise and the creation of value chains. According to the Pakistan Microfinance Network, there is “huge potential for these providers to expand outreach in this niche market”, by way of diversifying the product set as well as extending geographic coverage. However, there is a need for further funding sources, including the Waqf and Takaful models, “each with their own strengths and weaknesses in terms of viability in the Pakistan context”.Yet, recognition has grown among practitioners about the potential market for Islamic MF, and the scope therefore increased for meeting the needs of the underserved, with special attention to target-ing those who have previously declined conven-tional microfinance.

Sources: State Bank of Pakistan, Reuters, IDB, ADB, Edbiz Consulting, Kuwait Finance House, Islamic Finance Today, Pakistan Microfinance Network

GCCGulf markets defied the trend elsewhere, prolonging

2013’s extended rally, with all the region’s bourses

recording gains on conventional measures. Boosted

by the Expo bid and a storming real estate market,

Dubai has continued to stand out, up nearly 12% in

January, with the property component up nearly 20%.

Abu Dhabi’s index rose smartly too, by some 9%. In

both cases, the banking and financial service sectors

have prospered as well. The Saudi Tadawul index

improved moderately from the previously restrained

mood of last year-end, with the retail sector bouncing

back. Qatar attracted investors eyeing low stock

valuations, while Kuwait remained held back, down

slightly on the Islamic-based gauge, constrained

by political and investment project snags. Better

sentiment supported notable impetus in Bahrain’s

index.

Egypt / MENA

By late January the Egyptian stock index had climbed

to its highest level in almost three years, as the

market’s optimism grew in association with relative

political stability, even while pockets of violence

continued to spark. The EGX approached a 50% vault

since last year’s military takeover, though experiencing

volatility along the way. Rallies in support of likely

presidential contender and armed forces chief al Sisi

have offset the intermittent concerns, despite Cairo

being shaken by a series of explosions and the further

deaths of followers of ousted president Morsi. The

Egyptian pound has appreciated in this environment,

which has seen 98% approval by voters of a revised

constitution. Otherwise, a stock buyback by EFG-

Hermes lifted sentiment, as did news that Dubai’s

Majid Al Futtaim would be investing $2.3bn in the

retail sector in the coming years. Gulf SWFs are said

also to be interested.

South East AsiaAsian stocks were very mixed in the latest period,

ranging from the weakened Thai bourse, beset by

the country’s political disarray and violence, to a

resurgent Philippine index, as foreign funds regained

a degree of confidence following the US Fed-related

turbulence in emerging markets. Malaysia’s index well

represented the downbeat mood. While American

monetary policy proceeded with the gradual tapering

and emollient outlook of incoming Fed chair Janet

Stock Markets

Page 14

Yellen, both US and Chinese economic data were

uneven, limiting the scope for international optimism,

with credit prospects tightening in both cases, amid

uncertain growth conditions. Sentiment overall was

upheld to some extent by positive earnings results.

The Philippines and Indonesia especially rebounded

well from previous sell-offs. Thailand’s bourse kept

surprisingly stable overall considering continuing

protests, an emergency decree and an inconclusive

election in early February.

Rest of the World

Equity markets globally slipped in the period covered,

led by falls in Asia and other emerging markets. The

key factor promoting turbulence was the decision

of the US Federal Reserve to proceed further with

its tapering plans for monetary stimulus, that has

evidently been upholding overseas investment. In

some cases (Brazil, Turkey, South Africa, India)

countries have had to respond with higher interest

rates to support their currencies, creating another drag

on stocks’ performance. US indices were also affected

for a while, retreating from all-time highs. For Asia the

fluctuating conditions in Chinese credit policy, besides

economic sluggishness, were another key influence.

Japan’s indices also went conspicuously into reverse,

with uncertainty persisting over Abenomics. European

bourses remained modestly firm with the sense that

the worst of the financial crisis has been left behind,

and recovery may be consolidating. A more positive

mood emerged later, as Fed chair Yellen promised

policy continuity, interpreted as sustaining an easy

money stance. US corporate earnings were also

predominantly beating prior estimates.

Sources: GIC, Global Investment House, Bank Audi,

Bloomberg, Reuters, broker reports

Page 15

Islamic or Shariah compli-ant indices exclude indus-tries whose lines of busi-

ness incorporate forbidden goods or where debts/

assets ratios exceed 33%. The increasing popular-ity of Islamic finance has

led to the establishment of Shariah compliant stock

indices in many stock markets across the world, even where local Muslim populations are relatively

small, such as in China and Japan.

Volatility is a measure of un-certaincy of market returns. It is calculated as the standard deviation of the returns in the reported month. The formula for the standard deviation is:

σ=E[(X-μ)2]1/2

Islamic Stock Indices

Conventional Stock Indices

Evolution of Islamic Stock Markets in January 2014 for GCC, Far East, Middle East North Africa (MENA) and Rest of the World markets. Prices represent the closing price of the respective index at 31/1/2014. Percent-age Month-to-Month (MTM) Change and percentage Volatility. Source: Datastream

Evolution of Stock Markets in January 2014 for GCC, Far East, Middle East North Africa (MENA) and Rest of the World markets. Price represent the closing price of the respective index at 31/1/2014. Per-centage Month-to-Month (MTM) Change and percentage Volatility. Source: Datastream

Page 16

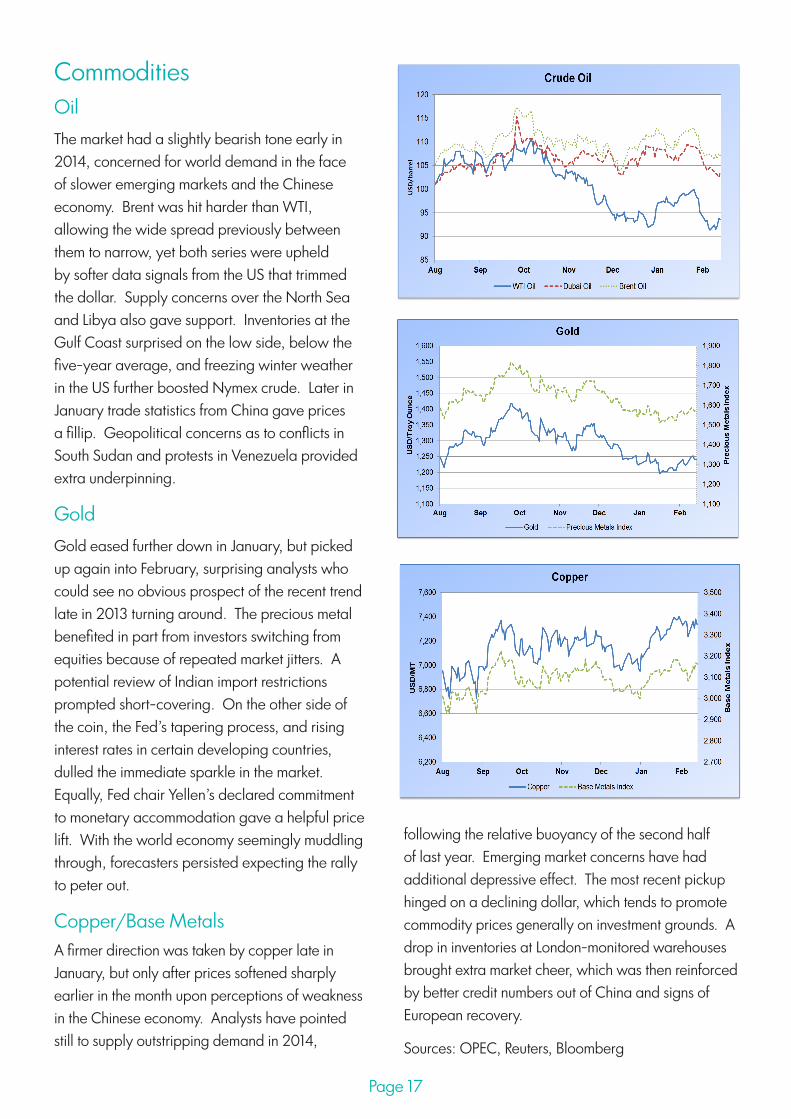

CommoditiesOilThe market had a slightly bearish tone early in 2014, concerned for world demand in the face of slower emerging markets and the Chinese economy. Brent was hit harder than WTI, allowing the wide spread previously between them to narrow, yet both series were upheld by softer data signals from the US that trimmed the dollar. Supply concerns over the North Sea and Libya also gave support. Inventories at the Gulf Coast surprised on the low side, below the five-year average, and freezing winter weather in the US further boosted Nymex crude. Later in January trade statistics from China gave prices a fillip. Geopolitical concerns as to conflicts in South Sudan and protests in Venezuela provided extra underpinning.

GoldGold eased further down in January, but picked up again into February, surprising analysts who could see no obvious prospect of the recent trend late in 2013 turning around. The precious metal benefited in part from investors switching from equities because of repeated market jitters. A potential review of Indian import restrictions prompted short-covering. On the other side of the coin, the Fed’s tapering process, and rising interest rates in certain developing countries, dulled the immediate sparkle in the market. Equally, Fed chair Yellen’s declared commitment to monetary accommodation gave a helpful price lift. With the world economy seemingly muddling through, forecasters persisted expecting the rally to peter out.

Copper/Base MetalsA firmer direction was taken by copper late in January, but only after prices softened sharply earlier in the month upon perceptions of weakness in the Chinese economy. Analysts have pointed still to supply outstripping demand in 2014,

Page 17

following the relative buoyancy of the second half of last year. Emerging market concerns have had additional depressive effect. The most recent pickup hinged on a declining dollar, which tends to promote commodity prices generally on investment grounds. A drop in inventories at London-monitored warehouses brought extra market cheer, which was then reinforced by better credit numbers out of China and signs of European recovery.

Sources: OPEC, Reuters, Bloomberg

GCC

Whereas emerging market bonds, like stocks, have been hit by the US Fed’s monetary tapering plans, creating a background of considerable volatility, Gulf trading kept a better profile, with only limited correlation with Treasury benchmarks, and spreads narrowing. Although defensive at the start of the year, regional investors were then looking to add to their books again, though focused on yield. Technical indicators were aligned to assist, and underlying demand was strong, but tending to wait for new issuance. Names such as DEWA and Bahrain were well bid, while much activity was oriented to Kipco’s 5-year issue. International accounts added to the interest further along the credit yield curve. A deal to restructure Dubai’s $10bn debt load helped sentiment.

Egypt / MENA

Similar momentum was found in the broader region, with the North African bond market showing well, as bonds from Egypt and Morocco were sought by both local and international buyers. The gradual restoration of what investors perceive as a workable political framework promoted trade in Egypt’s 2020 and 2040 eurobond issues, rallying above par. National Bank of Egypt’s issue also improved. January saw foreign exchange reserves rise for the first time in several months, and the government was in talks to secure further aid from the Gulf states. Credit default swaps (CDS) have dropped by over 400 basis points since the military takeover. Economic growth may reach 3.5% this year, according to the finance ministry.

Malaysia / South East Asia

Trends in Asian bonds were less convincing, having being revealed to be so dependent on US monetary policy, where the easing cycle has been curtailed. Initially in the period covered regional currencies reflected the retreat of international investors, typically holding 20-30% of the bloc’s

Bonds and CDS markets

sovereign debt, as they had drawn back to the dollar as safe haven. Borrowing costs locally were on the rise as expectations grew of higher yields over time across dollar-related zones. Inflation data also brought pressure to bear, for instance in Malaysia and the Philippines. Malaysian bonds fared reasonably well on a comparative basis, without the uncertainty of elections as are due in Thailand and

Page 18

Credit Default Swap Markets

Sovereign Bond Markets

Evolution of Bond Markets in January 2014 relative to the previous month. The table reports the price index on which the MTM Change is calculated (month-to-month) and the Yield of sovereign bond maturities typically between 6 months and 25 years. Data as at 31/1/2014.

Evolution of CDS Spreads in January 2014 relative to the previ-ous month. The index reported here represents the average ba-sis points (bp) of a 5-year CDS for protection against sovereign bonds. Data as at 31/1/2014. MTM Change refers to the change relative to the previous month.

Indonesia this year. Some improved data on Chinese growth and credit figures lifted Asian currencies later in the period, aiding market reaction to the collective sell-off that some saw as overdone.

Global Benchmarks

Though still in a negative mood during January, at the global level key benchmark series were strengthened into February by signs that assumptions about quickening economic recovery were not so well founded. Bonds for a while advanced in rotation with stocks, which dipped sharply. US data such as car sales, manufacturing and employment generated doubts about the revival, and encouraged thoughts of central bank restraint on interest rate hikes, as were then confirmed by policy statements. The US lead was followed by both core and peripheral European trades, as well as JGBs, with the sense that both the real economy and monetary settings were somewhat limited in giving guidance. In recent weeks the jury has remained out in terms of the market’s likely direction.

Source: GIC, Invest AD, Bloomberg, Bank Audi, ADB online, broker reports

Page 19

Islamic Bonds (Sukuk)

The sukuk secondary market was soft in the early part of the year, reflecting not only the retreat of conventional instruments but also that of emerging markets, and doubts for Gulf energy producers over oil prices.

Investors were looking for returns instead from primary issuance, which has been expected by analysts (S&P, Fitch Ratings) and by banks (e.g. HSBC) to put in a strong performance this year.

Activity was focused most recently on the issuance of Dubai Investment Park’s $300 million debut sukuk, with orders finalized at well over $4bn, launched at 35bps inside guidance at 265bps over mid-swaps, yielding 4.296%.

The deal was viewed as well-timed, into a market lacking Middle East paper, and likely to trigger other issuers from the region. It benefited from fast-improving sentiment towards Dubai, buoyed by its rapidly rebounding real estate sector. The company is owned by Dubai Investments, and focused mainly on leasing and property management.

Sukuk is the Arabic name for financial certificates, but commonly refers to the Islamic equivalent of bonds. Since fixed income, interest bearing bonds are not permissible in Islam, Sukuk securities

are structured to comply with the Islamic law and its investment principles, which

prohibits the charging, or paying of interest. Financial assets that comply with the Islamic law can be classified in ac-

cordance with their tradability and non-tradability in the secondary markets.

DIP’s main asset is a mixed industrial, commercial and residential block, next to the World Expo 2020 site, according to documentation. European accounts were much in evidence in the sale, also Islamic liquidity.

Conditions otherwise were relatively quiet.

Indonesia announced it would sell retail Islamic bonds this month, offering individual investors returns clearly above the interest rates given by the country’s leading banks. They would carry a coupon rate of 8.75% per annum, compared with bank deposit rates of 5-7.75%. The government auctioned a combination of 6-mth and 29-year project-based sukuk in mid-February.

Meanwhile, the UK Treasury (finance ministry) declared its proposed sukuk issuance would take place either in 2014 or 2015 by way of a syndicated offering, having previously announced plans for a £200m launch.

Sources: GIC, Invest AD, Bloomberg, Reuters, broker reports

Page 20

Perspective

A flurry of reports recently about the prospects for the sukuk market in 2014 all expect a pick-up in pace, for a number of reasons.

Standard & Poor’s envisages the industry expanding again, following a dip in volumes by some 13% in 2013, as the market digested the promised tapering of easy US monetary policy. The agency forecasts total issuance to exceed $100bn for the third successive year “if yields remain attractive”, driven by corporate and infrastructure deals in the Gulf, and the resumption of Malaysia’s investment programme.

The UAE and Saudi Arabia are anticipated to lead the way in the GCC, “as regulators continue to minimize barriers in the market”. Besides impetus from project spending, economic growth based on $100 oil prices will encourage banks as both borrowers and investors, also adjusting their capital bases to meet Basel 3’s gradual implementation. In Malaysia -- whose sukuk offerings dropped by 25% last year, though maintaining a dominant share of total -- a broad investor base and liquid market give underpinning. A phase of government cutbacks should be eased by GDP growth exceeding 5% in 2014, with demand for ringgit issues liable to be buoyant.

S&P made note too of investors seeking sukuk in non-traditional markets, and that “Africa may soon offer a fresh alternative”. Senegal and South Africa have been looking at issuing sukuk, while Tunisia, Egypt, and Morocco have been finalizing their legal frameworks to do so. Multilateral institutions may further stimulate sukuk activity, either themselves Islamic or representing countries with large Muslim populations. The IDB, ADB, and other forums, “are natural and prominent players”, aiming “to facilitate

intermediation and integration”, so benefiting Islamic debt capital markets.

Yet, S&P suggests that “without standardization and [the] architecture to support the industry, it is unlikely [to] reach a new dimension”, implying that official attention is necessary to complement potential market supply and demand.

Fitch Ratings, meanwhile, says Gulf nations’ efforts to become Islamic finance hubs “is also likely to spur sukuk issuance”. Last year’s decline was likely “to be a blip in the longer-term trend of steady growth,” it said. Fitch noted “evidence of increasing market efficiency”, with structuring costs having fallen significantly, and dealmaking times down “from as much as six months to a few weeks”. It mentioned, however, the caveat of “the lack of legal precedent over investors’ ability to enforce rights in many jurisdictions”.

Reported by Bloomberg, HSBC suggested issuance would probably rebound to a record level this year, echoing the idea of geographic dispersion, and observing banks trying to tailor conventional products to meet Shariah’s requirements, as in perpetual sukuk. US rate volatility might affect timing, but the pool of Islamic liquidity “remained strong”, and might be orientated to issuers in local currencies instead.

Moody’s has remarked on the increasing internationalization of sukuk, and “growing investor comfort with these instruments”. Longer maturities beyond 5-7 years are appearing, and enhancing the sector’s appeal. Like S&P, though, Moody’s saw the global market as “likely to remain fragmented”, a view which reflects awareness that differing locations around the world are tending to compete as much as co-operate, whether for a niche or a comprehensive role, chasing market share in this growing field.

Outlook for sukuk gains attention by Andrew Shouler

Page 21

Page 22

call for papers4th Islamic Banking and Finance Conference (IBF 2014)

23rd to 24th June 2014Venue: Lancaster University Management School

Keynote Speaker

Th orsten BeckProfessor of Banking and Finance, Cass Business School

The constraints applied by Islamic banks rendered them more resilient in the recent fi nancial crisis compared to their con-ventional counterparts. This has attracted the attention of market participants and researchers to their liquidity buffers, leverage ratios, managerial effi ciency and bespoke fi nancial products. Islamic banking products are now offered in more than twenty countries and their expanding suite includes bonds, equity indices and insurance. The sector is estimated to exceed $1trillion in value, while growing at about 15% per annum. Among many issues still subject to debate is the purity of Islamic fi nance in practice, given the need to compete and to operate with customers whose expectations have been formed by conventional banking practices.EIBF centre at Aston Business School in collaboration with GOLCER Lancaster University Management School is organis-ing a conference on Islamic Banking and Finance. The conference aims to provide a forum for an exchange of views on recent developments and to identify key issues/challenges underlying the paradigm of Islamic Banking and Finance in the 21st century.

Original contributions are invited on any of the listed topics:

• Financial risk and stability • Risk Management, Accountability and auditing• Transparency, governance and corporate social responsibility • Competition• Earnings management and impression management • Microfi nance and SMEs• Performance, effi ciency and convergence • Behavioural fi nance• Mutual funds

Special IssueJournal of Economic Behaviour and Organisation (JEBO)

Ana Timberlake Best paper Research Award: £500

Co-editors for the JEBO Special IssueOmneya Abdelsalam, Aston UniversityMohammed El-Komi, American University of CairoAna-Maria Fuertes, Cass Business SchoolStergios Leventis, International Hellenic UniversityGerald Steele, Lancaster University

Scientific committeeOmneya Abdelsalam (Aston University), Nathan Berg (University of Otago), Rachel Croson (University of Texas at Dallas), Mahmoud El-Gamal (Rice University), Mohamed El-Komi, (American University Cairo), Meryem Fethi (Leicester University), Ana-Maria Fuertes (Cass Business School), Mohamed Shahid Ibrahim (Bangor University), Marwan Izzeldin (Lancaster University), Jill Johnes (Lancaster University), Stergios Leventis (In-ternational Hellenic University), Kent Mathews (Cardiff Business School), Khelifa Mazouz (Bradford Business School), Philip Molyneux (University of Bangor), Andrew Mullineux (University of Bournemouth), Steven Ongena (University of Zurich), Vasileios Pappas (Lancaster University), Mo-hamed Shaban (Leicester University), Mustapha Sheikh (Leeds University), Gerald Steele (Lancaster University), Emili Tortosa-Ausina (Jaume I University), Mike Tsionas (Lancaster University)

Conference Organisers: Dr Omneya Abdelsalam (Aston University), Dr Marwan Izzeldin (Lancaster University)

Important DatesConference Abstract Submission

Conference Full Paper Submission

Submission for JEBO Special Issue

Special Issue Publication

31st March 2014 27th April 2014 1st October 2014 October 2015

Statistics • Econometrics • ForecastingT IMB ERL A K E

For paper submissions please email Marwa Elnahass: [email protected]

Page 23

Global Forum on Islamic Finance 2014 ConferenceDevelopments and The Way Forward

March 10-12, 2014Lahore, Pakistan

Organised byDepartment of Management Sciences

COMSATS Institute of Information Technology (CIIT)http://gfif.citilahore.edu.pk/

About the Conference The 2nd Global Forum on Islamic Finance (GFIF) will consider the spectacular political and socio-economic developments that we have been witnessing, and their probable effects on the performance and future posi-tion of Islamic financial institutions, the regulatory set-ups and popularity of Islamic products being offered to the public, governments and business.

Much has been said about the phenomenal growth of the Islamic finance industry over the past decade and the growth rates have been outstandingly impressive. Industry supporters have also lauded how successfully Islamic banking has largely weathered the global economic crisis that engulfed the conventional banking industry. However, despite these achievements, much still needs to be done if the industry is to truly flourish and play its part on the world stage.

On this great global forum, COMATS Institute of Information Technology will provide a platform to the leading industry players, academics and researchers to address key factors for achieving scale through novelty to strengthen the Islamic financial institutions and ensure long-term industry stability; GFIF 2014 will thus assist industry players to innovate the next generation of Islamic finance solutions that will meet the increas-ingly complex needs of corporate borrowers, consumers, issuers and investors; and create the conditions that will enable a more globally harmonized footprint for Islamic financial institutions - that, if achieved, will propel the Islamic finance industry to the next level of success.

GFIF welcomes participants from academia, research institutes, corporate world and government sector to share their experiences, learning and research. GFIF comprises various sessions to make it the most compre-hensive experience for its attendees.

Conference Topics

• Islamicprojectfinancing • Islamicwealthmanagement

• Socially-responsibleinvestmentstrategy • StructuringIslamicsecuritization

• Shariah-compliantriskmanagement • Marketpenetrationinnon-Islamiccontexts

• Islamicmicrofinance • Businesscycles,financialstability&crisis

• Management,leadershipandgovernanceofIslamicfinancialservicesproviders

• PrinciplesofIslamicjurisprudenceandlegalmaxims

• CorporatesocialresponsibilityofIslamicfinancialinstitutions

• HousingfinanceandShariah-compliantmortgageproducts

Research TeamGerry Steele

Vasileios [email protected]

Marwa El [email protected]

Marwan IzzeldinDirector

DISCLAIMER

This report was prepared by Gulf One Lancaster Centre for Economic Research (GOLCER) and is of a general nature and is not intended to provide specific advice on any matter, nor is it intended to be comprehensive or to address the circumstances of any particular individual or entity. This material is based on current public information that we consider reliable at the time of publication, but it does not provide tailored investment advice or recommendations. It has been prepared without regard to the financial circumstances and objectives of persons and/or organisations who receive it. The GOLCER and/or its members shall not be liable for any losses or damages incurred or suffered in connection with this report including, without limitation, any direct, indirect, incidental, special, or consequential damages. The views expressed in this report do not necessarily represent the views of Gulf One or Lancaster University. Redistribution, reprinting or sale of this report without the prior consent of GOLCER is strictly forbidden.

Andrew ShoulerEditor