Embed Size (px)

Citation preview

Aging and Disability Resource Connection

FEDERAL HEALTH REFORMOPTIONS TRAINING

Utah Heath Policy Project 4/19/11

Brief overview of the Patient Protection and Affordable Care Act

Overview of Medicare and Changes Overview of Medicaid and Changes Dual Eligible Long Term Care Accountable Care Organization (ACO) Preventive Services Fraud, Waste, & Abuse Future of health reform

Overview of Today's Priorities

Expand Coverage

Contain Costs

Ensure Quality

Goal of Health Reform

Private Health Insurance Market Reform Medicaid Expansion Establishes State Exchanges: Premium

Subsidies to help people buy insurance (up to 400% of FPL- sliding scale)

Major Changes

Part A –Hospital Insurance • Inpatient care, including skilled nursing

*Paid for by payroll taxes (Concerns about future solvency)

Part B – Outpatient Health Insurance Pays for additional medical services (like

doctors visits, diagnostic tests, and outpatient care) * Financed 75% by general revenues, 25% by monthly premiums ($110.50)

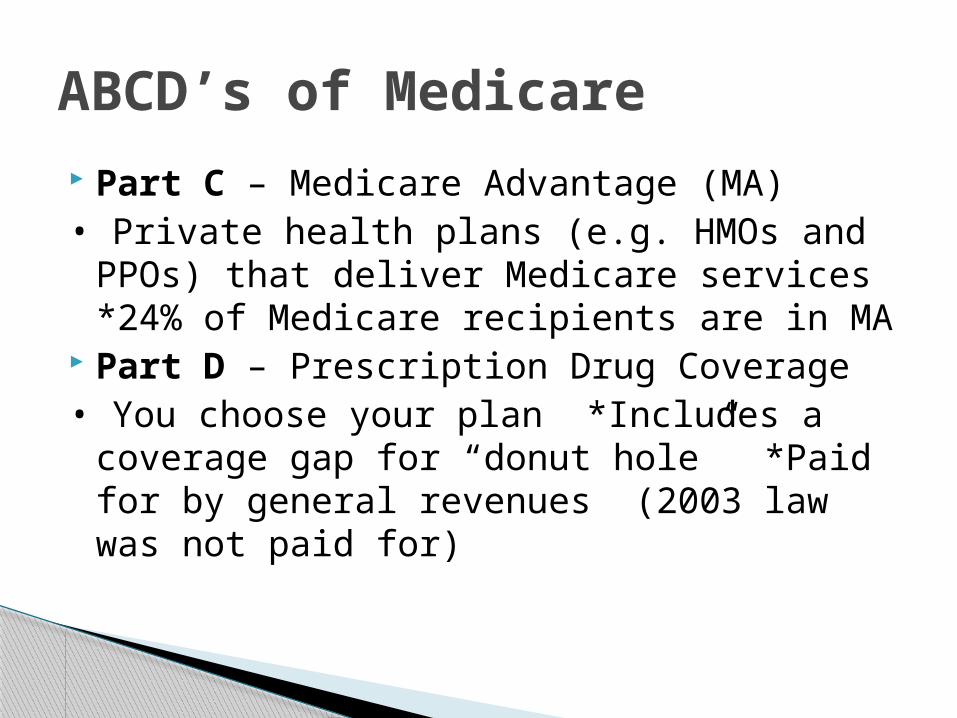

ABCD’s of Medicare

Part C – Medicare Advantage (MA)• Private health plans (e.g. HMOs and PPOs)

that deliver Medicare services *24% of Medicare recipients are in MA

Part D – Prescription Drug Coverage• You choose your plan *Includes a coverage

gap for “donut hole” *Paid for by general revenues (2003 law was not paid for)

ABCD’s of Medicare

Improvements in Benefits◦ Gradually closes Medicare prescription drug

coverage gap (“doughnut hole”)◦ Provides new annual wellness visit with

personalized prevention plan◦ Eliminates cost sharing for prevention services◦ Boosts payments for primary care

Medicare Savings◦ Reduces payments to Medicare Advantage plans◦ Reduces payments for hospitals and other medical

providers (not physicians)◦ Creates new Independent Payment Advisory Board

Summary of changes to Medicare

Delivery system reforms◦Shared Savings/Accountable Care Organizations◦New Center for Medicare and Medicaid

Innovations◦New Coordinated Health Care Office within CMS

for dual eligibles◦Numerous programs, pilots, demonstrations to

improve quality and efficiency

New revenues◦Income-related premiums◦Increase in payroll tax

Summary of changes to Medicare

Increased Revenues Higher payroll taxes for wealthy workers

($200/$250,000) Higher Part D premiums for 5% of wealthy Medicare

beneficiaries ($85/$170,000) Reduced Spending Slower growth in payments to providers (not doctors) Reduction in over-payments to Medicare Advantage

plans Average yearly Medicare spending ncreases down

from 6.8% to 5.7% NO CUTS in basic benefits

Financial Changes to Medicare

MA plans are paid about $1,100 more per person than people in original Medicare (13% higher)

Payments frozen in 2011 Beginning in 2012, these overpayments will

be gradually reduced

Changes to Medicare Advantage Plans

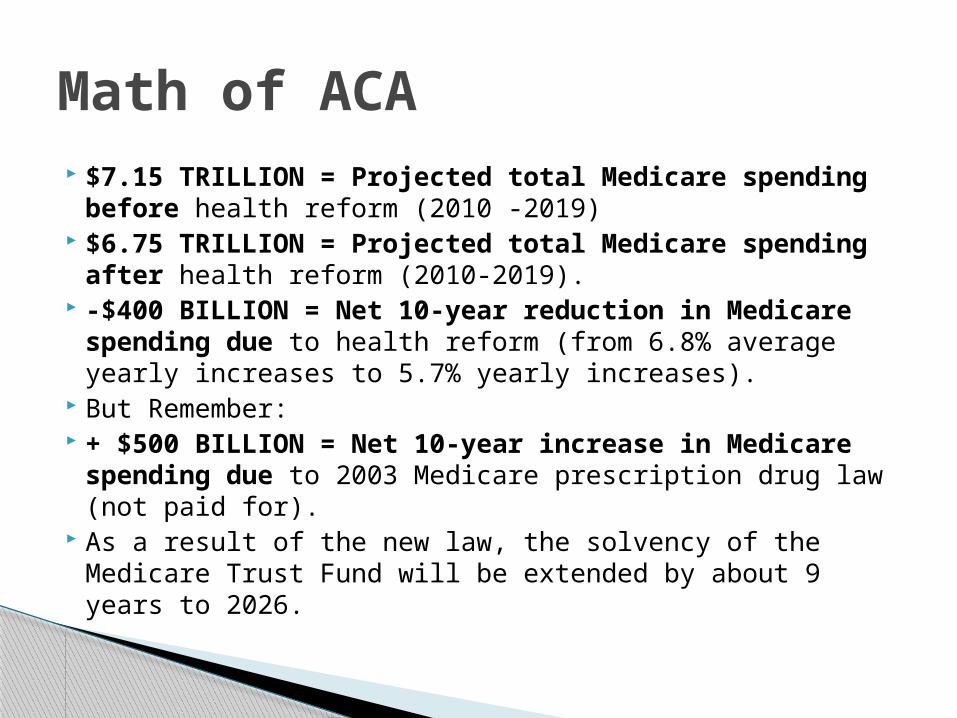

$7.15 TRILLION = Projected total Medicare spending before health reform (2010 -2019)

$6.75 TRILLION = Projected total Medicare spending after health reform (2010-2019).

-$400 BILLION = Net 10-year reduction in Medicare spending due to health reform (from 6.8% average yearly increases to 5.7% yearly increases).

But Remember: + $500 BILLION = Net 10-year increase in

Medicare spending due to 2003 Medicare prescription drug law (not paid for).

As a result of the new law, the solvency of the Medicare Trust Fund will be extended by about 9 years to 2026.

Math of ACA

Medicare Prescription Drug Improvements Better Preventive and Chronic Care Greater Access to Home and Community

Long-Term Care Services Other Improvements for Seniors (Early

Retirees, Primary Care, Elder Abuse, Workforce)

How does this impact you?

Changes in Medicare Advantage (MA) Plans? No one knows, but: Some plans may

eventually reduce benefits or increase premiums

New bonuses to reward high quality care New consumer protections to limit out-of-

pocket costs

Medicare Advantage

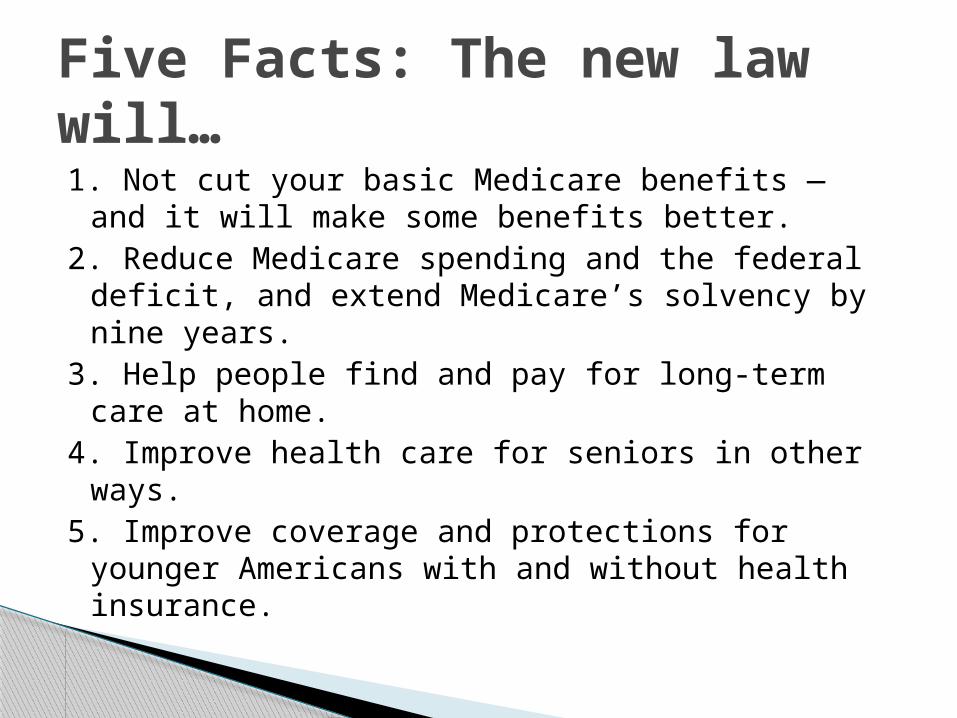

1. Not cut your basic Medicare benefits — and it will make some benefits better.

2. Reduce Medicare spending and the federal deficit, and extend Medicare’s solvency by nine years.

3. Help people find and pay for long-term care at home.

4. Improve health care for seniors in other ways.5. Improve coverage and protections for younger

Americans with and without health insurance.

Five Facts: The new law will…

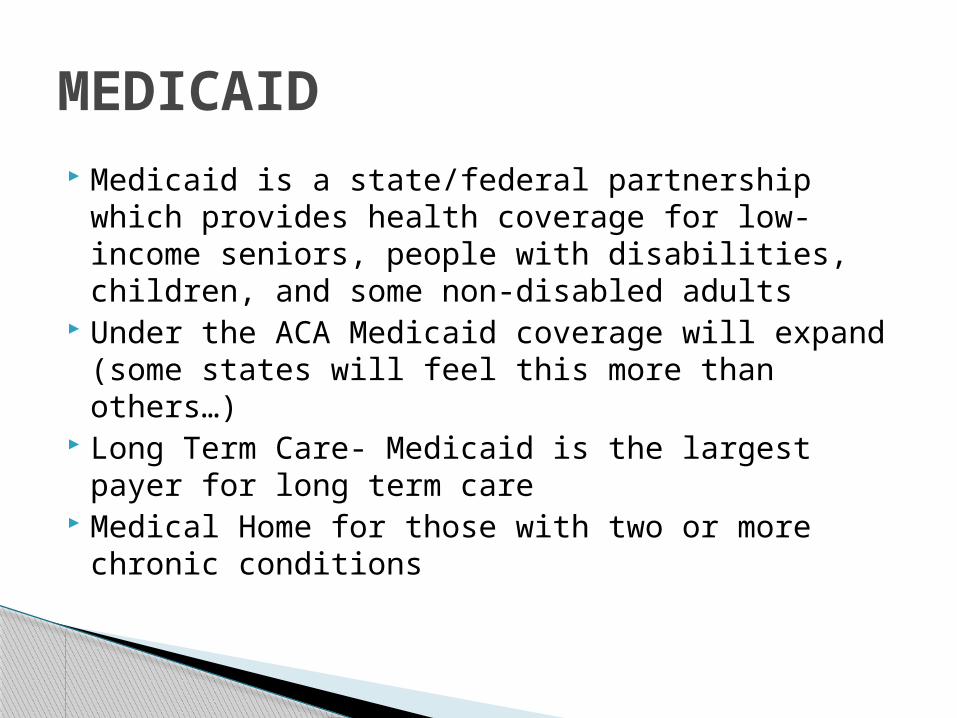

Medicaid is a state/federal partnership which provides health coverage for low-income seniors, people with disabilities, children, and some non-disabled adults

Under the ACA Medicaid coverage will expand (some states will feel this more than others…)

Long Term Care- Medicaid is the largest payer for long term care

Medical Home for those with two or more chronic conditions

MEDICAID

Medicaid and CHIP Income Eligibility in Utah

In 2010 Under the ACA

Children 200% FPL($44,100 / family of four)

200% FPL

Parents 44% FPL($9,702 / family of four)

133% FPL($29,328 / family of four)

Childless adults N/A 133% FPL

($14,404 / individual)

© Utah Health Policy Projectwww.healthpolicyproject.org

Medicaid Financing

© Community Catalyst 2010

Calendar Year FMAP for Newly Eligibles

2014 100%

2015 100%

2016 100%

2017 95%

2018 94%

2019 93%

2020 and beyond 90%

© Utah Health Policy Projectwww.healthpolicyproject.org

Dual Eligible's: A Crisis in Quality: A Fragmented System

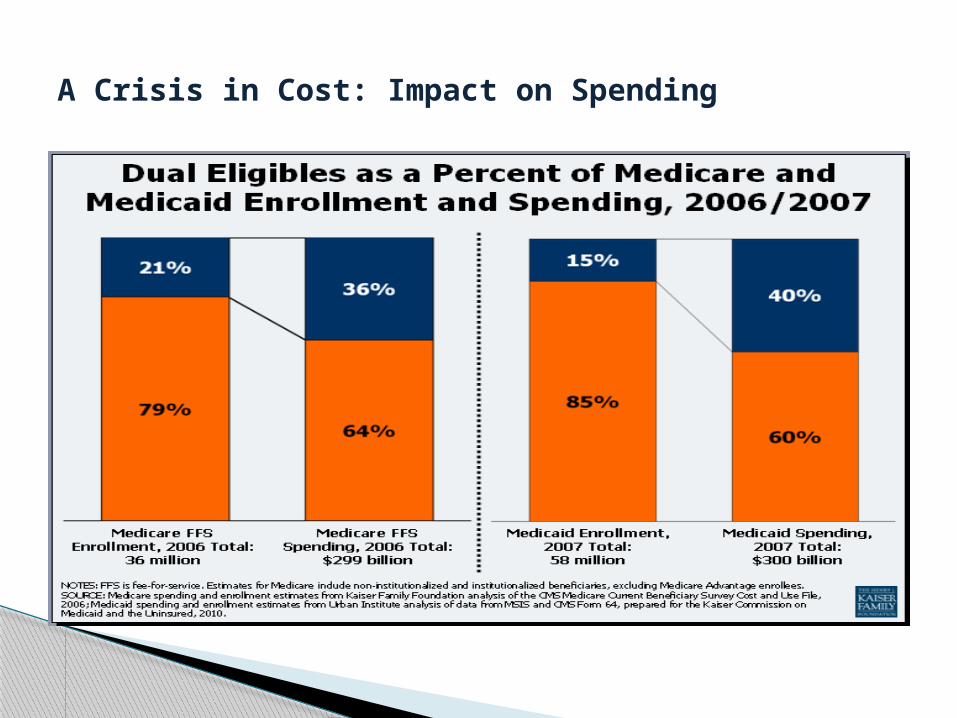

A Crisis in Cost: Impact on Spending

Improves Long-Term Care Choices • New tools and resources in the Elder Justice

Act, which was included in the new law, will help prevent and combat elder abuse and neglect, and improve nursing home quality.

• Individuals on Medicaid will receive improved home- and community-based care options, and spouses of people receiving home- and community-based services through Medicaid will no longer be forced into poverty.

LONG TERM CARE

About 10 million Americans need long-term care because they require help with daily activities such as bathing, dressing, eating, or walking. This kind of care can be provided at home, in the community, or in nursing homes.

Medicare does not cover the costs of long-term care, and most people have not purchased a private long-term care insurance policy. As a result, millions of Americans rely on family and friends for support to stay at home or are forced to spend their life savings on expensive and unwanted nursing home care.

What is Long Term Care

Health reform includes several provisions to help people find and pay for long-term care at home and in their communities, so they can avoid going into a nursing home. These provisions include changes to Medicaid and the CLASS program.

How does health reform affect long-term care?

Medicaid is a state-federal program that provides long-term care benefits to individuals with modest incomes and assets (excluding a home).

Right now, almost three-quarters of Medicaid long-term care spending goes for care in nursing homes and other institutions—even though most people would prefer to receive help at home, which is also less expensive.

How does the law affect Medicaid long-term care programs?

These include: A new Community First Choice option that gives states extra federal money

to provide home and community services to people who would otherwise need nursing home care (effective in 2011). [Sections 2401-2403]

A new State Balancing Incentives program that will improve standards for home care programs, encourage states to shift funds away from nursing homes, and increase the number of people receiving home and community services (effective in 2011). [Sections 2401-2403]

Spousal impoverishment protections to ensure that spouses of people needing Medicaid home and community services are no longer forced to spend-down their savings into poverty before getting help. While amounts vary by state, spouses will be able to keep half of the couple's countable assets—up to a ceiling as high as $110,000—with a maximum monthly income allowance of about $2,700 (effective in 2014). [Section 2404]

Added funding for better information and referrals to help people find and pay for long-term care and for programs to identify and support nursing home residents who can return to their homes.

***The first two new provisions are options to the states, and it's hard to predict how many will adopt these changes.

Several provisions in health reform offer states incentives to make long-term care available to people at home instead.

CLASS PROGRAM How the CLASS Program Works If you are age 18 or older, employed, and your employer participates

in the program, you will be enrolled in CLASS automatically unless you "opt out" by choosing not to participate. Your premiums will be paid through payroll deductions.

If your employer doesn't participate in the CLASS program, or if you are self-employed or have more than one employer, you will be able to purchase this insurance on your own.

Once you have paid the premiums for at least five years, have worked at least three of those initial five years, have a qualifying disability, and meet other eligibility requirements, you will be eligible for benefits.

Cash benefits will be paid if you have a qualifying disability that your health care provider certifies is expected to last for more than 90 days. You will receive payments for as long as you remain eligible, which depending upon your disability could be for your lifetime.

CLASS program enrollments will likely begin in 2012 or 2013. Federal officials will provide additional details, such as premium costs and the amount of cash benefits, as the new insurance program is implemented.

Participating in CLASS increases your options to live more independently if you have or develop a qualifying disability and meet the other eligibility requirements.

You can use the CLASS program's cash benefit, along with assistance from other public and private programs, your personal savings, care from family and friends, and private long-term care insurance, to help protect your financial security.

CLASS PROGRAM

Under the proposed rule, an ACO refers to a group of providers and suppliers of services (e.g., hospitals, physicians, and others involved in patient care) that will work together to coordinate care for the patients they serve with Original Medicare (that is, those who are not in a Medicare Advantage private plan). The goal of an ACO is to deliver seamless, high quality care for Medicare beneficiaries. The ACO would be a patient-centered organization where the patient and providers are true partners in care decisions.

Accountable Care Organizations

• Uncoordinated Care• Lack of Chronic Care Management• Poor Communication • Duplicative Tests

Consumers Face Considerable Challenges in Today’s Health Care System

• 77% of 65+ have multiple chronic conditions

• Those with 5+ chronic conditions average 37 doc visits, 14 different docs, and 50 separate Rx drugs

• Patients report duplicate tests and

procedures, conflicting diagnoses, contradictory medical information, and inadequate info about potential Rx interactions

Older Chronically Ill Patients Have an Even Harder Time

• Consumers need and want a better system for delivering health care

• New care models like ACOs are potentially promising approaches to improve health care delivery and payment – if done right

• Sec. 3022 - new Medicare FFS Shared Savings Program (ACO)

• Intended to Coordinate A/B Services • Encourages high quality and efficient

service delivery

New Ways of Care Delivery Needed to Address These Challenges

New coverage for Wellness Visits and Personalized Prevention Plans. This includes a health risk assessment, screening schedules for preventive services, BMI, etc…

Grade A and B recommended by the U.S. Preventive Services Task Force without asking you to pay a copayment or meet your deductible. Examples include: Alcohol misuse, blood pressure, cholesterol, diabetes, diet, certain cancer screenings, etc…

Preventive Services

Inhanced funding and enforcetment to reduce fraud waste and abuse in health care system

Medicare and Medicaid Health Care Fraud & Abuse Control Fund

Oversight of Durable Medical Equipment companies, nursing homes, hospitals, etc…

Requirement for reporting suspected fraud Etc…

Fraud, Waste, and Abuse

No more discrimination based on health status (no denial for people with pre-existing conditions)

No more capping annual and lifetime benefits

No more recision- or dropping coverage when people need care

Pre-existing Condition Insurance Pools Essential Benefits Package Increase Incentive for Primary Care

Physicians

General Provisions also Impact Aging and Disabled Communities

Medicare Benefits will NOT be cut

There are NO DEATH PANELS in the health reform law

Dispelling Myths

2012 Budget Plan- Big changes proposed for Medicare and Medicaid

Utah State Medicaid Reform

Efforts to Repeal

Supreme Court Ruling

FUTURE IS UNKNOWN…

Future of Health Reform