Embed Size (px)

Citation preview

Federal Policies and the Medical DevicesIndustry

November 1984

NTIS order #PB85-199552

Recommended Citation:Federal Policies and the Medical Device Industry (Washington, D. C.: U.S. Congress, Officeof Technology Assessment, OTA-H-230, October 1984).

Library of Congress Catalog Card Number 84-601125

For sale by the Superintendent of DocumentsU.S. Government Printing Office, Washington, D.C. 20402

Foreword

In recent decades, both the range of medical devices and the industry that manufac-tures them have greatly expanded. At the same time, there has been growing Federalinvolvement in the U.S. health care system. The Medicare and Medicaid programsestablished in the 1960s have increased the market for medical technologies and havegreatly influenced patterns of payment and use. The Federal Government instituted apremarketing approval process for medical devices in 1976. Other activities, such asfunding research and development, regulating the providers of medical devices, andproviding medical care for veterans, have involved the Government in the develop-ment and purchase of medical devices.

Since the late 1970s, congressional committees have been interested in the effectsof such Federal policies on the companies that manufacture medical devices. In early1982, this interest resulted in a request from the Senate Labor and Human ResourcesCommittee to the Office of Technology Assessment (OTA) for an assessment of Federalpolicies and their effect on the medical devices industry. The Senate Veterans’ AffairsCommittee endorsed the request and expressed particular interest in the activities ofthe Veterans Administration regarding device development and procurement.

In preparing this report, OTA staff drew upon the expertise of members of the ad-visory panel for the study, members of the OTA Health Program Advisory Commit-tee, and experts in health policy, industry, research and development, economics, healthadministration, and medicine. Drafts of the final report were reviewed by the advisorypanel, chaired by Dr. Richard R. Nelson; OTA’s Health Program Advisory Commit-tee, chaired by Dr. Sidney S. Lee; and other individuals and groups with expertise inthe area. We are grateful for their assistance. Key OTA staff involved in the prepara-tion of the document were Jane E. Sisk, Cynthia P. King, John C. Langenbrunner,Katherine E. Locke, Lawrence H. Miike, and Judith L. Wagner.

U JOHN H. GIBBONSDirector

,..Ill

Advisory Panel for Federal Policies and The Medical Devices Industry

Richard R. Nelson, ChairInstitute for Social and Policy Studies, Yale University

New Haven, CT

William F. BallhausInternational Numatics, Inc.Beverly Hills, CA

Ruth FarriseyMassachusetts General HospitalBoston, MA

Peter Barton HuttCovington & BurlingWashington, DC

Alan R. KahnConsultantCincinnati, OH

Grace KraftKidney Foundation of the Upper MidwestCannon Falls, MN

Joyce LashofSchool of Public HealthUniversity of CaliforniaBerkeley, CA

Penn LupovichGroup Health AssociationWashington, DC

Victor McCoyParalyzed Veterans of AmericaWashington, DC

Robert M. MoliterMedical Systems DivisionGeneral ElectricWashington, DC

Louise B. RussellThe Brookings InstitutionWashington, DC

Earl J. SaltzgiverForemost Contact Lens Service, Inc.Salt Lake City, UT ●

Rosemary StevensDepartment of History and Sociology of ScienceUniversity of PennsylvaniaPhiladelphia, PA

Allan R. ThiemeAmigo Sales, Inc.Albuquerque, NM

Eric von HippelSloan SchoolMassachusetts Institute of TechnologyCambridge, MA

Edwin C. WhiteheadTechnicon Corp.Tarrytown, NY

OTA Project Staff—Federal Policies and the Medical Devices Industry

Jane E. Sisk, Project Director

Cynthia P. King, Analyst

John C. Langenbrunner, Analyst1

Katherine E. Locke, Research Assistant

Lawrence H. Miike, Senior Associate

Elaine J. Power, Intern2

Judith L. Wagner, Senior Analyst

Kerry Britten Kemp, Health and Life Sciences Division Editor

Virginia Cwalina, Administrative Assistant

Rebecca I. Erickson, Secretary/Word Processing Specialist

Brenda B. Miller, Word Processor/P. C. Specialist

Clyde J. Behney, Health Program Manager

Roger C. Herdman3 and H. David Banta,4 Assistant Director, OTAHealth and Life Sciences Division

Contractors

James R. Barth and Joseph J. Cordes, George Washington University

Dennis J. Cotter, Georgetown University Health Policy Center

Pony M. Ehrenhaft, Washington, DC

Hope S. Foster, O’Connor & Hannan, Washington, DC

John Hutton, University of York, England

IMS America Ltd., Rockville, MD

Kaye, Scholer, Fierman, Hays & Handler, Washington, DC

Kornmeier, McCarthy, Lepon & Harris, Washington, DC

Anthony A. Romeo, University of Connecticut

1Until November 1983.2Summer 1983.3From December 1983.4Until August 1983.

v

Contents

Chapter Page

1.

2.

3.

4.

5.

6.

7.

Introduction and Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Characteristics of the Medical Devices Industry. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Payment Policies for Health Care and Medical Devices . . . . . . . . . . . . . . . . . . . . . . . 41

Research and Development Policies Related to Medical Devices . . . . . . . . . . . . . . . 77

Regulation of Medical Devices by the Food and Drug Administration . . . . . . . . . . 97

Regulation of the Providers of Medical Devices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

Veterans Administration Policies Regarding Medical Devices . . . . . . . . . . . . . . . . . . 157

Appendixes Page

A.

B.

c.D.

E.

F.

G.

H.

I.

J

Method of the Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

Acknowledgments and Health Program Advisory Committee . . . . . . . . . . . . . . . . . 182

The Innovative Process in the Medical Devices Field . . . . . . . . . . . . . . . . . . . . . . . . . 186

Patent Policy Regarding Medical Devices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 191

Method Used for OTA’s Analysis of Applications to the National Institutesof Health for Small Business Innovation Research Grants . . . . . . . . . . . . . . . . . . . . 196

The Database of Venture Economics, Inc., on Sourcesof Financial Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 197

Tax Policy and Research and Development on Medical Devices . . . . . . . . . . . . . . . 199

Consensus Standards Related to International Trade in Medical Devices . . . . . . . 204

Governmental Regulation of International Trade in Medical Devices:United States, Canada, Japan, United Kingdom, France,Federal Republic of Germany, and Mexico . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 216

Glossary of Acronyms and Terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 231

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 237

Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 257

1.

Introduction and Summary

No one has yet managed to measure the state of technical knowledge,much less the rate of change of technological knowledge.

—M. Blaug

Contents

Introduction and Summary . . . . . . . . . . . . . . . . . . . . . . . .Scope of the Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..................Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Payment Policies for Health Care and Medical Devices . . . . . . . . . . . . . . . . . . . .Regulation ofR&D PoliciesRegulation of

Medical Devices by the Food and Drug Administration . . . . . . .Related to Medical Devices . . . . . . . . . . . . . . . . . . . . . . . . . . . .the Providers of Medical Devices. . . . . . . . . . . . . . . . . . . . . . . .

Veterans Administration Policies Regarding Medical Devices . . . . . . . . . . . . . . .Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

34568

11111314

1. ■

Introduction and SummaryMedical devices are a striking feature of U.S.

medical care. The past generation has seen the de-velopment of a tremendous range of devices whoseuse has improved or prolonged people’s lives andrevolutionized medical practice.

Some medical devices have enabled people withwhat would otherwise be debilitating conditionsto improve their functioning. Artificial hip joints,for example, have enabled elderly people withcrippling disabilities to walk and live independ-ently. Other devices have extended people’s lives.The Scribner shunt has permitted long-term hemo-dialysis for end-stage renal disease, and the car-diac pacemaker has controlled certain arrhythmiasof the heart.

Still other devices have drastically altered med-ical diagnosis and treatment. Starting with auto-mated blood chemistry analyzers, clinical labora-tories have shifted from manual to mechanizedprocedures, with consequent improvements in thespeed, accuracy, and per-unit cost of tests. Newimaging devices, such as the computed tomogra-phy (CT) scanner, ultrasound, and mammography,often obviate the use of more dangerous, pain-ful, and costly procedures, such as exploratorysurgery. Innovations in needles, sutures, and micro-scopes have greatly improved cataract surgery.

The industry that manufactures medical devicesin the United States has grown in tandem withthese developments. From less than $1 billion in1958, industry sales grew to more than $17 bil-lion in 1983. Even after adjustment for inflation,industry sales increased sixfold during that period.About 3,500 companies now employ more than200,000 people, compared with about 65,000employees in 1958.

These changes in the medical devices industry

have occurred during an era of growing Federalinvolvement in the U.S. health care system. TheMedicare and Medicaid programs, which wereenacted in 1965, have greatly increased health in-surance coverage, expanded the market for med-ical devices, and influenced their development anduse. Between 1960 and 1982, primarily becauseof the growth in Federal programs, the share of

medical expenditures paid by third parties rosefrom 45 to almost 70 percent.

The kind of health insurance coverage that hasevolved in this country has insulated the buyersand users of medical technologies—mainly phy-sicians, hospitals, and patients—from the cost ofmany medical services, especially those providedin hospitals. The purpose of health insurance pro-grams such as Medicare is to permit people to ob-tain needed medical care without risking finan-cial ruin. But there is discretion involved in theuse of medical technology, and for many devices,insurance coverage has reduced the importanceof cost as one of the few factors that motivatediscretion. Some devices, especially those asso-ciated with prevention and rehabilitation, are lesslikely to be covered by insurance than others andmay be relatively underused.

The Medical Device Amendments of 1976 sig-nificantly expanded the Food and Drug Admin-istration’s (FDA) authority to regulate medicaldevices for safety and efficacy. This and otherFederal activities, such as supporting research anddevelopment (R&D), regulating the purchase anduse of devices by medical providers, and deliver-ing medical care to veterans, have substantiallyinvolved the Government in the market for med-ical devices.

Congressional committees have been interestedsince the late 1970s in the effect of Federal pol-icies on the companies that manufacture medicaldevices. There has been particular concern thatthe newly established Federal regulatory processfor devices might be harming technological in-novation and small companies. In early 1982, thisinterest resulted in a request from the Senate La-bor and Human Resources Committee to the Of-fice of Technology Assessment (OTA) for anassessment of Federal policies and their effect onthe medical devices industry. The Senate Com-mittee on Veterans’ Affairs, in endorsing thatrequest, raised issues related to the Veterans Ad-ministration (VA) and its role in technology de-velopment and procurement. This report has beenprepared in response to those requests.

3

4 ● Federal Policies and the Medical Devices Industry— .

SCOPE OF THE STUDYMedical devices span a vast array of supplies

and equipment, from frequently purchased itemswith low unit cost, such as bandages and syringes,to infrequently purchased items with high unitcosts, such as clinical laboratory and imagingequipment. The definition of a medical deviceused for this study is taken from the 1976 Medi-cal Device Amendments (Public Law 94-295) tothe Federal Food, Drug, and Cosmetic Act. Thus,the term medical device refers to any instrument,apparatus, or similar or related article that is in-tended to prevent, diagnose, mitigate, or treat dis-ease or to affect the structure or function of thebody. This definition excludes drugs, which achievetheir effects through chemical action within or onthe body. Medical devices are thus one class ofmedical technology as defined by OTA.l

A wide range of Federal policies helps to framethe social, political, and economic context of themarket for medical devices. This report concen-trates on Federal policies that have the greatestleverage over the kinds of medical devices pro-duced and the price at which they are sold: pol-icies pertaining to payment for health care, sup-port for R&D, regulation of the safety and efficacyof medical devices by FDA, regulation of medi-cal providers, and development and procurementof devices by the VA. Policies that extend to theentire economy, such as those regarding taxation,financial capital, patents, and export control, areexcluded from detailed analysis. Although thesebroader policies may affect medical devices, anyoptions for changing them would require an anal-ysis that reached well beyond the confines of themedical devices industry or this report.

As background to an analysis of Federal pol-icies regarding the medical devices industry, it isimportant to note that medical care differs frommany other products that are bought and sold.Patients often do not have the expertise to evaluatemedical technologies and therefore tend to relyon medical professionals for guidance concer-ning which medical services and devices to use.

IOTA has defined medical technology to include drugs, devices,medical and surgical procedures, and the organizational and sup-portive systems within which medical care is provided.

Photo credit: E. /. du Pont de Nemours & Co.

Medical devices encompass abroad range of products,including not only sophisticated, expensive equipmentsuch as computed tomography (CT) scanners, butrelatively simple and inexpensive items, such as

bandages, syringes, and stethoscopes.

Even medical professionals, however, often lackthe expertise to assess sophisticated devices, a factthat underlies the regulatory process establishedby the 1976 Medical Device Amendments.

Governmental programs such as Medicare re-flect the social concern that people be able to ob-tain some minimum level of care, regardless oftheir ability to pay. Benefits from the use of somemedical devices and other technologies, especiallythose to prevent and treat infectious disease, in-clude increases in overall levels of health and pro-ductivity and are thus greater for society than forthe individuals who use the technologies. Gov-ernmental public health programs to immunizeyoung children and to test their vision reflect thesocietal importance attached to the use of suchmedical technologies.

The remainder of this chapter summarizes thechapters in the body of the report: characteris-tics of the medical devices industry, payment pol-

Ch. 1—Introduction and Summary ● 5——-———- — — —

icies for health care and devices, FDA regulationof devices, R&D policies related to devices, reg-ulation of providers, and VA policies regardingdevices. Appendix A describes the method of con-ducting the study, and appendix B acknowledgesthe valuable assistance of several individuals. Ap-pendixes C through I contain material on topicsthat relate to but are broader than medical de-

SUMMARYIn recent years, a number of problems have

been perceived in the cost, efficiency, quality, andinnovation of medical devices, all of which relatein some way to Federal health care policies. Since1978, U.S. expenditures for medical care havebeen rising at an annual rate of 13 to 16 percent,much faster than the rate of growth in the U.S.gross national product. Although studies have notdocumented the precise role of medical technol-ogy in escalating medical care costs,2 the adop-tion of new, sophisticated medical devices, suchas CT scanners, and overuse of existing devices,such as automated clinical laboratory analyzers,have often been implicated as contributing factors.

In addition to concerns about the growth orlevel of health care expenditures, there is concernabout whether the benefits gained in improvedhealth or reduced worry have been worth thecosts. This concern stems from the prevalence ofhealth insurance, which has changed the balancebetween costs and benefits for people who buyand use medical technologies. Health insurance,especially Federal programs, was originally in-tended to make basic medical care accessible topeople who might otherwise not be able to payfor it. But recent concerns about costs have mutedsuch distributional issues. And some cost-effectiveinterventions that are not well covered by insur-ance, especially in preventive and rehabilitativecare, are probably underused.

Issues more directly related to medical devicespertain to the quality of products marketed andused, including their safety and efficacy, and to

‘See OTA’s report Medical Technology and Costs of the Medi-care Program (342) for estimates of technology’s aggregate contri-bution to health, hospital, and Medicare costs.

vices: innovative activity, patent policy, tax pol-icy, consensus standards in international trade,and foreign regulation of international trade. Inaddition to this main report, six case studies ofspecific devices, a technical memorandum on thepolicies of the VA, and a compilation of inven-tors’ vignettes are being published in connectionwith this assessment.

continued innovation in the field. Concerns raisedin the early 1970s about fraudulent and hazard-ous devices culminated in the 1976 Medical De-vice Amendments to the Food, Drug, and Cos-metic Act. The regulatory process for devicesunder this act, in turn, has led to concerns aboutwhether such regulation will impede innovation,which has long been a hallmark of the medicaldevices field, and whether the degree of consumerprotection gained is worth the costs.

The Federal policies most prominent and prob-ably most influential in the medical devices fieldhave been those pertaining to health insuranceprograms, chiefly Medicare and Medicaid, andregulation of marketing. As discussed in this re-port, however, policies pertaining to R&D, reg-ulation of providers, and veterans have had asubstantial role as well.

Federal funding of R&D has been a longstand-ing Federal activity, mainly within the purviewof the National Institutes of Health (NIH). Fed-eral R&D in medical devices, as in other fields,has been intended to stimulate worthwhile in-novations that private developers might not other-wise undertake.

Federal and State regulation of providers whopurchase and use devices was an early responseto rising medical expenditures. Such regulationhas had two goals in addition to cost containment:ensuring that people receive care of acceptablequality and ensuring that the distribution of fa-cilities is equitable.

The Federal Government has sought for manyyears to ensure that veterans have access to med-ical care, including devices. In carrying out its

6 ● Federal Policies and the Medical Devices Industry

mandate, the VA has been involved in the fullrange of activities from R&D through purchaseof devices. Because of the many VA medicalcenters and individual veterans who rely on theagency for devices, the VA has substantial lever-age in the market for many devices.

The Federal policies just mentioned are fre-quently inconsistent, as one would expect of pro-grams that have different, often conflicting, goals:ensuring access to medical care for veterans,elderly and poor people; containing the cost ofthat care; ensuring acceptable quality of care; pro-tecting public health and safety; stimulating worth-while innovations; and minimizing the adverse ef-fects of regulation on manufacturers. This reportand the remainder of this summary chapter de-scribe and analyze these policies with respect totheir effect on the medical devices industry.

A thorough grounding in current and recentFederal policies is particularly important forassessing policy changes that are contemplated orunder way. In the area of payment for medicalcare, tremendous changes are under way that mayaffect devices. Medicare and some private third-party payers are beginning to pay hospitals a fixedamount set in advance for each case.3 The adop-tion of this type of prospective payment methodfor hospitals may substantially change the mar-ket for medical devices and may have implicationsfor the international trade position of U.S. man-ufacturers. In the process of implementing the newpayment system, Medicare is developing policiesthat will affect medical devices, such as how topay for capital expenditures and how to ensureuse of care that conforms to an acceptable levelof quality.

Another important policy area is FDA regula-tion of medical devices and the balance betweenprotecting the public’s health and minimizing theregulatory burden on manufacturers. Major por-tions of the Medical Device Amendments have yetto be implemented, and implementation of somemay not be feasible.

3See OTA’s technical memorandum Diagnosis Related Groups(DRGs) and the Medicare Program: Implications for Medical Tech-nology (341).

Payment Policies for Health Careand Medical Devices

In general, health insurance has stimulated themedical devices field by providing a secure andgrowing market for the products used in medicalcare. The effects of insurance on the market forspecific devices have varied, depending on thecoverage of the devices as benefits, the methodsof payment for covered devices, and the finan-cial relationship between the payer and providerof care.

In recent decades, the sales of devices whoseuse has been well covered by insurance, such asX-ray and electromedical equipment and surgi-cal equipment and supplies, have grown muchmore rapidly than sales of devices such as dentalsupplies and ophthalmic goods, for which patientspay a much greater share of the cost. Medicareand most other health insurance programs coverinpatient hospital care more fully than care pro-vided in other locations, such as physicians’ of-fices and ambulatory laboratories. Some kinds ofmedical care and their associated devices, such aspreventive technologies, eyeglasses, and hearingaids, are excluded from coverage or covered toa very limited extent.

Most methods of third-party payment for med-ical care used in the past have encouraged theadoption and use of medical devices because pro-viders have received more payment with greateruse of technology. Physicians and clinical labora-tories have been paid by Medicare, some Medic-aid, and many Blue Cross/Blue Shield plans forthe charges they have billed, subject to limits setaccording to the fee levels prevailing in the area.Besides stimulating use of technology, these charge-based payment methods have encouraged priceincreases because insurers have used recentlybilled charges to set new levels of payment.

Hospitals have traditionally been paid accord-ing to the charges they have billed or the coststhey have incurred. Traditional hospital paymentmethods have encouraged the adoption and useof medical technologies and have discouragedprice or cost containment.

Recently, however, Medicare and some Stateshave begun to pay hospitals prospectively (i.e.,

Ch. 1—Introduction and Summary ● 7

with rates set in advance of the time when theyapply). In October 1983, Medicare started to payhospitals a fixed amount per admission that variesacross 470 different diagnosis related groups(DRGs). The amount now covers only inpatientoperating costs; capital, outpatient, and teachingexpenses are continuing to be paid on a cost basisfor the time being.

Medicare’s DRG payment system provides in-centives for hospitals to become much more costconscious in their adoption and use of medicaldevices and other resources. Whereas hospitalpayment methods in the past have encouragedproviders and manufacturers to emphasize non-price factors, DRG payment encourages them togive more prominence to price considerations.Especially favored by DRG hospital payment aredevices that lower the cost of a hospital stay byreducing the costs of services provided or byshortening the length of stay. Hospitals are likelyto increase group purchasing, standardize theirpurchases, and require competitive bidding forequipment and supplies.

How DRG rates are changed in future years toreflect changes in prices and technology will af-fect incentives to develop and use new devices.As payment incentives change, many U.S. devicemanufacturers will face an adjustment in theirproduct development and marketing strategies,from stressing quality to placing more emphasison price. However, such a change promises tomake U.S. devices more competitive interna-tionally if U.S. companies can more effectivelychallenge foreign ones on the basis of price as wellas technology.

The exclusion of capital expenses from the DRGhospital payment rate fosters the adoption ofdurable equipment and facilities relative to morelabor-intensive services, with inadequate regardfor the total benefits and costs of each. Congresshas stated its intention of including capital in theprospective rate by 1986. Another problem is thatbecause Medicare’s DRG payment system appliesonly to operating costs for inpatient care, it en-courages the adoption and use of devices andother resources in settings such as home healthcare and hospital outpatient facilities, where DRGpayment is not in effect. In some cases, such as

surgery for cataract removal and placement of anintraocular lens, it is possible that the movementaway from inpatient care may reduce cost andbenefit the patient. But DRG payment as nowestablished fosters changes in that direction withinadequate regard for the effects on total costs ofcare or benefits to patients.

Policy options can address these problems inspecific areas of medical care and device use. Oneapproach would be to develop payment methodswith financial incentives that are more neutralwith respect to physicians’ decisions to use devicesand that encourage physicians to select the leastcostly settings of use. Currently, for example,physicians have financial incentives to order andperform clinical laboratory tests in their offices

Photo credit: E. I. du Pont de Nemours & Co.

Automated clinical chemistry analyzers, first developedin the 1950s, improve the speed and accuracy andlower the per-unit costs of laboratory tests on bloodsamples. Their use, however, has been implicated as

a source of rising medical expenditures,

8 ● Federal Policies and the Medical Devices Industry

and to use procedures associated with new devicesfor which high fees may be set. Congress couldrequire Medicare to experiment with paymentmethods for laboratory and physician servicesthat are mindful of incentives regarding the useof different technologies and locations of care.

Congress could also encourage Medicare to ex-periment with alternatives to reasonable chargereimbursement of durable medical equipment andto unify payment policies regarding parenteral orenteral nutrition therapy for patients receiving andnot receiving home health services. Congressmight also consider including capital in Medicare’sDRG hospital payment rates, so that hospitalsconsider the cost of equipment and facilities whenmaking decisions about resources to purchase anduse.

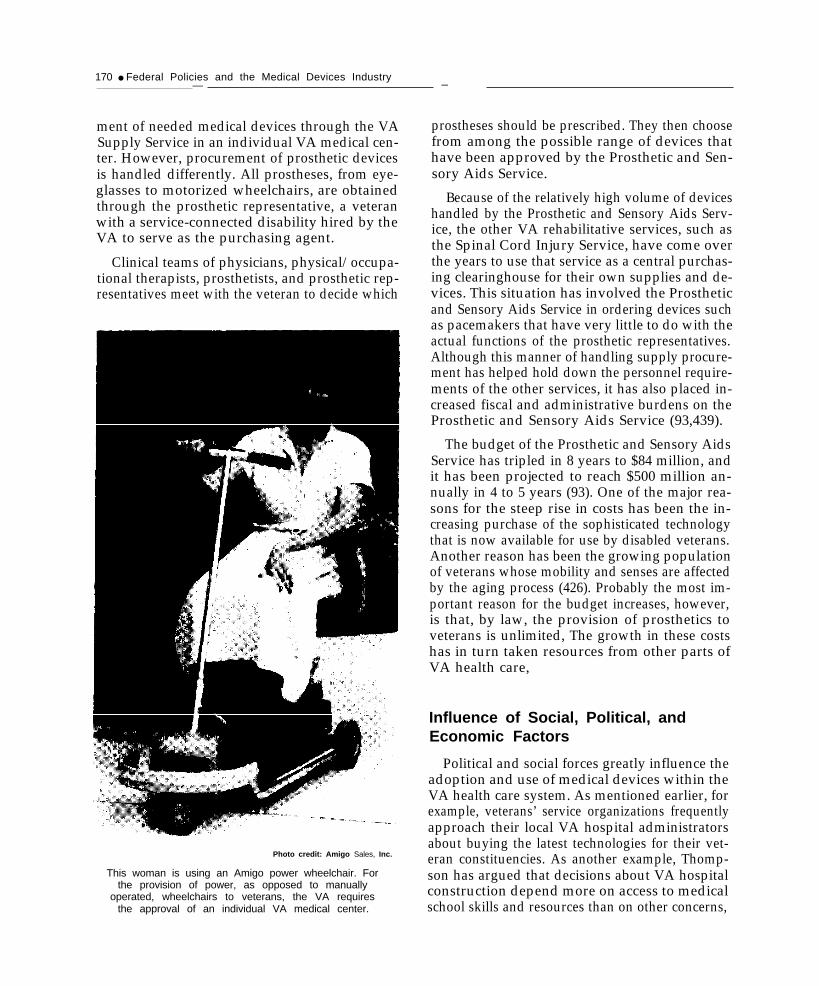

The above options that address problems inspecific areas of medical care and device usewould continue payment methods with basicshortcomings. These methods encourage the useof medical technologies, including devices, be-cause providers are paid more for using more serv-ices, and encourage technology use to shift to lessrestricted, more lucrative locations. The resultingpattern of use of devices and other technologiesis unlikely to reflect their relative costs and bene-fits. A different policy approach would be tomove Medicare in the direction begun with DRGpayment. Congress could encourage Medicare toset overall limits on the amount to be paid for careand to permit providers and patients to determinethe use of specific devices and other technologieswithin that limit. Such methods of per-case or per-person payment could be applied to physicianservices, all hospital care, or the full range of med-ical care.

Regulation of Medical Devices by theFood and Drug Administration

FDA regulation of medical devices was intendedto protect consumers’ health and safety by ensur-ing that marketed products are effective and safe.The Medical Device Amendments of 1976 pro-vided more effective methods for dealing withfraudulent devices and attempted to anticipate andminimize the potential risks associated with in-

creasingly sophisticated devices. Congress also in-tended that the regulation impede innovation inthe field as little as possible.

The Medical Device Amendments provided forregulation according to the degree of potential riskposed by a device. Devices that had been mar-keted before 1976 were to be assigned to one ofthree classes: Class I, encompassing devices forwhich general controls such as good manufactur-ing practices were deemed adequate to ensuresafety and efficacy; Class II, an intermediate cat-egory, for devices for which general controls weredeemed insufficient to ensure safety and efficacyand for which performance standards could be de-veloped; and Class III, for devices that supportlife, prevent health impairment, or present anunreasonable risk of illness or injury and requireFDA approval before marketing.

With limited resources, FDA has set prioritiesin implementing the 1976 Medical Device Amend-ments. By early 1984, while the majority of themedical specialty classification panels set up byFDA had completed classification of the devicetypes4 assigned to them, the others had only pro-posed classifications. Twenty-seven percent of thedevice types are in Class I; 64 percent are in ClassII; and 8 percent are in Class III.

To obtain FDA’s market approval, all Class 111devices are required to show evidence of safetyand effectiveness. However, preamendments ClassIII devices were given a 30-month grace periodbefore FDA could require such evidence, and FDAmay extend that period. Furthermore, until evi-dence is required for their preamendments equiv-alents, postamendments devices found “substan-tially equivalent” to Class III preamendmentsdevices may be marketed without additional proofof safety and effectiveness.

FDA could have expedited the classification ofpotentially high-risk Class III device types withineach medical specialty category, thereby startingthe grace period after which evaluation of Class

— — —4A device type may include all products of a particular type (e. g.,

cardiac pacemakers) or grouping of devices that are similar (e.g.,obstetrics-gynecology specialized manual instruments).

Ch. 1—Introduction and Summary ● 9

III preamendments devices of these types couldbegin. Instead, FDA has completed classificationsof device types in the medical specialty catego-ries in which most of the device-associated deathsand injuries have been and continue to be re-ported—e.g., cardiovascular (pacemakers, heartvalves) and obstetrics-gynecology (intrauterinedevices (IUDs)). Furthermore, in September 1983,FDA expressed its intention of reviewing evidenceof safety and effectiveness for 13 preamendmentsClass III device types that it considers of highestpriority. Documentation of safety and effective-ness of products of these types will be needed fortheir continued marketing.

Another of FDA’s priorities has been to imple-ment the premarket approval process for post-amendments Class III devices. Guidelines for theprocedures by which investigational Class IIIdevices may be tested and evidence gathered hadbeen completed by FDA by 1980.

FDA’s premarket approval process has been ap-plied to only a small fraction of the devices mar-keted after 1976. Postamendments devices that arefound substantially equivalent to a device alreadyon the market are automatically classified and reg-ulated like their preamendments equivalent. Bythe end of fiscal year 1981, only about 300 of the17,000 products submitted for clearance to FDAafter 1976 had been found not substantiallyequivalent. Although products that are not sub-stantially equivalent are automatically placed inClass III, the manufacturer can petition FDA forreclassification, and some manufacturers havedone this. *

No performance standards have yet been de-veloped for Class II devices. In practice, there-fore, Class II devices have been regulated likeClass I devices. In mid-1983, FDA identified 11priority Class II device types for which it wasstarting to develop the first performance stand-ards. There is a consensus among industry andconsumers that although an intermediate class ofdevices is advisable, it is impractical for FDAto formulate performance standards for themore than 1,000 device types now designated asClass II.

Other examples of how FDA has set prioritiesin implementing the Medical Device Amendmentscan be cited. In 1980, for example, FDA exempted30 Class I device types in the General Hospitaland Personal Use category from the requirementthat their manufacturers notify FDA before mar-keting them. The manufacturers of these devicetypes, which include medical absorbent fibers andspecimen containers not represented to be ster-ile, continue to be subject to FDA registration andsurveillance for conformity with good manufac-turing practices regarding manufacture, packing,and storage.

Substantial negative effects of the 1976 Medi-cal Device Amendments on the medical devicesindustry have not been documented to date. Per-haps this result is not surprising, because majorsections of the law have not been fully imple-mented. Patents on medical devices, one indicatorof innovative activity, have shown the sametrends as before the law, with a higher rate ofawards continuing for more sophisticated devices.Manufacturers have reported increases in R&D,sales, and new devices introduced since the Med-ical Device Amendments, and national data bearout these reports. One-third of the manufacturersresponding to a national survey in 1981 had enteredthe industry after the amendments, and 80 per-cent were optimistic about business in the fieldduring the next decade. Surprisingly, however,almost half of the survey respondents stated thatFederal regulation had been a major problem forthem.

The regulations have been more burdensometo small manufacturers than to large ones; smallermanufacturers reported higher regulatory costsper employee than larger ones. Small establish-ments are particularly important in the medicaldevices field: about 70 percent of all establish-ments have fewer than 20 employees, and thesesmall establishments have historically accountedfor substantial innovation. The law expressed par-ticular concern about small manufacturers by re-quiring that FDA establish an office to providethem information. Although large manufacturersin the 1981 survey were much more likely to con-sider producing a Class 111 device, it is noteworthy

25-406 0 - 84 - 2

10 ● Federal Policies and the Medical Devices Industry

that this situation existed before the amendmentsas well. Thus, regulation may intensify this pat-tern but did not originate it.

The amendments have posed the greatest prob-lem for small manufacturers of contact lenses. Be-cause some contact lenses were regulated as drugsbefore 1976, the newer types of lenses were auto-matically placed into Class III. Over the years,small manufacturers have found it difficult to en-ter the market because of the expense of gather-ing clinical evidence on safety and effectiveness.The public policy goals at odds in this case arepreserving the confidentiality of information frommanufacturers who have already received ap-proval to market their devices versus increasingthe availability of products, with price competi-tion as one result.

Available information does not permit anassessment of consumer protection under theMedical Device Amendments. Although the pri-mary goal of the amendments is to protect pub-lic health and safety, there exists no systematicinformation on the extent to which problems ofsafety and effectiveness are occurring. Withoutsuch information, one cannot assess the effect ofFDA’s choice of priorities in implementing thelaw. Information from FDA’s present voluntarysystem of reporting device hazards and from prod-uct recalls is inadequate, because it does not in-dicate the magnitude or frequency of device-related problems. Voluntary reports and recallsfor high risks have mostly involved implantabledevices, often with electrical problems, and car-diovascular devices. Since 1980, FDA has pro-posed several approaches to mandatory reportingby manufacturers and expects to issue a revisedproposal in 1984.

Congress has several options to improve FDA’sregulation of medical devices. Insofar as an overallregulatory approach is concerned, Congress couldcontinue the basic framework and intent of the1976 law and adjust specific provisions to reflectjudgments on the appropriate balance betweenmethods of ensuring safety and effectiveness andthe costs of these methods. An alternative strat-egy would be to revise the law to reflect the statusquo with regard to FDA’s implementation of the

law. A third approach would be to revise the lawto exclude certain device types from regulationon the basis of their potential risk.

To address the issue of what evidence of safetyand effectiveness should be required for preamend-ments Class 111 devices, Congress could continueFDA’s emphasis on high-priority device types,limit requirements for evidence of safety and ef-fectiveness to device types identified as problems,or encourage FDA to accept a greater range ofevidence. To address the issue of when the evi-dence should be required, Congress could allowFDA to continue its interpretation that the endof the grace period is the earliest date that FDAcan require evidence, or could establish the endof the grace period as the date when FDA mustcall for evidence. Other congressional options per-tain to possible revisions in the substantial equiv-alence method of market entry for postamend-ments devices.

There is widespread agreement that perform-ance standards cannot be developed in a timelyfashion for all of the devices types that have beenplaced in Class II. Congress could authorize FDAto use other methods, such as voluntary stand-ards or designation of prescription devices, to reg-ulate Class II devices. Other options include leg-islating an additional category of Class II deviceswith different requirements or reclassifying mostexisting Class II device types into other classes.

Information on risks associated with medicaldevices is crucial to assessing the 1976 law andits effectiveness in consumer protection. Congresscould require FDA to develop better systems formonitoring and providing information on devicerisks or encourage FDA to selectively apply post-marketing controls to regulate Class II devices.

To help manufacturers, especially small ones,through the regulatory process, Congress couldencourage FDA to use publicly available infor-mation to down-classify Class 111 devices as soonas possible. FDA might also act as a broker be-tween small firms with promising devices and clin-ical investigations capable of gathering data tosupport premarket approval for Class 111 devices.

Ch. 1—Introduction and Summary ● 1 1. — — — — . —--——- ——-

R&D Policies Related to Medical Devices

The present level of private R&D for medicaldevices appears to be generally adequate. If in-dustrial R&D in medical devices responds to mar-ket opportunities, as it does in other fields, thegreater demand for most medical devices becauseof health insurance would argue that medicaldevices R&D has been adequately stimulated.

From 1974 to 1980, R&D grew at an averageannual rate of about 16 percent in medical devicescompanies, as compared with a rate of about 12percent in industry as a whole. In 1980, com-pany-sponsored R&D as a percentage of sales wasgreater in medical devices than in industry as awhole (2.9 percent compared with 1.6 percent).The percentage of company-sponsored R&Ddevoted to basic research differed only slightly inmedical devices firms and in industry as a whole(3.7 percent compared with 4.1 percent).

Basic research has long been recognized as sub-ject to underfunding by private companies. As re-search becomes more targeted to development ofa commercializable device, however, the case forgovernmental involvement declines. Federal sup-port has been lower for R&D conducted in medi-cal devices companies than for industrial R&D asa whole. In 1980, the Federal Government fundedless than 3 percent of the R&D conducted by med-ical devices firms, compared with 29 percent ofthat conducted by industry as a whole.

Under a new Federal program, the Small Busi-ness Innovation Research (SBIR) program, NIHand other Federal agencies with sizable R&Dbudgets must set aside a small percentage for R&Dawards to small businesses. Although NIH fundsfor the SBIR program may come at least partlyfrom funds that would otherwise have gone tobasic research and nonprofit institutions, theredistributional implications of the program arenot yet clear. The program’s solicitation and selec-tion methods merit attention as the funds devotedto this effort increase.

The Orphan Drug Act of 1983 (Public Law 97-414) charges the Federal Government to identifyand promote orphan products, including bothdrugs and medical devices. Devices that are veryvaluable to potential users, especially in relation

to their cost, and that are so costly that it wouldbe unreasonable or inequitable to expect poten-tial users to pay a price sufficient to cover pro-duction costs, are by definition worthy of sup-port. However, it is difficult to distinguish betweensuch orphan devices and devices that lack a suf-ficient market because they are not worthwhile.

Neither the Orphan Drug Act nor regulationshave provided sound criteria for identifying or-phan devices. By spreading payment across manypeople, third-party payment may render previ-ous orphan devices and services affordable. Medi-care coverage of dialysis for end-stage renal dis-ease is an example. Expensive devices are usuallycovered by health insurance, and many of thosenot covered, including preventive and rehabil-itative devices, may have a large enough marketto permit sale at a sufficiently low price. But theproblem of orphan devices may grow as third par-ties develop increasingly restrictive paymentpolicies.

The Orphan Drug Act makes available to or-phan drugs certain benefits (e.g., grants and con-tracts for clinical testing) that are not availableto devices. It appears premature to extend thebenefits of the Orphan Drug Act to devices untilcriteria are developed to distinguish orphan de-vices from those that are not worth their costs.However, an option would be for Congress tomandate that the Department of Health and HumanServices develop criteria and methods for identi-fying orphan devices.

Regulation of the Providers ofMedical Devices

Federal regulation of the providers of medicaldevices applies mainly to facilities, such as hos-pitals, but affects physicians indirectly. Such reg-ulation has been undertaken to promote goodquality medical care, to control rising costs byevaluating technology adoption and use, and toensure access to care, including medical devices.

As a condition of receiving funds from Medi-care, hospitals have periodically had to review themedical necessity of admissions, extended stays,

72 ● Federal Policies and the Medical Devices Industry— . ———.

and professional services. The reviews performedby Professional Standards Review Organizations(PSROs) focused more on reducing overutiliza-tion of inpatient care and on containing costs thanon reducing underuse or improving overall qualityof care. The emphasis of PSRO review was con-sistent with the incentives of Medicare’s cost-basedreimbursement system, which encouraged admis-sions and days and use of technologies even ifthere were few benefits. The PSRO review pro-gram often led to reductions in admissions andlengths of stay, but when the costs of the programare taken into account, it is not clear that it savedMedicare costs.

Under Medicare’s new DRG hospital paymentsystem, hospitals continue to have financial in-centives to increase admissions, but they also haveincentives to reduce lengths of stay and technol-ogy use for inpatients. In order to be paid byMedicare, participating hospitals are required tocontract by November 15, 1984, with utilizationand quality control peer review organizations(PROS), which will monitor hospital admissions,lengths of stay, and use of technologies. The focusof the PRO review program has changed fromthat of the PSRO program to reflect the incen-tives of the new payment system. Like PSROs,PROS will review hospital admissions for overuse.In addition, however, PROS must specificallymonitor cardiac pacemaker implantations andreimplantations for possible overuse. PROS willalso be more concerned than PSROs were withreviewing short lengths of stay and eventuallywith underuse of ancillary services.

Medical devices have been most directly regu-lated through provider regulation by the Statecertificate-of-need (CON) laws passed in responseto the National Health Planning and ResourcesDevelopment Act of 1974 (Public Law 93-641).These regulations sought to reduce expensiveduplication of technology and to ensure access tofacilities. By 1983, all States except one (Louisiana)had passed CON laws, but only 23 were in com-pliance with Federal requirements in 1984. Becauseof uncertainty about the future of the Federalhealth planning program, the current continuingresolution stipulates that noncomplying States arenot to be penalized.

Photo credit: U.S. Veterans Administration

The VA Prosthetics Center was involved in developingmost of the prosthetic limbs and fitting techniques

used today.

Institutions such as hospitals, nursing homes,kidney disease treatment centers, and ambulatorysurgical centers are required to obtain a CONfrom a State or State planning agency for capitalexpenditures that exceed a minimum threshold,substantially change bed capacity, or substantiallychange services. Medical research institutions andhealth maintenance organizations (HMOs) aregiven special consideration. Although State lawsmay cover investments in other locations, onlynine States cover equipment purchases for phy-sicians’ offices. Few devices have been expensiveenough to meet the threshold for CON review,which is now $600,000 for capital expenditures,$250,000 for annual operating costs from a changein services, and $400,000 for major medical equip-ment. Under the higher limits that have been pro-posed, fewer devices would come under review.

Ch. 1—introduction and Summary ● 1 3—

Evidence on the effect of CON laws on theadoption of medical devices has been inconclu-sive. Early studies indicated that numbers of hos-pital beds fell, but investment and assets per bed,which relate to devices, rose. This result is con-sistent with the CON emphasis on bed supply andthe high thresholds for review. There is no indica-tion that CON has controlled medical costs. Thisfinding is not surprising, because a CON agencyhas no limit on the annual capital expendituresthat it may approve and does not consider oper-ating costs, total costs, or use of devices and othertechnologies. The program was also charged withoften-conflicting goals of controlling cost andassuring access, and relied on consensus amongdecisionmakers with different interests. It is pos-sible, however, that CON procedures may havedeterred applications and purchases.

The different incentives for hospitals underDRG payment have implications for CON laws.Some of the change depends on how capital ex-penses are handled under the DRG system. UnderDRG payment, hospitals themselves may increas-ingly have financial incentives to adopt cost-reducing devices and to examine carefully cost-raising ones. And DRG payment has strengthenedthe incentive for providers to locate and use equip-ment and facilities outside of the more constrainedinpatient setting in such sites as ambulatory diag-nostic centers or physician offices.

Several approaches could be taken to deal withthe shortcomings of the CON process. Congresscould expand the scope of CON regulation tocover purchases of equipment in all locations, orit could place a limit on the annual level of capi-tal expenditures that CON agencies could ap-prove. Alternatively, Congress could eliminate theCON requirement from the National Health Plan-ning Act.

Veterans Administration PoliciesRegarding Medical Devices

With 172 medical centers, an annual budget ofabout $1.3 billion for equipment and supplies, andan R&D budget of almost $160 million, the VAhas the potential to exert substantial influence in

the market for medical devices, especially the mar-ket for rehabilitative devices.

Rehabilitation R&D in the VA is intended toimprove the quality of life and to further the in-dependence of physically disabled veterans. Theprogram has stressed developing practical devicesand increasing the availability of new devices onthe market, especially in prosthetics, sensory aids,and devices related to spinal cord injuries. In thepast, the VA Prosthetics Center was involved indeveloping most of the prosthetic limbs and fit-ting techniques used today and in demonstratinguses of electric wheelchairs, which were thenadopted by manufacturers. In recent years, fund-ing has shifted toward intramural projects, suchas rehabilitation R&D centers, which are affiliatedwith leading engineering schools. Adjusted for in-flation, VA funds committed to R&D in rehabil-itative devices have been stable or declining.

Responsibility for testing and evaluating med-ical devices is divided among several VA organiza-tional units. Despite the opportunity that the VAsystem presents to test devices under actual con-ditions of use, problems of coordination amongunits and of adherence to evaluation protocolshave hampered field testing of rehabilitative de-vices at VA medical centers.

The Testing and Evaluation Staff in Hines, IL,is responsible for testing nonrehabilitative devices,mainly standard stock items and smaller medicalequipment. These evaluations, which are aimedat validating manufacturers’ claims, consist mainlyof consumer research efforts. Although VA reg-ulations prohibit explicit comparison of differentproducts, some evaluations of classes of deviceshave been attempted. These evaluations are usedby purchasers of devices inside and outside of theVA system.

Through the VA Marketing Center in Hines,which manages and negotiates the VA’s nationalpurchasing contracts, the VA has a substantialposition in the markets for medical equipment andsupplies. Procurement by the VA Marketing Cen-ter has accounted for 5 to 10 percent of the na-tional sales of X-ray, nuclear diagnostic, hemo-dialysis, and patient monitoring equipment. Andthe VA has enhanced its market leverage by con-

14 ● Federal Policies and the Medical Devices Industry

tracting for the U.S. Public Health Service, theDepartment of Defense, and other Governmentagencies. The VA’s market power has allowed theVA to obtain favorable prices on medical suppliesthrough its centralized procurement channels.

VA medical centers purchase about 34 percentof their supplies through centralized procurementprograms run by the VA or the General ServicesAdministration. However, the medical centershave increasingly made purchases on the openmarket rather than through central supply chan-nels, their open market purchases having risenfrom 10 percent of total purchases in the early1960s to 39 percent in 1982. The VA medicalcenters’ reduced use of central purchasing preventsthe VA from taking advantage of lower pricesavailable through greater device standardizationand volume purchases.

The patterns of adoption and use of devices bythe VA health system are conflicting. Some typesof major medical equipment, such as CT scanners,may have been adopted by the VA less than war-ranted because of political pressures to containcosts. On the other hand, by statute, the provi-sion of prosthetic devices to eligible veterans isunlimited. The VA’s plan to set the budgets ofmedical centers on the basis of DRGs may dis-tribute funds more rationally. This DRG systembears monitoring as it is implemented for issuesof quality assurance and treatment of capital ex-penses.

Congressional options to improve VA policiestowards medical devices could focus on specificareas, such as increasing research for longer termdevelopment of rehabilitative devices and expand-ing field testing of rehabilitative devices. Congresscould also require the VA to move in the direc-tion of undertaking more comparative evaluationsof devices and increasing centralized procurementto take advantage of lower prices.

Conclusions

Since the purpose of the Medical Device Amend-ments of 1976 is to protect public health and

safety, assessment of the law and potential changesin the act or its implementation cannot proceedwithout systematic information on the hazardsassociated with device use. Such information isnow lacking. Available evidence indicates that themedical devices industry has not been system-atically affected by regulation of marketing byFDA, insofar as companies have continued to beprofitable and innovative and to enter the field.However, small manufacturers of contact lenseshave had particular problems.

The medical devices industry has responded toincentives in the market, especially those frompayment policies. As a result, the market has gen-erally rewarded attention to technological sophis-tication but not to price or cost-consciousness andhas fostered the development of devices used inacute care rather than in prevention and rehabil-itation. Medicare’s new method of paying hospi-tals on the basis of DRGs has the potential forcost containment and efficiency by providing in-centives for providers, and hence manufacturers,to become more cost conscious.

At the same time, Medicare’s DRG paymentsystem raises important concerns: assurance ofquality of care when providers have a financialincentive to minimize the use of technologies in-cluding devices, and possible inefficiencies if de-vices are purchased and used in locations lessfinancially constrained than hospitals. The appro-priate role of the CON program is tied to howcapital expenses are handled under the DRG pay-ment system. In any case, issues of access todevices for low-income and sparsely populatedareas will remain. And as health insurance cov-erage and payment become more constrained, theconcept of orphan devices may require moreprecise definition. The VA has the potential to useits leverage in the market, especially for rehabil-itative devices, to channel development and com-mercialization into orphan devices with substan-tial social need and worth.

2.Characteristics of the

Medical Devices Industry

An initial invention, however dramatic, needs many refinements before itis of widespread use. In the commercialisation of technology, the tortoiseswho carry out these refinements often beat the hares.

—The Economist

Contents

PageIntroduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Growth in the Medical Devices Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Diversity in Products.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Characteristics of Medical Devices Manufacturers. . . . . . . . . . . . . . . . . . . . . . . . 25Concentration in the Medical Devices Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . 28Innovation in Medical Devices .............. . . . . . . . . . . . . . . . . . . . . . . . . . . . 31International Competitiveness of U.S. Medical Devices . . . . . . . . . . . . . . . . . . . . 35Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

LIST OF TABLESTable No. Page

1. Current Dollar Value of Shipments of Medical Devices by SIC Code,Selected Years 1958-83 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2. Real (1972) Dollar Value of Shipments of Medical Devicesby SIC Code, Selected Years 1958-83 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3. Growth in Medical Device Companies, Establishments, and Employmentby SIC Code, Selected Years 1963-82 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

4. Number of Employees in the Medical Devices Industryby SIC Code, Selected Years 1958-83 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

5. Percent Return on Assets for Medical Devices and Selected Industriesby IRS Category, Selected Years 1963-80. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

6. Growth in the Output and Employment of Selected Industries, 1963-82 .,.. 227. Products in the Medical Devices Industry by SIC Code . . . . . . . . . . . . . . . . . . 238. Sales of Selected Medical Devices to Hospitals by SIC Code, 1982 . . . . . . . . 259. Medical Devices in an Internist’s Office . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

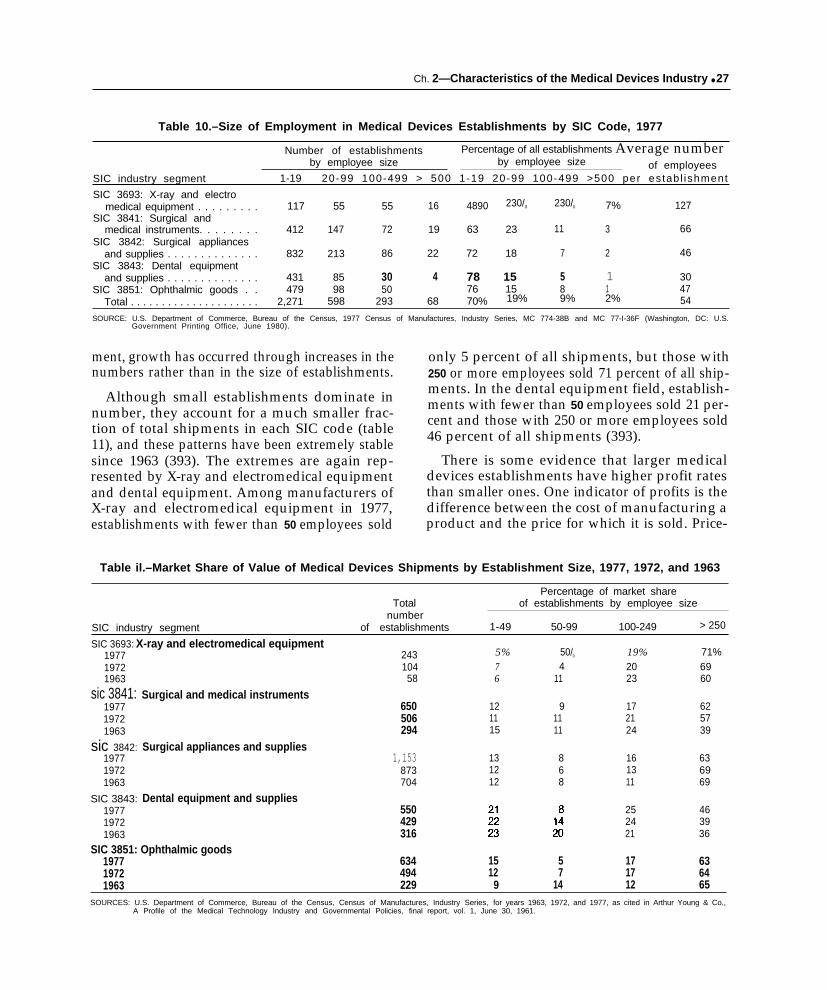

10. Size of Employment in Medical Devices Establishmentsby SIC Code, 1977 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

11. Market Share of Value of Medical Devices Shipmentsby Establishment Size, 1977, 1972, and 1963.. . . . . . . . . . . . . . . . . . . . . . . . . 27

12. Price-Cost Margins of Medical Devices Establishmentsby Employee Size, 1977 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

13. Market Share of Value of Medical Devices Shipmentsby Leading Companies, 1977 and 1963.... . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

14, Leading Companies’ Market Share of Hospital Salesof Medical Devices, 1982 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

15. Eight Leading Companies in Hospital Sales of Medical Devices in Threeor More Product Categories, 1982 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

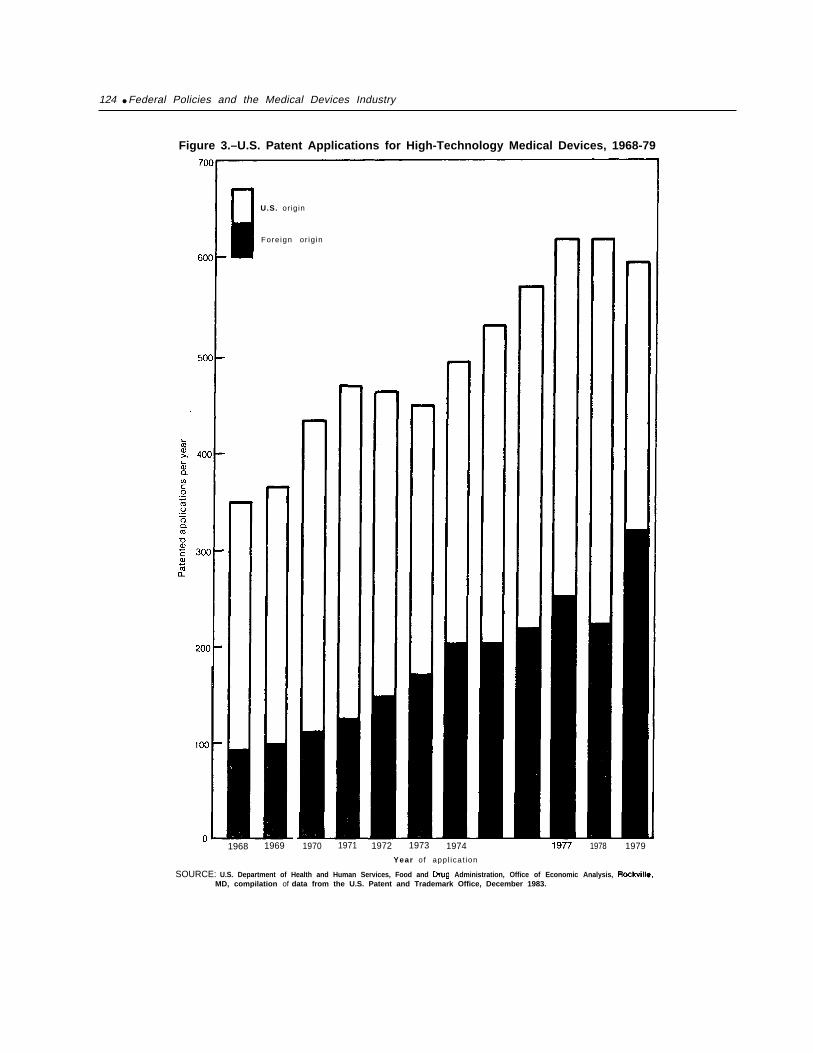

16. U.S. and Foreign Medical Devices Patents Granted by U.S. Patent Officeby Application Date, 1968-79 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

17. U.S. and Foreign Medical Devices Patents Granted by U.S. Patent Officeby Source and Selected Categories, 1968-79. . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

18. U.S. Exports and Imports of Medical Devices by SIC Code, 1979-83. . . . . . . 36

2.Characteristics of the

Medical Devices Industry

INTRODUCTIONIn recent decades, the industry that manufac-

tures medical devices has experienced continuousgrowth and change. As increased health insurancecoverage has expanded purchasing power formedical care, the market for medical devices hasgrown correspondingly. Growth has occurred notonly in the number of companies and employeesworking in the field, but also in the range of prod-ucts developed and marketed. Throughout all fac-ets of medical care—from diagnostic imaging andsurgery to dentistry and optometry-devices un-known a generation or even a decade ago are nowpart of routine practice.

This chapter presents the most notable featuresof the medical devices industry. Besides the dy -

namic nature of the field, several themes emerge.One is great diversity, both in the medical devicesthat are marketed and in the companies that makethem. Underlying the diversity in products is thehigh level of innovation. Another theme is that,more than in many other U.S. industries, smallfirms are particularly important in developing andproducing medical devices. U.S. medical devicesappear to be quite competitive internationally.Despite the diversity in companies and products,however, the concentration of production in med-ical devices is about the same as it is in a typicalindustry, i.e., a relatively small number of com-panies account for a sizable share of the market.

GROWTH IN THE MEDICAL DEVICES INDUSTRYDuring the past 25 years, sales (value of ship-

ments) of products in the five Standard IndustrialClassification (SIC) codes representing medicaldevices have grown from less than $1 billion tomore than $17 billion, an annual increase of morethan 12 percent (table 1). The growth has beenenormous, even when expressed in real dollars,which are intended to take account of price changesl

(table 2). By 1982, sales in real dollars had reachedsix times the 1958 level, having risen at an aver-age annual rate of 8 percent.

Growth in sales appears to have acceleratedafter 1963, a period which coincided with the earlyyears after implementation of the Medicare and

1Like most price indexes, those of the Department of Commercemeasure annual price changes in a market basket of devices thatwere specified in 1972 (369). A common problem with such indexesis their inability to take into account price changes associated withthe introduction of new products and with changes in productquality. This problem is particularly acute for medical devices, whichhave experienced constant and dramatic change.

Medicaid programs in 1966. From 1966 to 1982,total U.S. expenditures on personal health carein real dollars grew at an average annual rate of5 percent, and those of the Medicare programalone at 18.5 percent.

Although the start of Medicare and Medicaidwas the most notable change, both private andpublic third parties have accounted for an increas-ing share of the growing expenditures on personalhealth care—from 35 percent in 1950 (12 percentprivate, 12 percent State and local, 10 percent Fed-eral) to 51 percent in 1966 (25 percent private, 12percent State and local, 13 percent Federal) and69 percent in 1982 (28 percent private, 11 percentState and local, 29 percent Federal) (128). Al-though the exact relationship has not been doc-umented, growth in health care expenditures ex-panded the market for products such as medicaldevices that are used in the course of deliveringthat care (see ch. 3).

17

Table I.—Current Dollar Value of Shipments of Medical Devices by SIC Code, Selected Years 1958-83a

Current dollar value of shipments (in millions) Annual percentage changeb

X-ray and Surgical Surgical Dentalelectro- and appliances equipment X-ray and Surgical Surgical Dentalmedical medical and and Ophthalmic electro- and appliances equipment

equipment instruments supplies supplies goods medical medical and and OphthalmicYear (Sic 3693) (Sic 3841) (Sic 3842) (Sic 3843) (SIC 3851) Total equipment instruments supplies supplies goods Total

1983 c . . . . $5,500 $4,590 $6,140 $1,180 N Ad

$17,410e 21% 12% 90/0 70/ 0 — 13%e

1982 . . . . . 4,557 4,114 5,642 1,107 $1,358 16,778 42 30 19 -16 8 231981 . . . . . 3,203 3,158 4,734 1,314 1,263 13,672 27 17 23 5 4 181980 . . . . . 2,527 2,697 3,861 1,252 1,212 11,549 10 14 14 17 8 131977 . . . . . 1,885 1,833 2,597 787 972 8,074 34 14 12 14 11 161972 ..., . 444 962 1,454 409 568 3,8371967 . . . . .

14 15 12 13 6 12233 475 838 221 426 2,193 13 14 9 11 12 11

1 9 6 3 . . 144 284 597 148 273 1,446 9 17 5 5 7 81958 . . . . . 95 130 462 116 194 997 – — — — — —

aFor a Iwtlng of products In the Standard industrial Classification (SIC) codes used, see table 7‘For Inconsecutwe years, the compound annual growth rate, the annual rate of growth that makes the present value compound forward to equal a speclfled future value, was calculated.

‘AA = [( FVIPV)l IN – 1] 100, where O/OA = compound annual growth rateFV = future value (the value at the end of N compounding periods)PV = present valueN = total number of compounding periods

cPreliminary estimates.dNA Indicates information not available.‘Total does not include shipments of ophthalmic goods.

SOURCES: U.S. Department of Commerce, Bureau of Industrial Economics, Capital, Energy, and Productivity Studies Division, Washington, DC, unpublished data, January 1984; P. Marcus, U.S. Department of Commerce,Washin ton, DC, personal communication, Janua

8~ 1984; U.S. De partment of Commerce, Bureau of the Census, 7982 Census of kfamfacwres, Preliminary Report Industry Series, MC82-I-38F-3(P),

MC82-I- 8B-l(P), MC82-I-38B-2(P), MC82-I-38B-3(P), M 82-I-38 B-4(P), 1984; and E. Arakaki, U.S. Department of Commerce, Washington, DC, personal communication, August 1984.

Table 2.–Real (1972) Dollar Value of Shipments of Medical Devices by SIC Codea, Selected Years 1958=83

Real (1972) dollar value of shipments (in millions) Annual percentage changeb

X-ray and Surgical Surgical Dentalelectro- and appliances equipment X-ray and Surgical Surgical Dentalmedical medical and and Ophthalmic electro- and appliances equipment

equipment instruments supplies supplies goods medical medical and and OphthalmicYear (SIC 3693) (sic 3841) (Sic 3842) (Sic 3843) (SIC 3851) Total equipment instruments supplies supplies goods Total

1983C . . . . $2,145 $2,050 $2,975 $540 N Ad

$7,710’ 150% 70% 70% 20% 9%e

1982 . . . . . 1,858 1,915 2,790 528 $757 7,848 35 21 19 -20 8 181981 . . . . . 1,374 1,587 2,337 659 704 6,661 14 6 16 -4 -4 91980 . . . . . 1,210 1,494 2,007 685 735 6,131 -1.7 5 7 7 1 41977 . . . . . 1,274 1,273 1,649 564 707 5,467 23 6 3 7 4 71972 . . . . . 444 962 1,454 409 568 3,837 11 10 12 3 91967 . . . . . 311 568 920 234 479 2,512 9 11 7 10 11 91963. 217 377 705 160 312 1,771 8 15 5 4 6 71958 . . . . . 150 184 549 130 231 1,244 — — — — — —aFor a listing of products in the SIC categories used, see table 7“For inconsecutive years the compound annual growth rate, the annua! rate of growth that makes the present value compound forward to equal a specified future value. was calculated

0/0 J = [( FVIPV)l ‘N – 1 ] 100 where O/OA = compound annual growth rateFV = future value (the value at the end of N compounding periods)PV = present value

N = total number of compounding periods

cPreiiminary estimates.dNA indicates information not available.‘Total does not include shipments of ophthalmic goods.

SOURCES: U.S Department of Commerce, Bureau of Industrial Economics, Capital, Energy, and Productivity Studies Division, Washin ton, DC, unpublished data, January 1984; P. Marcus, U.S. Department of Commerce,Washington, DC, personal communication, January 1%34; M. Pavliscak, U.S. Department of Commerce, Washington, DC, persona communication, June 19S4; and E. Arakakl, U.S. Department of Commerce, Washington,fDC, personal communication, August 19S4.

20 ● Federal Policies and the Medical Devices Industry

All segments of the medical devices industryhave benefited from this growth, some more thanothers (tables 1 and 2). Most medical devices fallinto one of five SIC codes of the Department ofCommerce: 3693, X-ray, electromedical, andelectrotherapeutics equipment; 3841, surgical andmedical instruments; 3842, orthopedic, prosthetic,and surgical appliances and supplies; 3843, den-tal equipment and supplies; and 3851, ophthal-mic goods.2

2The most comprehensive statistics on the medical devices industrycome from the Census of Manufactures, which is conducted by theBureau of the Census in the Department of Commerce. The datarelate to domestic production by U.S. and foreign companies oper-ating in the United States. A complete census is conducted every

5 years and an Annual Survey of a sample in intervening years. Prod-ucts are categorized by Standard Industrial Classification (SIC) codes.Establishments are assigned to SIC “industries” on the basis of theirprimary line of business. A 1980 sample of 1,891 manufacturingestablishments registered with the Bureau of Medical Devices in theFood and Drug Administration (FDA) fell into 162 SIC codes: 47percent into the 5 major medical devices codes, which included anaverage of 177 establishments per code; 37 percent into 25 otherSIC codes, each with 10 or more establishments; and 16 percent into132 other SIC codes, each with fewer than 10 establishments (393).It can therefore be inferred that the establishments in the five medi-cal devices codes account for a greater volume of medical devicesproduction than those in other codes. Nevertheless, data by estab-lishment from the five medical devices SIC codes exclude someestablishments and perhaps some devices of multiproduct establish-ments whose primary products fall into other categories.

In addition, the FDA sample lists 47 establishments in SIC 2831,biological (393). Diagnostic substances and other biological rep-resent about 45 percent of all shipments in SIC 2831 (363), but thedata are not sufficiently detailed to permit separation of these med-ical devices products from other biologics, such as blood andvaccines.

SIC data on product shipments, however, include shipments ofall medical devices, both those produced by establishments classifiedin the five medical devices codes and those classified in other codes(393).

In both current and real dollars, sales of prod-ucts in SIC codes 3693, 3841, and 3842 are muchgreater than sales of dental equipment and sup-plies and ophthalmic goods. Not only are salesin these three codes the largest in absolute terms,but they have also experienced the highest ratesof increase, especially since 1980. SIC 3842 (sur-gical appliances and supplies), the category withthe greatest sales, has had the highest growthrates, followed closely by SIC 3693 (X-ray, elec-tromedical, and electrotherapeutics equipment).The tremendous growth in SIC 3693 from 1972to 1977 may be somewhat overstated; in 1977,products misclassified in other SIC codes, mainly3841, were assigned to 3693 (393).

Increases in the number of companies (firms)and establishments (plants) have paralleled the in-creases in sales (see table 3). From 1963 to 1982,SIC 3693 (X-ray and electromedical equipment),with annual rates of about 7 and 8 percent respec-tively, experienced the greatest rate of increase incompanies and establishments. During this period,the other four SIC codes had annual increasesranging from about 2 to 6 percent. In all five med-ical devices codes, firms entering a field have thusexceeded those exiting.

By 1982, employment in the establishments inthe SIC medical devices codes had exceeded200,000, a 68-percent increase over the 129,500employed in 1972 (see table 4). SIC 3693 (X-rayand electromedical equipment) again had thegreatest rates of increase, reflecting the hugegrowth in production and facilities during thedecade.

Table 3.–Growth in Medical Device Companies, Establishments, and Employment by SIC Codea, 1963-82

1982 levels (number) 1963-1982 compound annual growth rate

EmploymentSIC industry segment Companies Establishments (thousands) Companies Establishments Employment

Total . . . . . . . . . . . . . . . . . . . . . . 2,986 3,361 217.5 4.4% 4.0% 5.6%SIC 3693: X-ray and

electromedicalequipment . . . . . . . . . . . . . . . 205 260 49.2 7.1 8.2 11.5

SIC 3841: Surgical andmedical instruments . . . . . . 767 858 57.4 5.9 5.8 7.3

SIC 3842: Surgical appliancesand supplies . . . . . . . . . . . . . 1,212 1,365 68.6 4.5 3.5 4.8

SIC 3843: Dental equipmentand supplies . . . . . . . . . . . . . 435 474 15.4 2.6 2.2 3.5

SIC 3851: Ophthalmicgoods . . . . . . . . . . . . . . . . . . . 367 404 26.9 3.0 3.0 1.5

at=or a listing of products in the SIC categories used, see table 7.

SOURCES: U.S. Department of Commerce, Bureau of the Census, 1$%3 Census of Manufactures, Industry Series, MC63-I-36E and MC634-38A, 7982 Census of Marrufac-tures, Preliminary Report Industry Series (Washington, DC: U.S. Government Printing Office, 1966 and 1984).

Ch. 2—Characteristics of the Medical Devices Industry ● 2 1

Table 4.—Number of Employees in the Medical Devices Industry by SIC Codea,Selected Years 1958.83 (in thousands)

X-ray and Surgical—

Surgical Dentalelect ro- and appliances equipmentmedical medical and and Ophthalmic

equipment instruments supplies supplies goodsYear (SIC 3693) (SIC 3841) (SIC 3842) (SIC 3843) (SIC 3851) Total1983 b . . . . 50.5 62.0 71.2 16.2 N Ac 199.9d

1982 . . . . . . 49.2 57.4 68.6 15.4 26.9 217.51981 . . . . . . 41.5 54.6 64.9 17.4 26.4 204.81980 . . . . . . 38.8 51.3 61.8 16.7 29.4 198.01977 . . . . . . 30.9 43.2 53.9 16.3 30.0 174.31972, . . . . . 12.1 34.5 43.9 12.4 26.6 129.51967 ....., 7.9 22.0 35.2 10.2 25.6 100.91963 . . . . . . 6.2 15.1 28.3 8.0 20.3 77.91958 . . . . . . 5.3 10.3 24.2 7.2 18.2 65.2aFor a listing of proctucts In the SIC categories used, see table 7bPreliminary estimates.CNA indicates information not available.dTotal does not include employment in the ophthalmic goods Industry.

SOURCES: U.S. Department of Commerce, Bureau of the Census, Annual Survey of Manufactures, Statistics for Industry Groupsand Industries, for years 1958, 1983, 1987, 1972, 1977, and 1981; U S Department of Commerce, Bureau of IndustrialEconomics, 1984 US. Industrial Outlook (Washington, DC U S Government Printing Office, January 1984); andE Arakaki, Department of Commerce, Washington, DC, personal communication, August 1984.

In 1982, about 3,000 companies (firms) with3,400 establishments (plants) were manufactur-ing products in the five medical devices SIC codes(table 3). Although this information is the mostcomprehensive and most recent available, it ex-cludes multiproduct establishments with primaryproducts in other codes. Changes in employmentmay be used as a proxy for changes in numbersof companies and establishments. In 1980, 4,300establishments were registered with the Food andDrug Administration (FDA) as being engaged inmanufacturing medical devices (197).3

Available information from the Internal Reve-nue Service (IRS) indicates that the profit ratesof medical devices companies have exceeded thoseof many other manufacturing industries (table 5).The IRS category 3845 (optical, medical, and oph-thalmic goods) includes some firms that do notproduce medical devices (optical instrument andlenses firms) and excludes some that do (if theirprincipal line of business lies in a different cate-gory). Nevertheless, this category contains sub-stantial numbers of firms whose principal activ-ity is producing medical devices (26). Sales ofelectrical medical devices may represent a smallfraction—perhaps at the most 10 percent—of IRScategory 3698 (other electrical equipment) (26).

3As explained in ch. 5, several entities besides medical devices man-ufacturers also register with FDA.

Annual profit rates for both of these IRS catego-ries ranged from 10 to 18 percent (26), higher thanthe 9 to 11 percent in total manufacturing. In1980, firms in IRS category 3845 (optical, medi-cal, and ophthalmic goods), with 12.7-percent re-turn on assets, were more profitable than firmsin similar products such as other electrical equip-ment, chemicals and allied products, and electri-cal and electronic equipment.4

By any of these measures—sales, companies,establishments, employment, or profits—the growthof the medical devices industry has far exceededthat of many other industries (table 6). For ex-ample, from 1963 to 1982, the output of the totalmanufacturing sector grew at an annual rate of2.7 percent and employment at a 0.5-percent rate.Even chemicals and related products, electricaland electronic equipment, and instruments andrelated products—sectors with products similarto medical devices—achieved much lower annualincreases in output (from 4.3 to 5.6 percent an-nually) and in employment (from 1.4 to 2.9 per-cent annually).

4According to data from Dun & Bradstreet, returns on assets (in-dicators of profits) for medical devices SIC codes have equaled orexceeded returns on assets in other fields (95). For example, from1978 to 1980, returns on assets for SIC 3693 (X-ray, electromedi-cal, and electrotherapeutics devices) ranged from 8.8 to 11.4 percent,compared with a range of 9.0 to 9.8 percent for the broader SICcategory 36 (electrical and electronic machinery, equipment, andsupplies )

22 . Federal Policies and the Medical Devices Industry— — . — . .

Table 5.—Percent Return on Assetsa for Medical Devicesand Selected Industries by IRS Category, Selected Years 1963-80

Optical, medical Other Chemicals Electricaland ophthalmic electrical Total and allied and electronic

goods b equipment manufacturing products equipmentYear (IRS 3845) (IRS 3698) (IRS 40) (IRS 17) (IRS 25)

1980 . . . . . . 12.70/o 11 .0%0 10.50/0 11.29’0 9.6%1977 . . . . . . 14.5 11.2 10.6 12.5 10.51972 . . . . . . 13.1 9.6 8.8 11.3 7.71967 . . . . . . 17.9 13.6 10.2 12.8 11.41963 . . . . . . 12.1 12.9 10.2 14,0 9.5

aPercent return on assets =Net income (less deficit) + interest paid

Total assetsNet income (less deficit) equals “total receipts less total deductions” less “Interest on State and local Government obligations”