Embed Size (px)

Citation preview

FEDERAL TAX ALERTNews ItemsJusTicEs RuLE AgAinsT invEsToRs in WALL sTREET AnTiTRusT cAsEInvestors who lost money when the dot-com bubble burst have suffered a Supreme Court setback.

The court has sided with Wall Street banks that were alleged to have con spired to drive up prices on about 900 newly issued stocks in the late 1990s.

The justices have recently reversed a federal appeals court decision that would have enabled investors to pursue their case for anti-competitive practices.

The outcome of the antitrust case was vital to Wall Street because damages in antitrust cases are tripled, in contrast to penalties under the securities laws. But the Supreme Court may be about to raise the bar as well for cases under the securities laws.

The Supreme Court term that begins next fall could provide still more problems for trial lawyers and their clients who bring securities fraud cases, particularly those in the Enron scandal.

At issue are efforts to recover investment losses from Wall Street in-stitutions that allegedly colluded with scandal-ridden companies.

EX-EnRon EXEcuTivE Who TEsTiFiED gETs 27 MonThsThe former chief of Enron Corpora-tion's high-speed Internet unit, who turned government witness and testified in the trial of former Enron CEO Jeffrey Skilling and company founder Kenneth Lay, has recently been sentenced to 27 months in prison.

It has been nearly three years since Kenneth Rice pleaded guilty to securities fraud and agreed to help federal prosecutors on other cases related to the energy giant's collapse. His sentencing was postponed as he cooperated with prosecutors.

Before sentencing, Rice apologized for his role in the corporate scandal that wiped out thousands of jobs, more than $60 billion in market value and more than $2 billion in pension plans.

Rice had faced up to 10 years in prison and a fine of up to $1 million. The plea agreement with prosecutors also required him to forfeit $13.7 million in cash and property that included jewelry and exotic sports cars.

AFR RATEs FoR JunEApplicable Federal Rates are used when a taxpayer makes a loan or sells something on installment because a minimum interest rate normally has to be charged.

The minimum rate depends on the month of the loan or sale. The IRS releases the Applicable Federal Rates, AFRs, each month. The June AFR rates are as follows:

Semi- Annual annual Quarterly Monthly

short term 3 years or less 4.84 4.78 4.75 4.73

mid-term More than 3 years but no more than 9 years 4.64 4.59 4.56 4.55

Long term More than 9 years 4.91 4.85 4.82 4.82

QuARTERLy inTEREsT RATEs - ThiRD QuARTER 2007The Internal Revenue Service has announced the interest rates for the third quarter of 2007. The rates remain unchanged from the second quarter of 2007 as follows:

8% for most overpayments7% for corporation overpayments8% for underpayments10% for large corporation

underpayments5.5% for corporation overpayments

exceeding $10,000Revenue Ruling 2007-39 Rates effective July 1, 2007.

conTEnTsFrom the Editor . . . . . . . . . . . . 2IRS Action News . . . . . . . . . . . 2Tax Law Update . . . . . . . . . . . . 5Inside Washington. . . . . . . . . . 6 FYI . . . . . . . . . . . . . . . . . . . . . . 7Members in the Know . . . . . . . 7Tax Court Decisions. . . . . . . . . 8Et Cetera . . . . . . . . . . . . . . . . . 8Tax Rep Roundtable. . . . . . . . . 9Ethics Corner. . . . . . . . . . . . . 11Members Ask . . . . . . . . . . . . . 12Quotes of the Month . . . . . . . 16

insERTs■ Summer Client Tax Newsletter■ Plugged Into NSTP■ Regional Conferences■ Small Business And Work

Opportunity Act of 2007

A PublicAtion of the nAtionAl Society of tAx ProfeSSionAlS july 2007

MAn BiLks iRs ouT oF MoRE ThAn 1.3 MiLLion

News Items PAGe 2

congREss cLosEs kiDDiE TAX LoophoLE

tAX LAw UPDAte PAGe 5

FEWER pEopLE ARE sAving

et CeteRA PAGe 8

couRT DEcisions cAnnoT DETERMinE FEDERAL TAX LAW

tAX COURt DeCIsIONs PAGe 8

iRs cAnnoT scREEn FoR TERRoRisTs

IRs ACtION News PAGe 4

THE FEDERAL TAX ALERT – JULY 20072

The Federal Tax Alert is published 10 times a year by the National Society of Tax Professionals. Subscription rate is $200 a year; single copy $20. Mailing address: The Federal Tax Alert, 10818 NE Coxley Dr. Ste. A, Vancouver, WA 98662. Telephone: 800-367-8130.

Opinions expressed in The Federal Tax Alert are those of the editors and contributors. staff-Executive Editor: Beanna Whitlock; proof Editor: Ronald Larson; subscription services: Glyness Scott;

production: Melissa Bowden printer: Sunset Printing, Inc., Portland, Oregon.

MAn BiLks iRs ouT oF MoRE ThAn $1.3 MiLLionKetan R. Shah, the vice-president of Public Affairs International, Inc., was accused of submitting false claims under a contract with the Internal Revenue Service. He pled guilty to fraud of more than $1.3 million over three years.

The Silver Spring, a Maryland company, hired to organize federal tax law seminars, collected fees from par-ticipants and exhibitors between 2003 and 2004. The firm was supposed to subtract that income from the management fee it charged the IRS, after expenses.

But the company reported false income and expenses, so the IRS paid

the entire fee. Shah and other staff created fake invoices or altered original documents to reflect the inaccurate charges and decreased attendance.

Shah could receive a maximum of 10 years in jail for conspiracy to commit fraud, as well as a $250,000 fine and other penalties.

The U. S. Attorney's Office also is seeking $4.2 million in damages through a civil complaint filed against Public Affairs International and its president, Brosim S. Ekpone of Potomac, Maryland.

Public Affairs International (PAI) was the former contractor for the IRS Nationwide Tax Forums.

IRs ACtION NewsiRs upDATEs nATionAL REsEARch pRogRAM FoR inDiviDuALsInternal Revenue Service officials have announced plans to launch a new National Research Program (NRP) reporting compliance study for individual taxpayers that will provide updated and more accurate audit selection tools and support efforts to reduce the nation's tax gap.

The latest NRP study will be the first of an ongoing series of annual individual studies using an innovative multi-year following methodology. The study will begin in October 2007 and examine about 13,000 randomly selected tax year 2006 individual

Technical Tax advice provided by NSTP Hotline staff is based upon specific information conveyed by the member. Members should take special care in relying upon recommendations and opinions that reflect the understanding of the Hotline staff member. NSTP and the Hotline staff are not responsible for misapplication of information given. Members are responsible for the ultimate verifi-cation and application of any information provided by NSTP.

noTicETAX hoTLinEnEW hoTLinE nuMBER!

3 Days a WeekMonday, Wednesday, Friday

9 – 2 PST 10 – 3 MST 11 – 4 CST 12 – 5 EST

DiREcT LinE360-695-0556

NEW Website Password: taxlaw(use lowercase only)

FROm tHe eDItOR It was both my privilege and my pleasure to represent the members of the National Society of Tax Professionals at the 2007 IRS Research Conference at Georgetown School of Law in Washington DC on June 13th.

The morning began with panels from the U. S. Department of Treasury and the Internal Revenue Service presenting their research on various issues ranging from the Tax Gap to taxpayer compliance. A constant theme by the presenters seemed to be that Tax Professionals were part of the problem, unable to prepare returns correctly and in many instances preparing returns fraudulently to get their taxpayers tax benefits such as the Earned Income Tax Credit. Listening for any type of support for the Tax Professional community, I was stunned when from the audience a representative of TIGTA, Treasury Inspector General for Tax Administration, asked when was the IRS going to do something about regulating the tax profession.

After lunch was the panel in which NSTP participated. We were preceded in our pre-sentation by a representative of the IRS Small Business and Self-Employed operating division. They reported the results of conducting a study in the State of Connecticut where out of nineteen tax professionals “shopped” Revenue Agents pretending to be ordinary taxpayers, seventeen of the returns were prepared incorrectly.

The conclusion of their study was that an overabundance of incorrectly prepared returns is due to the lack of knowledge and in some cases the fraudulent preparation of return preparers. The nineteen firms included in the study were major tax preparation chains ranging from large firms to medium sized and smaller firms.

The report of the Taxpayer Advocate on how much better taxpayers who had been denied the EITC faired when represented than when the taxpayer did not have a taxpayer representative came next. The results of their research clearly indicated by over-whelming numbers that taxpayers who engaged and were represented by a taxpayer representative were more often allowed the EITC on appeal than when not represented.

I completely felt at ease presenting NSTP's paper on The Obstacles of Voluntary Compliance from the Taxpayer's perspective. The NSTP members who responded with their taxpayer issues, the members who read and commented upon the paper and the members who simply encouraged the presentation enabled NSTP to boldly go where no other tax professional organization had gone before. The presentation went smoothly complete with a power point supplement. When completed, my closing included, “Your research, facts and figures are very illuminating and thought provoking, however unless you partner your research with the experience of the Tax Profes-sional community it will be incomplete. Where you research, the Tax Professional lives the research. The people in the business of tax, both IRS and the Tax Professional community must work together to understand and surmount the hurdles of obstacles to voluntary compliance.”

After the presentation I was greeted by many participants and attendees expressing their gratitude for our presentation. On this day, NSTP blazed a new trail, being the first tax professional organization ever asked to present at the IRS Research Conference. You should be very proud. I know I am of you!

BeannaBeanna J. Whitlock, EA CSAEditorSan Antonio, [email protected]

JULY 2007 – THE FEDERAL TAX ALERT3

returns. Similar sample sizes will be used in subsequent tax years.

Using research from the prior NRP study, the IRS updated its audit selection system. Updated statistics enable the IRS to audit more efficiently and improve the detection of un-derreported income and overstated deductions and credits. The data also enables the IRS to audit fewer taxpayers with accurate tax returns, which lessens the burden on compliant taxpayers.

The research on individuals needs updating because as time passes, patterns of noncompliance change. The sample for the latest individual NRP is constructed to ensure that it contains sub-samples of individuals at different income levels as well as those engaged in farm and sole proprietor business activities.

The initial group of taxpayers whose returns are selected for audit under the new NRP study will start receiving official letters in October informing them that they are part of the research study. The majority of individuals will have specific lines of their returns confirmed through in-person audits with an IRS examiner. Some of the individuals whose returns are selected for inclusion will not be contacted if the IRS can obtain matching and third-party data that confirms the accuracy of their return. The targeted research design of the new individual NRP avoids the need for IRS agents to routinely check all the lines of a taxpayer's return.

In addition to the NRP for individuals, the IRS is in the final stages of a compliance research project examining reporting compliance of S corporations. This research encompasses approxi-mately 5,000 returns filed for tax years 2003 and 2004. Since the income and expense items for S corporations flow through to individual shareholders, this study will also help refine the tax gap estimates for individual income tax.

Recognizing the importance of the NRP S corp. audit, the 2007 NSTP Regional Conferences will provide 2 hours of CPE on an actual NRP S corp. audit followed by an 8 hour Track of S corps from formation, through operation, to liquidation.

iRs RELEAsEs Discussion DRAFT oF REDEsignED FoRM 990The IRS has released for public comment a discussion draft of a redesigned Form 990, Return of Or-ganizations Exempt from Income Tax, the form filed by many public charities and other exempt orga-nizations. The draft form and in-structions, as well as other key information, are available on the IRS Web site. IRS.gov/eo.

The IRS anticipates using the redesigned form for the 2008 tax year for returns filed in 2009.

The redesign of Form 990, the first since 1979, is based on three guiding principles:

Enhancing transparency to •provide the IRS and the public with a realistic picture of the organization, along with the basis for comparison to other organizations.Promoting compliance by •accurately reflecting the orga-nization's operations so the IRS may efficiently assess the risk of noncompliance.Minimizing the burden on •filing organizations.

The redesigned Form 990 consists of a 10-page core form to be completed by each Form 990 filer. In addition, the redesigned form's 15 schedules are designed to require reporting of information only from those organiza-tions that conduct particular activities.

Most organizations will not experience a material change in burden, while those with complicated compensation arrangements, related entity structures, and activities that raise compliance concerns, may see an increase in the effort required to provide information.

Among the highlights of the new form are the following:

A summary page providing •the organization's identifying information and a snapshot of the organization's key financial, compensation, governance, and operational information.A portion of the form requiring •governance information, including the composition of the board, and certain other governance and financial statement practices.Schedules that will focus •reporting on certain areas of interest to the public and the IRS fundraising, compensation, hospitals, tax exempt bonds and non-cash charitable contributions.

Questions and comments concerning the redesigned form and instructions should be:

E-mailed to the IRS at •[email protected] or

Mailed to the IRS at: •Form 990 Redesign, SE: T: EO 1111 Constitution Avenue, NW Washington, DC 20224

Comments are due no later than September 14, 2007.

nEW ELEcTRonic FiLing REQuiREMEnT FoR sMALL TAX-EXEMpT oRgAnizATionsBeginning in 2008, small tax-exempt organizations that previously were not required to file returns may be required to file an annual electronic notice, Form 990-N, Electronic Notice for Tax-Exempt Organizations Not Required to File Form 990 or 990-EZ. This filing requirement applies to tax periods beginning after December 31, 2006.Small tax-exempt organizations, whose gross receipts are normally $25,000 or less, are not required to file Form 990, Return of Organization Exempt From Income Tax, or Form 990-EZ Short Form Return of Orga-nization Exempt From Income Tax. With the enactment of the Pension Protection Act of 2006, these small tax-exempt organizations will now be required to file electronically Form 990-N, also known as the e-Postcard, with the IRS annually. Exceptions to this requirement include organiza-tions that are included in a group return, private foundations required to file Form 990-PR, and section 509(a)(3) supporting organizations required to file Form 990 or Form 990-EZ.

The IRS will mail educational letters starting in July 2007 notifying small tax-exempt organizations that they may be required to file the e-Postcard. The IRS is developing an electronic filing system (as there will be no paper form for the e-Postcard) and will publicize filing procedures when the system is completed and ready for use.

iRs hAs REvAMpED AppLicATion FoR An EMpLoyER iDEnTiFicATion nuMBERNow taxpayers can apply for an EIN using a completely redesigned web application that automati-cally validates the information. If the information passes the upfront validity checks, a permanent EIN will be issued to the taxpayer. If the information does not pass the validity checks, it is rejected immediately back to the taxpayer giving an opportunity to correct the information and resubmit the application.

In addition to automated processing, there are several burden-reducing enhancements:

Modernized Internet EIN is •interactive and asks questions tailored to the type of entity the taxpayer is establishing. It is similar to the popular tax processing software packages on the market. This should help reduce taxpayer confusion and reduce the number of EIN errors.

THE FEDERAL TAX ALERT – JULY 20074

Mod IEIN provides help screens •through the application process. This eliminates the need for taxpayers to print the EIN in-structions and search for answers during the application process.Mod IEIN conducts validation •of all IEIN applications in a real-time environment. Customers are notified immediately if their application was approved or if errors exist on the application. This allows the system to issue permanent EINs instead of provisional numbers.Taxpayers have the option to •view/print/save the CP-575 notice, as opposed to waiting for the IRS to mail it. Authorized third parties are provided with the EIN, but cannot view/print/save the CP-575; instead, it is mailed to the taxpayer.Modernized IEIN allows all •entity types, foreign and domestic, to apply online if they meet the criteria. Foreign filers must reside in either the U. S. or a U. S. territory in order to submit an EIN application. The individual filer must also have a valid TIN on file with the IRS.

chAngEs To sociAL sEcuRiTy nuMBER vERiFicATionBeginning August 25, 2007, the Social Security Administration will implement four changes to the Social Security Number Verification Service process. They include:

SSA will return all names and 1. numbers submitted, not just the mismatches.Where names and Social 2. Security numbers match, SSA will return only the last four digits of the Social Security number.A new unverified code “7” 3. will now be returned when appropriate.The eight position tracking 4. code will be replaced by a 16 position confirmation number.

For more detailed information go to: www.socialsecurity.gov/employer and select “Learn How to Use SSNVS.”

iRs WARns TAXpAyERs oF nEW E-MAiL scAMsThe Internal Revenue service has alerted taxpayers to the latest version of an e-mail scam intended to fool people into believing they are under investigation by the IRS Criminal In-vestigation division.

Recipients of questionable e-mails claiming to come from the IRS should not open any attachments or click on

any links contained in the e-mails. Instead, they should forward the e-mails to [email protected].

FEDERAL JuDgE sLAshEs FEEs soughT By ATToRnEy in pRo sE TAX vicToRyA federal bankruptcy court judge has slashed the fees sought by an attorney for representing himself in an action against the Internal Revenue Service.

Northern District of New York Bankruptcy Judge Robert E. Littlefield Jr. last May took the unusual step of allowing Paul S. Hudson to seek attorneys fees for his successful pro se efforts. Shortly afterward, Hudson submitted a bill for $21,206.

The dispute with Hudson involved the issue of the interest to be imposed on a trust recovery penalty. The judge had agreed with Hudson in his ruling last year, reducing the tax liability for Hudson and his late wife from over $50,000 to about $5,000.

The IRS objected to allowing Hudson to collect any fees in the case.

The judge decided that 26 U.S.C. §§7430(c) and 2412(d)(a)(B) permit fee awards to pro se attorneys who have prevailed in cases, who do not unnecessarily drag out the proceedings and who can show that their opponents' positions were not “substantially justified.”

The judge ruled that Hudson had met that standard; however he reduced the judgment for services from $21,206 to $6,831.

iRs MEMo puTs AccounT— FEE opTion in DouBTThe Internal Revenue Service is potentially eliminating a tax-saving strategy that could affect thousands of investors with brokerage accounts that charge a flat percentage fee instead of a commission, also known as wrap accounts.

For tax purposes, the annual fees that investors pay in these accounts, which can reach 3% of assets, are often treated as miscellaneous itemized deductions, with expenses deductible only to the extent that they exceed 2% of the taxpayer's adjusted gross income. But under a little-known provision, some taxpayers can instead opt to add the fees to the cost basis of the securities, which could reduce potential capital-gains taxes or enhance potential losses. Under a memo issued by the IRS's Office of Chief Counsel, that second option will be more difficult for taxpayers to choose.

With the increasing popularity of wrap accounts, a significant number of taxpayers are choosing to add the

fees to the cost basis of securities. For investors who do not have enough deductions to meet the 2% floor the next best thing would be to add the expenses to the basis of the stock.

The IRS says it does not break out how many taxpayers deduct their fees for investment advice as miscellaneous itemized deductions and how many instead add those fees to the cost basis, known as capitalizing the fees.

This move comes as Wall Street is shifting away from commission-based brokerage accounts to fee-based accounts, which provide a steady source of revenue. Investors have an estimated $1.5 trillion in “packaged-fee” accounts, compared with $4.7 trillion in commissioned accounts. One version of these accounts, known as fee-based brokerage accounts, has been under scrutiny in recent years, and a recent federal court decision sharply curtailed brokers from offering them if they are not registered as investment advisers.

The latest memo addresses a particular taxpayer's situation and is aimed at helping IRS agents. But because published guidance is so rare these days, taxpayers and their advisers rely on these publications. The memo may be bad news for taxpayers who are paying wrap fees for their non-IRA accounts. Taxpayers who capitalize their wrap fees could be at higher risk for an audit.

iRs cAnnoT FuLLy scREEn TERRoRisTsThe IRS screening of tax-exempt or-ganizations for potential terrorist activities is inefficient and incomplete, a new federal government audit warns.

The tax agency fails to system-atically match filings of tax-exempt groups against a comprehensive list of potential terrorists, the Treasury Inspector General for Tax Adminis-tration audit found. Instead, the IRS manually compares the filing with an incomplete list.

As a result, “The IRS provides only minimal assurance that tax-exempt organizations potentially involved in terrorist activities are being identified,” the audit concluded.

Since the September 11 terrorist attacks, the Treasury Department has designated six U. S.-based Muslim charities as terrorism supporters. The action halted their activities and led to seizure of millions of dollars in assets.

The targeted charities included the Benevolence International Foundation, an Illinois-based group whose former head, Enaam Arnaout, pleaded guilty to racketeering. None of the organi-zations or their top officers has been convicted of terrorism.

JULY 2007 – THE FEDERAL TAX ALERT5

Domestic charities submitted roughly 300,000 returns to the IRS for tax year 2003, most of them paper filings the latest statistics available show. The filings are reviewed by the IRS Tax Exempt and Government Entities Division for any terrorist ties.

The returns are checked by hand against the names and titles of about 1,600 terrorists or related organi-zations on a list maintained by the Treasury Department's Office of Foreign Assets Control. In all, 201 names were initially flagged for potential terrorist-related connections, the audit showed. None were ultimately found to be matches.

Auditors warned that potential terrorists could slip through the cracks because the IRS does not conduct a more comprehensive, automated check of the more than 200,000 entries on the federal Terrorist Screening Center watch list.

IRS reliance on the less-comprehen-sive list “may have contributed to the small number of potential terrorist-related cases identified to date,” the auditors concluded. They said the IRS should use the Terrorist Screening Center list and start an automated matching system.

Agreeing with the recommenda-tions, Steven Miller, head of the IRS Tax Exempt and Government Entities Division wrote: “We recognize the benefit of using an effective com-puter-based system to search these submissions, and have an active program underway to acquire, test and implement such a system.”

iRs DiD noT czEch iT ouTIn the five weeks prior to April 13, the Internal Revenue Service sent upward of $300,000 worth of one-time $30 federal telephone tax refunds to a single JPMorgan Chase Bank account in Ohio on behalf of at least 10,000 different taxpayers. An IRS lawsuit in Columbus, which led to a freeze on the account, alleged that one Ivo Brabec, listing an address in Edina, Minnesota, but believed to be in the Czech Republic, filed the refund requests, then asked the bank to send the money overseas. The bank blew the whistle to the IRS. In an e-mail filed in court, Brabec says he prepares tax returns for expatriates and did nothing wrong but admits he cannot produce signed authorizations for all the requests.

TERRi McFiELD nAMED spEciAL counsEL The Internal Revenue Service has announced the appointment of Terri McField to the position of Special Counsel to the Chief Counsel-Legis-

lation. She will be replacing Clarissa Potter who became the Deputy Chief Counsel in September 2006.

“We are extremely fortunate to have Terri McField join the Office of Chief Counsel,” said Donald L. Korb, IRS Chief Counsel. “Ms. McField's extensive experience and her substantial knowledge of the legislative process make her an excellent candidate for this position.”

The Special Counsel to the Chief Counsel-Legislation serves as program manager and senior advisor to the Chief Counsel on a broad array of activities designed to fulfill the Chief Counsel's responsibilities to prepare, review, and assist in the preparation of proposed legislation, and to provide legal support to the Internal Revenue Service in fulfilling its legislative responsibilities.

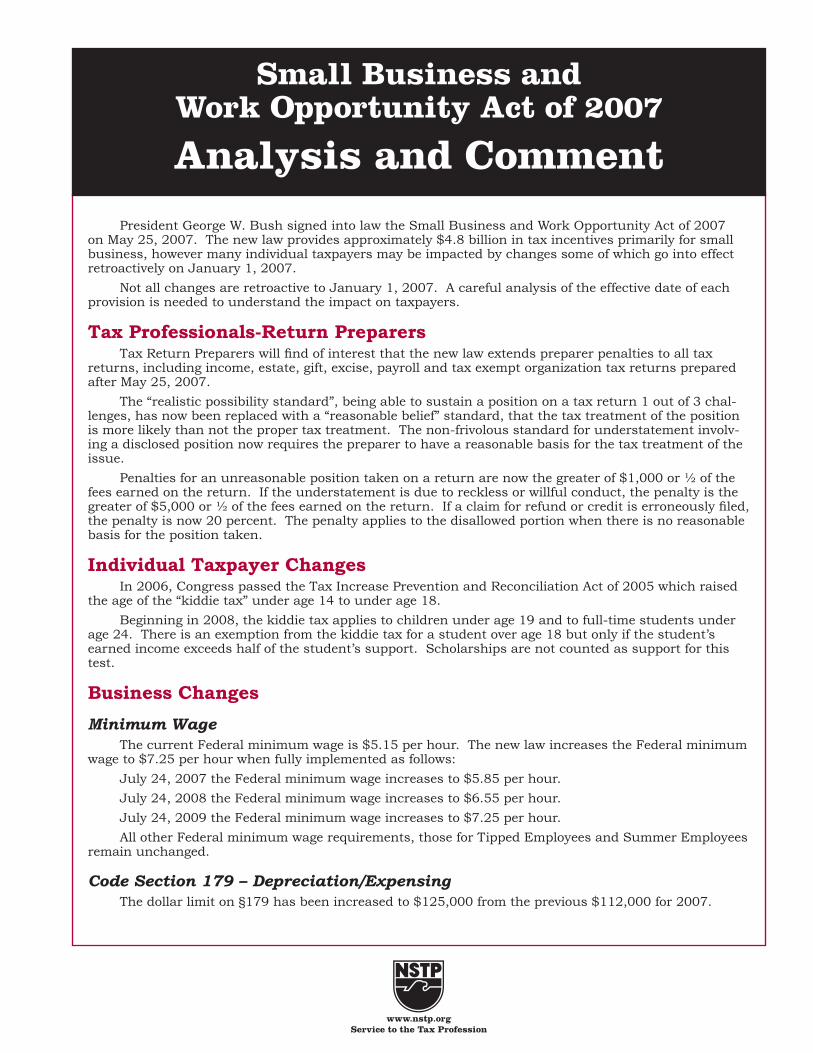

tAX LAw UPDAtecongREss cLosEs 'kiDDiE TAX' LoophoLEA new tax law further tightens the screws on wealthy parents who have made gifts to a child in order to take advantage of a lower tax rate on children's investment income.

The law, part of the Small Business and Work Opportunity Act of 2007, marks the second time in just over a year that Washington has extended the reach of the so-called kiddie tax, which subjects a child's income to a parent's higher tax rate.

What prompted Congress to further expand the kiddie tax were reports that some wealthy parents were planning to take advantage of a tax-law change designed for low-income people that will be effective next year. By extending the reach of the kiddie tax, Congress effectively eliminated many of the benefits of this strategy. Beginning in 2008, the tax rate on long-term capital gains and qualified dividends for those in the 10 percent or 15 percent tax bracket is zero, down from the 5 percent rate in 2007. Many families had anticipated being able to give appreciated stock or other assets to older children with the expectation that the children would sell the assets at a lower tax cost and help pay for their education. Unfortunately, the ability to use income-shifting to children under 19 or students under 24 in most cases, in order to take advantage of the zero rate, has effectively been removed.

Under the new law, the age limit will increase starting in 2008 to

children who are 18, or under 24 if the child is a full-time student. This expanded provision does not apply to financially independent kids, those who earn from working more than half the amount of their support.

Congressional staffers estimate the expanded kiddie tax provision will raise more than $1.4 billion over a decade.

The new law could give a boost to 529 college-savings plans, because investments in these accounts are not subject to the kiddie tax. Tax advisers also say that wealthy parents might seek to invest a child's money in investments that generate little or no taxable income, such as municipal bonds.

An analysis of the Small Business and Work Opportunity Act of 2007 is included as an “insert.”

pRoposAL WouLD chAngE hEALTh, pEnsion covERAgEWorkers would no longer get their health and retirement benefits directly from employers, but would shop through regional “benefit ad-ministrators,” under a proposal released by a group representing more than 100 of the nation's largest employers, including IBM, Tyco, DuPont and General Motors.

If adopted, the proposal could fun-damentally alter how more than 160 million Americans ge their health and retirement coverage, allowing employers a more arms-length approach to offering benefits.

The proposal, which would need con-gressional approval for some elements, comes as state lawmakers and members of Congress debate ways to reduce the number of uninsured and as employers express growing frustration with rising health insurance costs.

It is one of the first detailed approaches presented by American business in the current wave of interest in health reform. The proposal would:

Require everyone to have health •insurance and require workers to make contributions to their own retirement accounts.Allow employers to choose •between sending workers to private-sector benefit admin-istrators to select coverage or to continue to offer health and retirement benefits in-house.Create several standardized •health insurance plans for benefit administrators to offer.Allow the self-employed and •unemployed to purchase coverage through the adminis-trators and create subsidies to help lower-income people.

THE FEDERAL TAX ALERT – JULY 20076

Some consumer advocates see the proposal as an acknowledgment that employers want out.

Legislation would likely be needed for parts of the industry committee's proposal, such as requiring individuals to buy health insurance. The committee's proposal does not include cost estimates.

Employers would have the option of fully funding health insurance coverage, or requiring workers to pay part of it themselves, just as they do under the current system.

INsIDe wAsHINGtON13 BiLLion DoLLARs oF poRk in 2007 FEDERAL BuDgETThe non-profit organization Citizens against Government Waste has spotted 2,658 individual items of unnecessary spending in the 2007 federal budget.

They include:$1.2 billion for 20 F-22A fighter •jets that the General Accounting Office says the Defense Department does not need.$1.6 million for a project •to improve the shelf life of vegetables.

Even though the $13 billion might seem like a lot of pork, the dollar total is down from last year's record $29 billion. This new found fiscal discipline comes in part from lawmakers' desire to stay in office as voters have increasingly turned against high government spending.

The Citizens against Government Waste warn it is the year of the PIG!

RuLEs hiDing TRiLLions in DEBTThe federal government recorded a $1.3 trillion loss last year, far more than the official $248 billion deficit, when corporate-style accounting standards are used.

The loss reflects a continued deterio-ration in the finances of Social Security and government retirement programs for civil servants and military personnel. The loss equal to $11,434 per household is more than Americans paid in income taxes in 2006.

Modern accounting requires that corporations, state governments and local governments count expenses immediately when a transaction occurs, even if the payment will be made later.

The federal government does not follow the rule, so promises for Social Security and Medicare do not show

up when the government reports its financial condition.

The bottom line: Taxpayers are now on the books for a record $59.1 trillion in liabilities, a 2.3% increase from 2006. That amount is equal to $516,348 for every U. S. household. By comparison, U. S. households owe an average of $112,043 for mortgages, car loans, credit cards and all other debt combined.

Unfunded promises made for Medicare, Social Security and federal retirement programs account for 85% of taxpayer liabilities. State and local government retirement plans account for much of the rest.

This hidden debt is the amount taxpayers would have to pay immediately to cover govern-ment's financial obligations. Like a mortgage, it will cost more to repay the debt over time. Every U. S. household would have to pay about $31,000 a year to do so in 75 years.

The Financial Accounting Standards Advisory Board, which sets federal accounting standards, is considering requiring the government to adopt accounting rules similar to those for corporations. The change would move Social Security and Medicare onto the government's income statement and balance sheet, instead of keeping them separate.

Traditionally this type of accounting has been opposed by Washington arguing that the programs are not true liabilities because government can cancel or cut them.

The cost per U. S. household of unfunded promises made by federal, state and local governments:

Medicare $255,280Social Security 144,251Federal debt 43,380Military benefits 25,863State and local debt 17,537Federal civil-servant benefits 14,374State and local retiree benefits 13,114Other federal obligations 2,549total $516,348

hoW Much DoEs MEDicARE cosT AMERicA?In 2006, Medicare benefit payments tallied $374 billion, accounting for 13% of federal spending. Inpatient hospital services comprised the largest share of Medicare benefit payments, 34%, followed by physician and other outpatient services, 24%. Spending on the new prescription drug benefit accounted for a percent of total benefit payments in 2006. With the addition of prescription dug coverage, the composition of

Medicare expenditures is changing. It is predicted by 2010, prescrip-tion drugs will account for 20% of Medicare benefit payments.

Net federal spending on Medicare is projected to increase from $374 billion in 2006 to $564 billion in 2012. The annual growth in Medicare spending is influenced by factors that have general affect, including increasing volume and utilization of services and higher prices for healthcare services. Although Medicare spending increases each year, the average per capita spending growth rate between 1970 and 2004 was slightly lower for Medicare, 8.9%, than for private health insurance, 9.9%, for common benefits, excluding prescription drugs.

Medicare spending accounted for almost one-fifth of the $1.7 trillion in personal health care expendi-tures in the U. S. in 2005. Medicare's share of national personal healthcare expenditures varies by type of service, reflecting benefits covered and services used by the Medicare population. For example, in 2005, Medicare paid for 30% of all hospital spending and 38% of home healthcare spending but less than 2% of prescrip-tion drug costs. In 2006 and future years, Medicare is expected to pay a larger share of natural expenditures for prescription drugs through the Part D drug benefit.

Medicare spending is highly con-centrated among a small share of beneficiaries. A small share of the Medicare population accounts for a majority of Medicare spending. Ten percent of beneficiaries accounted for more than two-thirds of Medicare spending in 2003. At the other end of the spectrum, just over half of all Medicare beneficiaries, 52%, accounted for only 2% of total expen-ditures, while 22% of beneficiaries incurred no expenditures at all.

Medicare spending varies by eligibility category. In 2003, Medicare spending for each beneficiary averaged $5,694. Per capita payments were nearly $1,000 higher for the elderly, $6,191, than they were for under-65 beneficiaries with disabili-ties, $5,325.

Federal Spending in FY2006Program PercentageDefense—Discretionary 20%Social Security 19Nondefense—Discretionary 18Other 16Medicare 13Net Interest 8Medicaid 6

JULY 2007 – THE FEDERAL TAX ALERT7

conFiRMing iRs LEADER couLD pRovE DiFFicuLTConfirmation of the nation's 47th IRS commissioner faces unprecedented difficulties that could delay the nomination of a candidate for the job.

Because Former Commissioner Mark Everson is the first commis-sioner not to serve out an entire 5-year term as commissioner, replacing him is unprecedented and may prove difficult and delicate.

Any nominee will face not only the possibility of a bruising initial confirmation hearing in 2007, but also a second confirmation process in the midst of a presidential campaign in full swing. Additionally, the possibility that the next president, who will be sworn into office in January 2009, may want to appoint a new commissioner only complicates an already complex situation.

But the process could lead to a political agreement that would preempt possible confirmation con-troversies. Under present law, Kevin Brown, currently acting IRS commis-sioner, may serve for a maximum of 210 days. If the President does not nominate a replacement during that period, the President must again nominate an individual as acting com-missioner for another 210 day period. This individual could be the current acting commissioner, Kevin Brown, or someone else.

In all likelihood, Kevin Brown will serve as the acting commissioner until the end of the Bush adminis-tration. The new President will then appoint a permanent commissioner.

FYIQuALiFy FoR MEDicAiD AnD pRoTEcT AssETsThe passage of the Deficit Reductions Act of 2005 (DRA 05) set new rules for who can qualify for Medicaid as their payer for long-term care. Although DRA 05 makes it harder to shelter assets for the purpose of qualifying for Medicaid, it also paved the way for states to share Long-Term Care (LTC) costs with consumers and insurers.

California, Connecticut, Indiana and New York have longstanding LTC partnership arrangements. Arkansas, Colorado, Florida, Georgia, Hawaii, Idaho, Illinois, Iowa, Maryland, Mas-sachusetts, Michigan, Missouri, Montana, Nebraska, North Dakota, Ohio, Oklahoma, Pennsylvania, Rhode Island, Virginia and Washington have authorizing legislation on the books. More states undoubtedly will follow.

An LTC partnership allows those who buy partnership-qualified

LTC insurance policies to protect additional assets and still pass the as-set-eligibility test for Medicaid when their LTC insurance benefits run out. Here is how it works.

Say your policy pays a total of $100,000 in benefits. When you have depleted those benefits, you can shelter an equal amount of your assets ($100,000 in Certificates of Deposit, cash, property, stocks, bonds), plus your state's usual Medicaid allowance for cash, house car and any eligible spousal assets.

But LTC partnership insurance protects only assets, not income. Assets in excess of the dollar-for-dollar protection, as well as income from Social Security, pensions, investments, etc., must be used to pay for care before Medicaid jumps in.

Who should buy these partnership policies? They are designed for middle and low-middle-income consumers. With the new, stricter rules mandated by DRA 05, these are the people most at risk of losing everything in the event of a disabling illness or injury.

Should you wait to buy LTC insurance until your state rolls out a partnership program? You will never be healthier than you are today and only healthy people can buy LTC insurance.

pAiRED pLAns FoR Long-TERM cAREThe national average cost of a private room in a nursing home is $6,266 a month, which is about $75,000 a year. That is the number published by AARP using data from MetLife.

Yet when AARP surveyed Americans age 42 and older about the cost of long-term care, only 8% came within 20% of the real number.

Most respondents to the AARP survey said they through Medicare, the federal health insurance program, or Medigap, private insurance that supplements Medicare, would pay for a long stay in a nursing home. In fact, neither Medicare nor Medigap will pay for extended care in a nursing home.

Instead, about 65% of nursing home residents receive some, or all, of their support from Medicaid, a feder-al-state welfare program. To qualify for Medicaid, individuals must have few assets and low income.

Instead of relying upon Medicaid, one tactic to provide for possible nursing home costs is to buy long-term care, LTC insurance. These policies may cover home care, in addition to care in an assisted living facility.

LTC polices may be expensive. Suppose you buy an LTC policy that will pay a $200 daily benefit, around

$6,000 per month. You can stipulate a 90-day waiting period before these benefits begin, and then you can request a guaranteed purchase option that will allow you to pay for higher benefits in the future if you wish.

You can then ask for a policy that will pay your benefits for up to three years. A policy such as this might cost $1,300 to $1,400 a year, if you buy it at 60-years-old; however, the same policy might cost $1,700 to $1,800 a year, if you choose a five-year maximum payout instead. A policy that pays lifelong benefits will be more costly.

What is more, a married couple will have to pay almost twice these amounts in order to cover both spouses.

One solution is to buy LTC insurance with a “shared care rider.”

With this provision, both spouses could buy a less expensive policy with a three-year benefit period.

Then, if one spouse needs care for more than three years, he or she could use the benefit period of the other spouse's policy. If one dies without using his or her benefit period, the unused amount will be applied to the surviving spouse's maximum benefit.

This solution has worked well for spouses with large age differences. The older spouse gets an extended benefit period, while the premiums are paid at the younger spouse's lower rate.

There is a risk. The spouse who has been well may need care after the maximum benefit has been used up. If this is a concern, the younger spouse might purchase a longer benefit period, which may be more affordable for the younger and, perhaps, healthier spouse.

Long-Term Care Insurance Benefit Premiums Paid in 2006Nursing home care $1,203 millionAt-home care 1,119 millionAssisted living care 978 milliontotal $3.3 billion

Courtesy Gomes and Company, CPA's - Charles Gomes, NSTP Member- FL.

membeRs IN tHe KNOwDr. Bill Stevenson, NSTP Member from NY, learned at a recent IRS meeting that the IRS is using Accurint to research taxpayers' information. To find out what the IRS knows about your client, go to www.accurint.com.

THE FEDERAL TAX ALERT – JULY 20078

Accurint is the most widely accepted locate-and-research tool available to government, law enforcement and commercial customers. Its proprietary data-link-ing technology returns search results in seconds to the user's desktop.

Key features include:People Search….locates •neighbors, associates and possible relatives.Phones Plus….track down phone •numbers not typically available to increase your chances of finding your subject. Access over 50,000,000 non-directory assistance records, including cell phone numbers.People at Work….links more •than 132 million individuals to businesses and includes information such as business addresses, phone numbers, and possible dates of employment.Relavint….visually links •individuals with businesses, addresses, relatives and vehicles.Advanced Person Search….helps •find individuals when only old or fragmented data is available.

Member's In The Know is a new feature. NSTP members wanting to contribute information should email [email protected].

tAX COURt DeCIsIONsLAWREncE L. AnD pAMELA J. cRAnE, pRo sE v. coMMissionER T.c. suMMARy opinion 2007-108 JunE 25, 2007Dependency exemption deduction and child tax credit for the taxable year is at issue.

Mr. Crane is a warehouse manager for Weld Racing, Inc., in Kansas City, Missouri. Mr. Crane was previously involved in a relationship with Melissa Madrigal. Two children were born of the relationship. Mr. Crane and Ms. Madrigal were never married.

On April 3, 1995, a judgment was entered in the Circuit Court of Jackson County, Missouri, establishing Mr. Crane's paternity with respect to two minor children and the amount of child support to be provided to Ms. Madrigal on the children's behalf. The judgment set the amount of support at $233.50 per child or $475 monthly for both.

The judgment specifically provided that the primary physical custody of both children is to be with Ms. Madrigal. Mr. Crane will provide medical insurance. Ms. Madrigal will have the personal exemption for purposes of her State and Federal

income tax reports for child A. If and only if Mr. Crane is current in his child support at the end of the year in issue, he will receive the personal dependency exemption on his State and Federal income tax returns for child B.

During the taxable year in issue, both children resided with Ms. Madrigal. Mr. Crane had visitation with child B only on alternating weekends, holidays, and Father's Day during the year in question. Mr. Crane paid the total amount of his required child support during the year.

Mr. Crane claimed child B along with another minor child on his jointly filed tax return for 2002.

The IRS issued a notice of deficiency disallowing Mr. and Mrs. Crane's claimed exemption for child B on the grounds that another taxpayer had also claimed child B on their tax return. Mr. and Mrs. Crane maintain their entitlement “by contract and court order” to claim child B as their dependent during the year of 2002.

Mr. and Mrs. Crane bear the burden of proof that the Commissioner's de-termination in the notice of deficiency is erroneous.

Internal Revenue Code §151 allows deductions for personal exemptions, including exemptions for dependents of the taxpayers. §152(a) defines the term “dependent”, in pertinent part, to include a son or daughter of the taxpayer over half of whose support for the calendar year was received from the taxpayer.

§152 carves out a special exception to the provisions in the case of parents who are divorced or separate. Simply put, §152(e)(1)(B) provides that the parent having legal custody for the child at issue is entitled to claim the dependency exemption deduction for that child unless the noncustodial parent is shown entitled to the deduction under §152 or the custodial parent has validly executed a written release of his or her right to claim the deduction as the custodial parent of record.

In this case, the parties agreed, and the record is clear, that Mr. Crane was not the custodial parent of child B during the year in issue. The record is also clear that Ms. Madrigal did not execute a valid release pursuant to child B in 2002. Accordingly the remaining inquiry is whether Mr. Crane provided over half of the support for child B during the year in issue.

Mr. and Mrs. Crane submitted evidence showing they provided $3,347 in support for child B consisting of $2,729 in child support and $618 in medical and dental insurance costs. They credibly testified that they purchased clothing

and food for child B while in their custody but could provide no evidence of such. Additionally the Cranes could not provide evidence of the amount of total support expended on child B in order to substantiate the claim of providing more than half of the support for child B.

Mr. Crane, although unable to substantiate his claim of providing more than half of the support for child B, cited the judgment of child support and the written permission to claim child B.

The court reminded Mr. Crane that it is well settled that State courts, by their decisions, cannot determine issues of Federal tax law.

Unfortunately, irrespective of what is contained in the judgment as to Mr. Crane's right to claim a dependency exemption for child B the law is clear that the Cranes are entitled to a dependency exemption in the 2002 taxable year if, and only if, they are in compliance with §152. The Cranes have failed to meet this requirement.

With respect to the child tax credit the Cranes claimed for child B in 2002, §24 (a) authorizes a child tax credit with respect to each qualifying child of the taxpayer. The term “qualifying child” means an individual with respect to whom the taxpayer is allowed a deduction.

The Cranes are not allowed a deduction with respect to child B nor is she a qualifying child for the child tax credit, irrespective of language in the judgment to the contrary.

et CeteRAFEWER pEopLE ARE sAvingPercentage of U. S. households saving and investing for retirement.

Year Percentage2000 78%2001 69%2002 72%2003 71%2004 68%2005 69%2006 70%2007 66%

55+ savers have not saved much.Amount PercentageLess than $10,000 . . . . . . . . . 26%$10,000 to$24,999 . . . . . . . . . . 5%$25,000 to$49,999 . . . . . . . . . . 9%$50,000 to$99,999 . . . . . . . . . 11%$100,000 to$249,000 . . . . . . . . 20%$250,000 toMore . . . . . . . . . . . . 28%

JULY 2007 – THE FEDERAL TAX ALERT9

BABy BooMERs sTART BusinEssEs To ADD incoMEMore businesses are started by baby boomers, those aged 45 to 64, than by any other age group.

Many of the boomers are starting businesses because they are afraid they have not saved enough for the kind of retirement they have dreamed about. They hope a business can provide regular income or a retirement nest egg if the company can be sold at some point.

Some boomers even are using their savings to finance a new company, a risky and troubling gamble. What if the company fails, as they often do? The owners would lose everything.

Businesses are almost doomed from the start if owners do not build a support network around them. Legal, insurance, financial, accounting and tax professionals can reduce risks to help boomers achieve what they want from a new business, money for retirement.

RETiREMEnT AgE is EDging upA growing portion of the U. S. work force seems to have decided not to retire at age 65. After falling for more than 100 years, the retirement age chosen by working Americans is edging up again, and the trend could have broad consequences for households and the economy.

In the mid-1980's, just 18 percent of people in their late 60s still had jobs, according to the Bureau of Labor Statistics. That figure is up to 29 percent, and experts believe the level will rise as people confront the prospect of a lengthy and expensive old age with limited retirement benefits. More than 1 in 4 baby boomers, the generation born from 1946 to 1964, plan to never retire.

Many will not achieve that goal. Health problems and workplace pressures such as cutbacks force many workers into retirement earlier than they expect. Employers who have a choice often prefer the young, viewing older workers as costly and resistant to new technologies.

For many years, society made it increasingly easy to stop working. Social Security retirement benefits were enhanced repeatedly after World War II. The advent of Medicare in 1965 helped pay the medical bills. Large employers typically offered pensions that guaranteed payments for life.

Today's workers face a more hazardous landscape. Traditional pensions are increasingly rare. Companies are cutting back retiree health-care benefits.

Even the bulwark of Social Security is retrenching quietly. The traditional age of 65 to qualify for full retirement

benefits gradually is moving upward. Medicare Part B has increasingly higher premiums. These growing financial pressures might hit baby boomers particularly hard. As much as 80 percent of this group expects to work during what normally would be their retirement years.

Ten years ago, the typical age of retirement for all U. S. workers was 60. Recently, it has risen to 62 overall, a shift that researchers think might be partly tied to the increasing reliance on 401(k) plans and the decline of traditional pensions that guaranteed monthly payments for life.

The trend potentially could have a big effect on society, putting more money in the pockets of the elderly and even giving the economy a boost, as more workers continue paying income taxes in their golden years. It could also markedly reduce the projected shortfall in Social Security.

The economy's long-term shift toward knowledge-based jobs and away from physical labor is another force that might be increasing the rolls of older workers. Already, older employers with higher levels of education seem to be playing a major role in the trend. It remains unclear how far the trend toward working late in life will go. Society is much richer than the days when people worked almost until death, and early retirement continues to hold some of its allure.

tAX ReP ROUNDtAbLeiRs cRiMinAL invEsTigATion The IRS Criminal Investigation division has 4,400 employees worldwide. There are 2,800 Special Agents. IRS Criminal Investigation is the only division with jurisdiction over Title 26 violations and the tax law is their focus.

Their conviction rate is 91.3% and the ten-year average is 91.2%. The strategic plan for CI is to improve taxpayer service, enhance enforcement of the tax law, and to modernize the IRS through its people, processes and technology.

In FY2006 CI completed numerous investigations with an average of 46 months of prison time served by those convicted. Their publicity rate is at an all time high - 75.6% and many cases are indicted around the tax filing deadlines in order to make a greater impact. All of their cases must be approved by the Department of Justice. CI classifies their cases as legal source and illegal source cases.

Legal source cases are unreported income and fraudulent expenses. Illegal source cases are where the income comes from illegal activities. CI also investigates narcotics cases as very often drug dealers do not touch the drugs but always touch the money. The current areas of emphasis for CI include the following:

Corporate Fraud:• The Sarbanes-Oxley Act was passed in 2002. It holds corporate officers responsible for the content of their corporate financial statements and income tax returns. There was a 93% FY2006 conviction rate and the sentence can be up to 20 years in prison.employment tax: • These schemes commonly include pyramiding, employment leasing, paying employees in cash, filing false payroll tax returns or failing to file payroll tax returns, and illegal alien cases. There was a 98.1% conviction rate in FY2006.Abusive tax schemes:• Schemes are usually complex involving multi-layer transactions for the purpose of concealing the true nature and ownership of the taxable income and/or assets. The most common are abusive trusts. There was a 93.1% conviction rate in FY2006.Non-Filers:• Non-filers are always a problem. There is case law that demonstrates if an individual does not file several years in a row with a substantial amount of unreported income that the charge can be elevated to a felony tax case. Most cases are still at the misdemeanor level, however, and Congress is considering a law that would make non-filing a felony offense. CI initiated 462 investigations in FY2006 on non-filers and 270 were sentenced and served an average of 41 months.Refund Crimes:• In FY2006, there was a 96.8% conviction rate for questionable refund cases and a 96.6% conviction rate for abusive return preparers. There are fraud detection centers located near each of the IRS campuses where many of the fraud schemes are detected. They investigate identity theft cases and most recently the telephone excise tax refunds as well as social security number fraud.e-Filed Returns:• There were 73 million e-filed tax returns received as of October 20, 2006. 52.9 million were filed by tax professionals and 20 million

THE FEDERAL TAX ALERT – JULY 200710

were filed from home computers and the rest were filed at a library or other offsite location. A large percentage of fraudulent e-filed returns exist. In FY2005, 74,000 of the fraudulent e-filed returns had RAL indicators on them. The top five states for false e-filed returns were New York, Florida, California, Georgia and Texas.Return Preparer Program: • For FY2006 there were 197 investi-gations initiated. 109 preparers were sentenced with 18 months being the average time served.Questionable Refund Program:• For FY2006 there were 219 inves-tigations initiated. 150 individuals were sentenced and 21 months was the average time served.National excise tax Refund:• A national press release will soon announce indictments. One false return alone claimed a credit of $137,228.money Laundering:• The main motivation of money laundering is to hide untaxed income from illegal sources. CI is the largest user of the Bank Secrecy Act data. Atlanta, GA has a high percentage of mortgage fraud.

For filing season 2005, there were ap-proximately 11,000 scheme referrals given to the IRS which included $29 million in refunds. These refunds were part of schemes totaling in excess of $255 million.

From the recent IRS Liaison meeting in Atlanta as reported by Laurie Conner Jarrett, NSTP Director.

inTERviEW WiTh ninA oLson, nATionAL TAXpAyER ADvocATEQuestion: Many practitioners will be interested in your concerns about the failure to keep the Internal Revenue Manual up to date and to reflect in it all internal directives, and various failures to post electronic guidance that should be posted publicly. This could involve guidance that is of interest to business as well as individuals. Please describe the guidance material that you believe to be not properly available to the public and whether the IRS response to your concerns will solve the problems.

Answer: This issue came up because over the years I would see IRS memos that to me were very important instructions to staff in a memo format as interim guidance that would ultimately be incorporated into the Internal Revenue Manual. Theoretically these memos have a shelf life of a year. If they are not in-

corporated into the IRM within that time, they are no longer effective, but they are still sitting out there on internal IRS websites and employees are following them. Yet taxpayers do not have a clue. They look at the IRM and say, “The IRM says you will do X, Y and Z.” Then they are on the phone with an employee who says, “Oh well, now we do A.” Then the taxpayers says, “But it says X, Y and Z.” “Well, no, we do A.”

That kind of irrationality, with taxpayers not knowing what is expected of them, is harmful to the taxpayer and also to the tax system as a whole. So I asked my staff to develop a project where we went to each part of the IRS, every operating division and Appeals and the Office of Chief Counsel. We looked at their internal procedures for posting things and for getting things into the IRM. We also looked at their redaction procedures if something was for official use only, then what did they do with internal guidance. We looked at specific examples of some internal guidance that had not been put into the IRM, although we thought it was very important and needed to be out there.

I have to say that the IRS's response was as a whole absolutely positive. There is a unit in the IRS whose job is to try to make everybody put the guidance into the IRM that needs to be there. They really welcomed our attention and, as part of the process of us working on the most serious problem for this year's annual report, they issued memos immediately after the annual report that they had been working on for a while. For example, they reminded the operating divisions about the interim guidance process and that there was already information out there that was directing the operating divisions to get these internal guidance memos into the IRM within a certain amount of time, such as ninety days. That was very positive.

Just recently the IRS sent out directions to its employees on how to redact IRMs, because one of the findings we found is that 25$ of some IRM pages were classified “official use only.” If there was just one mention on a page that was for official use only, employees would just redact the whole page. The new guidance says, “Here is how you do redactions- do not redact the whole page if you can just redact a line or a paragraph or a section.” That is an enormous improvement.

What we were really reviewing in this whole process was not necessarily what was required to be

provided by FOIA or by §6110 on any other provision of law, but what taxpayers need to know in order to comply with their tax obligations, which if they did not get it, they would be harmed. So we really set aside all legal and legalistic analysis, and just ask,”What do taxpayers need to know?” looking at it from the Taxpayer Advocate perspective.

I am pleased with the attention that the IRS is giving to the IRM. The IRM is very important to the practitioner. The Annual Report discussion also helped me understand better how these things happen because under-standing how they happen is the first step in coming up with a solution. I am also really pleased with that.

An interview with Nina E. Olson, ABA Section of Taxation News Quarterly.

iRs nATionAL puBLic LiAison puBLishEs signiFicAnT issuE REpoRTThe Internal Revenue Service Office of National Public Liaison has published their Significant Issue Report for Stakeholders for reporting period October 2006 through April 2007.

Among the issues reported:Issue for SB/SE - The NSTP member requests a listing of all tax specific service centers with addresses, such as OIC in Brookhaven and Memphis, etc. Is there a single location where a person could access the information?

Response/Resolution/ActionSeveral ideas were explored regarding how to make the information readily available to tax professionals. Many of the resources considered are not approved for external use. However, after speaking with SB/SE's Head-quarters Stakeholder Liaison staff, it was learned that they had a similar project well underway. They reviewed the suggestions and made some modifications to their new web page to include information on innocent and injured spouse issues. They are working to add contact information for insolvency issues as well.

We appreciated the time that NSTP took to work with SB/SE field liaison staff to ensure that everyone understood the suggestions properly and could build them into the new web page. The web page is now live and can be found at the following URL: http://www.irs.gov/businesses/small/article/0,,id=158633.00.html. It is also easily reached by clicking on the “Where to File” buttons on the left of most of IRS.gov screens.

JULY 2007 – THE FEDERAL TAX ALERT11

Issue for OPR:Can the IRS use Section 10.20(a) to require a practitioner to provide information that the taxpayer-client would not be obligated to provide through a summons enforcement proceeding?

Response/Resolution/ActionThe Service has not published guidance on this but has said that a taxpayer does not lose his/her ability to put the IRS to the test of summons enforcement simply by hiring a rep-resentative who is covered by Circular 230. If the client believes the request is improper or unlawful, the practitio-ner does not violate Circular 230 by declining to provide the information requested and forcing the IRS to exercise its rights under the IRC.

Issue for OPR:NSTP asked: Circular 230 seems to address the procedure by which an attorney, CPA, EA can be suspended or disbarred from practice before the IRS, including appeal to an Adminis-trative Law Judge, but there does not seem to be a procedure for appealing to federal court.

Response/Resolution/ActionAccording to the Office of Profes-sional Responsibility, in order to get to Federal District Count, all you need is to have an adverse final agency decision. Circular 230 covers the process from initial complaint to Administrative Law Judge trial, to appeal to the designee of the Secretary of the Treasury. That designee makes the Final Agency Decision.

iRs sMALL BusinEss opERATing Division hoLDs MEETing

At the June SB/SE National Practi-tioner Forum, NSTP was represented by Dr. Bill Stevenson, NSTP Member NY. Keith Huebel, NSTP Member from Maryland was unable to attend.

Issues of interest to the tax profes-sional community include:

Mike Mullin, IRS Program Analyst, working on National Standard Allowances indicated that there are several proposals being evaluated:

Elimination of income 1. ranges for national standard allowances.Adopt a new methodology 2. for calculating miscellaneous expense.

A lively discussion ensued regarding Revenue Officers not being encouraged to deviate from the published guidelines.

Several recommendations were made:

One recommendation was to auto-matically increase the standards by inflation each year.

Local Standards:Expand to include households 1. with a larger number of residents.Include an additional sum for 2. cell phones.Cable and Internet will not be 3. included and still considered to be a discretionary item. It can be included under the health and welfare of the taxpayer when allowed.

Transportation:Remove public transporta-1. tion from operating costs. Commutation will be considered as an additional expense.Change ownership and 2. operating costs for the second car to equal the first car. This will result in a reduction of the costs allowed for car one but increase it for car two. Docu-mentation will not be required unless the amount is higher than-the chart.

It was recommended that the IRM include the assumed mileage for commutation to allow practitioners to add costs for increased mileage beyond the assumption. This recommenda-tion, being very specific, was met with great enthusiasm by the IRS. There was discussion about future transpor-tation needs reducing the amount of the Installment Agreement during the payout period.

Health:There will be a new standard for out of pocket expenses above insurance premiums. Documentation will not be required for $17 under 65 and $75 for 65 and older taxpayers.

The adoption date for these new proposals to go into effect is uncertain.

Floyd Williams, National Director of Legislative Affairs, discussed recent legislation and pending legislation. While no one is ever sure about legislative agendas, he thought that the fate of private debt collections would be known by July 4. He was not optimistic about the registration of tax preparers feeling it might be revived at some time in the future but not passed this session.

Bob Erickson of Tax Forms and Publications explained that for 2008 there will not be a requirement to send in a signed 8453. Attachments will continue to be sent with either a newly titled Form 8453 or some other numbered form used as a transmittal.

Jodi Patterson, Director of the Office of Taxpayer Burden Reduction, discussed Forms 944 and 941X and a redesign of the 940. A new innocent spouse form will be published in the next few months.

We will be looking to the Federal Register at the end of July for the new Taxpayer Burden Tables showing how long it takes to prepare the various forms for tax preparation.

etHICs CORNeRTAX-shELTER inDicTMEnTs LEAvE cLouD ovER ERnsTBroadening a high-profile probe into the sale of improper tax shelters, federal prosecutors secured indictments of four current and former partners of accounting giant Ernst & Young LLP for designing and selling structures that brought the firm millions of dollars in fees.

The indictments show the U. S. Attorney in Manhattan is not backing down in the government's investiga-tion of fraudulent tax shelters despite recent setbacks in the prosecution of 16 former KPMG LLP executives similarly charged over shelters sold by that firm.

A trial in that case, billed by the government as the largest-ever criminal tax case in U. S. history, has already been twice delayed. A recent appellate-court ruling related to the defendants' legal fees threw the September trial date into doubt and raised the possibility that the case could be dismissed.

The recent indictment charges that the current and former Ernst partners designed and sold four types of tax shelters for the ultra rich that either generated paper losses based on sham investments to offset taxable income or disguise income as capital gains so that it would be taxed at a lower rate.

In both cases, Ernst received fees based on the amount of tax savings generated by the shelters.

The partners are also charged with trying to prevent detection by the Internal Revenue Service of the shelters and of using and selling to other Ernst partners a shelter that shielded $3.7 million in personal income.

Ernst itself is not expected to face criminal charges, however the firm is not completely out of the woods. The indictment noted that the sale of the allegedly bogus tax-shelter products brought the firm about $120 million in fees. Ernst and

THE FEDERAL TAX ALERT – JULY 200712

the government are continuing to discuss settlement options that would likely fall short of an indictment but include monetary sanctions.

Ernst in 2003 entered into a civil settlement with the IRS related to its shelters and agreed to pay a $15 million fine.

During the hearing in this most recent case, the indicted Ernst partners pleaded not guilty to charges that included conspiracy, obstruction of the IRS, making false statements and tax evasion. Attorneys for three of the men said they plan to fight the charges, while an attorney for one declined to comment. If convicted of all charges, the four men face prison terms ranging from 10 years to 18 years.

Prosecutors charged that the partners went to considerable lengths to create the impression that the shelters had valid business or trading purposes and were not simply designed to garner tax benefits. The partners had repeatedly stressed that clients should never be given materials that could one day find their way into the government hands. Included in an uncovered e-mail from one of the partners, “a fax of the materials to certain people in the government would have calamitous results,” the indictment said.

After learning the IRS was auditing some clients who used the tax shelter, one of the partners sent an e-mail to some Ernst staff telling them to “immediately delete and dispose of” the tax shelter documents.

This indictment marks another step in the government's pursuit of tax shelter promoters. They are also consistent with a strategy in which prosecutors have sought to criminally charge individuals, rather than firms.

In 2005, the government entered into a deferred prosecution agreement with KPMG that called for the firm to pay a $456 million penalty but allowed it to avoid criminal indictment.

FiLing coMpLAinTs—hoW ToHow to File a Complaint against a Licensed tax ProfessionalA complaint should be written in a letter format. The letter should include the tax practitioner's name, address, telephone number, designation (attorney, certified public accountant, enrolled agent, enrolled actuary, etc.), a detailed description of the allegations, and any documents that support those allegations. Direct all referrals to:

Internal Revenue Service Office of Professional Responsibility SE: OPR, Room 7238/IR 1111 Constitution Avenue NW Washington, DC 20224

Or fax to 202-622-2207. Questions concerning an allegation should be e-mailed to [email protected].

How to File a Complaint against an unenrolled tax preparerComplaints against unenrolled tax preparers can be reported by completing Form 3949-A or a letter with similar information to Internal Revenue Service, Fresno, CA 93888.

How to Report suspected tax Fraud ActivityIf you suspect or know of an individual or company that is not complying with the tax laws, you can report this activity by completing Form 3949-A or by writing a letter including the name and address of the person, the taxpayer identification number, a brief description of the alleged violation including how you became aware of or obtained the information, the years involved, the estimated dollar amount of any unreported income, and your name, address and daytime phone number. You may be entitled to a reward. Send this information to Internal Revenue Service, Fresno, CA 93888.

membeRs AsKpART ii. EDucATion issuEs— conTinuED FRoM JunE FEDERAL TAX ALERTADjUstmeNts tO INCOme stUDeNt LOAN INteRest DeDUCtION

student loan interest defined.Student loan interest is interest you paid during the year on a qualified student loan. It includes both required and voluntary interest payments.

student loan interest is defined as:A loan you took out solely to pay qualified education expenses that were:

For you, your spouse, or a person who was your dependent when you took out the loan;

Paid or incurred within a reasonable period of time before or after you took out the loan; and

For education provided during an academic period for an eligible student.

who is a dependent?Generally, your dependent is someone who:

Provides less than one-half of his or her own support.

Is either related to you or lives with you, and

Is a U. S. citizen, U. S. resident, or resident of Canada or Mexico?

eXCePtIONsFor the purpose of the student loan interest deduction, there are the

following exceptions to the general rules for dependents:

You can have a dependent even if you are the dependent of another taxpayer.

An individual can be your dependent even if the individual files a joint return with a spouse.

An individual can be your dependent even if the individual had gross income that was equal to or more than the exemption amount for the year.

Other issuesThe Student Loan Interest Deduction has a number of specific requirements including:

Qualified education expenses are treated as paid or incurred within a reasonable period of time before or after you take out the loan if they are paid with the proceeds of student loans that are part of a federal post-secondary education loan program.

Even if not paid with the proceeds of that type of loan, the expenses are treated as paid or incurred within a reasonable period of time if both of the following requirements are met:

The expenses relate to a specific academic period, and

The loan proceeds are disbursed within a period that begins 90 days before the start of that academic period and ends 90 days after the end of that academic period. The previous 60 day rule was extended to 90 days in 2006.

An eligible student is defined as a student who was enrolled at least half-time in a program leading to a degree, certificate, or other recognized educational credential.

“Enrolled at least half-time” is defined as taking at least half the normal full-time work load for his or her course of study.

Practitioner's Alert: The standard for what is half of the normal full-time work load is determined by each eligible educational institution. However, the standard may not be lower than any of those established by the Department of Education.

You cannot deduct interest on a loan you get from a related person. Related persons include:

Your spouse,•Your brothers and sisters,•Your half brothers and half •sisters,Your ancestors, parents, •grandparents, etc.,Your lineal descendants, •children, grandchildren, etc., andCertain corporations, partner-•ships, trusts, and exempt organizations.

Practitioner's Alert: You cannot deduct interest on a loan made under a qualified employer plan or under a contract purchased under such a plan.

JULY 2007 – THE FEDERAL TAX ALERT13

Qualified education expenses include:Tuition and fees.•Room and board.•Books, supplies, and equipment.•Other necessary expenses, such •as transportation.

The cost of room and board qualifies only to the extent that it is not more than the greater of:

The allowance for room and •board, as determined by the eligible educational institution, that was included in the cost of attendance for a particular academic period and living ar-rangements of the student, orThe actual amount charged if the •student is residing in housing owned or operated by the eligible educational institution.

what type of interest can be claimed?In addition to simple interest on the loan, if all other requirements are met, the following items can be student loan interest:

Loan origination fees.•Capitalized interest.•Interest on revolving lines •of credit.Interest on refinanced •student loans.Voluntary interest payments.•

Figuring the DeductionIn 2006, the deduction for student loan interest is generally the smaller of:

$2,500, orThe interest you paid in 2006.

tuition and Fees DeductionThe tuition and fees deduction can reduce the amount of income subject to tax by up to $4,000.

who can claim?Generally, you can claim the tuition and fees deduction if all three of the following requirements are met.

You pay qualified education expenses of higher education.

You pay the education expenses for an eligible student.

The eligible student is yourself, your spouse, or your dependent for whom you claim an exemption on your tax return.

who cannot claim the deduction?You cannot claim the tuition and fees deduction if any of the following apply:

Your filing status is married filing separately.

Another person can claim an exemption for you as a dependent on his or her tax return. You cannot take the deduction even if the other person does not actually claim that exemption.

Your modified adjusted gross income, MAGI, is more than $80,000 ($160,000 if filing a joint return).

You were a nonresident alien for any part of the year and did not elect to be treated as a resident alien for tax purposes.