Embed Size (px)

Citation preview

Stakeholder Feedback

Document

Future Energy Scenarios: January 2017

Welcome to the Future Energy Scenarios Stakeholder Feedback Document for

2017

This publication is part of our annual scenario development process. It summarises how we

have engaged with our stakeholders over the past year, key themes from this engagement,

how we develop our scenarios and our initial thoughts on the new suite of Future Energy

Scenarios (FES) for 2017. This year we have also included an annex containing a review of

the actions we said we would undertake in the 2016 Stakeholder Feedback Document and

the associated progress and outcomes. You will also find an overview of the team that

produces the FES.

This document is the latest of our suite of ‘Future of Energy’ publications which demonstrate

our commitment to transparency and meeting the needs of our stakeholders. This suite

includes: Electricity Ten Year Statement (ETYS), Gas Ten Year Statement (GTYS), System

Operability Framework (SOF), Network Options Assessment (NOA), Gas Future Operability

Planning (GFOP) along with our Winter Outlook Report (WOR) and Summer Outlook Report

(SOR).

Our Licence Requirement

National Grid’s Electricity Transmission Licence Standard Condition (C11) requires the

submission of our proposed future energy scenarios and associated stakeholder

engagement to Ofgem by the end of January each year. This document is our submission.

Foreword

Marcus Stewart, Head of Energy Insights

“I am excited to be leading the team that develops the FES and be a part of our

‘Future of Energy’ publications. Once again we’ve had some fantastic engagement

with our stakeholders which has delivered real intelligence and insight for us to

consider as we build FES 2017. In addition to this feedback we utilise a wide range of

different information sources and apply our judgement to help build a picture of the

future pathways for energy. There are so many uncertainties regarding the future of

energy for Great Britain and as you will have seen in the past year lots has changed

on both an economic and political front too.

You had a lot of positive things to say about FES 2016 with a wealth of ideas for FES

2017. I would like to take this opportunity to thank you for giving us your time and

energy during this engagement. We continue to seek improvements in our

engagement, modelling and outcomes to ensure we maintain great relationships with

our current stakeholders and target new stakeholders to enhance the richness of the

scenarios. We plan to do even more of this as we move forward in to 2017.

I hope you find this publication useful and we look forward to sharing the outcome of

our FES 2017 work with you later this year.”

Executive Summary

Enhancing our scenarios for FES 2017 Each year we review our scenarios to ensure they remain credible and fit for the various purposes that

we and our stakeholders use them for. This year we’ve seen big changes economically, politically and

within the energy sector. We take account of these changes, review the feedback we receive from our

stakeholders and apply our own analysis and expertise to shape the scenarios for 2017.

As in previous years, all of our scenarios will consider energy demand and supply with a whole system

view. To reflect recent trends in the electricity market, two of our four core scenarios for 2017 will have

high levels of distributed generation growth (compared to one last year), with the other two scenarios

featuring more moderate growth rates of distributed generation to reflect uncertainty over embedded

benefits.

In addition, we will use a wider range of economic growth forecasts for FES 2017 to account for the

uncertainty created by Brexit.

Building on our work in FES 2016 on different sensitivities on the Gone Green scenario and subsequent

stakeholder feedback, we will develop a broader range of sensitivities for FES 2017 to explore potential

outliers around the four main scenarios.

The name Gone Green will be retired to reflect that the scenario has changed in focus from renewable

generation to low carbon since it was introduced in 2011. The new name, ‘Two Degrees’, signifies that

this will continue to be our core scenario that meets the 2050 carbon reduction targets. We will also retire

the name ‘No Progression’ and replace it with ‘Steady State’ to better reflect the content of this scenario

and the stakeholder feedback we have received.

Making clear what has changed and why We take account of the latest data, trends and changes in the energy industry and evolve our scenarios

year on year. Our stakeholders have told us that it is crucial they understand what has changed since

the last FES publication, and why. Therefore, in addition to updating the scenarios to ensure they

continue to represent credible future pathways, we will make clear in our FES publications what the key

changes are.

Delivering our views and opinion Through the FES process we gather a wide range of information, including stakeholder feedback,

economic and industry data and discussions with subject matter experts. We review all of this

information, undertake our own analysis and use our judgement to create robust and well-informed views

about the energy future. Stakeholders have told us they would like to see more of our views in 2017. We

will introduce a series of thought pieces to provide our views and opinions on hot topics and key changes

within the energy industry. You will hear more on this throughout the year.

Widening our engagement Stakeholder feedback is a key part of the FES development process and we use it to feed into our own

analysis and test our approach and assumptions. We continually improve our approach to stakeholder

engagement to meet the needs of our customers and stakeholders. This year we held our first

stakeholder workshop in Wales, ran webinars for those unable to make the launch conference and

enhanced our summary FES in 5 document. During 2017 we will share our emerging analysis with

stakeholders to get earlier feedback and tap into the information and intelligence they hold as we

develop our analysis.

Contents Foreword Why do we create scenarios? Contents

Section one: Why do we create scenarios? Pages 1-5

Section two: Our engagement Pages 6-11

Section three: Our proposed scenarios for FES 2017 Pages 12-15

Section four: Stakeholder feedback and FES 2017 Pages 16-22

Section five: Next steps and future improvements Pages 23-24

Section six: Continuing the conversation Page 25

Section seven: Annex: Pages 27-40

Meet the Energy Insights Team Pages 27-29

Organisations engaged, breakdown Pages 30-34

FES 2016: You said, we did Pages 35-40

1

Why do we create scenarios?

We continue to be in a period of great uncertainty over the future of energy for Great Britain.

The political, economic, technological and consumer landscapes are changing at an

unprecedented rate. Against this backdrop it is impossible to forecast a single pathway for

our energy future over the long term. In response to this we use the approach of scenario

development to explore plausible and credible futures.

By providing a suite of credible pathways, we seek to help understand uncertainty and

provide our views to inform the energy market. Our stakeholders have told us that they like

this approach and that they use our scenarios for a range of purposes. We continually

evolve our approach to reflect the changing energy landscape and use of the scenarios. This

allows us to better prepare not only our business, but also our stakeholders for the different

outcomes, and to put in place best value solutions.

How do we develop our scenarios?

The production of our scenarios is an annual development process with several key stages,

which include our engagement, data and intelligence gathering , followed by high level

scenario creation and detailed modelling. At each stage in the development process we

apply our expertise and judgement to ensure we deliver plausible and credible scenarios.

Feedback from our stakeholders, such as industry experts within their fields, is a key part of

the development of FES, but we also undertake our own intelligence work and add our

expertise to the process. This ensures our scenarios are well-informed, up-to-date and

provide a robust basis for our own planning activities as well as for our stakeholders.

Within this document we will discuss in more detail the development of our scenarios and a

forward look at our proposed scenarios for 2017.

How do we use the scenarios?

We use our scenarios as a foundation for a range of modelling activities. FES is the starting

point for our regulated long term investment and operability planning as well as a reference

point for further analysis projects (see Figure 1 below). As each process has its own specific

requirements, further detailed analysis is undertaken building on from the FES. Below we

summarise where the FES is used within our business.

Se

ctio

n o

ne

2

Why do we create scenarios?

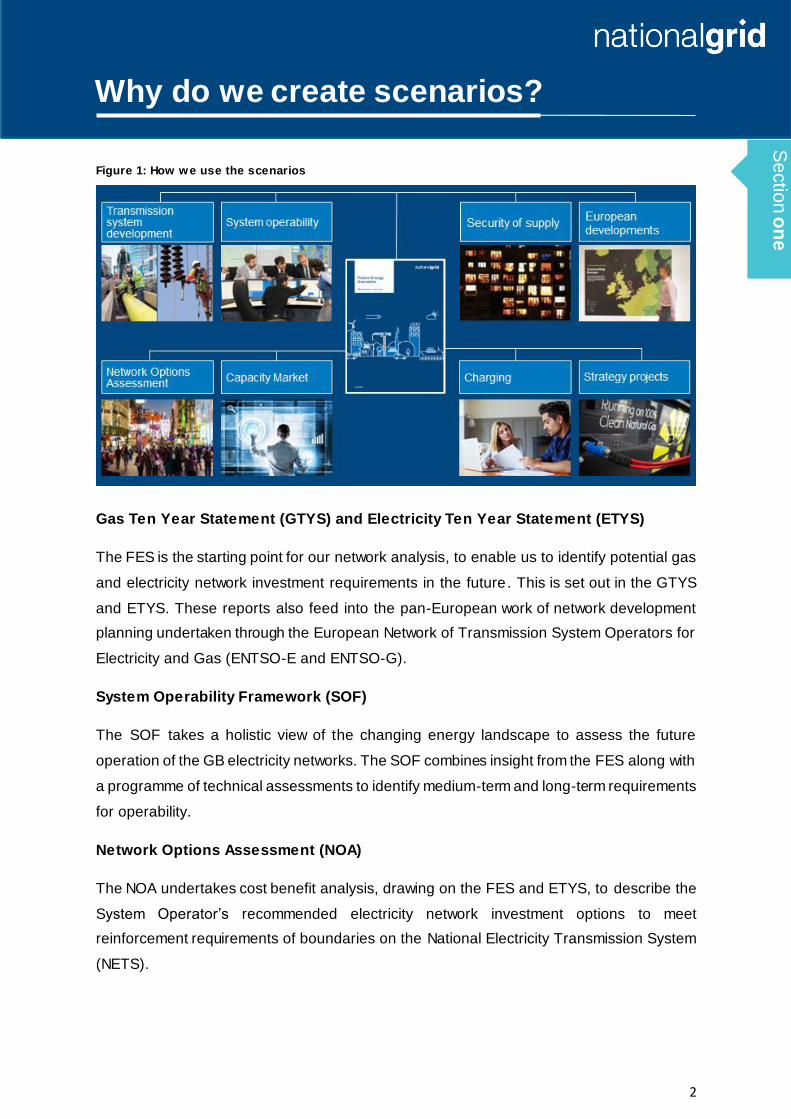

Figure 1: How we use the scenarios

Gas Ten Year Statement (GTYS) and Electricity Ten Year Statement (ETYS)

The FES is the starting point for our network analysis, to enable us to identify potential gas

and electricity network investment requirements in the future. This is set out in the GTYS

and ETYS. These reports also feed into the pan-European work of network development

planning undertaken through the European Network of Transmission System Operators for

Electricity and Gas (ENTSO-E and ENTSO-G).

System Operability Framework (SOF)

The SOF takes a holistic view of the changing energy landscape to assess the future

operation of the GB electricity networks. The SOF combines insight from the FES along with

a programme of technical assessments to identify medium-term and long-term requirements

for operability.

Network Options Assessment (NOA)

The NOA undertakes cost benefit analysis, drawing on the FES and ETYS, to describe the

System Operator’s recommended electricity network investment options to meet

reinforcement requirements of boundaries on the National Electricity Transmission System

(NETS).

Se

ctio

n o

ne

3

Why do we create scenarios?

Gas Future Operability Planning (GFOP)

The FES feeds through to the recently launched GFOP, which describes how changing

requirements may affect the future capability of the National Transmission System (NTS) out

to 2050, and the challenges that these may pose to the NTS operation and our processes.

Winter and Summer Outlook Reports

Our Winter and Summer Outlook reports present our view of security of supply for the

electricity and gas systems for the coming season. These reports are informed by the FES

and they feed into the pan-European security of supply planning undertaken through

ENTSO-E and ENTSO-G.

Electricity Capacity Report

National Grid, as the Electricity Market Reform (EMR) Delivery Body, produces the

“Electricity Capacity Report” that includes recommendations for the capacity that is to be

procured through Capacity Market auctions for one and four year ahead delivery. The FES is

the starting point for that analysis.

Charging and Strategic Projects

The FES scenarios are also used to underpin an increasing number of strategy projects,

such as our Future of Gas (FOG) programme. In addition they inform our future charging

forecasts for Transmission Network Use of System (TNUoS) tariffs.

Se

ctio

n o

ne

4

Why do we create scenarios?

How are they used by our stakeholders?

We strive to deliver value to our stakeholders and make sure FES continues to meet their

needs. In order to do so, we regularly engage with our stakeholders to understand how and

for what purposes they use the FES.

Our stakeholders have told us they use the FES in a variety of ways from a foundation to

build their own analysis and scenarios, to investment decisions, market view, reference

point, future planning and benchmarking through to academic material.

At our workshops held in October, we asked our stakeholders to provide more details on

how they use FES. A view of their feedback is provided below.

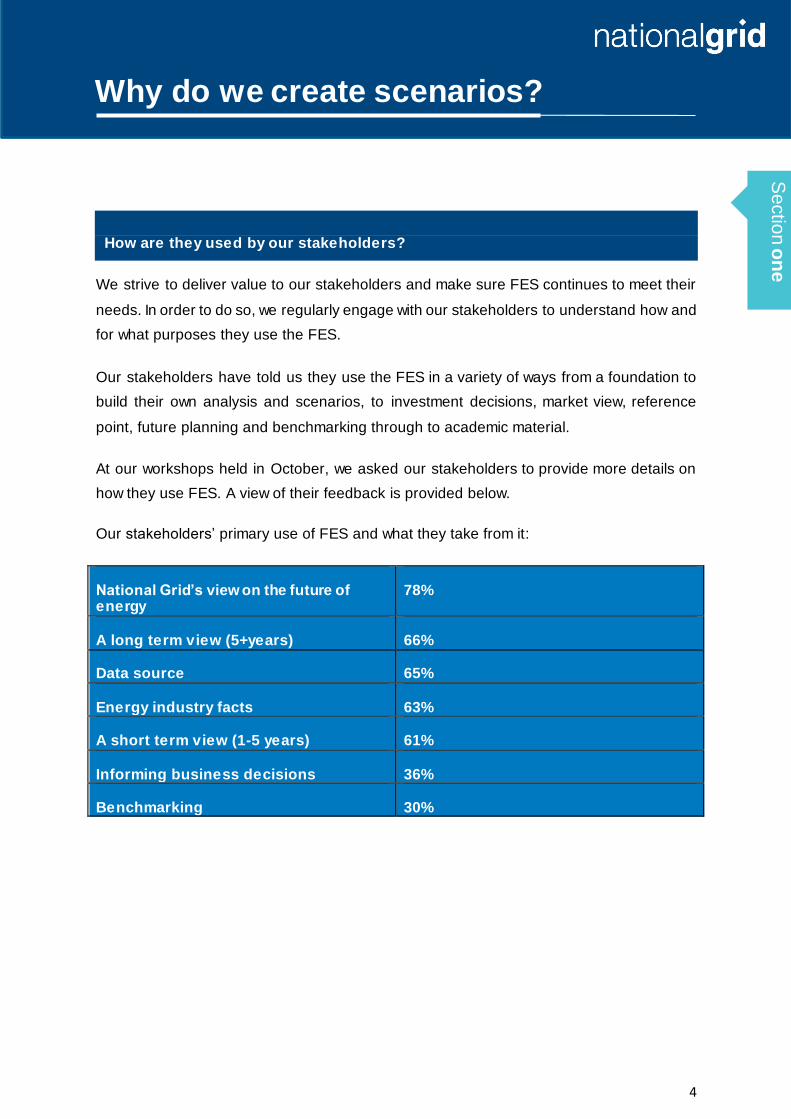

Our stakeholders’ primary use of FES and what they take from it:

National Grid’s view on the future of energy

78%

A long term view (5+years) 66%

Data source 65%

Energy industry facts 63%

A short term view (1-5 years) 61%

Informing business decisions 36%

Benchmarking 30%

Se

ctio

n o

ne

5

Why do we create scenarios?

Examples of how FES is used by our stakeholders:

“To understand future energy markets”

“Check our forecasts against the FES and a

comparison against our own scenarios”

“Updates and business and industry awareness”

“To understand the key elements of future energy

strategy and help determine our future business strategy”

“An informative guide which helps inform our

areas of focus”

“To inform our clients on progress and possible

routes ahead towards the key government targets in

the energy sector”

We have also been approached by companies from across the globe looking to learn from

our work, how we develop our scenarios and share our expertise as they see us as world

leaders in scenario development. This includes those working within the energy sectors in

Central Europe, Canada, America, Australia and Korea. This has also provided us with a

platform to share knowledge and understanding of how other countries seek to manage the

uncertainty of the future of energy, along with the challenges and opportunities they may

face.

Se

ctio

n o

ne

6

Our engagement

The role of stakeholders and FES

Our stakeholders are impacted by our work and GB’s energy future and it is therefore

essential that they have the opportunity to understand and debate the scenarios in detail. In

addition, we engage with experts from across the industry on specific areas in order to

enhance and validate the inputs into our future scenarios.

Our scenarios take into consideration a number of factors and data, including historical

trends, forecasts and views from across our stakeholder community. By involving our

stakeholders within this process, understanding their views and building this into our own

analysis, we are able to produce a set of credible future energy scenarios, allowing us to use

the insight gained to drive the evolution of the FES.

“Engaging with stakeholders allows us to check our modelling against

others in the industry, and confirm that our assumptions are

reasonable. One example of this is shale gas where we have been told

by multiple stakeholders that we are using the best source of data

available.”

Chris Parsons, Gas Modelling Analyst, Future Energy Scenarios

How do we engage with our stakeholders?

We interact with a diverse range of stakeholders from across the energy industry and

beyond and seek to adapt the way we engage accordingly. We consider the most effective

ways to gather this information through both qualitative and quantitative means. For

example, we use surveys to obtain quantitative feedback, and hold open discussion

sessions to receive qualitative feedback.

Se

ctio

n tw

o

7

Our engagement

Each year we run an engagement process where we consult our stakeholders and analyse

their feedback which then feeds into the creation and launch of the next round of scenarios,

together with our own analysis and intelligence (see Figure 2 below). This consists of a

launch conference, followed by a programme of webinars across the summer, four all day

workshops held across GB and a host of bilateral meetings that take place throughout the

year. Further details of these events are provided in the ‘Who do we engage with?’ section

below.

Figure 2: FES development cycle

Se

ctio

n tw

o

8

Our engagement

There are principally five ways we use stakeholder information in our scenarios;

Consensus: We engage with stakeholders to obtain their feedback and seek to achieve

broad consensus on the core FES elements such as the 2x2 scenario matrix, the ‘prosperity’

and ‘green ambition’ axes, the key themes and assumptions.

Subject matter experts/industry bodies: We engage with leading industry experts to gather

intelligence and feedback in more detail on particular topics, including emerging

development projects, forecasts and projections from manufacturers on energy trends and

innovation such as electric vehicles and boiler efficiencies. We also engage stakeholders

within the academic sector.

Project specific: We speak to developers and operators of specific energy projects, gaining

intelligence about their commissioning or closure plans.

Industry data: We draw on a wide range of data to inform our analysis, including official

statistics, economic forecasts as well as specialist industry information such as data on

rapidly developing technologies and pricing.

Consultancy: We engage with specialist consultancies to source market intelligence and add

expertise in specific areas (e.g. district heating, small modular reactors and electricity

interconnector flows) and benchmark our analysis.

Se

ctio

n tw

o

9

Our engagement

Who do we engage with?

Our events and engagement are open to all who are impacted by or who have an interest in

the FES and the future of energy. Through focused enhancements to our stakeholder

engagement activities we consulted 391 organisations this year, increasing our engagement

from 362 organisations last year.

A breakdown of the organisations per sector is detailed below:

Energy Industry 150

Customers 61

Small Businesses (including individuals) 35

Innovators 26

Supply Chain 25

Educational Interest 20

Investors 20

Political 19

Non-Government Organisations 18

Media 7

Communities and their representatives 5

Consumer Groups 3

Regulators 2

We always look at ways to improve who we engage with and how.

This year we have seen an increase in representation from the following sectors:

innovation/manufacturing, political, supply chain and small business/individuals (see

annex for details). Some of the organisations which have low representation numbers

in absolute terms, such as Consumer Groups, have attended more than one of our

engagement events. For 2017 we will look to understand where there are gaps in our

engagement within each sector and how we can improve this going forward.

Se

ctio

n tw

o

10

Our engagement

We have listened to our stakeholders and, following feedback on workshop locations,

we reviewed these to include Cardiff this year in addition to Warwick, Edinburgh and

London. Our workshop in Cardiff was a positive addition to our engagement

programme which was welcomed by our stakeholders. We will use these locations

again for the FES 2017 workshops in October.

This year we held a specific workshop looking at the 2050 climate change targets

with attendees from across the relevant sectors of the industry and academia. We

explored stakeholders thoughts further on related topics and will feed this through to

our environmental targets analysis and modelling for FES 2017.

We increased our webinars after the FES launch to allow those unable to attend the

launch event an opportunity to learn about the latest FES and ask any questions they

may have.

We enhanced our “FES in 5” document as a result of the feedback we received from

our stakeholders on the previous version. This has been very well received and we

will continue with a summary for FES 2017.

The number of organisations who attended our events and which sectors they

represented is set out in the annex.

Se

ctio

n tw

o

11

Our engagement

How will we further enhance our engagement for 2017?

Stakeholders told us they were happy with the existing methods of engagement but

suggested some enhancements to this. Based on this feedback, below are some of the key

changes we will be looking to make for 2017.

More agile engagement – engaging with our stakeholders when key changes or

updates are made and involving them within this process, for example, by

contributing and presenting our perspectives at relevant industry events and testing

our assumptions and analysis.

More of our views and opinion – stakeholders advised they wanted to hear more of

our opinion on hot topics and key changes. Therefore, at our October Workshops we

trialled a new method of doing so – our proposed thought pieces which would be

timely articles providing our views and thoughts. You’ll hear more about these

throughout this year and referenced in this document.

More regular communications – stakeholders asked for us to communicate outside

of our existing engagement cycle and specifically for a mail out of key updates or

changes including our views and opinion on key industry topics. We will therefore be

launching a regular communication email in 2017 which will include the latest

updates on our work, our thought pieces, upcoming events and spotlights on our

team’s work.

Flexible engagement – stakeholders told us for smaller companies it can be difficult

to resource attendance at our events. In 2017 we will be looking to come to existing

forums already attended by those smaller companies and explore the greater use of

webinars and video conference as an alternative method of engagement.

Se

ctio

n tw

o

12

Our proposed scenarios for 2017

In this section we describe our proposed high level scenarios for FES 2017 which will

provide the basis for the detailed modelling and analysis that feeds into the Future Energy

Scenarios we publish in July 2017.

The scenario framework

We use the scenario framework to set out a structured approach which provides a single

reference document to group all the inputs and assumptions that we use to build our

scenarios (see Figure 3 below). There has been strong support from our stakeholders over

the past year to keep this approach.

Figure 3: FES Framework

Central to the scenario framework is the scenario world. This effectively captures the core

elements which are fixed across the scenarios: the matrix, the axes and fixed rules (e.g.

security of supply). The next layer introduces the scenario themes: Political, Economic,

Social and Technological (PEST) which are used to structure the scenario narrative and

model assumptions. Sitting beneath each theme are all of the assumptions that feed into the

scenarios. Each assumption broadly aligns to sectorial models (e.g. onshore

Se

ctio

n th

ree

13

Our proposed scenarios for 2017

wind) and will be set at high, medium or low for each of the four scenarios. The final layer of

the framework is the specific model levers which are the detailed granular inputs into the

analysis – these cover all inputs to all the models used to produce the FES.

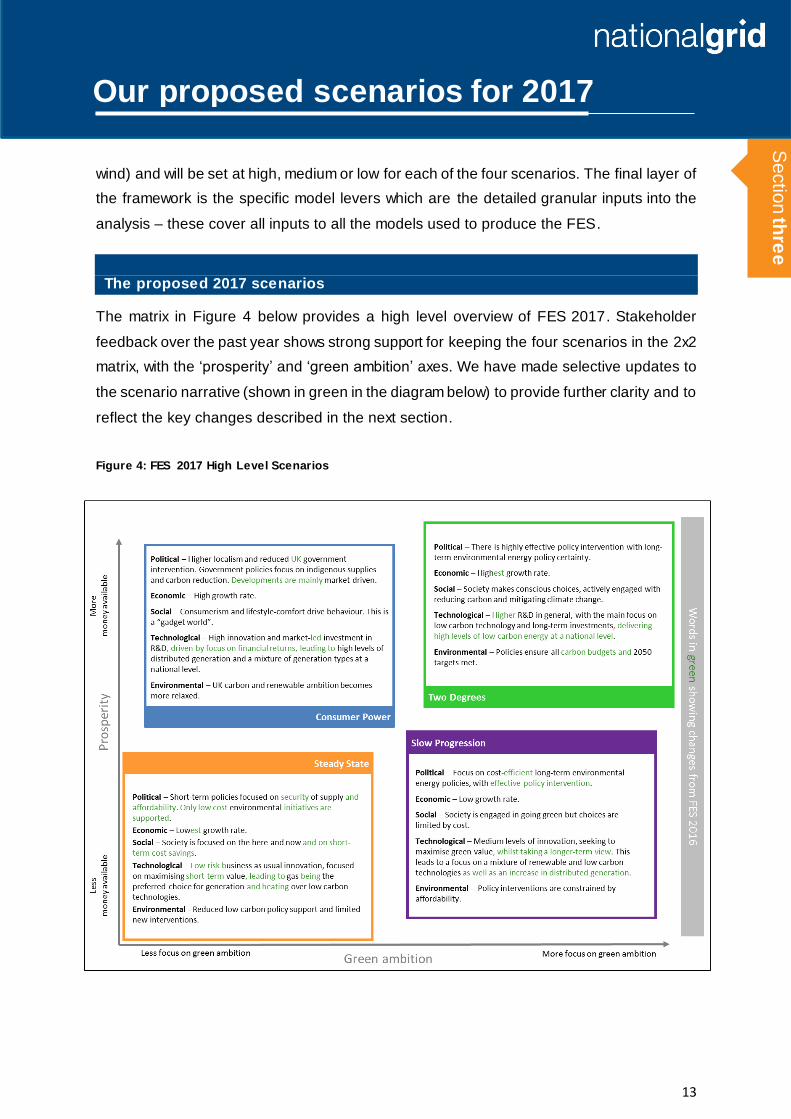

The proposed 2017 scenarios

The matrix in Figure 4 below provides a high level overview of FES 2017. Stakeholder

feedback over the past year shows strong support for keeping the four scenarios in the 2x2

matrix, with the ‘prosperity’ and ‘green ambition’ axes. We have made selective updates to

the scenario narrative (shown in green in the diagram below) to provide further clarity and to

reflect the key changes described in the next section.

Figure 4: FES 2017 High Level Scenarios

Se

ctio

n th

ree

14

Our proposed scenarios for 2017

Key changes for FES 2017

As we’ve mentioned, we continually look to review our scenarios and ensure they are

credible and fit for purpose. Our research, intelligence and stakeholder feedback over the

past year has led to the following key changes to date. Our work is ongoing and we will

update you on further changes that may arise.

Key changes so far for FES 2017:

Reflecting trends in distributed generation: As in previous years, all of our scenarios

will consider energy demand and supply with a whole system view. To reflect recent

trends in the electricity market, two of our four core scenarios for 2017 will have high

levels of distributed generation growth (compared to one last year), with the other two

scenarios featuring more moderate growth rates of distributed generation to reflect

uncertainty over embedded benefits. This has also been supported by stakeholder

views.

We will continue to monitor the potential for changes to the charging and regulatory

frameworks and subsidy arrangements to understand how this may affect the future

growth of distributed generation. We will feed this into our analysis as we develop FES

2017.

Impact of Brexit: Our analysis and stakeholder feedback has shown uncertainty around

the impact of Brexit. We will capture this by using a wider range of economic growth

forecasts for FES 2017, i.e. two high growth and two low growth forecasts (instead of

only one high and one low forecast in 2016). We will also include a section in FES 2017

to set out in more detail how we have considered Brexit in our scenario development.

Repositioning the scenarios on the axes: We have repositioned the scenarios on the

axes in the scenario matrix (see Figure 4 above). This reflects how we have distributed

the wider range of economic growth forecasts across the four scenarios (i.e. Two

Degrees being more prosperous than Consumer Power and Slow Progression being

more prosperous than Steady State). The repositioning also reflects differences between

the scenarios in the level of green ambition.

Se

ctio

n th

ree

15

Our proposed scenarios for 2017

Retiring the names ‘Gone Green’ and ‘No Progression’: These names have been

retired to more accurately reflect the scenarios.

The name Gone Green has remained the same since the scenario was first

introduced in 2011, but the scenario itself has evolved significantly over the years.

There has been a shift from a focus on renewable technologies to low carbon

technologies, and in FES 2016 the scenario no longer met the 2020 renewables

target (whilst still meeting the 2050 carbon reduction target). The name Gone Green

is replaced by ‘Two Degrees’ and the scenario will continue to be our core scenario

that meets the 2050 carbon reduction target (none of the other core scenarios will

meet this target without further intervention). The name Two Degrees signifies that

the scenario is consistent with the UK carbon budgets and the 2050 target which is

the UK’s contribution to the Paris Agreement of seeking to hold the increase in the

global average temperature to well below 2 °C above pre -industrial levels.

Our stakeholders have told us they don’t think the name No Progression accurately

reflects the scenario. The name could suggest ‘no change’, despite there being some

business as usual progress and innovation. The new name, ‘Steady State’, better

reflects the scenario which continues to represent a world where current levels of

progress and innovation are reflected out to 2050.

Development of wider sensitivities: The four core scenarios will continue to

provide our view, informed by analysis and stakeholder feedback, of plausible and

credible energy futures. In addition to this, we propose to develop a broader range of

sensitivities around the four main scenarios that represent other possible futures.

These sensitivities could consider, for example, the impact of potentially ground

breaking technological developments or potential major developments in UK or

international policy. The sensitivities will not provide a full suite of analysis at the level

of the core scenarios, but they will be used to ‘flex’ the scenario range. We are in the

process of considering what sensitivities we’ll apply and we’ll share further details

with our stakeholders in due course.

Se

ctio

n th

ree

16

Stakeholder feedback and FES 2017

To build our scenarios we collect a significant amount of data. The information we receive

from our stakeholders is one of the elements in helping the development of our FES. We

explore each comment and apply our own judgement and expertise to consider it against the

themes we are hearing from across our stakeholder engagement. This is supported with our

own analysis, facts, projections and historical data.

In carrying out our modelling, we look at the different sectors that impact supply and demand

for both electricity and gas. For example, heat, power and transport, as well as the global

commodity market, technology, build rates, generator economics and the supply chain.

We have a number of models for different sectors, which we use to develop trends for each

of the elements. For example, we model how electric vehicle growth and industrial and

commercial business activities impact electricity demand, along with other drivers of

demand. We use the outputs from these models to build a holistic energy future for each

scenario.

In this section we explore in more detail the feedback received from stakeholders and

demonstrate what it means for FES 2017. We have also included examples of where we

may not be able to take a view forward and the rationale behind our decisions.

“An overwhelming majority of you said you believe the way we use

energy in our homes will undergo a revolution over the coming

decades. You mentioned the introduction of smart technology, electric

vehicles and potentially home storage had a big part to play in this. We

will review the impact of this on our residential demand assumptions

for FES 2017.”

Lilia Jakobsson, Electricity Modelling Analyst, Future Energy Scenarios

Se

ctio

n fo

ur

17

Stakeholder feedback and FES 2017

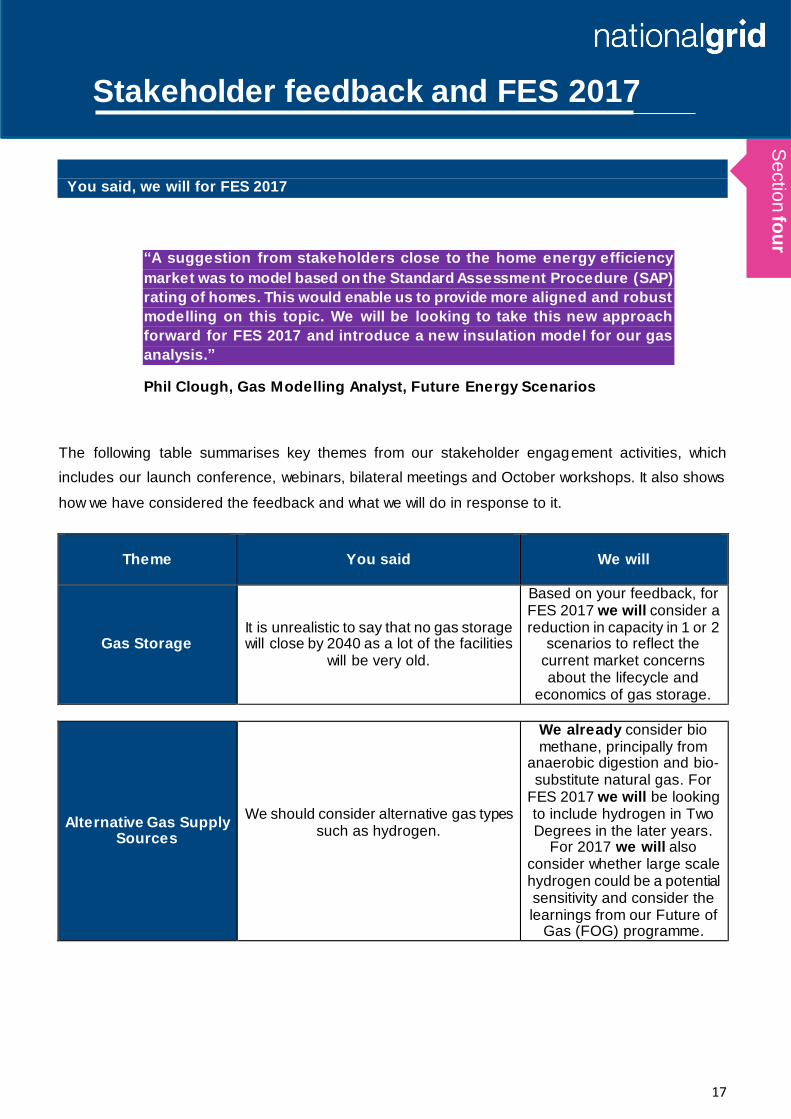

You said, we will for FES 2017

“A suggestion from stakeholders close to the home energy efficiency

market was to model based on the Standard Assessment Procedure (SAP)

rating of homes. This would enable us to provide more aligned and robust

modelling on this topic. We will be looking to take this new approach

forward for FES 2017 and introduce a new insulation model for our gas

analysis.”

Phil Clough, Gas Modelling Analyst, Future Energy Scenarios

The following table summarises key themes from our stakeholder engagement activities, which

includes our launch conference, webinars, bilateral meetings and October workshops. It also shows

how we have considered the feedback and what we will do in response to it.

Theme

You said

We will

Gas Storage It is unrealistic to say that no gas storage will close by 2040 as a lot of the facilities

will be very old.

Based on your feedback, for FES 2017 we will consider a reduction in capacity in 1 or 2

scenarios to reflect the current market concerns about the lifecycle and

economics of gas storage.

Alternative Gas Supply Sources

We should consider alternative gas types such as hydrogen.

We already consider bio methane, principally from

anaerobic digestion and bio-substitute natural gas. For

FES 2017 we will be looking to include hydrogen in Two Degrees in the later years.

For 2017 we will also consider whether large scale hydrogen could be a potential sensitivity and consider the learnings from our Future of

Gas (FOG) programme.

Se

ctio

n fo

ur

18

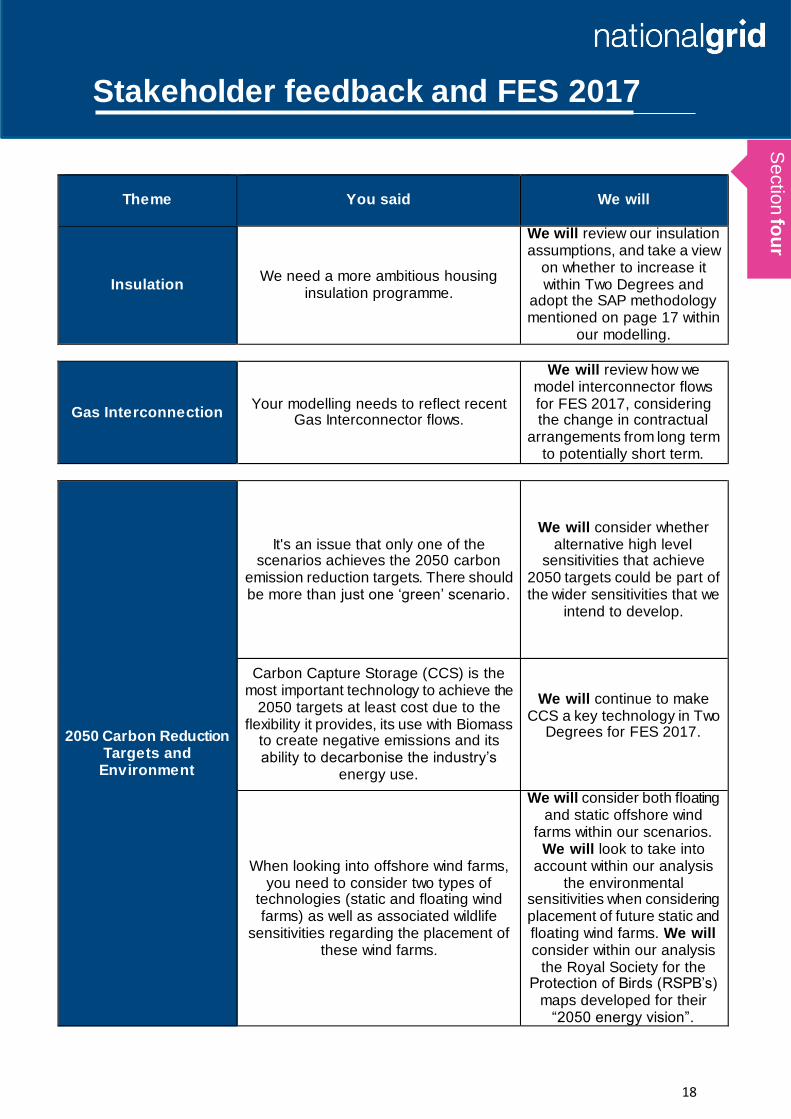

Stakeholder feedback and FES 2017

Theme

You said

We will

Insulation We need a more ambitious housing

insulation programme.

We will review our insulation assumptions, and take a view

on whether to increase it within Two Degrees and

adopt the SAP methodology mentioned on page 17 within

our modelling.

Gas Interconnection Your modelling needs to reflect recent

Gas Interconnector flows.

We will review how we model interconnector flows for FES 2017, considering the change in contractual

arrangements from long term to potentially short term.

2050 Carbon Reduction Targets and

Environment

It's an issue that only one of the scenarios achieves the 2050 carbon

emission reduction targets. There should be more than just one ‘green’ scenario.

We will consider whether alternative high level

sensitivities that achieve 2050 targets could be part of the wider sensitivities that we

intend to develop.

Carbon Capture Storage (CCS) is the most important technology to achieve the

2050 targets at least cost due to the flexibility it provides, its use with Biomass

to create negative emissions and its ability to decarbonise the industry’s

energy use.

We will continue to make CCS a key technology in Two

Degrees for FES 2017.

When looking into offshore wind farms, you need to consider two types of

technologies (static and floating wind farms) as well as associated wildlife

sensitivities regarding the placement of these wind farms.

We will consider both floating and static offshore wind

farms within our scenarios. We will look to take into

account within our analysis the environmental

sensitivities when considering placement of future static and floating wind farms. We will consider within our analysis

the Royal Society for the Protection of Birds (RSPB’s)

maps developed for their “2050 energy vision”.

Se

ctio

n fo

ur

19

Stakeholder feedback and FES 2017

Theme

You said

We will

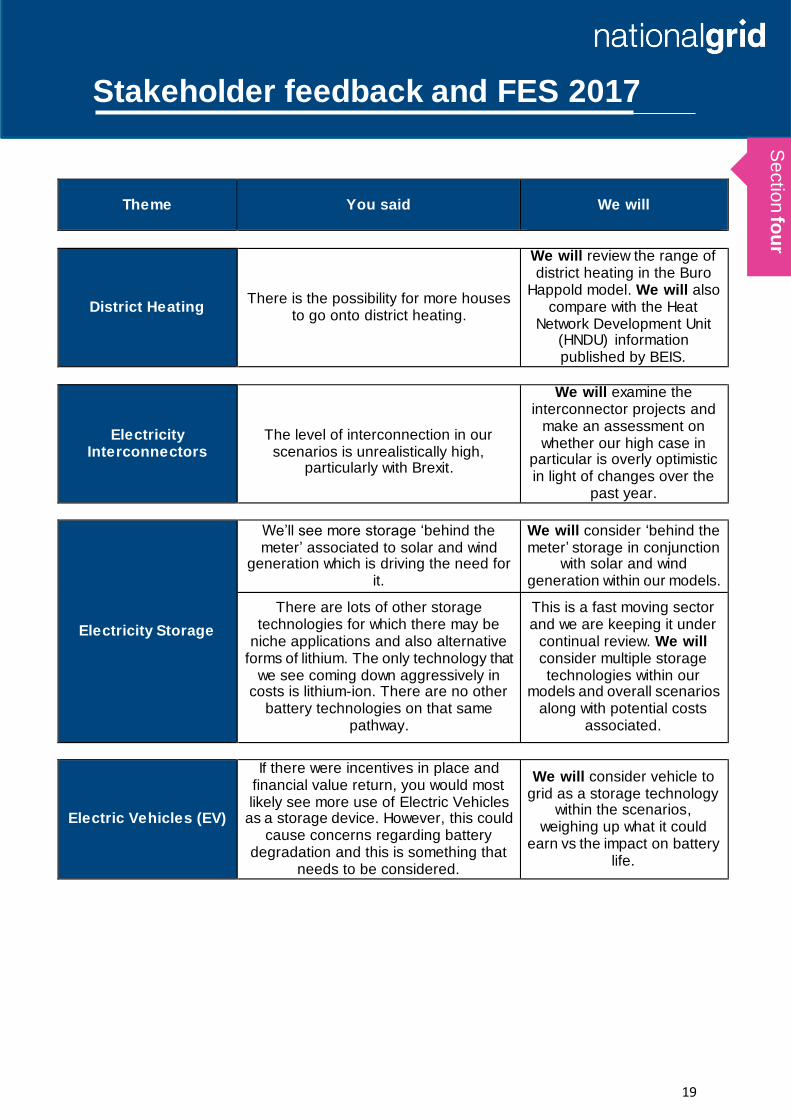

District Heating There is the possibility for more houses

to go onto district heating.

We will review the range of district heating in the Buro

Happold model. We will also compare with the Heat

Network Development Unit (HNDU) information published by BEIS.

Electricity Interconnectors

The level of interconnection in our

scenarios is unrealistically high, particularly with Brexit.

We will examine the interconnector projects and

make an assessment on whether our high case in

particular is overly optimistic in light of changes over the

past year.

Electricity Storage

We’ll see more storage ‘behind the meter’ associated to solar and wind

generation which is driving the need for it.

We will consider ‘behind the meter’ storage in conjunction

with solar and wind generation within our models.

There are lots of other storage technologies for which there may be

niche applications and also alternative forms of lithium. The only technology that

we see coming down aggressively in costs is lithium-ion. There are no other

battery technologies on that same pathway.

This is a fast moving sector and we are keeping it under

continual review. We will consider multiple storage technologies within our

models and overall scenarios along with potential costs

associated.

Electric Vehicles (EV)

If there were incentives in place and financial value return, you would most likely see more use of Electric Vehicles

as a storage device. However, this could cause concerns regarding battery

degradation and this is something that needs to be considered.

We will consider vehicle to grid as a storage technology

within the scenarios, weighing up what it could

earn vs the impact on battery life.

Se

ctio

n fo

ur

20

Stakeholder feedback and FES 2017

Theme

You said

We will

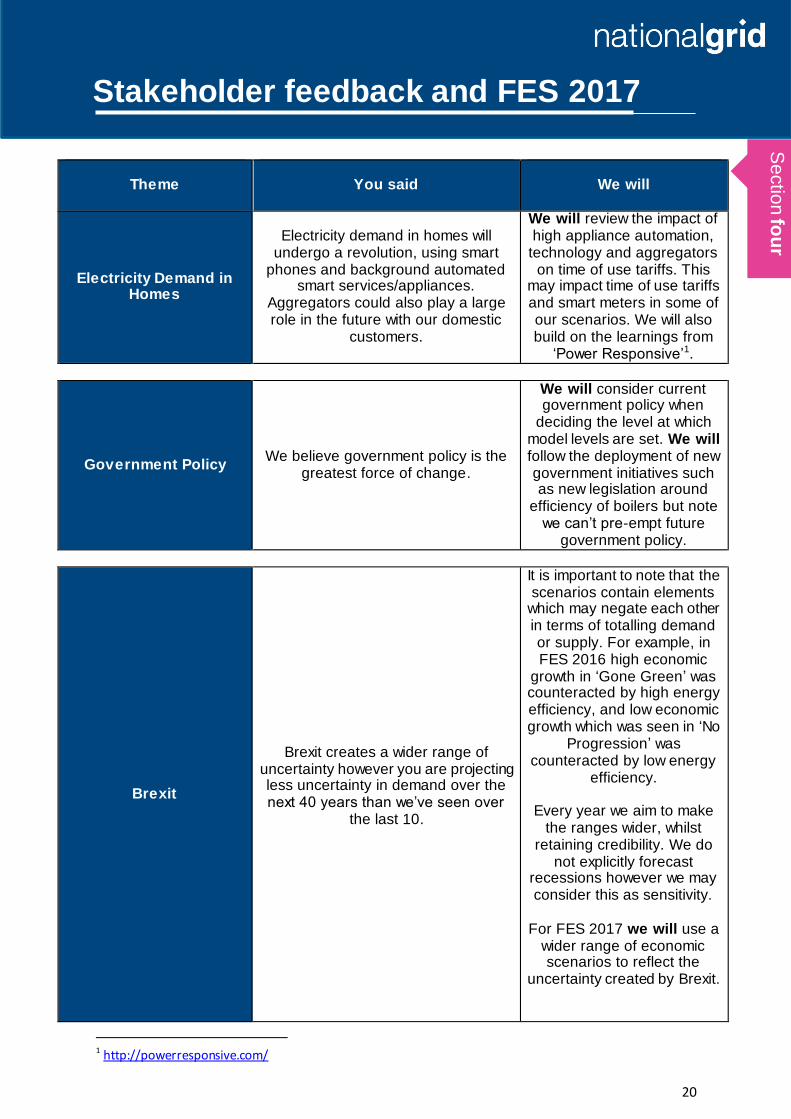

Electricity Demand in Homes

Electricity demand in homes will undergo a revolution, using smart

phones and background automated smart services/appliances.

Aggregators could also play a large role in the future with our domestic

customers.

We will review the impact of high appliance automation,

technology and aggregators on time of use tariffs. This

may impact time of use tariffs and smart meters in some of our scenarios. We will also build on the learnings from

‘Power Responsive’1.

Government Policy We believe government policy is the

greatest force of change.

We will consider current government policy when

deciding the level at which model levels are set. We will follow the deployment of new government initiatives such as new legislation around

efficiency of boilers but note we can’t pre-empt future

government policy.

Brexit

Brexit creates a wider range of uncertainty however you are projecting less uncertainty in demand over the next 40 years than we’ve seen over

the last 10.

It is important to note that the scenarios contain elements

which may negate each other in terms of totalling demand or supply. For example, in FES 2016 high economic

growth in ‘Gone Green’ was counteracted by high energy efficiency, and low economic growth which was seen in ‘No

Progression’ was counteracted by low energy

efficiency.

Every year we aim to make the ranges wider, whilst

retaining credibility. We do not explicitly forecast

recessions however we may consider this as sensitivity.

For FES 2017 we will use a

wider range of economic scenarios to reflect the

uncertainty created by Brexit.

1 http://powerresponsive.com/

Se

ctio

n fo

ur

21

Stakeholder feedback and FES 2017

You said, we won’t and why for FES 2017

It’s great to understand our stakeholders’ views, learn from each other and help make our scenarios

as rich and robust as possible. Sometimes the decision is made not to take this feedback forward into

our modelling, this may be because other information contradicts this or we have come to a different

view based on our own analysis and informed judgement. We will endeavour to explore this with you.

Examples of this are detailed below:

Theme

You said

We won’t and why

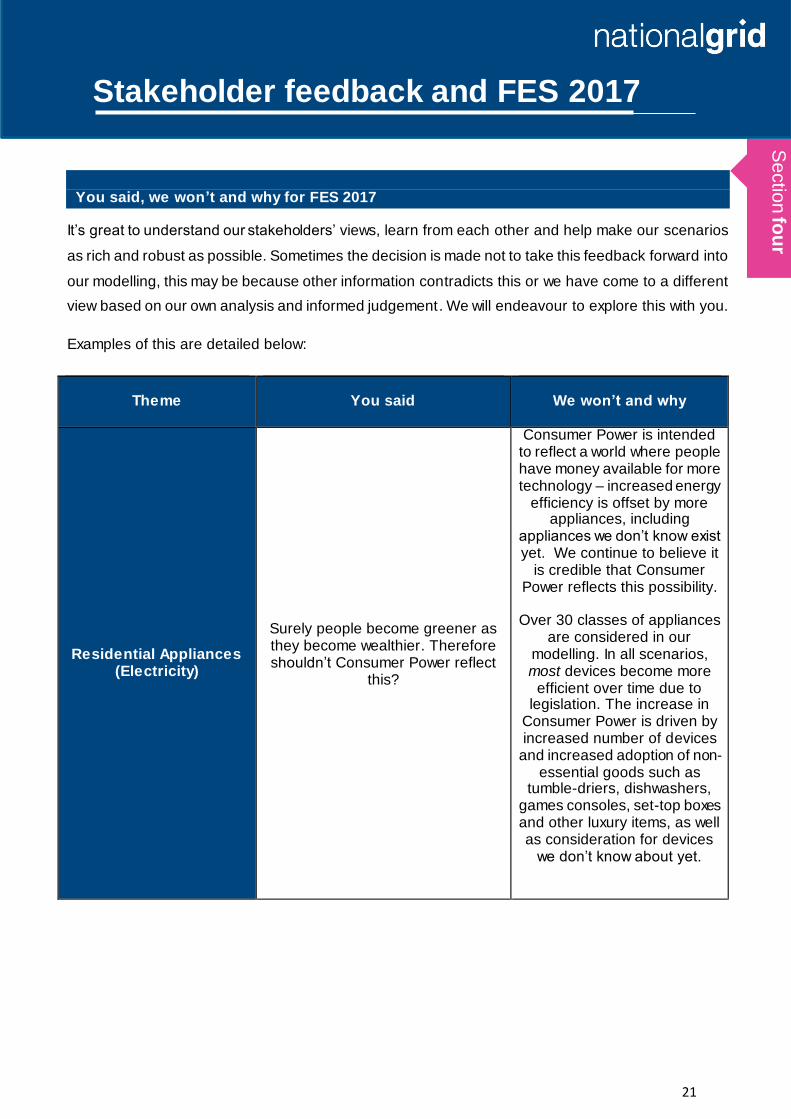

Residential Appliances (Electricity)

Surely people become greener as they become wealthier. Therefore shouldn’t Consumer Power reflect

this?

Consumer Power is intended to reflect a world where people have money available for more technology – increased energy

efficiency is offset by more appliances, including

appliances we don’t know exist yet. We continue to believe it

is credible that Consumer Power reflects this possibility.

Over 30 classes of appliances

are considered in our modelling. In all scenarios, most devices become more

efficient over time due to legislation. The increase in

Consumer Power is driven by increased number of devices

and increased adoption of non-essential goods such as

tumble-driers, dishwashers, games consoles, set-top boxes and other luxury items, as well as consideration for devices

we don’t know about yet.

Se

ctio

n fo

ur

22

Stakeholder feedback and FES 2017

Theme

You said

We won’t and why

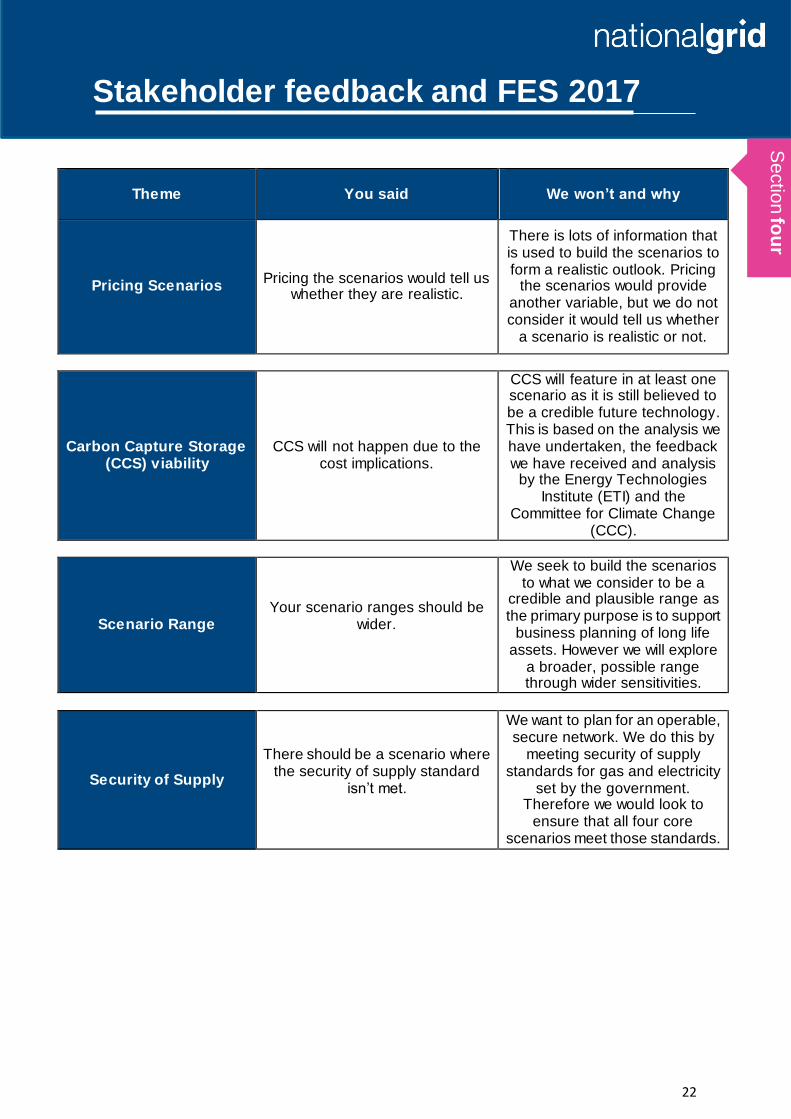

Pricing Scenarios Pricing the scenarios would tell us

whether they are realistic.

There is lots of information that is used to build the scenarios to form a realistic outlook. Pricing

the scenarios would provide another variable, but we do not consider it would tell us whether

a scenario is realistic or not.

Carbon Capture Storage (CCS) viability

CCS will not happen due to the cost implications.

CCS will feature in at least one scenario as it is still believed to be a credible future technology. This is based on the analysis we have undertaken, the feedback we have received and analysis

by the Energy Technologies Institute (ETI) and the

Committee for Climate Change (CCC).

Scenario Range Your scenario ranges should be

wider.

We seek to build the scenarios to what we consider to be a

credible and plausible range as the primary purpose is to support

business planning of long life assets. However we will explore

a broader, possible range through wider sensitivities.

Security of Supply

There should be a scenario where the security of supply standard

isn’t met.

We want to plan for an operable, secure network. We do this by

meeting security of supply standards for gas and electricity

set by the government. Therefore we would look to

ensure that all four core scenarios meet those standards.

Se

ctio

n fo

ur

23

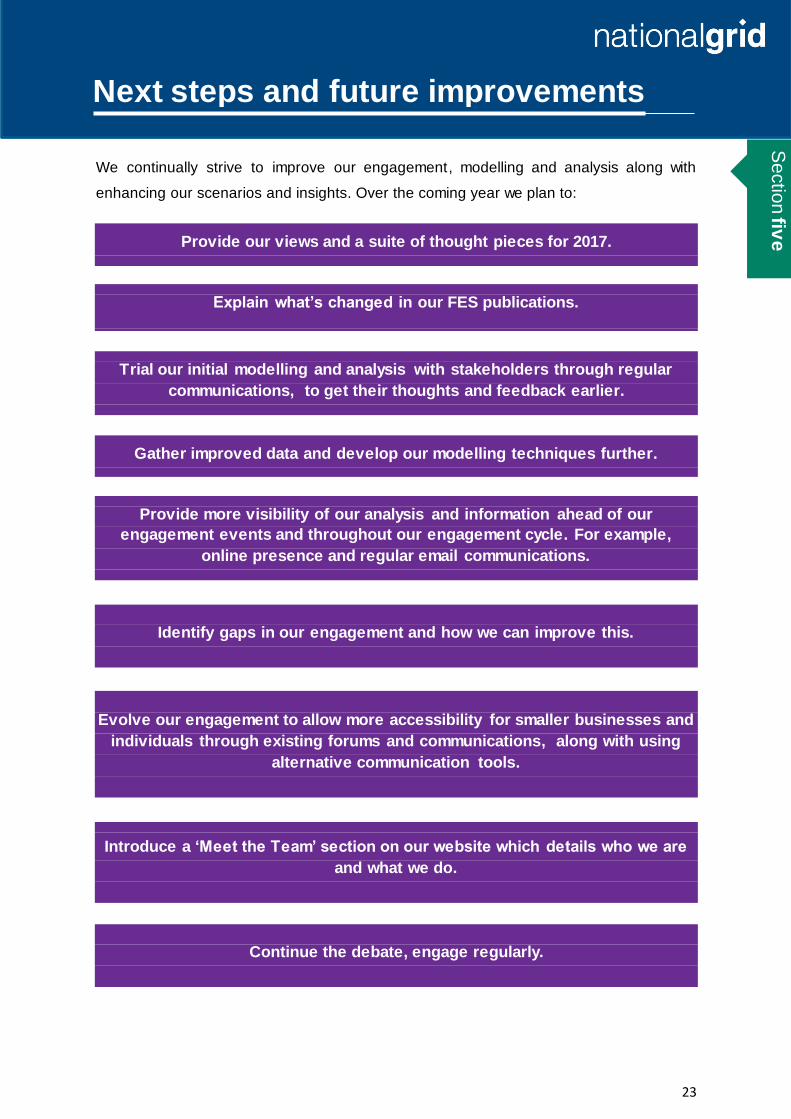

Next steps and future improvements

We continually strive to improve our engagement, modelling and analysis along with

enhancing our scenarios and insights. Over the coming year we plan to:

Provide our views and a suite of thought pieces for 2017.

Explain what’s changed in our FES publications.

Trial our initial modelling and analysis with stakeholders through regular

communications, to get their thoughts and feedback earlier.

Gather improved data and develop our modelling techniques further.

Provide more visibility of our analysis and information ahead of our

engagement events and throughout our engagement cycle. For example,

online presence and regular email communications.

Identify gaps in our engagement and how we can improve this.

Evolve our engagement to allow more accessibility for smaller businesses and

individuals through existing forums and communications, along with using

alternative communication tools.

Introduce a ‘Meet the Team’ section on our website which details who we are

and what we do.

Continue the debate, engage regularly.

Se

ctio

n fiv

e

24

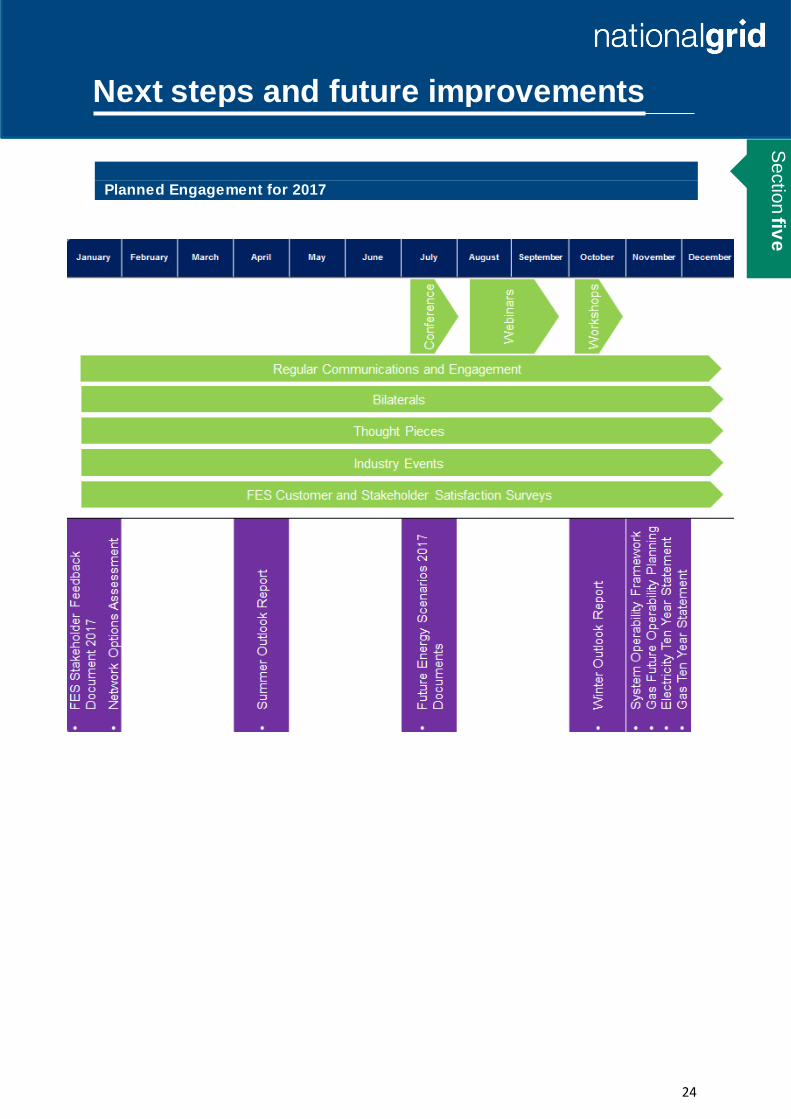

Next steps and future improvements

Planned Engagement for 2017

Se

ctio

n fiv

e

25

Continuing the conversation

Sign up to our mailing list:

Keep up to date with the latest news and developments, and hear about our

forthcoming events. To subscribe, email us at

Visit our website:

Access our current and past FES documents, Stakeholder

Feedback Documents, data and multimedia at

http://fes.nationalgrid.com

Email us:

With your views on this document or the FES documents at

[email protected] and one of our experts will get in touch

Write to us:

SO Strategy, Energy Insights, National Grid House, Warwick Technology Park, Gallows Hill, Warwick, CV34 6DA

Twitter and Linked in:

Get involved in the debate on the future of energy on Twitter, tweeting us

@nationalgriduk and join our LinkedIn group ‘Future of Energy by National

Grid’

Se

ctio

n s

ix

26

Meet the Energy Insights Team

What

Annex

27

Meet the Energy Insights Team

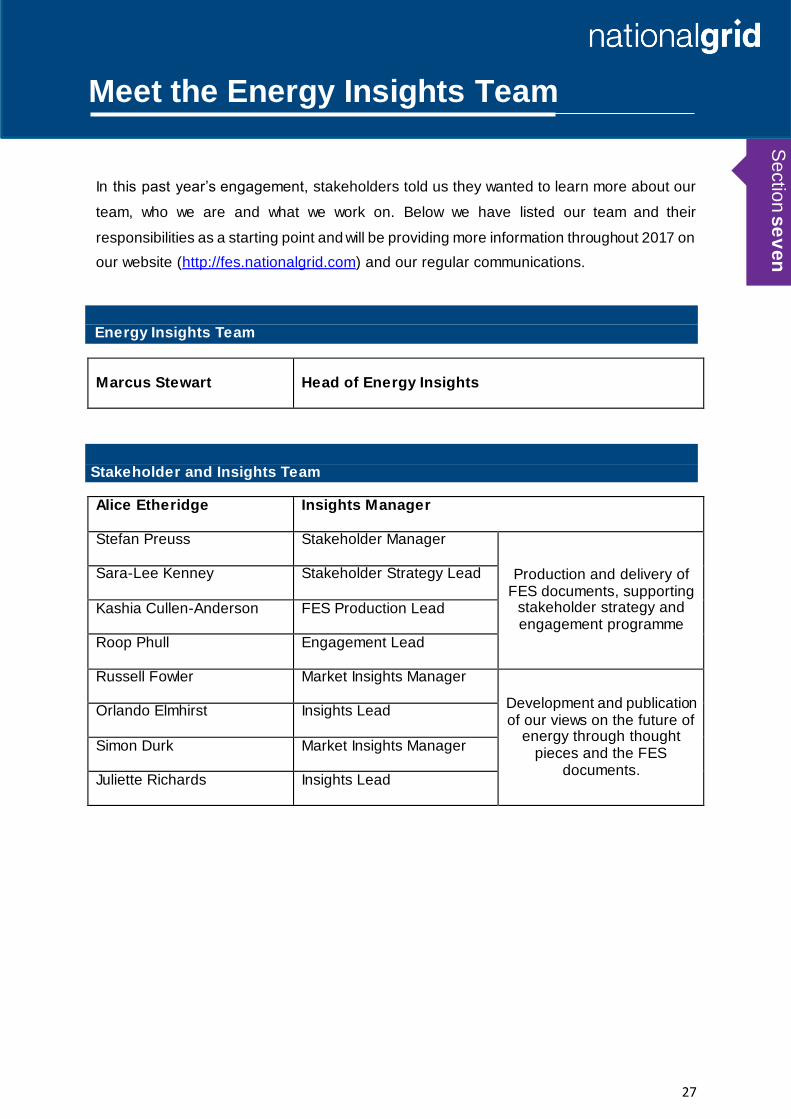

In this past year’s engagement, stakeholders told us they wanted to learn more about our

team, who we are and what we work on. Below we have listed our team and their

responsibilities as a starting point and will be providing more information throughout 2017 on

our website (http://fes.nationalgrid.com) and our regular communications.

Energy Insights Team

Marcus Stewart

Head of Energy Insights

Stakeholder and Insights Team

Alice Etheridge

Insights Manager

Stefan Preuss

Stakeholder Manager

Production and delivery of FES documents, supporting

stakeholder strategy and engagement programme

Sara-Lee Kenney

Stakeholder Strategy Lead

Kashia Cullen-Anderson

FES Production Lead

Roop Phull

Engagement Lead

Russell Fowler Market Insights Manager

Development and publication of our views on the future of

energy through thought pieces and the FES

documents.

Orlando Elmhirst Insights Lead

Simon Durk Market Insights Manager

Juliette Richards Insights Lead

Sectio

n s

ev

en

28

Meet the Energy Insights Team

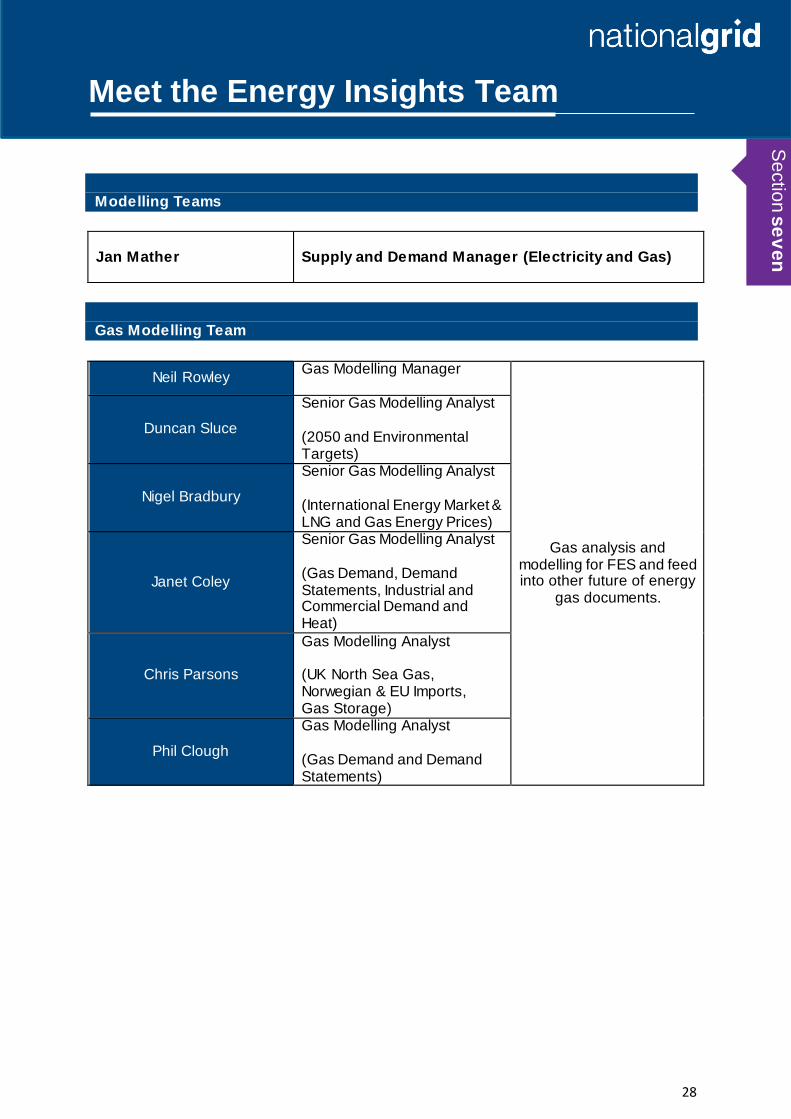

Modelling Teams

Jan Mather

Supply and Demand Manager (Electricity and Gas)

Gas Modelling Team

Neil Rowley Gas Modelling Manager

Gas analysis and modelling for FES and feed into other future of energy

gas documents.

Duncan Sluce

Senior Gas Modelling Analyst (2050 and Environmental Targets)

Nigel Bradbury

Senior Gas Modelling Analyst (International Energy Market & LNG and Gas Energy Prices)

Janet Coley

Senior Gas Modelling Analyst (Gas Demand, Demand Statements, Industrial and Commercial Demand and Heat)

Chris Parsons

Gas Modelling Analyst (UK North Sea Gas, Norwegian & EU Imports, Gas Storage)

Phil Clough

Gas Modelling Analyst (Gas Demand and Demand Statements)

Sectio

n s

ev

en

29

Meet the Energy Insights Team

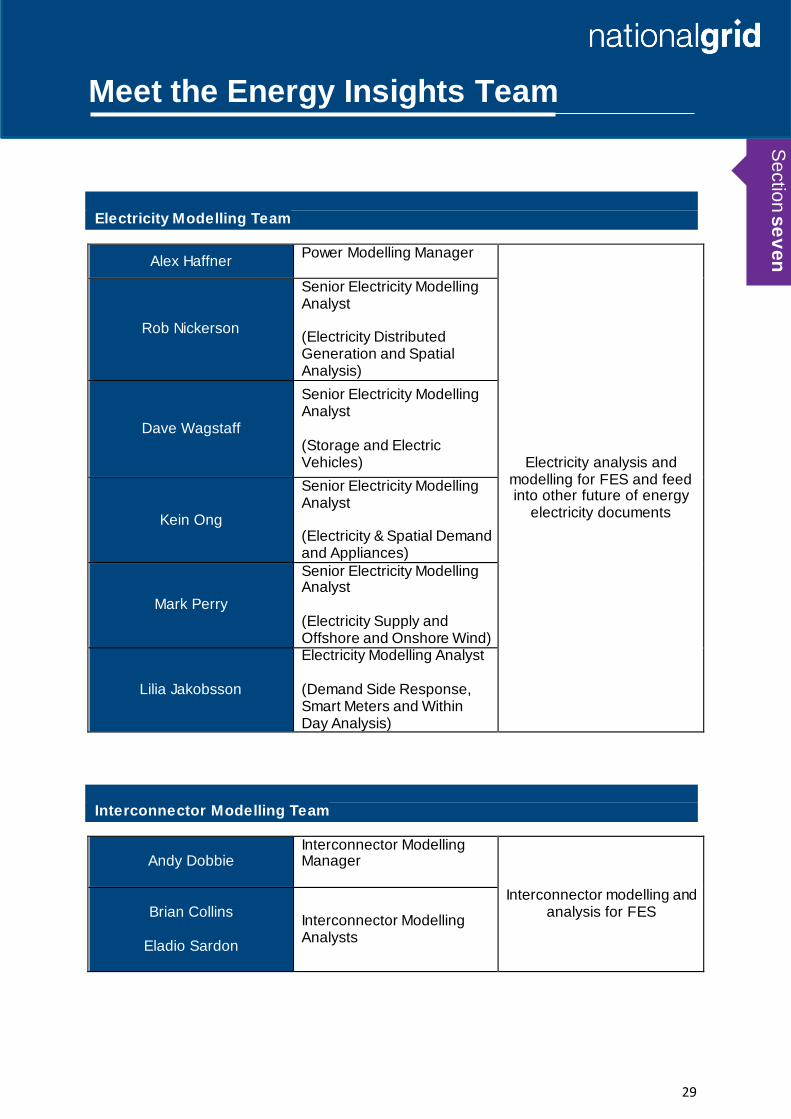

Electricity Modelling Team

Alex Haffner Power Modelling Manager

Electricity analysis and modelling for FES and feed into other future of energy

electricity documents

Rob Nickerson

Senior Electricity Modelling Analyst (Electricity Distributed Generation and Spatial Analysis)

Dave Wagstaff

Senior Electricity Modelling Analyst (Storage and Electric Vehicles)

Kein Ong

Senior Electricity Modelling Analyst (Electricity & Spatial Demand and Appliances)

Mark Perry

Senior Electricity Modelling Analyst (Electricity Supply and Offshore and Onshore Wind)

Lilia Jakobsson

Electricity Modelling Analyst (Demand Side Response, Smart Meters and Within Day Analysis)

Interconnector Modelling Team

Andy Dobbie Interconnector Modelling Manager

Interconnector modelling and analysis for FES Brian Collins

Eladio Sardon

Interconnector Modelling Analysts

Sectio

n s

ev

en

30

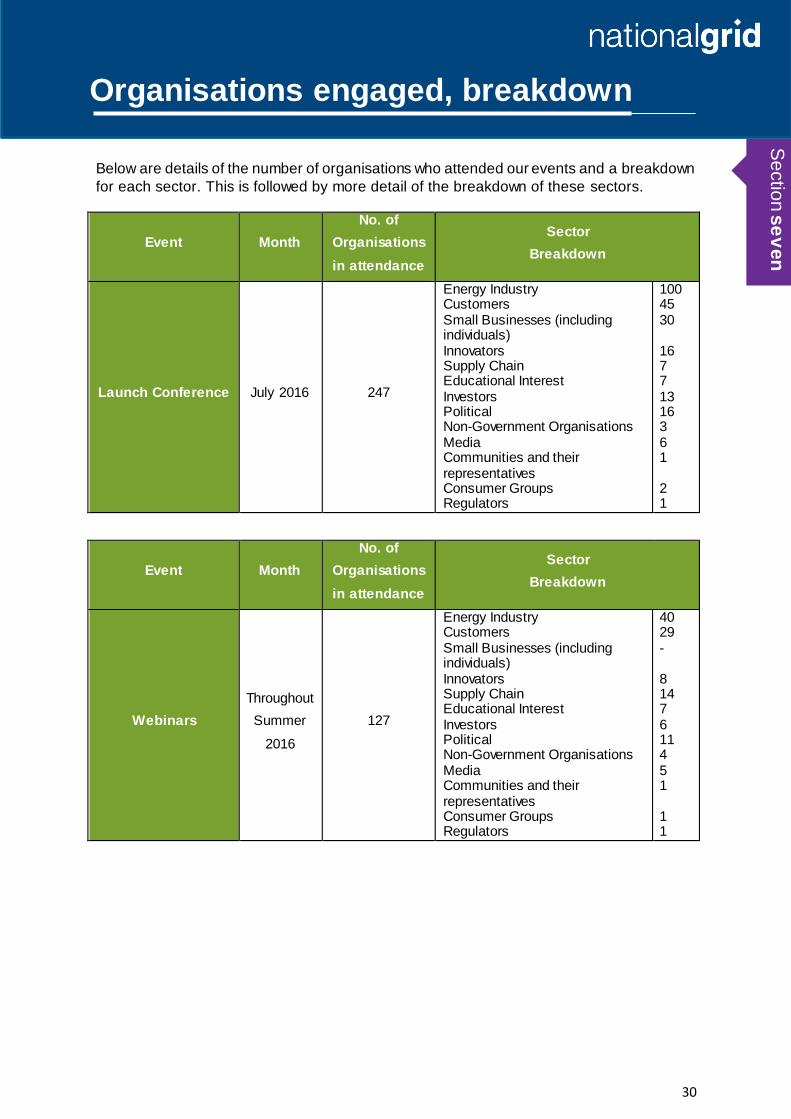

Organisations engaged, breakdown

Below are details of the number of organisations who attended our events and a breakdown

for each sector. This is followed by more detail of the breakdown of these sectors.

Event Month

No. of

Organisations

in attendance

Sector

Breakdown

Launch Conference July 2016 247

Energy Industry Customers Small Businesses (including individuals) Innovators Supply Chain Educational Interest Investors Political Non-Government Organisations Media Communities and their representatives Consumer Groups Regulators

100 45 30 16 7 7 13 16 3 6 1 2 1

Event Month

No. of

Organisations

in attendance

Sector

Breakdown

Webinars

Throughout

Summer

2016

127

Energy Industry Customers Small Businesses (including individuals) Innovators Supply Chain Educational Interest Investors Political Non-Government Organisations Media Communities and their representatives Consumer Groups Regulators

40 29 - 8 14 7 6 11 4 5 1 1 1

Sectio

n s

ev

en

31

Organisations engaged, breakdown

Event Month

No. of

Organisations

in attendance

Sector

Breakdown

Bilaterals Throughout

2016 36

Energy Industry Customers Small Businesses (including individuals) Innovators Supply Chain Educational Interest Investors Political Non-Government Organisations Media Communities and their representatives Consumer Groups Regulators

12 11 - 1 - 3 - 7 - - - - 2

Event Month

No. of

Organisations

in attendance

Sector

Breakdown

Workshops October

2016 103

Energy Industry

Customers

Small Businesses (including

individuals)

Innovators

Supply Chain

Educational Interest

Investors

Political

Non-Government Organisations

Media

Communities and their

representatives

Consumer Groups

Regulators

41

21

6

6

7

7

1

6

2

2

1

2

1

Se

ctio

n s

ev

en

32

Organisations engaged, breakdown

Event Month

No. of

Organisations

in attendance

Sector

Breakdown

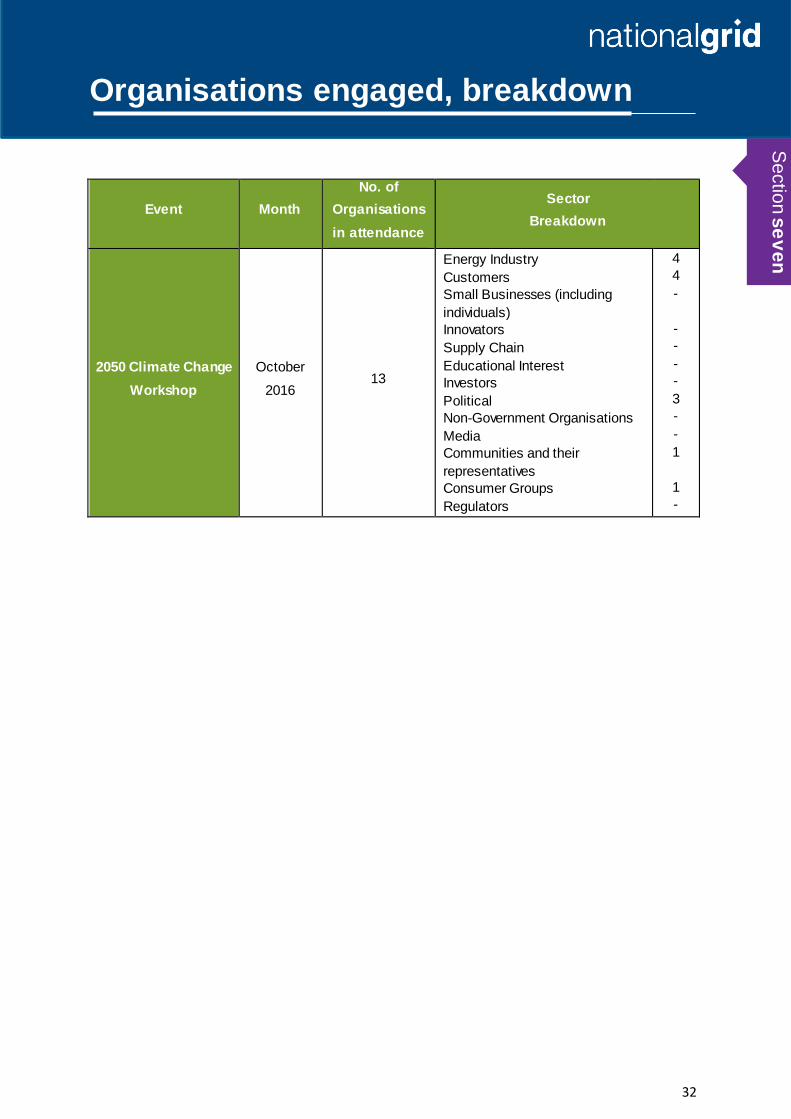

2050 Climate Change

Workshop

October

2016 13

Energy Industry

Customers

Small Businesses (including

individuals)

Innovators

Supply Chain

Educational Interest

Investors

Political

Non-Government Organisations

Media

Communities and their

representatives

Consumer Groups

Regulators

4

4

-

-

-

-

-

3

-

-

1

1

-

Sectio

n s

ev

en

33

Organisations engaged, breakdown

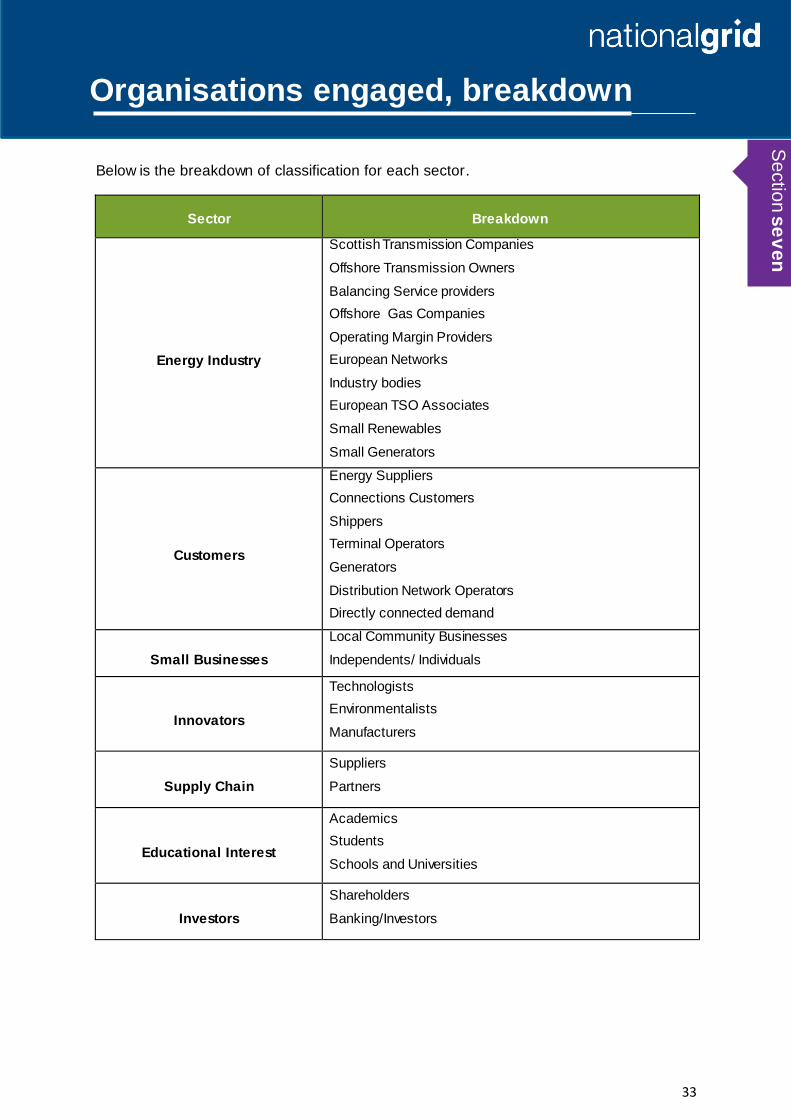

Below is the breakdown of classification for each sector.

Sector Breakdown

Energy Industry

Scottish Transmission Companies

Offshore Transmission Owners

Balancing Service providers

Offshore Gas Companies

Operating Margin Providers

European Networks

Industry bodies

European TSO Associates

Small Renewables

Small Generators

Customers

Energy Suppliers

Connections Customers

Shippers

Terminal Operators

Generators

Distribution Network Operators

Directly connected demand

Small Businesses

Local Community Businesses

Independents/ Individuals

Innovators

Technologists

Environmentalists

Manufacturers

Supply Chain

Suppliers

Partners

Educational Interest

Academics

Students

Schools and Universities

Investors

Shareholders

Banking/Investors

Sectio

n s

ev

en

34

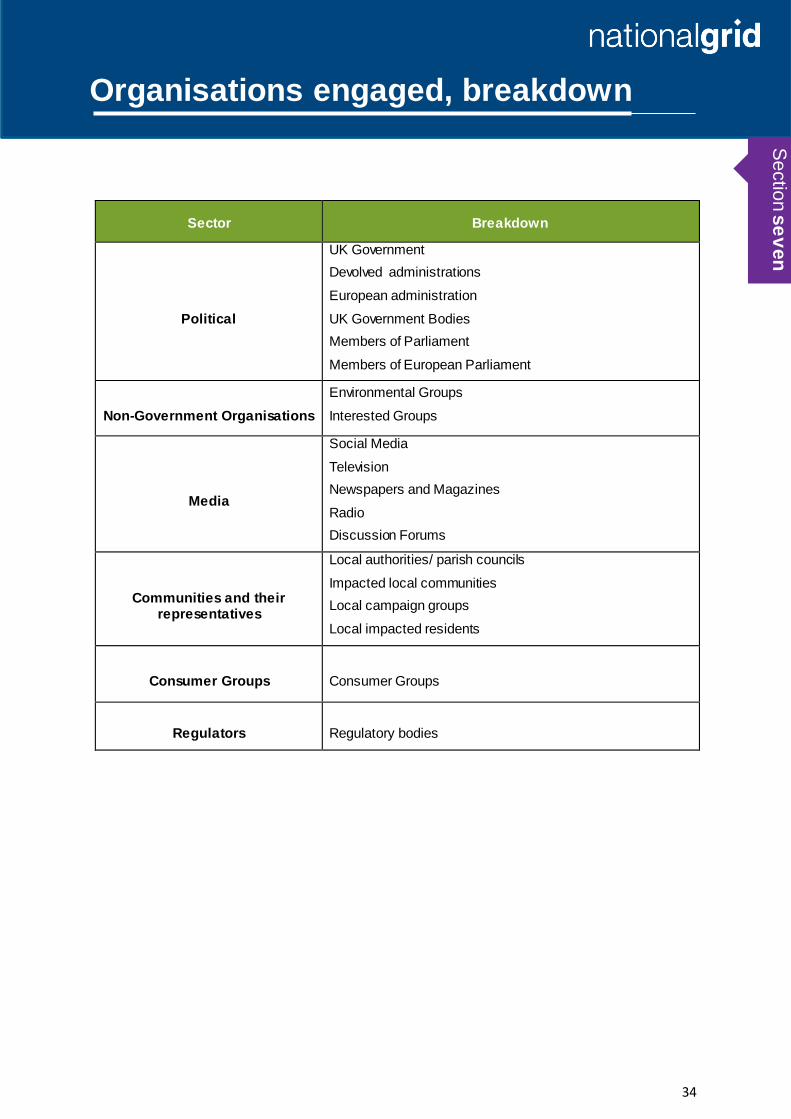

Organisations engaged, breakdown

Sector Breakdown

Political

UK Government

Devolved administrations

European administration

UK Government Bodies

Members of Parliament

Members of European Parliament

Non-Government Organisations

Environmental Groups

Interested Groups

Media

Social Media

Television

Newspapers and Magazines

Radio

Discussion Forums

Communities and their representatives

Local authorities/ parish councils

Impacted local communities

Local campaign groups

Local impacted residents

Consumer Groups Consumer Groups

Regulators Regulatory bodies

Sectio

n s

ev

en

35

FES 2016: You said, we did

Provided below is a review of the content specific feedback from our stakeholders which we

published in our 2016 Stakeholder Feedback Document with an update on the actions we

said we would deliver for FES 2016.

You said, we did – a look back at the 2016 FES Stakeholder Feedback Document

Electricity Interconnectors

“Consumer Power should have more interconnection”

We advised we had developed a new capacity model for the analysis of

interconnectors. Also that using this we have validated what our stakeholders have

told us and for FES 2016 Consumer Power would have more interconnection. We

did: Consumer Power increased from 10.8GW of interconnection in 2035 in FES

2015 to 23.3GW in 2035 in FES 2016.

“Last year we said we were going to improve our interconnector methodology,

have we done this? For example, we don’t take into account what is happening

across the EU in terms of interconnection flows”

We advised that for FES 2016 we would implement a more robust method and

introduce a generic timeline for interconnector development so we can understand

the minimum time it takes to connect. We advised we had commissioned Baringa to

undertake European modelling work to deliver FES 2016 annuals and peaks which

considered flows across Europe. We also advised we were in the process out to

tender for the enduring European model which would be used from FES 2017

onwards. We did: we commissioned consultants to undertake European flow

analysis on the proposed interconnector capacities and utilised this information within

the FES for annual and peak flows. We also tendered for a new Pan European

market model which is now used in the latest Network Options Assessment (NOA)

process.

Electricity Supply

“It would be really useful to understand how load factors will change over the

study period”

We advised we would consider how we might be able to show load factors within our

scenarios and aim to include this in FES 2016. We did not: include any specific load

factor analysis in the publication. However they can be back calculated from the

annual generation charts, reflecting historic outputs. We did: show capacity in FES

without load factors in order to indicate the uncertainty around output.

Sectio

n s

ev

en

36

FES 2016: You said, we did

“We should be more aggressive in how deployment of new technologies is

reflected, e.g. marine”

We advised we formed our technology projections after engaging with a variety of

stakeholders and included those technologies which demonstrated clear evidence of

deployment. We advised that within FES 2016 we would include a number of

‘Spotlights’ for technologies where there is currently insufficient data to include as a

direct input to our analysis. We did: cover spotlights in FES 2016 on the ‘Changing

faces of electricity supply’, ‘Onshore wind repowering’ and ‘Are small modular

reactors the next chapter in GB’s nuclear story?’.

“We should take into consideration the increasing influence of small -scale

generation on the electricity supply mix. We should consider a fully

decentralised scenario”

We advised that FES 2015 saw Consumer Power reach 40 percent small-scale

decentralised generation by 2035, doubling from today’s level. The Government had

signed multiple large-scale generation contracts going 15-35 years out; as such none

of our scenarios would be fully decentralised. We advised we were working on

improvements in our understanding of the volume and type of small-scale generation

and the interactions with large-scale generation. We also advised we aimed to

include more on this within FES 2016. We did: we included a section in FES 2016

titled “Shift from transmission to distribution connections” which highlighted the

expected increase in distributed generation. Consumer Power has by far the most

distributed generation profile with 89GW connected at the local level by 2040, making

up 49 per cent of total generation capacity and providing 40 per cent of generation

output.

Electricity Demand

“There is greater potential for demand side response (DSR) to be reflected in

the FES”

We advised for FES 2016 we would look to improve the process for creating

scenarios for Triad avoidance, which formed a major part of our Industrial and

Commercial Demand Side Response (DSR) scenarios. We advised we were working

closely with National Grid’s ‘Power Responsive’ campaign around engagement with

the demand side industry, allowing us to increase the range of stakeholders we see

in this area. We did: for FES 2016 we more closely examined recent Triad

avoidance, and the recent Capacity Auction results. This resulted in an increase in

the amount of potential available DSR. The impact of electricity storage was also

factored into future years’ DSR values. We will continue: to review the amount of

DSR in our scenarios.

Sectio

n s

ev

en

37

FES 2016: You said, we did

“You told us that our residential demand scenarios were too high. Some of you

said that we had not properly taken into account pending EU energy efficiency

legislation which will have a measurable effect on future demand”

We advised we would gather more data on EU energy efficiency legislation and

reflect it in the scenarios which feature greater energy efficiency. We advised for the

less energy efficient scenarios, we continued to believe it was credible for residential

demand to increase if conditions changed, if a new technology was adopted or if

technology is used to enhance quality of life rather than save energy. We did: we

consulted experts who provided guidance and data. This work was built into the

residential appliance models. Gone Green assumed the EU 2030 energy efficiency

targets are met on time, in order to meet the UK’s longer term decarbonisation goals.

Slow Progression assumed the targets are met in 2040. Consumer Power and No

Progression did not specifically target the EU energy efficiency goals, to reflect less

green ambition. We will: keep this approach for FES 2017.

“For residential air conditioning, over 40% of those who attended the webinar

felt our projections were too high in Consumer Power, whereas for the other

scenarios the feeling was our projections were about right”

We advised we will revise our projections for residential air conditioning in Consumer

Power. We did: for Consumer Power we considered the likelihood of different parts

of the country adopting air conditioning, taking into account demographics and urban

setting and penetration was revised to 60% by 2050. Gone Green remained the

same to reflect increased wealth. Slow Progression and No Progression were revised

down to existing penetration levels (~1% of homes) to 2050 to reflect lower wealth

levels. We will: review this approach for FES 2017.

“How about using different population and housing growth scenarios?”

We advised we use a single forecast for population and housing growth across our

scenarios. This allows easy comparison between the scenarios and the impact of

scenario components to be highlighted more effectively e.g. energy efficiency,

technology adoption and heating demand.

“All smart meters should be in by the end of 2020”

We advised in our Gone Green scenario the rollout programme is completed in 2020.

We believe it is prudent that our other scenarios model futures where differing rollout

scenarios are experienced.

Sectio

n s

ev

en

38

FES 2016: You said, we did

Electricity Storage

“We should include electricity storage in the scenarios – Gone Green and

Consumer Power provide the best environments for electricity storage to

prosper”

We advised we had engaged with developers and the value proposition had

improved for storage, therefore, we would include electricity storage penetration in

the FES 2016 analysis – focusing growth in Gone Green and Consumer Power. This

would cover transmission, distribution and behind the meter electricity storage . We

did: we embedded electricity storage within all the FES 2016 scenarios.

Gas Demand

“The Natural Gas Vehicle (NGV) market is heading towards pure gas vehicles

rather than hybrids”

We advised for FES 2016, we would review our NGV analysis to focus on pure gas

vehicles. We did: we included this within our analysis and modelling for FES 2016.

“You would like to see more depth to our district heat analysis”

We advised we had a district heat model, created in collaboration with Buro Happold,

which explored opportunities for district heat giving a richer picture of deployment in

the UK. In addition we advised for FES 2016, we will advance this project to allow an

extra layer of depth to be included in our analysis. We did: for FES 2016 we included

a spotlight covering this. We also plan to publish the detailed report by Buro Happold

and a thought piece on this topic.

“You believe that the 20 percent reduction of gas demand per house identified

in Gone Green and Slow Progression through a Home Energy Management

System (HEMS) is too ambitious”

We advised we would review the gas demand reduction associated with a HEMS for

FES 2016 and would continue to gather more data on new technologies to enhance

the inputs to our analysis. We did: for FES 2016 we revised down our projections to

10% and 5% across our scenarios and we will continue to include the suggested data

collection within our future analysis.

“You are surprised that low carbon heating uptake is not more prevalent in

Slow Progression; you would expect it to be closer to Consumer Power”

We advised we would re-evaluate the assumptions in our heating technology model.

We did: reduce the number of Heat Pumps in the ‘Gone Green’ FES Scenario.

Sectio

n s

ev

en

39

FES 2016: You said, we did

Gas Supply

“Locally produced shale gas should be greener in terms of overall lifecycle

carbon emissions than liquefying gas in the Middle East, shipping it several

thousand miles to the UK and re -gasifying it”

We advised we do not reflect lifecycle carbon emissions as an input to our analysis

as current carbon accounting does not include emissions incurred from activities

outside the UK. In addition we advised for FES 2016, we will look to explore this

further in a ‘Spotlight’. We didn’t: include as a specific spotlight for FES 2016 as a

report produced by DECC was published ahead of then. Instead we explained within

FES 2016 (page 116) our thoughts and a footnote to the report from DECC.

“It is unrealistic to say that no infrastructure will close; by 2035 some of the

facilities will be quite old”

We acknowledged this can be seen as a limitation in our analysis, however we did

not assume a facility will close when the owner of the facility has not made such a

decision public. In addition we advised for FES 2016 we would consider whether an

objective means of reducing capacity, possibly based on age of facility, can be

developed. This was considered for FES 2016 and for the coming year we plan to

produce a thought piece to explore this further.

“We should consider alternative sources of gas supply such as bio-synthetic

natural gas (SNG) or hydrogen from electricity to gas schemes”

We advised that we already considered bio methane, principally from anaerobic

digestion, but have not so far considered bio-SNG, gas from waste or hydrogen from

electricity to gas schemes. These are all potential sources that are more likely to

connect to the distribution networks than the transmission network and we are in

dialogue with the gas distribution networks to understand the maturity of these

technologies. We advised we would investigate this further in a ‘Spotlight’ for FES

2016. We did: model the development of bio-SNG within the FES 2016 ‘Gone Green’

scenario.

“The balance between LNG and continental gas is ‘unknowable’ and we should

not demonstrate any sort of split as this would imply an unwarranted level of

confidence”

We advised that Market intelligence at the time, both from our stakeholders and

commercial sources, is that LNG availability is likely to be high for at least the next 5

years. Also that there may have been some scope for increasing the LNG minimum

level slightly and reducing, but not removing, the ‘generic import’ category. We

advised will continue to engage with our stakeholders on this and review for FES

2016. We did: this is ongoing and will be used for future FES modelling as well.

Sectio

n s

ev

en

40

FES 2016: You said, we did

2050 Environmental Targets

“We should include further analysis on aviation and shipping as they will

dominate emissions in 2050”

We advised for FES 2016 we would enhance our 2050 analysis regarding shipping

and aviation emissions. We did: review the emissions within shipping and aviation

and incorporated within our analysis.

Sectio

n s

ev

en

41

October 2016 Workshops

Feedback

Disclaimer

For the purpose of this statement, National Grid Gas plc and National Grid Electricity Transmission plc will together be referred to as National Grid. The information contained within the Future Energy Scenarios Stakeholder Feedback document (“the Document”) is disclosed voluntarily and without charge to you in order to facilitate and encourage discussion of the scenarios used by National Grid in its electricity and gas planning processes.

The Document does not replace the Gas Ten Year Statement (GTYS) or the Electricity Ten Year Statement (ETYS) (or any other document published by National Grid containing substantially the same information as those documents) published in accordance with the relevant l icence conditions.

While National Grid have not sought to mislead any party as to the content of the Document and, whilst the content represents National Grid’s best views as of 27 January 2017, readers should not place any reliance on the content of the Document. The Document (including, without limitation, information as regards capacity planning, future investment and the resulting capacity) must be considered as illustrative only and no warranty can be or is made as to the accuracy and completeness of such Document, nor shall anything within the Document constitute an offer capable of acceptance or form the basis of any contract. Other than in the event of fraudulent misstatement or fraudulent misrepresentation, National Grid does not accept any responsi bility for any use which is made of the information contained within this Document.

Copyright National Grid 2017, all rights reserved. No part of the Document may be reproduced in any material form (including photocopying and storing in any medium or electronic means and whether or not transiently or incidentally) without the written permission of National Grid except in accordance with the provisions of the Copyright, Designs and Patents Act 1988.