Embed Size (px)

Citation preview

FIA-Paper FFM

Foundations in Financial

Management

For exams in 2015

theexpgroup.com

Notes

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 2 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

Contents

About ExPress Notes

1. Cash receipts and payments 7

2. Cash balances 12

3. Working capital management 17

4. Credit granting 23

5. Debt collection 26

6. Sources of finance 29

7. Short-term decisions 37

8. Capital investments 44

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 3 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

START

About ExPress Notes

We are very pleased that you have downloaded a copy of our ExPress notes for this paper.

We expect that you are keen to get on with the job in hand, so we will keep the introduction

brief.

First, we would like to draw your attention to the terms and conditions of usage. It’s a condition of printing these notes that you agree to the terms and conditions of usage.

These are available to view at www.theexpgroup.com. Essentially, we want to help people

get through their exams. If you are a student for the ACCA exams and you are using these

notes for yourself only, you will have no problems complying with our fair use policy.

You will however need to get our written permission in advance if you want to use these

notes as part of a training programme that you are delivering.

WARNING! These notes are not designed to cover everything in the syllabus!

They are designed to help you assimilate and understand the most important areas for the

exam as quickly as possible. If you study from these notes only, you will not have covered

everything that is in the ACCA syllabus and study guide for this paper.

Components of an effective study system

On ExP classroom courses, we provide people with the following learning materials:

The ExPress notes for that paper

The ExP recommended course notes / essential text or the ExPedite classroom

course notes where we have published our own course notes for that paper

The ExP recommended exam kit for that paper.

In addition, we will recommend a study text / complete text from one of the ACCA

official publishers, but we do not necessarily give this as part of a classroom course,

as we think that it can sometimes slow people down and reduce the time that they

are able to spend practising past questions.

ExP classroom course students will also have access to various online support materials,

including:

The unique ExP & Me e-portal, which amongst other things allows “view again” of the classroom course that was actually attended.

ExPand, our online learning tool and questions and answers database DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 4 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

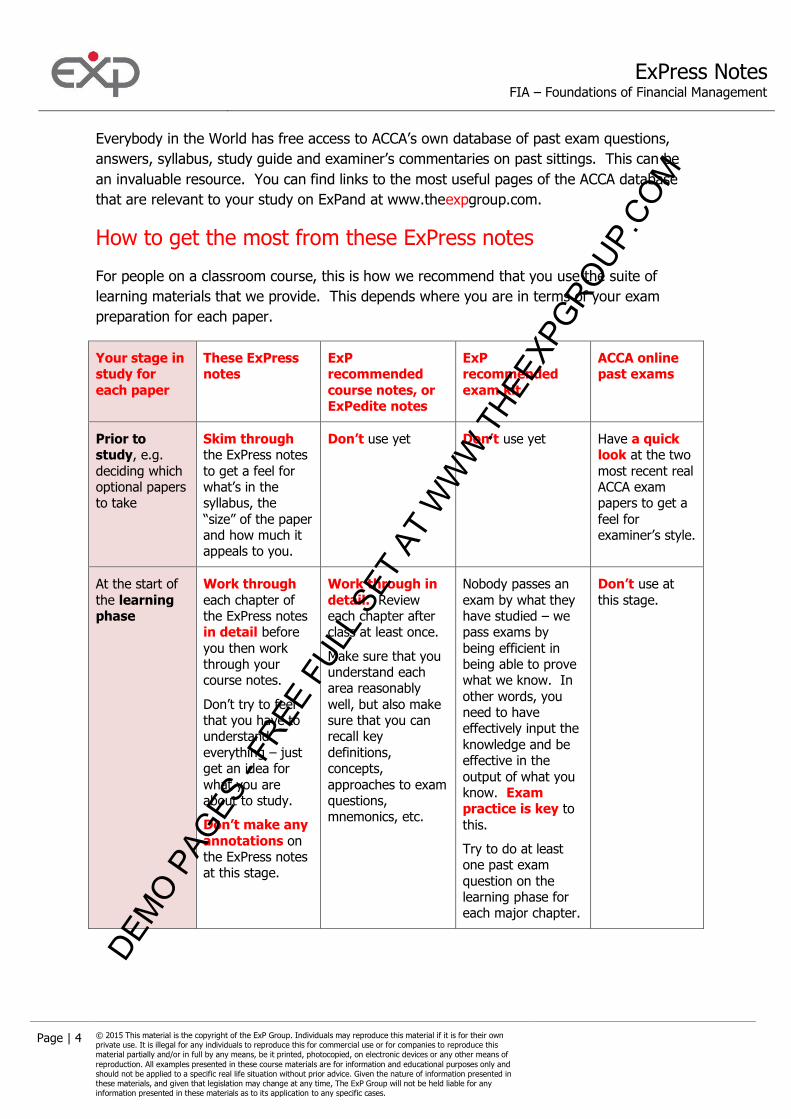

Everybody in the World has free access to ACCA’s own database of past exam questions, answers, syllabus, study guide and examiner’s commentaries on past sittings. This can be an invaluable resource. You can find links to the most useful pages of the ACCA database

that are relevant to your study on ExPand at www.theexpgroup.com.

How to get the most from these ExPress notes

For people on a classroom course, this is how we recommend that you use the suite of

learning materials that we provide. This depends where you are in terms of your exam

preparation for each paper.

Your stage in study for

each paper

These ExPress notes

ExP recommended

course notes, or ExPedite notes

ExP recommended

exam kit

ACCA online past exams

Prior to study, e.g.

deciding which optional papers to take

Skim through the ExPress notes

to get a feel for what’s in the syllabus, the

“size” of the paper and how much it appeals to you.

Don’t use yet Don’t use yet Have a quick look at the two

most recent real ACCA exam papers to get a

feel for examiner’s style.

At the start of

the learning phase

Work through

each chapter of the ExPress notes in detail before

you then work through your course notes.

Don’t try to feel that you have to understand

everything – just get an idea for

what you are about to study.

Don’t make any annotations on the ExPress notes at this stage.

Work through in

detail. Review each chapter after class at least once.

Make sure that you understand each area reasonably

well, but also make sure that you can recall key

definitions, concepts,

approaches to exam questions, mnemonics, etc.

Nobody passes an

exam by what they have studied – we pass exams by

being efficient in being able to prove what we know. In

other words, you need to have effectively input the

knowledge and be effective in the

output of what you know. Exam practice is key to

this.

Try to do at least one past exam

question on the learning phase for each major chapter.

Don’t use at

this stage.

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 5 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

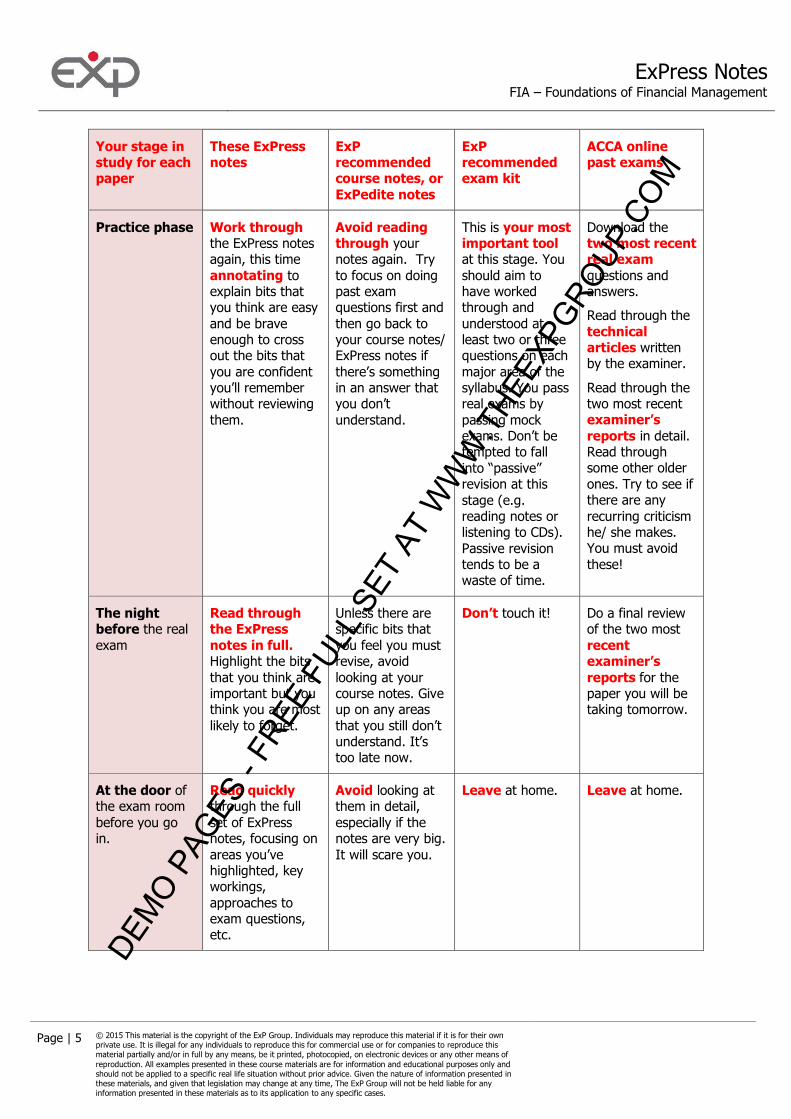

Your stage in study for each paper

These ExPress notes

ExP recommended course notes, or

ExPedite notes

ExP recommended exam kit

ACCA online past exams

Practice phase Work through the ExPress notes again, this time

annotating to explain bits that you think are easy

and be brave enough to cross out the bits that

you are confident you’ll remember without reviewing

them.

Avoid reading through your notes again. Try

to focus on doing past exam questions first and

then go back to your course notes/ ExPress notes if

there’s something in an answer that you don’t understand.

This is your most important tool at this stage. You

should aim to have worked through and

understood at least two or three questions on each

major area of the syllabus. You pass real exams by

passing mock exams. Don’t be tempted to fall

into “passive” revision at this

stage (e.g. reading notes or listening to CDs).

Passive revision tends to be a waste of time.

Download the two most recent real exam

questions and answers.

Read through the

technical articles written by the examiner.

Read through the two most recent examiner’s reports in detail. Read through some other older

ones. Try to see if there are any

recurring criticism he/ she makes. You must avoid

these!

The night before the real

exam

Read through the ExPress

notes in full. Highlight the bits

that you think are important but you think you are most

likely to forget.

Unless there are specific bits that

you feel you must revise, avoid

looking at your course notes. Give up on any areas

that you still don’t understand. It’s too late now.

Don’t touch it! Do a final review of the two most

recent examiner’s reports for the paper you will be taking tomorrow.

At the door of the exam room

before you go in.

Read quickly through the full

set of ExPress notes, focusing on

areas you’ve highlighted, key workings,

approaches to exam questions, etc.

Avoid looking at them in detail,

especially if the notes are very big.

It will scare you.

Leave at home. Leave at home.

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 6 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

Our ExPress notes fit into our portfolio of materials as follows:

Notes

Notes

Notes

Provide a base

understanding of the most important areas of the

syllabus only.

Provide a

comprehensive coverage of the syllabus and

accompany our face to face

professional exam courses

Provide detailed

coverage of particular technical areas and are used

on our Professional Development and

Executive Programmes.

To maximise your chances of success in the exam we recommend you visit

www.theexpgroup.com where you will be able to access additional free resources to help

you in your studies.

START About The ExP Group

Born with a desire to be the leading supplier of business training services, the ExP Group

delivers courses through either one of its permanent centres or onsite at a variety of

locations around the world. Our clients range from multinational household corporate

names, through local companies to individuals furthering themselves through studying for

one of the various professional exams or professional development courses.

As well as courses for ACCA and other professional qualifications, our portfolio of

expertise covers all areas of financial training ranging from introductory financial awareness

courses for non financial staff to high level corporate finance and banking courses for senior executives.

Our expert team has worked with many different audiences around the world ranging from

graduate recruits through to senior board level positions.

Full details about us can be found at www.theexpgroup.com and for any specific enquiries

please contact us at [email protected].

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 7 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

Chapter 1

Cash Receipts and Payments

KEY KNOWLEDGE

Cash and Cash Flow

Cash comprises both cash and bank deposits payable on demand and also cash equivalents

which are defined as “short-term, highly liquid investments that are readily convertible to

known amounts of cash and which are subject to an insignificant risk of changes in value”. The amount of cash held by a business at a point in time is found in the balance sheet

under “current assets”.

Cash flow refers to the movement of cash in and out of a business over a period of time.

This information is found in a statement of cash flows, which is a primary financial

statement. Such a statement is useful in that it is structured to show the extent to which a

company is able to generate net cash from its operating activities and how such net cash is

used in investing and/or financing activities.

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 8 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

Examples of cash receipts and payments include:

Operating: cash flow from trading activities, e.g. cash received from customers, cash

paid to suppliers and to employees;

Financing: Cash paid on interest;

Taxation: Actual cash paid during the year;

Investing: Cash flows on purchase or sale of non-current assets;

Financing: Cash flows on raising or redeeming long-term finance, such as shares or

debentures; dividends can also be included here.

Cash flow accounting

The relationship between cash flow accounting and accounting for income and expenditure

lies in the use of accruals and decisions as to the capitalisation of expenditures. Cash flow

accounting dispenses with the “matching” principle in financial accounting.

As the cash flow statement is derived from the income statement and the balance sheet,

adjustments need to be made to remove the effects of accrual accounting so that the cash

movements can be made more transparent.

Importance of cash flow management

Planning, tracking and collecting cash are all important because cash PAYS THE BILLS.

The failure to pay bills puts a company in danger of bankruptcy.

What begins as a condition of illiquidity can evolve into insolvency.

Cash flow is vital to going concern and commercial success, regardless of profitability.

Having enough cash on hand is therefore critical in being able to settle obligations when

they fall due (both planned and unforeseen); however, holding too much cash in a business

is costly. There is a trade-off between liquidity and profitability.

Determining the “optimal” amount of cash to hold becomes the challenge facing managers. Cash management functions are typically handled by treasury, and include:

Collecting cash from customers (as soon as possible);

Disbursing cash to suppliers (as late as practically possible);

Investing short-term cash surpluses in low-risk interest-bearing investments (such as

Treasury bills) in order to generate additional income for the company;

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 9 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

KEY KNOWLEDGE

Cash budgets

A cash budget is an estimate of the receipt and payments of cash in and out of the business

for a defined future period based on existing conditions and operating assumptions.

By understanding the nature and timing of cash receipts and expenditures, management is

better able to influence them and plan/budget for the future. The purpose is to ensure that

the company has sufficient cash on-hand to avoid missing disbursements when they fall

due.

There are statistical techniques which assist management in planning cash levels.

Cash budget/forecast

Businesses should develop their cash budget/forecast formats in a way which best reflects

the type of business conducted and transactions generated. Such tools serve as a

mechanism for monitoring and control.

KEY KNOWLEDGE

Cash forecasting

A cash forecast format/structure is shown below, in this case covering 6 months. Both

operating and non-operating cash flows are included.

The bottom of the table shows opening and closing cash balances.

Cash Budget Jan Feb Mar Apr May June

$ $ $ $ $ $

Receipts

Credit sales

Cash sales

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 10 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

Equipment disposal

Total

Payments

Materials

Labour

Variable Overheads

Fixed Costs

Equipment acquisition

Overdraft Interest

Current account interest

Income tax

Total

Net cash m-o-m variance

Cash balance at month-end

Completing the table above requires forecast assumptions relating to volume of

production/sales as well as prices and costs.

EXAMPLE

Unit Selling Price (on credit) $/unit payment terms given to credit customers:

Unit Selling Price (cash) $/unit discount granted to cash customers

Unit Variable Cost:

Material $/unit payment terms taken from suppliers:

Labour $/unit paid in the month

Overheads $/unit

Fixed Costs $/month

< Actual Forecast > Sales/Production volumes Nov Dec Jan Feb Mar Apr May June Total

actuals/forecast

Production (units)

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 11 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

Credit sales (units)

Cash sales (units)

Capex forecast New equipment acquisition

Old equipment sale

Inventory levels required +/- planned

Bank interest at % pa Bank interest at % pa

KEY KNOWLEDGE

Sensitivity of variables

Preparing cash forecasts requires assumptions, and assumptions are exposed to uncertainty.

This means that the actual amount of cash received or disbursed may vary from that budgeted.

Budgeting processes therefore include the testing of assumptions for sensitivity. If, for example, wage levels rise by 10% (instead of 5%), then what effect will this have on the

level of cash? Same question with regard to materials (and overheads and prices, etc.).

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 12 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

Chapter 2

Cash Balances

KEY KNOWLEDGE

Investing and financing

Cash surpluses and deficits occur as a result in timing differences between the receipt of

cash and the necessity to settle obligations punctually. If a deficit results, then the company

should have overdraft faciltities in place with a bank.

If deficits prove to be longer-term in nature, then the company should consider short-term

borrowing, or possibly, longer-term forms of finance if the deficit is expected to persist.

In the event of surpluses, these can be invested (e.g. T-bills mentioned earlier); other types

of investments include:

Bank deposits DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 13 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

Money- market deposits

Certificates of deposit

Government bonds

Local authority stock

KEY KNOWLEDGE

Optimum liquidity levels

Cash management models Holding too much cash is sub-optimal. A business with permanently excessive balances (not

required for operating purposes) should be paid out to shareholders.

Two techniques for monitoring the optimal level of cash are discussed below.

Baumol model

This model was developed several decades ago. One can think of:

cash as inventory;

selling marketable securities transactions as ordering costs;

Interest rate, representing the opportunity cost of holding cash

By determining the following:

N = the total annual amount of cash required

F = the cost of each securities transaction (sale)

i = the annual interest rate obtainable on the investment in securities

then

Z = the amount of cash that needs to be raised per transaction

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 14 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

The optimal level of Z = √2NF / i

The main drawback of the Baumol method is that it makes the simplified (and unrealistic)

assumption that cash disbursements are constant and predictable.

Miller-Orr

A second method addresses the issue of optimal cash balances and attempts to improve on

the drawback of the Baumol model.

Miller-Orr is based on statistically tracking the variability of net daily cash flows; this is

denoted as

V = Variability of net daily cash flows (variance or sigma squared)

The other variables are:

F = Cost of each securities transaction;

k = Interest rate per day on marketable securities; and

LL = Lower cash limit, which needs to be established by management

Based on the above, the cash balance return point (R) is

________ R = 3√3xFxV/4k + LL

The level R is the cash balance which must be restored when either the upper limit (UL) or

lower limit (LL) have been reached.

Once R is known, then the upper cash limit, or UL, is calculated thus:

UL = 3 R – 2(LL)

DEM

O PAG

ES -

FREE

FUL

L SE

T AT

WW

W.T

HEEX

PGRO

UP.C

OM

ExPress Notes FIA – Foundations of Financial Management

Page | 15 © 2015 This material is the copyright of the ExP Group. Individuals may reproduce this material if it is for their own private use. It is illegal for any individuals to reproduce this for commercial use or for companies to reproduce this material partially and/or in full by any means, be it printed, photocopied, on electronic devices or any other means of

reproduction. All examples presented in these course materials are for information and educational purposes only and should not be applied to a specific real life situation without prior advice. Given the nature of information presented in these materials, and given that legislation may change at any time, The ExP Group will not be held liable for any information presented in these materials as to its application to any specific cases.

KEY KNOWLEDGE

Working capital needs and funding strategies

The level of working capital required in a business depends on the industry it operates in,

the length of its working capital cycle and the range of funding options open to it. Retaining

flexibility is a key requirement. While overdraft financing is expensive, it does permit

spontaneous drawdowns and rapid repayments.

Funding strategies are guided by the following considerations:

Temporary cash shortages can be funded short-term, while

Permanent shortages should be funded long-term

The “matching principle” can be applied to the assets being financed:

Fixed assets are generally funded long-term, along with the permanent portion of

current assets (e.g. buffer stocks);

Current assets of a fluctuating nature can rely on short-term finance (e.g. seasonal

upswings in inventories / receivables)

Cash surpluses, on the other hand, can be dealt with based on whether they are:

Short-term: in this case they may be invested in short-term, low-risk, liquid

investments (e.g. Treasury bills or marketable securities);

Long-term: Make acquisitions; Reduce debt; Pay extraordinary dividend, etc.

KEY KNOWLEDGE

Liquidity ratios

The relationship between current assets and current liabilities is used as a measure of

liquidity in the firm:

Current ratio = Current assets Current liabilities DE

MO P

AGES

- FR

EE F

ULL

SET

AT W

WW

.THE

EXPG

ROUP

.COM