Embed Size (px)

Citation preview

2007 HEAVY VEHICLE CHARGES DETERMINATION

REGULATORY IMPACT STATEMENT VOLUME I

December 2007

Prepared by

National Transport Commission

National Transport Commission 2007 Heavy Vehicle Charges Determination: Regulatory Impact Statement

Report Prepared by: National Transport Commission ISBN: 1 921168 72 2

REPORT OUTLINE

Date: December 2007

ISBN: 1 921168 72 2

Title: 2007 Heavy Vehicle Charges Determination: Regulatory Impact Statement

Address: National Transport Commission Level 15/628 Bourke Street MELBOURNE VIC 3000

E-mail: [email protected] Website: www.ntc.gov.au

Type of report: Regulatory Impact Statement

Objectives: To improve transport efficiency, productivity and equity, reduce administration costs, improve road safety, and promote nationally consistent regulatory reform.

NTC Programs: Pricing

Key words: charges, heavy vehicles, road cost recovery, allocated costs, pricing.

FOREWORD

The Productivity Commission’s Road and Rail Infrastructure Pricing Inquiry, and the direction outlined by heads of government on 13 April 2007, clearly set out an agenda for pricing reform to unlock more productivity from the road network. As part of the first phase of this reform, the Australian Transport Council (ATC) and Council of Australian Governments (COAG) asked the National Transport Commission (NTC) to prepare a heavy vehicle charges determination for implementation in 2008. ATC and COAG specified that the determination should ensure that heavy vehicles continue to pay their share of increasing road expenditure by all levels of government. Thus the 2007 Heavy Vehicle Charges Determination (“the Determination”) will be the ‘building block’ for pricing reform. It will sustain the revenue base needed for governments to invest in better and safer roads, including the infrastructure upgrades needed for improved heavy vehicle access. In the past, updating heavy vehicle road use charges has been an emotive and often divisive issue. The NTC is encouraged by the cooperative approach of the freight industry in the development of this proposal. Indeed, the constructive views provided by industry have helped the NTC to better understand and respond proactively to the operating challenges it faces, and enabled the NTC to develop charges that are more flexible than they have been to date. In preparing this Final Regulatory Impact Statement (RIS), the NTC has reported differences between its recommended option and the industry’s views transparently and honestly. It has also made independent assessments of the impacts of its recommended option, and endeavoured to manage these impacts – for example, by recommending the phasing-in of charge increases to allow operators to better plan and re-negotiate freight contracts. Australia must maintain a world-class road and rail transport network to service the growing freight task, to reduce road trauma, and to ensure Australian businesses can compete cost-effectively in the global marketplace. The trucking industry has long supported the principle of paying its way. The NTC’s recommendations will ensure that this happens, and continues to do so between determinations. It is now time for governments to similarly respond by ensuring that productivity gains from the road asset – which are required by the industry to support a competitive economy – are released. The NTC acknowledges the work of Meena Naidu, Chris Egger, Matthew Clarke and Pauline Sullivan as the major contributors to this RIS. The statement has been presented in two volumes: Volume 1 describes the issues, options and recommendations; Volume II contains the technical appendices that underpin the analysis.

Michael Deegan

Chairman

SUMMARY

The road leading to the Determination

In 2006, the Productivity Commission conducted an inquiry into Road and Rail Freight Infrastructure Pricing (PC Inquiry), which included a review of the NTC’s methodology for developing recommendations on heavy vehicle charges. After the Productivity Commission broadly endorsed this methodology, the Australian Transport Council (ATC) directed the NTC to begin work on a new heavy vehicle charges determination, to replace the current Second Determination.

In April 2007, the Council of Australian Governments (COAG) outlined a road pricing reform plan, and endorsed the ATC directive for a 2007 Heavy Vehicle Charges Determination (“the Determination”) as part of the first phase of this plan. This reflected findings from the PC Inquiry that:

• heavy vehicle charges were set to under-recover costs: this Determination shows that in 2007/08 heavy vehicles will under-recover expenditure by $168m

• vehicles are subsidised if they do not recover their attributable costs: the Determination finds B-doubles under-recover their attributable costs by just over $11,000 per vehicle per year.

Addressing issues of cost recovery through the Determination is the first step in a broader COAG reform program which seeks to improve the efficiency and productivity of the road network through heavy vehicle price reform.

In line with specific directions from the ATC and COAG, the primary objectives of the 2007 Determination are to ensure that:

• road expenditure allocated to heavy vehicles in aggregate is fully recovered

• each vehicle class at least recovers its attributable expenditure, so that there are no cross-subsidies between vehicle classes

• charges accommodate high-productivity vehicles

• charges are consistent with the ATC approved pricing principles

• charges are updated in a way that enables them to continue to recover both allocated and attributable expenditure between determinations.

Following extensive consultation on the Draft Regulatory Impact Statement, NTC sought to achieve a further objective to maintain vehicle configuration flexibility, so that operators can change their vehicle configuration to meet the specific needs of each trip without facing adverse financial implications. This objective, which responds to trucking industry concerns, is consistent with COAG’s productivity reform agenda.

Process the NTC used to develop its recommendations

In July 2007, the NTC released a Draft Regulatory Impact Statement (RIS) that outlined a range of options (including its preferred options) for heavy vehicle charges. In developing these options, the NTC was informed by the Third Determination consultation process, the PC Inquiry, discussions and a technical workshop with industry representatives and government, and analyses of potential impacts of changes in the level of charges.

The NTC then completed comprehensive public consultation on the draft RIS. It invited industry and government stakeholders and other interested parties to make written submissions, receive industry briefings and/or participate in public focus group sessions held around the country. It received 22 written submissions and held focus groups in Melbourne, Sydney, Brisbane, Adelaide, Perth, Canberra and Darwin1. It also undertook further discussions with industry representative groups (including the Australian Trucking Association and its member associations and the National Farmers Federation) and governments.

Stakeholders raised a variety of concerns in relation to the draft RIS and the NTC’s preferred options. Key concerns included that:

• Competitive constraints make it difficult for industry to absorb increased costs

• Incentives for local government to provide access to the local road network are weak

• Enforcement costs should not be included in the cost base without a better enforcement and compliance framework

• The phasing in of charges needs to occur more evenly over the phase in period, to give industry time to better respond to changes

• The use of the proposed high productivity formula to set charges for higher productivity vehicles could impose significant administrative and enforcement burdens

• The proposed charges schedule constrained vehicle configuration flexibility.

After listening carefully to all stakeholders’ comments and views, the NTC responded by making significant changes to its preferred options in developing this Final RIS.

NTC’s recommendations

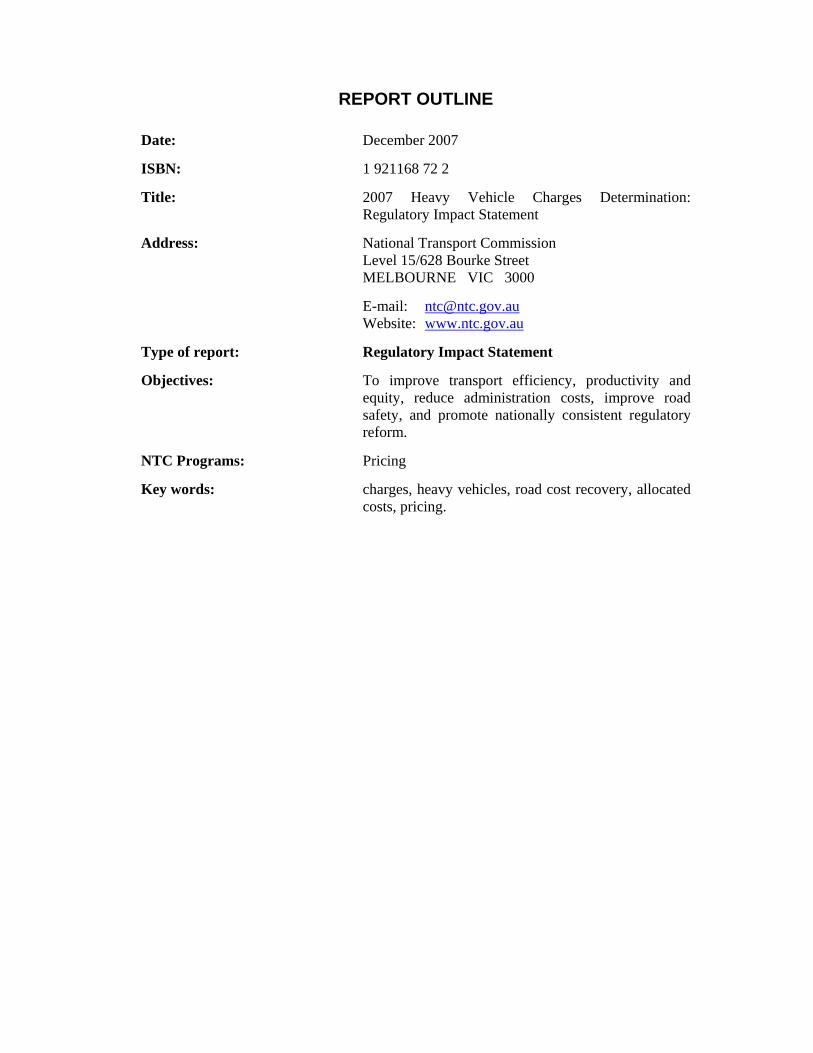

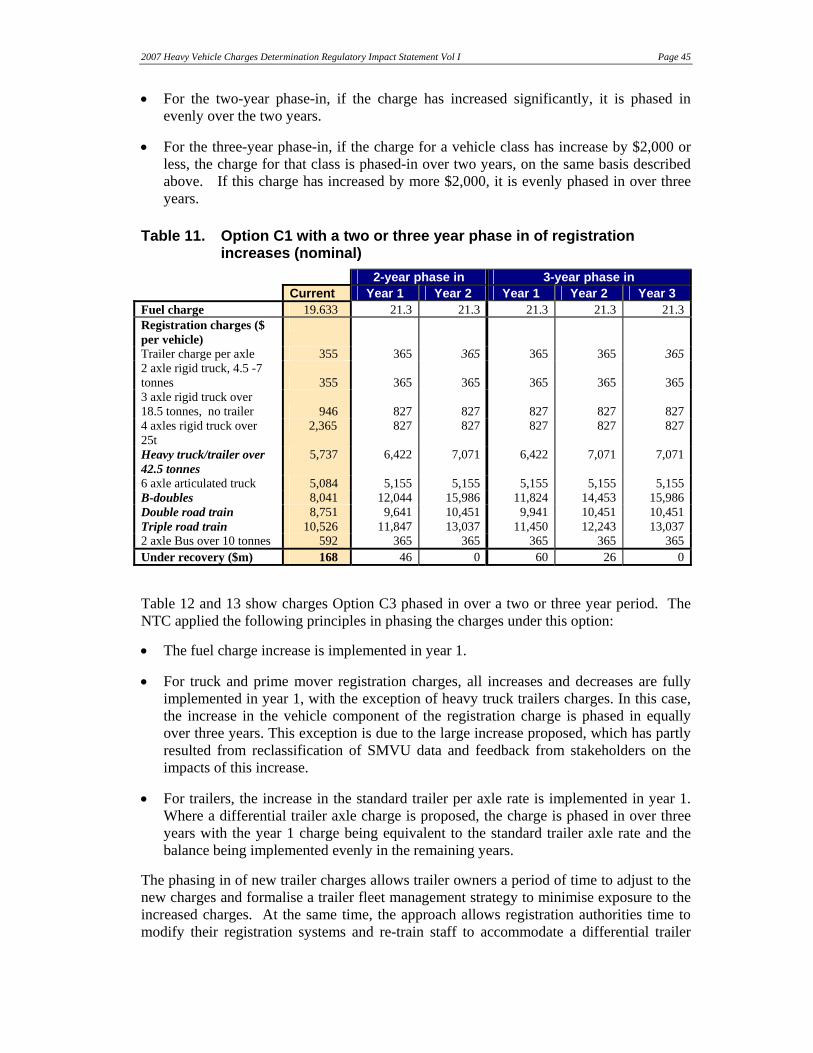

The NTC recommends the heavy vehicle charges schedule contained in Appendix I Vol. II of the Final RIS and shown for selected vehicles in Table ES1 below. These recommended charges are based on the preferred charging option described in the draft RIS, but the registration charges are more modular through the application of differentiated trailer axle charges rather than a uniform trailer axle charge.

The recommended charges meet all the objectives listed above, with two minor exceptions:

• The charges have been set to ensure that heavy vehicles fully recover their allocated expenditure in aggregate and each vehicle class at least recovers its attributable expenditure. However, the charges schedule includes a phase-in period of up to three years for some registration charges to establish a manageable implementation path for heavy vehicle operators and registration authorities. As a result of this phase-in period, the charges will not fully recover allocated and attributable expenditure until the final year of implementation (2010/11).

• The recommendations in relation to the annual adjustment process will enable charges to be updated so that they continue to fully recover allocated costs between determinations, and minimise the extent to which cross-subsidies across vehicle classes occur between determinations. The most precise way to ensure that no cross-subsidies

1 Focus group presentations and transcripts are available on the NTC website.

occur between determinations is to recalculate charges every year. However, the NTC did not favour this option because it may lead to charges volatility and will impose a significant regulatory burden.

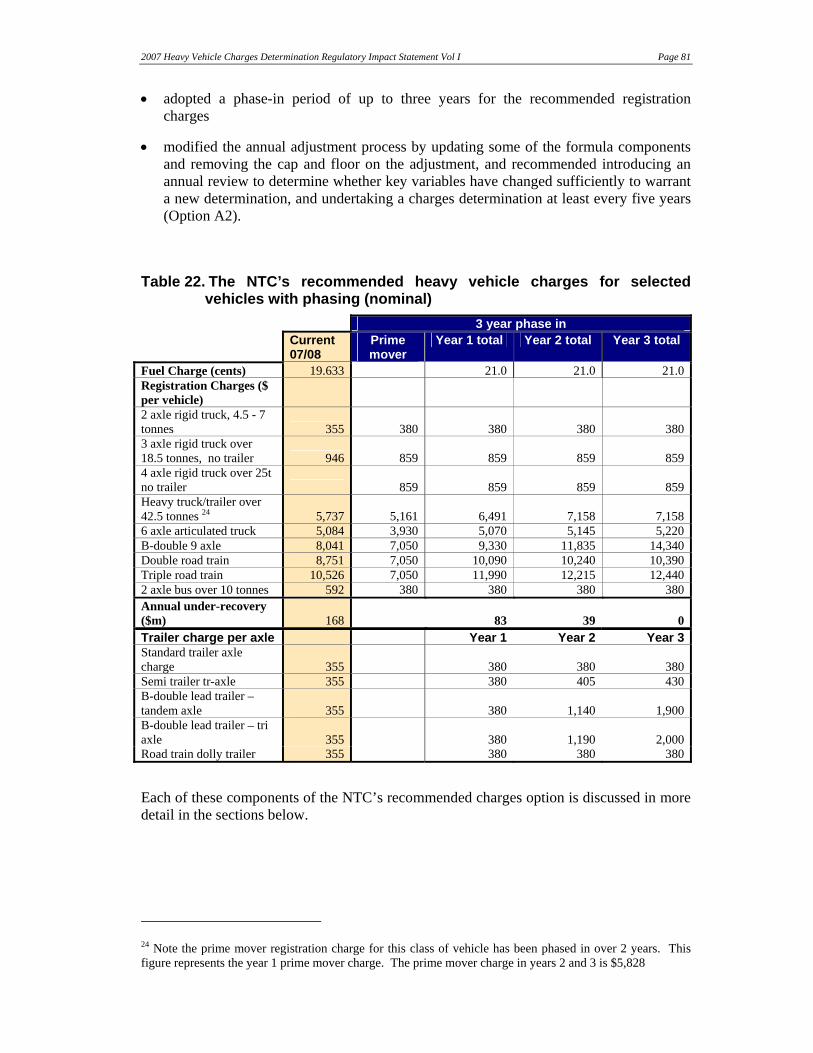

Table ES1. The NTC’s recommended heavy vehicle charges for selected vehicles (nominal)

3 year phase in Current

07/08 Prime mover

Year 1 total Year 2 total Year 3 total

Fuel charge (cents) 19.633 21.0 21.0 21.0Registration charges ($ per vehicle)

2 axle rigid truck, 4.5 - 7 tonnes 355 380 380 380 3803 axle rigid truck over 18.5 tonnes, no trailer 946

859 859 859 859

4 axle rigid truck over 25t no trailer 859 859 859 859Heavy truck/trailer over 42.5 tonnes 2 5,737 5,161 6,491 7,158 7,158 6 axle articulated truck 5,084 3,930 5,070 5,145 5,220 B-double 9 axle 8,041 7,050 9,330 11,835 14,340 Double road train 8,751 7,050 10,090 10,240 10,390 Triple road train 10,526 7,050 11,990 12,215 12,440 2 axle bus over 10 tonnes 592 380 380 380 380Annual under-recovery ($m) 168 83 39 0Trailer charge per axle Year 1 Year 2 Year 3Standard trailer axle charge 355 380 380 380Semi trailer tr-axle 355 380 405 430B-double lead trailer – tandem axle 355 380 1,140 1,900B-double lead trailer – tri axle 355 380 1,190 2,000Road train dolly trailer 355 380 380 380

In calculating the recommended charges, the NTC:

• included 2007/08 budget expenditure in the seven-year average expenditure figure used in establishing the cost base

• partially included enforcement costs in the cost base

• allocated costs in line with the methodology developed as part of the Third Determination workings, except for a modification to address trucking industry concerns about the costs allocated to double and triple road trains

• adopted a modular charges structure that maintains vehicle configuration flexibility and accommodates higher productivity vehicles within the charges schedule

2 Note the prime mover registration charge for this class of vehicle has been phased in over 2 years. This figure represents the year 1 prime mover charge. The prime mover charge in years 2 and 3 is $5,828

• adopted a phase-in period of up to three years for the recommended registration charges

• modified the annual adjustment process by updating some of the formula components and removing the cap and floor on the adjustment amount, and recommended introducing an annual review to determine whether key variables have changed sufficiently to warrant a new determination, and undertaking a charges determination at least every five years.

Inclusion of 2007/08 budget expenditure in the cost base

In calculating the expenditure figure included in the Final RIS cost base, the NTC used an average of seven years’ expenditure data, including 2007/08 budget expenditure and actual expenditure for 2001/02 to 2006/07. This resulted in a cost base of $1,978m, which is $125m more than the Draft RIS cost base.

The NTC considered using 2006/07 budget expenditure and actual expenditure for 2000/01 to 2005/06. However, it preferred the inclusion of 2007/08 budget expenditure because:

• This approach ensures that the expenditure figure used to calculate the cost base is as up-to-date as possible, reducing the lag in the recovery of the current year of expenditure.

• Although it leads to a higher cost base than the alternative option, the resulting higher charges can be phased in over up three years and so will create less of a price shock for vehicle operators.

• It is administratively simpler, because it avoids the need for an annual adjustment to occur on the same date as new charges under the 2007 Determination begin to be implemented.

• It is consistent with the current methodology.

Partial inclusion of enforcement costs in the cost base

In calculating the cost base, the NTC took the view that it is appropriate for heavy vehicle charges to recover the costs associated with enforcing axle mass limits, as the primary objective of these constraints is to manage road wear (and thus avoid expenditure on road maintenance). In addition, because of the difficulties in separating mass-related and safety-related costs, the NTC took the view that the enforcement costs reported by road agencies, discounted to account for the fact that the NSW road agency appears to spend significantly more on safety-related enforcement than road agencies in other jurisdictions, is a reasonable proxy for mass-related costs.

In reaching this view, the NTC considered two alternative options: full inclusion of enforcement costs (i.e., both mass- and safety-related costs) and full exclusion of enforcement costs. It also considered the PC Inquiry’s finding that “the costs of enforcing heavy vehicle mass and speed restrictions are appropriately recovered through road user charges”, and the ATC pricing principle that heavy vehicle charges should enable “full recovery of allocated infrastructure costs”. The NTC concluded that only the recovery of mass-related enforcement is appropriate. This is because safety-related enforcement costs

cannot be considered to be infrastructure costs. Therefore their recovery through heavy vehicle charges would be inconsistent with the ATC’s current pricing principles.

The NTC noted the strong view expressed by the trucking industry that the recovery of enforcement costs is not justified without a framework for enforcement that resulted in better, more targeted and efficient enforcement. The NTC considers that work currently being done, including the development of a National Heavy Vehicle Enforcement Strategy, will improve the consistency and quality of enforcement, and improve the national accreditation program. The recovery of enforcement costs through heavy vehicle charges provides an opportunity for the cost of these various initiatives to be recovered, and could also provide incentives for operators to participate in accreditation leading to safer roads.

Allocation of costs

The methodology the NTC used to allocate the cost base to the different vehicle classes is based on the best available research, and was updated and consulted on as part of the Third Determination process. The Productivity Commission found that this methodology is reasonable although conservative in nature. In general, the methodology also has the support of the trucking industry.

The methodology relies on road usage data from the Australian Bureau of Statistics’ Survey of Motor Vehicle Usage (SMVU) to allocate costs. In responses to the draft RIS, the trucking industry expressed concerns about the quality of this data. The NTC reviewed the data, and undertook further analysis on the reliability of the road train data. It found the standard error associated with road train vehicle kilometres travelled (VKT) is sufficiently large that the VKT for double and triple roads trains fell within a similar range applying a 95 per cent confidence interval.

Given the significant impact VKT has on cost allocation, the NTC applied an average road train VKT figure of 133,750 to both double and triple road trains. This increased the cost allocated to double road trains from $35,611 to $38,055 and decreased the cost allocated to triple road trains from $68,342 to $47,323 (before unsealed travel adjustments are made) compared to the draft RIS.

Adoption of a modular charges structure that maintains vehicle configuration flexibility and accommodates higher productivity vehicles

In the draft RIS, the NTC presented two options for charges:

• Option C1: Fuel-based charge of 21.3 cents per litre plus annual registration charges with differentiated prime mover charges, which ensured that heavy vehicles fully recover their allocated costs in aggregate, and all vehicle classes recover at least their attributable costs (marginal road use costs).

• Option C2: Fuel-based charge of 19.7 cents per litre plus annual registration charges with differentiated prime mover charges, which ensured that heavy vehicles fully recover their allocated costs in aggregate, and all vehicle classes recover their fully allocated costs (including common costs).

Consultations indicated that while there was broad support for the principle of attributable cost recovery, there were also concerns about the implications of the proposed options for vehicle configuration flexibility and the enforcement burden.

The trucking industry strongly put the view that operators should be able to change their vehicle configuration to meet their needs for specific trips without facing adverse financial implications. To enable a standard trailer axle charge, the draft RIS options proposed that

B-double, double road train and triple road train prime movers would all have different registration charges. The trucking industry expressed concern that the flexibility of the current charges arrangement would be lost by having a differentiated charge for a prime mover that is the same, except for the trailer configuration.

Some governments expressed concern that a change to the charges structure would result in a greater enforcement burden. This is because operators would be given an incentive to register their prime mover in the most inexpensive class (a double road train) but run it as part of a B-double or triple road train configuration.

In light of these concerns, and in consultation with the trucking industry, the NTC developed a third option:

• Option C3. Fuel-based charge of 21.0 cents per litre plus annual registration charges that, like Option C1, ensured that heavy vehicles fully recover their allocated costs in aggregate, and all vehicle classes recover at least their attributable costs.

However, unlike Option C1, this option maintains the flexibility of a prime mover by providing a multi-combinational prime mover charge. Cost recovery is achieved by differentiating the trailer axle charge by the type of trailer, not by the vehicle configuration. This modular approach is similar to the charging structure the ATA proposed in its submission in response to the draft RIS, and enables virtually any configuration of prime mover and trailers to be accommodated through the charges schedule.

This modular charge structure means that higher productivity vehicles can also be accommodated within the charges schedule. The NTC considers this is preferable to the use of higher productivity formula as proposed in the draft RIS, on the grounds that it is simpler and NTC analysis indicates that it results in very similar charges to the formula.

The NTC is conscious that although registration charges constitute a relatively small proportion of vehicle operating costs, its recommended registration charges for some vehicles represent a considerable cost increase. This is particularly the case for vehicles in classes that are currently under-recovering their attributable costs. Nevertheless, the NTC prefers its recommended charges option for the following reasons:

• as indicated above, this option meets all the primary objectives for the 2007 Heavy Vehicle Charges Determination

• unlike Options C1 and C2, it maintains vehicle configuration flexibility and accommodate higher productivity vehicles

• the charges under Option C3 better share the recovery of costs between the prime mover and the trailer. The charges under Option C2 do not adequately adhere to the pricing principle of having “regard to other pricing applications, such as light vehicle charges…” because they include a registration charge for two axle rigid vehicles that is below the mid point of the range of maximum charges for light vehicles.

Figure ES1 shows how total registration charges are derived under the recommended Option C3.

Figure ES1 Application of registration charges to vehicles

Adoption of a phase-in period of up to three years for registration charges

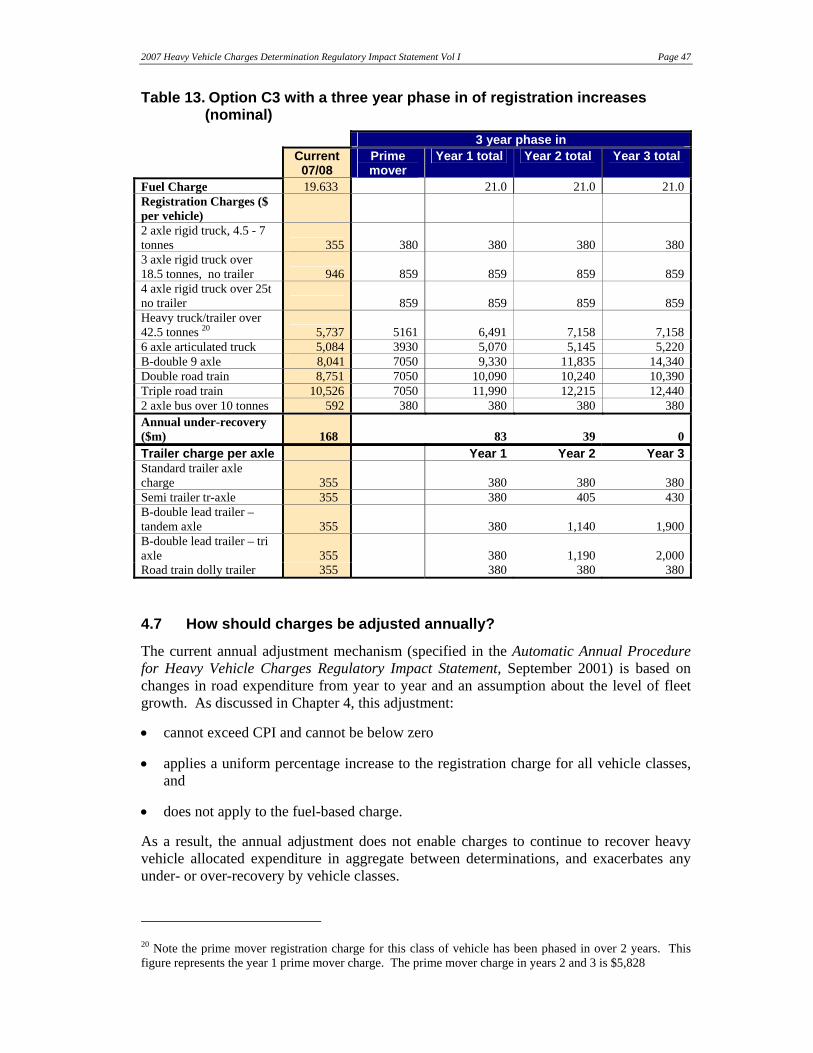

The recommended registration charges will result in cost increases for prime movers and trucks in some heavy vehicle classes, and the introduction of differential trailer axle charges will result in large cost increases for some trailer types. In recognition of this, the recommended charges schedule includes a phase-in period of up to three years. Under this schedule:

• The increased fuel-based charge is fully implemented in Year 1.

• For truck and prime mover registration charges, all increases and decreases are fully implemented in Year 1, except those for heavy truck trailers. In this case, the increase in the vehicle component of the registration charge is phased in evenly over three years. This exception is due to the large size of the increase, which has partly resulted from reclassification of SMVU data, and feedback from stakeholders on the impacts of this increase.

• For trailer registration charges, the increase in the standard trailer per axle rate is fully implemented in Year 1. Where a differential trailer axle charge is proposed, the charge is phased in over three years with the Year 1 charge being equivalent to the standard trailer axle rate and the balance being implemented evenly in the remaining years.

As noted above, this phasing in will result in a continued under-recovery of expenditure in Years 1 and 2. However, both the governments and heavy vehicle operators have indicated that it is necessary, to provide them with sufficient time to make the operational and system changes required to accommodate the new charges schedule.

Modification to the annual adjustment process

The NTC recommends modifying the current annual adjustment process by:

• Updating the formula components to align with the new 2007 Determination cost allocation model

• Removing the CPI cap and 0 per cent floor on registration charge increases

• Indexing the fuel-based charge by the Annual Adjustment Formula used to index registration charges.

In addition, the NTC recommends that it undertakes an annual review to evaluate whether key variables have moved sufficiently to warrant a new determination and that a charges determination occurs at least every five years (if not already undertaken as a result of the annual review).

The NTC considers that this approach to the annual adjustment (Option A2) is preferable to the alternative approaches it considered. It will ensure that charges continue to recover heavy vehicle allocated expenditure in aggregate in a way that is formula-driven, relatively simple, and will not require a new determination each year. In addition, when combined with an annual review process and more frequent determinations, it will minimise “ongoing cross-subsidisation across different heavy vehicle classes”.

In comparison:

• Options A1 (update formula components and include fuel indexation) does not achieve full recovery of allocated expenditure in aggregate or reduce cross-subsidisation across vehicle classes between determinations.

• Option A3 (index both registration charges and fuel-based charge by CPI or RCMP1) does not ensure that the adjusted charges match the estimated cost of road use over time, and therefore may result in the need for major corrections in subsequent determinations. In addition, it does not have much stakeholder support.

• Option A4 (annual recalculation of charges) is the most accurate way to ensure ongoing cost recovery and removal of cross-subsidisation, but it would introduce unnecessary charges volatility and require a significant amount of maintenance and consultation. Many stakeholders who commented on Option A4 expressed similar views.

The impact of new charges

NTC has considered the impacts of its recommended charges schedule. In general, it believes this schedule (which, as discussed above, includes a phase-in period) provides heavy vehicle operators with sufficient time to re-negotiate contracts and pass costs on to their customers, and to consider how they can achieve operational efficiencies, particularly in the use of their trailer fleet. It also provides registration agencies enough time to make the system changes required to facilitate the modified charges structure.

Impact on heavy vehicle operators

Under the recommended charges schedule, the fuel-based charge will increase by 1.367 cents per litre, or about 1.3 per cent. The increase will be implemented through a reduction in the fuel rebate from 18.51 cents per litre to 17.143 cents per litre.

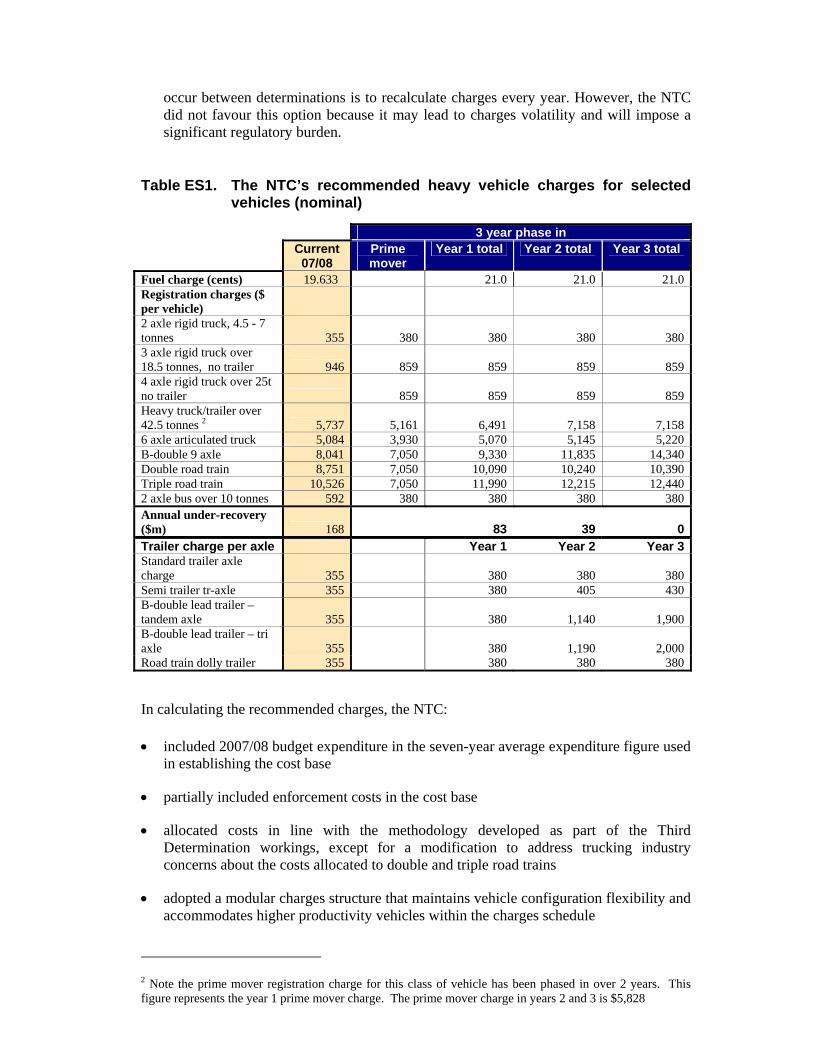

In addition, the registration charge for all vehicles and vehicle-trailer combinations will change. Around 25 per cent of vehicles will experience a decrease in their registration charge. The remaining 75 per cent of vehicles and 100 per cent of trailers will experience an increase in their registration charge.

These increases will have a direct impact on vehicle operating costs, but the impact will vary depending on a range of factors including heavy vehicle class and VKT. To illustrate the likely impact, the NTC modelled the average vehicle impacts within each heavy vehicle class. The results of this modelling for some key heavy vehicle types are shown in Table ES2.

Table ES2. Change in average vehicle operating costs for key vehicle types

Vehicle type 2007 average vehicle operating

costs $

Percentage change in

Year 1

Percentage change in

Year 2

Percentage change in

Year 3 2 axle rigid truck 4.5 to 7 tonnes (no trailer)

22,100 0.4 0.4 0.4

3 axle rigid truck over 18 tonnes (no trailer)

37,400 0.2 0.2 0.2

Heavy truck trailer over 42.5 tonnes

116,200 1.1 1.7 1.7

6 axle articulated truck 124,800 0.5 0.5 0.6 9 axle B-double 278,200 1.0 1.9 2.8 Double road train 252,200 1.0 1.1 1.1 Triple road train 301,300 1.0 1.0 1.1 Note: annual percentage changes are not cumulative

The table shows that a B-double with average vehicle class characteristics in terms of load and distance travelled per annum (179,000km) faces a rise of 2.8 per cent after charges are fully phased-in. However, a shorthaul B-double that travels around 120,000 kilometres per annum is likely to face a rise of 3.9 per cent, while a longhaul B-double that travels 240,000 kilometres per year will face a rise 2.3 per cent.

NTC has also recognised that different operators will be affected differently by this Determination. It has therefore undertaken a variety of case studies to understand the impacts on real operations. The impact of the Determination on the operations considered in the case studies did not exceed 2 per cent.

In line with the ATC’s request, the NTC also considered the substitution effects for vehicles with similar vehicle characteristics and carrying capacity that face different charges. It found that these effects are unlikely to be significant, because the recommended registration charges are more closely related to trailer type and capacity, and so there is closer alignment between vehicles of similar carrying capacity that are likely to be substitutes for each other. The NTC does not support locally based concessions aimed at discouraging substitution, as this would create incentives for vehicles in other jurisdictions to register their vehicles in the states/territories where the concessions exist.

Impacts on end users

The flow-through impact of the NTC’s recommended charges to consumer prices is difficult to assess, due to the lack of available information. However, the NTC estimated this impact on a trolley containing $100 worth of grocery items. If found that:

• For retail outlets dependent on B-doubles, the maximum additional cost per $100 trolley of goods would be 17 cents. This level of impact would occur in remote areas, and the impact in other areas would be less.

• For retail outlets dependent on road trains, the maximum impact would be an extra 7 cents per $100 trolley of goods in remote areas.3

The recommended charges may also have an impact on vehicles owned by primary producers. However, this impact is not expected to be significant, given that each government is able to, and generally does, provide concessions for primary producers of 40–50 per cent of heavy vehicle charges. NTC notes that primary producers using hire and reward operators will be more adversely affected.

The recommended charges will have impacts on small businesses, but on average they are not expected to be significant, particularly due to the low share of registration charges in annual vehicle operating costs.

Impact on government revenue

The recommended registration charges will lead to increases in the total revenue generated by these charges for each jurisdiction (see Table ES3), and mostly lead to increases in the revenue generated by registration charges for specific vehicle classes.

Table ES3 Registration revenue by jurisdiction $’000s (nominal)

State/Territory

Current revenue (2007/08)

Proposed revenue 2008/09

Proposed revenue 2009/10

Proposed revenue 2009/10

Percentage change in

revenue from current to 2009/10

NSW 150,313 150,144 159,228 166,778 11.0

Vic 171,433 172,147 185,841 197,894 15.4

Qld 146,881 149,445 160,107 169,816 15.6

SA 57,859 58,750 64,478 69,982 21.0

WA 86,169 87,452 90,940 94,113 9.2

Tas 14,940 14,864 15,726 16,503 10.5

NT 7,972 8,421 8,651 8,858 11.1

ACT 2,860 2,806 2,961 3,084 7.8

Total 638,428 644,030 687,933 727,028 13.9

The recommended fuel-based charge will increase the revenue generated by this charge from $1.146 billion to $1.226 billion – an increase of 6.9 per cent.

3 These estimates are based on averages, and consumer price impacts will vary depending on individual transport operator’s circumstances and the decisions made by individual retail outlets on cost mark-ups.

The NTC also considered the impact of the investment resulting from increased charges. In particular, it notes that the Monash University Accident Research Centre estimates that improved road investment (including shoulder sealing, audible edge lines, passing lanes and rest areas) will contribute at least 38 per cent of the total future reduction in heavy vehicle related road deaths and casualties under the current National Heavy Vehicle Safety Strategy, compared to 30 per cent from the effective use of speed limiters, 18 per cent from better fatigue management, 9 per cent from increased seatbelt use by heavy vehicle drivers and 5 per cent from safer heavy vehicles.

The next steps

ATC has stated this Determination will be implemented on 1 July 2008.

CONTENTS

1. INTRODUCTION ....................................................................................................1 1.1 The governmental directions leading to a new determination.....................................1 1.2 NTC’s role in developing heavy vehicle charges ........................................................2 1.3 Previous determinations .............................................................................................3 1.4 Developing the 2007 Heavy Vehicle Charges Determination .....................................4

2. WHAT IS THE PROBLEM .....................................................................................5 2.1 Heavy vehicle charges don’t recover heavy vehicle allocated

expenditure .................................................................................................................6 2.1.1 Increase in expenditure on roads..................................................................................6 2.1.2 Changes in the fleet numbers and usage ...................................................................10 2.1.3 The annual adjustment ...............................................................................................11 2.1.4 Impact on the level of cost recovery ...........................................................................11

2.2 Is it appropriate to recover enforcement costs through charges?.............................12 2.2.1 The principle for including enforcement costs.............................................................12 2.2.2 Getting a better outcome out of enforcement..............................................................13 2.2.3 Revenues association with enforcement.....................................................................14

2.3 Smoothing the variability in road expenditures .........................................................15 2.4 Developing charges for high-productivity vehicles....................................................16

3. THE OBJECTIVE .................................................................................................18 3.1.1 ATC approved pricing principles .................................................................................19 3.1.2 COAG requirements ...................................................................................................19 3.1.3 The considerations .....................................................................................................20

4. THE OPTIONS......................................................................................................22 4.1 Which years of expenditure should be averaged in determining the cost

base? ........................................................................................................................22 4.1.1 Option CB1: Include 2007/08 budget expenditure in the cost base ............................24 4.1.2 Option CB2: Include 2006/07 budget expenditure in the cost base ............................24

4.2 To what extent should enforcement costs be included in the cost base?.................25 4.2.1 Option a: Full inclusion of road agency enforcement costs .........................................26 4.2.2 Option b: Partial inclusion of road agency enforcement costs.....................................27 4.2.3 Option c: Full exclusion of enforcement costs.............................................................28 4.2.4 Comparing the impact of the options for enforcement costs .......................................29 4.2.5 A framework for enforcement .....................................................................................30

4.3 How should costs be allocated between vehicle classes? .......................................30 4.3.1 The importance of VKT in allocating costs..................................................................30 4.3.2 The reliability of road usage data................................................................................31

4.4 How should prices be set to fully recover heavy vehicle costs in aggregate and ensure all vehicle classes at least recover their attributable costs?.....................................................................................................31 4.4.1 Implications for B-doubles and road trains..................................................................32 4.4.2 Implications for vehicle flexibility and enforcement burden .........................................33 4.4.3 Option C1 ...................................................................................................................33 4.4.4 Option C2 ...................................................................................................................34 4.4.5 Option C3 ...................................................................................................................35

4.5 What charges should apply to high-productivity vehicles? .......................................38 4.5.1 Higher productivity vehicle charge formula .................................................................38 4.5.2 Modular approach to charges .....................................................................................41

4.6 Should charges under the 2007 Determination be phased in?.................................44 4.7 How should charges be adjusted annually? .............................................................47

4.7.1 Option A1: Maintain the current adjustment process with modifications and inclusion of fuel indexation...................................................................................48

4.7.2 Option A2: Option A1 with removal of the cap and floor ............................................48 4.7.3 Option A3: Indexation of both registration and fuel charges.......................................49 4.7.4 Option A4: Annual re-calculation of charges..............................................................50 4.7.5 Stakeholder comments on the options........................................................................50

5. ASSESSMENT OF POTENTIAL IMPACTS ....................................................... 54 5.1 Impact on fuel-based charge....................................................................................54 5.2 Impact on registration charge...................................................................................54

5.2.1 Impact on heavy vehicles ...........................................................................................54 5.2.2 Impact on jurisdictions’ registration revenue ...............................................................55

5.3 Impact on vehicle operating costs ............................................................................55 5.3.1 Impact on road user charges per net tonne kilometre.................................................57 5.3.2 Impact on the vehicle fleet ..........................................................................................58 5.3.3 Case studies of impact on operational costs...............................................................58

5.4 Impacts on industry production costs .......................................................................64 5.5 End user impacts......................................................................................................65

5.5.1 Impacts on the price of consumer goods ....................................................................65 5.5.2 Ability to pass on cost increases.................................................................................66 5.5.3 Impacts on primary producers ....................................................................................66 5.5.4 Impacts on small businesses......................................................................................67

5.6 Impacts on competition ............................................................................................67 5.7 Implications for government financing......................................................................68

5.7.1 The need for road investment .....................................................................................68 5.7.2 Charges contribution to road investment ....................................................................68

5.8 Impact of road investment on heavy vehicle productivity and safety........................69 5.8.1 Case studies of improved productivity ........................................................................69 5.8.2 Case studies of improved safety.................................................................................69

5.9 Potential productivity improvements.........................................................................70 5.9.1 COAG-endorsed NTC work program..........................................................................70 5.9.2 Targeted infrastructure improvements ........................................................................71 5.9.3 Other regulatory reforms.............................................................................................72

6. CONSULTATION................................................................................................. 73 6.1 The consultation process .........................................................................................73 6.2 Major issues raised and the NTC’s response...........................................................74

6.2.1 The treatment of enforcement costs ...........................................................................74 6.2.2 The methodology for estimating heavy vehicle charges revenue................................75 6.2.3 Estimation of the allocated cost base .........................................................................76 6.2.4 Impacts of differential multi-combination prime mover charges ..................................76 6.2.5 The inability of industry to pass on large increases in charges ...................................77 6.2.6 Concern over the adoption of the high-productivity vehicle formula ............................77 6.2.7 Need for productivity offsets by opening up the network more....................................78

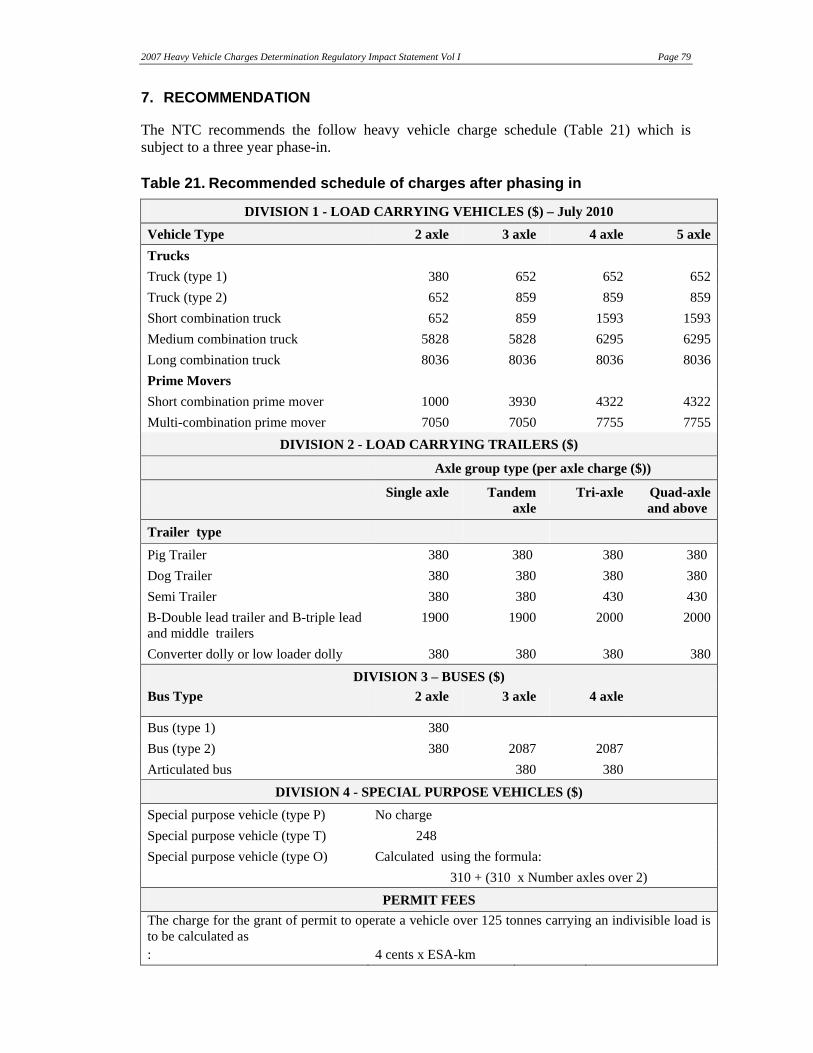

7. RECOMMENDATION .......................................................................................... 79 7.1 Recommended heavy vehicle charges ....................................................................80

7.1.1 Inclusion of 2007/08 budget expenditure in the cost base ..........................................82 7.1.2 Partial inclusion of enforcement costs in the cost base...............................................82 7.1.3 Allocation of costs.......................................................................................................82 7.1.4 Adoption of a revised charges structure......................................................................83 7.1.5 Adoption of a phase-in period of up to three years for registration charges ................83 7.1.6 Modification to the annual adjustment process ...........................................................84

7.2 Compliance issues ...................................................................................................85 7.3 Implementation issues..............................................................................................85 7.4 Legislative issues .....................................................................................................85

8. REFERENCES..................................................................................................... 87

9. GLOSSARY OF TERMS ..................................................................................... 89

LIST OF TABLES

Table 1. Total road construction and maintenance expenditure estimates ($2007/08m real terms)....................................................................................6

Table 2. Changes in fleet numbers since the Second Determination.....................10 Table 3. Heavy vehicle enforcement expenditure by state ......................................27 Table 4. Adjusted heavy vehicle enforcement expenditure by state ......................28 Table 5. Allocation of enforcement costs for each option ($/vehicle) ....................29 Table 6. Charges under Option C1 for select vehicles under different

enforcement scenarios .................................................................................34 Table 7. Charges under Option C2 for select vehicles under different

enforcement scenarios .................................................................................35 Table 8. Charges under Option C3 for select vehicles under different

enforcement scenarios .................................................................................36 Table 9. Modular charge components of higher productivity vehicles ..................42 Table 10. Registration charges for B-Triples and B-Doubles derived using the

different approaches .....................................................................................43 Table 11. Option C1 with a two or three year phase in of registration increases

(nominal) ........................................................................................................45 Table 12. Option C3 with a two year phase in of registration increases (nominal) .46 Table 13. Option C3 with a three year phase in of registration increases

(nominal) ........................................................................................................47 Table 14. Summary of stakeholder submission comments on options for annual

adjustment process.......................................................................................51 Table 15. Registration revenue by jurisdiction ($ ‘000s)............................................55 Table 16. All jurisdiction registration revenue by vehicle class ($ ‘000s) ................55 Table 17. Change in average vehicle operating costs for key vehicle types ...........56 Table 18. Changes in registration costs as a share of average vehicle operating

costs ...............................................................................................................57 Table 19. Changes in total heavy vehicle charges as a share of average vehicle

operating costs..............................................................................................57 Table 20. Impact on $100 worth of groceries (cents) .................................................66 Table 21. Recommended schedule of charges after phasing in ...............................79 Table 22. The NTC’s recommended heavy vehicle charges for selected vehicles

with phasing (nominal) .................................................................................81

LIST OF FIGURES

Figure 1. COAG road pricing reform plan.....................................................................2 Figure 2. Allocated arterial expenditure ($2007/08 real terms) ...................................7 Figure 3. Arterial, reported local and allocable local road expenditure

movements over the past seven years ($2007/08).......................................8 Figure 4. Forecast impact of the freight task on truck numbers ................................9 Figure 5. Growth in the total heavy fleet number since the Second

Determination ................................................................................................10 Figure 6. B-double under-recovery of fully allocated costs per vehicle (nominal).12 Figure 7. Process for developing, implementing and adjusting charges................22 Figure 8. Heavy vehicle allocated cost base ($nominal) ...........................................23 Figure 9. Application of charges under Option 3Cb to vehicles ..............................37 Figure 10. Comparison of changes in road expenditure to changes in RCMPI and

CPI (2000/01 = 100.0).....................................................................................50 Figure 11. Road user charges per net tonne kilometre (once fully implemented)....58 Figure 12. Case study 1: impact on vehicle operating cost shares ..........................59 Figure 13. Case study 2: impact on vehicle operating cost shares ..........................60 Figure 14. Case study 3: impact on vehicle operating cost shares ..........................61 Figure 15. Case study 4: impact on vehicle operating cost shares ..........................62 Figure 16. Case study 5: impact on vehicle operating cost shares ..........................63 Figure 17. Case study 6: impact on vehicle operating cost shares ..........................64

2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I Page 1

1. INTRODUCTION

1.1 The governmental directions leading to a new determination

In 2006 the Productivity Commission conducted an inquiry into Road and Rail Freight Infrastructure Pricing (PC Inquiry). As part of this inquiry, the Productivity Commission reviewed the methodology the National Transport Commission (NTC) uses to develop its recommendations on heavy vehicle charges. While the Productivity Commission identified some shortcomings and conservative assumptions in this methodology, it broadly endorsed the NTC’s approach.

Following this endorsement, the Australian Transport Council (ATC) directed the NTC to begin work on a new heavy vehicle charges determination, to replace the current Second Determination. The full direction is as follows:

(ATC) DIRECTED the NTC, having regard to the final report of the Productivity Commission and the deliberations of COAG on future pricing issues, to develop a Heavy Vehicle Pricing Determination that:

(i) considers the inclusion of heavy vehicle enforcement costs in the cost base; and

(ii) allows for incremental charging for higher productivity vehicles;

AGREED that its preferred timeframe for the delivery of a Heavy Vehicle Road Pricing Determination is mid 2007; and

DIRECTED the NTC to report to the next ATC meeting on a Heavy Vehicle Pricing Determination.4

On 13 April 2007, the Council of Australian Governments (COAG) outlined a road reform agenda, and endorsed the ATC directive for a new heavy vehicle charges determination as part of Phase 1 of this plan (see Figure 1).

4 Recorded in the draft minutes of the 13 October 2006 ATC meeting.

Page 2 2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I

Figure 1. COAG road pricing reform plan

At its May 2007 meeting, ATC reinforced its earlier direction and requested the NTC to begin preparing a Regulatory Impact Statement (RIS) so that a new determination could be implemented on 1 July 2008, in line with COAG’s timetable. The ATC clearly indicated that in preparing the RIS, the NTC should follow the pricing principles approved in 2004, and meet COAG’s requirement that the Determination “ensure ongoing delivery of aggregate cost-recovery and removal of cross-subsidisation across heavy vehicle classes” (COAG 2007).

1.2 NTC’s role in developing heavy vehicle charges

The NTC is responsible for recommending heavy vehicle charges to the ATC. This function is set out in the Inter-Governmental Agreement for Regulatory and Operational Reform in Road, Rail and Intermodal Transport (IGA), and is intended to ensure that nationally uniform charges are applied to heavy vehicles.

Clause 5.1 of the IGA sets out that one of the responsibilities and functions of the NTC is to:

(c) develop

(i) road use charging principles for Heavy Vehicles (until such time as the Council decides that another organisation should undertake this function);

(ii) Proposed Reforms in relation to Heavy Vehicle Road Use Charges based on charging principles agreed by the Council from time to time;

The IGA specifies that a:

End 2011

End 2014

Delivery of heavy vehicles Determination ⎪PBS and other agreed reforms

End 2009

Independent review of PAYGO and externalities

Feasibility study (incl. trials) on Incremental Pricing Scheme ⎪CSO Research

Evaluation of incremental pricing

Alternative institutional arrangements ⎪ Review of Road Freight Infra Regulation

Implementation of the result of Phase 1 and 2 work programs

Feasibility study of mass-distance location based charges

Implementation of the results of Phase 3 work programs

Phas

e 2

Phas

e 3

2007

Tim

elin

e fo

r ref

orm

National Guidelines for Transport System Management

Phas

e 1

2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I Page 3

Road Use Charge means a fee for payment for use of the road system, which in the case of a Heavy Vehicle, does not include: - a nominal or other administration charge associated with registration of a

vehicle; - stamp duties; - compulsory third party insurance premiums; - injury protection charges; and - administrative components of permit, licence or other fees.

In addition, the IGA makes it clear that heavy vehicle charges must apply uniformly in all jurisdictions. This is intended to stop heavy vehicle operators ‘shopping around’ for the jurisdiction with the lowest registration charges (which would distort price signals within the market) and to ensure that all heavy vehicles pay their allocated share of road expenditure.

In developing its recommended heavy vehicle charges, the NTC assesses the level and types of expenditure on roads, assesses the usage of roads by different vehicle classes, and consults with stakeholders. The ATC considers the NTC’s recommended heavy vehicle charges, and determines whether or not to approve them. If a majority of its members approves the recommendations, governments in all jurisdictions are obliged to implement them.

1.3 Previous determinations

The First Heavy Vehicle Charges Determination was approved in 1992 and implemented between July 1995 and October 1996. The Second Determination was approved in 2000 and implemented between July 2000 and December 2000. Both these determinations resulted in the implementation of charges with two components: a fuel-based component designed to recover two-thirds of costs, and an annual registration component to recover the remaining third.

After the Second Determination, an annual adjustment process was introduced. This process updates the registration charge component only, and does not account for changes in road use between vehicle categories or changes in the type of road works undertaken. It is subject to a maximum annual rise no greater than the change in the Consumer Price Index (CPI) and a floor applies so that annual registration charges cannot be reduced. There have been six annual adjustments to date.

The fuel-based road charge component is currently 20c/litre, and has not been reviewed since the Second Determination was implemented. Due to indexation of the diesel rebate coupled with the freezing of the fuel excise the effective rate has fallen to 19.633c/litre.

The First and Second Determinations sought to achieve a number of policy objectives. Their primary objective was to ensure that, in aggregate, heavy vehicle charges fully recover the expenditure on roads allocated to heavy vehicles. However, policy decisions in relation to the relative size of the fuel-based and registration charge components, the promotion of newer and safer vehicles, and simplicity in charges have meant that in most years the charges in aggregate over-recovered costs, while the charges for some vehicle classes did not recover their share of expenditure.

The recent PC Inquiry and COAG direction have lead to a new policy focus. The primary objective remains to ensure that heavy vehicle charges in aggregate achieve cost recovery.

Page 4 2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I

In addition, all vehicle classes should recover their attributable (or marginal) costs so that there is no cross-subsidisation between vehicles classes.

1.4 Developing the 2007 Heavy Vehicle Charges Determination

In 2006, the NTC put forward recommendations for a Third Determination. In reaching these recommendations, it undertook extensive consultation and released several reports that documented the technical underpinning of the Determination models and the changes made to these models since the Second Determination.

The ATC did not approve the Third Determination, but requested the NTC to begin work on a 2007 Determination in response to the PC Inquiry and COAG direction. In doing so, the NTC has built on some of the workings for the Third Determination, rather than duplicating this work. For example, it largely used the same methodology for assessing the cost base and allocating costs as it used in developing its recommendations for the Third Determination.5

In July 2007, the NTC released a draft RIS that outlined its preferred option for heavy vehicle charges. This option met the minimum COAG and ATC requirements that each vehicle class at least recover its attributable costs and that heavy vehicles in aggregate fully recover their allocated costs. It then completed comprehensive public consultation on the draft RIS, and considered the comments and issues raised by stakeholders.

As a result of this process, the NTC revised its preferred option. It then undertook further consultation with industry, interested parties and government before finalising its recommendations and preparing this final RIS.

5 Throughout this RIS, the NTC will refer to documents prepared for the Third Determination where appropriate, and identify any continuing concerns raised by stakeholders and detail any further changes since those reports were released.

2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I Page 5

2. WHAT IS THE PROBLEM

In recent years government spending on road infrastructure has increased. Whilst road usage of the heavy vehicle fleet has also increased, the increase in the overall fleet size has been relatively small. As a result of these changes, heavy vehicle charges in aggregate no longer recover heavy vehicle allocated expenditure, and the charges for some heavy vehicle classes do not recover these vehicles’ attributable expenditure. This is the primary problem that the 2007 Heavy Vehicle Charges Determination needs to address.

There are also several secondary problems that need to be addressed:

• The NTC has been asked to consider whether it would be appropriate to recover costs associated with enforcing laws relevant to heavy vehicles through heavy vehicle charges.

• The NTC has identified that the current practice of calculating the cost base to be recovered through heavy vehicle charges by averaging three years of road expenditure may not sufficiently smooth out the year-to-year variability in this expenditure. In addition, it has been asked to consider the feasibility of including budget expenditure for 2007/08 in calculating the cost base.

• The NTC has been asked to develop charges for the new generation of high-productivity vehicles.

• The NTC has been asked to consider whether the new charges should be phased in, in recognition of the fact that moving to charges that ensure all vehicle classes at least recover their attributable expenditure may result in significant increases in charges for some vehicle classes.

The sections below discuss these problems in more detail. Box 1 defines some of the key terms used in these sections.

Box 1: Definition of key terms

It is important to understand some of the terminology used to describe how the charges are calculated. The key terms are:

Total expenditure: This includes all road expenditure by all levels of government including local government, state/territories and Auslink.

Allocable expenditure: This is the total pool of expenditure after a certain percentage of local road expenditure, which is already recovered through rates, has been deducted.

Allocated expenditure: This is the allocable expenditure distributed across the various classes or groups. This report will generally refer to heavy vehicle allocated expenditure, which is the share of allocable expenditure recovered by all vehicles over 4.5 tonnes. Total allocated expenditure equals allocable expenditure.

Attributable expenditure: This is the expenditure related to the provision and maintenance of roads and which varies depending on the use of the road system by different types of vehicles. It is equivalent to the long run marginal cost and therefore includes capital as well as operational costs. These costs are directly attributable to vehicle types.

Common costs: These are costs that are not attributed to particular use and include such things as signage and expenditure related to the impact of weathering on the roads. These costs are also often referred to as non-attributable expenditure.

Page 6 2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I

2.1 Heavy vehicle charges don’t recover heavy vehicle allocated expenditure

The charges under the Second Determination were calibrated to ensure that at minimum, they recovered historic heavy vehicle allocated expenditure. In 2000, these charges over-recovered this historic expenditure by $140m in nominal terms. However, this situation has reversed, and the charges now under-recover this expenditure. The primary reasons are that expenditure has increased at a greater rate than fleet growth, and the annual adjustment has not been able to keep pace with the increase in expenditure because it is subject to a CPI cap.

2.1.1 Increase in expenditure on roads

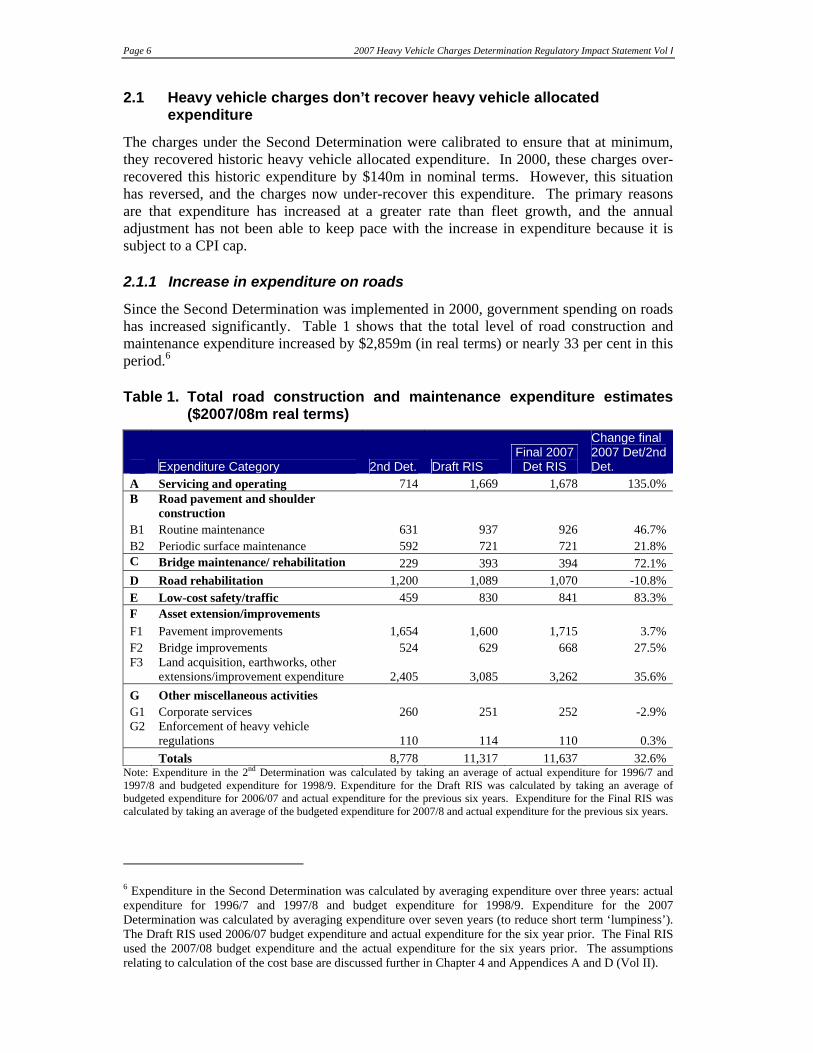

Since the Second Determination was implemented in 2000, government spending on roads has increased significantly. Table 1 shows that the total level of road construction and maintenance expenditure increased by $2,859m (in real terms) or nearly 33 per cent in this period.6

Table 1. Total road construction and maintenance expenditure estimates ($2007/08m real terms)

Expenditure Category 2nd Det. Draft RIS Final 2007

Det RIS

Change final 2007 Det/2nd Det.

A Servicing and operating 714 1,669 1,678 135.0% B Road pavement and shoulder

construction B1 Routine maintenance 631 937 926 46.7% B2 Periodic surface maintenance 592 721 721 21.8% C Bridge maintenance/ rehabilitation 229 393 394 72.1% D Road rehabilitation 1,200 1,089 1,070 -10.8% E Low-cost safety/traffic 459 830 841 83.3% F Asset extension/improvements F1 Pavement improvements 1,654 1,600 1,715 3.7% F2 Bridge improvements 524 629 668 27.5% F3 Land acquisition, earthworks, other

extensions/improvement expenditure 2,405 3,085 3,262 35.6% G Other miscellaneous activities G1 Corporate services 260 251 252 -2.9% G2 Enforcement of heavy vehicle

regulations 110 114 110 0.3% Totals 8,778 11,317 11,637 32.6%

Note: Expenditure in the 2nd Determination was calculated by taking an average of actual expenditure for 1996/7 and 1997/8 and budgeted expenditure for 1998/9. Expenditure for the Draft RIS was calculated by taking an average of budgeted expenditure for 2006/07 and actual expenditure for the previous six years. Expenditure for the Final RIS was calculated by taking an average of the budgeted expenditure for 2007/8 and actual expenditure for the previous six years.

6 Expenditure in the Second Determination was calculated by averaging expenditure over three years: actual expenditure for 1996/7 and 1997/8 and budget expenditure for 1998/9. Expenditure for the 2007 Determination was calculated by averaging expenditure over seven years (to reduce short term ‘lumpiness’). The Draft RIS used 2006/07 budget expenditure and actual expenditure for the six year prior. The Final RIS used the 2007/08 budget expenditure and the actual expenditure for the six years prior. The assumptions relating to calculation of the cost base are discussed further in Chapter 4 and Appendices A and D (Vol II).

2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I Page 7

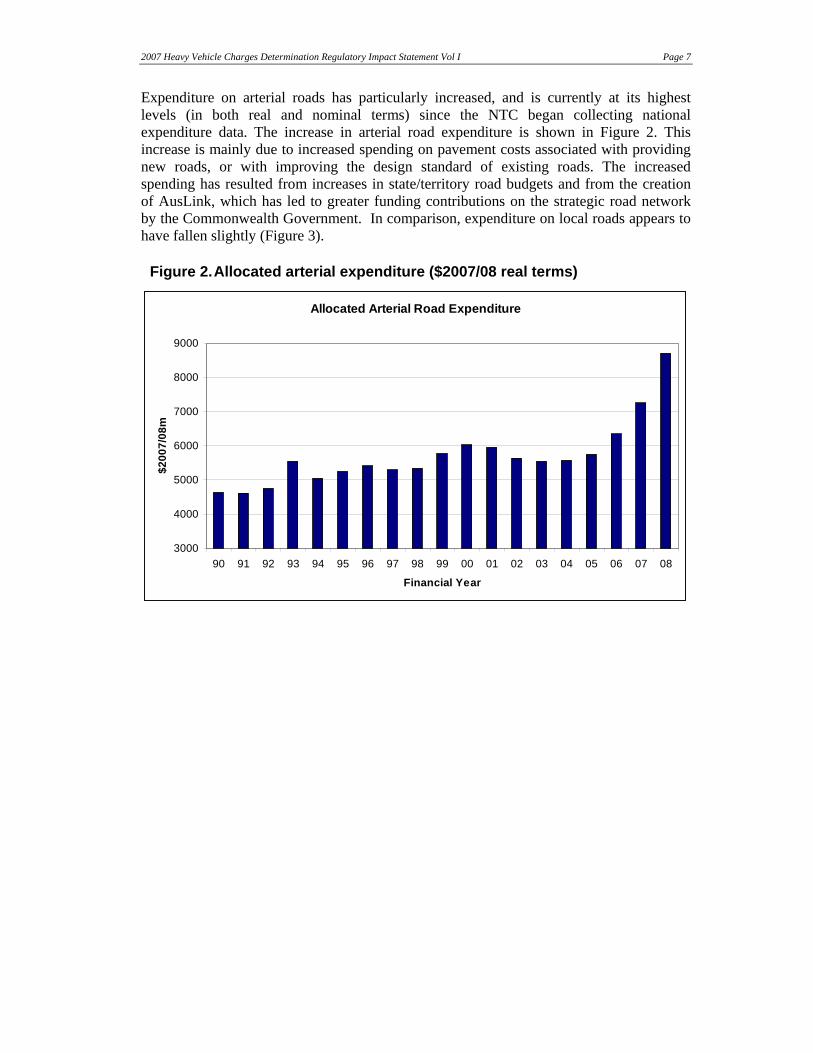

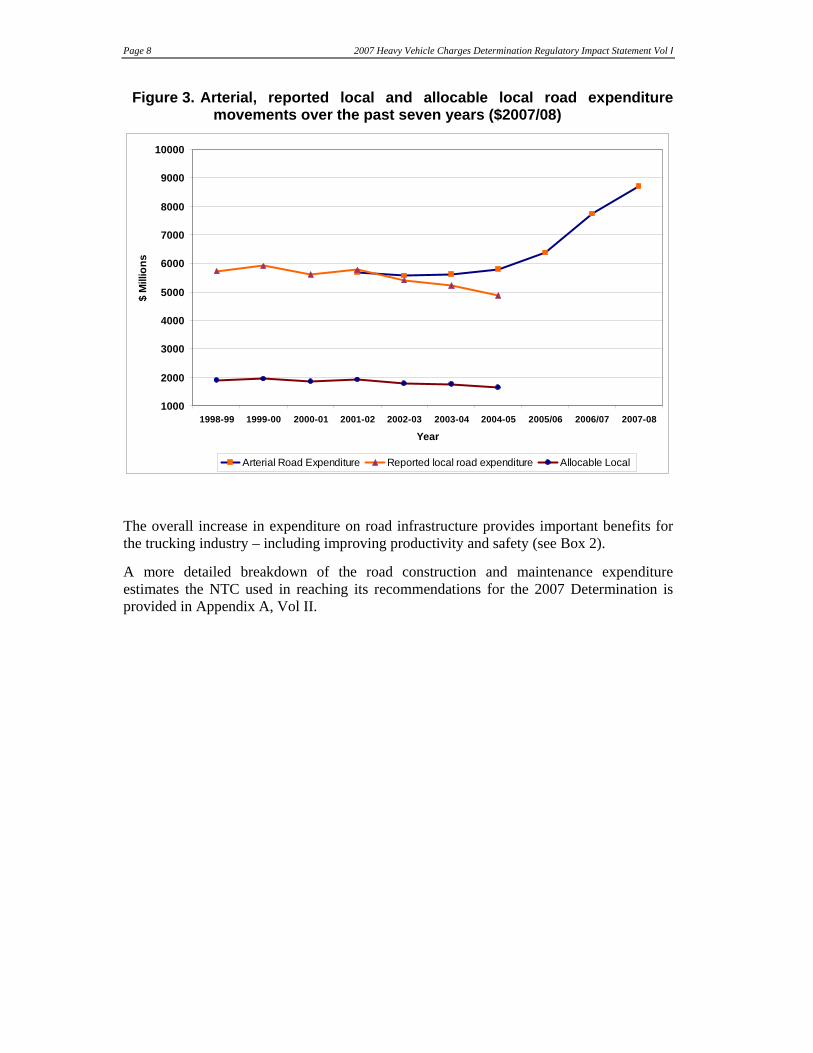

Expenditure on arterial roads has particularly increased, and is currently at its highest levels (in both real and nominal terms) since the NTC began collecting national expenditure data. The increase in arterial road expenditure is shown in Figure 2. This increase is mainly due to increased spending on pavement costs associated with providing new roads, or with improving the design standard of existing roads. The increased spending has resulted from increases in state/territory road budgets and from the creation of AusLink, which has led to greater funding contributions on the strategic road network by the Commonwealth Government. In comparison, expenditure on local roads appears to have fallen slightly (Figure 3).

Figure 2. Allocated arterial expenditure ($2007/08 real terms)

Allocated Arterial Road Expenditure

3000

4000

5000

6000

7000

8000

9000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Financial Year

$200

7/08

m

Page 8 2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I

Figure 3. Arterial, reported local and allocable local road expenditure movements over the past seven years ($2007/08)

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005/06 2006/07 2007-08

Year

$ M

illio

ns

Arterial Road Expenditure Reported local road expenditure Allocable Local

The overall increase in expenditure on road infrastructure provides important benefits for the trucking industry – including improving productivity and safety (see Box 2).

A more detailed breakdown of the road construction and maintenance expenditure estimates the NTC used in reaching its recommendations for the 2007 Determination is provided in Appendix A, Vol II.

2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I Page 9

Box 2. Link between road investments and productivity and safety There is a strong link between increased investment in the road network and improving the productivity and safety of heavy vehicles – and pricing reform plays a key role in enabling this investment.

The NTC’s Twice The Task report (February 2006) highlighted the importance of pricing reform for enabling continuing productivity and safety improvements to address the growing freight task (Figure 4).

Figure 4. Forecast impact of the freight task on truck numbers

The transport reform option (2020) is based on improved access for more productive heavy vehicles through more flexible regulations, pricing reform and infrastructure investment.

Source: Twice The Task (NTC/BTRE 2006)

COAG’s National Reform Agenda (10 February 2006) for quad axle groups, B-triples and Performance Based Standards involves significant infrastructure investment to improve access for this ‘new generation’ of high-productivity heavy vehicles. An Australian Industry Group survey (Transport & Logistics Operations in Australian Manufacturing 2006) also found that better infrastructure plays an important role in reducing general transport costs. Heavy vehicle charges can contribute to freight link upgrades, removing bottlenecks and reducing logistics costs for exports.

An international heavy vehicle road safety benchmarking study commissioned by the NTC in 2002 highlighted the important role of better roads on truck safety. It concluded that:

… if Australian roads were upgraded to having similar proportions of divided and limited access roads, as in the United States or Great Britain, the Australian truck fatality rate could be expected to be similar to that in these countries … upgrading of the Australian road system to these standards … require(s) significant investment.

The National Road Safety Strategy also concludes that improving the safety of roads is the single most significant achievable factor in reducing road trauma. The research shows improving the safety of the roads could save 332 lives a year – almost half of the national target.

Page 10 2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I

2.1.2 Changes in the fleet numbers and usage

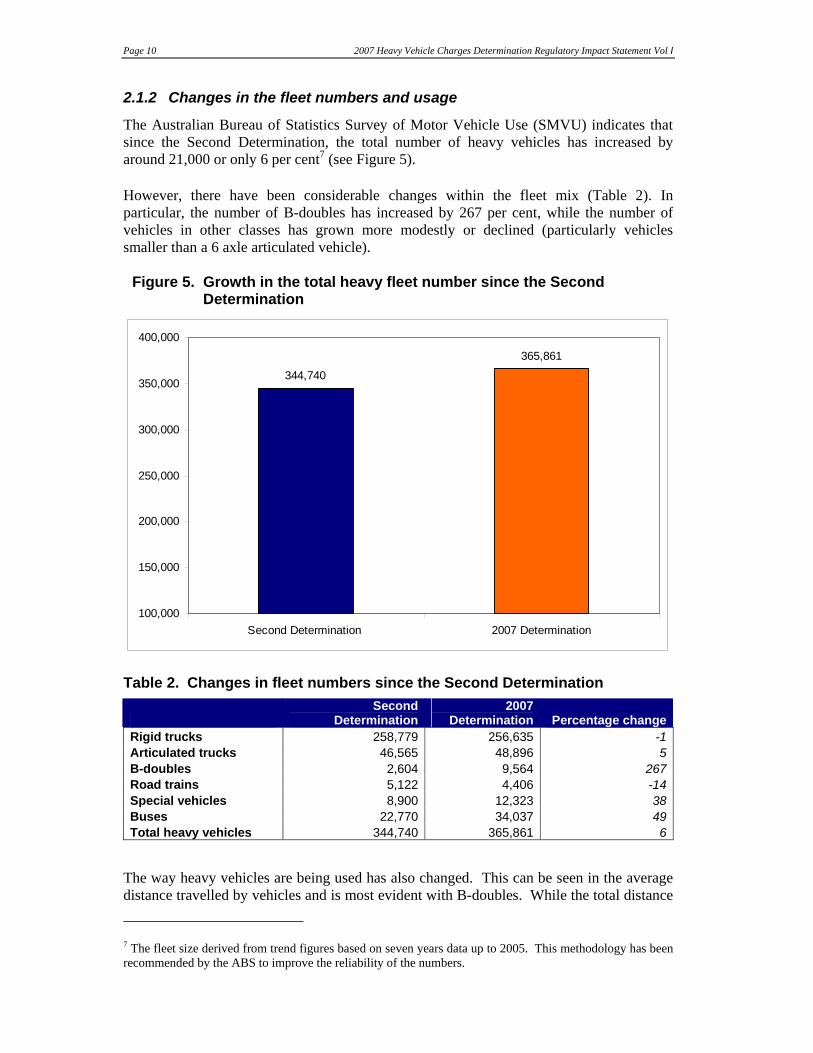

The Australian Bureau of Statistics Survey of Motor Vehicle Use (SMVU) indicates that since the Second Determination, the total number of heavy vehicles has increased by around 21,000 or only 6 per cent7 (see Figure 5).

However, there have been considerable changes within the fleet mix (Table 2). In particular, the number of B-doubles has increased by 267 per cent, while the number of vehicles in other classes has grown more modestly or declined (particularly vehicles smaller than a 6 axle articulated vehicle).

Figure 5. Growth in the total heavy fleet number since the Second Determination

344,740

365,861

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Second Determination 2007 Determination

Table 2. Changes in fleet numbers since the Second Determination

Second

Determination 2007

Determination Percentage change Rigid trucks 258,779 256,635 -1 Articulated trucks 46,565 48,896 5 B-doubles 2,604 9,564 267 Road trains 5,122 4,406 -14 Special vehicles 8,900 12,323 38 Buses 22,770 34,037 49 Total heavy vehicles 344,740 365,861 6

The way heavy vehicles are being used has also changed. This can be seen in the average distance travelled by vehicles and is most evident with B-doubles. While the total distance

7 The fleet size derived from trend figures based on seven years data up to 2005. This methodology has been recommended by the ABS to improve the reliability of the numbers.

2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I Page 11

travelled by vehicles in this class has increased from 562 million kilometres per annum to 1,687 million kilometres, the average distance travelled per trip has fallen by 18 per cent. This suggests that these larger, safer and more productive vehicles are being used more widely than for long haul trips. This may reflect the fact that these vehicles have broader network access and that heavy vehicle operators are changing their asset utilisation, to improve productivity and safety in urban areas with safer vehicles.

2.1.3 The annual adjustment

Since the Second Determination, an automatic annual adjustment has applied to heavy vehicle charges. The adjustment enables these charges to increase between determinations to reflect nominal changes in heavy vehicle allocated expenditure while taking into account changes in the overall fleet size. However, the adjustment applies only to the annual registration component of heavy vehicle charges, and is subject to a floor of current charges and a CPI cap. In addition, it does not take into account changes in road use between vehicle categories.

These shortcomings mean that the annual adjustment does not enable ongoing full cost recovery of road expenditure between determinations. For example, the CPI cap means that annual adjustment does not adequately accommodate increases in expenditure greater than the cost of general inflation (due to increased construction activity or higher than CPI increases in construction costs). In addition, because the adjustment does not apply to the fuel-based component, it only partly indexes heavy vehicle charges to expenditures.

In recognition of these shortcomings, COAG has asked ATC to instruct the NTC to amend the adjustment approach to enable continued full cost recovery in aggregate and for each vehicle class between determinations.

2.1.4 Impact on the level of cost recovery

The NTC has calculated that in 2007/08 heavy vehicles in aggregate under-recover heavy vehicle allocated expenditure by $168m. This figure was calculated using trend 2005 fleet numbers based on seven years of trend data over the 1999 to 2005 period, compared to road expenditure data based on the latest available seven year averages.8 This methodology eliminates any lumpiness in the data and provides a consistent basis for comparison.9

The under-recovery has arisen because of the increase in expenditure, and the change in fleet mix and the fact that not all vehicle classes are recovering their fully allocated and attributable costs. In particular, B-doubles significantly under-recover both their fully allocated and attributable costs. Therefore, a disproportionate growth in these vehicles since the Second Determination means that as a class, they under-recover to a greater extent than they did in 2000 (see Figure 6).

8 The period for arterial expenditure is 2001/02 – 2007/08 and the period for local government expenditure is 1998/99 – 2004/05 9 The methodology for calculating the level of charges recovery is detailed in Appendix C

Page 12 2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I

Figure 6. B-double under-recovery of fully allocated costs per vehicle (nominal)

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

Second Determination Current

Common costAttributable

The PC Inquiry considered this issue. It found that vehicles that recovered their attributable (long run marginal) costs, but not their fully allocated costs (including common costs), were still paying their way. The implication of this finding is that all heavy vehicle classes should at least recover their attributable costs.

2.2 Is it appropriate to recover enforcement costs through charges?

The ATC has directed the NTC to consider including enforcement costs in the cost base to be recovered through heavy vehicle charges. When looking to include a new cost category to a charging framework it is important to understand how that cost compares with other costs, to determine the appropriateness of including the cost at all.

2.2.1 The principle for including enforcement costs

The ATC direction requires that NTC consider whether, and to what extent, it is appropriate to recover enforcement costs. To answer this, it is important to consider the role of enforcement and the associated outcomes.

Enforcement costs means the costs involved in ensuring that heavy vehicles comply with laws associated with their access to the road network. The most relevant laws relate to safety (e.g., prevention of driver fatigue and speeding) and mass (e.g. constraints on loading):

• The objective of safety-related laws is to ensure that granting heavy vehicles access to the network does not impose additional, unwarranted safety-related costs on the community. They recognise that there may be short-term commercial incentives on heavy vehicle operators to operate in an unsafe way in order to reduce costs. They also

$8,400

$16,032

2007 Heavy Vehicle Charges Determination Regulatory Impact Statement Vol I Page 13

recognise that incidents involving heavy vehicles are likely to result in higher safety-related costs than those involving only light vehicles.

• Laws related to mass recognise the relationship between heavy vehicle road use and infrastructure cost by providing a mass limit on vehicles. Enforcement helps to ensure those mass limits are not breached. Therefore, it prevents additional costs associated with infrastructure provision which may be inefficient in terms of the amount of the cost and who bears it.

In the NTC’s view, heavy vehicles are required to recover costs associated with heavy vehicle access to the road network, to ensure efficient outcomes in the transportation of freight. Enforcement is similarly associated with heavy vehicle access and seeks to ensure efficient outcomes. Therefore, in principle, it is an appropriate cost to be recovered through charges.

This view is supported by the findings of the Productivity Commission, which also looked into this issue as part of its Inquiry. The Productivity Commission found that:

“The costs of enforcing heavy vehicle mass and speed restrictions are appropriately recovered through road user charges. However the inclusion of these costs is not likely to have a significant effect on heavy vehicle charges.” (PC 2007)

It noted that other countries recover heavy vehicle policing costs in road charges.

The NTC sought constitutional advice on the legality of recovering enforcement costs. This advice confirmed that there is no legal constraint to recovering enforcement costs, and referred to an analogous case of Airservices Australia v Canadian Airlines International Ltd (1999) 202 CLR 133 which was heard in the High Court. In this case McHugh J stated:

“[I]n my opinion, in characterising a charge as a fee for services …, it is legitimate to take account of the changing circumstances of government which are exemplified by the devolving of functions from government departments to statutory authorities or other corporate bodies which, under the terms of their enabling statutes, have a monopoly on the provision of a certain service and are directed by the legislature to provide those services on a ‘user pays’ basis. Charges by such authorities and bodies should be seen as essentially cost driven, imposed on users for the purpose of reimbursing the cost of services provided. They should not be approached as if they were imposed simply to raise revenue for the general government of the country.”

The extent to which enforcement costs should be recovered through heavy vehicle charges is discussed in Chapter 4.

2.2.2 Getting a better outcome out of enforcement

As the growing freight task places more pressure on the trucking industry, enforcement has become an increasingly important issue, for both government and the industry. During the consultation process, stakeholders put the view that a holistic approach to enforcement should be taken: that a broad framework is needed to strengthen enforcement and to ensure it is targeted and more consistent.