Embed Size (px)

Citation preview

OSTRICH INDUSTRY JUNE 2009

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

Telephone: 044 272 2210

Fax: 044 272 3337

Email: [email protected]

This document has been compiled by the South African Ostrich Business

Chamber Biodiversity Unit in collaboration with all the Project

Partners

LONG TERM BIODIVERSILONG TERM BIODIVERSILONG TERM BIODIVERSILONG TERM BIODIVERSITY TY TY TY

MANAGEMENT STRATEGY MANAGEMENT STRATEGY MANAGEMENT STRATEGY MANAGEMENT STRATEGY FOR THE FOR THE FOR THE FOR THE

SOUTH AFRICASOUTH AFRICASOUTH AFRICASOUTH AFRICANNNN

OSTRICH INDUSTRY OSTRICH INDUSTRY OSTRICH INDUSTRY OSTRICH INDUSTRY

THE OSTRICH INDUSTRY RECOGNISES AND

SAFEGUARDS THE UNIQUE BIODIVERSITY OF THE

KLEIN KAROO AND SUPPORTS SUSTAINABLE

FARMING METHODOLOGIES THAT STRIVE TO

BALANCE UTILISATION AND CONSERVATION

THROUGH IMPROVED VELD MANAGEMENT,

REHABILITATION WHERE APPROPRIATE, CLIMATE

CHANGE ADAPTATION AND SOUND RESEARCH IN

ORDER TO MAINTAIN ITS WORLD LEADER STATUS

The ostrich industry in the Klein Karoo supports a

process whereby producers will, by 2019, decrease

their impact on the biodiversity through improved

veld management and restoration, whilst pursuing

increased production based on sound research to

retain and expand international and local markets.

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

a

TABLE OF CONTENTS

LIST OF ACRONYMNS, PARTNERS, ACKNOWLEDGEMENTS ...............1

INTRODUCTION – SUMMARY....................................................................2

BACKGROUND............................................................................................3

SECTION A: DESCRIPTION OF THE BIODIVERSITY IMPORTANCE OF THE KLEIN KAROO, ECONOMIC IMPORTANCE OF THE OSTRICH INDUSTRY IN THE KLEIN KAROO, VISION AND OVERALL MANAGEMENT OBJECTIVES ....................................................................5

1. BIODIVERSITY IMPORTANCE OF THE KLEIN KAROO.....................5

2. ECONOMIC IMPORTANCE OF THE OSTRICH INDUSTRY IN THE

KLEIN KAROO......................................................................................7

2.1 BRIEF HISTORY OF THE INDUSTRY ..........................................7

2.2 SOCIO-ECONOMIC SITUATION IN THE KLEIN KAROO.............7

2.3 KLEIN KAROO REGIONAL ECONOMY........................................8

2.3.1 Regional Output ......................................................................8

2.3.2 Agriculture’s Importance to Regional Employment .................8

2.3.3 The Ostrich Industry’s Dominant Role in Klein Karoo Agriculture...............................................................................8

3. MAKING AN ECONOMIC CASE FOR PEN BREEDING AS ONE

ALTERNATIVE OVER FLOCK BREEDING..........................................9

3.1 THE ECONOMICS OF OSTRICH PEN-BREEDING......................9

3.1.1 Pen Breeding ..........................................................................9

3.1.2 Pen Breeding Cost..................................................................9

3.1.3 Economic Benefits of Pen-Breeding .......................................9

3.1.4 The Economics of “Tropparing” and Pen-Breeding Compared …………………………………………………………………….10

4. CURRENT SITUATION: OSTRICHES IN THE KLEIN KAROO.........11

4.1 THE FOOTPRINT OF THE OSTRICH INDUSTY ........................11

4.1.1 History...................................................................................11

4.1.2 Current..................................................................................11

4.1.3 Prospects..............................................................................12

4.1.4 Markets .................................................................................12

5. CURRENT SITUATION: BIODIVERSITY STATUS OF THE KLEIN

KAROO ...............................................................................................14

5.1 MAP OF ENDANGERED VEGETATION REMNANTS................14

5.2 CONSERVATION STATUS .........................................................14

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

b

6. MISSION AND VISION – Working Towards a Win-Win Situation .......16

7. OVERALL MANAGEMENT PRINCIPLES...........................................17

SECTION B: IMPLEMENTATION .............................................................18

8. OBJECTIVES......................................................................................18

8.1 OBJECTIVE 1: Ostrich farmers in the Klein Karoo are improving

management of sensitive and endangered veld as well as their ostrich production.........................................................................18

8.2 OBJECTIVE 2: A sustainable biodiversity unit for the ostrich industry in the Klein Karoo has been established and is working effectively by means of an integrated approach to Biodiversity Management, compliance and sustainable funding .....................19

8.3 OBJECTIVE 3: The Ostrich Industry has developed a climate change mitigation and adaptation strategy which is mainstreamed into the “best practice guidelines” ................................................19

8.4 OBJECTIVE 4: The ostrich industry has created an enabling environment for and is supporting research that supports biodiversity conservation and improved production .....................19

9. METHODOLOGY................................................................................20

9.1 BIODIVERSITY UNIT...................................................................20

9.1.1 Main functions of the Biodiversity Unit ..................................20

9.1.2 Staffing of the BU..................................................................21

9.1.3 Capacity Building and Training .............................................21

9.1.4 Data Capturing......................................................................21

9.1.5 Liaison and Awareness Raising............................................21

9.1.6 Provision of Services ............................................................22

9.1.7 Ostrich Standards / “Best Practice” Guidelines.....................22

9.1.8 Monitoring and Compliance ..................................................22

9.1.9 Rehabilitation ........................................................................22

9.1.10 Implementing Authority .........................................................23

9.1.11 Potential Funding..................................................................23

SECTION C: ALTERNATIVES TO FLOCK BREEDING .........................25

SECTION D: SUMMARY BUDGET FOR ESTABLISHING A BIODIVERSITY UNIT FOR THE OSTRICH INDUSTRY .........................25

SECTION E: ADDENDUMS.......................................................................26

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

1

LIST OF ACRONYMNS, PARTNERS, ACKNOWLEDGEMENTS

LIST OF ACRONYMS

AZEF Arid Zone Ecological Forum

BU Biodiversity Unit

BWI Biodiversity and Wine Initiative

CAPE Cape Action for People and the Environment

CEPF Critical Ecosystem Partnership Fund

CFR Cape Floristic Region

CN CapeNature

DEA&DP Department of Environmental Affairs and Development Planning

DEAT Department of Environmental Affairs and Tourism (National)

FF Fynbos Forum

GAP Good Agricultural Practise

GIS Geographical Information System

KKG Klein Karoo Group

M & E Monitoring and Evaluation

MoU Memorandum of Understanding

NDA National Department of Agriculture

NOPSA National Ostrich Processors of South Africa

NSPCA National

OIBMP Ostrich Industry Biodiversity Management Project

PMT Project Management Team

SA South Africa

SAOBC South African Ostrich Business Chamber

SAOPO South African Ostrich Producers Organisation

SKEP Succulent Karoo Ecosystem Profile

SK Succulent Karoo

TOR Terms of Reference

WC Western Cape

WHS World Heritage Site

LIST OF PARTNERS

CN CapeNature

DEA&DP Department of Environmental Affairs and Development Planning

NDA National Department of Agriculture

NOPSA National Ostrich Processors of South Africa

SAOBC South African Ostrich Business Chamber

SAOPO South African Ostrich Producers Organisation

ACKNOWLEDGEMENTS

OIBMP unit of the SAOBC OIMBP Biodiversity Working Group Working group for long term management document Sandveld Potato Project Rooibos Tea Project Biodiversity and Wine Initiative (BWI) Title page photo:

Date March 2009

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

2

INTRODUCTION – SUMMARY

This strategy is a direct result of the “Ostrich Industry Biodiversity Management Project” (OIBMP), a project that was funded by the Critical Ecosystem Partnership Fund (CEPF) with the aim to (i.a.) initiate a process whereby ostrich farmers in the Klein Karoo are encouraged to engage in improved veld management in the sensitive, fragile Succulent Karoo, with a number of critically endangered and endangered vegetation types. This project has confirmed that there is a need, from the industry’s side, for a biodiversity component/unit within or for the ostrich industry. This document aims to provide a pro-active road map for the industry to ensure that ostrich farmers in the Klein Karoo safeguard the unique biodiversity of the Klein Karoo, whilst. maintaining a sustainable production system. The purpose of the strategy is to identify ways of getting to this aim – identifying the strategic focus and anticipated outcomes. This plan will provide the SAOBC with useful guidelines regarding the strategic approach in pursuing the vision (see p16). SECTION A involves the description of the economic importance of the ostrich industry to the Klein Karoo region, as well as the biodiversity importance of the same region. It will also give an “economic case” for pen breeding as one of the preferred breeding methodologies, as well as overall management objectives related to the vision. SECTION B deals specifically with the implementation of these management objectives through various activities/projects and management actions (as well as the relevant party responsible for these). SECTION C addresses alternative strategies to be researched and investigated to achieve the aim and vision of maintaining biodiversity within a sustainable production system. SECTION D provides a summary budget for establishing a Biodiversity Unit for the Ostrich Industry, based on the detail provided in Section B. SECTION E contains the appendices mentioned in the strategic plan, providing additional information. All information used in this document is based on the biodiversity of the area, as well as the economic importance of the ostrich industry to the region. It aims to balance utilisation and conservation, specifically in the highly sensitive Succulent Karoo with its associated endangered vegetation. This document is particularly aimed at: � SAOBC Board of Directors � SA and WC Ostrich Producers Associations � Ostrich Industry in the Klein Karoo, particularly KKG and Mosstrich � Ostrich Marketers � Potential funders

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

3

BACKGROUND

Ostrich production consists of a number of production functions including breeding, hatching, chick-raising, and growing of ostriches to slaughter weight. It is only the breeding function that makes use of the veld, where "tropparing" involves flocks of breeding birds being kept in veld camps, where they are fed complete rations and provided with water, and where eggs are also collected for incubation. Breeding can last for 8 months after which birds have a 4-month rest period. A detailed vegetation degradation assessment of the Klein Karoo indicates that poor grazing practices have resulted in 28.2% of the region having been severely transformed, 60.1% moderately transformed, with only 1.8% described as pristine (Thompson et al. 2005). In some studies it was found to be ostrich veld-based breeding that has caused some of this severe transformation and degradation of the vegetation (Hoffman 1996; Cupido 2005) Much of this degradation is attributable to feeding activities and territorial behaviour of ostriches where it is the trampling that leads to soil compaction, the removal of the biological soil crust (Cupido 2005), which increases the risk of soil erosion by wind (Belnap 2001), destruction of sensitive plants and loss of biodiversity (Lombard & Wolf 2004; Cupido 2005). Little, if any, feed benefit exists in breeding ostriches on the severely to moderately transformed veld. The Succulent Karoo, the Fynbos biome (which is part of the Cape Floristic Region) and the Subtropical Thicket Biome are internationally recognised biodiversity hotspots. Safeguarding this unique biodiversity in the ostrich producing areas of the Klein Karoo, whilst ensuring continued international market access for the industry, lies at the bottom of this strategy. The two main drivers of this strategy are:

� Activities/projects emanating from this, MUST benefit biodiversity � Activities/projects emanating from this MUST benefit the industry and

individual farmers For this reason the strategic approach to support these drivers will assist in the optimal utilisation of resources and capacity of all the partners involved in biodiversity management and ostrich production, and will eventually contribute significantly to the reaching the goals set and vision.

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

4

Ten farmers initially participated in the Ostrich Industry Biodiversity Management Project, 9 of which received farm level biodiversity management plans. Project participants were selected based on 3 criteria: � Endangered gannaveld or apronveld (highly endangered types of the biome)

present on the farm � Flock breeding practiced or being practiced on the farm � Land owner willingness Rehabilitation on four denuded ostrich camps is taking place in partnership with RenuVeld Karoo and Conservation Management Services. Restoration methodology will be tested and results will be fed back to the industry. One site will be utilised as demonstration site, and a “best practice” guideline document for veld rehabilitation and restoration will be generated. Three processes are being piloted: � Assistance with DEA&DP applications pertaining to change of land-use, for

farmers who are considering pen breeding, and � Monitoring and auditing compliance regarding carrying capacity

The ostrich industry is a high risk industry, based on 2 realities: � Illnesses and susceptibility to weather changes � Capital intensive

Over the recent years environmental legislation has been streamlined, indicating the government’s recognition of the necessity of tightening the grip on irresponsible, unsustainable activities. Legislation pertaining to the Ostrich Industry includes the following: � The Constitution � National Environmental Management Act (107 of 1884) (NEMA) � National Environmental Management: Biodiversity Act (Act 10 of 2004) (NEMBA) � National Environmental Protected Areas Act (Act 56 of 2003) (NEMPA) � Environment Conservation Act (73 of 1989) (ECA) � Conservation of Agricultural Resources Act (43 of 1983) (CARA) � Western Cape Land Use Planning Ordinance (15 of 1985) (LUPO) � National Water Act (36 of 1998) � National Veld and Forest Fire Act (101 of 1989) (NVFFA) � National Heritage Resources Act (25 of 1999) � Western Cape Nature Conservation Laws Amendment Act (3 of 2000)

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

5

SECTION A: DESCRIPTION OF THE BIODIVERSITY IMPORTANCE OF THE KLEIN KAROO, ECONOMIC IMPORTANCE OF THE OSTRICH INDUSTRY IN THE KLEIN KAROO, VISION AND OVERALL MANAGEMENT OBJECTIVES

1. BIODIVERSITY IMPORTANCE OF THE KLEIN KAROO

(See Addendum A (p 26), from which this is an excerpt.) The Klein Karoo is recognised internationally as an area in which three of the 34 global biodiversity hotspots occur, the Succulent Karoo, Maputaland – Pondoland - Albany and the Cape Floristic Region Biodiversity hotspots. Biodiversity hotspots are recognised as earth’s biologically richest and most endangered terrestrial eco-regions. Each contains at least 1500 species of vascular plants as endemic species and have lost 70% or more original habitat. In addition to its floral diversity, the biome is a centre of diversity for reptiles and many groups of invertebrates. The Klein Karoo is extremely unique, in that it houses all three biomes – nowhere else in the world does one get this convergence of vegetation, which makes for exciting ecotone displays. The Klein Karoo forms part of the Southern Karoo (SK) Priority Area as described in the Succulent Karoo Ecosystem Profile1. It also forms part of the Cape Floristic Region (CFR), specifically the fynbos biome within the CFR. Eight portions of the CFR have been awarded World Heritage Site (WHS) status – of which there are only 175 in the world. The Greater Swartberg Mountain Range that is Central to the Klein Karoo, forms part of this WHS. This alone makes it an exceptionally unique and bio-diverse area; one that warrants action to safeguard, protect and conserve this natural jewel. A fine-scale map of the Klein Karoo vegetation and habitats that was done by Jan Vlok, revealed remarkable biological diversity - no less than 369 vegetation units in 56 habitat types. Each of the individual vegetation units constitute critical components of the Little Karoo environment that need to be understood before rational decisions and actions are taken to conserve the biodiversity of the region. It is recognised that the rich biodiversity of the Succulent Karoo is due to an extensive and complex array of habitat types derived from topographical and climatic diversity in the region’s rugged mountains and semi-arid shrub lands. Unfortunately much of this biodiversity has been degraded - a large proportion of the vegetation of the lower lying areas of the Klein Karoo has undergone severe degradation. The severity of the degradation resulted in a number of vegetation types being critically endangered, endangered or vulnerable (see Addendum A, p 26). In the lower lying areas of the Little Karoo where livestock farming, of which ostrich farming is most predominant the degradation of biodiversity results in long term detrimental impacts that affect not only the ecological systems but also the agricultural potential of the land and the wellbeing of society. Apart from the reasons given above, there are numerous other reasons why biodiversity needs to be

1 Succulent Karoo Ecosystem Profile: South African and Namibia, 2001

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

6

conserved in the Klein Karoo, including human encroachment on sensitive habitats, climate change, etc.

The loss of vegetation usually results in the loss of soil through water and wind erosion. This has a direct impact on agriculture and biodiversity. Vegetation plays a crucial role in water retention and water infiltration into the soil by reducing rainfall splash effect, slowing water runoff, providing dead plant material mulch that serve as natural erosion barriers and creating suitable habitat for biological soil crusts (mosses and lichens) that are so important in keeping these systems healthy. The healthy environment in which vegetation diversity and cover is sound provides critical natural services in terms of preventing excessive water run-off on the Klein Karoo plains. This prevents excessive flooding events and prevents salutation of water courses. The cost of damage incurred by extreme flooding events in the Klein Karoo is well known. Resilience of the ecological system is a crucial survival mechanism especially in harsh environments such as the Klein Karoo. Plants interact, some provide suitable environments for seeds to germinate and grow, larger species provide protection from the sun, provide shade and keep soils cooler, and others provide traps for wind blown seed and keep seed banks. Some species cover the gaps created by erosion or dying plants until other longer lived plants can develop. A diversity of plants allows for greater resilience to the impacts of periods of stress such as found in this normal arid biome. Climatic excessive droughts however greatly enhance the losses. It has also been shown that the open sky and unspoiled landscapes of the Klein Karoo are the number one draw cards for tourism (a major economic sector of the Klein Karoo). These are recognized critical tourist attractions. Degradation of biodiversity will have obvious impacts on this economic sector. As ostrich farming is the largest contributor to the economy of the Klein Karoo and because this activity has had such an impact on the biodiversity of the area, improved and sustainable ostrich farming methods need to be developed that will ensure the sustainability of the ostrich farming industry and the conservation of globally important biodiversity. (See Addendum A for full report.)

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

7

2. ECONOMIC IMPORTANCE OF THE OSTRICH INDUSTRY IN THE KLEIN KAROO

This section will briefly describe the economic significance of the ostrich industry for the Klein Karoo region. Please see Addendum B, p 33 for a detailed report.

2.1 BRIEF HISTORY OF THE INDUSTRY

Since the beginning of the ostrich industry in South Africa, the Klein Karoo played a leading role. Ostrich feather export increased with 100+% over a 30 year period between 1835 and 1865. This lead to a dramatic increase in the domestication and breeding of ostriches, particularly in the Oudtshoorn district and resulted in ostrich feathers being the fourth largest export commodity of the republic by 1913. From these humble beginnings (and experiencing some dramatic economic dips as well), the industry has developed into a highly sophisticated entity that slaughters between 200 000 and 300 000 ostriches per annum, mainly for leather and meat, with feathers playing a smaller role (with a peak in the late 90’s of around 300 000) . Some 75% of output originates from the Western Cape where the Klein Karoo dominates production. More than 65% of the world’s ostriches are now found in South Africa and South Africa accounts for 90% of ostrich products traded internationally, contributing R1, 2 billion per annum (2008) to the SA Economy.

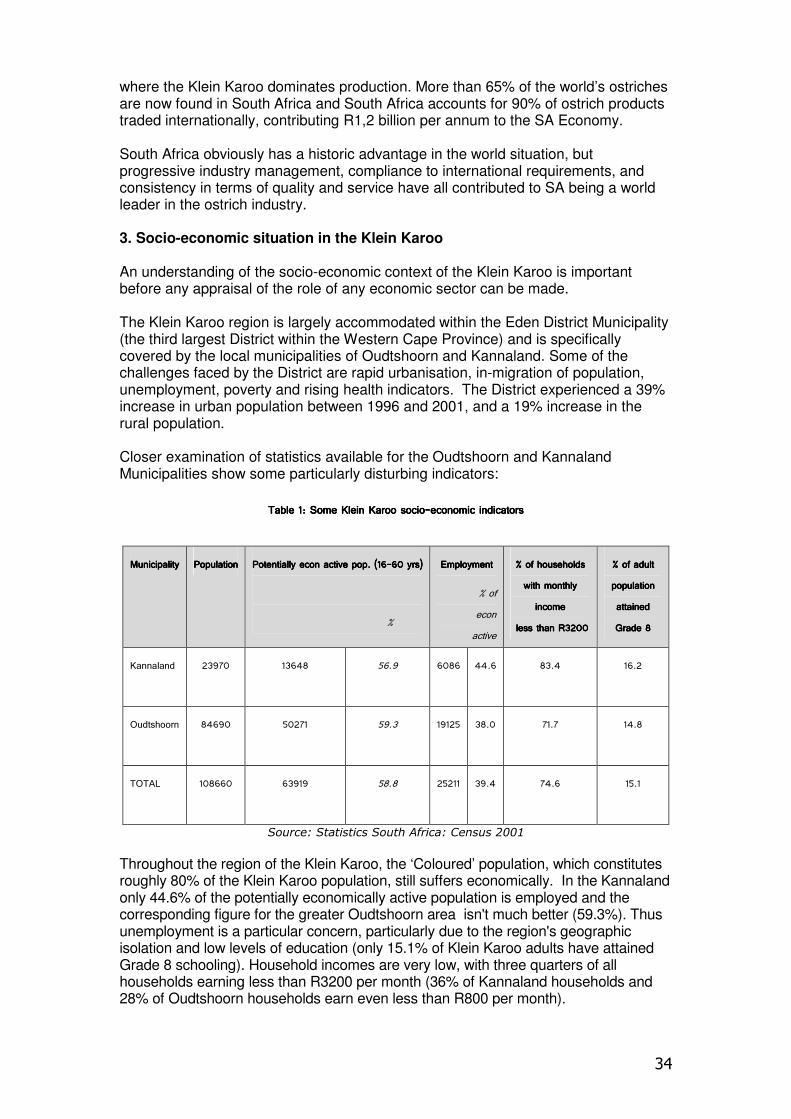

2.2 SOCIO-ECONOMIC SITUATION IN THE KLEIN KAROO

The Klein Karoo region is largely accommodated within the Eden District Municipality (the third largest District within the Western Cape Province) and is specifically covered by the local municipalities of Oudtshoorn and Kannaland. Some of the challenges faced by the District are rapid urbanisation, in-migration of population, unemployment, poverty and rising health indicators (TB, HIV etc) Unemployment is a particular concern; particularly due to the region's geographic isolation and low levels of education (only 15.1% of Klein Karoo adults have attained Grade 8 schooling). Household incomes are very low, with three quarters of all households earning less than R3200 per month. Combining population sizes and production levels, Oudtshoorn has the lowest per capita income levels of the large towns in the Southern Cape, i.e. R21 855 (2000 constant prices) in 2004 compared to R32 500 of George, R31 400 of Knysna and R28 200 of Mosselbay (Development Information Unit: DBSA Global Insight database, 2004). The poverty problem in the Klein Karoo has become more acute since 1998 with almost 30% (almost one out of three) of the population living in poverty in 2004 as opposed to 25% (one out of four) in 1998. Although still not on a national level, the percentage of people in Oudtshoorn living in poverty is much higher than the Provincial figure (23%) and higher than the percentages in George (18%); Knysna (19%) and Mossel Bay (25%).

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

8

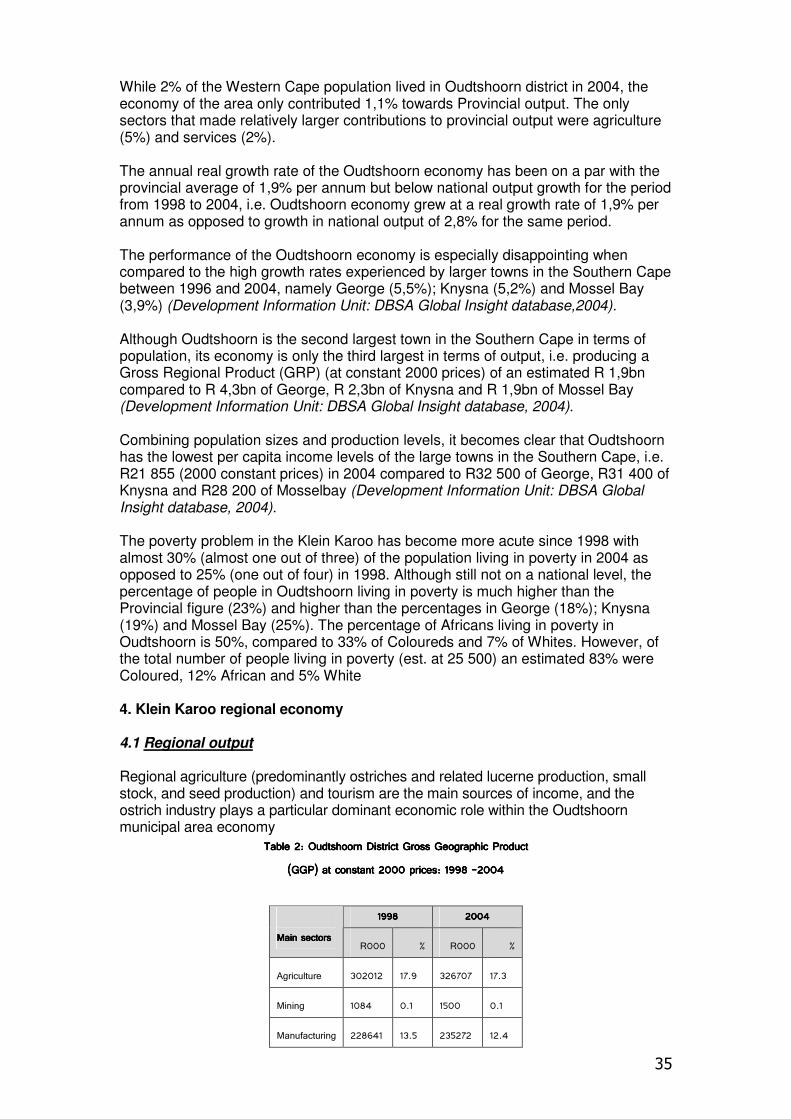

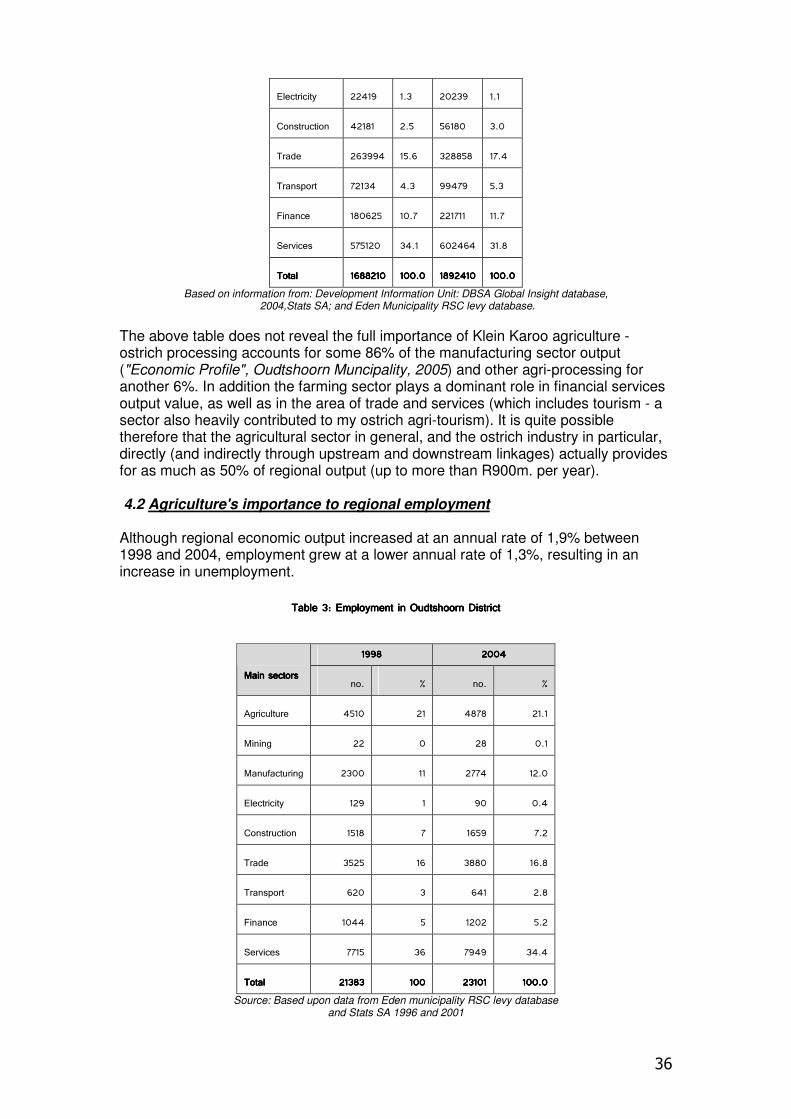

2.3 KLEIN KAROO REGIONAL ECONOMY

2.3.1 Regional Output

Regional agriculture (predominantly ostriches and related lucerne production, small stock, and seed production) and tourism are the main sources of income. The ostrich industry plays a particular dominant economic role within the Oudtshoorn municipal area economy.

2.3.2 Agriculture’s Importance to Regional Employment

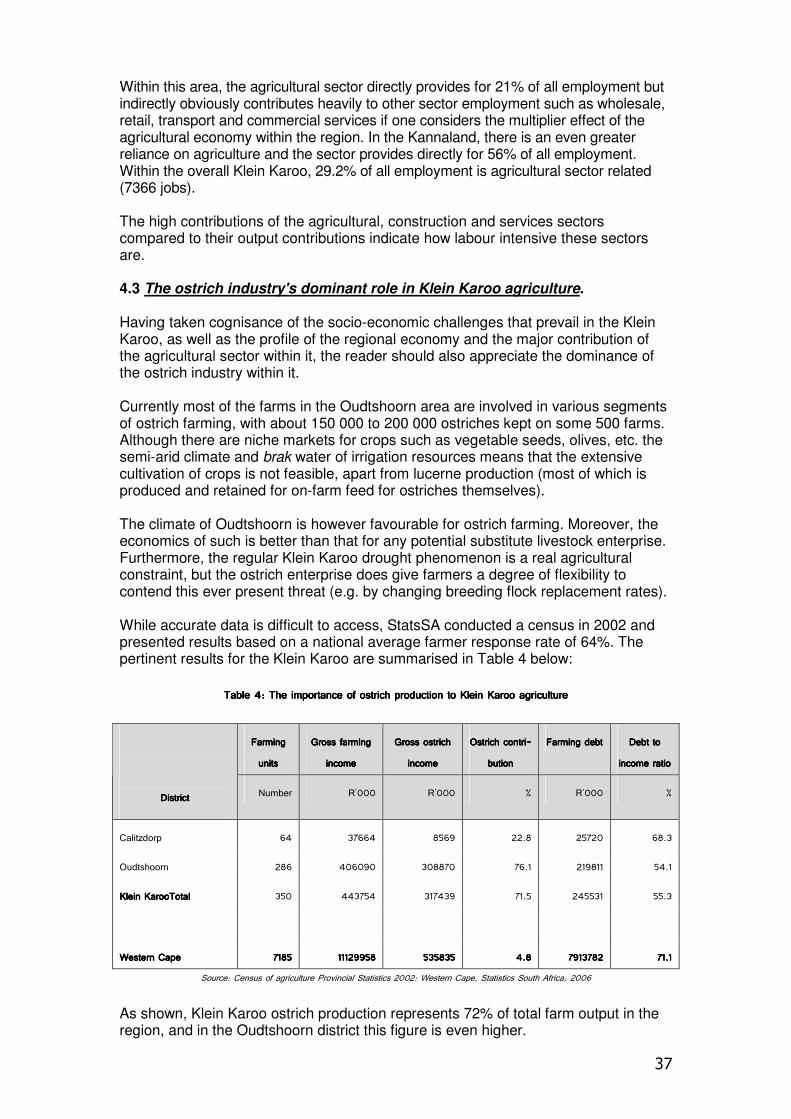

Within this area, the agricultural sector directly provides for 21% of all employment but indirectly obviously contributes heavily to other sector employment such as wholesale, retail, transport and commercial services if one considers the multiplier effect of the agricultural economy within the region. In the Kannaland, there is an even greater reliance on agriculture and the sector provides directly for 56% of all employment. Within the overall Klein Karoo, 29.2% of all employment is agricultural sector related (7366 jobs). The high contributions of the agricultural, construction and services sectors compared to their output contributions indicate how labour intensive these sectors are.

2.3.3 The Ostrich Industry’s Dominant Role in Klein Karoo Agriculture

Currently most of the farms in the Oudtshoorn area are involved in various segments of ostrich farming, with about 150 000 to 200 000 ostriches kept on some 500 farms. The climate of Oudtshoorn is favourable for ostrich farming. Moreover, the economics of such is better than that for any potential substitute livestock enterprise. Furthermore, the regular Klein Karoo drought phenomenon is a real agricultural constraint, but the ostrich enterprise does give farmers a degree of flexibility to contend this ever present threat (e.g. by changing breeding flock replacement rates). Klein Karoo ostrich production represents 72% of total farm output in the region, and in the Oudtshoorn district this figure is even higher. Thus the whole economic backbone of the Klein Karoo is the ostrich industry - a capital intensive enterprise with high risk due to exposure to the vagaries of the export market, the international financial situation, and threat of disease, droughts, and now the need to pay greater attention to biodiversity conservation. The industry has had many crisis points in its history, yet its regional advantage, good organisation and tight management, insistence on quality and meeting international standards, as well as a conservative financial strategy (e.g. its farmer debt to income ratio is 23% better than that of the Provincial average) has meant that it has ably played a dominant role in meeting the economic challenges of the region.

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

9

3. MAKING AN ECONOMIC CASE FOR PEN BREEDING AS ONE ALTERNATIVE OVER FLOCK BREEDING

This section will briefly describe the economic benefit of doing pen breeding instead of flock breeding. Please see Addendum C, p 38 for a detailed report.

3.1 THE ECONOMICS OF OSTRICH PEN-BREEDING

In considering various strategies to conserve the succulent Karoo, the SAOBC has identified a possible industry switch to pen-breeding as a key strategic initiative.

3.1.1 Pen Breeding

An industry adoption of pen-based ostrich breeding or strictly regulated and monitored “veld based trop paring” (as opposed to uncontrolled veld-based "tropparing) would seem to be a "win-win" option open to both conservationists and farmers. Under such a production switch, veld (low to moderate degradation) previously occupied by breeding ostriches would have a chance to rehabilitate due to breeding ostriches being brought off the veld and into breeding camps.

3.1.2 Pen Breeding Cost

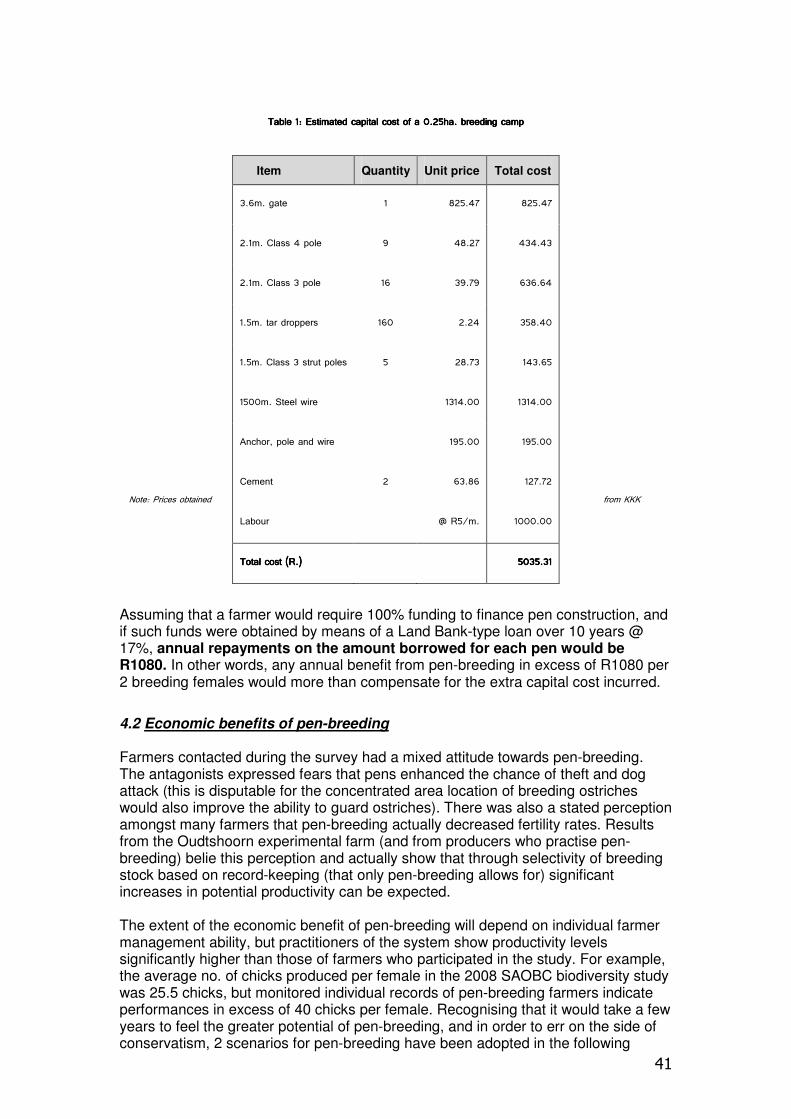

Under a pen-breeding regime, breeding duos, or preferably trios, would be kept in 0.25 ha.

The only significant cost differences between pen-breeding and "tropparing" are those associated with the capital and management costs of pen construction. (Costs related to theft, disease, nutrition, etc are unknown and will vary.) The capital cost of a pen or 0.25 ha. breeding camp (to house 1 breeding male and 2 breeding females under a trio system) has been estimated at R5035. See addendum C. Assuming that a farmer would require 100% funding to finance pen construction, and if such funds were obtained by means of a Land Bank-type loan over 10 years @ 17%, annual repayments on the amount borrowed for each pen would be R1080. In other words, based on assumptions and calculations, any annual benefit from pen-breeding in excess of R1080 per 2 breeding females would more than compensate for the extra capital cost incurred.

3.1.3 Economic Benefits of Pen-Breeding

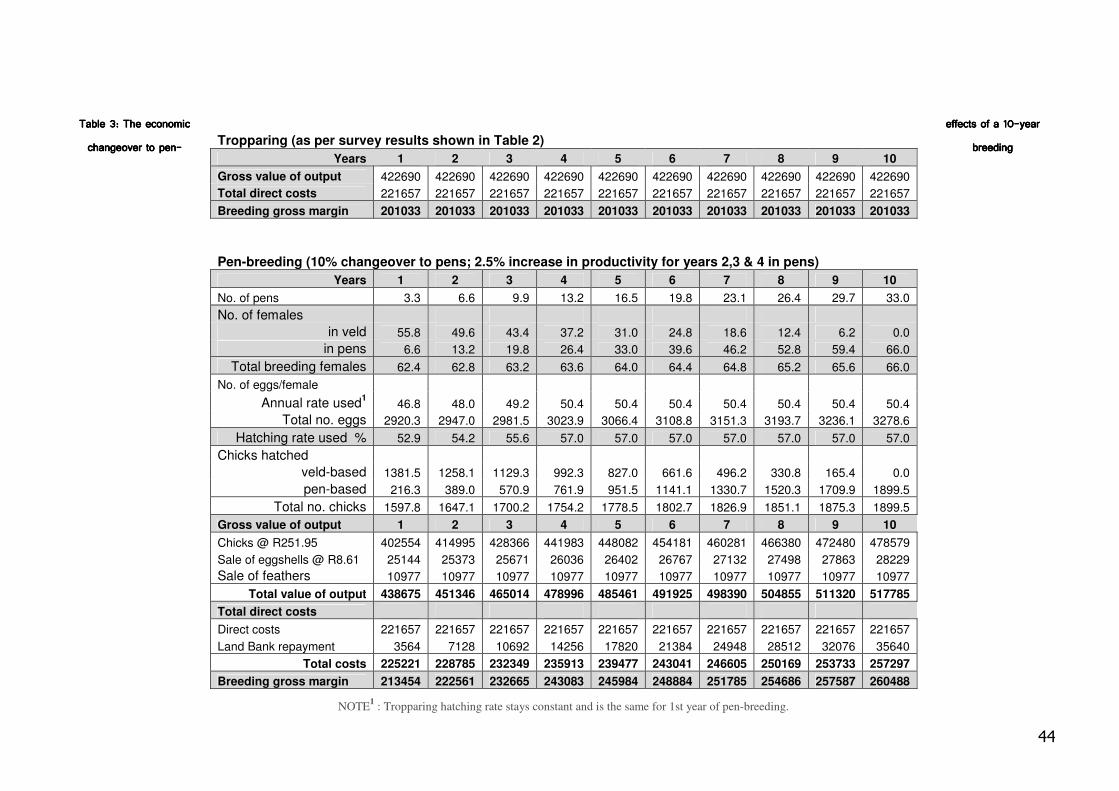

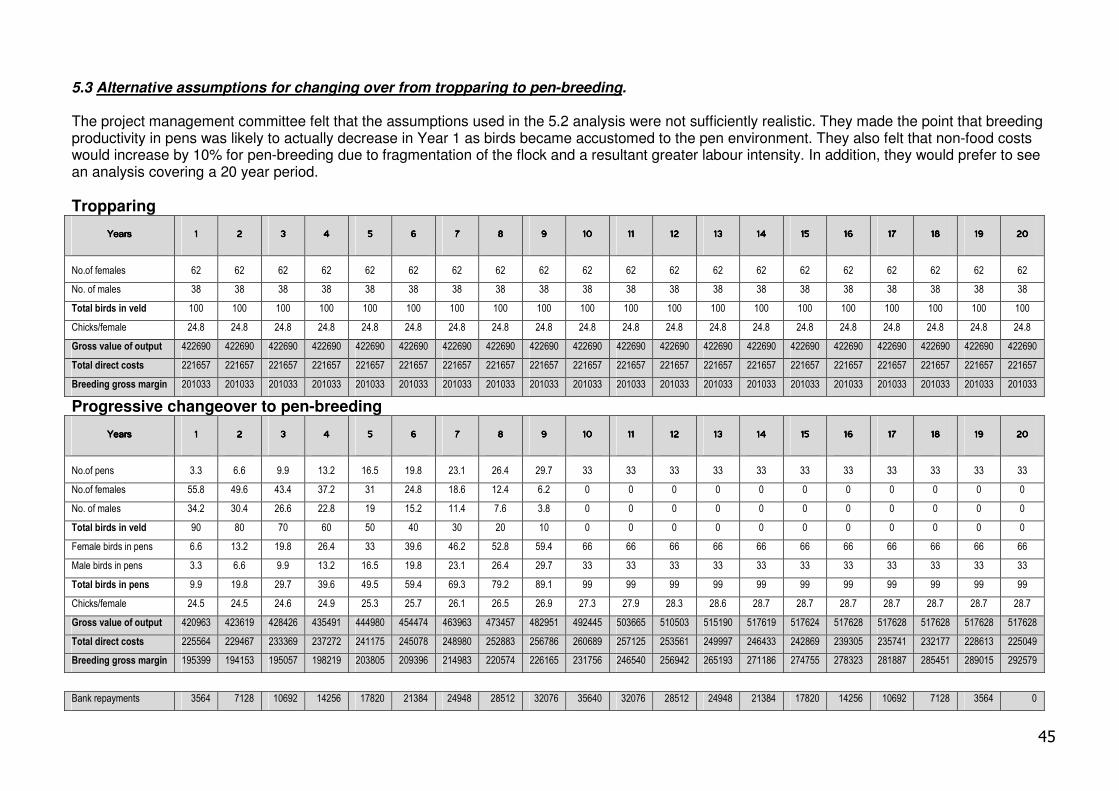

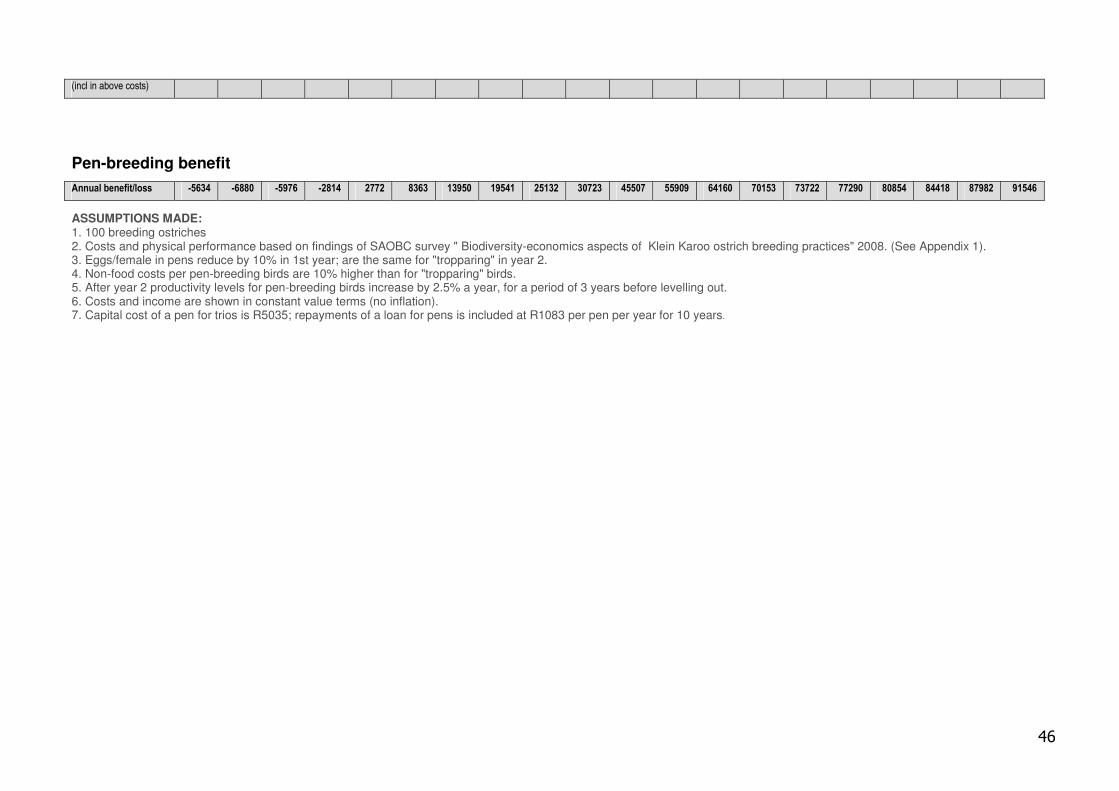

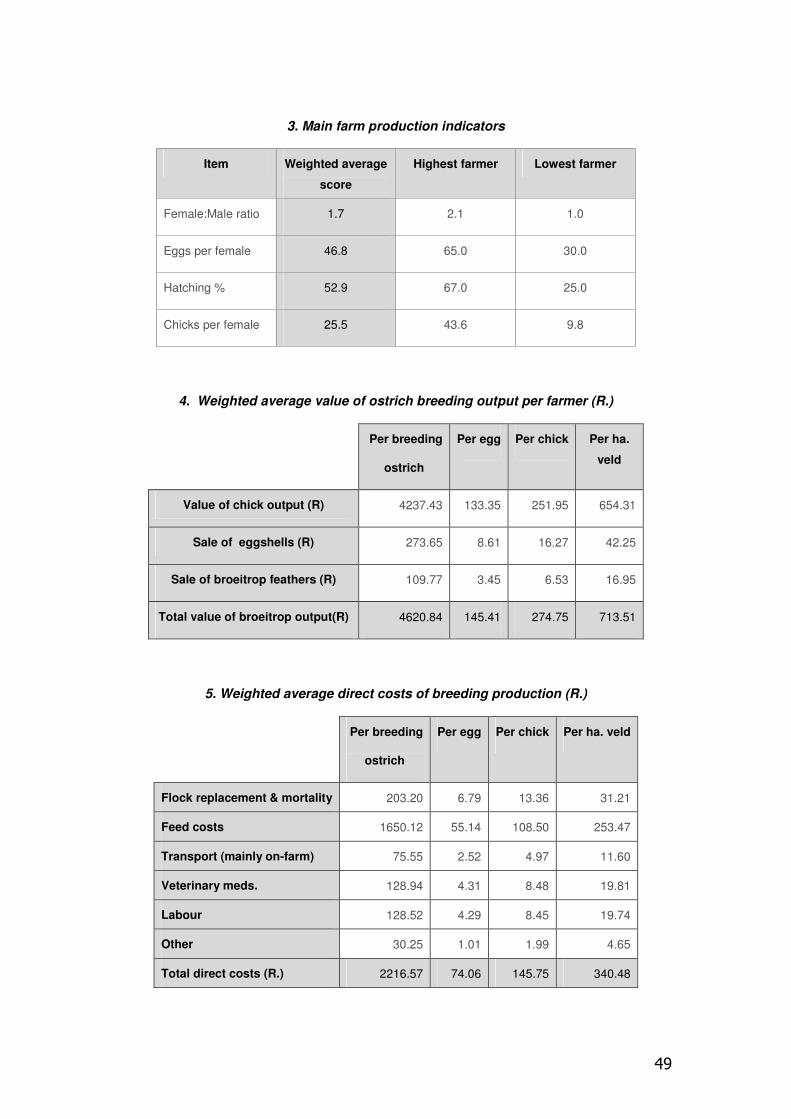

The extent of the economic benefit of pen-breeding will depend on individual farmer management ability, but some practitioners of the system show productivity levels that can be significantly higher than those of farmers who participated in a study done on 10 farmers’ ostrich production systems by the OIBMP. For example, the average no. of chicks produced per female in the 2008 OIBMP study was 25.5 chicks, but monitored individual records of pen-breeding farmers indicate performances in excess of 40 chicks per female. Recognising that it would take a few years to feel the greater potential of pen-breeding, and in order to err on the side of conservatism, 2 scenarios for pen-breeding have been adopted in the following economics models of pen-breeding - one at a an annual productivity increase of 2.5% for year 2 and year 3, and the other at a 5% increase.

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

10

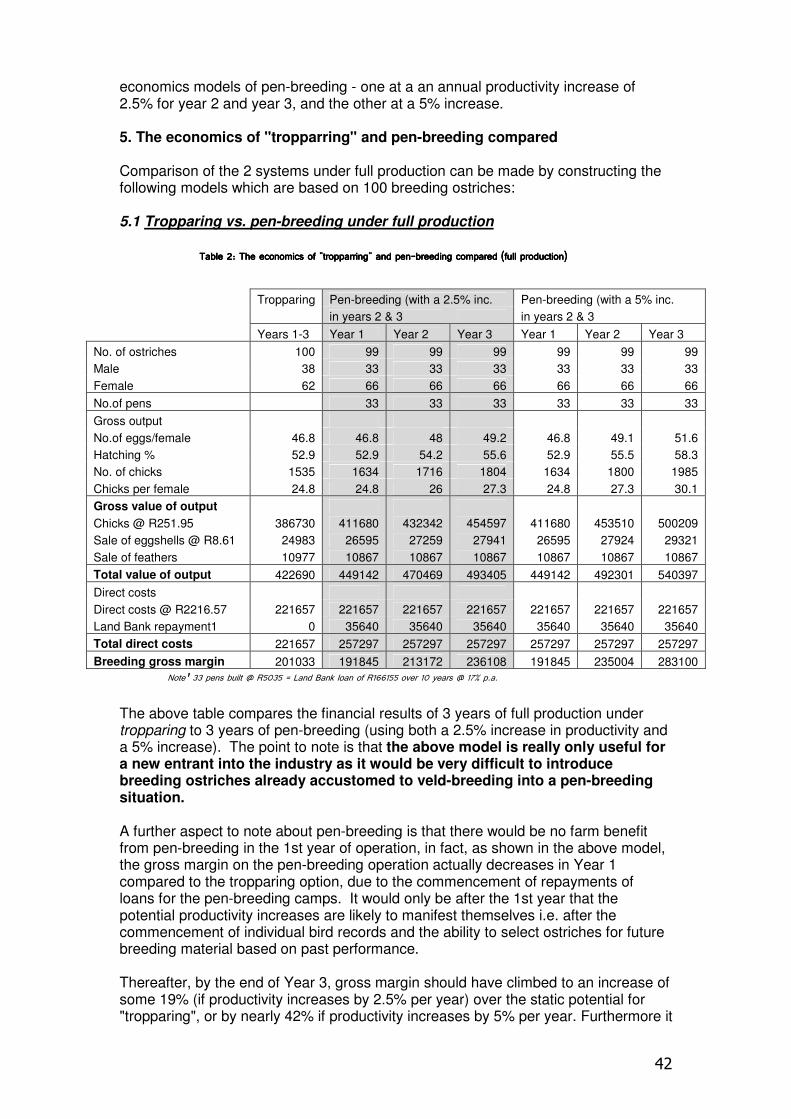

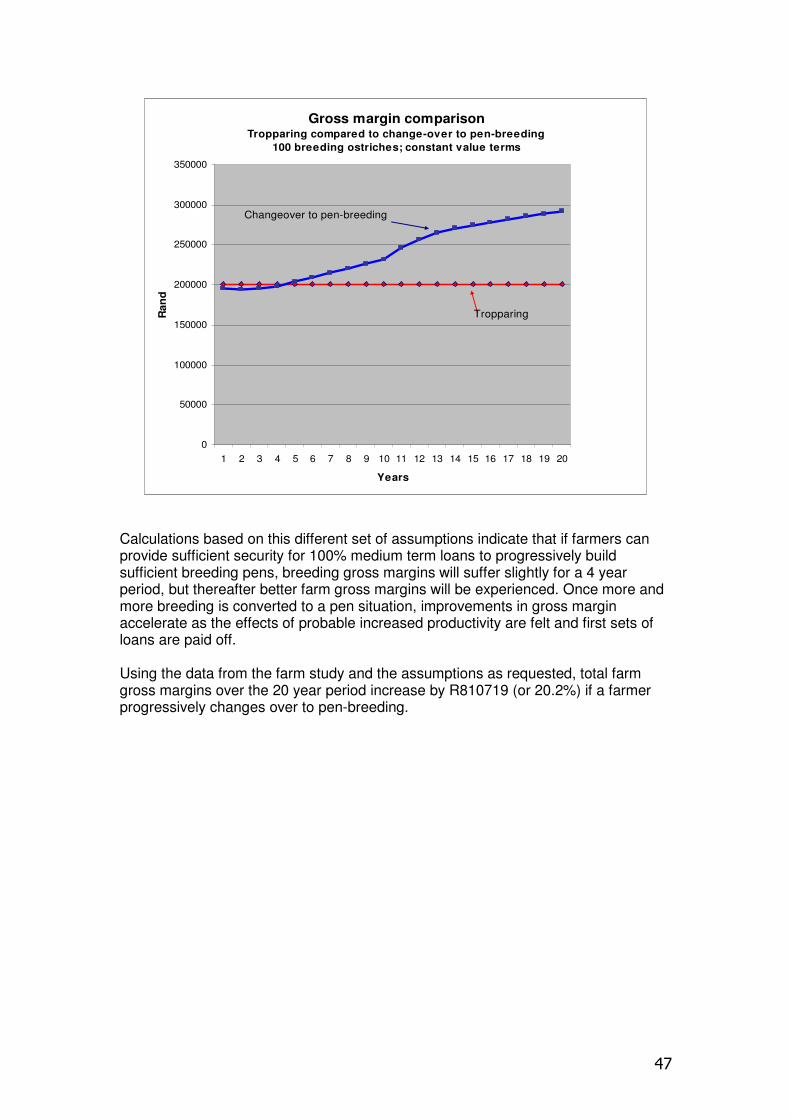

3.1.4 The Economics of “Tropparing” and Pen-Breeding Compared

A comparison of the 2 systems under full production was made by constructing models which are based on 100 breeding ostriches: These showed: � there would be no farm benefit from changing to the system in Year 1. In fact the

gross margin on the pen-breeding operation actually decreases in Year 1 compared to the tropparing option. It would only be after the 1st year that the potential productivity increases are likely to manifest themselves i.e. after the commencement of individual bird records and the ability to select ostriches for future breeding material based on past performance.

� Thereafter, by the end of Year 3, output should have climbed to an increase of some 19% (if productivity increases by 2.5% per year) over the static potential for "tropparing", or by nearly 42% if productivity increases by 5% per year. Furthermore it should be noted that increases of such magnitude are possible even after annual loan repayment has been made.

(This model will be tested with participating farmers in future.)

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

11

4. CURRENT SITUATION: OSTRICHES IN THE KLEIN KAROO

4.1 THE FOOTPRINT OF THE OSTRICH INDUSTY

4.1.1 History

The South African Ostrich Industry became established in 1864 with large-scale exports of feathers to Europe. The Industry flourished during what was referred to as the second ostrich feather boom between 1900 and 1914. Soon afterwards, the industry virtually collapsed as a result of changes in world fashion trends and the First World War. During the 1960s, the Industry was transformed into an intensively managed farming activity. The emphasis shifted from feather to leather production. More recently, ostrich meat became popular because of health aspects such as almost no fat and cholesterol, and richness in protein and iron. This increasing focus on a healthy lifestyle leads to a growing demand for ostrich meat worldwide and South Africa is the main supplier.

Since the deregulation of the marketing of agricultural products in South Africa during the 1990s, farming with ostriches has spread from the Little Karoo region to other parts of the country as well as to several other countries.

4.1.2 Current

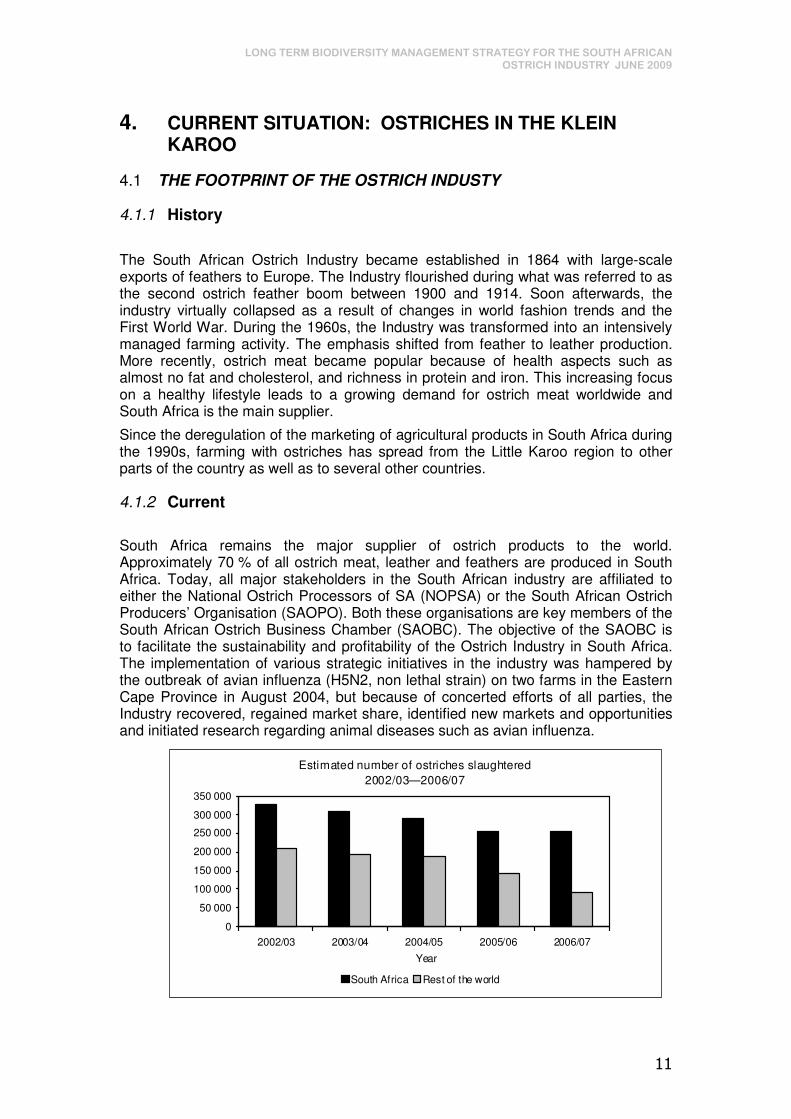

South Africa remains the major supplier of ostrich products to the world. Approximately 70 % of all ostrich meat, leather and feathers are produced in South Africa. Today, all major stakeholders in the South African industry are affiliated to either the National Ostrich Processors of SA (NOPSA) or the South African Ostrich Producers’ Organisation (SAOPO). Both these organisations are key members of the South African Ostrich Business Chamber (SAOBC). The objective of the SAOBC is to facilitate the sustainability and profitability of the Ostrich Industry in South Africa. The implementation of various strategic initiatives in the industry was hampered by the outbreak of avian influenza (H5N2, non lethal strain) on two farms in the Eastern Cape Province in August 2004, but because of concerted efforts of all parties, the Industry recovered, regained market share, identified new markets and opportunities and initiated research regarding animal diseases such as avian influenza.

Estimated number of ostriches slaughtered

2002/03—2006/07

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

2002/03 2003/04 2004/05 2005/06 2006/07

Year

South Africa Rest of the world

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

12

The number of birds slaughtered worldwide was estimated at approximately 300 000 for 2007/08, 214 000 of which were slaughtered in South Africa. In Europe the demand for ostrich meat remained high and the local consumption of ostrich meat showed a continued increase.

Income from leather varies significantly because of large price differences between raw skin grades. The SAOBC’s aim is that only higher-grade leather be placed on the market and therefore various research programmes regarding quality improvement and genetics are being launched. A producer earns approximately R1 500 for a raw first-grade skin and around R800 for a third-grade skin. The current worldwide economic crisis has lead to a dramatic drop in these prices, as ostrich-derived products are being perceived as luxury goods.

The average price that producers of ostrich meat received during 2008/09 was R32/kg and R150 for feathers per bird (depending on the quality).

4.1.3 Prospects

During the 2008/09 season, the number of ostriches slaughtered in South Africa is expected to remain at about 200 000, mainly as a result of the after-effects of avian influenza and the severe drought followed by floods in the main production areas during 2006. The situation could continue well into 2009, with even a further drop in slaughter numbers because of the fact that an ostrich can only be slaughtered after 14 months as well as increasing input costs (mainly feed, transport and labour) and interest rates, linked to the factors mentioned. A large reduction in breeder numbers were also observed as result of economic realities and disease outbreaks.

The SAOBC, being the representative body of the South Africa ostrich industry, accepted its role as partner with the Department of Agriculture in ensuring compliance with international export requirements. Generic marketing activities take place in collaboration with the Department of Trade and Industry to try and increase the ostrich industry’s contribution of R1, 75 billion per annum to the South African economy, as well as to safeguard more than 20 000 jobs.

4.1.4 Markets

Export statistics for 2007/2008 indicates the following: Meat comprises the bulk of income per ostrich (55%), with Europe (4 000 tonnes) and the Far East (350 tonnes) being the main importers. Ostrich meat is not a commodity, but an exotic, lifestyle product for health conscious consumers and customers are prepared to bay for quality, based on consistent supply. Distribution is done mainly through agents, wholesalers, reprocesses and repackages. Promotion of ostrich meat includes the development of a SA brand (SA Ostrich), educational campaigns via the healthy-living industry, joint promotions with selected retailers and/or restaurants and participating in international trade shows and food fairs. 42% of income per ostrich is derived from leather – some 200 000 skins were exported, the bulk of which to USA/Mexico, Europe and the Far East. Ostrich leather is used to manufacture handbags, boots, purses, belts, jackets, coats and dresses, and distribution is mainly done through agents, designer buyers and marketers. It is seen to be a high quality, luxury, exotic, durable item, and buyers pay a premium price due to quality and positioning. Promotion is done through fashion magazines (Versace, Gucci), participation in trade shows (Bologna, Hong Kong) and sponsorships to designers who participate in international fashion shows (Paris, Moscow).

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

13

The exotic feather market comprises the smallest income per ostrich, with feather dusters selling 1 million per annum. Other uses are for the fashion industry (handbags, clothing) and the entertainment industry (Rio Carnival, Moulin Rouge). Prices vary according to applications and marketing is done mainly through joint ventures and relationships.

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

14

5. CURRENT SITUATION: BIODIVERSITY STATUS OF THE KLEIN KAROO

5.1 MAP OF ENDANGERED VEGETATION REMNANTS

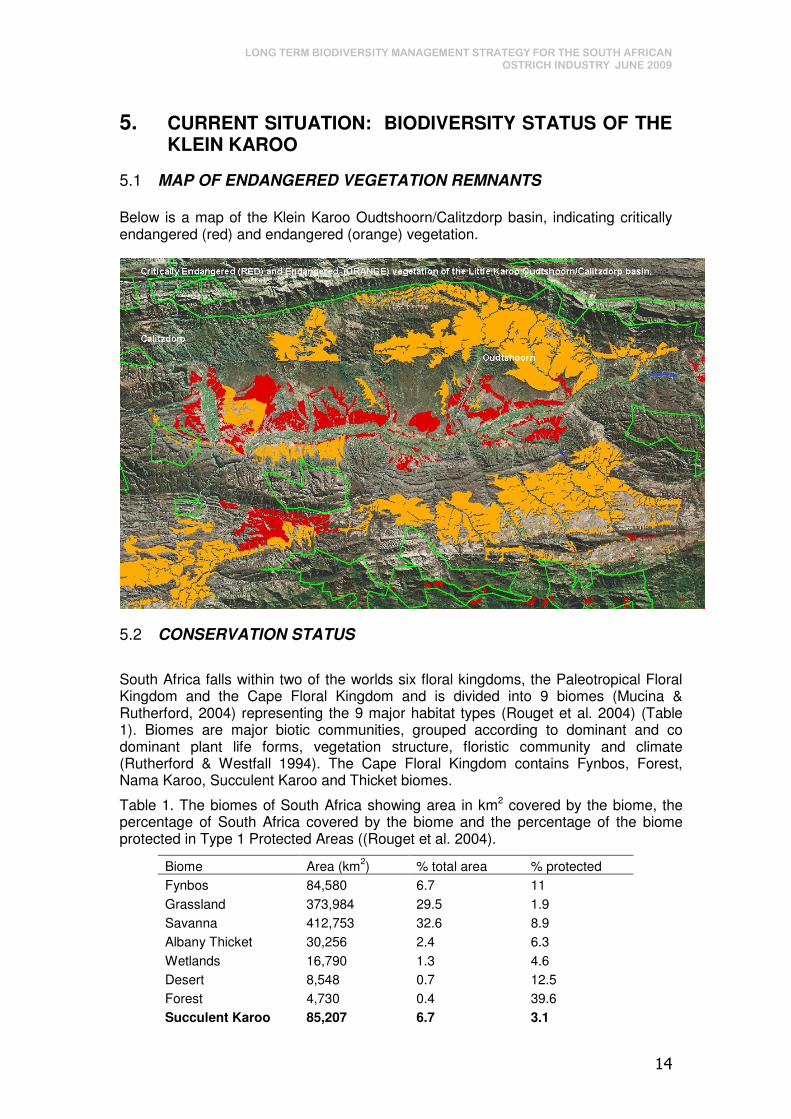

Below is a map of the Klein Karoo Oudtshoorn/Calitzdorp basin, indicating critically endangered (red) and endangered (orange) vegetation.

5.2 CONSERVATION STATUS

South Africa falls within two of the worlds six floral kingdoms, the Paleotropical Floral Kingdom and the Cape Floral Kingdom and is divided into 9 biomes (Mucina & Rutherford, 2004) representing the 9 major habitat types (Rouget et al. 2004) (Table 1). Biomes are major biotic communities, grouped according to dominant and co dominant plant life forms, vegetation structure, floristic community and climate (Rutherford & Westfall 1994). The Cape Floral Kingdom contains Fynbos, Forest, Nama Karoo, Succulent Karoo and Thicket biomes.

Table 1. The biomes of South Africa showing area in km2 covered by the biome, the percentage of South Africa covered by the biome and the percentage of the biome protected in Type 1 Protected Areas ((Rouget et al. 2004).

Biome Area (km2) % total area % protected

Fynbos 84,580 6.7 11

Grassland 373,984 29.5 1.9

Savanna 412,753 32.6 8.9

Albany Thicket 30,256 2.4 6.3

Wetlands 16,790 1.3 4.6

Desert 8,548 0.7 12.5

Forest 4,730 0.4 39.6

Succulent Karoo 85,207 6.7 3.1

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

15

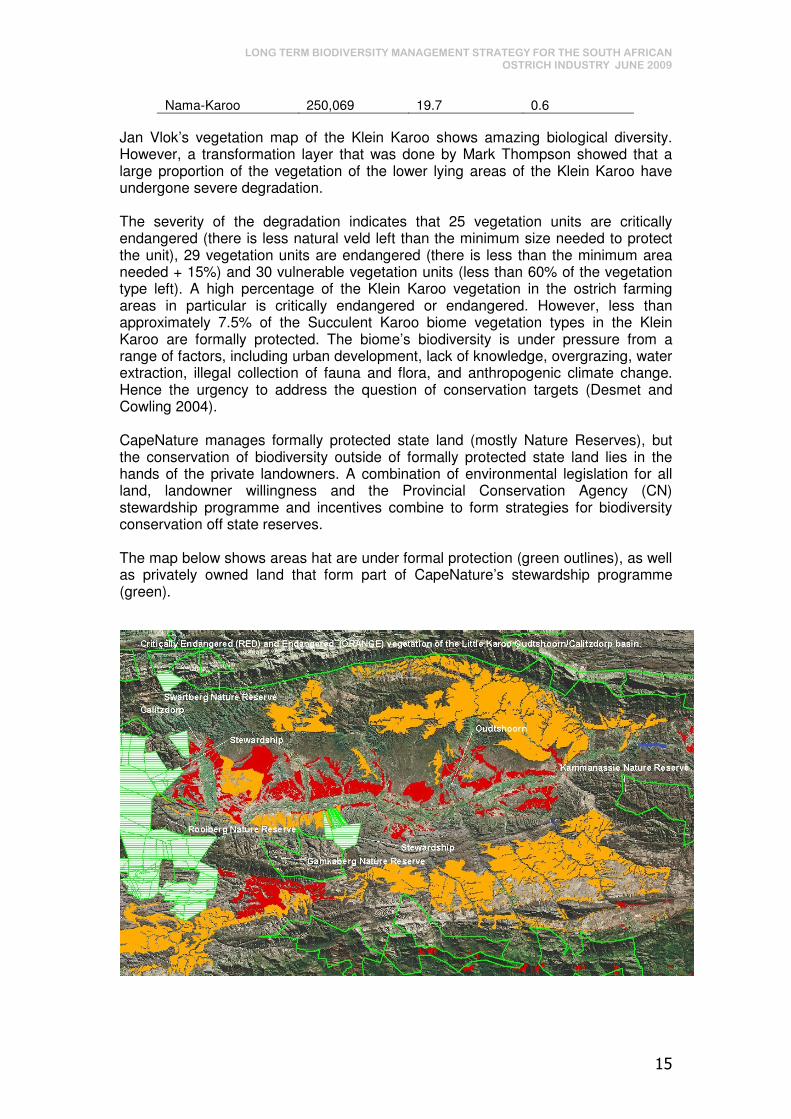

Nama-Karoo 250,069 19.7 0.6

Jan Vlok’s vegetation map of the Klein Karoo shows amazing biological diversity. However, a transformation layer that was done by Mark Thompson showed that a large proportion of the vegetation of the lower lying areas of the Klein Karoo have undergone severe degradation. The severity of the degradation indicates that 25 vegetation units are critically endangered (there is less natural veld left than the minimum size needed to protect the unit), 29 vegetation units are endangered (there is less than the minimum area needed + 15%) and 30 vulnerable vegetation units (less than 60% of the vegetation type left). A high percentage of the Klein Karoo vegetation in the ostrich farming areas in particular is critically endangered or endangered. However, less than approximately 7.5% of the Succulent Karoo biome vegetation types in the Klein Karoo are formally protected. The biome’s biodiversity is under pressure from a range of factors, including urban development, lack of knowledge, overgrazing, water extraction, illegal collection of fauna and flora, and anthropogenic climate change. Hence the urgency to address the question of conservation targets (Desmet and Cowling 2004). CapeNature manages formally protected state land (mostly Nature Reserves), but the conservation of biodiversity outside of formally protected state land lies in the hands of the private landowners. A combination of environmental legislation for all land, landowner willingness and the Provincial Conservation Agency (CN) stewardship programme and incentives combine to form strategies for biodiversity conservation off state reserves. The map below shows areas hat are under formal protection (green outlines), as well as privately owned land that form part of CapeNature’s stewardship programme (green).

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

16

6. MISSION AND VISION – Working Towards a Win-Win Situation

An agreed upon vision has been developed through various meetings and workshops with stakeholders – at the base of this lies the following principles: � Balance between utilisation and conservation – sustaining a balance between the

environment and the industry � Improved ostrich production, based on research � Ostrich industry to have less impact on biodiversity � Rehabilitation where appropriate � Climate change mitigation and adaptation

MISSION

The ostrich industry recognises and safeguards the unique biodiversity of the Klein Karoo and supports sustainable farming methodologies that strive to balance utilisation and conservation through improved veld management, rehabilitation where appropriate, climate change adaptation and sound research in order to maintain its world leader status.

VISION

The ostrich industry in the Klein Karoo supports a process whereby producers will, by 2019, decrease their impact on the biodiversity through improved veld management and restoration, whilst pursuing increased production based on sound research to retain and expand international and local markets.

LONG TERM BIODIVERSITY MANAGEMENT STRATEGY FOR THE SOUTH AFRICAN

OSTRICH INDUSTRY JUNE 2009

17

7. OVERALL MANAGEMENT PRINCIPLES

Improved biodiversity and improved ostrich production in the ostrich producing areas of the Klein Karoo will be managed to meet the following strategic management objectives: � Maintaining and improving the image of South African ostriches in the export

market � Maintaining the status as the world leader in quality ostrich products � Conforming to the consumer standards for export markets, including the national

and international animal welfare standards � Ensuring the conservation of important biodiversity – focussing on vegetation

types and not on individual farmers (an area-based approach) � Accepting that most ostriches and other animals should be removed from

sensitive areas or managed in a different way � Establishing solid partnerships with relevant conservation and agriculture experts,

statutory bodies, research institutions and other initiatives that promote the conservation of the natural environment in harmony with ostrich production

� Ensuring compliance to the guidelines for veld management that was produced � Raising awareness about the interdependency of and partnerships between the

industry and conservation � Making a contribution to the socio-economic wellbeing of the area � Promoting a phased approach to adopt pen breeding as an alternative to flock

breeding in natural veld � Accepting the existing and generating supporting data that underwrites this

strategy

18

SECTION B: IMPLEMENTATION

8. OBJECTIVES

In order to work towards achieving the vision and the mission, four objectives have been identified. Those objectives will form the basis of the strategy, and will play out over a 5 year time span in the Klein Karoo, initially focussing on sensitive vegetation. Thereafter it will be extrapolated to the rest of the Klein Karoo, and later to other ostrich producing regions, like the Eastern and Northern Cape.

8.1 OBJECTIVE 1: Ostrich farmers in the Klein Karoo are improving management of sensitive and endangered veld as well as their ostrich production

Means of verification: � An assessment of veld condition in the Klein Karoo against the footprint of the

industry is guiding biodiversity planning in the Klein Karoo � A GIS map has been produced and conservation targets for sensitive vegetation

have been set � A Klein Karoo Biodiversity Management Plan for the Ostrich Industry is guiding

farm level Biodiversity Management Plans � A systematic switch over to pen breeding has taken place where appropriate and

necessary � Farmers are recording their production systems and are showing an improvement

in production based on pen breeding or alternative systems � # ha under improved management / stewardship � The Industry, through commitment from partners, is providing an extension

service to the ostrich farmers � A monitoring system for improved veld management has been developed and is

implemented � A long term uniform system for auditing compliance has been set up and is

functional (M&E) � Appropriate rehabilitation of identified degraded veld is taking place and

information on rehabilitation methodology is relayed to the Industry � Awareness about the sensitive nature of the area, the benefits of the effect on

veld when ostriches are removed etc, is being raised at appropriate forums and during 1:1 visits – as well as awareness about the strategy and its implementation

� A 10-year time frame for achieving some results are suggested for the Klein Karoo

� By 2019 the # of ostriches in natural veld is acceptable (legally, ecologically, financially)

� An investigation pertaining to determining a realistic average ostrich stocking rate for sensitive and other areas in the Klein Karoo has been done and is guiding DEA&DP applications

� The Industry has adopted a Standard (“best practice”) Document and a Biodiversity Management Plan for the Klein Karoo

19

8.2 OBJECTIVE 2: A sustainable biodiversity unit for the ostrich industry in the Klein Karoo has been established and is working effectively by means of an integrated approach to Biodiversity Management, compliance and sustainable funding

Means of verification: � Opportunities for partnerships have been explored, fine-tuned and solidified by

year 5. � Various working groups (i.e. providing extension services and developing a

monitoring system for improved veld management; assisting with change of land-use applications; developing guideline documents; assisting with compliance, monitoring) have been established and are operational

� Compliance and monitoring systems and functions are established and functional � MoUs have been signed by partners with specific Service Level Agreements � Functions related to the Biodiversity Unit have been embedded in the TOR’s of

partner organisations � Ongoing fundraising and partnerships are supporting the BU � Farmers are engaging with “liaison basket” who assists with Biodiversity

Management Plans on farm level and on vegetation type level � Effective liaison w.r.t. extension, guideline documents, compliance, monitoring etc

is taking place

8.3 OBJECTIVE 3: The Ostrich Industry has developed a climate change mitigation and adaptation strategy which is mainstreamed into the “best practice guidelines”

Means of verification: � The likely impact of climate change for the Ostrich Industry has been determined � Adaptation strategies that can be undertaken and built into best practices have

been identified � The “green” footprint of the Industry has been established and recommendations

on how can it be reduced are considered by the Industry � Data in GIS analysis threshold has been developed � Recommendations for mitigation opportunities have been developed � Potential of carbon exchange has been investigated

8.4 OBJECTIVE 4: The ostrich industry has created an enabling environment for and is supporting research that supports biodiversity conservation and improved production

Means of verification: � Partnerships with various tertiary institutions and study groups have been

established � Research results are being conveyed at relevant groupings / meetings � Assistance is given to proposal writing

20

9. METHODOLOGY

9.1 BIODIVERSITY UNIT

A Biodiversity Unit for the Ostrich Industry, managed by the SAOBC, will be set up. This will require of the current biodiversity project to write a funding proposal and to source external funds. This BU will act as one-stop-shop for biodiversity matters within the Ostrich Industry, and will function to serve the Industry’s Biodiversity needs.

9.1.1 Main functions of the Biodiversity Unit

The main functions of the BU will be the execution of the 4 objectives, as described in B1. However, one of the main drives of Output 1 will be: By 2019 all ostrich producing farms in the Klein Karoo will engage in pen breeding or alternative practices, with acceptable numbers (ecologically and legally) of breeding birds in natural veld.

For this outcome, a phased approach will be adopted: The Industry, through the SAOBC’s Biodiversity Unit, will engage in a process whereby farmers are encouraged to: � place new ostrich stock in preferred alternative system from the start � reduce ostriches on natural veld by 10% per year � do record keeping in order to select better producers (and put in pens, based on

genetic capability) and slaughter non performers This will be done through extension and awareness raising. The BU will set up a “basket” of partners, consisting of representatives from the following institutions, to assist a designated extension officer to the ostrich industry with both extension and awareness raising: � Department of Agriculture (National and Provincial) � LandCare � Organised Agriculture � Veterinarian Services – Ostrich Industry � CapeNature � Department of Environmental Affairs and Development Planning (DEA&DP -

Provincial) / Department of Environmental Affairs and Tourism (DEAT - National) � NSPCA This grouping will also assist with environmental / biodiversity monitoring and compliance issues within the ostrich industry. To back this up, the following documents will be produced and communicated to the farmers through relevant forums and meetings: � Maps: current situation / vegetation / ideal situation in future � Economic case for alternative breeding options � Record keeping guidelines/templates � Climate change strategy In order to assist farmers with switching over to alternative breeding practices from flock breeding, the BU will:

21

� Use the following documents to lobby for support from government: o Economic value of Ostrich Industry in the Klein Karoo o Economic case for pen breeding over flock breeding o Economic case for alternative breeding practices over flock breeding

� Engage with relevant partners for in-kind support and shared resources

9.1.2 Staffing of the BU

� Co-ordinator: ensuring effective partnerships, project management and liaison. � Intern / trainees: student enrolled at NMMU (Saasveld) – to shadow extension

officer and extension teams, to assist project wherever possible (trainee funding to be sourced from government funding)

� Extension officer: to provide extension and other services in partnership with extension team . (Other services: i.e. disease surveillance, farm auditing etc)

� Unit assistant / admin person: to assist with administration, logistics etc � Consultants: to be appointed when necessary � Partnerships: to be sought and solidified with institutions mentioned in 12.1

9.1.3 Capacity Building and Training

� Training in the effective use of the newly acquired GIS system: extension officer,

intern, 1 current SAOBC staff member � Insights training: SAOBC and BU staff � Relevant knowledge exchange trips for staff and ostrich producers � Biodiversity and Ostrich related information sharing at Dept of Agriculture

Information Days � Selected study group meetings when necessary � Training in communication related practices (website / newsletters etc)

9.1.4 Data Capturing

� Generating relevant maps: current situation / vegetation / ideal situation in future � Capturing data re successes and failures of pen breeding systems � M&E data and procedures � Compliance data and procedures

9.1.5 Liaison and Awareness Raising

To be done continuously, and specifically at forums / meetings / workshops / conferences such as:

o Fynbos Forum / Arid Zone Ecological Forum (AZEF) o CAPE / SKEP conferences / opportunities o Agricultural Information Days o Field Trips o Agricultural Unions o CapeNature liaison days

� Liaison with CN/NDA/DEA&DP w.r.t. legislation: ensuring that compliance issues, listed activities etc are smoothed out in order to ease the switch over from flock to pen breeding

� A structured awareness raising campaign, carrying across the message of the importance of complying to veld management guidelines, will be designed and implemented

22

� A marketing strategy and awareness raising w.r.t. climate change adaptation and mitigation strategy

9.1.6 Provision of Services

The extension team (“basket” of partners as stipulated in 12.1) will meet quarterly to discuss in which ways they could provide the following services to individual farmers: � Extension w.r.t. biodiversity and agricultural matters � Raising awareness of preferred farming methodologies � Raising awareness of endangered vegetation and uniqueness of biodiversity � Recommendations w.r.t. switching from flock to pen breeding or alternative

systems � Recommendations w.r.t. placing camsp � Recommendations w.r.t. rehabilitation methodology and options � Guidance w.r.t. stewardship options and participation � Collective farm level and area wide planning � Other recommendations

9.1.7 Ostrich Standards / “Best Practice” Guidelines

The Industry is currently engaging in a process whereby ostrich producers and processors are developing a “best practice” for biodiversity document based on the GlobalGAP® model. The function of the BU is to ensure that biodiversity “best practices” are incorporated in this document. Also to assist in obtaining the buy-in from the industry to adopt this document. “Tropparing” on natural veld being phased out to acceptable and legal levels – pen breeding and alternative practices being promoted, with continual research into improved or alternative strategies. Climate change adaptation to form part of this document – ostrich industry to calculate carbon footprint and plan to get it down – use as marketing tool.

9.1.8 Monitoring and Compliance

A long term biodiversity monitoring and compliance function will be established, with the following functions: � Establishing a working group to meet quarterly in order to streamline applications,

monitoring and system � This will include biological monitoring (including rehabilitation) in order to

measure successes and the benefit of the effect on the veld if ostriches are removed

� This will include the monitoring of the implementation of the biodiversity management plans per farm

� Establishing a system whereby non-compliance is identified, recommendations for rectification is given, and ultimately given over to NDA and temporarily de-registered

� Establishing a system whereby compliance is recognised and awarded � Monitoring carrying capacity -

9.1.9 Rehabilitation

Areas for effective rehabilitation, based on realistic goals for specific vegetation types, will be identified, business plans for rehabilitation will be drawn up and

23

rehabilitation will be implemented. Information sign boards along the road will be put up, adding to the awareness raising of the uniqueness of the area. A monitoring system will be established to ensure that veld is rehabilitated

9.1.10 Implementing Authority

The SAOBC and the BU will start engaging with partners i.t.o. sustainable funding for the Biodiversity Unit. The SAOBC will remain the implementing authority, until partners decide otherwise and it is so accepted by the PMT.

9.1.11 Potential Funding

Climate change strategy – Industry – rapid assessment (1 year) – build outcomes into best practice / De Beers / Nat Dept Agric / German funder – land management / Dept Science and Technology Strategic Climate Change Funding / Conservation International Biodiversity Unit: KKG/ Mosstrich / SAOBC / Partners Funding for training of permanent staff member in GIS - SAOBC Rehab – SKEPPIES / De Beers (Tessa Oliver) Capacity Building – CAPE CI – Sarshen Marais – CAP (Climate Action Partnership)

24

SECTION C: ALTERNATIVES TO FLOCK BREEDING The Ostrich Industry engages in various methods of ostrich breeding. This biodiversity management strategy focuses on pen breeding as the preferred alternative, as this methodology encourages continuous genetic improvement through proper record keeping and selection and shows huge potential for increased production. The rationale behind promoting pen breeding is to decrease the pressure on the natural veld – if a farmer can achieve increased production from a pen breeding system, he will take ostriches off the natural veld and do breeding in pens. However, many ostrich farmers show resistance to switch from flock breeding to pen breeding – for various reasons (ranging from lack of knowledge, costs of pen construction and management adaptation to preferring the current style of farming based on history). Alternative strategies to achieve the aim and vision of maintaining biodiversity within a sustainable production system thus have to be investigated, researched, proved and communicated. One of the strategies would be to consider “trade-offs” – i.e. to sacrifice portions of land (albeit endangered vegetation) for concentrated flock breeding. This would mean allowing more ostriches per hectare on natural veld than the prescribed stocking rate, BUT signing an agreement with the mandated conservation authority to improve veld management on other parts of the property. This would include making an official application to the Department of Environmental Affairs and Development Planning, for changed land use. Another strategy would be to investigate the optimum ostrich numbers in pen breeding systems. Where pen breeding normally houses 2, 3 or 4 ostriches per pen, it could be investigated to increase the number of ostriches per pen (and increasing the pen size). These and other strategies need to be work shopped with producers, processors, conservation authorities and other role-players.

25

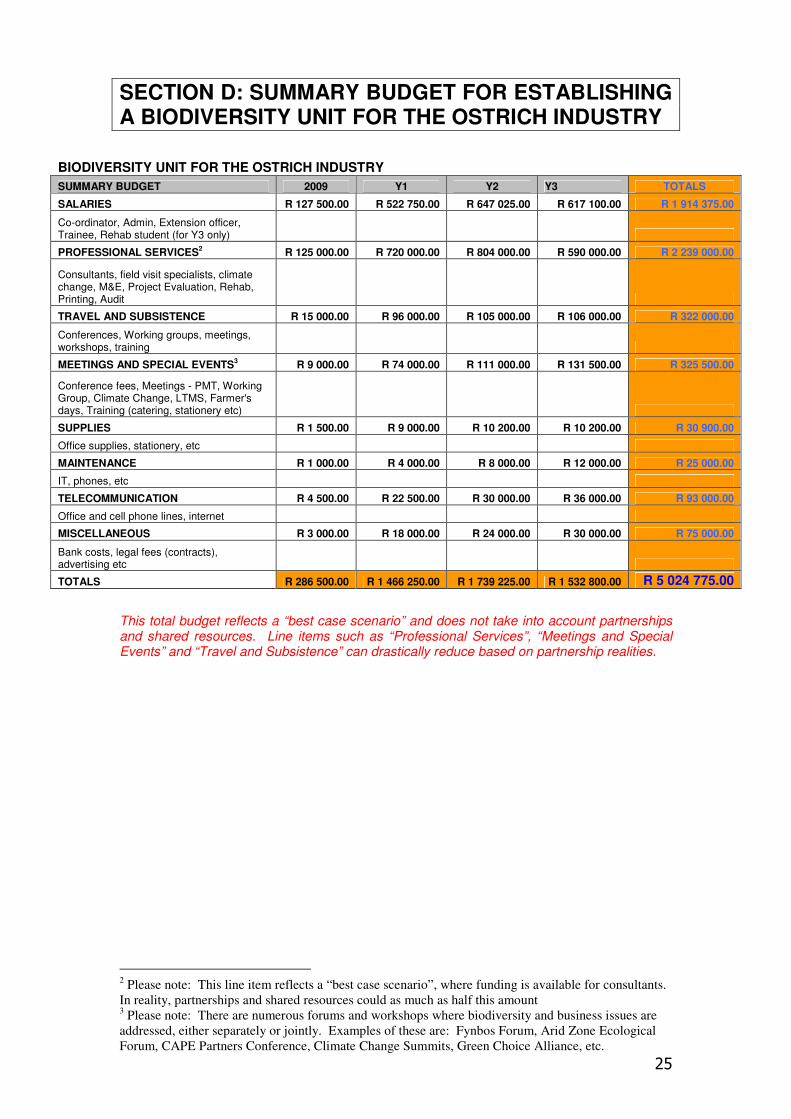

SECTION D: SUMMARY BUDGET FOR ESTABLISHING A BIODIVERSITY UNIT FOR THE OSTRICH INDUSTRY

This total budget reflects a “best case scenario” and does not take into account partnerships and shared resources. Line items such as “Professional Services”, “Meetings and Special Events” and “Travel and Subsistence” can drastically reduce based on partnership realities.

2 Please note: This line item reflects a “best case scenario”, where funding is available for consultants.

In reality, partnerships and shared resources could as much as half this amount 3 Please note: There are numerous forums and workshops where biodiversity and business issues are

addressed, either separately or jointly. Examples of these are: Fynbos Forum, Arid Zone Ecological

Forum, CAPE Partners Conference, Climate Change Summits, Green Choice Alliance, etc.

BIODIVERSITY UNIT FOR THE OSTRICH INDUSTRY

SUMMARY BUDGET 2009 Y1 Y2 Y3 TOTALS

SALARIES R 127 500.00 R 522 750.00 R 647 025.00 R 617 100.00 R 1 914 375.00

Co-ordinator, Admin, Extension officer, Trainee, Rehab student (for Y3 only)

PROFESSIONAL SERVICES2 R 125 000.00 R 720 000.00 R 804 000.00 R 590 000.00 R 2 239 000.00

Consultants, field visit specialists, climate change, M&E, Project Evaluation, Rehab, Printing, Audit

TRAVEL AND SUBSISTENCE R 15 000.00 R 96 000.00 R 105 000.00 R 106 000.00 R 322 000.00

Conferences, Working groups, meetings, workshops, training

MEETINGS AND SPECIAL EVENTS3 R 9 000.00 R 74 000.00 R 111 000.00 R 131 500.00 R 325 500.00

Conference fees, Meetings - PMT, Working Group, Climate Change, LTMS, Farmer's days, Training (catering, stationery etc)

SUPPLIES R 1 500.00 R 9 000.00 R 10 200.00 R 10 200.00 R 30 900.00

Office supplies, stationery, etc

MAINTENANCE R 1 000.00 R 4 000.00 R 8 000.00 R 12 000.00 R 25 000.00

IT, phones, etc

TELECOMMUNICATION R 4 500.00 R 22 500.00 R 30 000.00 R 36 000.00 R 93 000.00

Office and cell phone lines, internet

MISCELLANEOUS R 3 000.00 R 18 000.00 R 24 000.00 R 30 000.00 R 75 000.00

Bank costs, legal fees (contracts), advertising etc

TOTALS R 286 500.00 R 1 466 250.00 R 1 739 225.00 R 1 532 800.00 R 5 024 775.00

26

SECTION E: ADDENDUMS

ADDENDUM A: BIODIVERSITY IMPORTANCE OF THE KLEIN KAROO – Alan Wheeler (CapeNature)

South African Ostrich Business Chamber Biodiversity Management Project.

Long term biodiversity management strategy.

The importance of Little Karoo biodiversityThe importance of Little Karoo biodiversityThe importance of Little Karoo biodiversityThe importance of Little Karoo biodiversity.

A.D. Wheeler Western Cape Nature Conservation Board, Private Bag X658, Oudtshoorn 6620, South Africa. March 2009.

South Africa falls within two of the worlds six floral kingdoms, the Paleotropical Floral Kingdom and the Cape Floral Kingdom and is divided into 9 biomes (Mucina & Rutherford, 2004) representing the 9 major habitat types (Rouget et al. 2004) (Table 1). Biomes are major biotic communities, grouped according to dominant and co dominant plant life forms, vegetation structure, floristic community and climate (Rutherford & Westfall 1994). The Cape Floral Kingdom contains Fynbos, Forest, Nama Karoo, Succulent Karoo and Thicket biomes.

Table 1. The biomes of South Africa showing area in km2 covered by the biome, the percentage of South Africa covered by the biome and the percentage of the biome protected in Type 1 Protected Areas ((Rouget et al. 2004).

Biome Area (km2) % total area % protected

Fynbos 84,580 6.7 11

Grassland 373,984 29.5 1.9

Savanna 412,753 32.6 8.9

Albany Thicket 30,256 2.4 6.3

Wetlands 16,790 1.3 4.6

Desert 8,548 0.7 12.5

Forest 4,730 0.4 39.6

Succulent Karoo 85,207 6.7 3.1

Nama-karoo 250,069 19.7 0.6 In 2004 the South African National Spatial Biodiversity Assessment (Rouget et al. 2004) used priority scores obtained for species, habitats and ecological processes across the nine biomes to identify overall priority conservation areas in South Africa (Table 2).

27

Table 2: South Africa’s nine priority terrestrial conservation areas ((Rouget et al. 2004).

Priority terrestrial conservation areas

North Eastern Escarpment

Bushveld-Bankenveld

Wet Grasslands

Dry Grasslands

South Eastern Escarpment

Maputaland Pondoland

Albany Thicket and Wild Coast

Cape Floristic Region

Succulent Karoo

The Little Karoo is an east–west oriented valley in the semi desert Succulent Karoo biome located between two parallel mountain ranges that run along the south coast of the Western Cape of South Africa (Le Maitre et al. 2007). The Langeberg – Outeniqua - Tsitsikamma mountain range separates it from the coastal belt in the south and the Witteberg – Swartberg - Baviaanskloof mountain range separates it from the Great Karoo in the north. The area lies between 33 15 34.00 S and 20 30 23.40 E and extends roughly from the town of Uniondale in the east to Montagu in the west (Cupido 2005, Vlok et. al 2005). The mountains have relatively high rainfall (> 900 mm per year), but the Little Karoo lies in a rain shadow, receiving only 150–350 mm annually. The rainfall season occurs in summer in the east and in winter in the west (Le Maitre et al. 2007). The Little Karoo is recognised internationally as an area in which three of the 34 global biodiversity hotspots occur, the Succulent Karoo, Maputaland – Pondoland - Albany and the Cape Floristic Region Biodiversity hotspots (Mittermeier et al. 2005). Biodiversity hotspots are recognised as earth’s biologically richest and most endangered terrestrial eco-regions. Each contains at least 1500 species of vascular plants as endemic species and have lost 70% or more original habitat. In addition to its floral diversity, the biome is a centre of diversity for reptiles and many groups of invertebrates (Desmet and Cowling 2005). The following section uses information regarding the importance of Succulent Karoo biodiversity as described by Desmet and Cowling (2005) in Conservation Internationals Hotspots Revisited (Mittermeier et al. 2005). Plants The Succulent Karoo biodiversity hotspot has extraordinarily high plant endemism. It has the richest succulent plant diversity in the world. In total, there are more than 6,350 vascular plant species in this hotspot, nearly 2,440 of which are endemic (40 percent) and 936 (17%) of which are Red Data Listed (Driver et al. 2003). Local plant species richness is very high, with an average of 70 species found in 0.1 hectare test plots. Many plants in the Succulent Karoo, especially succulents, are specialists for a limited range of environmental conditions and are restricted to specific habitats. 80 genera of plants are found nowhere else in the world. The SKEP (Succulent Karoo Ecosystem programme) global plant list includes 6 356 species in 1 002 genera and 168 families. Approximately 29% of the flora is succulent plants and 18% geophytes. Twenty-six percent (1630) are strict endemics and 14% (905) are near-endemics (i.e. their centre of distribution is in the Succulent Karoo). Eighty

28

genera are endemic, mostly succulent and bulb genera. Seventeen percent (936) of Succulent Karoo plant species are Red Data Listed. Birds The avifauna of the Succulent Karoo includes more than 225 species. This includes the black harrier (Circus maurus), which has the most restricted range of the world’s 13 harrier species, Karoo bustard (Eupodotis vigorsii), Ludwig's bustard (Neotis ludwigii), Karoo chat (Cercomela schlegelii), dune lark (Certhilauda erythrochlamys), and dusky sunbird (Nectarinia fusca). Mammals There are roughly 75 mammal species in the Succulent Karoo hotspot, of which two are endemic: De Winton's golden mole (Cryptochloris wintoni), and the Namaqua dune mole rat (Bathyergus janetta). An important flagship species in the region is the Critically Endangered riverine rabbit (Bunolagus monticularis), found in the Succulent Karoo, and whose population is thought to have declined by 60 percent over the past 70 years. The endangered Cape Mountain Zebra occurs in Provincially Protected Areas in the Little Karoo. Reptiles Reptile diversity is relatively high in the Succulent Karoo, with more than 90 species, about 15 of which are endemic. All of the endemics are geckos and lizards, representing about a quarter of the nearly 60 gecko and lizard species in the hotspot. These endemics include seven species of girdled lizards of the genus Cordylus, including the armadillo girdled lizard (Cordylus cataphractus). This lizard has a heavily armoured body and spiny tail and is known for rolling into a tight ball when threatened. As in the rest of South Africa, tortoise diversity is very high in the Succulent Karoo, with seven species. Amphibians Amphibians are poorly represented in the Succulent Karoo with just over 20 species. All of these species are frogs (5 (29%) strict endemics). Freshwater fishes There are about 26 species of freshwater fish in the Succulent Karoo, none of which are endemic. Invertebrates Invertebrate diversity is quite high in the Succulent Karoo, and evidence suggests that more than half of the species in some insect groups are endemic. Of the 70 species of scorpions found in the hotspot, nearly 20 are endemic. Monkey beetles, which are almost exclusively found in southern Africa, are concentrated in the area. Along with many types of wasps and bees, these beetles pollinate the hotspot's diverse plant species. There are 177 recorded bee and termite species (68 (38%) strict endemics). Apart from being recognised internationally as one of the worlds most biologically diverse and most threatened environments, the Little Karoo has also been recognised as a critical biodiversity area at a more local level. The Little Karoo falls within an area (named the Central Little Karoo) identified by the biodiversity conservation initiative SKEP (Succulent Karoo Ecosystem Programme) as one of nine geographic priority areas of South Africa and Namibia for conservation in the Succulent Karoo biome (Driver et al. 2003). The Gouritz Initiative is another biodiversity conservation initiative in the area that has, through a number of scientific and stakeholder workshops, identified the area as a critically important biodiversity area. The Gouritz Initiative serves as an anchor project that aims to support a system of sustainable living landscapes that is representative of the regions biodiversity through the co-existence of all stakeholders.

29

One of the most revealing documents published recently in terms of the complexity and diversity of the Little Karoo vegetation and habitats is the Vegetation map of the Little Karoo (Vlok et al. 2005). This fine scale vegetation mapping project has revealed no less than 369 vegetation units in 56 habitat types that occur in the Little Karoo. As Vegetation maps serve as convenient and effective ways of mapping habitats (Rouget et al. 2004), and as it is recognised that the rich biodiversity of the Succulent Karoo is due to an extensive and complex array of habitat types derived from topographical and climatic diversity in the region’s rugged mountains and semi-arid shrublands (Driver et al. 2003) the vegetation map of the Little Karoo shows that the area encompasses a remarkable biological diversity. Each of the individual vegetation units constitute critical components of the Little Karoo environment that need to be understood before rational decisions and actions are taken to conserve the biodiversity of the region (Vlok et al. 2005).

Unfortunately much of this biodiversity has been degraded. A study of the transformation of Little Karoo vegetation (Thompson et al. 2005) shows a large proportion of the vegetation of the lower lying areas of the Little Karoo having undergone severe degradation. A conservation assessment by Reyers (2008) highlights the severity of the degradation showing that 25 vegetation units are critically endangered (there is less natural veld left than the minimum size needed to protect the unit), 29 vegetation units are endangered (there is less than the minimum area needed + 15%) and 30 vulnerable vegetation units (less than 60% of the vegetation type left). Kirkwood et al. (2007) show a high percentage of the Little Karoo vegetation in the ostrich farming areas in particular to be critically endangered or endangered. However, less than approximately 7.5% of the Succulent Karoo biome vegetation types (Vlok et al. 2005) in the Little Karoo are formally protected. The biome’s biodiversity is under pressure from a range of human impacts including crop agriculture, ostrich farming, overgrazing, illegal collection of fauna and flora, and anthropogenic climate change (Driver et al. 2003, Cupido 2005, Vlok and Coetzee 2008, Vlok and Schutte-Vlok 2008, Murray 2008, Shaw 2008). Hence the urgency to address the question of conservation targets (Desmet and Cowling 2004).

In the lower lying areas of the Little Karoo where ostrich farming is most predominant the degradation of biodiversity results in long term detrimental impacts that effect not only the ecological systems but also the agricultural potential of the land and the wellbeing of society. Apart from the reasons given above, there are numerous other reasons why biodiversity needs to be conserved in the Little Karoo and a few relevant to this chapter are briefly mentioned below.

The loss of vegetation usually results in the loss of soil through water and wind erosion. This has a direst impact on agriculture and biodiversity. Vegetation plays a crucial role in water retention and water infiltration into the soil by reducing rainfall splash effect, slowing water runoff, providing dead plant material mulch that serve as natural erosion barriers and creating suitable habitat for biological soil crusts (mosses and lichens) that are so important in keeping these systems healthy. The healthy environment in which vegetation diversity and cover is sound provides critical natural services in terms of preventing excessive water run-off on the Klein Karoo plains. This prevents excessive flooding events and prevents siltation of water courses. The cost of damage incurred by flooding events in the Klein Karoo is well known. Resilience of the ecological system is a crucial survival mechanism especially in harsh environments such as the Little Karoo. Plants interact, some provide suitable environments for seeds to germinate and grow, larger species provide protection from the sun, provide shade and keep soils cooler, others provide traps for wind blown seed and keep seed banks. Some species cover the gaps created by erosion or dying plants until other longer lived plants can develop. A diversity of plants allows for greater resilience to the impacts of periods of stress such as drought.

30

It has also been shown (Gelderblom 2006) that the open sky and unspoiled landscapes of the Little Karoo are the number one draw cards for tourism (a major economic sector of the Little Karoo). These are recognized critical tourist attractions. Degradation of biodiversity will have obvious impacts on this economic sector. As ostrich farming is the largest contributor to the economy of the Little Karoo and because this activity has had such an impact on the biodiversity of the area, improved ostrich farming methods need to be developed that will ensure the sustainability of the ostrich farming industry and the conservation of globally important biodiversity.

31

References: Cowling, R.M., Pressey R., Lombard A., Desmet P. and Ellis A. 1999. From representation to persistence: requirements for a sustainable reserve system in the species-rich Mediterranean-climate deserts of southern Africa. Diversity and Distributions 5:51–71. Cupido C. 2005. Assessment of veld utilization practices and veld condition in the Little Karoo. M.Sc. Thesis. Department of Conservation Ecology. University of Stellenbosch. Dean W. and S.J Milton (eds) 1999. The Karoo: ecological patterns and processes. Cambridge University Press, Cambridge, UK. Desmet P. and Cowling R. M. 2005. Succulent Karoo Biodiversity Hotspot. In Mittermeier, R. A., Gil, P.R., Hoffman, M., Pilgrim, J., Brooks, T., Mittermeier, C.G., Lamoreux, J., & de Fonseca, G.A.B. (2005) Hotspots Revisited: Earth's Biologically Richest and Most Endangered Ecoregions. The University of Chicago Press. Desmet P.G. and R. Cowling. 2004. Using the species–area relationship to set baseline targets for conservation. Ecology and Society 9(2). Driver A., Desmet P.G., Rouget M., Cowling R.M. and Maze K.E. 2003. Succulent Karoo Ecosystem Plan Biodiversity Component Technical Report. Cape Conservation Unit, Botanical Society of South Africa, Cape Town, South Africa. Driver A., Maze K. E., Rouget M., Lombard A.T., Nel J.j Turpie J.K., Cowling, R.M., Desmet,P.G., Goodman P., Harris J., Jonas Z., Reyers B., Sink K. and Strauss, T. 2005. National Spatial Biodiversity Assessment 2004. Priorities for Biodiversity Conservation in South Africa. Strelitzia 17. South African National Biodiversity Institute, Pretoria. Gelderblom C. 2006. What attracts tourists to the Little Karoo? Internal CSIR Technical Report. Kirkwood D., Ralston S., Manual J., Pence G. and Wolfaardt A. 2007. Integrated Biodiversity Layer for Land-use Decision making in the Western Cape. An unpublished biodiversity conservation assessment and compilation of existing products for the Western Cape. CapeNature, DEA&DP & SANBI. Le Maitre D. C., Milton S.J., Jarmain C., Colvin C.A., Saayman I. and Vlok J.H.J. 2007. Linking ecosystem services and water resources: landscape-scale hydrology of the Little Karoo. Frontiers in Ecology and the Environment. 5 (5): 261 – 270. Lombard A. T., Cowling R. M., Pressey R. L., and A. G. Rebelo. 2003. Effectiveness of land classes as surrogates for species in conservation planning for the Cape Floristic Region. Biological Conservation 112(1-2):45–62. Mittermeier, R. A., Gil, P.R., Hoffman, M., Pilgrim, J., Brooks, T., Mittermeier, C.G., Lamoreux, J., and de Fonseca, G.A.B. 2005. Hotspots Revisited: Earth's Biologically Richest and Most Endangered Ecoregions. The University of Chicago Press. Mittermeier R. A., Myers N., Thomsen J. B., da Fonseca G. A. B., and Olivieri S. 1998. Biodiversity hotspots and major tropical wilderness areas: approaches to setting conservation priorities. Conservation Biology 12:516–520. Mucina L. and Rutherford M.C. (eds.) 2004. Vegetation map of South Africa, Lesotho and Swaziland. Strelitzia 18. South African National Biodiversity Institute, Pretoria.

32