Embed Size (px)

Citation preview

CCH® CPELink Nonprofit Financial Statements

You will see controls at the bottom of the screen for adjusting

the volume and advancing slides.

The sidebar shows an outline of each slide and review

questions. You may use the sidebar to jump to a particular

slide at any time.

Materials, including a copy of your final exam questions, are

available to download from the top bar. The final exam is

available to take at the end of the course.

Nonprofit Financial Statements

Nonprofit Financial StatementsDiane E. Edelstein, CPA

©2020, CCH Incorporated. All Rights Reserved.

1

2

CCH® CPELink Nonprofit Financial Statements

3Nonprofit Financial Statements

Today’s Topics

• Big Picture

• The Financial Statements

• Unique Nonprofit Areas

• Other Tidbits

Nonprofit Financial Statements

The Big Picture

3

4

CCH® CPELink Nonprofit Financial Statements

5Nonprofit Financial Statements

Three Key Characteristics

Contributions

Operating Purpose

Absence of commercial ownership interest

6Nonprofit Financial Statements

Review Question 1

5

6

CCH® CPELink Nonprofit Financial Statements

7Nonprofit Financial Statements

Types of Not-for-Profit Entities

• Cemetery entities

• Civic and community entities

• Colleges and universities

• Elementary and secondary schools

• Federated fundraising entities

• Fraternal entities

• Health care entities (see discussion)

• Labor unions

• Libraries

• Museums

• Other cultural entities

• Performing arts entities

8Nonprofit Financial Statements

Types of Not-for-Profit Entities

• Political parties

• Political action committees

• Private and community foundations

• Professional associations

• Public broadcasting stations

• Religious entities

• Research and scientific entities

• Social and country clubs

• Trade associations

• Voluntary health and welfare entities

• Zoological and botanical societies

7

8

CCH® CPELink Nonprofit Financial Statements

9Nonprofit Financial Statements

Fund Accounting

• Many NFP entities use fund accounting for internal recordkeeping purposes.

• FASB ASC 958 requires reporting aggregated information about an organization’s net assets that are classified based solely on donor-imposed restrictions.

10Nonprofit Financial Statements

FASB ASC and Not-for-Profit Entities

• Because the FASB Accounting Standards Codification (ASC) contains incremental industry-specific guidance specifically for NFP entities (FASB ASC 958), it is important to be clear about which entities must follow the industry-specific guidance.

• Other parts of FASB apply the same to NFP and for-profits

• Leases

• Revenue Recognition

• Subsequent events.

9

10

CCH® CPELink Nonprofit Financial Statements

11Nonprofit Financial Statements

Unique Reporting Practices

• Contributions—NFP entities often receive substantial amounts of contributions. Recording and reporting contributions provides a unique challenge for NFP entities. In addition, many contributions contain restrictions and other conditions that must be reported and disclosed.

• Net Assets—What do we call the difference between assets and liabilities? For business, it is often referred to as “stockholder’s equity.” For an NFP organization, it is called “net assets.” In addition, net assets are further divided between net assets without donor restrictions and net assets with donor restrictions.

• Financial Statements—Because the financial reporting objectives are different for NFP entities, the financial statements are somewhat different from those of a business. The three general-purpose financial statements for an NFP entity are the statement of financial position, the statement of activities, and the statement of cash flows. NFP entities must also present an analysis of expenses by function and nature in one location. This may be presented in the notes, in the statement of activities or as a separate statement.

12Nonprofit Financial Statements

Unique Features of NFP F/S

• Importance of contributions

• Contributed services

• Net assets

• Donor-imposed restrictions

• Expenses disclosed by function

11

12

CCH® CPELink Nonprofit Financial Statements

13Nonprofit Financial Statements

Review Question 2

14Nonprofit Financial Statements

The Classification of Expenses

One key difference between NFPs and business entities is that NFPs have operating purposes other than to provide goods or services at a profit.

▪ Donors wish to see service efforts (program vs supportive costs)

▪ Creditors wish to see natural costs

13

14

CCH® CPELink Nonprofit Financial Statements

15Nonprofit Financial Statements

Program Services

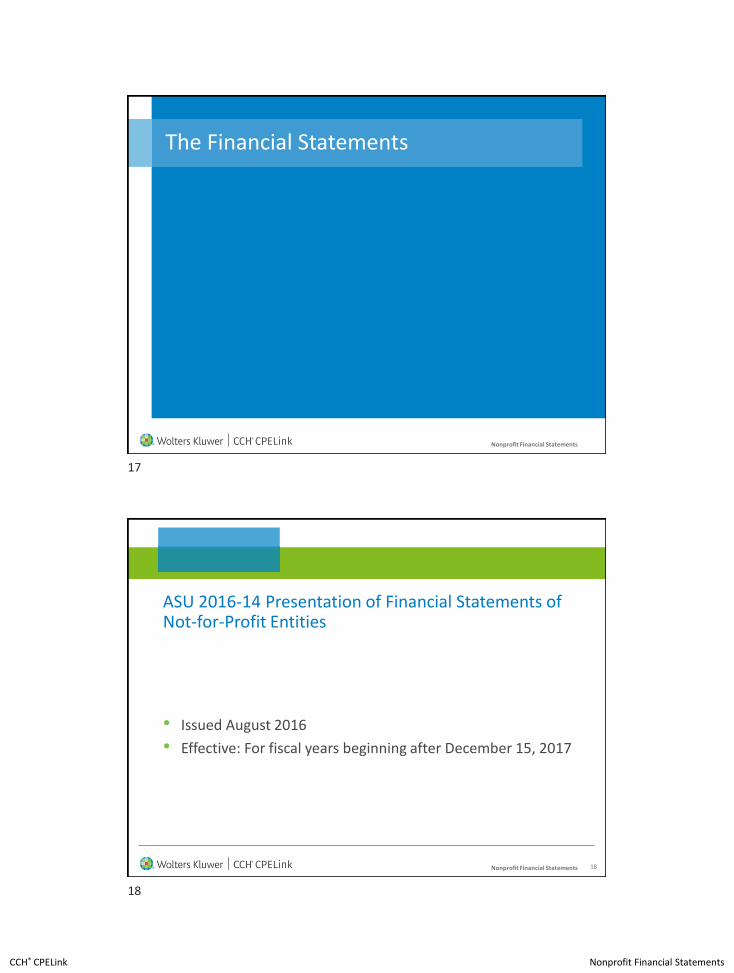

• Program

▪ Activities that result in goods and services being distributed to beneficiaries, members or customers that fulfill the purpose or mission for which the NFP exists

16Nonprofit Financial Statements

Supporting Activities

• Management and General

▪ Activities that are not directly identifiable with one or more program, fundraising, or membership development activities

• Fundraising

▪ Activities undertaken to induce potential donors to contribute money, securities, services, materials, facilities or other assets

• Membership Development

▪ Include soliciting for prospective members and membership dues, membership relations, and similar activities

15

16

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

The Financial Statements

18Nonprofit Financial Statements

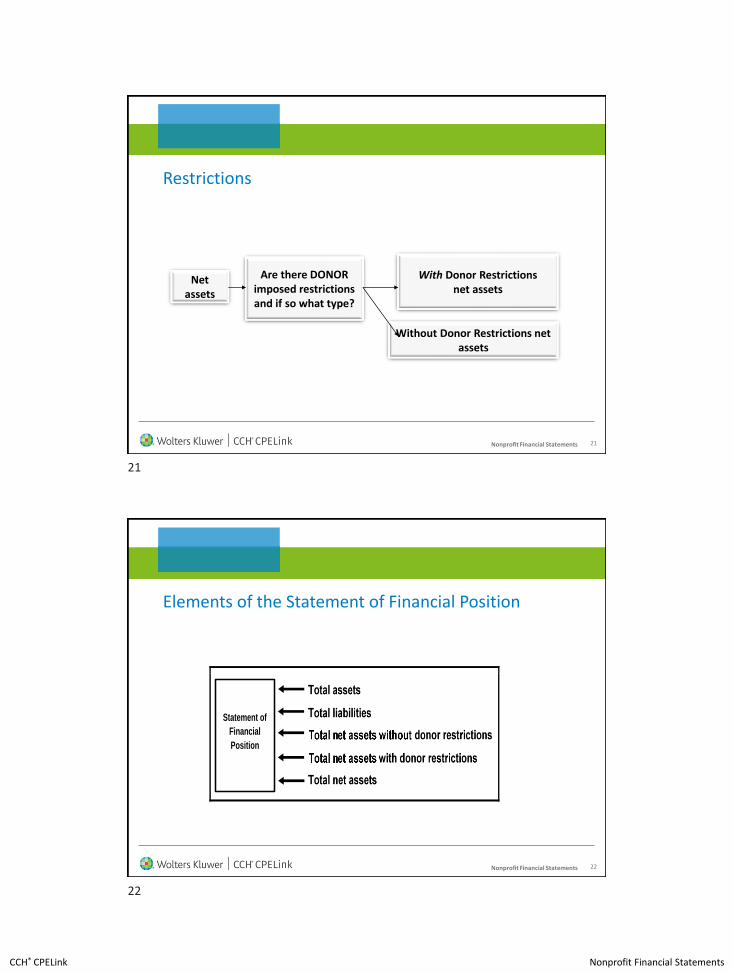

ASU 2016-14 Presentation of Financial Statements of Not-for-Profit Entities

• Issued August 2016

• Effective: For fiscal years beginning after December 15, 2017

17

18

CCH® CPELink Nonprofit Financial Statements

19Nonprofit Financial Statements

Basic Financial Statements

• Statement of financial position (balance sheet)

• Statement of activities

• Statement of cash flows

Report of expense by function is required:

can use a Statement of Functional expense

20Nonprofit Financial Statements

Statement of Financial Position

• Net Asset Classes

▪ Net Assets with Donor Restrictions

▪ Net Assets without Donor Restrictions

• Includes Board designated

• Liquidity & Availability

▪ Face & Notes

19

20

CCH® CPELink Nonprofit Financial Statements

21Nonprofit Financial Statements

Restrictions

Net assets

Are there DONOR imposed restrictions and if so what type?

With Donor Restrictionsnet assets

Without Donor Restrictions net assets

22Nonprofit Financial Statements

Elements of the Statement of Financial Position

Statement of

Financial

Position

21

22

CCH® CPELink Nonprofit Financial Statements

23Nonprofit Financial Statements

Review Question 3

24Nonprofit Financial Statements

Statement of Activities

While the primary focus of a business entity’s income statement is the entity’s net income or bottom line, the primary focus of an NFP’s statement of activities is how the NFP’s activities related to mission fulfillment. So, instead of reporting net income, NFPs report the change in net assets.

23

24

CCH® CPELink Nonprofit Financial Statements

25Nonprofit Financial Statements

Elements of the Statement of Activities

The

Statement of

Activities

26Nonprofit Financial Statements

Statement of Cash Flows

• Cash receipts from contributions restricted for long-term purposes (endowment or purchases of equipment) are financing activities.

• Otherwise, similar to a for-profit entity.

25

26

CCH® CPELink Nonprofit Financial Statements

27Nonprofit Financial Statements

NFP Cash Flows

• Operating

• Investing

• Financing

28Nonprofit Financial Statements

Statement of Cash Flows

• Use of either the direct or indirect method is allowed

• No longer required to show reconciliation of change in net assets to cash flows from operating activities if using direct method

27

28

CCH® CPELink Nonprofit Financial Statements

29Nonprofit Financial Statements

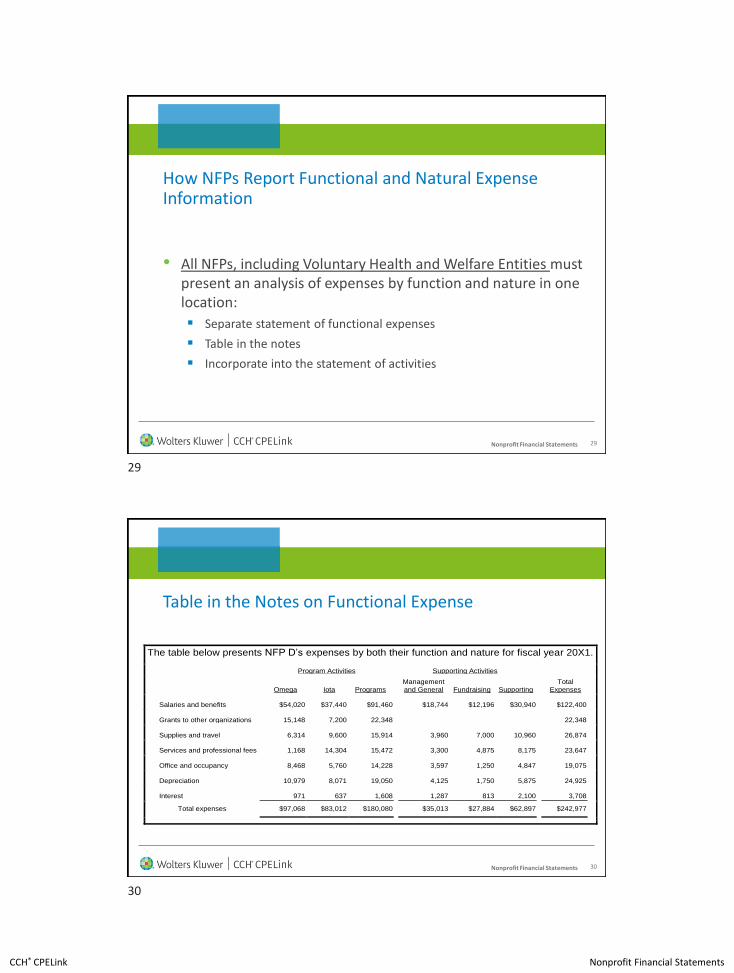

How NFPs Report Functional and Natural Expense Information

• All NFPs, including Voluntary Health and Welfare Entities must present an analysis of expenses by function and nature in one location:

▪ Separate statement of functional expenses

▪ Table in the notes

▪ Incorporate into the statement of activities

30Nonprofit Financial Statements

Table in the Notes on Functional Expense

The table below presents NFP D’s expenses by both their function and nature for fiscal year 20X1.

Program Activities Supporting Activities

Omega Iota Programs Management and General Fundraising Supporting

Total Expenses

Salaries and benefits $54,020 $37,440 $91,460 $18,744 $12,196 $30,940 $122,400

Grants to other organizations 15,148 7,200 22,348 22,348

Supplies and travel 6,314 9,600 15,914 3,960 7,000 10,960 26,874

Services and professional fees 1,168 14,304 15,472 3,300 4,875 8,175 23,647

Office and occupancy 8,468 5,760 14,228 3,597 1,250 4,847 19,075

Depreciation 10,979 8,071 19,050 4,125 1,750 5,875 24,925

Interest 971 637 1,608 1,287 813 2,100 3,708

Total expenses $97,068 $83,012 $180,080 $35,013 $27,884 $62,897 $242,977

29

30

CCH® CPELink Nonprofit Financial Statements

31Nonprofit Financial Statements

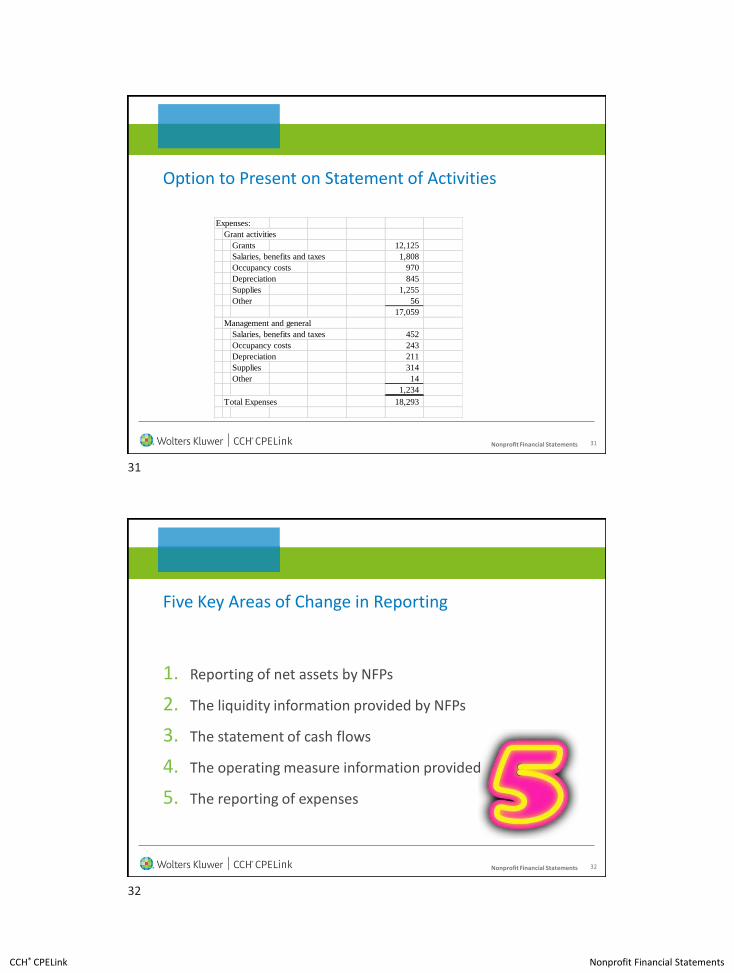

Option to Present on Statement of Activities

Expenses:

Grant activities

Grants 12,125

Salaries, benefits and taxes 1,808

Occupancy costs 970

Depreciation 845

Supplies 1,255

Other 56

17,059

Management and general

Salaries, benefits and taxes 452

Occupancy costs 243

Depreciation 211

Supplies 314

Other 14

1,234

Total Expenses 18,293

32Nonprofit Financial Statements

Five Key Areas of Change in Reporting

1. Reporting of net assets by NFPs

2. The liquidity information provided by NFPs

3. The statement of cash flows

4. The operating measure information provided

5. The reporting of expenses

31

32

CCH® CPELink Nonprofit Financial Statements

33Nonprofit Financial Statements

Review Question 4

Nonprofit Financial Statements

Reporting of Net Assets

33

34

CCH® CPELink Nonprofit Financial Statements

35Nonprofit Financial Statements

Reporting of Net Assets

A. Reducing and renaming the classifications of net assets

B. Emphasizing the amounts and purposes of board-designated net assets

C. Reporting expirations of restrictions on gifts related to long-lived assets

D. Reporting amounts related to underwater endowment funds

36Nonprofit Financial Statements

Reducing and Renaming Net Assets

• Unrestricted net assets become Net Assets without Donor Restriction

▪ Includes board designated

• Temporarily and Permanently restricted net assets are combined to become Net Assets with Donor Restriction

35

36

CCH® CPELink Nonprofit Financial Statements

37Nonprofit Financial Statements

Example from theStatement of Financial Position Presentation

Net Assets:

Without donor restrictions:

Undesignated 152,000

Board Designated 250,000

Total without donor restrictions 402,000

With donor restrictions 75,000

Total Net Assets: 477,000

Total Liabilities and Net Assets xxx,xxx

38Nonprofit Financial Statements

How a Statement of Activities Might Appear

Without Donor Restrictions

With Donor Restrictions Total

Revenues, gains, and other support:

Contributions $145,368 $56,776 $202,144

Fees 4,546 4,546

Investment return, net 63,181 63,670 126,851

Other 2,026 2,026

Net assets released from restrictions:

Satisfaction of program restrictions 25,058 (25,058)

Satisfaction of equipment acquisition

restrictions 4,000 (4,000)

Expiration of time restrictions 11,012 (11,012)

Appropriation from donor endowment and

subsequent satisfaction of any related donor

restrictions 6,000 (6,000)

Total net assets released from restrictions 46,070 (46,070)

Total revenues, gains, and other support 261,191 74,376 335,567

Expenses:

Program Omega 97,068 97,068

Program Iota 83,012 83,012

Management and general 35,013 35,013

Fundraising 27,884 27,884

Total expenses 242,977 242,977

Change in net assets 18,214 74,376 92,590

Net assets at beginning of year 244,571 297,836 542,407

Net assets at end of year $262,785 $372,212 $634,997

37

38

CCH® CPELink Nonprofit Financial Statements

39Nonprofit Financial Statements

Net Asset Disclosure Requirements

• Disclosure requirements

▪ Composition of net assets with donor restrictions

▪ Emphasis on how/when resources can be used

• Purpose

• Time

• Perpetual

40Nonprofit Financial Statements

Net Asset Disclosure Requirements

• NFPs will continue to provide information about the nature and amounts of different types of donor-imposed restrictions either by

▪ Reporting their amounts on the face of the statement of financial position

▪ Including relevant details in the notes to the financial statements.

39

40

CCH® CPELink Nonprofit Financial Statements

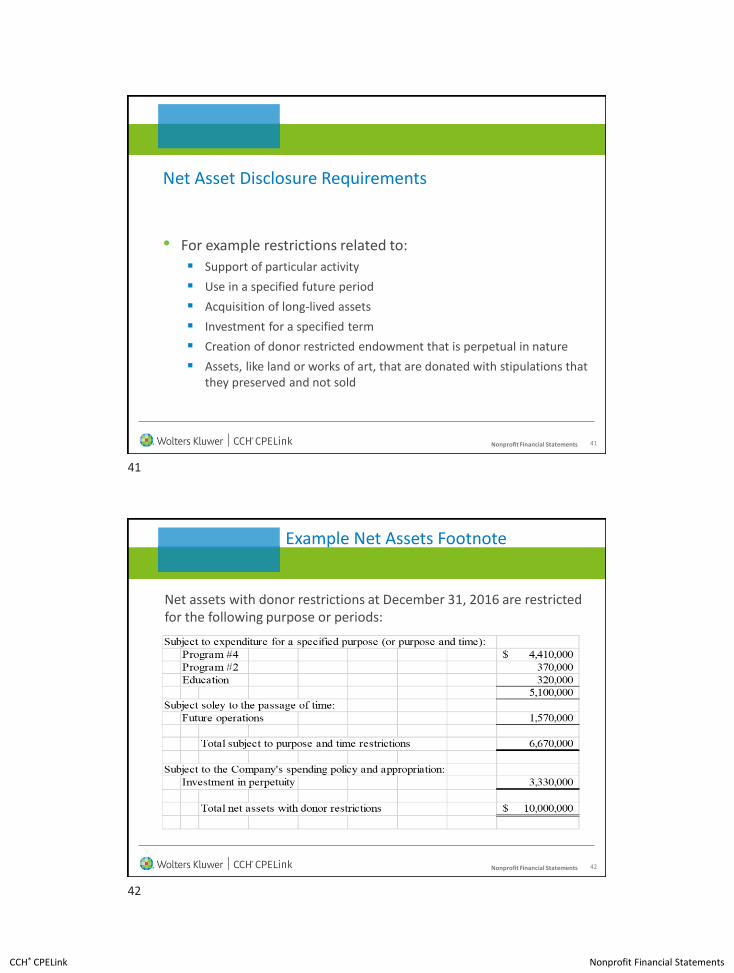

41Nonprofit Financial Statements

Net Asset Disclosure Requirements

• For example restrictions related to:

▪ Support of particular activity

▪ Use in a specified future period

▪ Acquisition of long-lived assets

▪ Investment for a specified term

▪ Creation of donor restricted endowment that is perpetual in nature

▪ Assets, like land or works of art, that are donated with stipulations that they preserved and not sold

42Nonprofit Financial Statements

Example Net Assets Footnote

Net assets with donor restrictions at December 31, 2016 are restricted for the following purpose or periods:

41

42

CCH® CPELink Nonprofit Financial Statements

43Nonprofit Financial Statements

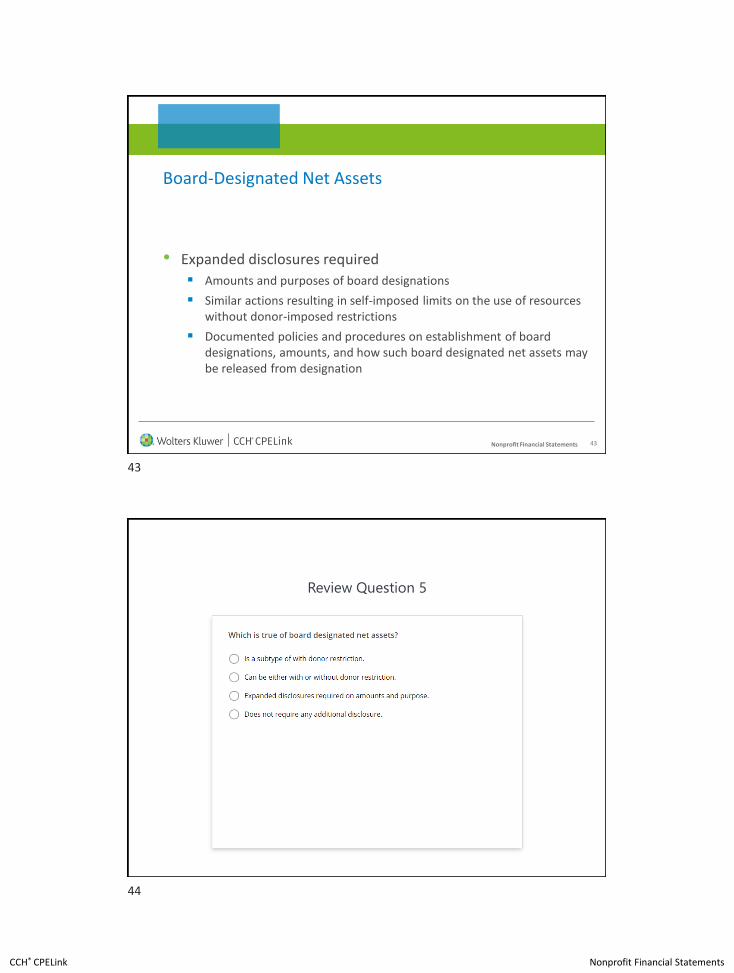

Board-Designated Net Assets

• Expanded disclosures required

▪ Amounts and purposes of board designations

▪ Similar actions resulting in self-imposed limits on the use of resources without donor-imposed restrictions

▪ Documented policies and procedures on establishment of board designations, amounts, and how such board designated net assets may be released from designation

44Nonprofit Financial Statements

Review Question 5

43

44

CCH® CPELink Nonprofit Financial Statements

45Nonprofit Financial Statements

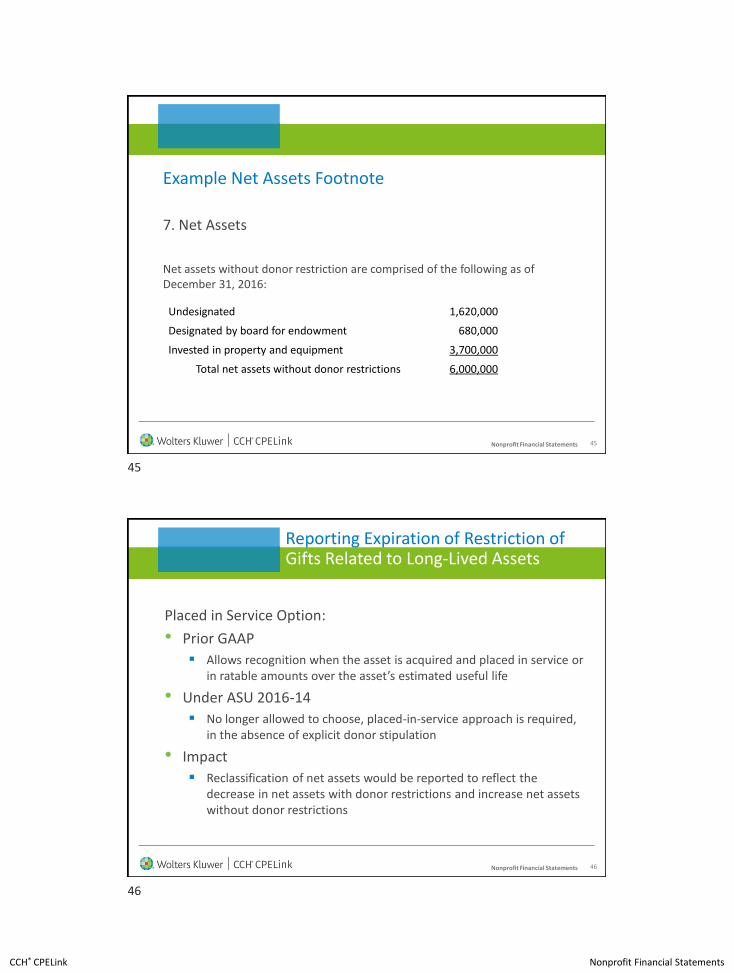

Example Net Assets Footnote

7. Net Assets

Net assets without donor restriction are comprised of the following as of December 31, 2016:

Undesignated 1,620,000

Designated by board for endowment 680,000

Invested in property and equipment 3,700,000

Total net assets without donor restrictions 6,000,000

46Nonprofit Financial Statements

Reporting Expiration of Restriction of Gifts Related to Long-Lived Assets

Placed in Service Option:

• Prior GAAP

▪ Allows recognition when the asset is acquired and placed in service or in ratable amounts over the asset’s estimated useful life

• Under ASU 2016-14

▪ No longer allowed to choose, placed-in-service approach is required, in the absence of explicit donor stipulation

• Impact

▪ Reclassification of net assets would be reported to reflect the decrease in net assets with donor restrictions and increase net assets without donor restrictions

45

46

CCH® CPELink Nonprofit Financial Statements

47Nonprofit Financial Statements

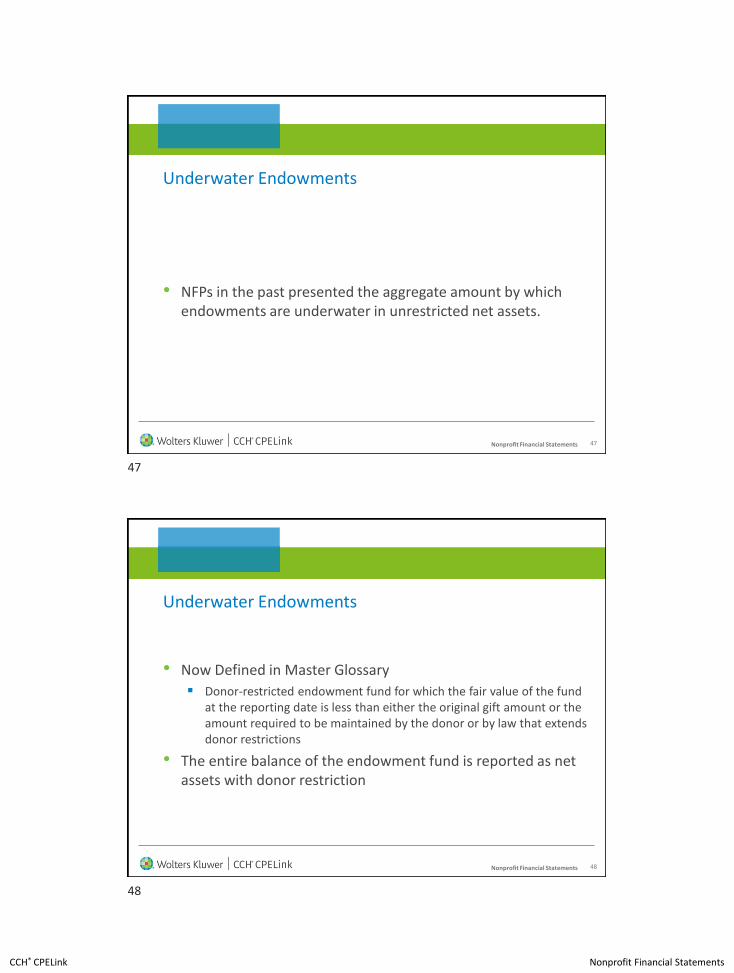

Underwater Endowments

• NFPs in the past presented the aggregate amount by which endowments are underwater in unrestricted net assets.

48Nonprofit Financial Statements

Underwater Endowments

• Now Defined in Master Glossary

▪ Donor-restricted endowment fund for which the fair value of the fund at the reporting date is less than either the original gift amount or the amount required to be maintained by the donor or by law that extends donor restrictions

• The entire balance of the endowment fund is reported as net assets with donor restriction

47

48

CCH® CPELink Nonprofit Financial Statements

49Nonprofit Financial Statements

Underwater Endowments

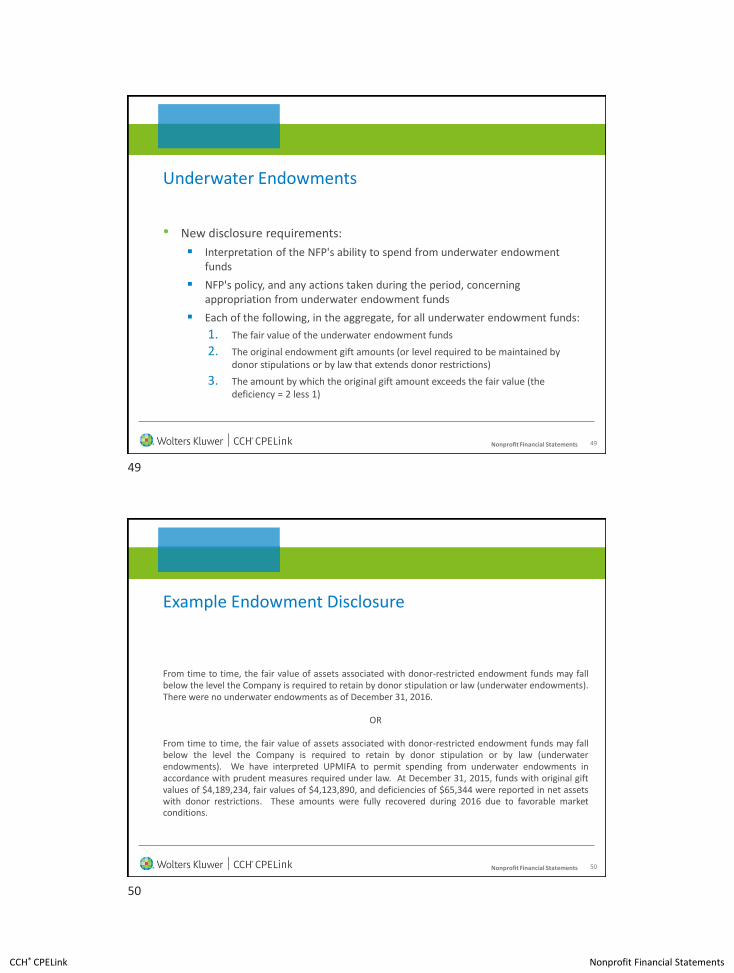

• New disclosure requirements:

▪ Interpretation of the NFP's ability to spend from underwater endowment funds

▪ NFP's policy, and any actions taken during the period, concerning appropriation from underwater endowment funds

▪ Each of the following, in the aggregate, for all underwater endowment funds:

1. The fair value of the underwater endowment funds

2. The original endowment gift amounts (or level required to be maintained by donor stipulations or by law that extends donor restrictions)

3. The amount by which the original gift amount exceeds the fair value (the deficiency = 2 less 1)

50Nonprofit Financial Statements

Example Endowment Disclosure

From time to time, the fair value of assets associated with donor-restricted endowment funds may fallbelow the level the Company is required to retain by donor stipulation or law (underwater endowments).There were no underwater endowments as of December 31, 2016.

OR

From time to time, the fair value of assets associated with donor-restricted endowment funds may fallbelow the level the Company is required to retain by donor stipulation or by law (underwaterendowments). We have interpreted UPMIFA to permit spending from underwater endowments inaccordance with prudent measures required under law. At December 31, 2015, funds with original giftvalues of $4,189,234, fair values of $4,123,890, and deficiencies of $65,344 were reported in net assetswith donor restrictions. These amounts were fully recovered during 2016 due to favorable marketconditions.

49

50

CCH® CPELink Nonprofit Financial Statements

51Nonprofit Financial Statements

Example Endowment Disclosure

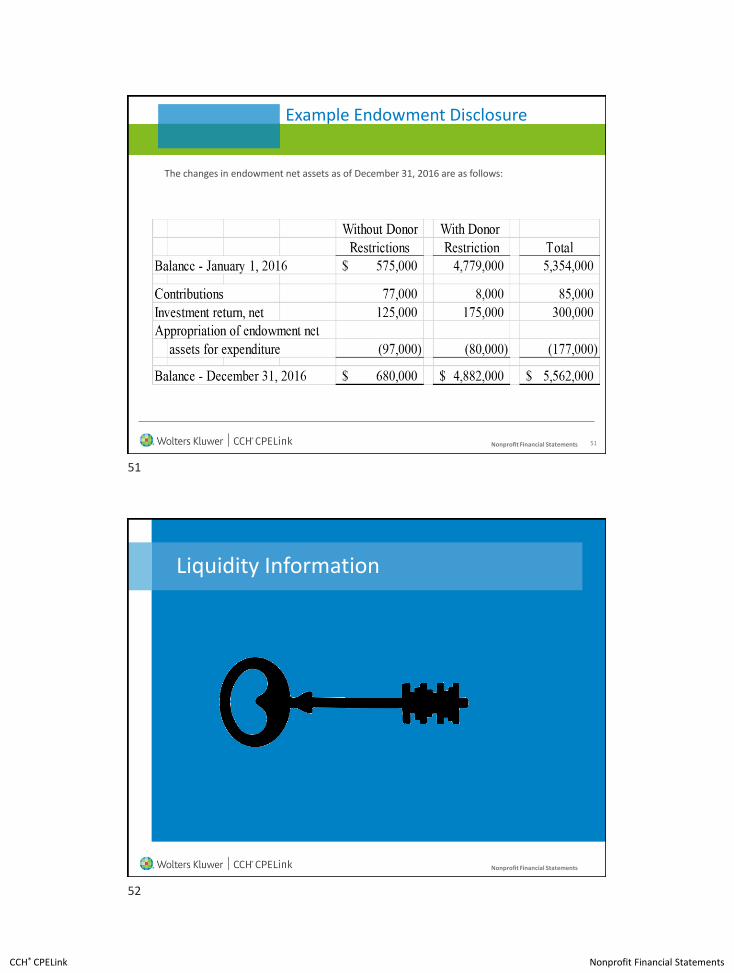

The changes in endowment net assets as of December 31, 2016 are as follows:

Nonprofit Financial Statements

Liquidity Information

51

52

CCH® CPELink Nonprofit Financial Statements

53Nonprofit Financial Statements

New Disclosures Required

• NFPs are required to provide information about liquidity by any of the following

▪ Sequencing assets according to their nearness of cash and sequencing liabilities according to nearness to maturity

▪ Classifying assets and liabilities as current and noncurrent

▪ Disclosing in the notes to the financial statements relevant information about the liquidity

54Nonprofit Financial Statements

New Disclosures Required

• Qualitative information on how an NFP manages its liquid resources available to meet cash needs for general expenditures within 1 year of the balance sheet date

• Quantitative information that communicates the availability of financial assets at the balance sheet date to meet cash needs for general expenditures within 1 year of the balance sheet date

53

54

CCH® CPELink Nonprofit Financial Statements

55Nonprofit Financial Statements

Liquidity and Availability Footnote

Liquidity and Availability

The Company manages its liquid resources by focusing on fundraising efforts to ensure theentity has adequate contributions and grants to cover the programs that are beingconducted. The Company prepares very detailed budgets and has been very active incutting costs to ensure the entity remains liquid.

As discussed in Note X, the Company maintains a line of credit to assist in meeting cashneeds if they experience a lag between the receipt of contributions and grants and thepayment of costs.

The following reflects the Company’s financial assets (cash and cash equivalents, pledgesreceivable, investments, and other assets) as of December 31, 2016 expected to be availablewithin one year to meet the cash needs for general expenditures.

56Nonprofit Financial Statements

Liquidity and Availability Footnote

55

56

CCH® CPELink Nonprofit Financial Statements

57Nonprofit Financial Statements

Review Question 6

Nonprofit Financial Statements

Statement of Cash Flows

57

58

CCH® CPELink Nonprofit Financial Statements

59Nonprofit Financial Statements

Statement of Cash Flows

• Use of either the direct or indirect method is allowed

• No longer required to show reconciliation of change in net assets to cash flows from operating activities if using direct method

60Nonprofit Financial Statements

Review Question 7

59

60

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

The Operating Measure Information Provided by Some NFPs

62Nonprofit Financial Statements

Operating Measure

• NFPs are allowed but not required to have a self-defined operating measure on the statement of activities. (Operating vs Non-Operating)

• If NFP chooses to do this, it is required to:

▪ Report the change in without donor restrictions

▪ If the use of the term operations is not apparent from the details, include a note to the financial statements describing the nature of the reported measure of operations.

61

62

CCH® CPELink Nonprofit Financial Statements

63Nonprofit Financial Statements

Operating Measure

• Under ASU No. 2016-14, NFPs will continue to follow current guidance. However, NFPs that choose to present internal board designations, appropriations, and similar actions on the face of the financial statements affecting that measure will have additional reporting requirements. Specifically, such NFPs will be required to report those types of internal transfers appropriately disaggregated and described by type, either on the face of the financial statements or in the notes.

64Nonprofit Financial Statements

Operating Measure – Why the change?

The term operating activates is currently not defined in NFP GAAP. A NFP is typically not required to provide any disclosure about its reported intermediate measure of operations other than describing the reported measure if that information is not apparent. The FASB noted that some NFPs report an operating measure on the statement of activities which is impacted by governing board designations, appropriations, and similar transfers. Some NFPs currently present these transfers as a single line item and it is difficult to determine if one or multiple transfers are occurring (and possibly being netted). FASB believes that such transfers can involve amounts that warrant separate line items or disclosures.

63

64

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Reporting of Expenses

66Nonprofit Financial Statements

Reporting of Expenses

A. Changing how investment expenses are reported

B. Providing additional information related to allocated costs

C. Refining/updating the definition of management and general activities

D. Adjusting how NFPs report functional and natural expense information

65

66

CCH® CPELink Nonprofit Financial Statements

67Nonprofit Financial Statements

Review Question 8

68Nonprofit Financial Statements

Investment Return

• Report net of all external and direct internal investment expenses

• No longer required disclose components of netted expenses

67

68

CCH® CPELink Nonprofit Financial Statements

69Nonprofit Financial Statements

Investment Return

• Internal expenses include the direct conduct or direct supervision of the strategic and tactical activities involved in generating investment return

▪ Salaries, benefits, travel, and other costs associated with staff responsible for development and execution of investment strategy, including supervision, selecting and monitoring external managers

▪ Excludes costs not associated with generating investment return, such as administrative management, contracts, pooled-fund administration

70Nonprofit Financial Statements

Additional Information Related to Allocated Costs

• A NFP is still required to disclose certain information related to joint costs (costs which are part fundraising and part other functional category)

• ASU No. 2016-14 requires including a description of the method(s) used to allocate costs among program and support functions

69

70

CCH® CPELink Nonprofit Financial Statements

71Nonprofit Financial Statements

Sample Disclosure Related to Allocated Costs

The financial statements of NFP B report certain categories of expenses that are attributable to more than one program or supporting function. Therefore, these expenses require allocation on a reasonable basis that is consistently applied. The expenses that are allocated include depreciation and occupancy costs, which are both allocated on a square footage basis, as well as salaries and benefits, which are allocated on the basis of time and effort studies.

72Nonprofit Financial Statements

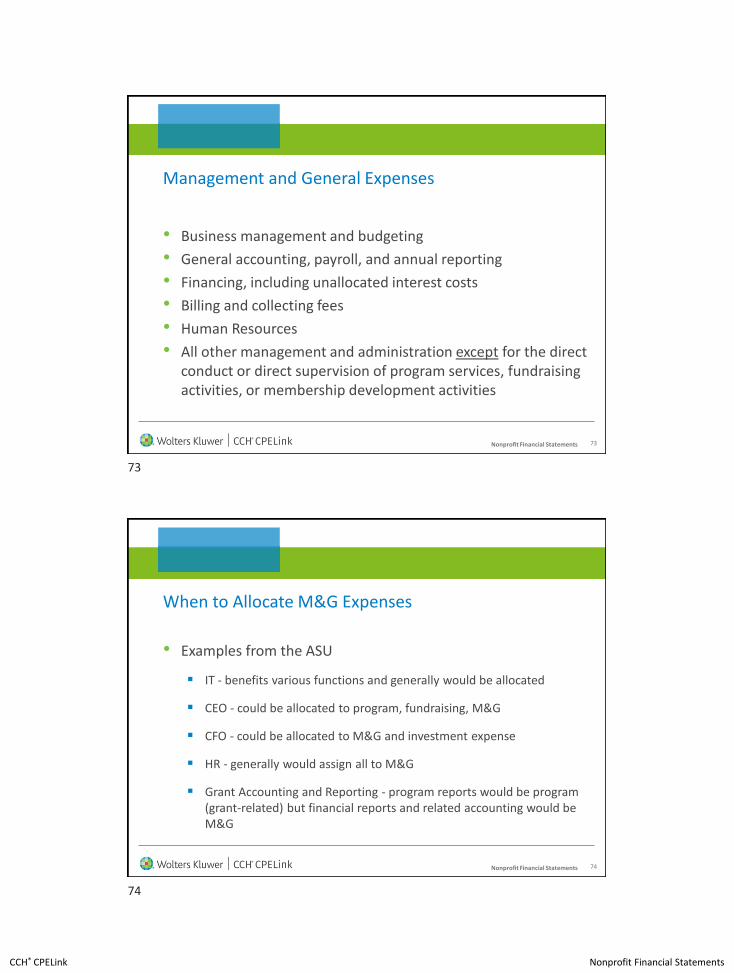

Refining/Updating the Definition of Management and General Activities

ASU No. 2016-14, management and general activities of NFPs will be defined as supporting activities that are not directly identifiable with one or more program, fundraising, or membership development

71

72

CCH® CPELink Nonprofit Financial Statements

73Nonprofit Financial Statements

Management and General Expenses

• Business management and budgeting

• General accounting, payroll, and annual reporting

• Financing, including unallocated interest costs

• Billing and collecting fees

• Human Resources

• All other management and administration except for the direct conduct or direct supervision of program services, fundraising activities, or membership development activities

74Nonprofit Financial Statements

When to Allocate M&G Expenses

• Examples from the ASU

▪ IT - benefits various functions and generally would be allocated

▪ CEO - could be allocated to program, fundraising, M&G

▪ CFO - could be allocated to M&G and investment expense

▪ HR - generally would assign all to M&G

▪ Grant Accounting and Reporting - program reports would be program (grant-related) but financial reports and related accounting would be M&G

73

74

CCH® CPELink Nonprofit Financial Statements

75Nonprofit Financial Statements

Adjusting how NFPs Report Functional and Natural Expense Information

• Over the years various opinions have been expressed on the importance of functional and natural expense information

▪ Creditors: Natural expense information more important that functional

▪ Donors/Rating Agencies: Functional expense information more important than natural

• From a recording standpoint, expenses generally originate in natural form and then require additional coding and allocation to get to functional

76Nonprofit Financial Statements

Adjusting how NFPs Report Functional and Natural Expense Information

• All NFPs, including Voluntary Health and Welfare Entities must present an analysis of expenses by function and nature in one location:

▪ Separate statement of functional expenses

▪ Table in the notes

▪ Incorporate into the statement of activities

75

76

CCH® CPELink Nonprofit Financial Statements

77Nonprofit Financial Statements

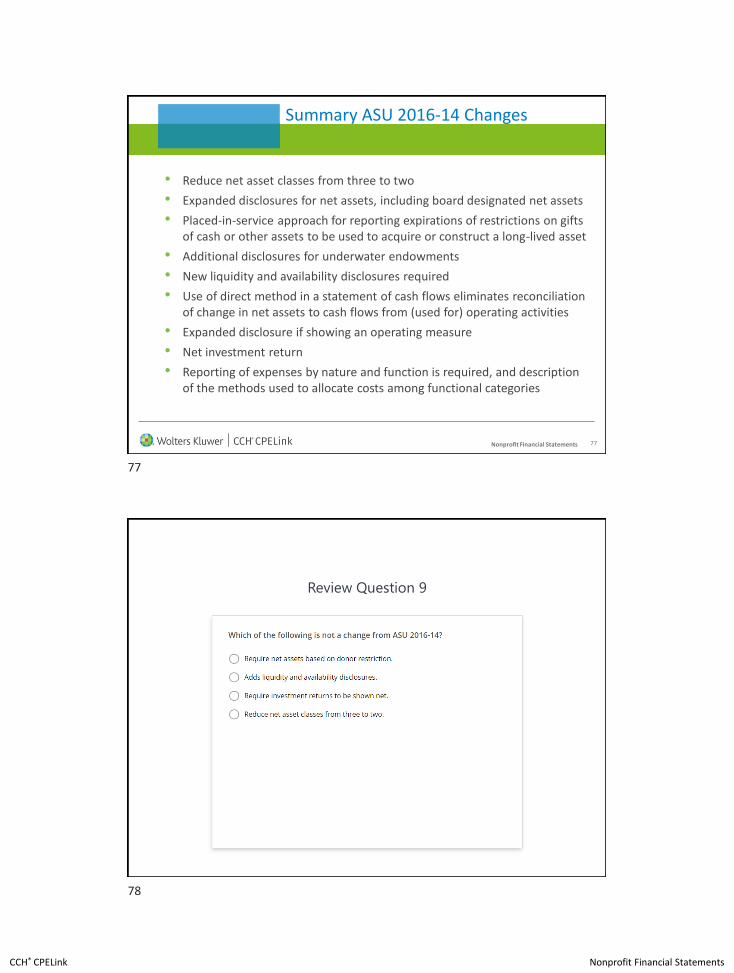

Summary ASU 2016-14 Changes

• Reduce net asset classes from three to two

• Expanded disclosures for net assets, including board designated net assets

• Placed-in-service approach for reporting expirations of restrictions on gifts of cash or other assets to be used to acquire or construct a long-lived asset

• Additional disclosures for underwater endowments

• New liquidity and availability disclosures required

• Use of direct method in a statement of cash flows eliminates reconciliation of change in net assets to cash flows from (used for) operating activities

• Expanded disclosure if showing an operating measure

• Net investment return

• Reporting of expenses by nature and function is required, and description of the methods used to allocate costs among functional categories

78Nonprofit Financial Statements

Review Question 9

77

78

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Note Disclosure

80Nonprofit Financial Statements

Example of Significant Accounting Policies

• Meaning of net asset classes

• Management estimates

• Definition of cash equivalents

• Prior year information

• Contributed services

• Other investments

• Intentions to give

• Implying time restrictions

• Cost allocations, including joint costs

• Revenue recognition

79

80

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Financial Reporting Options

82Nonprofit Financial Statements

Financial Reporting Options

• Present one year only

• Present comparative statements

• Present with comparative totals

81

82

CCH® CPELink Nonprofit Financial Statements

83Nonprofit Financial Statements

Comparative Information

Just labeling prior-year summarized financial information “for comparative purposes only” without further disclosure in the notes to the financial statements would not constitute the use of an appropriate title.

Nonprofit Financial Statements

Unique Nonprofit Areas

83

84

CCH® CPELink Nonprofit Financial Statements

85Nonprofit Financial Statements

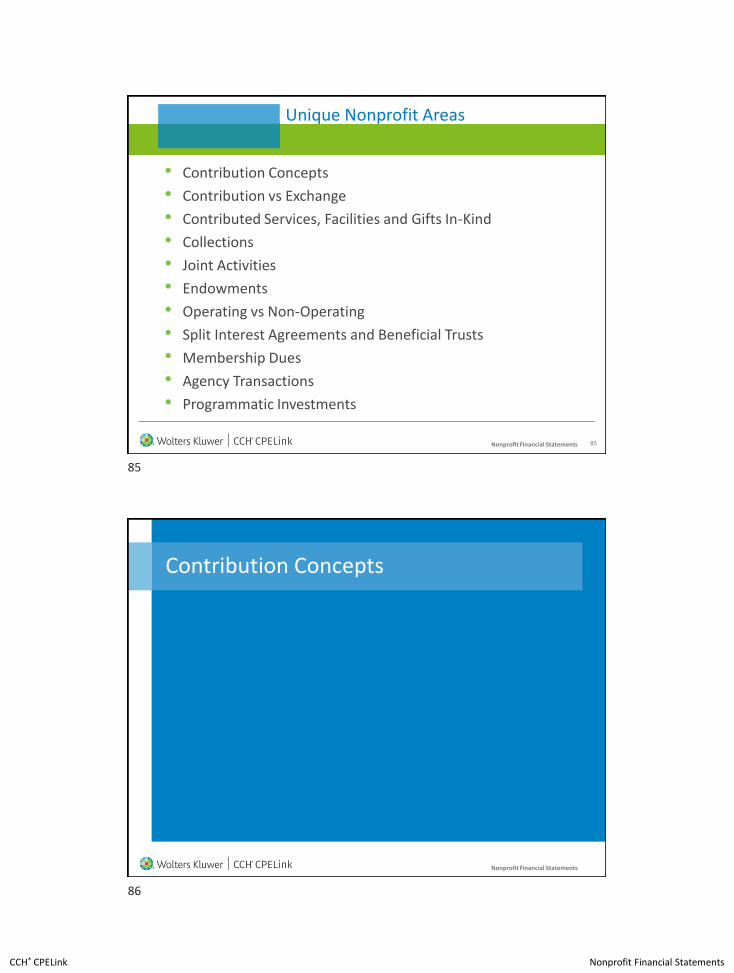

Unique Nonprofit Areas

• Contribution Concepts

• Contribution vs Exchange

• Contributed Services, Facilities and Gifts In-Kind

• Collections

• Joint Activities

• Endowments

• Operating vs Non-Operating

• Split Interest Agreements and Beneficial Trusts

• Membership Dues

• Agency Transactions

• Programmatic Investments

Nonprofit Financial Statements

Contribution Concepts

85

86

CCH® CPELink Nonprofit Financial Statements

87Nonprofit Financial Statements

Definition

• The FASB defines a contribution in ASC 958 as

▪ an unconditional transfer of cash or other assets to an entity or a settlement or cancellation of its liabilities in a voluntary nonreciprocaltransfer by another entity acting other than as an owner.

• ASU 2018-08 “Clarifying the Scope and the Accounting Guidance for Contributions Received and Contributions made” effective for periods beginning after December 15, 2018 has further clarified conditional contributions for the resource recipient.

88Nonprofit Financial Statements

Key Contribution Recognition and Disclosure Requirements

• Core recognition and measurement

▪ Donor-imposed conditions

▪ Donor-imposed restrictions

▪ Measure at fair value

• Unconditional promises to give

• Intentions to give

87

88

CCH® CPELink Nonprofit Financial Statements

89Nonprofit Financial Statements

Contribution Recognition

• Clarification of explicit and implicit restrictions

▪ When to imply time restrictions

• Pledges due in less than a year

• Multi-year pledges/long term pledges

Nonprofit Financial Statements

Contribution versus Exchange Transaction

89

90

CCH® CPELink Nonprofit Financial Statements

91Nonprofit Financial Statements

Definitions

• Contribution

▪ an unconditional transfer of cash or other assets to an entity or a settlement or cancellation of its liabilities in a voluntary nonreciprocal transfer by another entity acting other than as an owner.

• Exchange Transaction

▪ a reciprocal transfer between two entities that results in one of the entities acquiring assets or services or satisfying liabilities by surrendering other assets or services or incurring other obligations.

92Nonprofit Financial Statements

Accounting

• Part contribution/part exchange

▪ Membership

▪ Dinners

▪ Golf outings

▪ Girl Scout cookies

91

92

CCH® CPELink Nonprofit Financial Statements

93Nonprofit Financial Statements

Review Question 10

94Nonprofit Financial Statements

Indicators

• Recipient not-for-profit entity’s (NFP’s) intent in soliciting the asset

• Resource provider’s expressed intent about the purpose of the asset to be provided by recipient NFP

• Method of delivery

• Method of determining amount of payment

• Penalties assessed if NFP fails to make timely delivery of assets

• Delivery of assets to be provided by the recipient NFP

93

94

CCH® CPELink Nonprofit Financial Statements

95Nonprofit Financial Statements

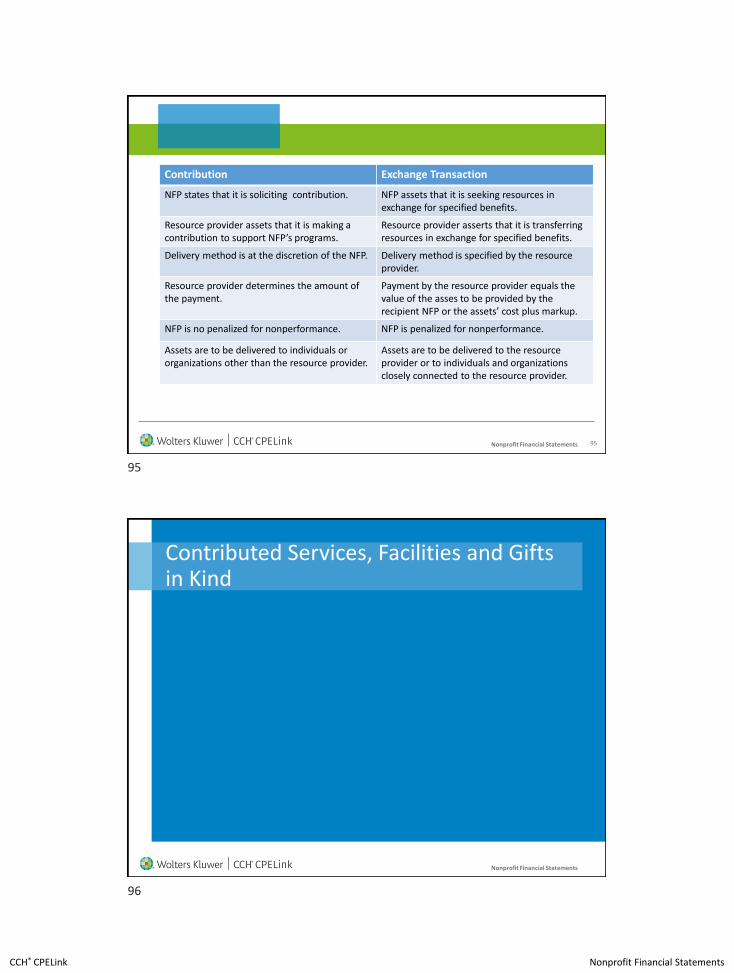

Contribution Exchange Transaction

NFP states that it is soliciting contribution. NFP assets that it is seeking resources in exchange for specified benefits.

Resource provider assets that it is making a contribution to support NFP’s programs.

Resource provider asserts that it is transferring resources in exchange for specified benefits.

Delivery method is at the discretion of the NFP. Delivery method is specified by the resource provider.

Resource provider determines the amount of the payment.

Payment by the resource provider equals the value of the asses to be provided by the recipient NFP or the assets’ cost plus markup.

NFP is no penalized for nonperformance. NFP is penalized for nonperformance.

Assets are to be delivered to individuals or organizations other than the resource provider.

Assets are to be delivered to the resource provider or to individuals and organizations closely connected to the resource provider.

Nonprofit Financial Statements

Contributed Services, Facilities and Gifts in Kind

95

96

CCH® CPELink Nonprofit Financial Statements

97Nonprofit Financial Statements

Contributed Services

• Record if they create or enhance a nonfinancial asset

OR

• if they typically would be purchased; and

• if they require specialized skills; and

• if they are performed by individuals that possess those skills.

98Nonprofit Financial Statements

Examples of Specialized Skills

Accountants, architects, carpenters, doctors, electricians, lawyers, nurses, plumbers, teachers, and other professionals and craftsmen.

97

98

CCH® CPELink Nonprofit Financial Statements

99Nonprofit Financial Statements

Gifts in Kind

• Gifts in kind that can be used or sold should be measured at fair value.

• Proper valuation

100Nonprofit Financial Statements

Review Question 11

99

100

CCH® CPELink Nonprofit Financial Statements

101Nonprofit Financial Statements

Use of Long-Lived Assets

The not-for-profit organization should report a contribution for the difference between the fair rental value of the property and the stated amount of the lease payments.

Nonprofit Financial Statements

Collections

101

102

CCH® CPELink Nonprofit Financial Statements

103Nonprofit Financial Statements

Collections

Works of art, historical treasures, or similar assets that are (a) held for public exhibition, education, or research in furtherance of public service rather than financial gain; (b) protected, kept unencumbered, cared for, and preserved; and (c) subject to an organizational policy that requires the proceeds of items that are sold to be used to acquire other items for collections.

ASU 2019-03 adds; to support the direct care of existing collections. (effective 12/31/2020 YE, can early adopt)

104Nonprofit Financial Statements

Collection Options

• Capitalization

• No capitalization

This Photo by Unknown Author is licensed under CC BY-SA

103

104

CCH® CPELink Nonprofit Financial Statements

105Nonprofit Financial Statements

Review Question 12

106Nonprofit Financial Statements

Recognition

• Capitalized

▪ Purchased or acquired

▪ Donated

• Not part of a collection

• Not-capitalized still catalogued, and protected

105

106

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Joint Activities

108Nonprofit Financial Statements

Expense Types

• Program

• Fund-raising

• Supporting

107

108

CCH® CPELink Nonprofit Financial Statements

109Nonprofit Financial Statements

Cost Allocation

• Direct—tracing

• Indirect—allocation

110Nonprofit Financial Statements

Joint Activities

A joint activity is an activity that is part of the fundraising function and has elements of one or more other functions, such as programs, management and general, membership development, or any other functional category used by the entity.

109

110

CCH® CPELink Nonprofit Financial Statements

111Nonprofit Financial Statements

Three Criteria

If the criteria of purpose, audience, and content are met, the costs of a joint activity that are identifiable with a particular function should be charged to that function and joint costs should be allocated between fundraising and the appropriate program or management and general function.

112Nonprofit Financial Statements

Joint Costs

• Joint costs are the costs of conducting joint activities that are not identifiable with a particular component of the activity.

• For example, the cost of postage for a letter that includes both fundraising and program components is a joint cost.

• Joint costs may include the costs of salaries, contract labor, consultants, professional fees, paper, printing, postage, event advertising, telephones, airtime, and facility rentals.

111

112

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Endowments

114Nonprofit Financial Statements

Endowment

• Definition of donor-restricted endowment fund

▪ an endowment fund that is created by a donor stipulation requiring investment of the gift in perpetuity or for a specified term. Some donors may require that a portion of income, gains, or both be added to the gift and invested subject to similar restrictions

113

114

CCH® CPELink Nonprofit Financial Statements

115Nonprofit Financial Statements

Underwater Endowments

• Now Defined in Master Glossary

▪ Donor-restricted endowment fund for which the fair value of the fund at the reporting date is less than either the original gift amount or the amount required to be maintained by the donor or by law that extends donor restrictions

• The entire balance of the endowment fund is reported as net assets with donor restriction

116Nonprofit Financial Statements

Underwater Endowments

• New disclosure requirements:

▪ Interpretation of the NFP's ability to spend from underwater endowment funds

▪ NFP's policy, and any actions taken during the period, concerning appropriation from underwater endowment funds

▪ Each of the following, in the aggregate, for all underwater endowment funds:

1. The fair value of the underwater endowment funds

2. The original endowment gift amounts (or level required to be maintained by donor stipulations or by law that extends donor restrictions)

3. The amount by which the original gift amount exceeds the fair value (the deficiency = 2 less 1)

115

116

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Operating versus Non-Operating

118Nonprofit Financial Statements

Additional Classifications

• Classifying revenues, expenses, gains, and losses within classes of net assets does not preclude incorporating additional classifications within a statement of activities.

• For example, within a class or classes of net assets, an NFP may classify items as follows: operating and nonoperating, expendable and nonexpendable, earned and unearned, recurring and nonrecurring, or in other ways.

117

118

CCH® CPELink Nonprofit Financial Statements

119Nonprofit Financial Statements

Intermediate Measure of Operations(Excess or Deficit of Operating Revenues Over Expenses)

Operations is not defined in the standards.

So if a measure is used, must be clear in the statement of activities or described in notes.

120Nonprofit Financial Statements

Review Question 13

119

120

CCH® CPELink Nonprofit Financial Statements

121Nonprofit Financial Statements

Operating Measure

Under ASU No. 2016-14, NFPs that choose to present internal board designations, appropriations, and similar actions on the face of the financial statements affecting that measure will have additional reporting requirements. Specifically, such NFPs will be required to report those types of internal transfers appropriately disaggregated and described by type, either on the face of the financial statements or in the notes.

122Nonprofit Financial Statements

Financial Statement Flexibility

The statement of activities focuses on the entity as a whole and must report certain totals for the period. Entities have significant flexibility

• Disaggregate information by using columns

• Revenues, gains, expenses, losses and reclassifications can be arranged in a variety of orders

• Report some intermediate measure of operations

121

122

CCH® CPELink Nonprofit Financial Statements

123Nonprofit Financial Statements

Example Entities

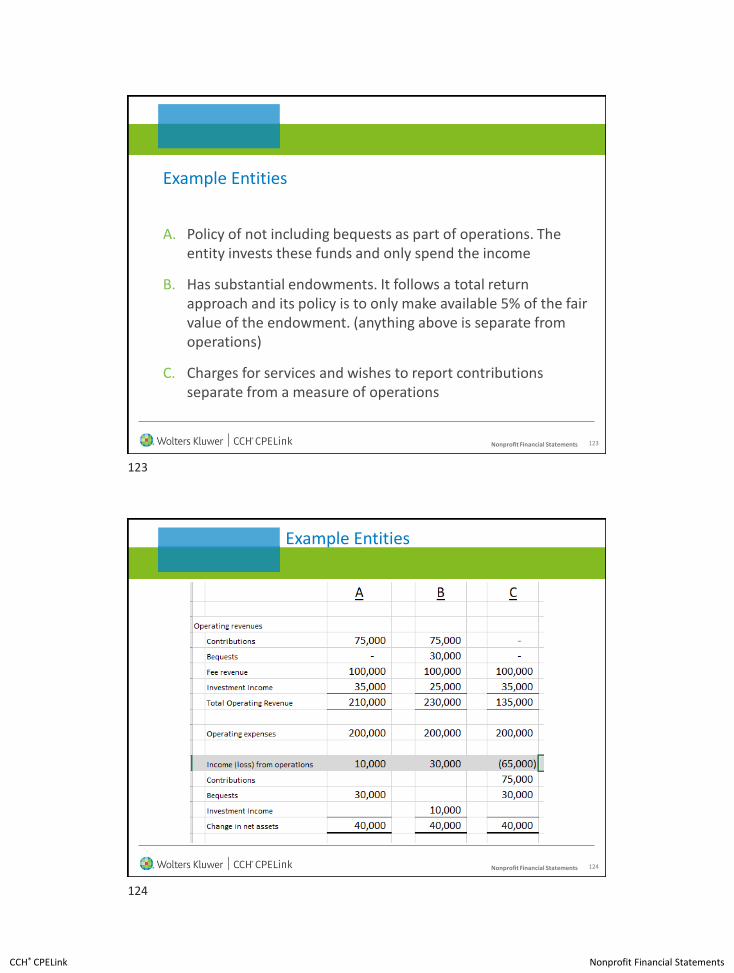

A. Policy of not including bequests as part of operations. The entity invests these funds and only spend the income

B. Has substantial endowments. It follows a total return approach and its policy is to only make available 5% of the fair value of the endowment. (anything above is separate from operations)

C. Charges for services and wishes to report contributions separate from a measure of operations

124Nonprofit Financial Statements

Example Entities

123

124

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Split Interest Agreements and Beneficial Trusts

126Nonprofit Financial Statements

Split-Interest Agreement

• Trust or other arrangements initiated by donors under which not-for-profit organizations receive benefits that are shared with either the donor or third-party beneficiaries.

• These gifts include lead interests and remainder interests.

125

126

CCH® CPELink Nonprofit Financial Statements

127Nonprofit Financial Statements

Revocable

• Treated as intentions to give

• Not recorded

• Possible footnote disclosure

128Nonprofit Financial Statements

Charitable Lead Trust

• A trust established in connection with a split-interest agreement, in which the not-for-profit organization receives distributions during the agreement’s term.

• Upon termination of the trust, the remainder of the trust assets is paid to the donor or to third-party beneficiaries designated by the donor.

127

128

CCH® CPELink Nonprofit Financial Statements

129Nonprofit Financial Statements

Charitable Remainder Trust

• A trust established in connection with a split-interest agreement, in which the donor or a third-party beneficiary receives specified distributions during the agreement’s term.

• Upon termination of the trust, a not-for-profit organization receives the assets remaining in the trust.

Nonprofit Financial Statements

Membership Dues

129

130

CCH® CPELink Nonprofit Financial Statements

131Nonprofit Financial Statements

Is it Contribution or Exchange

• Recipient NFP’s expressed intent concerning purpose of dues payment

• Extent of benefits to members

• NFP’s service efforts

• Duration of benefits

• Expressed agreement concerning refundability of the payment

• Qualifications for membership

132Nonprofit Financial Statements

Review Question 14

131

132

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Agency Transactions

134Nonprofit Financial Statements

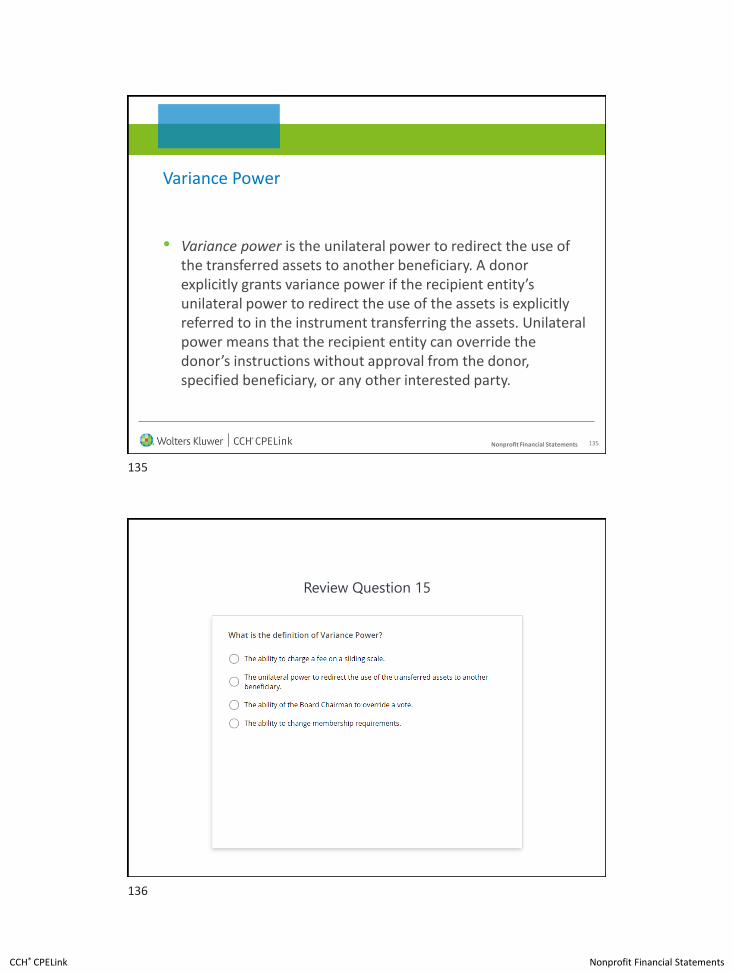

Transfers of Assets to an NFP or Charitable Trust That Raises or Holds Contributions for Others

Resource Provider

or Donor

Recipient

Organization

Specified

Beneficiary

133

134

CCH® CPELink Nonprofit Financial Statements

135Nonprofit Financial Statements

Variance Power

• Variance power is the unilateral power to redirect the use of the transferred assets to another beneficiary. A donor explicitly grants variance power if the recipient entity’s unilateral power to redirect the use of the assets is explicitly referred to in the instrument transferring the assets. Unilateral power means that the recipient entity can override the donor’s instructions without approval from the donor, specified beneficiary, or any other interested party.

136Nonprofit Financial Statements

Review Question 15

135

136

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Programmatic Investments

138Nonprofit Financial Statements

Programmatic Investments

• Three types of PI

▪ Loans

▪ Equity interests

▪ Guarantees

137

138

CCH® CPELink Nonprofit Financial Statements

139Nonprofit Financial Statements

Programmatic Investments

• PI is any investment by a not-for-profit that meets the following two criteria:

1. Its purpose is to further the tax exempt objectives of the NFP.

2. A market return (income or asset appreciation) is not a significant purpose of the investment.

140Nonprofit Financial Statements

Programmatic Investments

• Assess whether the initial investment transaction is a PI.

▪ Determine if the PI contains a contribution element because, by definition, a market return is not a significant element.

▪ Loans, equity interest, and guarantees PI are subject to the same accounting standards as other investments, except for any contribution element.

▪ The relative significance of the investments to an NFP’s operations and financial position and the quantitative and qualitative risks associated with them is considered for financial statement presentation and disclosures, even if the amount may be considered immaterial.

139

140

CCH® CPELink Nonprofit Financial Statements

Nonprofit Financial Statements

Other Tidbits

142Nonprofit Financial Statements

Other Tidbits

• All nonprofits except for churches file 990 with the IRS

• Most states require registration of nonprofits soliciting contribution

• Audits are not always required

• Federal funds $750,000 and more will require a Single Audit

141

142

CCH® CPELink Nonprofit Financial Statements

143Nonprofit Financial Statements

Final Takeaways

• Nonprofits final goal is mission

• Nonprofits needs financial resources to pay their bills

• Nonprofits are different from each other

• FASB has special guidance for Nonprofits

• Take time to educate Board members and others about the unique qualities of your nonprofit

144Nonprofit Financial Statements

Thank You for Attending Today’s Program

143

144

CCH® CPELink Nonprofit Financial Statements

145Nonprofit Financial Statements

Final Exam

145