Embed Size (px)

Citation preview

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 1/98

DiversificationBesanko Chapter

5http://www.icmrindia.org/casestud

ies/catalogue/Business%20Strategy1/ITC%20Diversification%20Strategy.h

tm

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 2/98

Lecture overview

This lecture will cover the following points:

The rationale for diversification"

Economics based reasons"

Economies of scale/ scope" Transaction costs"

Incentives and agency costs"

Efficiency arguments"

Evidence on diversification"

Summarise key points

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 3/98

3

Lecture overview

This lecture will cover the following points: The rationale for diversification

Economics based reasons

± Economies of scale/ scope

± Transaction costs ± Incentives and agency costs

Efficiency arguments

Evidence on diversification

Summarise key points

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 4/98

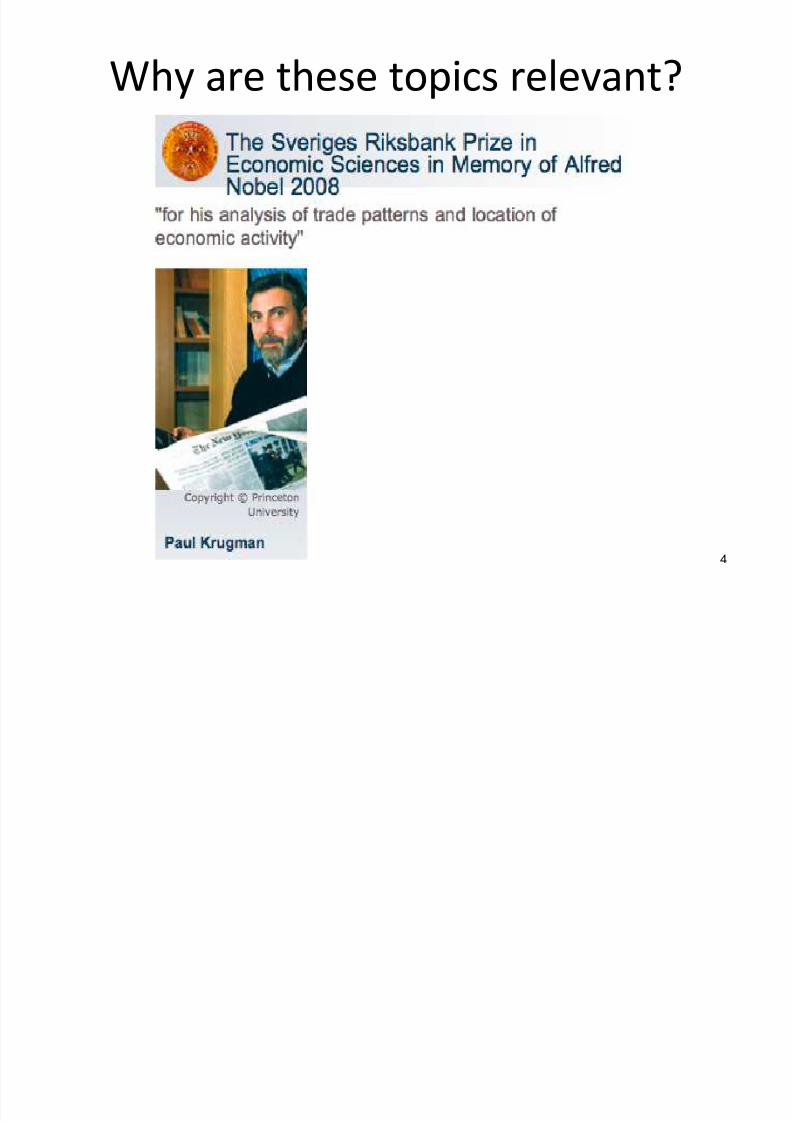

Why are these topics relevant?

4

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 5/98

Krugmans New Trade Theory - Why does Toyota sell cars

in Germany and Mercedes sell cars in Japan?

International Trade and Economic Geography

What are the effects of free trade and globalization?

What are the driving forces behind worldwide urbanisation?

many goods and services can be produced more cheaply in long series,

a concept generally known as economies of scale. As a result, small-scale production for a local market is replaced bylarge-scale production for the world market, where firms with similarproducts compete with one another.Economies of scale combined with reduced transport costs also help to

explain why an increasingly larger share of the world population lives incities and why similar economic activities are concentrated in the samelocations.

- Royal Swedish Academy of Sciences

5

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 6/98

6

diversify?

Most well known firms serve multiple product

markets

± Apple: Music/ computers/ software/ operating systems

± Virgin: Transport/ communications/ media

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 7/98

DIFFERENT TYPES OF DIVERSIFICATION

Vertical Integration - Firm decides to enter one or more parts of its value chain that it has hitherto not entered.

An automobile firm that has only been assembling cars might decide

to produce some critical sub assemblies or components.

E.g. Maruti used to initially only assemble cars. It progressivelyintroduced engine and transmission manufacture into its operations.

On the other hand a firm might decide to move up the value chain.

Reliance, in its textile operation only manufactured the cloth. Later

on it opened exclusive retail outlets which addressed not only the

sales and distribution aspects of its business, but also contributed to

brand building.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 8/98

DIFFERENT TYPES OF DIVERSIFICATION

Horizontal Integration or Related Diversification - Firmenters businesses that are related to its existing businesses.

Hindustan Lever, the FMCG major, used to be largely in the soaps anddetergents business. In the last ten years, it has diversified into the

foods and beverages business largely through the acquisition of firstLipton the tea company and later the acquisition of Brooke Bond.

Larsen & Toubro a leading engineering firm who has been dominantin the construction equipment industry entered the cement industrywhich is a related business.

IBM has entered the Infotech consultancy business another exampleof related diversification. Looking at the factors that have beencompelling for these firms it would be obvious that

The growth compulsion was stronger here than the capacityutilisation imperative that drives other firms to go in for VI

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 9/98

DIFFERENT TYPES OF DIVERSIFICATION

Unrelated or Conglomerate Diversification. This at times takesplace when a firm wishes to or is forced to exit from anunattractive or undesirable industry.

The tobacco firms who have diversified out of tobacco are the

obvious examples. American firms Phillip Morris and R.J. Reynolds entered the

FMCG arena specifically in Food and Beverages,

General Electric is the ultimate example of a firm which has

pursued unrelated diversification with dizzying success forseveral years.

Kingfisher

ITC

Reliance 9

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 10/98

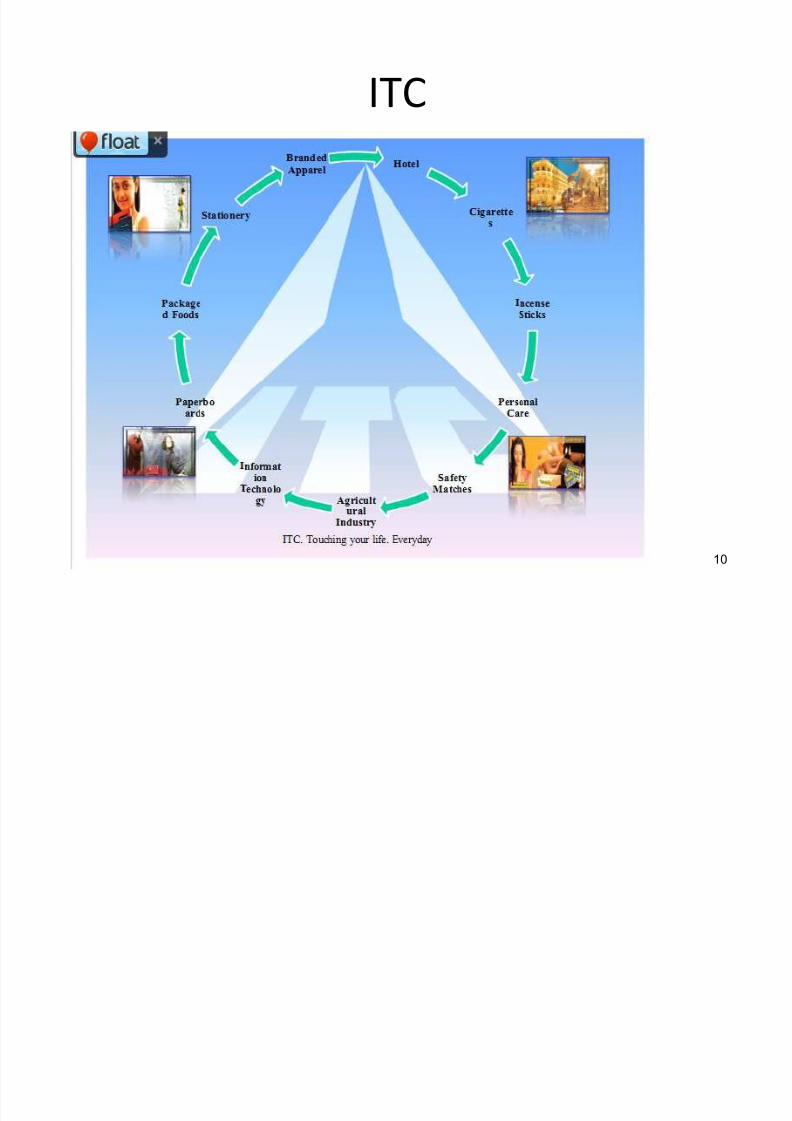

ITC

10

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 11/98

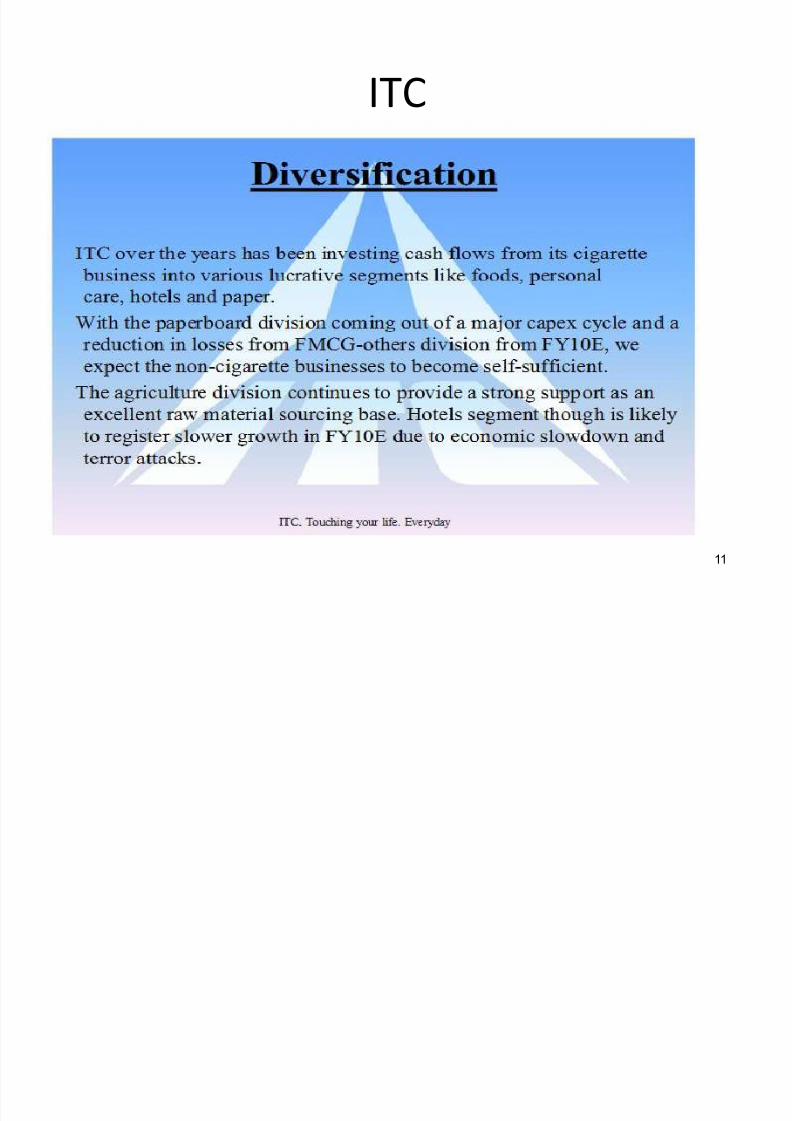

ITC

11

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 12/98

Nestle

Wants to operate only those businesses aboutwhich it has some special knowledge andexpertise

Instant coffee, infant foods, milk products UHT Milk, butter and curd and noodles,chocolates, confectioneries and other semiprocessed food products, mineral water

Leading brands Cerelac, Nestum, Nescafe,Maggie, Kitkat, Munch, Pure Life

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 13/98

DIFFERENT TYPES OF DIVERSIFICATION

Global Diversification - Firms that have successfully dominated their homemarkets are attracted by the prospect of growth in the markets of other

nations.

Enter markets in emerging economies.

The diversifying firm adjusts its strategies to comply with the cultural

requirements and preferences of the countries that it enters.

Kellogg the giant breakfast food cereal marketer made the cardinal error of

assuming that Indian families would accept and adopt the concept of cold

breakfasts. Indians have a unanimous preference for hot meals especially

the morning repast. As a result of this critical oversight, Kellogg has failed to

make a major impact in India.

McDonalds on the other hand has with great marketing sagacity exploited

the Indian preference for vegetarian food, and spiciness of a high order,

understood that Chicken is the favoured meat, appealed to the Indian

orientation towards family and scored significant successes in its foray into

the fast food industry in our country.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 14/98

Measuring/levels of Diversification:

relatedness

To identify economies of scale in multi

business firms, the relatedness concept was

developed by Richard Rumelt.

Two businesses are related if they share

technological characteristics, production

characteristics and/ or distribution channels.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 15/98

15

Levels and Types of Diversification

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 16/98

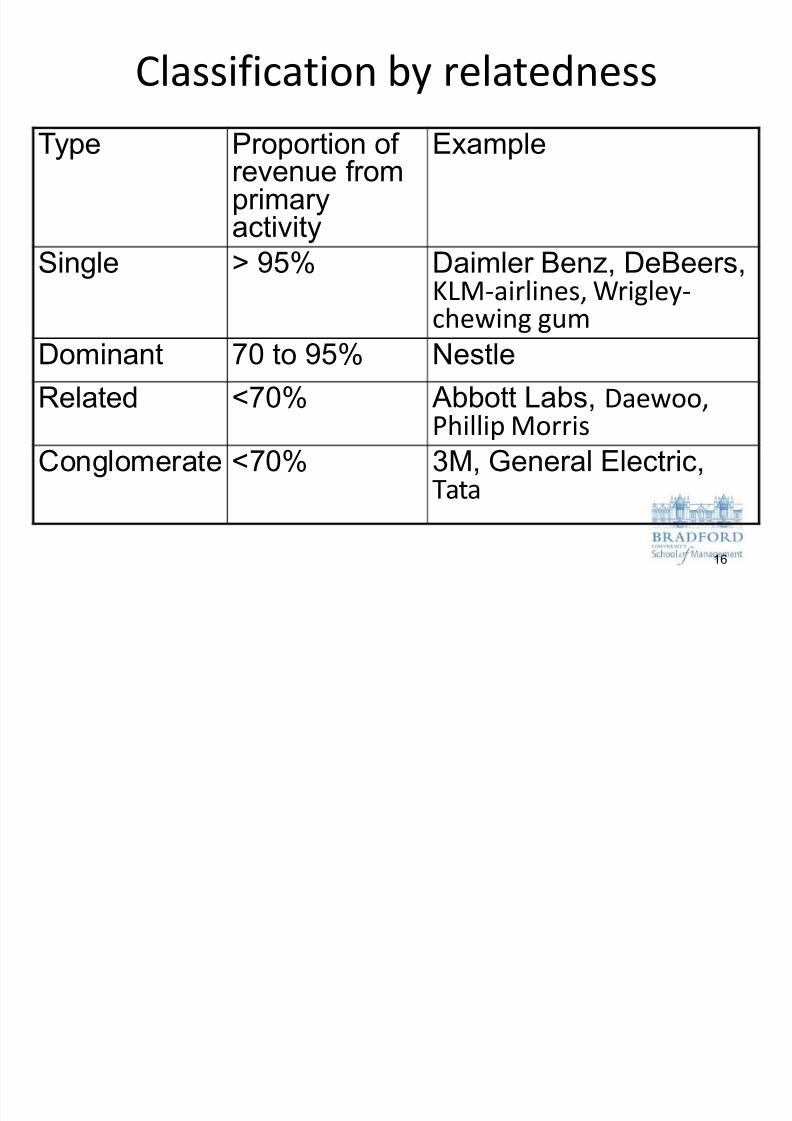

Classification by relatedness

Type Proportion of revenue fromprimaryactivity

Example

Single >95% D

aimler Benz,D

eBeers,KLM-airlines,Wrigley-chewing gum

Dominant 70 to 95% Nestle

Related <70% Abbott Labs, Daewoo,Phillip Morris

Conglomerate <70% 3M, General Electric,Tata

16

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 17/98

Examples

Most well known firms serve multiple product markets

Apple: Music/ computers/ software/ operatingsystems

Virgin: Transport/ communications/ media Diversification across products and across markets can

be due to economies of scale and scope

Diversification that occur for other reasons tend to be

less successful Nokia - wood pulp and paper/ footwear/ televisions/capacitors

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 18/98

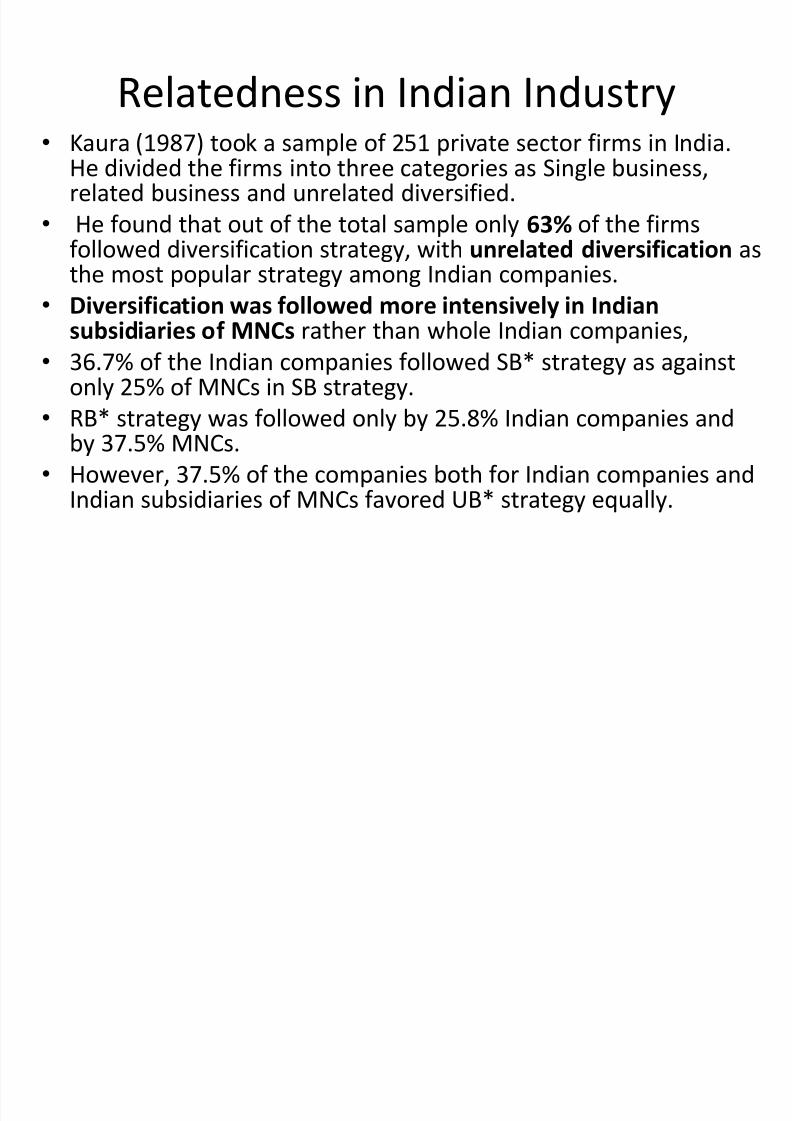

Relatedness in Indian Industry

Kaura (1987) took a sample of 251 private sector firms in India.He divided the firms into three categories as Single business,related business and unrelated diversified.

He found that out of the total sample only 63% of the firmsfollowed diversification strategy, with unrelated diversification as

the most popular strategy among Indian companies. Diversification was followed more intensively in Indian

subsidiaries of MNCs rather than whole Indian companies,

36.7% of the Indian companies followed SB* strategy as againstonly 25% of MNCs in SB strategy.

RB* strategy was followed only by 25.8% Indian companies andby 37.5% MNCs.

However, 37.5% of the companies both for Indian companies andIndian subsidiaries of MNCs favored UB* strategy equally.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 19/98

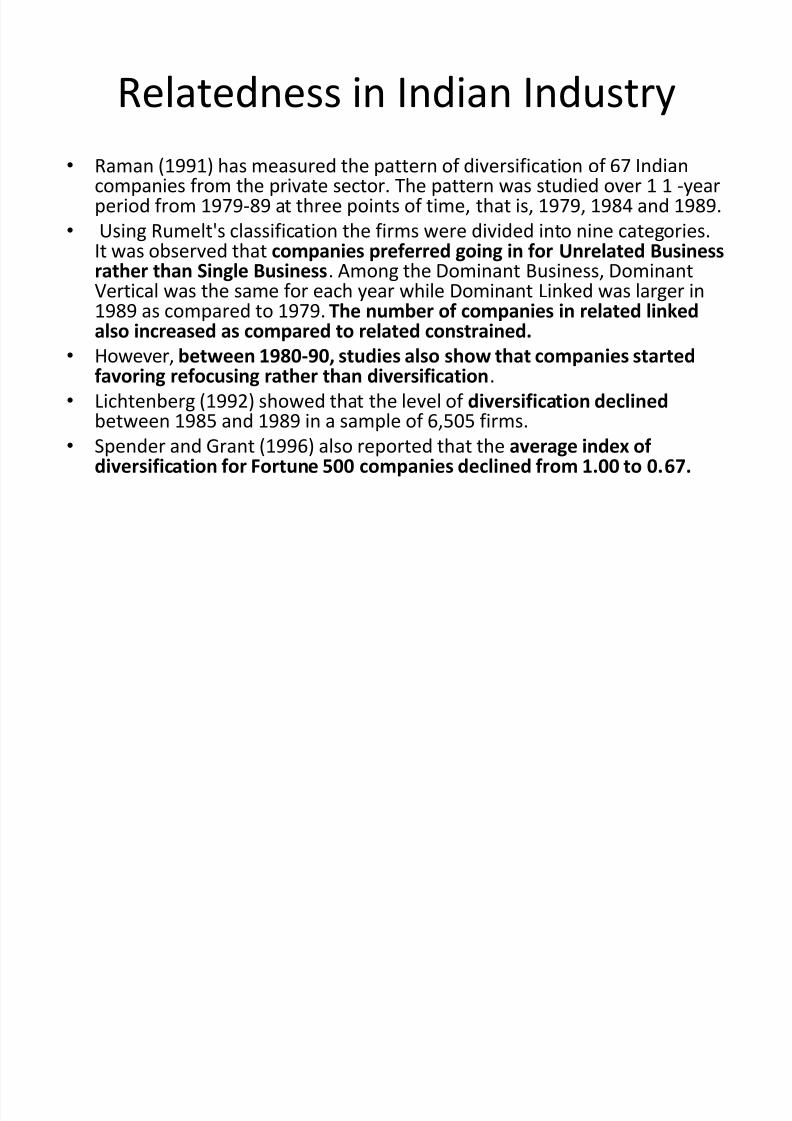

Raman (1991) has measured the pattern of diversification of 67 Indiancompanies from the private sector. The pattern was studied over 1 1 -yearperiod from 1979-89 at three points of time, that is, 1979, 1984 and 1989.

Using Rumelt's classification the firms were divided into nine categories.It was observed that companies preferred going in for Unrelated Business

rather than Single Business. Among the Dominant Business, DominantVertical was the same for each year while Dominant Linked was larger in1989 as compared to 1979. The number of companies in related linkedalso increased as compared to related constrained.

However, between 1980-90, studies also show that companies startedfavoring refocusing rather than diversification.

Lichtenberg (1992) showed that the level of diversification declined

between 1985 and 1989 in a sample of 6,505 firms. Spender and Grant (1996) also reported that the average index of

diversification for Fortune 500 companies declined from 1.00 to 0.67.

Relatedness in Indian Industry

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 20/98

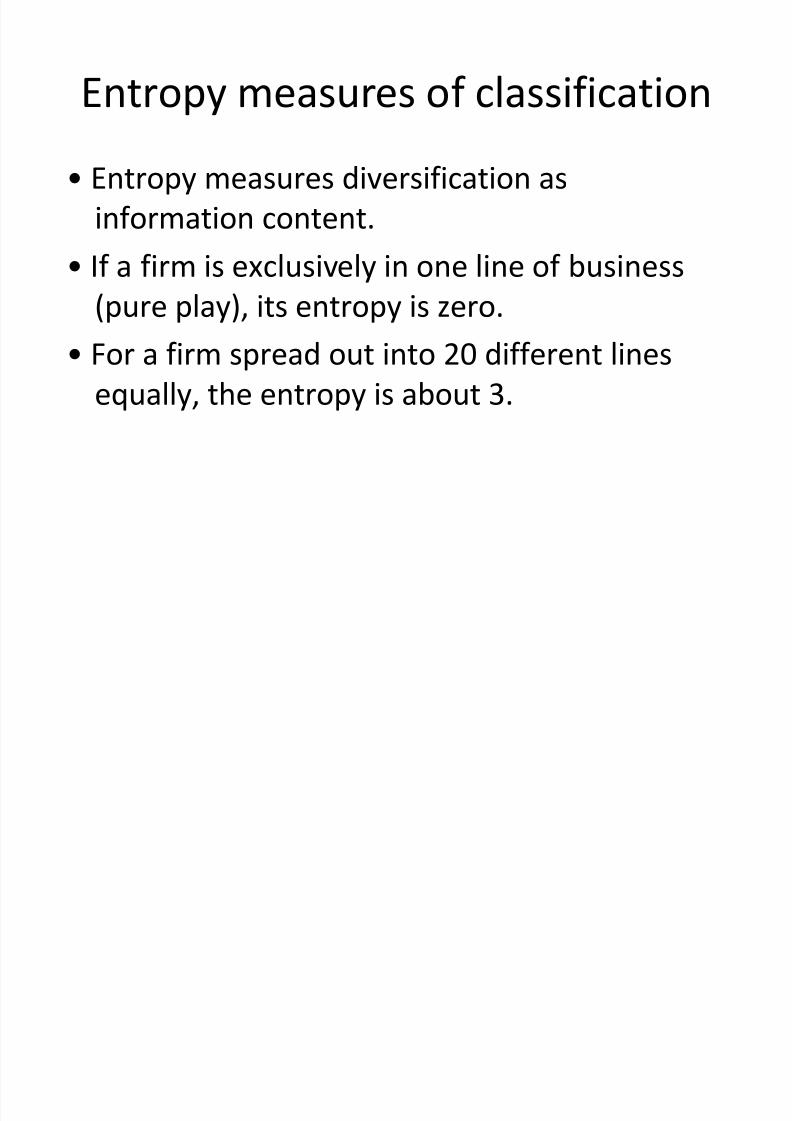

Entropy measures of classification

Entropy measures diversification as

information content.

If a firm is exclusively in one line of business(pure play), its entropy is zero.

For a firm spread out into 20 different lines

equally, the entropy is about 3.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 21/98

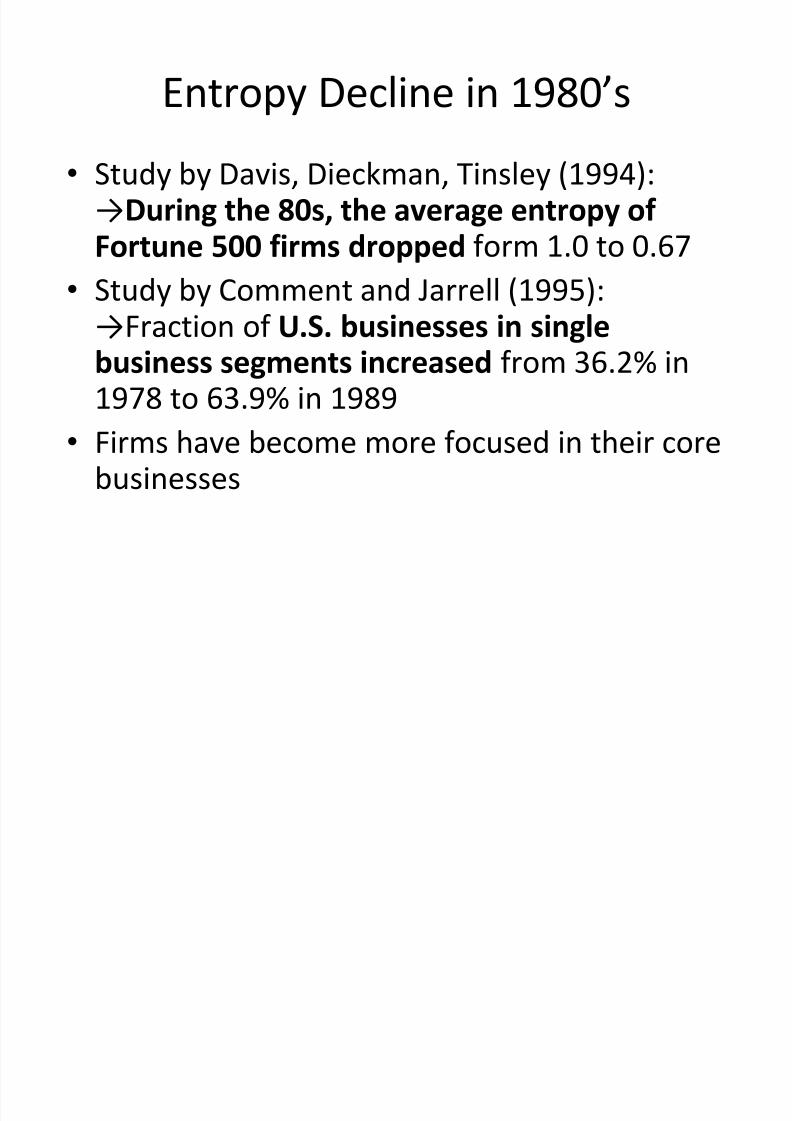

Entropy Decline in 1980s

Study by Davis, Dieckman, Tinsley (1994):During the 80s, the average entropy of Fortune 500 firms dropped form 1.0 to 0.67

Study by Comment and Jarrell (1995):Fraction of U.S. businesses in singlebusiness segments increased from 36.2% in1978 to 63.9% in 1989

Firms have become more focused in their corebusinesses

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 22/98

22

EntropyIn Management Strategy I

Managers are interested in knowing how

diversified are the firms lines of business

It has been considered (and aptly discussedand hotly debated) that more diverse

businesses are more profitable

± May not always be the case though

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 23/98

23

EntropyIn Management Strategy II

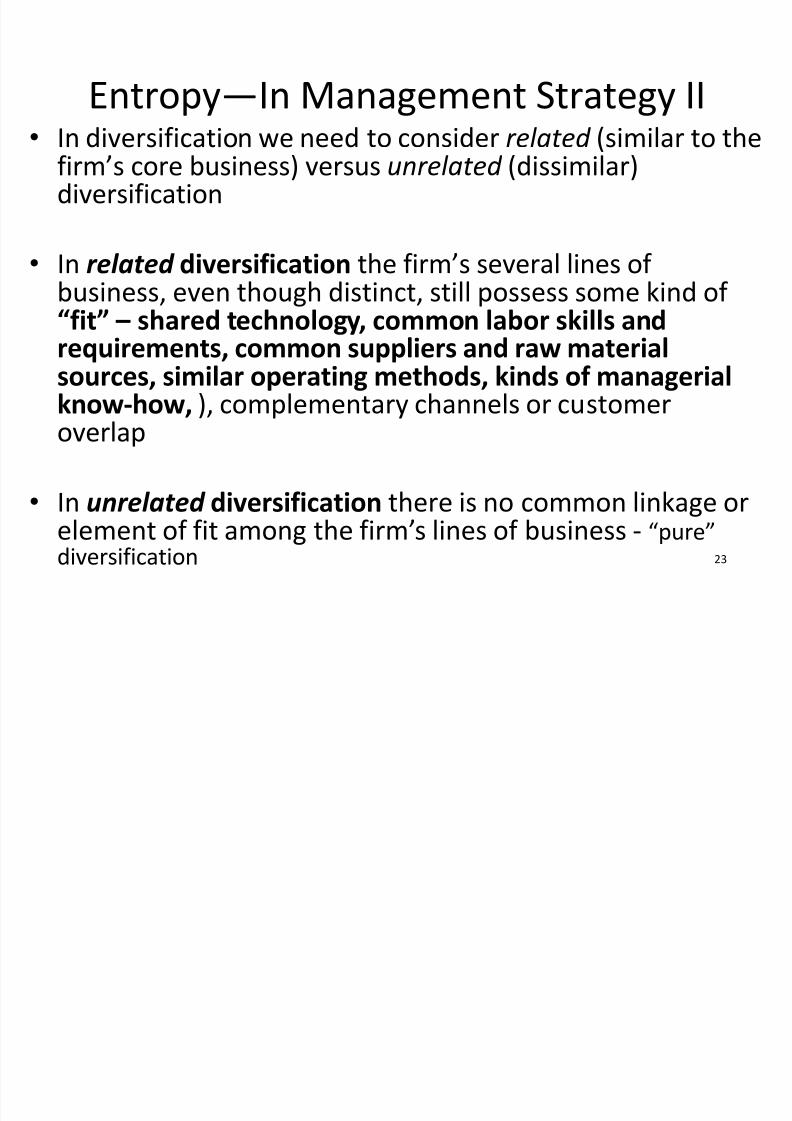

In diversification we need to consider related (similar to thefirms core business) versus unrelated (dissimilar)diversification

In related diversification the firms several lines of business, even though distinct, still possess some kind of fit shared technology, common labor skills andrequirements, common suppliers and raw materialsources, similar operating methods, kinds of managerial

know-how, ), complementary channels or customeroverlap

In unrelated diversification there is no common linkage orelement of fit among the firms lines of business - pure

diversification

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 24/98

24

DiversityAn Example

If we take a beaker of water (H2O) and a very

concentrated solution of red food coloring and we

then add a drop of the coloring to the water we will

see the red color diffusing throughout the water andthus, we go from concentration to diversification

Economists, as well as chemists and physicists, want

to define concentration vs. diversification

Concentration and diversification are two ends of the

spectrum

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 25/98

Ways to diversify

Firms can diversify in different ways

They can develop new lines of business

internally. They can form joint ventures in new areas of

business.

They can acquire firms in unrelated lines of business.(M&A)

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 26/98

Why do Firms Diversify?

Efficiency based reasons

a) Economies of scale and scope

b) Economizing on transactions costsc) Financial Synergies

± Internal capital markets

±Shareholder diversification

± Identifying undervalued firms

Managerial Reasons for Diversification

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 27/98

Reasons for diversification

a) Economies of Scale and Scope

The idea is that it is less costly or more

valuable to producers for two activities to be

pursued jointly than separately

Economies of scope might arise because of

relatedness among products in terms of: raw

materials and/or technology and/or output

markets

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 28/98

If a merger is motivated by scale economies,

the market share of the merged firm should

increase immediately following the merger

(scale).

Data from manufacturing industries show that

changes in market share were in line with

expectations (scale).

Reasons for diversification - Evidenceof a) Economies of Scale and Scope

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 29/98

If firms pursue economies of scope through

diversification, large firms should be expected

to sell related set of products in different

markets (scope).

Evidence indicates that this happens only

occasionally (scope).

Reasons for diversification - Evidenceof a) Economies of Scale and Scope

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 30/98

Reasons for diversification a) -Scope

Economies outside technology and markets -

: Unrelated activities Several firms produce unrelated products and

serve unrelated consumer groups (scope).

Firms that produce unrelated products and serveunrelated markets could be pursuing scope

economies in other dimensions.

Two explanations that take this approach are

Resource based view of the firm (Edith Penrose).

Dominant general management logic (C K

Prahlad).

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 31/98

Resource based view of the firm (Edith Penrose)utilize managerial and organizationalunderutilzed resources in new areas when

growth in existing market is constrained Dominant general management logic (Prahalad

and Bettis): Managers of diversified firms mayspread their own managerial talent acrossnominally unrelated business areas.Management has specific skills that can beapplied in different areas of activity e.g.

information systems, finance, advertising etc.

Reasons for diversification a) Scope

Economies outside technology and markets

Unrelated activities

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 32/98

Reasons for diversification

b) Economizing on Transactions Costs

If transactions costs complicate coordinationamong independent firms, merger may be theanswer

Transactions costs arises in relationships withindependent firms when production processinvolves specialized assets such as humancapital, organizational routines or other forms of proprietary knowledge.

Transaction costs are not likely to be a problemMarket coordination may be superior in theabsence of specialized assets

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 33/98

Example:The University as a

Conglomerate

An undergraduate university is a conglomerate of

different departments

Economies of scale (common library, dormitories,athletic facilities) dictate common ownership and

location

Value of one departments investments depends on

the actions of the other departments (relationship

specific assets)

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 34/98

Reasons for diversification

3. Financial synergies

a) Internal capital markets

b) Diversifying Shareholders diversification

c) Identifying undervalued firms

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 35/98

Reasons for diversification

3. Financial synergies :

a)Internal Capital Markets In a diversified firm, some units generate

surplus funds that can be channeled to units

that need the funds (Internal capital market)

The key issue is whether the firm can do a

better job of evaluating its investment

opportunities than an outside banker can do

Internal capital market also engenders

influence costs

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 36/98

Reasons for diversification - 3.

Financial synergies :

b)Diversifying Shareholders Portfolios Individual shareholders benefit from investing indiversified portfolios and smoothens the earningsstream

A broadly diversified firm may receive only a small % of

its revenues from any one line of business. Soshareholder can invest in a single diversified firm andachieve the benefits of portfolio diversification.

But the shareholders do not benefit from this sincethey can diversify their portfolio themselves.

Only when shareholders are unable to diversify do theybenefit from firm diversifying into different products.

easons or ers ca on

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 37/98

easons or vers ca on

3. Financial synergies :

c) Identifying Undervalued Firms Firms shareholders may benefit from diversification if its managers are able to identify other firms that areundervalued by the stock market.

W

hen the acquired firm is in an unrelated business, theacquiring firm is more likely to have overvalued thetarget

The key question is: Why did other potential acquirersnot bid as high as the successful acquirer?

Winners curse could wipe out any gains from financialsynergies ( paying the highest price as compare toother bidders)

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 38/98

Managerial Reasons for Diversification

Growth may benefit managers even when it

does not add value for the shareholders

When growth cannot be achieved throughinternal development, diversification may be

an attractive route to growth

When related mergers were made difficult by

law (anti trust law) conglomerate mergers

became popular

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 39/98

Managerial Reasons for Diversification

Managers may feel secure if the firm

performance mirrors the performance of the

economy (which will happen with diversification)

Diversification will offer managers room for

lateral movement and allow them to invest in

firm specific skills

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 40/98

Potential Costs of diversification

Diversified firms may incur substantial influence costsand may need elaborate control systems to rewardand punish managers.

Internal capital markets may not function well. Growth may benefit managers even when it does notadd value for the shareholders.

Managers could be engaged in empire building andenhancing their status in their network at the expenseof the shareholders.

If managers undertake unwise acquisitions, the stockprice drops, reflecting overpayment for the acquisition

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 41/98

Corporate governance issues

Shareholders are knowledgeable regarding the

value of an acquisition to the firm.

Shareholders have weak incentive to monitor

the management.

Acquiring firms tend to experience loss of

value.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 42/98

Market for corporate control: Evidence

Hostile takeovers tend to occur in decliningindustries and industries experiencing drasticchanges where managers have failed to

readjust scale and scope of operations.Corporate raiders have profited handsomely

for taking over and busting up firms thatpursued unprofitable diversification.

Such redistribution of wealth may adverselyaffect economic efficiency.

E id Di ifi i d

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 43/98

Evidence: Diversification and

Operating Performance

Operating Performance is usually measured as

accounting profits or as productivity.

Major results are:

Unrelated diversification harms productivity

Diversification into narrow markets does

better than diversification into broad markets

E id Di ifi i d

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 44/98

Improvements in newly acquired plants may

come at the expense of performance at the

existing plants.

Gains from diversification depends onspecialised resources of the firm.

Evidence: Diversification and

Operating Performance

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 45/98

Evidence : Diversification and long term

performance

Long term performance of diversified firms appear tobe poor.

One third to one half of all acquisitions and over half of all new business acquisitions are eventually divested.

Corporate refocusing of the 1980s (and later) could beviewed as a correction to the conglomerate mergerwave of the 1960s.

Past conditions could have favoured unrelateddiversification and these conditions could since havechanged (example: anti-monopoly behaviour basedregulations).

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 46/98

Evidence: Valuation and Event Studies

Compare stock market valuations of

diversified to those of undiversified firms

shares of diversified firms trade at a discount

relative to those of their undiversified

counterparts (up to 15%): diversification

discount

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 47/98

Evidence: Valuation and Event Studies

Why?

a) Combining two unrelated businesses reduces

value in some way or

b) Unrelated businesses elected to combine

had low market values even before the

combination

Recent empirical evidence shows that b) might

be motivation, at least partly

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 48/98

Evidence: Summary

Diversification can create value, although its

benefits relative to non-diversification are

unclear Diversifications in related activities

outperform those in unrelated activities

h i i i di f

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 49/98

The Transition Process in India from

Diversified to Focused

Conglomerates are leveraging their existing setups (internalfunds, brand equity, trust and relationships) into venturingand streamlining their processes.

There is a transition happening with a move towards

focusing on core competencies and outsourcing all thesecondary domains.

Focused approaches would reduce gross inefficiencies,accelerate the decision making process and also enhanceentrepreneurship.

When the conglomerates would become successful inestablishing themselves as global players in their coreareas, they might hive off or sell off their peripheral areasof business.

49

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 50/98

Indian Business

Bui ld ing on Core Competenci es

Outsour cing Secondary Ac t ivi t i es: The

contender i s most comfortable in bui ld ing on

i ts core abi l i t i es and competes in pr ov en

gr ounds. H enc e many emer ging Ind i an

compani es hav e deci ded t o re focus on core

competenci es, whi le outsour cing or shedd ingoff secondary operat ions.

50

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 51/98

Lecture summary

We have considered the rationale for

diversification.

We have assessed some examples and some

trends related to diversification.

We have employed ideas such as:

Economies of scale and scope

Transaction costs.

Efficiency factors.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 52/98

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 53/98

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 54/98

54

The Extent of Diversification

What factors determine the extent to which a firmdiversifies across different industries?

Diversification will be efficient if there is SYNERGY

SYNERGY can come from ± economies of scope

± exploitation of specific assets

± reduction of risk and uncertainty

BUT DOES IT REALLY EXIST IN PRACTICE?

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 55/98

55

The history of diversification is not good

In the 1960s and 1970s the conglomerate was a

favourite form of business

Although the purchased firms were usually good

performers, the merged firm tended to have poorperformance

It became clear in the 1980s and 90s that there is a

diversification discount of about 15% on average

WHY?

± Firms seemed to not understand the sectors they

entered

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 56/98

56

Alternative forms of of merger Horizontal:

with competitors

Vertical:

with suppliers or customers

Conglomerate:

with unrelated firms

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 57/98

57

Mergers in a perfect world

All managers are efficient;they work in the interests of

shareholders; stock markets price shared efficiently;no

uncertainty; everyone uses the same discount rate

In that situation there are only two reasons for mergers to

take place:

± SYNERGY: 2+2>4; economies of scope or scale, joint

use of key resources or capabilities

± MARKET POWER: merger gives some degree of

monopoly power

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 58/98

58

The performance consequences of

mergers

Shareholders of the acquired firms gain -

because the acquiring firm pays a premium

The pattern of results for the acquiring firm is

very mixed with values tending to fall, not

rise!

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 59/98

59

Are mergers really for managers?

CEOs and senior managers like mergers

± larger firms involve more prestige and often more

pay

± larger and more diverse firms reduce risk for

managers (but not for shareholders who could do

it another way)

±publicity is welcomed by many CEOs

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 60/98

60

Partnerships and Value Constellations

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 61/98

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 62/98

0

10

20

30

40

50

60

70

1950 1960 1970 1983 1993

Single business

Dominant

business

Related business

Unrelatedbusiness

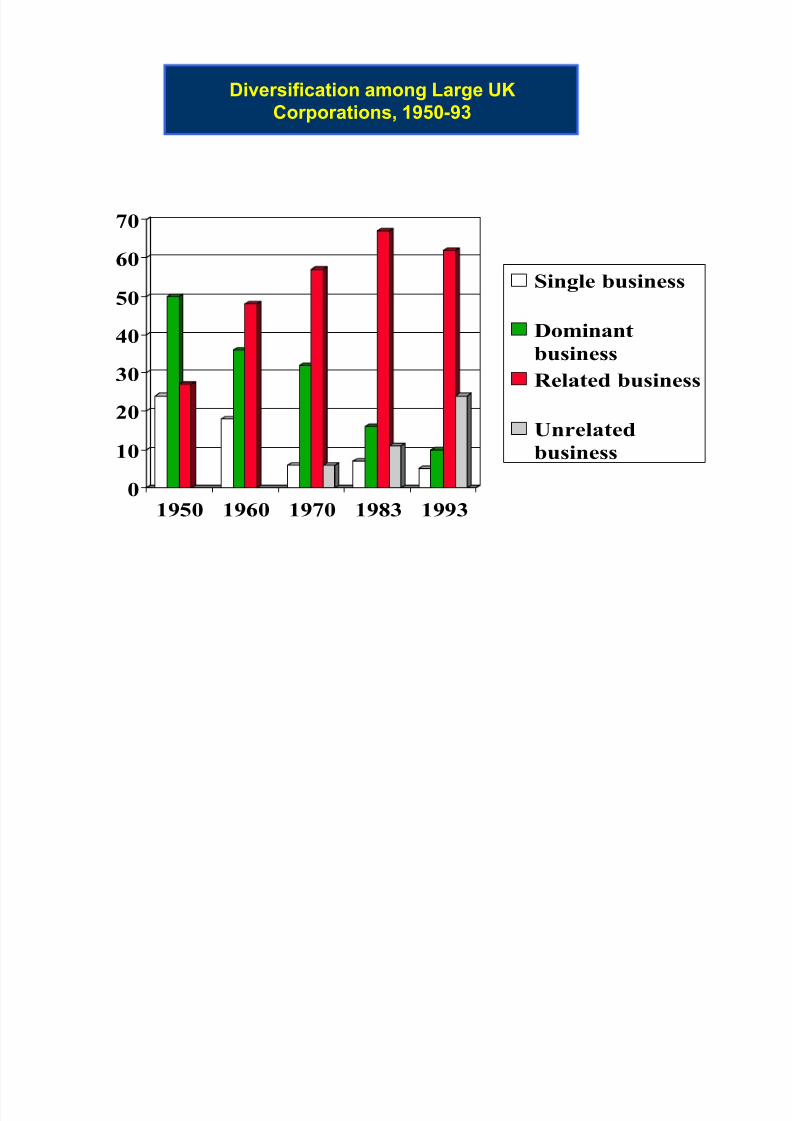

Diversification among Large UK

Corporations, 1950-93

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 63/98

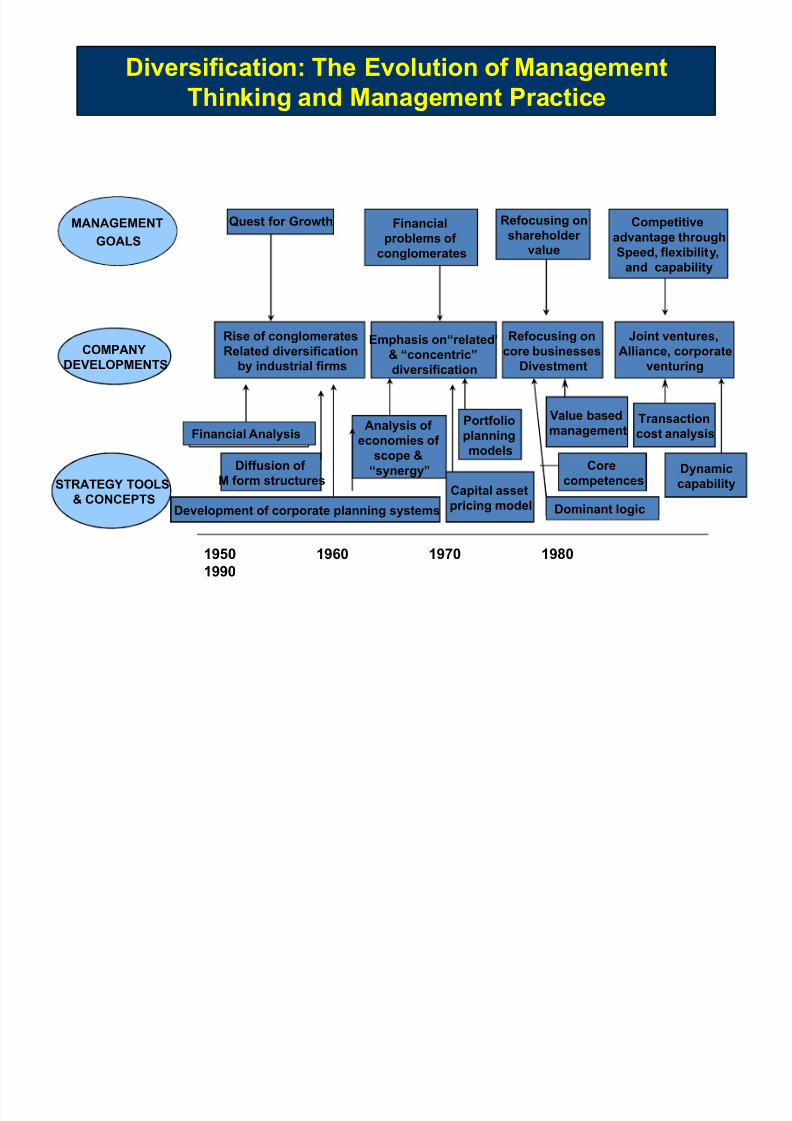

COMPANY

DEVELOPMENTS

MANAGEMENT

GOALS

STRATEGY TOOLS

& CONCEPTS

1950 1960 1970 1980

1990

Financial

problems of

conglomerates

Refocusing on

shareholder value

Rise of conglomerates

Related diversification

by industrial firms

Emphasis on³related¶

& ³concentric´

diversification

Refocusing on

core businesses

Divestment

Diffusion of

M form structures

Analysis of economies of

scope &

³synergy´

Value based

management

Capital asset

pricing model

Portfolioplanning

models

Core

competences

Transactioncost analysis

Development of corporate planning systems

Diversification: The Evolution of Management

Thinking and Management Practice

Joint ventures,

Alliance, corporate

venturing

Competitive

advantage through

Speed, flexibility,

and capability

Dynamic

capability

Quest for Growth

Financial Analysis

Dominant logic

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 64/98

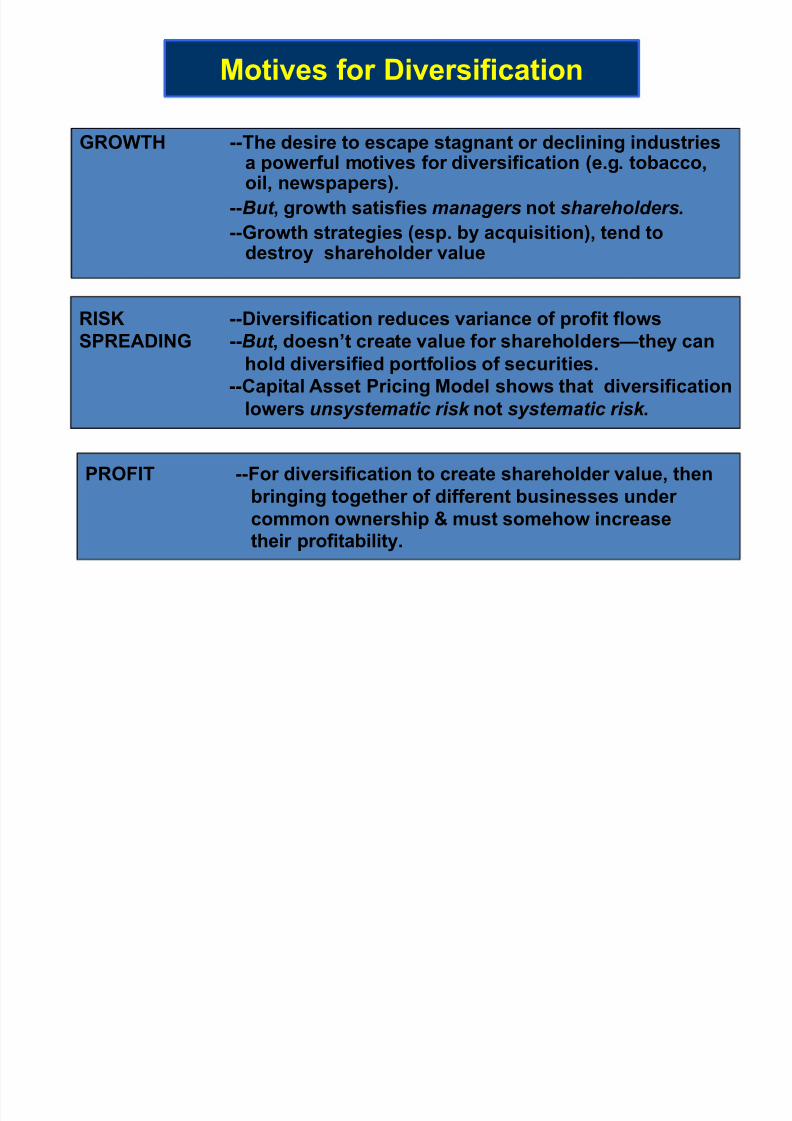

Motives for Diversification

GROWTH --The desire to escape stagnant or declining industriesa powerful motives for diversification (e.g. tobacco,oil, newspapers).

--But , growth satisfies managers not shareholders.

--Growth strategies (esp. by acquisition), tend todestroy shareholder value

RISK --Diversification reduces variance of profit flows

SPREADING --But , doesn¶t create value for shareholders²they can

hold diversified portfolios of securities.

--Capital Asset Pricing Model shows that diversification

lowers unsystematic risk not systematic risk .

PROFIT --For diversification to create shareholder value, then

bringing together of different businesses under

common ownership & must somehow increasetheir profitability.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 65/98

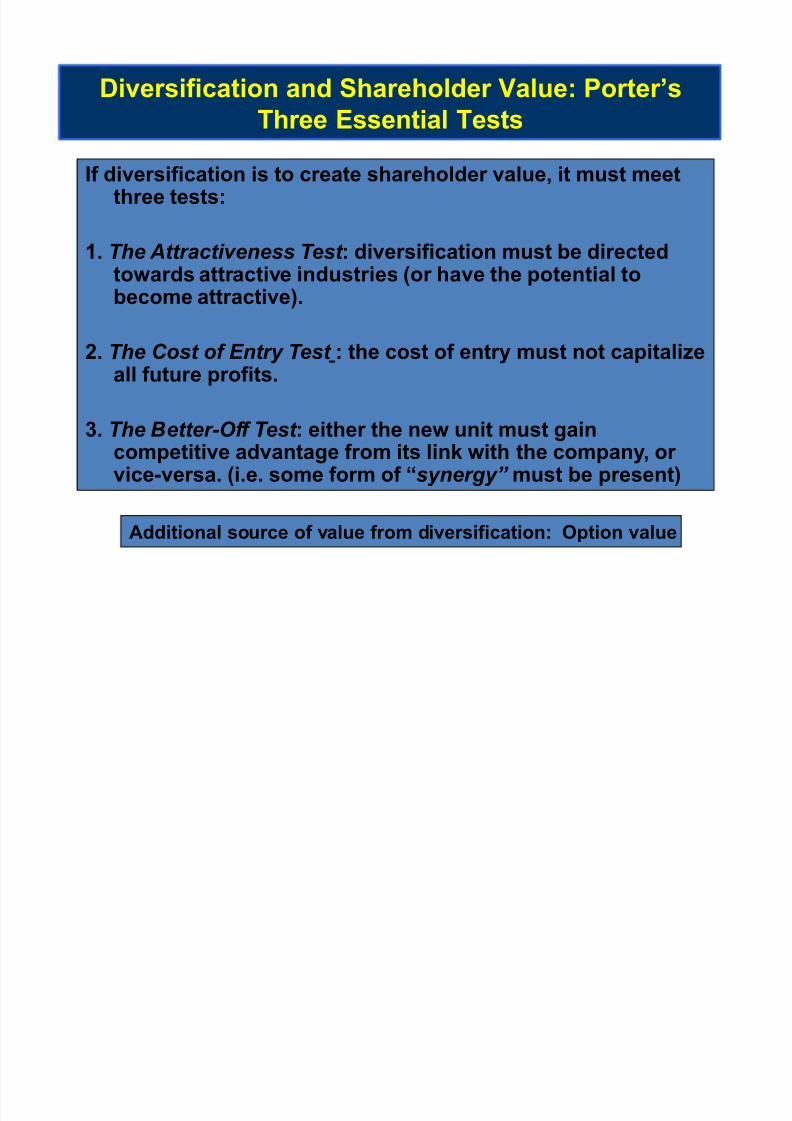

Diversification and Shareholder Value: Porter¶s

Three Essential Tests

If diversification is to create shareholder value, it must meetthree tests:

1. T he Attractiveness T est : diversification must be directedtowards attractive industries (or have the potential tobecome attractive).

2. T he Cost of Entry T est : the cost of entry must not capitalizeall future profits.

3. T he Better-Off T est : either the new unit must gaincompetitive advantage from its link with the company, or vice-versa. (i.e. some form of ³synergy´ must be present)

Additional source of value from diversification: Option value

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 66/98

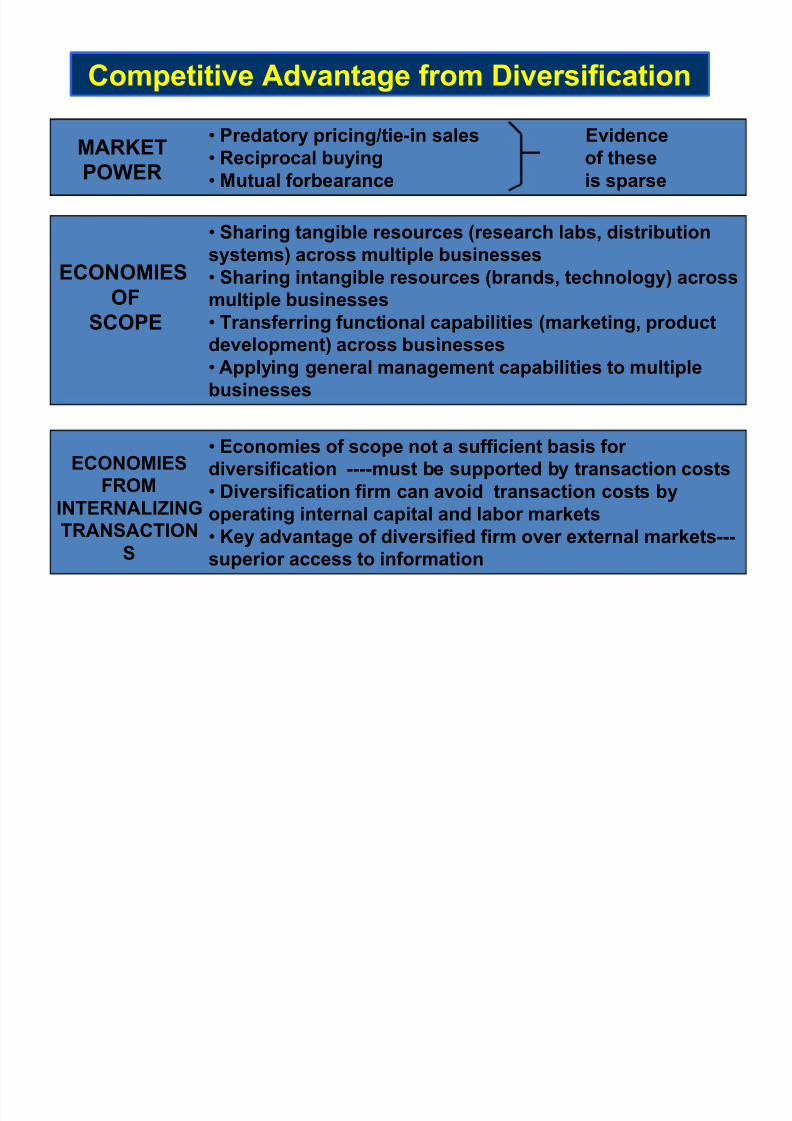

Competitive Advantage from Diversification

Predatory pricing/tie-in sales Evidence

Reciprocal buying of these

Mutual forbearance is sparse

MARKETPOWER

Sharing tangible resources (research labs, distribution

systems) across multiple businesses

Sharing intangible resources (brands, technology) acrossmultiple businesses

Transferring functional capabilities (marketing, product

development) across businesses

Applying general management capabilities to multiple

businesses

Economies of scope not a sufficient basis for

diversification ----must be supported by transaction costs

Diversification firm can avoid transaction costs by

operating internal capital and labor markets

Key advantage of diversified firm over external markets---

superior access to information

ECONOMIES

OF

SCOPE

ECONOMIES

FROM

INTERNALIZING

TRANSACTION

S

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 67/98

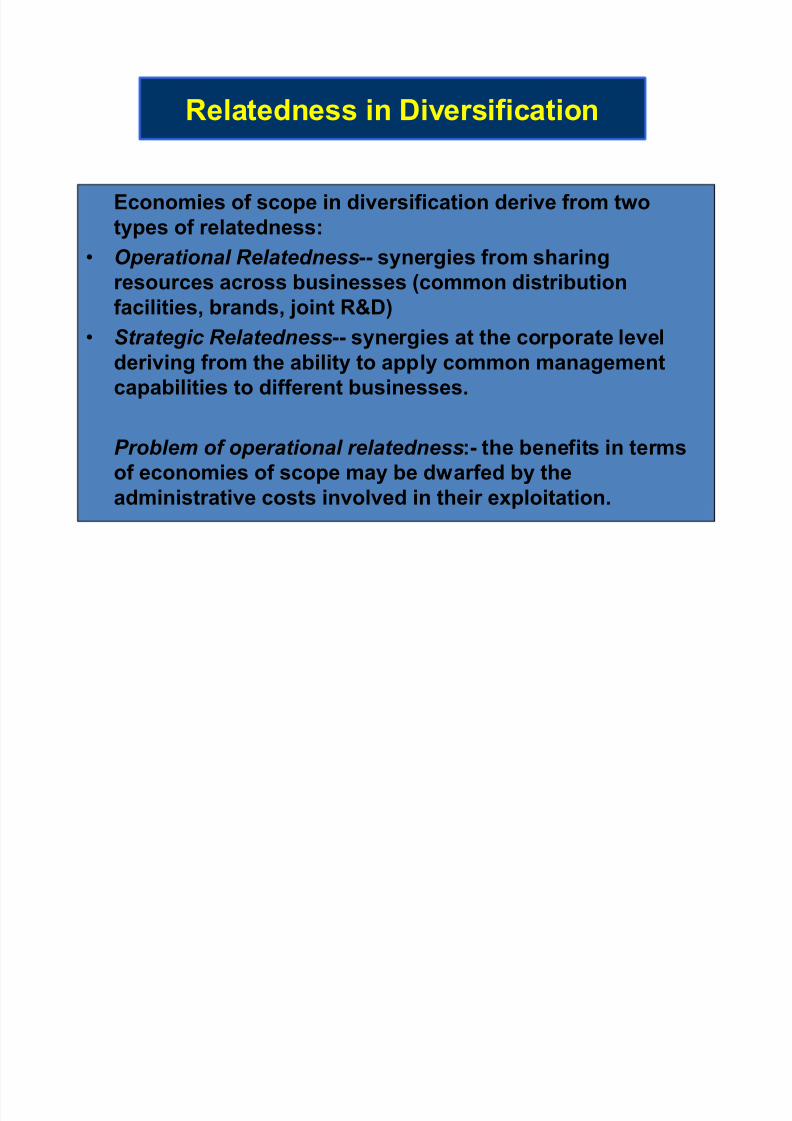

Relatedness in Diversification

Economies of scope in diversification derive from two

types of relatedness:

Operational Relatedness-- synergies from sharing

resources across businesses (common distributionfacilities, brands, joint R&D)

S trategic Relatedness-- synergies at the corporate level

deriving from the ability to apply common management

capabilities to different businesses.

P roblem of operational relatedness:- the benefits in terms

of economies of scope may be dwarfed by the

administrative costs involved in their exploitation.

B & th Vi i C i M ki t t i

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 68/98

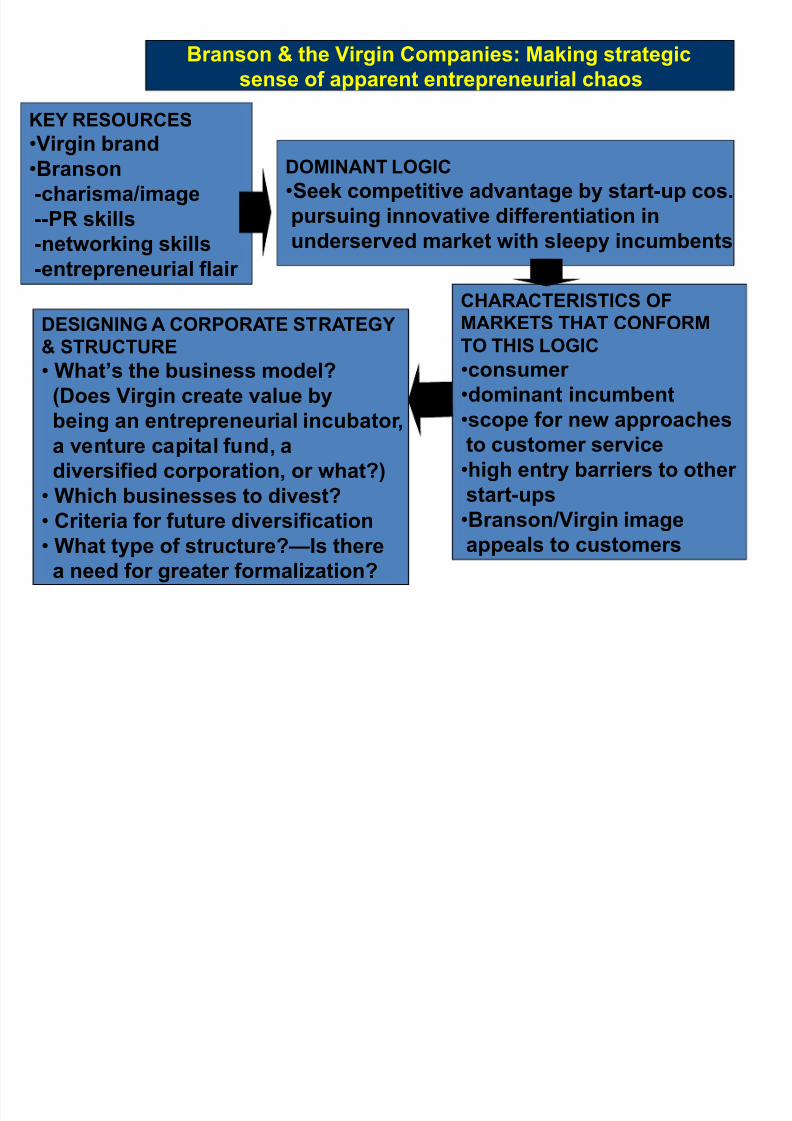

Branson & the Virgin Companies: Making strategic

sense of apparent entrepreneurial chaos

KEY RESOURCES

Virgin brandBranson

-charisma/image

--PR skills

-networking skills

-entrepreneurial flair

DOMINANT LOGIC

Seek competitive advantage by start-up cos.

pursuing innovative differentiation in

underserved market with sleepy incumbents

CHARACTERISTICS OF

MARKETS THAT CONFORM

TO THIS LOGIC

consumer

dominant incumbent

scope for new approachesto customer service

high entry barriers to other

start-ups

Branson/Virgin image

appeals to customers

DESIGNING A CORPORATE STRATEGY

& STRUCTURE

What¶s the business model?

(Does Virgin create value by

being an entrepreneurial incubator,a venture capital fund, a

diversified corporation, or what?)

Which businesses to divest?

Criteria for future diversification

What type of structure?²Is there

a need for greater formalization?

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 69/98

Virgin Conglomorate

Business opport uni t i es are l ik e buses, t heres al w ays anot her one coming Richard Branson

Virgin Group is a diversified group of more than 200 privately heldcompanies. The largest of these are Virgin Atlantic Airways, the numbertwo airline in the United Kingdom; Virgin Holidays, a vacation touroperator; the Virgin Retail Group, which operates numerous Virgin

Megastores, a retail concept featuring videos, music CDs, and computergames; and Virgin Direct, which offers financial services. Other Virginbusinesses include beverage maker Virgin Cola, a record label, book andmusic publishing operations, hotels, an Internet service provider, movietheaters, a radio station, cosmetics and bridal retailing concepts, and aline of clothing. Holding this disparate group of companies together is thecombination of Richard Branson and the Virgin brand name. Britishentrepreneur Branson dropped out of boarding school at the age of 17, in1967, to start his own magazine. That venture called Student was animmediate success, establishing the foundation for what would become amultibillion-dollar conglomerate.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 70/98

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 71/98

STRATEGY AND COMPETITIVESTRATEGY AND COMPETITIVE

ADVANTAGE IN DIVERSIFIEDADVANTAGE IN DIVERSIFIEDCOMPANIESCOMPANIES

Diversification

f d

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 72/98

Diversification and Corporate

Strategy

A company i s d iv ersifi ed when i t i s in t wo or more l ines of business

Strategy-making in a d iv ersifi ed company is abigger picture exercise than crafting a strategy for asingle line-of-business

± A diversified company needs a mult i -ind ustry, mult i -business strategy

±

A strategic ac t ion plan must be developed forsev eral different businesses competing in d iv erseind ustry environments

When Does Diversification

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 73/98

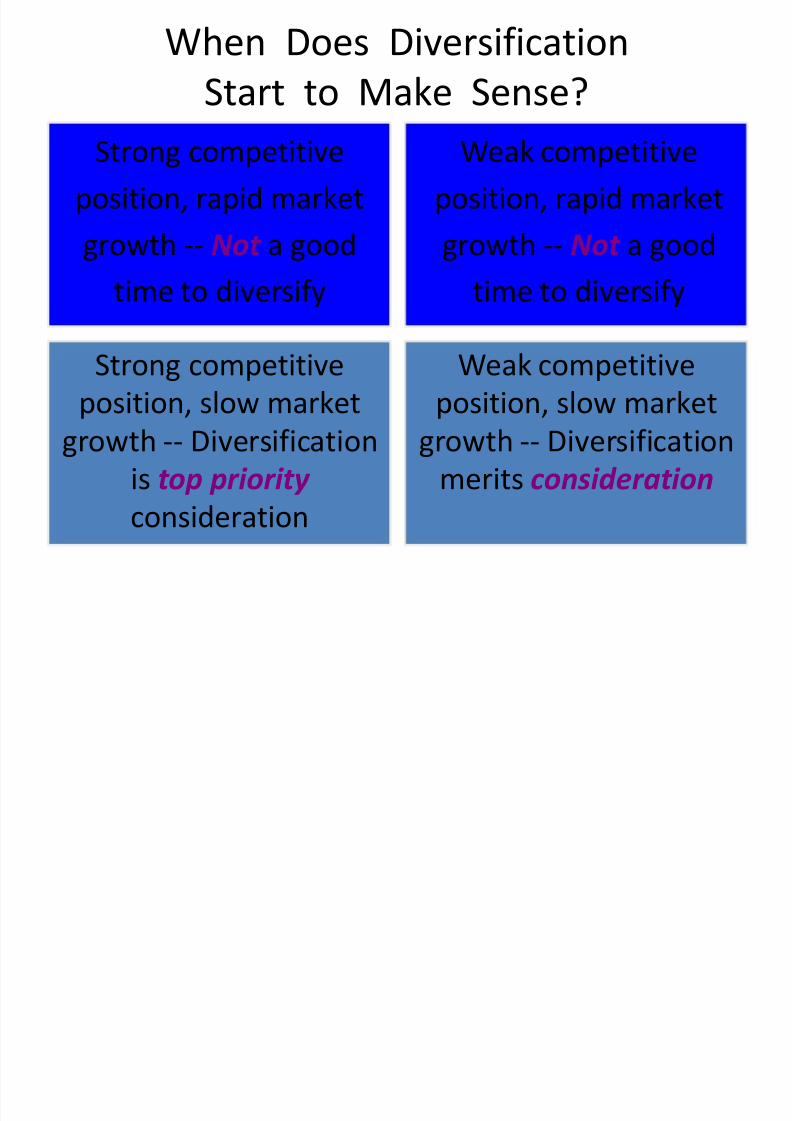

When Does Diversification

Start to Make Sense?

Strong competitiveposition, rapid market

growth -- N ot a good

time to diversify

Strong competitive

position, slow market

growth -- Diversification

is t op pr ior i ty

consideration

Weak competitiveposition, rapid market

growth -- N ot a good

time to diversify

Weak competitive

position, slow market

growth -- Diversification

merits consi derat ion

S i f i

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 74/98

Strategies for Entering

New Businesses

Acquire existing company

Start-up new business internally

Joint venture with another company

A i C Al d i h

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 75/98

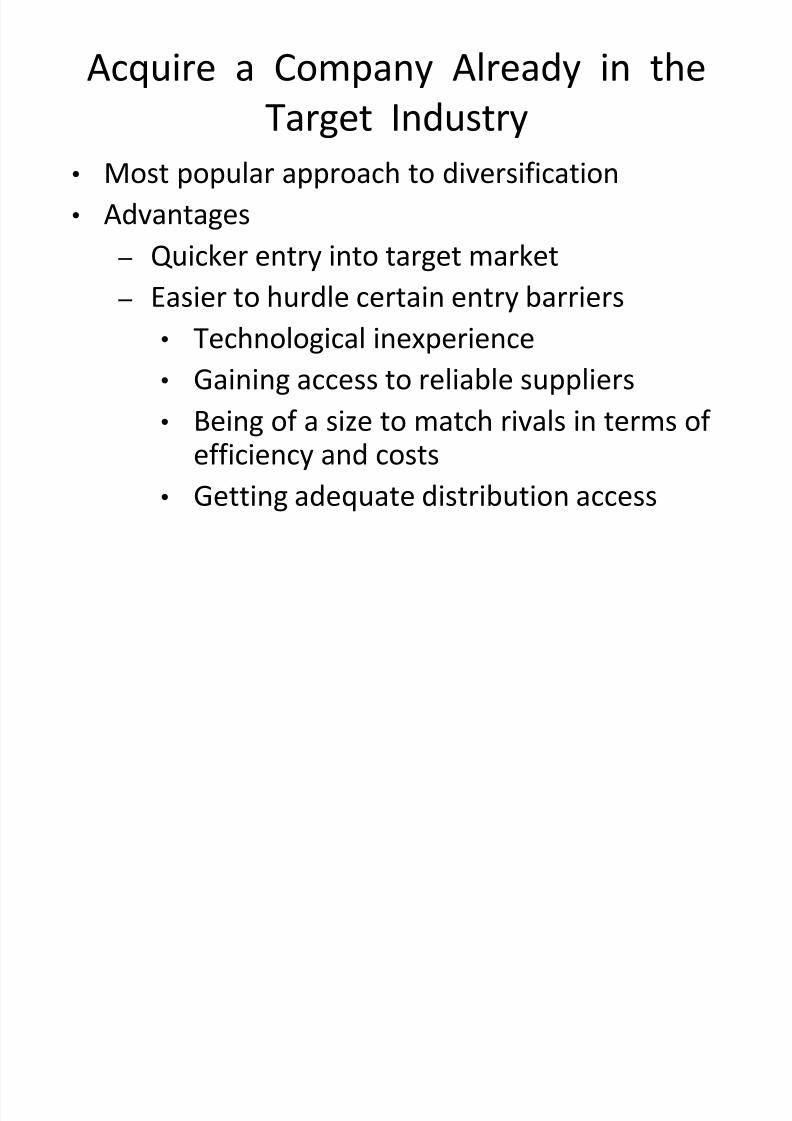

Acquire a Company Already in the

Target Industry

Most popular approach to diversification

Advantages

± Quicker entry into target market

± Easier to hurdle certain entry barriers

Technological inexperience

Gaining access to reliable suppliers

Being of a size to match rivals in terms of efficiency and costs

Getting adequate distribution access

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 76/98

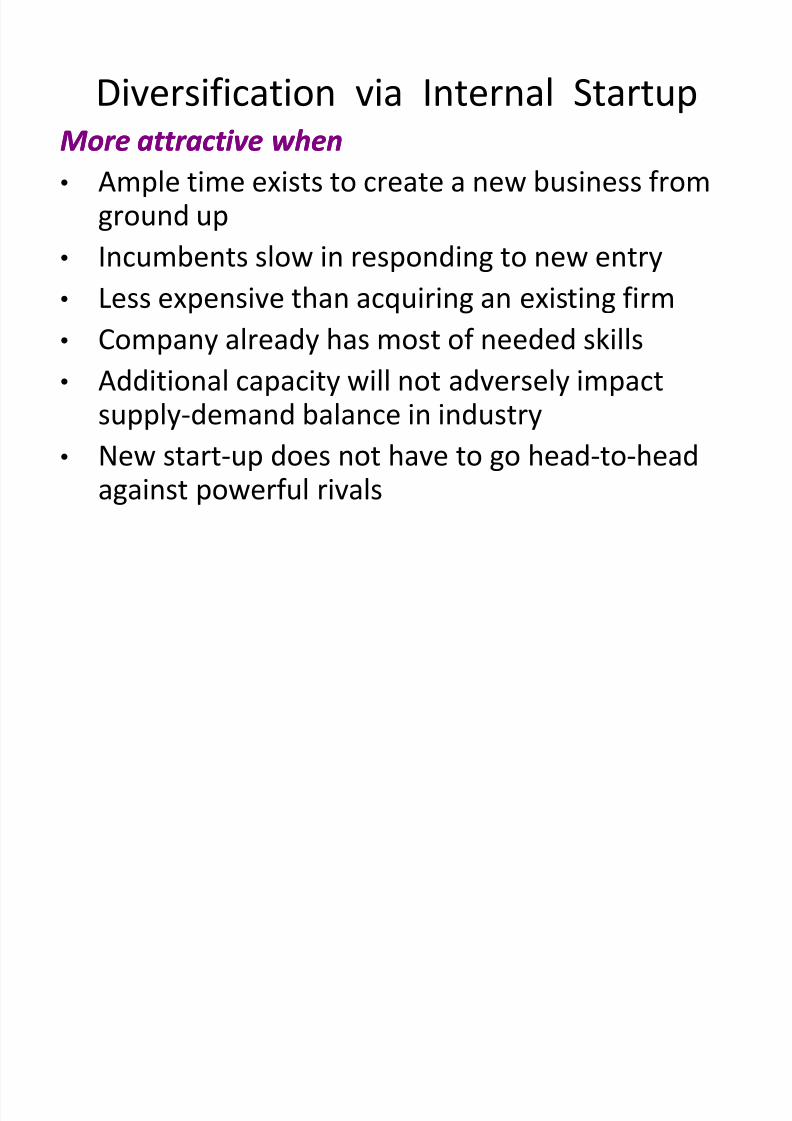

Diversification via Internal Startup

More attrac t iv e whenMore attrac t iv e when Ample time exists to create a new business from

ground up

Incumbents slow in responding to new entry

Less expensive than acquiring an existing firm

Company already has most of needed skills

Additional capacity will not adversely impact

supply-demand balance in industry New start-up does not have to go head-to-head

against powerful rivals

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 77/98

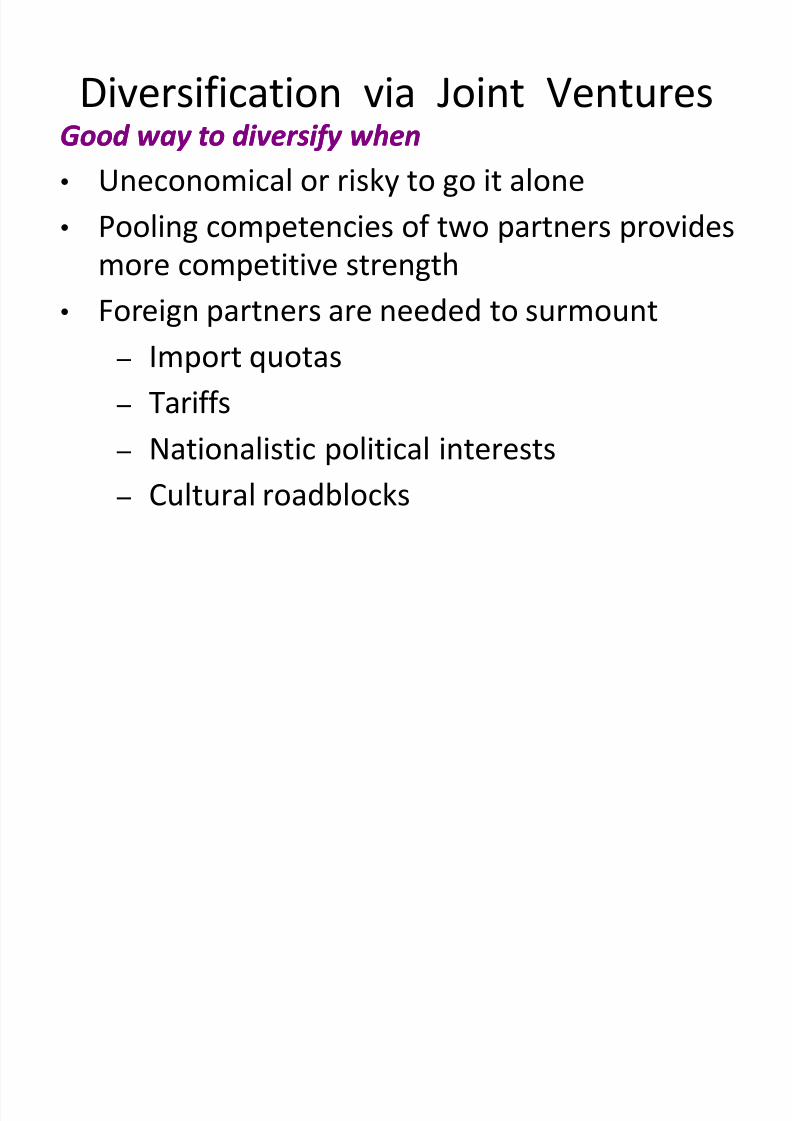

Diversification via Joint VenturesG

ood w ay t o d iv ersif y whenG

ood w ay t o d iv ersif y when Uneconomical or risky to go it alone

Pooling competencies of two partners provides

more competitive strength

Foreign partners are needed to surmount

± Import quotas

± Tariffs

± Nationalistic political interests

± Cultural roadblocks

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 78/98

What Is Related Diversification?

Involves diversifying into businesses whosev al ue chains possess competitively valuable

strategic fi ts with the value chain(s) of the

present business(es)

Capturing the strategic fi ts makes related

diversification a 2 + 2 = 5 phenomenon

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 79/98

Benefits of Related Diversification

Preserves uni ty in its business activities Reap compet i t iv e ad v antage benefits of

± Skills transfer

± Lower costs

± Common brand name usage

Spread investor r i sk s over a broader base

Achieve consol i dated per for manc e greater than thesum of what individual businesses can earn

operating independently

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 80/98

Concept: Economies of Scope

Arise from ability to el iminate costs by operatingtwo or more businesses under same corporateumbrella

Exist when it is less costly for two or morebusinesses to operate under centralizedmanagement than to function independently

Cost saving opportunities can

stem from interrelationshipsanywhere along businessesv al ue chains

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 81/98

Capturing Benefits of Strategic FitBene fi ts d ont occur by t hemsel v es ! ± Businesses with sharing potential must be

reorganized to coordinate activities

± Means must be found to make skills transfer

effective

Benefits of some strategic coord inat ion must exist to

justify sacrificing business-unit autonomy

Compet i t iv e ad v antage potential exists ± To expand resources and strategic assets and

± To create new ones faster and cheaper than rivals

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 82/98

Involves diversifying into businesses with

± N o strategic fit

± N o meaningful value chain

relationships

± N o unifying strategic theme

Approach is to venture into any business

in which we think we can make a profit Firms pursuing unrelated diversification are often

referred to as congl omerates

What Is Unrelated Diversification?

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 83/98

Post-Diversification Strategies

Divestiture and liquidation

Corporate turnaround

Corporate retrenchment

Portfolio restructuring

Multinational diversification

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 84/98

Comment: Trend in Diversification

The present trend toward narrower

diversification has been driven by a

growing preference to gear

diversification around creating strong

competitive positions in a few, well-

selected industries as opposed to

scattering corporate investments across

many industries!

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 85/98

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 86/98

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 87/98

87

Procter & Gambles Diversification Strategy

Purpose of diversification: Use expertise andknowledge gained in one business by diversifyinginto a business where it can be used in a related

way ± Builds synergy: value added by corporate office adds up to morethan the value if different businesses in the portfolio wereseparate and independent

Procter & Gamble (P&G) ± Product mix: beauty products targeting women and baby care

products

± 2005: Acquired Gillette (consumer health care products)focused on masculine market

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 88/98

88

Procter & Gambles Diversification Strategy

Procter & Gamble (P&G) (Contd)

± Synergy created with combining toothbrush and toothpaste

businesses

Had to sell off product lines with Gillette acquisition, lost some

prospective market power

Good for retailers (shelf space)

Although strategy appeared to have potential, it was more difficult

to create actual operational relatedness between the products

±Comingle employees requiring actual physical re-location/talent exit

± Different ways to make business decisions

± Conflicting organizational cultures

l f f

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 89/98

89

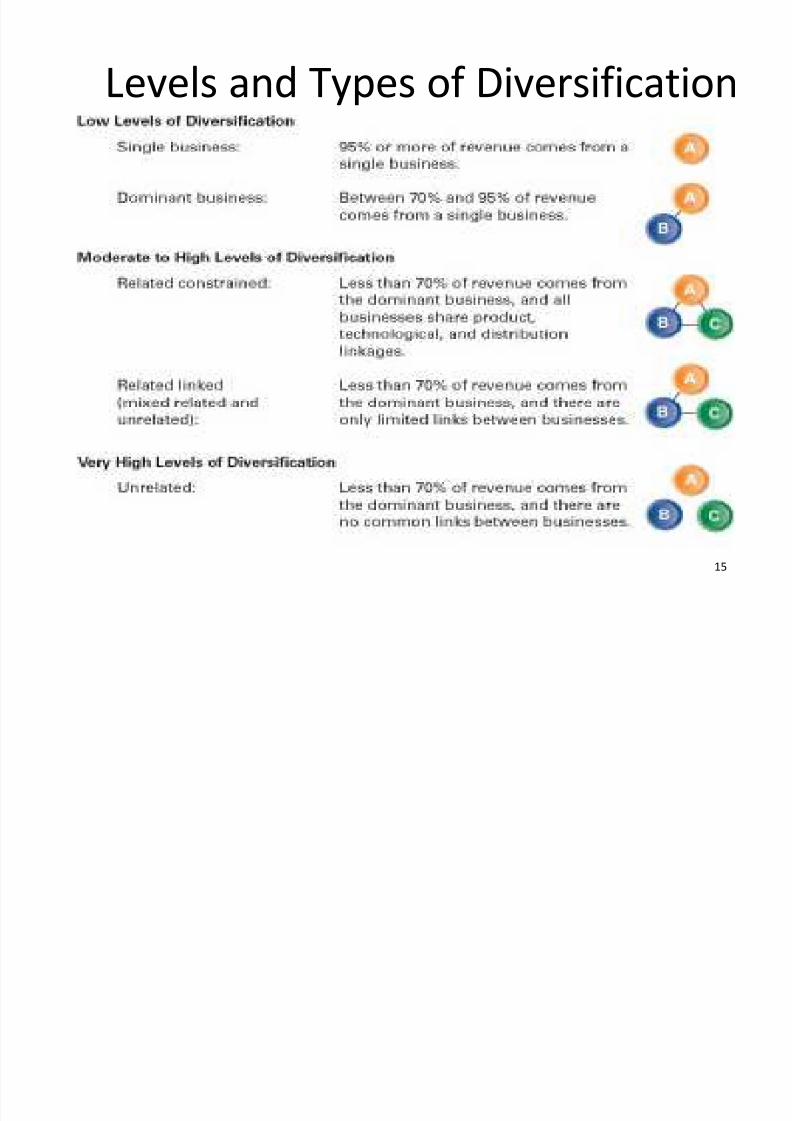

Levels of Diversification

1. Low Levels

± Single Business Strategy

Corporate-level strategy in which the firm generates 95% or more of

its sales revenue from its core business area

E.g. Daimler Benz, DeBeers

± Dominant Business Diversification Strategy

Corporate-level strategy whereby firm generates 70-95% of total sales

revenue within a single business area

Nestle

l f f

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 90/98

90

Levels of Diversification

2. Moderate to High Levels

± Related Constrained Diversification Strategy

Less than 70% of revenue comes from the dominant business(fromprimary activity)

Di rect l i nks (I.e., share products, technology and distribution linkages)between the firm's businesses

E.gn Abott Labs

± Related Linked Diversification Strategy (Mixed related and

unrelated ) Less than 70% of revenue comes from the dominant business

Mixed: Linked firms sharing f ewer resources and assets among theirbusinesses (compared with related constrained, above), concentrating onthe transfer of knowledge and competencies among the businesses

L l f i ifi i

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 91/98

91

Levels of Diversification

3. Very High Levels: Unrelated (Conglomerate)

Less than 70% of revenue comes from (primary activity)dominant

business

No relationships between businesses E.g. 3M, General Motors

Cost of Diversification: Internal

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 92/98

Cost of Diversification: Internal

CapitalMarket in Oil Companies

If internal capital markets worked well, nonoil

investments should not be affected by the

price of oil. Lamont (1997) found on the

contrary that investments in non-oilsubsidiaries fell sharply after the drop in oil

prices.

Managerial reasons may dominate theinvestment decisions

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 93/98

Indian companies 1979-89

Raman (1991) has measured the pattern of diversification of 67 Indian companiesfrom the private sector. The pattern was studied over 1 1 -year period from 1979-89 at three points of time, that is, 1979, 1984 and 1989. Using Rumelt'sclassification the firms were divided into nine categories. It was observed that

companies preferred going in for Unrelated Business rather than Single Business.

Among the Dominant Business, Dominant Vertical was the same for each year

while Dominant Linked was larger in 1989 as compared to 1979. The number of companies in related linked also increased as compared to related

constrained.

However, between 1980-90, studies also show that companies started favoringrefocusing rather than diversification.

Lichtenberg (1992) showed that the level of diversification declined between 1985

and 1989 in a sample of 6,505 firms. Spender and Grant (1996) also reported that the average index of diversification

for Fortune 500 companies declined from 1.00 to 0.67.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 94/98

94

Why do firms diversify

Diversification across productsand across markets can be due to

economies of scale and scope.

Diversification that occurs for

other reasons tends to be less

successful.Nokia - wood pulp and paper/

footwear/ televisions/ capacitors

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 95/98

E conomi es of sc ale and scope ± Operational synergies can be realized.

± Spreading the firm's unutilised organizational resources to other areas can create value.

± Leveraging skills across businesses can create value.

T ransac t ion costs

± Coordination among independent firms may involve higher transaction costs.

Inter nal c a pi tal mar k et ± Cash from some businesses can be used to make profitable investments.

± External finance may be more costly due to transaction costs, monitoring costs,etc.

Div ersif y ing shareholders port fol ios

± Individual shareholders may benefit from investing in a diversified portfolio.

I dent if y ing under v al ued fi r ms ± Shareholders may benefit from diversification if its managers are able to identify

firms that are undervalued by the stock market.

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 96/98

Why do firms diversify Growth is an implicit objective in nearly all organisations. Stock

markets tend to reward growing companies.

± Managers find growth extremely attractive because it hold out the

prospects of increased earnings for the firm leading to increased

compensations for themselves. They also see the acquisition of

new knowledge as instrumental in improving their self actualisation prospects.

Fuller utilisation of Resources and Capabilities - Firms find that they

have un utilised or under utilised capacities sometimes in

manufacturing some times in Alternatively a firm could find that it can perform a business

activity at a lower cost and with better timeliness than if it utilised its

internal capabilities.

96

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 97/98

Why do firms diversify To make use of surplus Cash flows. There are several examples of

this to be found in Indian Industry. Bajaj Auto and Bombay Dyeing

have consistently over the last few years invested surplus cash from

their core businesses in Two Wheelers and Textiles respectively into

treasury operations mostly short term lending to other cash strapped

Corporates. At times a firm might use surpluses from one of its cashrich businesses to cross fund other businesses.

Managerial Reasons - Managers find growth extremely attractive

because it hold out the prospects of increased earnings for the firm

leading to increased compensations for themselves. They also see the

acquisition of new knowledge as instrumental in improving their self

actualisation prospects.

97

Cons

5/12/2018 Final Week 6 Lecture 6 - Diversification - slidepdf.com

http://slidepdf.com/reader/full/final-week-6-lecture-6-diversification 98/98

Cons Combining two businesses in a single firm is likely to result

in substantial influence costs. Resource allocation can be influenced by lobbying.

Costly control systems may be needed that reward

managers based on division profits and discipline

managers by tying their careers to business unitobjectives.

Internal capital markets may not work well in practice.

Shareholders can diversify their own personal portfolios.Corporate managers are not really needed to do this.

Identifying undervalued firms may not be as easy as it

sounds